Embed Size (px)

Citation preview

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 1/6

43

4C H A P T E R

The Pitfalls of Ignoring Macro Influences

Accidental Success

Markets are constantly in a state of uncertainty and flux and money is

[made] by discounting the obvious and betting on the unexpected.1

—George Soros

Investors ignore the influence of macro on their portfolios for a

variety of reasons, but almost always at their own peril. Commonly,this occurs when an investor’s perception is skewed by “accidentalsuccess.” Making a few correct calls using only a bottom-up strategy may influence investors to think that they are great stock pickers.In reality, it’s more likely that they have just been on the right sideof macro trends without realizing it, such as choosing stocks froma sector that was in favor. The dot-com bubble of the late 1990s

was a perfect example of this phenomenon. It was a “throw a dart

at the stock charts” era when everyone from taxi drivers to financialprofessionals had a profitable day-trading account. The successesfooled people into thinking that they were genius stock pickers,but in fact they were riding the wave of the tech revolution andmass speculation. This was a macro-driven story, albeit a bubble,but not a stock-picking market at all. Technology and telecommstocks ruled the day. Almost any company with a “dot-com” at theend of its name had the potential to post exponential gains in ashort period of time, regardless of the health (or even existence) of

c04.indd 43c04.indd 43 6/30/11 2:54:34 PM6/30/11 2:54:34 PM

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 2/6

44 The Era of Uncertainty

its balance sheet. When the fall came, it was indiscriminate as well.

Technology companies with positive earnings growth and high-quality management were not spared the pain exacted on the sector as a

whole. Tech giants such as Cisco and Oracle have yet, as of early 2011, to regain their highs reached in 2000. Top-down trends ruledboth the rise and the fall of this market cycle.

Some successful investors may actually make decisions agnostic of macro influences, and merely benefit from a combination of goodluck and timing. There are countless stories of hedge fund managersand traders who bet the farm on black and were lucky enough to havethe roulette wheel reward their gamble—managers who shorted Enronon a bad feeling in the early 2000s or bet against subprime mortgagesin 2007 using synthetic derivatives they did not even understand.Investors who follow winner-take-all strategies like these must makenot only the correct directional call, but also pull the trigger at theright time. Even if an investor foresaw the potential carnage aheadin the real estate market—as François wrote about in 2005—puttingthat trade in motion too early could have wiped out a fund beforethe bubble actually burst. For each of the high-profile stories of hedge funds that made spectacular gains in 2007 and 2008, there

are thousands of others that had the story right and the timing wrong. Using the context of the macro environment was the essentialelement that many of those unsuccessful managers missed.

Macro Lessons Are Learned through Experience

The signals sent by the business cycle before, during, and after thecredit bubble are compelling examples of how macro trends can beused to navigate the equity markets. It is surprising that investorscould be confronted with a powerful illustration such as this andstill fail to embrace the influence of top-down trends. Memories areremarkably short in the financial industry, however, and like most life lessons they are better learned firsthand than by proxy. There isan incredible ability on Wall Street to believe that the pain exactedon other investors will not befall oneself. This belief is partially rooted in hubris, but partially due to the relatively short length of

Wall Street careers. The make-it-big-and-get-out career path leaves30 year olds calling the shots in more cases than the average personmight imagine. Astute investors who are able to turn the massivelosses experienced in 2008 into a lesson learned will be ahead of

the pack when the next bubble arrives.

c04.indd 44c04.indd 44 6/30/11 2:54:34 PM6/30/11 2:54:34 PM

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 3/6

The Pitfalls of Ignoring Macro Influences 45

David Einhorn of Greenlight Capital—arguably most famous

for shorting Lehman Brothers in 2007—told his personal tale of learning this lesson at the Value Investing Congress in October2009. He referred to a speech he delivered in May 2005 at the IraSohn Investment Research Conference when he recommendedMDC Holdings, a homebuilder, at $67 per share. The stock reached$89 within two months, but anyone who held on to the positionrode it down with the rest of the sector in 2007. He said,

Some of my MDC analysis was correct: it was less risky than

its peers and would hold up better in a down cycle because it

had less leverage and held less land. But this just meant that almost half a decade later, anyone who listened to me would

have lost about 40 percent of his investment, instead of the

70 percent that the homebuilding sector lost.

