Embed Size (px)

Citation preview

Industry Trends

ReportBy Shahin HatamianVice President, Product Management and Strategy, Casualty Solutions Group, Mitchell

Five Qualities of an Effective Business Workflow Solution

FEATURED IN THIS ISSUE

Volume Five Number Three Q3 2016 Published by Mitchell International

Industry Trends

ReportTable of Contents

Volume Five Number Three

4 70 Years of Supporting Our Clients and Their Important Work An Interview with Alex Sun on Technology Trends

12 Quarterly FeatureFive Qualities of an Effective Business Workflow Solution

20 Bonus Features Break Down Traditional Bill Review Procedures Make a Bigger Impact on Third Party Auto Claims

28 WCS Medical Price Index

34 ACS Medical Price Index

38 Compliance Corner

42 Current Events

43 Partner Spotlight

44 About Mitchell

45 Mitchell in the News

A Message from the CEO

What’s Trending in Technology?

Welcome to the Q3 edition of the 2016 Mitchell Casualty Industry

Trends Report. As you know, we are celebrating our 70th anniversary

this year. In the last issue I shared some of my thoughts around how

the company has evolved throughout the years and where we’re

headed next. This quarter, I’m excited to share some of the current

and emerging industry trends I’m following. There are so many

interesting things happening in technology today, and it’s fascinating

to see the impact and opportunities they will bring to the insurance

industry down the road.

In this issue, we have several articles from our in-house experts that

look at additional ways organizations can approach challenges in

our industry for better business results. First up is our feature article,

Five Qualities of an Effective Workflow Solution, by Shahin Hatamian.

Shahin explains how these qualities can help companies that process

medical bills outperform their goals and differentiate themselves

from the competition. Shahin also emphasizes the need for insurers

and third party administrators to tailor workflow solutions to their

individualized business needs.

Our bonus articles this quarter include an analysis of traditional bill

review procedures and detail how specialty bill review can achieve

better results. We also discuss the current state of third party claims

and a few recommended methods to contain the associated costs.

As I finish up the second half of my interview for this issue, I’d like to

take a moment to remind you of how important you are to Mitchell.

We certainly wouldn’t be here today without you, and I’m excited

for what we can achieve together in the years ahead. Enjoy the rest

of your summer, and thank you for your continued readership of the

Industry Trends Report.

Report.

Alex Sun President and CEO Mitchell

Q3 2016

Alex Sun President and CEO, Mitchell

View the Auto Physical

Damage Edition

evolved is through the adoption of technology.

We’ve come a long way since our manuals were

printed on paper—and the current explosion

of both available and emergent technologies

promises further change and opportunity.

Mitchell was founded in Glenn Mitchell’s garage 70

years ago. The world has changed a lot since 1946,

and Mitchell has evolved right along with it. While

remaining true to our roots in collision repair, we’ve

expanded our reach into auto physical damage, auto

casualty, workers’ compensation, out-of-network

solutions, and now pharmacy. Another way we’ve

years of (m)powering better outcomes

70 Years of Supporting Our Clients and Their Important Work

Alex Sun, President and CEO

As we look toward the future, we anticipate

ongoing evolution, but here’s what will remain

the same: we’ll continue to focus on technology,

expertise and connecting to bring additional value

to our clients. We’ll also continue to support the

important work they do by focusing on empowering

better outcomes.

As part of our ongoing celebration of our 70th

anniversary, we asked President and CEO, Alex Sun,

about some of the technology and trends that are

not only changing the world we live in, but also

having an impact on both insurers and

collision repairers.

Read part II of our 70th anniversary interview.

Another way we’ve evolved is through the adoption of technology.

pilot ways to leverage these types of technologies,

marrying them with the vast amounts of data

we captured in our systems to drive either better

decisioning, or using machines to automate tasks

that may have historically been done by individuals.

And the third trend I’m seeing is the focus on the

digital consumer experience. Insurance, generally,

is a very competitive marketplace. One area where

many carriers, particularly on the personal lines side,

are beginning to focus as a point of differentiation is

on creating interesting consumer experiences. This

encompasses everything from how they quote, to

how they manage their daily interactions, to how

they handle a claim. With the ubiquity of mobile

smartphones and increased access to broadband,

we’re beginning to see clients embracing major

digital consumer initiatives.

Other things that are impacting the insurance

industry, both in favorable ways and in ways that

need to be considered as they relate to future

business models, are technologies like the Internet

of Things—whether that’s the connected car,

the self-driving car or nanotechnology related to

healthcare. These are part of a spectrum of new

technologies being deployed that will not only

affect how customers expect to be interacted with,

in terms of either buying insurance or having their

claims handled, but also how companies themselves

will operate.

What technology and trends are you following that you anticipate will have an impact on the P&C industry?

There are a number of big trends that are affecting

the entire industry. The first is a general recognition

that in order to remain competitive you need to

have the right technology infrastructure to do

so. Many insurance companies across all lines

of coverage are beginning to go through very

large scale technology transformations, starting

with either their claims systems, their policy

administration systems or their billing systems.

The intent is to create a unified, scalable and

extensible environment so they can create new

experiences and new capabilities for reaching out to

their customers and managing them.

A second major trend that is really just starting to

emerge, is we’re all beginning to recognize there is

real, tangible, practical use for things like machine

learning or artificial intelligence. We’re beginning to

Many insurance companies across all lines of coverage are beginning to go through very large scale technology transformations.

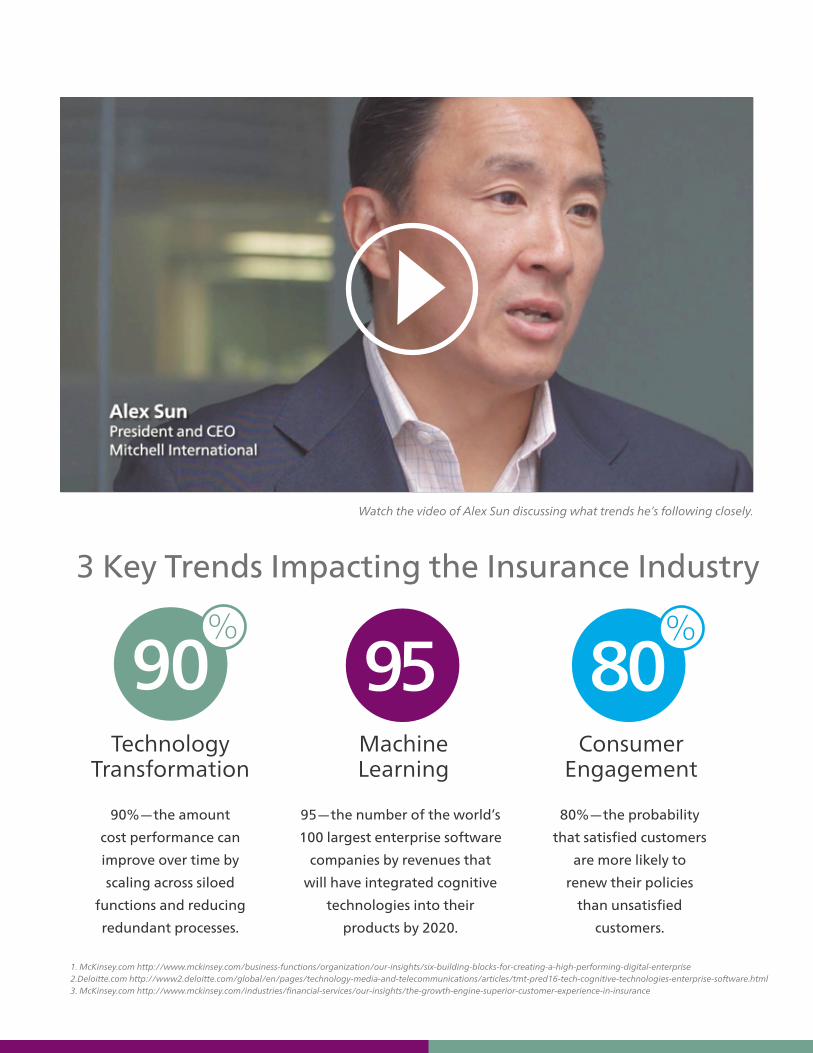

3 Key Trends Impacting the Insurance Industry

1. McKinsey.com http://www.mckinsey.com/business-functions/organization/our-insights/six-building-blocks-for-creating-a-high-performing-digital-enterprise 2. Deloitte.com http://www2.deloitte.com/global/en/pages/technology-media-and-telecommunications/articles/tmt-pred16-tech-cognitive-technologies-enterprise-software.html3. McKinsey.com http://www.mckinsey.com/industries/financial-services/our-insights/the-growth-engine-superior-customer-experience-in-insurance

Watch the video of Alex Sun discussing what trends he’s following closely.

3 Key Trends Impacting the Insurance Industry

MachineLearning

ConsumerEngagement

TechnologyTransformation

90%—the amount

cost performance can

improve over time by

scaling across siloed

functions and reducing

redundant processes.

95—the number of the world’s

100 largest enterprise software

companies by revenues that

will have integrated cognitive

technologies into their

products by 2020.

