Embed Size (px)

Citation preview

Time-value calculations using Excel

(Note: I don’t use “Numbers” for Mac – so I encourage you to get Excel for Mac)

Module 2.1

Copyright © 2013 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

4-2

Overview There are a lot of “black box” tools for

solving time-value problems on the internet. You can also use a financial calculator to

handle many basic types of calculations Building your own spreadsheets, gives you:

the ability to handle virtually any time-value problem

the flexibility to structure problems as best fits your needs

4-3

Excel shortcuts Excel has many financial functions just like

your calculator and the text seems to encourage the use of these shortcuts: FV, PV, NPV, IRR, etc..

Instead, I encourage you to enter formulas directly: gives you more direct control over calculations improves the learning experience

4-4

The embedded spreadsheets The spreadsheets embedded in this

powerpoint presentation will be accessible to you two ways. First, you can download the file containing all the

spreadsheets directly to your computer Second, you can click on the embedded

spreadsheet – and that should bring up a working excel spreadsheet on your computer

4-5

We will build spreadsheets for: 1. Simple PV and FV problems

Including a little graphing Working with “goal seek”

2. The calculation of EARs given various compounding periods

3. PV and FV of annuities 4. PV and FV of growing annuities 5. PV of perpetuities

4-6

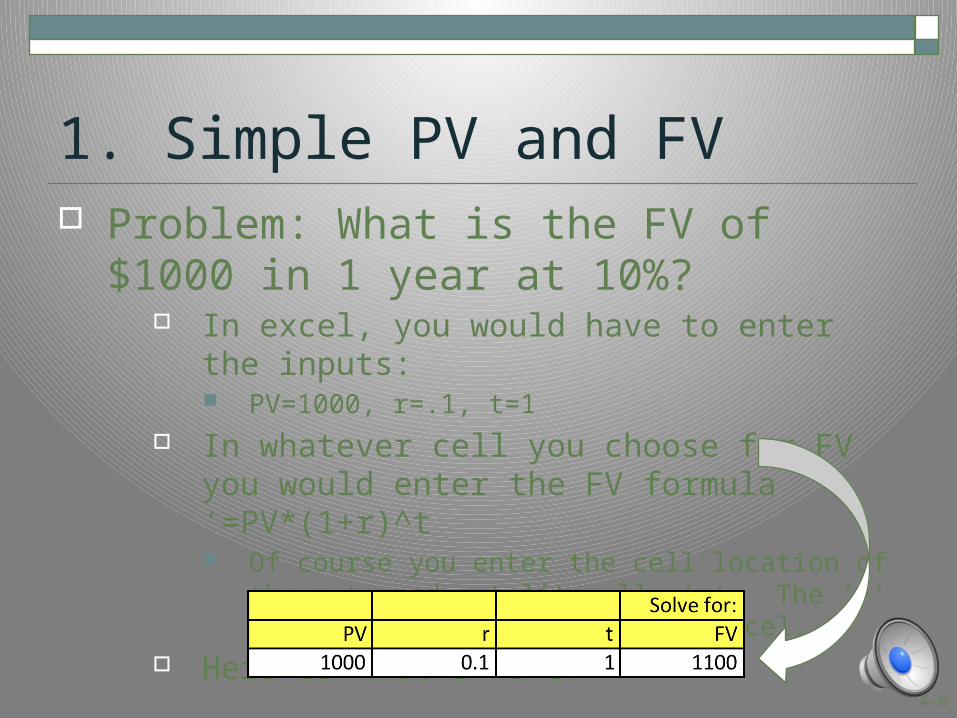

1. Simple PV and FV Problem: What is the FV of $1000 in 1 year at

10%? In excel, you would have to enter the inputs:

PV=1000, r=.1, t=1 In whatever cell you choose for FV you would enter

the FV formula ‘=PV*(1+r)^t Of course you enter the cell location of the rate and not

literally ‘r’. The ‘^’ is the exponent indicator in Excel. Here is what I have:

4-7

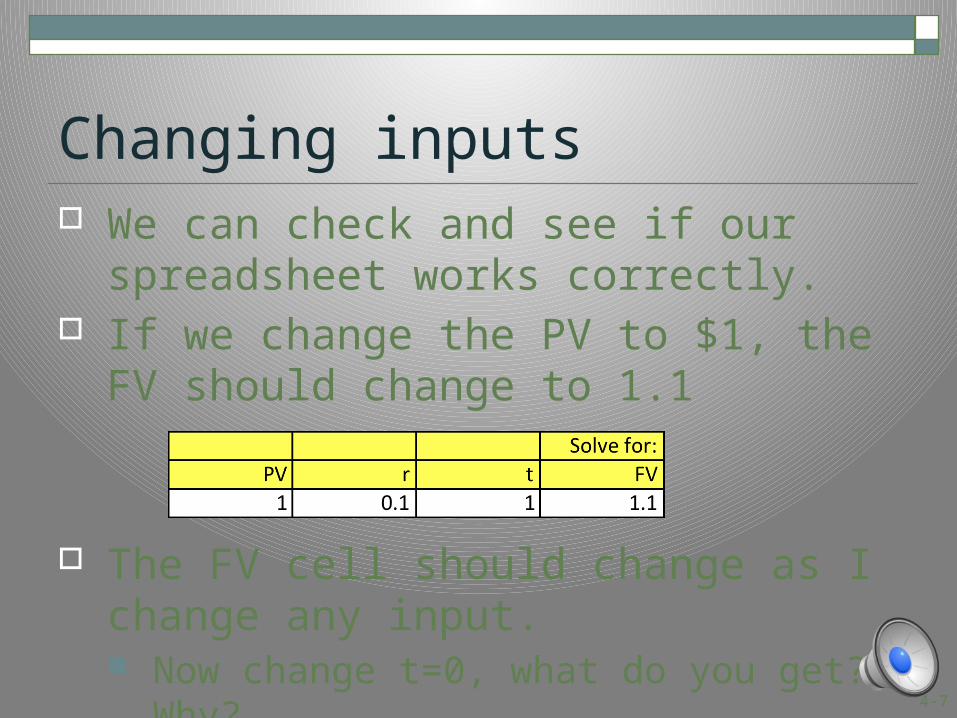

Changing inputs We can check and see if our spreadsheet

works correctly. If we change the PV to $1, the FV should

change to 1.1

The FV cell should change as I change any input. Now change t=0, what do you get? Why?

