Embed Size (px)

Citation preview

UNAUDITED INTERIM REPORT FOR THE6 MONTHS PERIOD ENDED 30 SEPTEMBER 2015

LAPORAN INTERIM TIDAK DIAUDIT BAGI TEMPOH

6 BULAN BERAKHIR 30 SEPTEMBER 2015

MANAGER:BIMB INVESTMENT MANAGEMENT BERHAD (276246-X)

2

Table of Contents

No. Particulars Page

1.0 Manager‟s Report 3

1.1

Fund Name/ Fund Type/ Fund Category/ Fund Investment

Objective/ Fund Performance Benchmark/ Fund Distribution Policy

3

1.2 Performance for the 6 months period ended 30 September

2015 4

1.3 Economic and Market Review 6

1.4 Market Outlook And Strategy 8

1.5 Asset Allocation as at 30 September 2015 10

1.6 Other Performance Data for the 6 months period ended 30 September 2015

11

1.7 Unit Holdings as at 30 September 2015 12

1.8 Policy on Rebate And Soft Commission 12

2.0 Trustee‟s Report 24

3.0 Shariah Committee‟s Report 25

4.0 Directors‟ Declaration Report 26

5.0 Unaudited Financial Statements 27

6.0 Corporate Directory 55

3

1.0 Manager’s Report

Dear Unit Holders,

We are pleased to present the Manager‟s report of BIMB i Flexi Fund for the 6 months

period ended 30 September 2015

1.1 Fund Name/ Fund Type/ Fund Category/ Fund Investment Objective/ Fund

Performance Benchmark/ Fund Distribution Policy

Fund Name BIMB i Flexi Fund

Fund Type Growth

Fund Category Shariah-compliant mixed asset

Fund Investment Objective

The Fund seeks to achieve long term1 capital growth by

investing in a diversified portfolio of Shariah-compliant securities.

Note: Any material change to the investment objective of the

Fund would require Unit Holders’ approvals.

Fund Performance Benchmark

The selected performance benchmark for this Fund is

based on 50:50 ratios of the FBM Emas Shariah Index and 12-month General Investment Account (GIA) rate of Bank Islam Malaysia Berhad.

Note: The benchmark reflects the investment and asset allocation

strategies of the Fund, where the Fund is allowed to invest its asset in Shariah-compliant equities as well as Sukuk and Islamic money market instruments, depending on the

outlook of the market. The risk profile of the Fund is not the same as the risk profile of the performance benchmark.

Fund Distribution Policy

The distribution of income is incidental.

1 Long term in this context refers to a period of more than five (5) years.

4

1.2 Performance for the 6 months period ended 30 September 2015

1.2.1 Performance review

For the period under review, BIMB i Flexi Fund (“the Fund”) registered a return of -12.94%

as compared to its Benchmark‟s return of -3.87%.

The selected performance benchmark for the Fund is 50:50 ratio of the FBM Emas

Shariah Index and 12-month Bank Islam General Investment Account (GIA) rates.

Our strategy has remained to focus on well-established companies that could potentially

pay sustainable dividends and have better prospects for earnings growth and capital

appreciation.

As at 30 September 2015, the Fund has 37.8% exposure to equities, 9.9% to Sukuk and

52.3% in short term investments, cash and cash equivalents. The total Net Asset Value

(NAV) of the Fund is RM10.3 million whereas the NAV per unit of the Fund is RM0.2159.

For the period under review, there were higher cash allocations to the Fund, executed as

a tactical move to preserve unit holders‟ value as adverse market conditions prevailed.

Moving forward, the Manager will resume investing in companies with good earnings

visibility, strong balance sheet, and high dividend yield with good valuation prospects

given the suitable opportunity arises.

For the financial period under review, there were no significant changes to the state of

affairs of the Fund and no circumstances that materially affect the interest of unit holders

that have taken place up to the date of this Manager‟s report.

1.2.2 Total return and average total return for the respective period ended 30 September

2015

BIMB i Flexi Fund Benchmark

Total Return

(%)

Average Total

Return

(%)

Total Return

(%)

Average Total

Return

(%)

1 year Period -12.91 -12.91 -3.25 -3.25

6-Months Period -12.94 N/A -3.87 N/A

5

1.2.3 Total return for the financial year

Total Return

BIMB i Flexi Fund (%)

Benchmark (%)

25 March 2014 (Date of

commencement) to 31 March 2015 -0.80

2.17

Figure 1: Fund and Benchmark Total Return for the financial period from 25 March

2014 (date of commencement) to 31 March 2015

Note:

Data Source : BIMB Investment Management Berhad

Data verified by : Novagni Analytics & Advisory Sdn. Bhd. (formerly known

as Perkasa Normandy Advisers Sdn. Bhd.)

Benchmark : 50: 50 FBM Emas Shariah Index &

12-month General Investment Account (GIA) rate of Bank

Islam Malaysia Berhad

6

Notes:

1. Total Return of the Fund has been verified by Novagni Analytics & Advisory Sdn.

Bhd. (formerly known as Perkasa Normandy Advisers Sdn. Bhd.) (363145-w)

2. Average Total return is derived by this formula:

Total Return

Number of Years under Review

Past performance is not necessarily indicative of future performance and unit prices and

investment returns may go down, as well as up.

1.3 Economic and Market Review

1.3.1 Economy

a) Global

The United States („US‟) Gross Domestic Product (GDP) grew at a rate of 3.7%

in the second quarter of 2015 as compared to 0.6% growth in the first quarter

of 2015 and 2.1% in the fourth quarter of 2014. The second quarter reflected

positive contributions from personal consumption expenditures, exports, state

and local government spending and fixed assets investments. American

households and businesses, backed by gains in employment, rising home

prices and lower fuel costs had contributed to the pace of expansion during the

quarter.

US headline inflation rate declined to -0.1% in August from 0.1% in April 2015

due to lower energy prices. US core inflation rate remained stable at 1.8% from

April thru September 2015.

US unemployment rate fell to 5.1% in August from 5.4% in April 2015,

supported by rising incomes, consumer spending and economic growth

The Euro zone economy grew by 0.4% in the second quarter of 2015 as

compared to 0.5% in the first quarter 2015 and 0.4% in the fourth quarter of

2014.Germany‟s economic growth improved while France and Italy‟s stagnated

as economic disparities between the 19-nation economy persist.

Euro zone‟s annual inflation declined to -0.1% in September from 0.0% in April

2015 as falling energy prices offset rises in industrial goods.

The Euro zone unemployment rate fell to 10.8% in August from 11.1% in April

2015 due to significant improvement of unemployment rate in Italy, Spain and

Portugal.

7

The Chinese economy maintained a growth rate of 7.0% for the second quarter

of 2015, maintaining comparable economic growth rate to the first quarter of

2015 as China‟s ruling Communist party moves towards a more sustainable

economic model based on domestic consumption instead of trade and

investment. China‟s first and second quarter‟s economic growth in 2015 was

the weakest performance since the global economic crisis.

(Source: Bloomberg, Bank Negara Malaysia and RHB Research Institute Sdn Bhd)

b) Local

The Malaysian economy moderated at 4.9 % in the second quarter of 2015

underpinned by notable impact from the Goods and Services Tax (GST), weak

commodity prices and challenging external demand among others. The 2015

second quarter‟s growth was the weakest since 3rd

quarter 2013 compared to

5.6% in the first quarter of 2015 and 5.7% in the fourth quarter of 2014.

Malaysia‟s headline inflation in August increased to 3.1% from 1.8% in April

2015 due to the continued effects of Goods and Services Tax (GST),

implemented on 1st April 2015.

Bank Negara‟s international reserve stood at USD 93.3 billion as at 30

September from US$105.8 billion in April 2015 as a result of capital flight

outside domestic economy. At these levels, the foreign exchange reserves are

sufficient to finance 8.6 months of retained imports and cover 1.2 times the

short term external debt of the nation.

Loan growth gained from 8.8% in April to 9.7% in September 2015 due to

higher lending to real estate, finance, insurance, transport and construction

sectors.

(Source: Bloomberg, Bank Negara Malaysia and RHB Research Institute Sdn Bhd)

1.3.2 Market Review

Equity

FTSE Bursa Malaysia EMAS Shariah Index (“FBM Shariah Index”) commenced the

period under review at 13,122.2 points and reached the highest of 13,388.9 points on

27th April 2015. The FBM Shariah index declined to the lowest of 10,705.63 points on 25

August 2015 before closing at 11,889.1 points on 30th September 2015. For the period

under review, the FBM Shariah index declined 1233.1 points or 9.40% whereas the FBM

KLCI index declined 209.7 points or 11.5% to close at 1,621.0 points. Among the key

factors that contributed to the movement of the index are highlighted below:

Oil price recovery of more than 40% from USD 46.59 on 13 January 2015 to USD

66.78 per barrel on 30 April 2015.

8

In May thru June, continued selling pressure from foreign institutions on mounting

concerns over the outcome of Fitch‟s announcement on Malaysia‟s sovereign

rating together with the possible negative outcome of Greece exiting the Euro

zone.

On 30 Jun 2015, Fitch affirmed Malaysia‟s sovereign credit rating at “A-” with

outlook upgraded to “Stable” on the backs of improving fiscal position, financing

flexibility and favorable GDP growth.

In early August, the Ringgit depreciated further against the US dollar as foreign

investors flee domestic equity and bond markets as fear of U.S interest rate hike

escalated. This was also underpinned by the growing concerns of the domestic

political landscape that continue to remain fluid.

In late August, the Shanghai and Shenzhen stock exchange tumble over

concerns of China‟s economic hard landing that triggered a regional sell-off

throughout Asia. This has subsequently led to a contagion effect in Europe and

the U.S. Worries over China‟s weaker consumption have also eroded oil prices

that plunged to a six-and-a-half year low of USD42.51 per barrel, adding concerns

to the global oil supply glut.

In August alone, the Ringgit had depreciated 9.7% from USD/MYR 3.82 to

USD/MYR 4.19 in light of the unfolding events during the month. Speculation over

the timing of the US interest rate hike remains uncertain in August and poses

further market volatility risk in the near term as the Ringgit continues to devalue.

Collectively, the August sell-off had erased 7% to 10% of global market

capitalization.

The U.S. Federal Reserve declined to raise interest rates in September on the

back of deteriorating global economic conditions given any possibility of monetary

tightening may interrupt global growth. During the month, global markets rallied as

investors‟ price in a deferred interest rate hike by the U.S. Federal Reserve.

