Embed Size (px)

Citation preview

1

1

May 30th 2014 Week 22

HIGHLIGHTS

Capesize: A firming

market is pushing

rates upward

Panamax: Increasing

number of grain car-

goes out of US

L&S INDEX OF DRY

BULK STOCKS*

Due to somewhat higher de-mand for iron ore and coal, we have seen a firming Cape mar-ket with West Australia/ Qing-dao rates pushing above US$8/Mt for the first time in a while. The transatlantic market has seen improved activity with much of the spot/prompt ton-nage fixed. The front haul mar-ket keeps edging upwards, and charterers are aiming at US$ 19.25/Mt. Towards the end of the week rates in the Pacific surged even more, and the highest reported fixture was reported at US$8.85/Mt. Not too much action for period rates, 1 year TC was said to be fixed at US$20,500/day with early delivery in Brazil.

At the beginning of the week there was still oversupply of tonnage and not enough fresh enquiries to boost the rates in the Pacific. Rates for US Gulf/ Far East remained unchanged, likewise for East Coast South Australia. Owners willing to take the trip at this moment are still able to hold out for slightly higher rates, and wait for the activity from US Gulf to pick up. Mid- week, we started to see better sentiment in the market, more US grain cargoes started to fill the market for September and stimulated owners to increase their rates from approximately US$41.5/Mt up to US$43-44/Mt. This could tempt owners to switch their focus away from transat-lantic onto front haul voyag-es. We have seen more DOP fixing in the East this week, although there is not enough

volume to exclude the APS market. The East Coast South Australia market also firmed towards the week-end.

Both Handymax and Supramax markets continued to move upwards last week with gains across the board. Although rates in the Pacific finished higher at the close of the week, rates are still on the low side, with a lot of tonnage available in the South East Asia region. Activity in the Atlantic contin-ued to increase, and is ex-pected to continue with the US Gulf market on the rise and the coming grain season in the Black Sea upon us. With the winding down of summer holi-days we expect to see contin-ued improvement in both ba-sins.

Week 33

CAPESIZE PANAMAX

SUPRAMAX/HANDY

-Shipbrokers and consultants since 1919-

Weekly Dry Bulk Report

0

20,000

40,000

60,000

80,000

100,000

120,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

US$/day Capesize Timecharter Average (TCA)

5 Yr Low 5 Yr High 5 Yr Avg 2014 Ytd

2

2

Iron Ore

-Shipbrokers and consultants since 1919-

Oversupply in coal market

can mean fourth quarter

seasonal demand has less

effect on prices than usual

Spot iron ore prices sat at

US$93.40/ton by week’s end,

down from US$95.30/ton at

the beginning of the week.

The closing price was still up

from midweek lows. The iron

ore price has slumped by 31

per cent from US$135/ton at

the beginning of the year.

The average price for the

year this far is US$108.40/

ton, should this be indicative

of developments for the re-

mainder of 2014, iron ore

producers would take a

US$18 bn hit to revenues.

Iron ore futures in China fell

to a two-week low last week,

reflecting an oversupplied

market where demand from

the Chinese steel-industry is

growing at a lower rate than

previously. Cash and credit

restrictions in the Chinese

property market seem to be

keeping the steel-making

industry from undertaking a

major restocking of iron ore

at the moment. Chinese trad-

ers cut their offers for iron

ore cargoes stocked at port

by 5-10 Yuan/ton last week,

according to the Steel Index.

Australia’s BC Iron ltd. has

completed a deal to buy Iron

Ore Holdings ltd. with a com-

bination of cash and stocks

totaling US$233 million. The

transaction will create a new

midsize producer in Western

Australia’s Pilbara region,

which produces more than

half of the world’s iron ore

for seaborne trade. (Sources:

WSJ, Reuters)

Coal

Grain

Low thermal coal prices are

reflecting the oversupply

and weak demand in the

current market. Some play-

ers argue that the market is

set to balance itself, leading

to an increase in prices in

the coming year citing that

falling investment in new

production in Australia and

Indonesia is likely to create

less supply. The plentiful

supplies might however be

in volumes enough to offset

a price gain from increased

seasonal demand as the

Western Hemisphere moves

into the winter months,

causing price levels to gain

less momentum than usual.

Prices increased by 8.1 per

cent in the same period in

2013, and 7.6 percent in

2012.

Takeover in Australia as

BC Iron ltd. buys Iron Ore

Holding ltd.

Wheat crops in France, EU’s

top wheat exporter and the

benchmark for Western Eu-

rope prices, have been se-

verely affected by heavy

rains this summer, and the

country’s exports are set to

remain predominantly within

the EU trading area for the

first time in seven years.

French exporters are increas-

ingly turning to feedstock

traders in the region as large

crop volumes are rated at a

lower quality than that de-

manded by large importers in

the Middle East and North

Africa. Ukraine’s grain ex-

ports were reported to be up

by 60 per cent to 2.7 million

tons in the past five weeks, a

multi-year record. A weaker

credit market as a result of

the current crisis has caused

farmers to increase sales to

cover cost of planting and

sowing preparations.

3

3

-Shipbrokers and consultants since 1919-

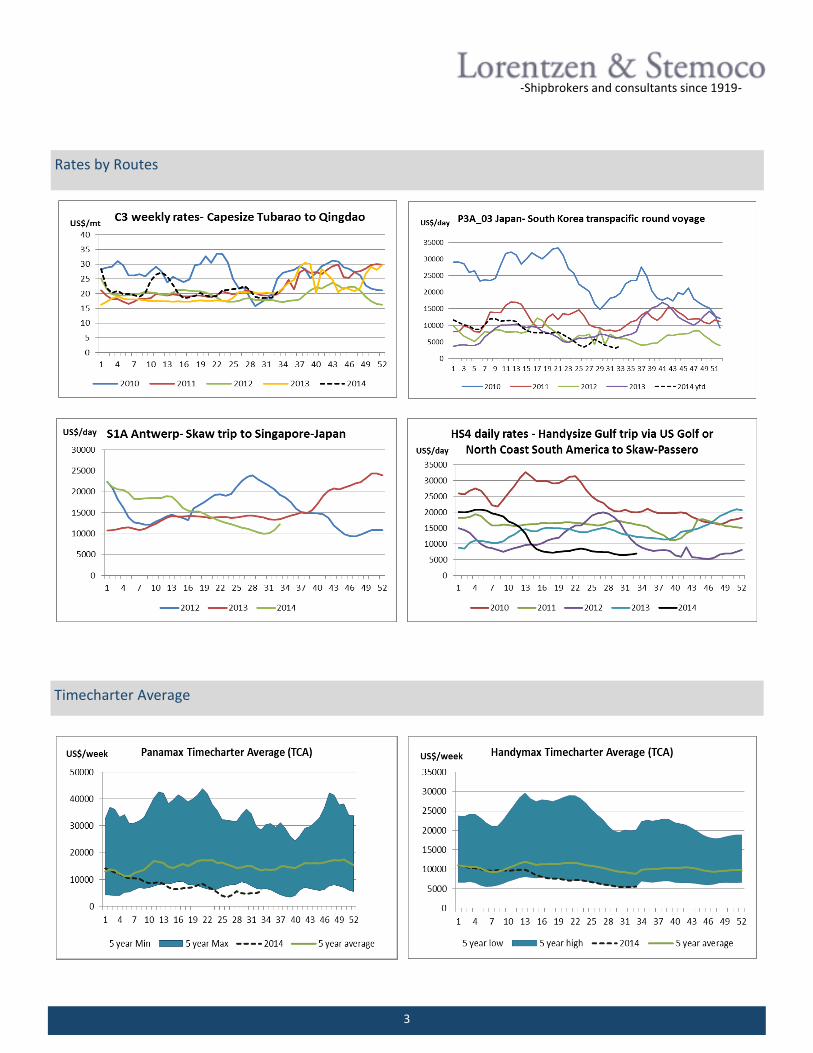

Rates by Routes

Timecharter Average

4

4

-Shipbrokers and consultants since 1919-

*Basket of stocks for L&S Index on page 1 includes: Golden Ocean Group Ltd., Western Bulk ASA, Scorpio Bulkers Inc., Paragon Shipping

Inc., Baltic Trading Ltd., Diana Shipping Inc., DryShips Inc., Safe Bulkers Inc., and Star Bulk Carriers Corp.

The Baltic Exchange Dry Index Last Week This Week Trend

Weekly Baltic Average C5 (US$/pmt) 7.60 8.34 Firming

Weekly Baltic Average C3 (US$/pmt) 18.64 20.50 Firming

Weekly Baltic Average H4 (US$/day) 6,627 6,941 Firming

Weekly Baltic Average P3A IV (US$/pmt) 11.44 11.72 Firming

Weekly BDI Average 762 891 Firming

FFA Last Week This Week Trend

Capesize (C3+2Q) (US$/day) 19,127 19,800 Firming

Panamax (P1EA+2Q) (US$/day) 8,810 9,623 Firming

Supramax (5TC_S+2Q) (US$/day) 9,545 10,481 Firming

Bunker Prices Last Week This Week Trend

Rotterdam IFO 380 (US$/pmt) 567 566 Softening

Rotterdam MGO (US$/pmt) 854 859 Firming

Singapore IFO 380 (US$/pmt) 598 592 Softening

Singapore MGO (US$/pmt) 873 882 Firming

5

5

Dry Cargo Offices

Office Name Telephone number E-mail

Athens

Lars Juul Jørgensen +30 6948 364 642 [email protected]

Tony Westbrook +30 6947 401 636 [email protected]

Chris Allen +30 6951 666 788 [email protected]

Singapore

Mehmet Burak Ughur +65 6349 8400 [email protected]

Ertugrul Erdem +65 6714 1015 [email protected]

Pierre Lambert +65 6348 8403 [email protected]

Nicolas Lamoine +65 6349 8400 [email protected]

Daan Van Velzen +65 6349 8402 [email protected]

Ella Tang +65 6349 8419 [email protected]

Sebastian Bull Øvrevik +65 6349 8411 [email protected]

Erling Lystad +65 6349 8420 [email protected]

Ivan Andrade +65 9383 7125 [email protected]

Ulas Durali +65 6349 8415 [email protected]

Jiajun Wang +65 6349 8417 [email protected]

Eystein Lyche +65 6349 8407 [email protected]

Parijat Mishra +65 6349 8406 [email protected]

Kwai Leng Seetoh +65 6349 8401 [email protected]

Shanghai

Einar Karlsen +86 21 6391 5663 [email protected]

Joseph Wang +86 21 6391 5595 [email protected]

Nick Chen +86 21 6391 5768 [email protected]

Yajie Luo (Jessica) +86 21 6391 5553 [email protected]

Wenyan Zhang (Kelvin) +86 21 6391 5552 [email protected]

Richard Brayshaw +86 21 6391 5878 [email protected]

New York

Nicholas Tangney +1 212 684 2503 [email protected]

Robert B. Tangney +1 914 244 1006 [email protected]

Michael Perry +1 212 684 2505 [email protected]

Research

Knut Stangebye Olsen +47 22 52 77 03 [email protected]

Silje Elise Lien +47 22 52 77 14 [email protected]

Marthe Lamp Sandvik +47 22 52 77 00 [email protected]

Operation Michael Hansson +47 22 52 77 23 [email protected]