Embed Size (px)

Citation preview

Applied Energy 87 (2010) 2392–2400

Contents lists available at ScienceDirect

Applied Energy

journal homepage: www.elsevier .com/ locate/apenergy

Uncertainty modeling of CCS investment strategy in China’s power sector

Wenji Zhou a, Bing Zhu a,b,*, Sabine Fuss b, Jana Szolgayová b,c, Michael Obersteiner b, Weiyang Fei a

a Department of Chemical Engineering, Tsinghua University, Beijing 100084, PR Chinab International Institute for Systems Analysis (IIASA), Schlossplatz 1, A-2361 Laxenburg, Austriac Department of Applied Mathematics and Statistics, Faculty of Mathematics, Physics and Informatics, Comenius University, Bratislava, Slovakia

a r t i c l e i n f o

Article history:Received 29 September 2009Received in revised form 22 January 2010Accepted 22 January 2010Available online 13 February 2010

Keywords:Carbon capture and storageUncertaintyReal optionsEnergy investmentChinese climate policy

0306-2619/$ - see front matter � 2010 Elsevier Ltd. Adoi:10.1016/j.apenergy.2010.01.013

* Corresponding author. Address: Department of ChUniversity, Beijing 100084, PR China. Tel./fax: +86 10

E-mail address: [email protected] (B. Zhu)1 According to 2007 data, the shares of coal, petrol

21%, and 3%, respectively. With respect to renewabledeveloped, accounting for 3%. Nuclear and wind powebut still constitute very small shares.

a b s t r a c t

The increasing pressure resulting from the need for CO2 mitigation is in conflict with the predominance ofcoal in China’s energy structure. A possible solution to this tension between climate change and fossil fuelconsumption fact could be the introduction of the carbon capture and storage (CCS) technology. However,high cost and other problems give rise to great uncertainty in R&D and popularization of carbon capturetechnology. This paper presents a real options model incorporating policy uncertainty described by car-bon price scenarios (including stochasticity), allowing for possible technological change. This model isfurther used to determine the best strategy for investing in CCS technology in an uncertain environmentin China and the effect of climate policy on the decision-making process of investment into carbon-savingtechnologies.

� 2010 Elsevier Ltd. All rights reserved.

2

1. Introduction

According to the report from the International Energy Agency(IEA) [1], China ranks the first place in terms of CO2 emissions byfuel combustion among countries in the world. In recent years,due to the rapid growth of high energy-consumption sectors suchas power, steel, cement and chemical industries, China’s CO2 emis-sions have risen dramatically. A key characteristic of China’s en-ergy structure is that coal dominates in energy use, accountingfor about 70% in total energy consumption [2], while oil and natu-ral gas constitute a relatively small part only.1 This situation is ex-pected to last for several decades in the future, mainly due to China’sconsiderable coal reserves. This fact together with the increasinglyperceivable need to decrease the global CO2 emissions imposes greatpressure on policy makers and therefore poses huge challenges toChina both with regard to energy security and climate change.

Carbon capture and storage (CCS) is considered as an importantapproach to control CO2 emissions caused by fossil fuel consump-tion. The power industry is one of the main CO2 emissions sectors,in particularly in China. More than 80% of electricity is generatedby coal combustion [2], with relatively low-efficiency coal-fired

ll rights reserved.

emical Engineering, Tsinghua62782520.

.eum and natural gas are 73%,energy, hydro power is mostr are under fast development,

technology. This indicates that to reduce CO2 emissions in China,the power industry needs to be considered as one of the firstsources. Installing CCS devices in power plants is an attractive op-tion, as it enables further use of abundant coal resources, while atthe same time cutting emissions from that combustion by a con-siderable amount. However, the high cost of CCS and the uncer-tainty associated with its technological development areobstacles to a fast diffusion of this technology, particularly indeveloping countries like China. The Chinese government has beenstrengthening related R&D efforts and some demonstration pro-jects are under construction.2 From the energy companies’ point-of-view, CCS installation is still associated with high cost and couldonly be considered if it was profitable for the whole value chain.This, however, remains highly uncertain due to the lack of knowl-edge about the direction of future climate policy.

China’s power industry is now confronted by big challengesfrom increasingly strict environmental policies aiming at thereduction of pollutants. With respect to environmental regulation,the requirement of environmental protection has become much

CO2 capture technology in China has been applied in some industrial sectors suchas ammonia, hydrogen and petroleum for several decades. However, R&D of large-scale capture in the power sector just started a few years ago. In 2005, CCS technologywas listed in the National Outlines for Medium and Long-term Planning for Scientificand Technological Development (2006–2020), which significantly spurred relevantresearch. In July 2008, the first demonstration carbon capture project in China hasbeen completed in the Beijing Thermal Power Plant owned by Huaneng Group, with acapacity of 3000 tons of CO2 captured per year. In the meantime, some otherdemonstration projects with larger capture capacity are also at different stages ofcompletion.

W. Zhou et al. / Applied Energy 87 (2010) 2392–2400 2393

stricter than before. For example, power plants are compelled toinstall desulfurization devices by regulation issued in recent years.However, there is currently not such a stringent requirement forChina’s power industry to reduce greenhouse gas emissions. Chinais included in the clean development mechanism (CDM),3 however,and some energy enterprises have benefited from CDM projects. It isstill hard to predict whether and when the situation will change andwhat kinds of policy instruments will be adopted in the post-Kyotoperiod. Moreover, in a cap-and-trade market, the CO2 price will fluc-tuate. In the face of such an uncertain environment, strategic deci-sions on investment into CO2 mitigation technology cannot bebased on traditional discounted cash flow (DCF) analysis becausecompanies possibly choose to delay the decision rather than imme-diately make a now-or-never decision by using DCF, as the invest-ment is irreversible, involves high sunk costs and its payoff isuncertain. In order to capture these specific characteristics of theinvestment decision, real options analysis (ROA) has therefore beenchosen for the analysis [3]. Generally, ROA is designed to take threeimportant factors into account: the irreversibility of the investment,the uncertainty surrounding the future cash flows from the invest-ment (here through volatile CO2 price processes), and the opportu-nity of timing the investment flexibly (here through adding theCCS module earlier or later in the planning period) [4].

