Embed Size (px)

Citation preview

1

Q2, 2014 Management Roadshow WHA Corporation Public Company Limited

The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in WHA Corporation Public Company Limited (“WHA” and shares in WHA, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. In addition, this presentation contains projections and forward-looking statements that reflect the Company's current views with respect to future events and financial performance. These views are based on a number of estimates and current assumptions which are subject to business, economic and competitive uncertainties and contingencies as well as various risks and these may change over time and in many cases are outside the control of the Company and its directors. You are cautioned not to place undue reliance on these forward looking statements, which are based on the current view of the management of the Company on future events. No assurance can be given that future events will occur, that projections will be achieved, or that the Company's assumptions are correct. The Company does not assume any responsibility to amend, modify or revise any forward-looking statements, on the basis of any subsequent developments, information or events, or otherwise. These statements can be recognized by the use of words such as “expects,” “plans,” “will,” “estimates,” “projects,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and actual results may differ from those forecast and projected or in the forward-looking statements as a result of various factors and assumptions.

Disclaimer

2

Agenda

3

4

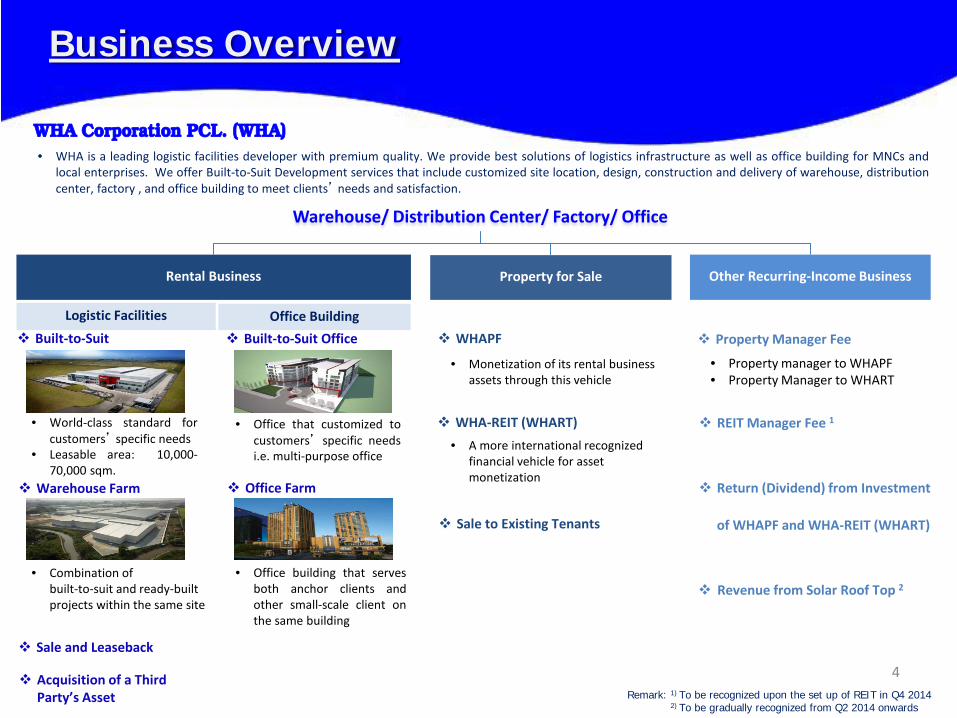

WHA Corporation PCL. (WHA)

Warehouse/ Distribution Center/ Factory/ Office

Warehouse Farm

Built-to-Suit

• World-class standard for customers’ specific needs

• Leasable area: 10,000-70,000 sqm.

• Combination of built-to-suit and ready-built projects within the same site

• Monetization of its rental business assets through this vehicle

Sale to Existing Tenants

WHAPF

Return (Dividend) from Investment

of WHAPF and WHA-REIT (WHART)

Property Manager Fee

• Property manager to WHAPF • Property Manager to WHART

Sale and Leaseback

Business Overview

Revenue from Solar Roof Top 2

Remark: 1) To be recognized upon the set up of REIT in Q4 2014 2) To be gradually recognized from Q2 2014 onwards

REIT Manager Fee 1

Office Farm

Built-to-Suit Office

• Office that customized to customers’ specific needs i.e. multi-purpose office

• Office building that serves both anchor clients and other small-scale client on the same building

Office Building Logistic Facilities

Acquisition of a Third Party’s Asset

Rental Business Property for Sale Other Recurring-Income Business

• WHA is a leading logistic facilities developer with premium quality. We provide best solutions of logistics infrastructure as well as office building for MNCs and local enterprises. We offer Built-to-Suit Development services that include customized site location, design, construction and delivery of warehouse, distribution center, factory , and office building to meet clients’ needs and satisfaction.

WHA-REIT (WHART) • A more international recognized

financial vehicle for asset monetization

GROWING PHASE • Monetization of the assets to WHAPF with the

value of THB 2,046mm (69,529 sqm) in the 1st quarter and injected another lot of THB 4,536mm worth of assets (173,367 sqm) in 4th Quarter which makes total fund size of THB 9,308mm

• This year WHA offered 2 stock dividends to existing shareholders on May, 2013 (5:1) and on September, 2013 (2:1)

• WHA is rated A- with stable outlook by Fitch Ratings (Thailand)

ESTABLISHMENT OF PUBLICLY LISTED FUND (WHAPF)

Establishment of WHAPF (initially known as M-WHA) with the total fund size of THB 1,283mm or USD 42.77mm with total leasable area of 39,808.80 sqm of 2 warehouses and 1 factory

ESTABLISHMENT OF WHA CORPORATION

WHA Corporation was founded on September 25, 2007 with a registered capital of THB 170mm by Mr.Somyos Anantaprayoon, founder, and Mrs.Jareeporn Anantaprayoon, cofounder. WHA Corporation focuses on developing high quality of warehouses, distribution centers, and factories to suitly serve the demand of the clients

WHA’S FIRST & THE BIGGEST DCs IN SEA

Establishment of Warehouse Asia Alliance (partner with GLOMAC, Malaysia) and WHA Alliance (partner with CWT, Singapore) to develop distribution centers for DKSH healthcare and consumer on Bangna-Trad km.19 and km.20 each with the leasable area of 53,000 sqm

Key Milestones and Developments

5

PRE-IPO RESTRUCTURING • WHA Corporation restructured itself by

acquiring 99.99% of WHA Alliance from CWT (Singapore) and co-founder, as well as 99.99% of Warehouse Asia Alliance from GLOMAC (Malaysia) and co-founder to become WHA Corporation’s subsidiaries.

• Development of first warehouse farm on Bangna-Trad km.18 with the leasable area of 72,179.48 sqm

2007

2006

2010

2011

IPO AND LISTED COMPANY • Monetization of 3 warehouses and

1 factory to WHAPF with the value of THB 1,827mm (107,277 sqm)

• On Nov 8, 2012, WHA Corporation became to be listed Co. and first traded in SET, raising up the capital to THB 1,709mm or USD 56.97mm

• The post-IPO paid-up capital was THB 510mm

2013

2012

NEW OPPORTUNITIES • Establishment of WHA REM to pave

the way to set up new WHA REIT • Commence of solar energy sale

revenue recognition in May • More value-added services focus

i.e. cold storage, online warehouse, and other comprehensive services

• Tap into built-to-suit office and acquire a new office place on Vibhavadi-Rangsit Rd.

2014

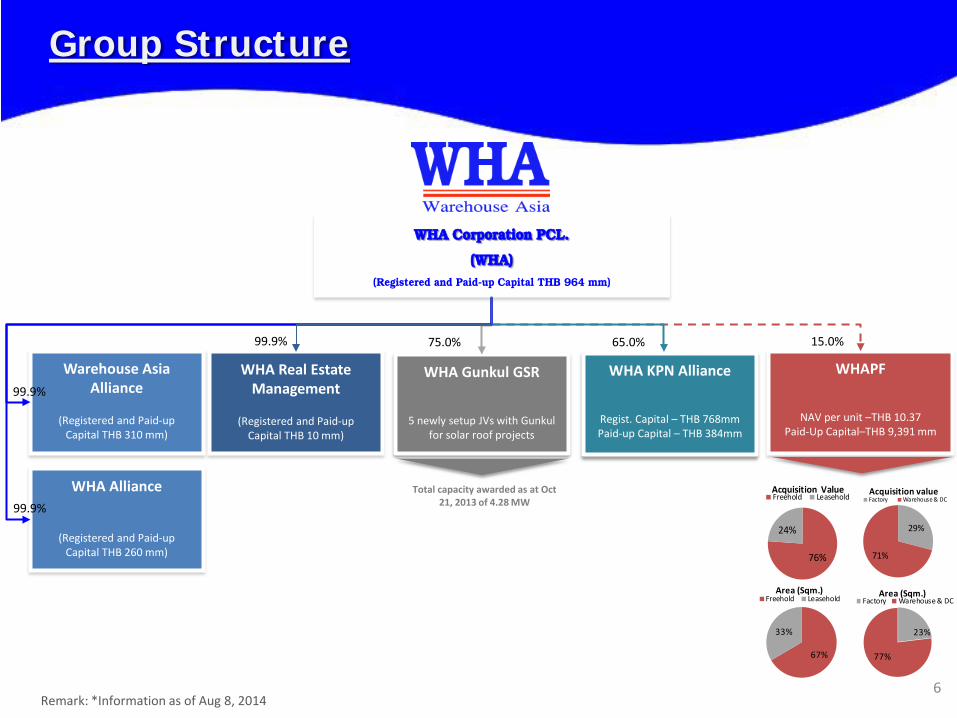

Warehouse Asia Alliance

(Registered and Paid-up

Capital THB 310 mm)

WHA Alliance

(Registered and Paid-up Capital THB 260 mm)

WHAPF

NAV per unit –THB 10.37 Paid-Up Capital–THB 9,391 mm

WHA Gunkul GSR

5 newly setup JVs with Gunkul for solar roof projects

Total capacity awarded as at Oct 21, 2013 of 4.28 MW

99.9%

15.0% 75.0%

WHA Corporation PCL.

(WHA) (Registered and Paid-up Capital THB 964 mm)

Group Structure

WHA KPN Alliance

Regist. Capital – THB 768mm Paid-up Capital – THB 384mm

76%

24%

Acquisition ValueFreehold Leasehold

29%

71%

Acquisition valueFactory Warehouse & DC

67%

33%

Area (Sqm.)Freehold Leasehold

23%

77%

Area (Sqm.)Factory Warehouse & DC

65.0%

6

99.9%

WHA Real Estate Management

(Registered and Paid-up

Capital THB 10 mm)

