Embed Size (px)

Citation preview

Toledo Accountants.net

Tax Talk for 2011 Presenter: Charlie Finley

FILING BASICS

Sections of Form 1040

Total Income Adjustments (Not available on

1040EZ) Adjusted Gross Income Itemized or Standard

Deduction/Exemptions Taxable Income Tax Non Refundable Credits Payments, Refundable Credits Refund or Balance Due

MAJOR SCHEDULESSch- A (Itemized Deductions)Sch- B (Interest and Dividends)Sch- C (Self employed Income)Sch- D Cap Gains Income)(Sale of Stock and Personal Prop)Sch- E (Rental Prop and Royalties)Sch- F (Farm Income)Sch- EIC (Earned Income Credit)Sch- R (Credit for the Elderly)Sch- SE (Self employment Tax)

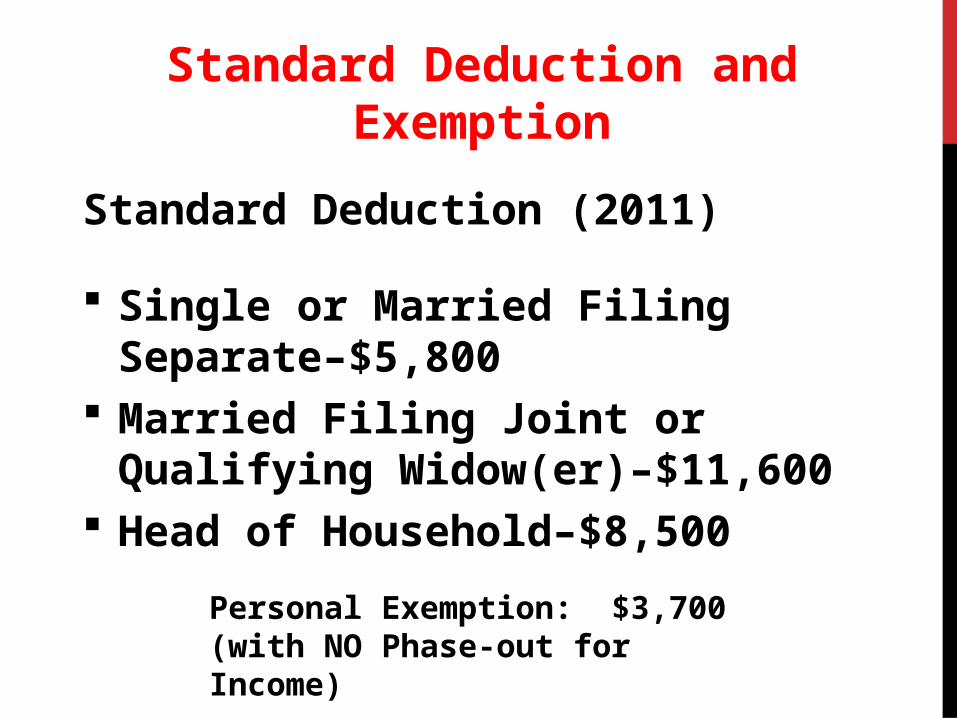

Standard Deduction and Exemption

Standard Deduction (2011)

Single or Married Filing Separate–$5,800

Married Filing Joint or Qualifying Widow(er)–$11,600

Head of Household–$8,500

Personal Exemption: $3,700 (with NO Phase-out for Income)

