Embed Size (px)

Citation preview

The Regulation of Financial Services

Gaps 1-3

Financial Services, Regulation & Ethics

Resources Compliance (UK) Ltd

Gaps 1-3

2

The UK financial services industry:

1. Additional oversight - senior management, external compliance support

services

2. FSMA 2000

3. Role of the FSA, HM Treasury and the Bank of England in regulating

markets

3. Role of the ‘Tripartite’ authorities

3

HM Treasury

Bank of England

Financial Services Authority

HM Treasury

4

Runs UK Government’s financial and economic policy

Raise the rate of sustainable growth

Maintain financial stability

Work on financial contingencies

Bank of England

5

UK’s central bank

Core purposes

Monetary stability

stable prices: inflation target

confidence in the currency

Financial stability

detecting and reducing threats

acting as the lender of last resort.

Financial Services Authority

6

Sole UK financial services industry regulator

Independent body

Powers under FSMA 2000

Regulates most financial services markets, exchanges and firms

Created 2001 from SIB, PIA, SFA, IMRO , DTI, BofE, BSC, FSC & others

FSA: Statutory objectives

7

The FSA has been given a wide range of rule-making, investigatory and enforcement powers in order to meet four statutory objectives:

Market confidence;

Financial stability;

Consumer protection; and

Reduction of financial crime.

FSA: Principles of good regulation

8

The FSA is also obliged to give regard to the principles of good regulation which involve awareness of:

Efficiency and economy;

Role of management;

Proportionality;

Innovation;

International character;

Competition; and

Public awareness.

FSA: Strategic aims

9

The FSA summarises its statutory objectives and principles of good

regulation in three strategic aims:

Promoting efficient, orderly and fair markets;

Helping retail consumers achieve a fair deal; and

Improving their business capability and effectiveness.

A peek into 2013

10

New ‘twin peaks’ regulatory structure:

Financial Policy Committee

Prudential Regulation Authority

Financial Conduct Authority

National Crime Agency

2. Financial Services & Markets Act 2000 “FSMA”

11

The objective of FSMA was to bring together the regulation of all sectors of the financial services industry under one regulatory system.

Previously, different parts of the financial services industry were regulated under different Acts.

2. Financial Services & Markets Act 2000 “FSMA”

12

Consolidation under one regulator of:

Banking Act 1987;

Building Societies Act 1986;

Friendly Societies Act 1992;

Insurance Companies Act 1982;

Financial Services Act 1986

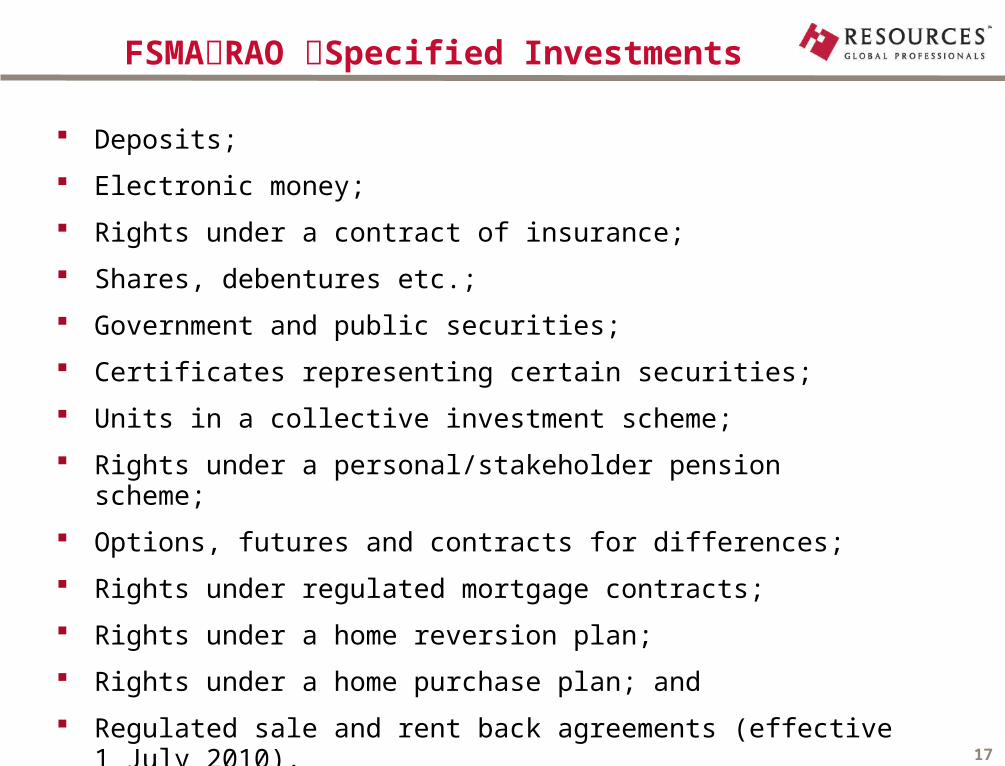

Scope of FSMA 2000

13

Financial Services & Markets Act 2000 (Regulated Activities Order) 2001 “RAO” - as secondary legislation - lists:

Regulated Activities (Part II)

Specified Investments (Part III)

FSMARAO Regulated Activities

14

Banking

Accepting deposits; and

Issuing e-money.

Investment

Advising on investments;

Providing basic advice on stakeholder products;

Arranging deals in investments;

Managing investments;

Dealing in investments (as principal or agent); and

Safeguarding and administering investments.

FSMARAO Regulated Activities

15

Insurance

Effecting or carrying out contracts of insurance as principal; and

Assisting in the administration and performance of a contract of insurance.

Scheme operator

Establishing, operating or winding-up collective investment schemes and/or stakeholder pension schemes.

FSMARAO Regulated Activities

16

Home finance

Advising on home finance activities;

Arranging home finance activities; and

Entering into and/or administering a home finance activity.

Agreeing to do most of the above activities.

FSMARAO Specified Investments

17

Deposits;

Electronic money;

Rights under a contract of insurance;

Shares, debentures etc.;

Government and public securities;

Certificates representing certain securities;

Units in a collective investment scheme;

Rights under a personal/stakeholder pension scheme;

Options, futures and contracts for differences;

Rights under regulated mortgage contracts;

Rights under a home reversion plan;

Rights under a home purchase plan; and

Regulated sale and rent back agreements (effective 1 July 2010).

1. Additional oversight

18

Senior management,

Compliance support services Other persons

Senior management

19

Overall responsibility

Risk assessment

Leadership

Treating Customers Fairly

Control

Oversight

Management Information (and KPIs)

Senior management

20

Leadership & Tone From The Top

Business Definition & Purpose

Business Plan

Director/Partner/Management Competence

Risk appetite

Risk Assessment

Capital & Liquidity Assessment (formal ICAAP where needed)

Financial Control

Culture

Competence of advisers and staff

Oversight and Management of people and resources

Senior management

21

Business Metrics – Measuring Performance

Financial Metrics (profit/loss, cashflow/balance sheet)

Performance to Plan

Capital Adequacy

TCF Metrics/Client Feedback

Client Activity Metrics

Compliance/Quality Control/Quality Assurance Metrics

Complaints Data & Metrics

Marketing Activity Metrics

Training and Competence Activity & Metrics

You can’t monitor if you don’t measure!

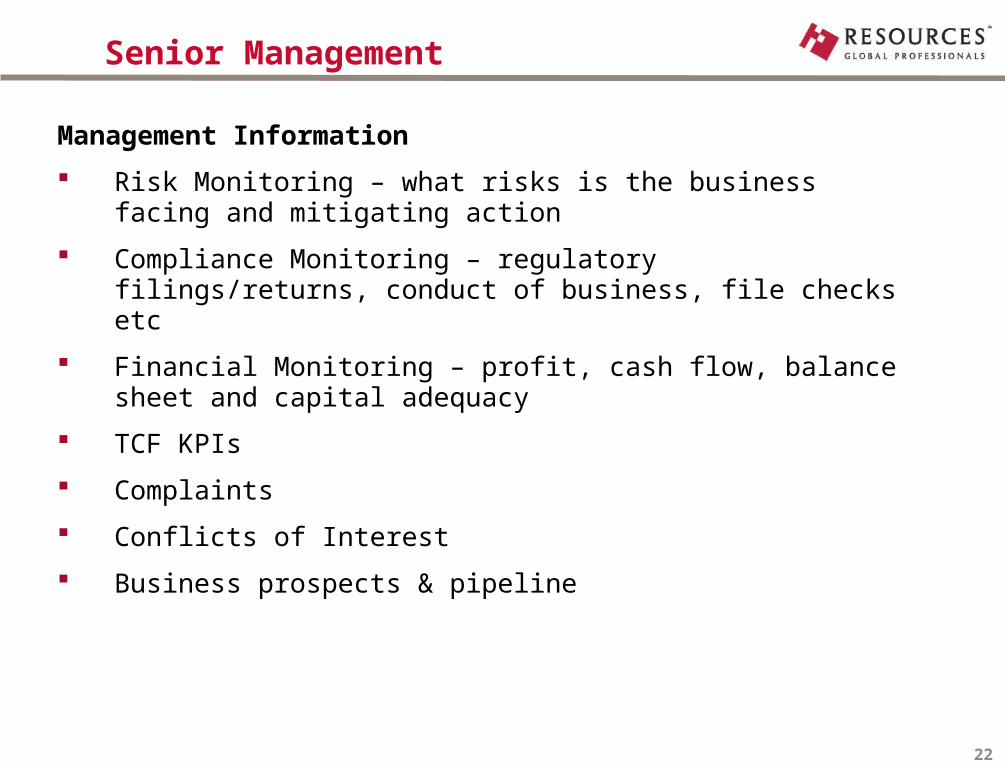

Senior Management

22

Management Information

Risk Monitoring – what risks is the business facing and mitigating action

Compliance Monitoring – regulatory filings/returns, conduct of business, file checks etc

Financial Monitoring – profit, cash flow, balance sheet and capital adequacy

TCF KPIs

Complaints

Conflicts of Interest

Business prospects & pipeline

Senior Management

23

Service/Product Design & Treating Customers Fairly (TCF)

The 6 TCF Consumer Outcomes (COs)

1. Consumers can be confident that they are dealing with firms where the fair treatment of customers is central to the corporate culture.

2. Products and services marketed and sold in the retail market are designed to meet the needs of identified consumer groups and are targeted accordingly.

3. Consumers are provided with clear information and are kept appropriately informed before, during and after the point of sale.

4. Where customers receive advice, the advice is suitable and takes account of their circumstances

5. Consumers are provided with products that perform as firms have led them to expect, and the associated service is both of an acceptable standard and as they have been led to expect.

6. Consumers do not face unreasonable post-sale barriers imposed by firms to change product, switch provider, submit a claim or make a complaint.

Senior Management

24

RETAIL DISTRIBUTION REVIEW (RDR)

RDR READINESS

Independent Advice or Restricted Advice (or Multi-Tied /Tied)

Adviser Firm Remuneration – client agreed remuneration

Professionalism – QCF Level 4 qualification/Gap Fill

Client Agreements/Terms of Business

Branding & Marketing Literature/Website

Compliance support services

25

Internal and/or External

Cannot contract out regulatory obligations

Firms must have a framework for:

assessing and covering the risks to their business;

meeting regulatory requirements; and

checking the firm continues to be compliant.

Compliance support services

26

Using a Compliance Consultant

Compliance is the firm’s responsibility

Establishing the needs: choosing the right service

Assessing and monitoring consultants

Acting on recommendations

Compliance support services

27

In summary: Compliance and controls are always the firm’s responsibility.

The firm must have appropriate processes and controls in place and have a good understanding of the compliance processes and monitoring arrangements it operates.

The firm cannot delegate its responsibility for compliance to another party, but it can get help to ensure its controls are appropriate.

Firms should take action if any reviews undertaken by their consultants reveal weaknesses in their compliance with FSA requirements.

Other persons

28

Accountants

Financial reporting

Capital adequacy

Auditors

Companies Acts statutory audit

Client assets audits

Trustees

exercising their duties under a trust: utmost diligence

exercising discretion: ‘prudent man’