The reason he gave for revisiting this story was that it was not bad luck, but bad analysis . He contrasted what he said that day with what he heard from legendary hedge fund manager Stan Druckenmiller abit later in the conference. Stan’s chosen topic was the grim story of the problems we faced from an expanding housing bubble inflatedby a growing debt bubble. David wondered, even if Stan were correct,how would one translate such a big picture macro view into a success-ful investment strategy? He soon had the answer to his own question:

I ignored Stan, rationalizing that even if he were right,

there was no way to know when he would be right. This was

an expensive error. The lesson that I have learned is that it isn’t

reasonable to be agnostic about the big picture. For years I had

believed that I didn’t need to take a view on the market or

the economy because I considered myself to be a “bottom up”investor. Having my eyes open to the big picture doesn’t mean

abandoning stock picking, but it does mean managing the

long-short exposure ratio more actively, worrying about what

may be brewing in certain industries, and when appropriate,

buying some just-in-case insurance for foreseeable macro risks

even if they are hard to time.

David then proceeded to discuss the macro risks he believed were facing the markets at that point in late 2009. We couldn’t have

said it better ourselves.

c04.indd 45c04.indd 45 6/30/11 2:54:35 PM6/30/11 2:54:35 PM

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 4/6

46 The Era of Uncertainty

Business Cycle Analysis Can Enhance the Power of Quant

Quantitative investment strategies have exploded in the last several decades as

computing power became exponentially faster and cheaper. Everything from

data mining to genetic algorithms has been employed to try to squeeze another

few basis points of alpha from the markets. These types of strategies can, and

do, work—quant models have played a huge role in successful investing over

the last several decades. The most common problem is that very often manag-

ers blindly accept the output of these models without any qualitative judgment.

Research shows that incorporating business cycle trends into quantitative

analysis can greatly enhance its power.

Black box models based on broad historical data add little value at inflection

points. Investors who rely solely on optimizers or other quantitative methodologies

can end up loading up on what has worked, instead of investing for what is to

come. Take the recent experience with the credit/housing bubble—it is unlikely

that the same factors that add value in a cyclically driven market environment (led

by consumer discretionary stocks and financials) would perform as well when

moving into a defensive market environment (led by consumer staples and

utilities). This was indeed the case. Tilting factors between cyclicality and stability

