Embed Size (px)

DESCRIPTION

It does not take much to see that Vietnam is in the midst of a resurgent real estate market. From Hanoi in the north to Ho Chi Minh City (HCMC) in the south (which together comprise about 85% of the market1 ) and Danang in between, there appears to be construction underway on every corner. Vietnam has experienced robust development cycles in the past, with real estate being one of the preferred avenues for investment – despite the fact that reasonably priced property is in finite supply. Is what we are currently seeing the start of a new bubble? Or have the changes that have occurred created a market that is more fundamentally sound?

Citation preview

VinaCapital Real Estate Report

Overview of Current Property Market and Future Trends

www.vinacapital.com

VinaCapital Real Estate Report

2

October 2015

HAS VIETNAM’S REAL ESTATE MARKET TURNED A CORNER?

It does not take much to see that Vietnam is in the midst of a resurgent real estate

market. From Hanoi in the north to Ho Chi Minh City (HCMC) in the south (which

together comprise about 85% of the market1) and Danang in between, there appears to

be construction underway on every corner. Vietnam has experienced robust

development cycles in the past, with real estate being one of the preferred avenues for

investment – despite the fact that reasonably priced property is in finite supply. Is what

we are currently seeing the start of a new bubble? Or have the changes that have

occurred created a market that is more fundamentally sound?

In short, we believe that the real estate market is indeed at the onset of an early stage

recovery. Driven largely by Vietnam’s domestic growth story and progress in

restructuring the economy, the recent developments in the market are undoubtedly

positive. However, there remain a number of areas that require further attention and

reform if Vietnam is going to truly grow a sustainable real estate market.

Residential: Solid demand across all segments, but what about supply?

The last economic downturn brought the real estate sector to a standstill and halted a

number of ongoing development projects. At their 2008 peak2, average asking prices

(USD) across all residential real estate segments were about 29% higher than today,

while mortgage rates were about 3x higher3. For Vietnamese buyers, prices were out of

reach for most, while foreigners were forbidden from purchasing properties. All of this

stands in stark contrast to today’s real estate market, where prices and unit sizes have

decreased, commercial lending has resumed, there is increasing availability of

mortgages4, and changes in law that in principle open up the market to foreign buyers.

The residential sector constitutes approximately 85% of the real estate market5. HCMC

and Hanoi had a record number of condominium launches in 3Q15. Compared to

regional peers, Vietnam still offers bargains, being generally less expensive across all

segments, with the exception of luxury (USD3,000-5,000/m2) in HCMC6, which is priced

just below Jakarta but still well below Bangkok (see Graph 1).

1 VinaCapital research, Sep 2015

2 CIMB, Navigating Vietnam, Jan 2015

3 Ibid

4 CIMB, Vietnam’s Largest Property Developer, July 2015

5 VinaCapital research, Sep 2015

6 CBRE, HCMC Market Insight, Sep 2015

Stable macro

fundamentals, virtually

no inflation and

foreign direct

investment (FDI)

contribute to the

country’s resurgence

and our confidence in

Vietnam’s domestic

growth story.

Condo asking prices in

HCMC and Hanoi are

lower relative to major

cities within Southeast

Asia.

3

Graph 1: Primary asking price (USD/m2)

Source: CBRE

High-end vs. low-end supply

Renewed interest in real estate investment has been stimulated by several signature

high-end and luxury condominium developments near the central business district

(CBD) in HCMC as well as lower interest rates that allow rental yields to offer a higher

return than government bonds. Similar high-end projects are launching in districts

adjacent to the CBD where many expats and wealthy Vietnamese reside. HCMC has

about 18,000 new units launching in the next 2-3 years7 which we believe could lead to

oversupply in the short term.

With the CBDs being out of reach for most home buyers, the most popular

developments are nearby (such as Novaland’s Sunrise City and Vingroup’s Vinhomes

Central Park); in close proximity to FDI parks like the new Samsung development in

Saigon Hi-Tech Park; or adjacent to newly built or soon to be completed infrastructure,

such as HCMC’s metro line 1 (Thao Dien Investment’s Masteri Thao Dien). This has

shifted residential growth in both HCMC and Hanoi, to the east and south, and south

and west, respectively.