Investment strategy in the power sector has been analyzed byusing real options methods before, but only a few of them focuson climate change policies, and it is hard to find any discussionon this issue for developing countries like China. Laurikka [5]presents a simulation model implementing ROA to assess theimpact of emissions trading scheme on integrated coal gasifica-tion combined cycle (IGCC). The study simulates three types ofstochastic variables: the price of electricity, the price of fueland the price of emission allowances. Yang et al. [6] value realoptions using a dynamic programming approach for technologyinvestment choices under uncertain climate policy. Three casesfor gas, coal and nuclear power investments are considered. En-ergy prices and the CO2 price are set to change randomly; forthe latter one, a price jump was incorporated to represent pol-icy-related shocks.

All these studies are based on a specific emissions trading sys-tem, which cannot be applied directly to the case of China. Further-more, the absence of technological improvement in those studiesimplies neglecting one of the most important drivers for low-car-bon technology adoption. Kumbaroglu et al. [7] integrate techno-logical learning curves into a real options framework to appraiserenewable energy technologies. Fuss and Szolgayová [8] use a realoptions model with stochastic technical change and stochastic fos-sil fuel prices, to investigate their impact on replacement invest-ment decisions in the electricity sector.

Unlike the studies above, this paper attempts to model and ana-lyze climate policy uncertainty in China’s energy industry underconsideration of technological change and establish a real optionsmodel to obtain CCS investment strategies from the point-of-viewof a typical energy enterprise, hence providing policy implicationsfor CO2 mitigation in the coming post-Kyoto period. The paper con-sists of six sections. Following this introduction, Section 2 presentsthe methodological framework of the real options model used inthe study. In Section 3, the factors of policy uncertainty and tech-nological progress are analyzed. Section 4 describes the features ofthree representative types of technologies considered. These are apulverized coal power plant, a wind farm and an IGCC plant. The

3 The clean development mechanism is an arrangement under the Kyoto protocolallowing industrialized countries with a greenhouse gas reduction commitment(Annex 1 countries) to invest in projects that reduce emissions in developingcountries as an alternative to more expensive emission reduction in their owncountries.

data used and the assumptions are explained in detail. The scenar-ios generated by varying underlying model parameters are ana-lyzed in Section 5. Finally, the policy implications of the resultsfrom this real options model and its features as a policy analysistool are presented in the conclusion.

2. Model description

A typical CCS system consists of three parts: capture, transportand storage. The capture part contains chemical devices such asabsorber and desorber, accounting for 70–80% of the total cost[9]. These devices can be in-built, when a new modern plant is con-structed, or they can be added to an existing plant by retrofitting itat higher cost.

In the model we consider an investor maximizing the sum of hisexpected discounted profits over the planning period, who facesuncertain climate policy. The real options model determines theoptimal timing of investing into a CCS module given that a coalplant already exists. Several possible types of coal plants (and cor-responding CCS systems) are analyzed separately. It also derivesthe corresponding profit distribution resulting from optimalinvestment. Several scenarios for CO2 price development (involv-ing both deterministic and stochastic processes) were imple-mented to reflect different possible policy outcomes and examinetheir impact on CO2 mitigation technology investment behavior.In Fig. 1, we show an overview of price assumptions used in themodel. Only the CO2 price is assumed to be uncertain, all otherprices are modeled as deterministic. The motivation for an uncer-tain fluctuating carbon price CO2 price can be seen for examplein a policy resulting in CO2 credits or allowances being tradedamongst firms. We consider the planning horizon equal to the life-time of the power plant, i.e. 30 years and that the decisions can bedone on a yearly basis.

The investor faces an optimization problem of timing the deci-sion to invest into the CCS module so that the sum of discountedexpected future profits is maximized. Let xt denote the state thatthe system is currently in year t, i.e. it tells whether the basic plant,the CCS module or both have been built and whether the CCS mod-ule is currently running, let at be the action (i.e. the control) whichthe decision-maker chooses to undertake in year t. Possible actionsare to either build the CCS module (which is feasible only in case ithas not been built yet) or do nothing. xt+1 depends only on the ac-tion at and xt, with at as an element from the set of feasible actions.The yearly profit p for a given state x and actions a can be ex-pressed as:

pðx; a; PcÞ ¼ qeðaÞPe � qcðaÞPc � qf ðaÞPf � OMCðaÞ � cðaÞ; ð1Þ

where Pc represents the price of CO2 (or CO2 credit when Pc is neg-ative), according to which energy companies could either be penal-ized by paying for CO2 emissions required by a stringent policy, orbenefit from selling CO2 credits in a CDM-type market. The variableis created to describe a possible climate policy variation in the fu-ture. qe and qf refer to annual quantities of electricity output andfuel consumption, Pe and Pf represent prices of electricity and fuelrespectively. OMC refers to operational and maintenance cost, andc denotes the cost associated with the undertaken action. In casethe action is to build the CCS module, it is equal to the expenditurefor retrofitting an existing plant with a CCS module. In case the ac-tion is to do nothing, this cost is equal to zero.