80%—the probability

that satisfied customers

are more likely to

renew their policies

than unsatisfied

customers.

90%

95 80%

1. Ducker Worldwide. (2015). Metallic Material Trends in the North American Light Vehicle. Accessed online Aug. 3, 2016.2. Ducker Worldwide. (2014). 2015 North American Light Vehicle Aluminum Content Study. Accessed online Aug. 3, 2016.

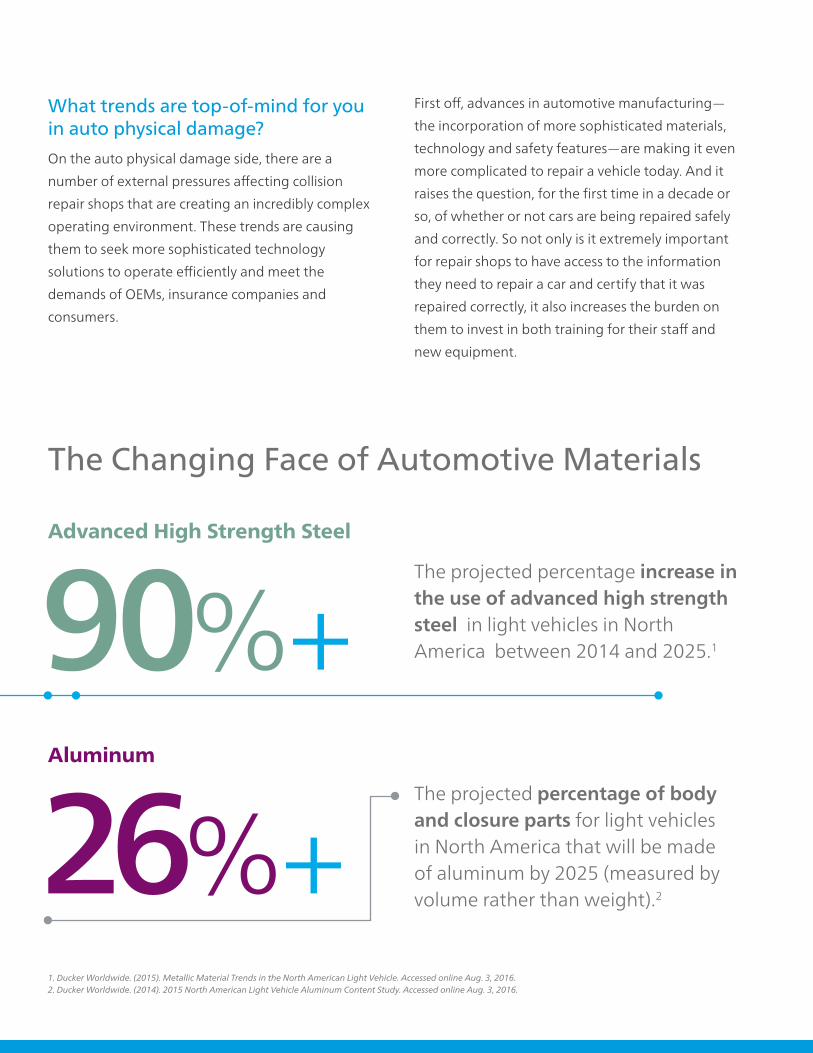

What trends are top-of-mind for you in auto physical damage?

On the auto physical damage side, there are a

number of external pressures affecting collision

repair shops that are creating an incredibly complex

operating environment. These trends are causing

them to seek more sophisticated technology

solutions to operate efficiently and meet the

demands of OEMs, insurance companies and

consumers.

First off, advances in automotive manufacturing—

the incorporation of more sophisticated materials,

technology and safety features—are making it even

more complicated to repair a vehicle today. And it

raises the question, for the first time in a decade or

so, of whether or not cars are being repaired safely

and correctly. So not only is it extremely important

for repair shops to have access to the information

they need to repair a car and certify that it was

repaired correctly, it also increases the burden on

them to invest in both training for their staff and

new equipment.

The Changing Face of Automotive Materials

90%+

26%+

Advanced High Strength Steel

Aluminum

The projected percentage of body and closure parts for light vehicles in North America that will be made of aluminum by 2025 (measured by volume rather than weight).2

The projected percentage increase in the use of advanced high strength steel in light vehicles in North America between 2014 and 2025.1

Insurance companies, for their part, are becoming

increasingly reliant on collision repair partners in

their vehicle repair programs to manage more

administrative and customer service-oriented tasks

like estimating, coordinating vehicle rentals and

ultimately, doing whatever it takes to get an owner

back into their vehicle.

In addition, many insurance companies are focused

not just on the safety and quality of a repair, but

also on the timeliness of the repair process. This

puts significant pressure on the collision repairer

to make sure they can perform their work not only

cost efficiently, but also on a timely basis, and with

regular status updates. As a result, collision repairers

are looking to leverage technology to do things like

streamline parts procurement and manage client

scheduling.

Lastly, consumers are driving another big trend

that is affecting collision repair shops—and really

operators of any small business. More consumers

are looking for outside information sources to aid

them in making decisions on what collision repair

shop to work with, and social media is increasingly

influencing this decision. I believe now more than

ever, collision repairers are going to need to be

smart about how they leverage social media and

their presence on the web in order to position

themselves for success.

Today, we’re really focused on the technologies

collision repair shops need to adopt to allow them

to operate more efficiently, especially with all the

increased demands placed on them by OEMs,

insurance companies and consumers—as well as the

changes in what is required to deliver a safe repair.

Today, we’re really focused on the technologies collision repair shops need to employ to allow them to operate more efficiently.

The Changing Face of Automotive Materials

1. ISO Fast Track data2. –4. Mitchell data

Are there any trends specific to auto casualty that you are following?

One trend that’s having a big impact on auto

casualty insurers is that both frequency and severity

continue to rise. Cost containment solutions that

address these issues are top of mind both for us and

for our clients.

On the first party side, we continue to look for

ways to adapt elements of a managed care cost

containment model to a non-managed care setting

in order to drive more efficient, accurate claims

outcomes. Whether we’re focusing on provider

networks, out-of-network discounting capabilities,

out-of-network pricing capabilities, nurse review,

or even pharmacy, we’re really taking a lot of

the concepts that have evolved in the managed

care world and adapting them for use in the auto

casualty model.

On the third party side, there’s been about a

12 percent increase in bodily injury claims costs

over the last five years. The average use of medical

services is up about 18 percent, and many injuries

are becoming more expensive to diagnose and

treat. As a result, our insurance carrier clients are

operating in an environment in which, more than

ever, they need to keep third party claims costs

in check.

At the same time, the adjuster workforce

demographics are starting to change. Many

seasoned adjusters are now reaching retirement

age, so there is a loss of expertise in an extremely

complex space. It’s becoming imperative for the

insurance industry to adopt technologies that allow

them to codify in a system the best practices of their

third party adjusters. That’s a big focus point for

us—it’s a problem we’re really working to solve.

The Rising Cost of Third Party Claims

18%

36% 15%

11%Claims costs over the last five years

Claimants with nerve or disc injuries over the last five years

Average charge per claimant with nerve or disk injuries over the last five years

Frequency of use of medical services over the last five yearsIncrease Increase

Increase Increase

For more industry insights from Alex and other Mitchell leaders, follow us on LinkedIn

and read our corporate blog.

What trends are you seeing in workers’ compensation?

The workers’ compensation market has been

dynamic for quite some time, due in part to the

recession. It’s further complicated by an equally

dynamic market on the healthcare delivery side.

The consolidation that’s taking place with health

insurers, health systems and managed care

organizations—and, of course, the implementation

of the Affordable Care Act—are all contributing

factors. Despite a small decline in the volume of

claims, we’re continuing to see rising medical

care costs.

Another trend that is contributing to this dynamic

environment is the dramatic rise in opioid abuse.

In fact, there were a record number of drug-

related deaths in 2014, and 61% of these were

caused by opioids. This prompted the CDC to

issue new prescribing guidelines earlier this

year. Many states and organizations such as

the Work Loss Data Institute that publishes the

Official Disability Guidelines are also tightening

their recommendations to keep patients safe

and curb the threat of addiction. Because of

these factors, we’re seeing an increased focus on

pharmacy benefit management as a way to more

appropriately manage the distribution of opioids

and to keep claimants safe and on the road to

recovery.

As a result of these trends, it’s become even more

important for our workers’ compensation clients

to focus on enabling technologies that allow them

to operate their organizations more effectively

and efficiently. Our clients are looking to use

technology to more tightly integrate with the

other service providers and partners they interact

with throughout the claims resolution process.

They’re also looking for ways to leverage data that

is captured in the use of these technologies, in a

way that gives them greater insight into cost drivers

and helps them deliver better outcomes for their

organizations and their claimants.

It’s become even more important for our workers’ compensation clients to focus on enabling technologies that allow them to operate their organizations more effectively and efficiently.

1212

Five Qualities of an Effective Business Workflow Solution

No two payors are the same, so their business

workflow solutions shouldn’t be identical either.

