Embed Size (px)

Citation preview

What You Need to Know for the FAR ExamAugust 3, 2016

Introductions

• Denise ProbertCPA, CGMAWiley Director of Curriculum,Accounting Test Prep

• Julie SnowWiley CPAexcel Product Support

Webinar Agenda

• Current format of the FAR exam• Current content tested on the FAR exam• Format and content changes expected to the FAR exam on

and after April 1, 2017• Tips and techniques for passing FAR• Raffle!• Ask the Expert

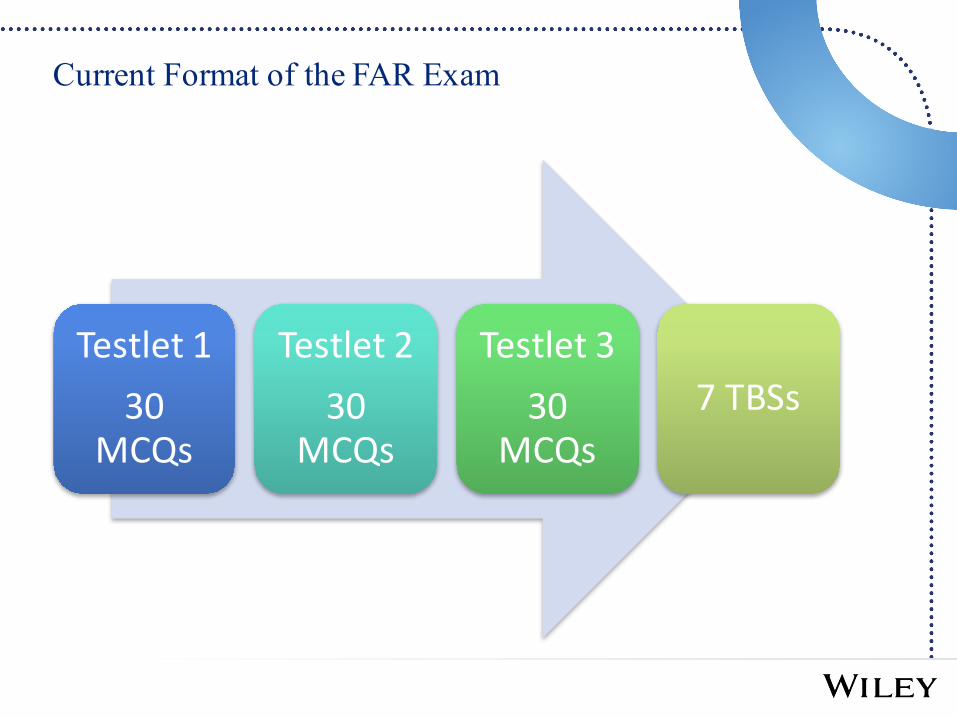

Current Format of the FAR Exam

Testlet 130

MCQs

Testlet 230

MCQs

Testlet 330

MCQs7 TBSs

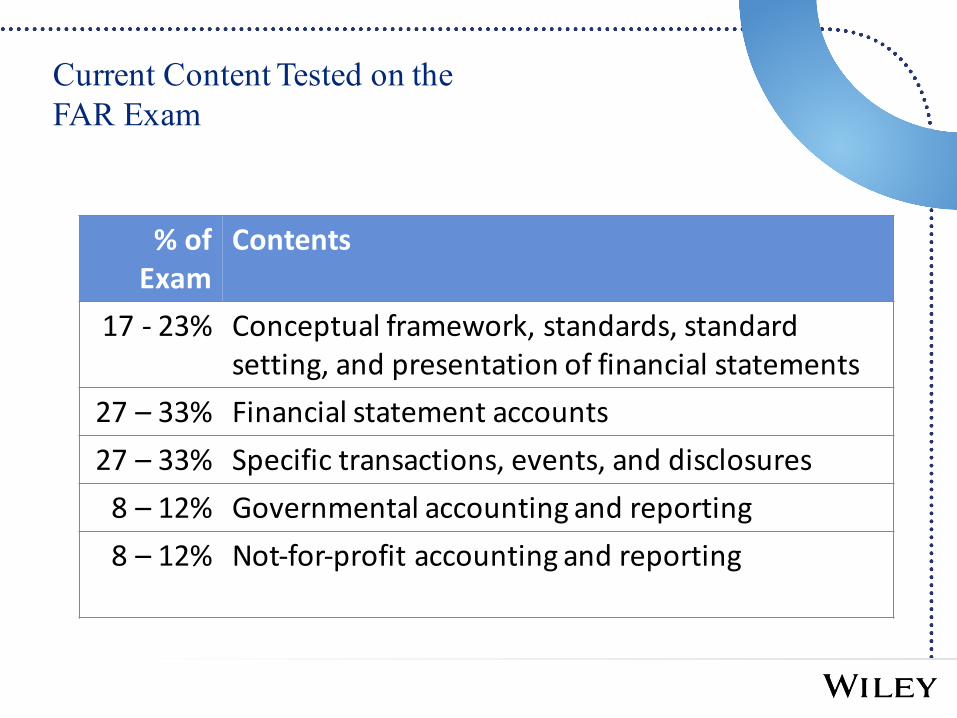

% of Exam

Contents

17 -‐ 23% Conceptual framework, standards, standard setting, and presentation of financial statements

27 – 33% Financial statement accounts27 – 33% Specific transactions, events, and disclosures8 – 12% Governmental accounting and reporting8 – 12% Not-‐for-‐profit accounting and reporting