99.9%

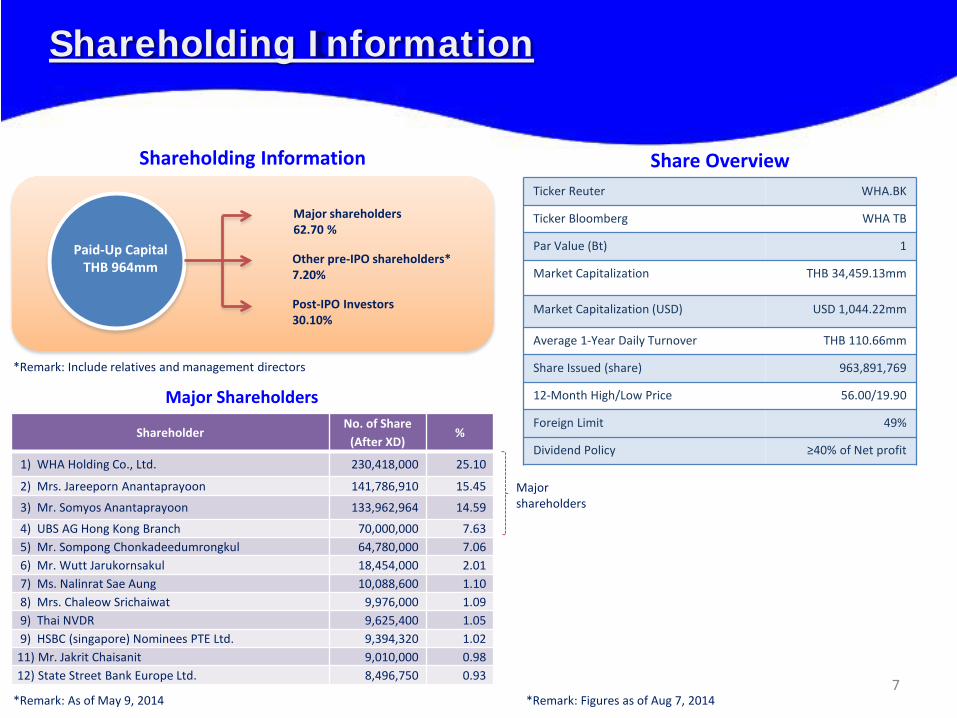

Remark: *Information as of Aug 8, 2014

7

Shareholding Information

Major Shareholders

Shareholder No. of Share

(After XD) %

1) WHA Holding Co., Ltd. 230,418,000 25.10

2) Mrs. Jareeporn Anantaprayoon 141,786,910 15.45

3) Mr. Somyos Anantaprayoon 133,962,964 14.59

4) UBS AG Hong Kong Branch 70,000,000 7.63 5) Mr. Sompong Chonkadeedumrongkul 64,780,000 7.06 6) Mr. Wutt Jarukornsakul 18,454,000 2.01 7) Ms. Nalinrat Sae Aung 10,088,600 1.10 8) Mrs. Chaleow Srichaiwat 9,976,000 1.09 9) Thai NVDR 9,625,400 1.05 9) HSBC (singapore) Nominees PTE Ltd. 9,394,320 1.02 11) Mr. Jakrit Chaisanit 9,010,000 0.98 12) State Street Bank Europe Ltd. 8,496,750 0.93

Paid-Up Capital THB 964mm

Major shareholders 62.70 %

Other pre-IPO shareholders* 7.20%

Post-IPO Investors 30.10%

Share Overview

*Remark: As of May 9, 2014

*Remark: Include relatives and management directors

*Remark: Figures as of Aug 7, 2014

Shareholding Information

Ticker Reuter WHA.BK

Ticker Bloomberg WHA TB

Par Value (Bt) 1

Market Capitalization THB 34,459.13mm

Market Capitalization (USD) USD 1,044.22mm

Average 1-Year Daily Turnover THB 110.66mm

Share Issued (share) 963,891,769

12-Month High/Low Price 56.00/19.90

Foreign Limit 49%

Dividend Policy ≥40% of Net profit

Major shareholders

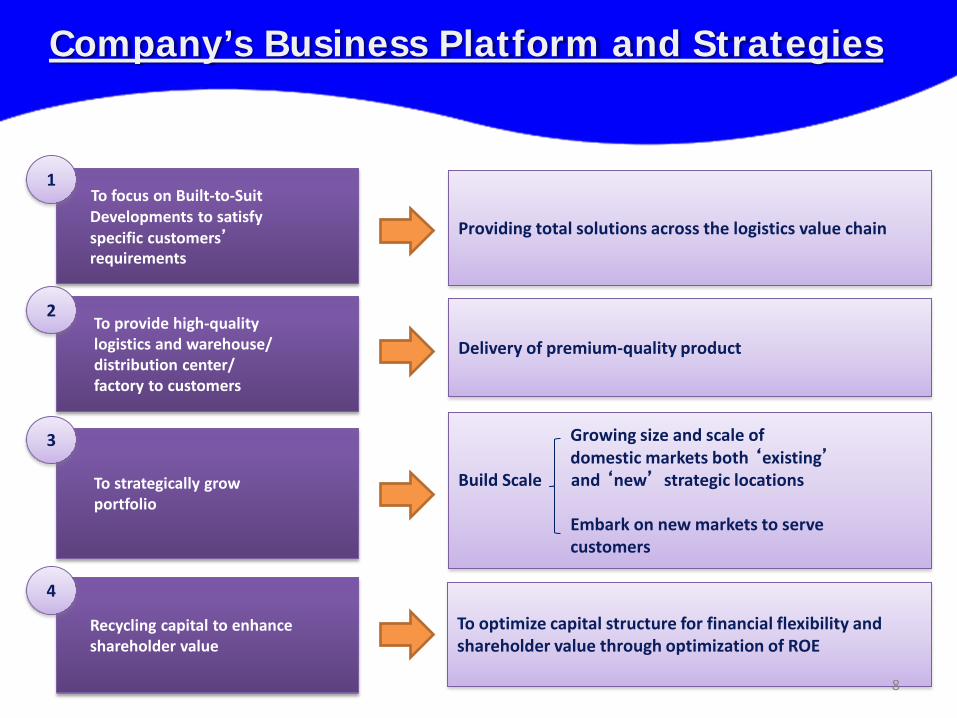

To optimize capital structure for financial flexibility and shareholder value through optimization of ROE

Growing size and scale of domestic markets both ‘existing’ Build Scale and ‘new’ strategic locations Embark on new markets to serve customers

Delivery of premium-quality product

Providing total solutions across the logistics value chain

8

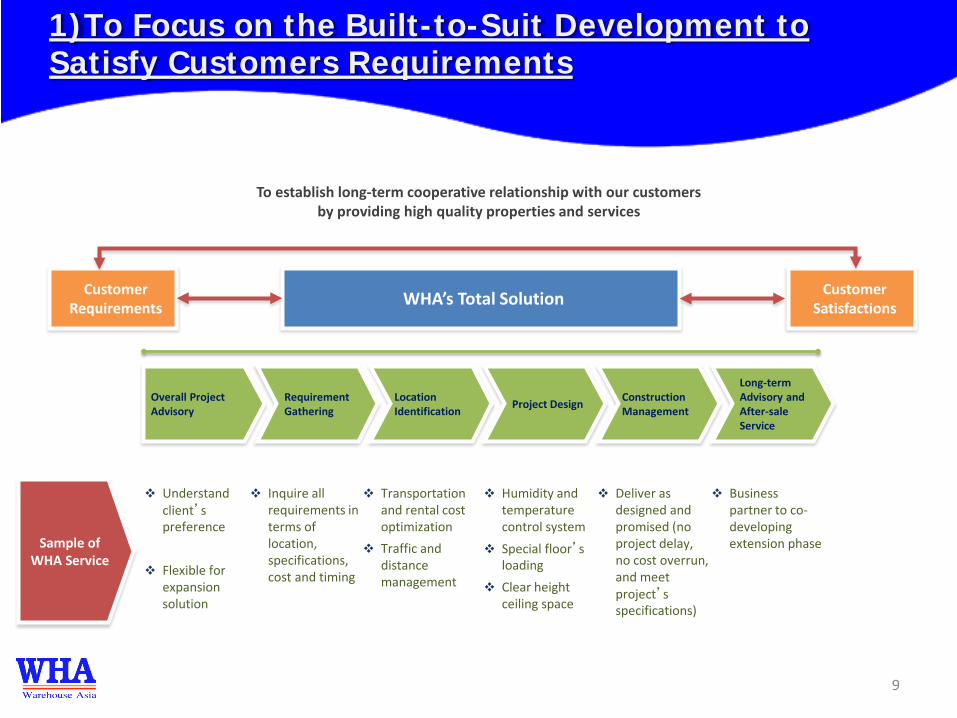

To focus on Built-to-Suit Developments to satisfy specific customers’ requirements

To provide high-quality logistics and warehouse/ distribution center/ factory to customers

To strategically grow portfolio

Recycling capital to enhance shareholder value

1

2

3

4

Company’s Business Platform and Strategies

Inquire all requirements in terms of location, specifications, cost and timing

Transportation and rental cost optimization

Traffic and distance management

Humidity and temperature control system

Special floor’s loading

Clear height ceiling space

Deliver as designed and promised (no project delay, no cost overrun, and meet project’s specifications)

Business partner to co-developing extension phase

Understand client’s preference

Flexible for expansion solution

Overall Project Advisory

Requirement Gathering

Location Identification Project Design Construction

Management

Long-term Advisory and After-sale Service

Customer Requirements

Customer Satisfactions WHA’s Total Solution

To establish long-term cooperative relationship with our customers by providing high quality properties and services

Sample of WHA Service

9

1)To Focus on the Built-to-Suit Development to Satisfy Customers Requirements

10

Various Features of our High-Quality Warehouse and Distribution Center

Large Floor Area Clear Height High Load Tolerance Dock Leveler Wide Column Spacing

Burnished Floor Finish

One Continuous Metal Sheet Roof

Air Gap Roof Insulation

Natural Ventilation

Steel Pipe Structure

10,000-70,000 sqm. 10-13 meters 3-5 tons/sqm.

Mirror floor finish Eliminate the leakage

on the roof Lower inside temperature

Maximize wind flow Less dust

accumulation

Increase usable area Hydraulic Dock Leveler

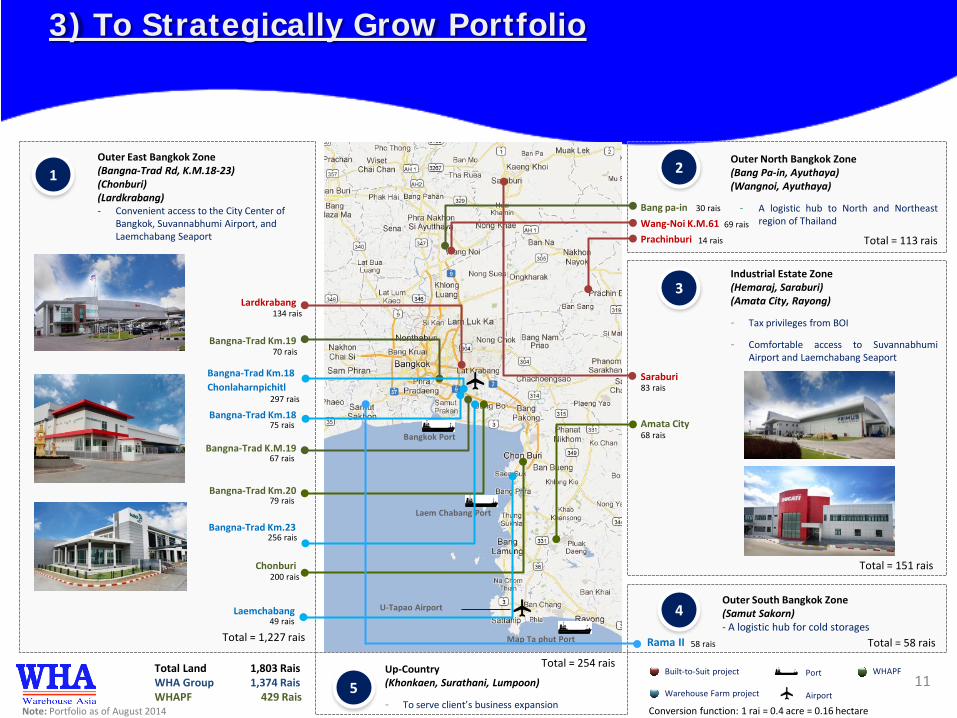

2) To Provide High-Quality Logistics and Warehouse/ Distribution Center/ Factory to Customers

U-Tapao Airport

Bangkok Port

Laem Chabang Port

Map Ta phut Port

Bangna-Trad K.M.19

Bangna-Trad Km.18

Bangna-Trad Km.19

Lardkrabang

Chonburi

Bangna-Trad Km.20

Saraburi

Amata City

Bang pa-in Wang-Noi K.M.61

Outer East Bangkok Zone (Bangna-Trad Rd, K.M.18-23) (Chonburi) (Lardkrabang) - Convenient access to the City Center of

Bangkok, Suvannabhumi Airport, and Laemchabang Seaport

Industrial Estate Zone (Hemaraj, Saraburi) (Amata City, Rayong)