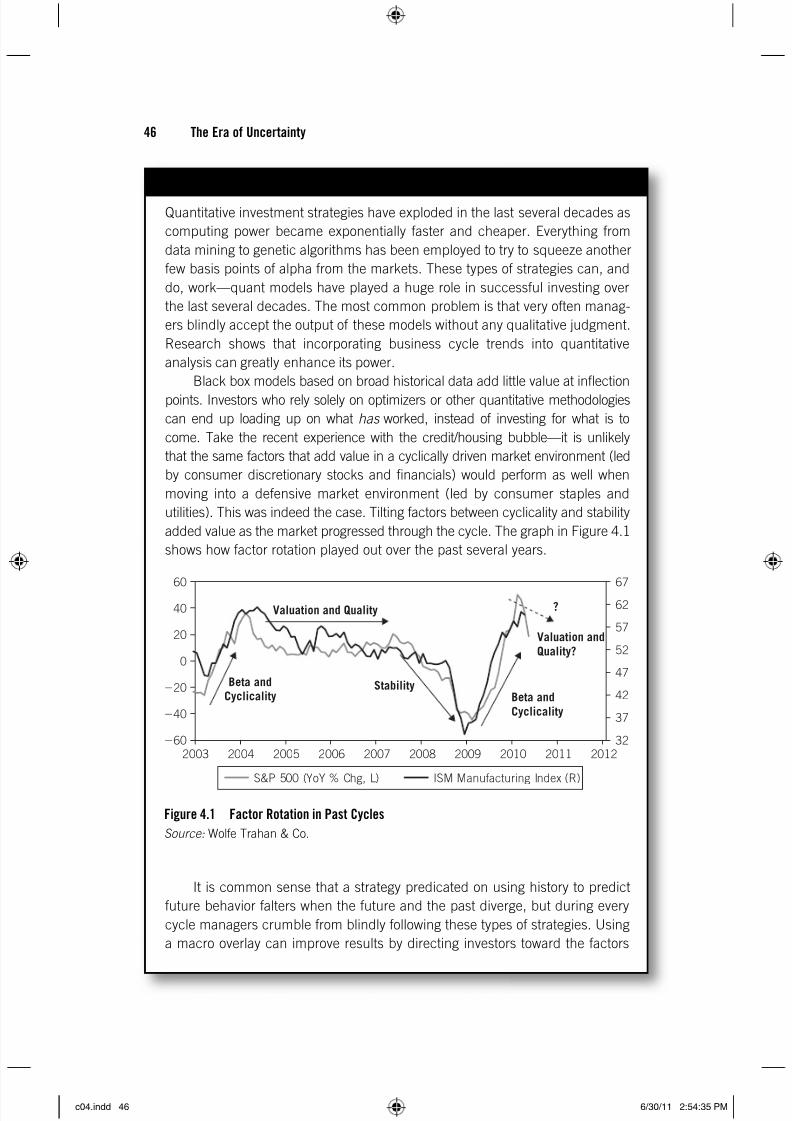

added value as the market progressed through the cycle. The graph in Figure 4.1

shows how factor rotation played out over the past several years.

It is common sense that a strategy predicated on using history to predict

future behavior falters when the future and the past diverge, but during every

cycle managers crumble from blindly following these types of strategies. Using

a macro overlay can improve results by directing investors toward the factors

Beta andCyclicality

Valuation and Quality

StabilityBeta and

Cyclicality

Valuation and

Quality?

?

60

40

20

0

20

40

60

2003 2004 2005 2006 2007 2008 2009 2010 2011 201232

37

42

47

52

57

62

67

S&P 500 (YoY % Chg, L) ISM Manufacturing Index (R)

Figure 4.1 Factor Rotation in Past Cycles

Source: Wolfe Trahan & Co.

