Embed Size (px)

Citation preview

U.S. Economic Outlook and Monetary Policy

Bank of Portugal February 24, 2014

Spencer Krane Senior Vice President, Federal Reserve Bank of Chicago The views expressed are my own and not those of the Federal Reserve Bank of Chicago or the Federal Reserve System

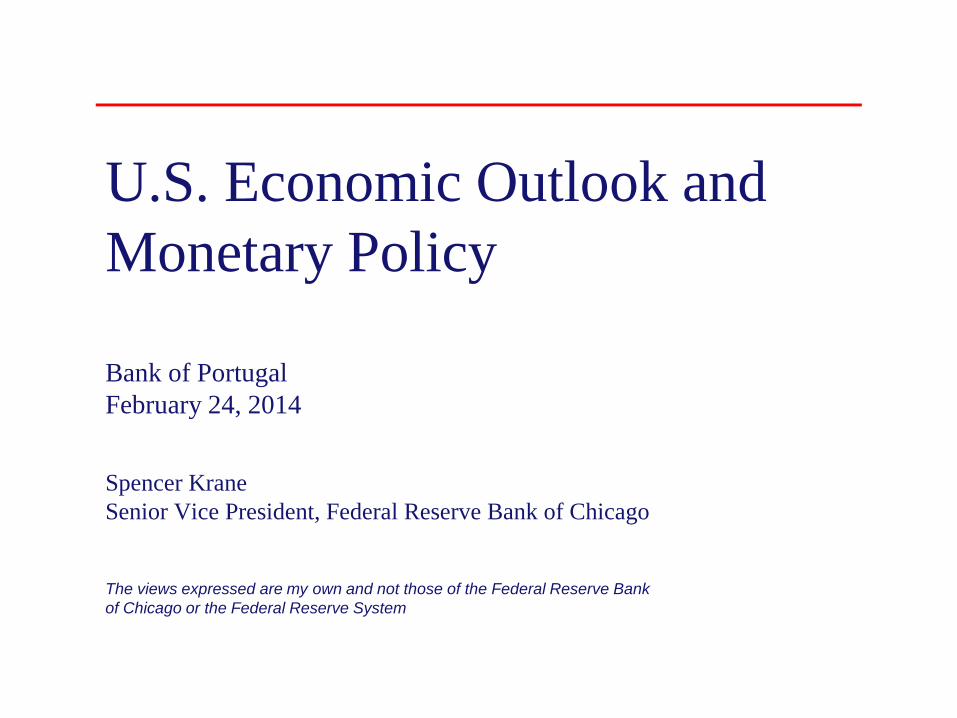

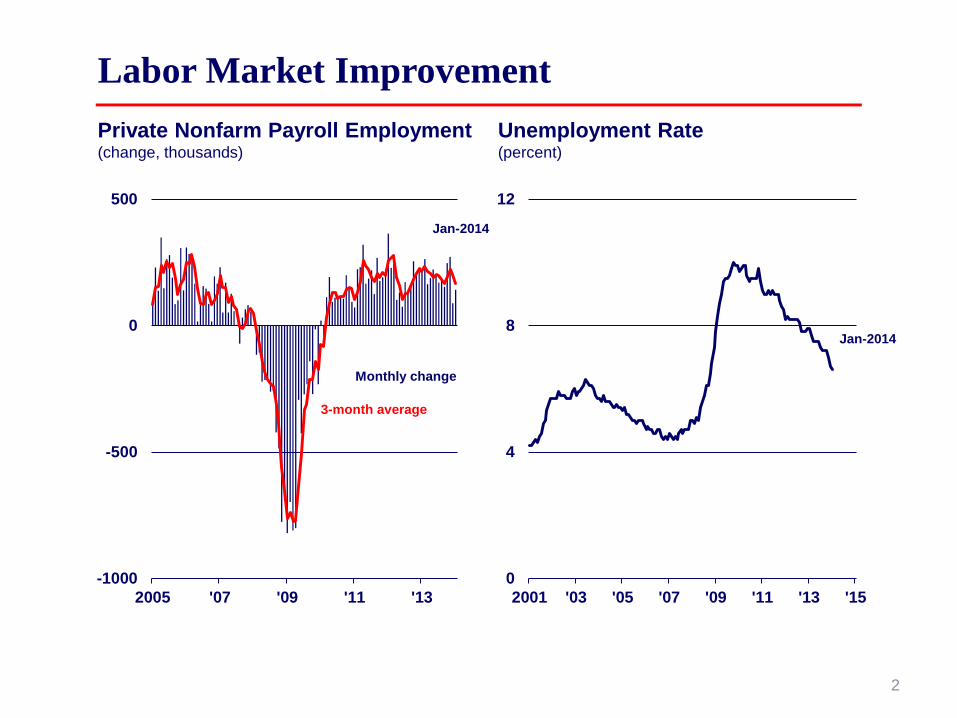

Overview Recent developments

– Data on activity mixed – Significant cumulative improvement in labor markets since 9/12 – Inflation remains very low

Outlook – Moderately above trend growth in 2014, better 2015 – Gradual updrift in inflation

Monetary policy at the zero lower bound – Forward guidance – Large scale asset purchases

1

0

4

8

12

2001 '03 '05 '07 '09 '11 '13 '15-1000

-500

0

500

2005 '07 '09 '11 '13

Labor Market Improvement Private Nonfarm Payroll Employment (change, thousands)

Unemployment Rate (percent)

Monthly change

3-month average

Jan-2014

Jan-2014

2

0

4

8

12

2001 '03 '05 '07 '09 '11 '13 '15-1000

-500

0

500

2005 '07 '09 '11 '13

Labor Market Improvement Private Nonfarm Payroll Employment (change, thousands)

Unemployment Rate (percent)

Monthly change

3-month average

Jan-2014

Jan-2014

FOMC long run

Aug-2012

3

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

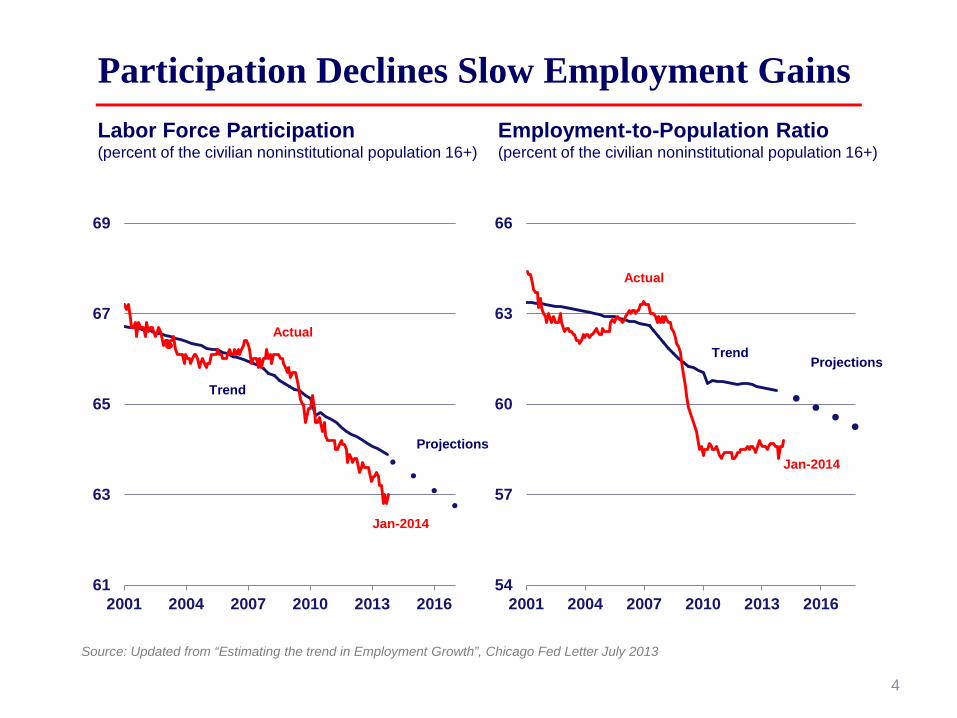

61

63

65

67

69

2001 2004 2007 2010 2013 2016

Jan-2014 19

8019

8219

8419

8619

8819

9019

9219

9419

9619

9820

0020

0220

0420

0620

0820

1020

1220

1420

1620

1820

20

54

57

60

63

66

2001 2004 2007 2010 2013 2016

Jan-2014

Participation Declines Slow Employment Gains

Source: Updated from “Estimating the trend in Employment Growth”, Chicago Fed Letter July 2013

Labor Force Participation (percent of the civilian noninstitutional population 16+)

Trend

Actual

Projections

Employment-to-Population Ratio (percent of the civilian noninstitutional population 16+)