- Tax privileges from BOI

- Comfortable access to Suvannabhumi Airport and Laemchabang Seaport

2 Outer North Bangkok Zone (Bang Pa-in, Ayuthaya) (Wangnoi, Ayuthaya)

- A logistic hub to North and Northeast region of Thailand

Note: Portfolio as of August 2014

Built-to-Suit project

Warehouse Farm project

WHAPF Port

Airport

Bangna-Trad Km.23

3

1

11

Prachinburi

Bangna-Trad Km.18 Chonlaharnpichitl

Laemchabang 4

Rama II 58 rais

134 rais

70 rais

297 rais

75 rais

67 rais

79 rais

256 rais

200 rais

49 rais

30 rais

14 rais

83 rais

68 rais

69 rais

Total = 1,227 rais

Total = 113 rais

Total = 151 rais

Outer South Bangkok Zone (Samut Sakorn) - A logistic hub for cold storages

Total Land 1,803 Rais WHA Group 1,374 Rais WHAPF 429 Rais

135 rais

Up-Country (Khonkaen, Surathani, Lumpoon)

- To serve client’s business expansion 5

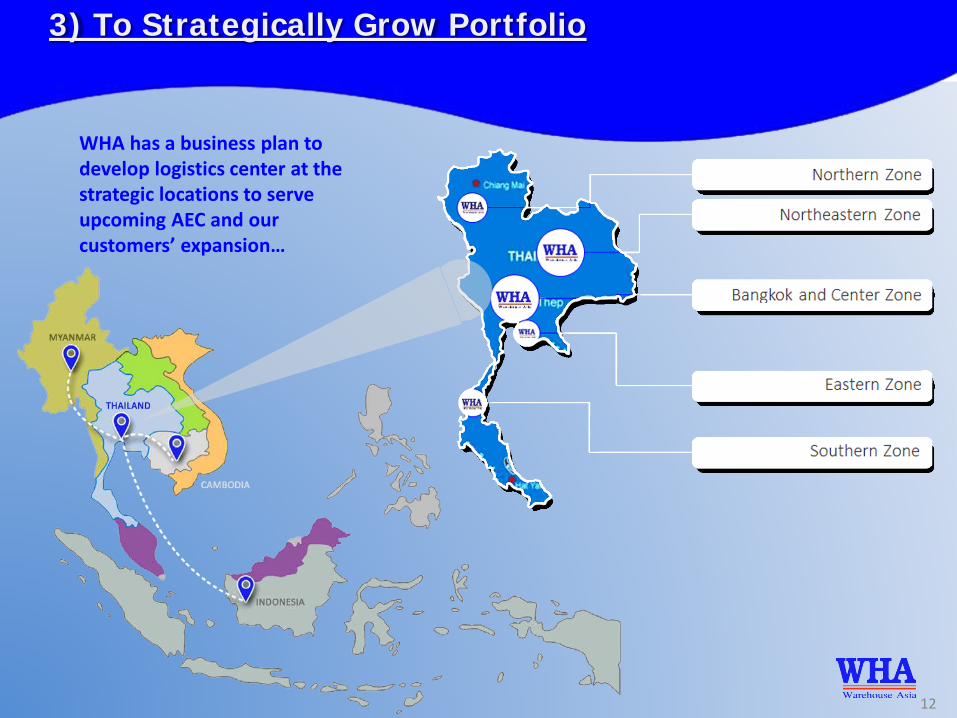

3) To Strategically Grow Portfolio

Total = 254 rais

Total = 58 rais

Conversion function: 1 rai = 0.4 acre = 0.16 hectare

12

3) To Strategically Grow Portfolio

WHA has a business plan to develop logistics center at the strategic locations to serve upcoming AEC and our customers’ expansion…

Highly Stable CF from

Investment

Utilize Recurring

Income Stream

Well-balanced Portfolio and

Capital Structure

All Invested Assets Generate Revenue

Strong track record in terms of occupancy rate

To hold minimal non-income generating assets

Strong Stability of Rental Profit

Secured L-T contract with growth in rental

Appx. 85% EBITDA margin

Low maintenance cost

Capital Structure Optimization

Asset-Optimization Model

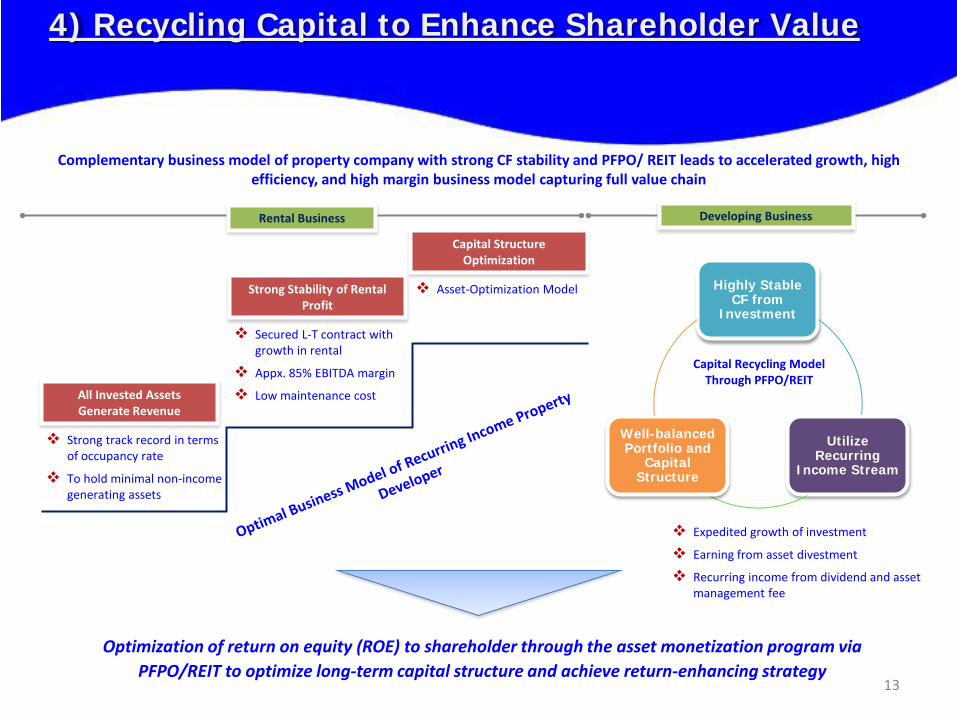

Optimization of return on equity (ROE) to shareholder through the asset monetization program via PFPO/REIT to optimize long-term capital structure and achieve return-enhancing strategy

Rental Business Developing Business

Expedited growth of investment

Earning from asset divestment

Recurring income from dividend and asset management fee

Complementary business model of property company with strong CF stability and PFPO/ REIT leads to accelerated growth, high efficiency, and high margin business model capturing full value chain

Capital Recycling Model Through PFPO/REIT

13

4) Recycling Capital to Enhance Shareholder Value

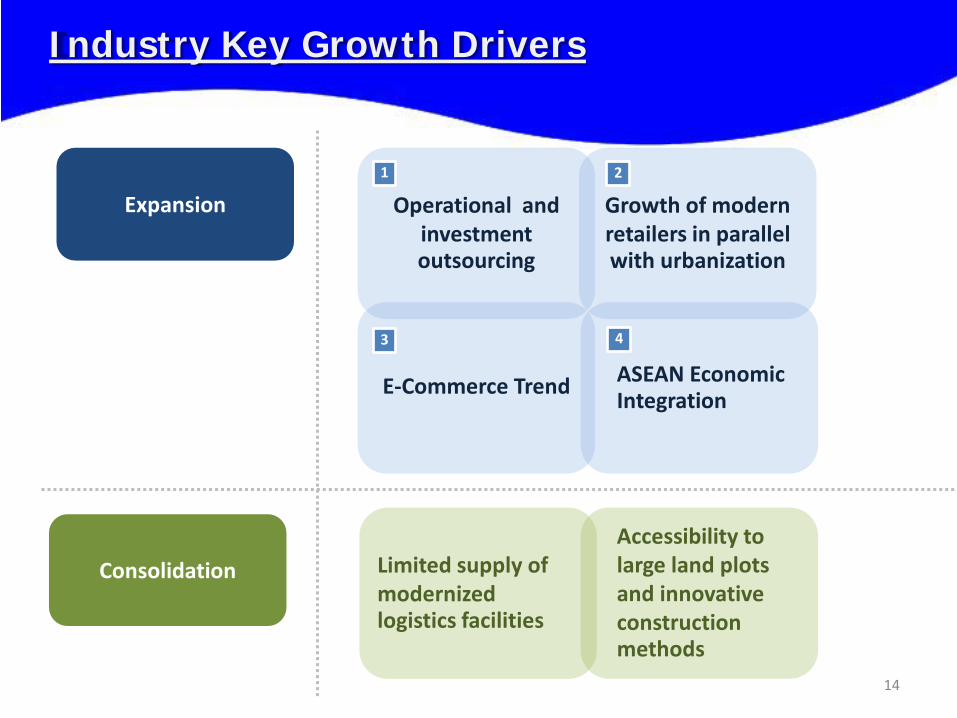

Expansion

Consolidation

Operational and investment outsourcing

Growth of modern retailers in parallel with urbanization

E-Commerce Trend ASEAN Economic Integration

Limited supply of modernized logistics facilities

Accessibility to large land plots and innovative construction methods

Industry Key Growth Drivers

14

1 2

4 3

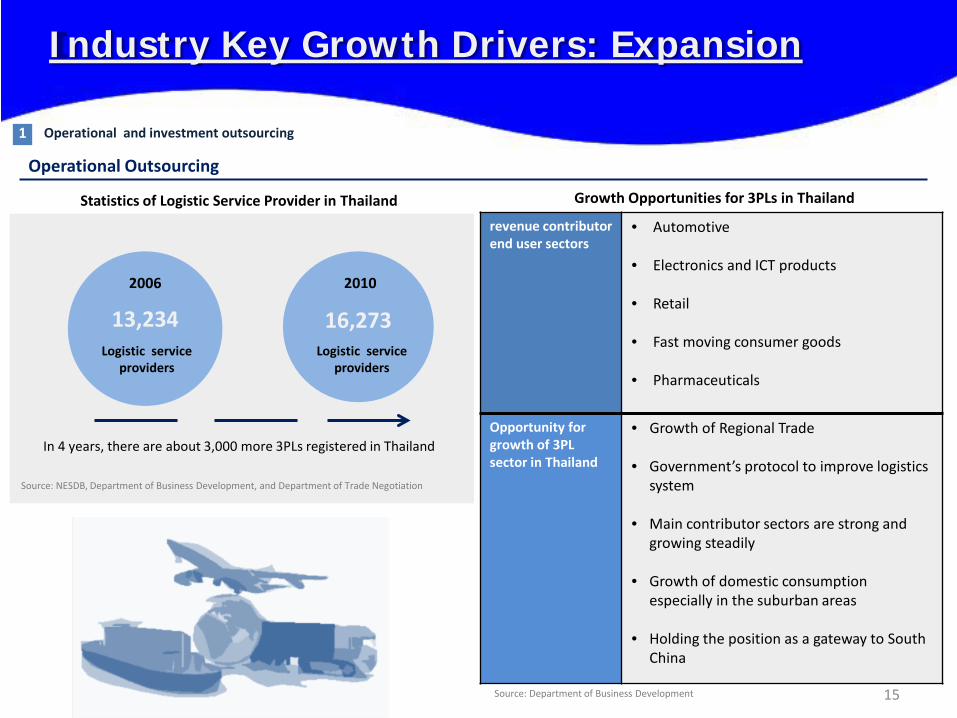

Statistics of Logistic Service Provider in Thailand

13,234

2006

Logistic service providers

16,273

2010

Logistic service providers

In 4 years, there are about 3,000 more 3PLs registered in Thailand

Source: NESDB, Department of Business Development, and Department of Trade Negotiation

