Embed Size (px)

Citation preview

U.S. Economic Outlook

Mark Vitner, Managing Director & Senior EconomistMarch 18, 2015

Economic Outlook 2

Five Critical Questions About the Economic Outlook

Overall Growth

Oil Prices Why have oil prices fallen so dramatically and what

does it tell us about the global economy and U.S. economic outlook?

Interest Rates Will the global economic slowdown and deflation

fears pull interest rates lower and keep the Fed on hold?

Housing Will 2015 be the year the housing recovery finally

gains traction?

GlobalEconomy

Just how sluggish is the global economy and what will it take to get Europe, Japan and China back on track?

How much of last year’s strong momentum will carry over into 2015?

Overall Growth

Economic Outlook 4

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2000 2002 2004 2006 2008 2010 2012 2014 2016

U.S. Real GDP Bars = CAGR Line = Yr/Yr Percent Change

GDP - CAGR: Q4 @ 2.2%

GDP - Yr/Yr Percent Change: Q4 @ 2.4%

Forecast

Economic Growth

Real GDP growth is expected to average close to

a 3 percent pace over the next few years.

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

Economic Outlook 55

Employment Situation

Job growth appears to have ratcheted up over the past year but wage gains have not. The improvement in job growth is evident across industries and regions.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Unemployment RateNonfarm Employment

-1,000

-800

-600

-400

-200

0

200

400

600

-1,000

-800

-600

-400

-200

0

200

400

600

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nonfarm Employment ChangeChange in Employment, In Thousands

Monthly Change: Feb @ 295K

0%

2%

4%

6%

8%

10%

12%

0%

2%

4%

6%

8%

10%

12%

65 70 75 80 85 90 95 00 05 10 15

Unemployment and Wage RatesWages for Production & Nonsupervisory Workers, SA

Unemployment Rate: Feb @ 5.5%Hourly Earnings - Yr/Yr % Change: Feb @ 1.6%

Economic Outlook 6

2%

6%

10%

14%

18%

2%

6%

10%

14%

18%

94 96 98 00 02 04 06 08 10 12 14

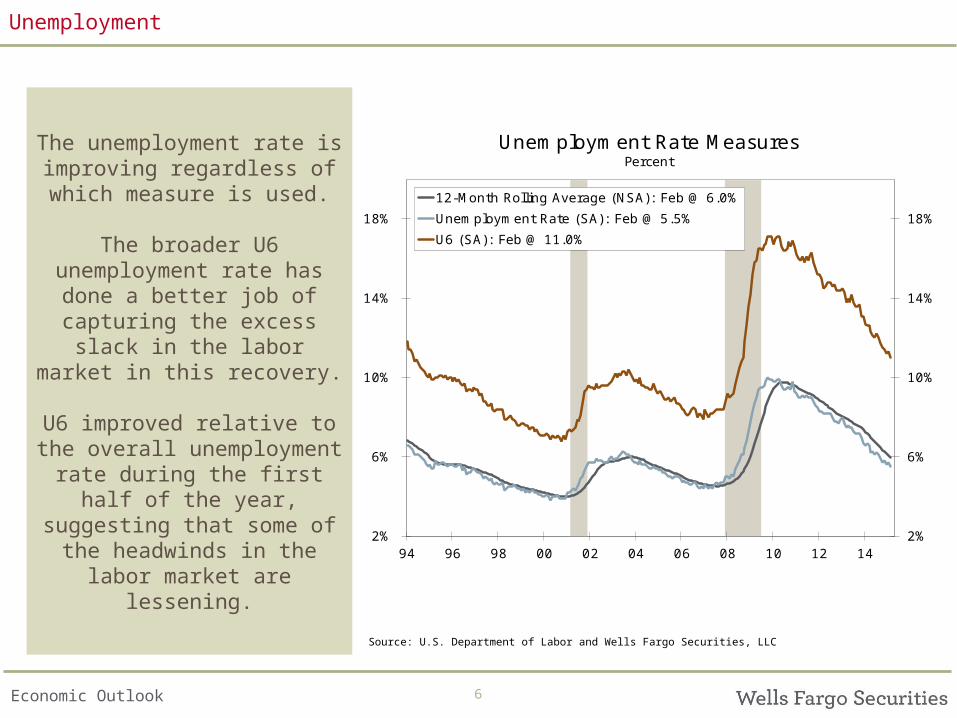

Unemployment Rate MeasuresPercent

12-Month Rolling Average (NSA): Feb @ 6.0%

Unemployment Rate (SA): Feb @ 5.5%

U6 (SA): Feb @ 11.0%

Unemployment

The unemployment rate is improving regardless of which measure is used.

The broader U6 unemployment rate has

done a better job of capturing the excess slack in the labor market in this

recovery.

