Embed Size (px)

Citation preview

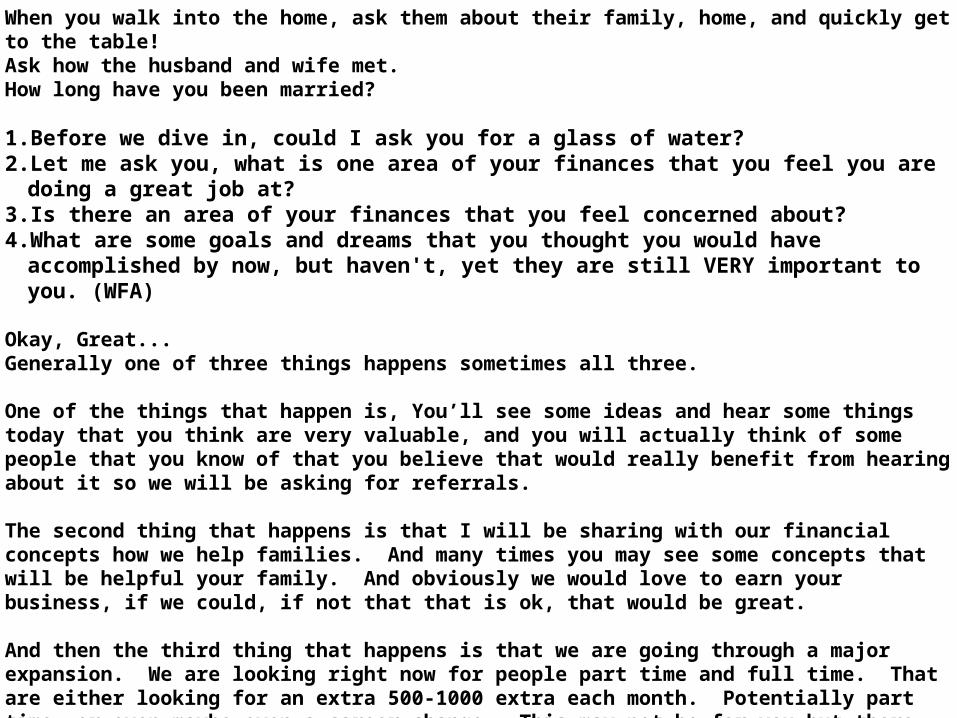

When you walk into the home, ask them about their family, home, and quickly get to the table!Ask how the husband and wife met.How long have you been married? 1. Before we dive in, could I ask you for a glass of water?2. Let me ask you, what is one area of your finances that you feel you are doing a great job

at?3. Is there an area of your finances that you feel concerned about?4. What are some goals and dreams that you thought you would have accomplished by now,

but haven't, yet they are still VERY important to you. (WFA)

Okay, Great...Generally one of three things happens sometimes all three.

One of the things that happen is, You’ll see some ideas and hear some things today that you think are very valuable, and you will actually think of some people that you know of that you believe that would really benefit from hearing about it so we will be asking for referrals.

The second thing that happens is that I will be sharing with our financial concepts how we help families. And many times you may see some concepts that will be helpful your family. And obviously we would love to earn your business, if we could, if not that that is ok, that would be great.

And then the third thing that happens is that we are going through a major expansion. We are looking right now for people part time and full time. That are either looking for an extra 500-1000 extra each month. Potentially part time, or even maybe even a career change. This may not be for you but there are 5 different groups of people that are drawn to our company...

The Five Reasons People Desire A Change

Can you see where most people would be

interested in at least one of these areas?

1Don’t like

current job –looking for a

career change,

better incomepotential

2Love what

theydo, but earning

extra part-time income

would make adifference

3Want financial

education –learn howto win the

money game

4Love helpingpeople andmaking adifference

5Dream ofhaving

their ownbusiness

2

The Financial Services Company For the 21st Century

• Founded in 1977 with 85 people

• Approximately 100,000 licensed representatives

• 6 million clients in the United States, Canada and Puerto Rico

• Largest Financial Services marketing organization in North America

• (PRI) Listed on NYSE

All accomplished without

any national TV or radio

advertising!