4-8

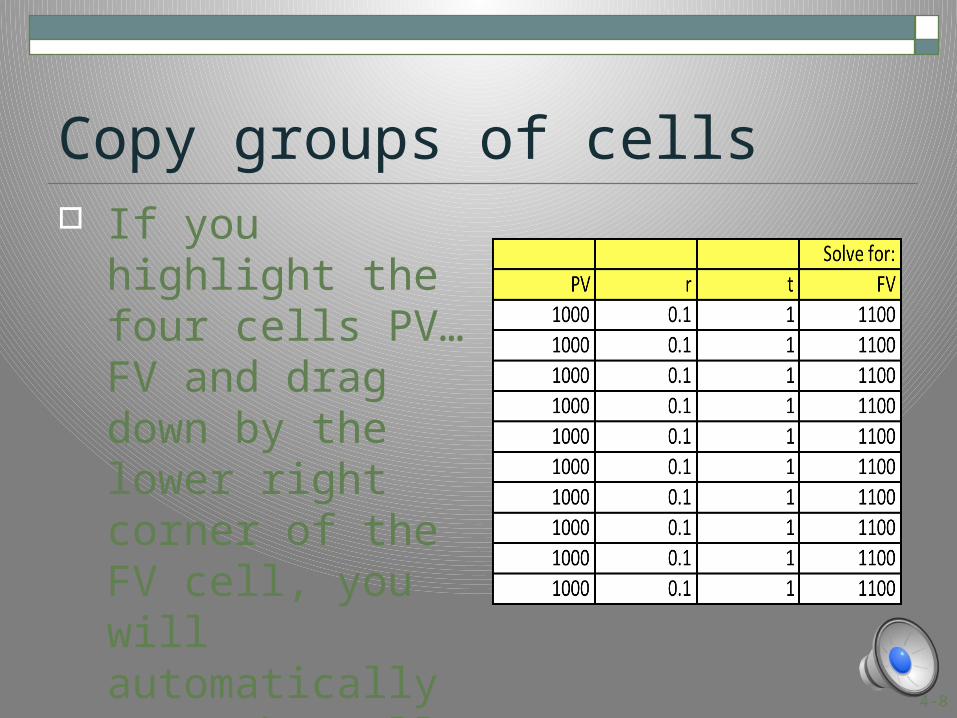

Copy groups of cells If you highlight the

four cells PV…FV and drag down by the lower right corner of the FV cell, you will automatically copy the cells down the page.

4-9

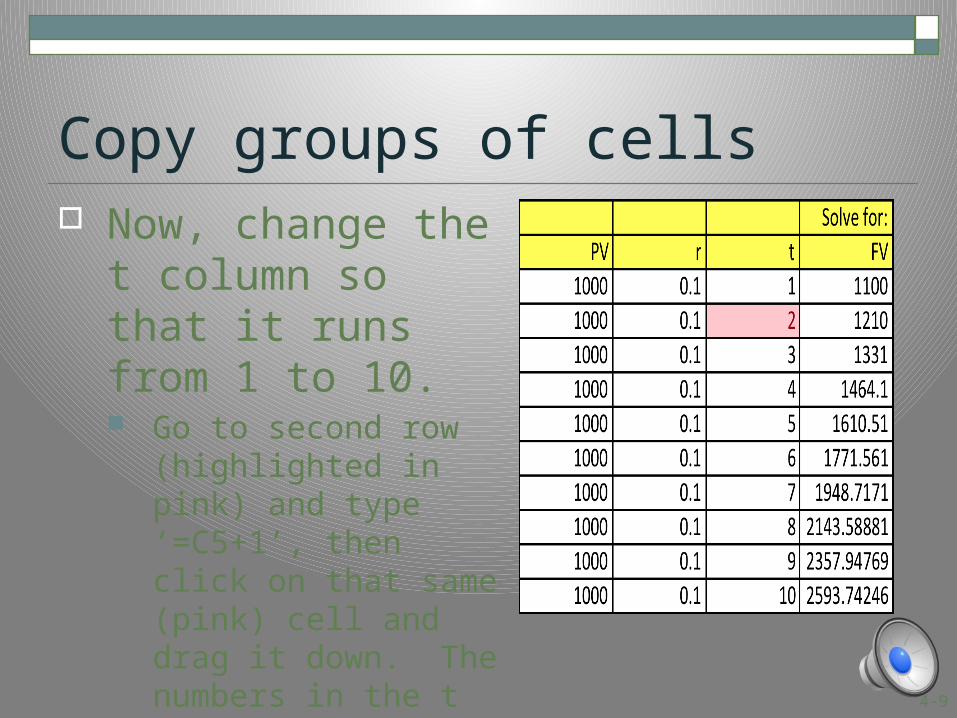

Copy groups of cells Now, change the t

column so that it runs from 1 to 10. Go to second row

(highlighted in pink) and type ‘=C5+1’, then click on that same (pink) cell and drag it down. The numbers in the t column should grow by 1 as you copy that cell.

4-10

What does this spreadsheet show? The FV column shows

how a single $1000 deposit today would grow at a rate of 10% over 10 years. That is, after 10 years this single deposit would be worth $2593.74

4-11

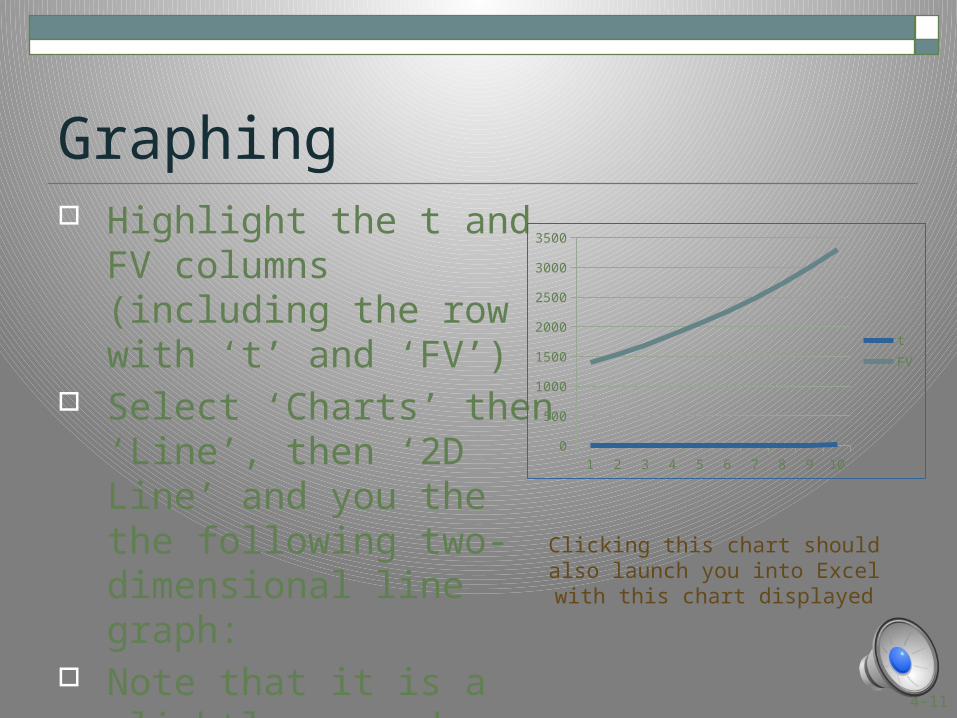

Graphing Highlight the t and FV

columns (including the row with ‘t’ and ‘FV’)

Select ‘Charts’ then ‘Line’, then ‘2D Line’ and you the the following two-dimensional line graph:

Note that it is a slightly curved line. Why?

