Embed Size (px)

Citation preview

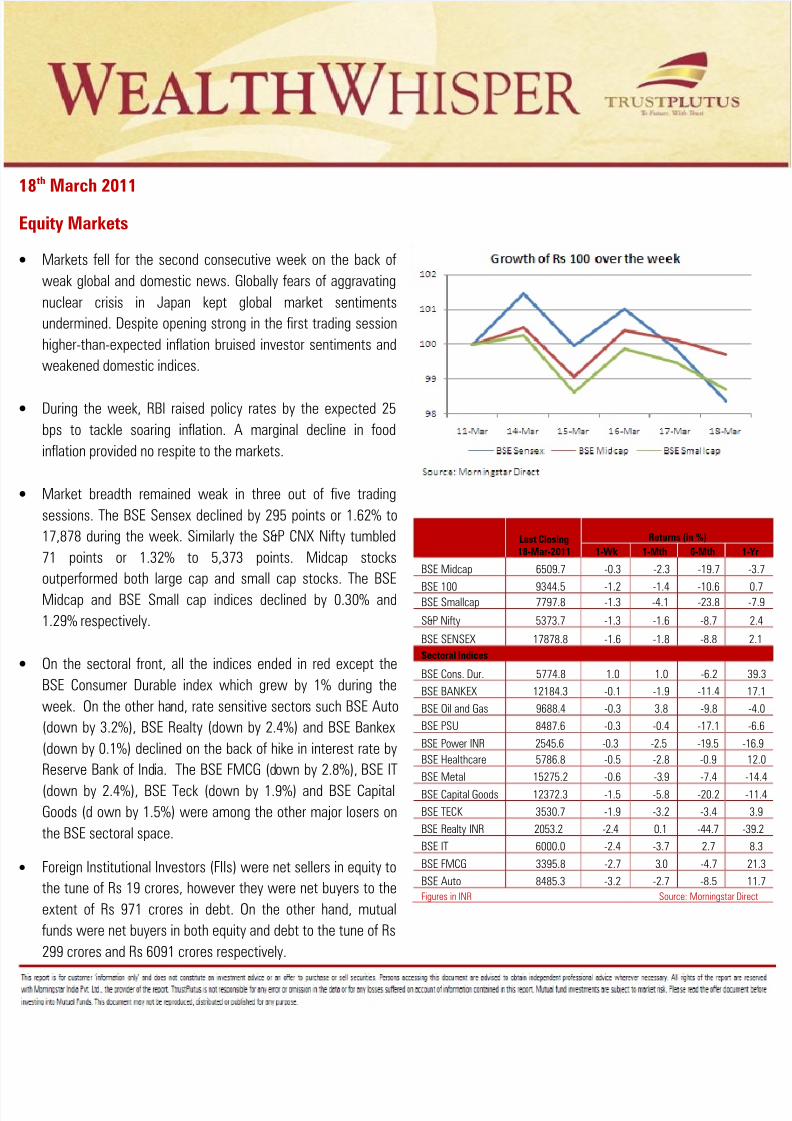

8/7/2019 Wealth Whisper - March 18 2011

http://slidepdf.com/reader/full/wealth-whisper-march-18-2011 1/5

8/7/2019 Wealth Whisper - March 18 2011

http://slidepdf.com/reader/full/wealth-whisper-march-18-2011 2/5

MFs & FIIs Net Investments

1 Wk MTD YTD

MFs*

Equity 298.9 562.0 2595.1

Debt 6091.4 29368.1 89439.9

FIIs ^

Equity -19.3 1,824.7 -7,577

Debt 971.6 2618 14,110.5

Figures in INR Crores. *MF data as on March 17, 2011. ^FII data as on March 18, 2011.

NSE Advance/ Decline ratio

Date Advances Declines Advance/Decline ratio

14-Mar-11 794 634 1.315-Mar-11 248 1196 0.216-Mar-11 1013 425 2.417-Mar-11 504 917 0.518-Mar-11 445 994 0.4

Source: NSE Website

Fixed Income

Government bonds ended the week lower primarily on theback of concerns over rising crude oil prices, which may stokeinflation further.