®

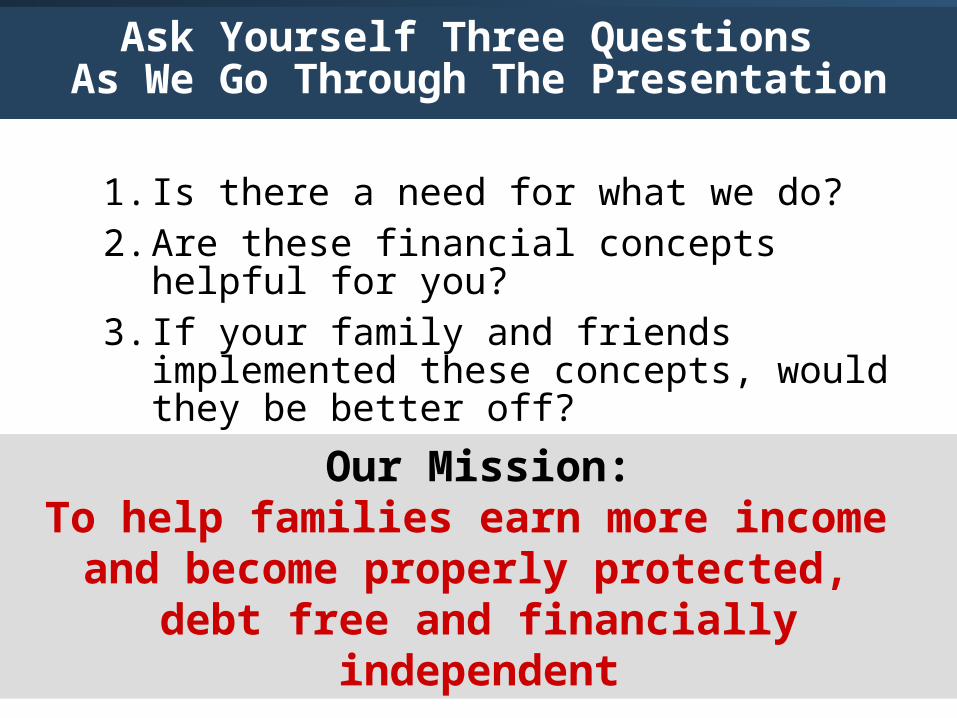

Ask Yourself Three Questions As We Go Through The Presentation

1. Is there a need for what we do?2. Are these financial concepts helpful for

you?3. If your family and friends implemented

these concepts, would they be better off?