revenue contributor end user sectors

• Automotive

• Electronics and ICT products

• Retail

• Fast moving consumer goods

• Pharmaceuticals

Opportunity for growth of 3PL sector in Thailand

• Growth of Regional Trade

• Government’s protocol to improve logistics system

• Main contributor sectors are strong and growing steadily

• Growth of domestic consumption especially in the suburban areas

• Holding the position as a gateway to South China

Growth Opportunities for 3PLs in Thailand

Source: Department of Business Development

Industry Key Growth Drivers: Expansion

15

1 Operational and investment outsourcing

Operational Outsourcing

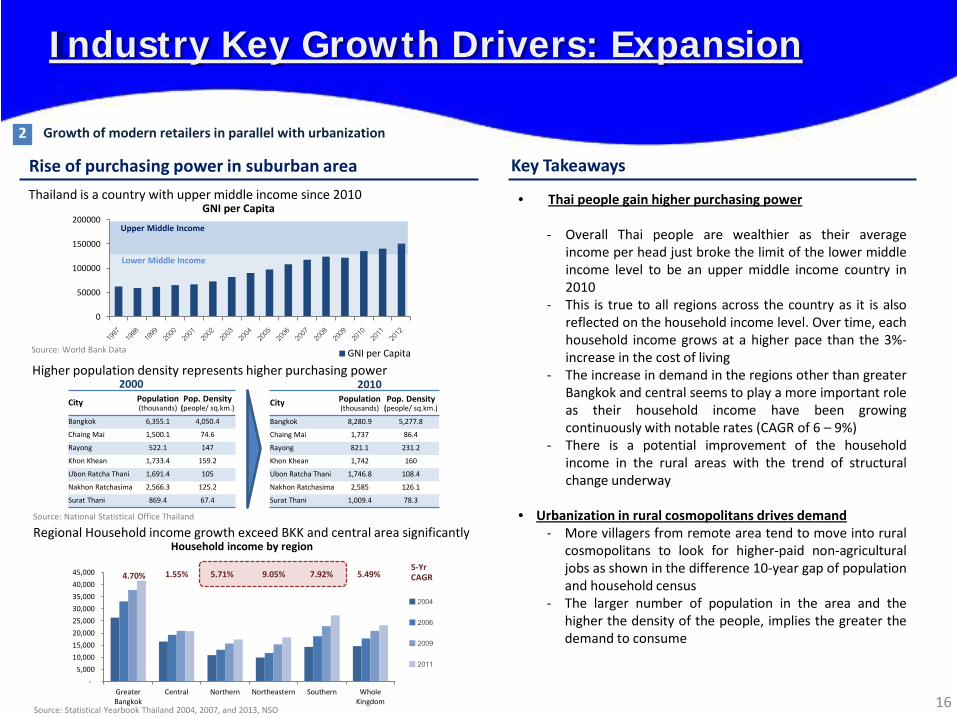

Thailand is a country with upper middle income since 2010

0

50000

100000

150000

200000GNI per Capita

GNI per Capita

Upper Middle Income

Lower Middle Income

Source: World Bank Data

Source: Statistical Yearbook Thailand 2004, 2007, and 2013, NSO

Regional Household income growth exceed BKK and central area significantly

16 -

5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

GreaterBangkok

Central Northern Northeastern Southern WholeKingdom

Household income by region

2004

2006

2009

2011

4.70% 1.55% 5.49% 5-Yr CAGR 5.71% 9.05% 7.92%

Higher population density represents higher purchasing power

Source: National Statistical Office Thailand

City Population (thousands)

Pop. Density (people/ sq.km.)

Bangkok 6,355.1 4,050.4

Chaing Mai 1,500.1 74.6

Rayong 522.1 147

Khon Khean 1,733.4 159.2

Ubon Ratcha Thani 1,691.4 105

Nakhon Ratchasima 2,566.3 125.2

Surat Thani 869.4 67.4

City Population (thousands)

Pop. Density (people/ sq.km.)

Bangkok 8,280.9 5,277.8

Chaing Mai 1,737 86.4

Rayong 821.1 231.2

Khon Khean 1,742 160

Ubon Ratcha Thani 1,746.8 108.4

Nakhon Ratchasima 2,585 126.1

Surat Thani 1,009.4 78.3

2000 2010

Key Takeaways Rise of purchasing power in suburban area

• Thai people gain higher purchasing power - Overall Thai people are wealthier as their average

income per head just broke the limit of the lower middle income level to be an upper middle income country in 2010

- This is true to all regions across the country as it is also reflected on the household income level. Over time, each household income grows at a higher pace than the 3%-increase in the cost of living

- The increase in demand in the regions other than greater Bangkok and central seems to play a more important role as their household income have been growing continuously with notable rates (CAGR of 6 – 9%)

- There is a potential improvement of the household income in the rural areas with the trend of structural change underway

• Urbanization in rural cosmopolitans drives demand - More villagers from remote area tend to move into rural

cosmopolitans to look for higher-paid non-agricultural jobs as shown in the difference 10-year gap of population and household census

- The larger number of population in the area and the higher the density of the people, implies the greater the demand to consume

Industry Key Growth Drivers: Expansion

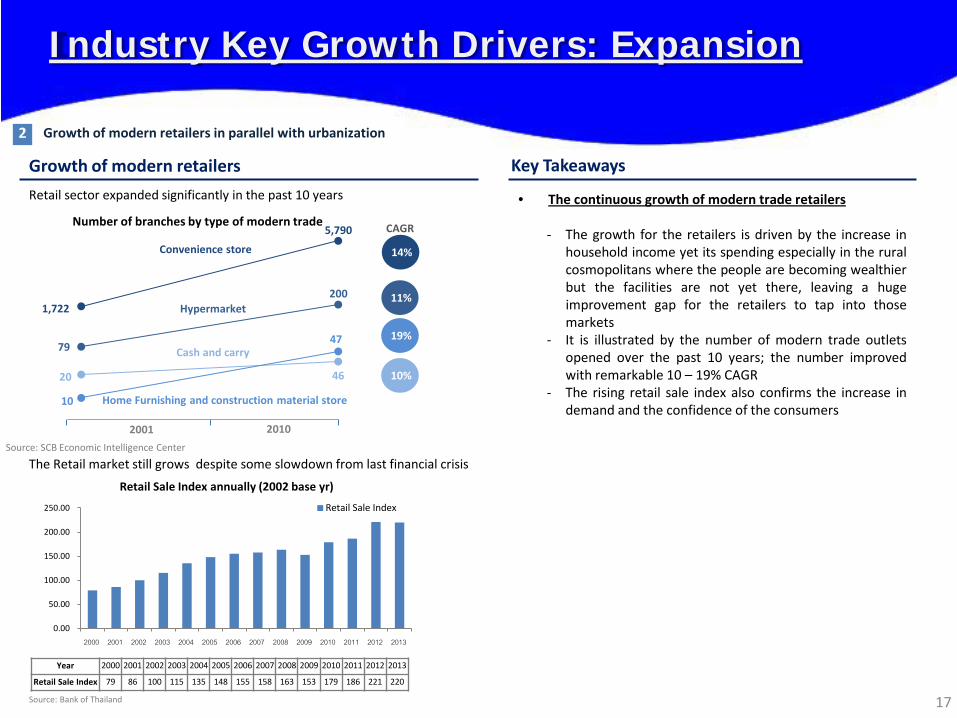

2 Growth of modern retailers in parallel with urbanization

Growth of modern retailers

Retail sector expanded significantly in the past 10 years

1,722

5,790

79

200

20

10

47

46

Convenience store

Hypermarket

Cash and carry

Home Furnishing and construction material store

2001 2010

14%

11%

19%

10%

CAGR Number of branches by type of modern trade

Source: SCB Economic Intelligence Center

17

0.00

50.00

100.00

150.00

200.00

250.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Retail Sale Index annually (2002 base yr)

Retail Sale Index

Source: Bank of Thailand

The Retail market still grows despite some slowdown from last financial crisis

Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Retail Sale Index 79 86 100 115 135 148 155 158 163 153 179 186 221 220

Key Takeaways

• The continuous growth of modern trade retailers - The growth for the retailers is driven by the increase in

household income yet its spending especially in the rural cosmopolitans where the people are becoming wealthier but the facilities are not yet there, leaving a huge improvement gap for the retailers to tap into those markets

- It is illustrated by the number of modern trade outlets opened over the past 10 years; the number improved with remarkable 10 – 19% CAGR

- The rising retail sale index also confirms the increase in demand and the confidence of the consumers

Industry Key Growth Drivers: Expansion

2 Growth of modern retailers in parallel with urbanization

Source: Nielsen, UBS research

31.2m Thais online 46% of population

Value of online shopping is up to THB 6.23bn

18

Source: Thailand Yearbook of Telecommunications Indicators 2012-2013, NBTC

11.70% 14.30% 17.07% 21.53% 27.21% 29.43%

0%

50%

100%

2008 2009 2010 2011 2012 2013 Non-Voice Voice

93.01% 98.58% 106.56% 114.58%

127.85%

138.51%

Mobile Penetration138% mobile penetration rate

35% of Thai people online wirelessly

Remark: Information as of 2013

Population = 68m

Country Population (millions)

Online Users (millions, share of population)

Retail Sales (billions USD)

E-commerce (share of retail)

Opportunity* (billions USD)

Thailand 67.90 31.20 (46.0%) 94.40 0.2% 4.7

Indonesia 244.80 75.90 (31.0%) 100.20 0.1% 1.5

Philippines 97.70 33.60 (34.4%) 34.00 0.3% 1.7

Vietnam 88.80 31.00 (35.0%) 79.60 0.1% 4

Malaysia 29.50 18.50 (62.6%) 98.20 0.2% 4.9

Singapore 5.30 3.90 (74.0%) 29.60 1.0% 1.5

Aggregate 534 194.20 (36.4%) 436 0.2% 21.8

China 1,344 618.00 (46.0%) 3,812 8.0% N/A

Remark: *This amount is calculated based on 5% portion of retail sales

E-Commerce Trend

Type of Mobile Service and Mobile Penetration

Portion of E-Commerce Spending Compared to Retail Spending

The penetration of mobile usage continue to rise while Thai people tend to use more of non-voice service

E-commerce market in ASEAN is still on the beginning stage with plenty of room to grow

Industry Key Growth Drivers: Expansion

3 E-Commerce Trend

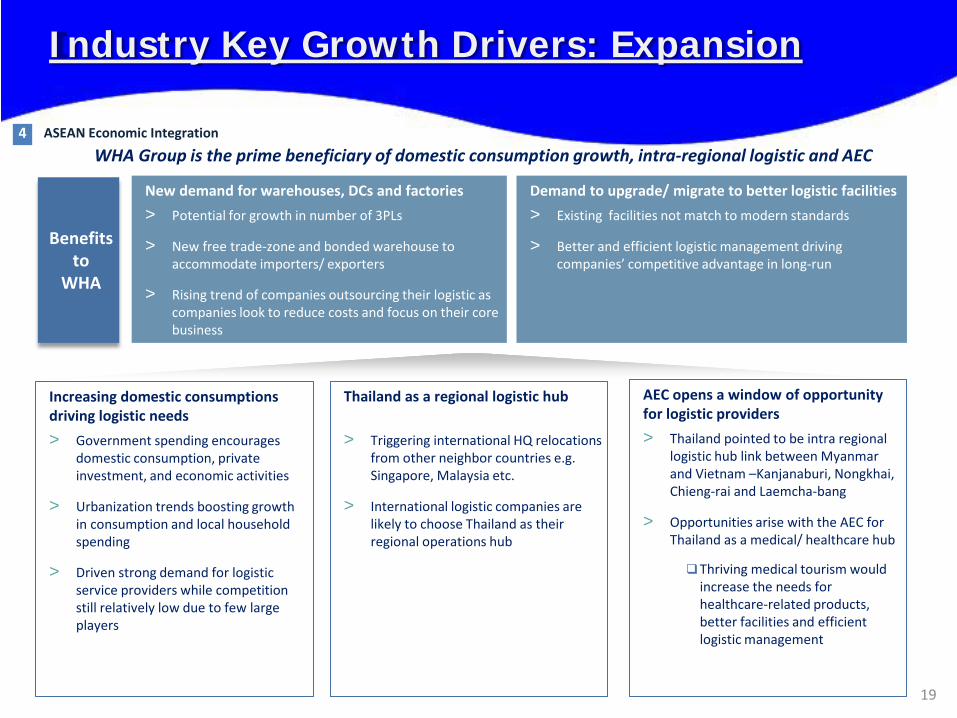

Increasing domestic consumptions driving logistic needs > Government spending encourages

domestic consumption, private investment, and economic activities

> Urbanization trends boosting growth in consumption and local household spending

> Driven strong demand for logistic service providers while competition still relatively low due to few large players

New demand for warehouses, DCs and factories > Potential for growth in number of 3PLs

> New free trade-zone and bonded warehouse to accommodate importers/ exporters

> Rising trend of companies outsourcing their logistic as companies look to reduce costs and focus on their core business

Demand to upgrade/ migrate to better logistic facilities > Existing facilities not match to modern standards

> Better and efficient logistic management driving companies’ competitive advantage in long-run

AEC opens a window of opportunity for logistic providers > Thailand pointed to be intra regional

logistic hub link between Myanmar and Vietnam –Kanjanaburi, Nongkhai, Chieng-rai and Laemcha-bang

> Opportunities arise with the AEC for Thailand as a medical/ healthcare hub

Thriving medical tourism would increase the needs for healthcare-related products, better facilities and efficient logistic management

Thailand as a regional logistic hub > Triggering international HQ relocations

from other neighbor countries e.g. Singapore, Malaysia etc.

