Embed Size (px)

Citation preview

The Global Economic Outlook

Tim Quinlan, EconomistApril 14, 2010

2Economics

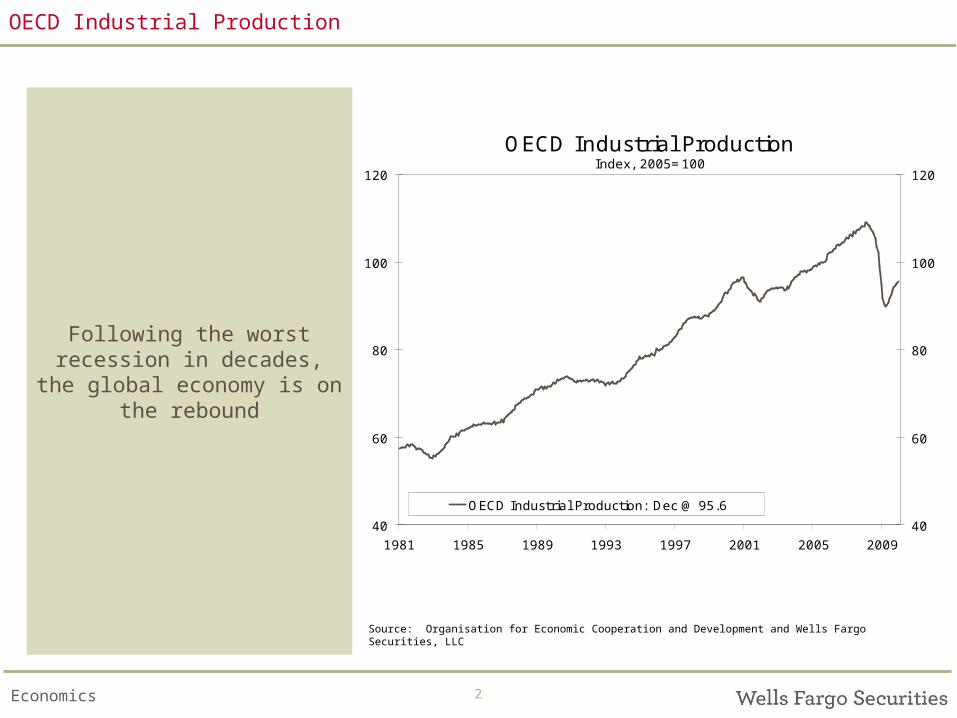

OECD Industrial ProductionIndex, 2005=100

40

60

80

100

120

1981 1985 1989 1993 1997 2001 2005 2009

40

60

80

100

120

OECD Industrial Production: Dec @ 95.6

OECD Industrial Production

Following the worst recession in decades, the global economy is on the

rebound

Source: Organisation for Economic Cooperation and Development and Wells Fargo Securities, LLC

3Economics

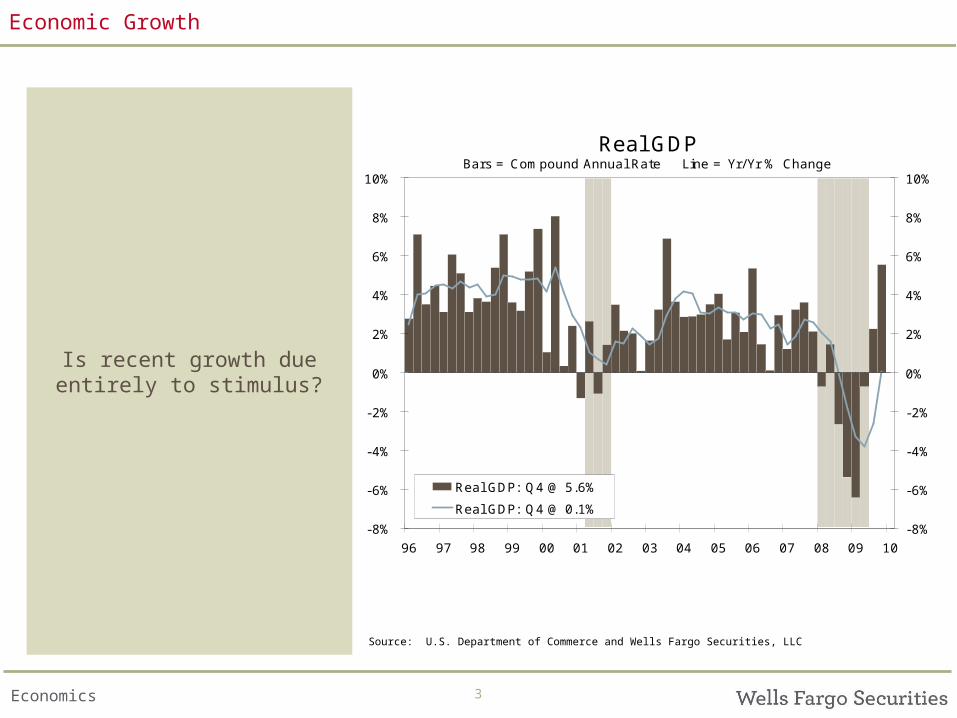

Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Real GDP: Q4 @ 5.6%

Real GDP: Q4 @ 0.1%

Economic Growth

Is recent growth due entirely to stimulus?

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

4Economics

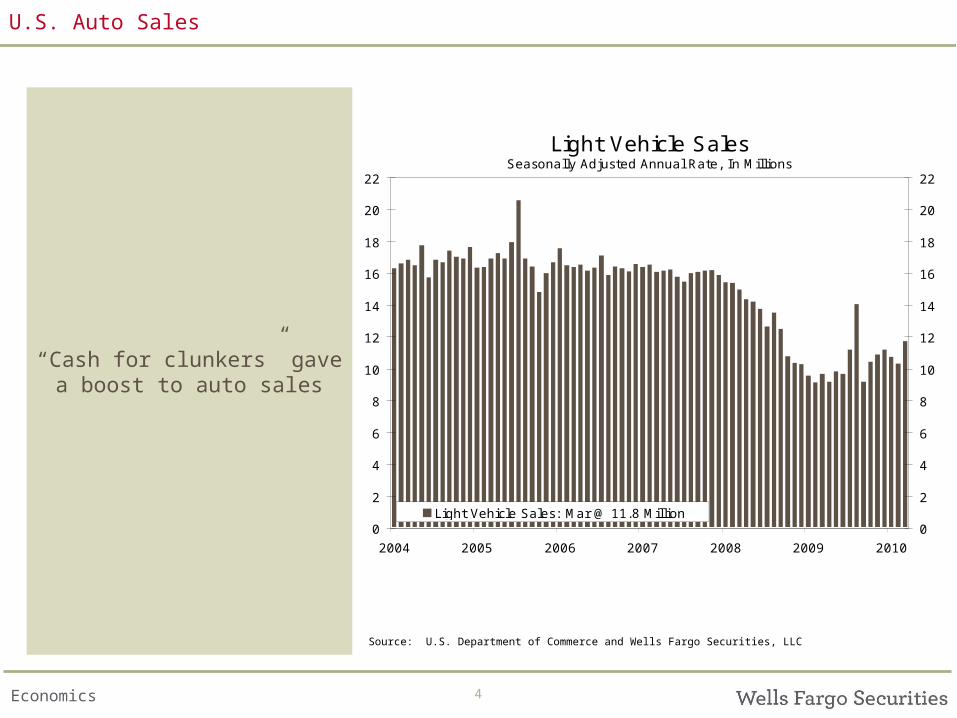

Light Vehicle SalesSeasonally Adjusted Annual Rate, In Millions

0

2

4

6

8

10

12

14

16

18

20

22

2004 2005 2006 2007 2008 2009 2010

0

2

4

6

8

10

12

14

16

18

20

22

Light Vehicle Sales: Mar @ 11.8 Million

U.S. Auto Sales

“Cash for clunkers” gave a boost to auto sales

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

5Economics

Housing Starts Seasonally Adjusted Annual Rate, In Millions

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

01 02 03 04 05 06 07 08 09 10

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

Housing Starts: Feb @ 575K

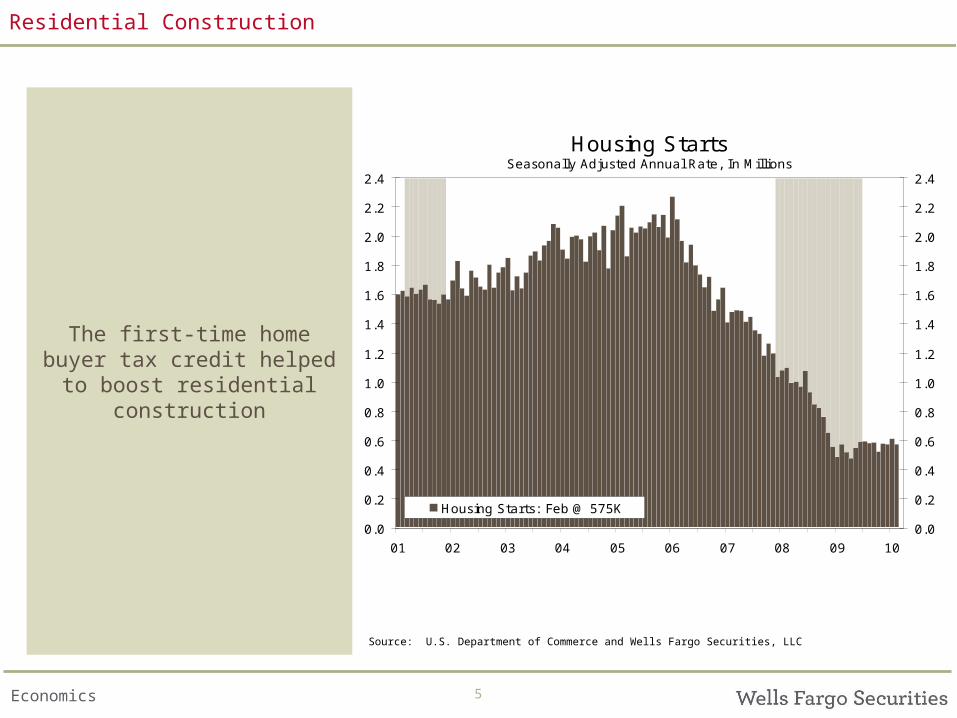

Residential Construction

The first-time home buyer tax credit helped to boost residential construction

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

6Economics

Retail Sales Ex-Autos, Gas & Building Materials

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Year-over-Year Percent Change: Feb @ 2.7%3-Month Annual Rate: Feb @ 4.6%