Every insurer or third party administrator knows

their business best and needs a workflow solution

which adapts itself to their unique business priorities

and rules. Now learn the five qualities that make a

business workflow work for your business.

1) Customizable and FlexibleWhyIt’s important for companies to be able to optimize

their workflow to their own specific requirements

since every business has different needs. Businesses

shouldn’t be limited to a “one size fits all” model. A

workflow, or a set of business processes that work

together, should be customizable so each business

can create a process order that works best for them.

For example, each company should be able to

decide at which point in the workflow business rules

should be triggered, when bills should be routed for

nurse review and adjuster authorization and when

to pend and transmit bills for preferred provider

organization repricing. Insurers, TPAs and managed

care companies shouldn’t be limited to one static,

pre-defined process that mandates one process -

bills go through bill review, then trigger rules, then

go to the PPO network. Decision makers need to

have complete control over what happens to a bill

after it gets imported into the system.

Quarterly Feature

Decision makers need to have complete control over what happens to a bill after it gets imported into the system.

By Shahin Hatamian Vice President, Product Management and Strategy, Casualty Solutions Group, Mitchell

13 Quarterly Feature

HowIn combination with the workflow solution, the

rules engine should allow for complete flexibility

in creating business rules in order to get the best

outcomes. The rules engine should be separate from

the application logic, giving more control to the

business user. The engine should be robust enough

to allow the user to modify rules as the user requires.

This ensures the workflow more closely aligns with

the company’s internal guidelines and goals.

A large part of having a customizable workflow

solution is being able to update it quickly and easily.

This includes being able to update business rules

within the rules engine in an efficient manner. A

rules engine is not as valuable if a company has to

contact an external vendor to request rule changes

every time it needs a rule modification. This type of

approach may take weeks and can be an expensive

process.

To help solve this problem, the rules engine must

be easy enough to setup, learn and use so that an

employee without a development background

could master the knowledge required to make and

edit rules with minimal training. If payors are able to

customize the workflow process to their needs, they

are better equipped to develop new ways to ensure

cost containment and improve efficiency.

ExampleInsurance Company A and Insurance Company B are

setting up their business workflows. In particular,

they are interested in making sure that their team

reviews all high-dollar inpatient hospital bills. It’s

also important to them that in their workflow

process, utilization review recommendations are

applied before the bill goes through the review

process. However, Insurance Company B may have

no downstream reporting requirements and may

set up their business workflow to have upfront

adjuster oversight since the bill may be denied and

will give their resources more time to process clean

bill edits. Both companies have their own specific

needs, but Company A and Company B should be

able to select a workflow process and rules engine

solution which is flexible enough to meet their

different business needs. If they are both able to

customize their workflow and write rules specific to

their needs, both companies are closer to meeting

their own business goals.

A large part of having a customizable workflow solution is being able to update it quickly and easily.

14 Quarterly Feature

BenefitsUsing a fully-customized workflow solution sets

customers up to produce the best outcomes and

gain an edge on the competition in the process.

By choosing a scalable and customizable workflow,

a company has a greater opportunity to take the

subject matter expertise of their best employees and

efficiently scale it across the business. If a company

can create rules that are tailored exactly to its

needs, they can see huge benefits in return. Expert

bill review employees can focus on adjudicating

more complex bills. Flexible and customizable

workflow and rules engine solutions enable insurers

and TPAs to have more control over the business,

reduce operational costs, write rules that align

with company objectives and improve employee

productivity.

2) Facilitates AutomationWhyWith the right automated process, adjusters don’t

need to review each and every bill. A workflow

that uses a rules engine can determine which bills

require an adjuster’s oversight and which bills can

be automatically adjudicated. When a rules engine

enables the setup of auto-adjudication within a

workflow, it allows the adjusters to focus only on

those bills that require an expert decision.

HowIdeal Automation RateAn efficient workflow usually passes through 60-70

percent of bills automatically. Though each business

might shoot for a different rate of automation, a

rules engine should allow them to reach this level of

efficiency if they choose.

A reliable workflow combined with an intelligent

rules engine creates a more effective way of

performing the bill review process. For example, by

establishing rules based on thresholds, treatment

codes or document type, bills can be presented to

adjusters only when their oversight is necessary. A

strong workflow should include business rules that

look for exceptions in the data.

This capability helps automate tasks that normally

required manual processing, and allow the

routing of bills to their required destination. Such

a combination of reliable workflow and a robust

rules engine can run items through the bill review

process faster, and more efficiently than a traditional

bill review product. It also can help minimize the

variances in adjudication decisions that may arise

from different skills and experiences.

ExampleIn order to maximize adjuster efficiency, Insurance

Company A doesn’t want employees spending any

time on bills that are under $50 or bills that include

physical therapy sessions.

The rules engine Insurance Company A uses should

let them specify these needs and let the identified

bills pass through without any human intervention.

So when a bill goes through the system for $40, no

employee time will be spent approving the payment.

Insurance Company A’s adjusters will then have

more time to focus on bills that do require their

oversight and can give more attention to claims that

need further negotiation and investigation.

By using a robust workflow and a rules engine that

gives Insurance Company A complete control to

decide which bills can be automated through the

system and which need to stop, the payor is able to

improve efficiency.

15

About the Quarterly Feature author…

By Shahin Hatamian, Vice President, Product Management and Strategy, Casualty Solutions Group, Mitchell

Shahin Hatamian leads the

Product Management group

and is responsible for product

direction, marketing, partnerships

and strategic initiatives for

Mitchell Auto Casualty and

Workers’ Compensation Solutions.

With over 20 years of high-tech

industry experience, Shahin has an

extensive and proven knowledge

of Product Development,

Marketing,Organizational

Leadership, Business Strategy,

Partnerships and Global Business.

Shahin holds an MSEE and an

MBA.

BenefitsAside from automating bills adjusters don’t need

to work on, an effective workflow/rules engine

combination drives down turnaround time.

Efficiency will increase, leaving adjusters more time

to focus on their core responsibilities.

Another benefit of process automation is that

it helps the payor stay compliant with timeline-

related service level agreements in order to submit

payments on time.

By making on-time payments, the payor can avoid

late-penalties in some states. A rules engine aids

in cost containment by checking that providers are

billing correctly and helping payors decide what the

correct amount is to pay on each bill.

3) Manages Multiple WorkflowsWhy

A good workflow model should make a complex

process easy. TPAs work in a complicated

environment because they manage multiple unique

businesses that have different requirements and

goals. It can get complicated to operate separate

workflows for each of their clients. As a result,

sometimes TPAs can only offer a single business

workflow process across all of their clients, meaning

each organization cannot set its own guidelines.

How

TPAs should have a simple way to organize

workflows and rule sets separately for each

customer. This way, it’s easy for each TPA to

ensure they are applying the right business rules

and sending medical bills to the right destination

for each customer. Without an efficient way to

customize and manage multiple workflows and

multiple sets of rules, TPAs may lose out to more

sophisticated competitors.

Quarterly Feature

16 Quarterly Feature

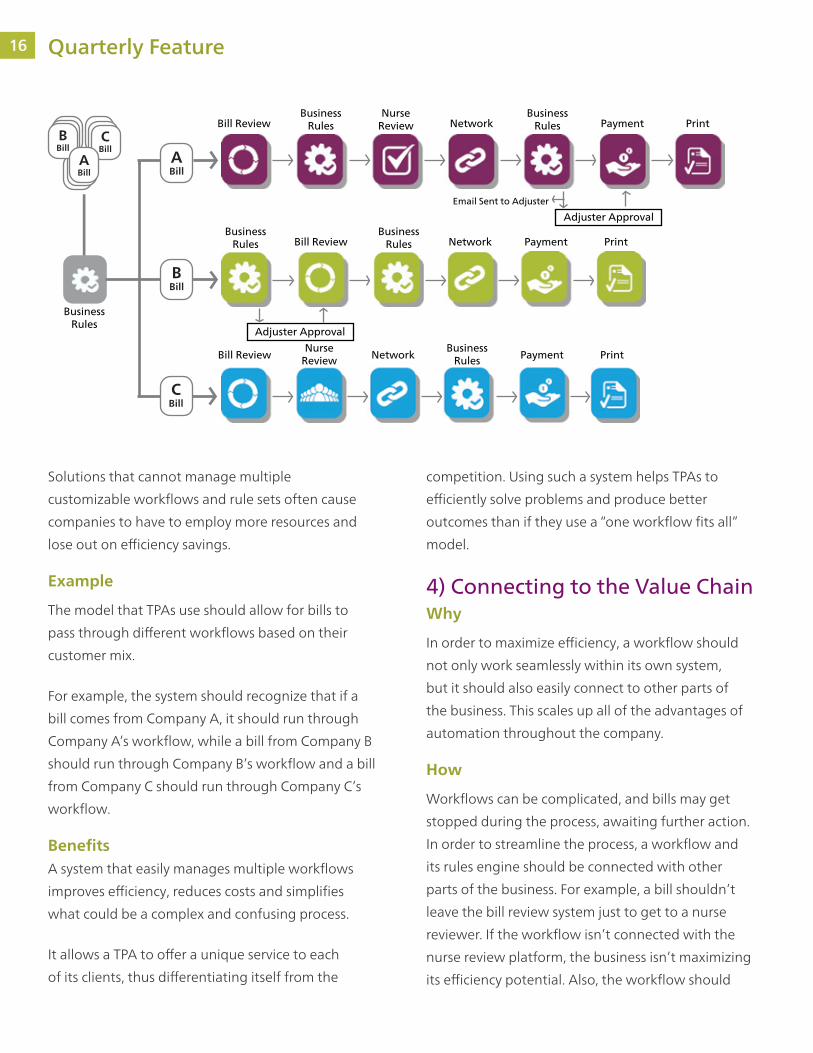

Solutions that cannot manage multiple

customizable workflows and rule sets often cause

companies to have to employ more resources and

lose out on efficiency savings.

