Embed Size (px)

Citation preview

Karsten Müller

University of Warwick

THE STRUCTURE OF

CREDIT MARKETS

BoE, BHC, CEPR and CFM Workshop on Finance, Investment,

and Productivity, 15/16 December 2016

2

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

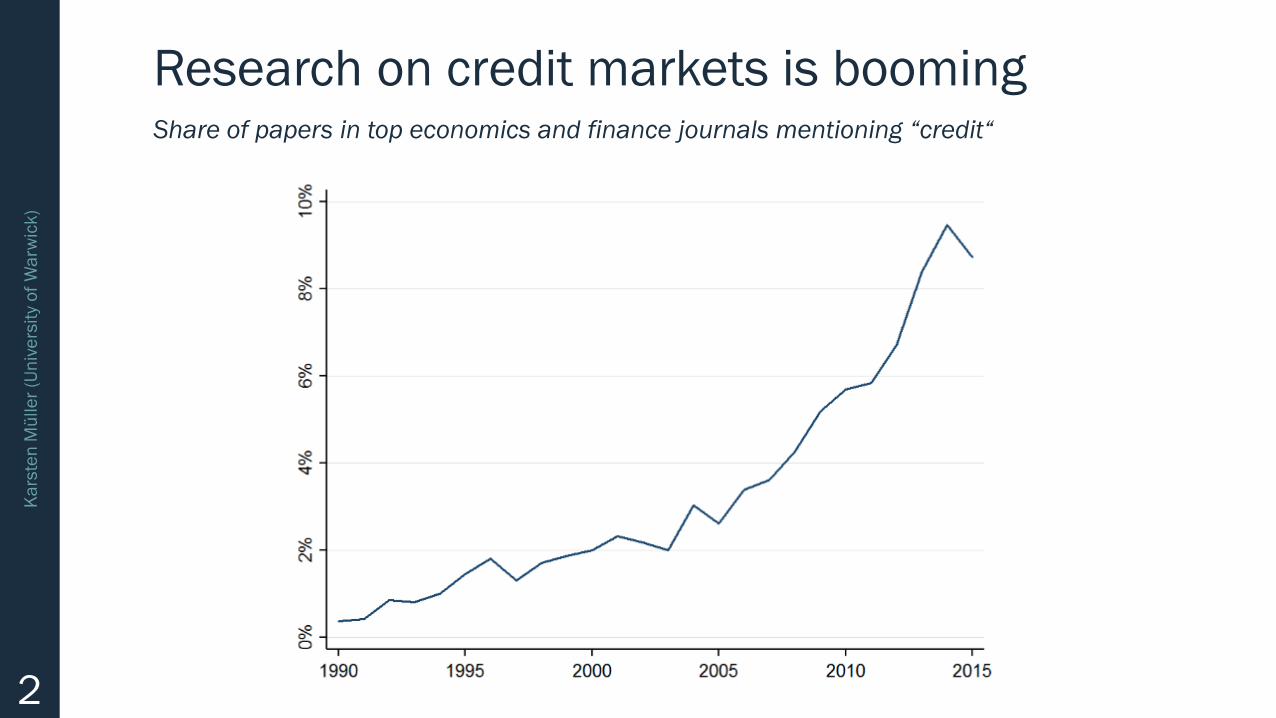

Research on credit markets is boomingShare of papers in top economics and finance journals mentioning “credit“

3

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

New and old questions

■ Pre-crisis view

– Access to finance is really, really good 1

■ Post-crisis view

– Is more finance always a good idea? 2

– What does the financial sector actually do? 3

– Is there enough financing for productive investments? 4

– What should policy makers do?

What do we know about finance and the real economy?

1 e.g. Beck (2011); Levine (1997, 2005); Rajan and Zingales (1998)2 e.g. Cecchetti and Kharroubi (2012, 2014); Arcand et al. (2015); Mian and Sufi (2014); Verner, Mian, and Sufi (2016);

Schularick and Taylor (2012); Gourinchas and Obstfeld (2012); Hombert and Matray (2016)3 e.g. Kay (2016); Jordà et al. (2016); Claessens (2016)4 e.g. Bahaj et al. (2016); Zingales (2015); Turner (2016); Foroohar (2016)

4

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

Why we need more detailed data

“It’s not particularly helpful to analyse banking like salt in

cooking or water on your vegetable patch, and conclude

that “some is good, too much is bad”. Unlike salt and water,

banking services are complex and diverse. There’s a

difference between a mortgage, a payday loan, life

insurance, a credit derivative, a venture capital investment

and an equity tracker fund. They’re all financial services,

though.”

- Tim Harford

5

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

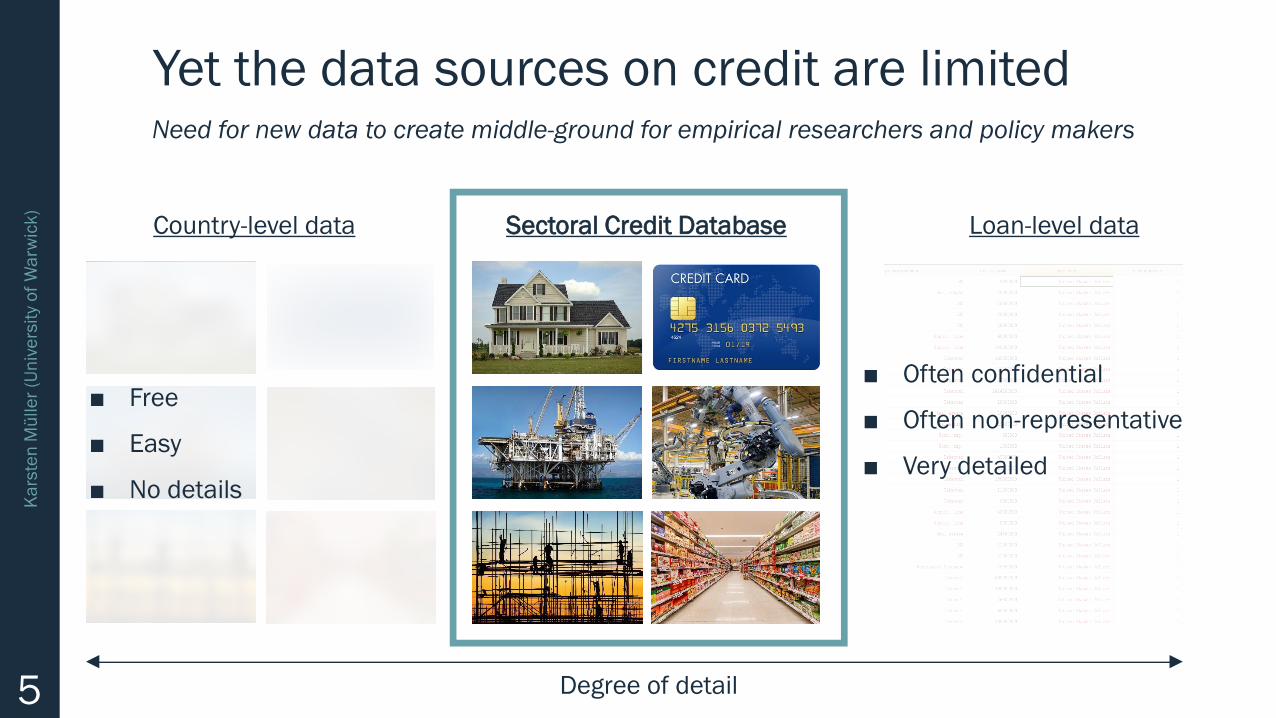

Yet the data sources on credit are limitedNeed for new data to create middle-ground for empirical researchers and policy makers

