Embed Size (px)

Citation preview

The Right Strategy for anThe Right Strategy for an Evolving Health Care Market

Larry MerloyPresident & Chief Executive Officer

34th Annual J.P. Morgan Healthcare ConferenceJanuary 12, 2016

Forward-looking Statements

During today’s presentation, we will make forward-looking statementswithin the meaning of the federal securities laws. By their nature, allforward looking statements involve risks and uncertainties Actualforward-looking statements involve risks and uncertainties. Actualresults may differ materially from those contemplated by the forward-looking statements for a number of reasons as described in our SECfilings including the risk factors section and cautionary statementfilings, including the risk factors section and cautionary statementdisclosure in those filings.

During this presentation, we will also use some non-GAAP financialh t lki b t ’ f i l dimeasures when talking about our company’s performance, including

free cash flow, cash available to enhance shareholder value andAdjusted EPS. In accordance with SEC regulations, you can find thedefinitions of these non-GAAP items as well as reconciliations todefinitions of these non-GAAP items, as well as reconciliations tocomparable GAAP measures, on the investor relations portion of ourwebsite.

2

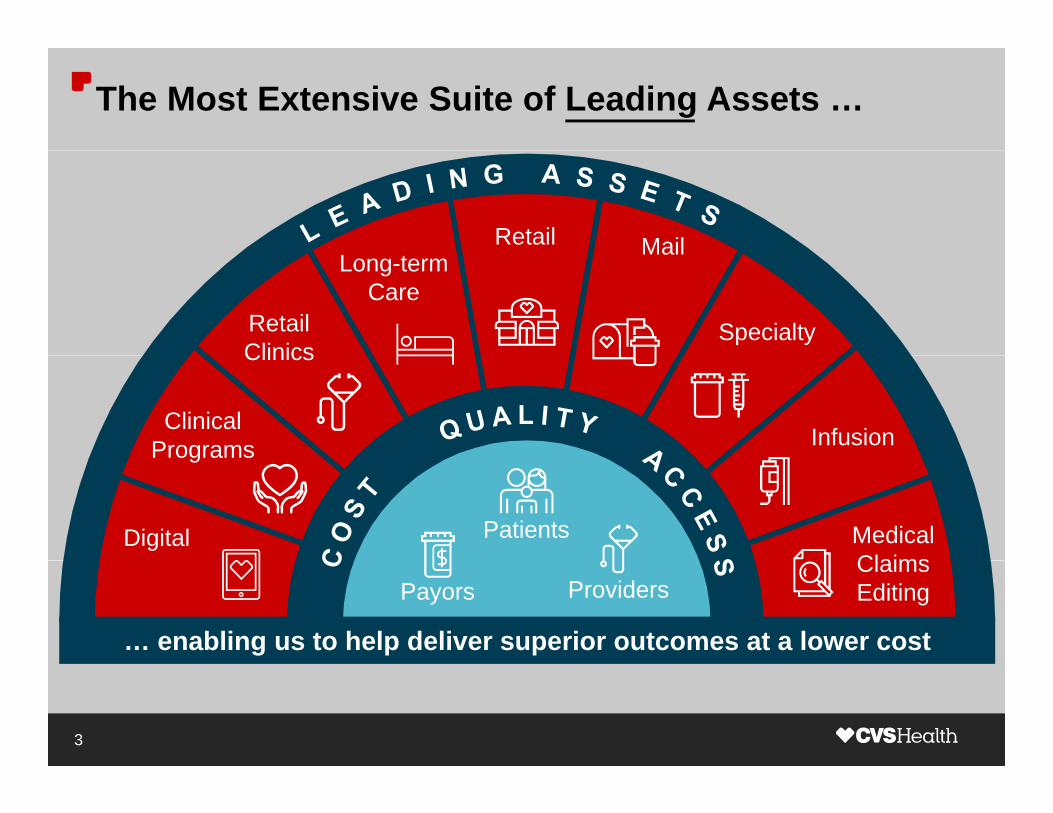

The Most Extensive Suite of Leading Assets …

Retail MailMailLong-term

CareRetailClinics

Specialty

Infusion

Clinics

Clinical Programs

Patients Medical Claims

Digital

g

Payors ProvidersClaims Editing

… enabling us to help deliver superior outcomes at a lower cost

3

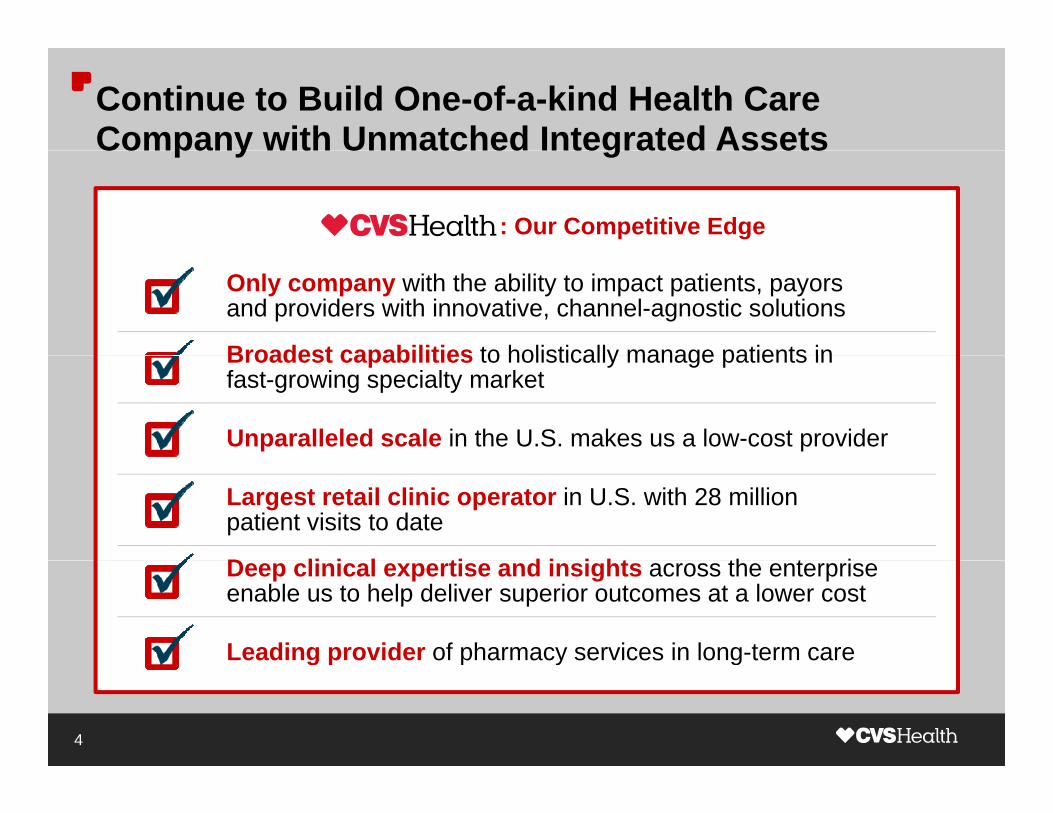

Continue to Build One-of-a-kind Health Care Company with Unmatched Integrated AssetsCompany with Unmatched Integrated Assets

: Our Competitive Edge

Only company with the ability to impact patients, payors and providers with innovative, channel-agnostic solutions

Broadest capabilities to holistically manage patients inBroadest capabilities to holistically manage patients infast-growing specialty market

Unparalleled scale in the U.S. makes us a low-cost provider

Largest retail clinic operator in U.S. with 28 million patient visits to date

D li i l ti d i i ht th t iDeep clinical expertise and insights across the enterpriseenable us to help deliver superior outcomes at a lower cost

Leading provider of pharmacy services in long-term care

4

g p p y g

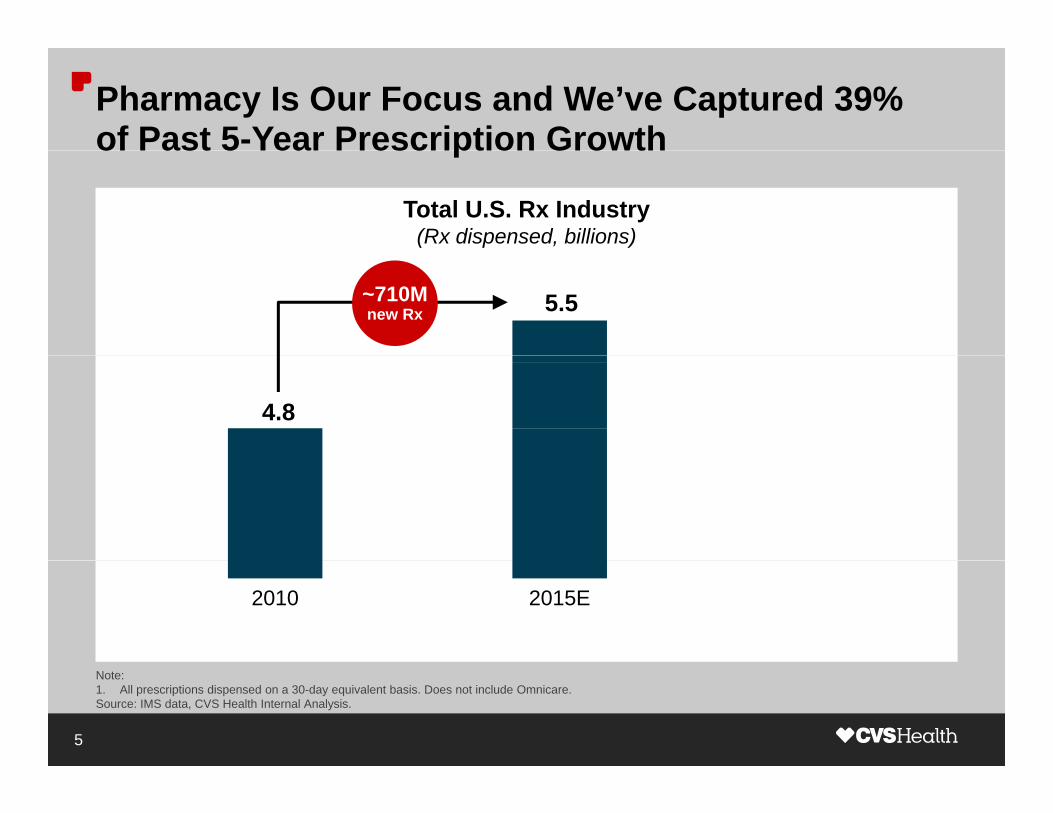

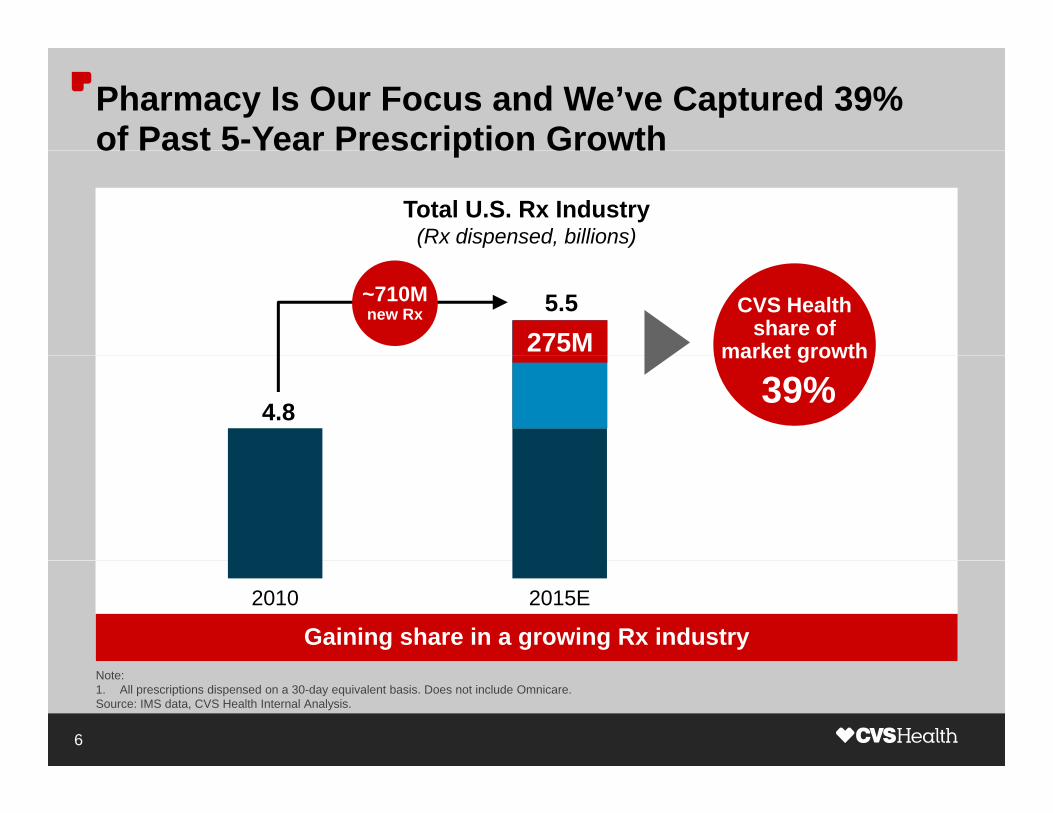

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5~710Mnew Rx

4.8

2010 2015E

Note:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

5

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5 CVS Healthshare of

market growth275M

~710Mnew Rx

4.8

market growth

39%

2010 2015E

Gaining share in a growing Rx industryNote:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

