Embed Size (px)

Citation preview

Digital Realities Shaping Customer expectations in the banking Industry June 1, 2015Pooneh Mohazzabi

The journey of the future

May 29, 2015

2

May 29, 2015

PwC

PwC

MegatrendsFive forces shaping our lives and our world

Sources: PwC, 2014 US CEO Survey, January 2014

1 2 3 4 5

These represent some of our biggest challenges and opportunities

3

May 29, 2015

PwC

PwC

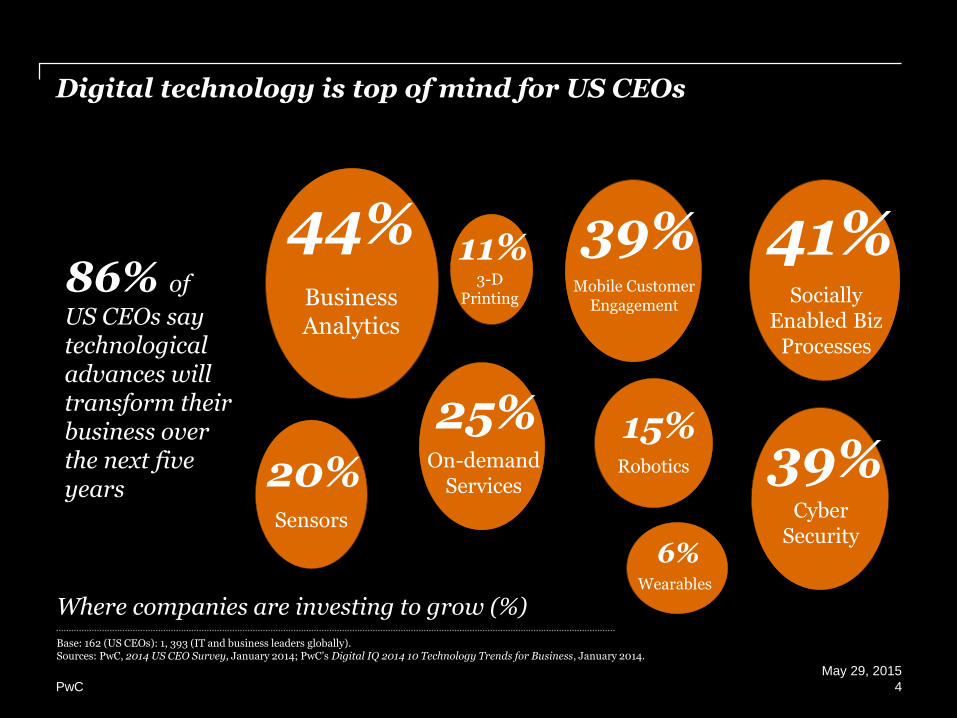

Digital technology is top of mind for US CEOs

Base: 162 (US CEOs): 1, 393 (IT and business leaders globally).Sources: PwC, 2014 US CEO Survey, January 2014; PwC’s Digital IQ 2014 10 Technology Trends for Business, January 2014.

86% of

US CEOs say technological advances will transform their business over the next five years

Where companies are investing to grow (%)

39%Cyber

Security

44%Socially

Enabled Biz Processes

41%Business Analytics

On-demand Services

25%

Sensors

20%

3-D Printing

11%

Wearables

6%

Robotics

15%

39%Mobile Customer

Engagement

4

May 29, 2015

PwC

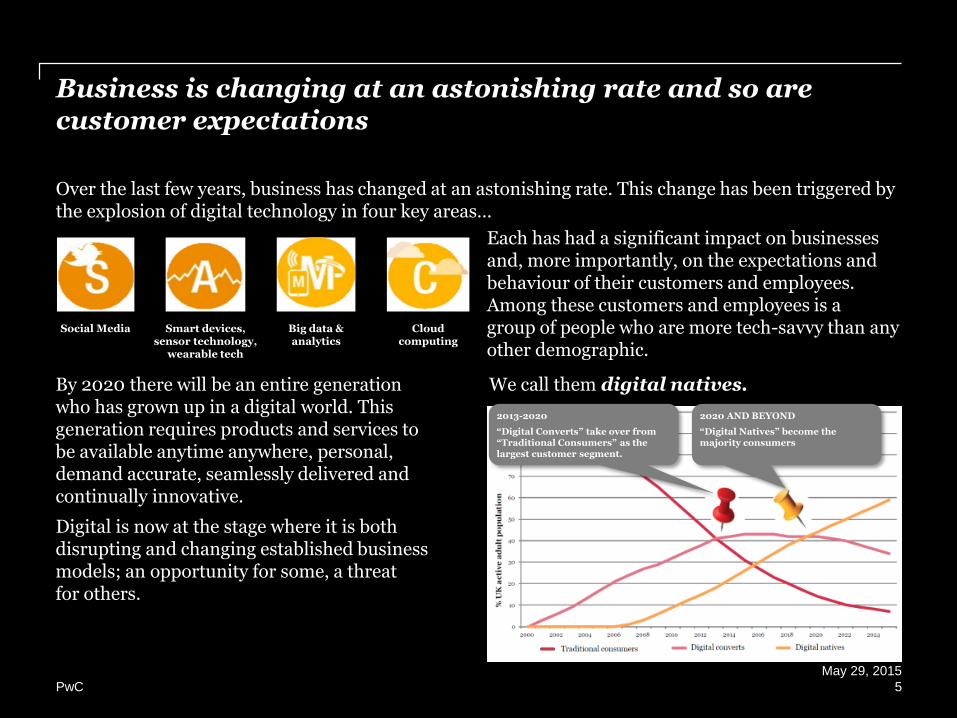

Over the last few years, business has changed at an astonishing rate. This change has been triggered by the explosion of digital technology in four key areas…

Each has had a significant impact on businesses and, more importantly, on the expectations and behaviour of their customers and employees. Among these customers and employees is a group of people who are more tech-savvy than any other demographic.

By 2020 there will be an entire generation who has grown up in a digital world. This generation requires products and services to be available anytime anywhere, personal, demand accurate, seamlessly delivered and continually innovative.

Digital is now at the stage where it is both disrupting and changing established business models; an opportunity for some, a threat for others.

2020 AND BEYOND

“Digital Natives” become the majority consumers

2013-2020

“Digital Converts” take over from “Traditional Consumers” as the largest customer segment.

We call them digital natives.