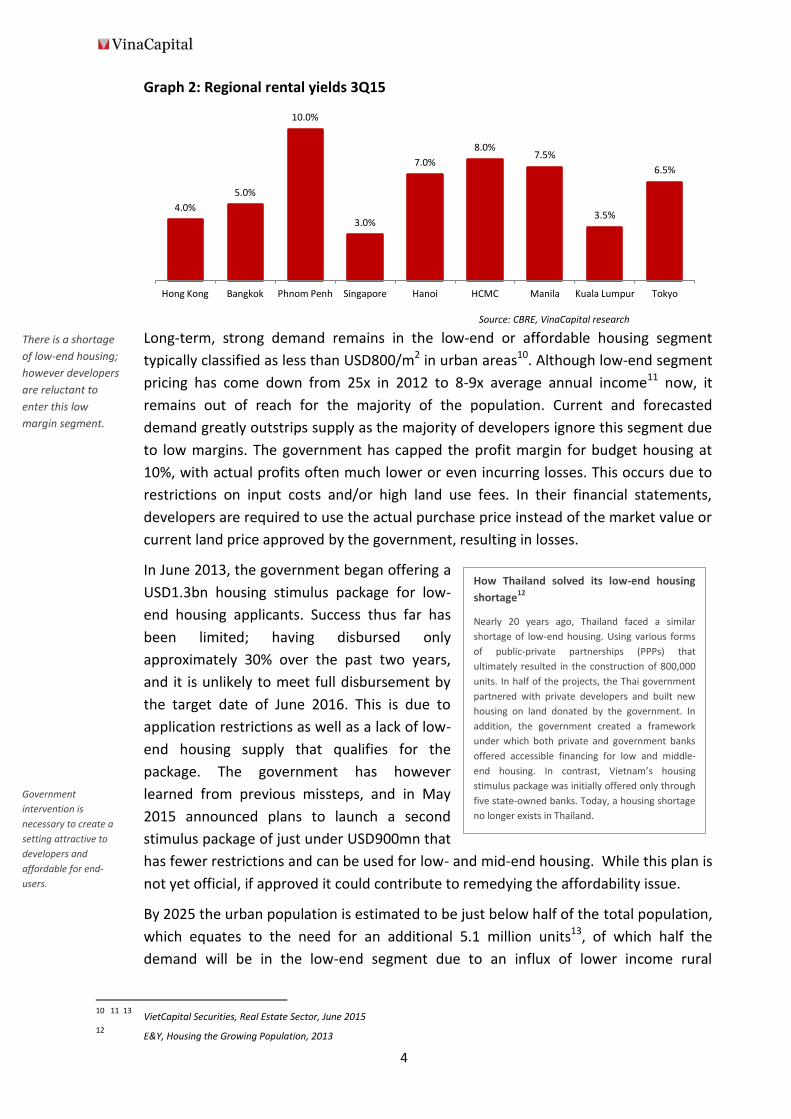

An estimated 25% of high-end and luxury purchases are done so as rentals8, as yields in

Vietnam are 1.5x-2.5x higher than Hong Kong, Bangkok and Singapore9 (see Graph 2).

Questions remain about the depth of demand since most activity is in the high-end.

7 VietCapital Securities, Real Estate Sector, June 2015

8 Ibid

9 CBRE, Finding Opportunities in a Changing Market, Sep 2015

-

2,000

4,000

6,000

8,000

Hanoi HCMC Phnom Penh Manila Jakarta Bangkok

Luxury High-end Mid-end Affordable

4

Graph 2: Regional rental yields 3Q15

Source: CBRE, VinaCapital research

Long-term, strong demand remains in the low-end or affordable housing segment

typically classified as less than USD800/m2 in urban areas10. Although low-end segment

pricing has come down from 25x in 2012 to 8-9x average annual income11 now, it

remains out of reach for the majority of the population. Current and forecasted

demand greatly outstrips supply as the majority of developers ignore this segment due

to low margins. The government has capped the profit margin for budget housing at

10%, with actual profits often much lower or even incurring losses. This occurs due to

restrictions on input costs and/or high land use fees. In their financial statements,

developers are required to use the actual purchase price instead of the market value or

current land price approved by the government, resulting in losses.