Country-level data Loan-level dataSectoral Credit Database

■ Often confidential

■ Often non-representative

■ Very detailed

Degree of detail

■ Free

■ Easy

■ No details

6

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

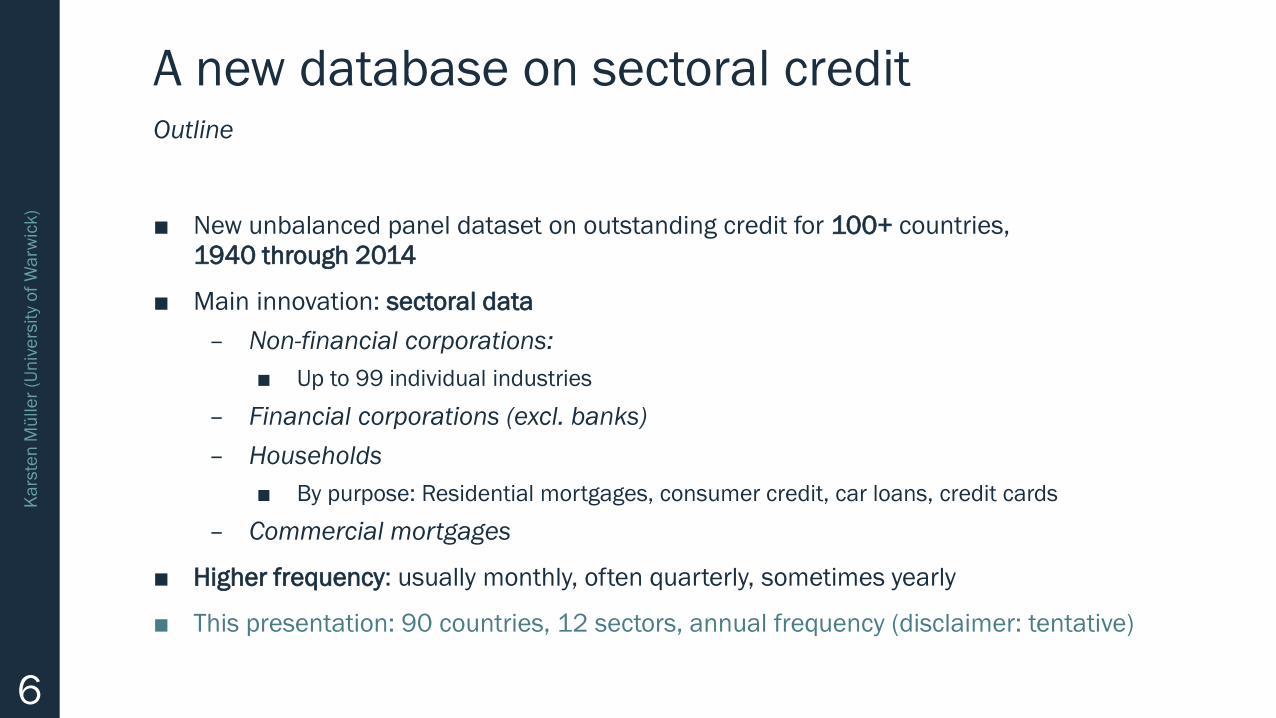

A new database on sectoral credit

■ New unbalanced panel dataset on outstanding credit for 100+ countries,

1940 through 2014

■ Main innovation: sectoral data

– Non-financial corporations:

■ Up to 99 individual industries

– Financial corporations (excl. banks)

– Households

■ By purpose: Residential mortgages, consumer credit, car loans, credit cards

– Commercial mortgages

■ Higher frequency: usually monthly, often quarterly, sometimes yearly

■ This presentation: 90 countries, 12 sectors, annual frequency (disclaimer: tentative)

Outline

7

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

A new database on sectoral credit

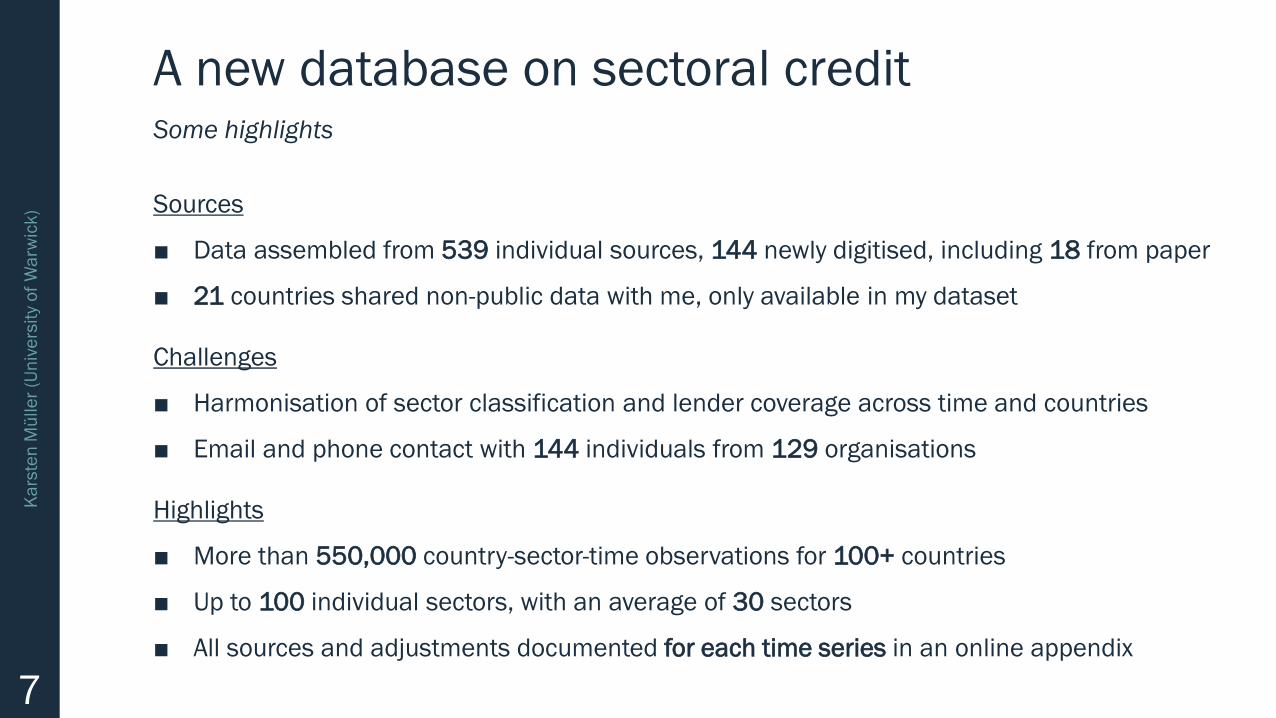

Sources

■ Data assembled from 539 individual sources, 144 newly digitised, including 18 from paper

■ 21 countries shared non-public data with me, only available in my dataset

Challenges

■ Harmonisation of sector classification and lender coverage across time and countries

■ Email and phone contact with 144 individuals from 129 organisations

Highlights

■ More than 550,000 country-sector-time observations for 100+ countries

■ Up to 100 individual sectors, with an average of 30 sectors

■ All sources and adjustments documented for each time series in an online appendix