Social Media Smart devices, sensor technology,

wearable tech

Big data & analytics

Cloud computing

Business is changing at an astonishing rate and so are customer expectations

5

May 29, 2015

PwC

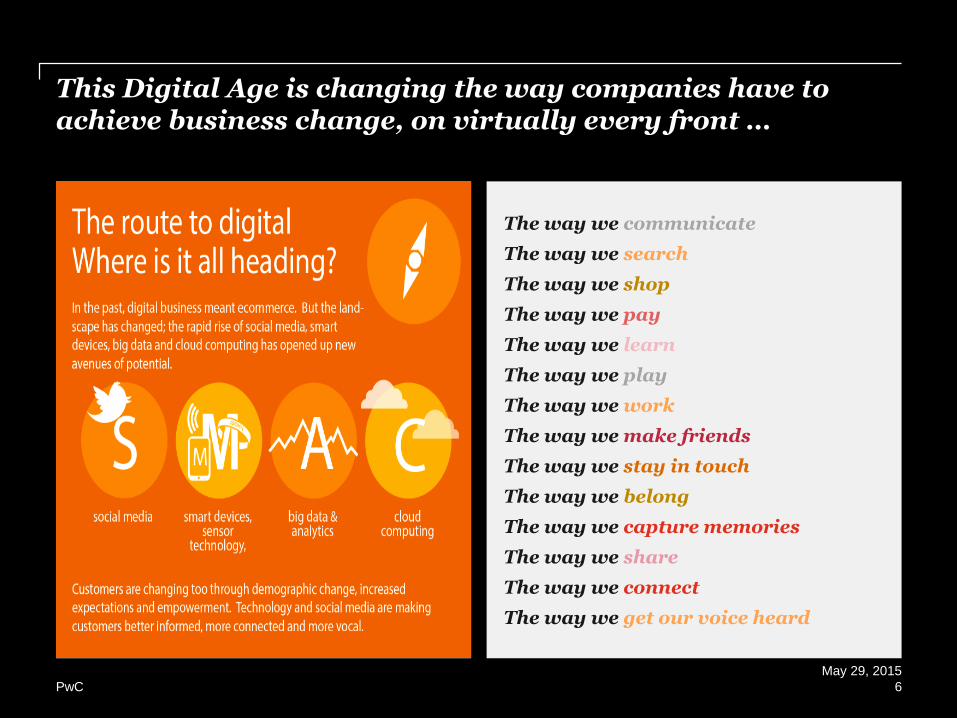

The way we communicate

The way we search

The way we shop

The way we pay

The way we learn

The way we play

The way we work

The way we make friends

The way we stay in touch

The way we belong

The way we capture memories

The way we share

The way we connect

The way we get our voice heard

This Digital Age is changing the way companies have to achieve business change, on virtually every front …

6

May 29, 2015

PwC

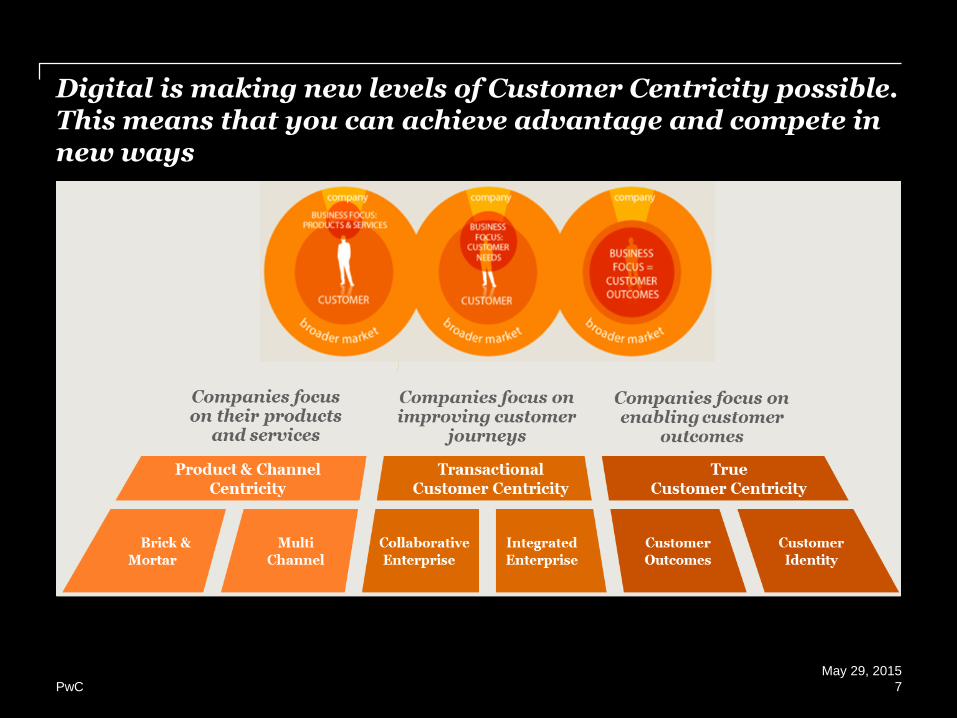

Digital is making new levels of Customer Centricity possible. This means that you can achieve advantage and compete in new ways

7

May 29, 2015

PwC

PwC

Draft

WELCOMETO THE AGE OF DISRUPTION

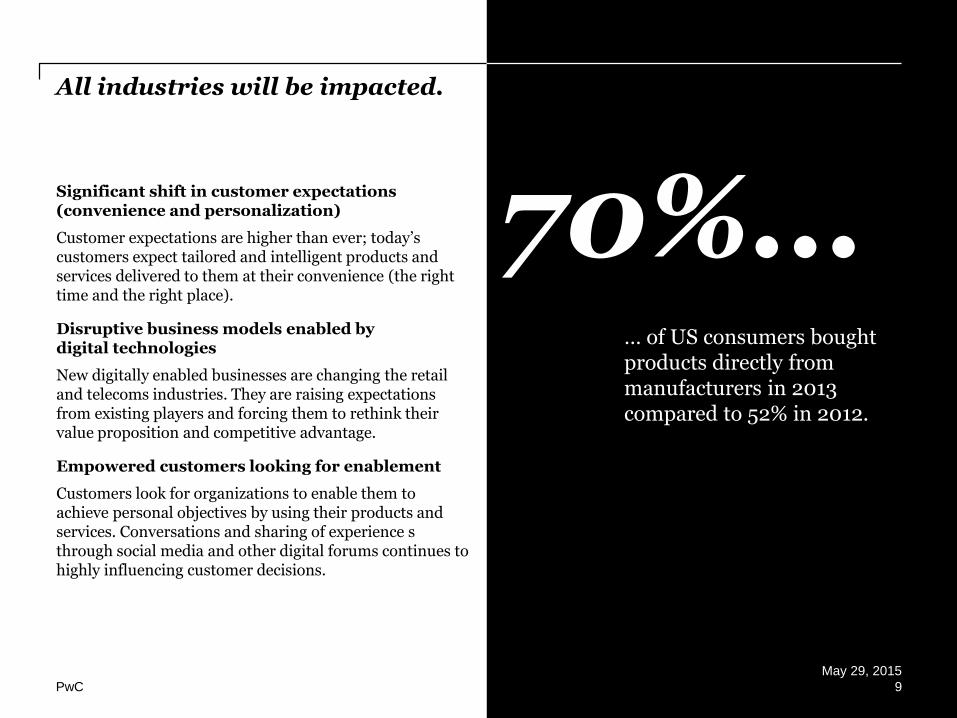

Significant shift in customer expectations (convenience and personalization)

Customer expectations are higher than ever; today’s customers expect tailored and intelligent products and services delivered to them at their convenience (the right time and the right place).