Based on this profit function, the investor’s optimization prob-lem can be formulated as follows:

maxatðxt ;Pc

t Þ2AðxtÞ

P30

t¼1e�rtE pðxt ; atðxt; P

ct Þ; P

ct Þ

� �

s:t: xtþ1 ¼ Fðxt ; atðxt ; Pct ÞÞ

ð2Þ

1978 1985 20080

100

200

300

400

500

600

700

year

yuan

/MW

H

5 10 15 20 25 300

100

200

300

400

500

600

700

year

yuan

/MW

H

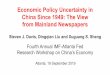

Fig. 2. Trend of on-grid electricity price.

Fig. 1. Framework of the real options model.

2394 W. Zhou et al. / Applied Energy 87 (2010) 2392–2400

together with an assumption on the CO2 price. In the maximizationproblem, A is the set of feasible actions for a given state xt, r is dis-count rate, and E[�] denotes the expected value. The investor’sproblem is thus to determine the optimal investment strategyfatðxt ; P

ct Þg

Tt¼1. Since the model is formulated as a optimum control

model with discrete time on a finite horizon, it can be solved by dy-namic programming. The value function can be calculated recur-sively by the Bellman equation:

V30ðx; PÞ ¼ 0Vtðx; Pc

t Þ ¼maxa2AðxÞ

pðx; a; Pct Þ þ e�rE Vtþ1ðFðx; aÞ; Pc

tþ1Þjx; Pct

� �� � ð3Þ

where the optimum action for each state and price in each year isobtained as the argument that maximizes the term on the right sideof the Bellman equation. The equation indicates that the value ofthe project in year t is composed of two parts: one is the immediateprofit p(xt, at, Pc

t ), and the other is the expected and discounted va-lue of next year, which is also called continuation value by Dixit andPindyck [3]. To calculate E[Vt+1(F(x, a),Pc

tþ1)|x, Pct )], we discretize the

carbon prices and use the Monte Carlo simulations. The Monte Carlosimulations approach can be easily implemented and despite thegeneral disadvantage that a large amount of simulations are re-quired to obtain a sufficiently reliable results [10], it has provento remain efficient in this framework for a rather high degree ofcomplexity and delivers the same results as the partial differentialequations approach [5].

The solution of the recursive optimization part is a multidimen-sional table containing the optimum action at for every t, x, and Pc

t .These optimum actions are further referred to as ‘‘strategies”. In or-der to analyze the final outcome, possible price paths are simulatedand discretized subsequently (so a relatively fine price grid isneeded in order to obtain precise results). The corresponding deci-sions are extracted from the output. In this way we can derive boththe profit distribution and the frequency with which the CCSinvestment option is exercised.

3. Impact factors modeling

3.1. Deterministic variables

Electricity price and technology cost are modeled as determin-istic variables, from several reasons. The electricity price does nothave an impact on the optimum decisions in the model, since theoutput of the power plant both with and without CCS is the same.Therefore, there would be no added value in a stochastic electricityprice. On top of this, in China, the electricity pricing is regulated bythe National Development and Reform Commission (NDRC), whichmakes it rather stable compared to price evolution in Westernmarkets. To simulate the future trend, historical information ofChina’s on-grid price4 was collected from [11,12], as shown in the

4 On-grid price refers to the electricity price sales from individual power plants tothe national power grid.

left panel of Fig. 2. Historical data showed that after the long periodof central planning, the 1985 reform in China’s power industry re-sulted in a growing electricity price. Based on current policy condi-tion in China’s power industry, we assume that in the comingdecades the trend will continue, and follow an exponential processwith parameters obtained from historical data fitting, as shown inthe panel of Fig. 2.

Although the real development of cost for immature but prom-ising technologies like CCS is very volatile, in some cases even‘‘negative learning” phenomena occur, in our model we considerthe technology cost as exogenous and deterministic. According toseveral studies [13–15], the cost improves over time due to thereduction in input factor prices, financing cost or improvementsin organizational efficiency. This effect is explained by the techno-logical progress and learning-by-doing, where the concept of alearning curve is widely used, indicating that the development ofmarginal or average unit cost is a function of cumulative produc-tion or capacity. To introduce directly such a functional form intoour profit equation is not feasible5, hence we need to formulatetechnical change as a function of time rather than cumulative in-stalled capacity. Technology cost is assumed constant in the scenar-ios without technological improvement. For the scenario that takestechnical change into account, only modern technologies such asIGCC and CCS are considered to experience decreasing costs. Thedownward trend is assumed to follow an exponential process asshown in Fig. 3.

5 Remember that this is a plant-level analysis and the investment option getsexercised only once, after which learning from installing more is not an optionanymore.

5 10 15 20 25 300

1

2

3

4

5

6

7

8x 109

year

IGCC with CCS

IGCC without CCS

cost(t)=cost(0)*e-0.01*t

Fig. 3. Decreasing capital costs of IGCC with and without CCS module.

5 10 15 20 25 30-50

0

50

100

150

200

250

300

350

400

450

500

year

Fig. 4. Simulation of future trend of CO2 price.