6

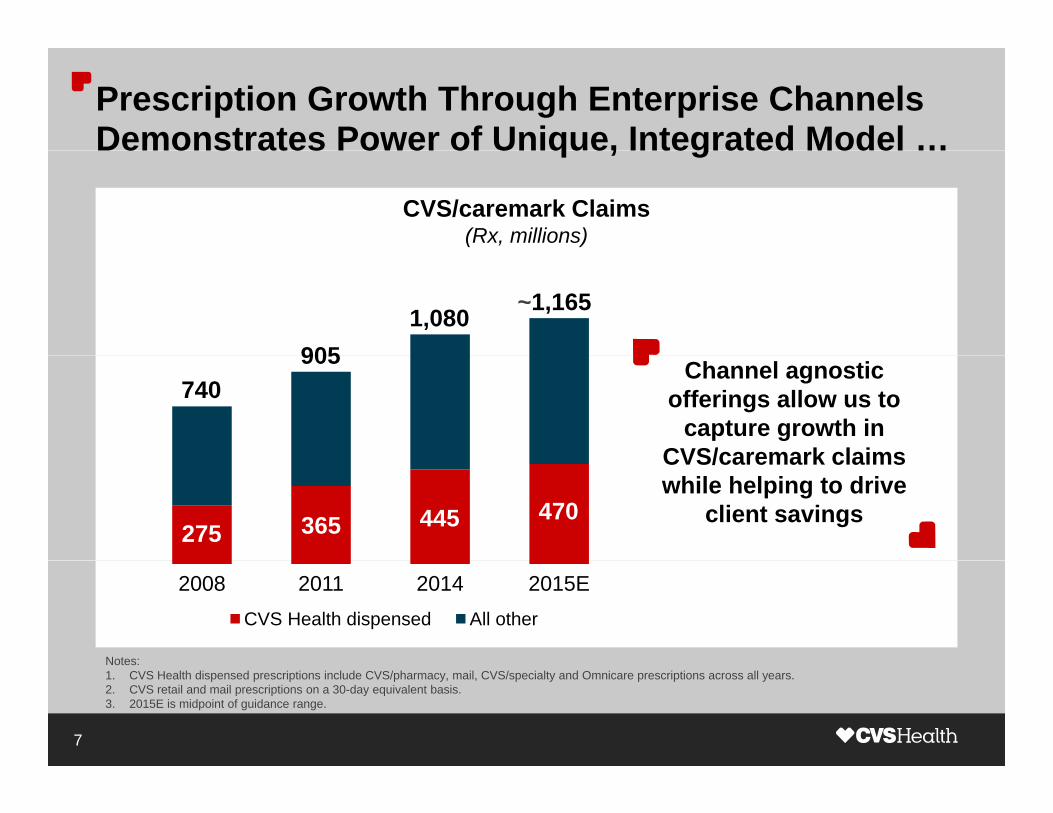

Prescription Growth Through Enterprise Channels Demonstrates Power of Unique, Integrated Model …Demonstrates Power of Unique, Integrated Model …

CVS/caremark Claims(Rx, millions)

9051,080 ~1,165

740905 Channel agnostic

offerings allow us to capture growth in

CVS/caremark claims

275 365 445 470

CVS/caremark claims while helping to drive

client savings

Notes:

2008 2011 2014 2015ECVS Health dispensed All other

Notes:1. CVS Health dispensed prescriptions include CVS/pharmacy, mail, CVS/specialty and Omnicare prescriptions across all years.2. CVS retail and mail prescriptions on a 30-day equivalent basis.3. 2015E is midpoint of guidance range.

7

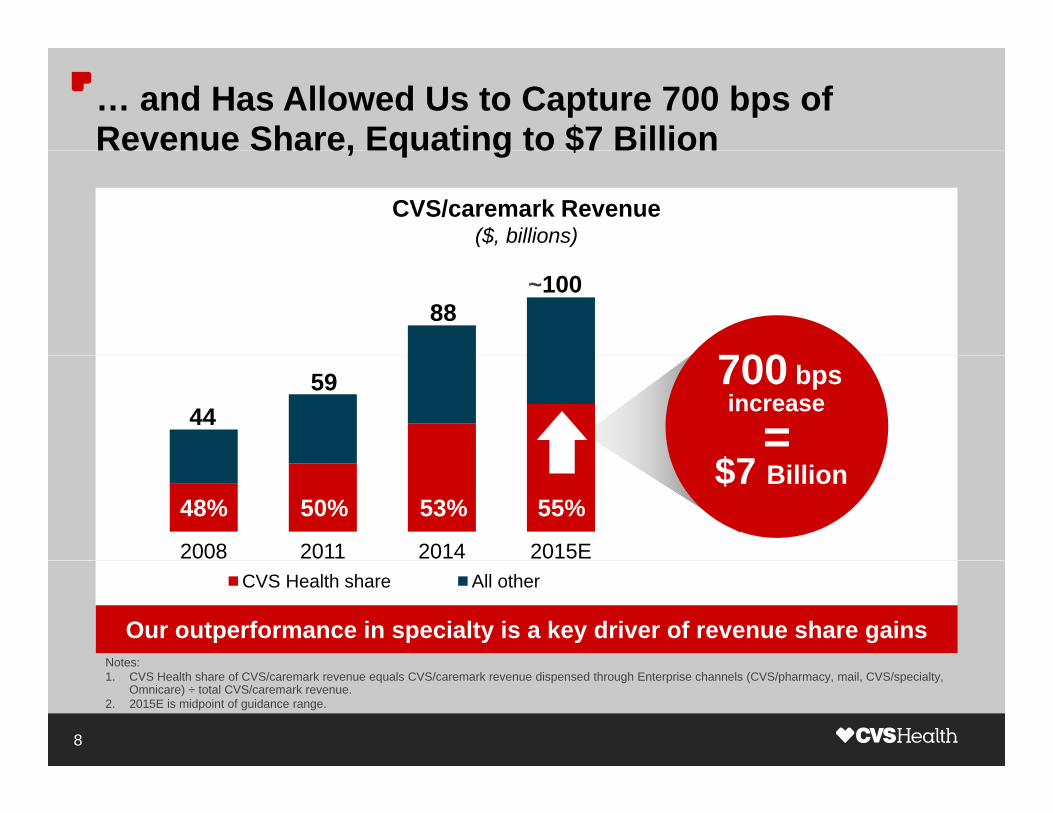

… and Has Allowed Us to Capture 700 bps of Revenue Share, Equating to $7 BillionRevenue Share, Equating to $7 Billion

CVS/caremark Revenue($, billions)

70088

~100

$7

700 bpsincrease

=4459

$7 Billion

2008 2011 2014 2015E

48% 50% 53% 55%

Notes:

CVS Health share All other

Our outperformance in specialty is a key driver of revenue share gainsNotes:1. CVS Health share of CVS/caremark revenue equals CVS/caremark revenue dispensed through Enterprise channels (CVS/pharmacy, mail, CVS/specialty,

Omnicare) ÷ total CVS/caremark revenue.2. 2015E is midpoint of guidance range.

8

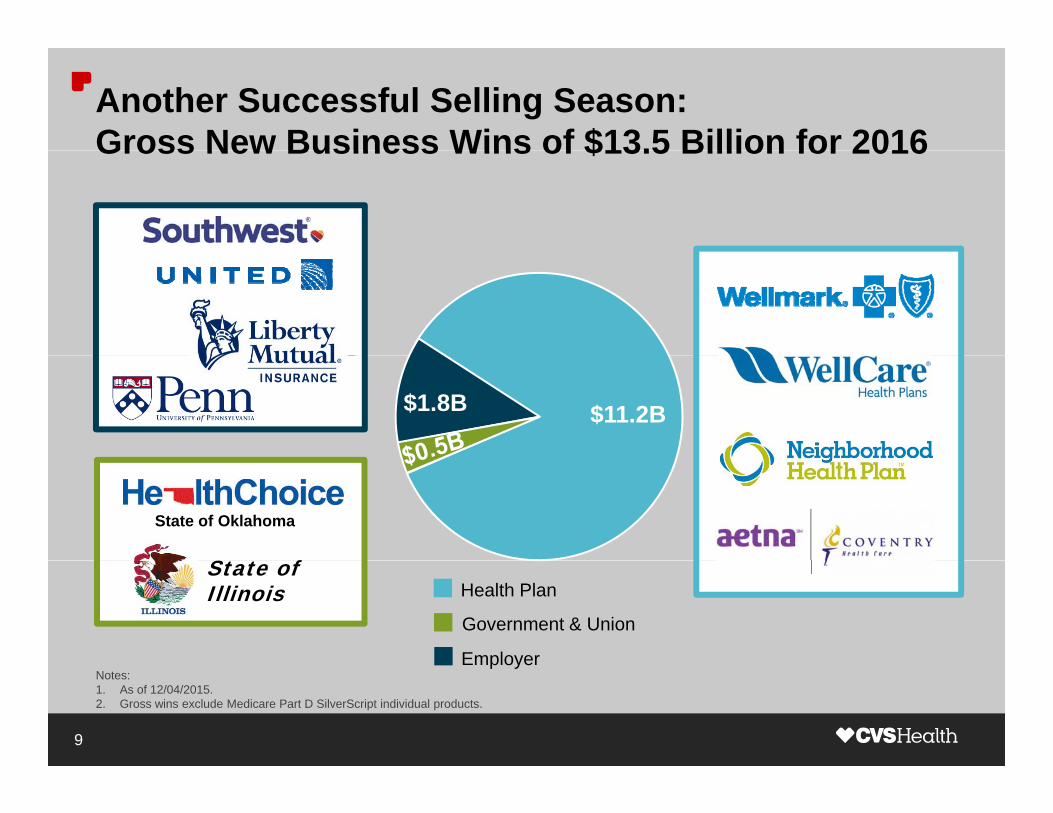

Another Successful Selling Season: Gross New Business Wins of $13.5 Billion for 2016Gross New Business Wins of $13.5 Billion for 2016

13 5B13.5BIN NEW

$11.2B$1.8B

BUSINESS WINS

St t f

State of Oklahoma

Government & Union

Employer

State of Illinois Health Plan

9

EmployerNotes:1. As of 12/04/2015.2. Gross wins exclude Medicare Part D SilverScript individual products.

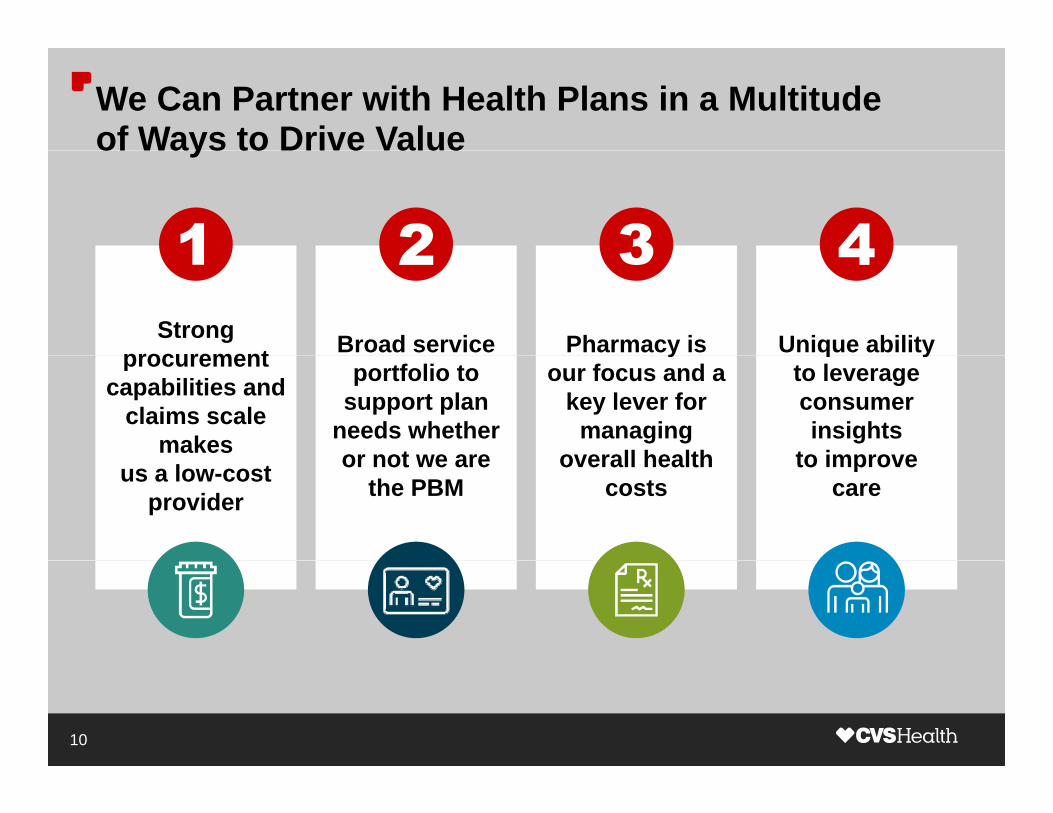

We Can Partner with Health Plans in a Multitudeof Ways to Drive Valueof Ways to Drive Value

Strong procurement Broad service Pharmacy is Unique ability procurement

capabilities and claims scale

makes

portfolio to support plan

needs whether or not we are

your focus and a

key lever for managing

overall health

q yto leverage consumer insights

to improveus a low-cost provider

or not we are the PBM

overall health costs

to improvecare

10

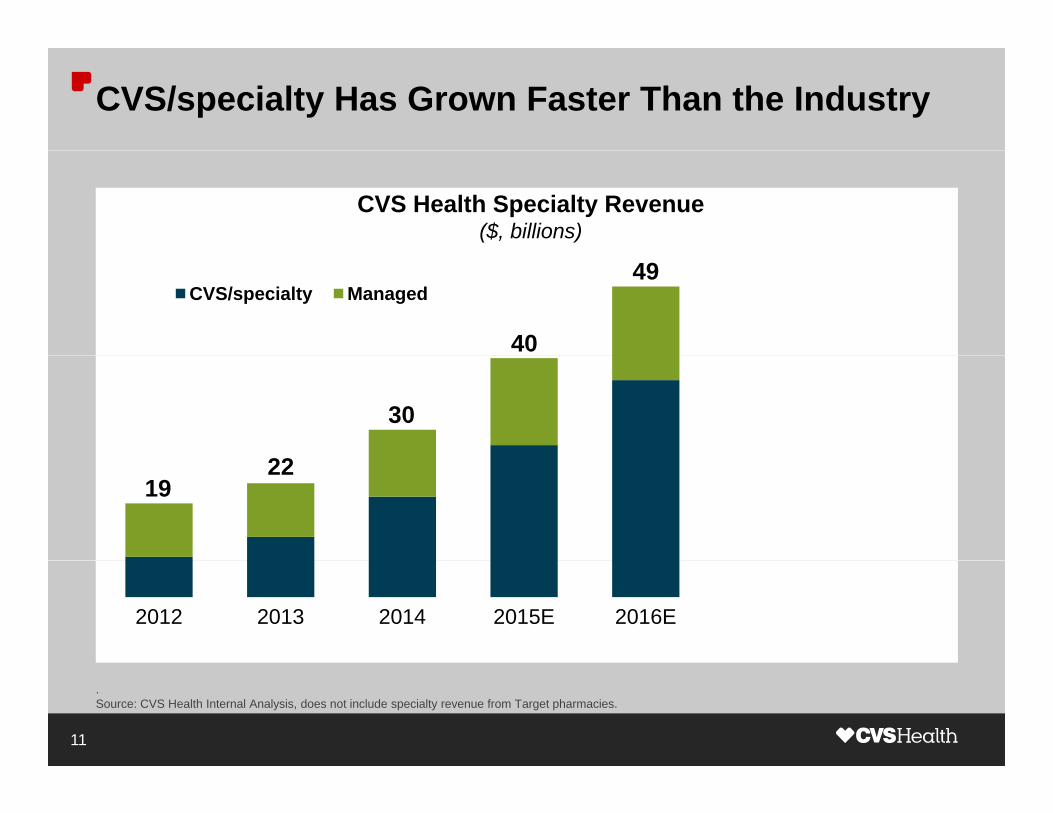

CVS/specialty Has Grown Faster Than the Industry

CVS Health Specialty Revenue($, billions)

CVS/specialty Managed

40

49

30

222219

2012 2013 2014 2015E 2016E

.Source: CVS Health Internal Analysis, does not include specialty revenue from Target pharmacies.

11

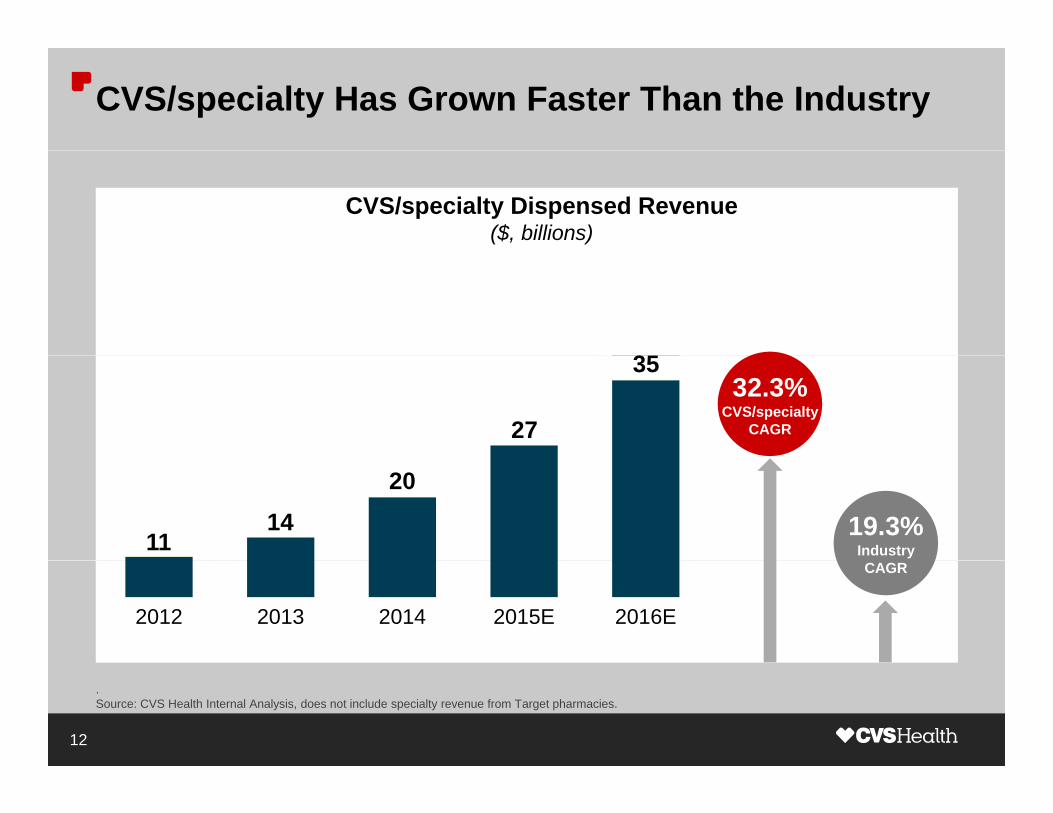

CVS/specialty Has Grown Faster Than the Industry

CVS/specialty Dispensed Revenue($, billions)

3532.3%

CVS/specialtyCAGR27

35

19.3%Industry

2014

11

2012 2013 2014 2015E 2016E

CAGR

.Source: CVS Health Internal Analysis, does not include specialty revenue from Target pharmacies.

12

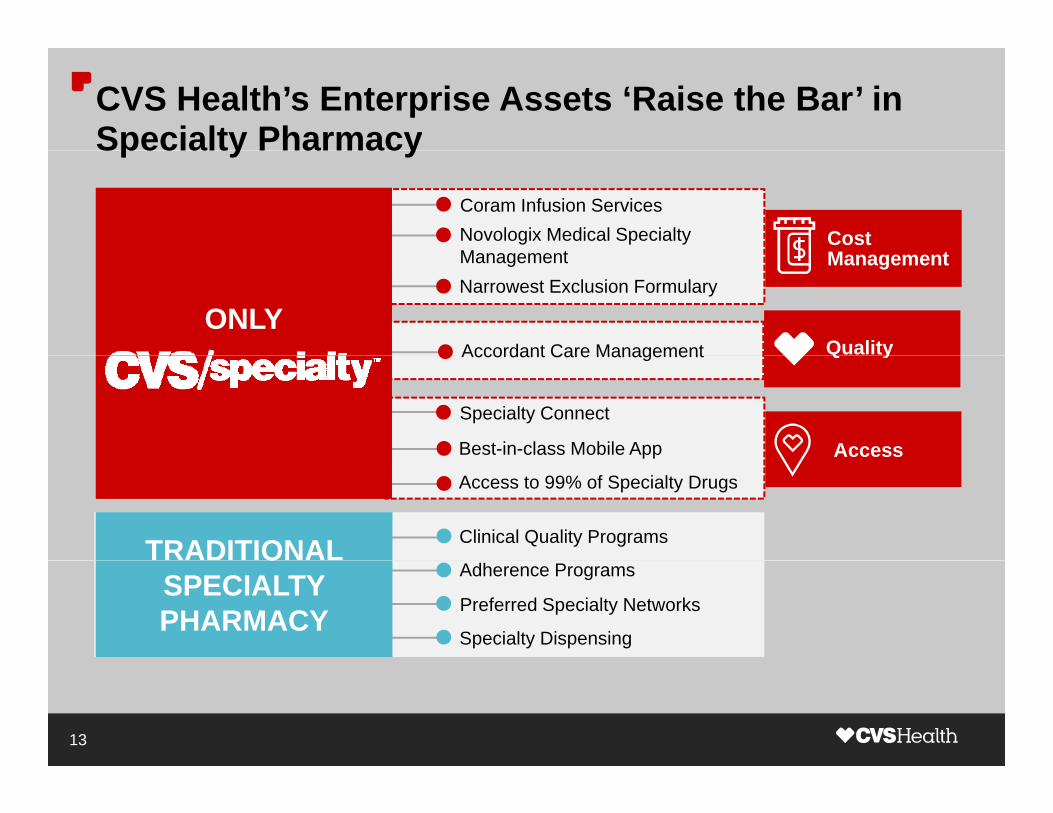

CVS Health’s Enterprise Assets ‘Raise the Bar’ in Specialty PharmacySpecialty Pharmacy

Novologix Medical Specialty M t

Coram Infusion Services

Cost M t

Accordant Care Management

Narrowest Exclusion Formulary Management

ONLY

Management

Quality

Best-in-class Mobile App

Specialty Connect

Accordant Care Management

Access

Q y

Clinical Quality Programs

Access to 99% of Specialty Drugs

pp

TRADITIONAL

Specialty Dispensing

Adherence Programs

Preferred Specialty Networks

OSPECIALTY PHARMACY

13

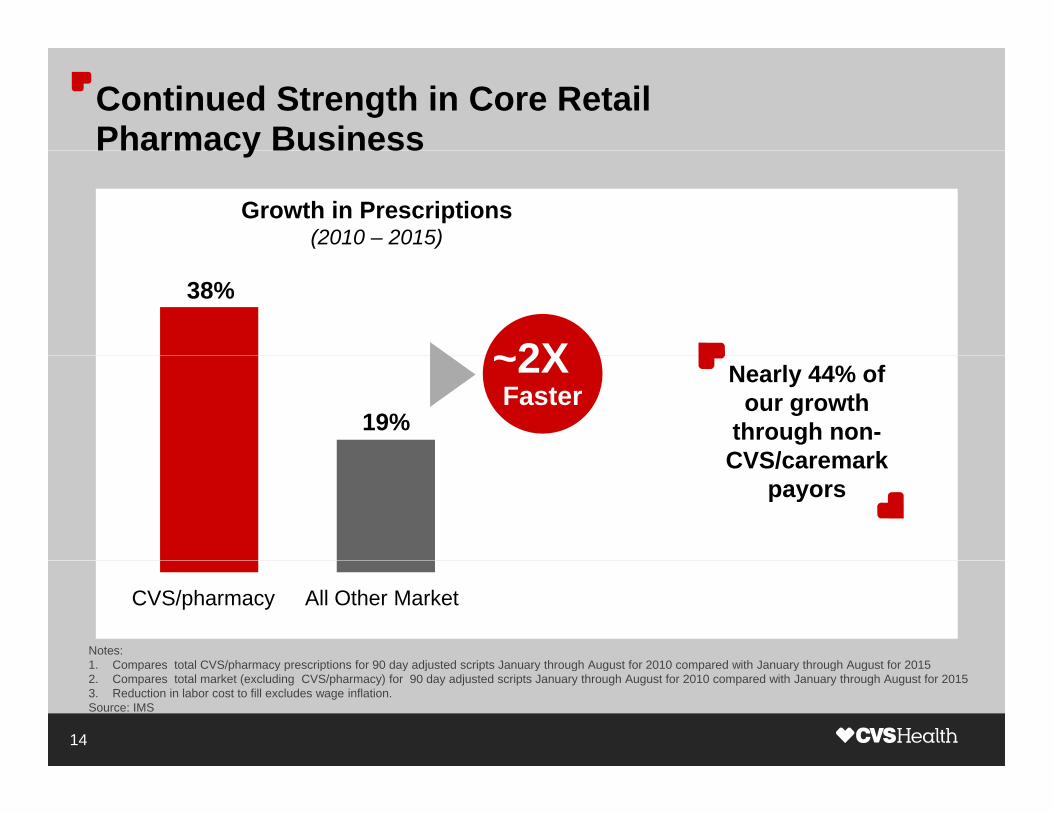

Continued Strength in Core RetailPharmacy BusinessPharmacy Business

Growth in Prescriptions(2010 – 2015)

38%

~2X19%

~2X Faster

Nearly 44% of our growth

through non-CVS/caremarkCVS/caremark

payors

All Other MarketCVS/pharmacy

Notes:1 Compares total CVS/pharmacy prescriptions for 90 day adjusted scripts January through August for 2010 compared with January through August for 20151. Compares total CVS/pharmacy prescriptions for 90 day adjusted scripts January through August for 2010 compared with January through August for 2015 2. Compares total market (excluding CVS/pharmacy) for 90 day adjusted scripts January through August for 2010 compared with January through August for 20153. Reduction in labor cost to fill excludes wage inflation.Source: IMS

14

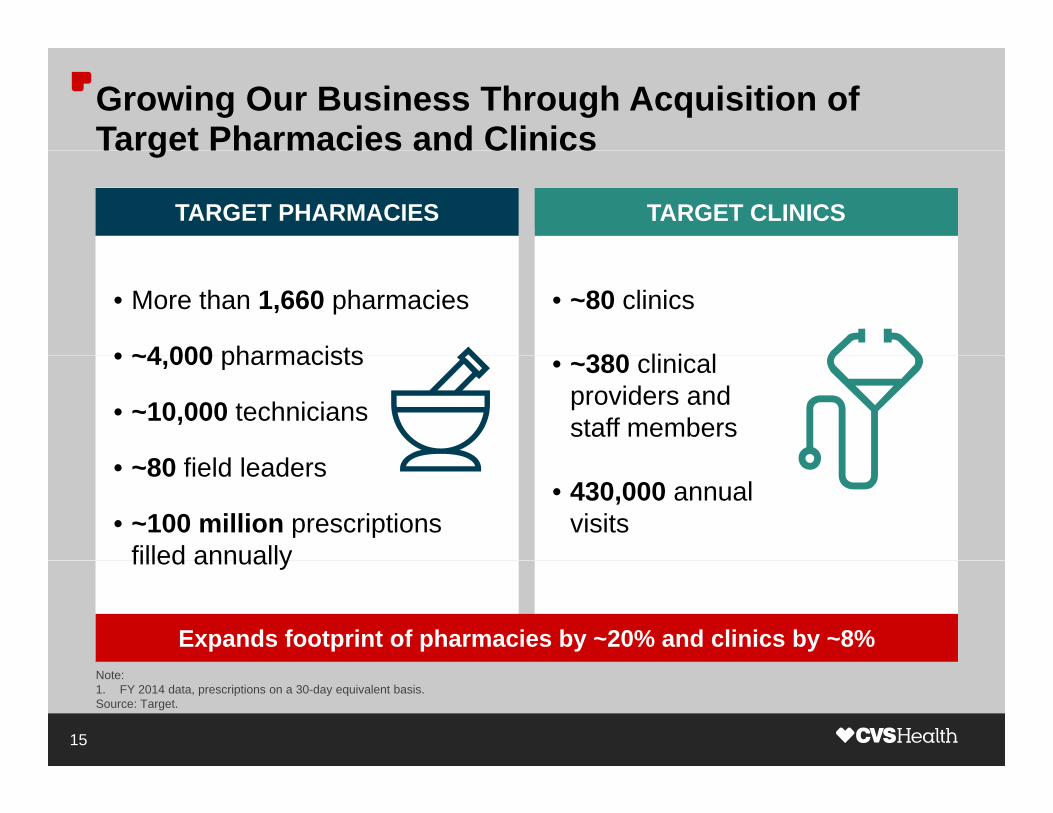

Growing Our Business Through Acquisition of Target Pharmacies and ClinicsTarget Pharmacies and Clinics

TARGET PHARMACIES TARGET CLINICS

• ~80 clinics

380 li i l

• More than 1,660 pharmacies

• ~4 000 pharmacists • ~380 clinical providers and staff members

• ~4,000 pharmacists

• ~10,000 technicians

80 fi ld l d• 430,000 annual

visits

• ~80 field leaders

• ~100 million prescriptions filled annuallyfilled annually

Expands footprint of pharmacies by ~20% and clinics by ~8%

15

Note:1. FY 2014 data, prescriptions on a 30-day equivalent basis.Source: Target.

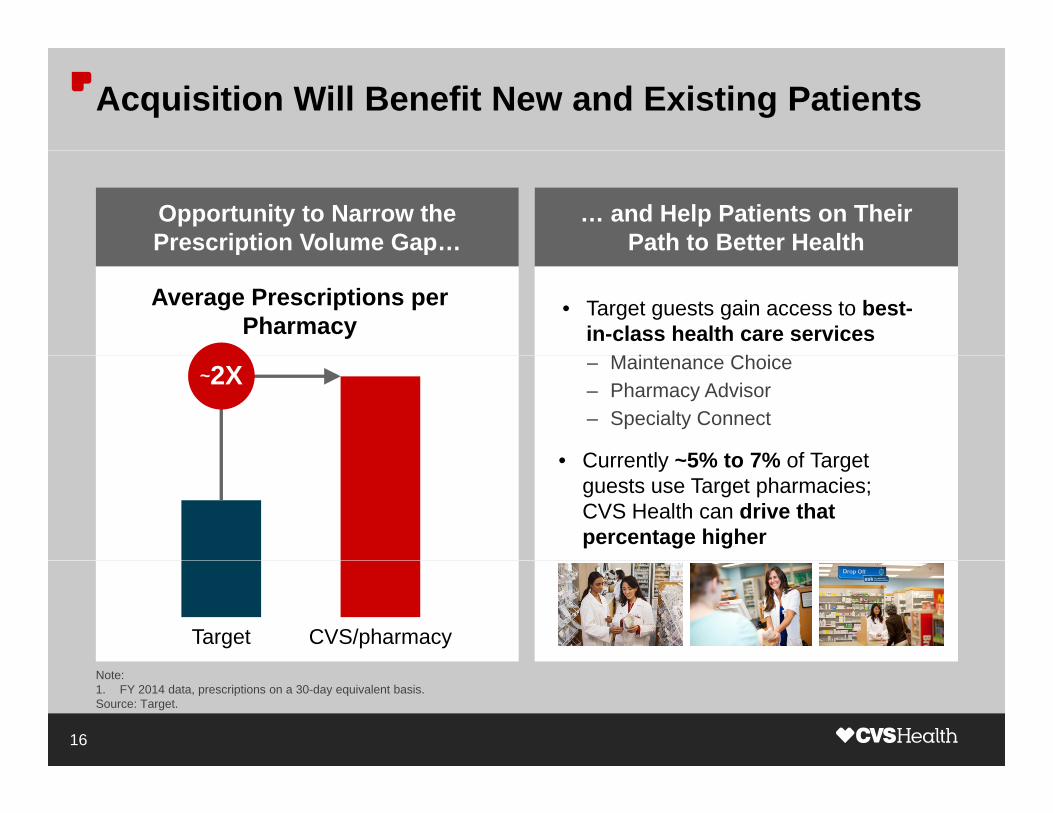

Acquisition Will Benefit New and Existing Patients

Opportunity to Narrow the Prescription Volume Gap…

… and Help Patients on Their Path to Better Health

• Target guests gain access to best-in-class health care services

M i t Ch i

Average Prescriptions per Pharmacy

p p

– Maintenance Choice– Pharmacy Advisor– Specialty Connect

• Currently ~5% to 7% of Target

~2X

• Currently ~5% to 7% of Target guests use Target pharmacies; CVS Health can drive that percentage higher

Target CVS/pharmacy

16

Note:1. FY 2014 data, prescriptions on a 30-day equivalent basis.Source: Target.

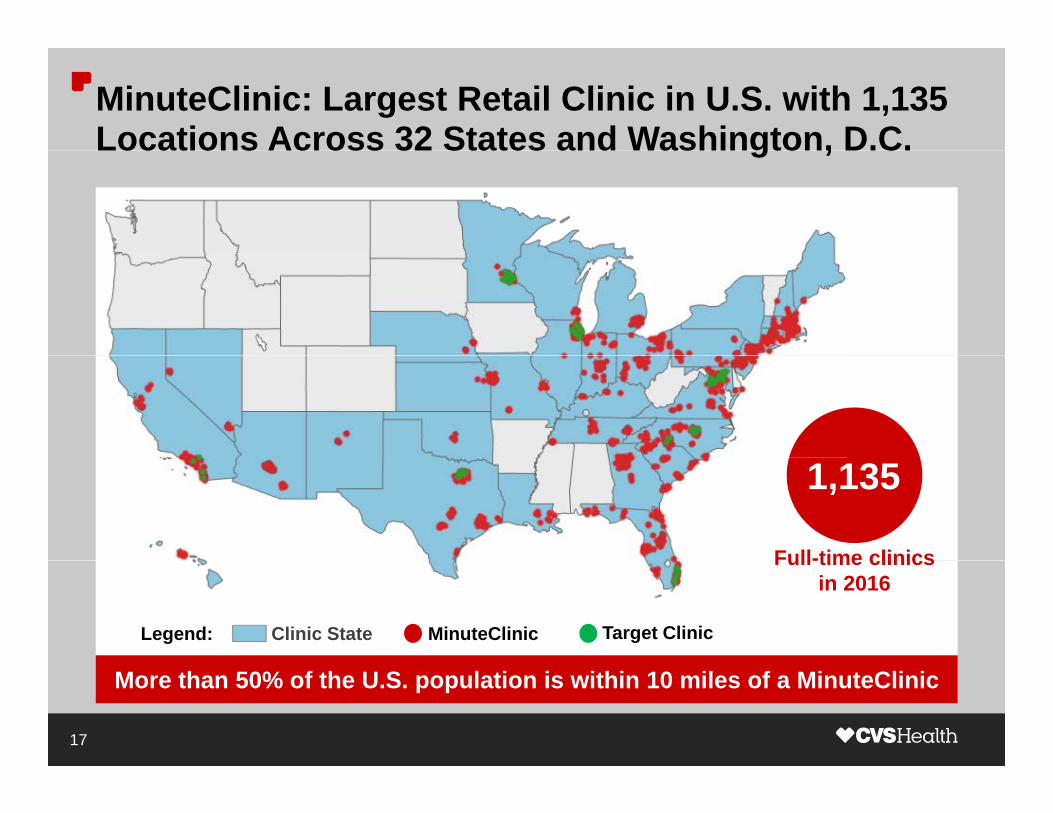

MinuteClinic: Largest Retail Clinic in U.S. with 1,135 Locations Across 32 States and Washington, D.C.Locations Across 32 States and Washington, D.C.

Full-time clinics

1,135

MinuteClinic Target ClinicClinic StateLegend:

Full-time clinicsin 2016

More than 50% of the U.S. population is within 10 miles of a MinuteClinic

17

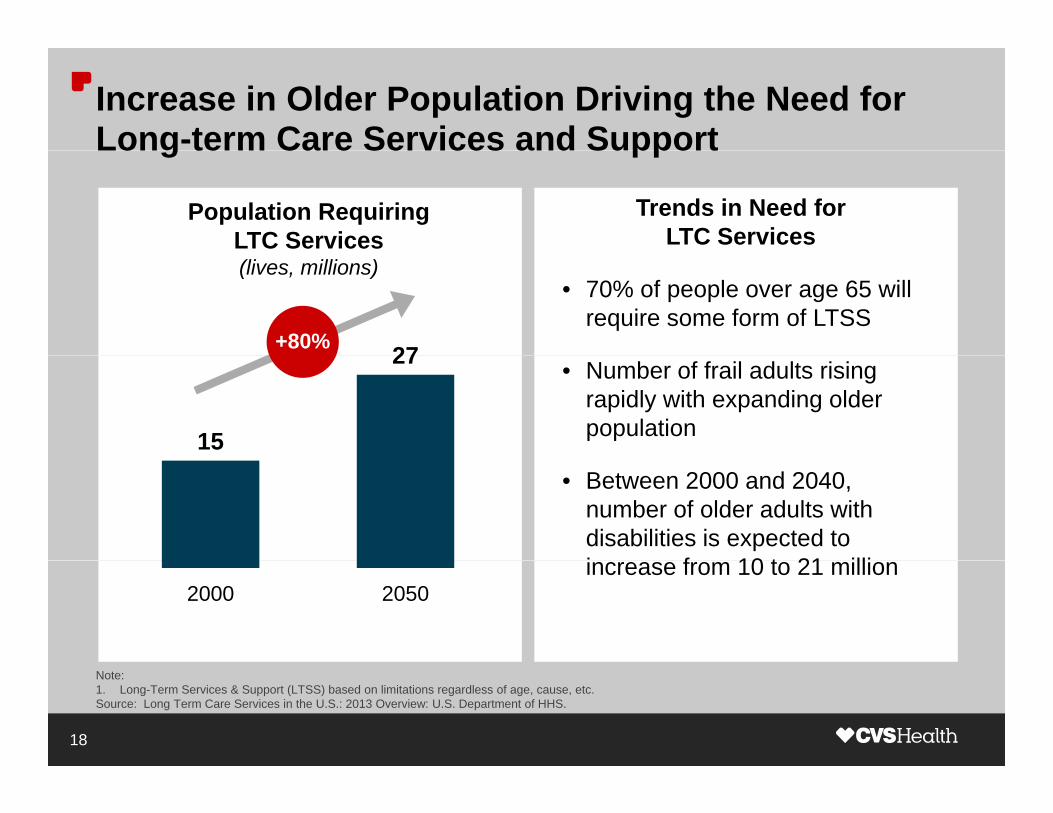

Increase in Older Population Driving the Need for Long-term Care Services and SupportLong term Care Services and Support

Population Requiring LTC Services

Trends in Need for LTC Services

27+80%

(lives, millions)• 70% of people over age 65 will

require some form of LTSS

15

27 • Number of frail adults rising rapidly with expanding older population

• Between 2000 and 2040, number of older adults with disabilities is expected to i f 10 t 21 illi

2000 2050increase from 10 to 21 million

Note:1. Long-Term Services & Support (LTSS) based on limitations regardless of age, cause, etc.Source: Long Term Care Services in the U.S.: 2013 Overview: U.S. Department of HHS.

18

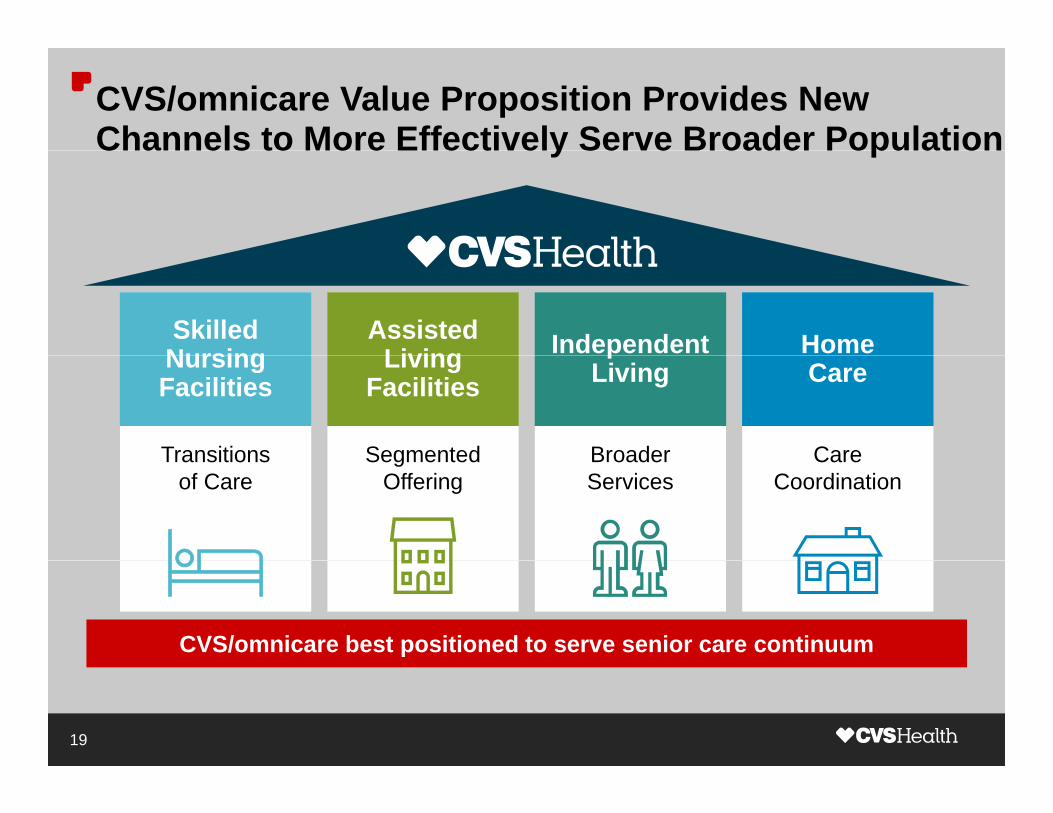

CVS/omnicare Value Proposition Provides New Channels to More Effectively Serve Broader PopulationChannels to More Effectively Serve Broader Population

Skilled Nursing

Assisted Living Independent HomeNursing

Facilities

Transitions Segmented

Living Facilities

pLiving

Broader

Care

CareTransitionsof Care

Segmented Offering

Broader Services

Care Coordination

CVS/omnicare best positioned to serve senior care continuum

19

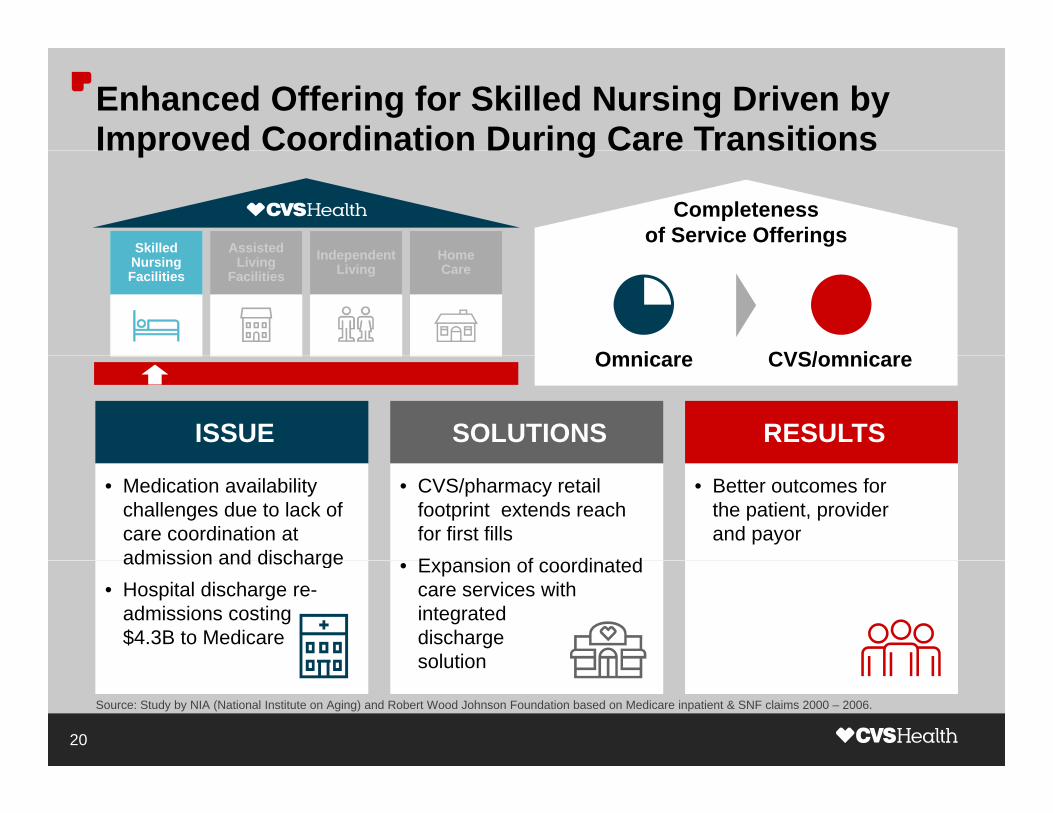

Enhanced Offering for Skilled Nursing Driven by Improved Coordination During Care Transitions

Skilled Assisted Independent Home

Improved Coordination During Care Transitions

Completenessof Service Offerings

Nursing Facilities

Living Facilities

Independent Living

HomeCare

Omnicare CVS/omnicare

ISSUE RESULTSSOLUTIONS

Omnicare CVS/omnicare

• Medication availability challenges due to lack of care coordination at admission and discharge

• CVS/pharmacy retail footprint extends reach for first fillsE i f di t d

• Better outcomes for the patient, provider and payor

admission and discharge• Hospital discharge re-

admissions costing $4.3B to Medicare

• Expansion of coordinated care services with integrateddischarge solution

20

solution

Source: Study by NIA (National Institute on Aging) and Robert Wood Johnson Foundation based on Medicare inpatient & SNF claims 2000 – 2006.

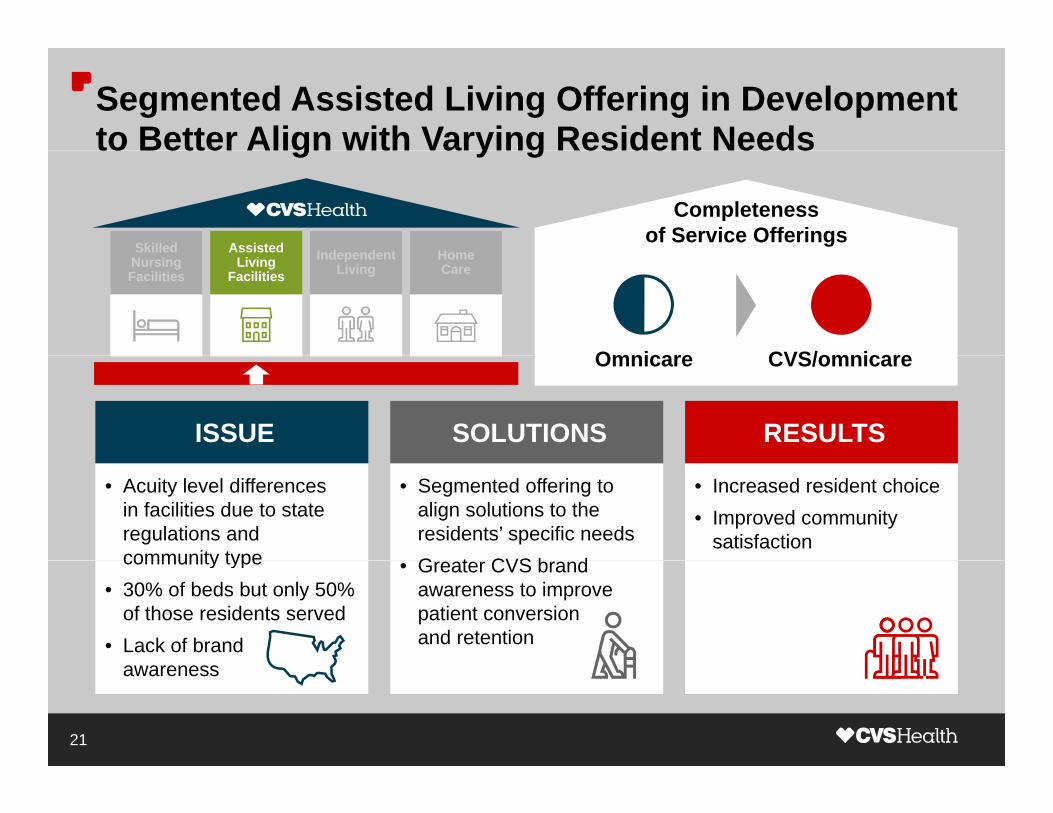

Segmented Assisted Living Offering in Development to Better Align with Varying Resident Needs

Skilled Assisted Independent Home

to Better Align with Varying Resident Needs

Completenessof Service Offerings

Nursing Facilities

Living Facilities

Independent Living

HomeCare

Omnicare CVS/omnicare

ISSUE RESULTSSOLUTIONS

Omnicare CVS/omnicare

• Acuity level differences in facilities due to state regulations and community type

• Segmented offering to align solutions to the residents’ specific needsG t CVS b d

• Increased resident choice• Improved community

satisfactioncommunity type

• 30% of beds but only 50% of those residents served

• Lack of brand

• Greater CVS brand awareness to improve patient conversion and retention

21

awareness

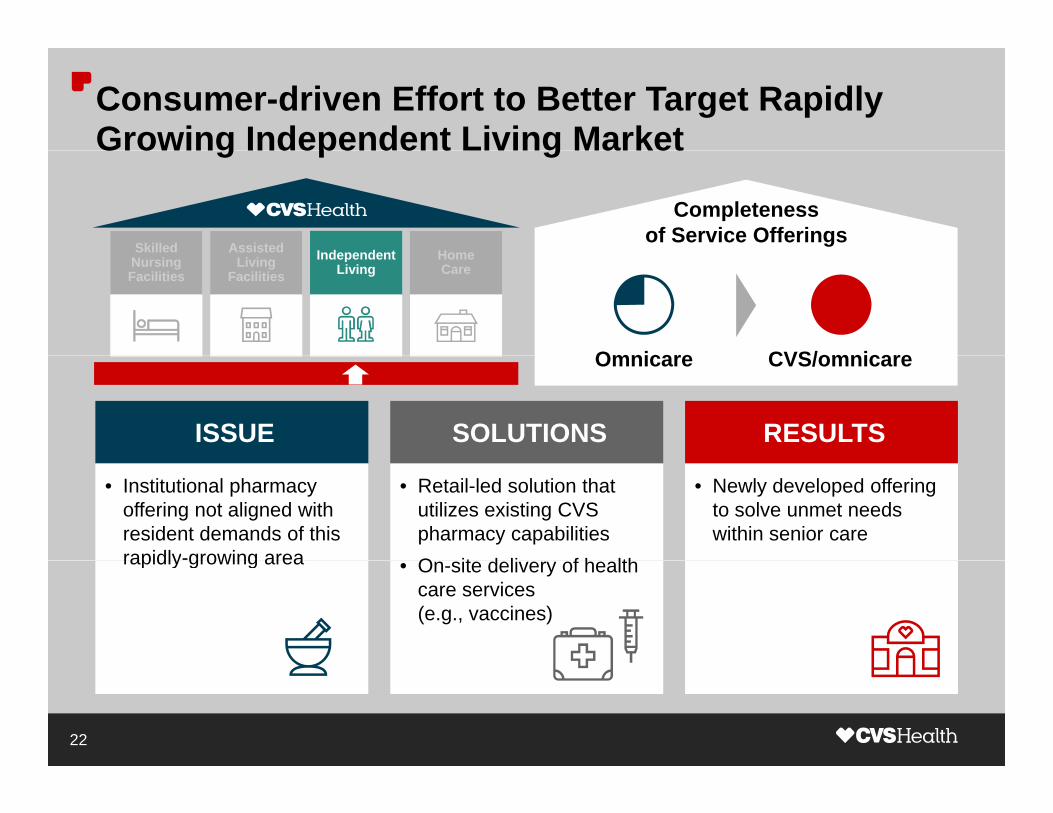

Consumer-driven Effort to Better Target Rapidly Growing Independent Living Market

Skilled Assisted Independent Home

Growing Independent Living Market

Completenessof Service Offerings

Nursing Facilities

Living Facilities

Independent Living

HomeCare

Omnicare CVS/omnicare

ISSUE RESULTSSOLUTIONS

Omnicare CVS/omnicare

• Institutional pharmacy offering not aligned with resident demands of this rapidly-growing area

• Retail-led solution that utilizes existing CVS pharmacy capabilitiesO it d li f h lth

• Newly developed offering to solve unmet needs within senior care

rapidly growing area • On-site delivery of health care services (e.g., vaccines)

22

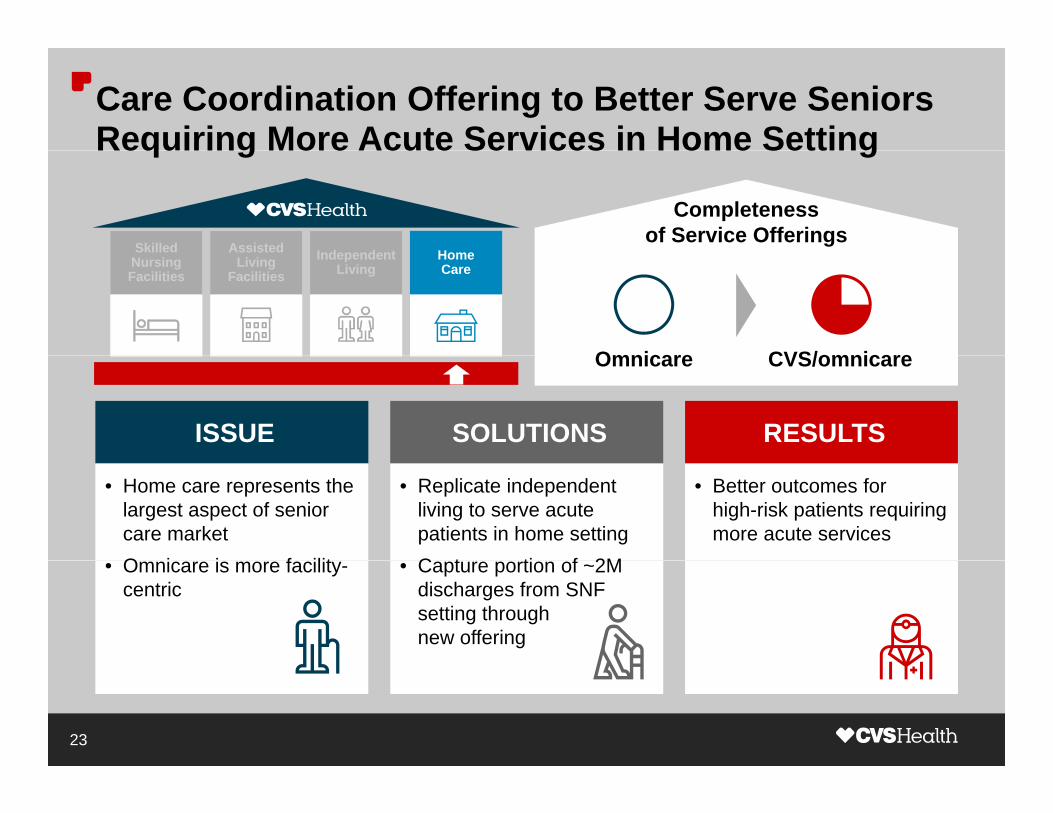

Care Coordination Offering to Better Serve Seniors Requiring More Acute Services in Home Setting

Skilled Assisted Independent Home

Requiring More Acute Services in Home Setting

Completenessof Service Offerings

Nursing Facilities

Living Facilities

Independent Living

HomeCare

Omnicare CVS/omnicare

ISSUE RESULTSSOLUTIONS

Omnicare CVS/omnicare

• Home care represents the largest aspect of senior care marketO i i f ilit

• Replicate independent living to serve acute patients in home settingC t ti f 2M

• Better outcomes for high-risk patients requiring more acute services

• Omnicare is more facility-centric

• Capture portion of ~2M discharges from SNF setting through new offering

23

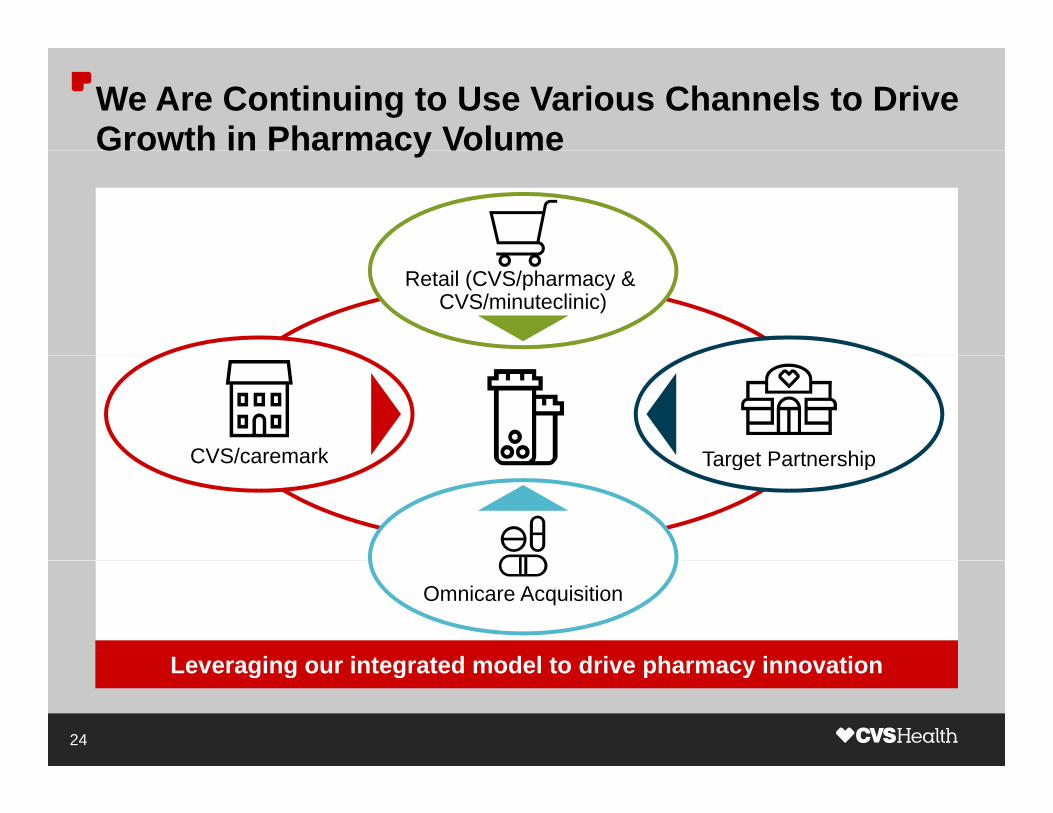

We Are Continuing to Use Various Channels to Drive Growth in Pharmacy VolumeGrowth in Pharmacy Volume

Retail (CVS/pharmacy & CVS/minuteclinic)

CVS/caremark Target PartnershipCVS/caremark Target Partnership

Omnicare Acquisition

Leveraging our integrated model to drive pharmacy innovation

24

Leveraging our integrated model to drive pharmacy innovation

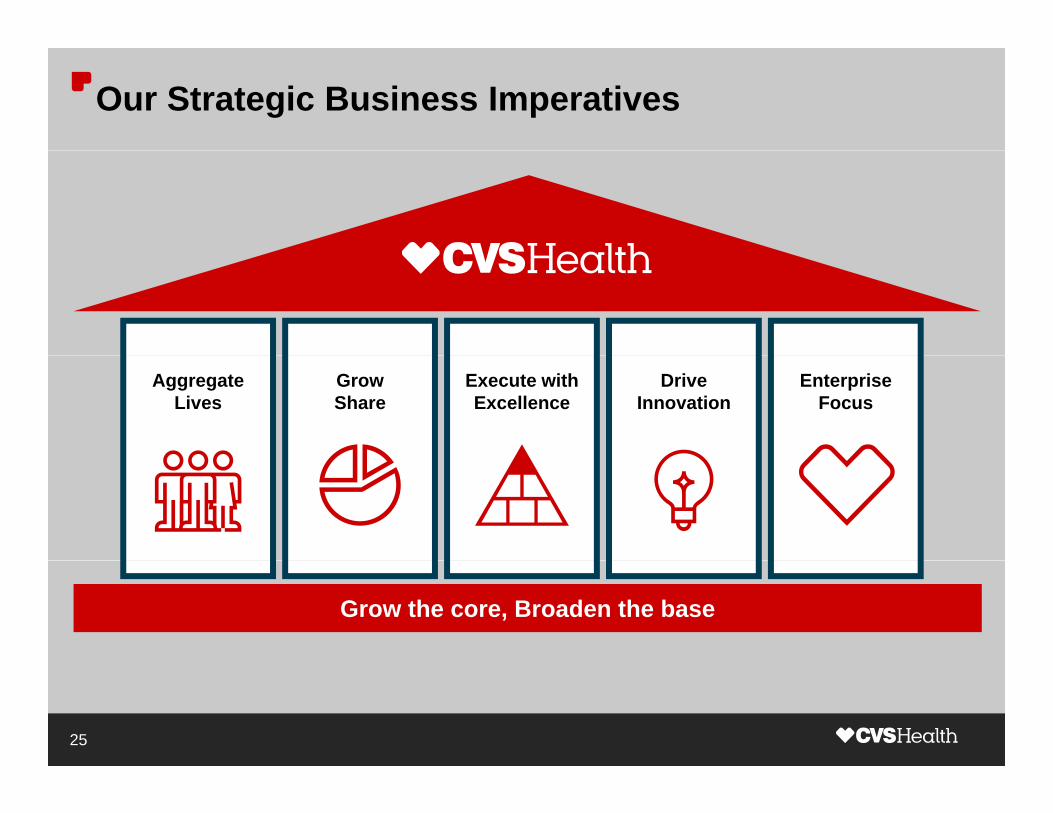

Our Strategic Business Imperatives

AggregateLives

GrowShare

Execute with Excellence

DriveInnovation

Enterprise Focus

Grow the core, Broaden the base

25

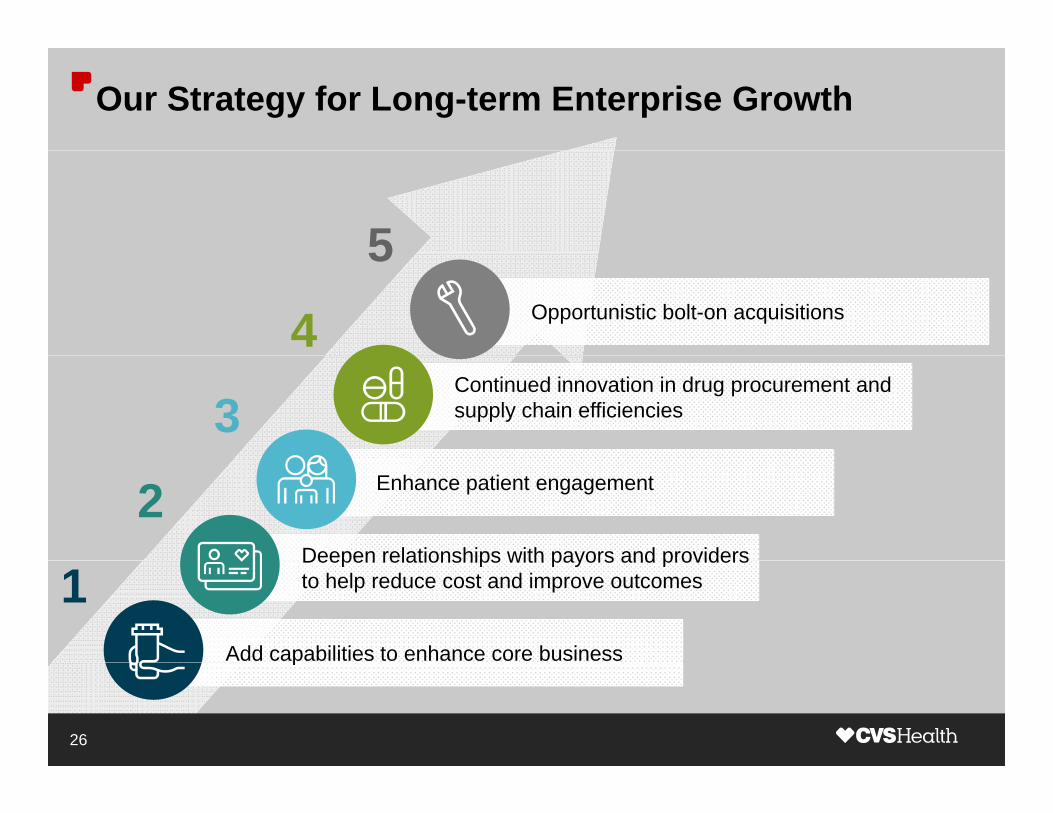

Our Strategy for Long-term Enterprise Growth

5Opportunistic bolt-on acquisitions4

5

Continued innovation in drug procurement and supply chain efficiencies3

Enhance patient engagement

Deepen relationships with payors and providers

2Deepen relationships with payors and providers to help reduce cost and improve outcomes

Add capabilities to enhance core business

1

26

p

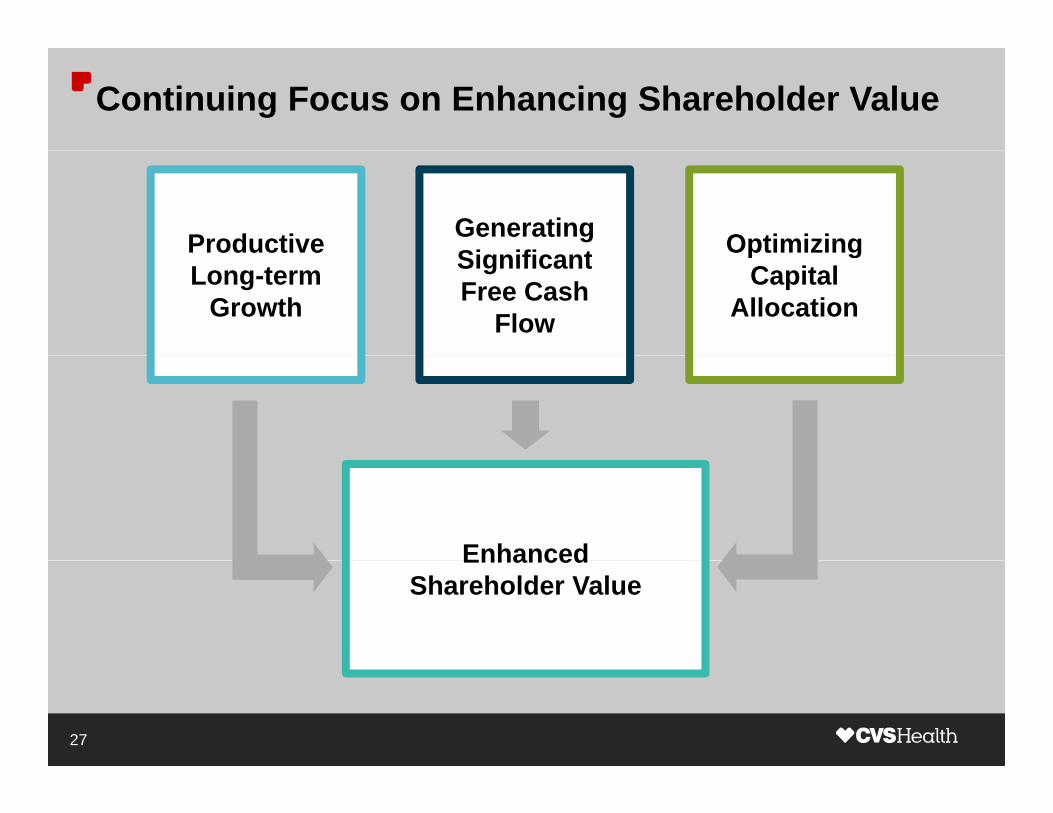

Continuing Focus on Enhancing Shareholder Value

Productive Generating Si ifi t Optimizing

Long-term Growth

SignificantFree Cash

Flow

Op gCapital

Allocation

EnhancedEnhancedShareholder Value

27

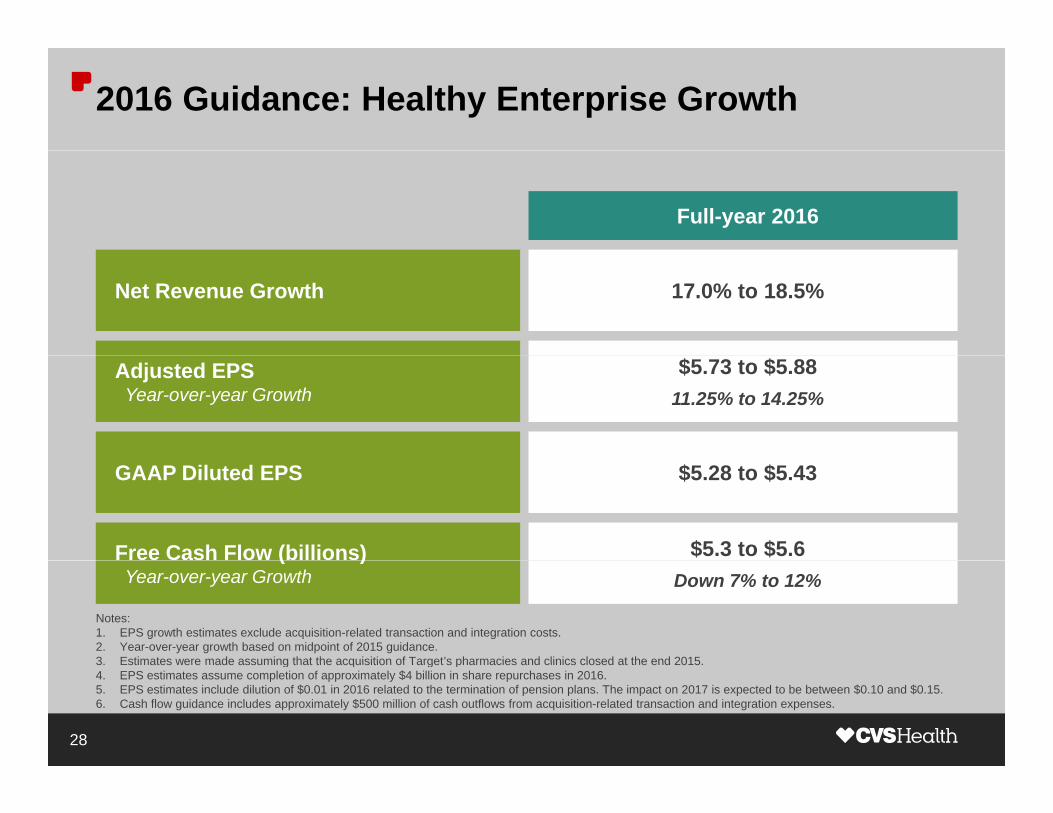

2016 Guidance: Healthy Enterprise Growth

Full-year 2016

Net Revenue Growth 17.0% to 18.5%

Adjusted EPSYear-over-year Growth

$5.73 to $5.8811.25% to 14.25%

GAAP Diluted EPS $5.28 to $5.43

Free Cash Flow (billions) $5.3 to $5.6( )Year-over-year Growth Down 7% to 12%

Notes:1. EPS growth estimates exclude acquisition-related transaction and integration costs.2. Year-over-year growth based on midpoint of 2015 guidance.3 Estimates were made assuming that the acquisition of Target’s pharmacies and clinics closed at the end 20153. Estimates were made assuming that the acquisition of Target s pharmacies and clinics closed at the end 2015.4. EPS estimates assume completion of approximately $4 billion in share repurchases in 2016.5. EPS estimates include dilution of $0.01 in 2016 related to the termination of pension plans. The impact on 2017 is expected to be between $0.10 and $0.15.6. Cash flow guidance includes approximately $500 million of cash outflows from acquisition-related transaction and integration expenses.

28

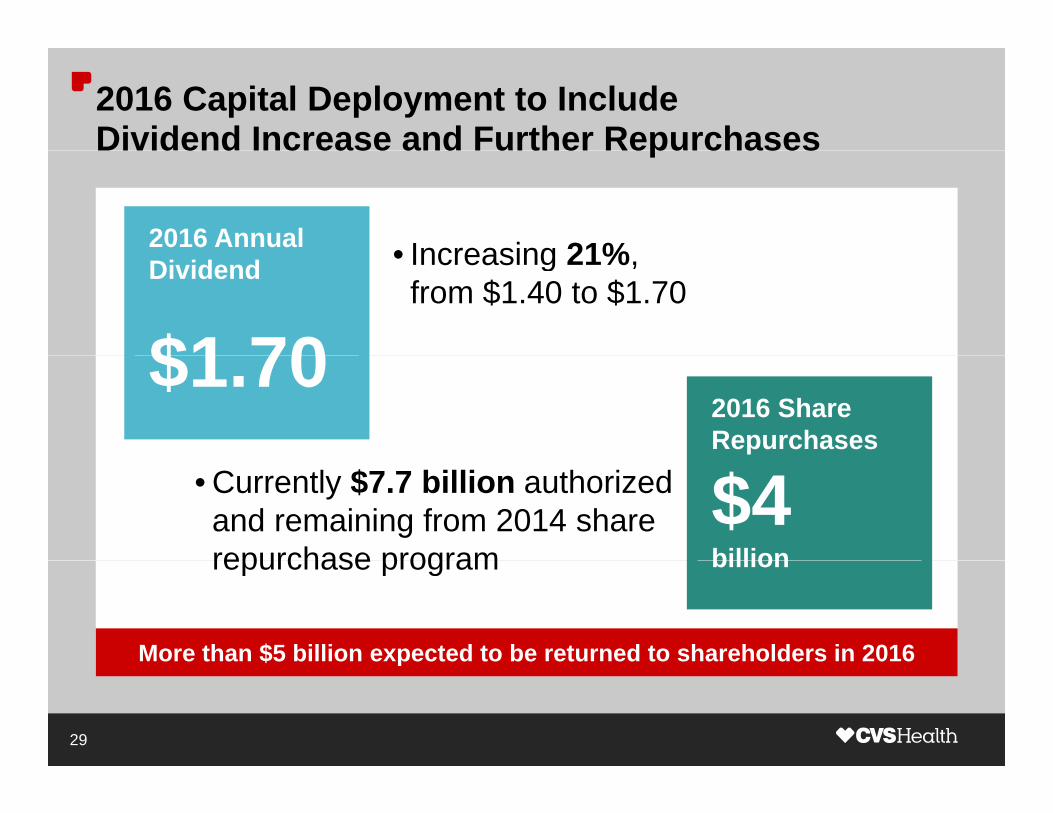

2016 Capital Deployment to IncludeDividend Increase and Further Repurchases

• Increasing 21%

Dividend Increase and Further Repurchases

2016 Annual • Increasing 21%,from $1.40 to $1.70

Dividend

$1 70$1.702016 Share Repurchases

$4billion

• Currently $7.7 billion authorized and remaining from 2014 share repurchase program billionrepurchase program

More than $5 billion expected to be returned to shareholders in 2016$ p

29

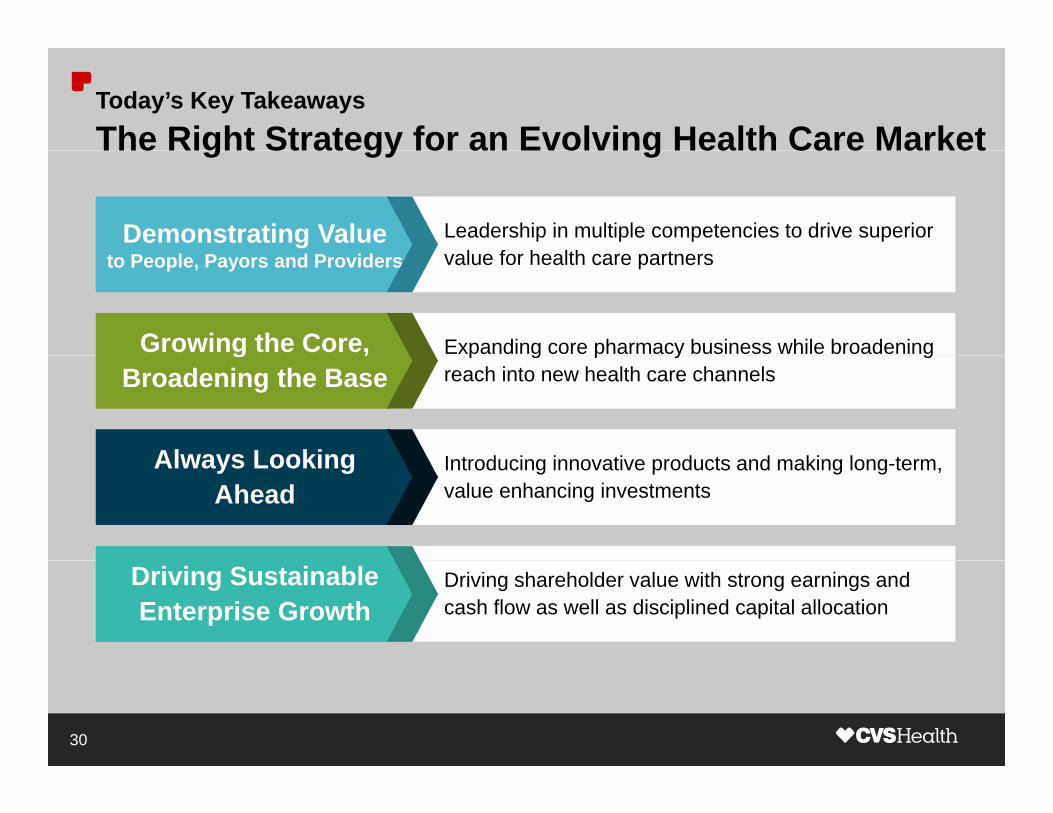

Today’s Key Takeaways

The Right Strategy for an Evolving Health Care MarketThe Right Strategy for an Evolving Health Care Market

Leadership in multiple competencies to drive superior l f h lth t

Demonstrating Valuevalue for health care partnersto People, Payors and Providers

Expanding core pharmacy business while broadening Growing the Core, p g p y greach into new health care channels

g ,Broadening the Base

I t d i i ti d t d ki l tAlways Looking Introducing innovative products and making long-term, value enhancing investments

Always Looking Ahead

Driving shareholder value with strong earnings and cash flow as well as disciplined capital allocation

Driving Sustainable Enterprise Growth

30

The Right Strategy for anThe Right Strategy for an Evolving Health Care Market

Larry MerloyPresident & Chief Executive Officer

34th Annual J.P. Morgan Healthcare ConferenceJanuary 12, 2016