All Series are 3-Month Moving Averages

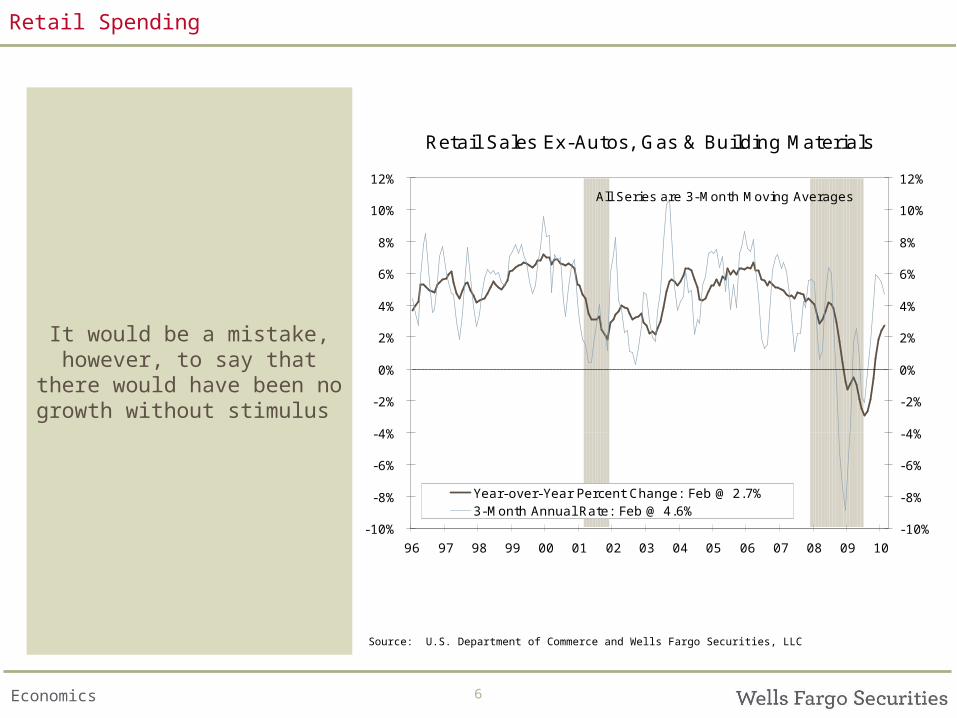

Retail Spending

It would be a mistake, however, to say that there

would have been no growth without stimulus

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

7Economics

NonDefense Capital Goods Orders, Ex-AircraftSeries are 3-Month Moving Averages

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

93 95 97 99 01 03 05 07 09

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

3-Month Annual Rate: Feb @ 9.3%

Year-Over-Year Percent Change: Feb @ 5.4%

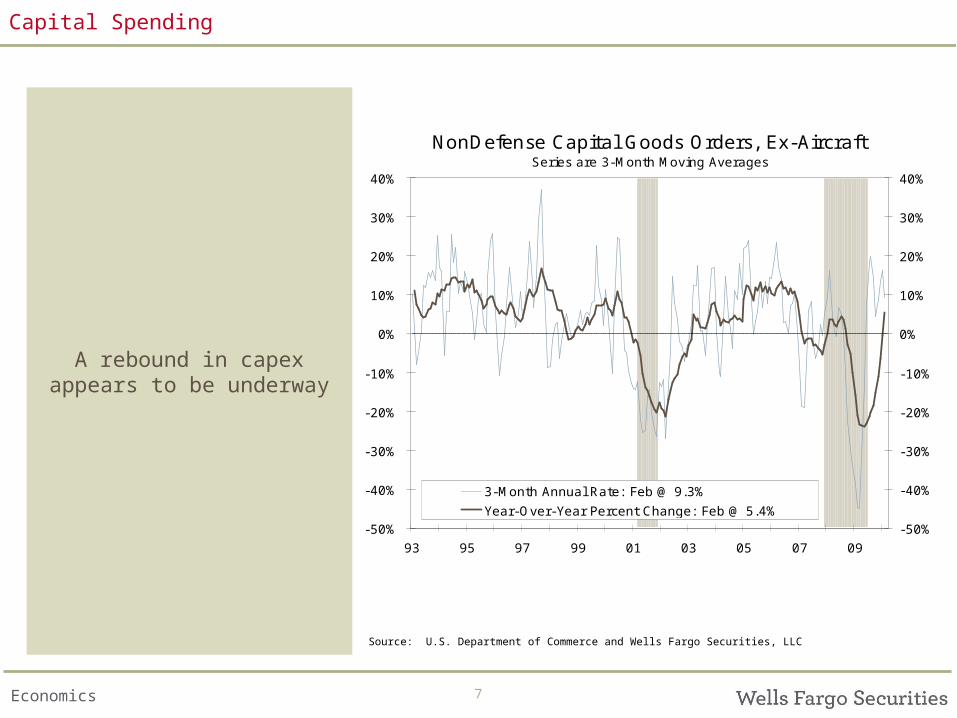

Capital Spending

A rebound in capex appears to be underway

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

8Economics

Exports & Imports of Goods, Constant Dollar Billions of Dollars

$50

$70

$90

$110

$130

$150

$170

1997 1999 2001 2003 2005 2007 2009

$50

$70

$90

$110

$130

$150

$170Exports: J an @ $89.5 Billion

Imports: J an @ $130.5 Billion

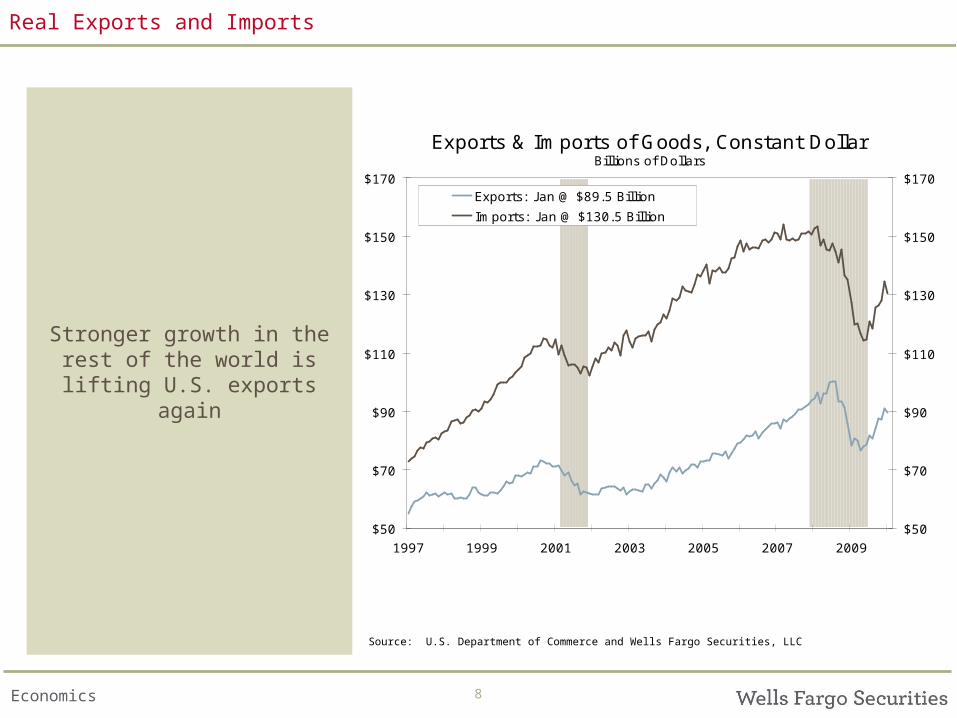

Real Exports and Imports

Stronger growth in the rest of the world is lifting U.S.

exports again

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

9Economics

Change in Real Inventories Billions of Dollars, Annual Rate

-$200

-$175

-$150

-$125

-$100

-$75

-$50

-$25

$0

$25

$50

$75

$100

$125

2000 2002 2004 2006 2008 2010

-$200

-$175

-$150

-$125

-$100

-$75

-$50

-$25

$0

$25

$50

$75

$100

$125

Change in Private Inventories: Q4 @ -$19.7B

Forecast

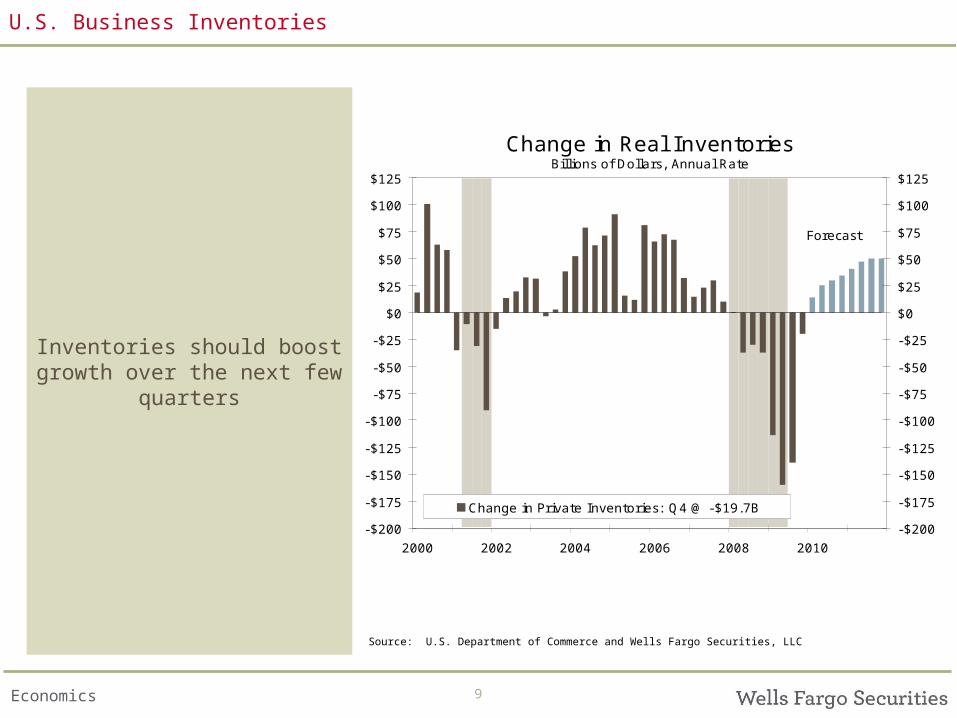

U.S. Business Inventories

Inventories should boost growth over the next few

quarters

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

10Economics

Real GDP Bars = CAGR Line = Yr/Yr Percent Change

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2000 2002 2004 2006 2008 2010