(Source: Bloomberg and RHB Research Institute Sdn Bhd)

1.4 Market Outlook and Strategy

Equity

The equity market outlook is expected to experience continual volatility in 2015.

Notwithstanding the QE (Quantitative Easing) in Euro zone and Japan, global

economic recovery will face headwind from multiple aspects including the

strengthening US Dollar, potential US interest rate hike, concerns over China‟s

economic slow-down and currency devaluation along with global oil production

glut affecting oil prices.

9

On the domestic front, the Bursa Malaysia should be supported by domestic

liquidity and strong buying support from local funds. The uncertainties over the US

interest rate hike may induce volatility within the local bourse and incite capital

flight outside Malaysia‟s economic borders, deepening the Ringgit‟s devaluation.

The weakening crude oil price may also pose larger repercussion on the country‟s

oil and gas industry as well as its fiscal position in the near term.

Fundamentally, the Malaysian economy is in good stead to grow at 4.0% to 5.5%

in 2015 as domestic demand remains the growth driver supported by broad-based

capital spending by both the private and public sectors. The Malaysian

government had taken necessary steps to strengthen the economy, stabilise the

currency, and restore investor confidence, affirming that both the banking system

and the capital market are resilient and able to cope with potential economic

uncertainty.

Currently, the Fund is adopting a temporary defensive strategy via maintaining

higher cash portion within its portfolio. The equity strategy remains to invest in

companies with good earnings visibility, strong balance sheet, and high dividend

yield with good valuation prospects given the suitable opportunity arise.

Sukuk

The Ringgit Islamic Debt Securities (IDS) market is expected to be volatile. The

continued reduction in accommodative monetary policy by the Federal Reserve in

the United States and weak Ringgit will be negative for IDS price. However, the

ample liquidity in the domestic market and demand from local institutions will

support the IDS market.

Bank Negara Malaysia decided to maintain the Overnight Policy Rate (OPR) at

3.25% at the Monetary Policy Committee (MPC) meeting 11 September 2015. The

MPC statement stated that future changes in OPR will depend on economic data on

growth and inflation as well as risks of destabilising financial imbalances. Moving

forward, the OPR is expected to remain unchanged at least until Q1 2016.

Headline inflation is expected to trend higher due to GST. The lower fuel prices will

partially offset other domestic cost factors. While month-on-month headline inflation

would be subjected to the volatility in global oil prices, underlying inflation is

expected to remain contained amid the stable domestic demand conditions.

Inflation is expected to be between 2.5% to 3.5% in the next 12 months.

(Source: Bloomberg and RHB Research Institute Sdn Bhd)

10

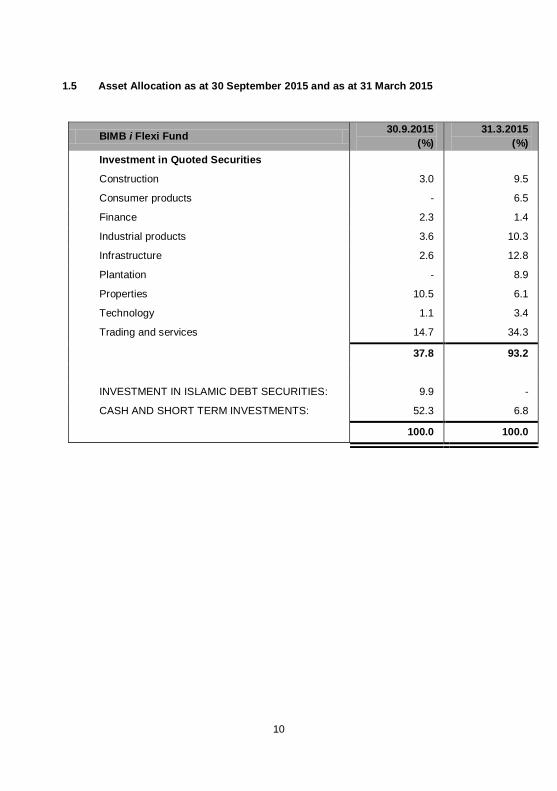

1.5 Asset Allocation as at 30 September 2015 and as at 31 March 2015

BIMB i Flexi Fund 30.9.2015

(%)

31.3.2015

(%)

Investment in Quoted Securities

Construction 3.0 9.5

Consumer products - 6.5

Finance 2.3 1.4

Industrial products 3.6 10.3

Infrastructure 2.6 12.8

Plantation - 8.9

Properties 10.5 6.1

Technology 1.1 3.4

Trading and services 14.7 34.3

37.8 93.2

INVESTMENT IN ISLAMIC DEBT SECURITIES: 9.9 -

CASH AND SHORT TERM INVESTMENTS: 52.3 6.8

100.0 100.0

11

1.6 Other Performance Data for the 6 months period ended 30 September 2015 and

last financial year ended 31 March 2015

BIMB i Flexi Fund 6 months ended

30.9.2015 31.3.2015

Unit Prices (RM)

Highest NAV per unit for the period 0.2547 0.2555

Lowest NAV per unit for the period 0.2052 0.2269

Net Asset Value (NAV) and Units in

Circulation (UIC) as at the End of the Period

Total NAV (RM) 10,328,044 15,802,032

Units in Circulation (UIC) 47,833,224 63,707,317

NAV per unit (RM) 0.2159 0.2480

Return of Fund (%)(a)

Capital Growth (%)(b)

-12.94 -0.80

Income Return (%)(c)

- -

Return of Fund (%) -12.94 -0.80

Management Expense Ratio (MER) (%)(d)

1.92 1.71

Portfolio Turnover Ratio (PTR) (times)(e)

3.37 11.69

Note:

a) Return of the Fund = NAV per unit (end of period) - 1 NAV per unit (opening of period)

b) Capital Growth = Total Return of the Fund – Income Return

c) Income Return = {Income Distribution per Unit / NAV per Unit @

opening of period} x 100

d) Management

Expenses Ratio

= The Management Expenses Ratio is the total

management expenses expressed as an annual

percentage of the Fund‟s average Net Asset Value

of the Fund calculated on a daily basis.

e) Portfolio Turnover

Ratio

= It represents the average of the total acquisitions

and disposals of the investment in the Fund for the

interim period over the average Net Asset Value of

the Fund calculated on a daily basis.

12

1.7 Unit Holdings as at 30 September 2015

Size of Holdings

BIMB i Flexi Fund

No. of Unit Holders No. of Units Held

No. % Units %

5,000 and below 21 22.34 79,599.41 0.17

5,001 to 10,000 9 9.57 67,145.72 0.14

10,001 to 50,000 45 47.87 1,198,519.48 2.51

50,001 to 500,000 16 17.02 3,008,114.05 6.29

500,001 and above * 3 3.20 43,479,845.87 90.89

Units Held by Holders 94 100.00 47,833,224.53 100.00

Unit Held by Manager 0 0.00 0.00 0.00

Grand Total for The Fund 94 100.00 47,833,224.53 100.00

* Included under this category are nominee accounts

1.8 Policy on Rebate and Soft Commission

Any stock broking rebates received by the Manager will be directed into the account of

the Fund. Any soft commissions received from the broker which are in the form of

research and advisory services that assist in the decision-making process relating to the

Fund‟s investment may be retained by the Manager. The Manager received soft

commission from brokers in the form of research and advisory services during the period

under review.

For and on behalf of

The Manager

BIMB INVESTMENT MANAGEMENT BERHAD

Date: 30 November 2015

13

1.0 Laporan Pengurus

Para Pemegang Unit yang Dihormati,

Kami dengan sukacitanya membentangkan Laporan Pengurus BIMB i Flexi Fund bagi

tempoh 6 bulan berakhir pada 30 September 2015.

1.1 Nama Dana/ Jenis Dana/ Kategori Dana/ Objektif Pelaburan Dana/ Penanda Aras

Dana/ Polisi Agihan Dana

Nama Dana BIMB i Flexi Fund

Jenis Dana Dana Pertumbuhan

Kategori Dana Aset Campuran berlandaskan Shariah

Objektif Pelaburan Dana

Tujuan utama Dana ini adalah untuk mencapai pertumbuhan modal dalam jangkamasa panjang

1 dengan melabur dalam

pelbagai portfolio sekuriti patuh Syariah. Nota: Sebarang perubahan ketara kepada objektif pelaburan Dana memerlukan kelulusan daripada Pemegang Unit.

Penanda Aras Dana

Penanda aras prestasi terpilih bagi dana ini adalah berdasarkan

kepada nisbah 50:50 Indeks FBM Emas Syariah dan pulangan 12 bulan Akaun Pelaburan Am (GIA) Bank Islam Malaysia Berhad.

Nota: Penanda aras ini mencerminkan strategi pelaburan dan peruntukan aset Dana, di mana Dana dibenarkan untuk

melaburkan asetnya ke dalam ekuiti patuh Shariah, Sukuk dan instrumen pasaran wang Islam, bergantung kepada prospek pasaran. Profil risiko Dana tidak sama dengan profil risiko

penanda aras prestasi.

Polisi Agihan

Dana Pengagihan pendapatan adalah sampingan

1 Jangkamasa panjang dalam konteks ini merujuk kepada tempoh lebih dari lima (5) tahun.

14

1.2 Pencapaian Dana bagi tempoh 6 bulan berakhir 30 September 2015.

1.2.1 Kajian Pencapaian

Bagi tempoh kewangan dalam kajian, BIMB i Flexi Fund ("Dana") mencatatkan

pulangan sebanyak -12.94% berbanding penanda arasnya sebanyak -3.87%.

Penanda aras terpilih prestasi Dana ialah nisbah 50:50 Indeks Syariah Emas

FBM dan kadar 12-bulan Akaun Pelaburan Am (GIA) Bank Islam.

Kami mempunyai strategi yang secara konsistennya memberikan tumpuan

kepada syarikat-syarikat yang sudah terkemuka yang berpotensi untuk

membayar dividen secara berkekalan dan mempunyai prospek pertumbuhan

pendapatan dan peningkatan modal yang lebih baik.

Sehingga 30 September 2015, Dana mempunyai pendedahan dalam ekuiti

sebanyak 37.8%, 9.9% dalam Sukuk dan 52.3% dalam pelaburan jangka

pendek dan wang tunai. Jumlah Nilai Aset Bersih (NAB) Dana ialah RM10.3

juta manakala NAB seunit dana ialah RM0.2159.