Current Content Tested on the FAR Exam

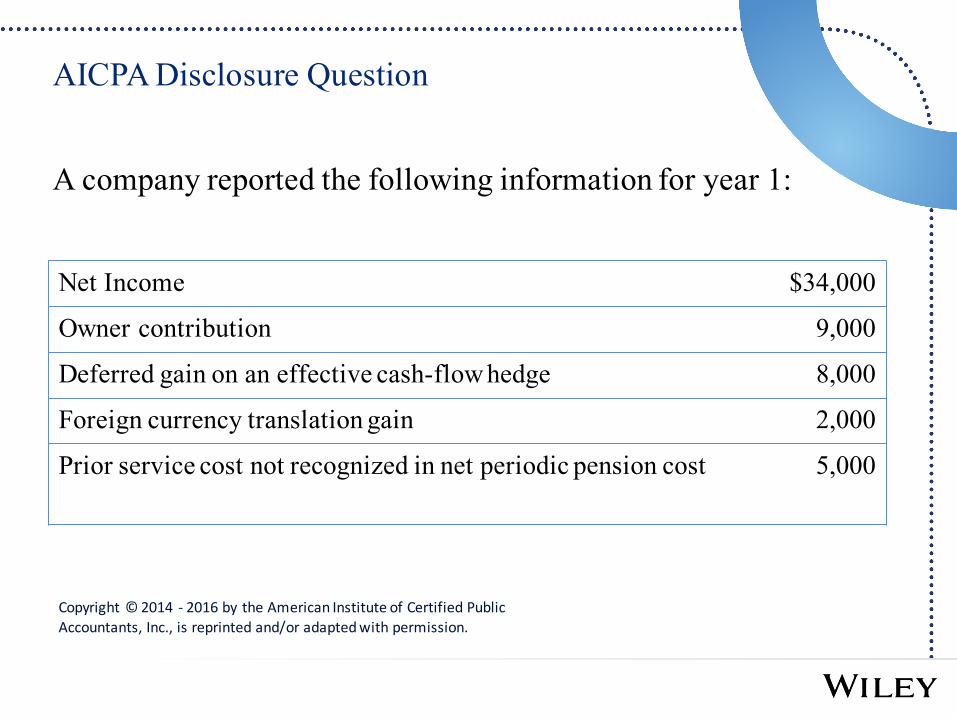

Net Income $34,000

Owner contribution 9,000

Deferred gain on an effective cash-flow hedge 8,000

Foreign currency translation gain 2,000

Prior service cost not recognized in net periodic pension cost 5,000

AICPA Disclosure Question

A company reported the following information for year 1:

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

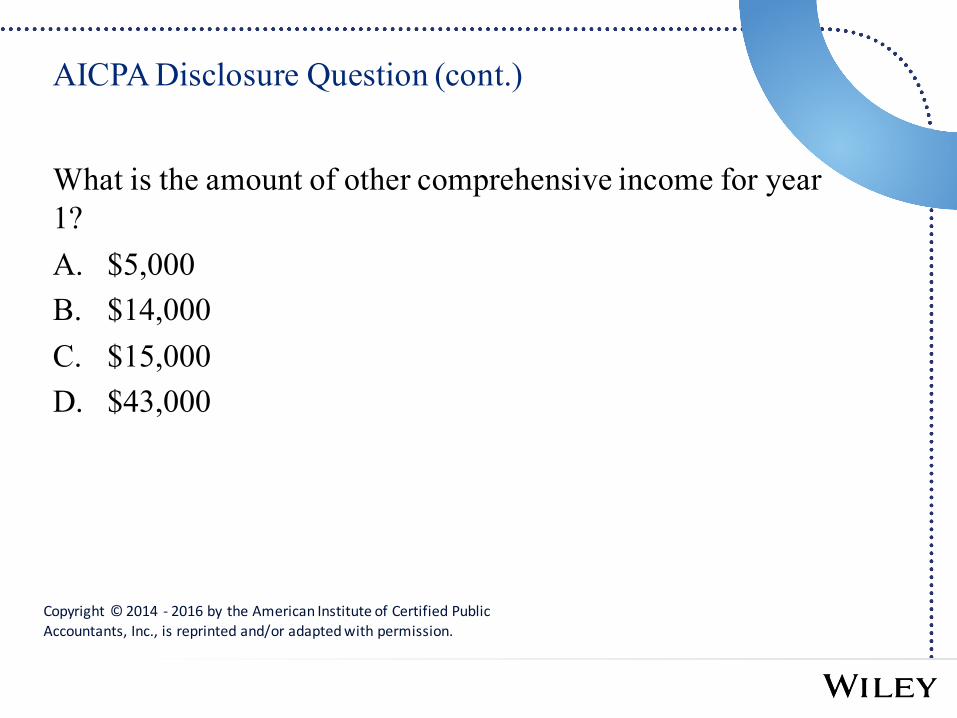

AICPA Disclosure Question (cont.)

What is the amount of other comprehensive income for year 1?A. $5,000B. $14,000C. $15,000D. $43,000