Disruptive business models enabled by digital technologies

New digitally enabled businesses are changing the retail and telecoms industries. They are raising expectations from existing players and forcing them to rethink their value proposition and competitive advantage.

Empowered customers looking for enablement

Customers look for organizations to enable them to achieve personal objectives by using their products and services. Conversations and sharing of experience s through social media and other digital forums continues to highly influencing customer decisions.

70%...… of US consumers bought products directly from manufacturers in 2013 compared to 52% in 2012.

All industries will be impacted.

9

May 29, 2015

PwC

PwC

Draft

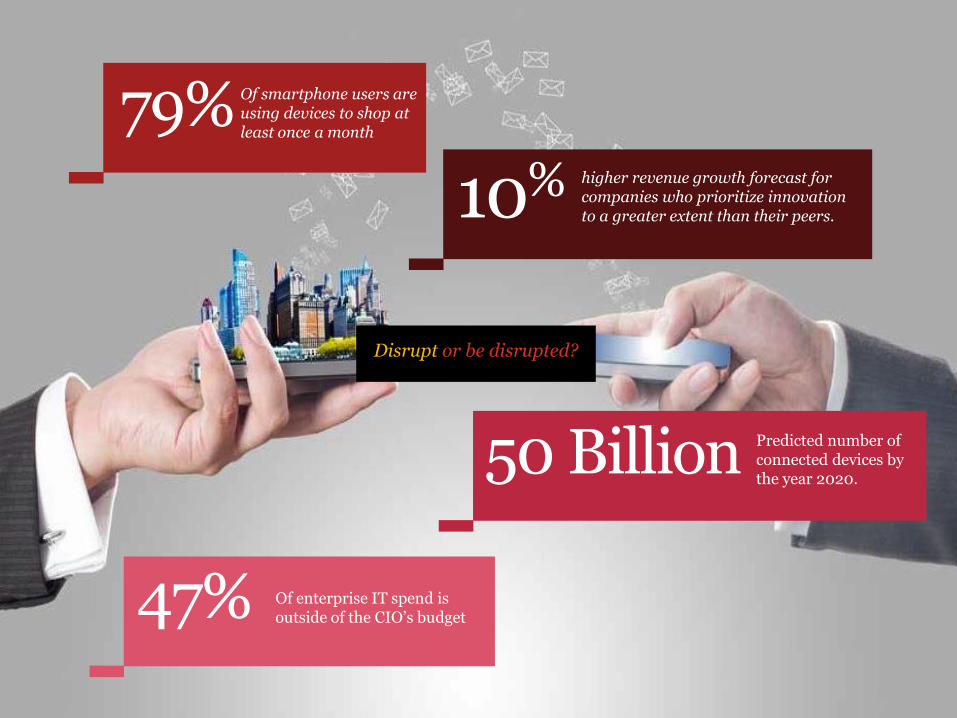

Disrupt or be disrupted?

79% Of smartphone users are using devices to shop at least once a month

Of enterprise IT spend is outside of the CIO’s budget47%

Predicted number of connected devices by the year 2020.

50 Billion

higher revenue growth forecast for companies who prioritize innovation to a greater extent than their peers.10%

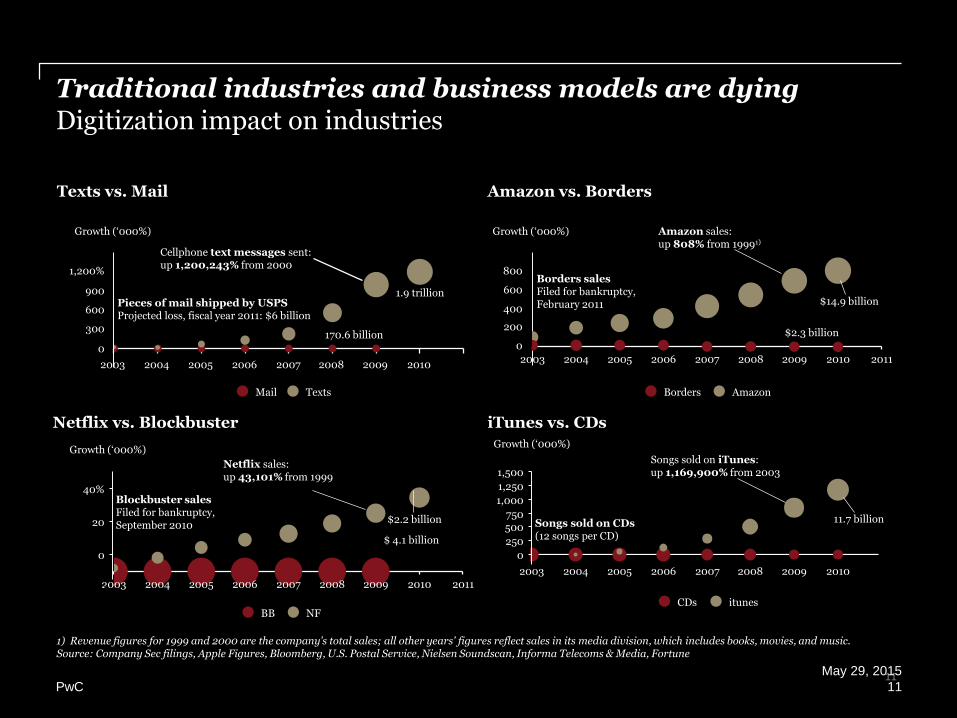

2003 2004 2005 2006 2007 2008 2009 2010 2011

11

40%

20

0

Growth (‘000%)

Netflix sales:up 43,101% from 1999

$2.2 billion

0

20102009200820072006200520042003

1,000

1,500

1,250

500750

250

Growth (‘000%)

11.7 billion

Songs sold on iTunes:up 1,169,900% from 2003

2003 2004 2005 2006 2007 2008 2009 2010 2011

0

200

600

800

400

Growth (‘000%)

$14.9 billion

Amazon sales:up 808% from 19991)

200520042003

900

2008

600

1,200%

2006

300

2007 20102009

0

Cellphone text messages sent:up 1,200,243% from 2000

1.9 trillion

Growth (‘000%)

Pieces of mail shipped by USPSProjected loss, fiscal year 2011: $6 billion

170.6 billion $2.3 billion

Songs sold on CDs(12 songs per CD)

Borders salesFiled for bankruptcy,February 2011

Blockbuster salesFiled for bankruptcy, September 2010

$ 4.1 billion

1) Revenue figures for 1999 and 2000 are the company’s total sales; all other years’ figures reflect sales in its media division, which includes books, movies, and music.Source: Company Sec filings, Apple Figures, Bloomberg, U.S. Postal Service, Nielsen Soundscan, Informa Telecoms & Media, Fortune

TextsMail

Texts vs. Mail

Netflix vs. Blockbuster

NFBB

Amazon vs. Borders

iTunes vs. CDs

Borders Amazon

CDs itunes

Traditional industries and business models are dyingDigitization impact on industries

