Embed Size (px)

Citation preview

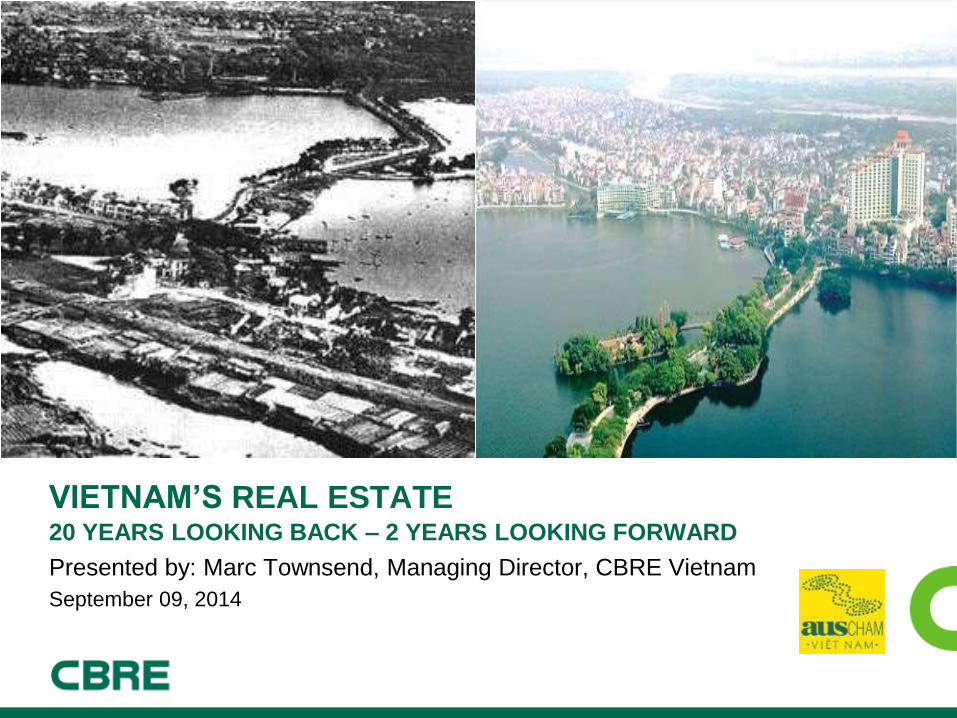

Presented by: Marc Townsend, Managing Director, CBRE Vietnam

September 09, 2014

VIETNAM’S REAL ESTATE 20 YEARS LOOKING BACK – 2 YEARS LOOKING FORWARD

2 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Past and present…

VIETNAM REAL ESTATE MARKET

Source: Google.