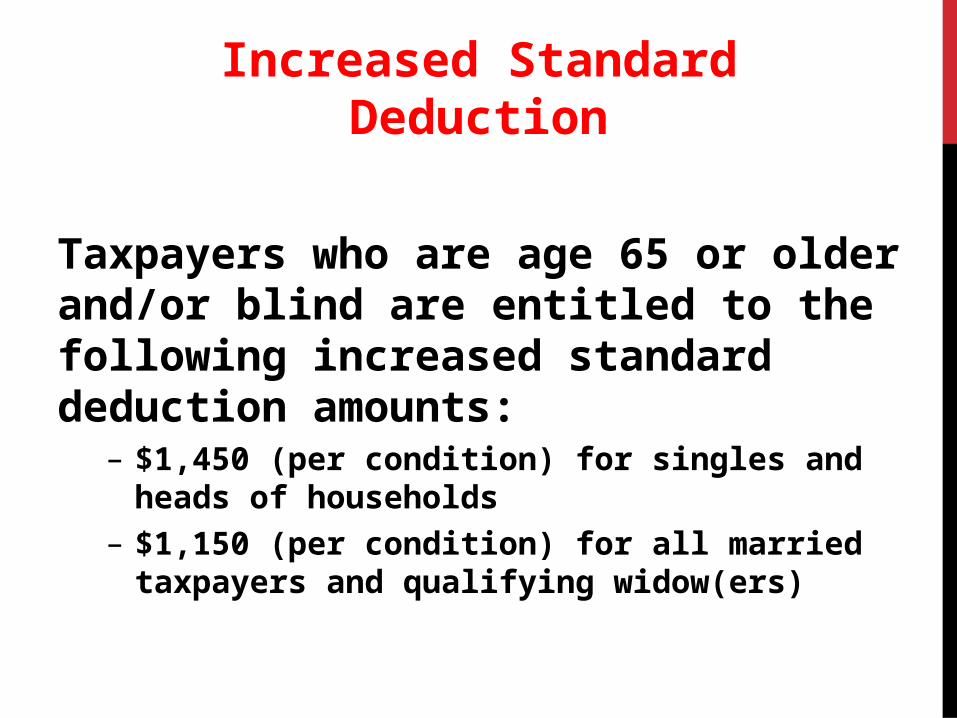

Increased Standard Deduction

Taxpayers who are age 65 or older and/or blind are entitled to the following increased standard deduction amounts:

– $1,450 (per condition) for singles and heads of households

– $1,150 (per condition) for all married taxpayers and qualifying widow(ers)

WHAT’S NEW FOR 2011

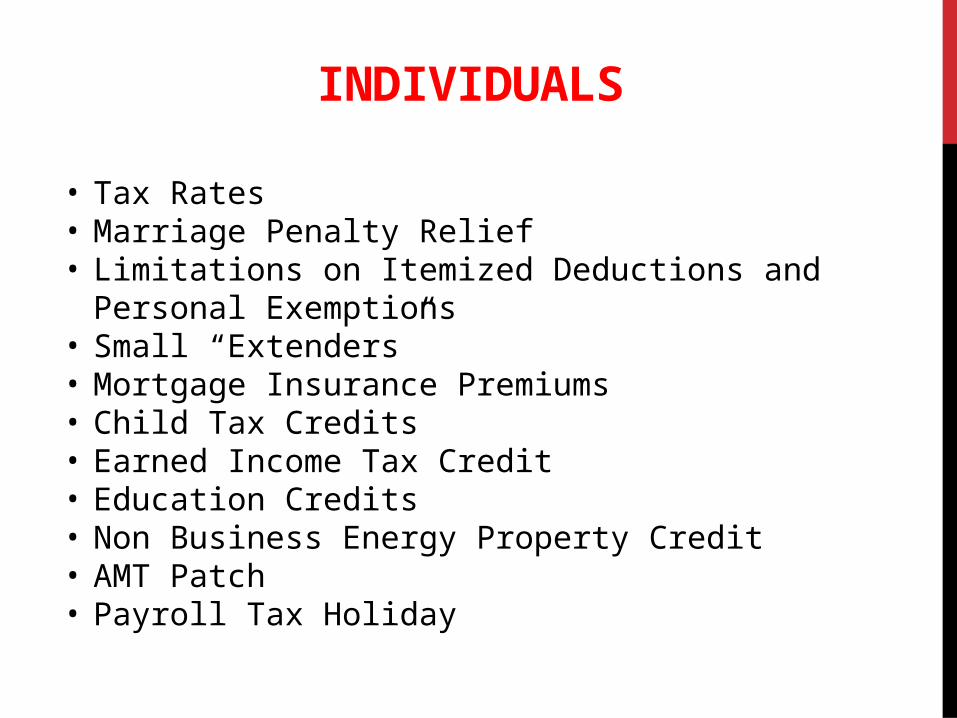

INDIVIDUALS

• Tax Rates• Marriage Penalty Relief• Limitations on Itemized Deductions and Personal

Exemptions• Small “Extenders”• Mortgage Insurance Premiums• Child Tax Credits• Earned Income Tax Credit• Education Credits• Non Business Energy Property Credit• AMT Patch• Payroll Tax Holiday