W. Zhou et al. / Applied Energy 87 (2010) 2392–2400 2395

3.2. Stochastic variable

To investigate how uncertainty in climate policy for the comingdecades affects energy technology investment behavior, the CO2

price is chosen to be stochastic, which could mimic subsequentadaptation of policy by the government or fluctuations due toimperfections in carbon markets in case an emission tradingscheme-type (ETS) system would be chosen as regulatory frame-work. As mentioned above, this variable denotes either the pricefor a CO2 allowance (or a CO2 tax) or the credit granted for savingCO2, which depends on the scenario. Since the CO2 price is believedto increase, once the government commits to a GHG target [16,17],a geometric brownian motion (GBM)6 is employed, which is de-scribed by the following equation:

dPc ¼ lPcdt þ rPcdz ð4Þ

where the parameter l is the drift, representing the positive trendof the CO2 price, r represents the volatility and dz is the incrementof a Wiener process. Fig. 4 shows a CO2 price trajectory in a ‘‘carbonpenalty” scenario, in which the emission of CO2 will be penalizedstarting from year 4, which would correspond to the post-Kyotoperiod.

4. Technology and data

4.1. Technology description

Three types of technologies are examined in this paper: a con-ventional pulverized coal power plant, an IGCC plant and a windfarm of comparable size.7 The first type, the conventional coalpower plant, is one of most widely implemented technologies in Chi-na’s power sector. The second one, IGCC, represents more advanced

6 GBM process is applicable to situations where the price trends follow theexponential curve. In fact, many of the market prices don’t meet this requirement, forexample, energy prices in long run [3]; however, in a 30 years time scale, it isreasonable to assume a GBM process for the prices according to historical data [3].Since the history of carbon trading market is rather short, there is no reliablehistorical series yet from which to extract that info empirically, thus in mostresearches carbon prices are assumed to follow GBM processes, for example [18], forthe simplicity of the model, in this research, we make the same assumption.

7 CCS investment is not relevant for wind power. The profits for wind technologyare nevertheless computed, so as to have a benchmark to compare the coal-firedpower plants to. This enables us to form an idea about the profitability of renewablescompared to traditional fossil-fuel-fired technologies.

and more efficient power generation technologies, which have notbeen installed in China yet.8 Because of China’s large wind energypotential and favorable policy environment, China’s wind powerhas experienced rapid growth in recent years, and it is recognizedas a very promising renewable technology for the future. With re-spect to CO2 mitigation, these three types of technologies can beviewed as three different approaches to reduce carbon emissions,which are carbon capture, energy efficiency improvement, andrenewable energy.

There are three main technologies currently proposed for CO2

capture. In post-combustion capture, most of the CO2 from thecombustion products are removed before vented to the atmo-sphere. The most commercially advanced methods use wet scrub-bing with aqueous amine solution [19]. Pre-combustion captureinvolves removal of CO2 prior to combustion, to produce hydro-gen-rich fuel gas which could be used in many applications suchas IGCC. The separation process typically uses a physical solventsuch as methanol or glycol. Because CO2 is present in much higherconcentrations in syngas than in post-combustion flue gas, CO2

capture should be less expensive for pre-combustion capture thanfor post-combustion capture. Oxygen-combustion uses nearly pureoxygen instead of air, resulting in a flue gas that is mainly CO2 andH2O and thus easily to be separated. Normally, a range of other op-tions for capturing and separating CO2 including, for example, ionicliquid and membrane processes offer the potential for a stepwisereduction in the cost and energy needed for CO2 capture.

For the conventional coal power plant, we assume that the CCSmodule can be added to the existing plant. IGCC is more efficientthan the conventional plant and can be retrofitted with CCS at arelatively lower cost due to its higher concentration of CO2 in itsflue gas. The third way of CO2 mitigation, renewable energy is rep-resented by wind power. Details of each technology are describedbelow.

4.1.1. Conventional pulverized coal power plantThere are various kinds of power generation technologies

among pulverized coal (PC) plants. Currently in China, the powersector strategically chooses ultra-supercritical (USC) PC and super-critical (SC) PC plants for new capacity additions coupled with pol-lution control technologies, and CFB (supercritical circulating

8 However, several IGCC demonstration projects are under construction or are atthe stage of planning.

Table 1Power plant data for PC, IGCC and wind.

Parameters PC PC + CCS IGCC IGCC + CCS Wind

Installed capacity (MW) 650 800 685 725 1500Electricity output (MWh) 3.6 � 106 3.6 � 106 3.6 � 106 3.6 � 106 3.6 � 106

Capital cost (yuan) 2.6 � 109 5.2 � 109 5.14 � 109 7.45 � 109 1.1 � 1010

O&M costa (yuan/year) 2.1 � 108 4.1 � 108 2.82 � 108 4.1 � 108 4.5 � 108

Electricity cost (yuan/MWh) 276 433 360 479 650CO2 emissions (ton/year) 28,80,000 459,200 25,20,000 410,400 0Coal consumption (ton) 12,24,000 14,96,000 1188000 1254000 0

a In O&M cost here, fuel cost is separated for PC and IGCC.

2396 W. Zhou et al. / Applied Energy 87 (2010) 2392–2400

fluidized bed, which is another advanced power generation tech-nology) as supplement. According to the national industry policy,600 MW and larger-capacity units are required for thermal powergeneration in the coming years [20]. And a developing trend ofclean and high-efficiency power generation technologies is inevita-ble. Therefore, we choose supercritical PC as the representativetechnology for the conventional coal power plant. When an exist-ing PC plant is retrofitted with CO2 capture, the major new techno-logical units that get added to the original system are: (1) theabsorption process: the flue gas exiting the flue gas desulfurization(FGD) system is introduced into an inhibited chemical or physicalabsorber–stripper system, and (2) the CO2 compression process:to facilitate the transport of CO2 captured from flue gas, gaseousCO2 needs to be compressed by a CO2 compression unit, which willresult in extra electric power consumption and represent anotherparasitic load. Adding of these devices will result in a reductionof net electric efficiency.