Bagi tempoh kewangan ini, Dana mendapat peruntukan tunai yang lebih tinggi

sebagai langkah taktikal untuk mengekalkan nilai para pemegang unit

berikutan keadaan pasaran yang terus menjejaskan. Dalam melangkah ke

hadapan, Pengurus akan meneruskan pelaburannya dalam syarikat-syarikat

yang dilihat memberikan pendapatan yang baik, keadaan kewangan yang

kukuh, dan hasil dividen yang tinggi dengan prospek penilaian yang baik

apabila timbulnya peluang-peluang yang sesuai.

Bagi tempoh kewangan ini, tidak terdapat sebarang perubahan ketara dalam

hal ehwal pengurusan Dana dan tiada berlakunya sebarang keadaan yang

menjejaskan kepentingan para pemegang unit sehingga tarikh Laporan

Pengurus disediakan.

1.2.2 Jumlah pulangan dan purata jumlah pulangan bagi setiap tempoh kewangan

berakhir 30 September 2015

BIMB i Flexi Fund Penanda Aras

Jumlah

Pulangan (%)

Purata

Jumlah Pulangan

(%)

Jumlah

Pulangan (%)

Purata

Jumlah Pulangan

(%)

Jangkamasa 1 tahun -12.91 -12.91 -3.25 -3.25

Jangkamasa 6-Bulan -12.94 N/A -3.87 N/A

15

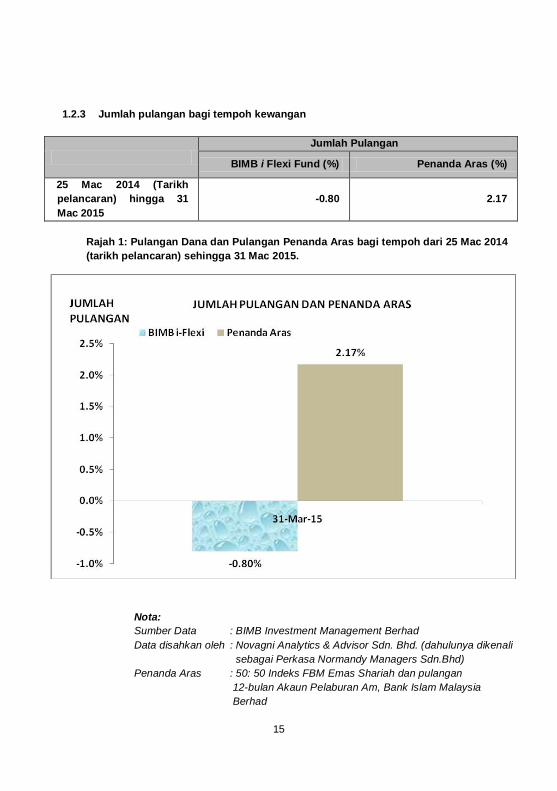

1.2.3 Jumlah pulangan bagi tempoh kewangan

Jumlah Pulangan

BIMB i Flexi Fund (%) Penanda Aras (%)

25 Mac 2014 (Tarikh

pelancaran) hingga 31

Mac 2015

-0.80 2.17

Rajah 1: Pulangan Dana dan Pulangan Penanda Aras bagi tempoh dari 25 Mac 2014

(tarikh pelancaran) sehingga 31 Mac 2015.

Nota:

Sumber Data : BIMB Investment Management Berhad

Data disahkan oleh : Novagni Analytics & Advisor Sdn. Bhd. (dahulunya dikenali

sebagai Perkasa Normandy Managers Sdn.Bhd)

Penanda Aras : 50: 50 Indeks FBM Emas Shariah dan pulangan

12-bulan Akaun Pelaburan Am, Bank Islam Malaysia

Berhad

16

Nota:

1. Jumlah Pulangan telah disahkan oleh Novagni Analytics & Advisor Sdn. Bhd.

(dahulunya dikenali sebagai Perkasa Normandy Managers Sdn. Bhd.) (363145-w)

2. Jumlah Pulangan Purata adalah berpandukan formula berikut:

Jumlah Pulangan

Bilangan Tahun Bawah Kajian

Prestasi masa lepas tidak semestinya menjadi petunjuk prestasi masa depan dan harga

unit serta pulangan pelaburan mungkin turun dan naik.

1.3 Ekonomi dan Kajian Pasaran

1.3.1 Ekonomi

a) Global

Keluaran Dalam Negara Kasar (GDP) Amerika Syarikat ('AS') telah

berkembang sebanyak 3.7% dalam suku kedua 2015 berbanding dengan

pertumbuhan 0.6% dalam suku pertama 2015 dan 2.1% dalam suku keempat

tahun 2014. Prestasi suku kedua mencerminkan sumbangan positif daripada

perbelanjaan penggunaan individu, eksport, perbelanjaan kerajaan negeri dan

tempatan dan aset tetap pelaburan. Isi rumah dan perniagaan negara itu,

peningkatan dalam guna tenaga, kenaikan harga rumah dan kos bahan api

yang lebih rendah telah menyumbang kepada peningkatan kadar

pertumbuhan pada suku tersebut.

Kadar inflasi utama Amerika Syarikat menurun kepada -0.1% dalam bulan

Ogos daripada 0.1% pada bulan April 2015 disebabkan oleh harga bahan api

yang lebih rendah. Kadar inflasi teras AS kekal stabil pada 1.8% daripada

bulan April hingga September 2015

Kadar pengangguran AS jatuh kepada 5.1% dalam bulan Ogos 2015 daripada

5.4% dalam bulan April 2015, disokong oleh peningkatan pendapatan,

perbelanjaan pengguna dan pertumbuhan ekonomi

Ekonomi Euro zon meningkat sebanyak 0.4% pada suku kedua 2015

berbanding 0.5% pada suku pertama 2015 dan 0.4% pada suku keempat

2014. Pertumbuhan ekonomi Jerman bertambah baik manakala Perancis dan

Itali pula terbantut dalam keadaan ketaksamaan ekonomi yang berterusan

dalam kalangan 19 buah negara anggotanya.

17

Kadar inflasi tahunan Zon Euro merosot kepada -0.1% pada bulan September

daripada 0.0% pada bulan April 2015 apabila kejatuhan harga bahan api

mengimbangi kenaikan dalam barangan industri.

Kadar pengangguran zon Euro jatuh kepada 10.8% pada bulan Ogos daripada

11.1% pada bulan September 2015 disebabkan oleh peningkatan yang ketara

dalam kadar pengangguran di Itali, Sepanyol dan Portugal.

Kadar pertumbuhan ekonomi China kekal sebanyak 7.0% pada suku kedua

2015, berada pada paras setanding dengan suku pertama sebelumnya

apabila parti komunis yang memerintah China bergerak ke arah mencapai

model ekonomi yang lebih mampan berdasarkan kepada penggunaan

domestik dan bukan lagi kepada perdagangan dan pelaburan. Kadar

pertumbuhan China pada suku pertama dan kedua tahun 2015 merupakan

yang paling lemah sejak krisis ekonomi global.

(Sumber: Bloomberg, Bank Negara Malaysia dan RHB Research Institute Sdn Bhd)

b) Dalam Negara

Ekonomi Malaysia berkembang dalam kadar yang sederhana iaitu 4.9% pada

suku kedua 2015 diperkuatkan oleh antaranya kesan ketara daripada cukai

barangan dan perkhidmatan (GST), harga komoditi yang lemah dan permintaan

luar yang mencabar antara lain. Pertumbuhan suku kedua 2015 adalah yang

paling lemah sejak suku ketiga 2013 berbanding dengan 5.6% pada suku

pertama 2015 dan 5.7% pada suku keempat 2014.

Kadar inflasi utama Malaysia pada bulan Ogos meningkat kepada 3.1%

daripada 1.8% pada bulan April 2015 disebabkan oleh kesan berterusan Cukai

Barangan dan Perkhidmatan (GST), yang dilaksanakan pada 1 April 2015.

Rizab antarabangsa Bank Negara Malaysia berjumlah AS$93.3 bilion pada 30

September daripada AS$ 105.8 bilion pada bulan April 2015 akibat pengaliran

keluar modal daripada ekonomi domestik. Pada tahap ini, rizab pertukaran

asing adalah memadai untuk membiayai 8.6 bulan import tertangguh dan

menampung 1.2 kali hutang luar negara bagi tempoh jangka pendek.

Pertumbuhan pinjaman meningkat daripada 8.8% pada bulan April 2015

kepada 9.7% pada bulan September 2015 berikutan pinjaman yang diberikan

kepada hartanah, kewangan, insurans, pengangkutan dan pembinaan.

(Sumber: Bloomberg, Bank Negara Malaysia dan RHB Research Institute Sdn Bhd)

18

1.3.2 Kajian Pasaran

Ekuiti

Indeks Syariah EMAS FTSE Bursa Malaysia ("FBM Syariah indeks") memasuki tempoh

kajian pada paras 13,122.2 mata dan mencapai paras tertingginya iaitu 13,388.9 mata

pada 27 April 2015. FBM Syariah indeks jatuh ke paras terendahnya iaitu 10,705.63

mata pada 25 Ogos 2015 sebelum ditutup kepada 11,889.1 mata pada 30 September

2015. Bagi tempoh kajian, FBM Syariah indeks jatuh kepada 1,233,1 mata atau 9.40%

manakala FBM KLCI indeks susut 209.7 mata atau 11.5% untuk ditutup pada 1,621.0

mata. Antara faktor utama yang menyumbang kepada pergerakan indeks dinyatakan di

bawah:

Harga minyak mentah kembali pulih lebih daripada 40% daripada AS$46.59 pada

13 Januari 2015 kepada AS$66.78 setong pada 30 April 2015.

Pada bulan Mei hingga Jun, tekanan jualan terus berlaku daripada institusi-

institusi asing dengan memuncakkan kebimbangan berkaitan keputusan

pengumuman Fitch terhadap penarafan kedaulatan Malaysia bersama-sama

dengan kemungkinan yang negatif Greece keluar dari zon Euro.

Pada 30 Jun 2015, Fitch mengesahkan penarafan kredit berdaulat Malaysia

kepada "A-" dengan tinjauan peningkatan taraf kepada "stabil" berikutan

kedudukan fiskal yang semakin baik , fleksibiliti pembiayaan dan pertumbuhan

KDNK yang menggalakkan.

Pada awal bulan Ogos, nilai mata wang Ringgit terus susut berbanding mata

wang dolar AS kerana pelabur asing “lari” daripada pasaran ekuiti dan bon

domestik kerana meningkatnya kebimbangan mereka terhadap kenaikan kadar

faedah AS. Ini juga disokong oleh kekhuatiran yang semakin meningkat tentang

landskap politik dalam negeri yang terus berubah-ubah.