HC

MC

Ha

no

i

3 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Ho Chi Minh

City

Hanoi

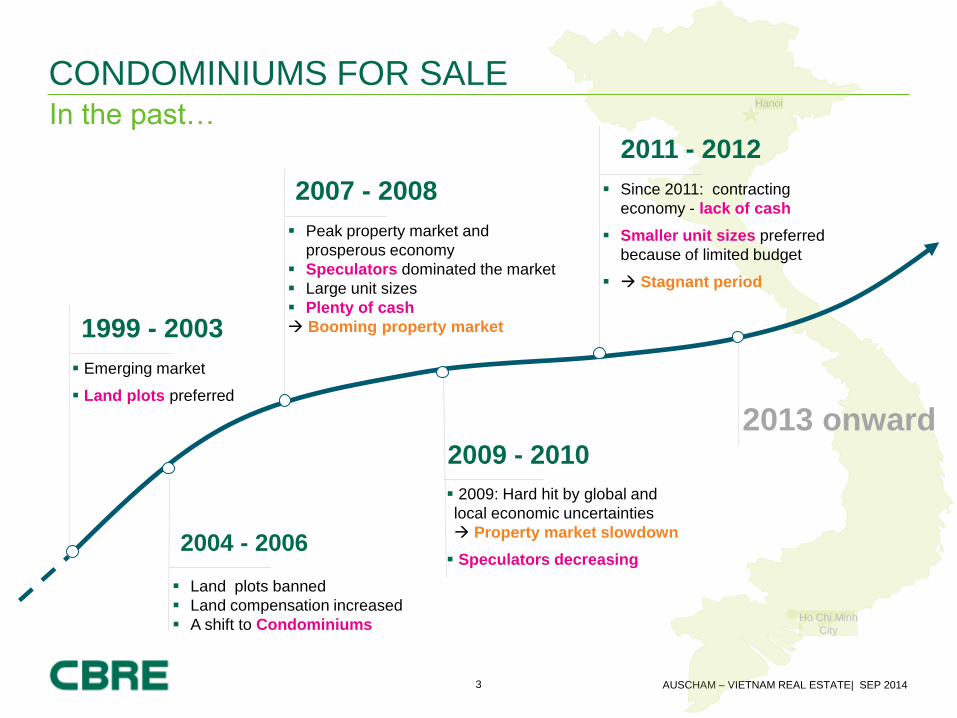

In the past…

CONDOMINIUMS FOR SALE

1999 - 2003

Emerging market

Land plots preferred

2004 - 2006

Land plots banned

Land compensation increased

A shift to Condominiums

2007 - 2008

Peak property market and

prosperous economy

Speculators dominated the market

Large unit sizes

Plenty of cash

Booming property market

2009 - 2010

2009: Hard hit by global and

local economic uncertainties

Property market slowdown

Speculators decreasing

2011 - 2012

Since 2011: contracting

economy - lack of cash

Smaller unit sizes preferred

because of limited budget

Stagnant period

2013 onward

4 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

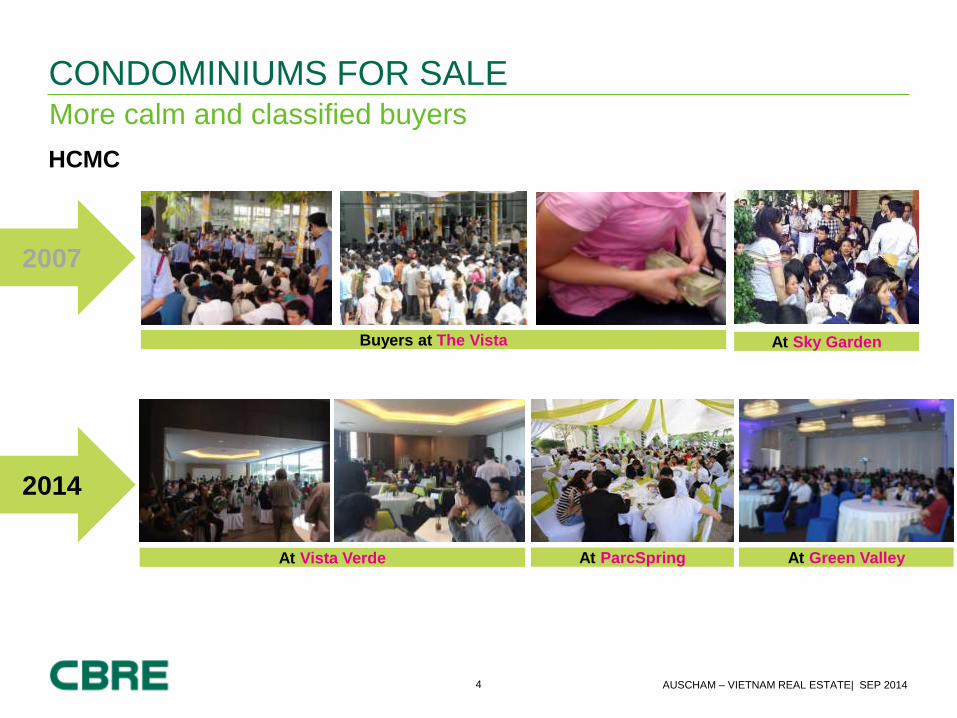

More calm and classified buyers

CONDOMINIUMS FOR SALE

2007

Buyers at The Vista

At Green Valley

At Sky Garden

At ParcSpring

2014

At Vista Verde

HCMC

5 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

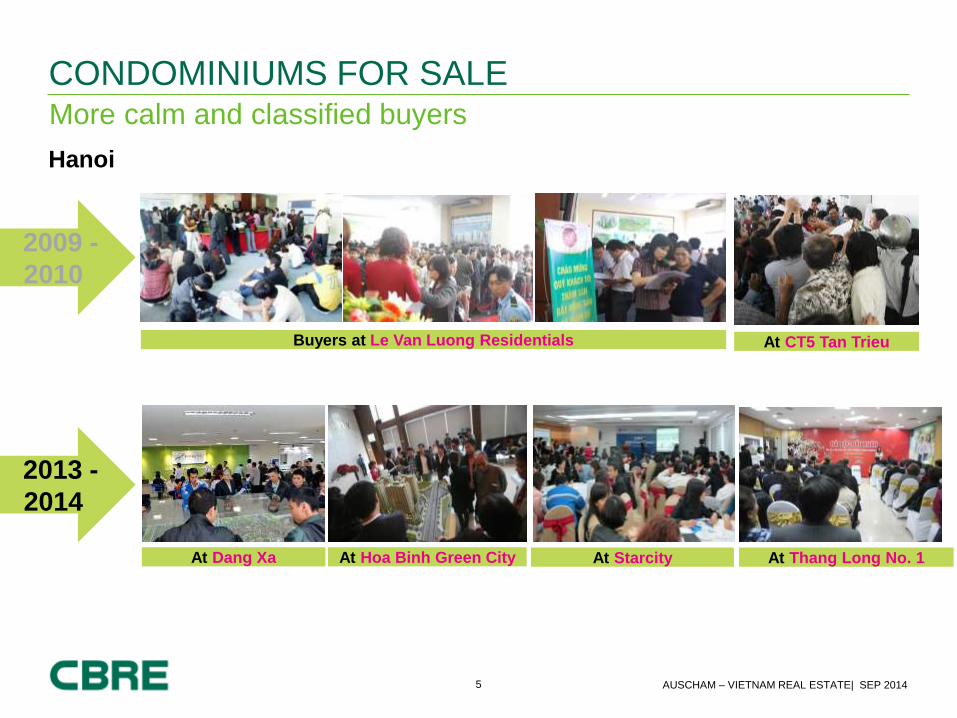

More calm and classified buyers

CONDOMINIUMS FOR SALE

2009 -

2010

Buyers at Le Van Luong Residentials

At Thang Long No. 1

At CT5 Tan Trieu

At Starcity

2013 -

2014

At Hoa Binh Green City At Dang Xa

Hanoi

VIETNAM REAL ESTATE MARKET MARKET SITUATION UPDATE

7 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

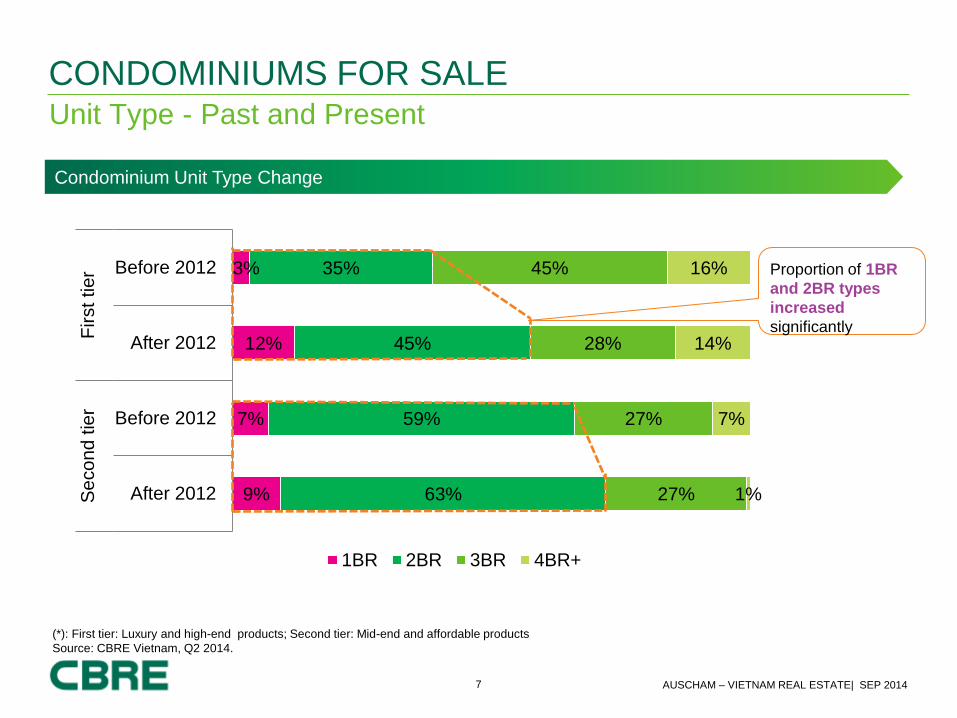

Unit Type - Past and Present

CONDOMINIUMS FOR SALE

(*): First tier: Luxury and high-end products; Second tier: Mid-end and affordable products

Source: CBRE Vietnam, Q2 2014.

Condominium Unit Type Change

9%

7%

12%

3%

63%

59%

45%

35%

27%

27%

28%

45%

1%

7%

14%

16%

After 2012

Before 2012

After 2012

Before 2012

Se

co

nd

tie

rF

irst

tier

1BR 2BR 3BR 4BR+

Proportion of 1BR

and 2BR types

increased

significantly

8 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

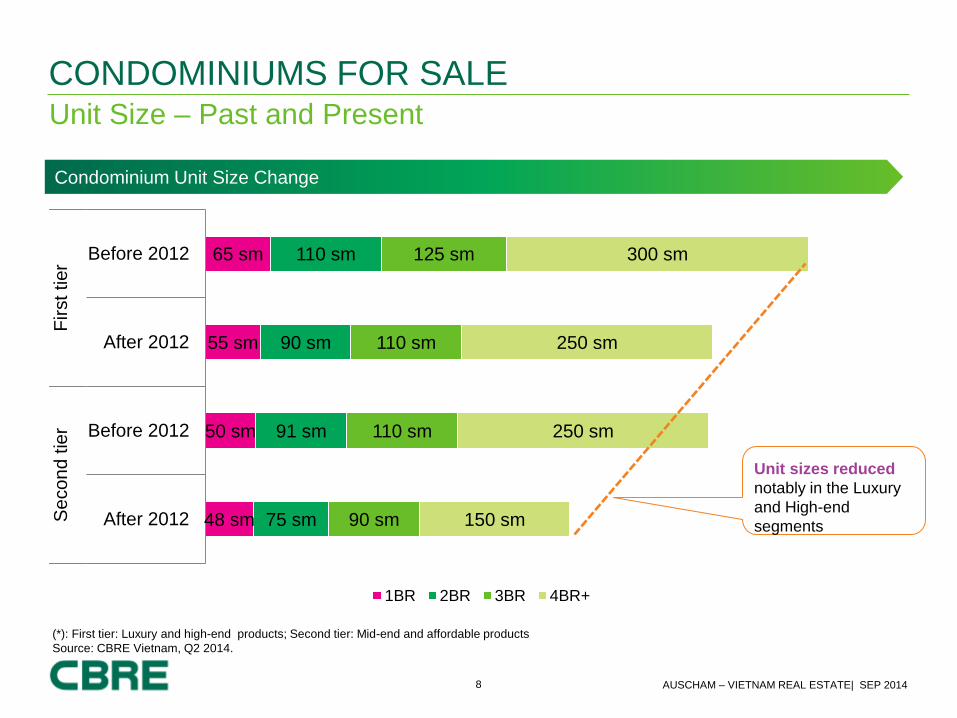

Unit Size – Past and Present

CONDOMINIUMS FOR SALE

(*): First tier: Luxury and high-end products; Second tier: Mid-end and affordable products

Source: CBRE Vietnam, Q2 2014.