1 2 3 4 5 6 7 8 9 100

500

1000

1500

2000

2500

3000

3500

t

FV

Clicking this chart should also launch you into Excel with this chart displayed

4-12

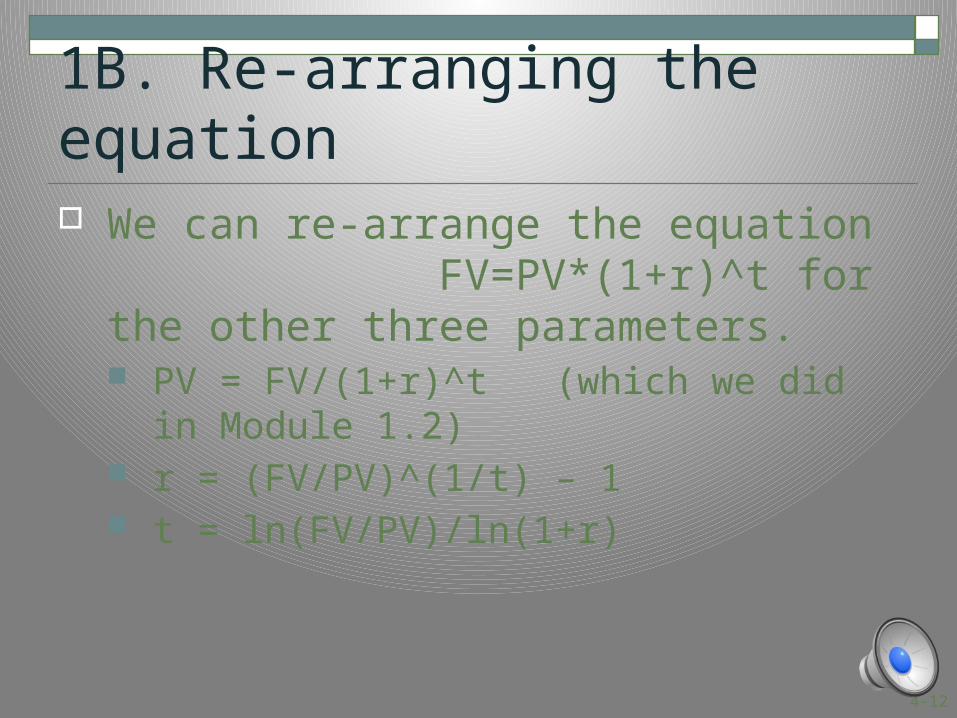

1B. Re-arranging the equation We can re-arrange the equation

FV=PV*(1+r)^t for the other three parameters. PV = FV/(1+r)^t (which we did in Module 1.2) r = (FV/PV)^(1/t) – 1 t = ln(FV/PV)/ln(1+r)

4-13

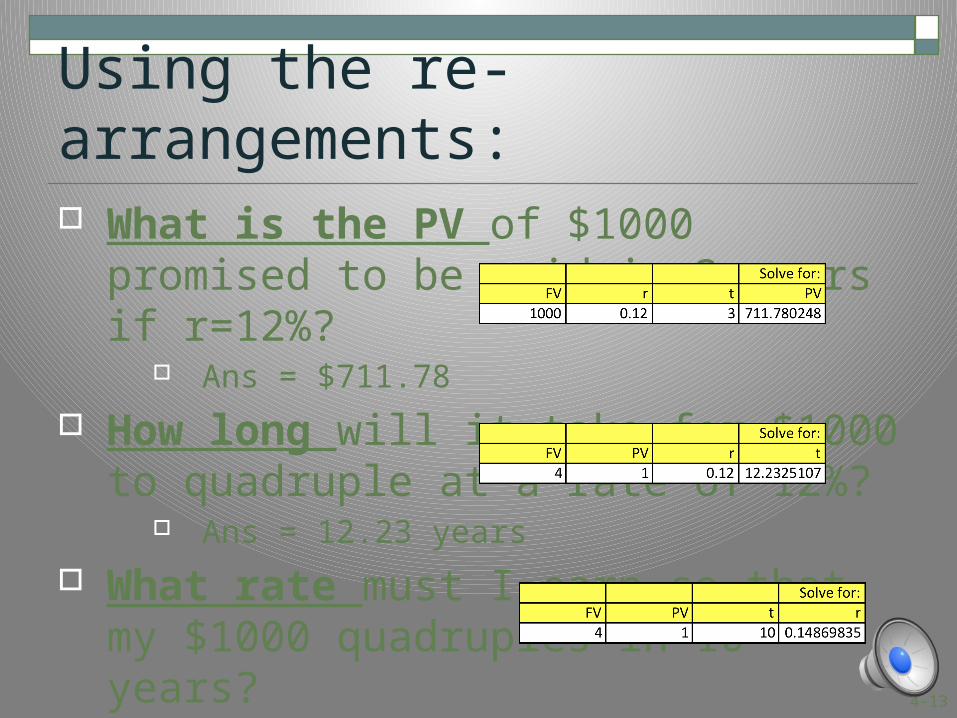

Using the re-arrangements: What is the PV of $1000 promised to be paid

in 3 years if r=12%? Ans = $711.78

How long will it take for $1000 to quadruple at a rate of 12%?

Ans = 12.23 years

What rate must I earn so that my $1000 quadruples in 10 years?