2011 TAX RATES

2011 Federal Tax Rate Single MFJ

Standard Deduction $5,800 $11,600

10% $8,500 $17,000

15% $34,500 $69,000

25% $83,600 $139,350

28% $174,400 $212,300

33% $379,150 $379,150

35% $379,151+ $379,151+

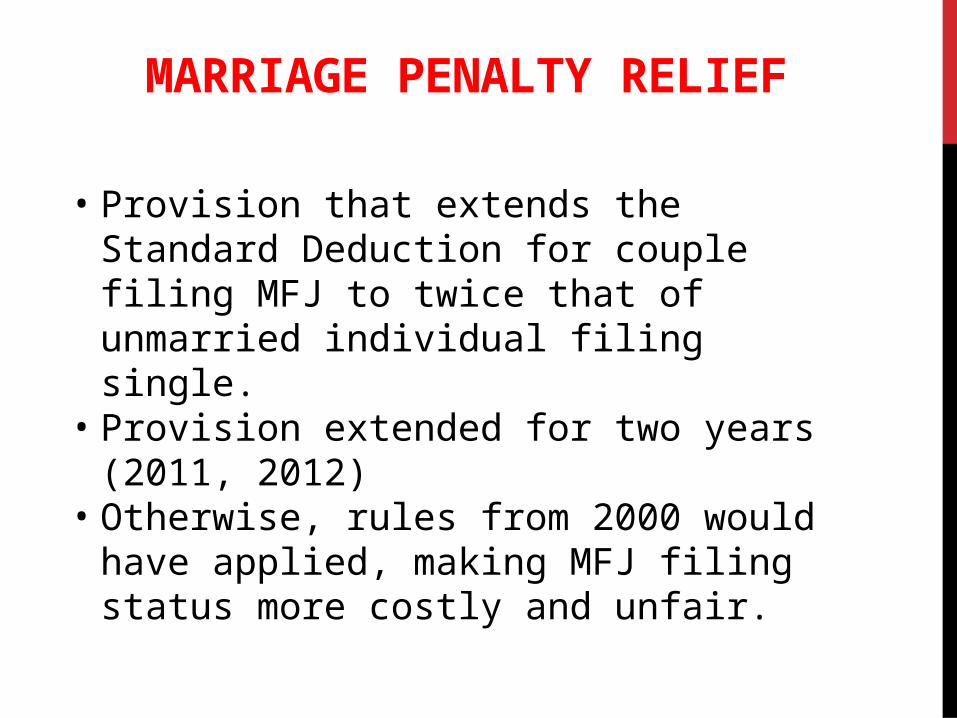

MARRIAGE PENALTY RELIEF

• Provision that extends the Standard Deduction for couple filing MFJ to twice that of unmarried individual filing single.

• Provision extended for two years (2011, 2012)

• Otherwise, rules from 2000 would have applied, making MFJ filing status more costly and unfair.