Pada akhir bulan Ogos, bursa saham Shanghai dan Shenzhen menjunam

disebabkan oleh kebimbangan terhadap kejatuhan mendadak ekonomi China

yang mencetuskan penjualan secara besar-besaran seluruh rantau Asia.

Keadaan ini, membawa kepada kesan penularan di Eropah dan AS.

Kebimbangan terhadap penggunaan yang lemah di China juga menyebabkan

terjejasnya harga minyak yang menjunam ke paras rendah dalam masa enam

setengah tahun iaitu AS$42.51 setong, sekali gus meningkatkan kebimbangan

kepada berlakunya lebihan bekalan minyak global.

Bagi bulan Ogos sahaja, Ringgit telah menyusut sebanyak 9.7% daripada AS$

/RM3.82 kepada AS$ /RM4.19 dengan berlakunya peristiwa-peristiwa tertentu

pada bulan itu. Spekulasi berlakunya kenaikan kadar faedah AS terus tidak

dapat dipastikan dalam bulan Ogos dan mendedahkan lagi kepada berlakunya

risiko turun naik pasaran dalam tempoh terdekat apabila mata wang Ringgit terus

mengalami penurunan nilai. Secara kolektifnya, penjualan besar-besaran yang

19

berlaku pada bulan Ogos, telah menghakis 7% hingga 10% daripada

permodalan pasaran global.

Rizab Persekutuan AS enggan menaikkan kadar faedah pada bulan September

berikutan keadaan ekonomi global yang semakin buruk memandangkan

sebarang usaha mengetatkan dasar kewangan akan menjejas pertumbuhan

global. Pada bulan ini, pasaran global meningkat apabila harga pelabur berada

dalam kenaikan kadar faedah tertunda oleh Rizab Persekutuan AS.

(Sumber: Bloomberg dan RHB Research Institute Sdn Bhd)

1.4 Tinjauan Pasaran dan Strategi

Ekuiti

Tinjauan pasaran ekuiti dijangkakan tidak menentu pada tahun 2015. Meskipun

terdapat kelonggaran kuantitatif (QE) di zon Euro dan Jepun, pemulihan ekonomi

sejagat akan berdepan dengan halangan daripada pelbagai aspek termasuk

pengukuhan dolar AS, potensi kenaikan kadar faedah, kebimbangan tentang

pertumbuhan perlahan ekonomi China dan penilaian semula mata wang

bersama-sama dengan terdapat lebihan pengeluaran minyak mentah yang

menjejaskan harga komoditi itu.

Di dalam negara , Bursa Malaysia dilihat mampu mendapat sokongan mudah

tunai domestik dan juga sokongan belian kukuh daripada dana-dana tempatan.

Ketidakpastian terhadap kenaikan kadar faedah AS boleh menyebabkan

berlakunya keadaan turun naik dalam bursa tempatan dan membawa kepada

modal “lari” keluar daripada sempadan ekonomi Malaysia, menurunkan lagi nilai

mata wang Ringgit. Kejatuhan harga minyak mentah boleh menimbulkan kesan

lebih besar kepada industri minyak dan gas negara ini dan juga kedudukan fiskal

dalam jangka masa terdekat.

Pada dasarnya , ekonomi Malaysia berada dalam kedudukan yang baik untuk

berkembang pada kadar 4.0% hingga 5.5% pada tahun 2015 kerana permintaan

domestik kekal menjadi pemacu kepada pertumbuhan dengan sokongan

perbelanjaan modal secara menyeluruh oleh sektor awam dan swasta. Kerajaan

Malaysia telah mengambil langkah-langkah yang perlu untuk mengukuhkan

ekonomi, menstabilkan mata wang, memulihkan keyakinan pelabur ,

mengesahkan bahawa sistem perbankan dan pasaran modal adalah berdaya

tahan dan berupaya untuk menghadapi sebarang potensi ketidaktentuan

ekonomi .

Pada masa ini, Dana menerima pakai strategi defensif yang bersifat sementara

dengan mengekalkan sebahagian besar pegangan tunai dalam portfolionya .

Strategi ekuiti kekal ditumpukan kepada melabur dalam syarikat-syarikat yang

menawarkan prospek pendapatan yang baik, lembaran kira-kira yang kukuh, dan

hasil dividen yang tinggi dengan prospek penilaian yang baik sekiranya adanya

peluang-peluang yang dirasakan sesuai.

20

Sukuk

Pasaran sekuriti hutang Islam (IDS) dalam mata wang Ringgit dijangka tidak

menentu . Pengurangan berterusan dalam dasar monetari yang akomodatif oleh

Rizab Persekutuan di Amerika Syarikat dan kelemahan nilai mata wang Ringgit

akan memberikan impak negatif kepada harga IDS. Walau bagaimanapun, mudah

tunai yang lebih daripada mencukupi dalam pasaran domestik dan permintaan

institusi domestik akan menyokong pasaran IDS .

Bank Negara memutuskan untuk mengekalkan Kadar Dasar Semalaman (OPR)

pada paras 3.25 % dalam mesyuarat Jawatankuasa Dasar Kewangan (MPC) yang

diadakan pada 11 September 2015. MPC dalam kenyataannya berkata, perubahan

OPR pada masa depan akan bergantung kepada data ekonomi tentang

pertumbuhan dan inflasi serta risiko ketidakstabilan akibat ketidakseimbangan

kewangan yang menjejaskan.

Kadar inflasi utama dijangka berada dalam aliran meningkat berikutan

pelaksanaan GST. Harga bahan api yang lebih rendah akan mengimbangi

sebahagian faktor kos domestic yang lain. Walaupun inflasi bulanan tertakluk

kepada turun naik harga minyak global , inflasi asas dijangka kekal terkawal di

tengah-tengah permintaan dalam negeri yang stabil. Kadar inflasi dijangka antara

2.5% kepada 3.5% dalam tempoh 12 bulan akan datang.

(Sumber: Bloomberg dan RHB Research Institute Sdn Bhd)

21

1.5 Peruntukan Aset pada 30 September 2015 dan pada 31 Mac 2015

BIMB i Flexi Fund 30.9.2015

(%) 31.3.2015

(%)

Pelaburan Sekuriti Tersiarharga:

Pembinaan 3.0 9.5

Barangan pengguna - 6.5

Kewangan 2.3 1.4

Barangan industri 3.6 10.3

Infrastruktur 2.6 12.8

Perladangan - 8.9

Hartanah 10.5 6.1

Teknologi 1.1 3.4

Perdagangan dan perkhidmatan 14.7 34.3

37.8 93.2

PELABURAN DALAM SEKURITI HUTANG SECARA ISLAM: 9.9 -

TUNAI DAN PELABURAN JANGKA PENDEK: 52.3 6.8

100.0 100.0

22

1.6 Lain-lain data prestasi bagi tempoh 6 bulan berakhir 30 September 2015 dan tahun

kewangan berakhir 31 Mac 2015

BIMB i Flexi Fund 6 bulan berakhir

30.9.2015 31.3.2015

Harga Unit (RM)

NAB tertinggi seunit dalam tempoh 0.2547 0.2555

NAB terendah seunit dalam tempoh 0.2052 0.2269

Nilai Aset Bersih (NAB) dan Unit Dalam Edaran (UDE) pada Akhir Tempoh

Jumlah NAB (RM) 10,328,044 15,802,032

Unit Dalam Edaran (UDE) 47,833,224 63,707,317

NAB seunit (RM) 0.2159 0.2480

Jumlah Pulangan Dana (%)(a)

Pertumbuhan Modal (%)(b)

-12.94 -0.80

Pulangan Pendapatan (%)(c)

- -

Pulangan Dana -12.94 -0.80

Nisbah Perbelanjaan Pengurusan (NPP) (%)(d)

1.92 1.71

Nisbah Pusing Ganti Portfolio (NPG) (Kali)(e)

3.37 11.69

Nota:-

a) Pulangan ke atas Dana = Harga seunit (pada akhir tempoh) - 1

Harga seunit (pada awal tempoh)

b) Pertumbuhan Modal = Jumlah Pulangan Dana – Pulangan Pendapatan

c) Pulangan Pendapatan = {Pengagihan Pendapatan Se Unit / NAB se unit

pada awal tempoh} x 100

d) Nisbah Perbelanjaan

Pengurusan

= Ia dikira dengan mengambil jumlah perbelanjaan

pengurusan sepertimana yang dinyatakan sebagai

peratusan tahunan daripada jumlah purata Nilai

Aset Bersih Dana yang dikira pada asas harian.

e) Nisbah Pusing Ganti

Portfolio

= Ia dikira dengan mengambil purata jumlah

perolehan dan pelupusan pelaburan dalam Dana

bagi tempoh setengah tahun dibahagi dengan

purata Nilai Aset Bersih Dana yang dikira pada

asas harian.

23

1.7 Pecahan Pegangan Unit pada 30 September 2015

Saiz Dipegang

BIMB i Flexi Fund

Bilangan Pemegang Unit Bilangan Pegangan Unit

Bilangan % Bilangan Unit %

5,000 dan ke bawah 21 22.34 79,599.41 0.17

5,001 hingga 10,000 9 9.57 67,145.72 0.14

10,001 hingga 50,000 45 47.87 1,198,519.48 2.51

50,001 hingga 500,000 16 17.02 3,008,114.05 6.29

500,001 dan ke atas * 3 3.20 43,479,845.87 90.89

Unit yang dipegang oleh Pemegang unit

94 100.00 47,833,224.53 100.00

Unit yang dipegang oleh Pengurus

0 0.00 0.00 0.00

Jumlah Keseluruhan Dana

94 100.00 47,833,224.53 100.00

* Akaun penama juga termasuk di bawah kategori ini

1.8 Polisi Rebat dan Komisyen Bukan Tunai

Sebarang rebat broker saham yang diterima oleh Pengurus akan dimasukkan ke akaun

Dana. Apa-apa komisyen bukan tunai yang diterima daripada broker dalam bentuk

perkhidmatan penyelidikan dan nasihat yang membantu dalam proses membuat

keputusan yang berkaitan dengan pelaburan Dana boleh disimpan oleh Pengurus.

Pengurus menerima komisen bukan tunai daripada broker dalam bentuk perkhidmatan

penyelidikan dan khidmat nasihat bagi tempoh dalam kajian.