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

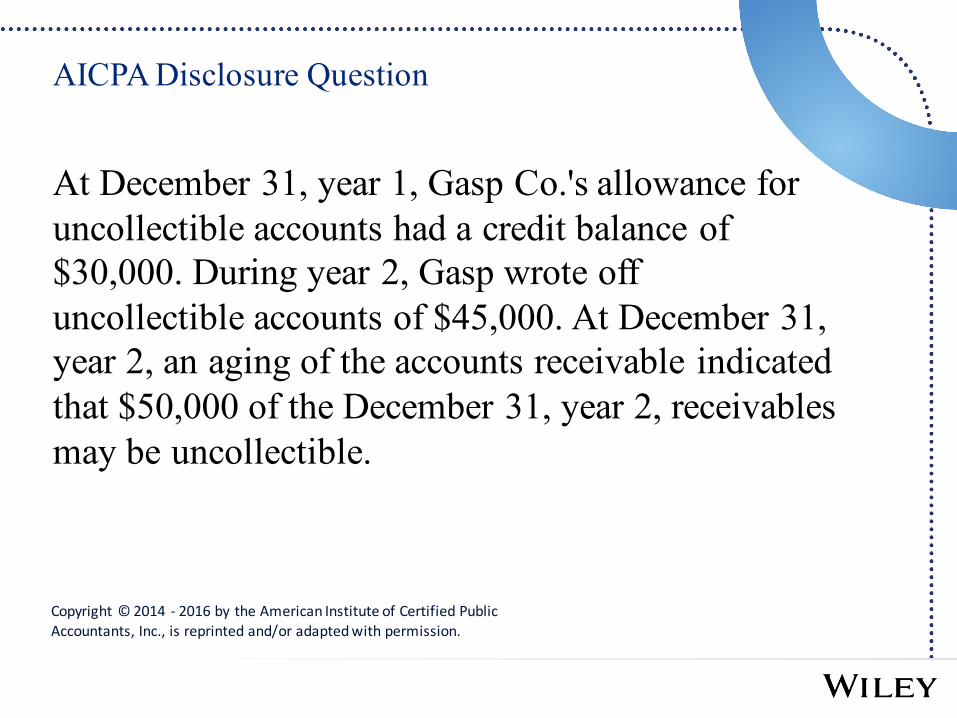

AICPA Disclosure Question

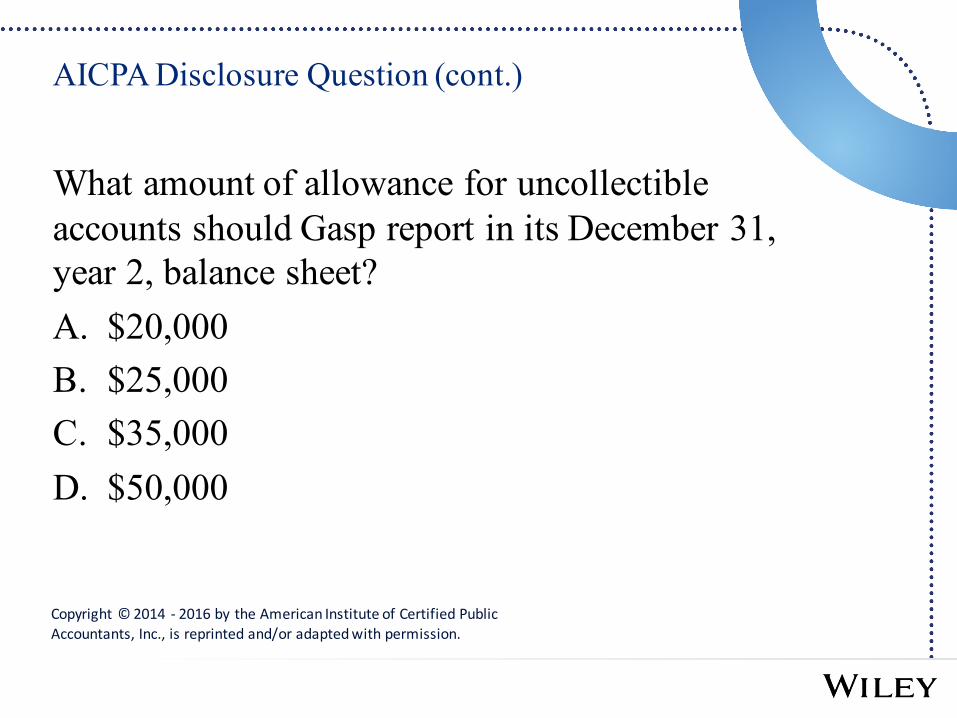

At December 31, year 1, Gasp Co.'s allowance for uncollectible accounts had a credit balance of $30,000. During year 2, Gasp wrote off uncollectible accounts of $45,000. At December 31, year 2, an aging of the accounts receivable indicated that $50,000 of the December 31, year 2, receivables may be uncollectible.

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question (cont.)

What amount of allowance for uncollectible accounts should Gasp report in its December 31, year 2, balance sheet?A. $20,000B. $25,000C. $35,000D. $50,000

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

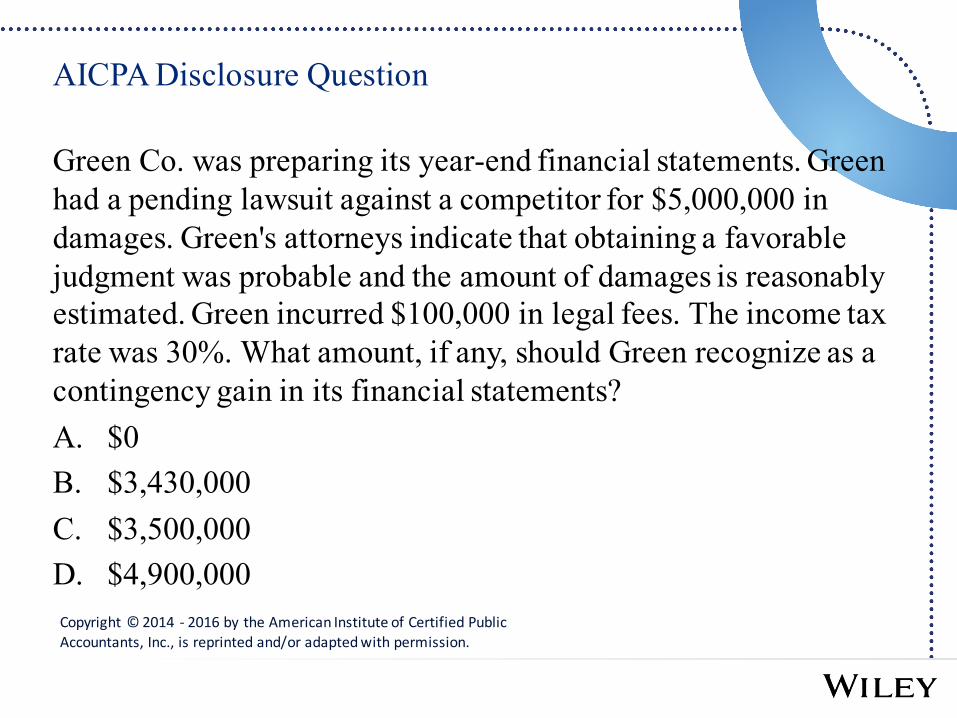

Green Co. was preparing its year-end financial statements. Green had a pending lawsuit against a competitor for $5,000,000 in damages. Green's attorneys indicate that obtaining a favorable judgment was probable and the amount of damages is reasonably estimated. Green incurred $100,000 in legal fees. The income tax rate was 30%. What amount, if any, should Green recognize as a contingency gain in its financial statements?A. $0B. $3,430,000C. $3,500,000D. $4,900,000Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

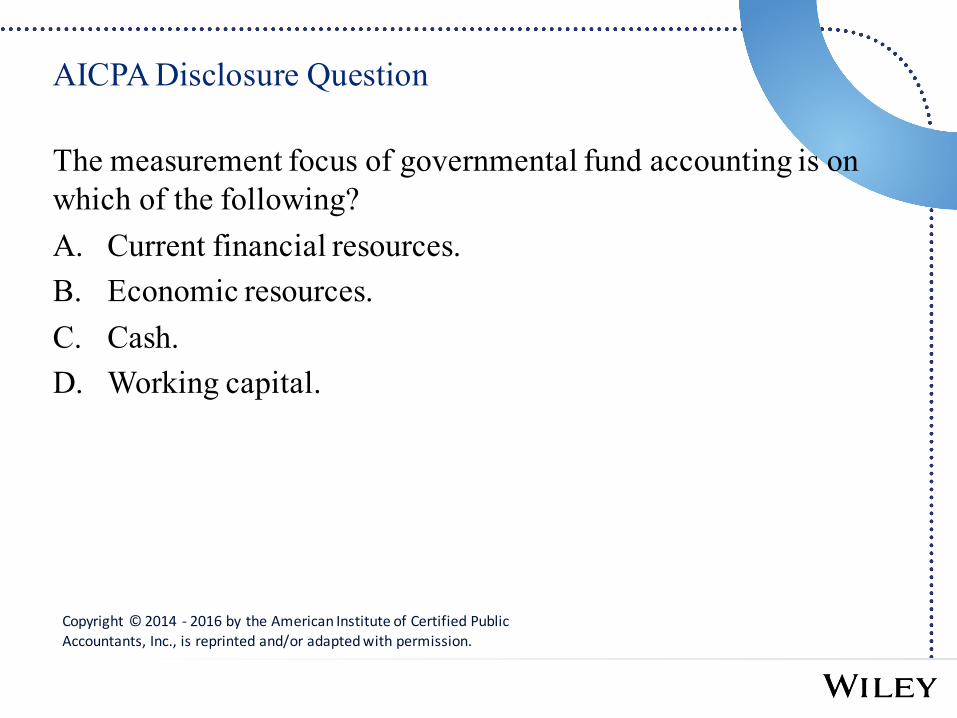

The measurement focus of governmental fund accounting is on which of the following?A. Current financial resources. B. Economic resources. C. Cash. D. Working capital.