In June 2013, the government began offering a

USD1.3bn housing stimulus package for low-

end housing applicants. Success thus far has

been limited; having disbursed only

approximately 30% over the past two years,

and it is unlikely to meet full disbursement by

the target date of June 2016. This is due to

application restrictions as well as a lack of low-

end housing supply that qualifies for the

package. The government has however

learned from previous missteps, and in May

2015 announced plans to launch a second

stimulus package of just under USD900mn that

has fewer restrictions and can be used for low- and mid-end housing. While this plan is

not yet official, if approved it could contribute to remedying the affordability issue.12

By 2025 the urban population is estimated to be just below half of the total population,

which equates to the need for an additional 5.1 million units13, of which half the

demand will be in the low-end segment due to an influx of lower income rural

10

11 13

VietCapital Securities, Real Estate Sector, June 2015 11

12 E&Y, Housing the Growing Population, 2013

13

4.0%

5.0%

10.0%

3.0%

7.0%

8.0% 7.5%

3.5%

6.5%

Hong Kong Bangkok Phnom Penh Singapore Hanoi HCMC Manila Kuala Lumpur Tokyo

How Thailand solved its low-end housing

shortage12

Nearly 20 years ago, Thailand faced a similar

shortage of low-end housing. Using various forms

of public-private partnerships (PPPs) that

ultimately resulted in the construction of 800,000

units. In half of the projects, the Thai government

partnered with private developers and built new

housing on land donated by the government. In

addition, the government created a framework

under which both private and government banks

offered accessible financing for low and middle-

end housing. In contrast, Vietnam’s housing

stimulus package was initially offered only through

five state-owned banks. Today, a housing shortage

no longer exists in Thailand.

There is a shortage

of low-end housing;

however developers

are reluctant to

enter this low

margin segment.

Government

intervention is

necessary to create a

setting attractive to

developers and

affordable for end-

users.

5

migrants. Social housing (about USD150-300/m2) is an alternate solution, but similar to

affordable housing has a low margin and has yet to attract a critical mass of

developers14. It will be important for the State to help create the right environment for

low-end development via policy changes and economic incentives that both ensure

adequate affordable housing supply and higher returns for private developers in this

sector.

Key players in the market

Local developers continue to dominate the market. The three largest players, Vingroup,

Novaland and Bitexco, have secured over 25 development sites year to date15.

Vingroup has made some of the highest profile acquisitions with their purchase of

state-owned enterprise (SOE) properties such as Saigon port in HCMC and Vietnam

Exhibition Fair Centre in Hanoi, which have been rezoned for residential and

commercial development. M&A activity has also played a role in this consolidation,

with larger local players acquiring development sites from weaker ones.

It appears that local developers can more seamlessly complete projects and cater to

the needs of the market over the long term. They also appear to have an advantage in

their ability to get government approvals quicker, not only due to their experience in

navigating the bureaucracy but also because they will often contribute infrastructure

improvements such as road and expressway upgrades and expansions, which is a key

government priority. This not only assists the government in meeting aggressive

infrastructure goals but also has the added benefit of providing the new developments

with immediate access, an important benefit in a country where projects can be

delayed due to inadequate infrastructure.

To finance expansion, Vingroup and Novaland have turned abroad for additional

fundraising solutions as it has become more difficult to raise money in the local market.

Vingroup has raised USD300mn from Warburg Pincus since 2013 to finance its retail

segment, while Novaland held a USD47mn convertible debt offering in June, in which

VinaCapital participated for USD15mn. Although Vingroup is among the top three

highly leveraged listed developers with a 1.24 debt/equity ratio as of June 201516, it has

not yet warranted market concern. It has the highest profile of the development

companies, having delivered high-end residential, shopping malls, Grade A offices and

five star resorts in record time. The Vinpearl hotel in Phu Quoc boasts 750 rooms – the

largest hotel on the island – in addition to an entertainment area and golf course, and

was completed in just 10 months. Typically, projects of that magnitude take up to 24

months17.