Untuk dan bagi pihak Pengurus

BIMB INVESTMENT MANAGEMENT BERHAD

Tarikh:

Nota:

Laporan ini telah diterjemahkan daripada laporan asal (dalam Bahasa Inggeris). Jika

terdapat perbezaan, sila rujuk kepada laporan Bahasa Inggeris.

24

2.0 Trustee’s Report

To the Unit Holders of

BIMB i FLEXI FUND

We, AMANAHRAYA TRUSTEES BERHAD, have acted as Trustee of BIMB i FLEXI FUND for

the 6-month period ended 30 September 2015. In our opinion, BIMB INVESTMENT

MANAGEMENT BERHAD, the Manager, has managed BIMB i FLEXI FUND in accordance

with the limitations imposed on the investment powers of the management company and the

Trustee under the Deed, other provisions of the Deed, the applicable Guidelines on Unit Trust

Funds, the Capital Markets and Services Act 2007 and other applicable laws for the period

ended on that date.

We are of the opinion that:

(a) the procedures and processes employed by the Manager to value and/or price the

units of BIMB i FLEXI FUND are adequate and that such valuation/pricing is carried

out in accordance with the Deed and other regulatory requirement; and

(b) creation and cancellation of units are carried out in accordance with the Deed and

other regulatory requirement.

Yours faithfully

AMANAHRAYA TRUSTEES BERHAD

____________________

HABSAH BINTI BAKAR

Chief Executive Officer

Kuala Lumpur, Malaysia

Date: 30 November 2015

25

3.0 Shariah Committee’s Report

UNAUDITED INTERIM REPORT FOR THE 6-MONTH PERIOD

ENDED 30 SEPTEMBER 2015

يب ٱب ٱلر س م ـ ب ٱلر ب يب ب س

To the Unit Holders of

BIMB i Flexi Fund

We have acted as the Shariah Committee of BIMB i Flexi Fund.

Our responsibilities are to ensure that the procedures and processes employed by BIMB

Investment Management Berhad and that the provisions of the Deed dated 27 March 2013

are in accordance with Shariah principles.

In our opinion, BIMB Investment Management Berhad has managed BIMB i Flexi Fund in

accordance with Shariah principles and complied with applicable guidelines, rulings or

decisions issued by the Securities Commission pertaining to Shariah matters for the 6-

month period ended 30 September 2015.

In addition, we also confirm that the investment portfolio of BIMB i Flexi Fund comprises

securities which have been classified as Shariah-compliant by the Shariah Advisory

Council (SAC) of the Securities Commission, as the case may be and that all deposits and

money market instruments placed by the Fund are Shariah-compliant.

أعٱي واهللا

For and on behalf of the Shariah Committee

………………………………………………..

USTAZ DR. AHMAD SHAHBARI@SOBRI SALAMON

(Chairman)

………………………………………………..

USTAZ DR. YUSOF RAMLI

(Committee Member)

………………………………………………..

USTAZAH DR. ASMAK AB. RAHMAN

(Committee Member)

Date: 30 November 2015

26

4.0 Directors’ Declaration

UNAUDITED INTERIM REPORT FOR THE 6-MONTH PERIOD

ENDED 30 SEPTEMBER 2015

To the Unit Holders of

BIMB i Flexi Fund

We, Mustapha Bin Hamat and Najmuddin Bin Mohd Lutfi, being two of the directors of the

Manager, BIMB Investment Management Berhad, for BIMB i Flexi Fund do hereby state

that in our opinion, the accompanying Statement of Financial Position, Statement of Profit

or Loss and Other Comprehensive Income, Statement of Changes in Net Asset Value and

Statement of Cash Flows are drawn up so as to give true and fair view of the Statement of

Financial Position of the Fund as at 30 September 2015 and Statement of Profit or Loss

and Other Comprehensive Income, Statement of Changes in Net Asset Value and

Statement of Cash Flows for the period ended on that date.

For and on behalf on the Board of Directors,

……………………………………………

MUSTAPHA BIN HAMAT

(Non Executive Independent Director)

…………………………………………..

NAJMUDDIN BIN MOHD LUTFI

(Chief Executive Officer)

Date: 30 November 2015

27

5.0 Unaudited Financial Statements

Fair Value of Financial Instruments

All Assets and Liabilities of the Fund are carried at fair values. The accounting policies on

recognition and measurement of the fair value for the Fund‟s investments are disclosed in

their respective accounting policies.

The fair value for the amount due to the Manager and Trustee, cash at bank, sundry

receivables, sundry payables and accruals approximate their respective carrying

amounts as at the balance sheet date due to the relatively short-term maturity of these

Financial Instruments.

28

BIMB i Flexi Fund

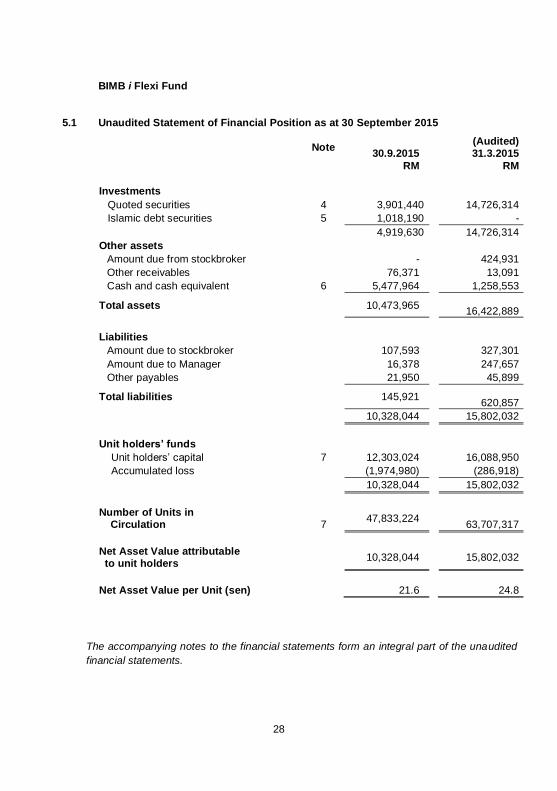

5.1 Unaudited Statement of Financial Position as at 30 September 2015

The accompanying notes to the financial statements form an integral part of the unaudited

financial statements.

Note 30.9.2015

(Audited) 31.3.2015

RM RM

Investments

Quoted securities 4 3,901,440 14,726,314

Islamic debt securities 5 1,018,190 -

4,919,630 14,726,314

Other assets

Amount due from stockbroker - 424,931

Other receivables 76,371 13,091

Cash and cash equivalent 6 5,477,964 1,258,553

Total assets 10,473,965 16,422,889

Liabilities

Amount due to stockbroker 107,593 327,301

Amount due to Manager 16,378 247,657

Other payables 21,950 45,899

Total liabilities 145,921 620,857

10,328,044 15,802,032

Unit holders’ funds

Unit holders‟ capital 7 12,303,024 16,088,950

Accumulated loss (1,974,980) (286,918)

10,328,044 15,802,032

Number of Units in Circulation 7

47,833,224

63,707,317

Net Asset Value attributable to unit holders

10,328,044 15,802,032

Net Asset Value per Unit (sen) 21.6 24.8

29

5.2 Unaudited Statement of Profit or Loss and Other Comprehensive Income for the

6 months financial period ended 30 September 2015

Note 1.4.2015

to 30.9.2015

25.3.2014

to 30.9.2014

RM RM

Income

(Loss) / Gain on sale of shares (1,533,034) 19,498

Gross dividends from shares quoted in Malaysia

270,328 119,521

Income from Islamic debt securities 1,293 -

Income from short term investments 22,031 56,779

Hibah from Al-Wadiah account 490 628

Net unrealised loss from financial instruments at fair value through profit or

loss

(323,730) (317,541)

(1,562,622) (121,115)

Less : Amortisation of premium (371) -

Gross loss (1,562,993) (121,115)

Expenses

Manager‟s fee 8 97,645 98,052

Trustee‟s fee 9 3,255 3,268

Audit fee 4,990 5,040

Tax agent fee 1,501 1,392

Administrative expenses 17,678 5,368

125,069 113,120

Net loss before taxation (1,688,062) (234,235)

Tax expense - -

Net loss after taxation (1,688,062) (234,235)

Other comprehensive income for the period - -

Total comprehensive loss for the period (1,688,062) (234,235)

Total comprehensive loss for the period

consist of:

Realised (loss)/income (1,364,332) 83,306

Unrealised amount (323,730) (317,541)

(1,688,062) (234,235)

The accompanying notes to the financial statements form an integral part of the unaudited

financial statements.

30

5.3 Unaudited Statement of Changes in Net Asset Value for the 6 months financial

period ended 30 September 2015

Unit holders’

capital (RM)

Accumulated

loss (RM)

Total

(RM)

At date of commencement

Movement in unit holders‟

contribution

Creation of units 20,359,284 - 20,359,284

Cancellation of units (346,370) - (346,370)

Total attributable to unit holders

20,012,914 - 20,012,914

Net loss for the period - (234,235) (234,235)

As at 30 September 2014 20,012,914 (234,235) (19,778,679)

Unit holders’

capital (RM)

Accumulated

loss (RM)

Total

(RM)

As at 1 April 2015 16,088,950 (286,918) 15,802,032

Movement in unit holders‟

contribution

Creation of units 33,861 - 33,861

Cancellation of units (3,819,787) - (3,819,787)

Total attributable to unit holders

(3,785,926) - (3,785,926)

Net loss for the period - (1,688,062) (1,688,062)

As at 30 September 2015 12,303,024 (1,974,980) 10,328,044

The accompanying notes to the financial statements form an integral part of the

unaudited financial statements.

31

5.4 Unaudited Statement of Cash Flows for the 6 months financial period ended

30 September 2015

1.4.2015

to 30.9.2015

25.3.2014

to 30.9.2014

RM RM

Cash flows from operating activities

Dividend received 225,396 103,894

Profit received from debt securities and short

term investments 5,465 54,959

Payment for other fee and expenses (15,659) (328)

Audit fee paid (11,000) -

Trustee fee paid (3,472) (2,402)

Manager‟s fee paid (104,172) (72,072)

Proceeds from sale of investments 17,657,258 4,493,722

Purchase of investments (8,483,887) (16,810,772)

Purchase of debt securities (1,018,600) -

Net cash generated/(used in) operating activities

8,251,329 (12,232,999)

Cash flows from financing activities

Creation of units 33,861 20,311,475

Cancellation of units (4,065,779) (337,451)

Net cash (used in)/generated from financing

activities (4,031,918) 19,974,024

Net increase in cash and cash equivalents 4,219,411 7,741,025

Cash and cash equivalents as at 1 April and at date of commencement

1,258,553 -

Cash and cash equivalents at 30 September

5,477,964 7,741,025

Cash and cash equivalents comprise:

Cash at bank 275,878 426,150

Short term investments 5,202,086 7,314,875

5,477,964 7,741,025

The accompanying notes to the financial statements form an integral part of the

unaudited financial statements.