4.1.2. IGCCIGCC is an advanced power generation system that combines

coal gasification with a highly efficient cycle. It is composed oftwo main parts, one of which is called coal gasification. The otherpart is a combined cycle of gas–steam to generate electricity. Gen-erally speaking, compared to conventional coal-fired power plants,IGCC is not only more energy-efficient, but also environmentallysounder. Pollutants like SO2, NOx and particulate matter emissionsfrom an IGCC system are relatively minor [20]. Due to the high con-centration of CO2 in the flue gas, which could be captured using thepre-combustion method, it will also be less costly to retrofit theIGCC plant with CCS. According to [21], the capital expense andoperational expense of an IGCC unit are about 80–90% of those ofpulverized coal combustion power plants.

4.1.3. Wind powerA significant advantage of wind power is its zero fuel cost. In

fact, almost no fossil fuel is needed in the whole generation process(except during the construction phase of the actual wind mill). Thismeans that the electricity produced by the wind farm hardlycauses greenhouse gases or other pollutants. On the other hand,it has shortcomings as well. For example, the strength of the windis not constant and it varies from zero to storm force. This meansthat wind turbines do not produce the same amount of electricityall the time. There will be times when they produce no electricityat all.9

To summarize, all of the three technologies have their advanta-ges and disadvantages. PC has low capital and operational ex-penses, but the energy- and environment-related costs arecomparatively at low grade. In addition, the cost of retrofittingwith CCS is higher than that of IGCC, which has higher capital

9 However, we are not considering differences between base and peak loadtechnologies in this model and want to emphasize again that this is a technologyrepresentative for renewable energy in general.

and operational costs but performs better in energy and environ-mental terms. Wind power, representing renewable energy in thisstudy, has the highest capital costs, but near-zero fossil fuel con-sumption and CO2 emissions.

4.2. Data and assumptions

We collect the data required for the model and for unavailabledata; some assumptions are made on the basis of data reported byrelated literature [20–24]. The parameters are shown in Table 1,where the electricity output for each type of power plant is nor-malized. Table 1 shows that wind power is most expensive interms of investment and operational costs, while IGCC ranks sec-ond, and PC is the cheapest alternative. It is also shown that to pro-duce the same amount of electricity, the required capacity for thepower plant with CCS is larger than for those without CCS, indicat-ing that installing and running the CCS module will cause extra en-ergy consumption or partial losses of the electricity produced.Comparing the additional capital and O&M costs for retrofittingof the PC plant to those of the IGCC plant, we can see that the costsfor the latter one are less. The reason for this is mainly because it iseasier to retrofit an IGCC plant with CCS than a PC plant, as ex-plained earlier in this section. In addition, the coal price is assumedto be constant, since we do not want to confuse fuel price effectswith the impact of policy uncertainty.10

5. Scenario analysis

Two scenarios of different types of climate policy and one sce-nario focusing on technological improvement are developed toinvestigate the energy investor’s behavior under different circum-stances. There are numerous studies and proposals for the designof post-2012 climate regime [25,26]. These involve suggestionsto improve financial channels or to enhance market mechanismsto facilitate developing countries’ participation in global GHGabatement actions. Starting from this, we build one scenario witha carbon credit market and one scenario involving a carbon pen-alty. In the first scenario, a carbon credit market is designed andthis represents a relatively loose policy constraint, under whichChina’s energy companies have an option to participate in carboncredit trading on a voluntary basis. This is similar to the currentCDM framework. The second scenario, on the contrary, reflects astringent policy, where energy companies are obligated to reducethe CO2 emissions, which need to be covered by purchasing CO2

allowances in market. Considering technological progress, thethird scenario emphasizes the influence of decreasing carbon cap-ture cost on companies’ investment decision.

10 In addition, from a more technical perspective, the amount of different stochasticprices for each technology in a real options framework using our methodology, whichcan be included, is limited by the degree of computational complexity this creates.

Table 2Reference settings for carbon credit market scenario.

Variable Expression Value of parameters

Pct Pc

t = 56 (t 6 3)dPc = lPc dt + rPc dz(t > 3)

l = 0.02, r = 0.02, with a starting pricePc

4 = 200

Pet Pe

t = Pe0 exp(�let) le = 0.02

W. Zhou et al. / Applied Energy 87 (2010) 2392–2400 2397

5.1. Carbon credit market

We assume that a new market for trading carbon credits will becreated upon expiration of the current CDM policy. This is assumedto occur within 4 years from now. The market might emerge from apolicy framework, which is similar with CDM, but will includetrade among enterprises within China. Thus, a specific energy com-pany will benefit from selling carbon credits obtained by imple-menting low-carbon technologies. CCS is also assumed to beincorporated into the market.11

The only stochastic variable in this scenario, the CO2 creditprice, reflects fluctuations in the credit market. The year beforethe policy is enacted, the CO2 credit price is assumed to be constantat 56 yuan/ton CO2. This is the standard price in the current CDMmarket. Afterwards, the price jumps to 200 yuan/ton CO2 and fol-lows a GBM process subsequently as shown in Table 2.

The results for the reference case for the PC plant include theoptimal timing of investment in CCS and the corresponding profitdistributions as presented in Fig. 5. CCS option values are calcu-lated, to reflect the value gained by having the possibility to installCCS in the face of policy uncertainty. Similarly, Blyth et al. [18]show that policy uncertainty creates a risk premium by increasingthe payoffs required from the project in order to justify proceedingwith the project immediately rather than waiting.