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

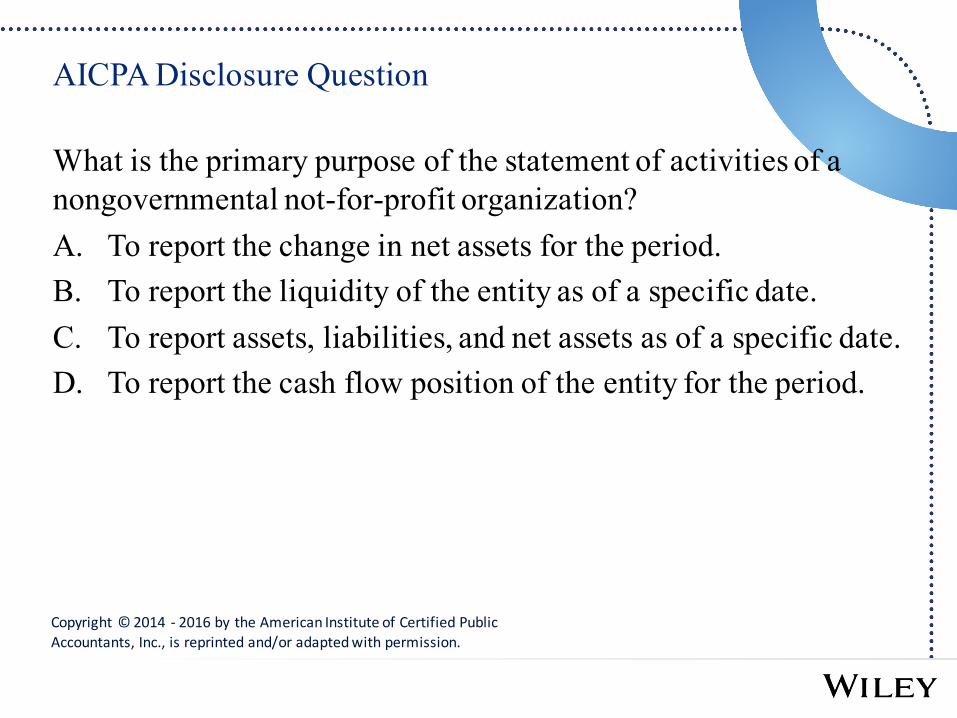

What is the primary purpose of the statement of activities of a nongovernmental not-for-profit organization?A. To report the change in net assets for the period. B. To report the liquidity of the entity as of a specific date. C. To report assets, liabilities, and net assets as of a specific date. D. To report the cash flow position of the entity for the period.