32

5.5 Notes to the Financial Statements

1. Information on the Fund

BIMB i Flexi Fund (hereinafter referred to as “the Fund”) was constituted pursuant to the

execution of a Deed dated 27 March 2013 between the Manager - BIMB Investment

Management Berhad, the Trustee – AmanahRaya Trustees Berhad and the registered

holders of the Fund. The address of the registered office and principal place of business

of the Fund are as follows:

Registered office

Level 32, Menara Bank Islam

No. 22, Jalan Perak

50450 Kuala Lumpur

Principal place of business

Level 19, Menara Bank Islam

No.22, Jalan Perak

50450 Kuala Lumpur

The principal activity of the Fund is to invest in Authorised Investments as defined in the

Deed, which include stocks and shares of companies quoted on Bursa Malaysia and

short term placements.

The Manager, BIMB Investment Management Berhad, a company incorporated in

Malaysia, is a subsidiary of Bank Islam Malaysia Berhad.

The financial statements were approved by the Board of Directors of the Manager on

30 November 2015.

2. Basis of Preparation

(a) Statement of Compliance

The financial statements of the Fund have been prepared in accordance with the

Securities Commission‟s Guidelines on Unit Trust Funds, the Deed, Malaysian

Financial Reporting Standards (“MFRSs”) and International Financial Reporting

Standards.

The following are accounting standards, amendments and interpretations that

have been issued by the Malaysian Accounting Standards Board (“MASB”) but

have not been adopted by the Fund:

33

2. Basis of Preparation

(a) Statement of Compliance (continued)

MFRSs, Interpretations and amendments effective for annual periods beginning

on or after 1 January 2016

Amendments to MFRS 5, Non-current Assets Held for Sale and Discontinued

Operations (Annual Improvements 2012-2014 Cycle)

Amendments to MFRS 7, Financial Instruments: Disclosures (Annual

Improvements 2012-2014 Cycle)

Amendments to MFRS 10, Consolidated Financial Statements and MFRS 128,

Investments in Associates and Joint Ventures – Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture

Amendments to MFRS 10, Consolidated Financial Statements, MFRS 12,

Disclosure of Interests in Other Entities and MFRS 128, Investments in

Associates and Joint Ventures – Investment Entities: Applying the Consolidation

Exception

Amendments to MFRS 11, Joint Arrangements – Accounting for Acquisitions of

Interests in Joint Operations

MFRS 14, Regulatory Deferral Accounts

Amendments to MFRS 101, Presentation of Financial Statements – Disclosure

Initiative

Amendments to MFRS 116, Property, Plant and Equipment and MFRS 138,

Intangible Assets – Clarification of Acceptable Methods of Depreciation and

Amortisation

Amendments to MFRS 116, Property, Plant and Equipment and MFRS 141,

Agriculture – Agriculture: Bearer Plants

Amendments to MFRS 119, Employee Benefits (Annual Improvements 2012-2014

Cycle)

Amendments to MFRS 127, Separate Financial Statements – Equity Method in

Separate Financial Statements

Amendments to MFRS 134, Interim Financial Reporting (Annual Improvements

2012-2014 Cycle)

MFRSs, Interpretations and amendments effective for annual periods beginning

on or after 1 January 2017

MFRS 15, Revenue from Contracts with Customers

MFRSs, Interpretations and amendments effective for annual periods beginning

on or after 1 January 2018

MFRS 9, Financial Instruments (2014)

34

2. Basis of Preparation (continued)

(a) Statement of Compliance (continued)

The Fund plans to apply the abovementioned accounting standards, amendments

and interpretations:

from the annual period beginning on 1 April 2016 for those accounting

standards, amendments or interpretations that are effective for annual periods

beginning on or after 1 January 2016 except for MFRS 5, MFRS 10, MFRS 11,

MFRS 14, MFRS 116, MFRS 119, MFRS 127 and MFRS 134 which are not

applicable to the Fund.

from the annual period beginning on 1 April 2017 for those accounting

standards, amendments or interpretations that are effective for annual periods

beginning on or after 1 January 2017.

from the annual period beginning on 1 April 2018 for those accounting

standards, amendments or interpretations that are effective for annual periods

beginning on or after 1 January 2018.

The Fund is currently assessing the financial impact of adopting the abovementioned

standards, amendments and interpretations.

(b) Basis of Measurement

The financial statements are prepared on the historical cost basis except as disclosed

in note 3(a).

(c) Functional and Presentation Currency

These financial statements are presented in Ringgit Malaysia (RM), which is the

Fund‟s functional currency.

(d) Use of Estimates and Judgments

The preparation of financial statements in conformity with MFRSs requires

management to make judgments, estimates and assumptions that affect the

application of accounting policies and the reported amounts of assets, liabilities,

income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions

to accounting estimates are recognised in the period in which the estimate is revised

and in any future periods effected.

There are no significant areas of estimation uncertainty and critical judgments in

applying accounting policies that have significant effect on the amounts recognised in

the financial statements.

35

3. Significant Accounting Policies

The accounting policies set out below have been applied consistently to the periods

presented in these financial statements, unless otherwise stated.

(a) Financial instruments

(i) Initial recognition and measurement

A financial instrument is recognised in the statement of financial position when,

and only when, the Fund becomes a party to the contractual provisions of the

instrument.

A financial instrument is recognised initially, at its fair value plus, in the case of a

financial instrument not at fair value through profit or loss, transaction costs that

are directly attributable to the acquisition or issue of the financial instrument.

(ii) Financial instrument categories and subsequent measurement

The Fund categories financial instruments as follows:

Financial assets

(a) Financial assets at fair value through profit or loss

Fair value through profit or loss category comprises financial assets that are

held for trading, or financial assets that are specifically designated into this

category upon initial recognition. These include quoted securities and

Islamic debt securities.

Financial assets categorised as fair value through profit or loss are

subsequently measured at their fair values with the gain or loss recognised

in the statement of profit or loss and other comprehensive income.

(b) Financing and receivables

Financing and receivables category are debt instruments that are not

quoted in an active market and these comprises other receivables, amount

due from stockbroker, amount due from Manager, cash at bank and short

term investments. Financial assets categorised as financing and

receivables are subsequently measured at amortised cost using the

effective profit method.

All financial assets except for those measured at fair value through profit or loss,

are subject to review for impairment, Note 3(d).

36

3. Significant Accounting Policies (continued)

(a) Financial instruments (continued)

Financial liabilities

Financial liabilities measured at amortised cost comprises amount due to

stockbroker, amount due to Manager and other payables.

(iii) Derecognition

A financial asset or part of it is derecognised when, and only when the

contractual rights to the cash flows from the financial asset expire or the financial

asset is transferred to another party without retaining control or substantially all

risks and rewards of the asset. On derecognition of a financial asset, the

difference between the carrying amount and the sum of the consideration

received (including any new asset obtained less any new liability assumed) and

any cumulative gain or loss that had been recognised in equity is recognised in

profit or loss.

A financial liability or a part of it is derecognised when, and only when, the

obligation specified in the contract is discharged or cancelled or expires. On

derecognition of a financial liability, the difference between the carrying amount

of the financial liability extinguished or transferred to another party and the

consideration paid, including any non-cash assets transferred or liabilities

assumed, is recognised in profit or loss.

(b) Income Recognition

(i) Dividend income

Dividend from quoted investments is recognised when right to receive payment is

established.

(ii) Income from short term investments

Income from short term investments and Islamic debt securities are recognised in

the statement of profit or loss and other comprehensive income as it accrues,

taking into account the effective profit on the asset.

(c) Cash and Cash Equivalents

Cash and cash equivalents consist of cash at bank and short term investments with

licensed financial institutions which are readily convertible to cash with an insignificant

risk of changes in value. Cash and cash equivalents are categorised and measured as

financing and receivables in accordance with policy Note 3(a)(ii)(b).

37

3. Significant Accounting Policies (continued)

(d) Impairment

Financial assets

All financial assets (except for financial assets categorised as fair value through profit

or loss) are assessed at each reporting date whether there is any objective evidence

of impairment as a result of one or more events having an impact on the estimated

future cash flows of the asset. Losses expected as a result of future events, no matter

how likely, are not recognised.

An impairment loss in respect of financing and receivables is recognised in profit or

loss and is measured as the difference between the asset‟s carrying amount and the

present value of estimated future cash flows discounted at the asset‟s original

effective profit rate. The carrying amount of the asset is reduced through the use of

an allowance account.

(e) Taxation

Tax expense comprises current and deferred tax. Tax expense is recognised in the

statement of profit or loss and other comprehensive income except to the extent that it

relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable on the taxable income for the year, using tax

rates enacted or substantively enacted at the statement of financial position date, and

any adjustment to tax payable in respect of previous years.

(f) Unit holders’ capital

The Fund issues cancellable units, which are cancelled at the holder‟s option and are

classified as equity. Cancellable units can be put back to the Fund at any time for

cash equal to a proportionate share of the Fund‟s net asset value. The outstanding

units is carried at the redemption amount that is payable at the financial position date

if the holder exercises the right to put the unit back to the Fund.

Units are created and cancelled at the holder‟s option at prices based on the Fund‟s

net assets value per unit at the time of creation or cancellation. The Fund‟s net assets

value per unit is calculated by dividing the net assets attributable to unit holders with

the total number of outstanding units. In accordance with the Securities Commission‟s

Guidelines on Unit Trust Funds in Malaysia, investment positions are valued based on

the last traded market price for the purpose of determining the net assets value per

unit for creations and cancellations.

38

3. Significant Accounting Policies (continued)

(f) Unit holders’ capital (continued)

The units in the Fund are puttable instruments, classified as equity, which entitle the

unit holders to a pro-rata share of the net asset of the Fund. The units are

subordinated and have identical features. There is no contractual obligation to deliver

cash or another financial asset other than the obligation on the Fund to repurchase

the units. The total expected cash flows from the units are based on the change in the

net asset of the Fund.