Some highlights

8

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

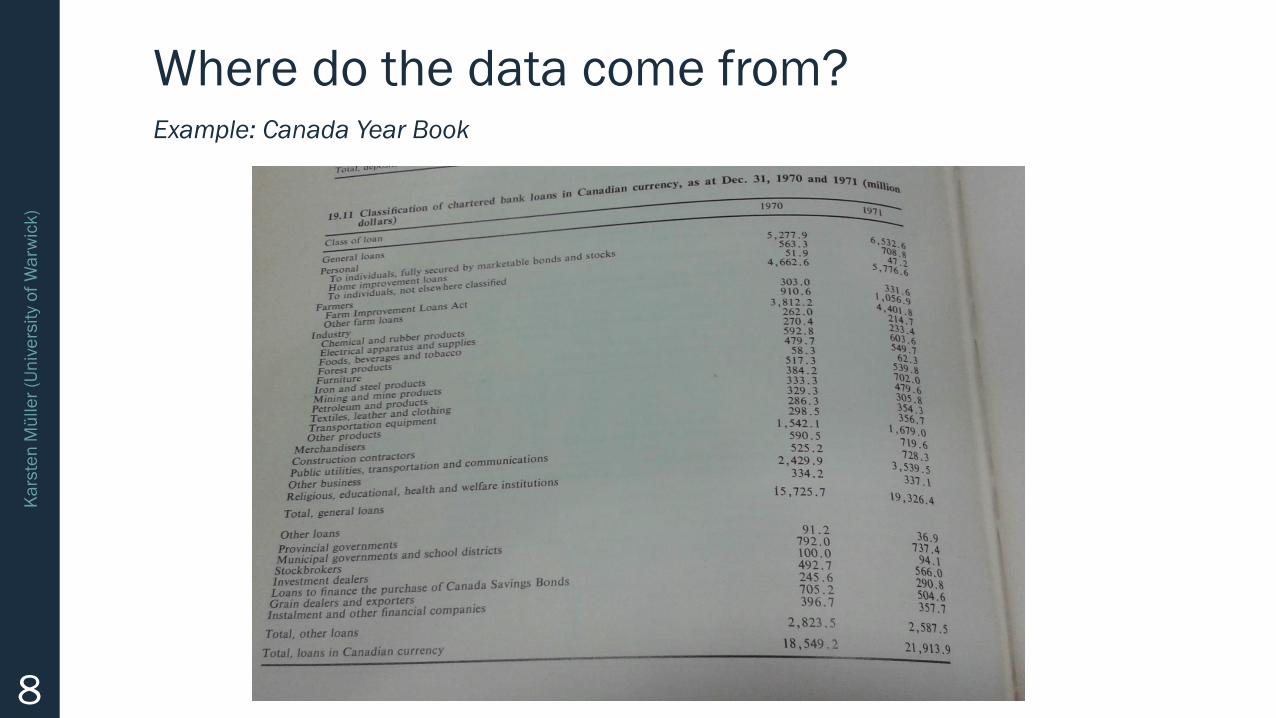

Where do the data come from?Example: Canada Year Book

9

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

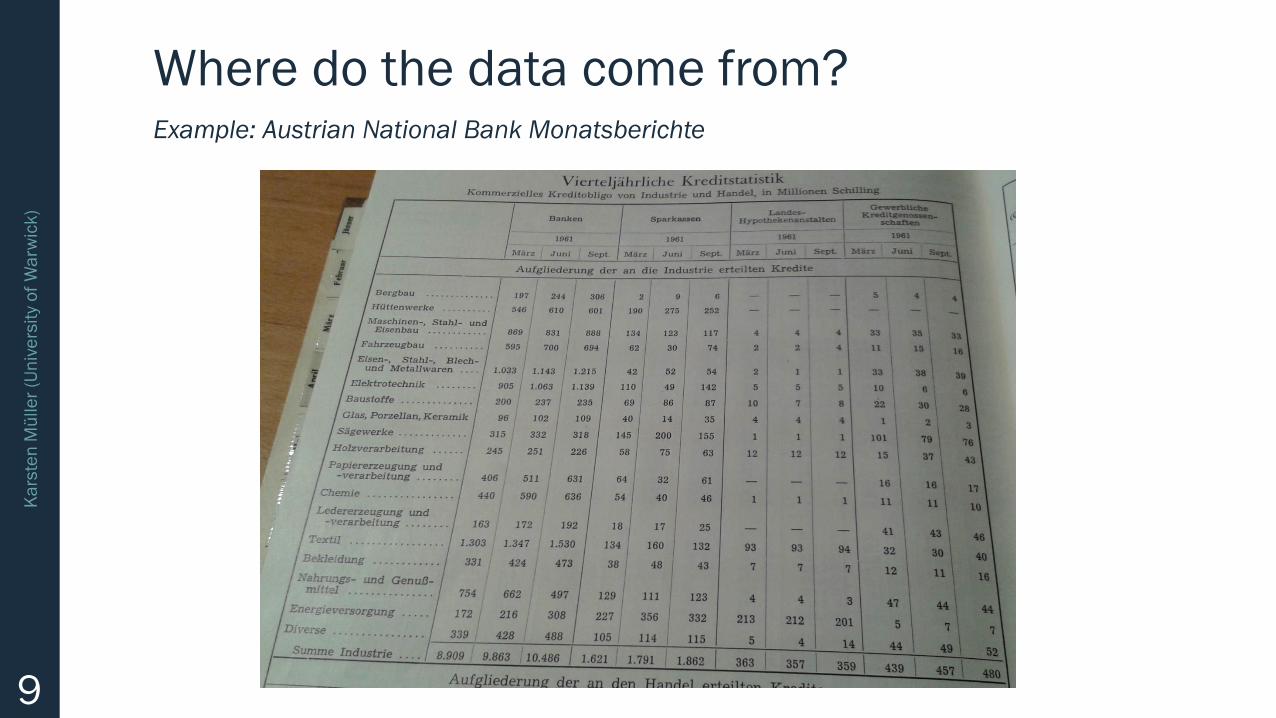

Where do the data come from?Example: Austrian National Bank Monatsberichte

10

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

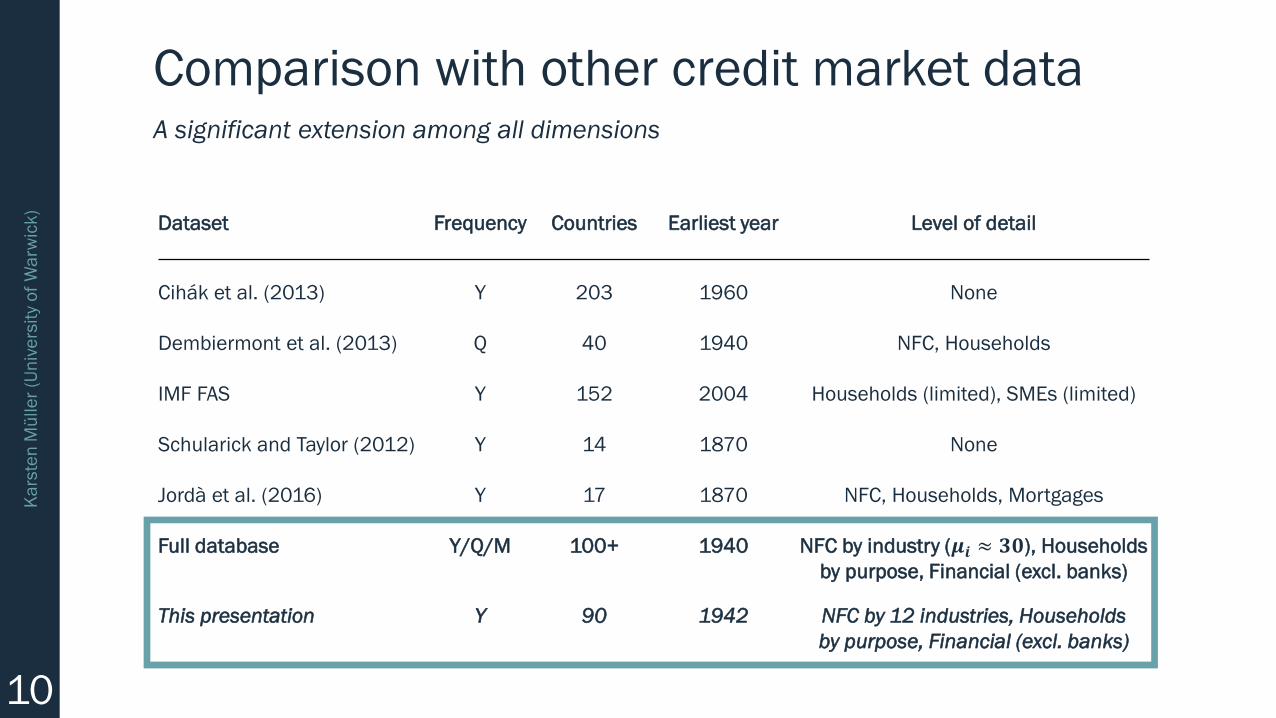

Comparison with other credit market dataA significant extension among all dimensions

Dataset Frequency Countries Earliest year Level of detail

Cihák et al. (2013) Y 203 1960 None

Dembiermont et al. (2013) Q 40 1940 NFC, Households

IMF FAS Y 152 2004 Households (limited), SMEs (limited)

Schularick and Taylor (2012) Y 14 1870 None

Jordà et al. (2016) Y 17 1870 NFC, Households, Mortgages

Full database Y/Q/M 100+ 1940 NFC by industry (𝝁𝒊 ≈ 𝟑𝟎), Households

by purpose, Financial (excl. banks)

This presentation Y 90 1942 NFC by 12 industries, Households

by purpose, Financial (excl. banks)