c04.indd 46c04.indd 46 6/30/11 2:54:35 PM6/30/11 2:54:35 PM

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 5/6

The Pitfalls of Ignoring Macro Influences 47

that work in the environment at hand. It can also turn a factor that appears to

add no value into a very profitable input. Return on Assets (ROA) is a great

example. The power of the business cycle becomes evident when timing the

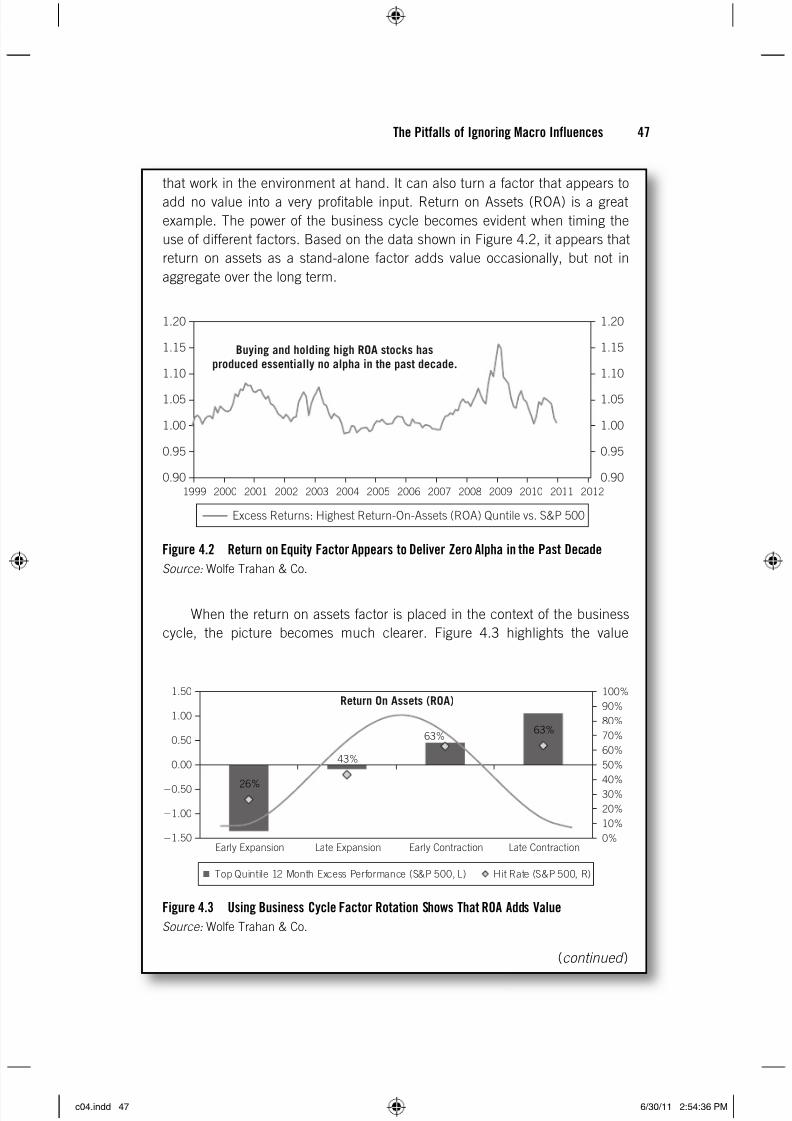

use of different factors. Based on the data shown in Figure 4.2, it appears that

return on assets as a stand-alone factor adds value occasionally, but not in

aggregate over the long term.

When the return on assets factor is placed in the context of the business

cycle, the picture becomes much clearer. Figure 4.3 highlights the value

Buying and holding high ROA stocks hasproduced essentially no alpha in the past decade.

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Excess Returns: Highest Return-On-Assets (ROA) Quntile vs. S&P 500

Figure 4.2 Return on Equity Factor Appears to Deliver Zero Alpha in the Past Decade

Source: Wolfe Trahan & Co.

Return On Assets (ROA)

43%

26%

63%63%

1.50

1.00

0.50

0.00

0.50

1.00

1.50

Early Expansion Late Expansion Early Contraction Late Contraction0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top Quintile 12 Month Excess Performance (S&P 500, L) Hit Rate (S&P 500, R)

Figure 4.3 Using Business Cycle Factor Rotation Shows That ROA Adds Value

Source: Wolfe Trahan & Co.

(continued )

c04.indd 47c04.indd 47 6/30/11 2:54:36 PM6/30/11 2:54:36 PM

8/4/2019 VIL August Wiley Excerpt

http://slidepdf.com/reader/full/vil-august-wiley-excerpt 6/6

48 The Era of Uncertainty

Business Cycle Analysis Can Enhance the Power of Quant (Continued )

added from ROA when used in the contraction phases of the business cycle.

Waiting to incorporate ROA as a factor until the peak in leading indicators

leads to outperformance 63 percent of the time. Conversely, 74 percent of the

time, investing in stocks with the highest return on assets in the early expansion

phase of the cycle leads to market underperformance.

Chapter Summary

Investors ignore the influence of macro on their portfoliosfor a variety of reasons, but almost always at their own peril.The dot-com bubble of the late 1990s was a perfect exampleof accidental success. The successes fooled people into thinkingthat they were genius stock pickers, but in fact they were ridingthe wave of the tech revolution and mass speculation.Some successful investors may actually make decisions agnosticof macro influences, and merely benefit from a combination of good luck and timing.The signals sent by the business cycle before, during, and

after the credit bubble are compelling examples of howmacro trends can be used to navigate the equity markets. It issurprising that investors could be confronted with a powerfulillustration such as this and still fail to embrace the influenceof top-down trends.

•

•

•

•

c04 indd 48 6/30/11 2:54:37 PM

![· [Ni(NH ) 12+ [COC14]2- [Mn041- Liganden 6 NH3 5 CN- + 1 H- 5 co 4 co Oxidationszahl des Zentralatoms Vil Koordinations- zahl L. H. Gade, Koordinationschemie, Wiley-VCH, 1998](https://img.pdfslide.us/doc/110x75/5d03456988c993c2488dd500/-ninh-12-coc142-mn041-liganden-6-nh3-5-cn-1-h-5-co-4-co-oxidationszahl.jpg)