Example

The model that TPAs use should allow for bills to

pass through different workflows based on their

customer mix.

For example, the system should recognize that if a

bill comes from Company A, it should run through

Company A’s workflow, while a bill from Company B

should run through Company B’s workflow and a bill

from Company C should run through Company C’s

workflow.

BenefitsA system that easily manages multiple workflows

improves efficiency, reduces costs and simplifies

what could be a complex and confusing process.

It allows a TPA to offer a unique service to each

of its clients, thus differentiating itself from the

competition. Using such a system helps TPAs to

efficiently solve problems and produce better

outcomes than if they use a “one workflow fits all”

model.

4) Connecting to the Value ChainWhy

In order to maximize efficiency, a workflow should

not only work seamlessly within its own system,

but it should also easily connect to other parts of

the business. This scales up all of the advantages of

automation throughout the company.

How

Workflows can be complicated, and bills may get

stopped during the process, awaiting further action.

In order to streamline the process, a workflow and

its rules engine should be connected with other

parts of the business. For example, a bill shouldn’t

leave the bill review system just to get to a nurse

reviewer. If the workflow isn’t connected with the

nurse review platform, the business isn’t maximizing

its efficiency potential. Also, the workflow should

ABill

ABill

CBill

BBill

BBill

CBill

Bill Review

Bill Review

Bill Review Payment Print

Email Sent to Adjuster

NetworkNurse

Review

NurseReview

Network

Network

Payment

Payment

BusinessRules

BusinessRules

BusinessRules

BusinessRules

BusinessRules

BusinessRules

Adjuster Approval

Adjuster Approval

17

be connected to an alerting system for people

who work on bills. An adjuster or nurse reviewer

shouldn’t be required to constantly check the system

to see if there are bills that require attention and/or

further action. Employees’ time can be utilized more

efficiently when the workflow is set up to alert when

it sends a bill out for review.

Example

Insurance Company A always wants to keep an eye

on any closed claims that are being reopened. In

order to keep those costs under control, it requires

that either Joe or Mary look at any new bills that

come through the system that are related to a claim

that has already been closed. Both Joe and Mary are

very busy, and they don’t have time to continuously

check the system to see if there are bills to review.

If Insurance Company A has a workflow and a

rules engine that are connected externally, this

won’t be a problem. It will be able to create a

rule that says: “If a bill is related to a closed

claim, email [email protected]

and [email protected] for review.”

Now, Joe and Mary are able to spend less time

manually checking the system and more time

working on their other duties.

Insurance Company B frequently uses nurse

reviewers, but has noticed that often, nurses’

recommendations aren’t being applied during the

bill review process. Insurance Company B uses a

homegrown workflow system. It’s losing money

on every bill since nurse recommendations are

not being applied, all the while the company is

still paying for the nurses’ time. Once they realized

the problem, Insurance Company B switched to a

workflow solution that integrates with their nurse

review platform. Now, the nurses’ suggestions are

automatically applied to every bill when it goes

through the company workflow. By switching over

to the robust, enterprise-grade solution, Insurance

Company B is taking better control of its medical

spend and improving efficiency within the nurse

review and bill review process.

BenefitsBy integrating the rules engine with other

departments and parts of the business, bills get

processed more efficiently. It keeps everything in

one place, making it quicker and easier for a medical

bill to be sent through the system. This ultimately

keeps costs low and saves employees time. Also,

when a workflow is capable of alerting an employee

that a bill is awaiting his or her review, it benefits

the company in two ways. First, it allows employees

who audit bills as a small part of their job to focus on

other tasks when there isn’t work waiting in his or

her queue.

If they know they’ll be alerted every time a bill

requires their attention, then they don’t have to

worry about constantly checking in. Second, alerting

the employees involved in the workflow speeds up

turnaround time and minimizes the chance of a bill

pending for an employee to route it to the next step.

Connecting the different steps within a workflow

with other parts of the company business is an

important part in running a productive business.

An adjuster or nurse reviewer shouldn’t be required to constantly check the system to see if there are bills that require attention and/or further action.

Quarterly Feature

18 Quarterly Feature

5) Powerful & Always ImprovingWhy

A powerful workflow is one that can help

companies learn and evolve over time to help

improve business outcomes. The workflow and

rules engine should be powerful enough to meet

just about any business need a company could

have. The workflow shouldn’t be restrictive, but

instead, it should empower a business to improve its

efficiencies and processes. The rules engine should

automate the routing, assignment and tracking of

work tasks. It should allow payors to create various

types of rules, such as decisioning rules, declarative

rules that compute values, transformation rules

that map and parse data and integration rules that

determine the correct system connection to make in

each circumstance.

How

One factor that makes workflow modelers and rules

engines powerful is the business value it generates

for customers. A commercial-grade rules engine

or workflow that’s processed hundreds of millions

of transactions over its lifetime can provide a lot

of value to a business and is an ideal candidate for

payors selecting workflow solutions. An important

way a rules engine can continue to add value to

a business is by giving decision makers workflow

process suggestions and rule modifications that

they can use to improve their business outcomes.

It should also be easy to measure the power of a

workflow. The financial and operational benefits

of a customized workflow and rules engine should

be easily determinable. For example, if a bill was

reduced by a fee schedule ground rule, a user and

a custom business rule, all three savings categories

should be available for impact analysis. The ability

to run this type of analysis is also important in

evaluating the financial and operational benefits

that a rules engine can provide. Workflows and

rules should be able to evolve over time to continue

improving financial and operational benefits.

Example

A powerful, mature, dependable and smart

workflow allows payors to use it with confidence.

Companies should be able to easily customize the

workflow to flag bills an employee needs to review

and alternatively, pass through bills the company

decides adjusters don’t need to see. A commercial-

Business Rules Business Rules Business Rules

Business Rules

Business RulesAdjuster Approval

Adjuster Approval

Finalize

Finalize

Payments

Payments

Finalize

FeeSchedule

FeeSchedule

FeeSchedule

Networks

Networks

ExternalRules

Auto Adjudication

Impact Analysis

Turn Around Time

Automated Savings Rate

75%

1.9 Days

55%

19

grade rules engine gives companies an unlimited

amount of opportunities to make specific business

decisions resulting in improved efficiency and better

business outcomes and providing both financial and

operational benefits.

Benefits

A powerful, mature, dependable and smart

workflow allows insurers to use it without worries.

Companies should be able to easily customize

the workflow to flag bills an employee needs to

review and pass through bills the company has

decided adjusters don’t need to see. A commercial-

grade rules engine gives companies an unlimited

amount of opportunities to make specific business

decisions resulting in improved efficiency and better

business outcomes and provides both financial and

operational benefits.

SummaryWith today’s continuous goal of achieving cost and

quality effectiveness, the flexible and customizable

rules engine has become an integral part of

an efficient business workflow system. When

a workflow is powerful and flexible enough to

adapt to any business need, it can automatically

produce better outcomes and can help companies

that process medical bills outperform their distinct

business goals while differentiating themselves from

their competition.

Quarterly Feature

2020

Payors often fall into a pattern of sending their

workers’ compensation medical bills through

the same process they always have, and are

consequently getting the same results they’ve

always gotten.

Now, a few payors are catching on to a new,

innovative trend of switching up their cost

containment methods to achieve better results—

using specialty bill review (SBR) before traditional

networks in their bill review process. Many times,

network discounts aren’t robust, meaning that by

only sending medical bills through the traditional

network route, some payors are overpaying on

medical bills. SBR is already the highest yielding

solution applied to a medical bill set. By positioning

it in different places in the workflow stack and not

confining themselves to one traditional bill review

order, payors are seeing even better results through

improved savings, specifically on facility bills.

What is Specialty Bill Review?SBR is a service that helps provide additional cost

containment above and beyond the traditional

bill review method. As a differentiated “specialty”

solution, SBR identifies and corrects issues not

captured by traditional bill review systems,

like coding errors, bundling redundancies and

misapplied policies, using repricing algorithms

By Greg Gaughan Vice President and General Manager, Out of Network Solutions, Mitchell Casualty Solutions Group

By Joshua Dickerson Director of Product Management, Out of Network Solutions, Mitchell Casualty Solutions Group

Break Down Traditional Bill Review Procedures

Bonus Feature

Positioning SBR higher in the stack is easy to do if your bill review engine allows for flexibility and customization and doesn’t require one specific workflow.