11

May 29, 2015

PwC

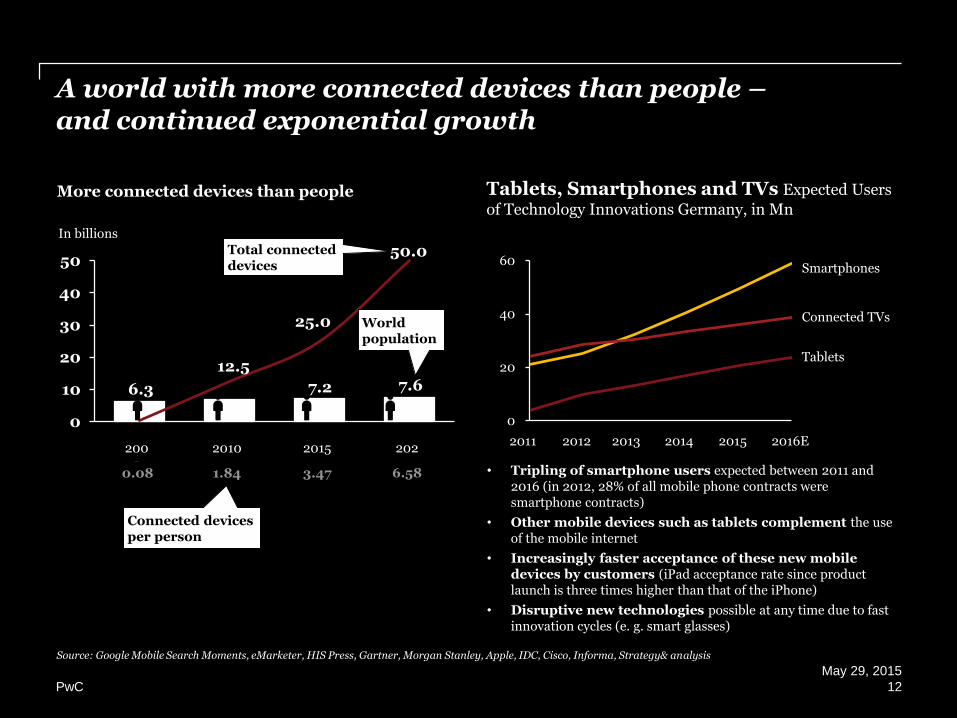

6.3 7.2 7.612.5

25.0

0

10

20

30

40

5050.0

In billions

2020

201520102003

0

20

40

60

20132012

Connected TVs

2016E20142011

Tablets

2015

Smartphones

• Tripling of smartphone users expected between 2011 and 2016 (in 2012, 28% of all mobile phone contracts were smartphone contracts)

• Other mobile devices such as tablets complement the use of the mobile internet

• Increasingly faster acceptance of these new mobile devices by customers (iPad acceptance rate since product launch is three times higher than that of the iPhone)

• Disruptive new technologies possible at any time due to fast innovation cycles (e. g. smart glasses)

More connected devices than people

Total connected devices

Worldpopulation

0.08 1.84 3.47 6.58

Connected devices per person

Tablets, Smartphones and TVs Expected Users

of Technology Innovations Germany, in Mn

Source: Google Mobile Search Moments, eMarketer, HIS Press, Gartner, Morgan Stanley, Apple, IDC, Cisco, Informa, Strategy& analysis

A world with more connected devices than people –and continued exponential growth

12

May 29, 2015

PwC

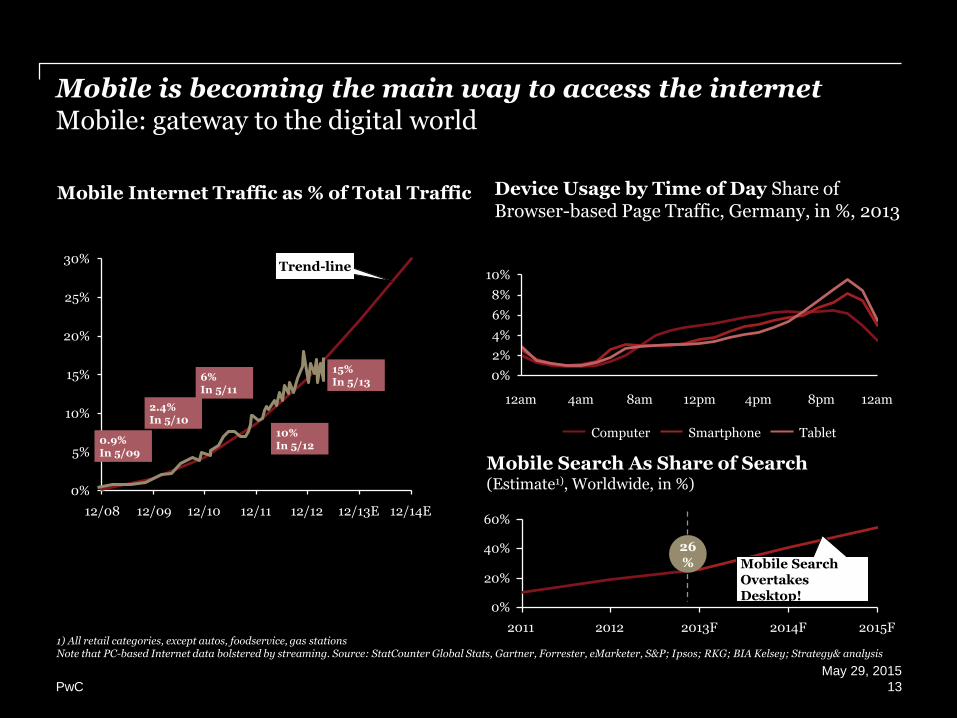

0%

5%

10%

15%

20%

25%

30%

12/09 12/1212/08 12/14E12/1112/10 12/13E

15%In 5/13

10%In 5/12

0.9%In 5/09

6%In 5/11

2.4%In 5/10

2013F 2015F

60%

2011 2014F

0%

2012

40%

20%

26%

0%

2%

4%

6%

8%

10%

12am 4am 8am 12am8pm4pm12pm

Smartphone TabletComputer

Mobile Search As Share of Search(Estimate1), Worldwide, in %)

Mobile Search Overtakes Desktop!

Trend-line

Mobile Internet Traffic as % of Total Traffic Device Usage by Time of Day Share of Browser-based Page Traffic, Germany, in %, 2013

1) All retail categories, except autos, foodservice, gas stationsNote that PC-based Internet data bolstered by streaming. Source: StatCounter Global Stats, Gartner, Forrester, eMarketer, S&P; Ipsos; RKG; BIA Kelsey; Strategy& analysis

Mobile is becoming the main way to access the internetMobile: gateway to the digital world

13

May 29, 2015

PwC

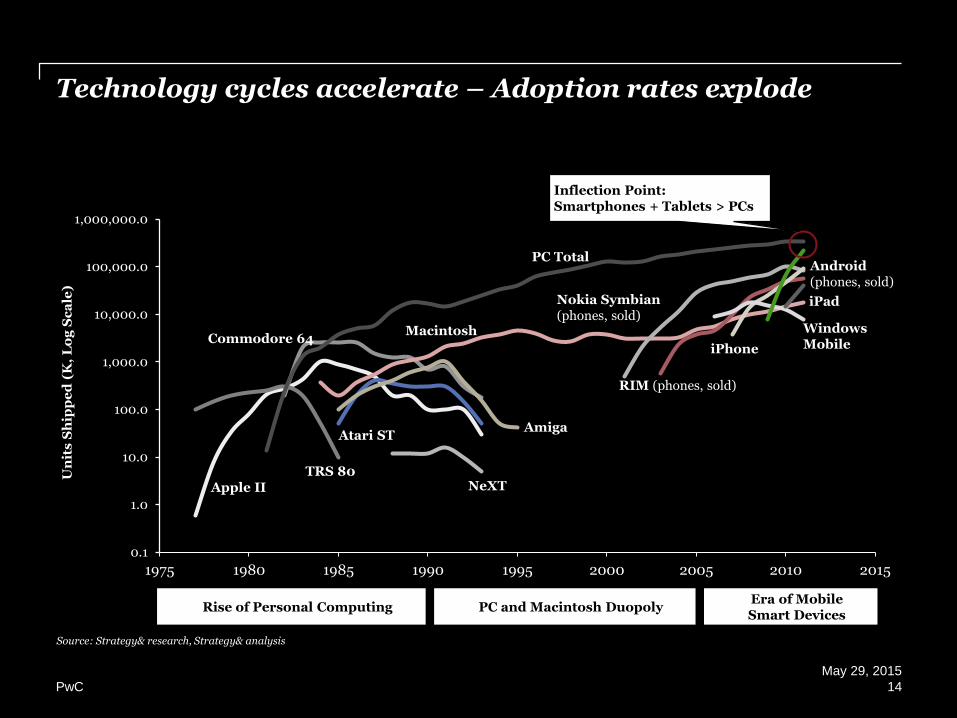

14

0.1

1.0

10.0

100.0

1,000.0

10,000.0

100,000.0

1,000,000.0

1975 1980 1985 1990 1995 2000 2005 2010 2015

Apple II

Commodore 64

PC Total

TRS 80NeXT

AmigaAtari ST

Macintosh

Nokia Symbian(phones, sold)

RIM (phones, sold)

Android(phones, sold)

iPad

iPhone

WindowsMobile

Un

its

Sh

ipp

ed

(K

, L

og

Sc

ale

)

Inflection Point:Smartphones + Tablets > PCs

Rise of Personal Computing PC and Macintosh DuopolyEra of MobileSmart Devices

Source: Strategy& research, Strategy& analysis

Technology cycles accelerate – Adoption rates explode

14

May 29, 2015

PwC

PwC

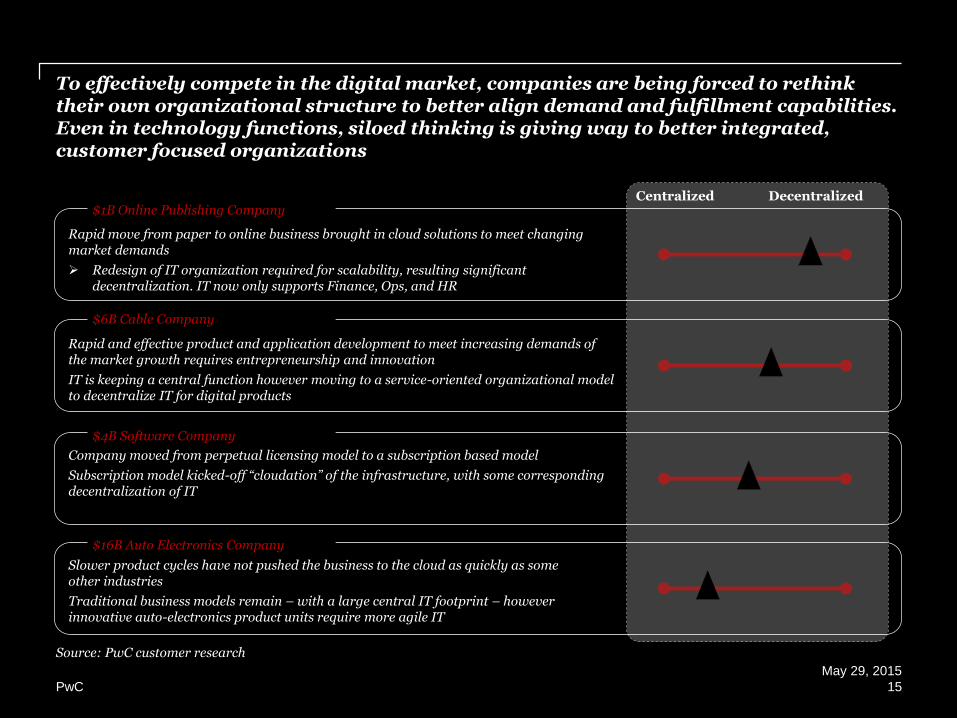

To effectively compete in the digital market, companies are being forced to rethink their own organizational structure to better align demand and fulfillment capabilities. Even in technology functions, siloed thinking is giving way to better integrated, customer focused organizations

Source: PwC customer research

Centralized Decentralized$1B Online Publishing Company

Rapid move from paper to online business brought in cloud solutions to meet changing market demands

Redesign of IT organization required for scalability, resulting significant decentralization. IT now only supports Finance, Ops, and HR

Company moved from perpetual licensing model to a subscription based model

Subscription model kicked-off “cloudation” of the infrastructure, with some corresponding decentralization of IT

Slower product cycles have not pushed the business to the cloud as quickly as some other industries

Traditional business models remain – with a large central IT footprint – however innovative auto-electronics product units require more agile IT

Rapid and effective product and application development to meet increasing demands of the market growth requires entrepreneurship and innovation

IT is keeping a central function however moving to a service-oriented organizational model to decentralize IT for digital products