U6 improved relative to the overall unemployment rate during the first half of the year, suggesting that some

of the headwinds in the labor market are lessening.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Economic Outlook 7

108

111

114

117

120

123

126

129

128

131

134

137

140

143

146

149

07 08 09 10 11 12 13 14 15

Th

ousa

nds

Th

ousa

nds

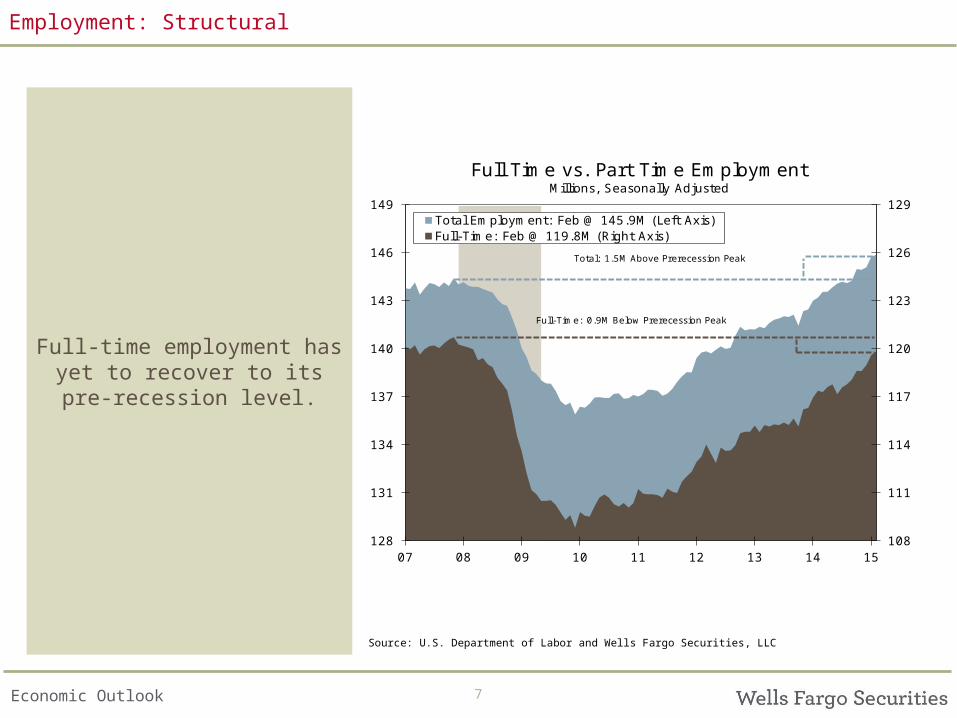

Full Time vs. Part Time EmploymentMillions, Seasonally Adjusted

Total Employment: Feb @ 145.9M (Left Axis)Full-Time: Feb @ 119.8M (Right Axis)

Total: 1.5M Above Prerecession Peak

Full-Time: 0.9M Below Prerecession Peak

Employment: Structural

Full-time employment has yet to recover to its pre-

recession level.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Oil Prices

Economic Outlook 99

Energy

Oil prices have collapsed in recent months and the number of active oil rigs has fallen sharply. We expect this trend to continue as companies slash capital

spending.

Source: IHS Global Insight, Baker-Hughes, U.S. Department of Energy, U.S. Department of Labor and Wells Fargo Securities, LLC

Production & EmploymentWTI

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Baker-Hughes Rig Count vs. Oil PricesOil Rotary Rigs; USD per Barrel

Oil Rig Count: Feb-27 @ 986 (Left Axis)WTI : Mar-06 @ $50.4 (Right Axis)

140

160

180

200

220

240

260

280

100

200

300

400

500

600

700

91 93 95 97 99 01 03 05 07 09 11 13 15

Oil Production vs. EmploymentThousands of J obs, Millions of Barrels per Month, 12-MMA

Oil & Gas Employment: Feb @ 640.9K (Left Axis)Oil Production: Dec @ 263.2M (Right Axis)

Interest Rates

Economic Outlook 1111

Inflation

Global disinflation has led more aggressive easing moves by the ECB and BOJ. We expect the Fed to look through this transitory slowdown, however, and raise the

federal funds rate.

Source: U.S. Department of Labor, IHS Global Insight and Wells Fargo Securities, LLC

Eurozone CPIU.S. CPI

-3%

0%

3%

6%

9%

12%

15%

-3%

0%

3%

6%

9%

12%

15%

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08 11 14

Headline CPIYear-over-Year Percent Change

CPI : J an @ -0.1%

-1%

0%

1%

2%

3%

4%

5%

-1%

0%

1%

2%

3%

4%

5%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Eurozone Consumer Price IndexYear-over-Year Percent Change

CPI : Feb @ -0.3%

Economic Outlook 12

0%

1%

2%

3%

4%

5%

6%

7%

0%

1%

2%

3%

4%

5%

6%

7%

00 02 04 06 08 10 12 14

10-Year Government Bond YieldsTreasury Yield, Average Government Bond Yield

Germany, J apan and UK Average: Mar @ 1.48%

United States: Mar @ 2.14%

Global Yields

Easing by central banks around the globe will likely keep downward pressure on U.S. interest rates and lead

to further dollar appreciation.