Some foreign developers, namely Singapore’s Keppel and CapitaLand, have successfully

entered the market, and their projects have seen solid demand due in large part to the

perceived high quality of their properties. But foreign developers still face significant

14

15

VinaCapital research, Sep 2015 15

16 Capital IQ

17 VinaCapital research, Sep 2015

Domestic financing is

limited and larger local

players have gone

abroad for fundraising.

6

challenges in the country, including disputes with local partners and contractors, and

slower approvals by the authorities, all of which can ultimately result in projects being

less profitable. Opportunities remain for foreign developers, however, that can bring

expertise and are a known brand, although to be successful, having the right local

partner is crucial. An alternative path for foreign investors is to do club deals, such as

GAW Capital’s (Hong Kong) recent acquisition of Indochina Plaza Hanoi, Hyatt Regency

Danang and Indochina Riverside Tower Danang from Indochina Land18.

Foreign Housing Law Reform: A good start, but more to be done

The recent significant change in laws to allow individual foreign investors to buy

property has generated a great deal of excitement in the industry, and was seen as a

catalyst for massive growth. While there is upside potential in the longer term, we see

little impact in the short term, as the market is awaiting the appropriate legal

framework.

Thus far, there has been no significant uptick in sales

to foreigners, due primarily to a number of barriers

that have been identified in the reformed law as it

currently stands, including restrictions on the

duration of mortgages, inequitable rules with respect

to the sale of property to foreign versus Vietnamese

buyers, and restrictions on repatriating sales profits.

Until these and related issues are resolved by further

reforms, significant foreign buying will likely not occur for another six to twelve

months, despite the HCMC Real Estate Association’s view that the new law offers a

level playing field for foreigners and locals.

Foreigners make up about 1% of the residential real estate market19. Most foreign

buyers are from Asia and have some tie to Vietnam, such as expatriates (Koreans are

the largest segment followed by Japanese) and Viet Kieu, with an estimated 500,000 to

1 million said to be interested in purchasing property that will enable them to retire in

their homeland20.

Nevertheless, headlines focus on strong sales to foreigners – despite the fact that it is

not yet feasible. Developers are running aggressive sales programs, although that has

resulted in few sales to foreigners, and brokers like Savills and JLL are not yet offering

consultancy services to foreigners at this time21. At this stage, foreign buyers can only

make reservations for property by putting down a minimal deposit. Despite this, there

does appear to be a higher level of foreign interest in purchasing property – once issues

are addressed. Thus far, the greatest interest is in the high-end segment, and in HCMC,

foreigner interest is focused in the south and along metro line 1. According to CBRE,

18

CBRE, HCMC Market Insights, Q3 2015, October 2015 19

20 21

VinaCapital research, Sep 2015

21

Minimal impact in the

short term due to lack

of a guiding circular,

but strong upside from

expats, Viet Kieu and

regional investors once

issues are addressed.

Key changes in the Foreign Housing Law

Foreigners with valid visas can buy property.

Limited to 30% of units in condo or 250 homes in a ward. No limit for Viet Kieu (overseas Vietnamese).

Foreign invested companies and rep offices allowed to purchase residential property.

Properties can be subleased, traded, inherited and used as collateral.

Foreign invested companies can acquire and own a completed building for their own use.

7

the Vinhomes Central Park launch event earlier this year resulted in 120 reservations

from foreigners.

The new law on foreign property ownership is also expected to generate some activity

in the industrial and commercial sectors as foreign invested companies and

representative offices are able to purchase new and existing facilities if they are

purchased for owner occupation.