(g) Distribution

Distributions are at the discretion of the Fund. A distribution to the Fund‟s unit holders

is accounted for as a deduction from realised reserves except when realised reserves

is not enough, it will be sourced out of distribution equalisation. The mode of the

income distribution is via creation of additional units based on NAV as at the date one

month after the accrual date. A proposed distribution is recognised in equity in the

period in which they are declared.

(h) Net Asset Value

As the distribution is to be reinvested, for this Fund, the Net Assets Value is calculated

after deducting the retained earnings allocated for distribution.

39

3. Significant Accounting Policies (continued)

(i) Fair value measurement

The fair value of an asset or a liability, except for share-based payment and lease

transactions, is determined as the price that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants at the

measurement date. The measurement assumes that the transaction to sell the asset

or transfer the liability takes place either in the principal market or in the absence of a

principal market, in the most advantageous market.

For non-financial asset, the fair value measurement takes into account a market

participant‟s ability to generate economic benefits by using the asset in its highest

and best use or by selling it to another market participant that would use the asset in

its highest and best use.

When measuring the fair value of an asset or a liability, the Fund uses observable

market data as far as possible. Fair value are categorised into different levels in a fair

value hierarchy based on the input used in the valuation technique as follows:

Level 1: quoted prices (unadjusted) in active markets for identical assets or

liabilities that the Fund can access at the measurement date.

Level 2: inputs other than quoted prices included within Level 1 that are

observable for the asset or liability, either directly or indirectly.

Level 3: unobservable inputs for the asset or liability.

The Fund recognises transfers between levels of the fair value hierarchy as of the

date of the event or change in circumstances that caused the transfers.

40

4. Quoted Investments

As at 30 September 2015 Company’s Name

Number of shares

held Cost

RM

Market value

RM

Percentage

of value of funds at

30.9.2015

%

(A) Main Market

(i) Construction

WCT Holdings Bhd. 227,711 448,868 311,964 3.02

(ii) Finance

Syarikat Takaful

Malaysia Bhd. 64,000 256,994 241,280 2.34

(iii) Industrial products

Petronas Chemicals

Group Bhd. 37,000 246,110 227,180 2.20

Petronas Gas Bhd. 6,700 159,396 147,132 1.42

405,506 374,312 3.62

(iv) Infrastructure

DiGi.Com Bhd. 48,100 277,479 266,955 2.58

(v) Properties

Eastern & Oriental

Bhd. 41,000 79,728 64,780 0.63

Malaysian Resources Corporation Bhd.

180,000 303,649 212,400 2.06

Matrix Concepts Holdings Bhd.

74,667 208,760 170,987 1.66

Sunway Bhd. 174,500 612,574 549,675 5.32

UEM Sunrise Bhd. 69,500 149,908 85,485 0.83

1,354,619 1,083,327 10.50

(vi) Technology

Unisem (M) Bhd. 55,000 107,576 111,650 1.08

41

4. Quoted Investments (continued)

As at 30 September 2015

Company’s Name

Number of

shares

held

Cost

RM

Market value

RM

Percentage

of value of funds at

30.9.2015

%

(A) Main Market (continued)

(vii) Trading and services

Axiata Group Bhd. 93,957 645,984 544,951 5.28

Dayang Enterprise Holdings Bhd.

61,000 186,916 102,480 0.99

Sime Darby Bhd. 54,000 502,643 420,660 4.07

Tenaga Nasional Bhd. 29,500 378,709 354,590 3.43

UMW Oil & Gas Corporation Bhd.

76,300 261,553 89,271 0.87

1,975,805 1,511,952 14.64

Total portfolio investment as at 30 September 2015

4,826,847 3,901,440 37.78

42

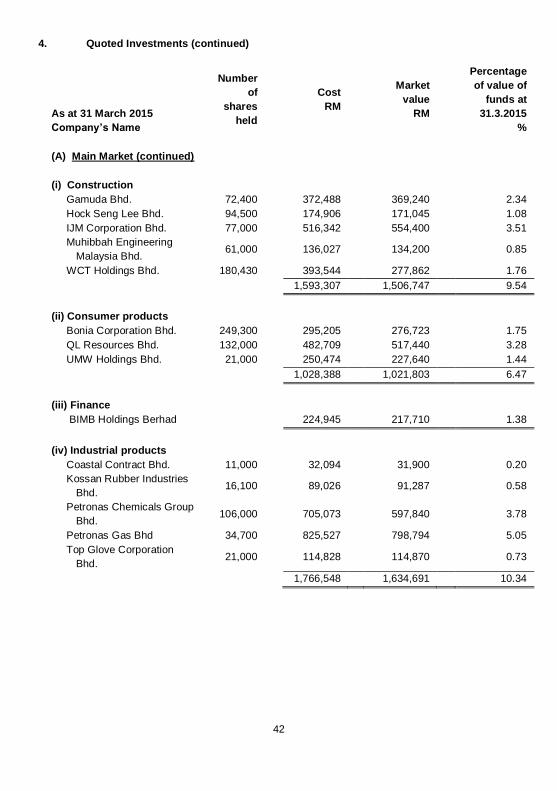

4. Quoted Investments (continued)

As at 31 March 2015

Company’s Name

Number

of

shares

held

Cost

RM

Market

value

RM

Percentage

of value of

funds at

31.3.2015

%

(A) Main Market (continued)

(i) Construction

Gamuda Bhd. 72,400 372,488 369,240 2.34

Hock Seng Lee Bhd. 94,500 174,906 171,045 1.08

IJM Corporation Bhd. 77,000 516,342 554,400 3.51

Muhibbah Engineering

Malaysia Bhd. 61,000 136,027 134,200 0.85

WCT Holdings Bhd. 180,430 393,544 277,862 1.76

1,593,307 1,506,747 9.54

(ii) Consumer products

Bonia Corporation Bhd. 249,300 295,205 276,723 1.75

QL Resources Bhd. 132,000 482,709 517,440 3.28

UMW Holdings Bhd. 21,000 250,474 227,640 1.44

1,028,388 1,021,803 6.47

(iii) Finance

BIMB Holdings Berhad 224,945 217,710 1.38

(iv) Industrial products

Coastal Contract Bhd. 11,000 32,094 31,900 0.20

Kossan Rubber Industries

Bhd. 16,100 89,026 91,287 0.58

Petronas Chemicals Group

Bhd. 106,000 705,073 597,840 3.78

Petronas Gas Bhd 34,700 825,527 798,794 5.05

Top Glove Corporation

Bhd. 21,000 114,828 114,870 0.73

1,766,548 1,634,691 10.34

43

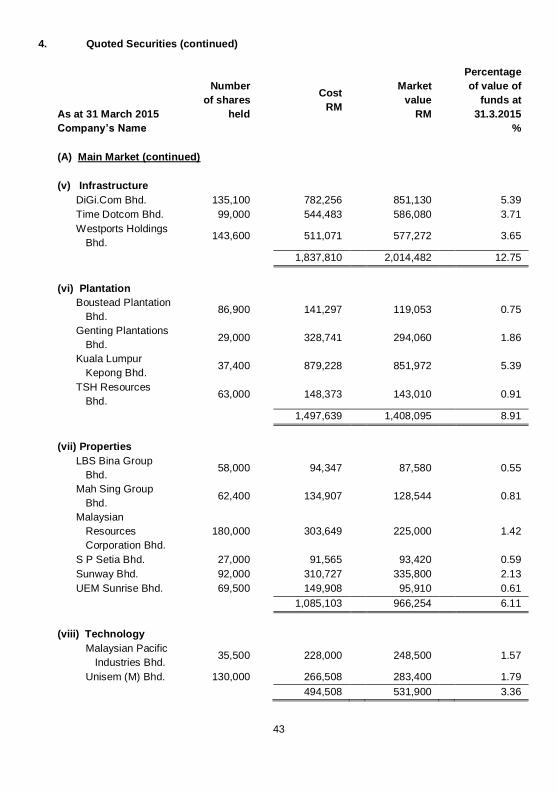

4. Quoted Securities (continued)

As at 31 March 2015

Company’s Name

Number

of shares

held

Cost

RM

Market

value

RM

Percentage

of value of

funds at

31.3.2015

%

(A) Main Market (continued)

(v) Infrastructure

DiGi.Com Bhd. 135,100 782,256 851,130 5.39

Time Dotcom Bhd. 99,000 544,483 586,080 3.71

Westports Holdings

Bhd. 143,600 511,071 577,272 3.65

1,837,810 2,014,482 12.75

(vi) Plantation

Boustead Plantation

Bhd. 86,900 141,297 119,053 0.75

Genting Plantations

Bhd. 29,000 328,741 294,060 1.86

Kuala Lumpur

Kepong Bhd. 37,400 879,228 851,972 5.39

TSH Resources

Bhd. 63,000 148,373 143,010 0.91

1,497,639 1,408,095 8.91

(vii) Properties

LBS Bina Group

Bhd. 58,000 94,347 87,580 0.55

Mah Sing Group

Bhd. 62,400 134,907 128,544 0.81

Malaysian

Resources

Corporation Bhd.

180,000 303,649 225,000 1.42

S P Setia Bhd. 27,000 91,565 93,420 0.59

Sunway Bhd. 92,000 310,727 335,800 2.13

UEM Sunrise Bhd. 69,500 149,908 95,910 0.61

1,085,103 966,254 6.11

(viii) Technology

Malaysian Pacific

Industries Bhd. 35,500 228,000 248,500 1.57

Unisem (M) Bhd. 130,000 266,508 283,400 1.79

494,508 531,900 3.36

44

4. Quoted Securities (continued)

As at 31 March 2015

Company’s Name

Number

of shares

held

Cost

RM

Market

value

RM

Percentage

of value of

funds at

31.3.2015

%

(A) Main Market (continued)

(ix) Trading and services

Axiata Group Bhd. 124,100 856,322 878,628 5.56

Brahims Holdings Bhd. 220,600 367,666 185,304 1.17

Dayang Enterprise

Holdings Bhd. 61,000 186,916 142,130 0.90

Dialog Group Bhd. 395,180 708,624 624,385 3.95

IHH Healthcare Bhd. 61,900 305,917 372,019 2.35

KPJ Healthcare Bhd. 26,000 110,079 110,760 0.70

Maxis Bhd. 49,000 332,582 352,310 2.23

MMC Corporation Bhd. 61,000 151,396 154,330 0.98

Sime Darby Bhd. 71,000 663,796 658,170 4.17

SapuraKencana

Petroleum Bhd. 24,600 103,370 58,056 0.37

Tenaga Nasional Bhd. 56,500 729,986 811,340 5.13

TH Heavy Engineering

Bhd. 372,500 295,523 126,650 0.80

Telekom Malaysia Bhd. 108,000 737,248 785,160 4.97

UMW Oil & Gas

Corporation Bhd. 49,300 195,422 113,390 0.72

Uzma Bhd. 25,000 54,935 52,000 0.33

5,799,782 5,424,632 34.33

Total portfolio investment

as at 31 March 2015 15,328,030 14,726,314 93.19

45

5. Islamic Debt Securities

Issuer

Maturity

date

Rating*

Cost

Market

value

Percentage

of value

of Funds at

30.9.2015

As at 30

September

2015

RM RM %

Malakoff

Power

Berhad 28.12.2016 AA3 1,018,600 1,018,190 9.86

* Rating is either by Rating Agency Malaysia Berhad or Malaysian Rating Corporation

Berhad, whichever applicable.

6. Cash and cash equivalents

As at

30.9.2015 RM

As at 31.3.2015

RM

Short term placements in licensed financial institutions:

Commodity Murabahah 2,502,086 -

Term Deposit-i (Tawarruq)-Special* - 1,013,355

Term Deposit 2,700,000 -

5,202,086 1,013,355

Cash at bank* 275,878 245,198

5,477,964 1,258,553

* Term Deposit-i (Tawarruq) - Special and cash at bank are placed with a related party,

Bank Islam Malaysia Berhad.

7. Unit holders’ Capital

1.4.2015 to 30.9.2015 25.3.2014 to 31.3.2015

No. of units (RM) No. of units (RM)

At beginning of the period/ commencement

63,707,317 16,088,950 - -

Creation during the period/year

152,040 33,861 82,464,105 20,670,986

Cancellation during the

period/year (16,026,133) (3,819,787) (18,756,788) (4,582,036)

At end of the period/year 47,833,224 12,303,024 63,707,317 16,088,950

46

8. Manager’s Fee

For the 6 months financial period ended 30 September 2015, the manager fee is recognised

at a rate of 1.50% per annum (30 September 2014: 1.50% per annum).

The manager‟s fee payable to the Manager of the Fund on a monthly basis, computed

based on the net asset value of the Fund calculated on a daily basis.

9. Trustee’s Fee

For the 6 months financial period ended 30 September 2015, the trustee fee is recognised

at a rate of 0.05% per annum (30 September 2014: 0.05% per annum).

The trustee‟s fee payable to the Trustee of the Fund on a monthly basis, computed based

on the net asset value of the Fund calculated on a daily basis.

10. Units held by related parties

The Manager and related party of the Manager do not hold any unit in the Fund as at 30

September 2015 (30 September 2014: Nil).

47

11. Transactions with related and other stock broking companies

1.4.2015 to 30.9.2015

Value of

trade

Percentage

of total

trade

Brokerage

fee

Percentage

of total

brokerage

fee

RM % RM %

BIMB Securities Sdn. Bhd.* 4,438,507 16.82 15,524 17.31

TA Securities Holdings

Berhad 3,746,833 14.20 12,818 14.29

Maybank Investment Bank

Berhad 3,146,612 11.92 11,929 13.30

Public Investment Bank

Berhad. 3,146,123 11.92 10,944 12.20

RHB Investment Bank

Berhad 3,049,828 11.56 10,373 11.56

Hong Leong Investment

Bank Berhad. 2,316,689 8.78 7,725 8.61

CIMB Investment Bank

Berhad 1,293,751 4.90 5,652 6.30

AmInvestment Bank Berhad 1,293,017 4.90 4,430 4.94

Kenanga Investment Bank

Berhad 1,147,228 4.35 4,083 4.55

Hong Leong Islamic Bank

Berhad 1,018,600 3.86 - -

Others

1,791,834

6.79

6,232

6.94

26,389,022 100.00 89,710 100.00

* Transactions with the related party have been entered into in the normal course of

business and have been transacted at arm‟s lengths basis.

48

11. Transactions with related and other stock broking companies (continued)

25.3.2014 to 30.9.2014

Value of

trade

Percentage

of total trade

Brokerage

fee

Percentage

of total

brokerage

fee

RM % RM %

TA Securities Holdings Bhd. 3,554,013 16.21 12,702 16.34

Maybank Investment Bank

Berhad. 3,268,131 14.91 11,331 14.58

MIDF Amanah Investment

Bank Berhad. 2,929,931 13.37 10,445 13.44

Kenanga Investment Bank

Berhad. 2,502,491 11.42 8,907 11.46

Hong Leong Investment

Bank Berhad. 2,446,519 11.16 8,704 11.20

RHB Investment Bank

Berhad. 2,323,720 10.60 8,198 10.55

CIMB Investment Bank

Berhad. 1,818,933 8.30 6,475 8.33

BIMB Securities Sdn Bhd.* 1,638,382 7.47 5,846 7.52

AmInvestment Bank

Berhad. 1,364,976 6.23 4,855 6.25

Public Investment Bank

Berhad. 73,122 0.33 260 0.33

Others 3,554,013 16.21 12,702 16.34

21,920,218 100.00 77,723 100.00

* Transactions with the related party have been entered into in the normal course of

business and have been transacted at arm‟s lengths basis.

12. Management Expense Ratio (“MER”)

The management expense ratio for the 6 months financial period is 1.92% (30 September

2014: 1.71%). Management expense ratio is the ratio of total fees and recovered expenses

of the Fund expressed as a percentage of the Fund‟s average net asset value. It is a total

management expenses expressed as an annual percentage of the Fund‟s average net

asset value.

13. Portfolio Turnover Ratio (“PTR”)

The portfolio turnover ratio for the 6 months financial period is 3.37 times (30 September 2014: 0.86 times). It represents the average of total acquisitions and disposals of the investments in the Fund for the financial period over the average net asset value of the

Fund calculated on a daily basis.

49

14. Financial Instruments

14.1 Categories of financial instruments

The table below provides an analysis of financial instruments categorised as follows: (a) Financing and receivables (F&R);

(b) Fair value through profit or loss (FVTPL);

(c) Other financial liabilities measured at amortised cost (OL).

Carrying

amount

RM

F&R/

(OL)

RM

FVTPL

RM

As at 30.9 2015

Financial assets

Quoted securities 3,901,440 - 3,901,440

Islamic debt securities 1,018,190 - 1,018,190

Receivables 76,371 76,371 -

Cash and cash equivalents 5,477,964 5,477,964 -

10,473,965 5,554,335 4,919,630

Financial liabilities

Payables (145,921) (145,921) -

As at 31.3.2015

Financial assets

Quoted securities 14,726,314 - 14,726,314

Receivables 438,022 438,022 -

Cash and cash equivalents 1,258,553 1,258,553 -

16,422,889 1,696,575 14,726,314

Financial liabilities

Payables (620,857) (620,857) -

50

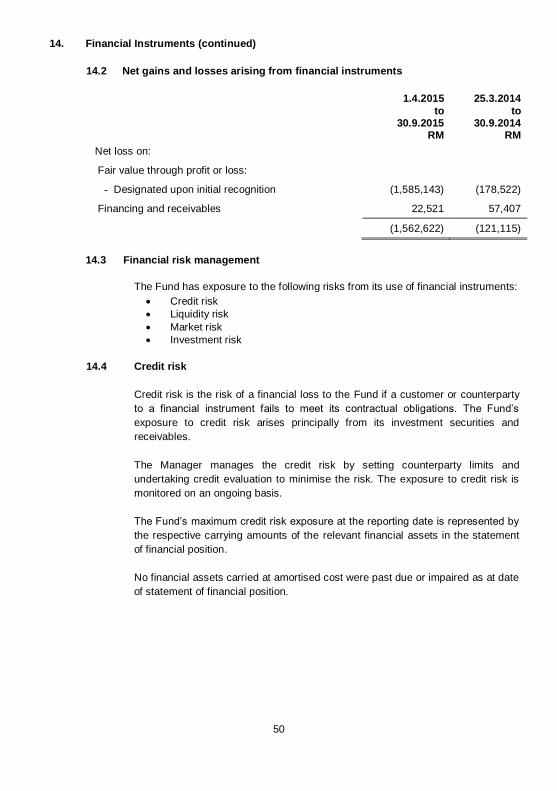

14. Financial Instruments (continued)

14.2 Net gains and losses arising from financial instruments

1.4.2015

to 30.9.2015

RM

25.3.2014

to 30.9.2014

RM

Net loss on:

Fair value through profit or loss:

- Designated upon initial recognition (1,585,143) (178,522)

Financing and receivables 22,521 57,407

(1,562,622) (121,115)

14.3 Financial risk management

The Fund has exposure to the following risks from its use of financial instruments:

Credit risk

Liquidity risk

Market risk

Investment risk

14.4 Credit risk

Credit risk is the risk of a financial loss to the Fund if a customer or counterparty

to a financial instrument fails to meet its contractual obligations. The Fund‟s

exposure to credit risk arises principally from its investment securities and

receivables.

The Manager manages the credit risk by setting counterparty limits and

undertaking credit evaluation to minimise the risk. The exposure to credit risk is

monitored on an ongoing basis.

The Fund‟s maximum credit risk exposure at the reporting date is represented by

the respective carrying amounts of the relevant financial assets in the statement

of financial position.

No financial assets carried at amortised cost were past due or impaired as at date

of statement of financial position.

51

14. Financial Instruments (continued)

14.5 Liquidity risk

Liquidity risk is the risk that the Fund will not be able to meet its financial

obligations as they fall due. The Fund‟s exposure to liquidity risk arises principally

from its various payables which are due within one year.

The Fund maintains sufficient level of liquid assets, after consultation with the

Trustee, to meet anticipated payments and cancellation of units by unit holders.

Liquid assets comprise cash and other instruments, which are capable of being

converted into cash within 7 days.

14.6 Market risk

Market risk is the risk that changes in market prices, such as profit rates and

market prices will affect the Fund‟s financial position or cash flows.

Profit rate risk

The profit rate profile of the Fund‟s significant profit-bearing financial instruments,

based on carrying amounts as at the end of reporting period was:

Fixed rate instruments As at

30.9.2015 RM

As at 31.3.2015

RM

Islamic debt securities 1,018,190 -

Short term investments 5,202,086 1,013,355

Fair value sensitivity analysis for fixed rate instruments

The Fund account for the Islamic debt securities at fair value through profit and

loss.

An increase of 100 basis points (bps) in profit rates at the end of the reporting

period would have decreased on the unit holders‟ fund and statement of

comprehensive income by RM 12,009 (30 September 2014: Nil). A decrease of