11

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

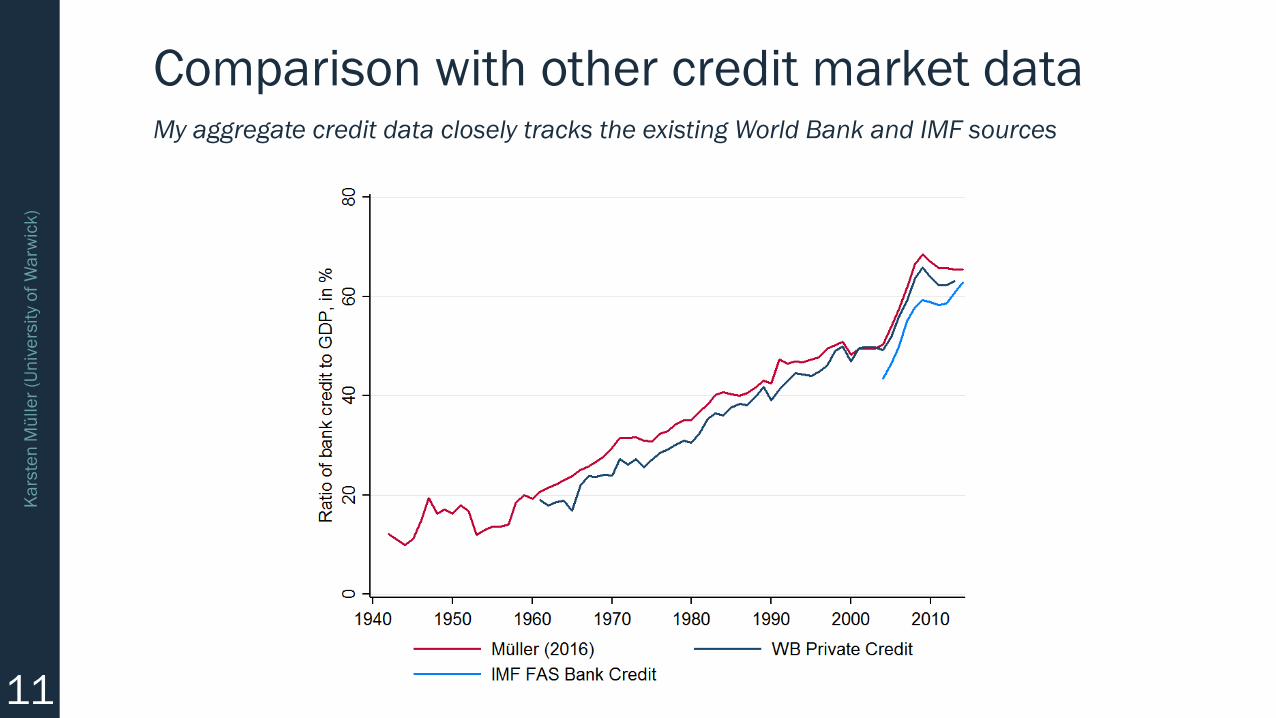

Comparison with other credit market dataMy aggregate credit data closely tracks the existing World Bank and IMF sources

12

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

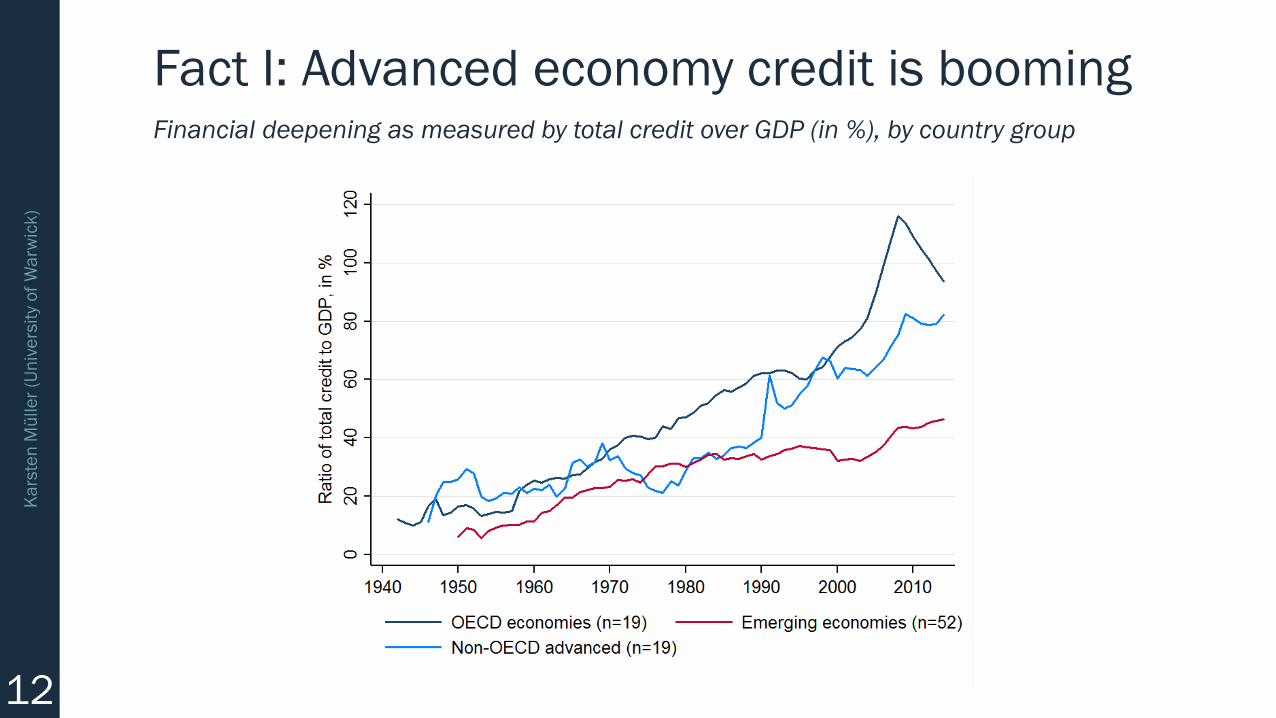

Fact I: Advanced economy credit is boomingFinancial deepening as measured by total credit over GDP (in %), by country group

13

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

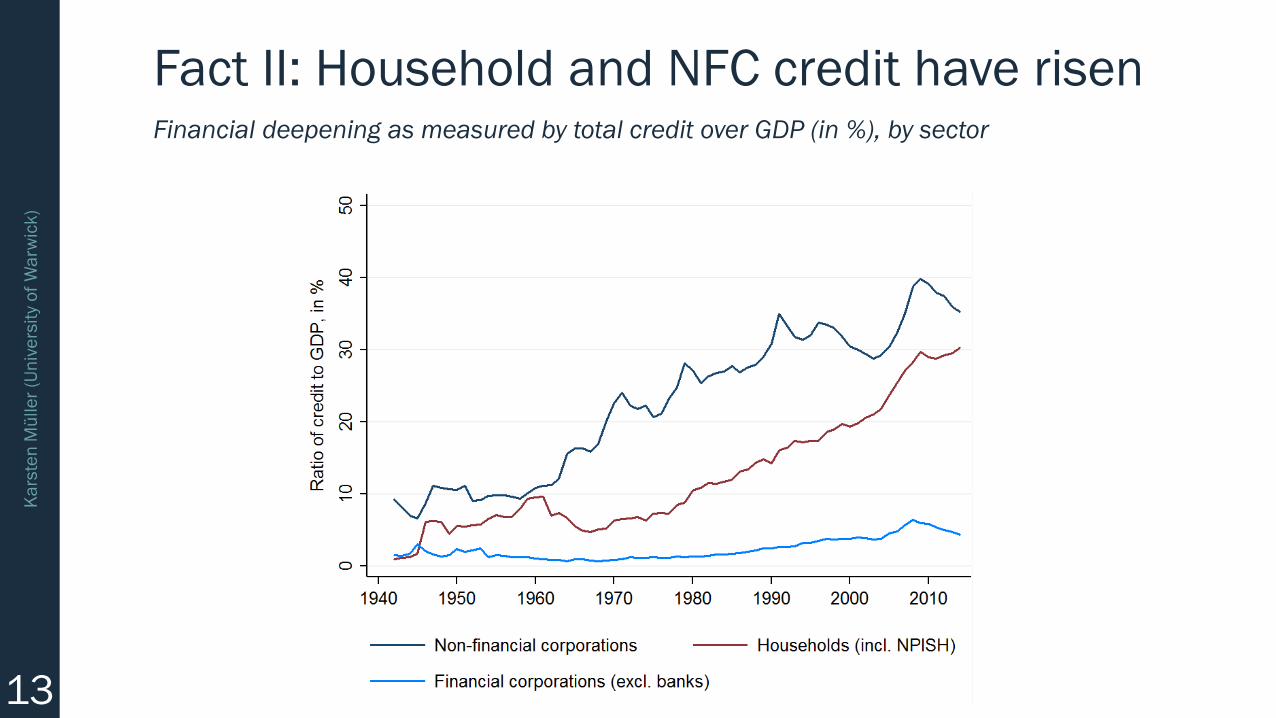

Fact II: Household and NFC credit have risenFinancial deepening as measured by total credit over GDP (in %), by sector