The results show that the optimal timing to add the CCS modulecenters in the first 2 years after the introduction of the policy. Theaverage profit is 10.8 billion yuan. The CCS module thus gets in-stalled almost immediately, since the CO2 credit price is very high.We therefore also examine the decisions given a lower startingprice, implying that a future CDM market will not be so attractiveto investors. In another experiment, a larger volatility is consideredas well. Table 3 shows the results for the three plant types. Themost important findings can be summarized as follows:

� Wind power, favored by the high CO2 credit price and zero fuelcost, is the most profitable technology for power generationamong the three technologies, even though its capital cost ishighest at present. IGCC is the least profitable type of technologybecause of its high capital and O&M cost, and PC lies in the mid-dle of the two.

� If the carbon credit price is too low, there is no incentive forcompanies to install CCS modules. As shown in the results, boththe PC and the IGCC plants will not be retrofitted with CCS in thescenario with low prices. For wind power, the expected profitwill be substantially decreased, but it still ranks highest amongthe three, although the gap shrinks substantially.

� Higher risk in the market has significant impacts on investmentbehavior. As the volatility increases, the investment will be post-poned, which is the typical options effect described by Dixit andPindyck [3] and verified in applications to energy investmentsunder price uncertainty by e.g. Fleten et al. [27].

11 CCS is not included in CDM projects currently, although the issue is still underdiscussion. In this article, we assume that credits from carbon capture can be tradedin the market.

� The value of being able to install CCS indicated by CCS optionvalue rises for the PC plant, as the volatility of the carbon creditprice increases. In addition, the comparison of IGCC and PC inthis regard shows that the IGCC plant will benefit more from ret-rofitting because both capital and O&M costs are much lower forCCS module installed on IGCC. So the expected profit of IGCCwith CCS is closer to that of PC with CCS compared to the casewithout CCS. This indicates vast potential for IGCC developmentin a CO2 reduction scenario.

5.2. Carbon penalty

The carbon penalty scenario implies a much more stringent pol-icy. It is similar to the European Union Emission TradingScheme (EU-ETS), in which a CO2 emission cap is set and thenthe corresponding amount of permits to be issued is determinedon the basis of the cap. Companies that need to increase their emis-sions beyond their allowance must buy credits from those whopollute less, so that the total emissions add up to the cap. We con-ducted several experiments: (1) the policy is enacted in year 4 ver-sus the case where it starts only in year 10; and (2) we increasedthe volatility of the GBM to reflect larger fluctuations within themarket (or externally inflicted by adjustments of policy throughthe government). The results for the PC plant are shown in Table 4.The major findings are:

� As the year of starting the policy is delayed, the investment intoCCS will also occur later. The expected profit is obviously consid-erably higher, since no CO2 payments are made before the policyis enacted. In addition, shifting the policy start to a later dateslightly slows down the adoption time: in the second scenariothe CCS module is adopted 2.3 years after the policy enactmenton average, but in the previous scenario the average adoptiontime was 1.5 years after the introduction of the carbon price.The reason for this effect is that the remaining planning horizonis much shorter when the carbon price is introduced later, so thetrigger price has to be higher than in the case where the policy isintroduced more in the beginning.

� Similar to the carbon credit market scenario, increasing volatil-ity of the carbon penalty price (when the starting time of thepolicy is in year 4) will result in a postponement of CCS installa-tion by 2 years.

Not surprisingly, compared to the carbon credit market sce-nario, expected profits in the carbon penalty scenario are substan-tially lower, implying that the payment for CO2 reduction willbecome a heavy burden on energy companies. However, thosewho tend to invest earlier into carbon reduction technologies havethe potential to make higher profits in a favorable policy environ-ment such as CDM.12

5.3. Technological improvement

The impact from technological change on investment behaviorwas determined by testing for different cost-decreasing rates.The main findings from the results presented in Table 5 are:

� An increase in the rate of technical change leads to a rise inexpected profits and earlier investment into CCS for both of IGCCand PC plants. These results illustrate that technological

12 Note that such analysis is beyond the scope of this paper, since real optionsmodeling rests on the assumption of a risk-neutral decision-maker, so early up-frontinvestments in order to hedge against an unfavorable future or to take advantage offavorable circumstances can never be an outcome of this model.

Table 3Numeric results for three types of power plants in different carbon credit market conditions.

Lower carbon credit price(starting price = 56, r = 0.02)

Reference(starting price = 200,r = 0.02)

Higher uncertain carboncredit market(starting price = 200, r = 0.05)

PCOptimal timing to invest in CCS No Year 5.5 Year 7.6Expected profit (unit: Yuan) 1 � 1010 1.08 � 1010 1.09 � 1010

CCS option valuea 0 7.9 � 108 8.5 � 108

IGCCOptimal timing to invest in CCS No Year 4 Year 4Expected profit (unit: Yuan) 6.7 � 109 9.2 � 109 9.2 � 109

CCS option value 0 2.5 � 109 2.5 � 109

WindExpected profit (unit: Yuan) 1.3 � 1010 1.9 � 1010 1.9 � 1010

a CCS option value denotes that compared to the strategy that CCS module would be never installed, the extra profit made by optimized real option strategy.

0 10 20 300

2000

4000

6000

year

Timing of CCS Investment

0.9 1 1.1 1.2 1.3

x 1010

0

500

1000

1500Profit distribution

0 10 20 30300

400

500

600

year

Yuan

/MW

h

Electricity price

0 10 20 30

-400

-300

-200

-100

0

year

Yuan

/tCO

2

CO2 credit price

Fig. 5. Profit and timing of CCS investment in PC case.

Table 4Optimal timing of CCS investment and expected profit with different penalty conditions for PC case.

