Embed Size (px)

Citation preview

CAUTIONRISING PRICES

$ FORECLOSUREAUCTIONAHEAD

GAS

Shopping ListWinning Shoppers in Turbulent Times

A Unilever Trip Management Report

To Our Retail Customers:

Study MethodologyThe research underlying this report consists of three primary parts: 1) Focus groups were held to develop preliminary hypotheses and in-depth understanding. 2) A proprietary survey of 47,031 Nielsen households, conducted between March 14 and April 3, 2008, looked at shopping behavior in a worsening economy. Survey is demographically and geographically representative of U.S. households. 3) The Nielsen panel was used to measure what shoppers are doing, category by category, outlet by outlet. For Trip iNSighTS, we ANAlyzed A ToTAl oF 125,000 hoUSeholdS, who TogeTher Took A ToTAl oF 10.7 MillioN TripS.

Behind the headlines of the slumping economy, shoppers are being forced to make some hard choices every day. what

these choices are, how they affect your business, and, most importantly, what their choices will be if the economy were

to worsen, are the subject of this important report.

our new study, the latest in Unilever’s groundbreaking series on Trip Management, reveals for the first time the

different shopping tactics that different demographic groups employ to navigate this new economy. it tells you how

trip missions are shifting, what compromises shoppers are willing to make to stay within budget, and what could spur

even more change in shopping behavior.

The bottom line is, your shoppers are looking for the same retail experience that has brought them to your stores in

the past. with insights gained from this report, and with a little creativity and determination, you can maintain – and

even strengthen – your bond with shoppers in uncertain times.

Sincerely,

kevin havelock

president, Unilever United States

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report4

While only recently it was consumer wealth and discretionary spend that led changes in retail, it’s now suddenly the shopping behavior of low and middle income groups that is most affecting the retail landscape.

Buffeted by today’s economic turbulence and very worried about the future, lower and middle

income shoppers are changing how and what they shop. Boomers, another key demographic

group in this study, are also fretful, even though they’ve seen it all before. Gallup says 46% of

Americans already feel the effect of higher food prices, which sting low income households more

than twice as much as middle and high income households, according to the poll.

Low and middle income shoppers have already committed to new survival strategies that will

quickly shake up the selling floor. Since they account for 61% of national retail spend, that’s a lot

of shake in every part of the store.

Fear motivates their new shopping approaches. An overlay of bad economic events – the housing

bubble, record debt levels, stock market volatility, pension takeaways, food and energy inflation

– prompted 43% of U.S. primary shoppers to tell Unilever researchers that they feel worse off

than a year ago. In response, more than 30% are eating at home more and eating out less.

An overwhelming 93% worry about rising food prices, and 79% about rising personal care

product prices. Of great importance to retailers, more than 7 households in 10 (72%) are ready to

reduce spending on household necessities (food and beverage, personal and home care items) if

economic conditions worsen.

They may have to: Warren Buffett believes the recession will be longer and deeper than most

people think. He’s unlikely to eat canned soup for dinner, but millions of other Americans could

soon be on recession diets.

CAUTIONRISING PRICES

$

CAUTIONRISING PRICES

$

CAUTIONRISING PRICES

$Will Reduce Spending

On Household Necessities

If Economy Worsens

Worry About

Rising Personal Care

Product Prices

Shoppers That

Worry About

Rising Food Prices

USE COUPONS

93%

79%72%

Anxiety Spurs Dramatic Change In Low And Middle Income Shopping

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

5Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

The Pinch Is On, Trips Are At StakeTo compensate for rising gas prices, half of consumers (49%) are reducing their retail spend, 70% combine shopping trips and errands, and 39% stay home more, according to Nielsen.

Trips are less secure in today’s environment. One consumer in four (24%) would shop for groceries in a less expensive store if food prices continue to rise. In the past year, that’s precisely what 12% have already done, according to a Citigroup Global Markets survey.

The CEO of an extreme-value retail chain cited a dramatic increase in new faces shopping his stores in recent months, which primarily serve low and middle income households.

And in a major West Coast chain, the CEO said sales of high-end items such as premium wines are down, and private label growth is four times higher than national brands (six times in center store) in the latest quarter.

Anxiety Spurs Dramatic Change In Low And Middle Income Shopping

More signs of the times:

• Wholesale clubs have had to limit rice and flour purchases to curb hoarding. A

new cookbook featuring dollar store foods is available, inspired by the BMWs and

Porsches its author saw in the parking lots, the Detroit News reported. No mirage:

Boomer trips to stock up at dollar stores are up 5% so far this year, according to

Nielsen.

• Some supermarkets offer 10 cents per gallon discounts on gasoline with $50

purchases in store. Others tack on 10% in shopping credits for people who bring

in their tax rebate and economic stimulus checks.

To succeed in the new economy means winning the new-style savings trips especially

of low and middle income shoppers, who individually spend less than the wealthy

but who collectively can determine retailer fortunes.

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report6

Supercenters, Dollar And Drug Win Key TripsAt Expense Of Food, Mass And Club

Percent change in trips, first quarter 2008 versus year agoSource: Unilever 2008 Winning Shoppers in Turbulent Times study

ChAnnel QuICk TrIPS MAjOr STOCk-uP

Food (0.1%) (0.8%)

drug 3.8% 12.3%

Mass (8.1%) (4.9%)

Supercenters 4.1% 6.2%

Club (3.2%) (1.1%)

dollar 0.1% 7.4%

A decline in Quick Trips (typically the most profitable trips for retailers, since Quick Trip shoppers prefer to save time over money) and Intermediate Needs Trips for the three demographic groups studied suggests that shoppers are carefully planning their shopping.

If this trend accelerates with rising prices, retailers may have to compete more

directly with lower-cost channels for share of wallet.

This is already apparent. Low and middle income and boomer trips to food stores

for almost every mission slid so far this year. Instead, these three groups shopped

dollar stores more often on Major Stock-Up and Restock Needs Trips. Among low

income shoppers, Major Stock-Up Trips to dollar stores rose 7%, and Restock

Needs Trips grew 6%; among middle income shoppers, they climbed 4% and 2%

Simply speaking, shoppers take two types of trips: Quick Trips and Major Stock-Up Trips. Quick Trips are short trips aimed at buying items that are needed right away or in the very near future. Major Stock-Up Trips are all about replenishing the items needed to maintain the household for a long period of time. Need States help to explain why shoppers take each of their trips. Today, we recognize the six most important Need States as: 1) Restocking The Home, 2) Buying Something For Immediate Needs (or For Immediate Use), 3) Buying Something For Intermediate Needs (or For Use Today or Tomorrow), 4) To Take Advantage Of A Special Offer, 5) Shopping For A Special Occasion or Just To Have Fun, and 6) To Purchase Non-Food Items.

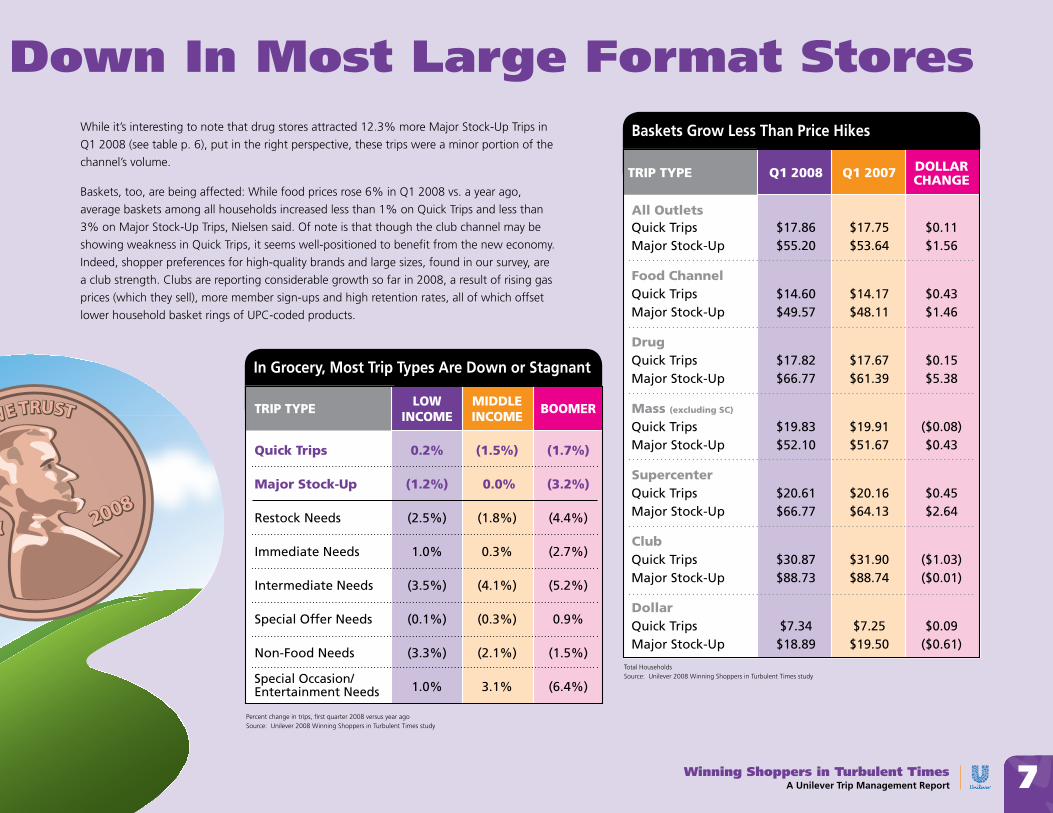

Quick Trips Decline Overall, And Are Down In Most Large Format Storesrespectively; among boomers, they were up 5% and 5%. Their trips to drug stores

and supercenters were also up, while mass merchants and club suffered along with

supermarkets.

Indeed, the economic tempest of 2007 has already led U.S. households to take 6

fewer shopping trips on average – compared with the five preceding years it took

for trips to fall by 11. Results of the harsh drop: 181 trips in 2001, 170 trips in 2006,

and 164 trips in 2007.

Hardest hit in trips were grocery stores, which fell from 72 in 2001 to 59 in

2007, and mass merchandisers, down from 24 to 15 in the same period, Nielsen

reported. By contrast, supercenters have leveraged their one-stop appeal to become

the biggest winners of trips, in both actual increases in trips and percentage

gains, according to Nielsen data. Their trips have risen in 2007 to 27 a year per

household—that’s more than twice a month—up from 20 in 2001,

a gain of 35%.

7Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

Quick Trips Decline Overall, And Are Down In Most Large Format StoresWhile it’s interesting to note that drug stores attracted 12.3% more Major Stock-Up Trips in

Q1 2008 (see table p. 6), put in the right perspective, these trips were a minor portion of the

channel’s volume.

Baskets, too, are being affected: While food prices rose 6% in Q1 2008 vs. a year ago,

average baskets among all households increased less than 1% on Quick Trips and less than

3% on Major Stock-Up Trips, Nielsen said. Of note is that though the club channel may be

showing weakness in Quick Trips, it seems well-positioned to benefit from the new economy.

Indeed, shopper preferences for high-quality brands and large sizes, found in our survey, are

a club strength. Clubs are reporting considerable growth so far in 2008, a result of rising gas

prices (which they sell), more member sign-ups and high retention rates, all of which offset

lower household basket rings of UPC-coded products.

Baskets Grow Less Than Price Hikes

Total HouseholdsSource: Unilever 2008 Winning Shoppers in Turbulent Times study

TrIP TyPe Q1 2008 Q1 2007 DOllAr ChAnge

All Outlets Quick Trips $17.86 $17.75 $0.11 Major Stock-Up $55.20 $53.64 $1.56

Food Channel Quick Trips $14.60 $14.17 $0.43 Major Stock-Up $49.57 $48.11 $1.46

Drug Quick Trips $17.82 $17.67 $0.15 Major Stock-Up $66.77 $61.39 $5.38 Mass (excluding SC)

Quick Trips $19.83 $19.91 ($0.08) Major Stock-Up $52.10 $51.67 $0.43

Supercenter Quick Trips $20.61 $20.16 $0.45 Major Stock-Up $66.77 $64.13 $2.64 Club Quick Trips $30.87 $31.90 ($1.03) Major Stock-Up $88.73 $88.74 ($0.01) Dollar Quick Trips $7.34 $7.25 $0.09 Major Stock-Up $18.89 $19.50 ($0.61)

Percent change in trips, first quarter 2008 versus year agoSource: Unilever 2008 Winning Shoppers in Turbulent Times study

In Grocery, Most Trip Types Are Down or Stagnant

TrIP TyPe lOw MIDDle BOOMer InCOMe InCOMe

Quick Trips 0.2% (1.5%) (1.7%)

Major Stock-up (1.2%) 0.0% (3.2%)

restock Needs (2.5%) (1.8%) (4.4%)

immediate Needs 1.0% 0.3% (2.7%)

intermediate Needs (3.5%) (4.1%) (5.2%)

Special offer Needs (0.1%) (0.3%) 0.9%

Non-Food Needs (3.3%) (2.1%) (1.5%)

1.0% 3.1% (6.4%)Special occasion/ entertainment Needs

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report8

Different Demographic Groups Use Different Shopping Strategies To Navigate A Troubled Economy

Low income shoppers are very smart shoppers. They do their research,

prioritize, and make trade-offs. They start their shopping trips around the kitchen table

in a near blizzard of coupons from newspapers, circulars, and direct mail offers. A new

sense of urgency pervades this activity. Before they get up from the kitchen table, LI

shoppers will have completed a detailed shopping list, matched to coupons and to

several menus they’ve planned for the week. Most importantly, they will have established

a budget, and they’ll take only that amount of cash with them when they shop.

LI shoppers will show up in the store on or near payday, budgeted cash in one hand and

calculator in the other. Down certain aisles they’ll go (some aisles will be skipped entirely)

looking for loyalty card discounts, and stocking up on essentials (food and personal care)

only if in-store deals make it possible. Snacks get purchased only on sale. They’ll use the

bag refund if offered – every little bit helps in times like these.

Middle income shoppers go through a similar, though looser, routine:

coupons for higher-ticket items; meal planning as a diversion rather than a budget-

driven necessity; and the comfort of some wiggle room for that impulse purchase. They

desire larger economy packs, but will continue to purchase familiar brands, especially in

personal care.

MI shoppers’ in-store behavior is also similar to LI shoppers’, just less pervasive. In-store

deals on essentials and on their favorite brands attract them, and there’s also some

couponing and specific meal budget calculating.

Boomers? This been-there-done-that demographic may collect a few coupons

but are likely as not to leave them at home. They’ll use a list, but just to remind, not to

constrain. Gas prices haven’t completely dissuaded them from shopping around a bit for

freshness and variety, or just to fit a schedule.

Boomers are much more likely to stockpile on quality sale items (good cuts of meat,

for example) and on their favorite brands. Since most people in this group are empty

nesters, decisions revolve around what they want, not the kids. To be sure, if there are

grandchildren involved in the trip, their “pester power” may change everything.

Shoppers can be forgiven if they feel beset by the tide of bad news. Price rises buffet them at every turn: Food. Gasoline. Housing. Healthcare.

Troubled times coupled with retailer inattention can snap the fragile bonds of

shopper trust. Or, savvy retailers can work harder at understanding shopper

attitudes in today’s economy and how these shoppers will behave if times get

worse.