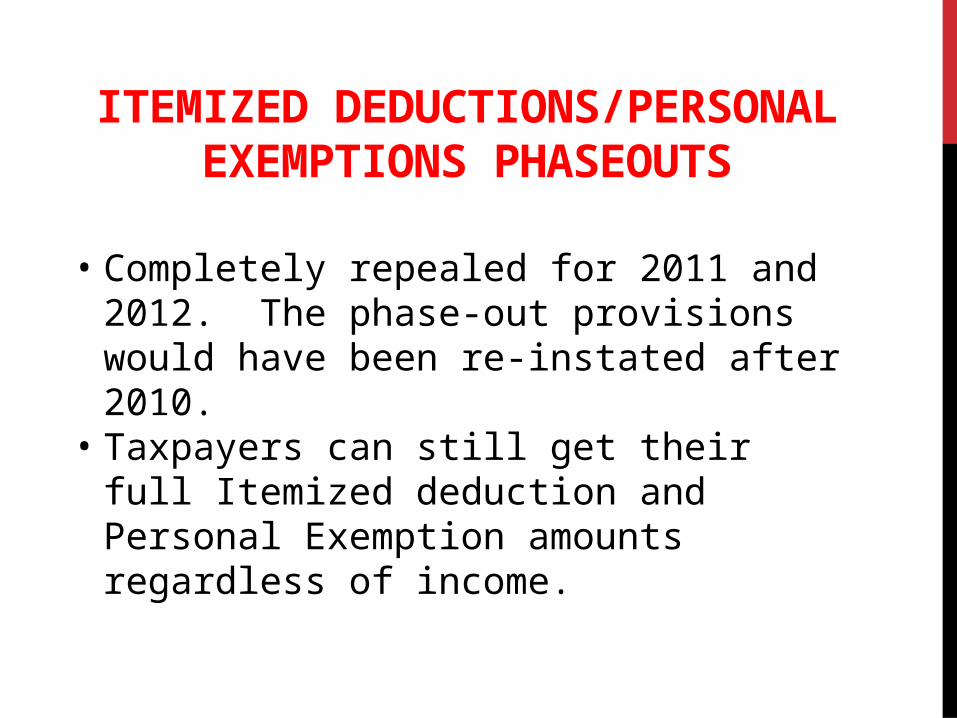

ITEMIZED DEDUCTIONS/PERSONAL EXEMPTIONS PHASEOUTS

• Completely repealed for 2011 and 2012. The phase-out provisions would have been re-instated after 2010.

• Taxpayers can still get their full Itemized deduction and Personal Exemption amounts regardless of income.

SMALL “EXTENSIONS”

• Tuition and Fees Deduction• Educator Expense Deduction• State and Local Sales Tax Deduction• Qualified Charitable Distributions from IRAs

Extended for 2010 and 2011

MORTGAGE INSURANCE PREMIUMS

• Mortgage Insurance Premiums paid by Taxpayer on a qualified mortgage may be deducted as mortgage interest on Sch. A, subject to phase-out based on Taxpayer’s AGI.

Extended for 2010 and 2011

CHILD TAX CREDIT

• Maximum CTC for each qualified child will remain at $1,000.

• Provision allowing refundability of the credit for earned income over $3,000 has also been extended.

• Phase out of CTC begins at $110,000 (MFJ) $75,000 (Single, HOH) $55,000 (MFS)

Extended for 2011, 2012

EARNED INCOME TAX CREDIT

Same criteria as 2010 were extended for 2011, 2012

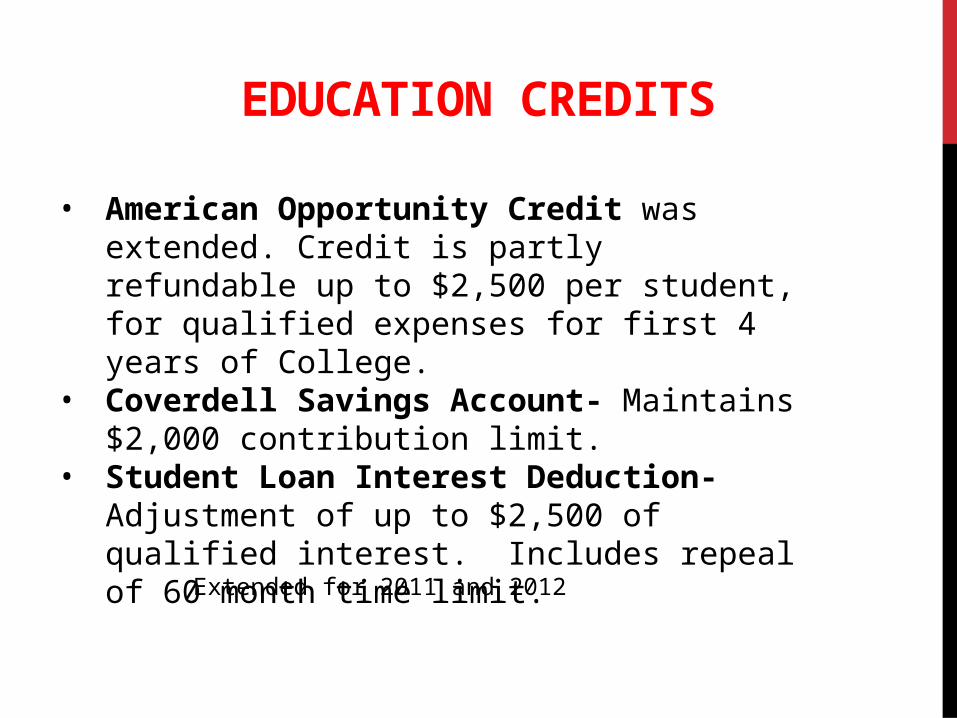

EDUCATION CREDITS

• American Opportunity Credit was extended. Credit is partly refundable up to $2,500 per student, for qualified expenses for first 4 years of College.

• Coverdell Savings Account- Maintains $2,000 contribution limit.

• Student Loan Interest Deduction- Adjustment of up to $2,500 of qualified interest. Includes repeal of 60 month time limit.

Extended for 2011 and 2012

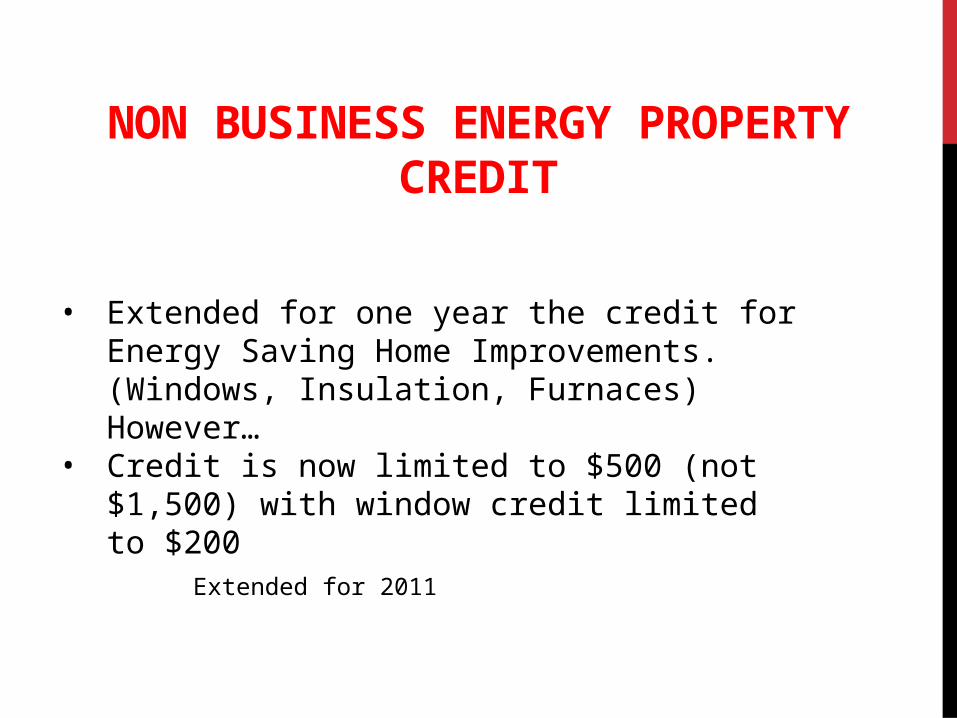

NON BUSINESS ENERGY PROPERTY CREDIT

• Extended for one year the credit for Energy Saving Home Improvements. (Windows, Insulation, Furnaces) However…

• Credit is now limited to $500 (not $1,500) with window credit limited to $200

Extended for 2011

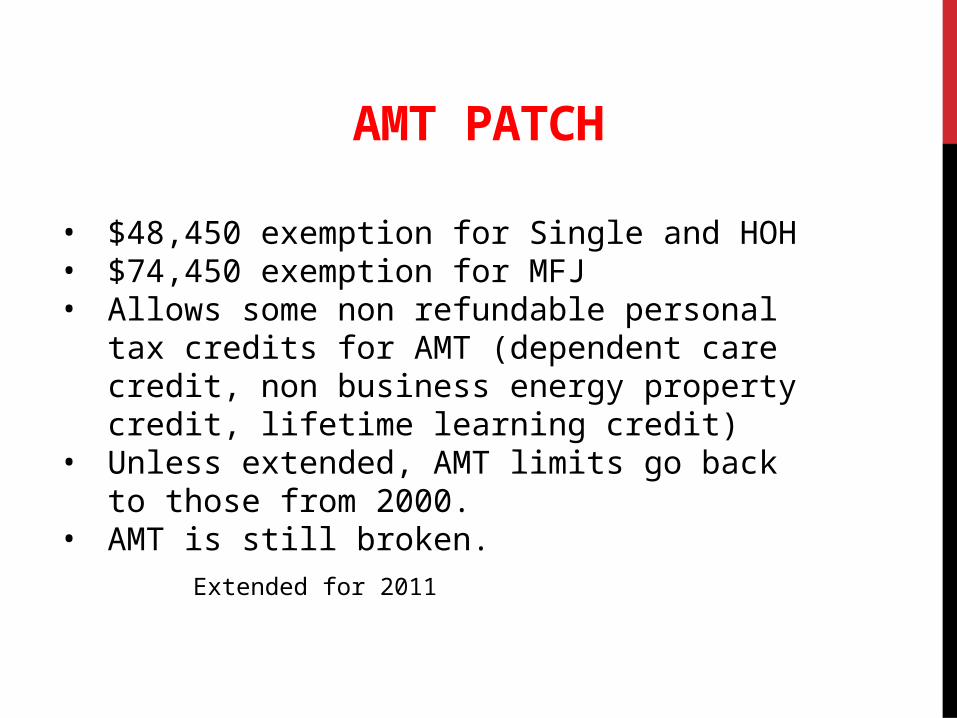

AMT PATCH

• $48,450 exemption for Single and HOH• $74,450 exemption for MFJ• Allows some non refundable personal tax credits

for AMT (dependent care credit, non business energy property credit, lifetime learning credit)

• Unless extended, AMT limits go back to those from 2000.

• AMT is still broken.

Extended for 2011

PAYROLL TAX HOLIDAY

• Reduction in the “Employee Only” portion of Social Security Tax.

• Reduced from 6.2% to 4.2% on first $106,800 of income.

• SE tax reduced from 12.4% to 10.4%.• Maximum reduction is $2,136.

Effective for 2011 only

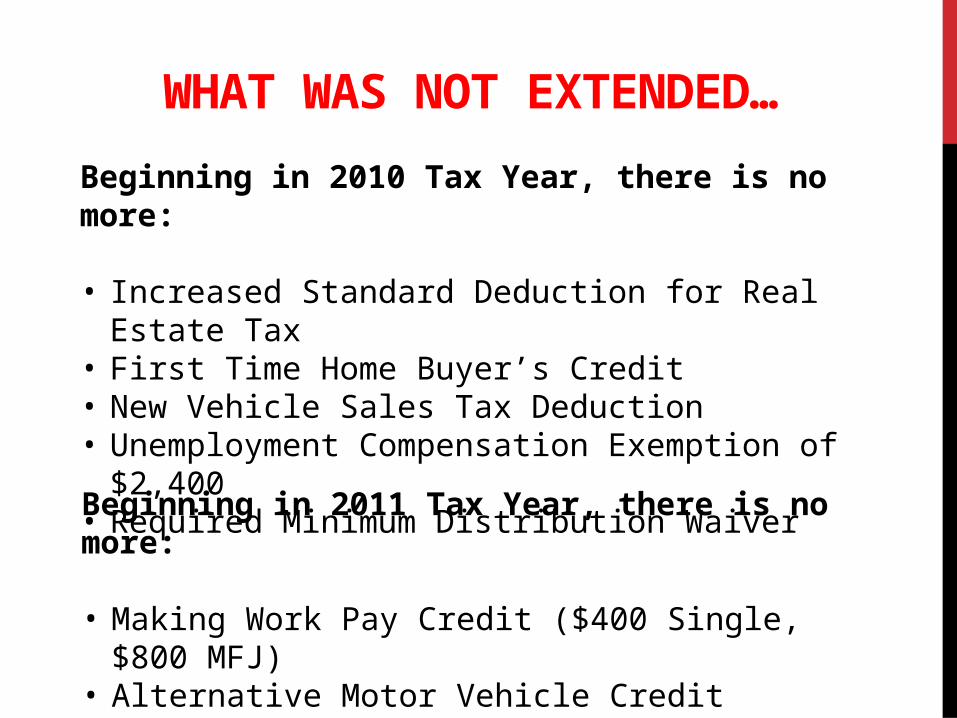

WHAT WAS NOT EXTENDED…

Beginning in 2010 Tax Year, there is no more:

• Increased Standard Deduction for Real Estate Tax• First Time Home Buyer’s Credit• New Vehicle Sales Tax Deduction• Unemployment Compensation Exemption of $2,400• Required Minimum Distribution Waiver

Beginning in 2011 Tax Year, there is no more:

• Making Work Pay Credit ($400 Single, $800 MFJ)• Alternative Motor Vehicle Credit