> International logistic companies are likely to choose Thailand as their regional operations hub

Benefits to

WHA

WHA Group is the prime beneficiary of domestic consumption growth, intra-regional logistic and AEC

19

Industry Key Growth Drivers: Expansion

4 ASEAN Economic Integration

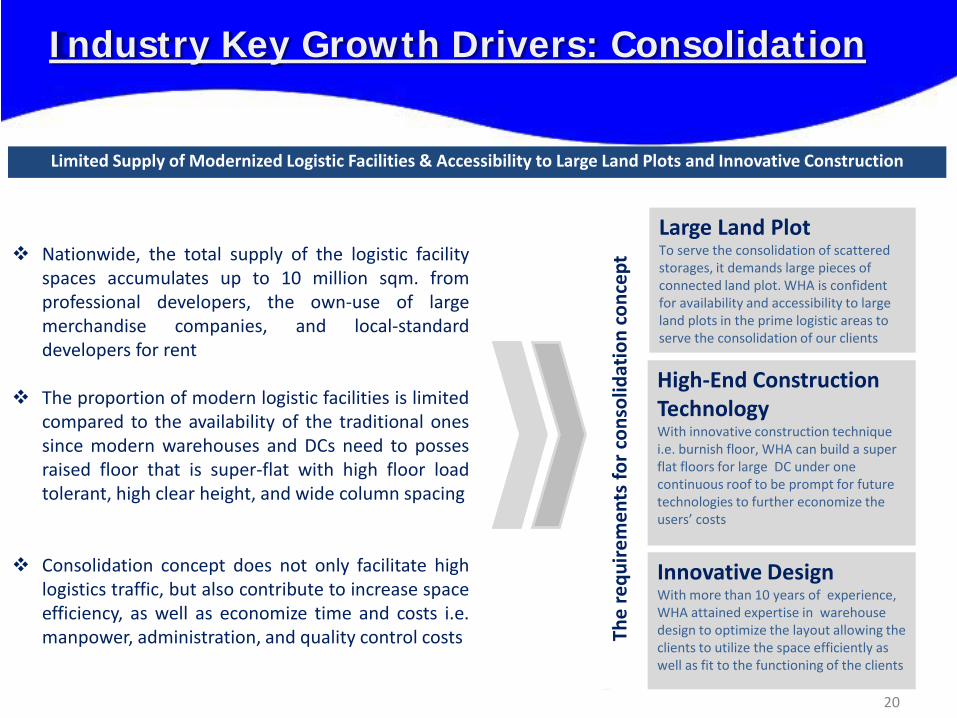

High-End Construction Technology With innovative construction technique i.e. burnish floor, WHA can build a super flat floors for large DC under one continuous roof to be prompt for future technologies to further economize the users’ costs

Innovative Design With more than 10 years of experience, WHA attained expertise in warehouse design to optimize the layout allowing the clients to utilize the space efficiently as well as fit to the functioning of the clients

Large Land Plot To serve the consolidation of scattered storages, it demands large pieces of connected land plot. WHA is confident for availability and accessibility to large land plots in the prime logistic areas to serve the consolidation of our clients

Limited Supply of Modernized Logistic Facilities & Accessibility to Large Land Plots and Innovative Construction

Nationwide, the total supply of the logistic facility spaces accumulates up to 10 million sqm. from professional developers, the own-use of large merchandise companies, and local-standard developers for rent

The proportion of modern logistic facilities is limited compared to the availability of the traditional ones since modern warehouses and DCs need to posses raised floor that is super-flat with high floor load tolerant, high clear height, and wide column spacing

Consolidation concept does not only facilitate high logistics traffic, but also contribute to increase space efficiency, as well as economize time and costs i.e. manpower, administration, and quality control costs

The

requ

irem

ents

for c

onso

lidat

ion

conc

ept

Industry Key Growth Drivers: Consolidation

20

21

Proven and Strong Track Record and Credentials in Thailand and SEA Region.

Pioneered Built-to-Suit Concept to Thai Logistics Market

Superior and Best-in-Class Warehouse, Distribution Center in Prime Locations

Like-Minded Logistic Consultant and Hands-on Management Team

Most Sophisticated Financial Engineering Tools to Serve the Capital-Intensive Business and Satisfy the Attractive Return on Capital to Shareholders

1

2

3

4

5

• WHA has become global contact for MNCs to expand and consolidate their hubs for AEC

• Tailor-made product to cater with each tenant’s specific requirements in order to optimize their long-term logistics costs

• With continuous research and development to improve the quality of our products e.g. floor (high-strength, super flat concrete), large continuous roof, natural ventilation, and ability to construct in each module concurrently to shorten the construction period

• Logistics mentality, dedicated top management to listen to clients’ requirements with in house design and construction management team to communicate with the clients directly

• Property Fund (WHAPF) • REIT (WHA REIT) • Upcoming Infrastructure Fund

Our Key Competitive Advantages

22

Agenda

23

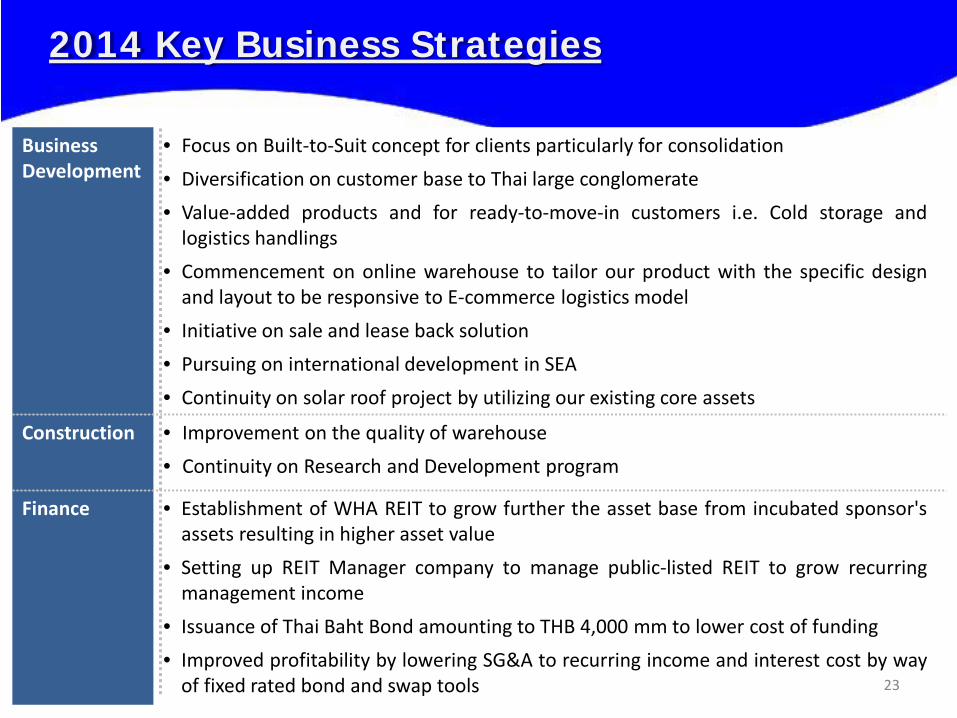

2014 Key Business Strategies

Business Development

• Focus on Built-to-Suit concept for clients particularly for consolidation • Diversification on customer base to Thai large conglomerate • Value-added products and for ready-to-move-in customers i.e. Cold storage and

logistics handlings • Commencement on online warehouse to tailor our product with the specific design

and layout to be responsive to E-commerce logistics model • Initiative on sale and lease back solution • Pursuing on international development in SEA • Continuity on solar roof project by utilizing our existing core assets

Construction • Improvement on the quality of warehouse • Continuity on Research and Development program

Finance • Establishment of WHA REIT to grow further the asset base from incubated sponsor's assets resulting in higher asset value

• Setting up REIT Manager company to manage public-listed REIT to grow recurring management income

• Issuance of Thai Baht Bond amounting to THB 4,000 mm to lower cost of funding • Improved profitability by lowering SG&A to recurring income and interest cost by way

of fixed rated bond and swap tools 23

24

Developed/ Developing & Occupied area for 2006-Q2 2014

OR 100% 100% 100% 100% 100% 100% 100% 100% 90%

Unit: Sqm.

2006 2007 2008 2009 2010 2011 2012 2013 Q2' 14

207,0431

294,261

389,982

147,086

256,434

258,330 152,532

1,701,010

697,8803

312,2952

389,982

264,4911

101,531

88,913 141,619 141,619 169,433 192,341

298,139

505,051 69%

73%

1,003,130

891,286

Area Completed– Area that currently generates revenue Area Available for Lease – Area that is available to serve immediate demand Area Pre-Leased – Area that is leased before the construction is finished Area Sold to WHAPF – Area that is sold to the property fund Land Held for Future Development – Area that is reserved for future development

36,362

Remark: 1This area includes the Built-to-suit offices with the leasable area of approximately 14,000 sqm. Also the area of 16,934 sqm. is written off in this quarter due to the cancellation of pre-leased contract 2 A part of this area, approximately 33,000 sqm., is under specific modification to prompt for the coming of new client

3This area is calculated from the estimated ratio of 1-rai of land = 1,000-sqm leasable area; the actual constructed area is subject to change depending on actual design to suit with clients’ requirement

Key Takeaways

Additional new contracts this quarter comprise to 50,502 sqm. In the first half of 2014 appeared a large number of new faces of clients from Japanese MNCs and large Thai conglomerates,

and state-own enterprise This ending Q2 2014 pre-leased number also includes the pre-leased area of built-to-suit office projects around 14,000 sqm.,

but excludes the area of the newly acquired office place, SJ Infinite 1 (Equinox) project

Impressive Track Record of Growth

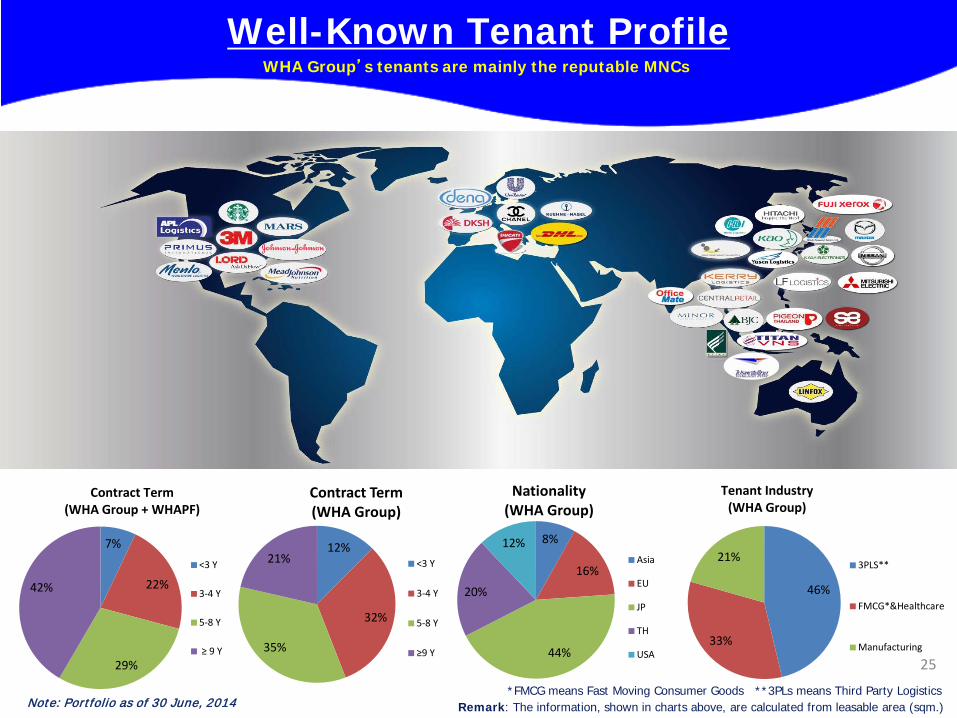

WHA Group’s tenants are mainly the reputable MNCs

Remark: The information, shown in charts above, are calculated from leasable area (sqm.)