48 sm

50 sm

55 sm

65 sm

75 sm

91 sm

90 sm

110 sm

90 sm

110 sm

110 sm

125 sm

150 sm

250 sm

250 sm

300 sm

After 2012

Before 2012

After 2012

Before 2012

Se

co

nd

tie

rF

irst tier

1BR 2BR 3BR 4BR+

Condominium Unit Size Change

Unit sizes reduced

notably in the Luxury

and High-end

segments

9 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Total Supply – Shift to Affordable Segment

CONDOMINIUMS FOR SALE

(*): Accumulative launches since 1999, including both completion and under construction units, sold and unsold units.

Source: CBRE Vietnam, Q2 2014.

Before 2010 After 2010

30.7%

31.2%

37.0%

1.1%

48.1%

24.5%

26.6%

0.8%

Market changes to adapt…..

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

Luxury

High-end

Mid-end

Affordable

10 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

CONDOMINIUMS FOR SALE Loans from banks

11 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

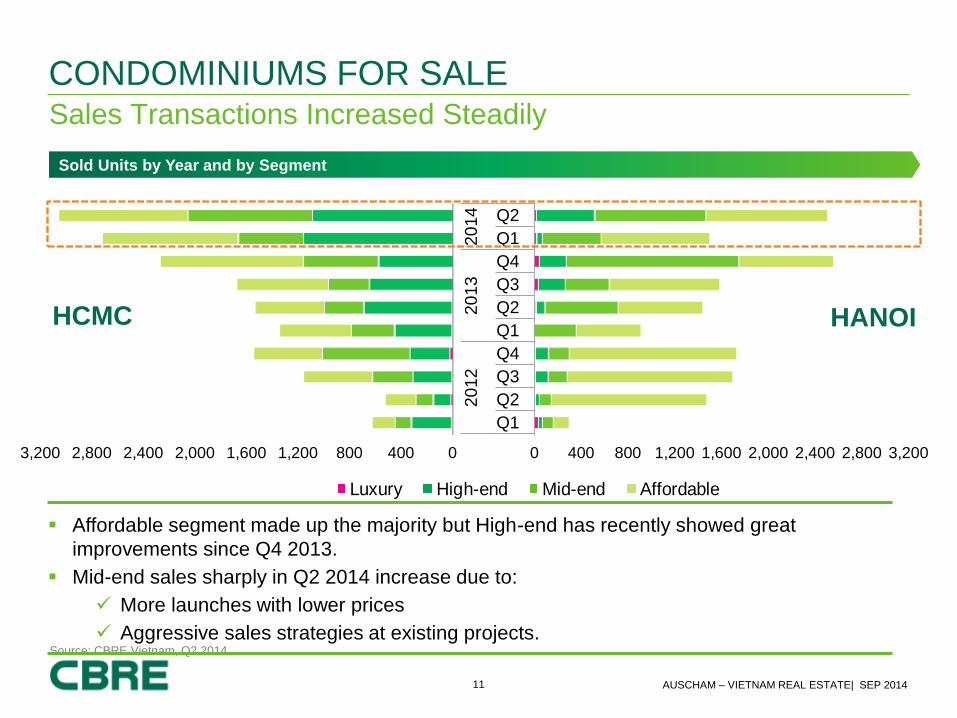

Sales Transactions Increased Steadily

CONDOMINIUMS FOR SALE

Source: CBRE Vietnam, Q2 2014.

Affordable segment made up the majority but High-end has recently showed great

improvements since Q4 2013.

Mid-end sales sharply in Q2 2014 increase due to:

More launches with lower prices

Aggressive sales strategies at existing projects.

Sold Units by Year and by Segment

0 500 1,000 1,500 2,000 2,500 3,000

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2012

2013

2014

Luxury High-end Mid-end Affordable

04008001,2001,6002,0002,4002,8003,200 0 400 800 1,200 1,600 2,000 2,400 2,800 3,200

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

20

12

20

13

20

14

HCMC HANOI

12 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

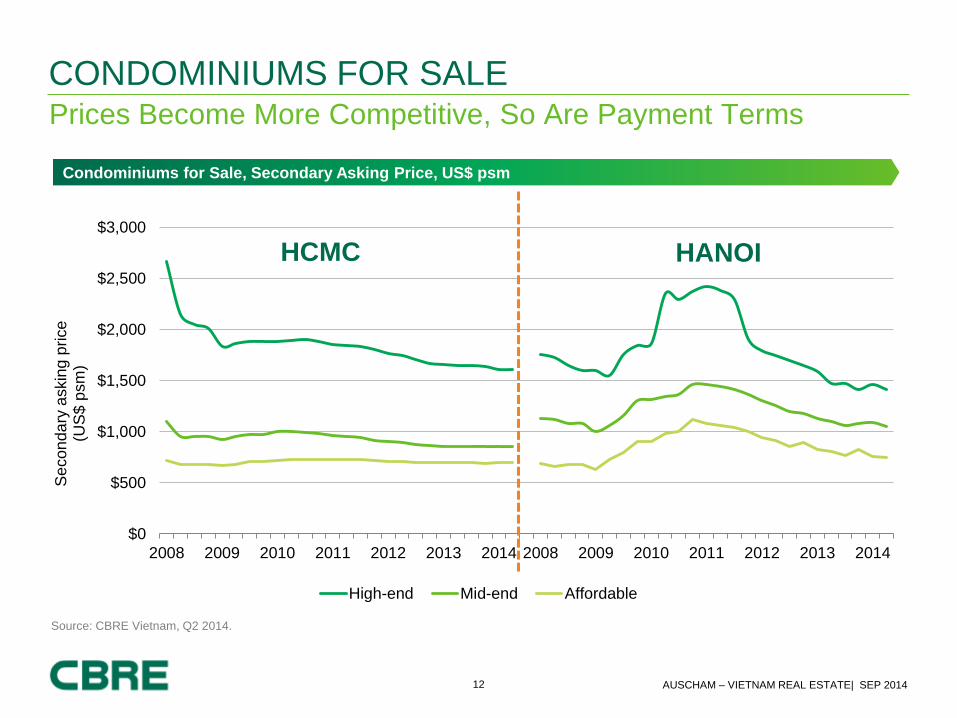

Prices Become More Competitive, So Are Payment Terms

CONDOMINIUMS FOR SALE

Source: CBRE Vietnam, Q2 2014.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Se

co

nd

ary

askin

g p

rice

(U

S$

psm

)