Source: IHS Global Insight and Wells Fargo Securities, LLC

Housing

Economic Outlook 14

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

Th

ousa

nds

Housing StartsMillions of Units

Multifamily StartsMultifamily ForecastSingle-family StartsSingle-family Forecast

Forecast

Housing

We continue to look for a gradual recovery in

homebuilding.

Apartment demand remains exceptionally strong but

supply is catching up with demand.

Single-family housing starts are beginning to ramp back

up. Gains will be more modest than in past building

cycles.

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

Global Growth

Economic Outlook 1616

Global

Slower global growth and a stronger dollar will likely be a drag on U.S. economic growth.

Source: International Monetary Fund, Bloomberg LP and Wells Fargo Securities, LLC

DollarGlobal Growth

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

1980 1985 1990 1995 2000 2005 2010 2015

Real Global GDP GrowthYear-over-Year Percent Change, PPP Weights

Wells Fargo ForecastIMF Forecast

Period Average

65

70

75

80

85

90

95

100

105

110

115

65

70

75

80

85

90

95

100

105

110

115

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

U.S. Trade Weighted Dollar Major IndexMarch 1973=100

Major Currency Index: Mar-06 @ 91.6

Economic Outlook 17

North Carolina & The Triangle

Economic Outlook

Large Metro Area’s Led The

State’s Recovery

The Triangle and Charlotte accounted for the bulk of the state’s job gains in the early part of the recovery. This past year saw gains broaden to other parts of the state.

Technology & Innovation

Technology & innovation are driving the state’s growth, which is fueling gains in urban areas. These new jobs also have relatively large multipliers, driving hiring in retailing and the leisure and hospitality sectors.

Manufacturing Is Making A Comeback

Industries are coming back to the U.S. and North Carolina. The new arrivals tend to be more capital intensive and require workers with advanced skills.

Commercial Real Estate

Demand for commercial real estate has steadily improved and construction has been slow to come back. Rising interest rates will present some challenges.

North Carolina remains one of the most attractive places in the nation to do business and live. Job growth has accelerated over the past year, led by tech and innovation.

Economic Outlook 18

Year-over-Year Percent Change in Personal Income: Q3 2014

U.S. = 3.9%

Greater than 4.5%

Less than 3.0%

4.0%–4.4%

3.7%–3.9%

3.0%–3.6%

WEST MIDWEST

NORTHEAST

SOUTH

AK5.9

HI4.1

WISD

OHNE

ND

MO

MN

MI

KS

INIL

IA

3.41.8

3.80.5

4.6

2.9

2.5

4.5

3.0

3.12.7

1.7CT 4.3

VT

RI

PA

NY

NJ

NH

ME

MA

4.2

3.5

3.8

3.1

4.4

3.3

3.8

3.6

WY

WA

UT

OR

NV

NM

MT

ID

COCA

AZ

4.8

5.1

4.4

4.7

4.0

4.5

4.2

5.3

5.34.2

4.0

TX

TN

SCOK

MS

LA

GA

FL

AR

AL

5.6

3.7

4.43.9

0.7

3.5

4.4

4.5

3.0

2.7

WV

VA

NC

MD3.1

3.0

3.7

3.74.1KY

4.1DE

DC4.2

Economic Outlook 1919

North Carolina

Employment growth has been broad-based in North Carolina. Professional services, technology and other knowledge industries are clear outperformers in

the state.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Employment by IndustryEmployment

-8%

-6%

-4%

-2%

0%

2%

4%

6%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

90 92 94 96 98 00 02 04 06 08 10 12 14

North Carolina Nonfarm Employment3-Month Moving Averages

QCEW: Yr/Yr Pct. Change: J un @ 2.3%North Carolina: J an @ 2.5%Household: Yr/Yr Pct. Change: J an @ 1.2% J anuary 2015

-2% 0% 2% 4% 6% 8%

Information

Other Services

Construction

Financial Activities

Leisure and Hospitality

Manufacturing

Prof. & Bus. Svcs.

Educ. & Health Services

Government

Trade, Trans. & Utilities

Total Nonfarm

North Carolina Employment Growth By IndustryYear-over-Year Percent Change, 3-MMA

Number of Employees

Less

More

Economic Outlook 20

-6.9%

-5.0%

-4.6%

-1.3%

0.2%

1.1%

2.3%

3.9%

4.0%

6.5%

7.9%

20.3%

20.8%

-15% 0% 15% 30%

Computer & Peripheral Equip. Manuf.

Communications Equip. Manuf.

Semiconductor & Electronic Component Manuf.

Scientific Research & Development

Telecommunications

Pharmaceuticals Manufacturing

California

Architectural & Engineering Services

Data Processing

Internet Publishing, Broadcasting & Search Portals

Computer Systems Design

Aerospace & Parts Manufacturing

Software Publishers

N.C. High-Tech Employment GrowthYear-over-Year Percent Change, 3-MMA, QCEW

J une 2014

North Carolina

Technology employment has led gains in North Carolina. Technology services have

outperformed manufacturing recently.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Economic Outlook 2121

North Carolina

North Carolina’s unemployment rate has fallen back in line with the national rate. Part of the drop is due to declining labor force participation, particularly outside

Raleigh and Charlotte.