$6B Cable Company

$4B Software Company

$16B Auto Electronics Company

15

May 29, 2015

PwC

PwC

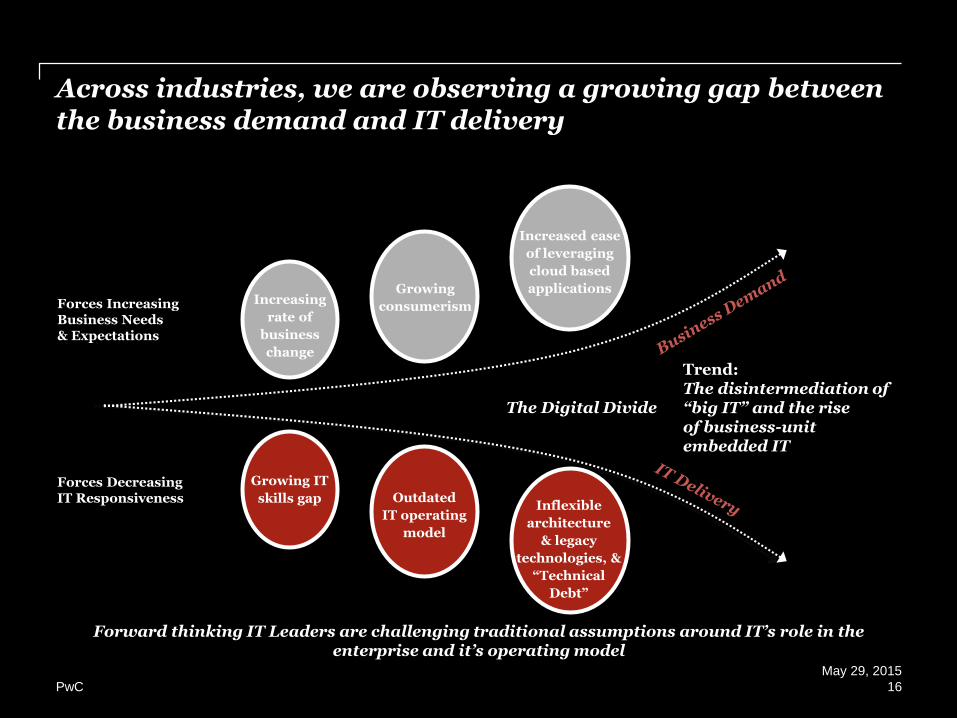

Across industries, we are observing a growing gap between the business demand and IT delivery

16

Forward thinking IT Leaders are challenging traditional assumptions around IT’s role in the enterprise and it’s operating model

Forces Decreasing IT Responsiveness

The Digital Divide

Increasing

rate of

business

change

Growing

consumerism

Increased ease

of leveraging

cloud based

applicationsForces Increasing Business Needs & Expectations

Inflexible

architecture

& legacy

technologies, &

“Technical

Debt”

Growing IT

skills gap Outdated

IT operating

model

Trend: The disintermediation of “big IT” and the rise of business-unit embedded IT

May 29, 2015

PwC

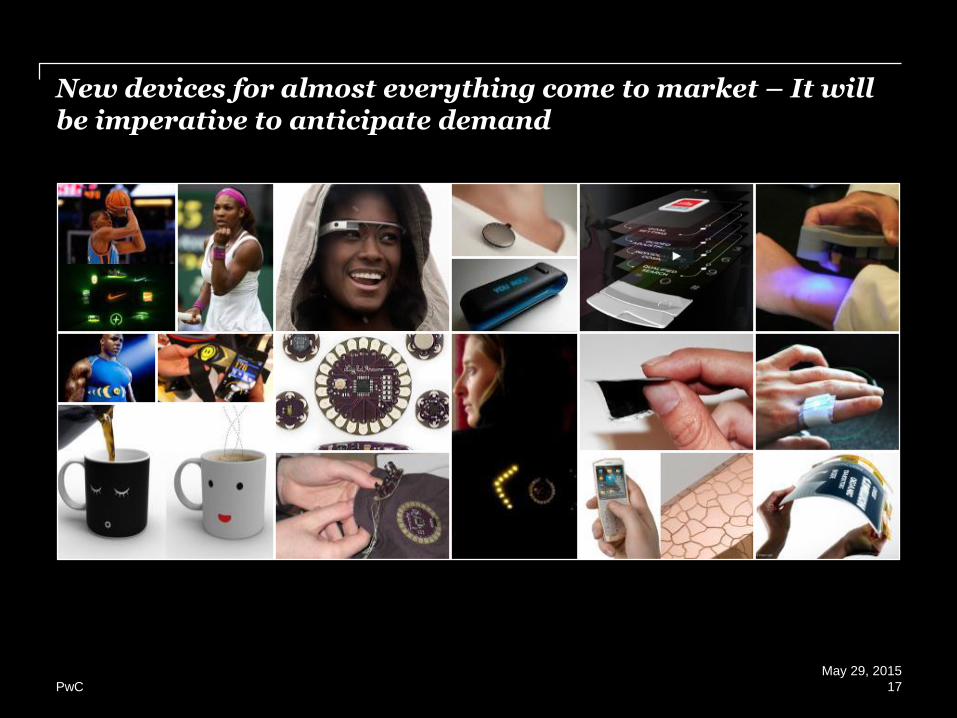

New devices for almost everything come to market – It will be imperative to anticipate demand

17

May 29, 2015

PwC

The impact of digitization on the banking industry

18

May 29, 2015

PwC

These market forces are creating both opportunities and issues in achieving

profitable revenue growth

Customer driven

economy

Customers are demanding ever higher

levels of service, pushing banking to catch up with other industries.

Growing market

The market is seeing a return to confidence with volumes

of business accelerating and most sectors predicting further growth, but competition constraining growth

RegulationRegulation is focusing on driving “better”

outcomes for customer, with increased transparency and increased choice and competition

Digital & emerging

technology

Technology is seen as an increasingly

important growth enabler with a particular focus on digital distribution

Changing demographics

Changing demographics is seeing 4

different generations in the market for the first time with different expectations and needs

Powerful forces are reshaping the future of the financial services industry and opportunity exists for those who can capitalize on it

19

May 29, 2015

PwC

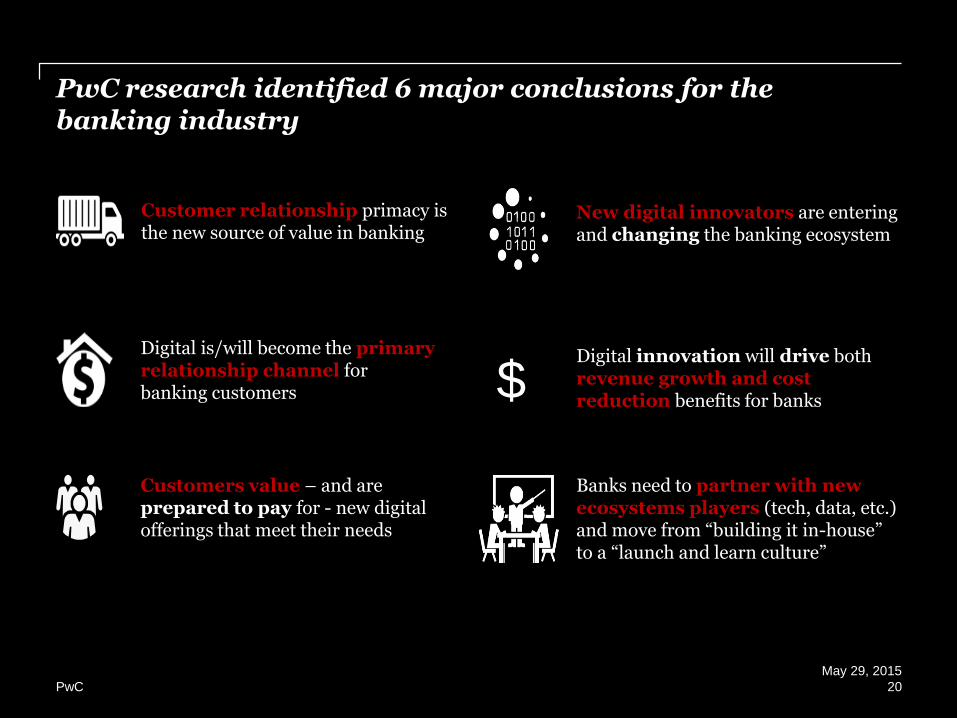

Digital innovation will drive both revenue growth and cost reduction benefits for banks$