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

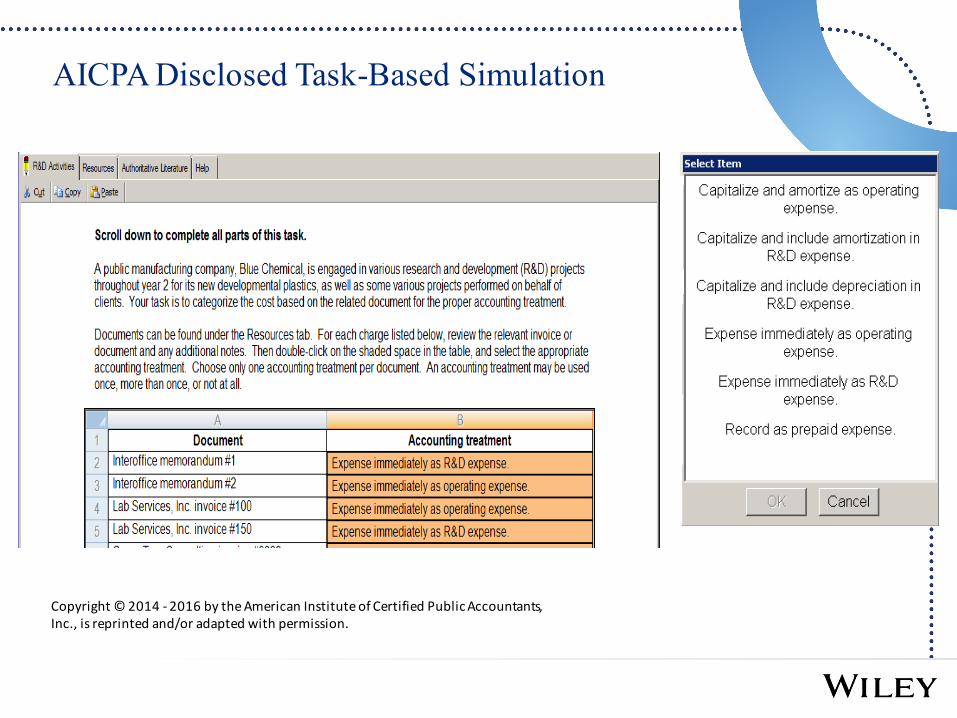

AICPA Disclosed Task-Based Simulation

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

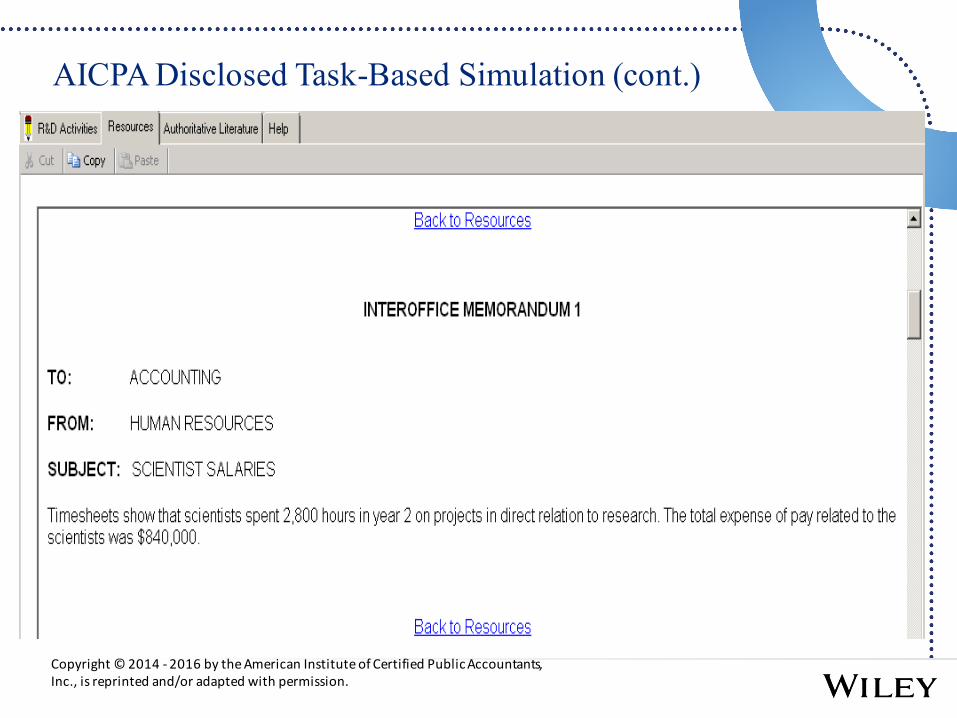

AICPA Disclosed Task-Based Simulation (cont.)

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

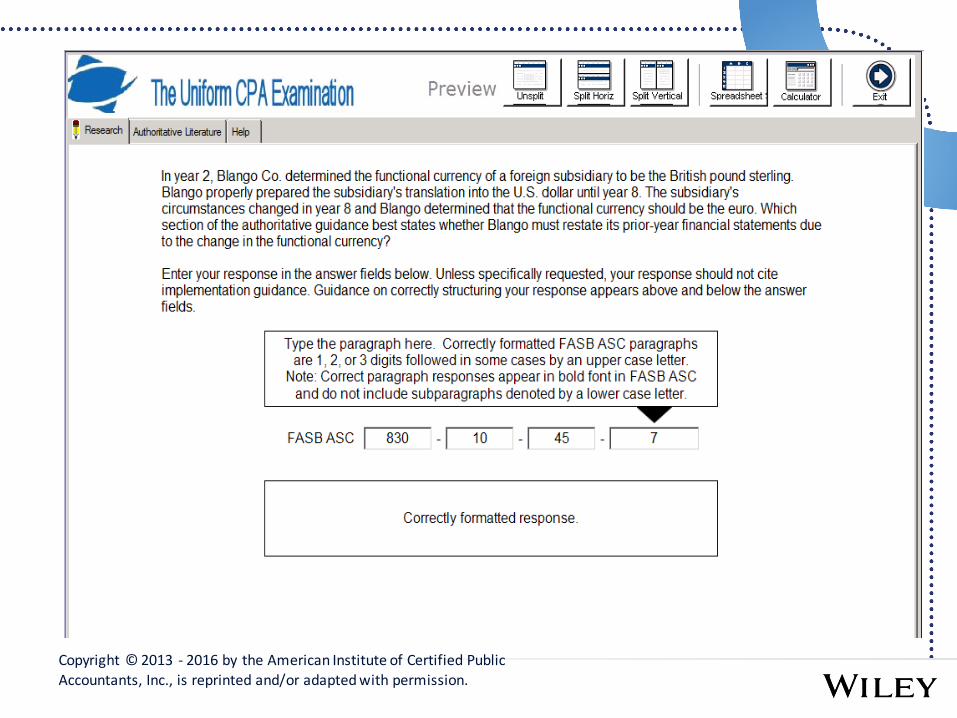

Copyright © 2013 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

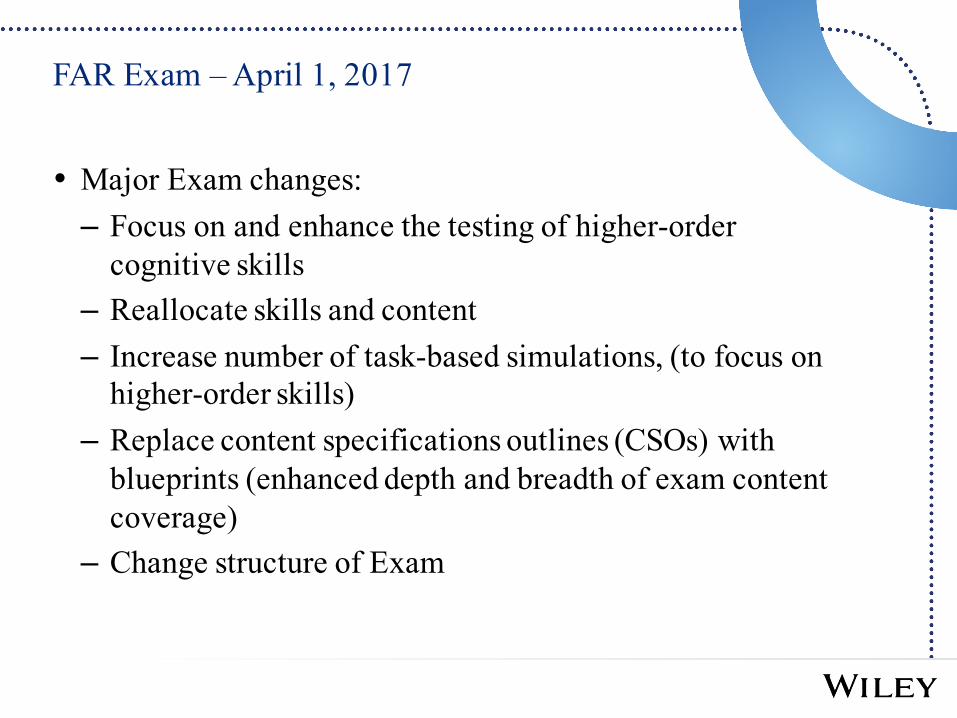

FAR Exam – April 1, 2017

• Major Exam changes:– Focus on and enhance the testing of higher-order

cognitive skills– Reallocate skills and content– Increase number of task-based simulations, (to focus on

higher-order skills)– Replace content specifications outlines (CSOs) with

blueprints (enhanced depth and breadth of exam content coverage)