Trend Projections

Actual

4

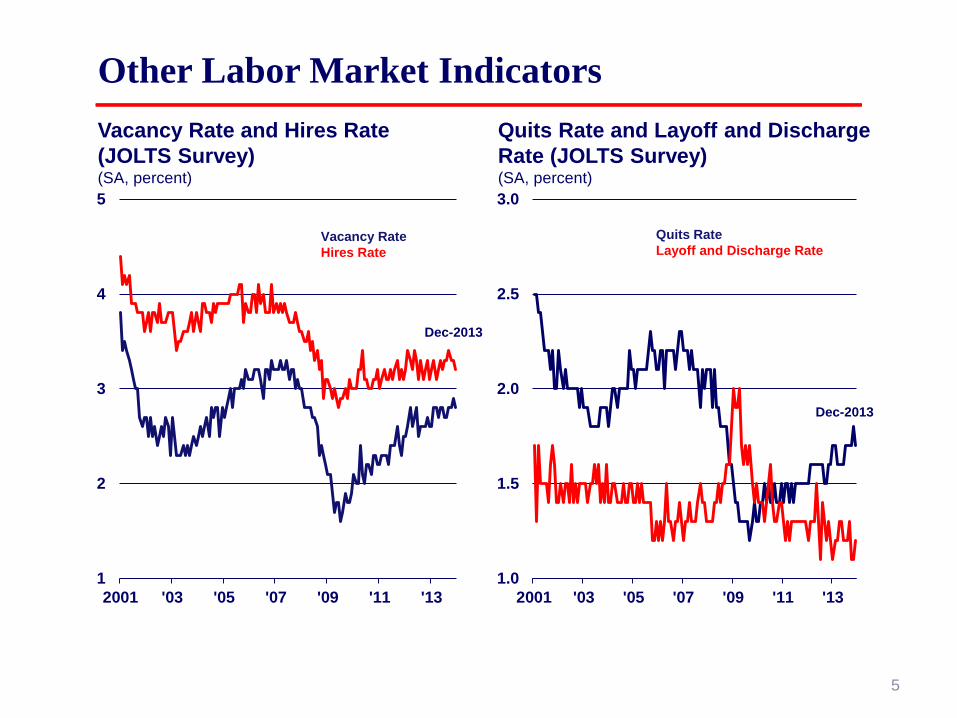

1.0

1.5

2.0

2.5

3.0

2001 '03 '05 '07 '09 '11 '131

2

3

4

5

2001 '03 '05 '07 '09 '11 '13

Other Labor Market Indicators Quits Rate and Layoff and Discharge Rate (JOLTS Survey) (SA, percent)

Vacancy Rate and Hires Rate (JOLTS Survey) (SA, percent)

Dec-2013

Dec-2013

Vacancy Rate Hires Rate

Quits Rate Layoff and Discharge Rate

5

0

50

100

150

200

250

0

400

800

1200

1600

2000

2000 '02 '04 '06 '08 '10 '12 '14

Consumption and Housing Housing Permits and Home Prices (millions of units, annual rate; Q1-2000=100)

Single Family Housing Permits CoreLogic Home Price Index

Jan-2014

-6

-4

-2

0

2

4

6

2007 '08 '09 '10 '11 '12 '13 '14

Q1-2014

Personal Consumption Expenditures (percent change, annual rate)

Dec-2013

2014 Q1 Estimate from the Survey of Professional Forecasters, Feb. 2014

6

Household Balance Sheets: Crisis and Aftermath

400

550

700

1985 '90 '95 '00 '05 '10

Household Net Worth (percent of disposable income)

Q3-2013

Household Liabilities and Homes with Mortgages in Negative Equity (percent of disposable income; millions of units)

0

10

20

50

100

150

1985 '90 '95 '00 '05 '10

Household Liabilities Single-Family Homes with Mortgages in Negative Equity

Q3-2013

7

Business Investment Indicators

45

50

55

60

65

70

2000 '02 '04 '06 '08 '10 '12

Nondefense Capital Goods ex. Aircraft (Bils. $, 3-month MA)

Nonresidential Private Construction (Bils. $)

Shipments New Orders

Dec-2013

200

250

300

350

400

450

2000 '02 '04 '06 '08 '10 '12

Dec-2013

8

-1

-0.5

0

0.5

1

2008 '09 '10 '11 '12 '13

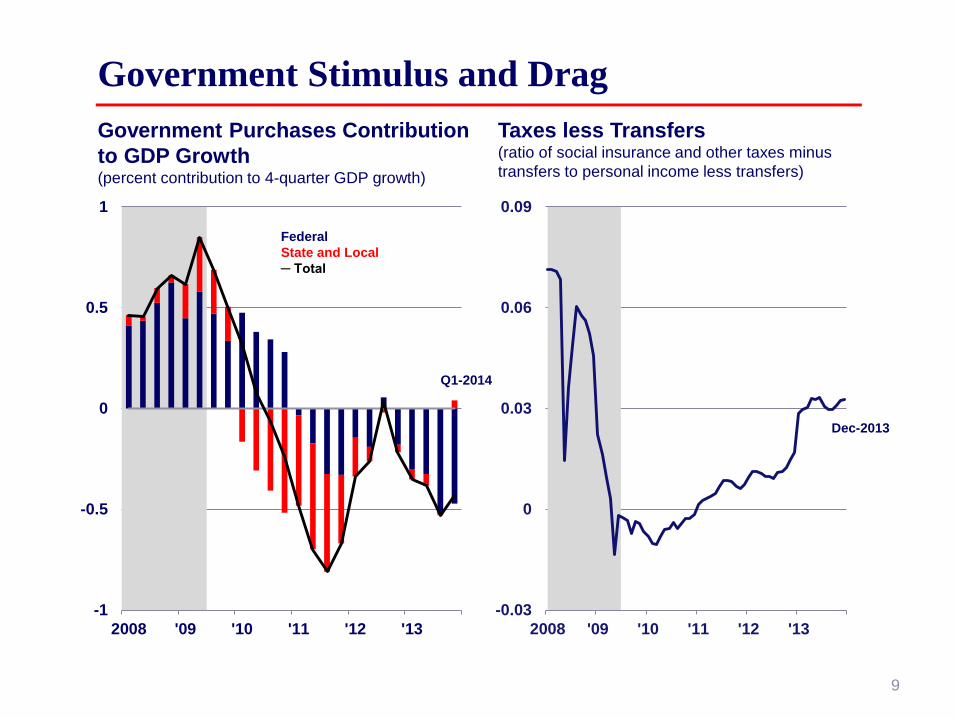

Government Stimulus and Drag

Federal State and Local ─ Total

Government Purchases Contribution to GDP Growth (percent contribution to 4-quarter GDP growth)

Q1-2014

Taxes less Transfers (ratio of social insurance and other taxes minus transfers to personal income less transfers)

-0.03

0

0.03

0.06

0.09

2008 '09 '10 '11 '12 '13

Dec-2013

9

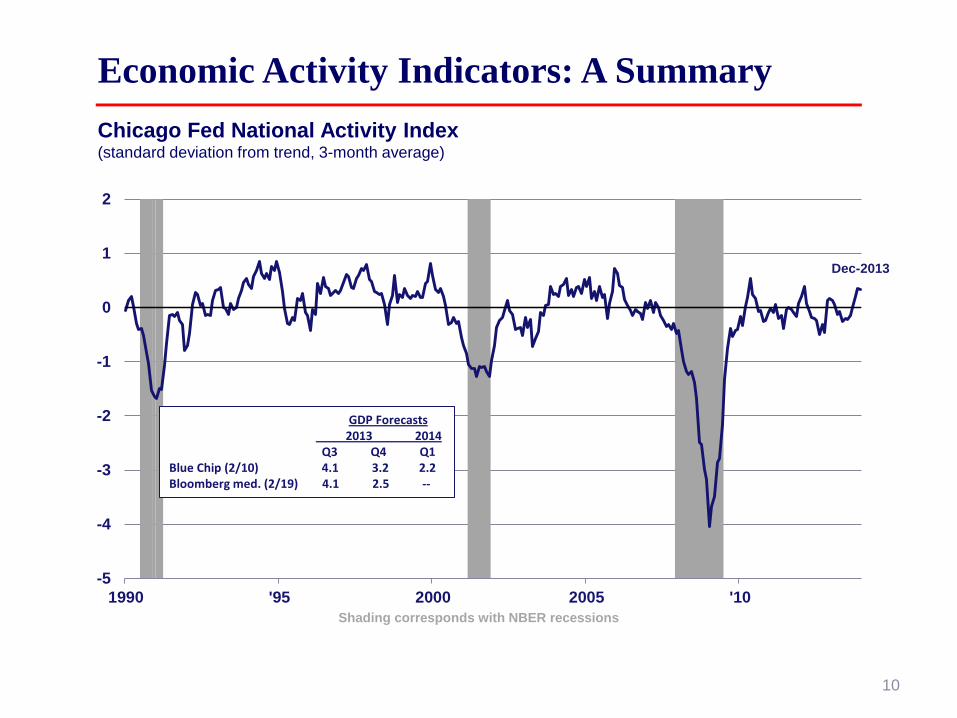

-5

-4

-3

-2

-1

0

1

2

1990 '95 2000 2005 '10

Economic Activity Indicators: A Summary Chicago Fed National Activity Index (standard deviation from trend, 3-month average)

Shading corresponds with NBER recessions

Dec-2013

GDP Forecasts 2013 2014 Q3 Q4 Q1 Blue Chip (2/10) 4.1 3.2 2.2 Bloomberg med. (2/19) 4.1 2.5 --

10

2013 2014 2015 2016

FOMC (12/19)

GDP1 2.25

(2.2, 2.3)

3.05

(2.8, 3.2)

3.25

(3.0, 3.4)

3.05

(2.5, 3.2)

Unemploy. 2 7.05

(7.0, 7.1)

6.45

(6.3, 6.6)

5.85

(5.8, 6.1)

5.45

(5.3, 5.8)

Blue Chip (2/10)

GDP1 2.7 2.7 3.0

Unemploy.2 7.0 6.4 5.9 FOMC forecasts are pseudo medians; central tendency in parentheses. 1. Percent change, Q4 to Q4 2. Fourth-quarter average