Source: U.S. Department of Labor, Moody’s Analytics and Wells Fargo Securities, LLC

Labor Force ParticipationUnemployment

2%

4%

6%

8%

10%

12%

2%

4%

6%

8%

10%

12%

90 92 94 96 98 00 02 04 06 08 10 12 14

North Carolina vs. U.S. Unemployment RateSeasonally Adjusted

North Carolina: J an @ 5.4%

United States: Feb @ 5.5%

58%

62%

66%

70%

74%

78%

58%

62%

66%

70%

74%

78%

2000 2002 2004 2006 2008 2010 2012 2014

North Carolina Labor Force Participation RatesSeasonally Adjusted

Charlotte: Dec @ 63.2%Raleigh: Dec @ 65.8%North Carolina: Dec @ 59.8%

Economic Outlook 22

Asheville

Rocky Mount

Raleigh-Cary

Jacksonville

Wilmington

Charlotte

Durham-Chapel Hill

Greensboro

Goldsboro

Hickory

Burlington

Fayetteville

Winston-Salem

Greenville

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-1% 0% 1% 2% 3% 4% 5%

3-M

onth

Perc

ent

Change

Year-over-Year Percent Change

North Carolina Employment Growth: J an. 20153-Month Moving Averages

Population SizeLess than 200,000

200,000-500,000More than 500,000

Recovering Expanding

Contracting Decelerating

North Carolina

Growth in major metros has been strong this past year, with growth accelerating in

some of the metros more closely tied to the

manufacturing sector.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Economic Outlook 2323

North Carolina

Most of the improvement in the housing market has been in apartments, much of which is taking place in urban areas or along key transit corridors.

Source: U.S. Department of Commerce, CoreLogic and Wells Fargo Securities, LLC

Home PricesPermits

0

20

40

60

80

100

120

0

20

40

60

80

100

120

90 92 94 96 98 00 02 04 06 08 10 12 14

Thou

sand

s

Thou

sand

s

North Carolina Housing PermitsThousands of Permits, Seasonally Adjusted Annual Rate

Single-Family: J an @ 29,172Single-Family, 12-MMA: J an @ 35,227Multifamily, 12-MMA: J an @ 15,242

Single-Family Average (1998-2003): 62,968

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

90 92 94 96 98 00 02 04 06 08 10 12 14

Core Logic HPI : NC vs. U.S.Year-over-Year Percent Change

United States: J an @ 5.7%North Carolina: J an @ 3.5%

Economic Outlook 2424

North Carolina

Most of the population growth has come from North Carolina’s largest metros.

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

Metro Population GrowthPopulation Growth

0

40

80

120

160

200

240

0

40

80

120

160

200

240

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

North Carolina Population GrowthIn Thousands

-2K

-2K

2K

3K

5K

6K

9K

9K

12K

16K

20K

26K

77K

102K

-20% 0% 20% 40% 60% 80% 100% 120%

Rocky Mount

Hickory

Goldsboro

Burlington

Greenville

J acksonville

Winston

Fayetteville

Asheville

Greensboro

Wilmington

Durham

Raleigh

Charlotte

North Carolina MSA Population GrowthThousands

2010-2013

Economic Outlook 2525

Raleigh

Growth in Raleigh has been quite strong, although employment gains have slowed as of late. High tech employment has led the way in Raleigh.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Employment by IndustryEmployment

-6%

-4%

-2%

0%

2%

4%

6%

8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

91 93 95 97 99 01 03 05 07 09 11 13 15

Raleigh MSA Nonfarm Employment

QCEW: Yr/Yr Pct. Change: J un @ 3.9%Nonfarm: Yr/Yr Pct. Change: J an @ 3.9%Household: Yr/Yr Pct. Change: Dec @ 2.5%

3-Month Moving Averages

-3% 0% 3% 6% 9% 12%

Information

Other Services

Financial Activities

Manufacturing

Construction, Nat. Res. & Mining

Leisure and Hospitality

Educ. & Health Services

Government

Trade, Trans. & Utilities

Prof. & Bus. Svcs.