Well-Known Tenant Profile

Note: Portfolio as of 30 June, 2014 *FMCG means Fast Moving Consumer Goods **3PLs means Third Party Logistics

25

8%

16%

44%

20%

12%

Nationality (WHA Group)

Asia

EU

JP

TH

USA

46%

33%

21%

Tenant Industry (WHA Group)

3PLS**

FMCG*&Healthcare

Manufacturing

12%

32%

35%

21%

Contract Term (WHA Group)

<3 Y

3-4 Y

5-8 Y

≥9 Y

7%

22%

29%

42%

Contract Term (WHA Group + WHAPF)

<3 Y

3-4 Y

5-8 Y

≥ 9 Y

Top 10 Tenants

26

Top 10 Tenants by Rental Income (WHA Group)

Top 10 Tenants by Rental Income (WHA Group and WHAPF)

Reve

nue

(THB

mm

)

Tenants

Reve

nue

(THB

mm

)

Tenants

18% 17%

16%

8%

6% 6% 6% 5%

4% 3%

28%

8% 7% 7% 6% 6% 5% 5%

3% 3%

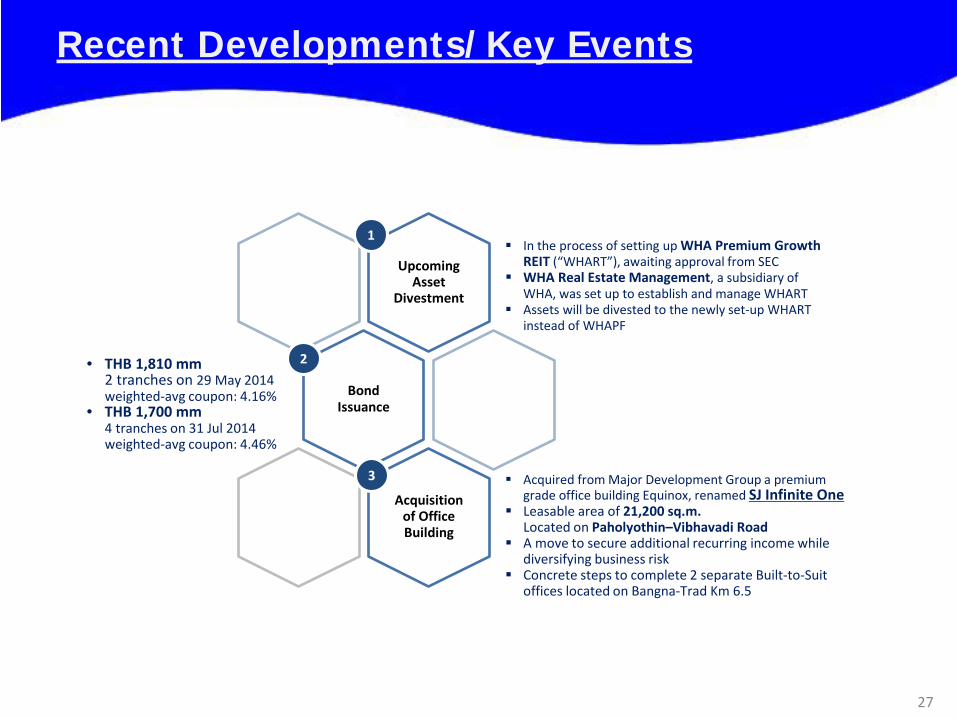

Recent Developments/Key Events

27

Upcoming Asset

Divestment

Bond Issuance

Acquisition of Office Building

1

2

3

In the process of setting up WHA Premium Growth REIT (“WHART”), awaiting approval from SEC

WHA Real Estate Management, a subsidiary of WHA, was set up to establish and manage WHART

Assets will be divested to the newly set-up WHART instead of WHAPF

• THB 1,810 mm 2 tranches on 29 May 2014 weighted-avg coupon: 4.16%

• THB 1,700 mm 4 tranches on 31 Jul 2014 weighted-avg coupon: 4.46%

Acquired from Major Development Group a premium

grade office building Equinox, renamed SJ Infinite One Leasable area of 21,200 sq.m.

Located on Paholyothin–Vibhavadi Road A move to secure additional recurring income while

diversifying business risk Concrete steps to complete 2 separate Built-to-Suit

offices located on Bangna-Trad Km 6.5

Recent Developments/Key Events (Cont’d)

28

Asset Leasable Area Tenant Snapshot

Distribution Center Ladkrabang Phase I & II

Khlong Sam Prawet, Ladkrabang, Bangkok

35,092.97 sqm

WHA Mega Logistics km 18

Bangna-Trad km 18, Samutprakarn

72,179.48 sqm

WHA Mega Logistics km 23

Bangna-Trad km 23, Samutprakarn 59,835.00 sqm

DSG Modification

Nongkae, Saraburi

-

2

3

1

4

Although WHAPF’s 4th Capital Increase of not more than THB 4,590 mm has been approved by WHAPF’s unitholders on 19 Dec 2013, WHA is establishing WHART where assets will be divested into instead in order to maximize gain from asset sale.

WHA will divest the following assets with a total leasable area of 167,107.451) sqm to REIT, expectedly in Q42014.

1) Not include rooftop leasable area of 73,690.30 sq.m.

UPCOMING ASSET DIVESTMENT 1

Will be divested to WHAPF since this modification is part of the DSG project which is currently owned by WHAPF

Recent Developments/Key Events (Cont’d)

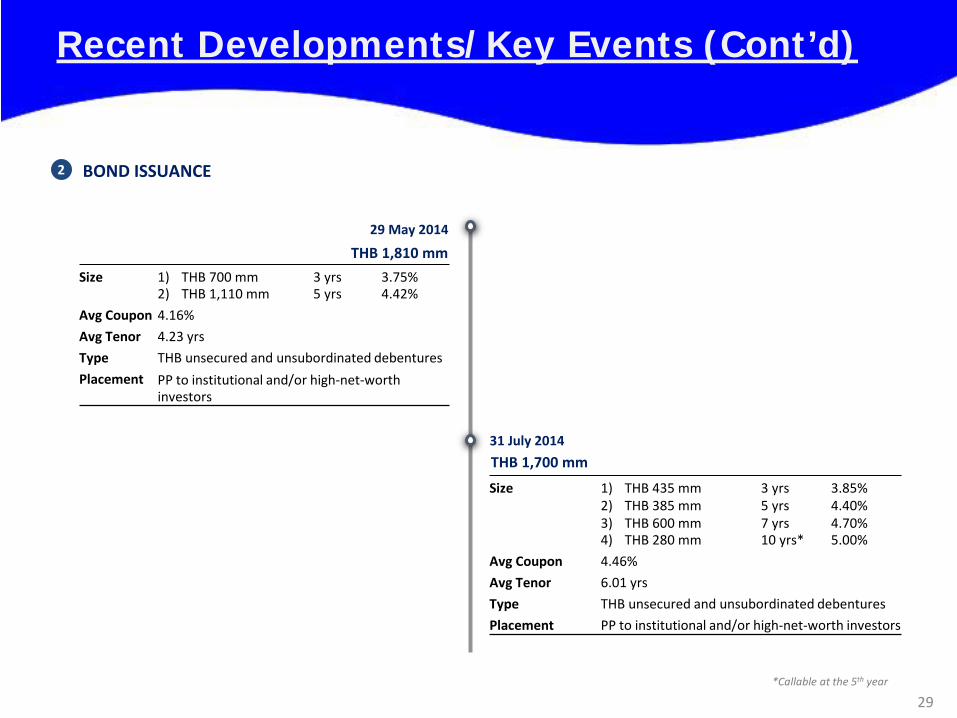

29

BOND ISSUANCE 2

29 May 2014

Size

1) THB 700 mm 2) THB 1,110 mm

3 yrs 5 yrs

3.75% 4.42%

Avg Coupon 4.16%

Avg Tenor 4.23 yrs

Type THB unsecured and unsubordinated debentures

Placement PP to institutional and/or high-net-worth investors

THB 1,810 mm

31 July 2014

Size

1) THB 435 mm 2) THB 385 mm 3) THB 600 mm 4) THB 280 mm

3 yrs 5 yrs 7 yrs 10 yrs*

3.85% 4.40% 4.70% 5.00%

Avg Coupon 4.46%

Avg Tenor 6.01 yrs

Type THB unsecured and unsubordinated debentures

Placement PP to institutional and/or high-net-worth investors

THB 1,700 mm

*Callable at the 5th year

Recent Developments/Key Events (Cont’d)

30

Transaction Rationales

High Quality Asset

Freehold asset in foreseeable prime location of BKK Building specification comparable to Grade-A office Unique cluster of energy and airline industry Close to mass transit and expressway Close to one of Bangkok’s largest green area

Maintain Financial Discipline

Improve overall financial strength by optimization of Debt to Equity while ensuring the maximization of sale value Off-balance sheet technique from REIT stand point

Ability to Grow Recurring

Income with Asset-Light

Model

Secured additional recurring income via REIT management fee and dividend received from REIT Diversify business risk to REIT Platform to grow office REIT in the future with optimal exposure to office asset

Value Appreciation of Freehold Asset

Upside potential from land price appreciation 7 – 10% per annum*

Remarks: *Sourced from Agency for Real Estate Affairs (AREA)

ACQUISITION OF OFFICE BUILDING 3

> 700 m from MRT Phahonyotin

> 800 m from BTS Mhorchit and MRT Chatuchak

> 3.5 km from Kampangpetch expressway

> 5.8 km from Din Daeng expressway

> 16 km from Don Muang airport

> 31 km from suvarnabhumi airport

Strategic Location

Recent Developments/Key Events (Cont’d)

31

Completion July 2014

No. of Storeys 30 (1st-31st floor/skip 13th floor)

Land Area 3-1-45.5 rais

Gross Floor Area 45,044 sqm.

Net Leasable Area 21,200 sqm. • Office: 19,400 sqm.

• Retail: 1,800 sqm.

Car Park Approx. 330 spaces

No. of Lifts 8 passenger lifts, 2 car park lift, and 1 service lift

Floor Plate 850 – 930 sqm.

Air-Condition VRF system

Other Features Floor to floor height • Office: 4.0 m • Retail: 6.0 m

Floor to ceiling height • Office: 2.9 m • Retail: 4.0 m

ACQUISITION OF OFFICE BUILDING 3

Building Attributes

Recent Developments/Key Events (Cont’d)

32

Building Attributes

Construction Start 21 October 2013

Completion 30 September 2014

No. of Storeys 7 floors

Land Area 1-2-65 rais (building A only)

Gross Floor Area 10,133 sqm.