Our Mission:To help families earn more income and become properly protected,

debt free and financially independent

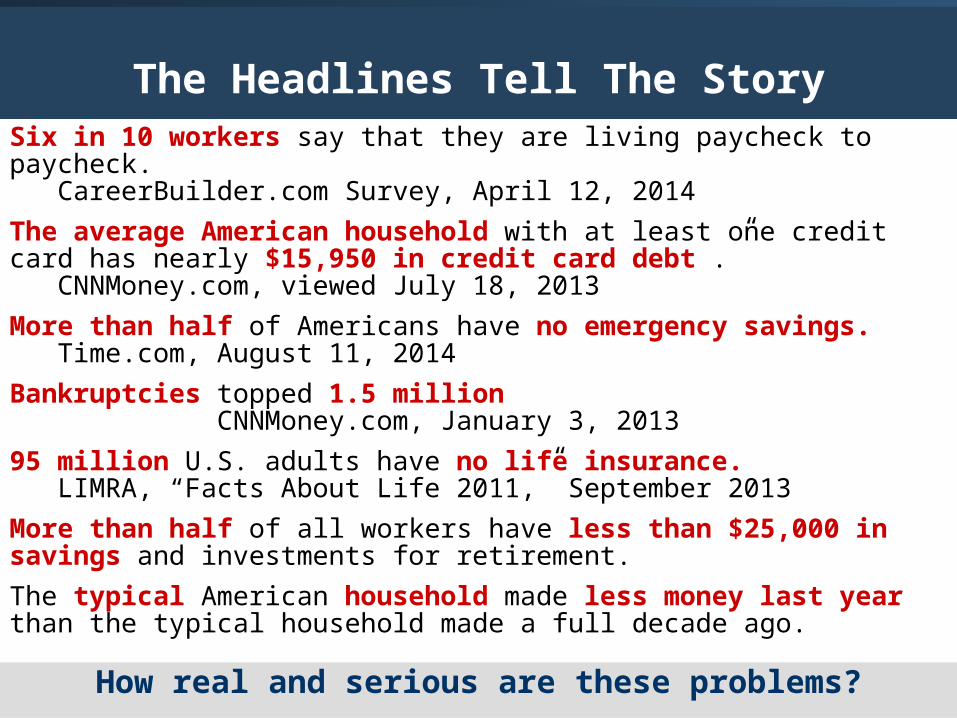

The Headlines Tell The StorySix in 10 workers say that they are living paycheck to paycheck.

CareerBuilder.com Survey, April 12, 2014

The average American household with at least one credit card has nearly $15,950 in credit card debt .”

CNNMoney.com, viewed July 18, 2013

More than half of Americans have no emergency savings.Time.com, August 11, 2014

Bankruptcies topped 1.5 million CNNMoney.com, January 3, 2013

95 million U.S. adults have no life insurance.LIMRA, “Facts About Life 2011,” September 2013

More than half of all workers have less than $25,000 in savings and investments for retirement.

The typical American household made less money last year than the typical household made a full decade ago.

How real and serious are these problems?

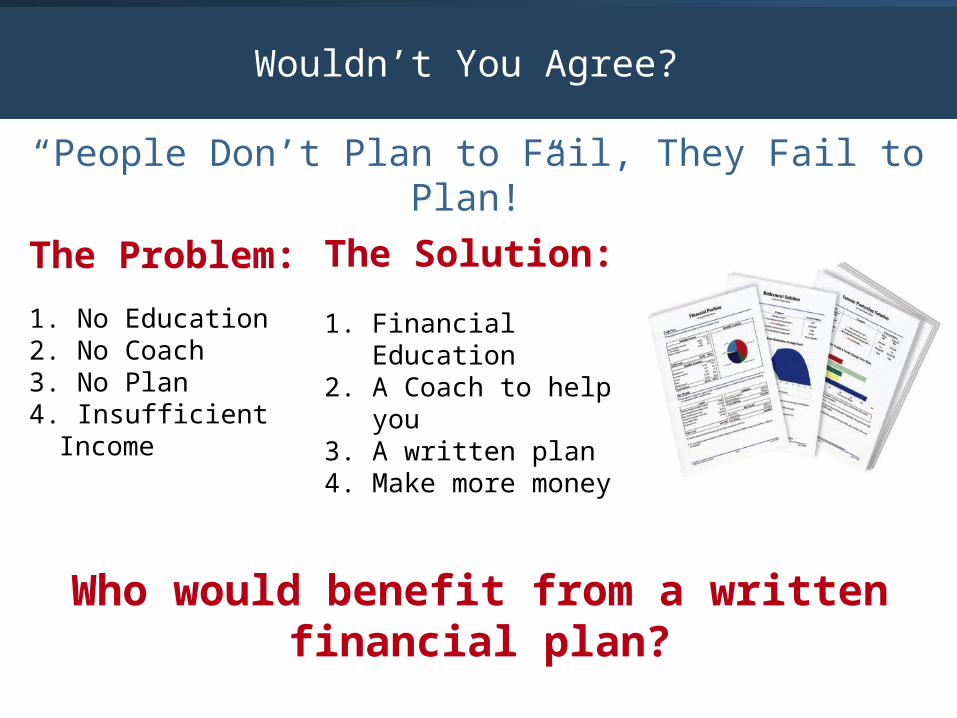

The Problem: 1. No Education2. No Coach 3. No Plan4. Insufficient

Income

Wouldn’t You Agree?

“People Don’t Plan to Fail, They Fail to Plan!”

The Solution:

1. Financial Education2. A Coach to help you3. A written plan4. Make more money

Who would benefit from a written financial plan?