Customer relationship primacy is the new source of value in banking

Digital is/will become the primary relationship channel for banking customers

New digital innovators are entering and changing the banking ecosystem

Customers value – and are prepared to pay for - new digital offerings that meet their needs

Banks need to partner with new ecosystems players (tech, data, etc.) and move from “building it in-house” to a “launch and learn culture”

PwC research identified 6 major conclusions for the banking industry

20

May 29, 2015

PwC

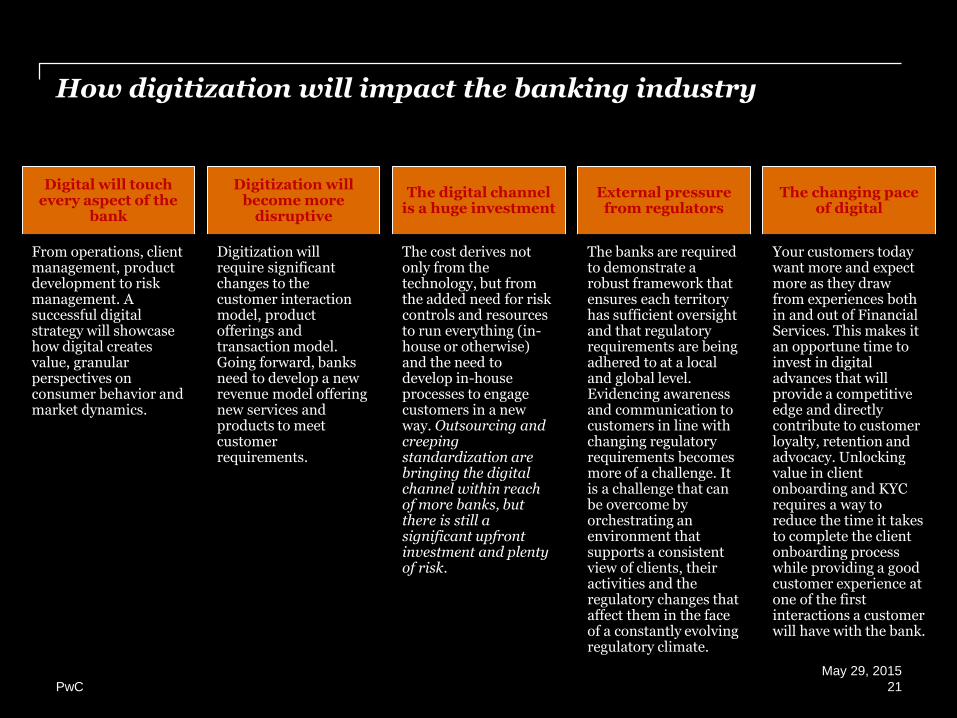

Digital will touch every aspect of the

bank

From operations, client management, product development to risk management. A successful digital strategy will showcase how digital creates value, granular perspectives on consumer behavior and market dynamics.

Digitization will become more

disruptive

Digitization will require significant changes to the customer interaction model, product offerings and transaction model. Going forward, banks need to develop a new revenue model offering new services and products to meet customer requirements.

The digital channel is a huge investment

The cost derives not only from the technology, but from the added need for risk controls and resources to run everything (in-house or otherwise) and the need to develop in-house processes to engage customers in a new way. Outsourcing and creeping standardization are bringing the digital channel within reach of more banks, but there is still a significant upfront investment and plenty of risk.

External pressure from regulators

The banks are required to demonstrate a robust framework that ensures each territory has sufficient oversight and that regulatory requirements are being adhered to at a local and global level. Evidencing awareness and communication to customers in line with changing regulatory requirements becomes more of a challenge. It is a challenge that can be overcome by orchestrating an environment that supports a consistent view of clients, their activities and the regulatory changes that affect them in the face of a constantly evolving regulatory climate.

The changing pace of digital

Your customers today want more and expect more as they draw from experiences both in and out of Financial Services. This makes it an opportune time to invest in digital advances that will provide a competitive edge and directly contribute to customer loyalty, retention and advocacy. Unlocking value in client onboarding and KYC requires a way to reduce the time it takes to complete the client onboarding process while providing a good customer experience at one of the first interactions a customer will have with the bank.

How digitization will impact the banking industry

21

May 29, 2015

PwC

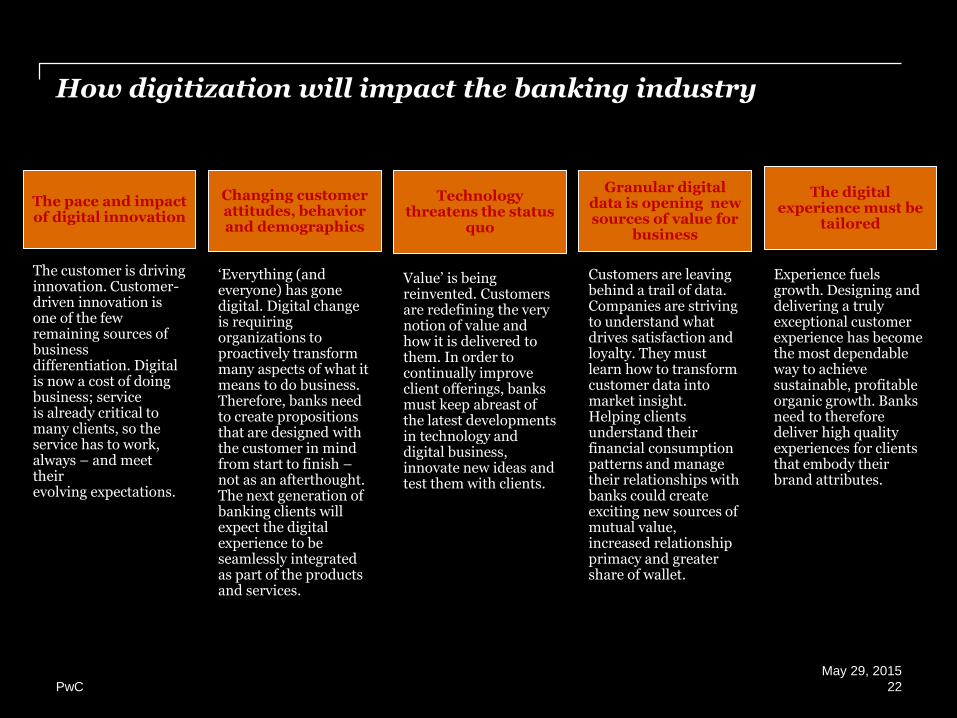

The pace and impact of digital innovation

The customer is driving innovation. Customer-driven innovation is one of the few remaining sources of business differentiation. Digital is now a cost of doing business; service is already critical to many clients, so the service has to work, always – and meet their evolving expectations.

Changing customer attitudes, behavior and demographics

‘Everything (and everyone) has gone digital. Digital change is requiring organizations to proactively transform many aspects of what it means to do business. Therefore, banks need to create propositions that are designed with the customer in mind from start to finish –not as an afterthought. The next generation of banking clients will expect the digital experience to be seamlessly integrated as part of the products and services.

Technology threatens the status

quo

Value’ is being reinvented. Customers are redefining the very notion of value and how it is delivered to them. In order to continually improve client offerings, banks must keep abreast of the latest developments in technology and digital business, innovate new ideas and test them with clients.

Granular digital data is opening new sources of value for

business

Customers are leaving behind a trail of data. Companies are striving to understand what drives satisfaction and loyalty. They must learn how to transform customer data into market insight. Helping clients understand their financial consumption patterns and manage their relationships with banks could create exciting new sources of mutual value, increased relationship primacy and greater share of wallet.

The digital experience must be

tailored

Experience fuels growth. Designing and delivering a truly exceptional customer experience has become the most dependable way to achieve sustainable, profitable organic growth. Banks need to therefore deliver high quality experiences for clients that embody their brand attributes.

How digitization will impact the banking industry

22

May 29, 2015

PwC

Digital Banking offers a better customer experience as well as allowing banks to develop a more efficient and effective operating model - enabled by digitization, optimization of technology and its underlying processes

Digital technologies increase a bank’s connectivity—not just with customers but also with employees and suppliers. This extends from online interactivity and payment solutions to mobile functionality and opportunities to boost bank brands in social media.

Digital draws on big data and advanced analytics to extend and refine decision making. Such analytics are being deployed by the most innovative banks in many areas, including sales, product design, pricing and underwriting, and the design of truly amazing customer experiences.

Creates value by enabling straight-through processing—that is, automating and digitizing a number of repetitive, low-value, and low-risk processes. Process apps, for example, boost productivity and facilitate regulatory compliance, while imaging and straight-through processing lead to paperless, more efficient work flows.

Digitization is a means of fostering innovation across products and business models. Examples of this include social marketing and crowdsourced support, as well as “digitally centered” business models.

There are several ways in which digital capabilities can create value for banks:

23

May 29, 2015

PwC

Client onboarding is a client’s first experience with a provider and has the potential to establish how the relationship will develop.

It is therefore a critical stage for a provider to engage with the client as the first interaction will set the foundations for long term loyalty and satisfaction, reduce abandonment, increase revenue, increase retention and profitability through cross selling opportunities – typically occurring during the first 90 days as a new client

Digital Client onboarding

24

May 29, 2015

PwC

A design based on the vision of front office practitioners, as well as a real understanding of client needs and what it will take to serve them and deliver the ultimate customer experience

A framework for managing client consent and other regulatory policy changes in a timely and seamless manner

A framework for managing and capturing consistent customer data

A method to capture accurate client data, by introducing self service functionality that captures data directly from the client and verifies this data using public and internal data sources with enhanced digital verification methods

Consistent client data that is used to inform other activities and processes down the line (e.g. sanctions and AML) with greater accuracy to stand up to regulatory rigour

Multichannel offering to customers reducing the time spent on manual paper forms and freeing RM’s to focus on relationships and sales

An innovative solution that ultimately serves to speed up client onboarding so clients are not left “unattended” or fall out of the onboarding experience, meaning loss of revenue and income to the bank

The value digital client onboarding will bring to the bank will be…

25

May 29, 2015

PwC

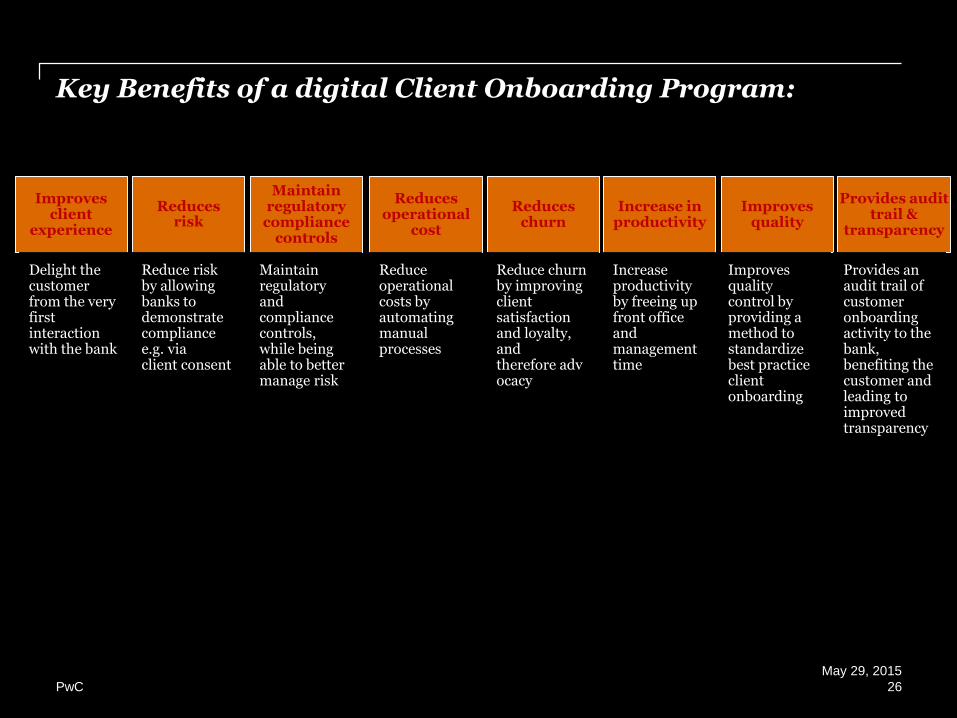

Key Benefits of a digital Client Onboarding Program:

26

May 29, 2015

PwC

Improves client

experience

Delight the customer from the very first interaction with the bank

Reduces risk

Reduce risk by allowing banks to demonstrate compliance e.g. via client consent

Maintain regulatory

compliance controls

Maintain regulatory and compliance controls, while being able to better manage risk

Reduces operational

cost

Reduce operational costs by automating manual processes

Reduces churn

Reduce churn by improving client satisfaction and loyalty, and therefore advocacy

Increase in productivity

Increase productivity by freeing up front office and management time

Improves quality

Improves quality control by providing a method to standardize best practice client onboarding

Provides audit trail &

transparency

Provides an audit trail of customer onboarding activity to the bank, benefiting the customer and leading to improved transparency

March 2015Slide 27

Q&A

27

May 29, 2015

PwC

Thank you

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United States

member firm, and may sometimes refer to the PwC network. Each member firm is a separate

legal entity. Please see www.pwc.com/structure for further details.