Ans = 14.87%

4-14

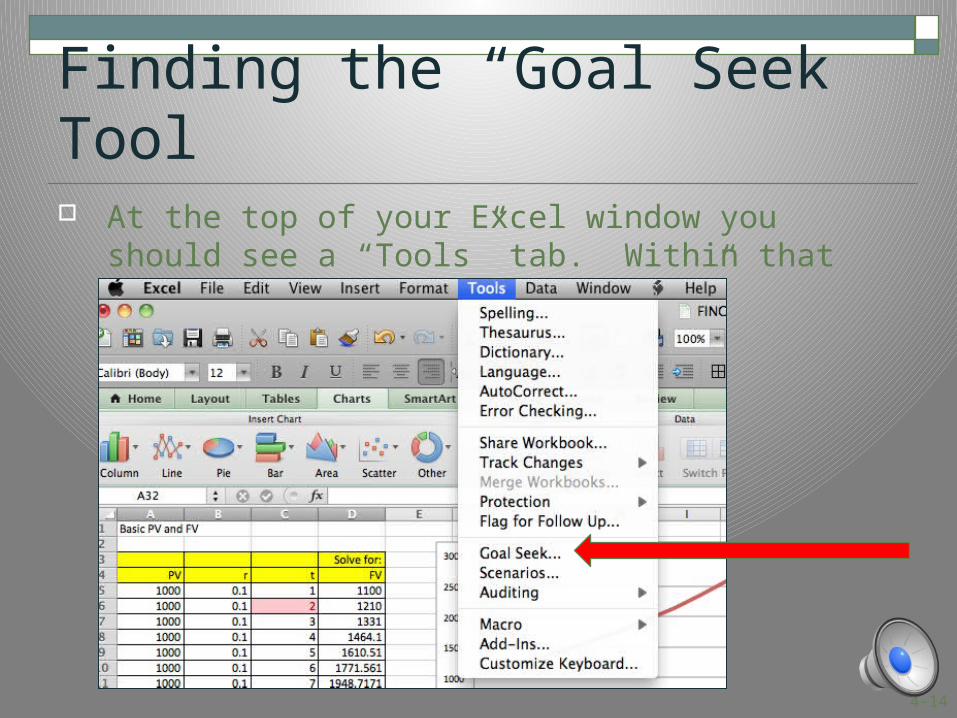

Finding the “Goal Seek” Tool At the top of your Excel window you should see a “Tools”

tab. Within that tab you should see a “Goal Seek” launcher:

4-15

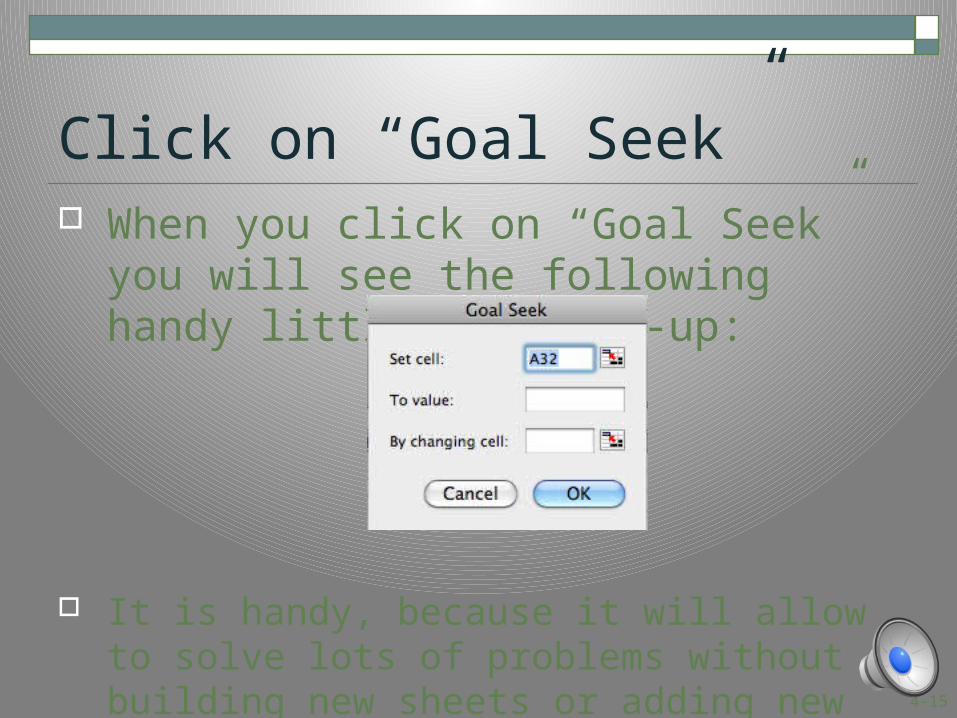

Click on “Goal Seek” When you click on “Goal Seek” you will see

the following handy little tool pop-up:

It is handy, because it will allow to solve lots of problems without building new sheets or adding new formulas (if that is how we wish to proceed)

4-16

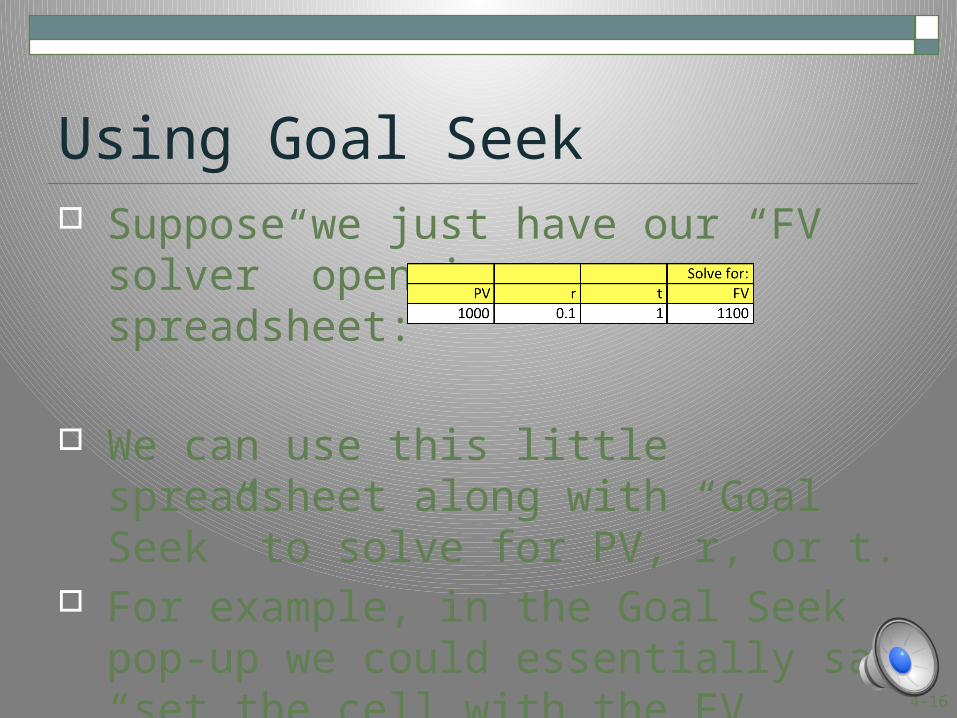

Using Goal Seek Suppose we just have our “FV solver” open in

our spreadsheet:

We can use this little spreadsheet along with “Goal Seek” to solve for PV, r, or t.