Office: Strong demand prevails in HCMC, softer in Hanoi

Over the next two years, HCMC will continue to experience a shortage of large office

space and limited Grade A office buildings, at least until 2017-18, when Deutsches Haus

(the first LEED platinum-designated building in Vietnam), The One and Saigon Centre

(phase 2) are released, resulting in approximately 95,000 m2 of new space22. One global

broker has said that it has received inquiries from multinationals seeking expansion

and/or relocation for double the amount of square meters than is usual. In the

medium to long-term, there is a shortage of land in the CBD so some degree of

decentralisation is to be expected.

In Hanoi, no new Grade A office buildings will launch in the CBD this year, although TNR

Tower, which is 15 minutes from the CBD, will launch by year-end, adding 56,000 m2 of

Grade A space23. There is currently an excess supply of Grade A & B office in Hanoi, a

dynamic we see persisting in the mid-term; this will likely lead to rental declines. Many

of Hanoi’s new developments are located on the fringe of the city centre or nearby

newer suburban areas, resulting in a further decentralised CBD.

A limited supply of available land to create core CBDs will be a complication in Tier 1

and Tier 2 cities due to the challenge of amalgamating plots of land. High population

density and generational occupation of sites are key factors contributing to this

challenge, which are unlikely to be resolved in the near term as the government is

reluctant to offer competitive land compensation and initiate clearance at the risk of

social unrest that can arise from relocating large numbers of residents. The challenge

for the State will be to develop a framework for cohesive development in major cities,

one that ensures an ample supply of quality office buildings to meet the tenancy needs

of multinational and domestic enterprises.

Thu Thiem: A possible solution

Just across the Saigon River from the CBD in District 1

sits the 657ha Thu Thiem New Urban Area. In the

planning phase for more than a decade, the land has

been cleared and is ready for development. Already

built are a tunnel and bridge (with more under

construction), which connect the area to the CBD, and

22

CBRE, Vietnam Real Estate- Time to Recalibrate, July 2015 23

Ibid

Hanoi Grade A vacancy

rates are 2.4x more

than HCMC.

Thu Thiem New Urban Area Photo credit: Son Dang

8

yet the space remains essentially undeveloped. How can this extremely unique asset –

few up-and-coming megacities have this much greenfield space in a central location –

be best leveraged? Initially, development plans made parallels to developing Thu Thiem

into a financial centre similar to Pudong in Shanghai or Canary Wharf in London. In our

view, Thu Thiem should be marketed as an integrated, mixed-use district, offering

convenience, easy access and modern infrastructure.

A number of projects are slated to begin construction by year-end or have just broken

ground such as Empire City, which will feature the tallest building in Vietnam as the

centrepiece of a complex that will also include a luxury shopping centre, five-star hotel,

and a condominium. Completion of the full project is expected in 202224. Leasing

prices in Thu Thiem are expected to be substantially lower than the CBD, although it

remains too early to gauge the impact on the market. Time is of the essence: three

mixed-use projects on the existing CBD side of the river have been approved (although

they have yet to begin land clearance); these could create an excess supply of property

in the pipeline, which could discourage the launch of new projects in Thu Thiem.

Retail: Favourable demographics driving growth

The grocery, hypermarket and fast-moving consumer goods (FMCG) retail sectors have

benefitted from Vietnam’s growth and burgeoning middle class. GDP per capita has

increased about 75% from 2008-2014, comparable to Thailand 20 years ago, and

Indonesia and the Philippines 5-7 years ago25. GDP has increased each year since 2012,

and coupled with a marked increase in consumer confidence, retail expansion has

accelerated. International retailers are taking notice of these trends and are steadily

entering the market, leading to a high demand for space, particularly in the CBD. In the

short-to-medium term, supply of retail space will be stable, with shopping malls being

built in both urban and suburban areas. By 2020, retail space in HCMC will be double

from what exists today.

Nevertheless, success for retail developers has been hit-or-miss. Large format, Western

style malls have faced challenges in attracting large numbers of Vietnamese consumers

outside of the cinema and restaurants. Parkson, a Malaysian department store that has

been operating in Vietnam for a decade, has also experienced difficulties, posting

losses and closing its store in Hanoi’s Landmark 72 tower in January26 as reported by

The Business Times in Singapore.