In order to contain inflationary pressure, RBI, in its mid-quartermonetary policy review on March 17, hiked repo and reverserepo rates by 25 bps each. Given the hike was on the expectedline supported the bond prices.

Government bonds also found support from the absence offresh supply of bonds this week; which may further extend tothe rest of the FY 2010-11.

During the week, government bonds were hit the most by thesurge in headline inflation and with the RBI raising its year-endinflation projection to 8% from 7% earlier.

• Also, the sharp rise in crude prices due to ongoinin Libya pose a threat for the domestic inflation.

• RBI, while announcing its monetary policy concerns that underlying inflationary pressuaccentuating, and high oil prices posed an upwThis fanned fear that RBI may have a case for hifurther in the near future.

• Concern over inflation also heightened after inflation for the week ended March 5, 2011 su12.79% from 9.48% in the prior week.

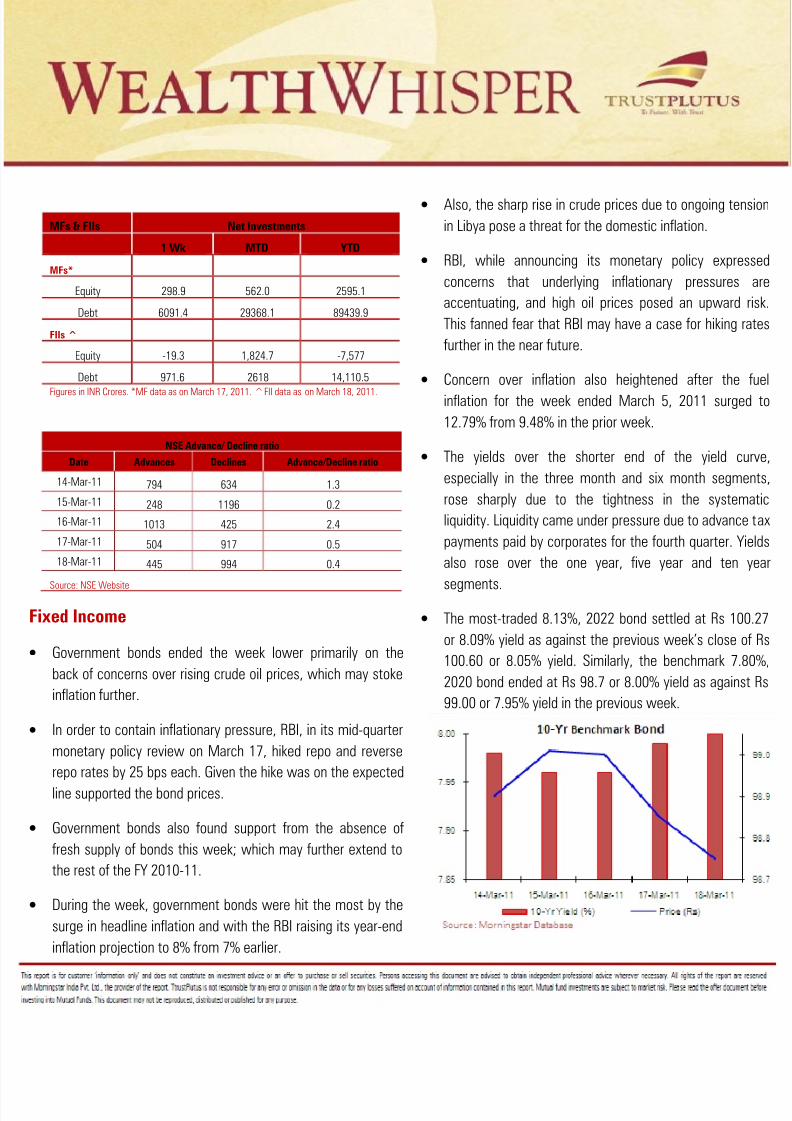

• The yields over the shorter end of the yielespecially in the three month and six month serose sharply due to the tightness in the sysliquidity. Liquidity came under pressure due to adpayments paid by corporates for the fourth quartealso rose over the one year, five year and t

segments.• The most-traded 8.13%, 2022 bond settled at Rs

or 8.09% yield as against the previous week’s clo100.60 or 8.05% yield. Similarly, the benchmar2020 bond ended at Rs 98.7 or 8.00% yield as ag99.00 or 7.95% yield in the previous week.

8/7/2019 Wealth Whisper - March 18 2011

http://slidepdf.com/reader/full/wealth-whisper-march-18-2011 3/5

Debt Indicators (Yield %)CurrentValue

1-WkAgo

1-MthAgo

6-MthAgo

1-YrAgo

Call Rate 7.47 6.80 6.82 6.11 3.34

90 Day T-Bill 7.20 7.13 7.12 6.10 4.38

7.17%, 2015 5-Yr GOI Bond 7.93 7.91 8.08 7.77 -

7.80%, 2020 10-Yr GOI Bond 8.00 7.95 8.10 7.98 -Source: CCIL, Morningstar Database; Current Value as on March 18, 2011

IndicesLast Closing18-Mar-2011

Return (in %)

1-Wk 1-Mth 6-Mth 1

US

DJ Industrial Avg. 11858.5 -1.5 -4.3 11.8

S&P 500 1279.2 -1.9 -4.8 13.6

NASDAQ 100 2221.1 -3.4 -7.2 13.6

Europe

UK: FTSE 100 5718.1 -1.9 -6.0 3.8

France: CAC 40 3810.2 -3.0 -8.3 2.4

Germany: DAX 3893.8 -4.6 -10.3 7.0

Asia Pacific

China: Shanghai 2906.9 -0.9 0.2 11.9

Singapore: STI 2935.8 -3.5 -4.9 -4.6

HK: Hang Seng 22300.2 -4.1 -5.5 1.5

Japan: Nikkei 225 9206.8 -10.2 -15.1 -4.4

Figures in Base Currency; Source: Morning

lobal Markets

nited States

U.S. stocks remained under pressure during the week on theback of uncertainty arising from the recent quake and thedamage it has caused. Accelerating inflation in China andfurther turmoil in Libya and Saudi Arabia added to the weaksentiment.

The U.S. Labor Department reported the consumer price indexrose 0.5% in February, driven by higher energy costs. Inflationrose 0.4% in the both the preceding months of December andJanuary.

U.S. industrial production decreased 0.1% in February,following a revised 0.3% gain in the month of January.

Europe

• European markets also were weak on the back of mlosses from the Japanese earthquake-tsunami, and uthe Middle East region.

• German markets fell the most during the week, as speculated how much loss the German insurance coand power companies would suffer from the recent

Japan.

• Following the downgrade of Spain, ratings agencycut Portugal’s credit rating last week by two notchon weaker growth prospects.

• Euro-zone inflation rose to 2.4% in February froJanuary, on the back of rising energy prices.

8/7/2019 Wealth Whisper - March 18 2011

http://slidepdf.com/reader/full/wealth-whisper-march-18-2011 4/5

CommoditiesLast Closing18-Mar-2011

Return (in %)

1-Wk 1-Mth 6-Mth 1-Yr

Crude - WTI ($/Barrel) 101 -1.23 19.31 36.06 22.36

Gold ($/Oz) 1,420 0.60 2.64 11.46 26.50

Silver ($/Oz) 35 3.08 10.05 68.59 101.07

Figures in Base Currency Source: Morningstar Direct

CurrencyLast Closing18-Mar-2011

1-WkAgo

1-MthAgo

6-MthAgo

US Dollar 45.1 45.2 45.3 45.9

Pound Sterling 73.0 72.5 73.2 71.7

Euro 63.8 62.6 61.6 59.9

Yen (Per Rs. 100) 55.6 55.3 54.4 53.4 Figures in INR Source: Morningstar

sia

Asian equities also closed the week on a weak note withJapan’s benchmark Nikkei index losing more than 10%. Thecountry’s nuclear crisis deepened after two more explosionsoccurred at Fukushima Daiichi nuclear power plant.

The Bank of Japan meanwhile pumped in records amount ofmoney into the nation’s money markets to soothe the jitterymarkets. The central bank injected 3.5 trillion yen into marketson Wednesday, which came after injections totaling 23 trillionyen.

China’s central bank meanwhile announced on Friday that it israising the bank reserve requirement ratio by 50 bps, effectivefrom March 25. This is the third such move this year by thePeo le’s Bank of China.

Commodities

During the week, international gold prices rose by a marginal0.60% to end at $ 1,420 per ounce. The rise in the gold pricesin the recent times can be attributable to the investor demandfor an alternative to volatile currencies.

Gold also gained as the fighting in Libya and unrest in Bahrainboosted demand for safer assets. This resulted in investorsturning towards gold, which drove its prices upwards.

• After falling marginally last week, silver rose by week in the global markets on higher industrial oinvestment buying.

• International crude oil prices fell for the week by$ 101 per barrel. The fall in oil prices was triggLibya said it would end military operations agaiand begin talks aimed at resolving the dispute truncated crude shipments. During the we

International Energy Agency announced that Liboil exports might be halted for many months dudamage to oil supplying facilities and intesanctions.

Forex

• The yen continued to appreciate against the dJapanese investors repatriated money back homethe nation’s biggest disaster since the Second WoThe yen breached the psychological barrier of 8the dollar but its rise was curbed after G7 nationto weaken the currency. The yen also appreciatedthe rupee during the course of the week.

• The dollar also weakened against the euro quiteduring the week with Euro zone leaders reachiprinciple agreement on a pact for the Euro to c

Performance of Rupee Vs other currencies

8/7/2019 Wealth Whisper - March 18 2011

http://slidepdf.com/reader/full/wealth-whisper-march-18-2011 5/5

Foreign Institutional Investors were net sellers to the tune of $4million in Indian equity markets during the week.

There were reports of some state owned banks in India sellingthe dollar, anticipating a hike in policy rates by the central bankin India. The RBI hiked both the repo and reverse repo rate by 25bps; leaving the CRR unchanged.

Key Economic News

Food inflation eased to 9.42% from 9.52% in the previous weekprimarily due to fall in prices of milk and onion. For the week,prices of vegetables increased by 0.28% while that of onion fell11.36%. Prices of fruits increased by 3.78%, while prices ofother sources of proteins registered a decline. However Inflationin fuel and power rose 3.31 percentage points to 12.79%.

Headline inflation accelerated in February increasing pressure on

the Reserve Bank of India to further tighten its monetary policy.The benchmark wholesale price index, or WPI, rose 8.31% fromthe year before. In January, inflation was at 8.23%. The rise inFebruary was despite a moderation in prices of food articles asrising fuel prices played a spoil sport.

The Reserve Bank of India raised policy rates for the eighth timein a year by the expected 25 basis points to tackle inflation.Repo rate has been raised 25 basis points to 6.75% which is still1.55 percentage points lower than the inflation rate. Reverserepo has been raised by a similar proportion to 5.75%. All otherrates were kept unchanged.

India Inc paid robust advance tax in the fourth quarter this fiscal,an indication of better corporate performance despite concernsover margins and slowdown. The collections for January-March2011 quarter are up about 30% from a year-ago period.

• Exports from special economic zones (SEZs)46.7% year-on-year to Rs 2.23 lakh crore durDecember period of the current fiscal. Tcontributed about one-fourth to the country'sexports.

Mutual Fund News

• Goldman Sachs Group Inc agreed to buy exchan

fund (ETF) specialist Benchmark Asset ManagRs 160 crore to benefit from rising affluencmillions of middle-class people. The acquisition Rs 3,000 crore in assets under management andplatform to expand itself.

• SBI Mutual Fund has declared dividend uMagnum Taxgain Scheme 1993, on the face val10 per unit. The quantum of dividend for distrib4 per unit. The record date for dividend distributiMarch 2011.

• HDFC Mutual Fund has declared Rs 4 per uniunder HDFC Equity Fund and HDFC Long TermThe record date for dividend distribution is 222011.

• DSP BlackRock Mutual Fund has declared diviDSP BlackRock Small & Mid Cap Fund. The dividend for distribution is Rs 1.25 per unit. Tdate for dividend distribution is 18th March 2011

• IDFC Mutual Fund has declared dividend undeAdvantage (ELSS) Fund. The quantum of didistribution is Rs 1 per unit. The record date fodistribution is 23rd March 2011.