Total Nonfarm

Raleigh MSA Employment Growth By Industry

Number of Employees

Less

More

Year-over-Year Percent Change, 3-MMA

J anuary 2015

Economic Outlook 2626

Raleigh

Raleigh’s manufacturing employment had large upward revisions. Office employment has been boosted by strong gains in professional and business

services.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Office EmploymentManufacturing Employment

-15%

-10%

-5%

0%

5%

10%

-15%

-10%

-5%

0%

5%

10%

91 93 95 97 99 01 03 05 07 09 11 13 15

Raleigh MSA Nonfarm Employment

Manufacturing Employment: J an @ 3.9%Non-Manufacturing: J an @ 3.5%

Year-over-Year Percent Change

-8%

-4%

0%

4%

8%

12%

16%

-8%

-4%

0%

4%

8%

12%

16%

91 93 95 97 99 01 03 05 07 09 11 13

Raleigh MSA Nonfarm Employment

Office Employment: Dec @ 9.2%Non-office Employment: Dec @ 1.3%

Year-over-Year Percent Change

Economic Outlook 2727

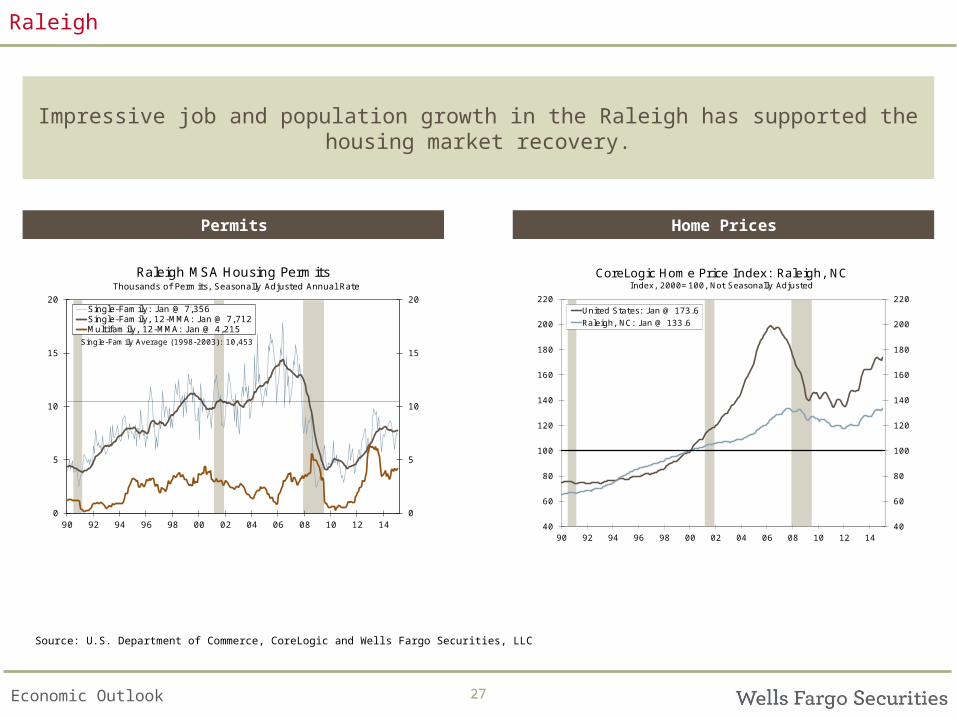

Raleigh

Impressive job and population growth in the Raleigh has supported the housing market recovery.

Source: U.S. Department of Commerce, CoreLogic and Wells Fargo Securities, LLC

Home PricesPermits

0

5

10

15

20

0

5

10

15

20

90 92 94 96 98 00 02 04 06 08 10 12 14

Thou

sand

s

Thou

sand

s

Raleigh MSA Housing Permits

Single-Family: J an @ 7,356Single-Family, 12-MMA: J an @ 7,712Multifamily, 12-MMA: J an @ 4,215

Single-Family Average (1998-2003): 10,453

Thousands of Permits, Seasonally Adjusted Annual Rate

40

60

80

100

120

140

160

180

200

220

40

60

80

100

120

140

160

180

200

220

90 92 94 96 98 00 02 04 06 08 10 12 14

CoreLogic Home Price Index: Raleigh, NCIndex, 2000=100, Not Seasonally Adjusted

United States: J an @ 173.6

Raleigh, NC: J an @ 133.6

Economic Outlook 2828

Durham

A revitalization of Durham’s downtown area has brought businesses and jobs back to the metro’s urban areas.

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Employment by IndustryEmployment

-12%

-8%

-4%

0%

4%

8%

12%

16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

91 93 95 97 99 01 03 05 07 09 11 13 15

Durham-Chapel Hill MSA Nonfarm Employment

3-Month Annual Rate: J an @ 0.1%Nonfarm: Yr/Yr Pct. Change: J an @ 1.9%Household: Yr/Yr Pct. Change: Dec @ 1.0%

3-Month Moving Averages

-2% 0% 2% 4% 6% 8% 10%

Information

Nat. Res. & Construction

Other Services

Financial Activities

Leisure and Hospitality

Manufacturing

Trade, Trans. & Utilities

Prof. & Bus. Svcs.

Educ. & Health Services

Government

Total Nonfarm

Durham-Chapel Hill MSA Employment Growth By Industry

Number of Employees

Less

More

Year-over-Year Percent Change, 3-MMA

January 2015

Economic Outlook 2929

Durham

Single-family permits continue to trek higher. Durham did not experience the same boom and bust cycle in housing as the rest of the nation.