For example, in the Goal Seek pop-up we could essentially say “set the cell with the FV formula = to $1400, by changing the time cell. When you click OK – it finds the solution

4-17

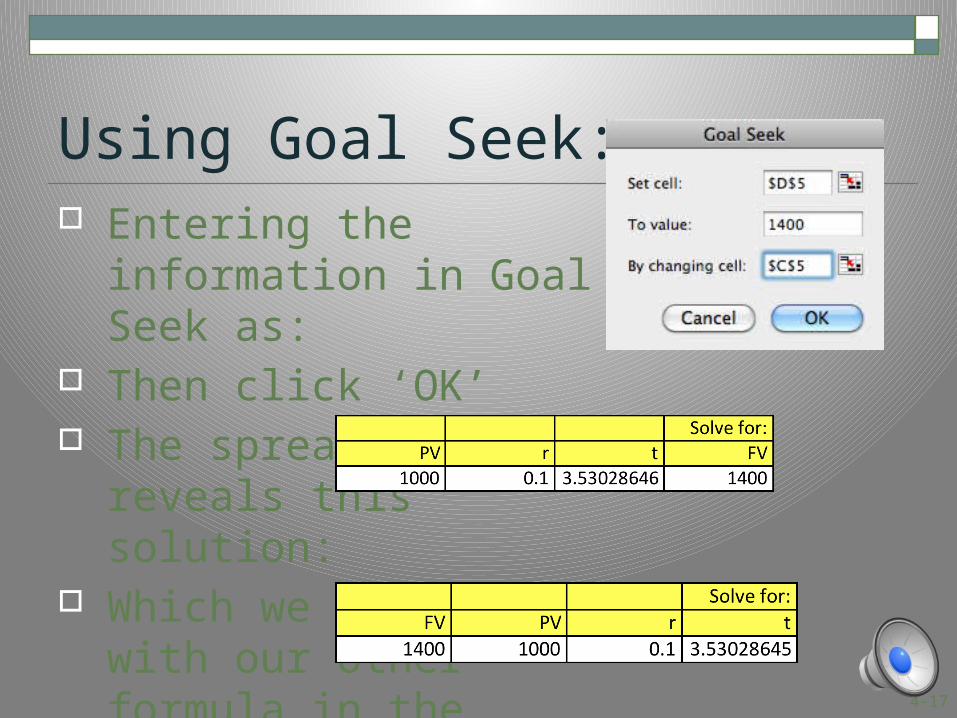

Using Goal Seek: Entering the information in

Goal Seek as: Then click ‘OK’ The spreadsheet reveals this

solution: Which we can verify with

our other formula in the sheet:

4-18

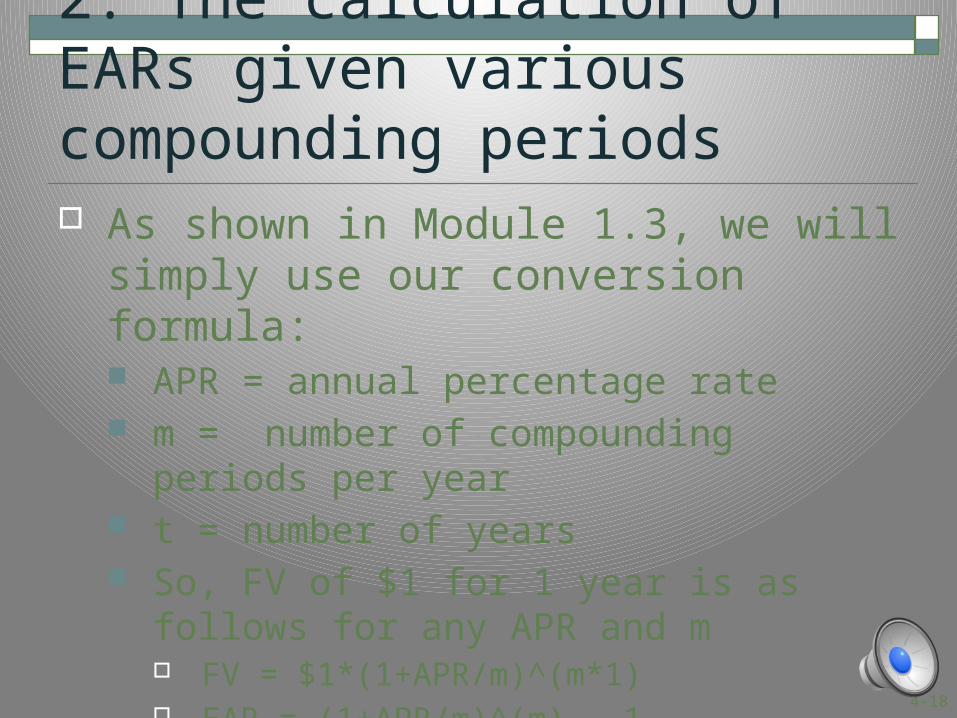

2. The calculation of EARs given various compounding periods As shown in Module 1.3, we will simply use

our conversion formula: APR = annual percentage rate m = number of compounding periods per year t = number of years So, FV of $1 for 1 year is as follows for any APR

and m FV = $1*(1+APR/m)^(m*1) EAR = (1+APR/m)^(m) – 1

4-19

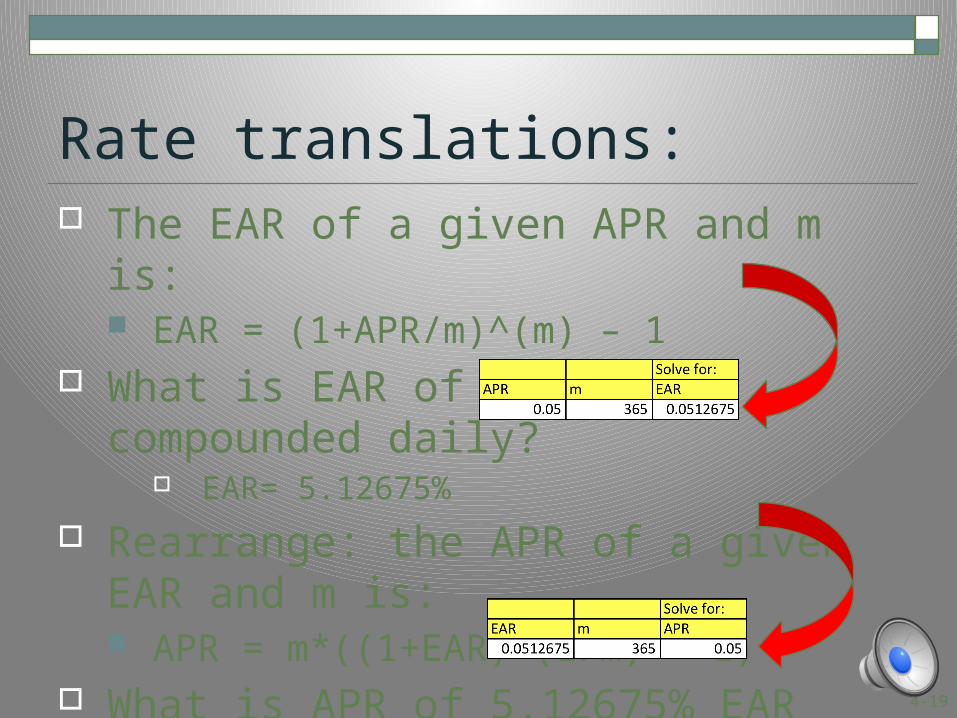

Rate translations: The EAR of a given APR and m is:

EAR = (1+APR/m)^(m) – 1 What is EAR of 5% APR compounded daily?