14

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

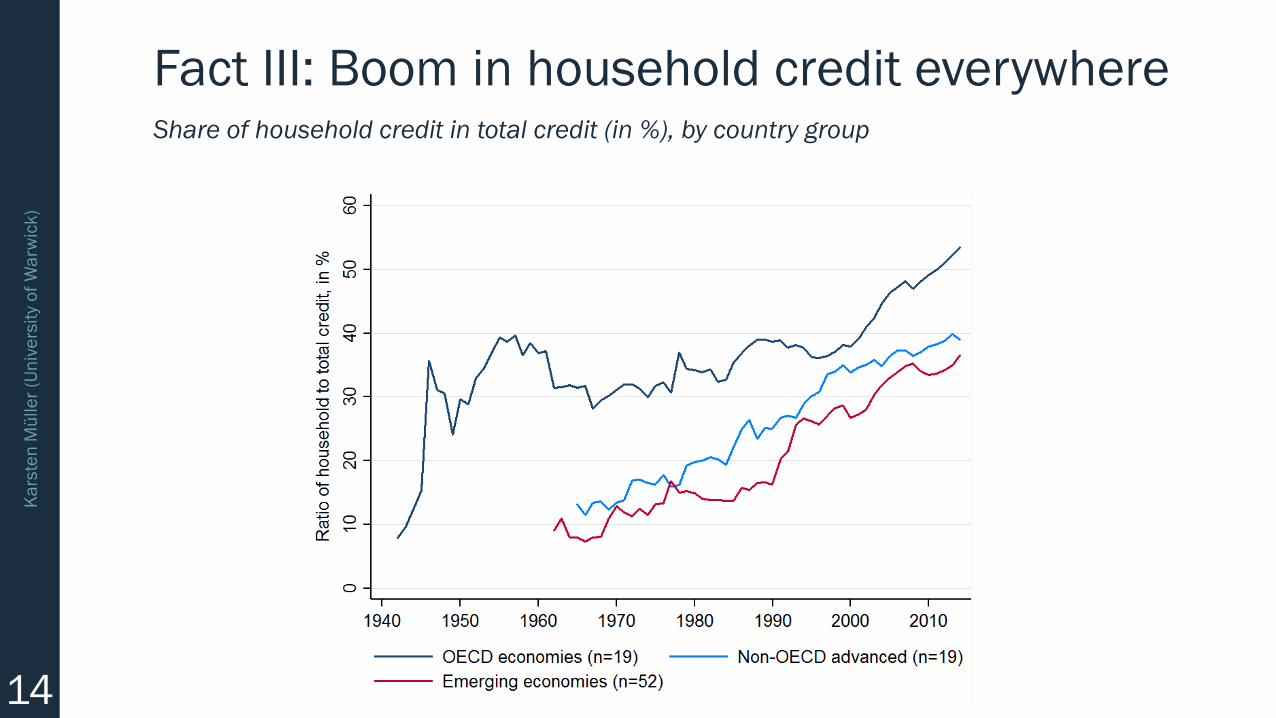

Fact III: Boom in household credit everywhereShare of household credit in total credit (in %), by country group

15

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

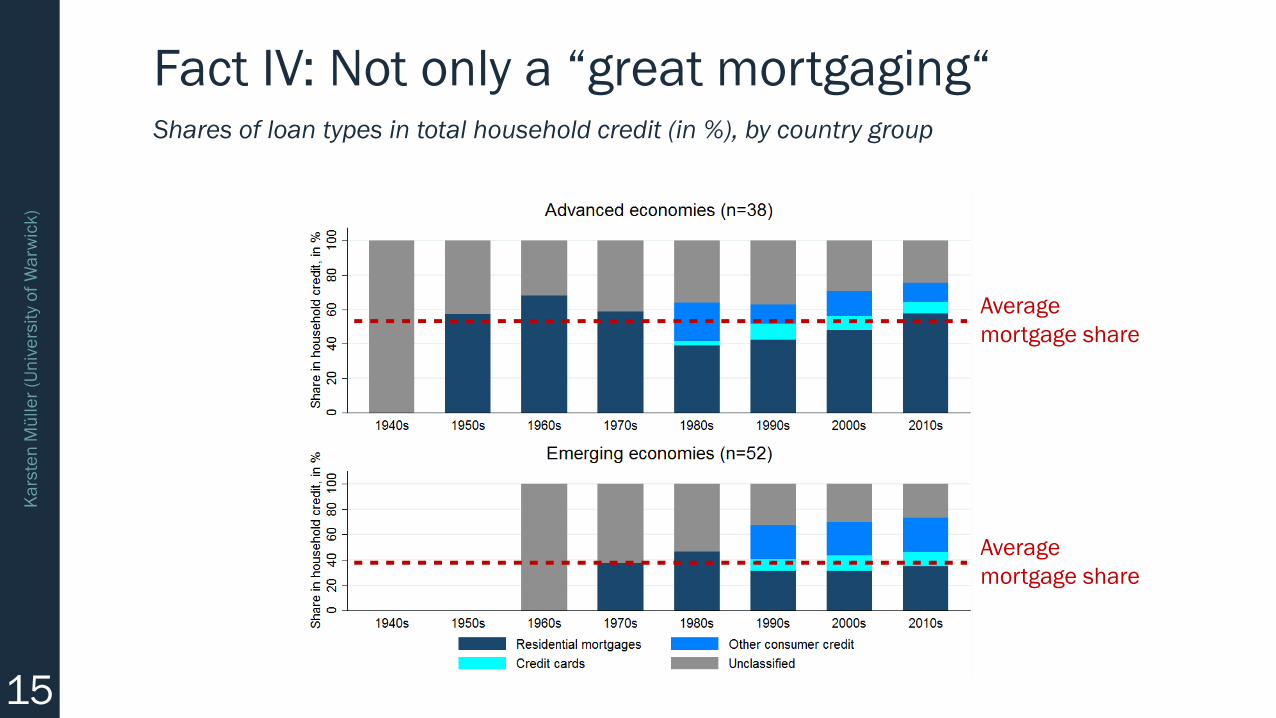

Fact IV: Not only a “great mortgaging“Shares of loan types in total household credit (in %), by country group

Average

mortgage share

Average

mortgage share

16

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

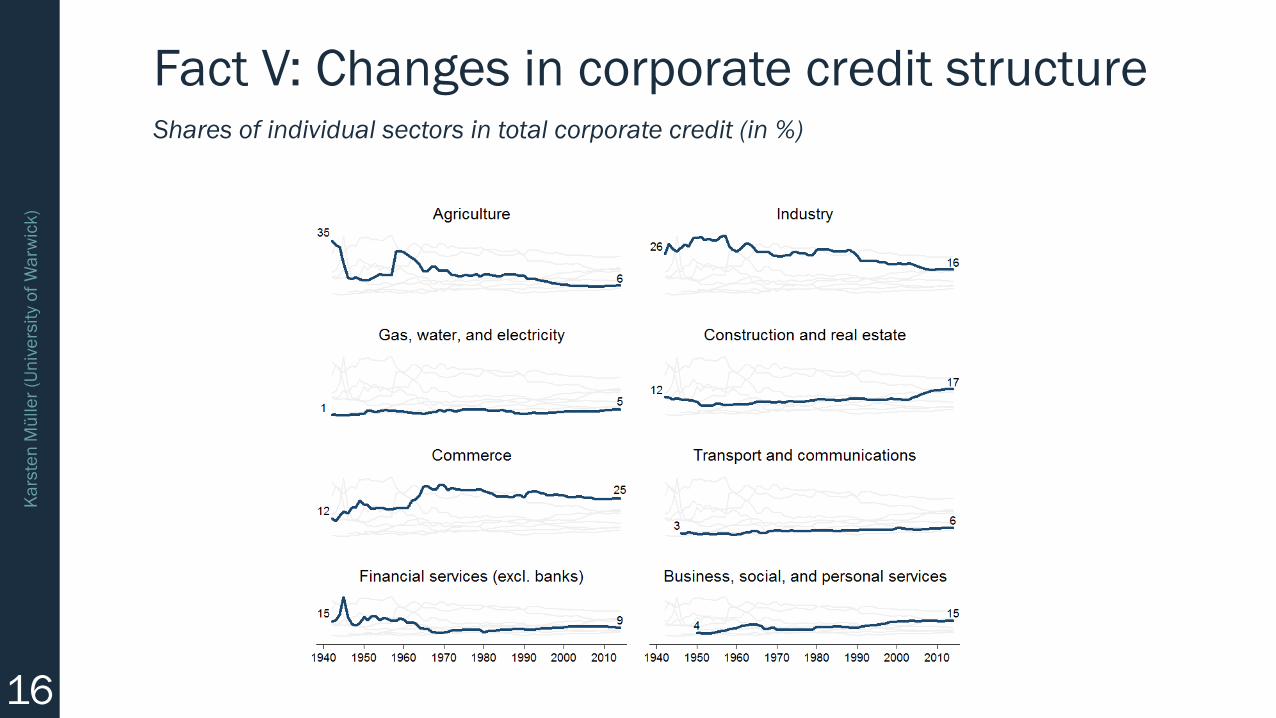

Fact V: Changes in corporate credit structureShares of individual sectors in total corporate credit (in %)