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%GDPR - CAGR: Q4 @ 5.6%

GDPR - Yr/Yr Percent Change: Q4 @ 0.1%

Forecast

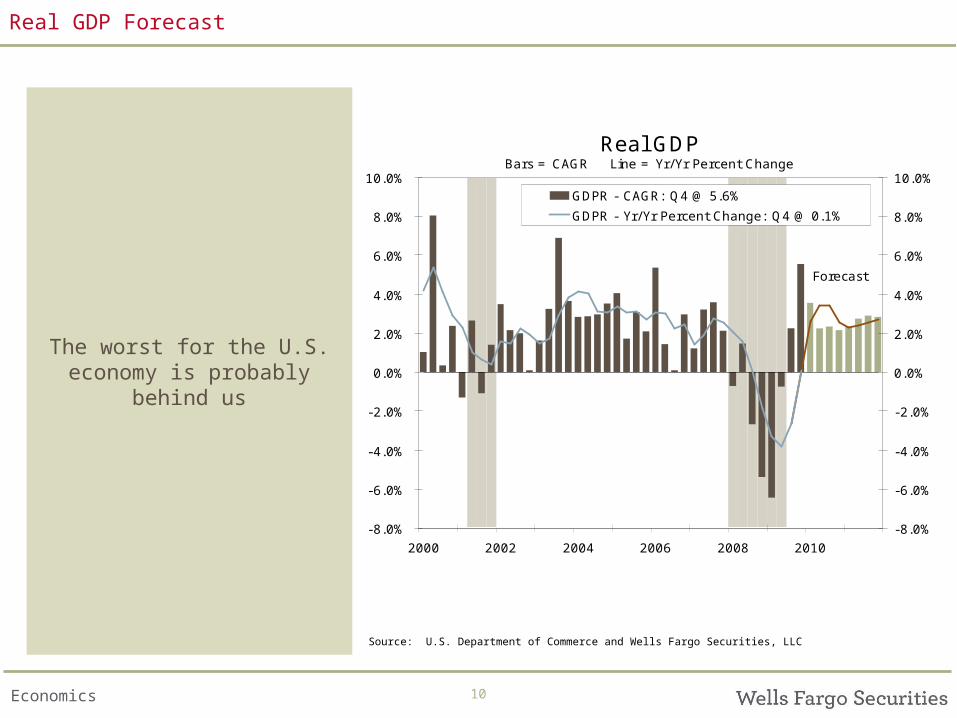

Real GDP Forecast

The worst for the U.S. economy is probably behind

us

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

11Economics

Real Personal Consumption ExpendituresBars = CAGR Line = Yr/Yr Percent Change

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2000 2002 2004 2006 2008 2010