EAR= 5.12675%

Rearrange: the APR of a given EAR and m is: APR = m*((1+EAR)^(1/m) – 1)

What is APR of 5.12675% EAR with m=365? APR= 5%

4-20

Rate translations So, in the previous example, if we are holding

the asset for 1 year, we would be indifferent between paying/earning 5% APR compounded daily, OR 5.12675% APR compounded annually

4-21

Intermission! Next, we will now build spreadsheets for the

PV of annuities. I will not re-arrange the equation for

parameters, but will show using “Goal Seek” how we can address interesting questions about the parameters.

4-22

2. Annuities Recall PV of an annuity with constant

payment $C at rate r over t periods of time.

PVannuity = C/r*(1-1/(1+r)^t)

FVannuity = PVannuity*(1+r)^t

Let’s put these into our spreadsheet

4-23

Solving PV of annuity What is the PV of a $500 monthly payment,

received for 5 years, starting one-month from today, if r=8% APR compounded monthly? Ans = $24,659.22 Parameters needed to solve: $C, r, and t

$C = 500, r =.08/12, and t =12*5 Note that r and t MUST be in same time-units

In this case both must be stated in units of months.

4-24

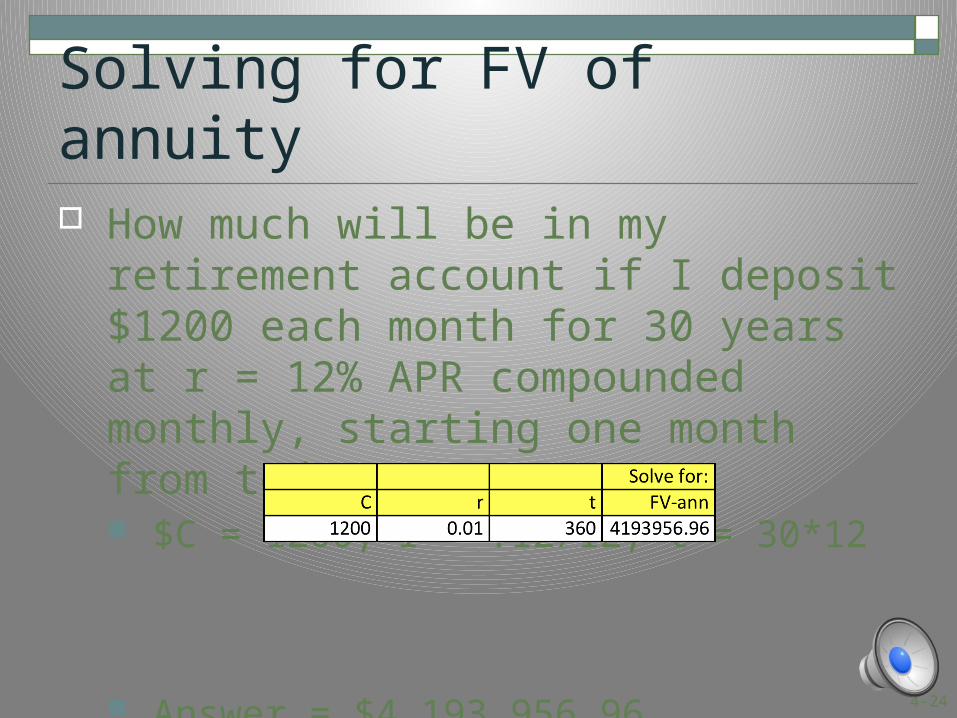

Solving for FV of annuity How much will be in my retirement account if

I deposit $1200 each month for 30 years at r = 12% APR compounded monthly, starting one month from today? $C = 1200, r = .12/12, t = 30*12

Answer = $4,193,956.96

4-25

Using “Goal Seek” – common question type 1 How much do I need to save each month over

30 years, at 12% APR compounded monthly, in order to have $6,000,000 in 30 years? Will ask Goal Seek to set FV value to 6000000

while changing the “C” cell. Answer = $1,716.75/month

4-26

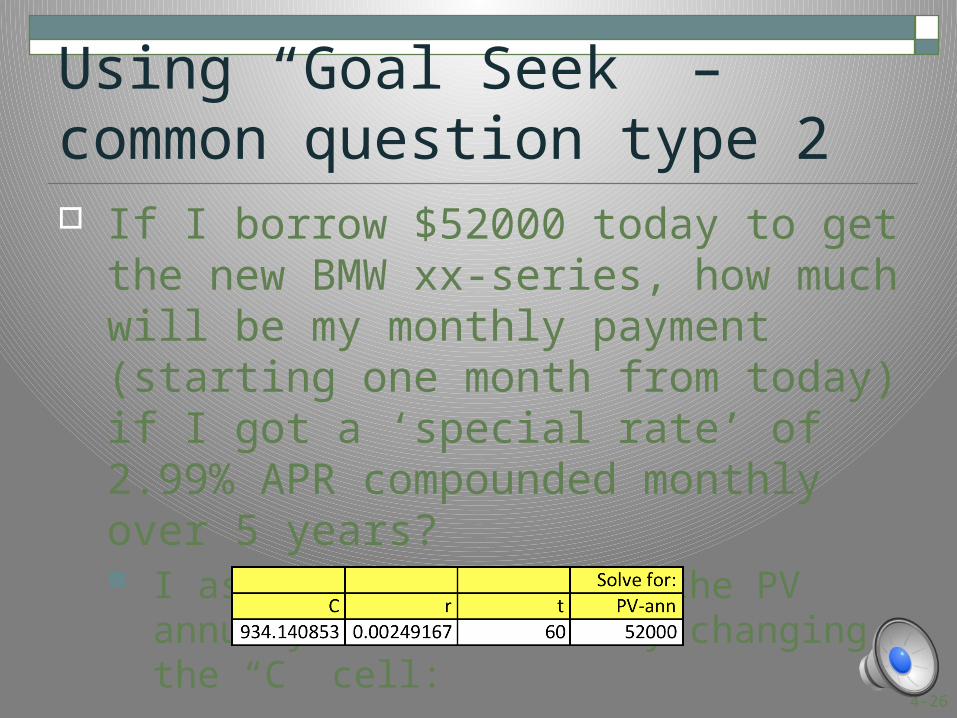

Using “Goal Seek” – common question type 2 If I borrow $52000 today to get the new

BMW xx-series, how much will be my monthly payment (starting one month from today) if I got a ‘special rate’ of 2.99% APR compounded monthly over 5 years? I ask Goal Seek to set the PV annuity cell =