21 Bonus Feature

After the review process, the CVA service reduces

invalid and inappropriate charges to help ensure

payors are only paying for necessary charges on a

medical bill.

After review, an SBR service should recommend a

payment at a rate that’s about 35 percent of the

original bill charge, on average. Once the payor then

offers the payment to the provider, the SBR vendor

should manage and resolve any issues that arise on

the payor’s behalf.

and methodologies based on historical negotiation

data and state standards for payment. Payors

traditionally use SBR to calculate a fair and

reasonable price on medical bills when they don’t

already have an agreement with the provider.

Two different components make up SBR services –

market value pricing (MVP) and charge validation

analysis (CVA). Market Value Pricing is the service

that’s most commonly used by payors who use SBR.

The MVP service analyzes bills line-by-line in an

effort to determine a fair value for medical services

performed, since many times, items such as implants,

devices or drugs don’t reflect the appropriate

pricing. By using rules-based technology based on

jurisdictional case law and legal benchmarks for

charge limitations combined with technology that

searches and analyzes different aspects like accepted

payment comparisons, the MVP service is able to

determine the fairest price on medical bills.

Payors typically use CVA, the other component of

SBR, to help catch invalid charges. The CVA service

uses automated evaluation technology to identify

inappropriate charges through an intensive review

for line item and coding accuracy. During the

review, CVA looks for errors like charges for items

and services that weren’t provided, charges that

are undocumented or unrelated, and treatment for

injuries or illness caused by the facility or provider.

After the review process, the CVA service reduces invalid and inappropriate charges to help ensure payors are only paying for necessary charges on a medical bill.

22 Bonus Feature

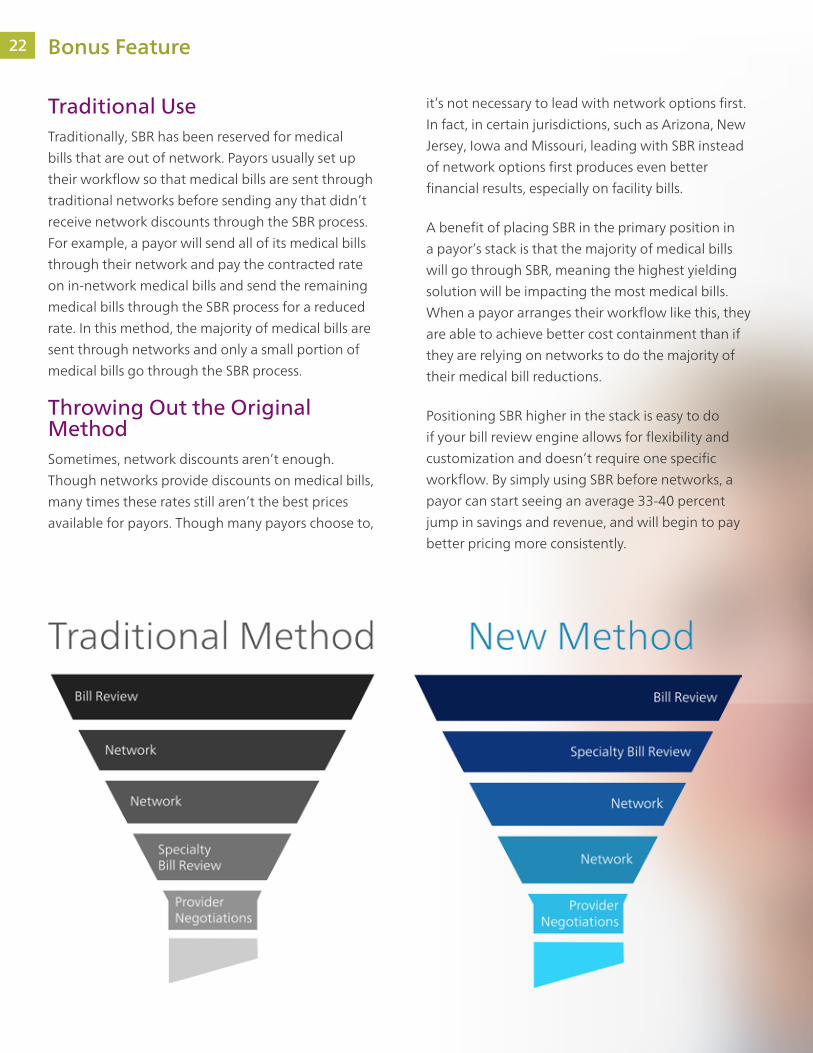

Traditional UseTraditionally, SBR has been reserved for medical

bills that are out of network. Payors usually set up

their workflow so that medical bills are sent through

traditional networks before sending any that didn’t

receive network discounts through the SBR process.

For example, a payor will send all of its medical bills

through their network and pay the contracted rate

on in-network medical bills and send the remaining

medical bills through the SBR process for a reduced

rate. In this method, the majority of medical bills are

sent through networks and only a small portion of

medical bills go through the SBR process.

Throwing Out the Original MethodSometimes, network discounts aren’t enough.

Though networks provide discounts on medical bills,

many times these rates still aren’t the best prices

available for payors. Though many payors choose to,

it’s not necessary to lead with network options first.

In fact, in certain jurisdictions, such as Arizona, New

Jersey, Iowa and Missouri, leading with SBR instead

of network options first produces even better

financial results, especially on facility bills.

A benefit of placing SBR in the primary position in

a payor’s stack is that the majority of medical bills

will go through SBR, meaning the highest yielding

solution will be impacting the most medical bills.

When a payor arranges their workflow like this, they

are able to achieve better cost containment than if

they are relying on networks to do the majority of

their medical bill reductions.

Positioning SBR higher in the stack is easy to do

if your bill review engine allows for flexibility and

customization and doesn’t require one specific

workflow. By simply using SBR before networks, a

payor can start seeing an average 33-40 percent

jump in savings and revenue, and will begin to pay

better pricing more consistently.

23 Bonus Feature

2424

In just one year, the average bodily injury claim cost

has risen about 4 percent, from $13,719 in 2014

to $14,280 in 20151. As medical costs increase,

claims costs increase as well. Since there aren’t fee

schedules applicable to third party injury claims, or

access to traditional Preferred Provider Organization

networks, payors need to look for other

opportunities to help contain these rising costs. As

bodily injury severity and utilization continue to

rise, many insurance companies are using a suite

of solutions including a few key cost containment

methods outside of traditional bill review to reach

the fairest price in the settlement of third party

claims.

What’s Happening in Third Party? Third party claim costs have been rising for quite

some time. From 2011 to 2015, bodily injury severity

rates have increased about 12 percent1. In addition,

we have seen utilization increase about 18 percent2.

These increases are due to several factors, including

rising medical costs, a higher frequency of surgeries

to treat injuries and more expensive diagnosis

procedures. These medical trends are having a direct

impact on third party claim costs.

The best way for payors to combat rising costs

across the third party auto casualty market is to

use a variety of cost containment services on both

represented and unrepresented claims. In addition

to bill review and demand package review services,

many companies would also benefit from using

nurse review and direct-to-provider negotiations as

a part of their third party solution suite.

Make a Bigger Impact on Third Party Auto Claims

Bonus Feature

By Norman Tyrrell Director, Product Management, Mitchell Casualty Solutions Group

By Jackie Payne Vice President, Medical Management Services, Casualty Solutions Group

The best way for payors to combat rising costs across the third party auto casualty market is to use a variety of cost containment services on both represented and unrepresented claims.

25

Direct-to-Provider NegotiationsNegotiating isn’t just for attorneys and adjusters. In

the third party auto market, insurance companies

should also be contacting a partner to negotiate

directly with providers on unrepresented claims

on their behalf. Many insurance companies don’t

use any cost containment methods on these

unrepresented claims, instead choosing to focus

their employee’s time on negotiating demand

packages for represented claims. Negotiation

services are an easy-to-use solution that won’t

add too much time to the third party workflow or

take up valuable adjuster time. By using provider

negotiation services with a prompt-pay model,

payors can often start to see benefits like reductions

compared to what they are currently paying, as

well as increased consistency throughout the

organization’s payments.

Companies that aren’t negotiating third party

medical bills are often paying providers on

unrepresented claims in full, since they don’t have

a strong cost containment methodology that they

use for these claims. By simply using a negotiation

service just like they would for first party auto or

workers’ compensation claims, companies can start

to quickly and easily see major improvements on

third party payments with minimal internal effort.

While many companies that do use direct-to-

provider negotiations keep their negotiations in

house, choosing to use a strategic partner is often

the most efficient and fruitful option. A partner is set

up to negotiate more accurately and efficiently than

adjusters can, since they are equipped with the right

tools and expertise. The strategic partner should

be using a combination of a proprietary platform,

expert negotiators and data from nearly every

provider in the country. If a negotiation service is set

up this way, it’s much more efficient than in-house

negotiations, and often produces much better

financial results. In addition, a partner can help free

up time for adjusters so they can focus on core tasks

instead of spending time calling providers. When

executed correctly, a strategic partner can often

secure an average price reduction of 20-50 percent

on each bill.

Negotiation services are a cost-efficient way to

manage rising third party claims costs in all 50

states. Typically, there is no investment required to

turn on the service, and insurance companies only

have to pay once they start receiving discounts. A

negotiation service is a low-cost way to improve

third party claim outcomes while streamlining an

insurance company’s operational workflows.

Negotiation services are a cost-efficient way to manage rising third party claims costs in all 50 states.

1. “Private Passenger Auto Loss Data and Trends, Multi-state.” Fast Track Plus™. 2016.2. Mitchell Data

Bonus Feature

26 Bonus Feature

Nurse ReviewAnother area for increased impact in third party

auto claims is the use of professional medical review

services. A nurse review service provides adjusters

with invaluable information to help them negotiate

successfully with plaintiff attorneys, which saves

insurance companies from overpaying on medical

specials. With bodily injury severity on the rise over

the past couple of years, many insurance companies

are turning to nurse review to help combat these

higher prices and overutilization of medical services.

Nurse review is most valuable when the service

employs registered nurses who are familiar with

trauma care and do a complete deep-dive review

of the claimant’s current medical record. A nurse

should personally look closely at all of the details of

the claim and medical records instead of just doing

a cursory review of the billing or using algorithms to

do the job for them. When the nurse review services

conduct their review in this manner, nurses are able

to pull out the most important information in the

medical record and the claim file and point to any

discrepancies in the type and course of treatment,

which can be used as negotiation points. When

discrepancies are noted, detailed negotiation points

can assist adjusters and defense attorneys with

settling the claim for significantly lower amounts.

Another key benefit to using professional nurse

review is that the review and negotiation points are

clear, concise and in a format that helps facilitate

negotiations. By receiving recommendations in

an easy-to-understand layperson’s explanation,

adjusters at all experience levels are able to not only

understand the situation, but also explain and rebut

key points with a plaintiff attorney more effectively.

The document should contain an overview of the

chronology of medical treatment starting with the

mechanism of injury and continuing through all

phases of treatment. The report should provide

detailed rationale to support their recommendations

making sure adjusters are prepared for the

sometimes difficult negotiation process. Along

with an easy-to-read format, a nurse review service

should also provide some training around how to

use a nurse review report to its maximum potential

and also include information around how to contact

the nurse reviewer with any questions that may

arise.

When a nurse review is executed correctly, it can

help insurance companies achieve significant cost

containment on third party claims. In fact, some

companies using nurse review have avoided paying

hundreds of thousands of dollars for treatments

that are completely unrelated to auto accidents.

Here’s one example: After a minor fender-bender,

a claimant had symptoms of chest pain that led to

a very costly workup and ultimately, open heart

surgery. The hospital bill alone was almost $200,000.

After a minor fender-bender, a claimant had symptoms of chest pain that led to a very costly workup and ultimately, open heart surgery. The hospital bill alone was almost $200,000.

27

Though the plaintiff attorney argued that the

claimant’s heart issues were a result of the accident,

the nurse who reviewed the case on behalf of

the insurance carrier found many details of the

claimant’s history that showed the conditions were

long-standing and pre-existing. The adjuster was

able to negotiate successfully that the condition was

unrelated to the auto claim, and eventually it was

determined that the insurance carrier would not

be responsible for paying for any of the treatments,

saving them from unnecessary payments.

By adding robust negotiation and nurse review

services into their third party solution suite,

insurance companies will be able to control costs on

both represented and unrepresented claims. These

services will not only improve adjuster efficiencies,

but will also better ensure that companies are

consistently paying the fairest price on third party

claims and result in improved financial results.

Bonus Feature

2828

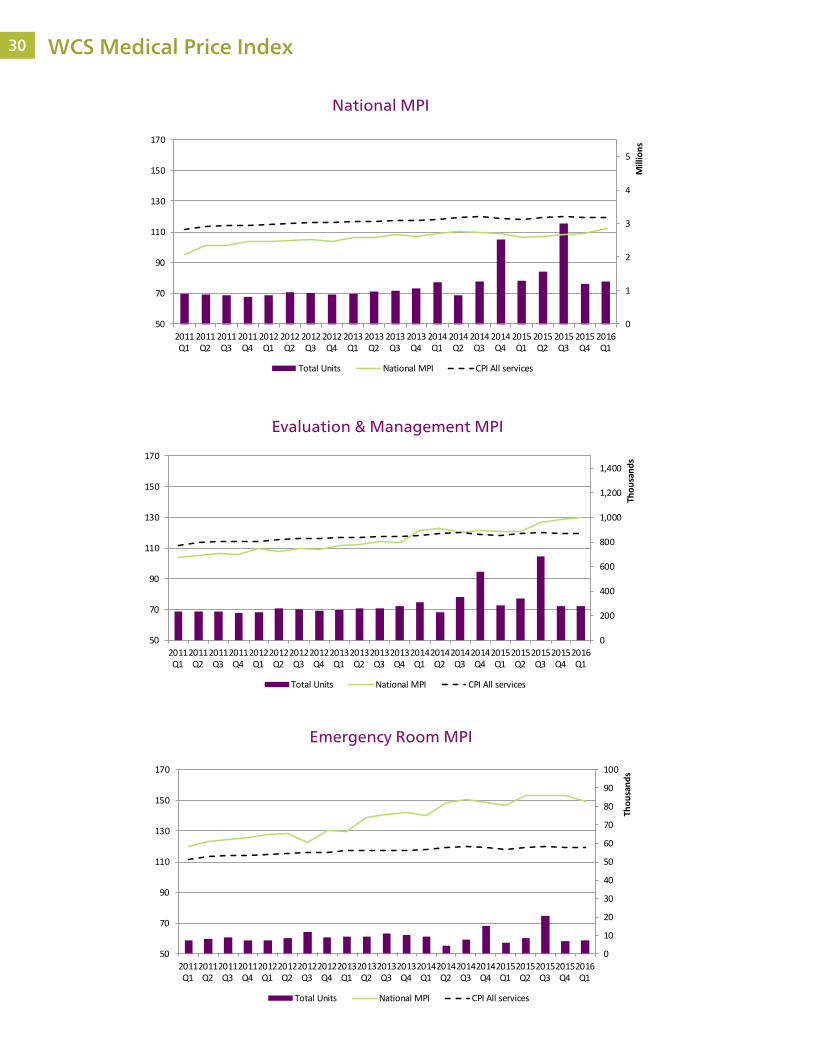

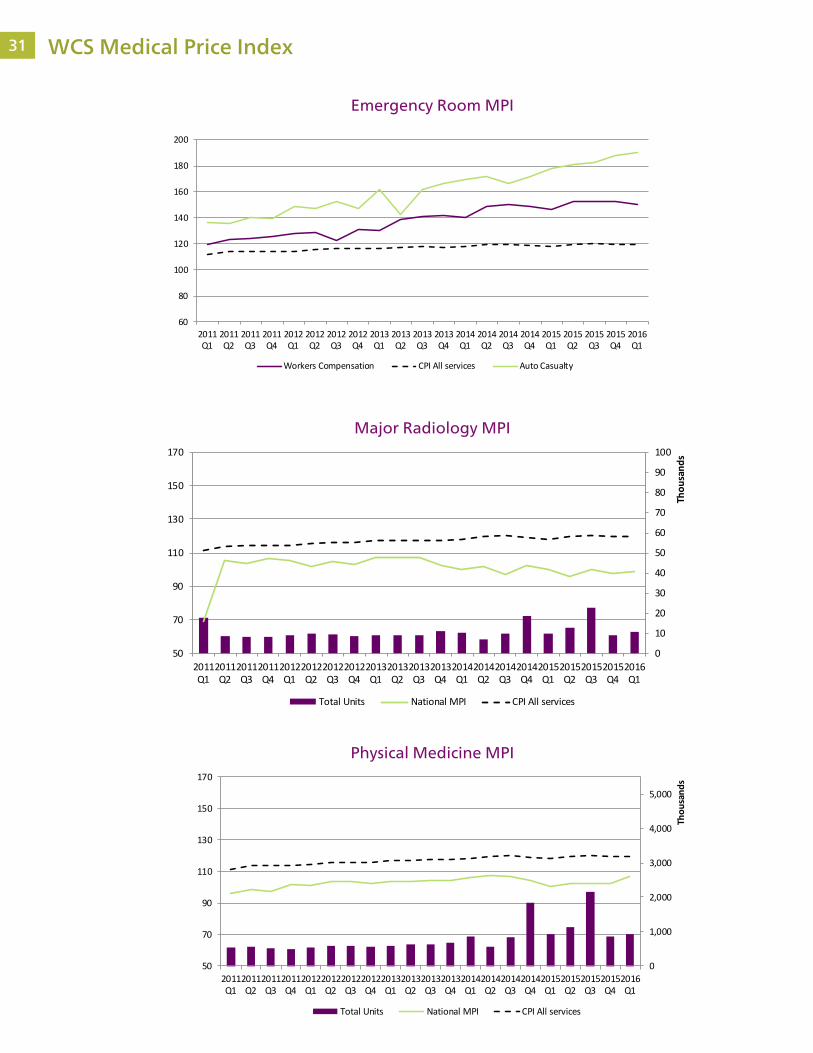

The National CPI for All Services, as reported by the

Bureau of Labor Statistics, is presently 119.33 which

is down 0.11 percent in Q1 2016 since Q4 2015.

For the same period of time, Q4 2015 to Q1 2016,

the National Workers’ Compensation Medical Price

Index increased by 3.16 percent and presently sits

at 112.21. Since Q1 2006, the National Workers’

Compensation MPI has increased 12.21 percent

while the National CPI for All Services increased

19.33 percent.

• Charges associated with physical medicine

services experienced a 3.8 percent increase since

Q4 2015. This increase brings the total unit cost

change for physical medicine since Q1 2006 to

6.62 percent, significantly below the National CPI

for All Services reported by the Bureau of Labor

Statistics. Recall that the physical medicine MPI

is looking strictly at unit charge while holding

utilization constant. No significant changes in

technology to deliver physical medicine services

have been discovered that might influence the

unit charge of these services.

Workers’ Compensation Medical Price Index

WCS Medical Price Index

Since Q1 2006, the National Workers’ Compensation MPI has increased 12.21 percent while the National CPI for All Services increased 19.33 percent.

By Ed OlsenSr. Business Process Consultant, Mitchell Casualty Solutions Group

• Since Q4 2015, the unit charge of professional

services performed in the emergency room

setting has decreased 3.16 percent. Despite this

decrease, the index reflects an overall increase

in the unit charge of this service group of 49.53

percent since Q1 2006. The index value for this

service group has experienced intermittent

decreases since Q1 2006 on it steady drive

upward. It is believed that this is just another

temporary improvement.

• Contrary to the trend in unit cost of Major

radiology services seen in the auto casualty

market, the unit cost experienced by workers’

compensation claims for this service group

remains flat reflecting a 1.0 percent increase since

Q4 2015. This service groups’ current index value

of 98.4 remains 1.6 percent below the Q1 2006 .

• The unit cost for evaluation & management

services increased in Q1 2016, bringing the

workers’ compensation index to 129.73 from

128.66 in Q4 2015. Since Q1 2006, evaluation

and management unit charge has increased

to 29.73.

Bonus Feature29

30

0

1

2

3

4

5

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Mill

ions

National MPI

Total Units National MPI CPI All services

WCS Medical Price Index

National MPI

0

200

400

600

800

1,000

1,200

1,400

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Evaluation & Management MPI

Total Units National MPI CPI All services

Evaluation & Management MPI

0

10

20

30

40

50

60

70

80

90

100

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Emergency Room MPI

Total Units National MPI CPI All services

Emergency Room MPI

31

0

1,000

2,000

3,000

4,000

5,000

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Physical Medicine MPI

Total Units National MPI CPI All services

0

10

20

30

40

50

60

70

80

90

100

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Major Radiology MPI

Total Units National MPI CPI All services

60

80

100

120

140

160

180

200

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Emergency Room MPI

Workers Compensation CPI All services Auto Casualty

WCS Medical Price Index

Physical Medicine MPI

Major Radiology MPI

Emergency Room MPI

32

0

5

10

15

20

25

30

35

40

45

50

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Nerve Testing MPI

Total Units National MPI CPI All services

0

5

10

15

20

25

30

35

40

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Minor Radiology MPI

Total Units National MPI CPI All services

WCS Medical Price Index

Nerve Testing MPI

Minor Radiology MPI

33 WCS Medical Price Index

0

5

10

15

20

25

30

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Pain Management MPI

Total Units National MPI CPI All services

0

5

10

15

20

25

30

50

70

90

110

130

150

170

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

Thou

sand

s

Major Surgery MPI

Total Units National MPI CPI All services

Pain Management MPI

Major Surgery MPI

3434 ACS Medical Price Index

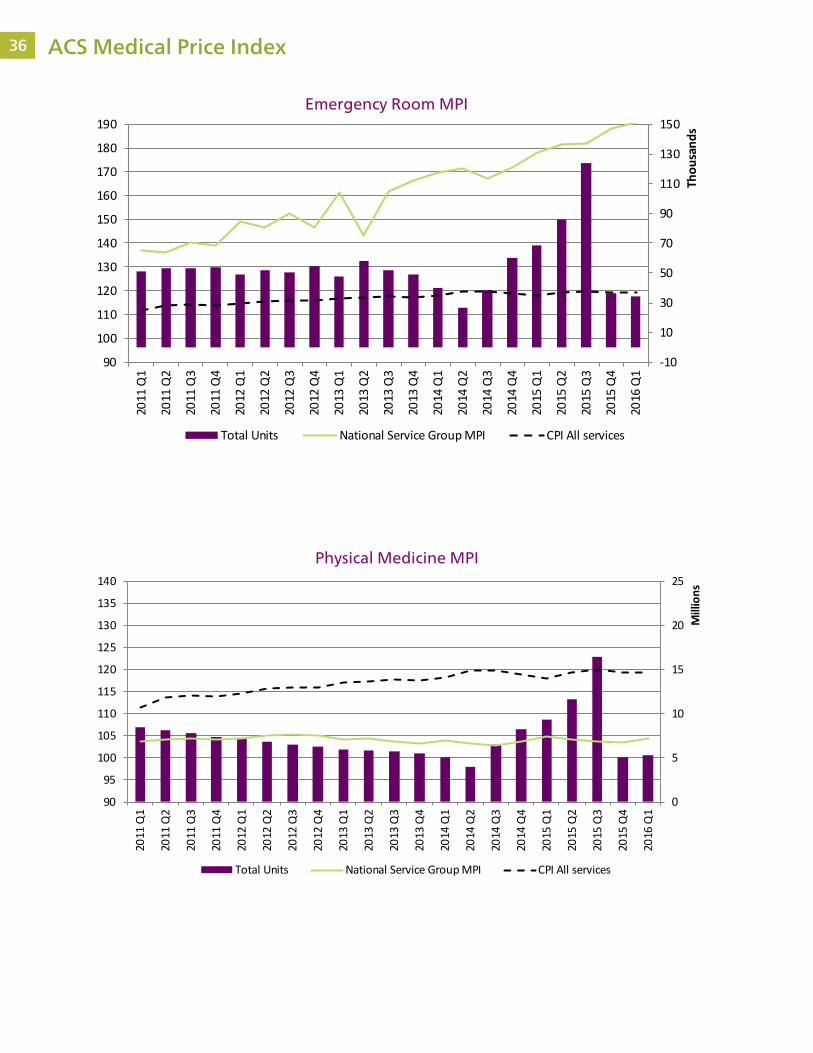

The National CPI for All Services, as reported by the

U.S. Bureau of Labor Statistics, is presently 119.33,

which is down 0.11 percent in Q1 2016 since Q4

2015. For the same period of time, Q4 2015 to Q1

2016, the National Auto Casualty Medical Price

Index increased 1.04 percent and presently sits

at 118.98. Since Q1 2006, the National MPI has

increased 18.98 percent while the National CPI for

All Services increased 19.33 percent.

• Charges associated with physical medicine

services experienced a 0.81 percent increase in

Q1 2016 from Q4 2015. This increase brings the

total unit cost change for physical medicine since

Q1 2006 to 4.2 percent, significantly below the

National CPI for All Services as reported by the

Bureau of Labor Statistics. Recall that the physical

medicine MPI is looking strictly at unit charge

while holding utilization constant. No significant

changes in technology to deliver physical

medicine services have been discovered that

might influence the unit charge of these services.

Auto Casualty Medical Price IndexBy Ed OlsenSr. Business Process Consultant, Mitchell Casualty Solutions Group

Since Q1 2006, the National MPI has increased 18.98 percent while the National CPI for All Services increased 19.33 percent.

35 ACS Medical Price Index

• The unit cost for major radiology services

increased 0.91 percent in Q1 2016 from Q4 2015

and presently sits at 124.3. Despite this increase,

MPI for major radiology services remains 4.5

percent below the service groups’ high of 128.75

experienced in Q4 2013.

• The unit cost for evaluation & management

services increased 2.67 percent in Q1 2016 when

compared with its Q4 2015 result. Since Q1 2006,

evaluation and management services have seen

unit charge increase 75.11 percent as reflected by

the index value of 175.11.

• The unit charge for professional services in the

emergency room continues to dominate the

conversation dealing dramatic increases in unit

charge. In Q1 2016, professional services in the

emergency room experienced a 2.26 percent

increase since Q4 2015. Since Q1 2006, this

service group has experienced a 90.5 percent

increase in the unit charge of professional

emergency room evaluation and management

services.

36 ACS Medical Price Index

-10

10

30

50

70

90

110

130

150

90

100

110

120

130

140

150

160

170

180

19020

11 Q

1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Thou

sand

s

Emergency Room MPI

Total Units National Service Group MPI CPI All services

Emergency Room MPI

0

5

10

15

20

25

90

95

100

105

110

115

120

125

130

135

140

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Mill

ions

Physical Medicine MPI

Total Units National Service Group MPI CPI All services

Physical Medicine MPI

37

0

5

10

15

20

25

90

95

100

105

110

115

120

125

130

135

140

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Mill

ions

National MPI

Total Units National MPI CPI All services

0

100

200

300

400

500

600

700

800

900

1,000

90

100

110

120

130

140

150

160

170

180

190

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Thou

sand

s

Evaluation & Management MPI

Total Units National Service Group MPI CPI All services

Evaluation & Management MPI

-10

10

30

50

70

90

110

130

150

90

95

100

105

110

115

120

125

130

135

140

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Thou

sand

s

Major Radiology MPI

Total Units National Service Group MPI CPI All services

Major Radiology MPI

National MPIACS Medical Price Index

3838

Medical Marijuana Prescription protocols for medical marijuana

are changing monthly due to new studies

promoting use and regulatory bodies that allow

the prescription of medical marijuana in their

states. Medical marijuana, sometimes referred

to as “Medical Jane,” has been used for medical

purposes since 1550 BC in ancient Egypt to treat

inflammation. It took thousands of years to actually

be able to prescribe medical marijuana legally in

the United States for the same ailment. In modern

history, the Food and Drug Administration (FDA) has

been the gate keeper for permitting drug use in the

United States. Marijuana was categorized with other

illegal drugs like opium and morphine since the early

1990s. By 1970, marijuana was a “Schedule I” drug

and was considered to have no medical use.

In November 1991, the very first proposition called

on the state of California and the California Medical

Association to “restore hemp medical preparations

to the list of available medicines in California, and

not to penalize physicians for prescribing hemp

preparations for medical purposes. The vote passed

overwhelmingly with nearly 80 percent in favor.

The state of California legalized medical marijuana

in 1996” (Procon.org, 2016). In addition to the

District of Columbia, medical marijuana is currently

legal in the following U.S. states: Alaska, Arizona,

California, Colorado, Connecticut, DC, Delaware,

Hawaii, Illinois, Maine, Maryland, Massachusetts,

Michigan, Minnesota, Montana, Nevada, New

Hampshire, New Jersey, New Mexico, New York,

Ohio, Oregon, Pennsylvania, Rhode Island, Vermont

and Washington.

The Compliance Corner

The Compliance Corner

Medical marijuana, sometimes referred to as “Medical Jane,” has been used for medical purposes since 1550 BC in ancient Egypt to treat inflammation.

By Michele Hibbert-Iacobacci, OHCC, CCSPVice President, Information Management & Support, Casualty Solutions Group

Medical Marijuana, Telemedicine and Opt-Out

39

Nearly all other states have propositions on the

books for legalizing medical marijuana.

There is a large difference between the legalization

of medical marijuana and the coverage of the drug

under insurance policies. Aside from the workers’

compensation cases in Minnesota and New Mexico

(Lewis v. Am. Gen. Media), there has not been a

broad acceptance by payors. This is a legal matter

left to interpretation by policy and regulations.

Today the FDA has not approved marijuana for

medical use and it is still classified under the same

umbrella with heroin, LSD and Ecstasy as a

Schedule 1 drug. The latest move to change the

drug class was in March 2015, when the CARERS Act

was introduced to the Senate proposing to reclassify

marijuana to Schedule II, recognizing the “accepted

medical use.” Schedule II drugs are those that can be

potentially addictive like oxycodone.

On June 2, 2016, the Property Casualty Insurers

Association of America (PCI) issued a statement

expressing their approval of the House Action on the

Marijuana-Impaired Driving Study.

Excerpt from National Highway Transportation and

Safety Association:

“PCI applauds the House Appropriations Committee

for including language in its THUD report that

directs the National Highway Traffic Safety

Administration (NHTSA), along with the National

Institute on Drug Abuse and other related agencies,

to conduct a study of marijuana-impaired driving,”

(PCI, 2016).

This commentary is on the heels of a review by PCI

and NHTSA examining the use of marijuana and

distracted driving leading to higher claim frequency

(NHTSA, 2016).

Click Here To View Full Statement

How regulations for casualty evolve will take time.

The use of medical marijuana, even if compensated

routinely, will still have challenges. Employers will

need to evaluate patients who are prescribed

medical marijuana for on-the-job liabilities and

determine the new norm of distracted driving, with

driving under the influence as a cause for the rise in

claim frequency.

There is a large difference between the legalization of medical marijuana and the coverage of the drug under insurance policies.

The Compliance Corner

1. NHTSA. (2016, Feb). National Highway Transportation and Safety Association. Retrieved Jun 2016, from www.nhtsa.gov: http://www.nhtsa.gov/About+NHTSA/Press+Releases/2015/nhtsa-releases-2-impaired-driving-studies-02-2015

2. PCI. (2016, June 2). www.PCIAA.net. Retrieved 2016, from Property Casualty Insurers of America: http://www.pciaa.net/pciwebsite/Cms/Content/ViewPage?sitepageid=455873. Procon.org. (2016, April 6). History of Marijuana as Medicine. Retrieved 2016, from www.procon.org: http://medicalmarijuana.procon.org/view.timeline.php?timelineID=000026

40 Compliance Corner

Telemedicine: New Innovations in the Old Program Telemedicine is the method of delivering health

care electronically through applications like smart

phones, email, and skype. Telemedicine started over

40 years ago with the intention of enabling health

care providers, mainly hospitals, to provide services

to patients in remote areas.

The concept expanded as a means to provide

more affordable services and better quality care

by health care providers after The Affordable Care

Act was introduced in 2012, mandating health

insurance coverage for all Americans. This legislation

introduced many new-comers to the healthcare

system that otherwise may have never been

provided health services. Over 30 million people

with coverage were added into the healthcare

system during this time, with the threat of not

enough providers to service those insured.

It is estimated that the United States currently holds

roughly 200 telemedicine networks, providing

connection to over 3,000 sites. A variety of services

including consultations, medical education modules,

vitals monitoring and meetings with primary care

providers are examples of the offerings made

available through telemedicine.

Timing is critical when it comes to delivering

emergency services for some medical conditions.

With timing being an influential role, it makes sense

that telemedicine continues to think about how

to develop quality clinical services and improve

innovation. One example of innovation used in the

telemedicine realm is “telestroke” services, which

have the ability to send information to neurologists

from rural facilities to assist identifying the sources

of strokes in patients. Initial studies in Canada have

shown a 92 percent decrease in the transferring of

patients to more expensive facilities, thus making

the care more affordable. What you won’t see in

telemedicine are chiropractic manipulations and

other hands-on care, but instead, the planning

and care coordination efforts as it relates to these

specific providers.

The Institute for Healthcare Consumerism (IHC) has

been reporting on “wait times” and the impact of

adding more patients into the system for several

years. For example, in San Diego, the average wait

time for a provider appointment is 20.2 days, and

27 days in Philadelphia. These long wait times

can impact a patient’s health and the use of

telemedicine can be invaluable in providing quality

of care in these instances. When a patient suffers

a severe injury as in a motor vehicle accident, they

go to the emergency room. The Center for Disease

Control has reported that nearly 80 percent of adults

are going to the emergency room because of a

lack of alternative health care resources, ultimately

impacting the people that really need to be treated

in the Emergency Room setting. Telemedicine could

serve as a solution in these cases.

The challenge we face in the Property and Casualty

(P&C) industry is delineating the necessity for

telemedicine, and positioning the benefit of

including it as an “add on” to services already

rendered. The intent of telemedicine is to provide

quality and affordable care, not to create another

line item on the provider bill for payment. For

telemedicine Professional Services claims, services

are to use the appropriate CPT or HCPCS code along

with the modifier GT (via interactive audio and video

telecommunications systems).

41

Imagine a $50 telemedicine bill on a claim replacing

the average $1,000 or more emergency room bill.

It certainly makes it a compelling alternative for the

future. The market assessments are not bad either,

with Insurancenewsnet.com reporting in January

2016 a potential market for telemedicine valued

over $45 billion by 2021.

Opt-Out: Hurry Up and WaitOpt-out in the workers’ compensation world is

2016’s buzzword for deregulation of payment for

workers’ compensation claims at the state level.

Opt-out is an alternate compensation model for the

injured worker whereby employers choose to opt-

out of state regulated systems. It has been promoted

in some states like Oklahoma and Texas. Although

not a new concept, new interests among both

advocates and non-supporters have been brought

to the horizon, including different proposed models.

Last May, the International Association of

Industrial Accident Boards and Commissions

(IAIABC) published an analysis of the treatment

of occupational injuries and illnesses under state

workers’ compensation systems and Opt-out

programs adopted in Oklahoma and proposed in

South Carolina and Tennessee. The study sought to

address key questions outlined below:

• What part of workers’ compensation law is the

employer renouncing by opting out?

• What are the conditions, or regulatory

requirements, that the state places on opt-out

employers?