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

PCE - CAGR: Q4 @ 1.6%

PCE - Yr/Yr Percent Change: Q4 @ 1.0%

Forecast

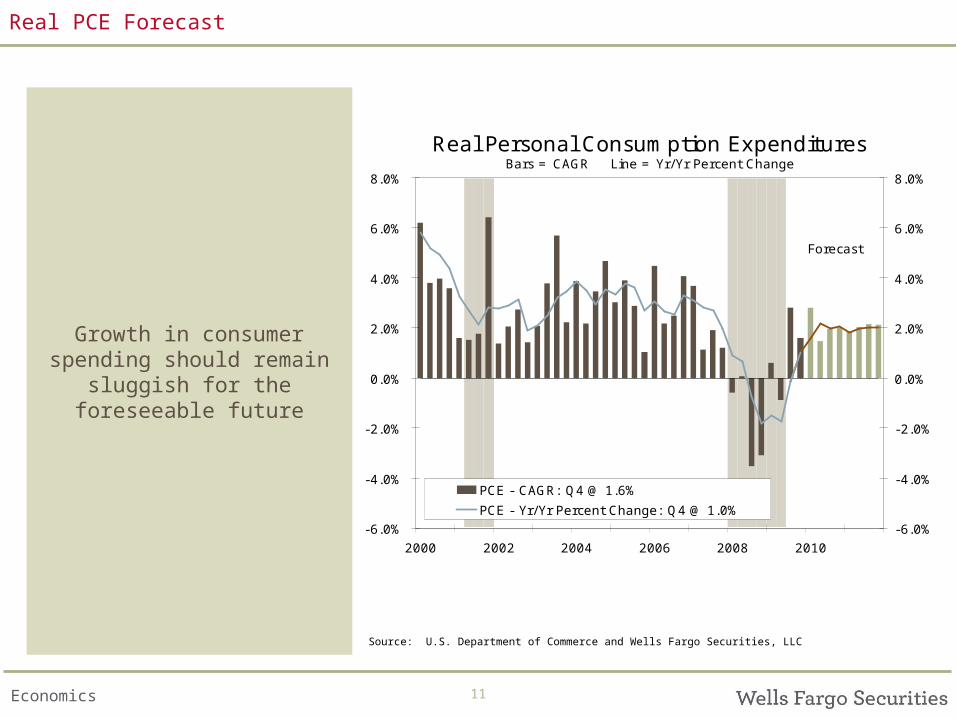

Real PCE Forecast

Growth in consumer spending should remain

sluggish for the foreseeable future

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

12Economics

Household Debt - Consumer & MortgageAs a Percent of Disposable Personal Income

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

Household Debt: Q4 @ 115.3%

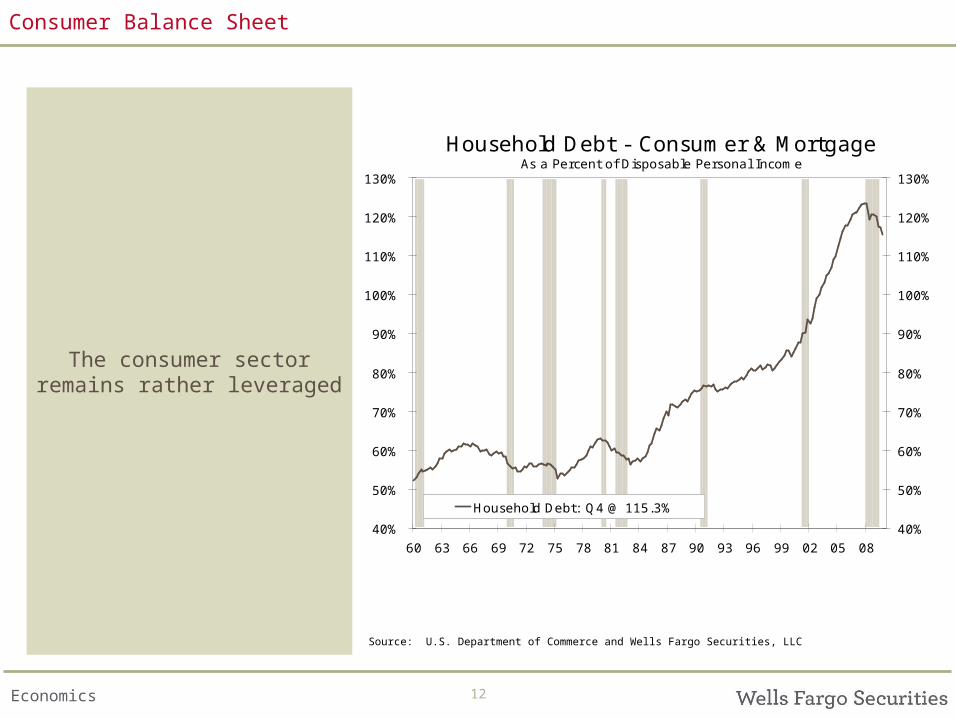

Consumer Balance Sheet

The consumer sector remains rather leveraged

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

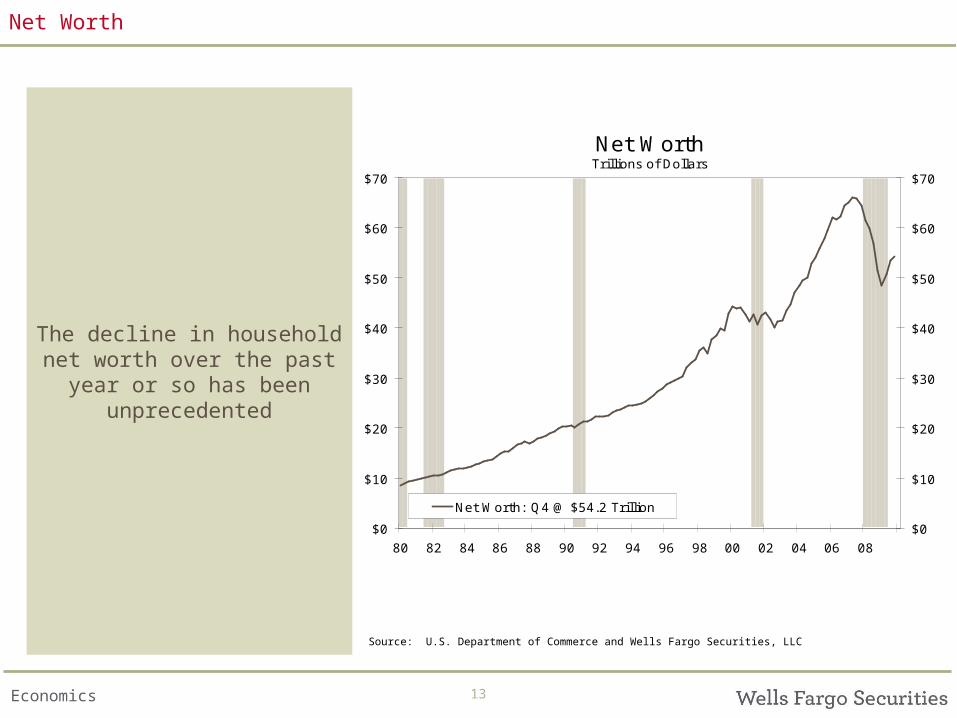

13Economics

Net WorthTrillions of Dollars

$0

$10

$20

$30

$40

$50

$60

$70

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

$0

$10

$20

$30

$40

$50

$60

$70

Net Worth: Q4 @ $54.2 Trillion

Net Worth

The decline in household net worth over the past year

or so has been unprecedented

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

14Economics

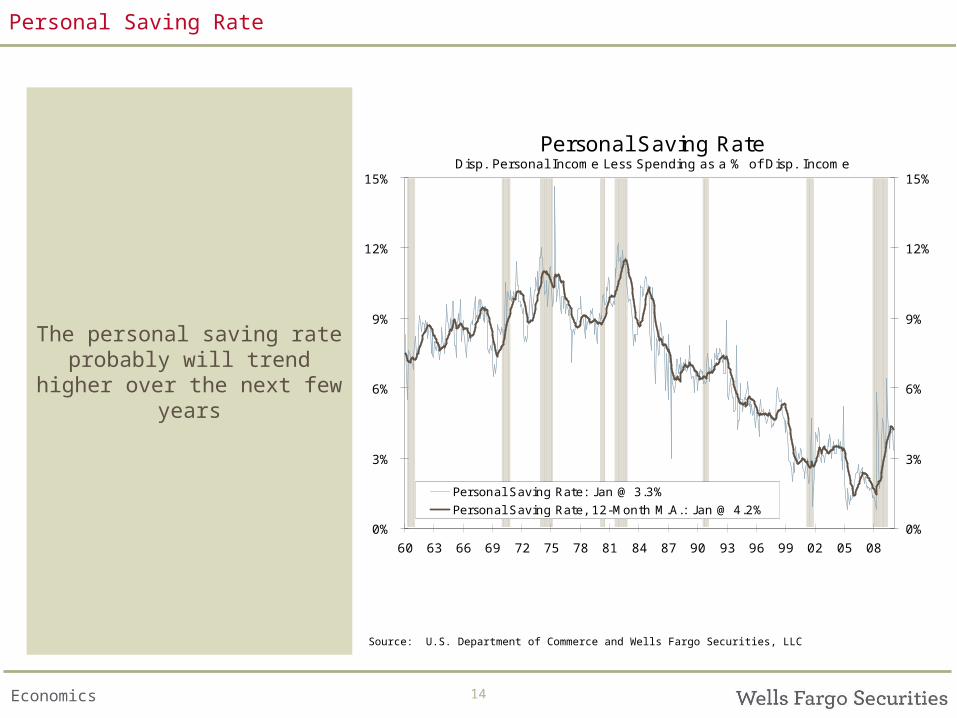

Personal Saving Rate Disp. Personal Income Less Spending as a % of Disp. Income

0%

3%

6%

9%

12%

15%

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

0%

3%

6%

9%

12%

15%

Personal Saving Rate: J an @ 3.3%

Personal Saving Rate, 12-Month M.A.: J an @ 4.2%

Personal Saving Rate

The personal saving rate probably will trend higher

over the next few years

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

15Economics

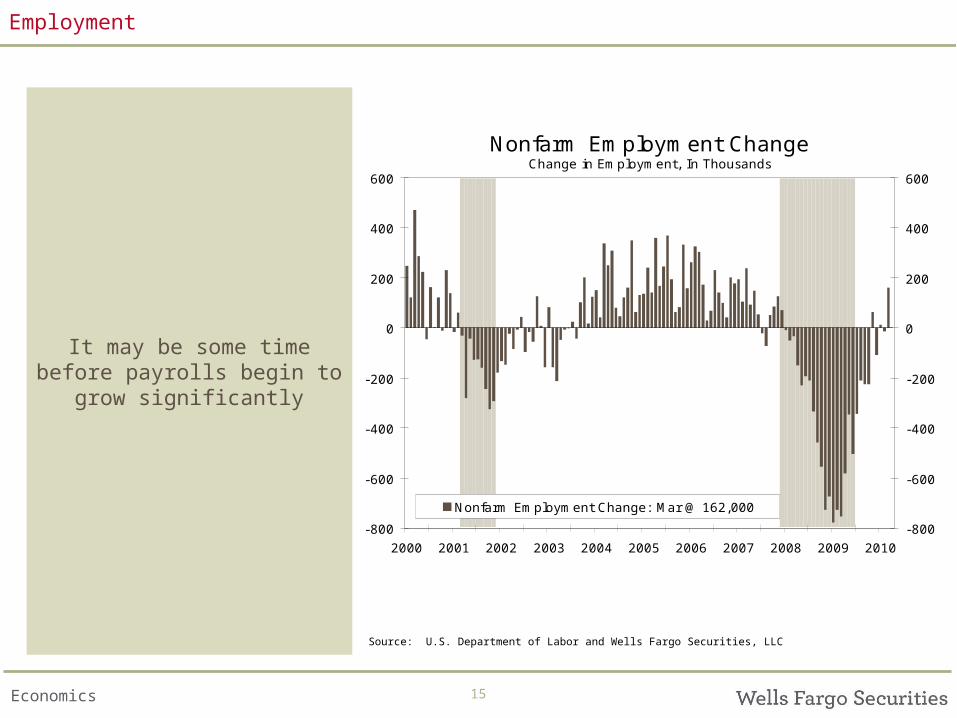

Nonfarm Employment ChangeChange in Employment, In Thousands

-800

-600

-400

-200

0

200

400

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

-800

-600

-400

-200

0

200

400

600

Nonfarm Employment Change: Mar @ 162,000

Employment

It may be some time before payrolls begin to grow

significantly

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

16Economics

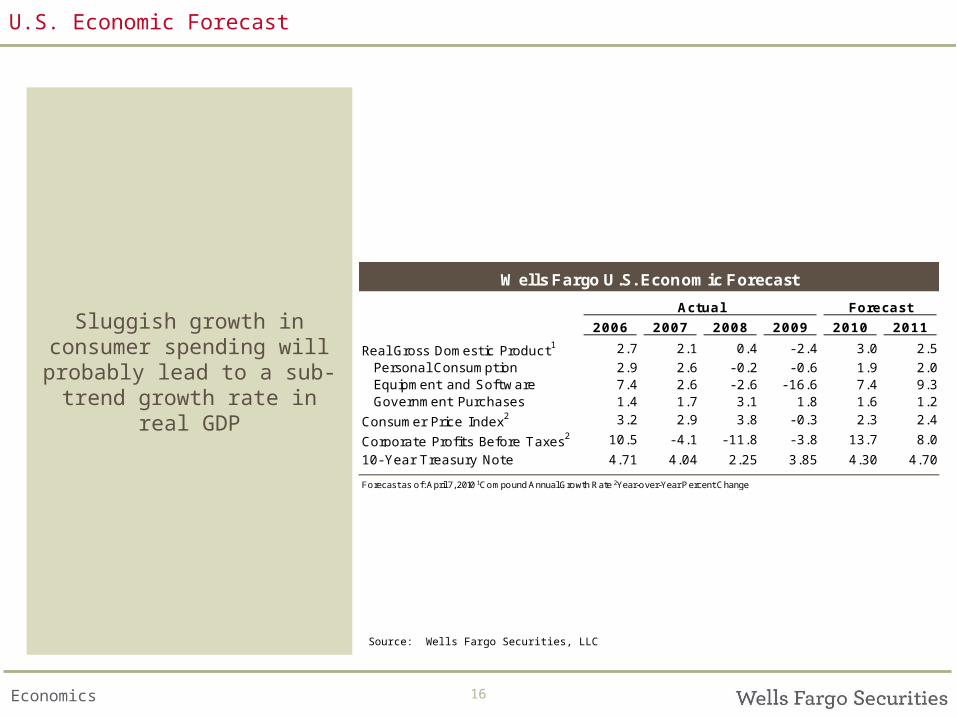

Wells Fargo U.S. Economic Forecast

Actual Forecast

2006 2007 2008 2009 2010 2011

Real Gross Domestic Product1 2.7 2.1 0.4 - 2.4 3.0 2.5

Personal Consumption 2.9 2.6 - 0.2 - 0.6 1.9 2.0Equipment and Software 7.4 2.6 - 2.6 - 16.6 7.4 9.3Government Purchases 1.4 1.7 3.1 1.8 1.6 1.2

Consumer Price Index2 3.2 2.9 3.8 - 0.3 2.3 2.4

Corporate Profits Before Taxes2 10.5 - 4.1 - 11.8 - 3.8 13.7 8.0

10- Year Treasury Note 4.71 4.04 2.25 3.85 4.30 4.70

Forecast as of: April 7, 2010 1Compound Annual Growth Rate 2Year-over-Year P ercent Change

U.S. Economic Forecast

Sluggish growth in consumer spending will

probably lead to a sub-trend growth rate in real GDP

Source: Wells Fargo Securities, LLC

17Economics

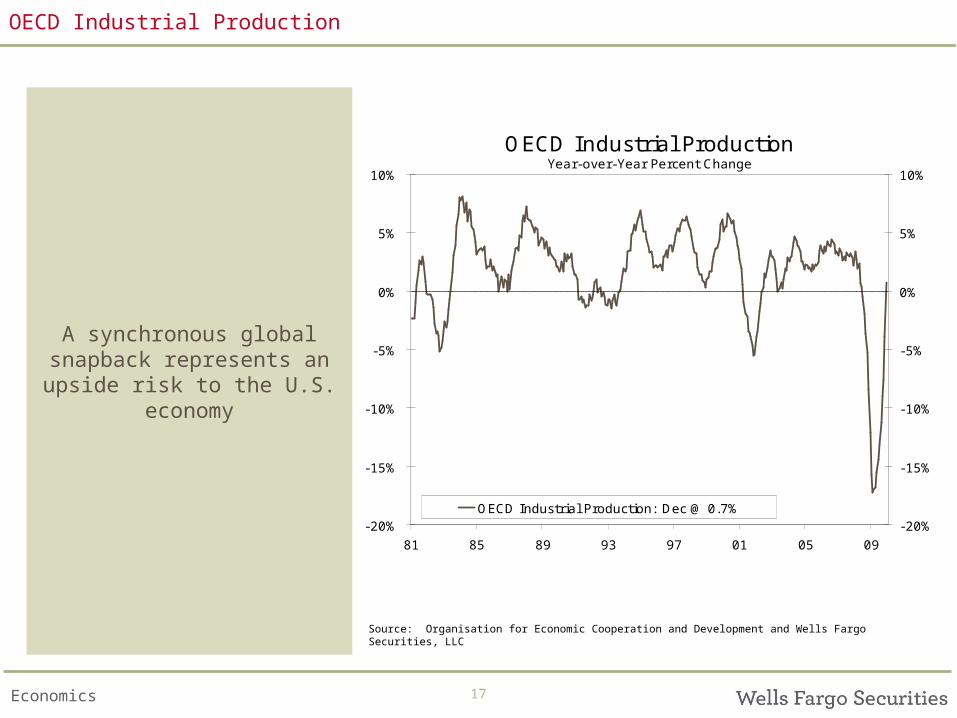

OECD Industrial ProductionYear-over-Year Percent Change

-20%

-15%

-10%

-5%

0%

5%

10%

81 85 89 93 97 01 05 09

-20%

-15%

-10%

-5%

0%

5%

10%

OECD Industrial Production: Dec @ 0.7%

OECD Industrial Production

A synchronous global snapback represents an upside risk to the U.S.

economy

Source: Organisation for Economic Cooperation and Development and Wells Fargo Securities, LLC