52000 by changing the “C” cell:

4-27

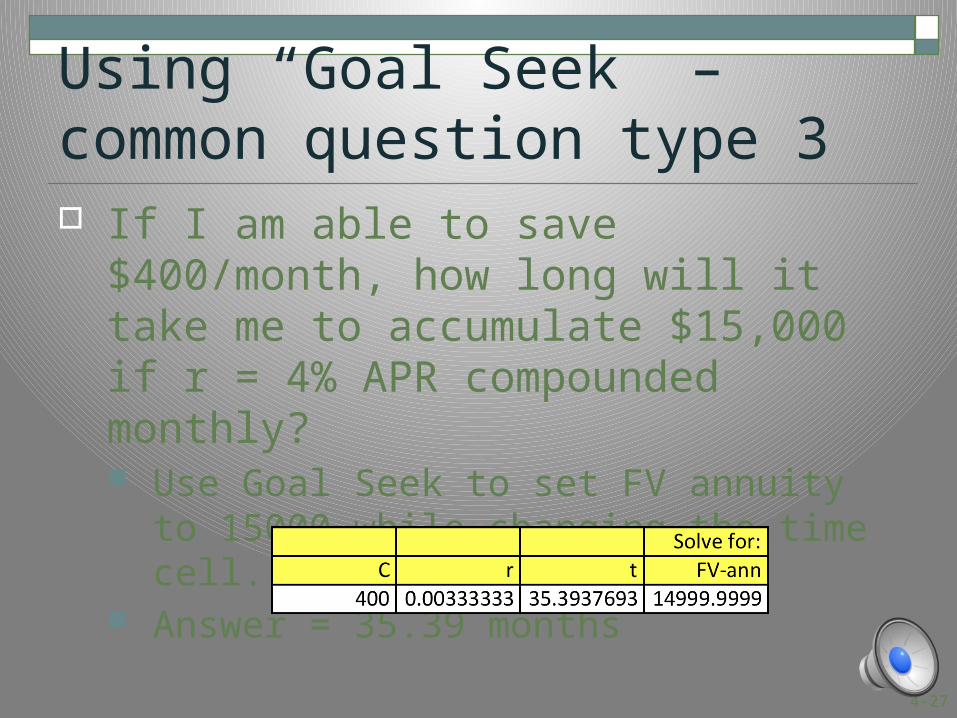

Using “Goal Seek” – common question type 3 If I am able to save $400/month, how long

will it take me to accumulate $15,000 if r = 4% APR compounded monthly? Use Goal Seek to set FV annuity to 15000 while

changing the time cell. Answer = 35.39 months

4-28

4. Growing annuities Recall: PVgr-ann = C/(r-g)*(1-((1+g)/(1+r))^t) FVgr-ann = PVgr-ann *(1+r)^t

We will put these into the spreadsheet while answering some common questions

4-29

PV growing annuity A note will pay you $10,000 next year, with

the payment growing at a rate of 4% per year for 20 years. If you require a return of 12% on such investments, what price would you be willing to pay for this note. Answer = $96,606.67

4-30

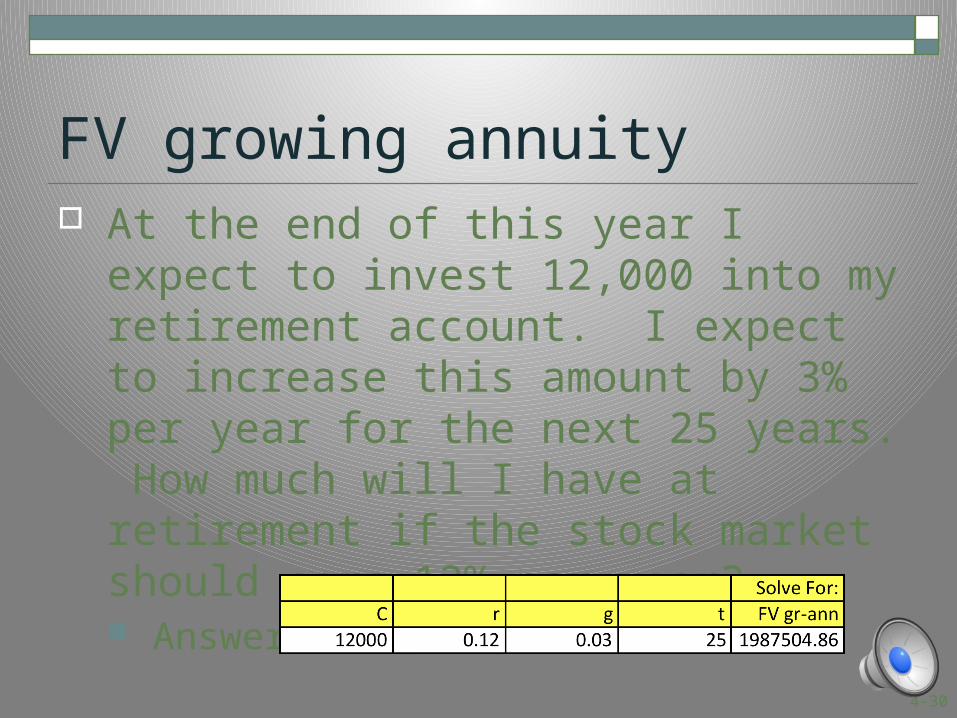

FV growing annuity At the end of this year I expect to invest

12,000 into my retirement account. I expect to increase this amount by 3% per year for the next 25 years. How much will I have at retirement if the stock market should earn 12% per year? Answer = $1,987,504.86