17

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

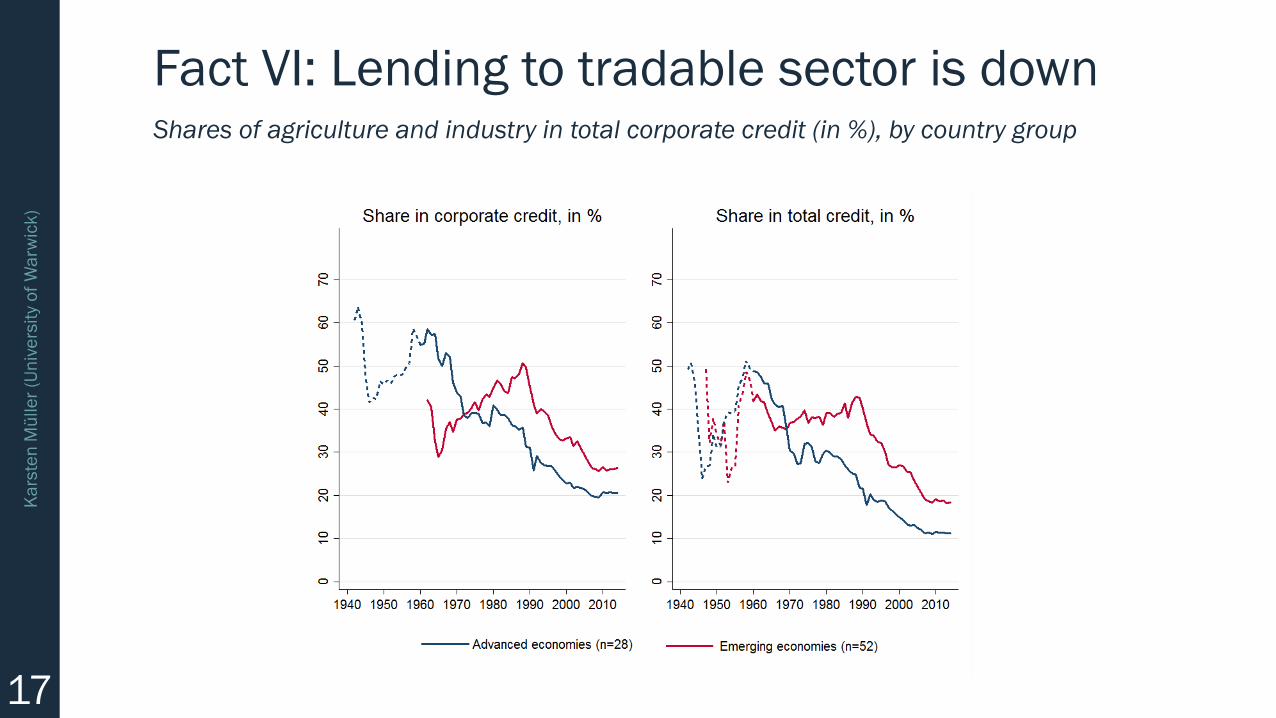

Fact VI: Lending to tradable sector is downShares of agriculture and industry in total corporate credit (in %), by country group

18

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

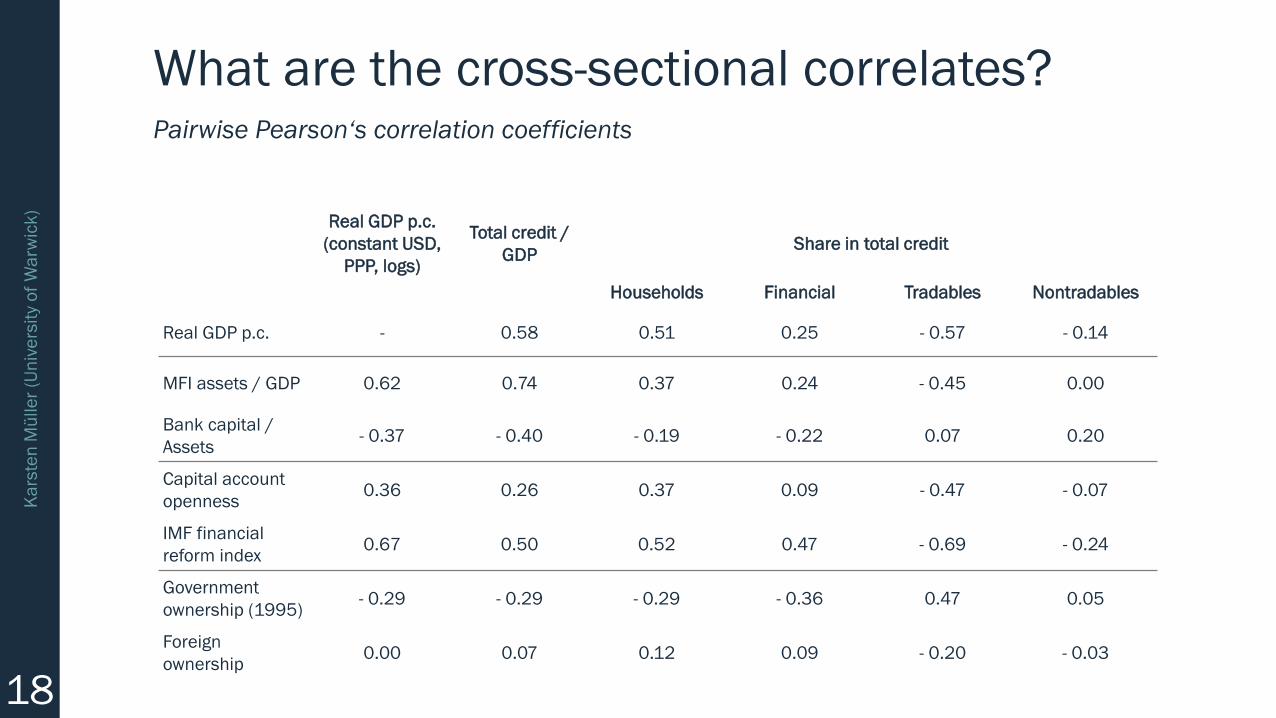

What are the cross-sectional correlates?Pairwise Pearson‘s correlation coefficients

Real GDP p.c.

(constant USD,

PPP, logs)

Total credit /

GDPShare in total credit

Households Financial Tradables Nontradables

Real GDP p.c. - 0.58 0.51 0.25 - 0.57 - 0.14

MFI assets / GDP 0.62 0.74 0.37 0.24 - 0.45 0.00

Bank capital /

Assets- 0.37 - 0.40 - 0.19 - 0.22 0.07 0.20

Capital account

openness0.36 0.26 0.37 0.09 - 0.47 - 0.07

IMF financial

reform index0.67 0.50 0.52 0.47 - 0.69 - 0.24

Government

ownership (1995)- 0.29 - 0.29 - 0.29 - 0.36 0.47 0.05

Foreign

ownership0.00 0.07 0.12 0.09 - 0.20 - 0.03

19

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

Does credit market structure matter?

■ Large literature on growth benefits of financial deepening 1

■ Recent studies suggest non-linearity: “too much finance“ may be detrimental 2

■ If that is indeed the case, what are the underlying factors?

– Long vs. short-run (Loayza and Rancière, 2006; Kaminsky and Schmukler, 2008)

– Good booms vs. bad booms (Gorton and Ordoñez, 2015)

– Credit allocation (Hsu, Tian and Xu, 2016; Beck et al., 2009)

■ I provide some new evidence from sectoral credit data

– Methodology: Bin scatter plots

The role of sectoral trends in the finance-growth nexus

1 e.g. King and Levine (1993); Rajan and Zingales (1998); Beck et al. (2000, 2002)2 e.g. Cecchetti and Kharroubi (2012, 2014); Arcand et al. (2015)

20

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

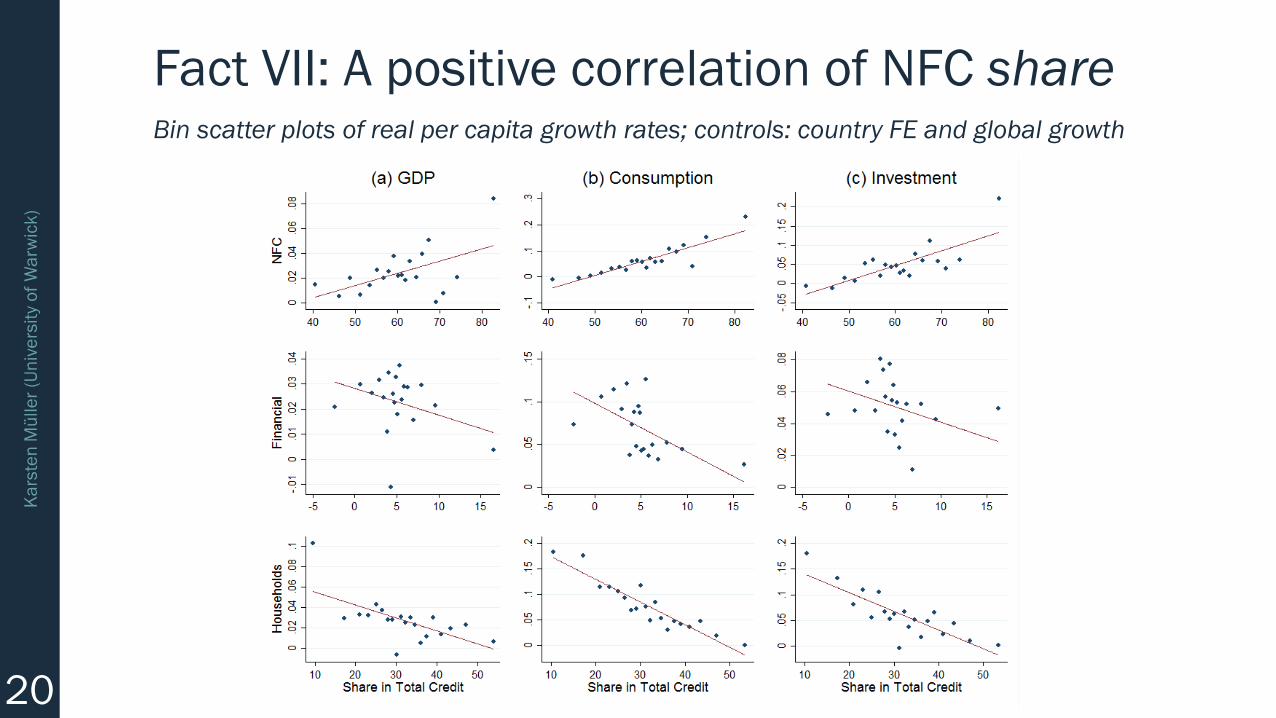

Fact VII: A positive correlation of NFC shareBin scatter plots of real per capita growth rates; controls: country FE and global growth

21

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

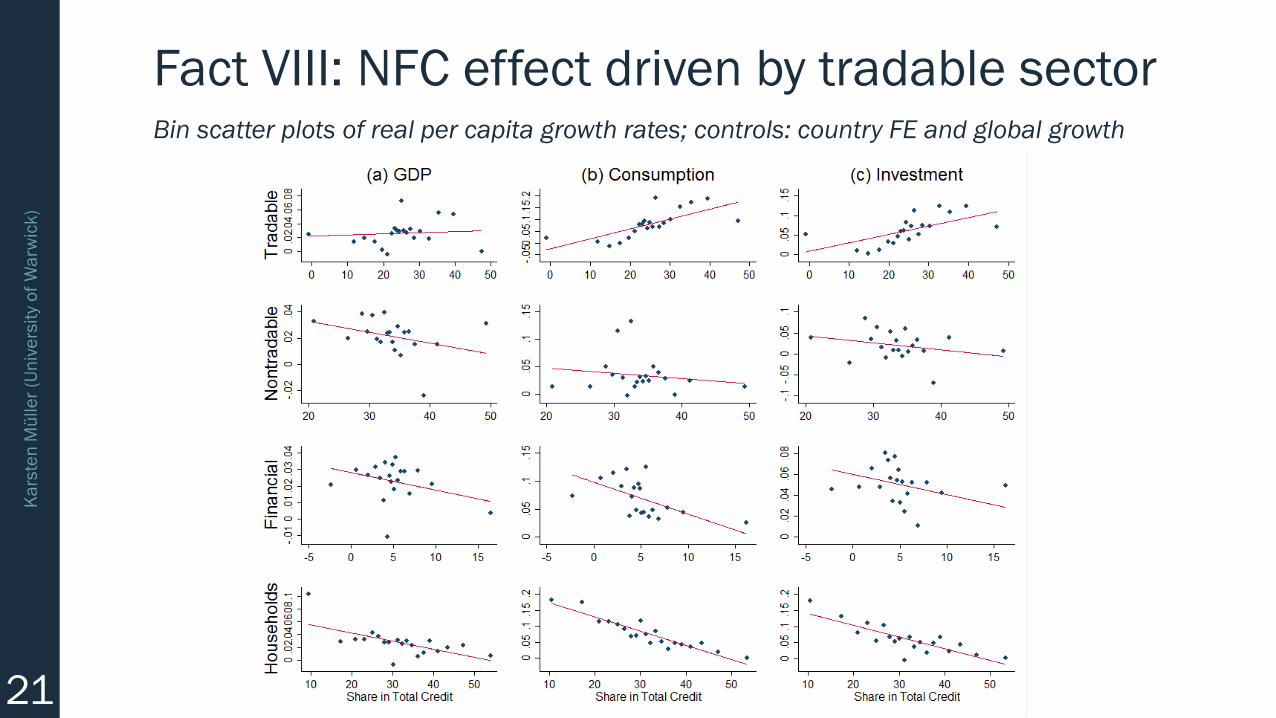

Fact VIII: NFC effect driven by tradable sectorBin scatter plots of real per capita growth rates; controls: country FE and global growth

22

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

Conclusion and outlook

■ I present a new dataset on sectoral credit for a large cross-section of countries

■ Preliminary analysis suggests that the business model of banking systems has

transformed rapidly, especially over the last four decades

■ Main beneficiaries are households, but not necessarily driven by mortgages; the

tradable sector, and manufacturing in particular, has lost significant shares

■ Taking the correlations in the data at face value, these changes suggest a role for

credit allocation when thinking about the growth benefits of financial development

■ Next steps: causal effects of the underlying drivers; more data

THANK YOU FOR YOUR ATTENTION! Any questions?

BACK UP SLIDES

25

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

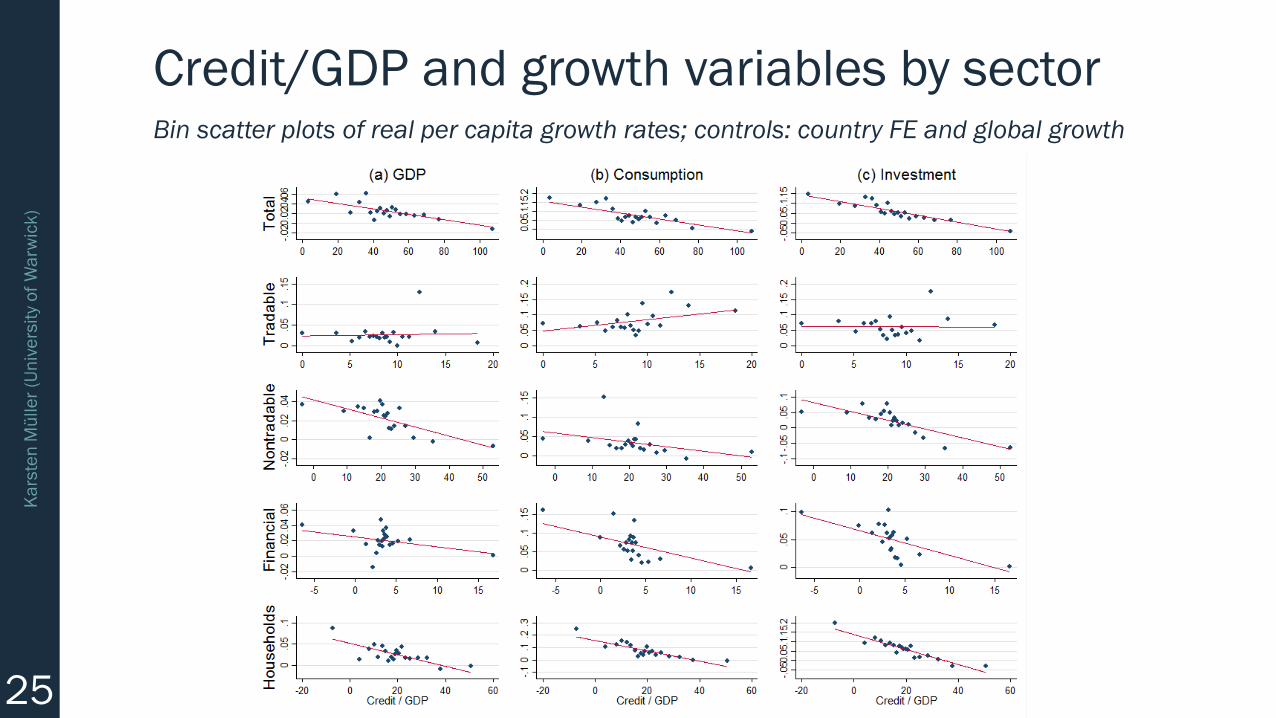

Credit/GDP and growth variables by sectorBin scatter plots of real per capita growth rates; controls: country FE and global growth