Using Unilever Trip Management tools and Nielsen information, we took a deep

dive into three distinct shopper groups: Low income (LI) households, middle

income (MI) households, and boomers of all income levels. (Looking at the

answers to our proprietary Nielsen survey, we saw that the most interesting

groups, those that showed signs of being the most different from the average,

were low income, middle income and boomers. The high income group was

not noteworthy because shoppers in this group are somewhat insulated, but

boomers are a large group who skew both higher income and being worried

about the economy.)

What we found:

• LI households are feeling more financially insecure about jobs, savings and retirement.

• Seventy percent of LI households are very concerned with rising food prices.

• LI households are not likely to make a major purchase in the next six months.

And while all income groups plan to reduce discretionary spending –

entertainment, clothing and travel/vacations – only LI shoppers are more likely to

reduce spending on healthcare and transportation as well.

InCOMe: unDer $30k

Low Income Shoppers

9Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

Pre-ShOP In-STOre

Current Strategies For The New Economy

• Coupons and sales flyers –

especially on higher-ticket

items

• Making a list off a meal

plan or menu

• Discount cards

• Bulk buying/stockpiling

• Switching between

quality brands

Pre-ShOP In-STOre

Current Strategies For The New Economy

• Coupons and sales flyers –

if they remember them

• A list only as a reminder

• Shopping around to fit

schedules

• Deals/specials, notably on branded goods

• Bundles (e.g. 4 for $7)

• Stockpiling on quality sale items

• Stockpiling on often-used healthy items

• Sampling to experiment, not to get a deal

InCOMe: $30k - $69.9k

Middle Income Shoppers

Age: 45-64

Boomer Shoppers

Average basket ring, Quick Trips: $17.70 Chg vs. yago: $0.31

Average basket ring, Major Stock-Up Trips: $54.73

Chg vs. yago: $1.72

Average basket ring, Quick Trips: $17.71 Chg vs. yago: $0.16 Average basket ring, Major Stock-Up Trips: $55.77

Chg vs. yago: $1.64

Pre-ShOP In-STOre

Current Strategies For The New Economy

• Monitor and compare prices

• Gather coupons from all sources

• Create list around coupons

• Plan meals around sales

• Set a firm budget

• Consider separate dollar store purchases

• Reduce shopping frequency

• Arrive with cash only, up to budget

• Stock up on essentials, preferably on deal

• Buy snacks only on deal

• Look out for sampling and attendant specials or deals

• Skip entire aisles• Switch sizes/package• Store brands• Dual purposing (Paper towels

for household cleaning and as napkins)

Average basket data for 3 shopper groups, all outlets, Q1 2008Source: Unilever 2008 Winning Shoppers in Turbulent Times study

Average basket ring, Quick Trips: $15.40 Chg vs. yago: $0.23

Average basket ring, Major Stock-Up Trips: $43.78 Chg vs. yago: $1.75

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report10

More Shoppers Are Poised To Be More Engaged In Planning Their ShoppingPeople’s attitudes about shopping provide another lens through which to view shopper behavior in today’s economy.

Highly engaged, active shoppers behave differently than passive, reluctant shoppers – those for whom shopping is a necessary-but-stultifying chore. When we examine engagement, middle income shoppers and boomers tend to blend together attitudinally. So for our purposes, we’ll combine the two and call them “higher affluent.” Low income shoppers remain attitudinally distinct.

We identified the lower-affluence, active shoppers as “proactive planners.” They plan because they have to. It’s a matter of survival. Their trips and buys are very consistent and budget-constrained.

Active higher affluents are “experimenters.” They can afford to try new items and stay with trusted brands. They may well use price instability as an excuse to try new brands within categories to save a little money.

For their part, lower-affluence passive, reluctant shoppers – we identify them as “basics-only”– are very selective about the categories in which they buy brands.

Basics-only are completely price-driven and will cut out entire categories, never purchase off-deal and use dollar stores extensively for non-food.

Somewhat more relaxed about shopping are the higher-affluence passive, reluctant shoppers: they’re “comfort seekers.” This group looks for in-store deals on good brands, uses loyalty cards/offers, and tends towards very routine shops – same spends, same items.

What happens to our attitudinal groups if prices continue to rise? Drawing on extensive qualitative research, we believe both higher-affluence groups (comfort seekers and experimenters) will assume proactive planner characteristics. They’ll start to shop and plan meals around sales circulars, aggressively budget, and stick to lists. Those who start out as proactive planners become basics-only when times go sour. Price is the all-consuming driver here, and what used to be an anticipated activity – shopping – is now an exercise in survival. Smart retailers will concentrate on improving the shopping experience for proactive planners – potentially the largest shopper attitudinal type.

Dinner dishes shift to casseroles (141 index)• skillet dishes (132) • stew (126) • poultry (118)

To Stay On Budget, Shoppers Are Cooking Up New Meal Strategies

Adults overallSource: NPD Group, How Do Economically Challenging Times Affect Consumers’ In-Home Meal Strategies study, March 2008

More than 50% of the financially challenged use up leftovers,prepare/cook meals at home and stock up• Pizza is the most common leftover at lunch• Poultry and beef at dinner• Vegetables are the most common leftover side dish

11Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

If The Economy Worsens, Coping Strategies Get Refined

What happens with the three distinct shopper groups – low and middle income households and boomers – if prices don’t let up?

The storm-tossed shopper ship becomes even more

unstable. Shoppers across income levels are really feeling

the squeeze in their world. Here’s what’s expected to

unfold:

In general, each group intensifies its familiar strategies.

But some new behaviors get mixed in as prices rise.

Low income (LI) shoppers will simply buy less.

Spending on extravagances such as bacon, steak, ice

cream, candy, and snacks will grind to a halt. No more

treats, barely a cookie. Very resourceful shoppers, they’ll

also look for dual-purposing opportunities: Paper napkins

or paper towels, but not both. In certain categories, they’ll

slide down to value brands and store brands (notably in

OTC drugs).

LI shoppers will carefully weigh what they need and

what they can do without. In non-food categories, only

personal care and laundry detergent seem “safe.” Even

then, these shoppers may size down or seek out dollar

stores for the brands they trust. Among foods, only

condiments and butter/margarine survive the trade-down.

Middle income (MI) shoppers also will look

at value and store brands for savings in select categories.

Cheaper snacks and non-essentials get explored. Buys

of prepared foods (for example packaged salads), ice

and bottled water all get reduced. Impulse purchasing is

reined in. Slightly more willing to drive, MI shoppers also

might switch to a lower-price store.

MI shoppers will be less likely to shy away from entire

categories than LI shoppers, our research shows. If

convinced of the quality of store brands, they’d shift to

them. They too have their sacred categories: condiments,

butter/margarine but also coffee/tea and boxed meals.

They’d rather save elsewhere in the shop than desert the

preferred brands they’ve spent considerable time finding.

Boomers, for their part, are acutely aware of the

boom-and-bust nature of the American economy and

know what to do in the trough. Still, they’re worried, and

as the economy worsens, they will start behaving a bit

like their LI and MI brethren: searching for familiar brands

on sale, using a list, couponing a bit. But there will also

be that “I’ll buy it anyway” free-spiritedness lurking near

the surface, waiting to re-emerge.

In this economic scenario, boomers are even more brand-

attached than MI shoppers. They’re extremely loyal to

their personal care and household cleaner standbys.

They’ve spent years (and dollars) trying out different

brands and identifying a favorite. They’ll cut back on

other areas of the shop – or non-shopping expenditures

– before they’ll abandon an old and trusted friend.

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report12

Savings Tactics Will Differ By CategoryAs prices rise, shoppers use eight different tactics to save throughout the store, Unilever research shows.The tactics vary more by category than income group. But importantly, the timing when

the tactics will be deployed will depend on the socioeconomic status of shoppers.

Note that low income shoppers already show much more involved pre-store and in-

store shopping behavior than the other shopper groups.

The big insight: The savings tactics that will be used will vary significantly from category

to category.

The crux of each category savings tactic: Does the primary household shopper perceive

the category as essential or peripheral to household needs? How strong are brand

loyalties? Is the category item perishable or can it last a long time in the home? Are

there easy substitutes?

The point of change to specific category savings tactics happens later for middle

income shoppers, but how they change is similar among all shopper groups. The

three groups’ behavior clusters suggest economic pressures are pushing people from

all corners of the nation toward similar conclusions about category relevancy to their

families’ well-being. Hence, they affect retailers in every kind of urban, suburban and

rural market. By delivering targeted ‘value’ solutions in specific categories, retailers

can help retain trips, motivate repeat visits, and help ease shopper price anxiety.

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

Shoppers Will Implement Eight Savings Tactics By Category

• Only buy it when it’s on sale

• Use coupons whenever I buy this

product

SeCOnDAry TACTICS – wIll VAry wITh CATegOry

PrIMAry TACTICS –heAVIly eMPlOyeD

• Stock up more when purchasing

• Switch to a less expensive name brand

• Switch to generic or private label

• Buy product less often

• Switch stores to search for savings

• Stop buying this product

I Will Not Change How I Shop For This

Product

44% 45% 46%

16% 16% 18% 20%18%

<1%<1%<1%

20%

17%

31% 32% 33%

28% 27%

14% 15% 15%

29%

3% 3%5%

16%18%

14% 15%

13%

7% 7% 8%

19%

17%

15% 16%

11%

15%

13%

29% 29%32%

43%42%

10% 10% 11%

45%

36%37% 38%

16%16%

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

I Will Not Change How I Shop For This

Product

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

Low Income

Middle Income

Boomer

13Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

I Will Not Change How I Shop For This

Product

44% 45% 46%

16% 16% 18% 20%18%

<1%<1%<1%

20%

17%

31% 32% 33%

28% 27%

14% 15% 15%

29%

3% 3%5%

16%18%

14% 15%

13%

7% 7% 8%

19%

17%

15% 16%

11%

15%

13%

29% 29%32%

43%42%

10% 10% 11%

45%

36%37% 38%

16%16%

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

I Will Not Change How I Shop For This

Product

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

Low Income

Middle Income

Boomer

Two Different Worlds, An Aisle Apart

Pet Food*

Cookies*

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

Sharp contrasts in the tactics shoppers will use to save in different categories

Note key differences in the use of savings tactics by Pet Food shoppers and Cookies shoppers. About triple the percentage of Pet Food shoppers (vs. Cookies shoppers) will buy the category same as always, 2X as many will stock up more when purchasing, and 1.5X will switch stores for savings. Cookies shoppers will be more than 10X willing (vs. Pet Food shoppers) to stop buying the category, and 9X as many will buy less often.

I Will Not Change How I Shop For This

Product

44% 45% 46%

16% 16% 18% 20%18%

<1%<1%<1%

20%

17%

31% 32% 33%

28% 27%

14% 15% 15%

29%

3% 3%5%

16%18%

14% 15%

13%

7% 7% 8%

19%

17%

15% 16%

11%

15%

13%

29% 29%32%

43%42%

10% 10% 11%

45%

36%37% 38%

16%16%

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

I Will Not Change How I Shop For This

Product

Stock Up More When Purchasing

Switch To Generic Or Store Brand

Switch To A Less Expensive Name Brand

Stop Buying This Product

Buy This Product

Less Often

Use Coupons Whenever I Buy

This Product

Only Buy It When It's On Sale

Switch Stores To Search

For Savings

Low Income

Middle Income

Boomer

*These are just two of the 36 deep-dive categories that Unilever analyzed.

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report14

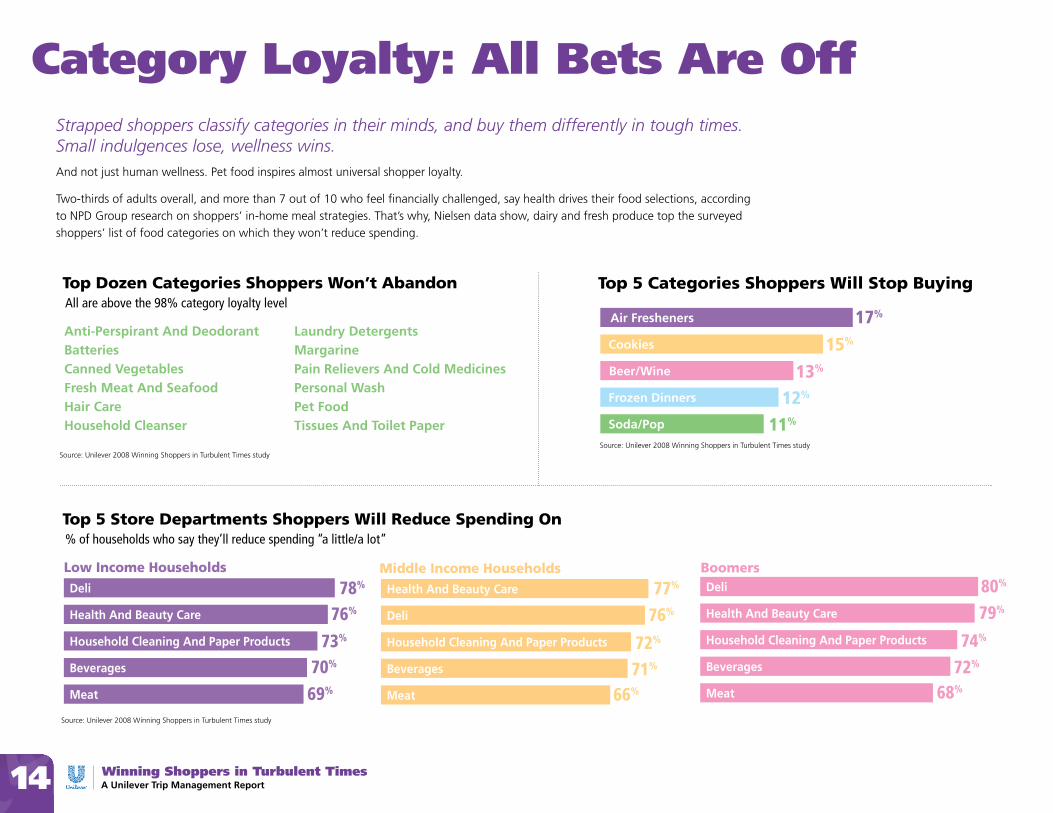

Category Loyalty: All Bets Are Off

17%

78%

76%

73%

70%

69%

15%

77%

76%

72%

71%

66%

13%

12%

11%Soda/Pop

Frozen Dinners

Beer/Wine

Cookies

Air Fresheners

Top 5 Categories Shoppers Will Stop Buying

Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Meat

Beverages

Household Cleaning And Paper Products

Deli

Health And Beauty Care

Low Income Households

Middle Income Households Boomers

MargarineCanned VegetablesFresh Meat And Seafood

Pain Relievers And Cold MedicinesBatteries

Household Cleanser

Personal Wash

Anti-Perspirant And Deodorant

Hair Care Pet Food

Laundry Detergents

Tissues And Toilet Paper

Top Dozen Categories Shoppers Won't AbandonAll are above the 98% category loyalty level

80%

79%

74%

72%

68%Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

17%

78%

76%

73%

70%

69%

15%

77%

76%

72%

71%

66%

13%

12%

11%Soda/Pop

Frozen Dinners

Beer/Wine

Cookies

Air Fresheners

Top 5 Categories Shoppers Will Stop Buying

Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Meat

Beverages

Household Cleaning And Paper Products

Deli

Health And Beauty Care

Low Income Households

Middle Income Households Boomers

MargarineCanned VegetablesFresh Meat And Seafood

Pain Relievers And Cold MedicinesBatteries

Household Cleanser

Personal Wash

Anti-Perspirant And Deodorant

Hair Care Pet Food

Laundry Detergents

Tissues And Toilet Paper

Top Dozen Categories Shoppers Won't AbandonAll are above the 98% category loyalty level

80%

79%

74%

72%

68%Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

% of households who say they’ll reduce spending “a little/a lot” Top 5 Store Departments Shoppers will reduce Spending On

Strapped shoppers classify categories in their minds, and buy them differently in tough times. Small indulgences lose, wellness wins.And not just human wellness. Pet food inspires almost universal shopper loyalty.

Two-thirds of adults overall, and more than 7 out of 10 who feel financially challenged, say health drives their food selections, according

to NPD Group research on shoppers’ in-home meal strategies. That’s why, Nielsen data show, dairy and fresh produce top the surveyed

shoppers’ list of food categories on which they won’t reduce spending.

17%

78%

76%

73%

70%

69%

15%

77%

76%

72%

71%

66%

13%

12%

11%Soda/Pop

Frozen Dinners

Beer/Wine

Cookies

Air Fresheners

Top 5 Categories Shoppers Will Stop Buying

Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Meat

Beverages

Household Cleaning And Paper Products

Deli

Health And Beauty Care

Low Income Households

Middle Income Households Boomers

MargarineCanned VegetablesFresh Meat And Seafood

Pain Relievers And Cold MedicinesBatteries

Household Cleanser

Personal Wash

Anti-Perspirant And Deodorant

Hair Care Pet Food

Laundry Detergents

Tissues And Toilet Paper

Top Dozen Categories Shoppers Won't AbandonAll are above the 98% category loyalty level

80%

79%

74%

72%

68%Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

17%

78%

76%

73%

70%

69%

15%

77%

76%

72%

71%

66%

13%

12%

11%Soda/Pop

Frozen Dinners

Beer/Wine

Cookies

Air Fresheners

Top 5 Categories Shoppers Will Stop Buying

Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Meat

Beverages

Household Cleaning And Paper Products

Deli

Health And Beauty Care

Low Income Households

Middle Income Households Boomers

MargarineCanned VegetablesFresh Meat And Seafood

Pain Relievers And Cold MedicinesBatteries

Household Cleanser

Personal Wash

Anti-Perspirant And Deodorant

Hair Care Pet Food

Laundry Detergents

Tissues And Toilet Paper

Top Dozen Categories Shoppers Won't AbandonAll are above the 98% category loyalty level

80%

79%

74%

72%

68%Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

17%

78%

76%

73%

70%

69%

15%

77%

76%

72%

71%

66%

13%

12%

11%Soda/Pop

Frozen Dinners

Beer/Wine

Cookies

Air Fresheners

Top 5 Categories Shoppers Will Stop Buying

Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

Meat

Beverages

Household Cleaning And Paper Products

Deli

Health And Beauty Care

Low Income Households

Middle Income Households Boomers

MargarineCanned VegetablesFresh Meat And Seafood

Pain Relievers And Cold MedicinesBatteries

Household Cleanser

Personal Wash

Anti-Perspirant And Deodorant

Hair Care Pet Food

Laundry Detergents

Tissues And Toilet Paper

Top Dozen Categories Shoppers Won't AbandonAll are above the 98% category loyalty level

80%

79%

74%

72%

68%Meat

Beverages

Household Cleaning And Paper Products

Health And Beauty Care

Deli

All are above the 98% category loyalty levelTop Dozen Categories Shoppers won’t Abandon

15Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

Even As They’re Squeezed, Shoppers Don’t Want To Give Up On Product Quality…

Shoppers are not ready to compromise on the quality of food and personal care products even if the economy were to get worse.

They’d rather see some creativity from manufacturers and retailers – in product packaging and

sales approaches – to help them sustain their lifestyles. Their preferences include: Offer them

larger pack sizes with a lower price per unit, introduce smaller pack sizes at lower prices, offer

same number of sales but reduce savings, modestly reduce package size but keep same price.

The least preferred option: produce slightly lower quality but keep the price the same.

Shoppers’ reluctance to switch away from brands approaches 100% in some pivotal categories. At least two-thirds of shoppers will not consider brand switching, even in the most susceptible categories, our research shows. The takeaway for retailers: keep brands prominent, even if they’re the highest priced in their category. People perceive value and will pay for it.

Middle income shoppers, for example, resist switching away from their preferred brands to private label in personal care, household products and foods including margarine, coffee and tea, condiments and boxed meals. They’re emotionally invested in the brands they buy, which have stood the test of time. Rather than forgoing brands – especially those perceptually connected with family health – they’ll cut spending on movie tickets or travel.

These shoppers are also less likely to cut back or opt out of categories than low income shoppers. When pushed by economic circumstance, though, they’d consider switching to a store brand of comparable quality.