18Economics

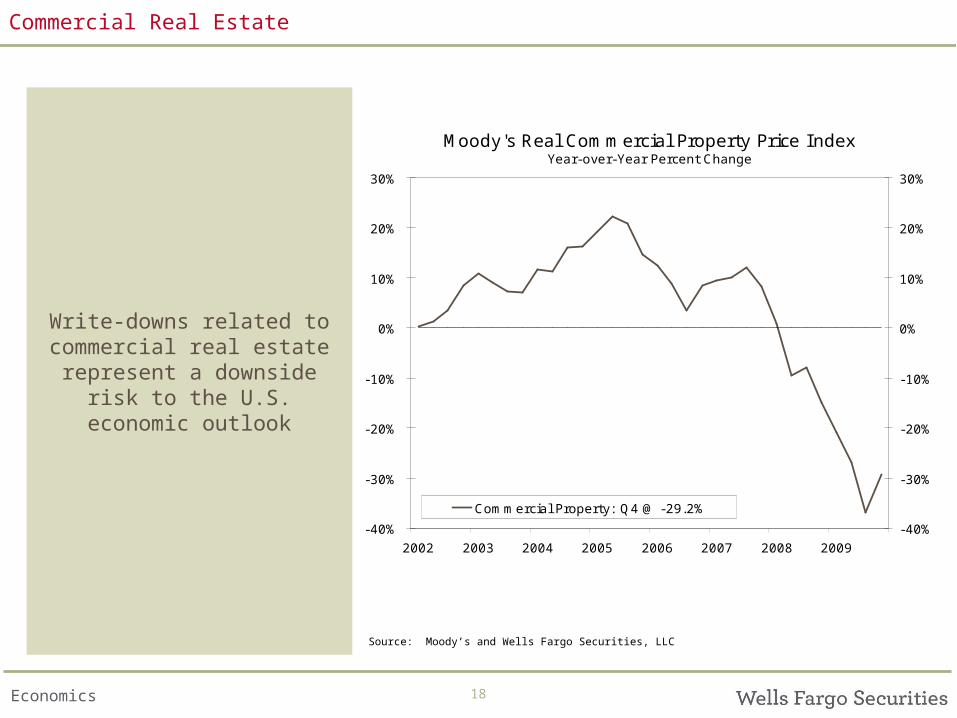

Moody's Real Commercial Property Price I ndexYear-over-Year Percent Change

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2002 2003 2004 2005 2006 2007 2008 2009

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Commercial Property: Q4 @ -29.2%

Commercial Real Estate

Write-downs related to commercial real estate

represent a downside risk to the U.S. economic

outlook

Source: Moody’s and Wells Fargo Securities, LLC

19Economics

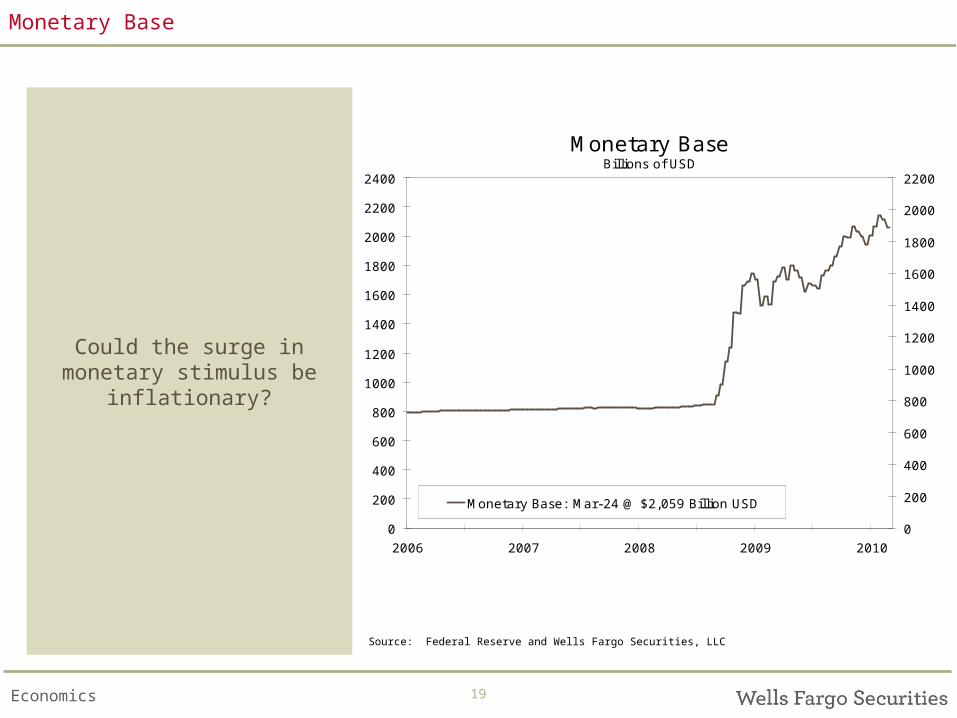

Monetary BaseBillions of USD

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

2006 2007 2008 2009 2010

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

Monetary Base: Mar-24 @ $2,059 Billion USD

Monetary Base

Could the surge in monetary stimulus be

inflationary?

Source: Federal Reserve and Wells Fargo Securities, LLC

20Economics

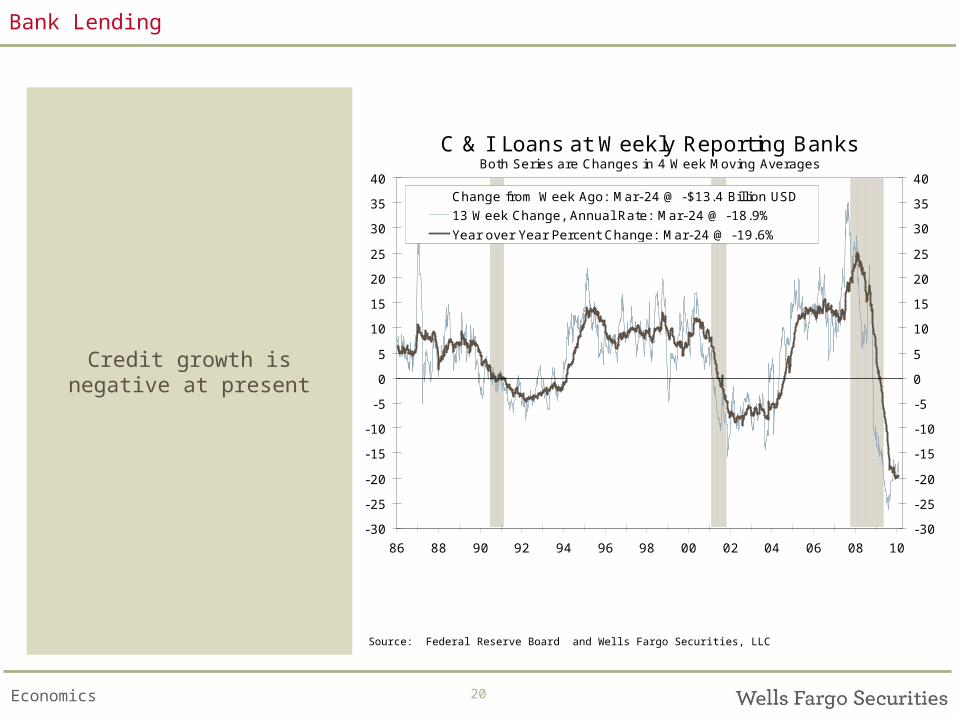

C & I Loans at Weekly Reporting BanksBoth Series are Changes in 4 Week Moving Averages

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

40

86 88 90 92 94 96 98 00 02 04 06 08 10

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

40Change from Week Ago: Mar-24 @ -$13.4 Billion USD

13 Week Change, Annual Rate: Mar-24 @ -18.9%

Year over Year Percent Change: Mar-24 @ -19.6%

Bank Lending

Credit growth is negative at present

Source: Federal Reserve Board and Wells Fargo Securities, LLC

21Economics

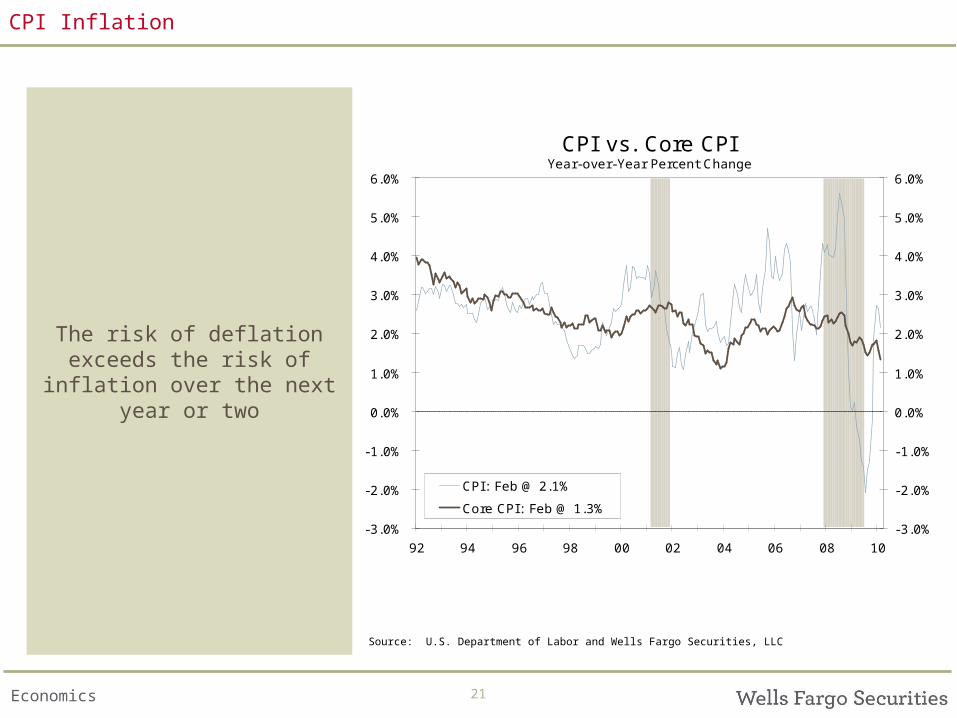

CPI vs. Core CPIYear-over-Year Percent Change

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

92 94 96 98 00 02 04 06 08 10

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

CPI: Feb @ 2.1%

Core CPI: Feb @ 1.3%

CPI Inflation

The risk of deflation exceeds the risk of inflation over the next year or two

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

22Economics

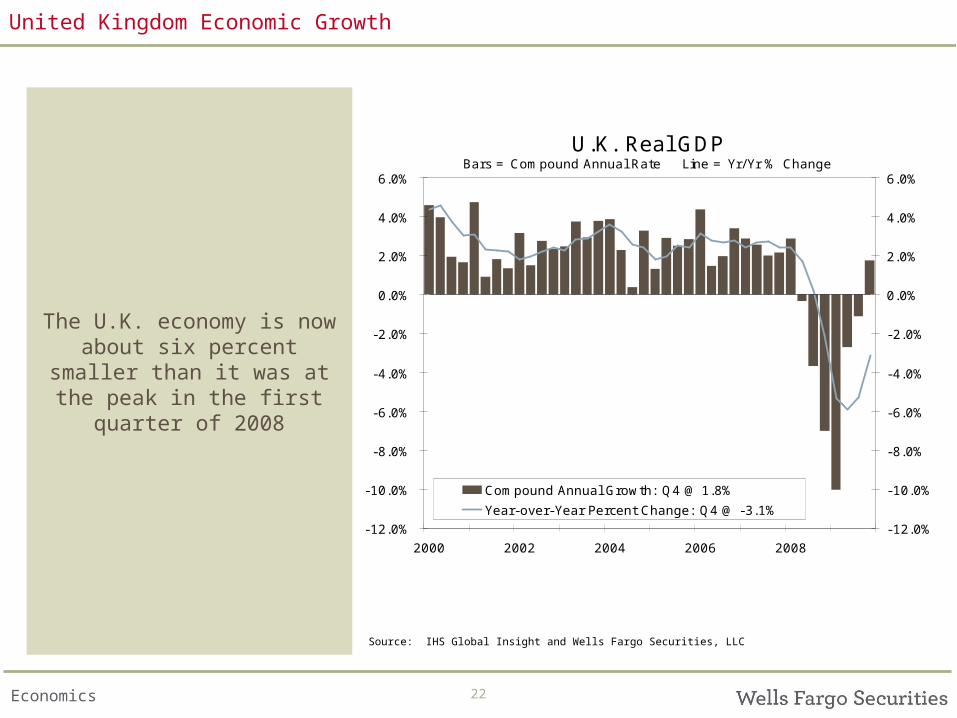

U.K. Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2000 2002 2004 2006 2008