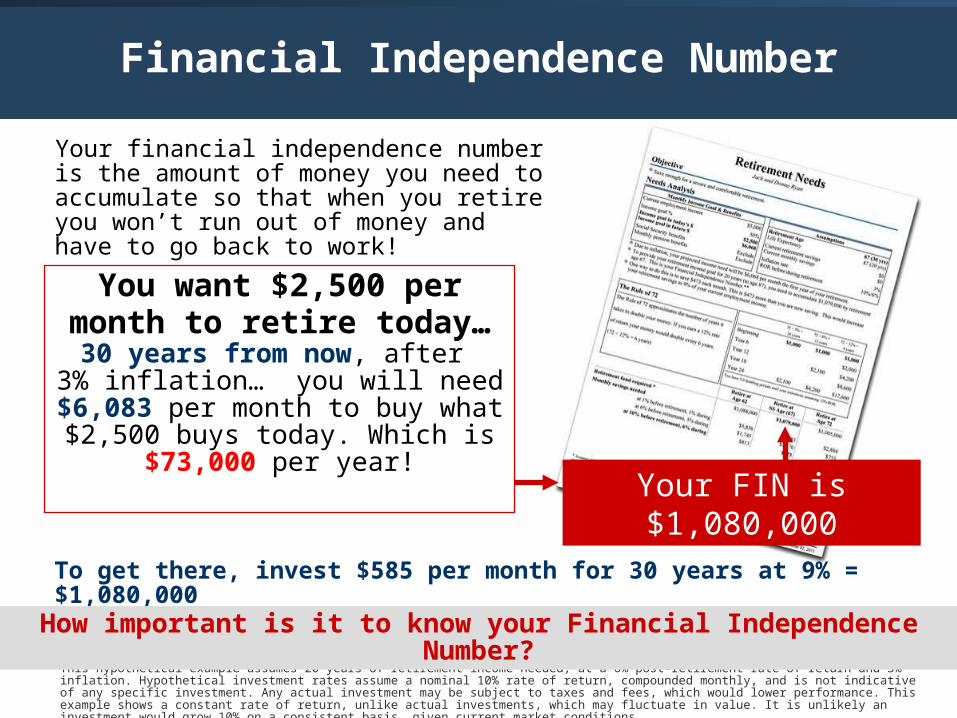

Financial Independence Number

Your financial independence number is the amount of money you need to accumulate so that when you retire you won’t run out of money and have to go back to work!

To get there, invest $585 per month for 30 years at 9% = $1,080,000

You want $2,500 per month to retire today…

30 years from now, after 3% inflation… you will need

$6,083 per month to buy what $2,500 buys today. Which is

$73,000 per year!Your FIN is $1,080,000

This hypothetical example assumes 20 years of retirement income needed, at a 6% post-retirement rate of return and 3% inflation. Hypothetical investment rates assume a nominal 10% rate of return, compounded monthly, and is not indicative of any specific investment. Any actual investment may be subject to taxes and fees, which would lower performance. This example shows a constant rate of return, unlike actual investments, which may fluctuate in value. It is unlikely an investment would grow 10% on a consistent basis, given current market conditions.

How important is it to know your Financial Independence Number?