Some trade-down is inevitable, most often in nonfoods. For example: In household cleansers 34% of low income shoppers would switch, as would 33% of middle income and 30% of boomers. In hair care, 29% of low income shoppers would move to a value brand, as would 28% of middle income and 29% of boomers.

Brands will Continue To hold Strong Appeal Across All key Categories Studied% of shoppers who won’t switch to private label

Source: Unilever 2008 Winning Shoppers in Turbulent Times study

Beer/Wine, Fresh Meat/Seafood

Frozen Dinners, Baby Food, Soda/Pop

Anti-Perspirant/Deodorant, Pet Food, Air Fresheners, Coffee, Ice Cream,Cookies, Facial Care, Mayonnaise, Salty Snacks, Yogurt, Tea Bags

Peanut Butter, Diapers, Batteries, Canned Soup, Pasta Sauce, Hand And Body Lotion, Salad Dressing, Olive Oil, Personal Wash, Laundry Detergents, Vitamins/Supplements, Margarine, Hair Care, Disposable Razors

Dry Sides, Cold Cereal, Tissues And Toilet Paper

Household Cleansers, Canned Vegetables,Pain Relievers/Cold Medicine

80% - 85%

65% - 69%

70% - 74%

75% - 79%

86% - 90%

91% - 100%

On the “Pain Meter,” Shoppers Prefer:

0 10 20 30 40 50 60 70 80

Produce Slightly Lower Quality Products, But Keep Price The Same

Raise Prices Of Existing Items Proportionately

Offer Fewer Sales

Modestly Reduce Package Size, Keep Same Price

Offer Same Number Of Sales But Reduce Savings

Introduce Smaller Pack Sizes At Lower Prices

Offer Larger Sizes With Lower Price Per Unit 77%

54%

44%

39%

36%

34%

16%

... And They’ll Continue To Search Out Trusted Brands Across The Store

10 Promotional Strategies To Connect To How Shoppers Are Shopping

Circular tactics built around whole meals will resonate with the growing number of shoppers carefully budgeting and planning their menus.

Sales across multiple quality levels within a category help maintain your store appeal with both brand loyalists and shoppers now more willing to trade down.

Increased sampling of product across the store can encourage shoppers – especially low income – to make a purchase they had not intended.

Shoppers are already skipping aisles and may do so even more – tempt them to shop all aisles with featured super-low prices on attractive items in every aisle.

With savings-minded shoppers increasingly buying big or small, let them know about the different product sizes you offer.

As shoppers of all types become more proactive in their planning, attract them with complementary product sales – buy a bagged salad, save on your favorite dressing.

Cross-promote right at the shelf to stimulate sales in categories consumers are ready to abandon in tough times – for example, coupons for cookies in the milk section.

With bulk buying for sharing on the rise, showcase “friends and family” specials of your economy sizes.

Tag products that have a high wellness quotient – two-thirds of adults say health drives their food selections.

Position yourself as a complete one-stop shop for essential categories to draw shoppers cutting back on trips due to high gas prices.

1234

56

89

10

7

Winning Shoppers in Turbulent TimesA Unilever Trip Management Report16

From smart circulars to sampling to complementary product sales, these tried and true techniques are even more critical now.

17Winning Shoppers in Turbulent TimesA Unilever Trip Management Report

Are Your Stores Positioned To Win Shoppers In Turbulent Times?

Shoppers Want Value & Savings• Are savings consistently offered in key categories?

• does your value proposition go beyond dollars and cents?

• is value communicated at every contact point with the shopper?

Shoppers Want Wellness• when shoppers are thinking of good-for-you food, are they

thinking of you?

• when they think good-for-you beyond food, is your store on their radar?

• do you offer special services or events that can stretch their wellness dollar?

Shoppers Want A Little Extra Help• do you have the personnel and programs to help shoppers make

smart shopping decisions?

• do you merchandise meal and home solutions that de-stress and simplify their shop?

• do you help them save money or make it convenient traveling to and from your store?

Shoppers Want Some Fun• do your stores have a “personality” that helps them forget their

daily challenges while they shop?

• do you encourage her to treat and take care of herself while she’s thinking of others as she walks the aisles?

• do you offer the occasional surprise reward for her big basket?

Collaborate with Unilever to create custom solutions for your shoppers.

Keeping The Shopping Experience Good For Everyone: Unilever’s Commitment To You

As a global leader, Unilever has a world of experience and resources to help

you and your shoppers successfully navigate the new economy. Unilever

delivers for you. With the brands and quality that instill high consumer

confidence. With product value tiers and packaging that are right for any

pocketbook. With the promotional savvy and merchandising expertise that

help your stores connect with today’s shopper.

Our research for this report has yielded great knowledge on how key shoppers

shop categories across your store in today’s economy. For the study, Unilever

looked at categories throughout the store, with a deep dive on 36 strategic

categories. This gives us a unique total store perspective that can drive

winning solutions.

We’re ready to share our insight with you.

Sustaining market leadership and success in the new economy requires working together and fresh thinking. Let’s start today.

Shopping List

Retail Solutions Begin With

FROM INSIGHT TO OPPORTUNITY

©2008 Unilever

™