Later policy start(starting year = 10, r = 0.02)

Reference(starting year = 4, r = 0.02)

Higher uncertain penalty(starting year = 4, r = 0.05)

PCOptimal timing to invest in CCS Year 12.3 Year 5.5 Year 7.6Expected profit (unit: Yuan) 4.2 � 109 1.35 � 109 1.42 � 109

2398 W. Zhou et al. / Applied Energy 87 (2010) 2392–2400

improvement can provide a significant incentive for CCS adop-tion. The IGCC plant will benefit more than the PC plant fromtechnical change. The CCS module is mostly added in the verybeginning of the new policy regime.

6. Policy implication and concluding remarks

Even though it is one of the major, potential CO2 mitigationmeasures, CCS needs to consume extra energy to reduce carbon

emissions, which makes it less cost-effective than renewable en-ergy alternatives and energy efficiency approaches. As a result,much debate has arisen on whether CCS should be further devel-oped considering its high cost and energy inefficiency, which isespecially important for developing countries like China. Waterconsumption in carbon capture operations may become anotherconcern considering water shortage being a common problem inChina. On the other hand, China still lacks integrated technologiesfor transportation, injection, monitoring and risk control, as well asrobust knowledge about storage potentials. Large-scale leakage

Table 5Results of different technology change rates scenarios for PC and IGCC.

Technology change rate Technical change(OMCt = OMC0 � e�at, a = 0.01)

No technicalchange (a = 0)

PCOptimal timing for CCS Year 4 Year 5.5Expected profit (Yuan) 1.4 � 109 1.35 � 109

CCS option value 8.4 � 108 7.9 � 108

IGCCOptimal timing for CCS Year 4 Year 4Expected profit (Yuan) 1.0 � 109 8.9 � 108

CCS option value 2.54 � 109 2.49 � 109

13 Note that this is different for biofuels, since the fuel in this case does not come atzero cost.

W. Zhou et al. / Applied Energy 87 (2010) 2392–2400 2399

and geological disaster are also of concern in relation to CCSdeployment in China, according to a survey [28]. These issuesmight become main barriers and hamper the large-scale deploy-ment of CCS in China.

Currently, most focus is put on energy efficiency improvementsin China’s climate policy. In the national 11th five-year plan (from2005 to 2010), energy-saving and pollutant-reducing actions arepromoted and their implementation becomes a criterion for theassessment of government officials’ performance. The energy con-servation law has also taken effect since August 2008. These poli-cies give an incentive to enterprises to reduce energyconsumption and thereby reduce CO2 emissions as well. However,these policies are not directly targeted at CO2 emissions and energycompanies are not under any obligation to conduct such actions.Most of the projects aiming at CO2 mitigation in China are underthe umbrella of CDM. The CDM projects in China involve renewableenergy such as wind power, energy efficiency improvements of e.g.power plants. The trading price is actually very low with about 50–70 yuan per ton [29]. Whether developing countries with largeemissions like China will be faced with commitments to CO2

reduction similar to Annex I countries some time in the future isstill not clear given the current situation of international climatenegotiation.

The objective of this study has been to analyze investmentstrategies for CCS in China’s energy sector in an uncertain environ-ment. To carry out the corresponding experiments, three kinds oftechnologies – a conventional pulverized coal power plant, an IGCCplant and a wind farm – have been selected as the representativesof the three approaches for CO2 mitigation (i.e. energy efficiencyimprovement, renewable energy, and carbon capture and storage)in China. Of these technologies, CCS modules can be added to theformer two. To incorporate the uncertain factors into the decisionprocess, a real options model has been developed, and scenarios tomimic various possible policy outcomes and rates of technicalchange have been analyzed and discussed. The key findings fromthe model and scenario analysis can be summarized as follows:

(1) Flexibility in CCS investment decision making has an eco-nomic value, and it increases with an increase in CO2 priceuncertainty. Some studies, as for example [30], present sim-ilar results. Moreover, this research illustrates that higheruncertainty with respect to the carbon market will increasethe CCS option value, i.e., the economic value of the possibil-ity to retrofit existing plants with CCS.

(2) The responding time of companies to install CCS to climatepolicy is shorter when the policy is implemented in thebeginning of the planning period. The result proves a conclu-sion from [18] by using a different approach. In particular,[18] (Energy Policy 2007, vol. 35, p. 5772) state that ‘‘the clo-ser in time a company is to a change in policy, the greaterthe policy risk will be, and the greater the impact on invest-ment decisions”. The real reason is that if the policy is

enacted later, then the remaining planning horizon is shorterand then a higher price is needed to trigger the CCSinvestment.

(3) The profitability of renewable energy will increase signifi-cantly in the long term. In a world more constrained by cli-mate policy, the zero-CO2-emission advantage of renewableenergy will improve the economics compared to fossil-fuel-consuming power plants. Technologies with zero fuel cost(e.g. wind, solar or hydro power) benefit even more becauseof zero fuel cost.13 For IGCC, the results show that its profit isnot so competitive, except under more stringent climate pol-icies. However, other advantages of IGCC, such as lower emis-sion levels of other pollutants, have not been considered inthis analysis. Therefore, a broader framework needs to bedeveloped to assess this technology more comprehensively.

(4) For China’s power industry, the expected profits of IGCCplants and conventional coal-fired power plants will not bevery different when considering technical change. CCSshould then be integrated in newly-built and more efficientpower plants such as IGCC, which is due to their lower cap-ture cost. Therefore, the three approaches to reduce carbonemissions in the electricity sector (CCS, energy efficiencyand renewable energy) should always be considered in com-bination with respect to the overall strategy for CO2 mitiga-tion. Furthermore, given the rather low cost of IGCC inWestern countries, technology transfer could enable China’spower industry to implement CCS at a larger scale and morecost-effectively under a more stringent climate policyregime.