At the root of this dichotomy is the fact that Vietnamese still have relatively low

incomes, earning USD4,000/year27 on average, resulting in weak demand for the

heavily taxed, fixed price, high-end consumer goods that tend to be sold in large

shopping malls. One possible solution: A modified wet market, the traditional open-air

market with individual stalls selling fresh meat and produce. When adapted to suit

modern trade, this format features generic stalls offering a range of products at lower

24

VinaCapital research, Sep 2015 25

26

27

VinaCapital research, Sep 2015 26

27

Free Trade Agreements

remove tariffs, making

imported goods more

competitive, further

stimulating retail.

9

price points and allowing price negotiation, all in an enclosed, air-conditioned space.

Successful examples of this format include Saigon Square 3 and Taka Plaza 2 in HCMC.

M&A may drive some retail growth

Given that grocery, hypermarket, and FMCG sectors are the bright spots in retail, it is

little surprise that they have attracted the majority of M&A activity, with several

notable transactions this year as Vietnam’s attractive demographics and increasing

domestic consumption draw the attention of other Asian investors. Average volume

growth within retail and FMCG is projected at 7.5% over the next five years28.

Companies from Thailand, Korea and Japan have taken a long-term view of the market

and have been the most active investors.

Thailand’s Central Group was the first and among the most active foreign retail

investors in Vietnam, which is its first international foray. To date it has opened two

Robin’s department stores, with plans to open seven more in the next four years29. It

also acquired a significant stake in electronics retailer Nguyen Kim.

Another Thai company, Berli Jucker Public Company Limited (BJC), has entered into an

agreement to purchase Metro Cash & Carry’s (MCC) Vietnam operations, including 19

wholesale stores. German parent Metro Group is seeking to exit the market due to

intense local competition – one of just a handful of markets from which it has

withdrawn, further illustrating the challenges faced by some foreign companies in the

country. BJC previously took over the Family Mart convenience stores in Vietnam that

had been operated as part of a joint venture between the Japanese parent and a local

partner, and renamed those stores B’s Mart. While BJC has continued to expand B’s

Mart, Family Mart has also opened stores under its own name.

Japan’s Aeon Co Ltd acquired a 49% stake in Citimart and a 30% stake in Fivimart

grocery outlets30. Aeon also owns two malls in the south and plans to open another 18

malls nationwide by 2020. Vietnam is Aeon’s second most important market in

Southeast Asia after Malaysia.

Meanwhile, long time Vietnam player, Korean company Lotte, has increased the

number of stores it operates to 10, and is planning to open 50 more in the next five

years31.

Industrial: The main beneficiary of strong FDI inflows

With the manufacturing sector accounting for 70% FDI inflow (USD6.2bn through

7M1532), industrial parks (IPs) are some of the primary beneficiaries of this investment.

To date, IPs have offered one of the few significant opportunities for foreign real estate

28

PWC, 2015-16 Outlook for the Retail & Consumer Products Sector in Asia, Feb 2015 29

VietnamNet Bridge, “Thai companies invade Vietnamese market, push aside Chinese products”, Sep 2015 30

Deal Street Asia, “Aeon buys into Vietnam’s Fivimart & Citimart”, Jan 2015 31

Thanh Nien News, “Foreign retailers arrive en masse”, Oct 2015 32

VPBS, Vietnam Real Estate Industry, Aug 2015

Singapore is the

largest foreign investor

in the industrial

segment.

Foreign interest in

retail has been highest

from companies from

Thailand, Korea and

Japan.

10

investors due to extensive growth of the manufacturing sector (garments, footwear

and electronics). Vietnam’s attractive demographics and lower labour costs, which has

led to a number of companies to move production from China and/or create an

alternate manufacturing base. As industrial parks have grown, so too have adjacent

residential and retail developments.