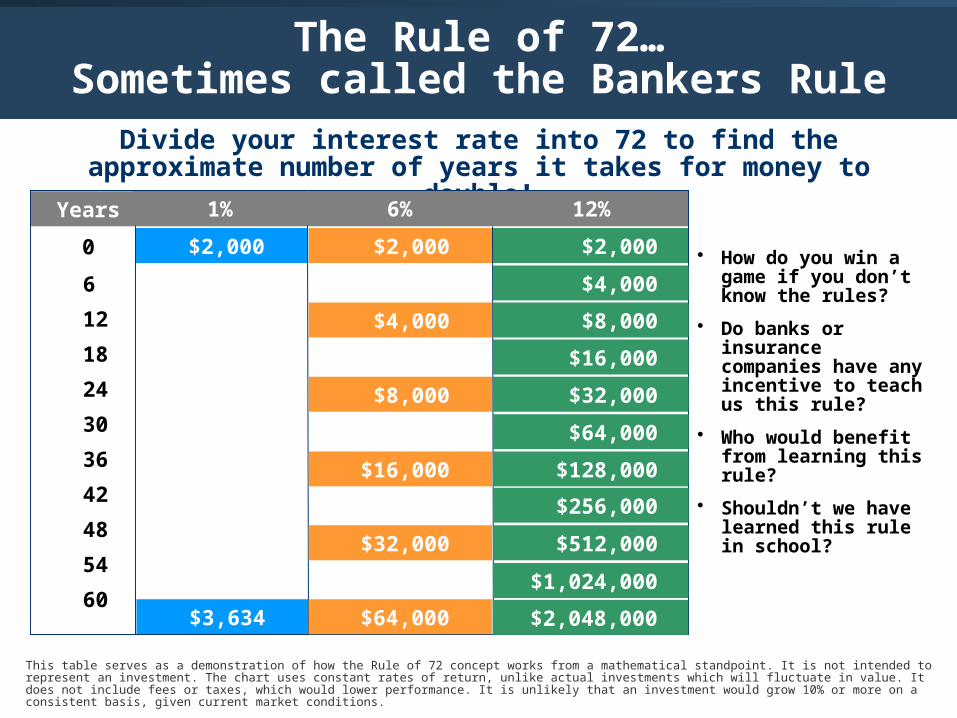

The Rule of 72…Sometimes called the Bankers Rule

Divide your interest rate into 72 to find theapproximate number of years it takes for money to

double!

This table serves as a demonstration of how the Rule of 72 concept works from a mathematical standpoint. It is not intended to represent an investment. The chart uses constant rates of return, unlike actual investments which will fluctuate in value. It does not include fees or taxes, which would lower performance. It is unlikely that an investment would grow 10% or more on a consistent basis, given current market conditions.

• How do you win a game if you don’t know the rules?

• Do banks or insurance companies have any incentive to teach us this rule?

• Who would benefit from learning this rule?

• Shouldn’t we have learned this rule in school?

Years 1% 6% 12%

$3,634

6

12

18

24

30

36

42

48

54

60

$2,000 $2,000 $2,0000

1% 6% 12%

$4,000

$8,000

$16,000

$32,000

$64,000

$4,000

$8,000

$16,000

$32,000

$64,000

$128,000

$256,000

$512,000

$1,024,000

$2,048,000

The First Step to Financial Success is Pay Yourself First

When you don’t, there’s a high cost of waiting.

$100 Monthly Savings @ 9% for 40 Years (Age 27-67)

42$112,950(-$358,690)

32 $296,380(-$175,260)

28 $430,040(-$41,600)

27 $471,640

Rates of return are constant and nominal rates, compounded monthly. Contributions are assumed to be made at the beginning of the month. The chart above is not indicative of any particular investment or savings vehicle where rates of return fluctuate. It does not take into consideration taxes or other applicable deductions, which would lower results.

Wait 15 years($18,000)

Wait 5 years($6,000)

Wait 1 year($1,200)

Who are people hurting if they wait?