– Change structure of Exam

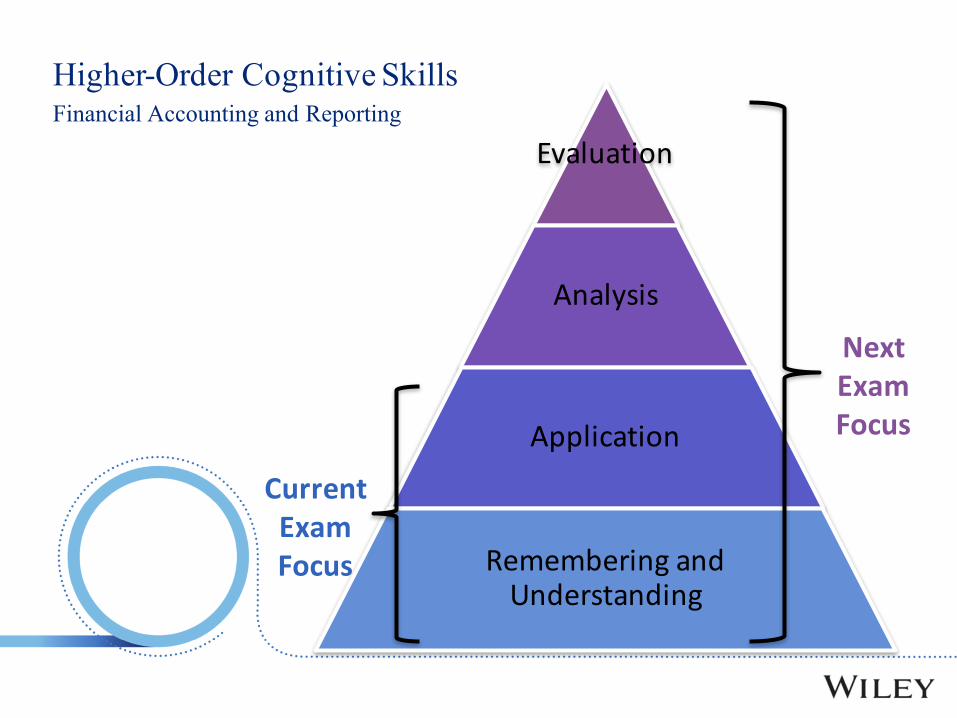

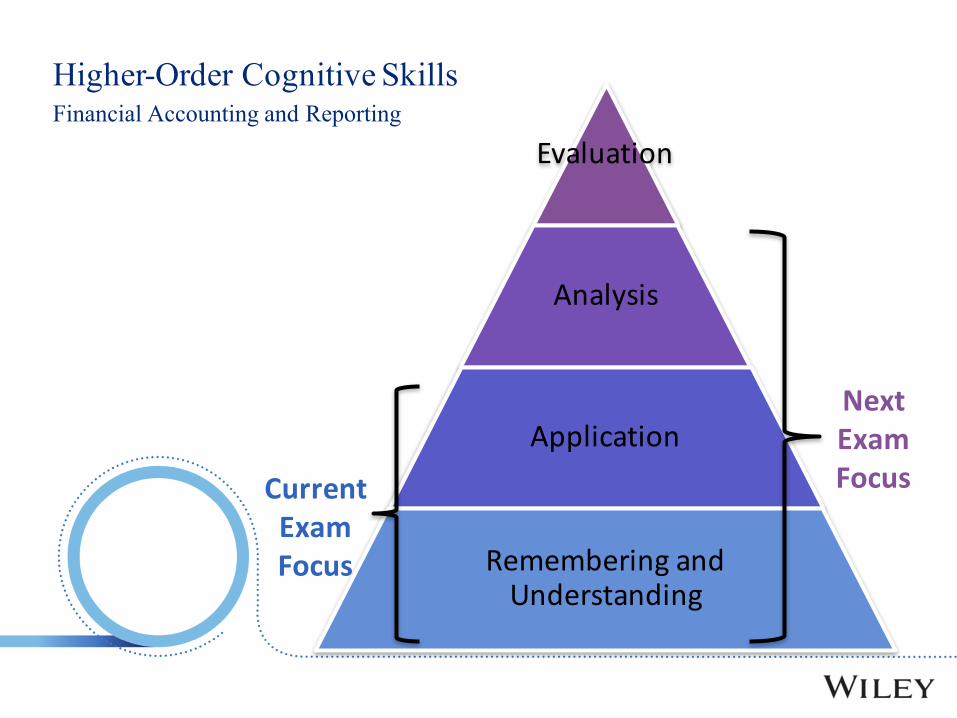

Higher-Order Cognitive SkillsFinancial Accounting and Reporting

Evaluation

Analysis

Application

Remembering and Understanding

Current Exam Focus

Next Exam Focus

Higher-Order Cognitive SkillsFinancial Accounting and Reporting

Evaluation

Analysis

Application

Remembering and Understanding

Current Exam Focus

Next Exam Focus

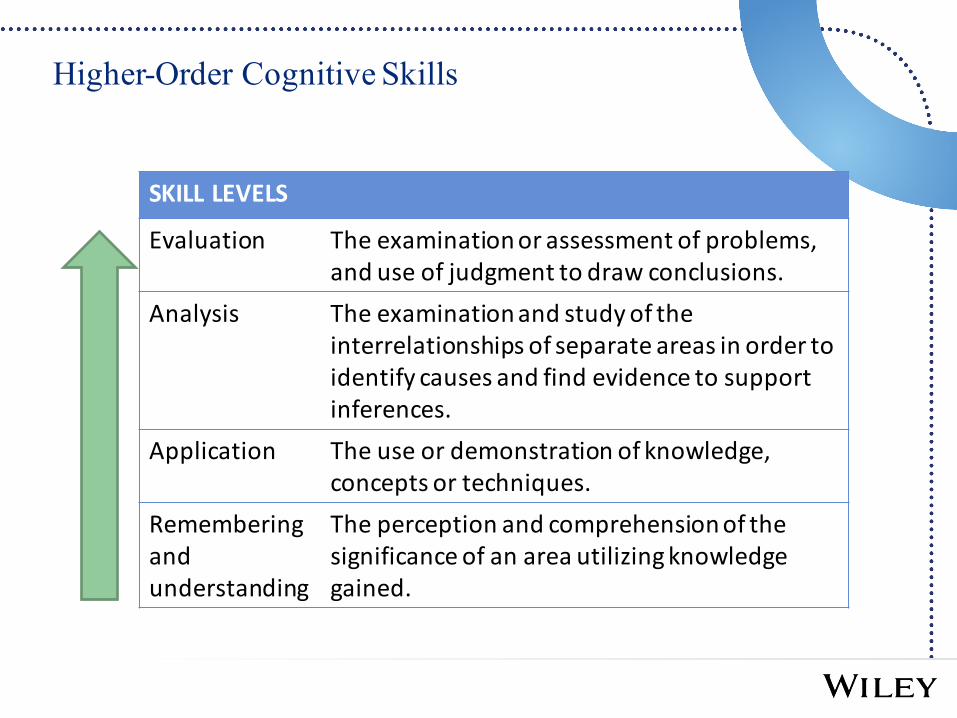

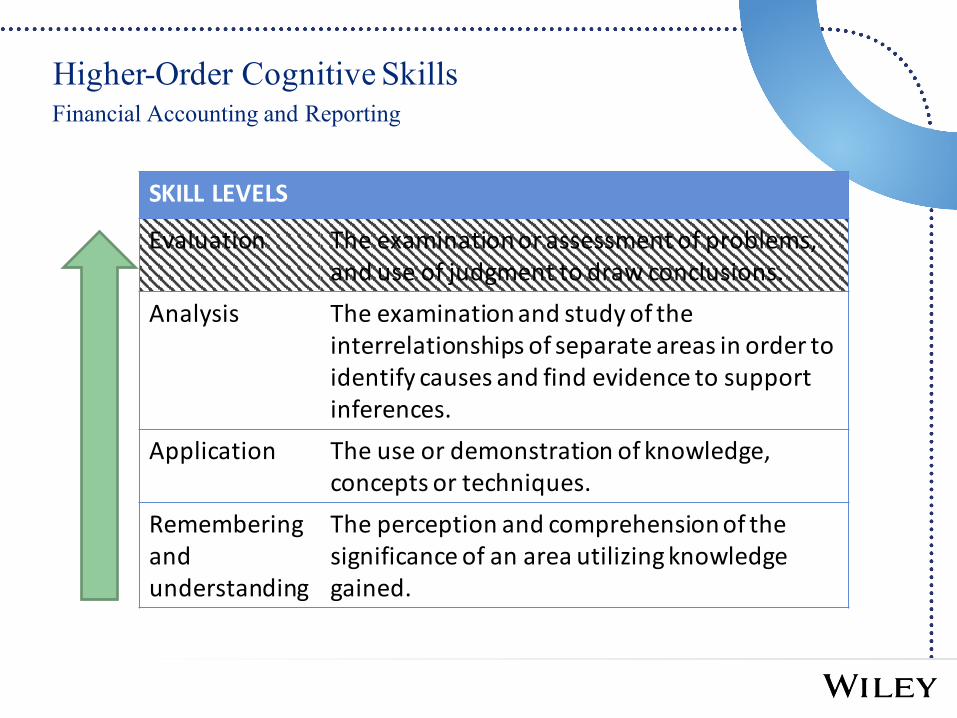

Higher-Order Cognitive Skills

SKILL LEVELS

Evaluation The examination or assessment of problems, and use of judgment to draw conclusions.

Analysis The examinationand study of the interrelationships of separate areas in order to identify causes and find evidence to support inferences.

Application The use or demonstration of knowledge, concepts or techniques.

Remembering and understanding

The perception and comprehension of the significance of an area utilizing knowledge gained.

Higher-Order Cognitive SkillsFinancial Accounting and Reporting

SKILL LEVELS

Evaluation The examination or assessment of problems, and use of judgment to draw conclusions.

Analysis The examinationand study of the interrelationships of separate areas in order to identify causes and find evidence to support inferences.

Application The use or demonstration of knowledge, concepts or techniques.

Remembering and understanding

The perception and comprehension of the significance of an area utilizing knowledge gained.