High-end Mid-end Affordable

HCMC HANOI

Condominiums for Sale, Secondary Asking Price, US$ psm

13 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

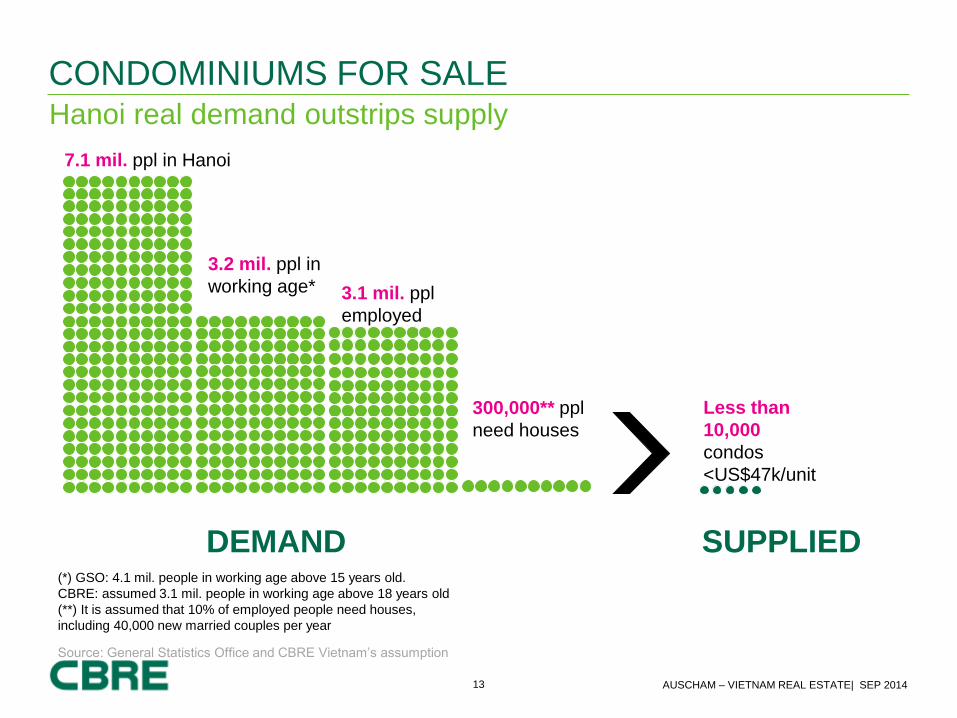

Hanoi real demand outstrips supply

CONDOMINIUMS FOR SALE

7.1 mil. ppl in Hanoi

3.2 mil. ppl in

working age* 3.1 mil. ppl

employed

Less than

10,000

condos

<US$47k/unit

300,000** ppl

need houses

DEMAND SUPPLIED (*) GSO: 4.1 mil. people in working age above 15 years old.

CBRE: assumed 3.1 mil. people in working age above 18 years old

(**) It is assumed that 10% of employed people need houses,

including 40,000 new married couples per year

Source: General Statistics Office and CBRE Vietnam’s assumption

14 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

FLC Garden City

Nam Tu Liem District

1,100 units

Expected price: US$563 psm

Developer: FLC Group

Scale and localisation (September – December 2014)

CONDOMINIUMS FOR SALE - FUTURE SUPPLY

Docklands Saigon

• District 7

• 365 units

• Expected price: N/A

• Developer: Paujar

Ehome 6

• District 9

• 500 units

• Expected price: US$755 psm

• Developer: Nam Long

Lucky Dragon • District 6

• 356 units

• Price: US$1,132 - $1,368 psm

• Developer: Novaland

Sunview Town - Sapphire

• District 9

• 330 units

• Expected price: US$684 psm

• Developer: Dat Xanh Group

HCMC HANOI

FLC Complex • Cau Giay Dist.

• 38 stories

• Expected price:

US$981 psm

• Developer: FLC Group

Source: CBRE Vietnam, Q2 2014.

Vista Verde • District 2

• 300 units (Phase 1)

• Official launch on Sep. 13

• Prices: US$1,400-$1,600 psm

• Developer: JV CapitaLand, Thien Duc

Gamuda Gardens (Apartments)

Hoang Mai District

1,500 units

Expected price: US$892 psm

Developer: Gamuda

15 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

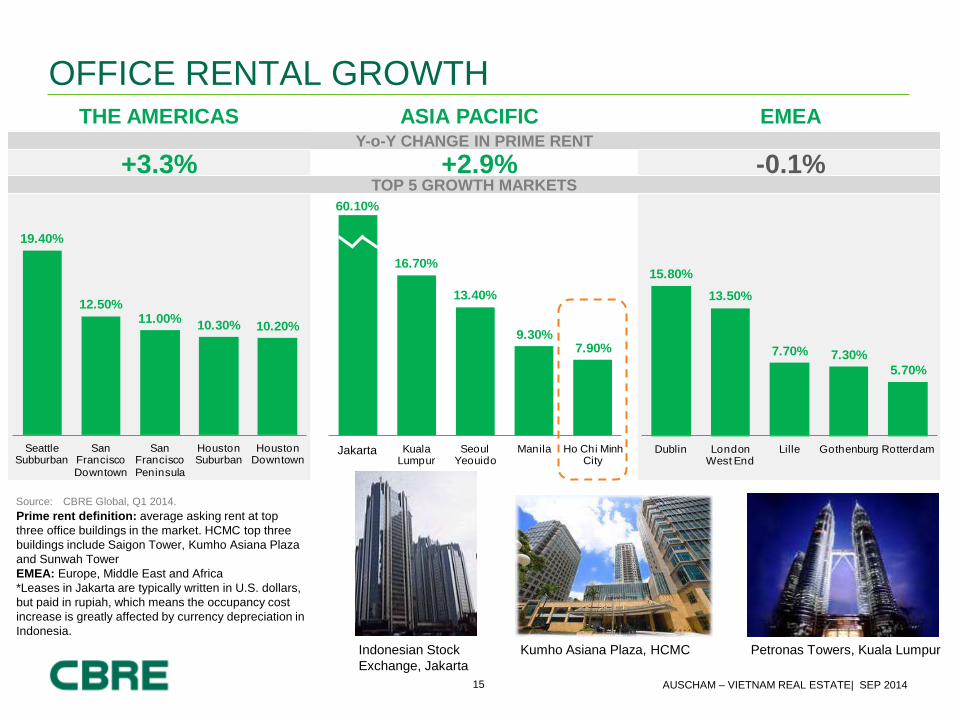

OFFICE RENTAL GROWTH

Y-o-Y CHANGE IN PRIME RENT

THE AMERICAS ASIA PACIFIC EMEA

+3.3% +2.9% -0.1% TOP 5 GROWTH MARKETS

19.40%

12.50%11.00%

10.30% 10.20%

Seattle Subburban

San Francisco

Downtown

San Francisco

Peninsula

Houston Suburban

Houston Downtown

15.80%

13.50%

7.70% 7.30%

5.70%

Dublin LondonWest End

Lille Gothenburg Rotterdam

60.10%

16.70%

13.40%

9.30%7.90%

Jarkarta* Kuala Lumpur

Seoul Yeouido

Manila Ho Chi Minh City

Prime rent definition: average asking rent at top

three office buildings in the market. HCMC top three

buildings include Saigon Tower, Kumho Asiana Plaza

and Sunwah Tower

EMEA: Europe, Middle East and Africa

*Leases in Jakarta are typically written in U.S. dollars,

but paid in rupiah, which means the occupancy cost

increase is greatly affected by currency depreciation in

Indonesia.

Source: CBRE Global, Q1 2014.

Kumho Asiana Plaza, HCMC Petronas Towers, Kuala Lumpur Indonesian Stock

Exchange, Jakarta

Jakarta

16 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

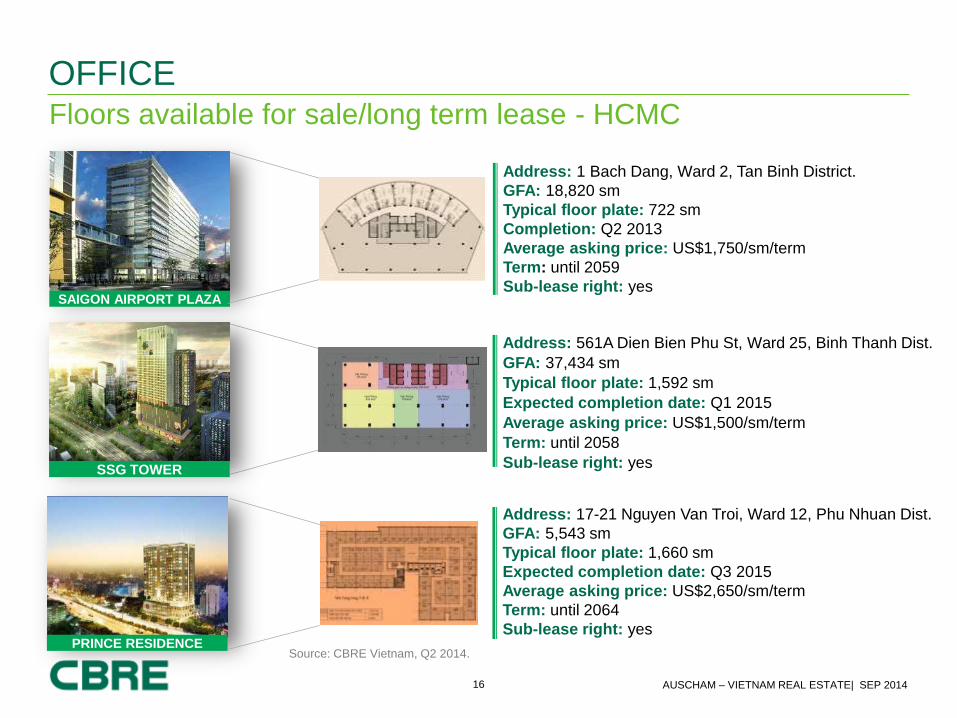

Floors available for sale/long term lease - HCMC

OFFICE

Address: 561A Dien Bien Phu St, Ward 25, Binh Thanh Dist.