26

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

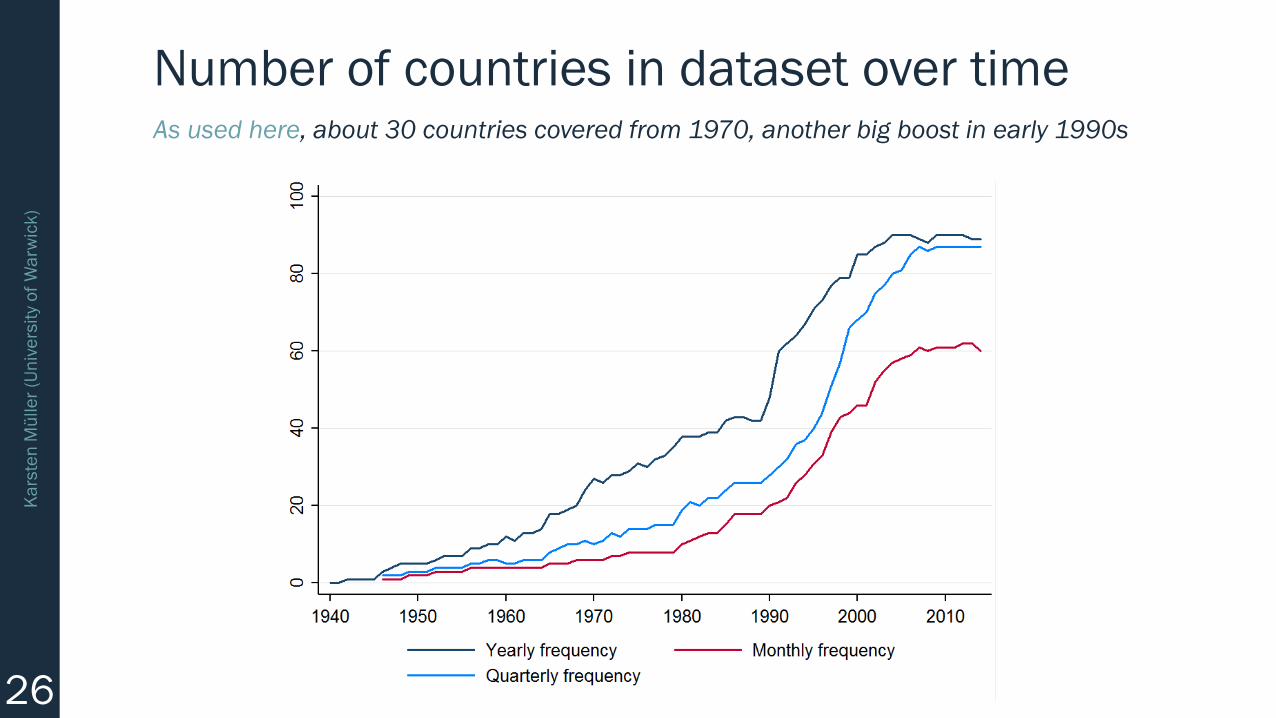

Number of countries in dataset over timeAs used here, about 30 countries covered from 1970, another big boost in early 1990s

27

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

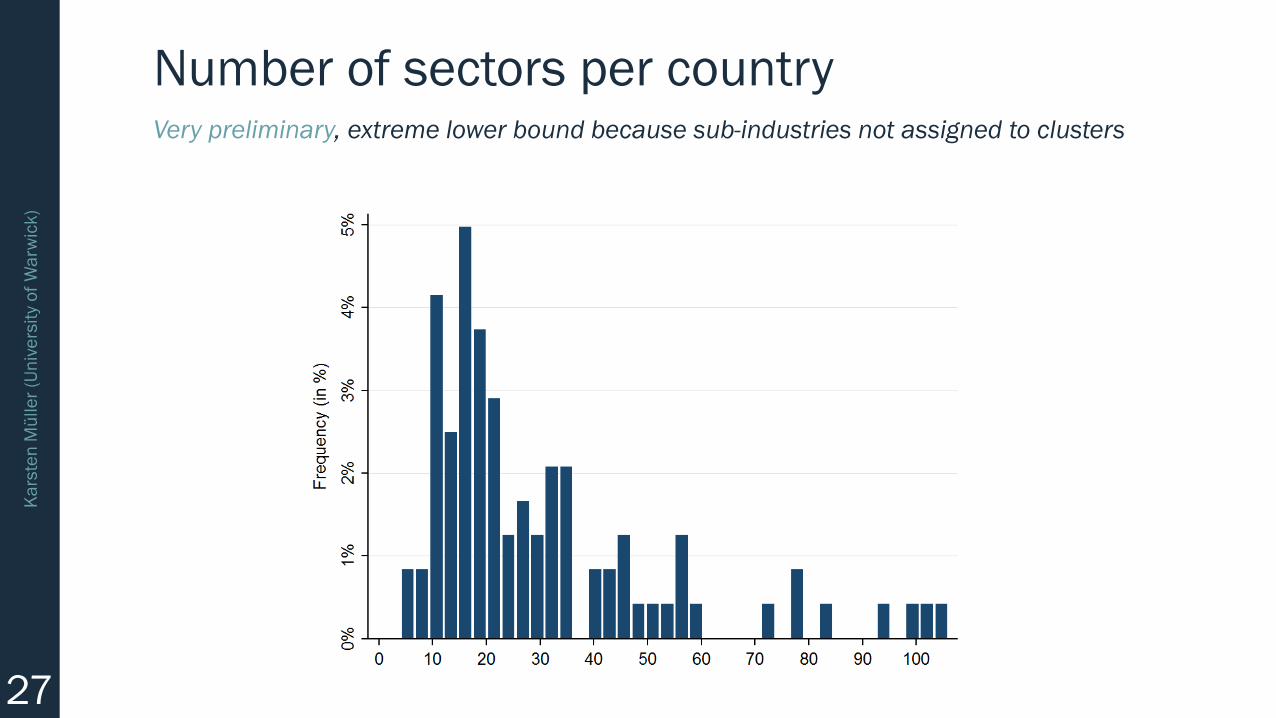

Number of sectors per countryVery preliminary, extreme lower bound because sub-industries not assigned to clusters

28

Ka

rste

n M

ülle

r (U

niv

ers

ity

of

Wa

rwic

k)

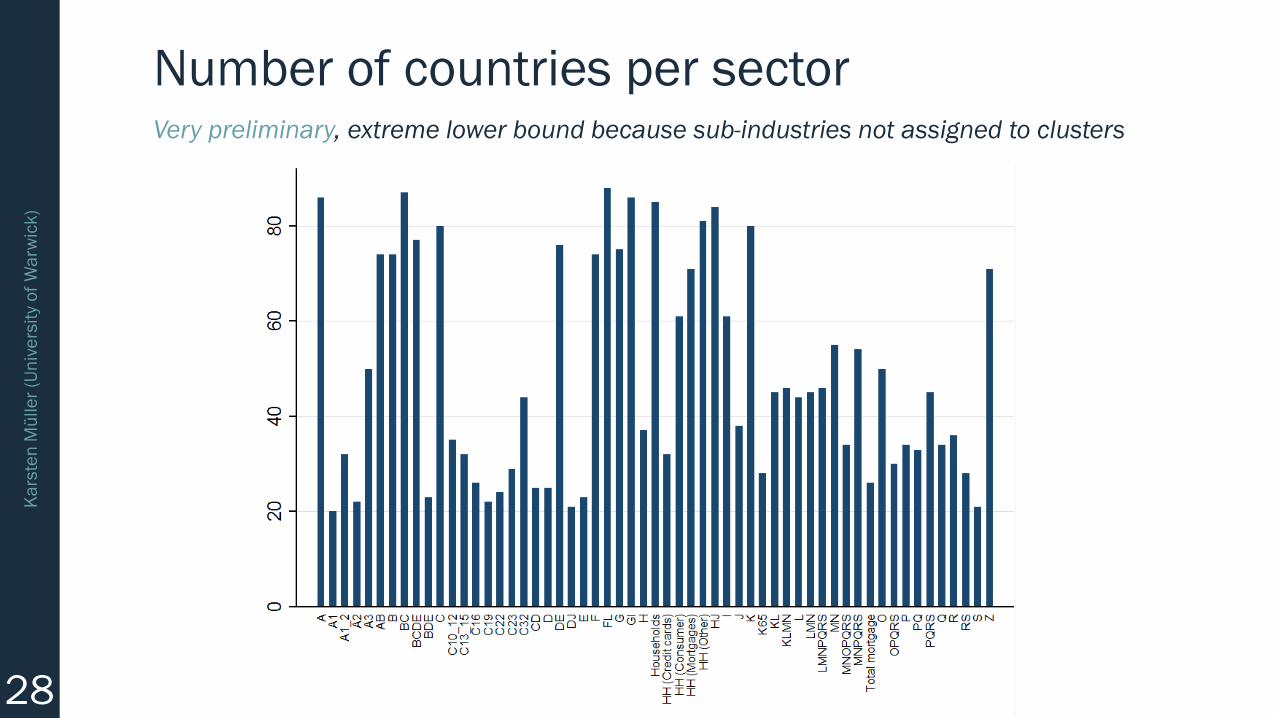

Number of countries per sectorVery preliminary, extreme lower bound because sub-industries not assigned to clusters