Source: U.S. Department of Commerce, CoreLogic and Wells Fargo Securities, LLC

Home PricesPermits

0

1

2

3

4

5

6

0

1

2

3

4

5

6

90 92 94 96 98 00 02 04 06 08 10 12 14

Thou

sand

s

Thou

sand

s

Durham-Chapel Hill MSA Housing Permits

Single-Family: J an @ 1,980Single-Family, 12-MMA: J an @ 2,169Multifamily, 12-MMA: J an @ 1,073

Single-Family Average (1998-2003): 3,515

Thousands of Permits, Seasonally Adjusted Annual Rate

40

60

80

100

120

140

160

180

200

40

60

80

100

120

140

160

180

200

90 92 94 96 98 00 02 04 06 08 10 12 14

CoreLogic Home Price Index: Durham-Chapel Hill, NCIndex, 2000=100, Not Seasonally Adjusted

Durham-Chapel Hill, NC: J an @ 137.9

United States: J an @ 165.0

Economic Outlook 3030

Commercial Real Estate

Rapid population growth has caused an apartment boom. Retail has also benefitted, although not to the same extent.

Source: Reis, Inc. and Wells Fargo Securities, LLC

RetailApartments

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2%

4%

6%

8%

10%

12%

14%

2007 2008 2009 2010 2011 2012 2013 2014

Raleigh-Durham Apartment Supply & DemandPercent, Thousands of Units

Apartment Completions: Q4 @ 2544 Units (Right Axis)Apartment Net Absorption: Q4 @ 1,938 Units (Right Axis)Apartment Vacancy Rate: Q4 @ 6.7% (Left Axis)

-200

0

200

400

600

800

7%

8%

9%

10%

11%

12%

2007 2008 2009 2010 2011 2012 2013 2014

Raleigh-Durham Retail Supply & DemandPercent, Thousands of Square Feet

Retail Completions: Q4 @ 0 SF (Right Axis)

Retail Net Absorption: Q4 @ 59,000 SF (Right Axis)

Retail Vacancy Rate: Q4 @ 9.0% (Left Axis)

Economic Outlook 3131

Commercial Real Estate

Strong growth in office using employment has fueled demand for office space. Manufacturing employment has been mixed, although industrial vacancy rates

continue to fall.

Source: Reis, Inc., CoStar Portfolio Strategy and Wells Fargo Securities, LLC

IndustrialOffice

-600

-300

0

300

600

900

1,200

8%

10%

12%

14%

16%

18%

20%

2007 2008 2009 2010 2011 2012 2013 2014

Raleigh-Durham Office Supply & DemandPercent, Thousands of Square Feet

Office Completions: Q4 @ 165,000 SF (Right Axis)Office Net Absorption: Q4 @ 91,000 SF (Right Axis)Office Vacancy Rate: Q4 @ 15.3% (Left Axis)

-2,200

-1,700

-1,200

-700

-200

300

800

1,300

1,800

0%

2%

4%

6%

8%

10%

12%

14%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Raleigh-Durham Warehouse Supply & DemandPercent, Thousands of Square Feet

Warehouse Completions: Q4 @ 0 SF (Right Axis)Warehouse Net Absorption: Q4 @ 432,000 SF (Right Axis)Warehouse Vacancy Rate: Q4 @ 7.5% (Left Axis)