Net Leasable Area 8,893 sqm.

Car Park Separated car park building

No. of Lifts 2 passenger lifts plus 1 service lift

Floor Plate 1,355 – 1,390 sqm.

Air-Condition Split-type air-conditioning system

Other Features Floor to floor height

• Office: 3.2 m Floor to ceiling height

• Office: 2.5 – 2.6 m

DEVELOPMENT OF BUILT-TO-SUIT OFFICE 3

33

Agenda

106.52 121.39

-

-18.90

31.08 125.42

152.47

21.6%

2Q2013 2 Q2 0 14

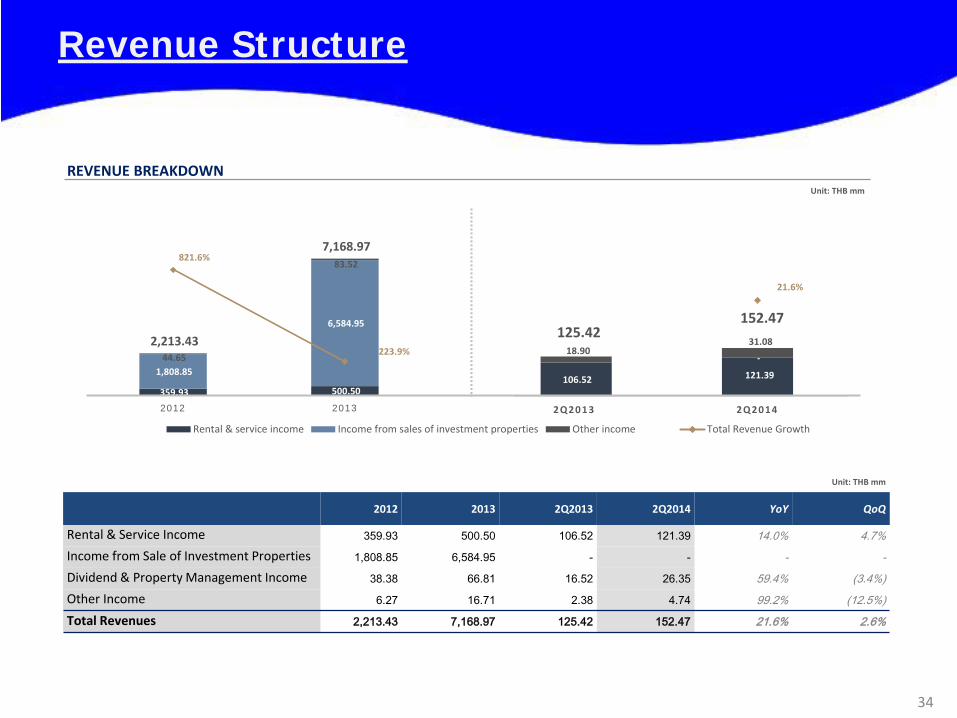

Revenue Structure

34

REVENUE BREAKDOWN

2012 2013 2Q2013 2Q2014 YoY QoQ

Rental & Service Income 359.93 500.50 106.52 121.39 14.0% 4.7% Income from Sale of Investment Properties 1,808.85 6,584.95 - - - - Dividend & Property Management Income 38.38 66.81 16.52 26.35 59.4% (3.4%) Other Income 6.27 16.71 2.38 4.74 99.2% (12.5%) Total Revenues 2,213.43 7,168.97 125.42 152.47 21.6% 2.6%

Unit: THB mm

Unit: THB mm

359.93 500.50

1,808.85

6,584.95

44.65

83.52

2,213.43

7,168.97 821.6%

223.9%

0%

200%

400%

600%

800%

1000%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2012 2013

Rental & service income Income from sales of investment properties Other income Total Revenue Growth

32.28

56.72

14.34 22.75

204.6%

75.7%58.7%

2012 2013 2 Q 2 0 1 3 2 Q 2 0 1 4

Dividend income Growth

6.10

10.09

2.19 3.60

176.3%

65.3% 64.6%

2012 2013 2 Q 2 0 1 3 2 Q 2 0 1 4

Property management income Growth

Revenue Structure (Cont’d)

35

RENTAL AND SERVICE INCOME

Gross Profit and Margin

WHA’s Leasable Area

SALE OF INVESTMENT PROPERTIES

PROPERTY MANAGEMENT AND DIVIDEND INCOME

Gross Profit and Margin WHAPF’s Leasable Area

Property Management Income Dividend Income

Unit: THB mm

1 2

3

126.00 178.99

233.93

321.51

359.93

500.50

65.0%64.2%

6

8

2012 2013

Cost of rental & service Gross profit GPM

Occupied area Available for lease area

Occupied area growth

39,809 39,809 39,809 39,809

107,277 107,277

69,530

173,366

39,809 39,809

147,086

389,982

2010 2011 2012 2013

IPO 1st PO 2nd PO 3rd PO

Remark: Occupied area of 312,295 sq.m. includes leasable area of approx. 33,000 sq.m. that is currently under some modification for the new clients

34.28 36.69

72.24 84.70

106.52 121.39

67.8%69.8%

2 Q 2 0 1 3 2 Q 2 0 1 4

256,434 294,261 270,170 312,295

36,362 256,434

294,261 270,170

348,657 30.7%

14.8%

15.6%

2012 2013 2 Q 2 0 1 3 2 Q 2 0 1 4

1,617.10

4,961.78

- -

191.76

1,623.18

- -

1,808.85

6,584.95

--

10.6%

24.6%

2 0 1 2 2 0 1 3 2 Q 2 0 1 3 2 Q 2 0 1 4

Cost of investment properties Gross profit GPM

No Asset Sale

13% 9% 4%

22% 20%22%

8%13% 10%

47% 56% 57%

9%3%

6%

26%

57%

22%

0%

10%

20%

30%

40%

50%

60%

0%

20%

40%

60%

80%

100%

2012 2013 2 Q 2 0 1 4

Cash & ST investments Non-current assets held for saleInvestment in available-for-sale Investment propertiesOthers IP Growth

1,095.40 983.32 591.17

1,861.57 2,225.07 2,935.13

653.19 1,387.46 1,366.33

3,936.61 6,167.21 7,513.93

750.74 285.79 848.83

0%

20%

40%

60%

80%

100%

2012 2013 2 Q 2 0 1 4Cash & ST investments Non-current assets held for saleInvestment in available-for-sale Investment propertiesOthers

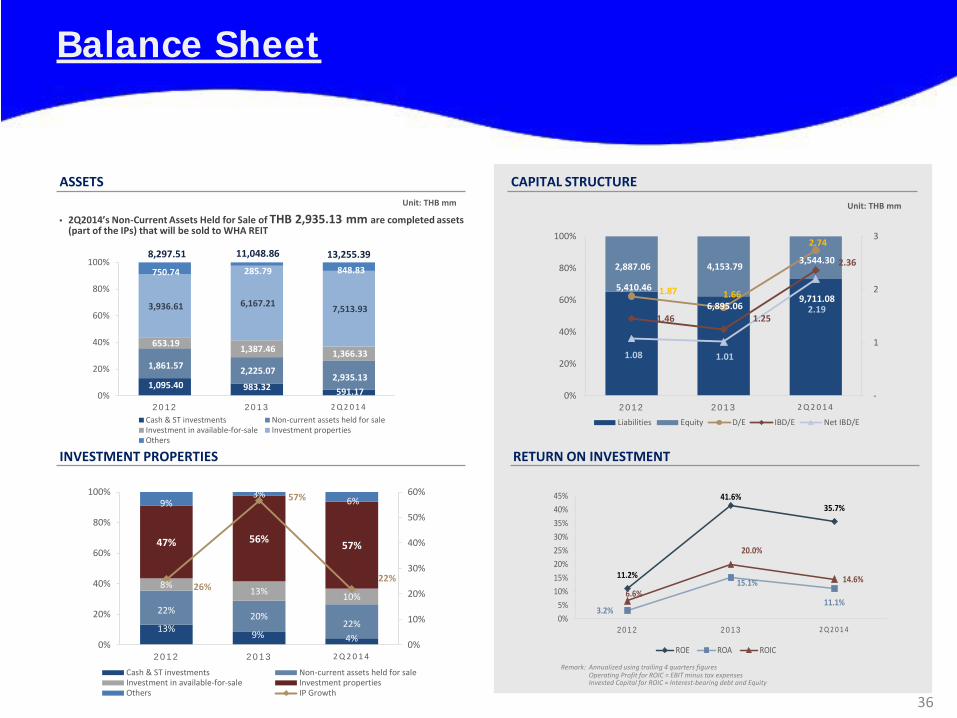

Balance Sheet

36

Unit: THB mm

CAPITAL STRUCTURE ASSETS Unit: THB mm

INVESTMENT PROPERTIES

• 2Q2014’s Non-Current Assets Held for Sale of THB 2,935.13 mm are completed assets (part of the IPs) that will be sold to WHA REIT

8,297.51 11,048.86

RETURN ON INVESTMENT

Remark: Annualized using trailing 4 quarters figures Operating Profit for ROIC = EBIT minus tax expenses

Invested Capital for ROIC = Interest-bearing debt and Equity

13,255.39

11.2%

41.6%35.7%

3.2%

15.1%

11.1%6.6%

20.0%

14.6%

0%5%

10%15%20%25%30%35%40%45%

2012 2013 2 Q 2 0 1 4

ROE ROA ROIC

5,410.46

6,895.06 9,711.08

2,887.06 4,153.79 3,544.30

1.87 1.66

2.74

1.46 1.25

2.36

1.08 1.01

2.19

-

1

2

3

0%

20%

40%

60%

80%

100%

2012 2013 2 Q 2 0 1 4

Liabilities Equity D/E IBD/E Net IBD/E

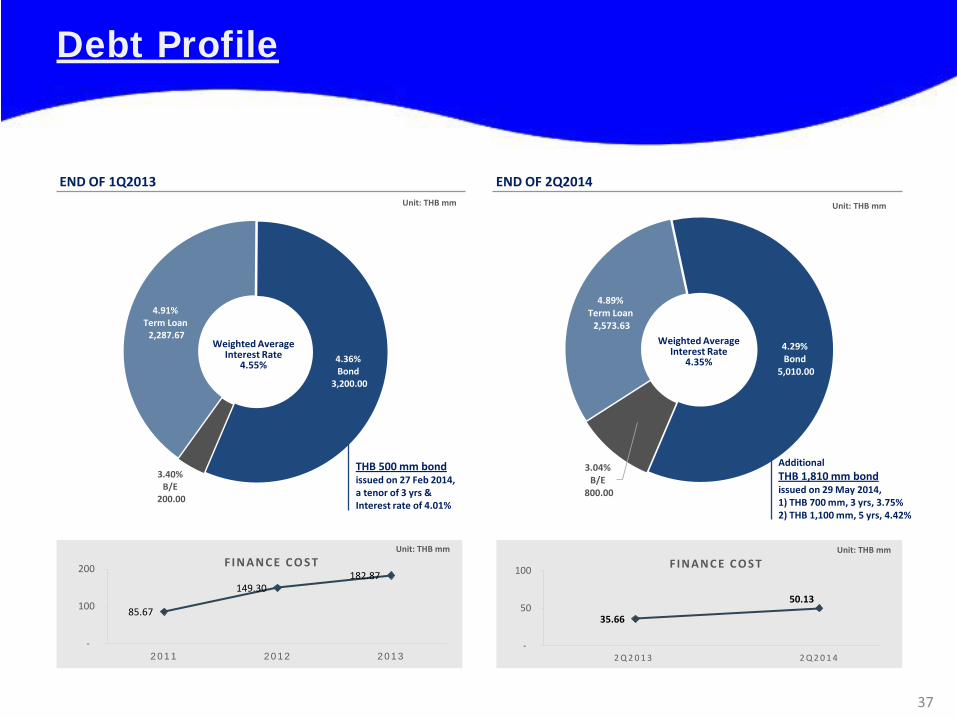

3.04%B/E

800.00

4.89%Term Loan

2,573.63

4.29%Bond

5,010.00

Debt Profile

37

Unit: THB mm

END OF 2Q2014 END OF 1Q2013

Weighted Average Interest Rate

4.35%

Additional THB 1,810 mm bond issued on 29 May 2014, 1) THB 700 mm, 3 yrs, 3.75% 2) THB 1,100 mm, 5 yrs, 4.42%