Medium Term Forecasts

11

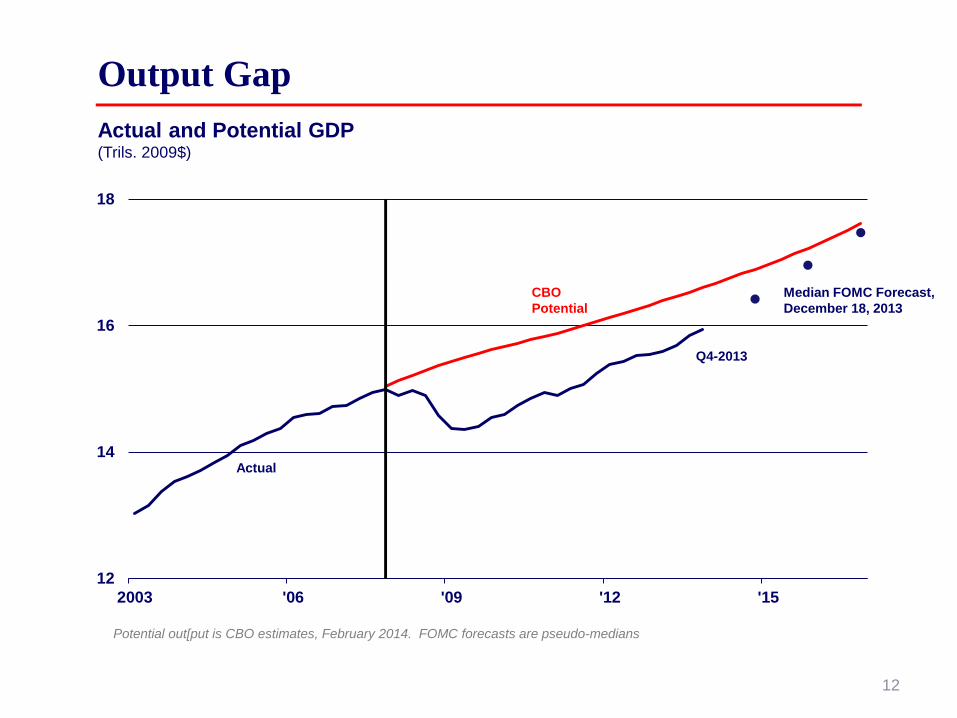

12

14

16

18

2003 '06 '09 '12 '15

Output Gap Actual and Potential GDP (Trils. 2009$)

Q4-2013

Median FOMC Forecast, December 18, 2013

Actual

CBO Potential

Potential out[put is CBO estimates, February 2014. FOMC forecasts are pseudo-medians

12

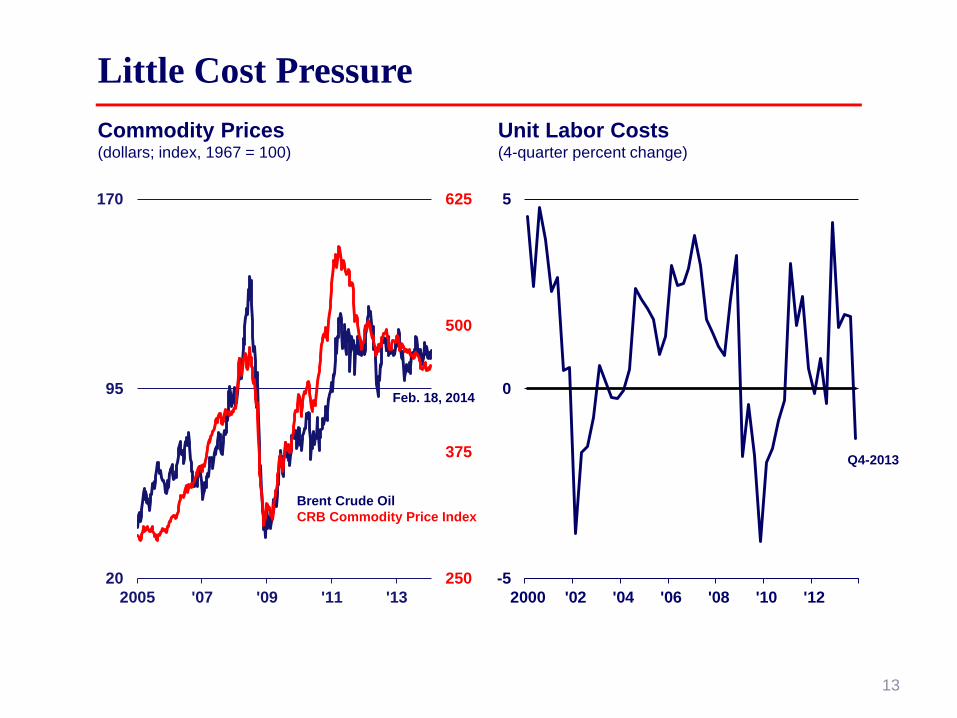

250

375

500

625

20

95

170

2005 '07 '09 '11 '13

Brent Crude Oil CRB Commodity Price Index

-5

0

5

2000 '02 '04 '06 '08 '10 '12

Little Cost Pressure Unit Labor Costs (4-quarter percent change)

Feb. 18, 2014

Q4-2013

Commodity Prices (dollars; index, 1967 = 100)

13

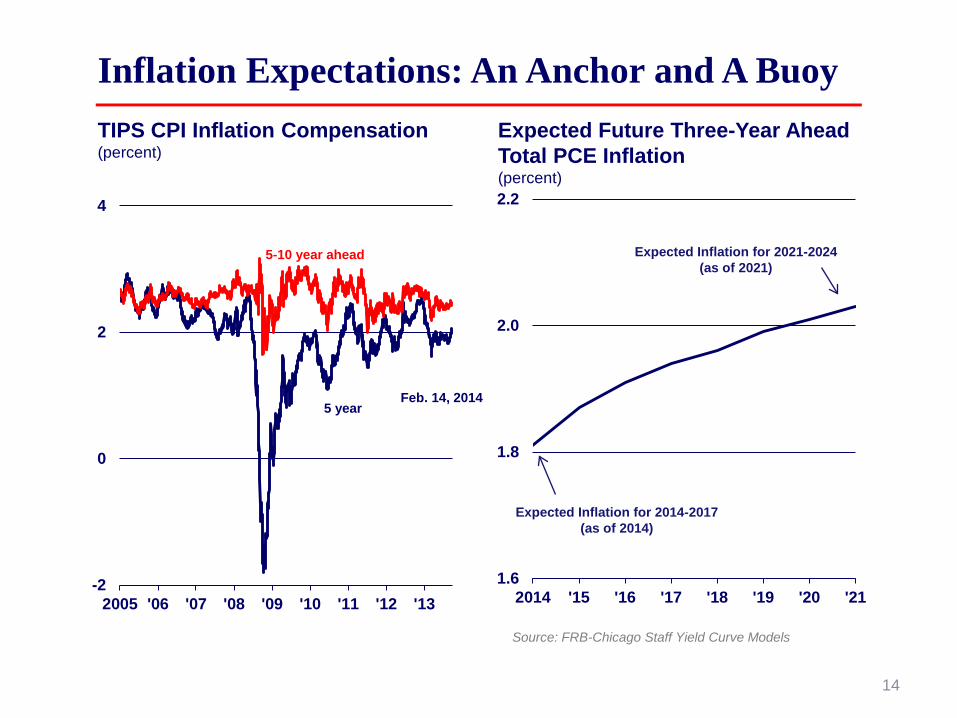

-2

0

2

4

2005 '06 '07 '08 '09 '10 '11 '12 '131.6

1.8

2.0

2.2

2014 '15 '16 '17 '18 '19 '20 '21

Inflation Expectations: An Anchor and A Buoy

Feb. 14, 2014

TIPS CPI Inflation Compensation (percent)

5 year

5-10 year ahead Expected Inflation for 2021-2024 (as of 2021)

Expected Inflation for 2014-2017 (as of 2014)

Expected Future Three-Year Ahead Total PCE Inflation (percent)

Source: FRB-Chicago Staff Yield Curve Models

14

Inflation Low; Expected to Return to Target PCE Price Index (percent)

-2

-1

0

1

2

3

4

5

1999 '02 '05 '08 '11 '14 '16

Target for Total PCE

Total

Core

Dec-2013

FOMC Forecasts* (December 18, 2013)

*Pseudo-medians of the forecasts made by the FOMC participants 15

-5

0

5

10

1989 1994 1999 2004 2009

Fed Funds Rate (percent)

History

Q4-2013

Policy Rate Constrained by Zero Lower Bound

Taylor (1999) Rule based on inflation and output gap

Taylor Rule based on CBO output gap, SPF long-run inflation forecast (before 2009), and FOMC SEP long-run inflation target (after 2009)