Economic Outlook 32

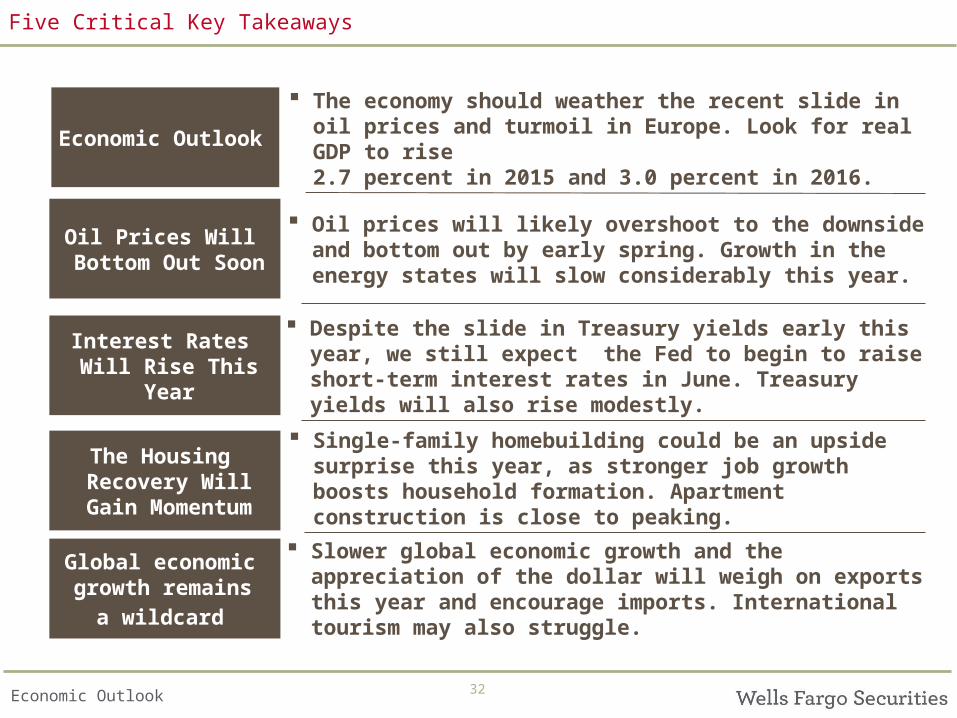

Five Critical Key Takeaways

Economic Outlook

Oil Prices Will Bottom Out

Soon

Oil prices will likely overshoot to the downside and bottom out by early spring. Growth in the energy states will slow considerably this year.

Interest Rates Will Rise This

Year

Despite the slide in Treasury yields early this year, we still expect the Fed to begin to raise short-term interest rates in June. Treasury yields will also rise modestly.

The Housing Recovery Will

Gain Momentum

Single-family homebuilding could be an upside surprise this year, as stronger job growth boosts household formation. Apartment construction is close to peaking.

Global economic growth remains

a wildcard

Slower global economic growth and the appreciation of the dollar will weigh on exports this year and encourage imports. International tourism may also struggle.

The economy should weather the recent slide in oil prices and turmoil in Europe. Look for real GDP to rise 2.7 percent in 2015 and 3.0 percent in 2016.

Economic Outlook 33

Our Forecast

Wells Fargo U.S. Economic Forecast

2012 2013 2014 2015 2016

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Real Gross Domestic Product 1 - 2.1 4.6 5.0 2.2 1.1 3.0 2.9 3.0 2.3 2.2 2.4 2.7 3.0

Personal Consumption 1.2 2.5 3.2 4.2 3.3 2.8 2.8 2.8 1.8 2.4 2.5 3.2 2.7

Inflation Indicators 2

PCE Deflator 1.1 1.6 1.5 1.1 0.2 0.1 0.3 0.9 1.8 1.2 1.3 0.4 2.0

Consumer Price Index 1.4 2.1 1.8 1.2 - 0.2 - 0.3 0.0 0.8 2.1 1.5 1.6 0.1 2.3

Industrial Production 1 3.9 5.7 4.1 4.3 3.0 4.9 3.5 3.1 3.8 2.9 4.2 4.0 3.6

Corporate Profits Before Taxes 2 - 4.8 0.1 1.4 3.4 4.2 4.2 4.7 3.7 11.4 4.2 0.1 4.2 3.4

Trade Weighted Dollar Index 3 76.9 75.9 81.3 85.1 91.3 92.5 93.8 95.0 73.5 75.9 78.5 93.1 97.5

Unemployment Rate 6.6 6.2 6.1 5.7 5.5 5.4 5.3 5.2 8.1 7.4 6.2 5.4 5.0

Housing Starts 4 0.93 0.99 1.03 1.06 1.07 1.13 1.21 1.24 0.78 0.92 1.00 1.15 1.31

Quarter- End Interest Rates 5

Federal Funds Target Rate 0.25 0.25 0.25 0.25 0.25 0.50 0.75 1.00 0.25 0.25 0.25 0.63 2.00Conventional Mortgage Rate 4.34 4.16 4.16 3.86 3.60 3.72 3.87 3.89 3.66 3.98 4.17 3.77 4.5610 Year Note 2.73 2.53 2.52 2.17 2.20 2.36 2.40 2.45 1.80 2.35 2.54 2.35 2.80

Forecast as of: March 11, 20151 Compound Annual Growth Rate Quarter-over-Quarter2 Year-over-Year Percentage Change3 Federal Reserve Major Currency I ndex, 1973=100 - Quarter End4 Millions of Units5 Annual Numbers Represent Averages

Forecast

2014

Actual

2015

ForecastActual

Appendix

Economic Outlook 35

Wells Fargo Economics Group Publications

To view any of our past research please visit:

http://www.wellsfargo.com/economics

To join any of our research distribution lists please

visit:http://www.wellsfargo.com/

economicsemail

A Sampling of Our Recent Special, Regional & Industry Commentary

Selected Recent Economic Reports

Date Title Authors

U.S. Macro

March- 13 Will Dollar Strength Scuttle U.S. Exports? Bryson, Quinlan & HouseMarch- 11 Millennials in the Economy House, Nelson & MoehringMarch- 10 Frictionless Models in a World Full of Frictions Silvia, Iqbal & NelsonMarch- 04 2015 Federal Fiscal Policy Outlook Part II: Outlay Growth Continues to Outpace RevenuesSilvia, Brown & Miller

U.S. Regional

March- 06 California Payrolls Stronger with Revisions Vitner & Wolf

March- 06 Texas Payrolls Strond Despite Oil and Revisions Vitner & Wolf

February- 24 California Economic Outlook: February 2015 Vitner, Wolf & Moehring

February- 12 North Carolina Economic Outlook: February 2015 Vitner, Wolf & Moehring