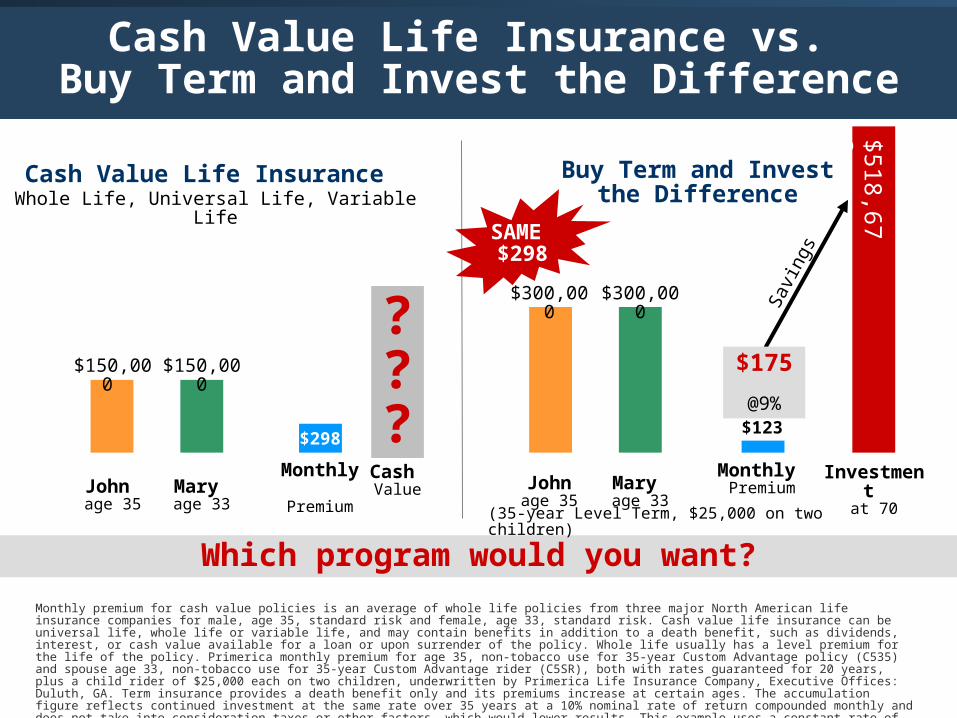

SAME $298

Cash Value Life Insurance vs. Buy Term and Invest the Difference

Cash Value Life Insurance Whole Life, Universal Life, Variable Life

Which program would you want?

Buy Term and Investthe Difference

(35-year Level Term, $25,000 on two children)

$150,000

John age 35

$150,000

Mary age 33

$300,000

Mary age 33

$300,000

Johnage 35

$298

Monthly

Premium

$123

Monthly Premium

Investment

at 70

$51

8,6

73

Monthly premium for cash value policies is an average of whole life policies from three major North American life insurance companies for male, age 35, standard risk and female, age 33, standard risk. Cash value life insurance can be universal life, whole life or variable life, and may contain benefits in addition to a death benefit, such as dividends, interest, or cash value available for a loan or upon surrender of the policy. Whole life usually has a level premium for the life of the policy. Primerica monthly premium for age 35, non-tobacco use for 35-year Custom Advantage policy (C535) and spouse age 33, non-tobacco use for 35-year Custom Advantage rider (C5SR), both with rates guaranteed for 20 years, plus a child rider of $25,000 each on two children, underwritten by Primerica Life Insurance Company, Executive Offices: Duluth, GA. Term insurance provides a death benefit only and its premiums increase at certain ages. The accumulation figure reflects continued investment at the same rate over 35 years at a 10% nominal rate of return compounded monthly and does not take into consideration taxes or other factors, which would lower results. This example uses a constant rate of return, unlike actual investments, which will fluctuate in value. This is hypothetical and does not represent an actual investment. It is unlikely an investment would grow 10% on a consistent basis, given current market conditions.

Cash Value

???

Savi

ngs

$175

@9%

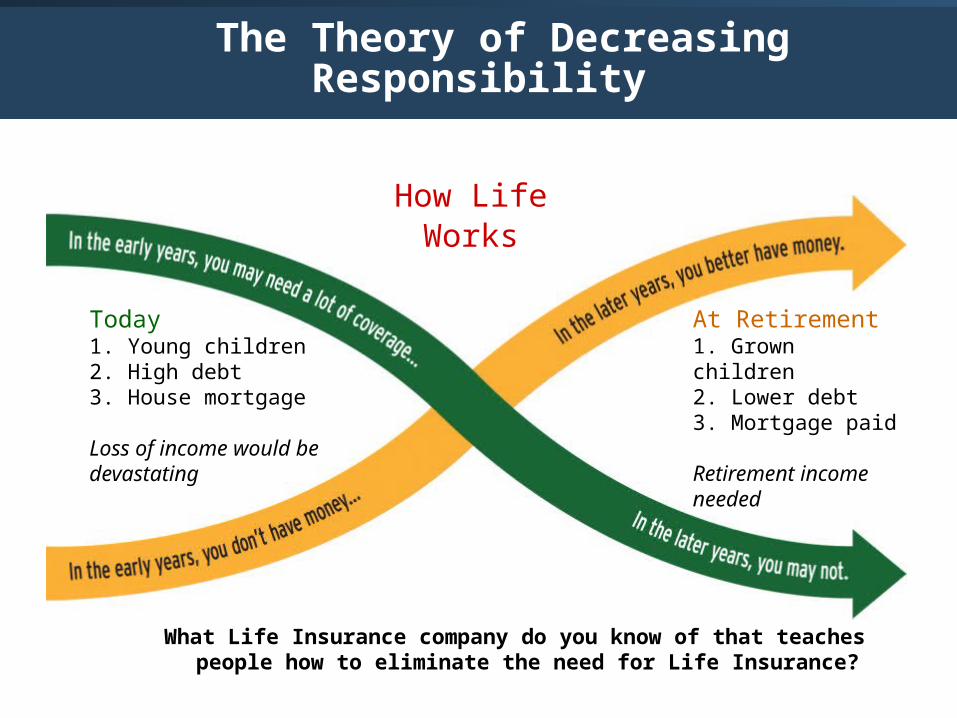

Today1. Young children2. High debt3. House mortgage

Loss of income would be devastating

At Retirement1. Grown children2. Lower debt3. Mortgage paid

Retirement income needed

How Life Works

The Theory of Decreasing Responsibility

What Life Insurance company do you know of that teaches people how to eliminate the need for Life Insurance?

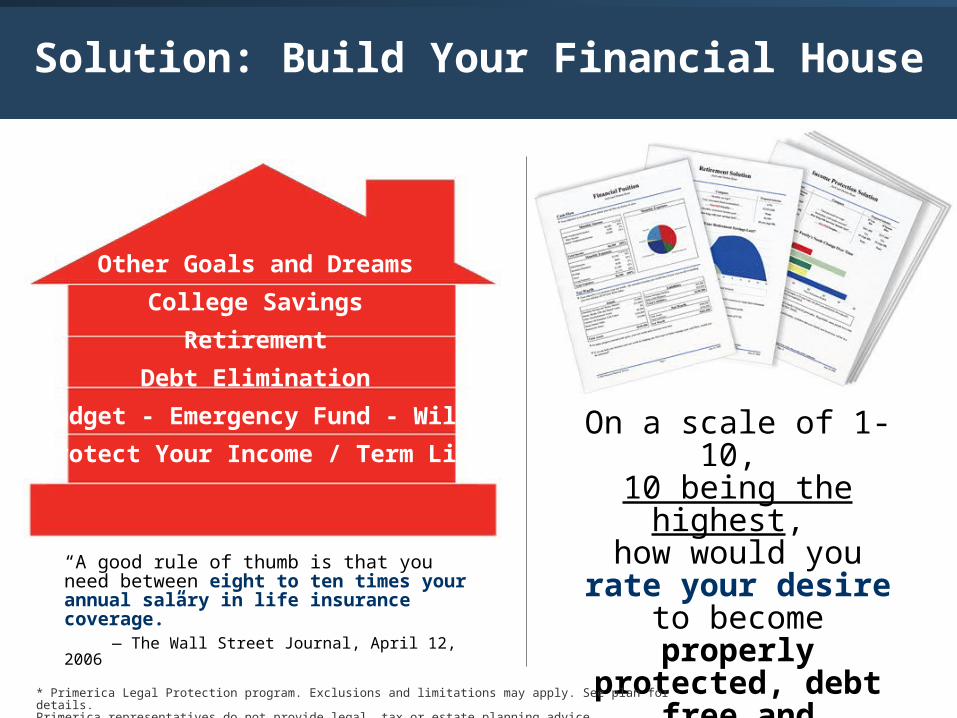

Solution: Build Your Financial House

“A good rule of thumb is that you need between eight to ten times your annual salary in life insurance coverage.”

— The Wall Street Journal, April 12, 2006

Other Goals and Dreams

College Savings

Retirement

Debt Elimination

Budget - Emergency Fund - Will*

Protect Your Income / Term Life On a scale of 1-10,

10 being the highest,

how would you rate your desire to

become properly protected, debt

free and financially

independent?* Primerica Legal Protection program. Exclusions and limitations may apply. See plan for details. Primerica representatives do not provide legal, tax or estate planning advice.