GFA: 37,434 sm

Typical floor plate: 1,592 sm

Expected completion date: Q1 2015

Average asking price: US$1,500/sm/term

Term: until 2058

Sub-lease right: yes SSG TOWER

SAIGON AIRPORT PLAZA

Address: 1 Bach Dang, Ward 2, Tan Binh District.

GFA: 18,820 sm

Typical floor plate: 722 sm

Completion: Q2 2013

Average asking price: US$1,750/sm/term

Term: until 2059

Sub-lease right: yes

PRINCE RESIDENCE

Address: 17-21 Nguyen Van Troi, Ward 12, Phu Nhuan Dist.

GFA: 5,543 sm

Typical floor plate: 1,660 sm

Expected completion date: Q3 2015

Average asking price: US$2,650/sm/term

Term: until 2064

Sub-lease right: yes

Source: CBRE Vietnam, Q2 2014.

17 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

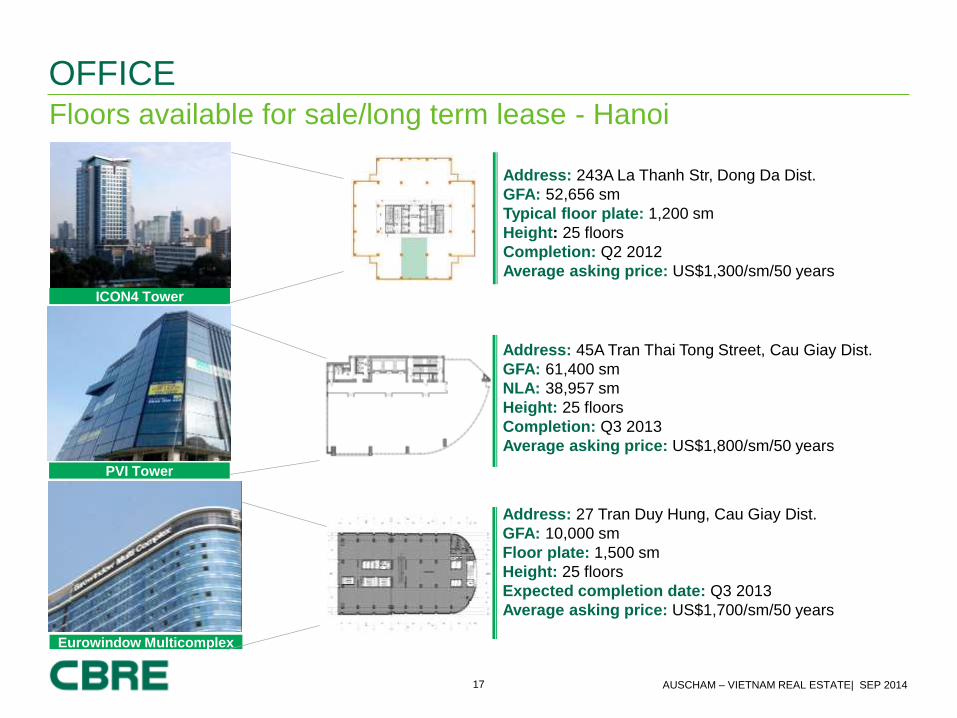

Floors available for sale/long term lease - Hanoi

OFFICE

Address: 45A Tran Thai Tong Street, Cau Giay Dist.

GFA: 61,400 sm

NLA: 38,957 sm

Height: 25 floors

Completion: Q3 2013

Average asking price: US$1,800/sm/50 years

PVI Tower

ICON4 Tower

Address: 243A La Thanh Str, Dong Da Dist.

GFA: 52,656 sm

Typical floor plate: 1,200 sm

Height: 25 floors

Completion: Q2 2012

Average asking price: US$1,300/sm/50 years

Eurowindow Multicomplex

Address: 27 Tran Duy Hung, Cau Giay Dist.

GFA: 10,000 sm

Floor plate: 1,500 sm

Height: 25 floors

Expected completion date: Q3 2013

Average asking price: US$1,700/sm/50 years

18 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Future supply

OFFICE

HCMC

Vietcombank Tower

5 Melinh Square, D1

GFA: 77,000 sm

Expected completion:

Q4/2014

Viettel Office & Trade

Center

285 CMT8, D10

GFA: 65,971 sm

Estimated completion:

Q1/2015

Lim Tower 2

158 Vo Van Tan, D3

GFA: 20,467 sm

Estimated completion:

Q1/2015

SSG Tower

561A Dien Bien Phu St, Ward

25, Binh Thanh.

GFA: 37,434 sm

Estimated completion: Q3/2015

Lotte Center Hanoi

Lieu Giai Street, Ba Dinh Dist

GFA: 65,000 sm

Completion: Sep 2014

Handico Tower

Me Tri NUA, Tu Liem Dist.

GFA: 29,040 sm

Expected completion: 2014

147 Hoang Quoc Viet

147 Hoang Quoc Viet, Cau

Giay Dist.

GFA: 39,419 sm

Estimated completion: 2014

Ho Guom Plaza

Mo Lao NUA, Ha Dong Dist.

GFA: 12,000 sm

Estimated completion: 2014

HANOI

Source: CBRE Vietnam, Q2 2014.

19 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

New retailer entries & expansions

RETAIL

New retailer entry

Robins department store

Expansion

• Opened 20th store in Q2

2014

• 1st store in Hanoi in July

2014

• 3 restaurants opened in

HCMC in 2014.

• Opened 8th store in

HCMC and to open 1st

store in Hanoi in Q3

2014.

• 1st shopping center in

Hanoi in March 2014

• 2nd shopping center in

Hanoi in September

2014

• To open 2nd mall in Binh

Duong in Q4 2014.

• 1st mall in Hanoi in 2015

• 1st store in Hanoi, 10,000 sqm in Vincom Megamall Royal City,

opened in March 2014

• 2nd store in HCMC, 12,000 sqm in The Crescent Mall, expected to

open in Nov 2014.

20 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

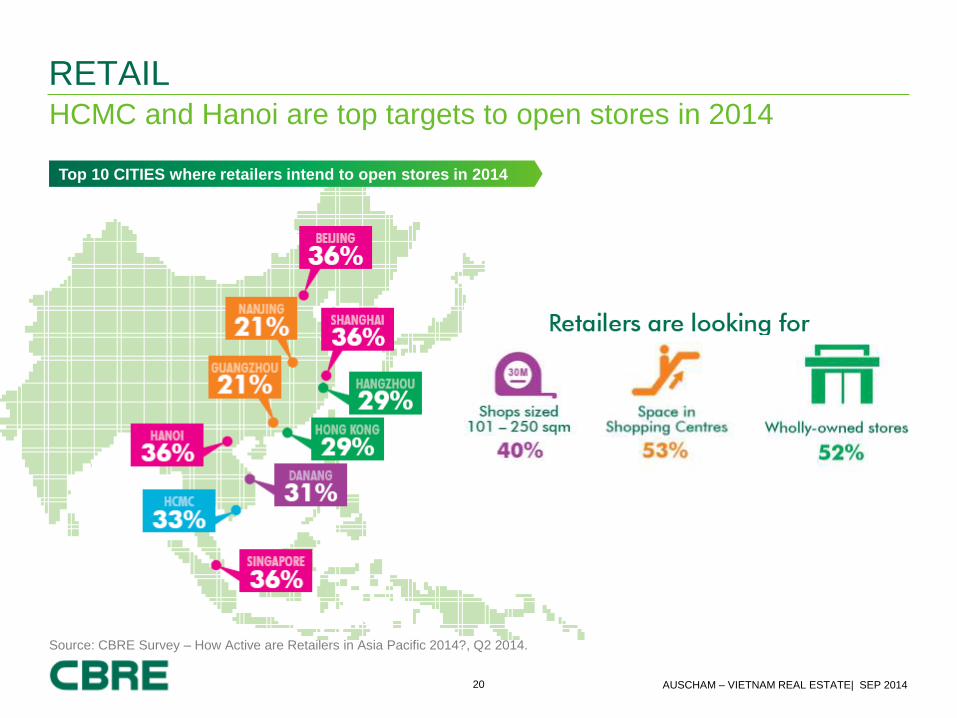

HCMC and Hanoi are top targets to open stores in 2014

RETAIL

Source: CBRE Survey – How Active are Retailers in Asia Pacific 2014?, Q2 2014.

Top 10 CITIES where retailers intend to open stores in 2014

21 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Future supplies with GFA greater than 20,000 sm

RETAIL

SC VivoCity

• District 7

• GFA: 72,000 sm

• Superstructure U/C. Leasing underway.

• To open in 2014

Sunrise City Phase 2

• District 7

• GFA: 25,000 sm

• Superstructure U/C.

• To open in 2015

SSG Tower

• District 3

• GFA: 20,500 sm

• Superstructure U/C.

• To open in 2015

HCMC HANOI

Mo Market

• Hai Ba Trung District

• GFA: 24,300 sm

• Fitting out.

• To open in 2014.

Ho Guom Plaza

• Ha Dong District

• GFA: 23,400 sm

• Completed. Leasing.

• To open in 2014.

Lotte Hanoi Center

• Ba Dinh

• GFA: 20,000 sm

• Completed. Leasing.

• Opened in Sep 2014.

Ciputra Mall Hanoi

• Tay Ho

• GFA: 130,000 sm

• Under planning.

• To open in 2015

Aeon Mall

• Long Bien district

• GFA: 108,000 sm

• Under construction.

• To open in 2015

Vincom Nguyen

Chi Thanh

• Dong Da

• GFA: 65,400 sm

• Under construction.

• To open in 2015

Source: CBRE Vietnam, Q2 2014.

22 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Ho Chi Minh

City

Hanoi

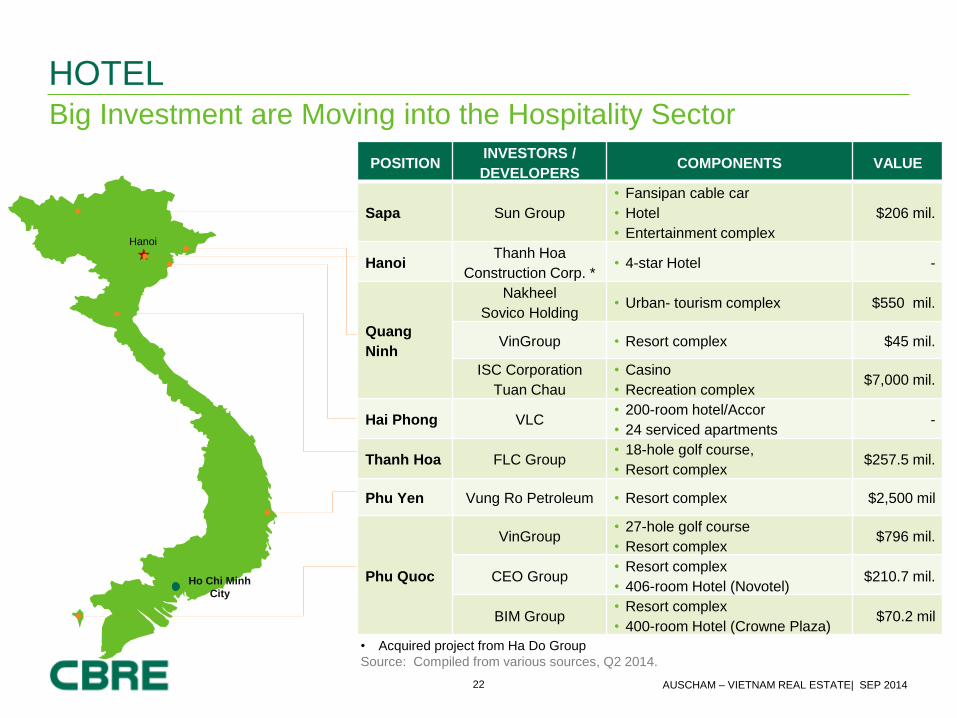

HOTEL Big Investment are Moving into the Hospitality Sector

• Acquired project from Ha Do Group

Source: Compiled from various sources, Q2 2014.

POSITION INVESTORS /

DEVELOPERS COMPONENTS VALUE

Sapa Sun Group

• Fansipan cable car

• Hotel

• Entertainment complex

$206 mil.

Hanoi Thanh Hoa

Construction Corp. * • 4-star Hotel -

Quang

Ninh

Nakheel

Sovico Holding • Urban- tourism complex $550 mil.

VinGroup • Resort complex $45 mil.

ISC Corporation

Tuan Chau

• Casino

• Recreation complex $7,000 mil.

Hai Phong VLC • 200-room hotel/Accor

• 24 serviced apartments -

Thanh Hoa FLC Group • 18-hole golf course,

• Resort complex $257.5 mil.

Phu Yen Vung Ro Petroleum • Resort complex $2,500 mil

Phu Quoc

VinGroup • 27-hole golf course

• Resort complex $796 mil.

CEO Group • Resort complex

• 406-room Hotel (Novotel) $210.7 mil.

BIM Group • Resort complex

• 400-room Hotel (Crowne Plaza) $70.2 mil

23 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

INVESTMENT TRENDS Foreign to Local

IFC helps build more homes for mid-

income earners in Vietnam

Source: Compiled from various newspapers.

24 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

Local to Local

INVESTMENT TRENDS

Source: CBRE Vietnam.