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Compound Annual Growth: Q4 @ 1.8%

Year-over-Year Percent Change: Q4 @ -3.1%

United Kingdom Economic Growth

The U.K. economy is now about six percent smaller than it was at the peak in the first quarter of 2008

Source: IHS Global Insight and Wells Fargo Securities, LLC

23Economics

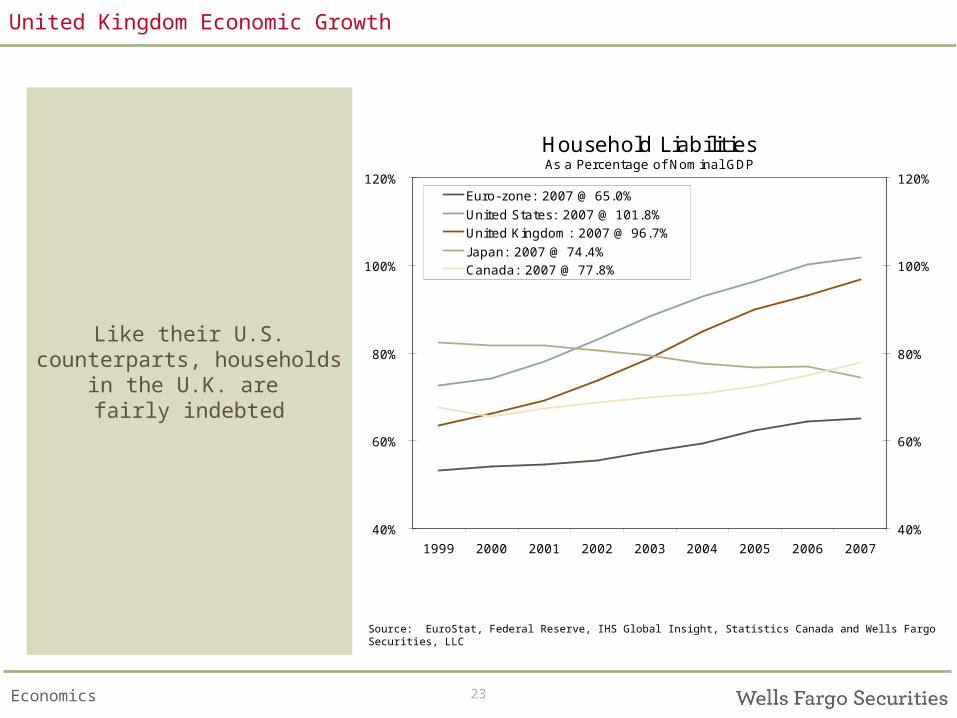

Household LiabilitiesAs a Percentage of Nominal GDP

40%

60%

80%

100%

120%

1999 2000 2001 2002 2003 2004 2005 2006 2007

40%

60%

80%

100%

120%Euro-zone: 2007 @ 65.0%

United States: 2007 @ 101.8%United Kingdom: 2007 @ 96.7%

J apan: 2007 @ 74.4%Canada: 2007 @ 77.8%

United Kingdom Economic Growth

Like their U.S. counterparts, households in

the U.K. are fairly indebted

Source: EuroStat, Federal Reserve, IHS Global Insight, Statistics Canada and Wells Fargo Securities, LLC

24Economics

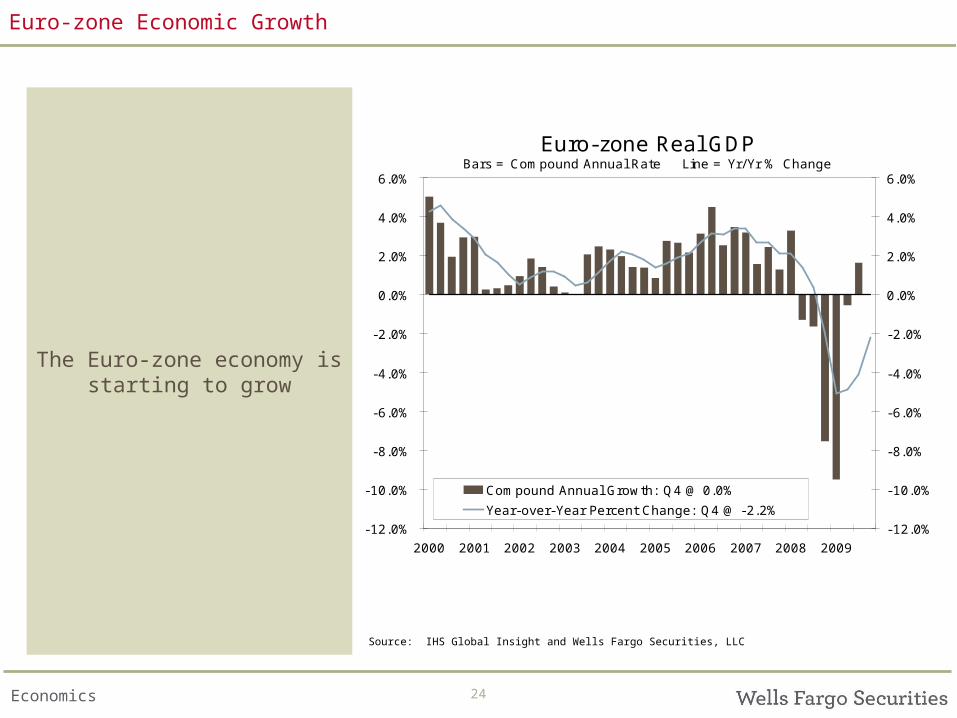

Euro-zone Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Compound Annual Growth: Q4 @ 0.0%