To date, most industrial parks have been built in and around the two main cities, with

some development extending to Haiphong in the north and central Danang. Employees

come from districts located on the outskirts of the city where the IPs are located, while

some companies build housing for their workers. Provided infrastructure investment

occurs, particularly ports and roads, other coastal cities such as Can Tho and Vinh could

be prime locations for new industrial parks beyond HCMC and Hanoi as demand for

such space continues to grow.

One cautionary note we would sound is PMI declined in September to 49.5 due to a

reduction in new orders and a contraction in output. The PMI has not fallen below 50

since August 2013. Exports have also declined this year, affecting the country’s balance

of trade. Nevertheless manufacturers remain positive as employment increased during

the month. We are closely monitoring this issue to see how it further develops and

whether it is a signal of weakening global demand that might have larger ramifications

on the sector. That said, the passage and ratification of the Trans-Pacific Partnership

(TPP), and the increased production and exports it is expected to generate, should

drive continued, long-term growth in the sector.

Outlook: Real estate is moving in the right direction

We see upside potential across all segments of the real estate market, especially in

residential, Grade A office and industrial. Vietnam’s domestic growth story remains the

significant driver for the expansion of the real estate market: a rapidly expanding

middle class, urbanisation, rising income levels and increased consumption benefit the

overall economy, and the residential real estate segment in particular.

With HCMC on track to becoming a vibrant metropolis and business centre for the

ASEAN Economic Community (AEC), the demand for residential and integrated Grade A

office space will likely remain strong for the foreseeable future as a result. Investment

in the industrial segment remains solid as Vietnam has a competitive labour force and

stands to further benefit upon the removal of tariffs upon the implementation of TPP.

There remain a number of important issues that must be addressed in order to fully

capitalize on the market’s great potential, particularly those relating to low-end

residential supply and the Foreign Housing Law. More specifically, clearer policies and

procedures regarding FDI, zoning, and approvals will further enhance the real estate

sector. Provided these steps occur in the near term, we are reasonably optimistic that

Vietnam’s real estate market is heading in the right direction in a way that is more

sustainable and rational than at any time in recent memory.

The market awaits

significant market

catalysts including

foreign housing law

legislation, low-end

housing support and

TPP legislation.

TPP is expected to

continue strong

demand for industrial,

despite some short-

term issues that

warrant monitoring.

Residential, Grade A

office and industrial

are the most attractive

segments.

11

Disclaimer by VinaCapital

Copyright 2015 VinaCapital (VNC). All rights reserved. This report has been prepared and is being issued

by VNC or one of its affiliates for distribution in Viet Nam and overseas. The information herein is based

on public sources believed to be reliable. With the exception of information about VNC, VNC makes no

representation about the accuracy of such information. Opinions, estimates and projection expressed in

this report represent the current views of the author at the date of publication only. They do not

necessarily reflect the opinions of VNC and are subject to change without notice. VNC has no obligation

to update, amend or in any way modify this report or otherwise notify a reader thereof in the event that

any of the subject matter or opinion, projection or estimate contained within it changes or becomes

inaccurate. The information herein was obtained from various sources which we believe to be reliable

but we do not guarantee its accuracy or completeness.

Prices and availability of financial instruments are also subject to change without notice. This published

research may be considered by VNC when buying or selling proprietary positions or positions held by

funds under its management. VNC may trade for its own account as a result of short term trading

suggestions from its analysts.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to

make an offer, to buy or to sell any securities or any option, futures or other derivative instruments in

any jurisdiction. Nor should it be construed as an advertisement for any financial instruments. Officers of

VNC may have a financial interest in securities mentioned in this report or in related instruments. This

research report is prepared for general circulation and for general information only. It does not have

regard to the specific investment objectives, financial situation or particular needs of any person who

may receive or read this report. Investors should note that the prices of securities fluctuate and may rise

and fall. Past performance, if any, is no guide to the future.

The financial instruments discussed in this report may not be suitable for all investors. Investors must

make their own financial decisions based on their independent financial advisors as they believe

necessary and based on their particular financial situation and investment objectives. This report may

not be copied, reproduced, published or redistributed by any person for any purpose without the

express permission of VNC in writing. Please cite sources when quoting.