27 TRUONG CHINH

8X THAI AN

GALAXY 9 ICON 56 LEXINGTON

RESIDENCE

GREEN CITY

• Scale: 608 condos

• Location: HCMC

• Seller: Kim Tam Hai

• Scale: 196 condos

• Location: HCMC

• Seller: Dat Lanh

• Scale: 7.5 ha

• Location: HCMC

• Seller: N/A

• Scale: 1,334 condos

• Location: HCMC

• Seller: Hoa Binh

• Scale: 312 condos

• Location: HCMC

• Seller: Hoa Binh

• Scale: 627 condos

• Location: HCMC

• Seller: Hoa Binh

WATER GARDEN SUNVIEW TOWN

• Scale: 2.1 ha

• Location: HCMC

• Seller: PPI

• Scale: ~1,200 condos

• Location: HCMC

• Seller: Savico Agent now becomes Developer

25 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

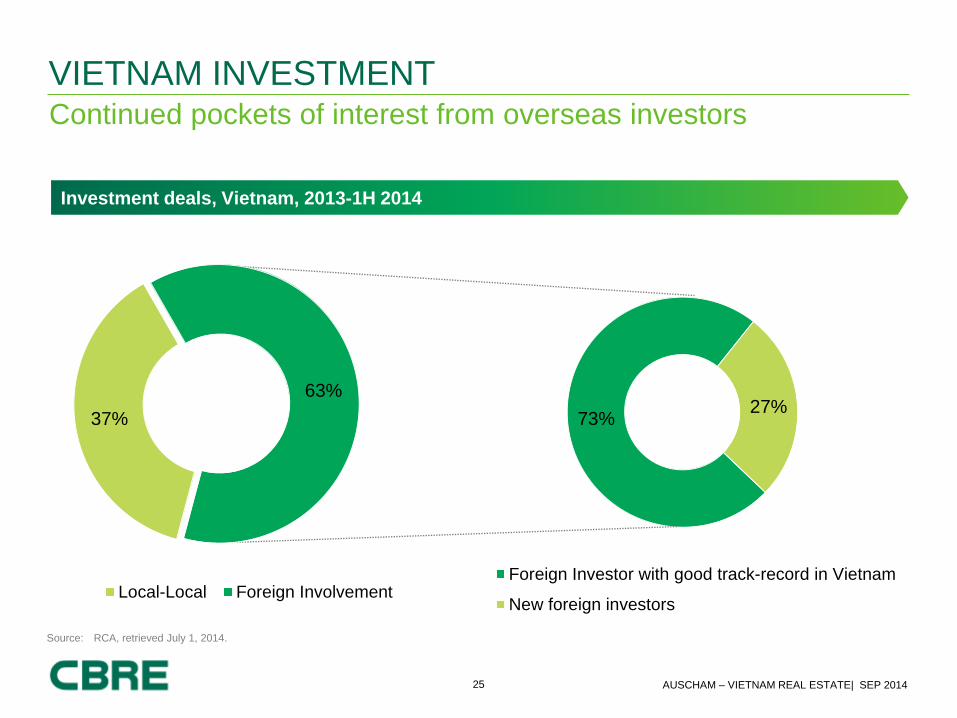

73% 27%

Foreign Investor with good track-record in Vietnam

New foreign investors

VIETNAM INVESTMENT Continued pockets of interest from overseas investors

Source: RCA, retrieved July 1, 2014.

37%

63%

Local-Local Foreign Involvement

Investment deals, Vietnam, 2013-1H 2014

VIETNAM REAL ESTATE MARKET OUTLOOK

27 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

The Good…..

VIETNAM REAL ESTATE MARKET

Macro-economic and Infrastructure

Macro-economic statistics and fundamentals, all

appear to be in good shape.

Infrastructure continues to amaze

SOE equitisation is moving ahead, slowly.

Residential

Affordable housing is still grabbing the

headlines.

Other developers are dusting off their old

Residential and Township plans.

More cranes to be seen on both sides of Hanoi

Highway (HCMC) and the Red River (Hanoi).

As pricing is coming down, people can move

up to the next quality bracket.

The mid- to high-end markets will receive more

end-users while the high-end segment will see

buy-to-let investors coming back.

28 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

The Good…..

VIETNAM REAL ESTATE MARKET

Office

Very few new entrants to the Vietnam market;

however, there are a noticeable number of up-

graders and re-inforcers.

Under revised Real Estate Law, strata-title

opportunities will open up more transactions.

However, this will require strong DMCs (shared

responsibilities amongst the owners).

The evolution of the modern workplace

29 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

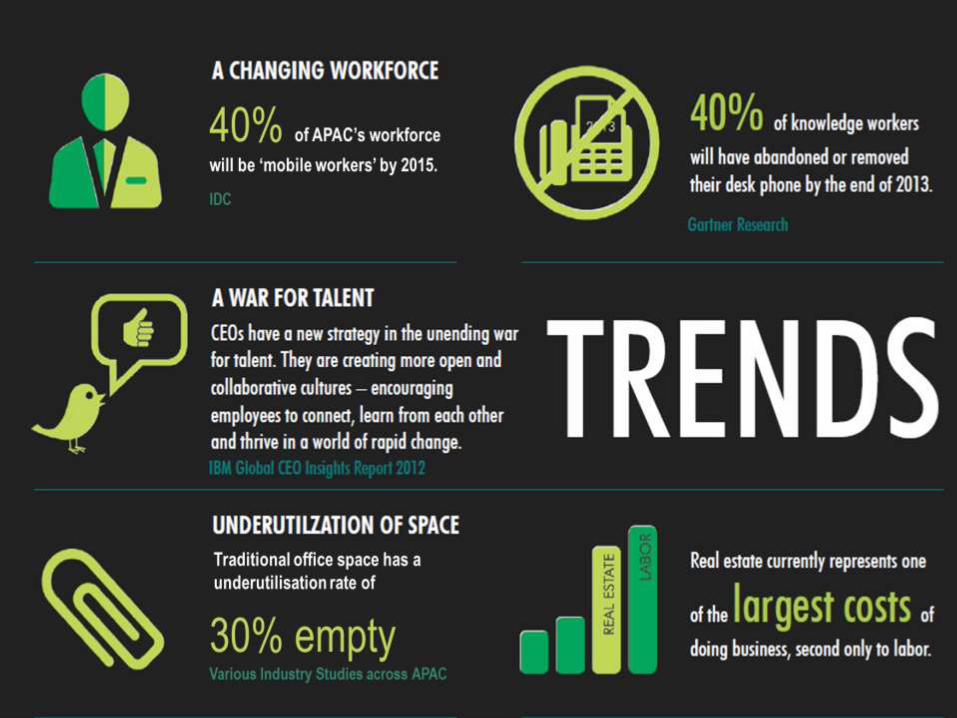

The World is Changing.

CBRE | Workplace Strategy 29

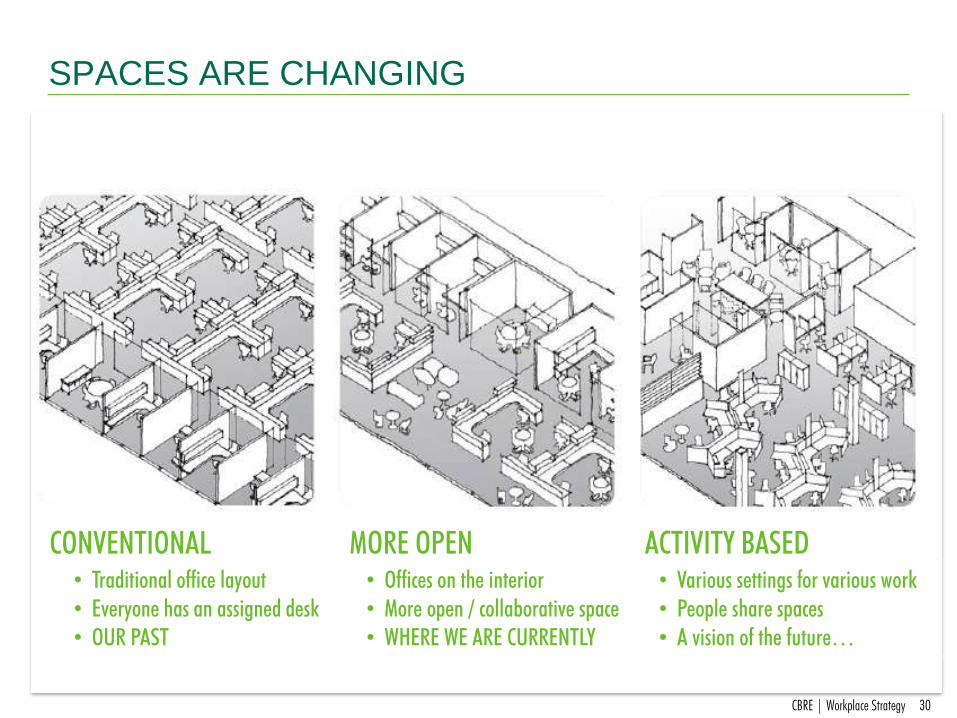

30 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

CONVENTIONAL MORE OPEN ACTIVITY BASED

• Traditional office layout

• Everyone has an assigned desk

• OUR PAST

• Offices on the interior

• More open / collaborative space

• WHERE WE ARE CURRENTLY

• Various settings for various work

• People share spaces

• A vision of the future…

CBRE | Workplace Strategy 30

SPACES ARE CHANGING

31 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

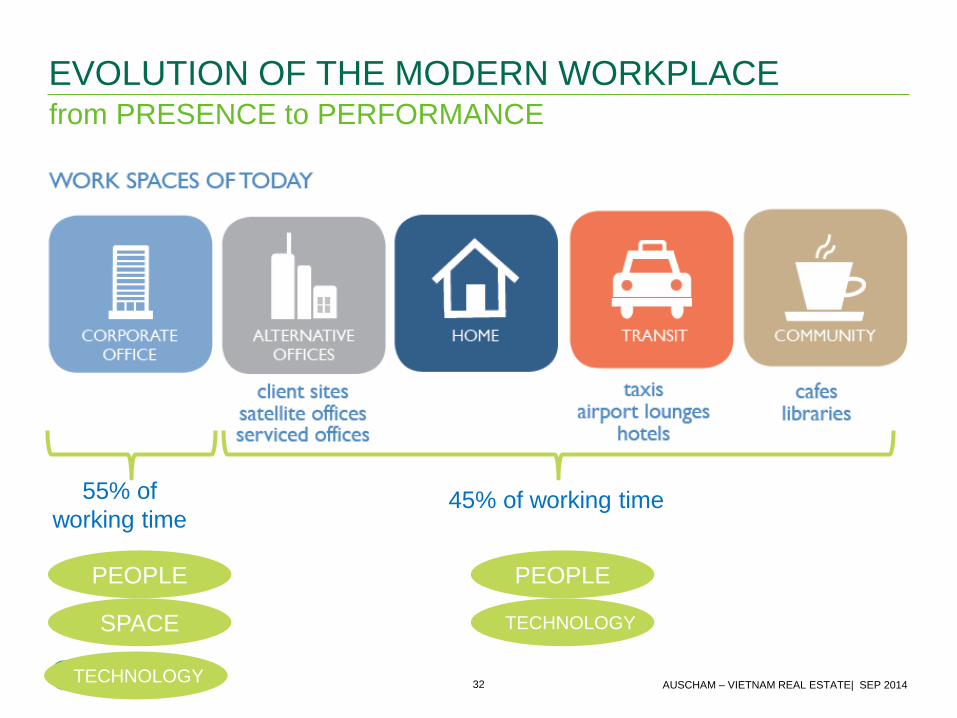

EVOLUTION OF THE MODERN WORKPLACE

EVOLUTION Maximize the opportunities for

INFORMATION EXCHANGE

32 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

from PRESENCE to PERFORMANCE

EVOLUTION OF THE MODERN WORKPLACE

WORKPLACE EVOLUTION

55% of

working time 45% of working time

PEOPLE PEOPLE

SPACE TECHNOLOGY

TECHNOLOGY

33 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

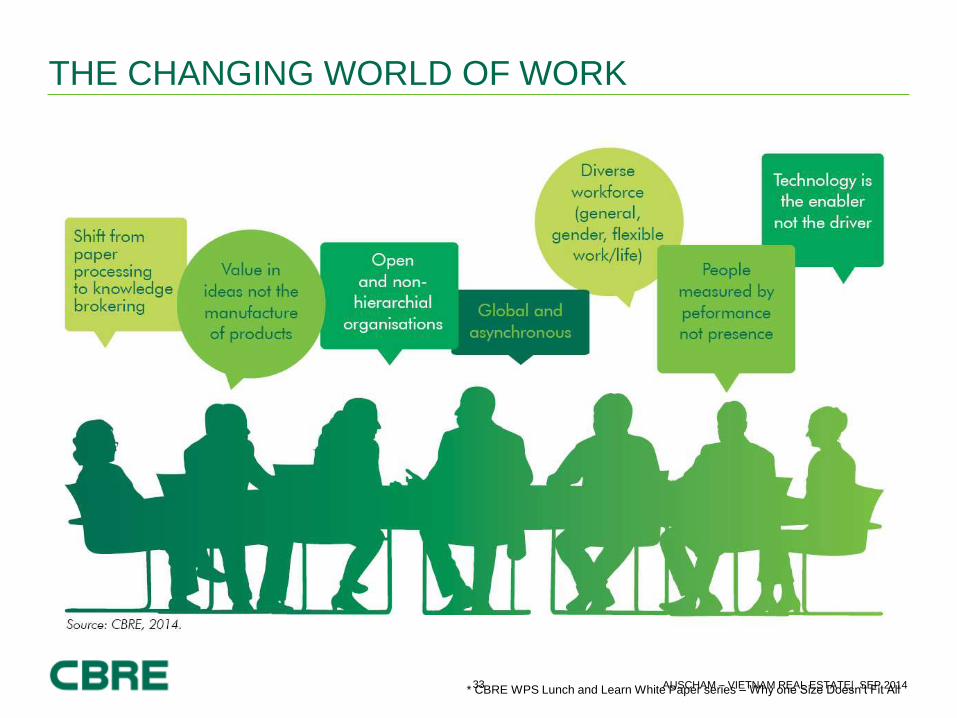

THE CHANGING WORLD OF WORK

* CBRE WPS Lunch and Learn White Paper series – Why one Size Doesn’t Fit All

34 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

The result : improving our efficiency

Reduction in overall space

Right size in the right location

Greater variety of spaces types to work in

More collaborative space

More AV / telepresence

Less on site storage

… and managing our costs

35 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

The Good…..

VIETNAM REAL ESTATE MARKET

Investment

Funds continue to dispose of their assets but also be

interested in acquiring well-priced assets.

Local and foreign buyers are STILL looking but not finding

well-priced assets.

Still a Tale of Two Cities.

Hospitality

Edward Snowden to go on holiday in Phu Quoc as

the Russians keep coming.

Coastal cities would be interesting but again, can

developments come at the right price?

Retail

Retail market has more confidence and supply

Foreign retail developers with modern, tried and tested

international concepts will create even more competition for

struggling local retail formats

International retailers will pay more attention as Vietnam will

open completely its market in January 2015 under WTO

obligations.

36 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

…..and the bad.

VIETNAM REAL ESTATE MARKET

TPP will not happen until 2015 at the

earliest. The EU FTA will happen

first.

Other Asia Pacific countries will put

their own relationship with China

before supporting Vietnam in the East

Sea (including the US).

“Bitten off more than you can chew?”

– perhaps the continued glut of office

space in Hanoi and the unfinished

buildings in HCMC.

No real investment urgency in the

market.

Prime-location projects stay still or

convert into other land-use purpose.

37 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

AT CBRE, WE LIVE AND BREATHE THE BUSINESS OF REAL ESTATE

Every quarter

QUARTERLY REPORT

Ad-hoc

VIEWPOINT & SPECIAL REPORT

38 AUSCHAM – VIETNAM REAL ESTATE| SEP 2014

AT CBRE, WE LIVE AND BREATHE THE BUSINESS OF REAL ESTATE

Every week

NEWSPAPER UPDATE

Every month

DASHBOARD

Every quarter

MARKETVIEW

Hanoi Vietnam Vietnam Vietnam

All materials presented in this report, unless specifically indicated otherwise, is under copyright and proprietary to CBRE. Information contained herein, including projections, has been obtained from materials and sources believed to be reliable at the date of publication. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. Readers are responsible for independently assessing the relevance, accuracy, completeness and currency of the information of this publication. This report is presented for information purposes only, exclusively for CBRE clients and professionals, and is not to be used or considered as an offer or the solicitation of an offer to sell or buy or subscribe for securities or other financial instruments. All rights to the material are reserved and none of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party without prior express written permission of CBRE. Any unauthorised publication or redistribution of CBRE research reports is prohibited. CBRE will not be liable for any loss, damage, cost or expense incurred or arising by reason of any person using or relying on information in this publication.