Year-over-Year Percent Change: Q4 @ -2.2%

Euro-zone Economic Growth

The Euro-zone economy is starting to grow

Source: IHS Global Insight and Wells Fargo Securities, LLC

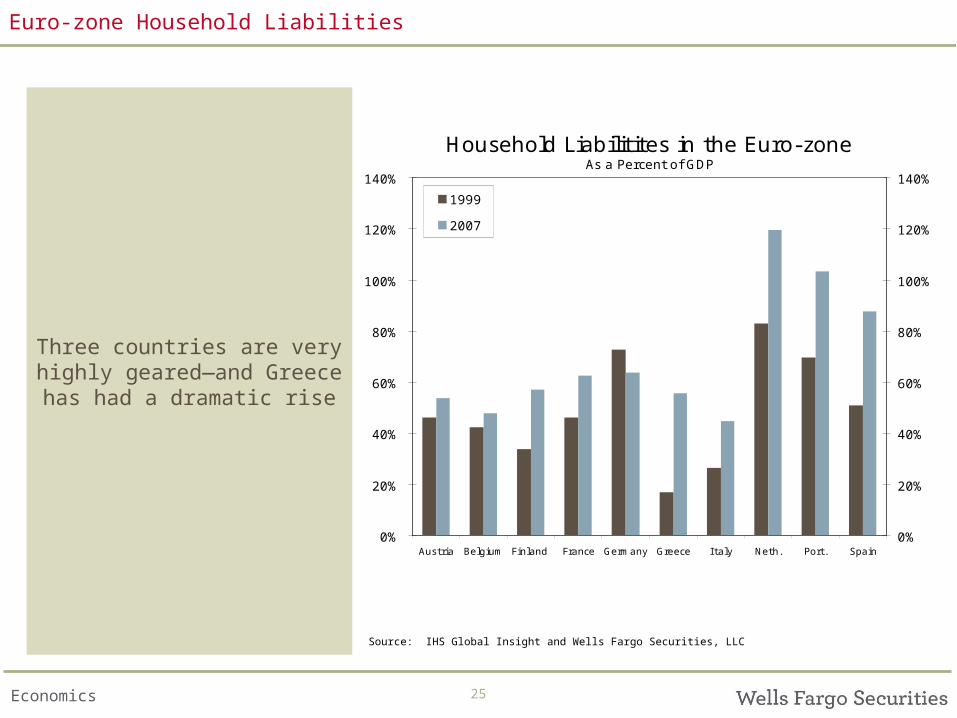

25Economics

Household Liabilitites in the Euro-zoneAs a Percent of GDP

0%

20%

40%

60%

80%

100%

120%

140%

Austria Belgium Finland France Germany Greece I taly Neth. Port. Spain0%

20%

40%

60%

80%

100%

120%

140%

1999

2007

Euro-zone Household Liabilities

Three countries are very highly geared—and Greece

has had a dramatic rise

Source: IHS Global Insight and Wells Fargo Securities, LLC

26Economics

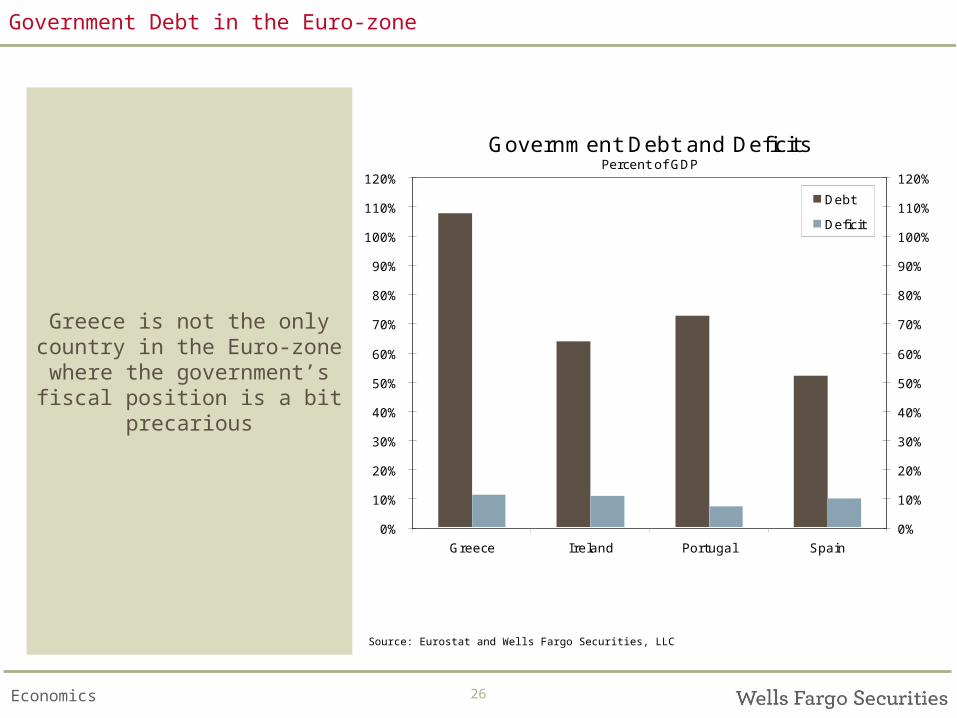

Government Debt and DeficitsPercent of GDP

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

Greece Ireland Portugal Spain

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

Debt

Deficit

Government Debt in the Euro-zone

Greece is not the only country in the Euro-zone where the government’s

fiscal position is a bit precarious

Source: Eurostat and Wells Fargo Securities, LLC

27Economics

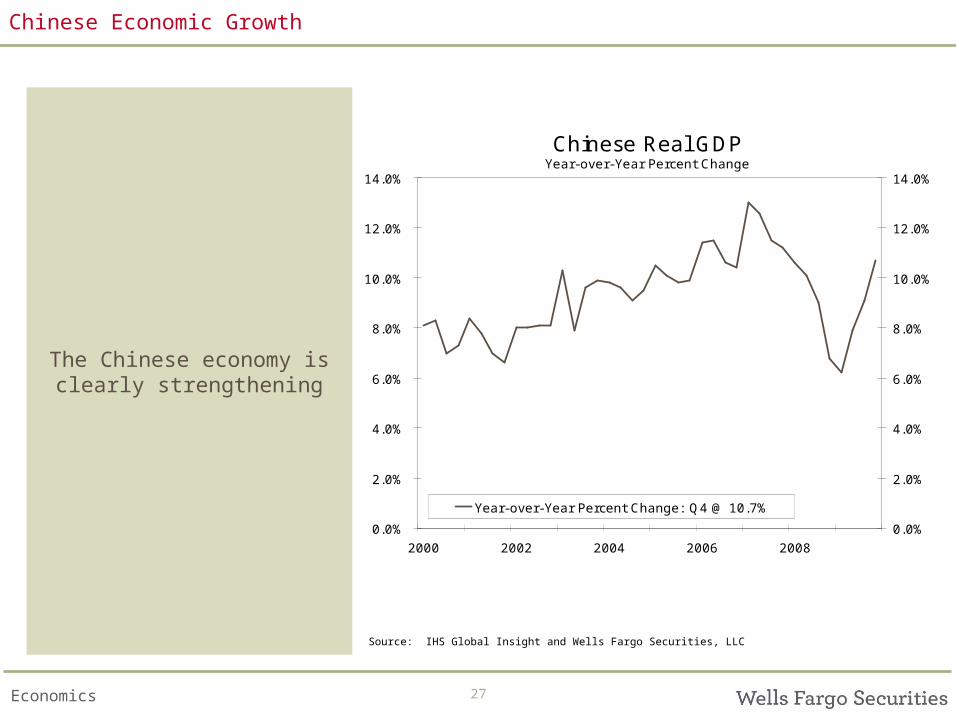

Chinese Real GDPYear-over-Year Percent Change

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2000 2002 2004 2006 2008

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Year-over-Year Percent Change: Q4 @ 10.7%

Chinese Economic Growth

The Chinese economy is clearly strengthening

Source: IHS Global Insight and Wells Fargo Securities, LLC

28Economics

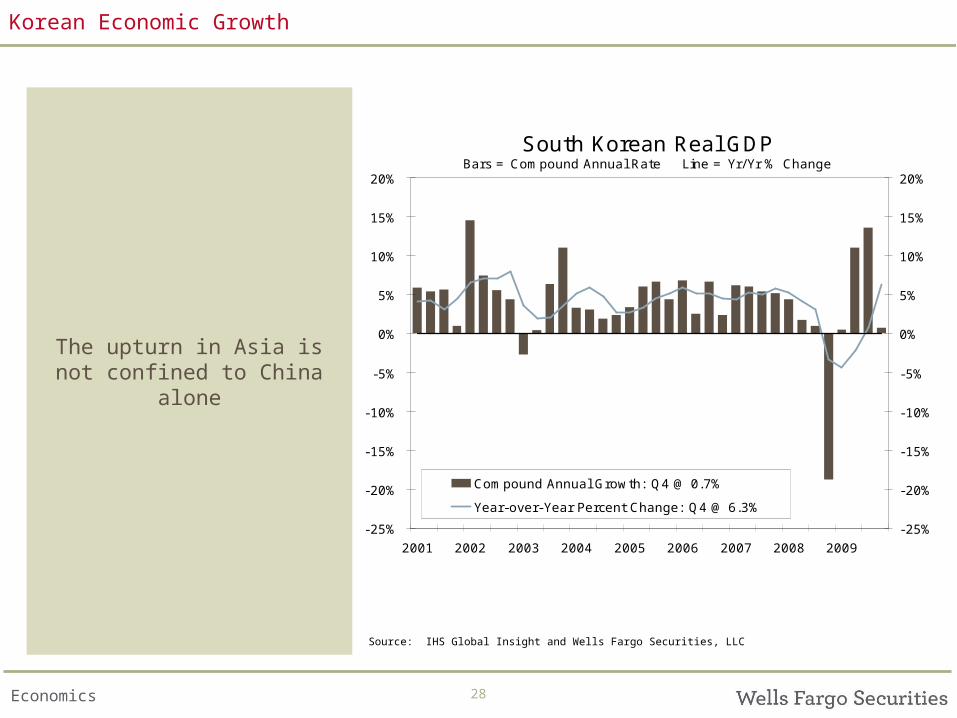

South Korean Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008 2009

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Compound Annual Growth: Q4 @ 0.7%