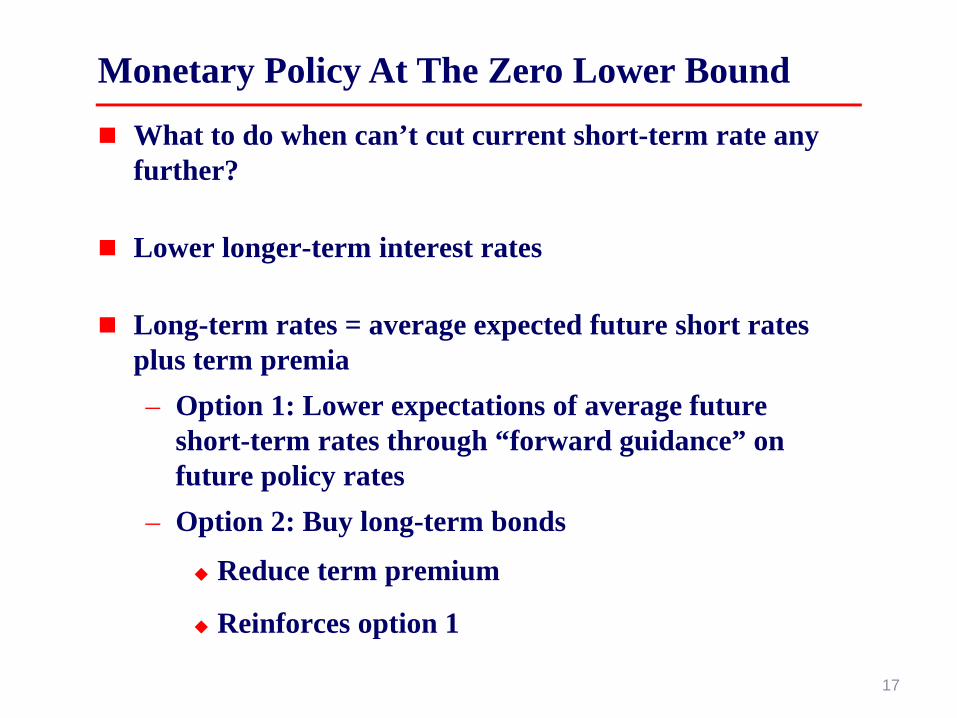

16

What to do when can’t cut current short-term rate any further?

Lower longer-term interest rates

Long-term rates = average expected future short rates plus term premia – Option 1: Lower expectations of average future

short-term rates through “forward guidance” on future policy rates

– Option 2: Buy long-term bonds

Reduce term premium

Reinforces option 1

Monetary Policy At The Zero Lower Bound

17

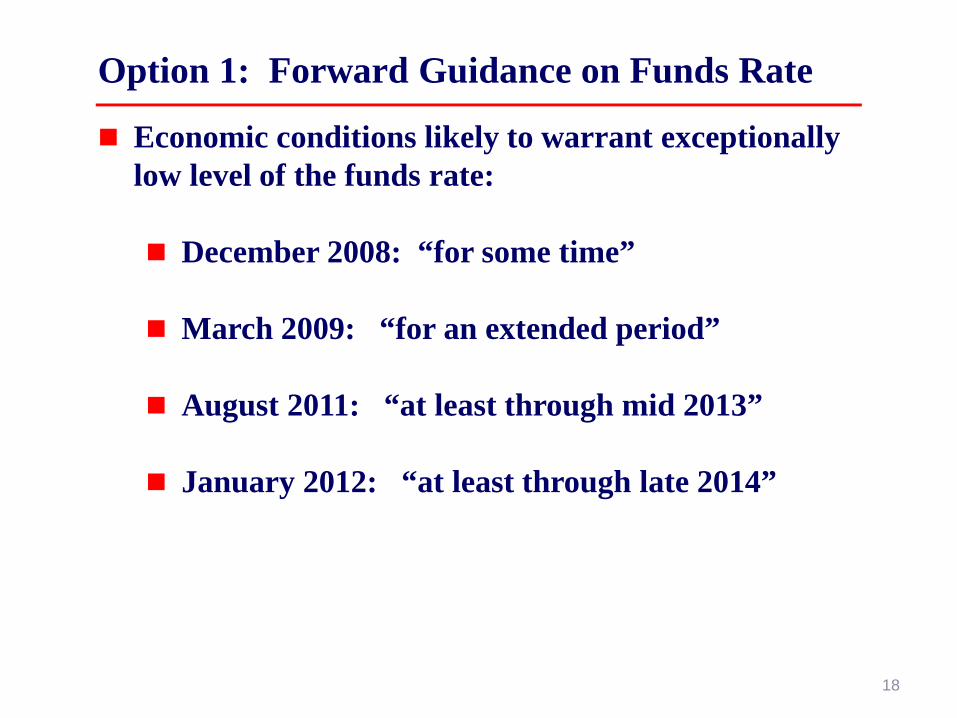

Option 1: Forward Guidance on Funds Rate

Economic conditions likely to warrant exceptionally low level of the funds rate:

December 2008: “for some time”

March 2009: “for an extended period”

August 2011: “at least through mid 2013”

January 2012: “at least through late 2014”

18

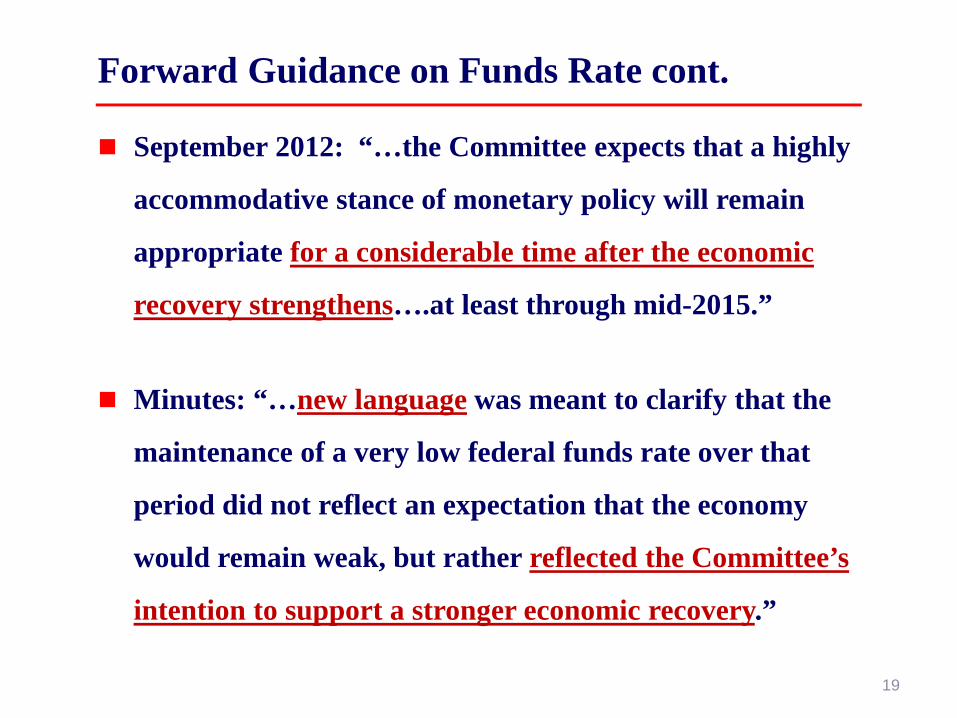

Forward Guidance on Funds Rate cont.

September 2012: “…the Committee expects that a highly

accommodative stance of monetary policy will remain

appropriate for a considerable time after the economic

recovery strengthens….at least through mid-2015.”

Minutes: “…new language was meant to clarify that the

maintenance of a very low federal funds rate over that

period did not reflect an expectation that the economy

would remain weak, but rather reflected the Committee’s

intention to support a stronger economic recovery.”

19

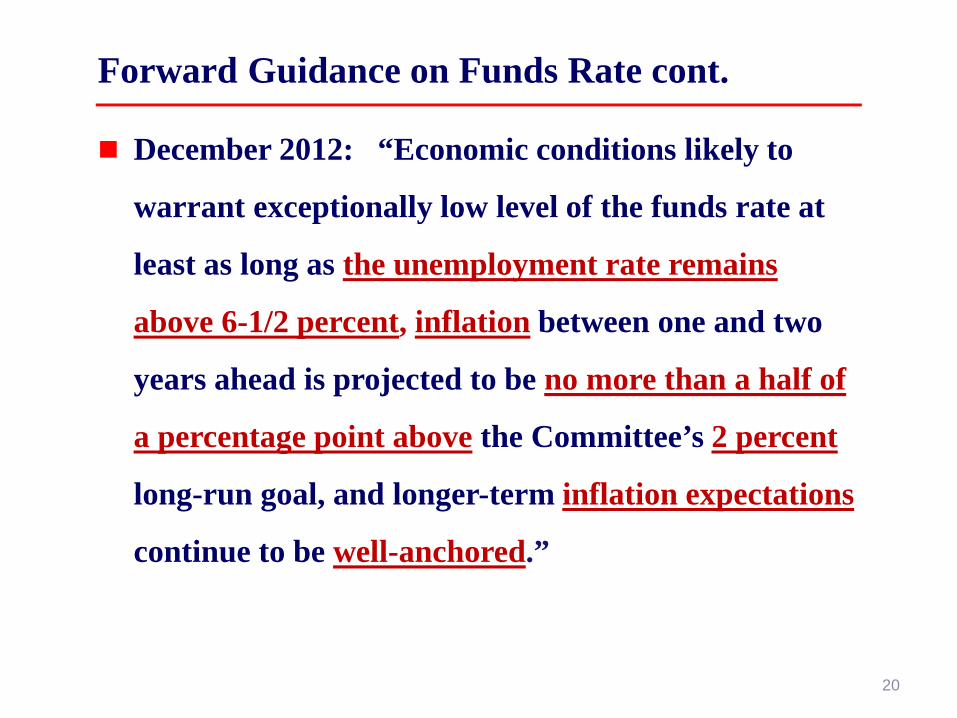

Forward Guidance on Funds Rate cont.

December 2012: “Economic conditions likely to

warrant exceptionally low level of the funds rate at

least as long as the unemployment rate remains

above 6-1/2 percent, inflation between one and two

years ahead is projected to be no more than a half of

a percentage point above the Committee’s 2 percent

long-run goal, and longer-term inflation expectations

continue to be well-anchored.”

20

Forward Guidance on Funds Rate cont.

December 2012 cont: “In determining how long to

maintain a highly accommodative stance of monetary

policy, the Committee will also consider other

information, including additional measures of labor

market conditions, indicators of inflation pressures

and inflation expectations, and readings on financial

developments.”

21

Forward Guidance on Funds Rate cont.

December 2013: “The Committee now anticipates,

based on its assessment of these factors, that it likely

will be appropriate to maintain the current target

range for the federal funds rate well past the time

that the unemployment rate declines below 6-1/2

percent, especially if projected inflation continues to

run below the Committee's 2 percent longer-run

goal.”

22

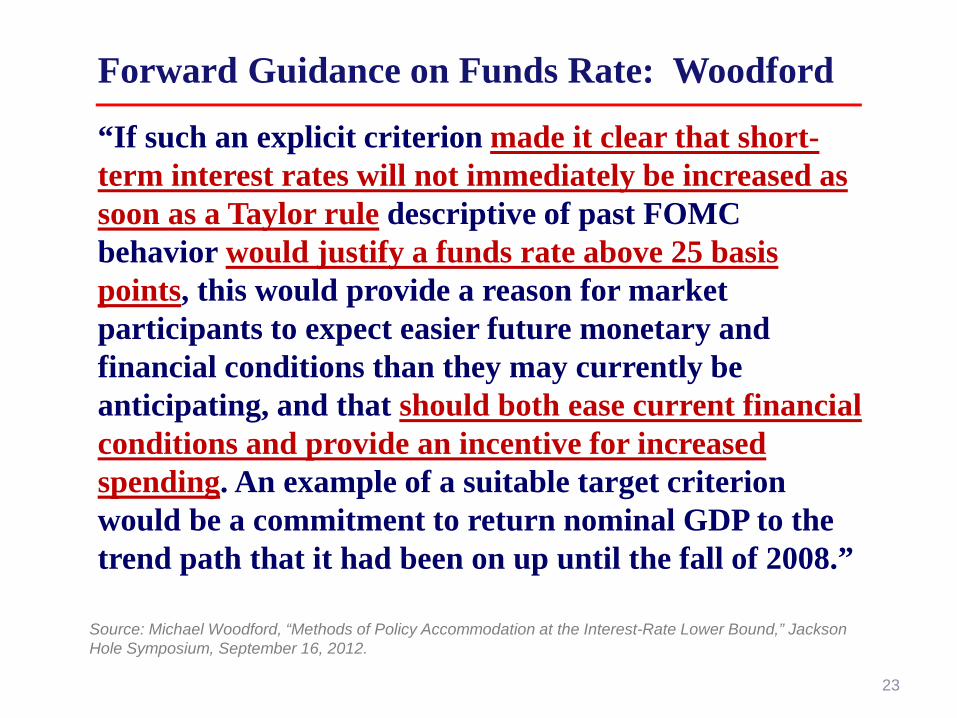

Forward Guidance on Funds Rate: Woodford

“If such an explicit criterion made it clear that short-term interest rates will not immediately be increased as soon as a Taylor rule descriptive of past FOMC behavior would justify a funds rate above 25 basis points, this would provide a reason for market participants to expect easier future monetary and financial conditions than they may currently be anticipating, and that should both ease current financial conditions and provide an incentive for increased spending. An example of a suitable target criterion would be a commitment to return nominal GDP to the trend path that it had been on up until the fall of 2008.”

Source: Michael Woodford, “Methods of Policy Accommodation at the Interest-Rate Lower Bound,” Jackson Hole Symposium, September 16, 2012.

23

Forward Guidance on Funds Rate cont.

October 2013 Minutes: “…statement could indicate

… anticipated keeping the rate below its longer-run

equilibrium value for some time, as economic

headwinds were likely to diminish only slowly. Other

factors … also mentioned as possibly providing a

rationale for maintaining a low trajectory for the

federal funds rate, including following through on a

commitment to support the economy by maintaining

more-accommodative policy for longer.

24

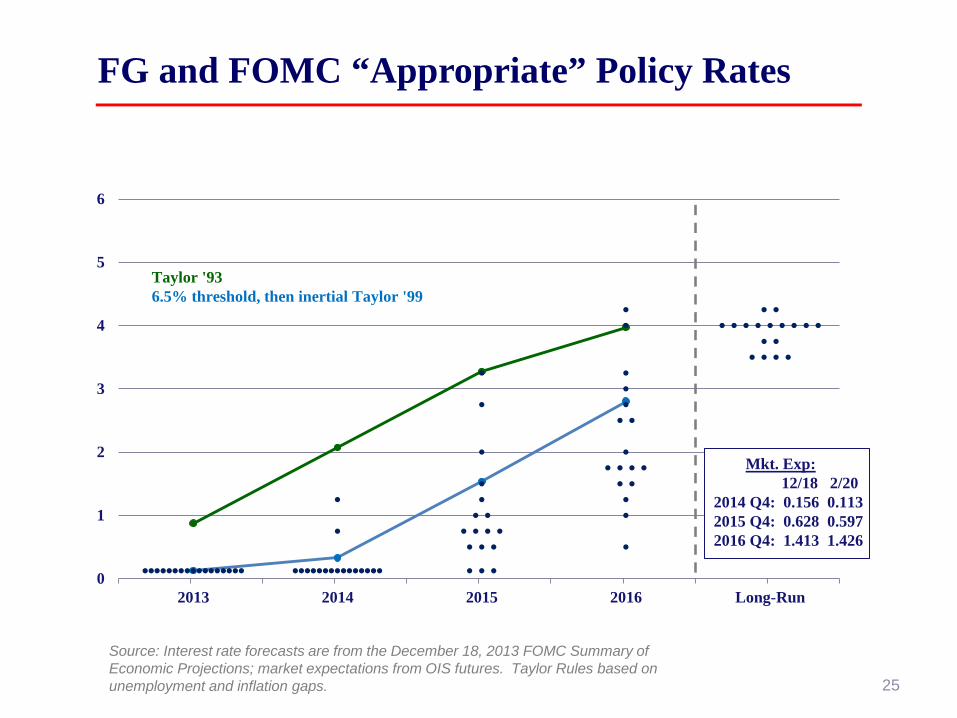

0

1

2

3

4

5

6

2013 2014 2015 2016 Long-Run

Taylor '93 6.5% threshold, then inertial Taylor '99

Mkt. Exp: 12/18 2/20 2014 Q4: 0.156 0.113 2015 Q4: 0.628 0.597 2016 Q4: 1.413 1.426

FG and FOMC “Appropriate” Policy Rates

Source: Interest rate forecasts are from the December 18, 2013 FOMC Summary of Economic Projections; market expectations from OIS futures. Taylor Rules based on unemployment and inflation gaps. 25

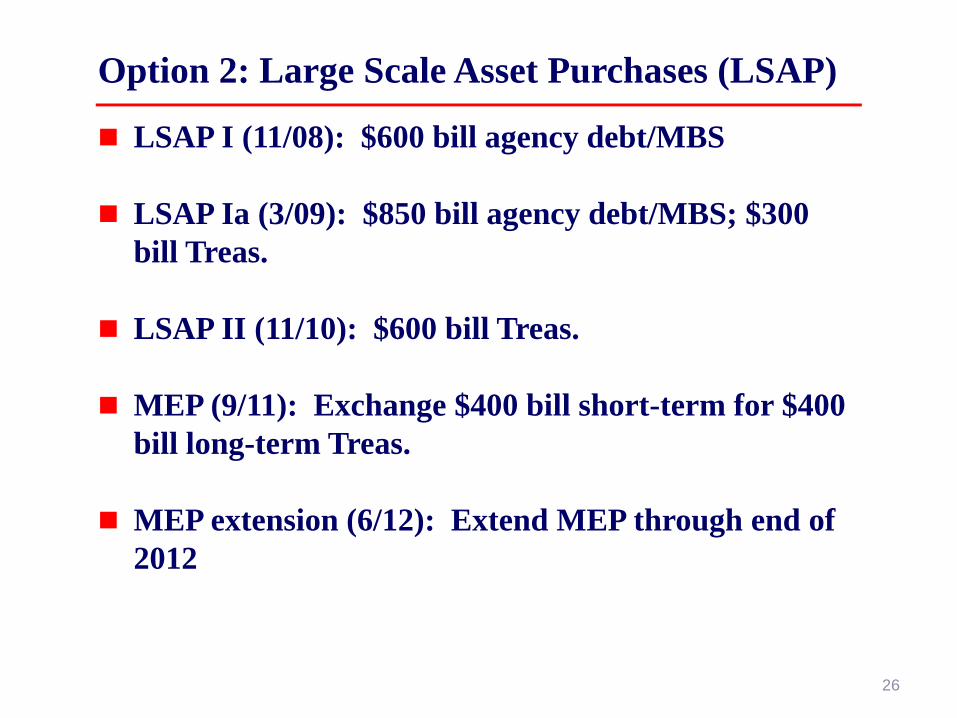

Option 2: Large Scale Asset Purchases (LSAP)

LSAP I (11/08): $600 bill agency debt/MBS

LSAP Ia (3/09): $850 bill agency debt/MBS; $300 bill Treas.

LSAP II (11/10): $600 bill Treas.

MEP (9/11): Exchange $400 bill short-term for $400 bill long-term Treas.

MEP extension (6/12): Extend MEP through end of 2012

26

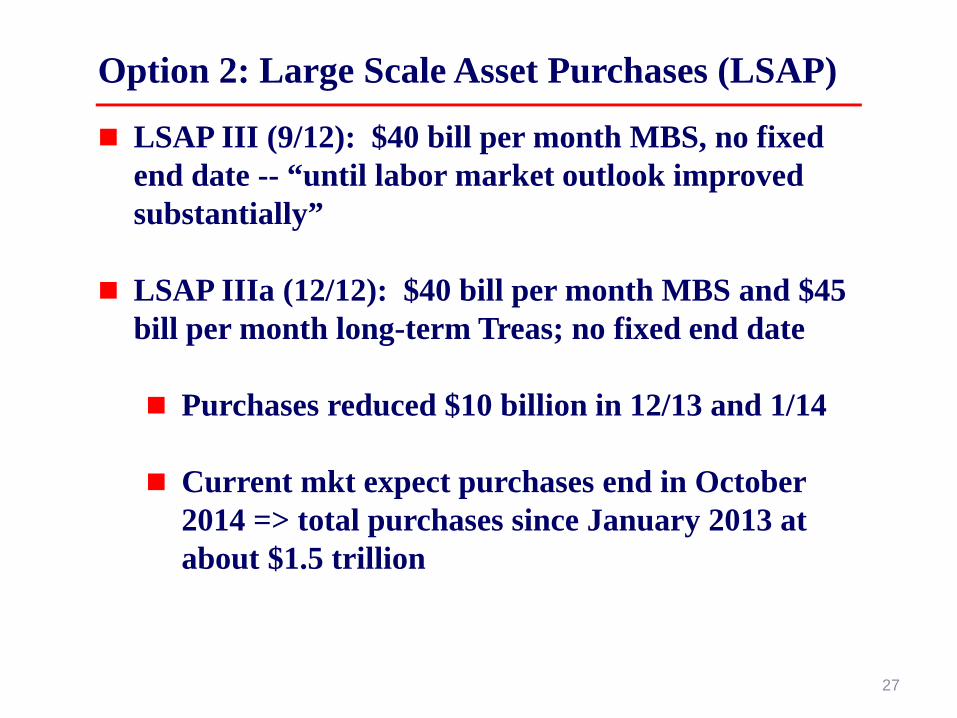

Option 2: Large Scale Asset Purchases (LSAP)

LSAP III (9/12): $40 bill per month MBS, no fixed end date -- “until labor market outlook improved substantially”

LSAP IIIa (12/12): $40 bill per month MBS and $45 bill per month long-term Treas; no fixed end date

Purchases reduced $10 billion in 12/13 and 1/14

Current mkt expect purchases end in October 2014 => total purchases since January 2013 at about $1.5 trillion

27

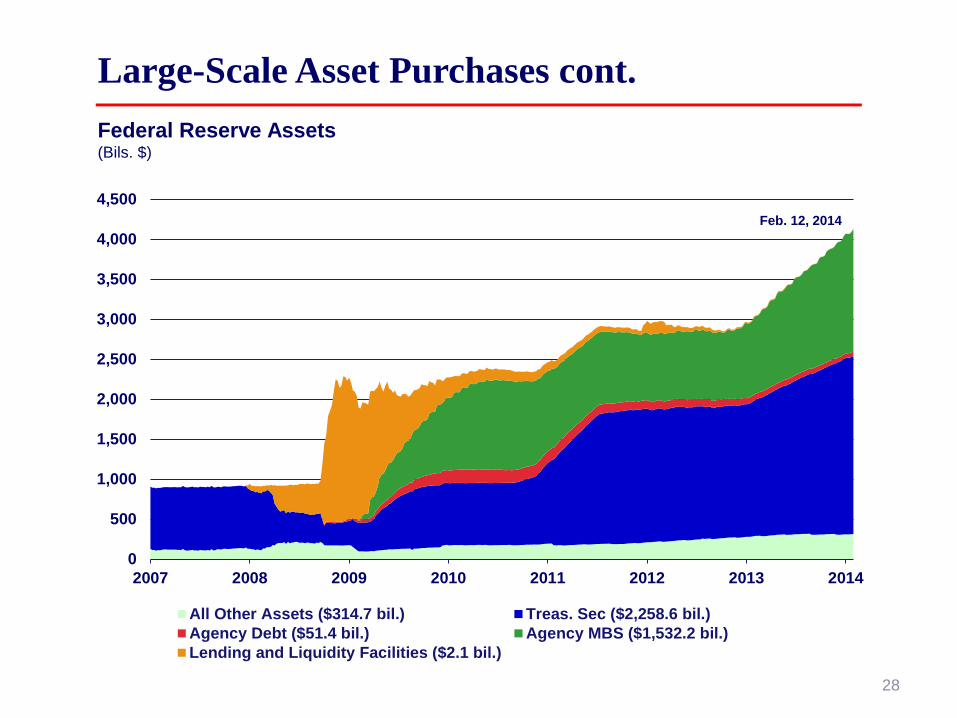

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2007 2008 2009 2010 2011 2012 2013 2014

All Other Assets ($314.7 bil.) Treas. Sec ($2,258.6 bil.)Agency Debt ($51.4 bil.) Agency MBS ($1,532.2 bil.)Lending and Liquidity Facilities ($2.1 bil.)

Large-Scale Asset Purchases cont. Federal Reserve Assets (Bils. $)

Feb. 12, 2014

28

Long-Term Rates Down Significantly

0

5

10

2007 '08 '09 '10 '11 '12 '13 '14

10-Year Treasury Conventional 30-Year Mortgages 48-Month New Car Loans BBB Corporate Bonds

Feb. 14, 2014

29

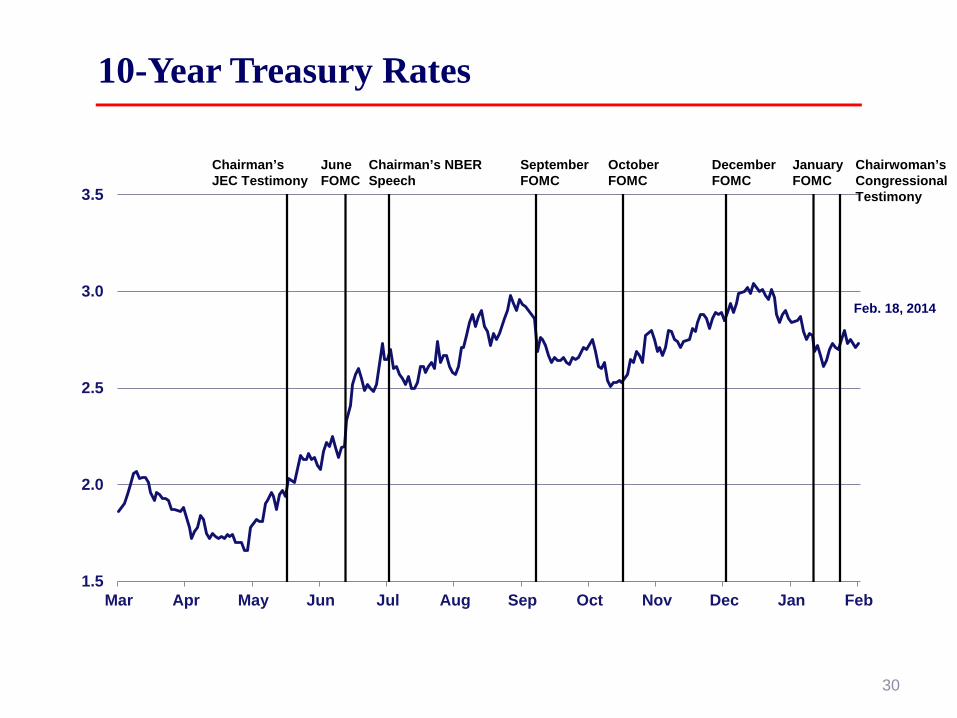

1.5

2.0

2.5

3.0

3.5

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

10-Year Treasury Rates

Feb. 18, 2014

Chairman’s JEC Testimony

September FOMC

June FOMC

Chairman’s NBER Speech

October FOMC

December FOMC

January FOMC

Chairwoman’s Congressional Testimony

30

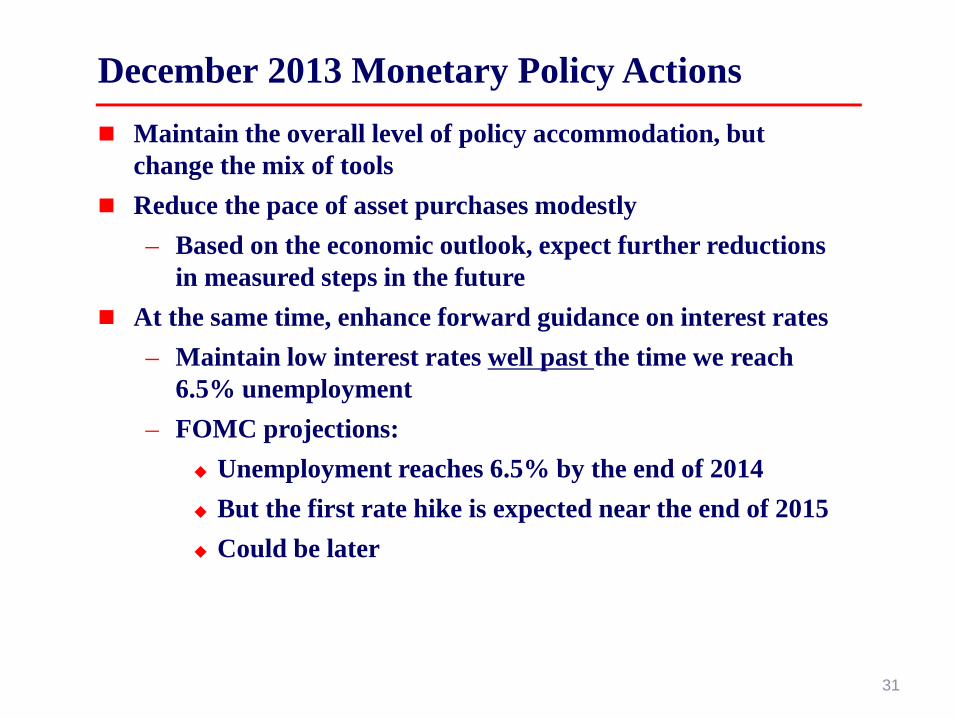

Maintain the overall level of policy accommodation, but change the mix of tools

Reduce the pace of asset purchases modestly – Based on the economic outlook, expect further reductions

in measured steps in the future At the same time, enhance forward guidance on interest rates