4-31

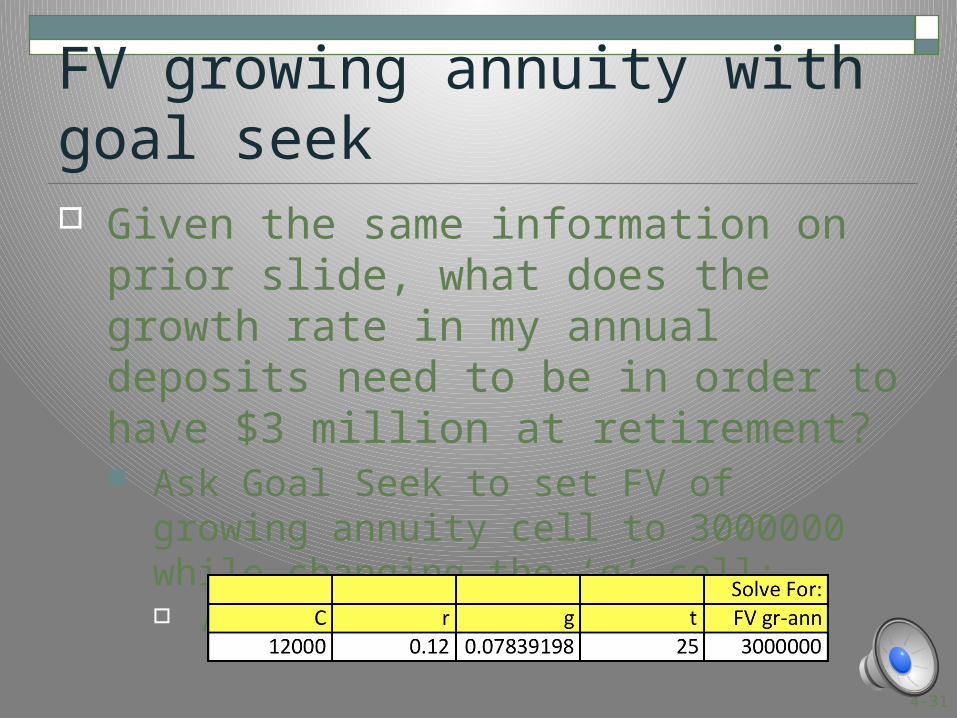

FV growing annuity with goal seek Given the same information on prior slide,

what does the growth rate in my annual deposits need to be in order to have $3 million at retirement? Ask Goal Seek to set FV of growing annuity cell

to 3000000 while changing the ‘g’ cell: Answer = 7.84% per year

4-32

Perpetuities We end with the simplest. Recall, that PV of perpetuity $C is: PV = C/(r-g)

If it is a constant perpetuity, just set g=0. Recall, like the annuities, these formulas assume

first payment is one-period from today.

4-33

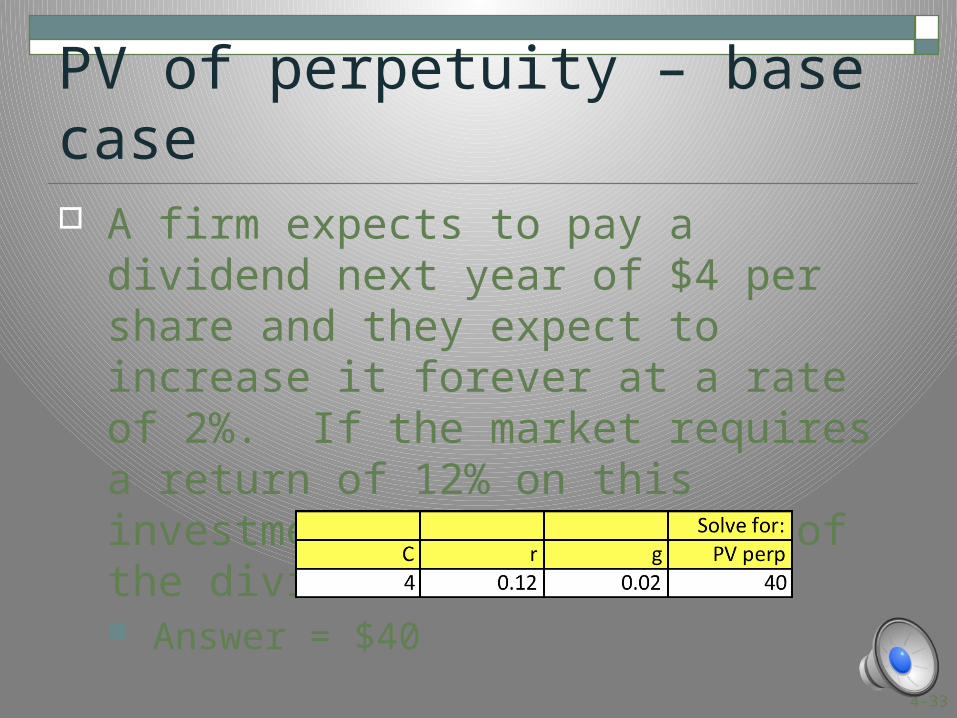

PV of perpetuity – base case A firm expects to pay a dividend next year of

$4 per share and they expect to increase it forever at a rate of 2%. If the market requires a return of 12% on this investment, what is the PV of the dividend stream? Answer = $40

4-34

PV Perpetuity – delayed case A firm expects to pay a dividend of $4 per

share starting 5 years from today, and they expect to increase it forever at a rate of 2%. If the market requires a return of 12% on this investment, what is the PV of the dividend stream?

Formula as given will find value at time=4, So we then have to discount the PV of that lump-sum

back another 4 years using our simple PV formula

4-35

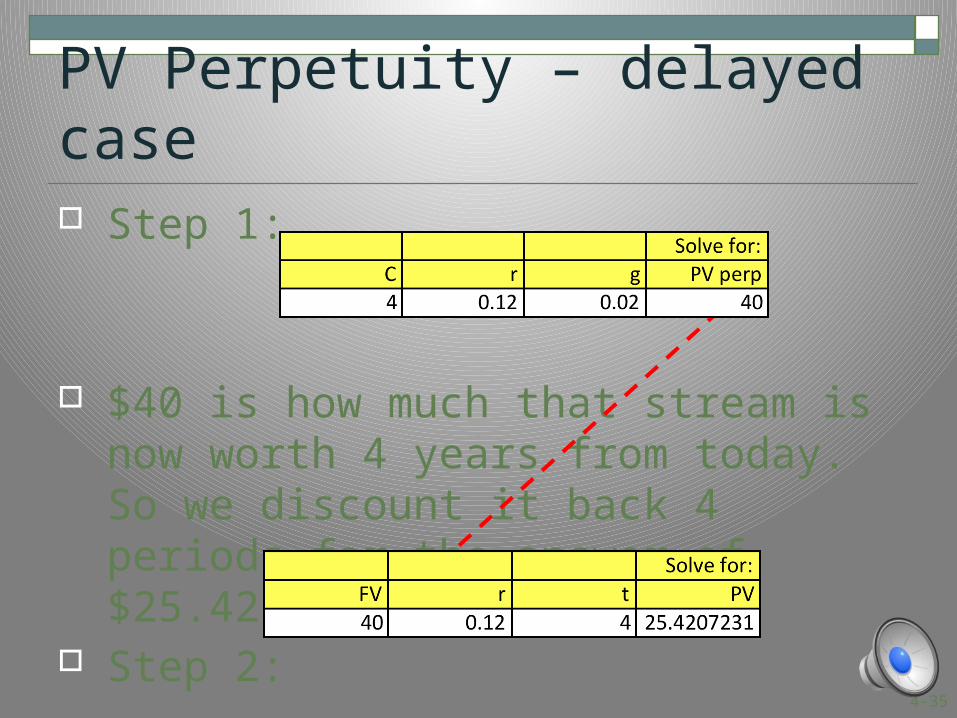

PV Perpetuity – delayed case Step 1:

$40 is how much that stream is now worth 4 years from today. So we discount it back 4 periods for the answer of $25.42

Step 2: