Embed Size (px)

Citation preview

The Right Strategy for anThe Right Strategy for an Evolving Health Care Marketg

Larry MerloyPresident & Chief Executive Officer

Analyst DayDecember 16, 2015

Forward-looking Statements

During today’s presentation, we will make forward-looking statementswithin the meaning of the federal securities laws. By their nature, allforward looking statements involve risks and uncertainties Actualforward-looking statements involve risks and uncertainties. Actualresults may differ materially from those contemplated by the forward-looking statements for a number of reasons as described in our SECfilings including the risk factors section and cautionary statementfilings, including the risk factors section and cautionary statementdisclosure in those filings.

During this presentation, we will also use some non-GAAP financialh t lki b t ’ f i l dimeasures when talking about our company’s performance, including

free cash flow, cash available to enhance shareholder value andAdjusted EPS. In accordance with SEC regulations, you can find thedefinitions of these non-GAAP items as well as reconciliations todefinitions of these non-GAAP items, as well as reconciliations tocomparable GAAP measures, on the investor relations portion of ourwebsite.

3

Key Accomplishments in 2015

Strong financial results Adj. EPS growth of ~15%; Free Cash Flow of ~$6.0B

Big wins in ’16 selling season

Superior specialty growth

$11.5B net new business; client retention of 98%

Continuing to outperform in the rapidly-growing specialty market with revenue growth of ~33%

Enhanced generic sourcing

New adjacent channel

p y g

Red Oak is hitting milestones and achieving goals

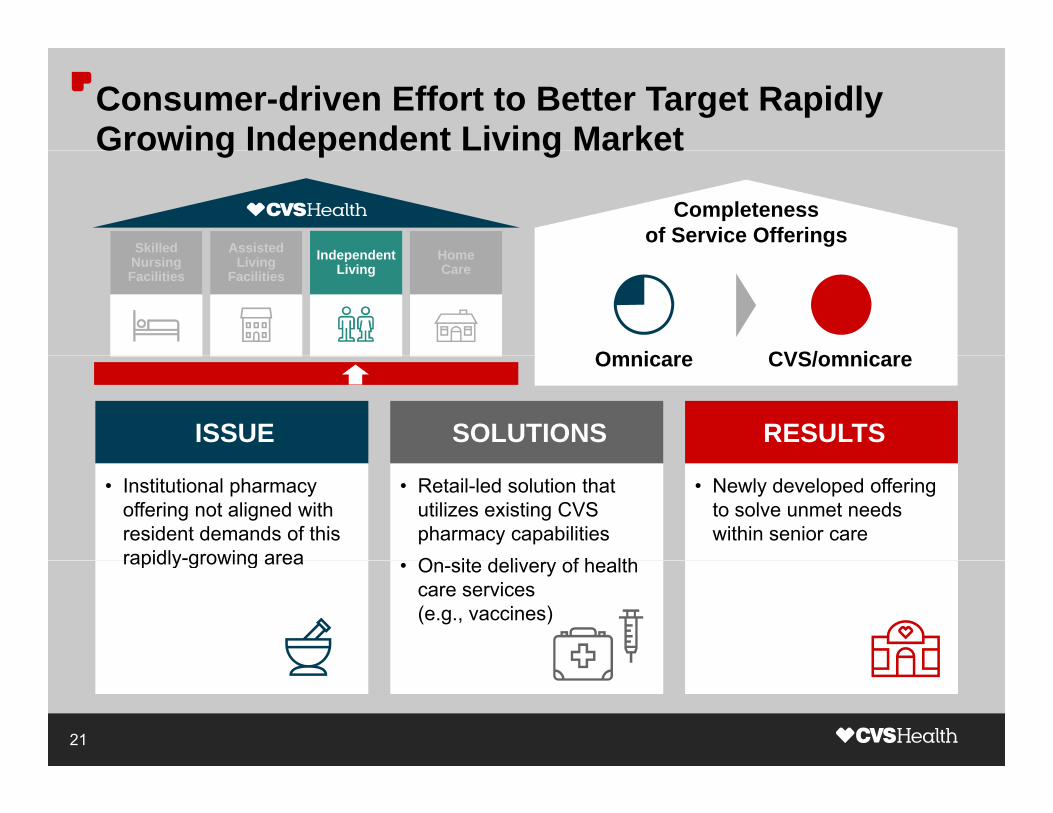

Acquired Omnicare, a leader in long-term

New, adjacent channel

Broader retail footprint

care pharmacy

Definitive agreement to purchase more than 1,660 Target pharmacies and approximately 80 retail clinics

Continued focus on enhancing health and beauty

Advanced front store strategies Continued focus on enhancing health and beauty offerings, store brands, personalization and digital

Built CVS Health brand identity Elevated awareness while continuing to play a leadership role in shaping the future of health care

Notes: See endnotes.

4

The Most Extensive Suite of Leading Assets…

Retail MailMailLong-term

CareRetailClinics

Specialty

Infusion

Clinics

Clinical Programs

Patients Medical Claims

Digital

g

Payors ProvidersClaims Editing

…providing the right strategy for an evolving health care market

5

Today’s Key Takeaways

The Right Strategy for an Evolving Health Care MarketThe Right Strategy for an Evolving Health Care Market

Leadership in multiple competencies to drive superior l f h lth t

Demonstrating Valuevalue for health care partnersto People, Payors and Providers

Expanding core pharmacy business while broadening Growing the Core, p g p y greach into new health care channels

g ,Broadening the Base

I t d i i ti d t d ki l tAlways Looking Introducing innovative products and making long-term, value enhancing investments

Always Looking Ahead

Driving shareholder value with strong earnings and cash flow as well as disciplined capital allocation

Driving Sustainable Enterprise Growth

6

Today’s Agenda

Topic Speaker

M i i i L t Sh h ld V l D D tMaximizing Long-term Shareholder Value Dave Denton

Driving Enterprise Growth in an Evolving Health Care Market Larry Merlo

Delivering Value Today, Ensuring Growth for Tomorrow Jon Roberts

Capitalizing on Growth Opportunities in Specialty Alan Lotvin

Changing the Face of Retail Pharmacy Through Innovation Helena FoulkesChanging the Face of Retail Pharmacy Through Innovation Helena Foulkes

Serving Patients Across the Continuum of Care Rocky Kraft

7

Appendixpp

Endnotes

1. Adj. EPS equals income before income tax provision plus amortization, less adjusted income tax provision, and other, which is comprised of earnings allocated to participating securities, divided by the weighted average diluted common shares outstanding.

2. Adj. EPS excludes a $521 million loss on early extinguishment of debt (approximately $0.27 per dil ted share) d ring 2014 and $52 million of acq isition related bridge financing costs and $147diluted share) during 2014, and $52 million of acquisition-related bridge financing costs and $147 million of acquisition-related transaction and integration costs during the nine months ended September 30, 2015. relating to the acquisition of Omnicare, Inc., and proposed acquisition of the pharmacies and clinics of Target Corporation. Adj. EPS also excludes any acquisition-related transaction and integration costs for the acquisition of Omnicare, Inc., and the proposed acquisition of the pharmacies and clinics of Target Corporation for the period from October 1 2015 throughof the pharmacies and clinics of Target Corporation for the period from October 1, 2015 through December 31, 2015.

3. Free Cash Flow as net cash provided by operating activities less net additions to properties and equipment (i.e., additions to property and equipment plus proceeds from sale-leaseback transactions).

4 Adj EPS growth and Free Cash Flow are based on midpoints of 2015 guidance4. Adj. EPS growth and Free Cash Flow are based on midpoints of 2015 guidance.5. Client retention rate is defined as: 1 less (projected 2016 lost revenues from known terminations

occurring after January 1, 2015, divided by estimated 2016 PBM revenues) expressed as a percentage. Both terminations and PBM revenues exclude the individual PDP business.

6. The following trademarks appear throughout the 2015 Analyst Day presentations: : , CVS Health CVS/caremark Omnicare CVS/Omnicare CVS/specialty CVS/caremark CVSCVS Health, CVS/caremark, Omnicare, CVS/Omnicare, CVS/specialty, CVS/caremark, CVS, Maintenance Choice, Coram, Navarro, Novologix, Omniview, MyOmniview, CVS/minuteclinic, Health Engagement Engine, Accordant, RX Insights, ScriptSync, MinuteClinic and Specialty Connect. They are trademarks or registered trademarks of CVS Pharmacy, Inc.

9

Maximizing Long-termMaximizing Long term Shareholder Value

Dave DentonExecutive Vice President &Chief Financial OfficerChief Financial Officer

Non-GAAP Financial Measures

Free Cash Flow and Cash Available forEnhancing Shareholder Value Adjusted Earnings per Share

Income before income tax provision

+ Amortization

Net cash provided by operating activities

Enhancing Shareholder Value

+ Amortization

- Adjusted income tax provision

- Earnings allocated to participatingsecurities

- Additions to property andequipment

+ Proceeds from sale-leasebacks securities

÷ Weighted average diluted sharesoutstanding

Adj d i h

Free cash flow

+/- Change in net debtAdjusted earnings per shareCash available for enhancing

shareholder value

Note:1. CVS Health finances a portion of its store development program through sale-leaseback transactions. Use of sale-leaseback financing is subject to change

as a variety of financing vehicles for future development are evaluated. This may also result in changes to CVS Health’s definition of free cash flow.

2

Agenda

Strong Record of ExecutionStrong Record of ExecutionStrong Record of ExecutionStrong Record of Execution

Marketplace MisconceptionsMarketplace Misconceptions

Looking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

Looking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

3

Continuing Focus on Enhancing Shareholder Value

Productive Generating Si ifi t Optimizing

Long-term Growth

SignificantFree Cash

Flow

Op gCapital

Allocation

EnhancedEnhancedShareholder Value

4

Our Leadership in Multiple Competencies Continued to Drive Shareholder Value in 2015

• Driving top- and bottom-line results through an

Continued to Drive Shareholder Value in 2015

Revenues and

• Delivering Adjusted EPS at high end of initial targets

• Driving top- and bottom-line results through an enterprise focus

Revenues and Operating Profit

Earnings per Share • 1¢ accretion from Omnicare acquisition and new debt

• Generating substantial free cash flow

Earnings per Share

Free Cash Flow

• Returning more than $6 billion to shareholders through dividends and share repurchasesShareholder Value

5

Note:1. Earnings per share excludes acquisition-related bridge financing, transaction and integration costs.

2015 Guidance Reaffirmed

Full-year 2015

Net Revenue Growth 9.75% to 10.25%

Adjusted EPS FromContinuing OperationsYear-over-year Growth

$5.14 to $5.1814.25% to 15.25%Year-over-year Growth

Free Cash Flow $5.9 to $6.2 billionFree Cash FlowYear-over-year Growth

$ $Down 4% to 10%

Notes:Notes:1. Excludes acquisition-related bridge financing, transaction and integration costs.2. Excludes $521 million loss on early extinguishment of debt recognized in 2014.3. Free cash flow in 2014 was approximately $500 million above goal due to receipt of some early payments from CMS, benefiting 2014 and to the detriment of 2015.

6

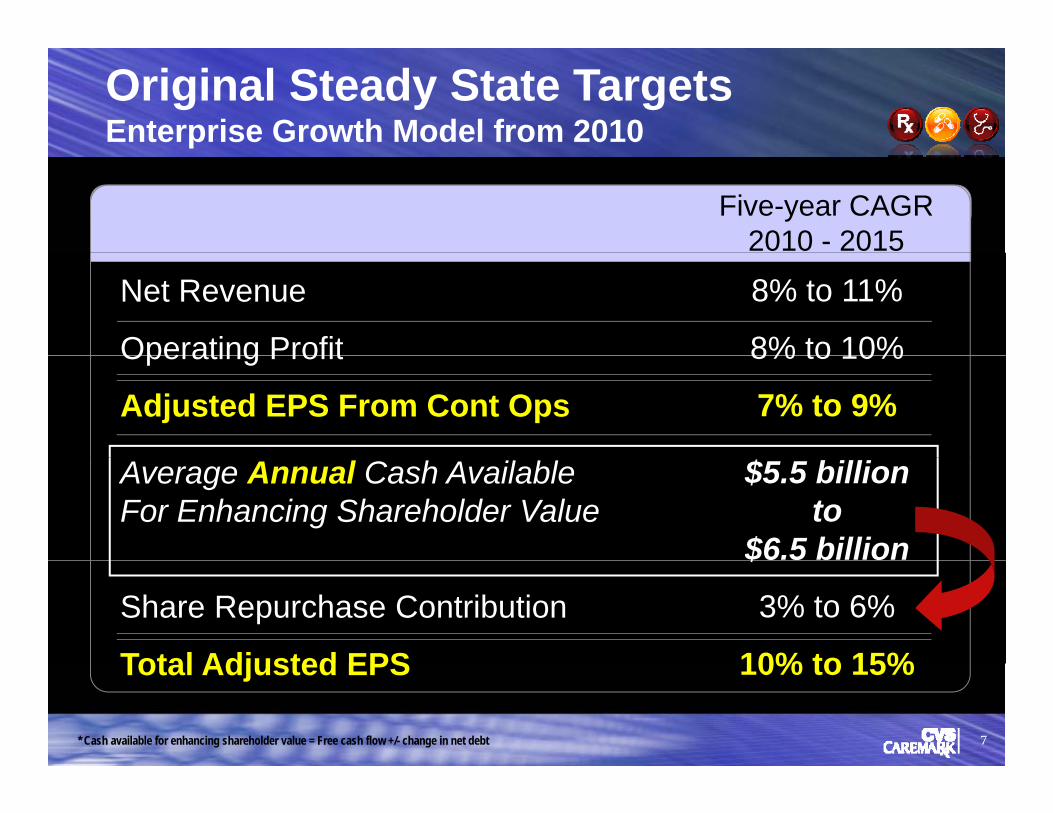

Original Steady State TargetsEnterprise Growth Model from 2010

Five-year CAGR2010 - 2015

Net Revenue

Operating Profit

8% to 11%

8% to 10%Operating Profit

Adjusted EPS From Cont Ops

8% to 10%

7% to 9%

Average Annual Cash Available For Enhancing Shareholder Value

$5.5 billionto

$6.5 billion

Share Repurchase Contribution

Total Adjusted EPS

$

3% to 6%

10% to 15%

7

Total Adjusted EPS 10% to 15%

* Cash available for enhancing shareholder value = Free cash flow +/- change in net debt

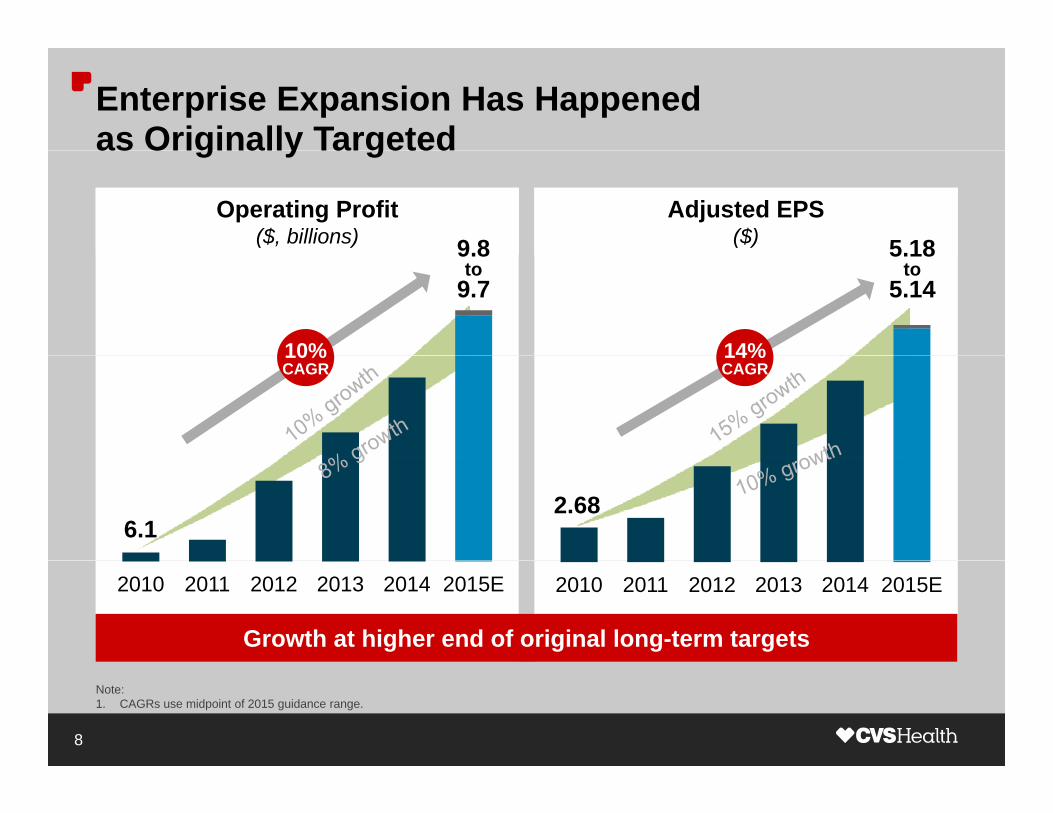

Enterprise Expansion Has Happenedas Originally Targetedas Originally Targeted

Operating Profit($, billions)

Adjusted EPS($) 5 189 8

10% 14%

5.18to

5.149.8to

9.7

10%CAGR

14%CAGR

6.12.68

Growth at higher end of original long-term targets

2010 2011 2012 2013 2014 2015E 2010 2011 2012 2013 2014 2015E

Note:1. CAGRs use midpoint of 2015 guidance range.

8

Strategic Capital Deployment with Acquisitions of Omnicare and Target Pharmacies and ClinicsOmnicare and Target Pharmacies and Clinics

OMNICARE TARGET

• Brings a new pharmacy dispensing channel to CVS as the leading provider of

• Enhances network and relevance of CVS Health’s integrated offeringsg p

pharmacy services to long-term care facilities

• CVS + Omnicare enhances

g g

• Enables Target guests to participate in unique CVS programs (e.g., Maintenance

ability to provide continuity of care for patients

• Complementary specialty

p g ( g ,Choice, Specialty Connect)– Provides convenience and

cost savings to consumers p y p ybusiness will augment our capabilities

and payors– Other pharmacies cannot

replicate what CVS provides

9

Well-laddered Debt Maturities Remain Core to Strong Balance SheetStrong Balance Sheet

Debt Maturity Profile (Bonds)($, billions)

1.71.2 1.1 1.3 1.2

0.5 0.6

1.31.0

0.50.7 0.5 0.8

2016 2017 2018 2019 2020 2021 2022 2023 2024 2027 2039 2041 2043

10

Well-laddered Debt Maturities Remain Core to Strong Balance SheetStrong Balance Sheet

Debt Maturity Profile (Bonds)($, billions)

3.53.2 3.2 3.0

3.5

2.0

1.2 1.1 1.2

0.6

1.31.0

0.50.7 0.5 0.8

Balance sheet remains healthy with addition of $15 billion of senior notes

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2027 2035 2039 2041 2043 2045

y $

11

Committed to Maintaining a Healthy Balance Sheet

As expected new debtAdjusted Debt-to-EBITDA

3.2

3.4

As expected, new debt increased leverage ratio above target of 2.7X3.30

2.8

3.0• Committed to returning to a

leverage ratio at target

– Driven mostly by strong EBITDA Target = 2.70

2.94

2 2

2.4

2.6 growth

– Will also pay down debt with upcoming maturities

2.66

2.392.2'13 '14 '15E '16E

2.39

Focused on maintaining high BBB credit ratingNote:1. Figures shown are as of the end of the fourth quarter for each respective year and do not include bridge financing, transaction and integration costs

associated with the acquisitions of Omnicare and the pharmacies and clinics of Target.

12

$41 Billion Available to Enhance2014 Through 2018 Returns2014 Through 2018 Returns

($8) $10~$39billion

~$31

($8)billion

$41$10billion

$31billion billion

Operating Cash Flow Net Capex Free

Cash FlowIncremental Debt

Cash Available

13

Efficient Cash Deployment 2014 Through 2018

Cash Available for Enhancing Shareholder g

Value

$41 billion

Dividends

Target payout ratio

Return on Invested Capital

Share Repurchases

of 35% by 2018

~18% implied dividend CAGR

Drive ROIC with value-enhancing

projects

$4 billion to $5 billion per year

Value creating

14

~$23 Billion Available for Returns in 2014 and 2015

Effective allocation of cash available in ‘14 and ‘15 through:

Cash Available & Capital Allocation ($, billions)g

• 56% increase of annual dividend– Payout ratio estimated to be nearly

29% at year endShare

h

22.9

9.0

23.8

29% at year-end

• Target and Omnicare acquisitions consistent with growing core and Acquisitions

repurchases9.0

12 0broadening base

• Expect to complete a total of $9 billion of repurchases by year-end

Dividends

Acquisitions

2.9

12.0

Cash Available Capital Allocatedbillion of repurchases by year end

~ $24 billion of deployed capital 2014 and 2015

Note:1. Cash available = Free cash flow plus increase in debt. 2. Acquisitions are shown net of cash acquired. 3. Figures may not foot due to rounding.

15

Solid History of Enhancing Returns Using All Three Pillars for Efficient Cash Deployment Pillars for Efficient Cash Deployment

Annual Dividendper Share

($)

ShareRepurchases

($ )

Acquisitionsand Ventures

1.40

29%CAGR

($)

5 0

$20bTotal

($, billions)Apr ’12

HealthNetPDP

Apr ’11

Universal American

PDP

0.650.90

1.101.40

3.0

4.3 4.0 4.05.0

Jan ’14

Coram

Feb ’13

DrogariaOnofre

Mar ’13

NovoLogix

0.500.65

Aug ’15

Omnicare

Jul ’14

Red Oak S i

Sep ’14

Navarro

'11 '12 '13 '14 '15E '11 '12 '13 '14 '15ESourcing

Deployment of capital in line with long-term targets

16

p y p g g

2016 Capital Deployment to IncludeDividend Increase and Further Repurchases

• Increasing 21%

Dividend Increase and Further Repurchases

2016 Annual • Increasing 21%,from $1.40 to $1.70

Dividend

$1 70$1.702016 Share Repurchases

$4billion

• Currently $7.7 billion authorized and remaining from 2014 share repurchase program billionrepurchase program

More than $5 billion expected to be returned to shareholders in 2016

17

$ p

Agenda

Strong Record of ExecutionStrong Record of Execution

Marketplace MisconceptionsMarketplace MisconceptionsMarketplace Misconceptions

Looking Ahead: 2016 Guidance Review

Marketplace Misconceptions

Driving Sustainable Enterprise Growth

Looking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

18

MYTH #1

ALL SPECIALTY PHARMACIES AREPHARMACIES ARE SIMILAR IN PRACTICE TOSIMILAR IN PRACTICE TO THE CAPTIVE “SPECIALTY” PHARMACIES THATPHARMACIES THATHAVE COME UNDER RECENT SCRUTINY

19

FACT #1

TRUE SPECIALTY PHARMACIES LIKEPHARMACIES LIKE CVS/SPECIALTY HAVECVS/SPECIALTY HAVEA DIFFERENT BUSINESS MODEL THAN THESE CAPTIVECAPTIVEPHARMACIES

20

Misconceptions in Marketplace Are Creating NoiseFACT #1: CVS/specialty Is Different

• These captive pharmacies are NOT specialty pharmaciesD i t j it f h l f f t

p y

– Derive vast majority of pharmacy volume from one manufacturer– Many don’t dispense specialty medications– Attempting to circumvent cost-saving solutions our clients have adopted

• To best manage access and cost, CVS/caremark determines which pharmacy is eligible to be an in-network provider

T i t h i lik th h f li– Terminate some pharmacies like these each year for non-compliance

• In contrast, CVS/specialty provides high-touch care to patients with complex specialty conditions requiring costly drug therapiescomplex specialty conditions requiring costly drug therapies– Extensive clinical services help to ensure proper adherence, better

health outcomes and lower trend

21

MYTH #2

THE RxCROSSROADSBUSINESS COULD BE ABUSINESS COULD BE A BIG RISK FOR CVSBIG RISK FOR CVS HEALTH GIVEN THATIT IS AT ODDS WITH CLIENTS’CLIENTSOBJECTIVES

22

FACT #2

THE RxCROSSROADSBUSINESS IS ALIGNEDBUSINESS IS ALIGNED WITH OUR FOCUS ONWITH OUR FOCUS ON COST, QUALITY AND ACCESS, AND IS IMMATERIAL TO OURIMMATERIAL TO OUR FINANCIAL RESULTS

23

Misconceptions in Marketplace Are Creating NoiseFACT #2: RxCrossroads Is Aligned

• RxCrossroads follows CVS Health’s philosophy of:C t lli t d tili ti f li t

g

– Controlling costs and utilization for our clients– Promoting better health outcomes for the patients we serve– Promoting access to appropriate prescription medication

• Patient assistance programs provide help to underinsured and uninsured patients who can’t afford drugs

• RxCrossroads is immaterial to CVS Health’s overall financial results– Analyzed as part of due diligence effortsy p g– Contributes less than 1¢ to earnings per share

24

MYTH #3

ALWAYS PARTICIPATE IN PREFERRED NETWORKSPREFERRED NETWORKS FOR OPTIMAL SUCCESSFOR OPTIMAL SUCCESS IN MEDICARE PART D

25

FACT #3

NOT ALL MEDICARE PART D NETWORKSPART D NETWORKSARE CREATED EQUAL …ARE CREATED EQUAL … FINANCIAL DISCIPLINEIS REQUIRED

26

Misconceptions in Marketplace Are Creating NoiseFACT #3: Med D Networks Are Not Equal

• In preferred networks, plan designs must offer pharmacies enough share gain to more than offset reduced margins

q

share gain to more than offset reduced margins– Significant incentive must be offered to patients to switch pharmacies

• Key areas of consideration with Med D networks:– Mix of lives important as some don’t experience any co-pay differential– Co-pay differential not always large enough to incent patients

• Will not participate in Aetna’s preferred Med D network for 2016• Will not participate in Aetna s preferred Med D network for 2016– Share gains won’t offset margin loss– Don’t expect to lose significant share; impact expected to be immaterial

• We participate in networks that make economic sense– Expect to have a significant presence in preferred Med D networks in

2016

27

MYTH #4

UNDERLYING GROWTHIN EACH SEGMENT ISIN EACH SEGMENT IS WHAT ULTIMATELYWHAT ULTIMATELYFUELS THE CVS HEALTH VALUE-CREATION ENGINEENGINE

28

FACT #4

CVS HEALTH’SSUCCESS WILL BESUCCESS WILL BE DRIVEN BY ENTERPRISEDRIVEN BY ENTERPRISE GROWTH … SOMETIMES AT THE EXPENSE OFONE OF THEONE OF THESEGMENTS

29

Misconceptions in Marketplace Are Creating NoiseFACT #4: Enterprise Growth Drives Success

• Critical to focus on enterprise growth

p

• Unique offerings are aligned across the company in support of the enterprise growth strategy

F l S i lt C t hift i t ll ll i lt l d– For example, Specialty Connectshifts virtually all specialty volume and growth to the PBM

• We are indifferent to channel and manage the business through an enterprise lens

30

Agenda

Strong Record of ExecutionStrong Record of Execution

Marketplace MisconceptionsMarketplace Misconceptions

Looking Ahead: 2016 Guidance ReviewLooking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

Looking Ahead: 2016 Guidance ReviewLooking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

31

2016 Guidance: Healthy Enterprise Growth

Full-year 2016

Net Revenue Growth 17.0% to 18.5%

Adjusted EPSYear-over-year Growth

$5.73 to $5.8811.25% to 14.25%

GAAP Diluted EPS $5.28 to $5.43

Notes:1. EPS growth estimates exclude acquisition-related transaction and integration costs.2 Year-over-year growth based on midpoint of 2015 guidance2. Year over year growth based on midpoint of 2015 guidance.3. Estimates assume that the acquisition of Target’s pharmacies and clinics closes at year-end 2015.4. EPS estimates assume completion of approximately $4 billion in share repurchases in 2016.5. EPS estimates include dilution of $0.01 in 2016 related to the termination of pension plans. The impact on 2017 is expected to be between $0.10 and $0.15.

32

2016 Guidance: Substantial Free Cash Flow … Growth Impacted by AcquisitionsGrowth Impacted by Acquisitions

Full-year 2016in billions

Operating Cash Flow $7.6 to $7.9

Gross Capital Expenditures ($2.6) to ($2.5)Sale-leaseback Proceeds $0.3 to $0.2

Net Capital Expenditures Approximately ($2.3)

Free Cash FlowYear-over-year Growth

$5.3 to $5.6Down 7% to 12%

Notes:1. Year-over-year growth based on midpoint of 2015 guidance.2 Estimates assume that the acquisition of Target’s pharmacies and clinics closes at year-end 20152. Estimates assume that the acquisition of Target s pharmacies and clinics closes at year-end 2015.3. Guidance includes approximately $500 million of cash outflows from acquisition-related transaction and integration expenses. 4. CVS Health finances a portion of its store development program through sale-leaseback transactions. Use of sale-leaseback financing is subject to change

as a variety of financing vehicles for future development are evaluated. This may also result in changes to CVS Health’s definition of free cash flow.

33

Healthy Enterprise Growth Expected to Continue

Operating Profit($, billions)

Adjusted EPS($)10.8

10%CAGR

14%CAGR

5.88to

5.73

10.8to

10.5

CAGR CAGR

8.0 3.96

2016 growth expected to be within or above target ranges

2013 2014 2015E 2016E 2013 2014 2015E 2016E

Notes:Notes:1. CAGRs are calculated using 2016E midpoint of guidance range.2. Excludes a $72 million gain from a legal settlement recognized in 2013. Excludes a $521 million loss on early extinguishment of debt during 2014. Excludes

acquisition-related bridge financing, transaction and integration costs in 2015 and 2016E (related to Omnicare and Target).

34

2016 Guidance: Strong Growth in Retail/LTC

Full-year 2016

Net Revenue Growth 14.25% to 15.5%

Same store sales 2.75% to 4.0%Same store salesSame store adjusted scripts

5% to 0%3.5% to 4.5%

Gross Profit Margin Significant declineg g

Operating Expense (% of revenue) Moderate improvement

Operating Profit Growth 6 25% to 8 25%Operating Profit GrowthOperating Profit Margin

6.25% to 8.25%Down 60 bps to 70 bps

Notes:1. Year-over-year growth based on midpoint of 2015 guidance.2. Same store sales and prescriptions exclude revenues from MinuteClinic®, and revenue and prescriptions from stores in Brazil, LTC operations and from

commercialization services.3 Same store adjusted scripts includes the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions This adjustment reflects3. Same store adjusted scripts includes the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions. This adjustment reflects

the fact that these prescriptions include approximately three times the amount of product days supplied compared to a normal 30-day prescription.4. Estimates assume that the acquisition of Target’s pharmacies and clinics closes at year-end 2015.5. Expectations exclude acquisition-related transaction and integration costs.

35

2016 Guidance: Even Stronger Growth in PBM

Full-year 2016

Net Revenue Growth 20.25% to 21.75%

Total Adjusted Claims 1.33 billion to 1.35 billion

Gross Profit Margin Moderate decline

Operating Expense (% of revenue) Modest improvementOperating Expense (% of revenue) Modest improvement

Operating Profit GrowthOperating Profit Margin

9.75% to 13.25%Down 25 bps to 35 bps

Notes:1 Year-over-year growth based on midpoint of 2015 guidance

Healthy enterprise growth in 2016

1. Year-over-year growth based on midpoint of 2015 guidance.2. Total adjusted claims includes the adjustment to convert 90-day, mail choice claims to the equivalent of three 30-day prescriptions. This adjustment reflects

the fact that these prescriptions include approximately three times the amount of product days supplied compared to a normal 30-day prescription.3. Expectations exclude acquisition-related transaction and integration costs.

36

Key Drivers of 2016 Expectations

• Reimbursement/pricing pressure andtiming of share gainstiming of share gains

• Growth in Specialty a plus

• Mix of business pressures margins

• Net benefit of Omnicare and Target assets

• Smaller incremental benefit from break-open generics

• Smaller incremental benefit from Red Oak Sourcing

37

Mix of Business Lowers Gross Margin %, but Drives Volumes and Gross Profit $ Over Time

• At enterprise level, lower-margin PBM segment is growing faster than Retail/LTC segment

Drives Volumes and Gross Profit $ Over Time

than Retail/LTC segment

• Multiple mix-driven impacts compressing underlying gross margins within underlying retail business:within underlying retail business:

– Pharmacy growth is expected to continue to outpace front store growth

– Medicare and Medicaid are becoming larger components of the patient g g p pmix; Lower margin rate and dollars per scripts, but higher margins per life due to higher utilization

– The mix of third party payors is also adversely changing in 2016y y y g g

38

Acquisitions Expected to Help Fuel Growth

• Omnicare expected to deliver ~20¢ to Adjusted EPS in 201619¢ i t ll ti– ~ 19¢ incrementally accretive year-over-year

– Includes associated financing and excludes amortization and integration expenses

• ~6¢ of Adjusted EPS dilution expected from Target in 2016– ~9¢ of dilution from reduced 2015 share repurchase and financing – ~3¢ of accretion from operation of assets, excluding amortization ¢ p g

and integration expenses– Pharmacies and clinics expected to be fully integrated and

rebranded within six to eight months– Significant purchasing synergies through Red Oak beginning in ‘16

• Fewer new store and clinic openings planned in 2016 as Target assets are integrated g

39

While the Level of Generic Introductions Ebbsand Flows Over Time …and Flows Over Time …

E t i fit thEnterprise profit growthwill continue to benefit

f ifrom generics

40

Generics Drive Financial Performance at CVS Health in Two WaysHealth in Two Ways

Brand-to-genericconversion

Increasingly effective sourcing of generics in CVS Health’s existing

base of business

41

Generics Remain an Opportunity1

Total Brand Market Sales of Expected Generic Launches($, billions)

16

23.9

17 3Abilify

16.5 17.3

Celebrex

Diovan

Nexium

Copaxone

Namenda

Crestor

Gleevec

5.53.6

Lovaza Zetia

Seroquel XRViagra

Cialis

2014 2015E 2016E 2017E 2018E

$26.4 billion Expected$40.4 billionNote:Note:1. 2014 includes all actual launches; 2015E forward includes all actual launches and only expected launches in total brand numbers whose annual sales exceed

$100M (key launches highlighted) and assumes 6 months pediatric extension on all launches. Forward-looking analysis assumes no “at risk” launches.Source: IMS Health; company estimates.

42

Incremental Break-open Benefit in 2016Less Than 2015

1

Less Than 2015

Total Brand Market Sales of Expected GenericLaunches in Break-open Periodp

($, billions)

8.7

14.4 15.5

11.1

5.0

2014 2015E 2016E 2017E 2018E

Notes:1. Break-open period for generic launches = 12 months from the point at which there are 3+ viable suppliers in the market (may span 2 calendar years), and

includes significant, “budgeted launch” products only. Brand market sales are at the time of first generic launch; break-open dates on the 15th or later were rounded to next full month; dates before the 15th credited for that monthrounded to next full month; dates before the 15th credited for that month.

2. 2014 includes all actual launches; 2015E forward includes all actual launches and only expected launches in total brand numbers whose annual sales exceed $100M and assumes 6 months pediatric extension on all launches. Forward-looking analysis assumes no “at risk” launches.

Source: IMS Health; company estimates.

43

Biosimilars Represent an AdditionalOpportunity

1

Opportunity

Total Market Sales($, billions)

19.5Total brand market sales ofexpected generic launchesin break open period

Total market sales of specialtydrugs losing exclusivity

8.7

14.4 15.5

11.1

in break-open period

5.0

Notes:1. Break-open period for generic launches = 12 months from the point at which there are 3+ viable suppliers in the market (may span 2 calendar years), and

includes significant, “budgeted launch” products only. Brand market sales are at the time of first generic launch; break-open dates on the 15th or later were rounded to next full month; dates before the 15th credited for that month

2016E – 2019E2014 2015E 2016E 2017E 2018E

rounded to next full month; dates before the 15th credited for that month.2. 2014 includes all actual launches; 2015E forward includes all actual launches and only expected launches in total brand numbers whose annual sales exceed

$100M and assumes 6 months pediatric extension on all launches. Forward-looking analysis assumes no “at risk” launches.Source: IMS Health; company estimates.

44

With Incremental Generic Benefits Declining, Biosimilars Will Become a Bigger Opportunity

1

• Biosimilars are expected to act more like brands than generics

Biosimilars Will Become a Bigger Opportunity

Total Market Sales of Specialty Drugs brands than generics

• Expected to increase competition in specialty categories 19.5

Losing Exclusivity($, billions)

• Expected to present opportunities for formulary strategies

– Lower cost for payors we support– Incremental margin opportunities for the

enterprise

Well-positioned to benefit from biosimilars

2016E – 2019E

45

Red Oak Sourcing to Add Smaller IncrementalValue in 2016 But Opportunity Remains

2

Venture with Cardinal Health continues to provide value to CVS Health in three ways:

Value in 2016 But Opportunity Remains

Venture with Cardinal Health continues toprovide value to CVS Health in three waysHealth in three ways:

• Fixed quarterly payments from Cardinal Health … $25.6 million per quarter

provide value to CVS Health in three ways

q– $75 million incremental benefit in 2015; neutral impact year-over-year

in 2016

• Additional milestone payments from Cardinal Health• Additional milestone payments from Cardinal Health– $20 million received in 2015; FY16 assumes $60 million

• Scale benefit from significantly higher combined volumes – Greatest marginal benefit recognized in 2014 and 2015 with initial bolus,

but opportunity remains

46

Combined Procurement Has Grown 50%Since Inception of Red Oak Sourcing

2

Relative Dollar Amount of Generics Procured Using Red Oak

Since Inception of Red Oak Sourcing

• Red Oak is the largest generic sourcing entity in the U Ssourcing entity in the U.S.

• Generic volumes sourced by Red Oak continue to grow

~50%

A i iti• Scale matters … incremental

value continues to be derived from additional volume Red Oak

Acquisitions

CardinalHealth

YE 2013 YE 2015

• More sophisticated procurement

• Introduce competition in f

CVSHealth

moleculesIncreasingly effective generic sourcing will add incremental value

Notes:1 Underlying data is not adjusted for any market activity (e g generic launches generic break opens)

proforma

47

1. Underlying data is not adjusted for any market activity (e.g., generic launches, generic break opens).2. Acquisitions include the generic volumes of Omnicare, the Target pharmacies and Cardinal Health’s acquisition of Harvard Drug Group before accounting for

any synergies derived from being added to Red Oak Sourcing.Source: CVS Health and Red Oak Sourcing estimates.

2016 Earnings Growth Significantly Back-half WeightedWeighted

EARNINGS GROWTHEARNINGS GROWTH

TIMING FACTORS

L dGeneric introductions / break-opens

TIMING FACTORSTIMING FACTORS

Leap day

Easter Shift benefits Q1to the detriment of Q2

Medicare Part D

Front store strategies’ benefits

Share repurchases

Tax rate

1st

2nd

Half

1Half

48

2016 Q1 Guidance: Challenging EPS Growth Due to Timing FactorsTiming Factors

Q1 2016

Net Revenue Growth 17% to 18.5%

Adjusted EPSYear-over-year Growth

$1.14 to $1.17Flat to up 3.0%p

GAAP Diluted EPS $1.03 to $1.06

Notes:Notes:1. EPS estimates exclude acquisition-related transaction and integration costs.2. Estimates assume that the acquisition of Target’s pharmacies and clinics closes at year-end 2015.3. EPS estimates assume completion of approximately $4 billion in share repurchases during full-year 2016.

49

Agenda

Strong Record of ExecutionStrong Record of Execution

Marketplace MisconceptionsMarketplace Misconceptions

Looking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise Growth

Looking Ahead: 2016 Guidance Review

Driving Sustainable Enterprise GrowthDriving Sustainable Enterprise GrowthDriving Sustainable Enterprise Growth

50

Steady State Targets Affirmed

Five-year CAGR (2013-2018)

Net Revenue Growth 9% to 13%

Operating Profit Growth 7% to 9%Operating Profit Growth 7% to 9%

Preliminary Adjusted EPS Growth 6% to 8%

Average Annual Cash Available for Enhancing Shareholder Value Approximately $8 billion

Share Repurchase Contribution 4% to 6%Share Repurchase Contribution 4% to 6%

Final Adjusted EPS Growth 10% to 14%

51

Capital Allocation Priorities Guide Use of Cash

Operational InvestmentsOrganic Growth• Store growth and remodelsp Sto e g o t a d e ode s• Continued technology improvements

Capital StructureMaintain capital structure• Credit rating of BBB+

G l f 2 7X Adj t d D bt t EBITDA• Goal of 2.7X Adjusted Debt-to-EBITDA

Capital Returned to

Dividends• 18% target CAGR 2014 through 2018• 35% target payout ratio by the end of 2018Capital Returned to

Shareholders35% target payout ratio by the end of 2018

Repurchase stock• Take advantage of share valuation, absent more attractive

alternatives

External Investment ‘Bolt-on’ acquisitions in core businesses• Minimum risk-adjusted return hurdle in mid teens

52

Many Initiatives You’ll Hear About Today to Continue to Drive Enterprise Profit GrowthContinue to Drive Enterprise Profit Growth

Health plans represent significant opportunity to drive valueand capture share, whether or not we’re the PBM

Our specialty business has unmatched assetsand continues to outpace the market

Target and Omnicare acquisitions enable pharmacyTarget and Omnicare acquisitions enable pharmacyshare gains

Near-term opportunities to gain retail share frommarket disruptionmarket disruption

Low-cost provider status expected to help drive share

Strategic acquisitions will continue to supplement growth

Opportunities remain within generics, Red OakSourcing and biosimilars

53

Strategic acquisitions will continue to supplement growth

The Right Strategy for an Evolving Health Care Market

Capturing significant share of new prescriptionsDemonstrating ValueAbility to pivot and provide value as market evolvesto People, Payors and Providers

Driving business decisions with enterprise mindsetGrowing the Core, Acquisitions delivering growth into new channels

g ,Broadening the Base

Best positioned to grow with unique assetsAlways Looking Best positioned to grow with unique assets

Growth algorithm remains strongAlways Looking

Ahead

Solid long-term growth targets and substantial cash

Optimizing capital allocation to drive shareholder valueDriving Sustainable Enterprise Growth

Maximizing Long-term Shareholder Value

Appendixpp

, CVS Caremark, Omnicare, CVS/specialty, CVS/caremark, CVS, Maintenance Choice, Coram, Navarro, Novologix, Omnicare, and Specialty Connect are trademarks or registered trademarks of CVS Pharmacy, Inc.

2016 Guidance: Consolidated Income Statement

Full-year 2016

Corporate Segment Expense $860 million to $870 million

Intercompany Eliminations(% f bi d t ) ~ 11.6%(% of combined segment revenues)

Gross Profit Margin Significant decline

Operating ExpenseOperating Expense(% of consolidated revenue) Moderate improvement

Operating Profit Margin Down 40 bps to 50 bps

Notes:1. Year-over-year growth based on midpoint of 2015 guidance.2. Expectations exclude acquisition-related transaction and integration costs.

56

2016 Guidance: Consolidated Income Statement

Full-year 2016

Net Interest Expense $1.13 billion to $1.14 billion

Effective Tax Rate ~ 39.0%

Weighted Average Shares ~ 1.08 billion

Consolidated Amortization ~ $800 millionConsolidated Amortization ~ $800 million

Consolidated Depreciation & Amortization ~ $2.5 billion

Notes:Notes:1. EPS estimates assume completion of approximately $4 billion in share repurchases in 2016. Timing of repurchases are expected to be weighted more in the

first half of the year rather than the second half.2. Expectations exclude acquisition-related transaction and integration costs.

57

2016 Q1 Guidance: Segment Performance Reflects Impact of Timing FactorsImpact of Timing Factors

Q1 2016

l/LTC

Net Revenue Growth 19% to 20.5%

Same store sales 4.5% to 6.0%

Ret

ai Same store adjusted scripts 4.75% to 5.75%

Operating Profit Growth 5.0% to 7.0%

arm

acy

rvic

es Net Revenue Growth 18% to 19.25%

Pha

Se Operating Profit Growth Flat to up 4.0%Notes:1. Same store sales and prescriptions exclude revenues from MinuteClinic, and revenue and prescriptions from stores in Brazil, LTC operations and from

commercialization services.2 Same store adjusted scripts includes the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions This adjustment reflects2. Same store adjusted scripts includes the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions. This adjustment reflects

the fact that these prescriptions include approximately three times the amount of product days supplied compared to a normal 30-day prescription.3. Estimates assume that the acquisition of Target’s pharmacies and clinics closes at year-end 2015.4. Operating profit growth estimates exclude acquisition-related transaction and integration costs.

58

Steady State Targets:Key Assumptions to Keep in MindKey Assumptions to Keep in Mind

Anticipated Impact

F bl i d t d hi Utili tiFavorable industry demographics Utilization

Generic pipeline Gross margin

Utilize compelling scale Gross marginUtilize compelling scale Gross margin

Retail share gains / SG&A leverage Operating profit

Net-new PBM contracts Mix/volume/livesNet new PBM contracts Mix/volume/lives

Innovative products and technology Volume/lives

High-return, bolt-on acquisitions Operating profitHigh return, bolt on acquisitions Operating profit

Increased compliance requirements / regulations Gross margin

Pharmacy pricing / reimbursement trends Gross margin

59

Driving EnterpriseDriving Enterprise Growth in an Evolving Health Care Market

Larry MerloPresident &Chi f E ti OffiChief Executive Officer

Agenda

Our Compelling Value PropositionOur Compelling Value PropositionOur Compelling Value PropositionOur Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

2

The Most Extensive Suite of Leading Assets …

Retail MailMailLong-term

CareRetailClinics

Specialty

Infusion

Clinics

Clinical Programs

Patients Medical Claims

Digital

g

Payors ProvidersClaims Editing

… enabling us to help deliver superior outcomes at a lower cost

3

Continue to Build One-of-a-kind Health Care Company with Unmatched Integrated AssetsCompany with Unmatched Integrated Assets

: Our Competitive Edge

Only company with the ability to impact patients, payors and providers with innovative, channel-agnostic solutions

Broadest capabilities to holistically manage patients inBroadest capabilities to holistically manage patients infast-growing specialty market

Unparalleled scale in the U.S. makes us a low-cost provider

Largest retail clinic operator in U.S. with 28 million patient visits to date

D li i l ti d i i ht th t iDeep clinical expertise and insights across the enterpriseenable us to help deliver superior outcomes at a lower cost

Leading provider of pharmacy services in long-term care

4

g p p y g

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5~710Mnew Rx

4.8

2010 2015E

5

Note:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5 CVS Healthshare of

market growth275M

~710Mnew Rx

4.8

market growth

39%

2010 2015E

Gaining share in a growing Rx industry

6

Note:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

Prescription Growth Through Enterprise Channels Demonstrates Power of Unique, Integrated Model …Demonstrates Power of Unique, Integrated Model …

CVS/caremark Claims(Rx, millions)

9051,080 ~1,165

740905 Channel agnostic

offerings allow us to capture growth in

CVS/caremark claims

275 365 445 470

CVS/caremark claims while helping to drive

client savings

Notes:

2008 2011 2014 2015ECVS Health dispensed All other

Notes:1. CVS Health dispensed prescriptions include CVS/pharmacy, mail, CVS/specialty and Omnicare prescriptions across all years.2. CVS retail and mail prescriptions on a 30-day equivalent basis.3. 2015E is midpoint of guidance range.

7

… and Has Allowed Us to Capture 700 bps of Revenue Share, Equating to $7 BillionRevenue Share, Equating to $7 Billion

CVS/caremark Revenue($, billions)

70088

~100

$7

700 bpsincrease

=4459

$7 Billion

2008 2011 2014 2015E

48% 50% 53% 55%

Notes:

CVS Health share All other

Our outperformance in specialty is a key driver of revenue share gainsNotes:1. CVS Health share of CVS/caremark revenue equals CVS/caremark revenue dispensed through Enterprise channels (CVS/pharmacy, mail, CVS/specialty,

Omnicare) ÷ total CVS/caremark revenue.2. 2015E is midpoint of guidance range.

8

Agenda

Our Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Our Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

9

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

10

Health Reform and Demographics Expanding Insured Population

1

Insured Population

Growth in U.S. Insured Lives(lives, millions)

1419 35286

306Individuals/Exchanges264

49 53 62

53 63 6514

Medicaid

Medicare

148 151 143 Employer-sponsored

2013 2015E 2019E

Medicare and Exchanges will be primary drivers

11

Source: CVS Health Internal Analysis; Medicare Trustees Report, 2015; Avalere Medicaid Model, September 2015; McKinsey MPACT 6.2, September 2014; CBO Public Exchange Estimates, March 2015; Accenture, 2015; Congressional Budget Office. Model assumes no additional Medicaid expansion in the 20 non-expansion states, further Medicaid expansion could improve long-term covered lives outlook. Figures may not foot due to rounding.

Aging U.S. Population Will Drive Prescription Utilization …

1

Utilization …

U.S. Population Aged 65+(lives, millions)

Retail Prescription Utilizationby Age Group

65.9

y g p(Rx per member per year)

+18Mlives

47.8

56.4 36.665+

16.219-64

2015E 2020E 2025E

4.10-18

Sources:1. U.S. Census Bureau.2. Utilization based on CVS/caremark book of business; all prescriptions on a 30-day equivalent basis; excludes Aetna.

12

… and Fuel Growth in Prescription Expenditures 1

U.S. Prescription Drug Expenditures($, billions)

464

5646.2%CAGR

328385

464

2015E 2018E 2021E 2024E

13

Source: CMS, Office of the Actuary, Prescription Drug Expenditures (figures as of July 30, 2015).

Pharmacy Is One of the Most Cost-efficient Ways to Manage Overall Health Care Costs

1

Ways to Manage Overall Health Care Costs

Healthcare Savings from Improved Adherence(PMPY)

Hyperlipidemia Diabetes Hypertension

$5,883 $5,676ROI9X ROI

9X

$3,311ROI5.5X

9X

($601) ($656) ($629)Added Rx spend Medical and productivity savings

14

Source: Roebuck MC, Liberman JN, Gemmill-Toyama M, Brennan TA. Medication adherence leads to lower health care use and costs despite increased drug spending. Health Affairs. 2011;30(1):91-99. Carls GS, Roebuck MC, Brennan TA, Slezak JA, Matlin OS, Gibson TB. Impact of medication adherence on worker productivity: an instrumental variables analysis in five chronic diseases. JOEM, 2012. Cholesterol savings from generic medications only.

CVS Health Can More Broadly Reach Patients Across the Continuum of Care

1

Across the Continuum of Care

CVS Health Standalone StandaloneCVS Health Retailer PBM

Retail pharmacy

Mail Order

Specialty/Infusion

LTC pharmacy

Retail clinics

Clinical programs

Channel connectivity

15

Growth in U.S. Population Over 85 Underscores Need for Long-term Care

1

Need for Long term Care

U.S. Population Aged 85+(lives, millions)

Omnicare is a leading pharmacy services provider to LTC facilities

11.9

• Nationwide footprint with leading positions in Assisted Living and Skilled Nursing facilities

~2X

6 37.5

g

• Ability to leverage clinical insights to improve care for patients

• CVS Health brings capabilities to6.3 CVS Health brings capabilities to better serve patients across the continuum of care

2015E 2025E 2035E

Source: U.S. Census Bureau.

16

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

17

Specialty Growth Will Be Primary Driver of Pharmacy Trend

2

Pharmacy Trend

Addressable Specialty Industry($, billions)

22014%CAGR

130

65

2012 2016E 2020E

18

Note:1. Addressable specialty industry currently excludes infused oncology.Source: NHE, Artemetrx, CVS Health Internal Analysis, 2015.

We Are Well-positioned as the Largest and Fastest-growing Specialty Pharmacy in the U.S. …

2

Fastest growing Specialty Pharmacy in the U.S. …

CVS Health Specialty Revenue($, billions)

4927%

40

30

CAGR

2219

2012 2013 2014 2015E 2016EDispensed Managed ACS (Omnicare)

19

.Source: CVS Health Internal Analysis. Does not include specialty revenue from Target pharmacies.

… with the Broadest Capabilities to Manage Trend and Improve Care

2

• Formulary strategies offer drug exclusions, step therapy and new-to-market control

Trend and Improve Care

FormularySolutions

• Exclusive Choice network can help reduce trend and drive incremental savings

and new-to-market controlSolutions

NetworkDesign

H lt t it i f i i

• Cost-effective, clinically-appropriate therapy solutions for each patient

Utilization Management

Sit f • Home or alternate-site infusion services can dramatically lower costs

• Novologix platform enables editing and re-pricing for

Site-of-careManagement

Medical Claims medical pharmacy claimsClaimsEditing

• Certified nurse case managers provide clinical supportCareCoordination

20

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

21

Retailization of Health Care Continues with Growth in Consumer-directed Health Plans

3

Growth in Consumer directed Health Plans

CDHP Enrollment(lives, millions) Drivers of Trend

• Employers looking to CDHPsto help control mounting health care costs

30 5

37.525%

− Employees have accountability in their health care decision-making

• Growth in CDHPs also driven by 22.0

30.5CAGR

health insurance choosers on the exchanges

6.1

12.5

2006 2008 2010 2012 2014

22

Sources: AIS’s Inside Consumer Directed Care; Kaiser; AHIP surveys.

Promoting Healthy Behavior Is Critical in Avoiding Unintended Consequences with CDHPs

3

As Patient Cost Share Rises…

Avoiding Unintended Consequences with CDHPs

CVS Health Advantages

More than 9,500 convenient locations

Costsustaining adherence CVS/minuteclinic

Innovative plan design options

Cost… sustaining adherence becomes more challenging

… patients may choose to cut th i h lth d

Unique programs: Pharmacy Advisor

Trusted brandAdherence

corners on their health andwellness needs to avoid costs

CVS Health is best-positioned to meet consumer needs

Trusted brand

23

Note:1. Retail pharmacy locations include more than 1,660 Target locations.

Example: Reduced Co-pay for Key Maintenance Medications Improves Adherence in CDHPs

3

Medications Improves Adherence in CDHPs

Member Adherence to Prescribed Hyperlipidemia Medication

82%

+130bps

Initiators Continuers

80% 82%+560bps

57%63%

Notes:1 Initiators defined as patients starting therapy during study period Continuers defined as patients on therapy before study period

With preventative drug listWithout preventative drug list

24

1. Initiators defined as patients starting therapy during study period. Continuers defined as patients on therapy before study period.2. Member adherence defined as average monthly proportion of days covered (PDC).Source: CVS/caremark Enterprise Analytics: Study of CDHP Design Impact on Utilization and Medication Adherence, 2014. Study based on subset of CVS/caremark book of business.

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

25

Payment Models Continue to Evolve Away fromFee-for-service and Towards Value-based Payments

4

Fee for service and Towards Value based Payments

Medicare Reimbursement by Payment Model

52%33%

18%34%

52%

Two-thirds in alternative

30% 33%

2015E 2018E

alternative models

Medicare Advantage Value-based FFS Volume-based FFS

By 2018, two-thirds of Medicare payments in alternative models

26

Source: Burwell S. Setting Value-Based Payment Goals – HHS Efforts to Improve U.S. Health Care. The New England Journal of Medicine. 2015; 372:897-899.

Public and Private Payors Taking Steps to Managing Outcomes and Total Cost of Care

4

Managing Outcomes and Total Cost of Care

Medicaremandatory bundles

for hips/knees

Largest health systems pledge to move

75% of business intovalue-based arrangements

2016 2017 2020

Medicare Part D Enhanced MTM modelEnhanced MTM model

Sources:

27

Sources:1. HHS, CMS finalizes bundled payment initiative for hip and knee replacements, November 2015.2. CMS, CMS announces Part D Enhanced Medication Therapy Management Model, September 2015.3. Health Care Transformation Task Force, Major Health Care Players Unite to Accelerate Transformation of US Health Care System, January 2015.

CVS Health Can Support Health Systems Across the Payment Continuum

4

the Payment Continuum

Evolving Contracting ArrangementsBirmingham, Sacramento,CAEvolving Contracting Arrangements

AL CA

Fee for Service(FFS)

FFS with Pay for

Performance

Bundled Payments

Shared Savings

Shared Risk

Global Capitation

28

Full Range of Tools and Services to Support Differentiated Needs of Providers

4

Health Hospital

Differentiated Needs of Providers

CVS/minuteclinic Engagement Engine

Hospital Transitions

Complementary health Powerful analytics Assisting patients to

Epic EMR

Enhanced connectivityComplementary health care services

Wellness and chronic care support

Powerful analytics capabilities

Essential in helping manage population health

Assisting patients to avoid adherence lapses

Enhanced care coordination

Enhanced connectivity to the health care system

>60% of Americans have Epic recordp

Well-positioned to excel regardless of how market evolves

29

CVS Health Best-in-class Tools to Drive Adherence 4

Medication Possession RatioDi b t Ch l t l H t i

83 84

DiabetesTherapy

CholesterolTherapy

HypertensionTherapy

+580bps

+650bps

73

77 7880+700

bps

bps

73

Top 3 Retail

CVS/pharmacy

Top 3 Retail

Top 3 Retail

CVS/pharmacy

CVS/pharmacy

Adherence for these common conditions can drive Star ratings

30

Note:1. Adherence measured by Medication Possession Ratio, calculated as total days supply divided by total days in evaluation period.Source: CVS Health Internal Analysis, based on rolling 12 month period: November 2014 to October 2015.

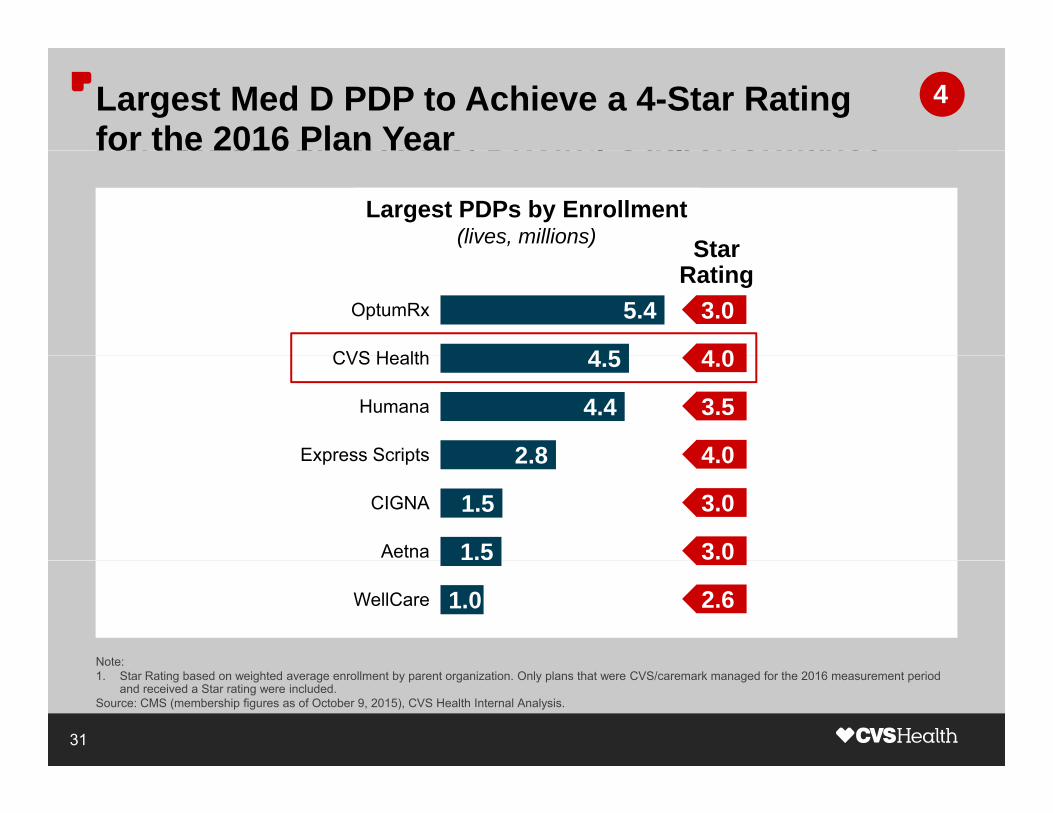

CVS Health Can Directly Impact a Significant Portion of Star Metrics, Driving Outperformance Largest Med D PDP to Achieve a 4-Star Rating for the 2016 Plan Year

4

Portion of Star Metrics, Driving Outperformance

Largest PDPs by Enrollment(lives, millions) Star

for the 2016 Plan Year

4 5

5.4

CVS Health

OptumRx 3.0

4 0

Star Rating

2 8

4.4

4.5

Express Scripts

Humana

CVS Health 4.0

3.5

4 0

1.5

1.5

2.8

Aetna

CIGNA

Express Scripts 4.0

3.0

3.0

1.0WellCare 2.6

Note:

31

Note:1. Star Rating based on weighted average enrollment by parent organization. Only plans that were CVS/caremark managed for the 2016 measurement period

and received a Star rating were included.Source: CMS (membership figures as of October 9, 2015), CVS Health Internal Analysis.

CVS Health Can Directly Impact a Significant Portion of Star Metrics, Driving Outperformance

4

Portion of Star Metrics, Driving Outperformance

Largest PDPs by Enrollment(lives, millions) Star

SilverScript is excelling…

O l PDP ith 50% l

4 5

5.4

CVS Health

OptumRx 3.0

4 0

Star Rating • Only PDP with >50% low-

income-subsidy lives to achieve 4 Star rating

2 8

4.4

4.5

Express Scripts

Humana

CVS Health 4.0

3.5

4 0

And we’re helping clients achieve their goals…

• Ability to directly impact more

1.5

1.5

2.8

Aetna

CIGNA

Express Scripts 4.0

3.0

3.0

y y pthan 80% of Med D and 55% of MAPD Star metrics

• Client lives in high performing

1.0WellCare 2.6

Note:

g p gplans: 73% vs. 49% for the overall market

32

Note:1. Star Rating based on weighted average enrollment by parent organization. Only plans that were CVS/caremark managed for the 2016 measurement period

and received a Star rating were included.Source: CMS (membership figures as of October 9, 2015), CVS Health Internal Analysis.

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

33

We Can Partner with Health Plans in a Multitudeof Ways to Drive Value

5

of Ways to Drive Value

Strong procurement Broad service Pharmacy is Unique ability procurement

capabilities and claims scale

makes

portfolio to support plan

needs whether or not we are

your focus and a

key lever for managing

overall health

q yto leverage consumer insights

to improveus a low-cost provider

or not we are the PBM

overall health costs

to improvecare

34

After Consolidation, Regional and Blues Plans Will Still Manage More Than Half of Total Lives

5

Will Still Manage More Than Half of Total Lives

AetnaAetnaHumana

Nationals Nationals Anthem 46%Cigna

Anthem

UnitedUnited

RegionalsRegionals

54%BluesBlues

35

Future MarketMarket Today

We Dispense 8X to 11X the Prescription Volume of the Proposed Combinations …

5

Volume of the Proposed Combinations …

2015 Estimated Rx Volume(Rx dispensed, millions) CVS Health Advantages

1,350• Generic purchasing scale makes

us a low-cost provider

Scale is further enhanced by Red• Scale is further enhanced by Red Oak sourcing

~8X ~11X

170 120

CVS Aetna AnthemCVS Health

Aetna Humana

Anthem Cigna

Notes:

36

Notes:1. Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark.2. Estimated dispensed Rx also displayed on a pro forma basis to include full year 2015 Dispensed Rx volume from Omnicare and Target.Source: CVS Health Internal Analysis, Company disclosures. All prescriptions dispensed on a 30-day equivalent basis.

… and We Manage 2X to 3X the Claims Volume of the Proposed Combinations

5

Volume of the Proposed Combinations

CVS Health Advantages2015 Estimated Claims Volume

(Rx managed, millions)

1,165

2X

• Substantial managed claims volume supports negotiations for rebates / formulary placement

600480

~2X ~3X • Creates value as majority of rebates are passed to clients

CVS / Aetna AnthemCVS / caremark

Aetna Humana

Anthem Cigna

37

Note:1. Estimated managed claims include all CVS/caremark network claims plus specialty and adjusted mail claims.Source: CVS Health Internal Analysis, Company disclosures. CVS/caremark claims represent midpoint of guidance range.

We Dispense 8X to 11X and Manage 2X to 3X the Volumes of the Proposed Combinations

5

Volumes of the Proposed Combinations

2015 Estimated Rx Volume(Rx dispensed, millions)

2015 Estimated Claims Volume(Rx managed, millions)

1,350 1,165

2X

~8X ~11X 600480

~2X ~3X

170 120

CVS Aetna Anthem CVS / Aetna Anthem

Note: Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark Dispensed Rx also

CVS Health

Aetna Humana

Anthem Cigna

CVS / caremark

Aetna Humana

Anthem Cigna

Scale is critical to being a low-cost provider

38

Note: Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark. Dispensed Rx also displayed on a pro forma basis to include full year 2015 Dispensed Rx volume from Omnicare and Target. Estimated dispensed prescriptions on a 30-day equivalent basis. Estimated managed claims include all CVS/caremark network claims plus specialty and adjusted mail claims.Source: CVS Health Internal Analysis, Company disclosures. CVS claims represent midpoint of guidance range.

Agenda

Our Compelling Value Proposition

Evolving Health Care Market Creates Opportunities

Our Compelling Value Proposition

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

Evolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

39

Our Strategic Business Imperatives

AggregateLives

GrowShare

Execute with Excellence

DriveInnovation

Enterprise Focus

Grow the core, Broaden the base

40

Our Strategy for Long-term Enterprise Growth

5Opportunistic bolt-on acquisitions4

5

Continued innovation in drug procurement and supply chain efficiencies3

Enhance patient engagement

Deepen relationships with payors and providers

2Deepen relationships with payors and providers to help reduce cost and improve outcomes

Add capabilities to enhance core business

1

41

p

Today’s Key Takeaways

The Right Strategy for an Evolving Health Care MarketThe Right Strategy for an Evolving Health Care Market

Leadership in multiple competencies to drive superior l f h lth t

Demonstrating Valuevalue for health care partnersto People, Payors and Providers

Expanding core pharmacy business while broadening Growing the Core, p g p y greach into new health care channels

g ,Broadening the Base

I t d i i ti d t d ki l tAlways Looking Introducing innovative products and making long-term, value-enhancing investments

Always Looking Ahead

Driving shareholder value with strong earnings and cash flow as well as disciplined capital allocation

Driving Sustainable Enterprise Growth

Driving Enterprise Growth in an Evolving Health Care Market

Endnote

1. , Omnicare, CVS/caremark, CVS/pharmacy, CVS Health, CVS/specialty, CVS/minuteclinic, and Health Engagement Engine are trademarks or registered trademarks of CVS Pharmacy, Inc.

43

Delivering Value Today,Delivering Value Today, Ensuring Growth for Tomorrow

Jon RobertsExecutive Vice President & President CVS/caremarkPresident, CVS/caremark

Agenda

Demonstrating Value: PBM P f Hi hli htDemonstrating Value: PBM Performance HighlightsPBM Performance Highlights

Addressing Clients’ Top Concern: CostAddressing Clients Top Concern: Cost

Ensuring Growth: Our Integrated Model and the E l i H lth C M k tEvolving Health Care Market

2

Continued Strong PBM Performance

Net Revenue($, billions)

Operating Profit($, billions)

121.515.6%CAGR

3.5

4.415.0%CAGR

58.9

88.4

2.2

3.5

2011 2014 2016E 2011 2014 2016E

3

Note:1. 2016E based on midpoint of 2016 guidance.

Another Successful Selling Season: Gross New Business Wins of $13.5 Billion for 2016Gross New Business Wins of $13.5 Billion for 2016

13 5B13.5BIN NEW

$11.2B$1.8B

BUSINESS WINS

St t f

State of Oklahoma

Government & Union

Employer

State of Illinois Health Plan

4

EmployerNotes:1. As of 12/04/2015.2. Gross wins exclude Medicare Part D SilverScript individual products.

Net New Client Business of $11.5 Billion for 2016with 98% Retentionwith 98% Retention

Revenues($, billions) 60% of client

l13.5 0.8

0.4

non-renewals due to acquisition

and retirees

11.5

0.8

Business Not Renewed

Gross New B i

Acquired Moved to Exchange (P i il R ti )

Competitive / Oth

Net New Business

Expect another highly successful welcome season

Business (Primarily Retirees) / Other

5

Notes:1. As of 12/04/2015.2. Gross wins exclude Medicare Part D SilverScript individual products.

Gross New Business Creates Share Gain Opportunity

ENTERPRISE SHAREGROSS WINS BY CHANNEL

54%$0.6B Mail Choice

data28%

22%$1.8B SpecialtySpecialty

$11.1BExisting

Health PlanExisting

EmployerNew

Business

$RetailNetworks

6

Notes:1. Enterprise share represents the percent of Rx volume dispensed through a CVS Health enterprise channel (Mail, Specialty, Retail).2. All claims on a 30-day equivalent basis.

Client Priorities: Prescription Drug Cost Top Concern Across SegmentsTop Concern Across Segments

AVOIDINGDISRUPTION

MEDICARE EXPERTISE

MEMBERSERVICE

UTILIZATION& CLINICALPROGRAMS

CLIENT SERVICE

PRESCRIPTION DRUG COST

LEVEL OF IMPORTANCE

7

Our Model Provides Flexibility to Address Client Priorities dd ess C e t o t es

EmployersEmployers

AVOIDINGDISRUPTION

MEDICARE EXPERTISE

MEMBERSERVICE

UTILIZATION& CLINICALPROGRAMS

CLIENT SERVICE

PRESCRIPTION DRUG COST

LEVEL OF IMPORTANCE

8

Our Model Provides Flexibility to Address Client Priorities dd ess C e t o t es

Health PlansHealth Plans

AVOIDINGDISRUPTION

MEMBERSERVICE

CLIENT SERVICE

PRESCRIPTION DRUG COST

UTILIZATION& CLINICALPROGRAMS

MEDICARE EXPERTISE

LEVEL OF IMPORTANCE

9

Our Model Provides Flexibility to Address Client Priorities Address Client Priorities

MedicareMedicare

AVOIDINGDISRUPTION

MEMBERSERVICE

CLIENT SERVICE

PRESCRIPTION DRUG COST

MEDICARE EXPERTISE

UTILIZATION& CLINICALPROGRAMS

LEVEL OF IMPORTANCE

10

Multi-segment PBM Market Demands Flexibility

Employers Government Health p yand Unions Plans

Expertise, flexibility and proven performance support our continued growth

11

Delivering on Client Priorities: Clients and Members Highly Satisfied with ServiceClients and Members Highly Satisfied with Service

2015 Member Satisfaction2015 Client Satisfaction

96% 95%

CVS/caremark scored highest in overall customer satisfaction in 2015 PBMI Survey

12

in 2015 PBMI SurveySource: PBMI 2015 Pharmacy Benefit Management Customer Satisfaction Report; PBMs with >20M members.

Delivering on Client Priorities: Medicare

A t i l / bid f l

Consultative Services

Progressive and

Competitiveness

Actuarial / bid, formulary and plan

design support

Progressive and integrated strategies to

help manage trend

ComplianceStar Ratings

MEDICARE HEALTH

PLAN

p

Robust compliance support for complex

g

73% of client lives are 4 to 5 Star plans

regulatory environmentp

13

Note:1. Star ratings for 2016 based on internal analysis of CMS data released October 2015. Star rating based on weighted average enrollment by parent

organization. Only plans that were CVS/caremark managed for the 2016 measurement period and received a Star rating were included.

Delivering on Client Priorities: Clinical Programs

ROBUST UTILIZATION PROGRAMS

6% savings for medical

MEDICATION RECONCILIATION

48% reduction in hospital 6% savings for medical and pharmacy benefits from specialty utilization management

preadmissions; $3,300 savings per patient counseled

PHARMACY ADVISORSPECIALTY CARE

MANAGEMENT NURSE

Pharmacist counseling:4% increase in adherence; 7.5% reduction in gaps in care

Enhanced outreach: 60% engagement rate; reduce hospitalizationsby 23%in care by 23%

Note:1. Savings quoted may vary based on various factors including things such as plan design, programs adopted and demographics.Sources:Pharmacy Advisor : CVS/caremark internal data 2013 Medication Reconciliation: CVS/caremark sample study 2014 Robust UM (integrated PA)

14

Pharmacy Advisor : CVS/caremark internal data, 2013. Medication Reconciliation: CVS/caremark sample study, 2014. Robust UM (integrated PA) CVS/caremark Specialty Client Solutions and Trend Management, 2013, internal analyses for estimated program savings. Specialty engagement source: Accordant® - Comprehensive Data Warehouse; SQL Server 2008. Greensboro, NC: care management Health Services, a CVS/caremark Company; 2013www.hpminstitute.org/content/wellness-and-disease-management-podcast-industry-specialist-judy-mueller.

Agenda

Demonstrating Value: PBM P f Hi hli ht

Addressing Clients’ Top Concern: Cost

PBM Performance Highlights

Addressing Clients’ Top Concern: CostAddressing Clients Top Concern: CostAddressing Clients Top Concern: Cost

Ensuring Growth: Our Integrated Model and the E l i H lth C M k tEvolving Health Care Market

15

Size and Scale Ensures Competitive Cost

Generic Purchasing

• Sourced through Red Oak, the largest generic sourcing entity in the U.S.

Formulary Management

• $6.4B in incremental client savings ‘12-’16E from our leading formulary management strategy

Specialty Pharmacy

• Largest specialty pharmacy; able to manage cost across pharmacy and medical benefit

Competitive Networks

• 1.34B adjusted claims estimated in 2016 through our multiple networks

Cost of Service

• Streamlining continues to deliver value as volume grows• Technology investments enable regulatory compliance

16

Note:1. 2016E based on midpoint of 2016 guidance.

Comprehensive Program Addresses 3 Possible Areas of Fraud, Waste and AbuseAreas of Fraud, Waste and Abuse

• Medication abuse / misuse

MEMBER

CVS/caremark provides:• Doctor shopping• Pharmacy shopping • Active and retrospective

claims monitoring• Review of high-riskPRESCRIBER Review of high risk

prescribing patterns• Robust network pharmacy

credentialing programPh di

PRESCRIBER

• Illegal or irresponsible prescribing

• Pharmacy audits• High- and low-touch

interventions

PHARMACY • Fraudulent billing • Inaccurate dispensing

For 2015, CVS/caremark pharmacy audits will lead to more than $240M in savings and recovery of incorrect improper or fraudulently-billed claims

• Drug diversion

savings and recovery of incorrect, improper or fraudulently-billed claims

17

Source: CVS/caremark internal data.

2014 Double-digit Pharmacy Trend: A Call to Action

IMPACT TO TREND1 0%

3.4%2.0%

1.0%

(5.9)%

2.1%1.5%

7.7%

11.8%

7.7%

Specialty Brand

Inflation

Utilization Hep C Compounds Generic Inflation

Drug MixNon-specialty

Brand Inflation

2014 Bookof Business

Trend

Note:1. Trend is net of rebates.Source: CVS Health Enterprise Analytics, Book of Business Trend Cohort.

18

RxInsights: Client-Specific Reporting on Trend Performance and Key Metricsy

EXECUTIVE SUMMARY

Note:1. Sample data, actual results may vary.

19

CVS HEALTH - COMPREHENSIVE SOLUTIONS TO MANAGE TRENDIDENTIFY EXPLORE MANAGE OPTIMIZEIDENTIFYEMERGINGTREND

EXPLOREROOT CAUSES

MANAGETHROUGHFORMULARY

OPTIMIZECHANNEL

Interactive RxInsightsIndividual classes are plotted below. The graph is showing the relationship between Cost and Contribution to Trend. Size represents the Cost/Days Supply for a given class.

3%

4%5%

CLASS ANALYSIS BY CONTRIBUTION

p g p g p p y pp y g

11.2%

TREND

RxInsights

-1%

0%

1%

2%RxInsights

Demo

$0 $1 $2 $3 $4 $5 $6 $7 $8-3%-2%

$

GROSS COST PMPM TREND

J 2014 M 2014 S t b 2014 J 2015 M 2015 S t b 2015

$80

$100

$120

©2015 CVS Health and/or one of itsJanuary 2014 May 2014 September 2014 January 2015 May 2015 September 2015 affiliates: Confidential and Proprietary

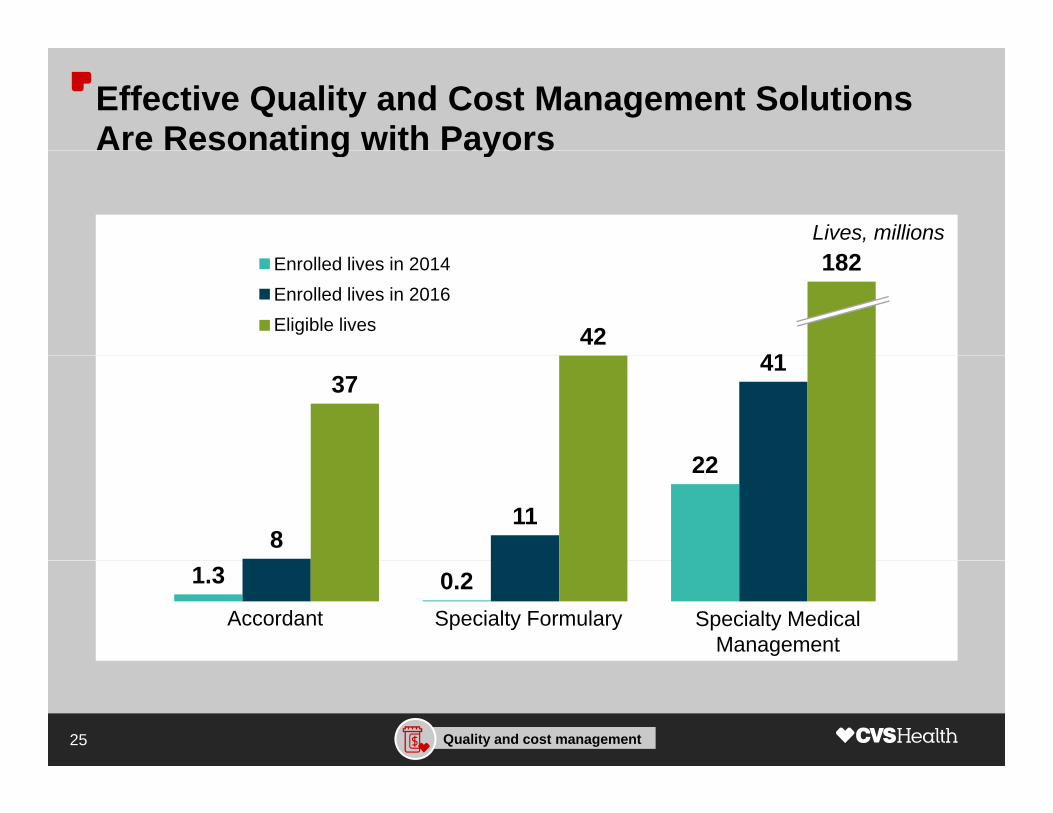

Strong Adoption of Key Cost Management Solutions … Meaningful Opportunity Remains… Meaningful Opportunity Remains

Current Lives Total LivesOpportunity Savings

TOTAL NETWORK

23MMAINTENANCE CHOICE Up to 4%44M

37M

25M

TOTAL NETWORK STRATEGIES

FORMULARY STRATEGIES

Up to 4%

Up to 12%

75M

53M

35M EXCLUSIVE SPECIALTY

STRATEGIES

Up to 7%50M

10M SPECIALTY MEDICAL MANAGEMENT Up to 13% 41M

Notes:1 Current Lives includes 2016 known enrollments

21

1. Current Lives includes 2016 known enrollments.2. Exclusive Specialty savings apply to specialty spend under the pharmacy benefit. 3. Specialty Medical Management opportunity based on Health Plan lives in PBM book of business; savings apply to specialty spend under the medical benefit.4. Savings results will vary based on a variety of factors including demographics, plan design and other programs implemented by the client.

Adoption of Our Plan Designs Helps Reduce Plan Costs While Growing Enterprise ShareCosts While Growing Enterprise Share

Enterprise Share Growth in a Multi-state Health Plan

31.3%11.4 ppincrease

19.9%

26.7%

2010 2013 2016E

Plan has implemented programs that reduce plan and member cost and grow enterprise shareand grow enterprise share

22

2014 Double-digit Pharmacy Trend: A Call to Action2015 Year-to-date Trend Summary

JAN THROUGH SEP COMMERCIAL TREND

2.3%1.6% (0.3)% (1.9)% 0.8%

(2.8)%6 7%

11.8%

6.7%6.4%

2014 Bookof Business

Trend

Specialty Brand

Inflation

Utilization Hep C Compounds Generic Inflation

Drug MixNon-specialty

Brand Inflation

2015 YTD Book of Business

Trend

Note:1. Trend is net of rebates.Source: CVS Health Enterprise Analytics, Book of Business Trend Cohort.

23

Agenda

Demonstrating Value: PBM P f Hi hli htPBM Performance Highlights

Addressing Clients’ Top Concern: CostAddressing Clients Top Concern: Cost

Ensuring Growth: Our Integrated Model and the E l i H lth C M k tEnsuring Growth: Our Integrated Model and the E l i H lth C M k tEvolving Health Care MarketEvolving Health Care Market

24

Driving Market Evolution: Government Programs Linking Payments to Quality

1 in 3 50% of traditional Medicare spending

g ay e ts to Qua ty

1 in 3 Americans are currently covered by government-sponsored health

50%

Medicare spending will be linked to quality incentives by 2018

% OF MEDICARE SPENDING TIED TO

QUALITY INCENTIVESpinsurance programs

$1 f $2 20%

QUALITY INCENTIVES

$1of every $2spent on health care goes through Medicare and M di id 2014 2018Medicaid 2014 2018

To succeed, payors and providers must align with CMS focus on quality

25

Notes:1. Health Affairs – National Health Expenditure Projections 2014-2024, July 2015.2. Modern Healthcare, January 26, 2015.