– Maintain low interest rates well past the time we reach 6.5% unemployment

– FOMC projections: Unemployment reaches 6.5% by the end of 2014 But the first rate hike is expected near the end of 2015 Could be later

December 2013 Monetary Policy Actions

31

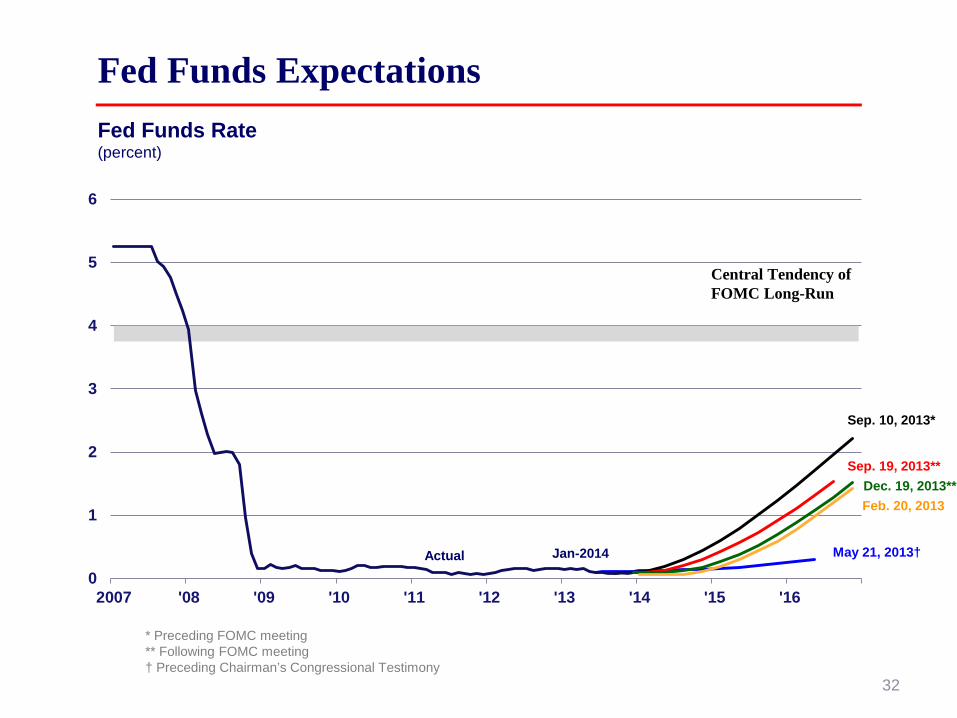

0

1

2

3

4

5

6

2007 '08 '09 '10 '11 '12 '13 '14 '15 '16

Central Tendency of FOMC Long-Run

Fed Funds Rate (percent)

Fed Funds Expectations

May 21, 2013† Jan-2014

Sep. 10, 2013*

Sep. 19, 2013**

Actual

Dec. 19, 2013**

* Preceding FOMC meeting ** Following FOMC meeting † Preceding Chairman’s Congressional Testimony

Feb. 20, 2013

32

Appendix

33

Empirical Facts about Term Premia

Source: Ben Bernanke, “Long-Term Interest Rates,” San Francisco, March 1, 2013 34

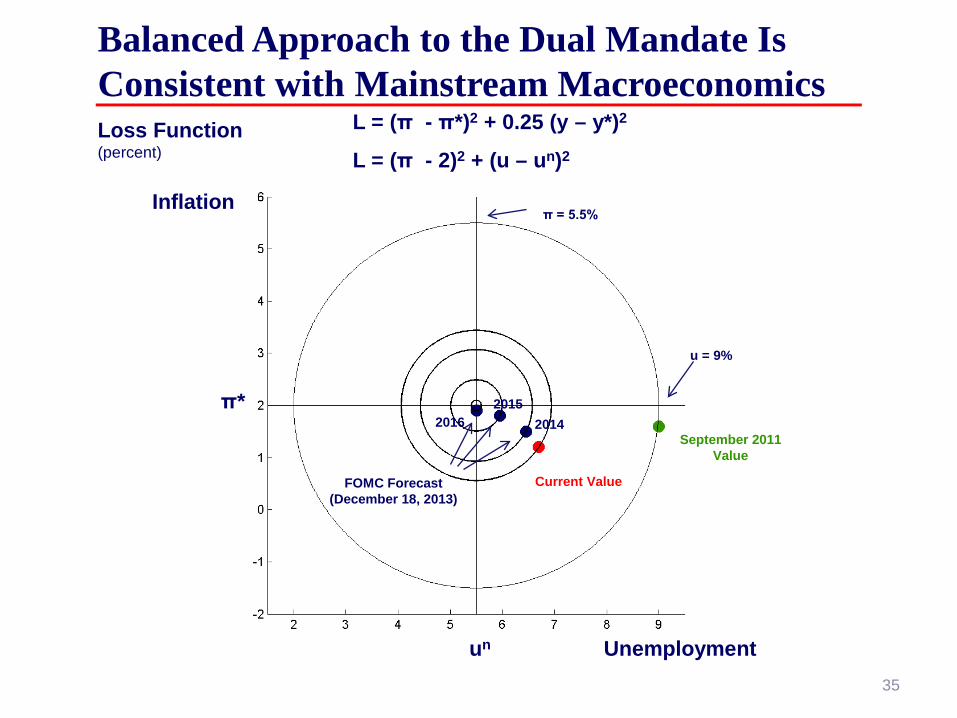

Balanced Approach to the Dual Mandate Is Consistent with Mainstream Macroeconomics Loss Function (percent)

L = (π - π*)2 + 0.25 (y – y*)2

L = (π - 2)2 + (u – un)2

FOMC Forecast (December 18, 2013)

Current Value

u = 9%

September 2011 Value

π = 5.5%

2016 2014 2015 π*

un

Inflation

Unemployment

35

0

1

2

3

4

5

6

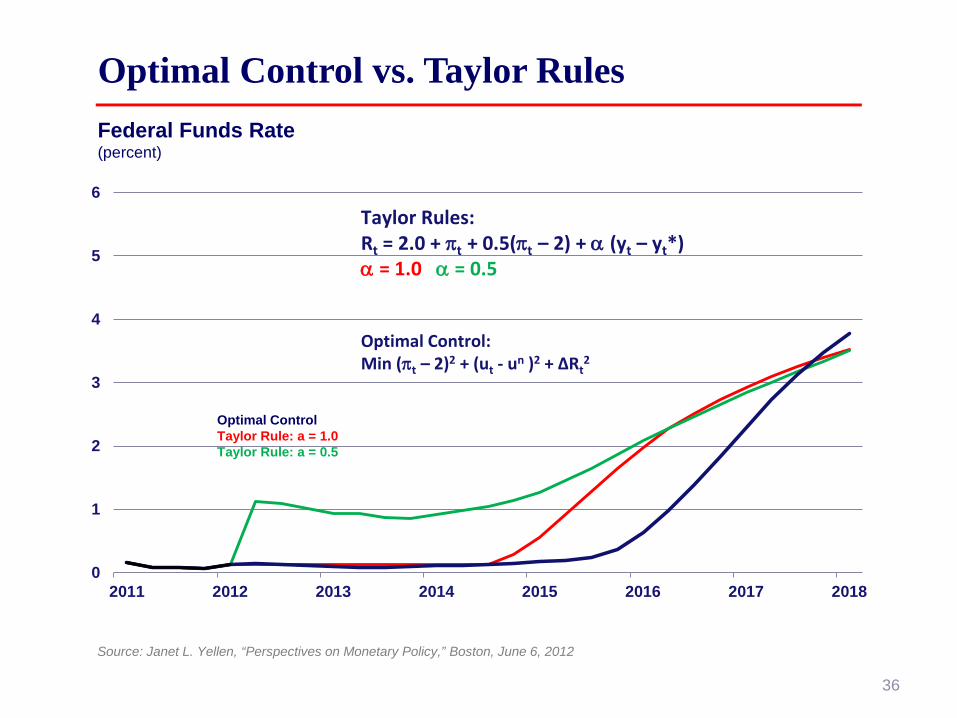

2011 2012 2013 2014 2015 2016 2017 2018

Taylor Rules: Rt = 2.0 + πt + 0.5(πt – 2) + α (yt – yt*) α = 1.0 α = 0.5

Optimal Control: Min (πt – 2)2 + (ut - un )2 + ΔRt

2

Optimal Control vs. Taylor Rules Federal Funds Rate (percent)

Optimal Control Taylor Rule: a = 1.0 Taylor Rule: a = 0.5

Source: Janet L. Yellen, “Perspectives on Monetary Policy,” Boston, June 6, 2012

36

4

5

6

7

8

9

10

2011 2013 2015 2017

Forecasts Under Alternative Policy Rules Unemployment Rate (percent)

Optimal Control Taylor Rule: a = 1.0 Taylor Rule: a = 0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2013 2015 2017

PCE Inflation (4-quarter percent change)

Source: Janet L. Yellen, “The Economic Outlook and Monetary Policy,” New York, April 11, 2012

Optimal Control Taylor Rule: a = 1.0 Taylor Rule: a = 0.5

37

10

12

14

16

18

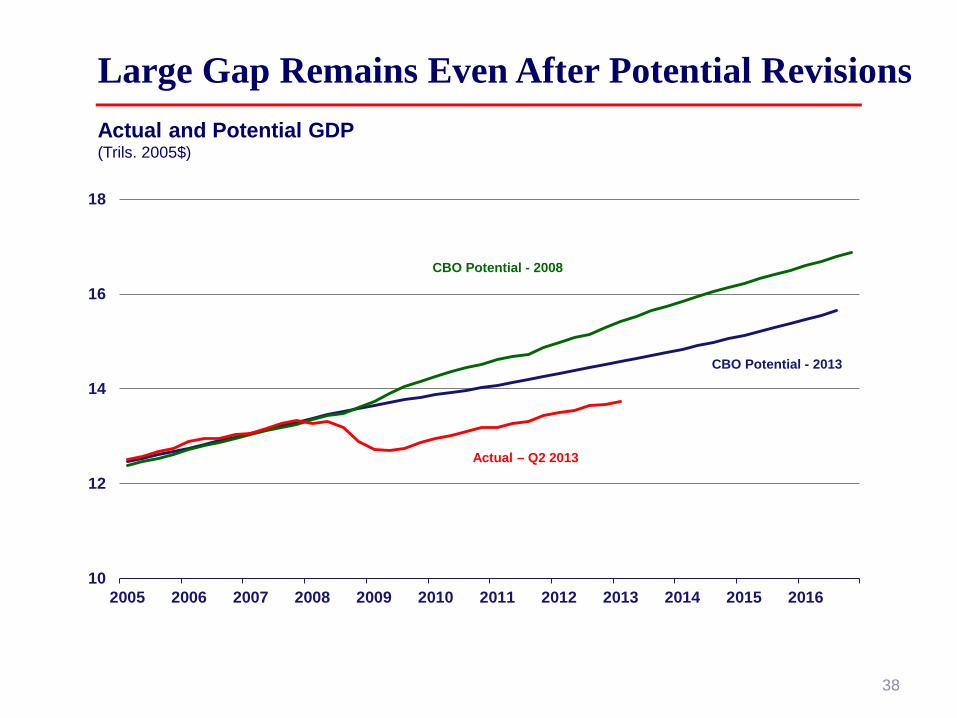

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Large Gap Remains Even After Potential Revisions Actual and Potential GDP (Trils. 2005$)

Actual – Q2 2013

CBO Potential - 2013

CBO Potential - 2008

38

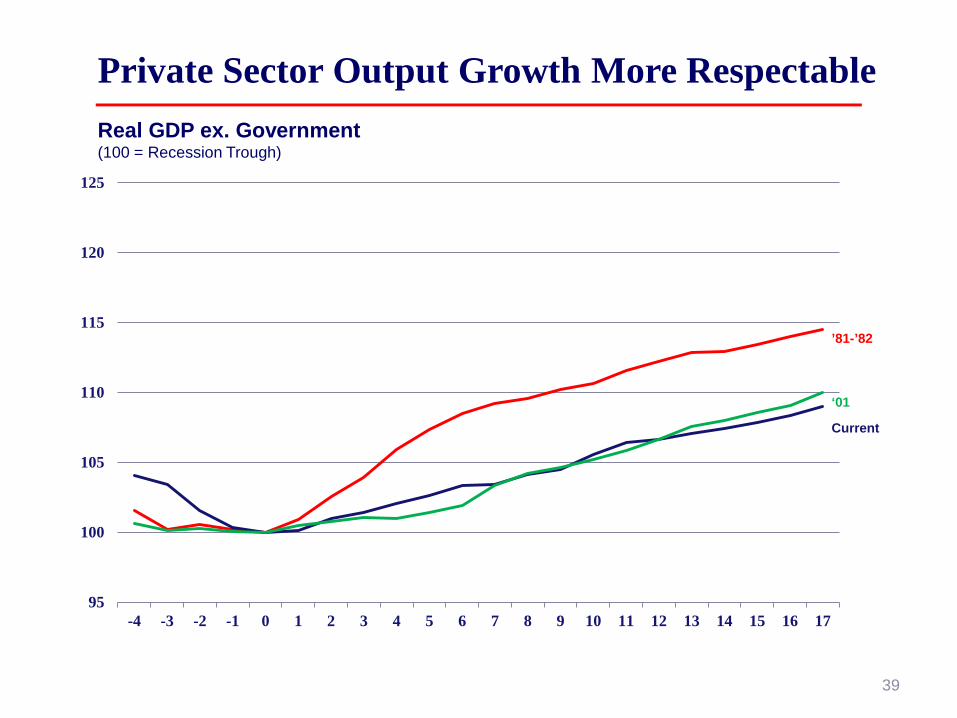

Private Sector Output Growth More Respectable Real GDP ex. Government (100 = Recession Trough)

Current

‘01

’81-’82

95

100

105

110

115

120

125

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

39

95

100

105

110

115

120

125

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Consumption Recovery Especially Slow Per Capita Real PCE (100 = Recession Trough)

Current

‘01

’81-’82

40

Forward Guidance on Funds Rate: Woodford “Standard New Keynesian models imply that a higher level of expected real income or inflation in the future creates incentives for greater real expenditure and larger price increases now; but in the case of a conventional interest-rate reaction function for the central bank, short-term interest rates should increase, and the disincentive that this provides to current expenditure will attenuate (without completely eliminating) the sensitivity of current conditions to expectations. If nominal interest rates instead remain unchanged, the degree to which higher expected real income and inflation later produce higher real income and inflation now is amplified…. it is precisely when the interest-rate lower bound is expected to be a binding constraint for some time to come that expectations about the conduct of policy after the constraint ceases to bind should have a particularly large effect on current economic conditions…”

Source: Michael Woodford, “Methods of Policy Accommodation at the Interest-Rate Lower Bound,” Jackson Hole Symposium, September 16, 2012.

41

-6

-3

0

3

6

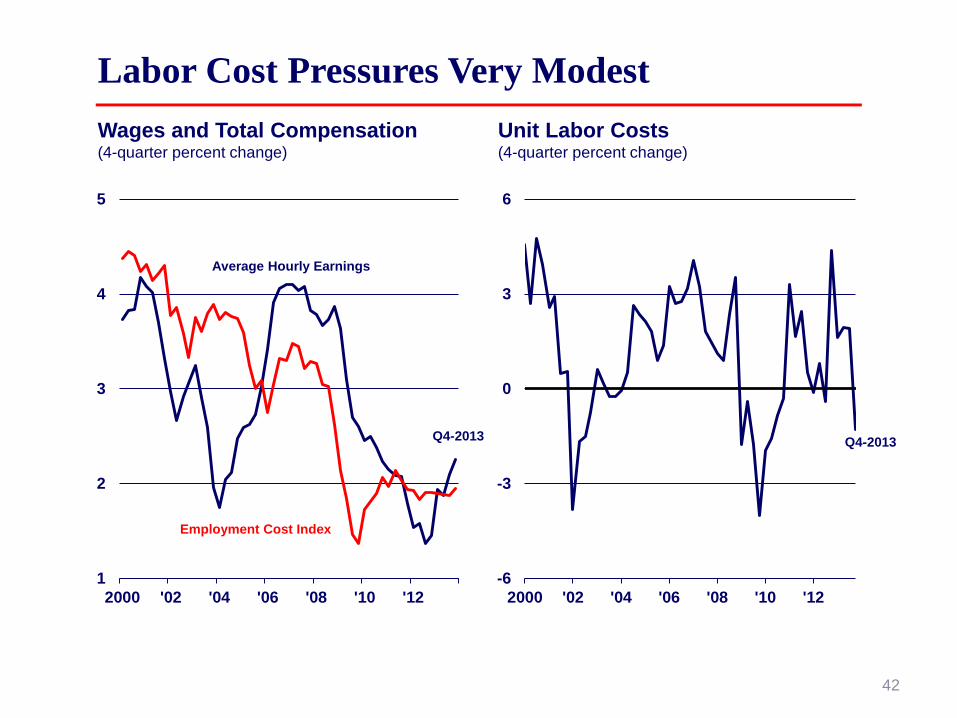

2000 '02 '04 '06 '08 '10 '121

2

3

4

5

2000 '02 '04 '06 '08 '10 '12

Labor Cost Pressures Very Modest Wages and Total Compensation (4-quarter percent change)

Unit Labor Costs (4-quarter percent change)

Employment Cost Index

Q4-2013 Q4-2013

Average Hourly Earnings

42