Acknowledgements

The first author is grateful for the support from National NaturalScience Foundation of China (NFSC) to participate in IIASA’s YoungScientist Summer Program (YSSP) when part of the work was con-ducted. Financial supports from NFSC (No. 20876087), China’s Na-tional Hi-Tech R&D Program (No. 2008AA062301) and Ph.D.Programs Foundation of Ministry of Education of China (No.20080030049) are also gratefully acknowledged. At IIASA, the re-search leading to these results has received funding from the Euro-pean Community’s Seventh Framework Programme (FP7) undergrant agreement No. 212535, Climate Change – Terrestrial Adapta-tion and Mitigation in Europe (CC-TAME), www.cctame.eu.

References

[1] International Energy Agency. CO2 emissions from fuel combustion, 2009 ed.,2009.

[2] China National Bureau of Statistics, China National Energy Administration.China energy statistics yearbook 2008. China Statistics Press; 2008.

[3] Dixit A, Pindyck R. Investment under uncertainty. Princeton: PrincetonUniversity Press; 1994.

[4] Fuss S, Szolgayová J, Obersteiner M, et al. Investment under market andclimate policy uncertainty. Appl Energy 2008;85:708–21.

[5] Laurikka H. Option value of gasification technology within an emissionstrading scheme. Energy Policy 2006;18:3916–28.

[6] Yang M, Blyth W, Bradley R, et al. Evaluating the power investment optionswith uncertainty in climate policy. Energy Econ 2008;30(4):1933–50.

[7] Kumbaroglu G, Madlener R, Demirel M. A real options evaluation model for thediffusion prospects of new renewable power generation technologies. EnergyEcon 2008;30:1882–908.

[8] Fuss S, Szolgayová J. Fuel price and technological uncertainty in a real optionsmodel for electricity planning. Appl Energy; 2009. doi:10.1016/j.apenergy.2009.05.020.

[9] Intergovernmental panel on climate change. Special report on carbon dioxidecapture and storage; 2005.

[10] Copeland T, Antikarov R. Real options: a practitioners’ guide. Thomson; 2003.

2400 W. Zhou et al. / Applied Energy 87 (2010) 2392–2400

[11] Lam PL. Pricing of electricity in China. Energy 2004;29(2):287–300.[12] China Electric Power Publishing Committee. China electric power

yearbook. Beijing: China Electric Power Publishing; 1999.[13] Riahi K, Rubin ES, Taylor MR, et al. Technological learning for carbon capture

and sequestration technologies. Energy Econ 2004;26:539–64.[14] Rubin ES, Taylor MR, Yeh S, et al. Learning curves for environmental

technology and their importance for climate policy analysis. Energy2004;29(9–10):1551–9.

[15] McDonald A, Schrattenholzer L. Learning rates for energy technologies. EnergyPolicy 2001;29:255–61.

[16] Daskalakis J, Psychoyios D, Markellos N. Modeling CO2 emission allowanceprices and derivatives: evidence from the European Trading Scheme. J BankFinance 2009;33(7):1230–41.

[17] Abadie ML, Chamorro MJ. European CO2 prices and carbon captureinvestments. Energy Econ 2008;30(6):2992–3015.

[18] Blyth W, Bradley R, Bunn D, et al. Investment risks under uncertain climatechange policy. Energy Policy 2007;35:5766–73.

[19] Gibbins J, Chalmers H. Carbon capture and storage. Energy Policy2008;36:4317–22.

[20] Zhao LF, Xiao YH, Gallagher KS, et al. Technical, environmental, and economicassessment of deploying advanced coal power technologies in the Chinesecontext. Energy Policy 2008;36:2709–18.

[21] Rubin ES, Chen C, Rao A. Cost and performance of fossil fuel power plants withCO2 capture and storage. Energy Policy 2007;35:4444–54.

[22] Huanga Y, Rezvania S, McIlveen D, Minchenerb A et al. Techno-economic studyof CO2 capture and storage in coal fired oxygen fed entrained flow IGCC powerplants. Fuel Process Technol; 2008.

[23] Riahi K, Rubin E, Schrattenholzer L. Prospects for carbon capture andsequestration technologies assuming their technological learning. Energy2004;29:1218–309.

[24] REN21. Renewables 2007 global status report. Paris: REN21 Secretariat andWashington (DC): World watch Institute; 2008.

[25] Aldy JE, Stavins RN. Designing the post-Kyoto climate regime: lessons from theharvard project on international climate agreements. Cambridge (Mass): Reportfor Harvard Project on International Climate Agreements, Belfer Center forScience and International Affairs, Harvard Kennedy School, November 24, 2008.

[26] Michaelowa A, Tangen K, Hasselknippe H. Issues and options for the post-2012climate architecture – an overview. Int Environ Agreements 2005;5:5–24.

[27] Fleten SE, Maribu K, Wangensteen I. Optimal investment strategies indecentralized renewable power generation under uncertainty. Energy2007;32:803–15.

[28] Reiner D, Liang X. Opportunities and hurdles in applying CCS technologies inChina – with a focus on industrial stakeholders. Energy Procedia2009;1:4827–34.

[29] Wang C, Fu P, Chen JN. Contribution of clean development mechanism to themitigation of greenhouse gas emissions. J Tsinghua Univ 2008;48(3):357–61.

[30] Sekar RC. Carbon dioxide capture from coal-fired power plants: a real optionsanalysis. MSc Thesis, MIT; 2005.