Global Economy

March- 12 Global Chartbook: March 2015 Bryson, Alemán & Quinlan

March- 04 No Cut from Australia's Reserve Bank Quinlan

March- 04 Bank of Canada on Hold After Strong Q4 GDP Print Quinlan

March- 03 Swiss GDP Growth Outpaces Expectations in Q4 Bryson & Griffiths

Interest Rates/Credit Market

March- 11 Are Rates Finally Starting to Rise? Silvia, Vitner & Brown

March- 04 Why March Matters Silvia, Vitner & Brown

February- 25 Net Treasury Issuance: A Longer- Term Outlook Silvia, Vitner & Brown

February- 18 Yield Curve Reactions In an Era of Losing Patience Policy Silvia, Vitner & Brown

Real EstateMarch- 13 Housing Data Wrap- Up: March 2015 Vitner & Khan

March- 09 Dodge Momentum Index Rebounds in February Khan

February- 27 Nonresidential Construction Recap: February Khan

February- 19 Architecture Billings Show Modest Dip in J anuary Khan

Economic Outlook

Wells Fargo Securities, LLC Economics Group

36

John E. Silvia … ...................... . … [email protected]

Global Head of Research and Economics

Diane Schumaker-Krieg ………………… ………[email protected] Head of Research & Economics

Chief Economist

Mark Vitner, Senior Economist……………....………. . .

Jay H. Bryson, Global Economist …………………....…… ….

Sam Bullard, Senior Economist [email protected]

Nick Bennenbroek, Currency Strategist ……[email protected]

Eugenio J. Alemán, Senior Economist… ………….

Anika R. Khan, Senior Economist … . [email protected]

Senior Economists

Mackenzie Miller, Economic Analyst [email protected]

Erik Nelson, Economic Analyst [email protected]

Alex Moehring, Economic Analyst [email protected]

Economists

Azhar Iqbal, Econometrician………………… ……………[email protected]

Tim Quinlan, Economist …………………… ……………[email protected]

Eric J. Viloria, Currency Strategist [email protected]

Sarah Watt House, Economist …………… …………[email protected]

Michael A. Brown, Economist ……………… … [email protected]

Michael T. Wolf, Economist ………………… … .

Economic Analysts

Administrative Assistants

Wells Fargo Securities Economics Group publications are produced by Wells Fargo Securities, LLC, a U.S broker-dealer registered with the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority, and the Securities Investor Protection Corp. Wells Fargo Securities, LLC, distributes these publications directly and through subsidiaries including, but not limited to, Wells Fargo & Company, Wells Fargo Bank N.A., Wells Fargo Advisors, LLC, Wells Fargo Securities International Limited, Wells Fargo Securities Asia Limited and Wells Fargo Securities (Japan) Co. Limited. Wells Fargo Securities, LLC. ("WFS") is registered with the Commodities Futures Trading Commission as a futures commission merchant and is a member in good standing of the National Futures Association. Wells Fargo Bank, N.A. ("WFBNA") is registered with the Commodities Futures Trading Commission as a swap dealer and is a member in good standing of the National Futures Association. WFS and WFBNA are generally engaged in the trading of futures and derivative products, any of which may be discussed within this publication. Wells Fargo Securities, LLC does not compensate its research analysts based on specific investment banking transactions. Wells Fargo Securities, LLC’s research analysts receive compensation that is based upon and impacted by the overall profitability and revenue of the firm which includes, but is not limited to investment banking revenue. The information and opinions herein are for general information use only. Wells Fargo Securities, LLC does not guarantee their accuracy or completeness, nor does Wells Fargo Securities, LLC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. Wells Fargo Securities, LLC is a separate legal entity and distinct from affiliated banks and is a wholly owned subsidiary of Wells Fargo & Company © 2015 Wells Fargo Securities, LLC.

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE

Important Information for Non-U.S. Recipients

For recipients in the EEA, this report is distributed by Wells Fargo Securities International Limited ("WFSIL"). WFSIL is a U.K. incorporated investment firm authorized and regulated by the Financial Conduct Authority. The content of this report has been approved by WFSIL a regulated person under the Act. For purposes of the U.K. Financial Conduct Authority’s rules, this report constitutes impartial investment research. WFSIL does not deal with retail clients as defined in the Markets in Financial Instruments Directive 2007. The FCA rules made under the Financial Services and Markets Act 2000 for the protection of retail clients will therefore not apply, nor will the Financial Services Compensation Scheme be available. This report is not intended for, and should not be relied upon by, retail clients. This document and any other materials accompanying this document (collectively, the "Materials") are provided for general informational purposes only.

Donna LaFleur, Executive Assistant.

Cyndi Burris, Senior Administrative Assistant [email protected]

![[Dean Vitner] SQL Server “Denali” Contained Databases](https://img.pdfslide.us/doc/110x75/5571fe3649795991699ae2cd/dean-vitner-sql-server-denali-contained-databases.jpg)