Unit: THB mm

85.67

149.30 182.87

-

100

200

2011 2012 2013

F IN AN C E C O S TUnit: THB mm Unit: THB mm

3.40%B/E

200.00

4.91%Term Loan

2,287.67

4.36%Bond

3,200.00

Weighted Average Interest Rate

4.55%

THB 500 mm bond issued on 27 Feb 2014, a tenor of 3 yrs & Interest rate of 4.01%

35.66

50.13

-

50

100

2 Q 2 0 1 3 2 Q 2 0 1 4

F IN AN C E C O S T

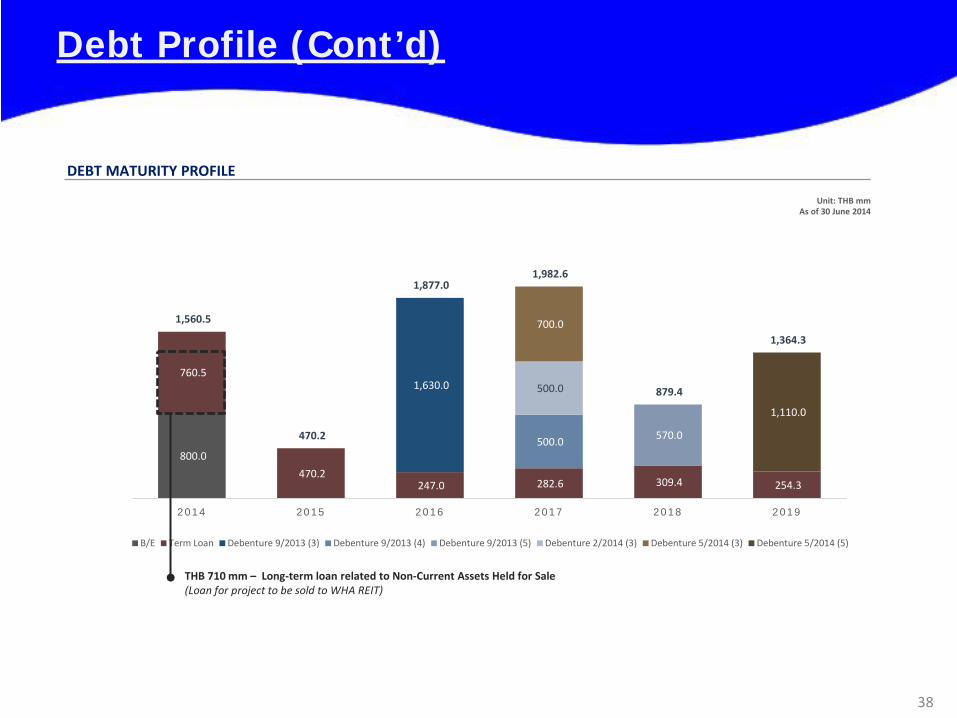

800.0

760.5

470.2 247.0 282.6 309.4 254.3

1,630.0

500.0 570.0

500.0

700.0

1,110.0

1,560.5

470.2

1,877.0 1,982.6

879.4

1,364.3

2014 2015 2016 2017 2018 2019

B/E Term Loan Debenture 9/2013 (3) Debenture 9/2013 (4) Debenture 9/2013 (5) Debenture 2/2014 (3) Debenture 5/2014 (3) Debenture 5/2014 (5)

Debt Profile (Cont’d)

38

Unit: THB mm As of 30 June 2014

DEBT MATURITY PROFILE

THB 710 mm – Long-term loan related to Non-Current Assets Held for Sale (Loan for project to be sold to WHA REIT)

39

Agenda

39

40

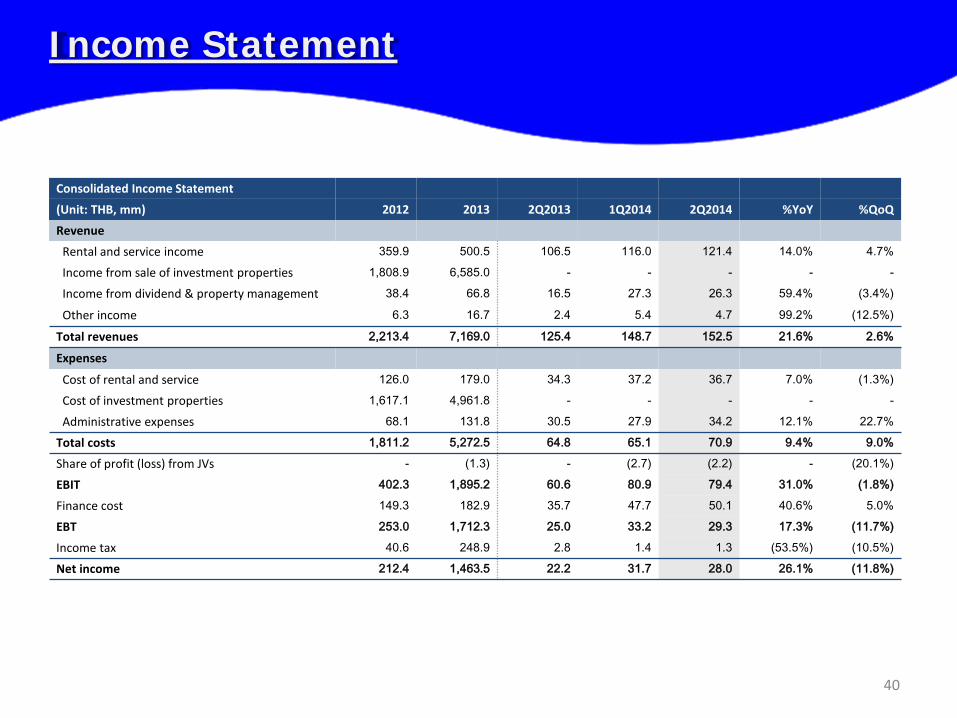

Income Statement

Consolidated Income Statement

(Unit: THB, mm) 2012 2013 2Q2013 1Q2014 2Q2014 %YoY %QoQ

Revenue

Rental and service income 359.9 500.5 106.5 116.0 121.4 14.0% 4.7%

Income from sale of investment properties 1,808.9 6,585.0 - - - - -

Income from dividend & property management 38.4 66.8 16.5 27.3 26.3 59.4% (3.4%)

Other income 6.3 16.7 2.4 5.4 4.7 99.2% (12.5%)

Total revenues 2,213.4 7,169.0 125.4 148.7 152.5 21.6% 2.6%

Expenses

Cost of rental and service 126.0 179.0 34.3 37.2 36.7 7.0% (1.3%)

Cost of investment properties 1,617.1 4,961.8 - - - - -

Administrative expenses 68.1 131.8 30.5 27.9 34.2 12.1% 22.7%

Total costs 1,811.2 5,272.5 64.8 65.1 70.9 9.4% 9.0%

Share of profit (loss) from JVs - (1.3) - (2.7) (2.2) - (20.1%)

EBIT 402.3 1,895.2 60.6 80.9 79.4 31.0% (1.8%)

Finance cost 149.3 182.9 35.7 47.7 50.1 40.6% 5.0%

EBT 253.0 1,712.3 25.0 33.2 29.3 17.3% (11.7%)

Income tax 40.6 248.9 2.8 1.4 1.3 (53.5%) (10.5%)

Net income 212.4 1,463.5 22.2 31.7 28.0 26.1% (11.8%)

41

Balance Sheet

Consolidated Balance Sheet (Unit: THB, mm) 2012 2013 1Q2014 2Q2014 Increase (Decrease) Current assets Cash and cash equivalents 978.7 319.8 77.2 483.5 406.3 526.3% ST investment 116.7 663.5 98.6 107.6 9.1 9.2% Non-current assets held-for-sale 1,861.6 2,225.1 2,921.5 2,935.1 13.6 0.5% Other current assets 473.6 123.4 183.2 137.2 (46.0) (25.1%) Total current assets 3,430.5 3,331.8 3,280.5 3,663.5 383.0 11.7% Non-current assets Investment properties (net) 3,936.6 6,167.2 6,487.7 7,513.9 1,026.2 15.8% Leasehold rights (net) 165.0 64.0 63.4 62.9 (0.5) (0.9%) Building improvement and equipment (net) 26.2 43.4 48.6 47.8 (0.8) (1.6%) Other non-current assets 739.2 1,442.4 1,699.9 1,967.3 267.3 15.7% Total non-current assets 4,867.0 7,717.0 8,299.6 9,591.9 1,292.3 15.6% Total assets 8,297.5 11,048.9 11,580.1 13,255.4 1,675.3 14.5% Liabilities Bank overdrafts and ST borrowings 4.3 198.7 198.7 792.6 593.9 298.9% Trade and other payables 645.4 1,123.1 1,210.9 1,015.7 (195.2) (16.1%) Current portion of LT borrowings – FN institutions

981.1 87.0 173.0 123.0 (50.0) (28.9%)

Other current liabilities 755.0 1,120.9 1,135.8 905.2 (230.6) (20.3%) LT borrowings – FN institutions (net) 2,603.6 1,501.9 1,404.7 1,740.6 336.0 23.9% Debentures (net) - 2,695.3 3,195.0 5,002.7 1,807.6 56.6% Other non-current liabilities 421.0 168.1 88.4 131.3 43.0 48.6% Total liabilities 5,410.5 6,895.1 7,406.5 9,711.1 2,304.6 31.1% Shareholders’ equity 2,887.1 4,153.8 4,173.7 3,544.3 (629.3) (15.1%) Total liabilities and Shareholders’ equity 8,297.5 11,048.9 11,580.1 13,255.4 1,675.3 14.5%

42

“Target at Well-known MNCs”

“Currently 80% of our customers are well-known MNCs because they realize the importance of logistic system that can substantially save their operating costs. Even though our price per sq.m. is 30-50% over that of the industry average, it’s worth investment for them”

Source: Business Thai

“ The largest premium warehouse in Southeast Asia”

“WHA aims to build large distribution centers that suit the customer’s specific needs. Right now, we are the largest premium warehouse in Southeast Asia constructed under well accepted international standard and equipped with innovative technology”

Source: logistic Digest

Dr. Somyos Anantaprayoon Chief Executive Officer A Director since incorporation Group’s CEO who originated the

idea of world-class standard Built-to-Suit Warehouse and DC

Ms. Jareeporn Anantaprayoon Managing Director A Director since incorporation Assist the CEO in business strategy

development Responsible for Group’s sales and

marketing

Mr. Surathian Chakthranont Director Advise on business strategy &plan Previous President of SC Asset

Corporation, PCL (1995 – 2005) More than 10 years experience in

Real Estate sector

Dr. Pichit Akrathit Independent Director Chairman of the Audit Committee An advisor to several leading

companies

Mr. Jakrit Chaisanit Director Head of Construction Management Division

Mr. Narong Kritchanchai Director

Mr. Somsak Boonchoyruengchai

Director Head of Accounting division

Dr. Somsak Pratomsrimek Independent Director Member of the Audit Committee

Dr. Kritsana Sukboonyasatit Independent Director Member of the Audit Committee

Mr. Arttavit Chalermsaphayakorn

Director Chief Financial Officer

“WHA Expertise”

“WHA Corporation is regarded as the world class built-to-suit warehouse developer with strong reputation in selecting prime location, operational efficiency and after sales service”

Source: www.freightmaxad.com

Board of Directors

Dr. Apichai Boontherawara Independent Director Member of the Audit Committee

43

1121 Moo.3 Theparak Rd., Theparak, A. Muang, Samutprakarn 10270 Thailand

Tel. +66 (0) 2 753 3750

Fax. +66 (0) 2 753 2750

e-mail: [email protected] Website: www.wha.co.th

WHA Corporation PCL.