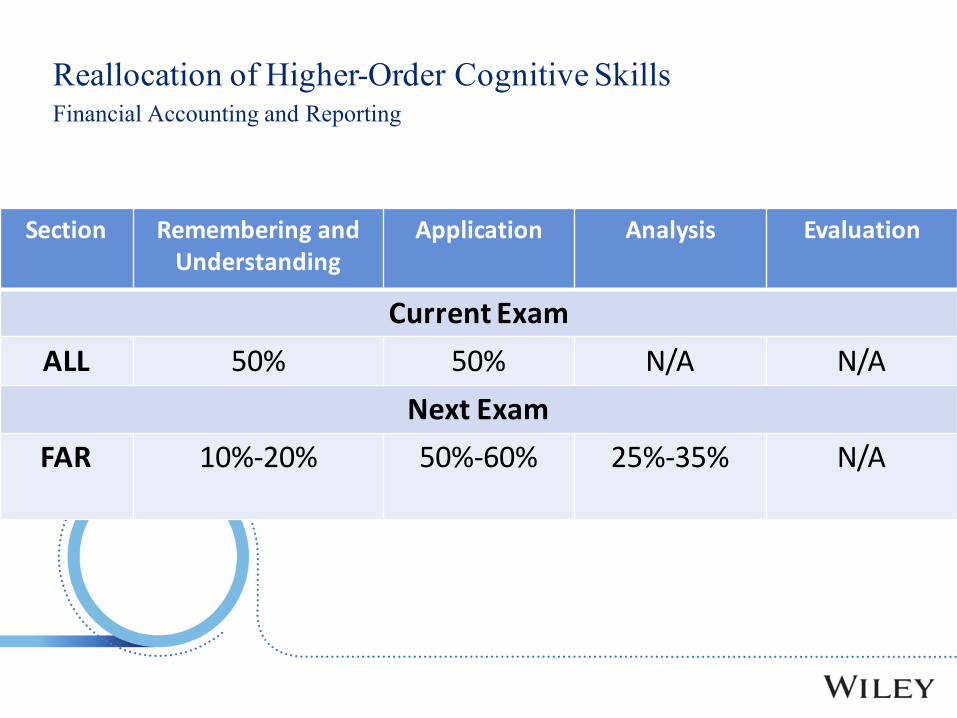

Reallocation of Higher-Order Cognitive SkillsFinancial Accounting and Reporting

Section Remembering and Understanding

Application Analysis Evaluation

Current ExamALL 50% 50% N/A N/A

Next ExamFAR 10%-‐20% 50%-‐60% 25%-‐35% N/A

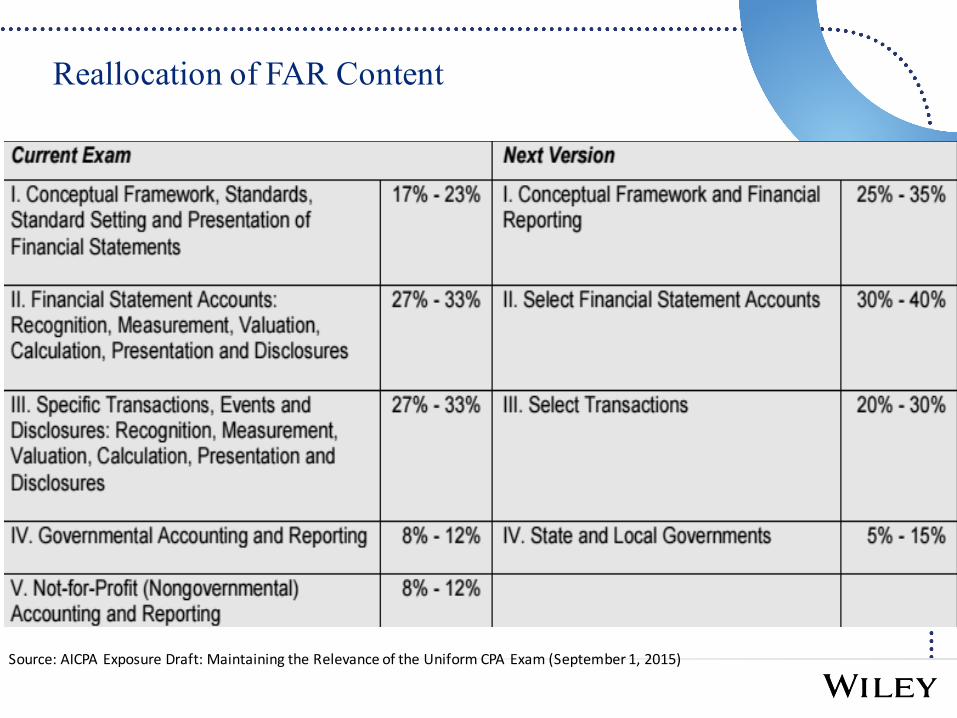

Reallocation of FAR Content

Source: AICPA Exposure Draft: Maintaining the Relevance of the Uniform CPA Exam (September 1, 2015)

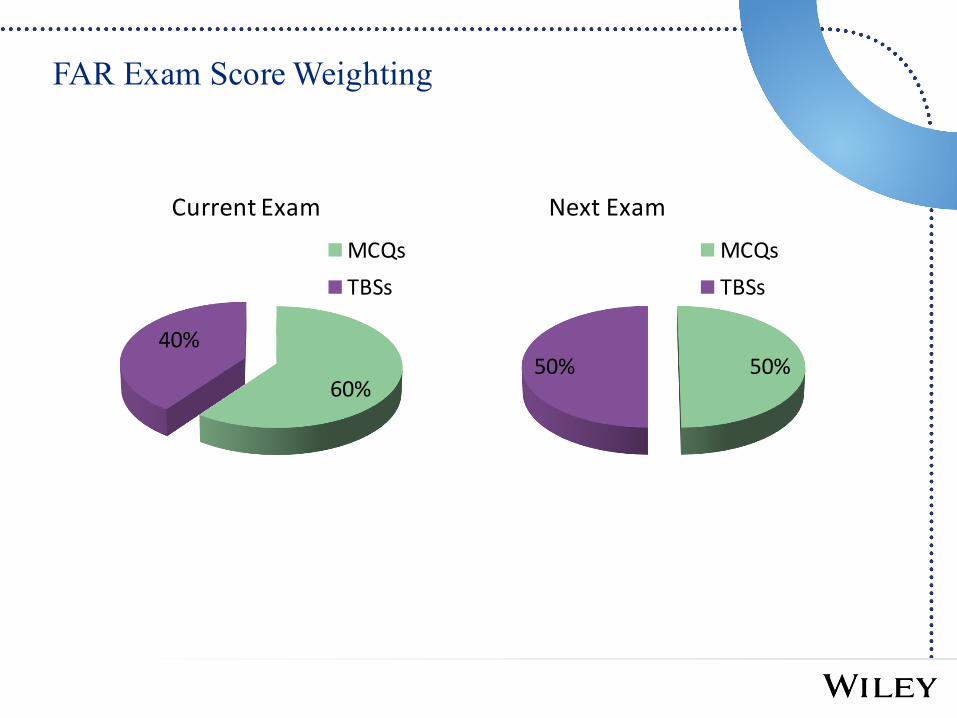

FAR Exam Score Weighting

60%

40%

MCQsTBSs

Current Exam

50%50%

MCQsTBSs

Next Exam

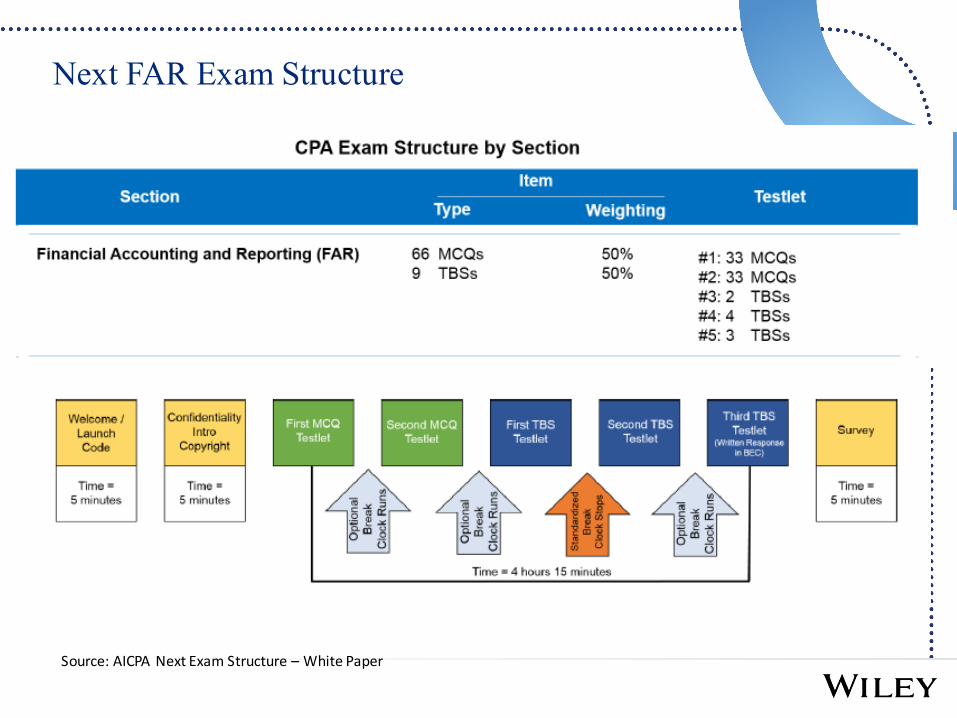

Next FAR Exam Structure

Source: AICPA Next Exam Structure – White Paper

Tips and Techniques for Passing FAR!

• FAR First!!• Study and practice• Time management• One question at a time• Do not leave a question blank• Be confident in yourself

Photo Credit: Probert, 2016

Raffle Time!

And the winner is…

We are giving away one complete Wiley CPAexcel Online Test Bank Retail value: $575

• 4,500+ CPA Exam Questions with Detailed Answers

• 160+ Task-based Simulations, Including 10+ New Document Review Simulations (DRS)

• Replicates the Prometric Interface

Ask the Expert