Year-over-Year Percent Change: Q4 @ 6.3%

Korean Economic Growth

The upturn in Asia is not confined to China alone

Source: IHS Global Insight and Wells Fargo Securities, LLC

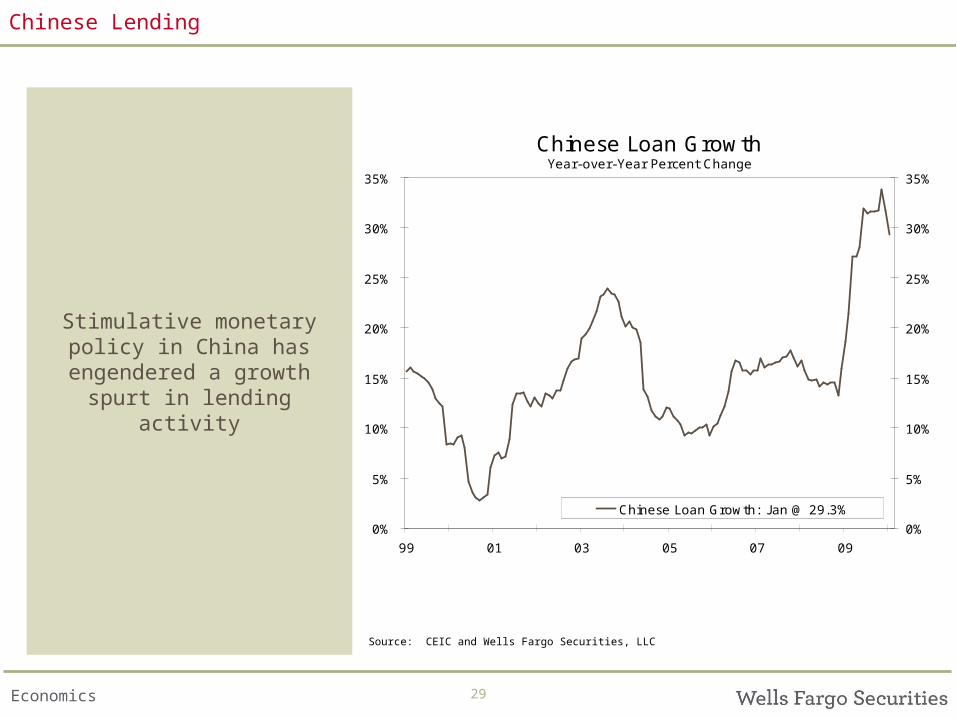

29Economics

Chinese Loan GrowthYear-over-Year Percent Change

0%

5%

10%

15%

20%

25%

30%

35%

99 01 03 05 07 09

0%

5%

10%

15%

20%

25%

30%

35%

Chinese Loan Growth: J an @ 29.3%

Chinese Lending

Stimulative monetary policy in China has engendered a

growth spurt in lending activity

Source: CEIC and Wells Fargo Securities, LLC

30Economics

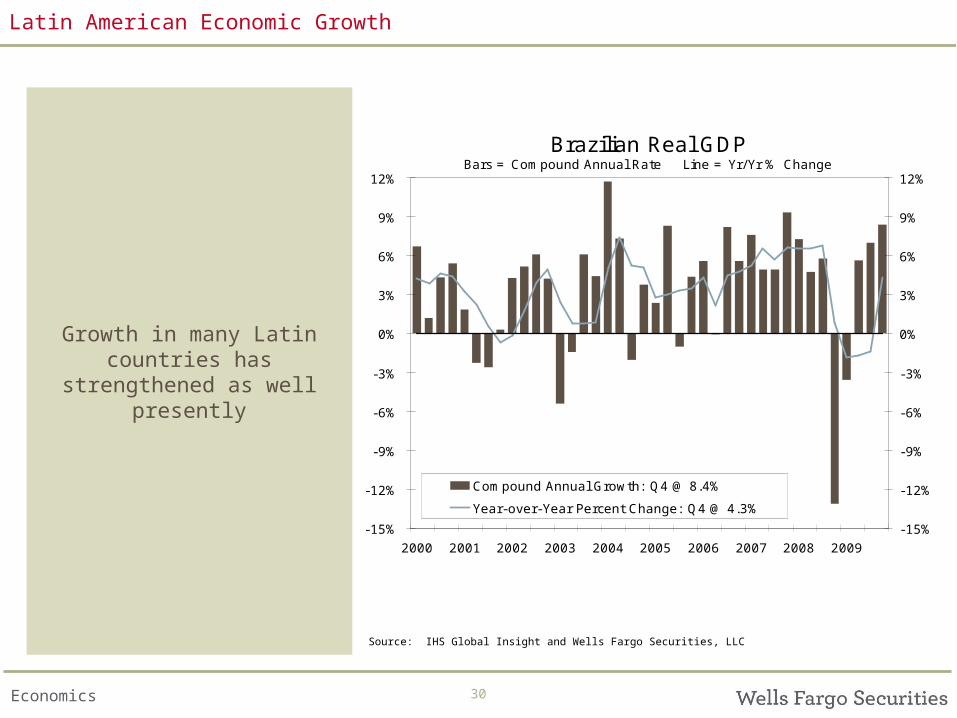

Brazilian Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

Compound Annual Growth: Q4 @ 8.4%

Year-over-Year Percent Change: Q4 @ 4.3%

Latin American Economic Growth

Growth in many Latin countries has strengthened

as well presently

Source: IHS Global Insight and Wells Fargo Securities, LLC

31Economics

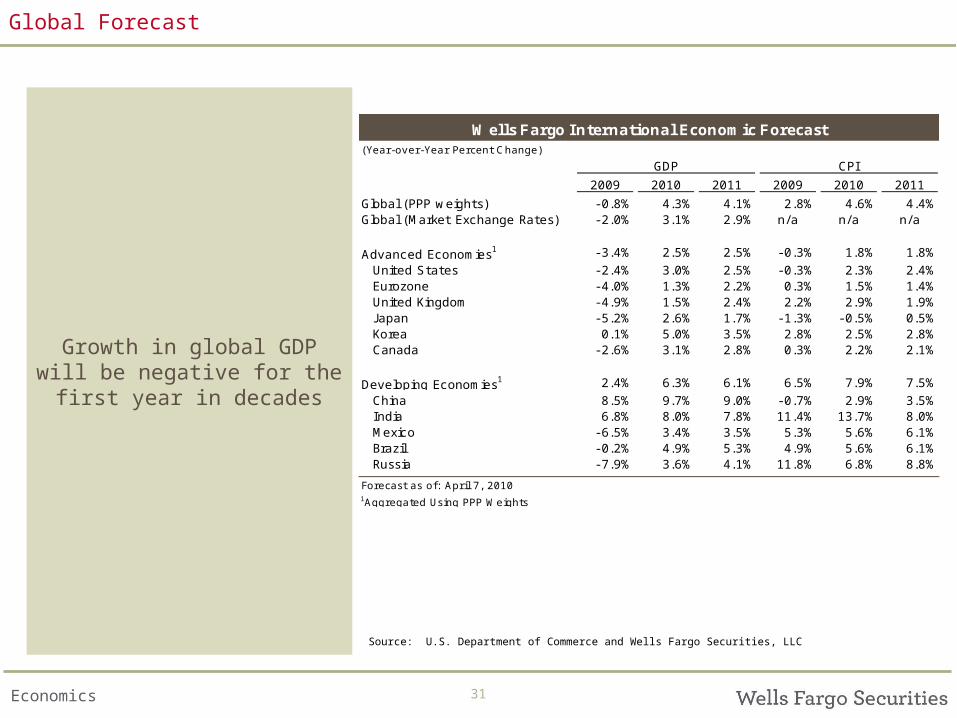

Wells Fargo International Economic Forecast(Year-over-Year Percent Change)

GDP CPI

2009 2010 2011 2009 2010 2011

Global (PPP weights) - 0.8% 4.3% 4.1% 2.8% 4.6% 4.4%Global (Market Exchange Rates) - 2.0% 3.1% 2.9% n/a n/a n/a

Advanced Economies1 - 3.4% 2.5% 2.5% - 0.3% 1.8% 1.8%

United States - 2.4% 3.0% 2.5% - 0.3% 2.3% 2.4%Eurozone - 4.0% 1.3% 2.2% 0.3% 1.5% 1.4%United Kingdom - 4.9% 1.5% 2.4% 2.2% 2.9% 1.9%J apan - 5.2% 2.6% 1.7% - 1.3% - 0.5% 0.5%Korea 0.1% 5.0% 3.5% 2.8% 2.5% 2.8%Canada - 2.6% 3.1% 2.8% 0.3% 2.2% 2.1%

Developing Economies1 2.4% 6.3% 6.1% 6.5% 7.9% 7.5%

China 8.5% 9.7% 9.0% - 0.7% 2.9% 3.5%India 6.8% 8.0% 7.8% 11.4% 13.7% 8.0%Mexico - 6.5% 3.4% 3.5% 5.3% 5.6% 6.1%Brazil - 0.2% 4.9% 5.3% 4.9% 5.6% 6.1%Russia - 7.9% 3.6% 4.1% 11.8% 6.8% 8.8%

Forecast as of: April 7, 20101Aggregated Using PPP Weights

Global Forecast

Growth in global GDP will be negative for the first

year in decades

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

32Economics

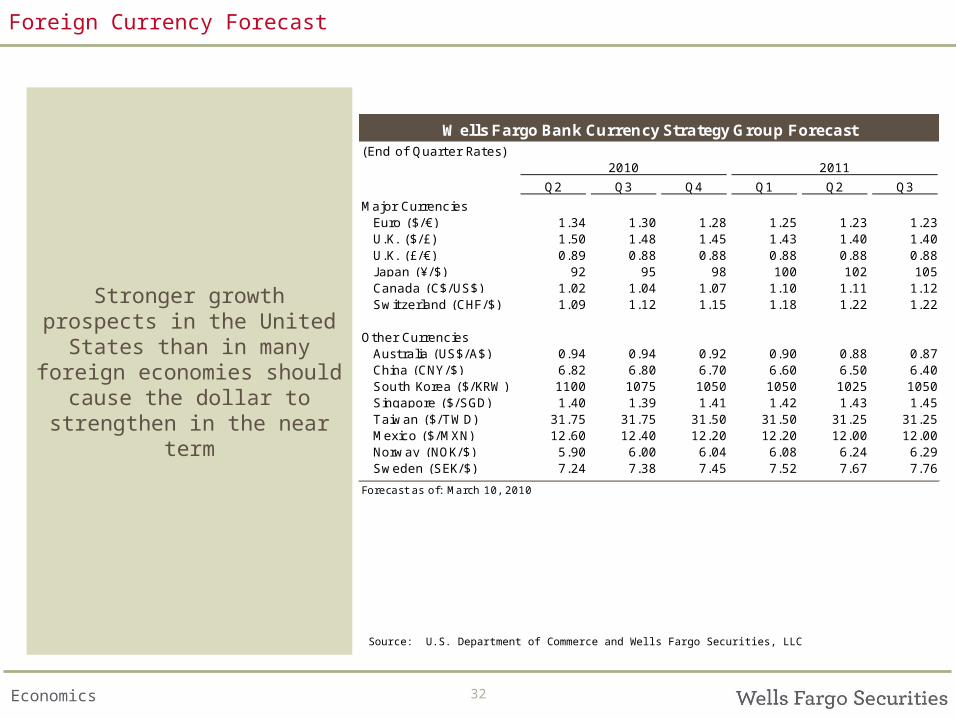

Wells Fargo Bank Currency Strategy Group Forecast(End of Quarter Rates)

2010 2011

Q2 Q3 Q4 Q1 Q2 Q3

Major CurrenciesEuro ($/€) 1.34 1.30 1.28 1.25 1.23 1.23U.K. ($/£) 1.50 1.48 1.45 1.43 1.40 1.40U.K. (£/€) 0.89 0.88 0.88 0.88 0.88 0.88J apan (¥/$) 92 95 98 100 102 105Canada (C$/US$) 1.02 1.04 1.07 1.10 1.11 1.12Switzerland (CHF/$) 1.09 1.12 1.15 1.18 1.22 1.22

Other CurrenciesAustralia (US$/A$) 0.94 0.94 0.92 0.90 0.88 0.87China (CNY/$) 6.82 6.80 6.70 6.60 6.50 6.40South Korea ($/KRW) 1100 1075 1050 1050 1025 1050Singapore ($/SGD) 1.40 1.39 1.41 1.42 1.43 1.45Taiwan ($/TWD) 31.75 31.75 31.50 31.50 31.25 31.25Mexico ($/MXN) 12.60 12.40 12.20 12.20 12.00 12.00Norway (NOK/$) 5.90 6.00 6.04 6.08 6.24 6.29Sweden (SEK/$) 7.24 7.38 7.45 7.52 7.67 7.76

Forecast as of: March 10, 2010

Foreign Currency Forecast

Stronger growth prospects in the United States than in

many foreign economies should cause the dollar to

strengthen in the near term

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

33Economics

The credit crunch caused the U.S. economy to enter its deepest recession in decades. A gradual recovery seems to be taking hold, but business conditions likely will remain challenging for the next few years as consumers retrench.

Most major foreign economies also fell into deep recessions. However, growth seems to be returning abroad as well.

Commodity prices are up from the lows that were reached earlier this year. Prices of most commodities will probably continue to trend higher, but another moonshot in commodity prices, à la 2008, does not seem likely, at least not until global recovery is firmly established.

We project that the dollar will appreciate modestly over the next few quarters versus most major currencies as the U.S. economic recovery prompts foreign buying of higher yielding U.S. assets. “Commodity” and emerging market currencies may weaken a bit in the near term, but they likely will appreciate further on a trend basis as higher levels of risk tolerance causes capital to flow to those countries.

The Federal Reserve will likely maintain an accommodative stance until recovery is firmly established.

Central banks in most major foreign economies have also responded to the crisis by slashing rates. Policy rates in most major countries probably won’t be raised until well into 2010.

Title

Growth Interest Rates

Insert slide callout

Summary of Near-Term Outlook

Summary

34Economics

Diane Schumaker-KriegGlobal Head of Research & Economics

Wells Fargo Securities, LLC Economics Group

John E. Silvia, Ph.D.Chief Economist

[email protected] U.S. Macro Economy Real Estate

U.S. Macro Economy

U.S. Macro Economy

[email protected] Global Economies

Mark VitnerSenior Economist

Jay H. Bryson, Ph.D.Global Economist

Scott Anderson, Ph.D. Senior Economist

Eugenio Aleman, Ph.D. Senior Economist

[email protected] U.S. Macro Economy

[email protected] U.S. Macro Economy Business Investment

U.S. Macro Economy

[email protected] Global Economies Business Investment

Ed KashmarekEconomist

Tim QuinlanEconomist

Kim WhelanEconomic Analyst

Yasmine KamaruddinEconomic Analyst

[email protected] U.S. Macro Economy Financial Services

[email protected] Quantitative Macro-

Economic Modeling

[email protected] U.S. Consumer Real Estate

[email protected] Real Estate Retail & Automotive

Sam BullardEconomist

Anika KhanEconomist

Azhar IqbalEconometrician

Adam G. YorkEconomist

Wells Fargo Securities Economics Group publications are produced by Wells Fargo Securities, LLC, a U.S broker-dealer registered with the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority, and the Securities Investor Protection Corp. Wells Fargo Securities, LLC, distributes these publications directly and through subsidiaries including, but not limited to, Wells Fargo & Company, Wachovia Bank N.A., Wells Fargo Bank N.A, Wells Fargo Advisors, LLC, and Wells Fargo Securities International Limited. The information and opinions herein are for general information use only. Wells Fargo Securities, LLC does not guarantee their accuracy or completeness, nor does Wells Fargo Securities, LLC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. Wells Fargo Securities, LLC is a separate legal entity and distinct from affiliated banks and is a wholly owned subsidiary of Wells Fargo & Company © 2010 Wells Fargo Securities, LLC.

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE