Embed Size (px)

Citation preview

1

New Zealand’s financial services regulation: The continuing wave of change

Presentation to AFMA: 24 April 2012By Lloyd Kavanagh and Jeremy Muir, PartnersMinter Ellison Rudd Watts, Auckland

5438009

2

Agenda

• Financial Markets Authority

• Financial Markets Conduct Bill

• Financial Service Providers registration

• Financial Advisers regulation

• Trans-Tasman mutual recognition

• Anti-Money Laundering regime

• Other developments

A New Regulator: the Financial Markets Authority

3

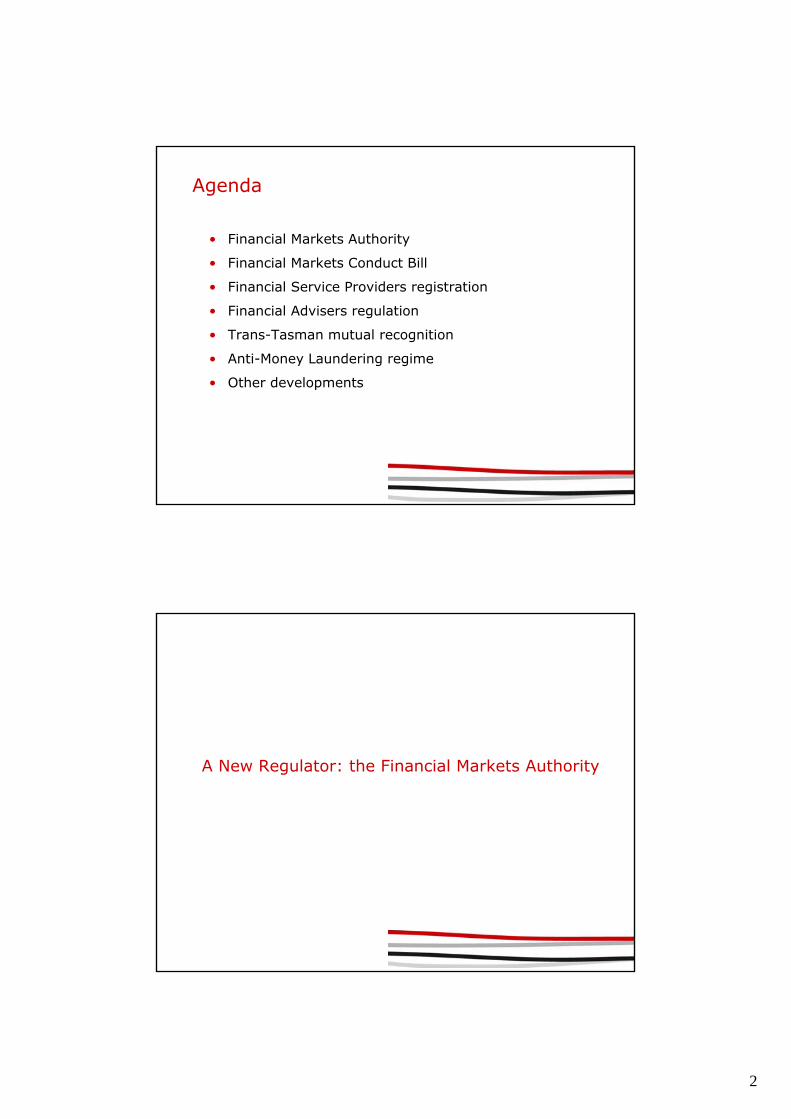

Financial Markets Authority

• New single market conduct regulator

• Took over functions of:

• The Securities Commission;

• The Government Actuary

• Other regulatory functions eg Companies Act, Financial Reporting Act, AMI/CFT Act

• Monitors compliance of financial markets participants

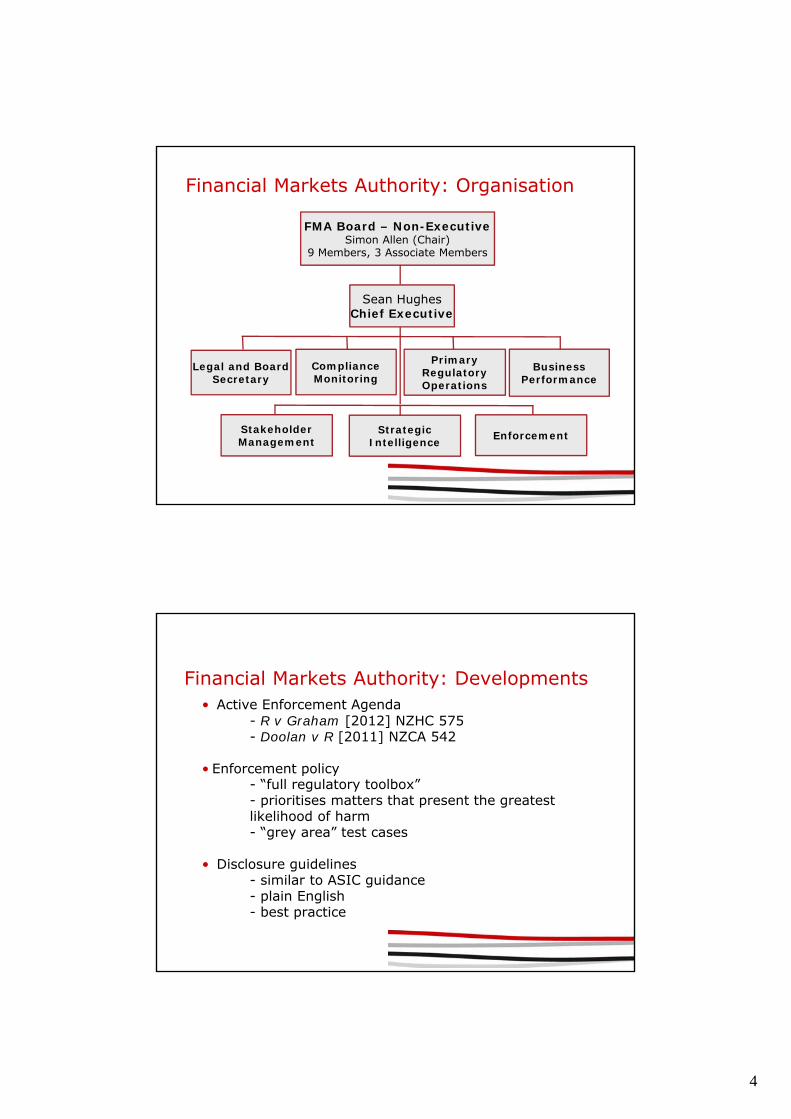

Financial Markets Authority: Organisation

FMA Board – Non-ExecutiveSimon Allen (Chair)

9 Members, 3 Associate Members

Sean HughesChief Executive

Legal and Board Secretary

Compliance Monitoring

Primary Regulatory Operations

Business Performance

Stakeholder Management

Strategic Intelligence Enforcement

4

Financial Markets Authority: Organisation

FMA Board – Non-ExecutiveSimon Allen (Chair)

9 Members, 3 Associate Members

Sean HughesChief Executive

Legal and Board Secretary

Compliance Monitoring

Primary Regulatory Operations

Business Performance

Stakeholder Management

Strategic Intelligence Enforcement

Financial Markets Authority: Developments• Active Enforcement Agenda

- R v Graham [2012] NZHC 575- Doolan v R [2011] NZCA 542

• Enforcement policy- “full regulatory toolbox”- prioritises matters that present the greatest likelihood of harm- “grey area” test cases

• Disclosure guidelines- similar to ASIC guidance- plain English- best practice

5

Financial Markets Conduct Bill

Financial Markets Conduct Bill

•The Bill is “a once-in-a-generation opportunity to re-write our securities law” (Simon Power)

•The Bill is the result of a comprehensive review of securities law and takes into account the work of the Capital Markets Development Taskforce, the effects of the global financial crisis, and the failure of finance companies

•700 clauses (500 pages)

•Regulations to follow

6

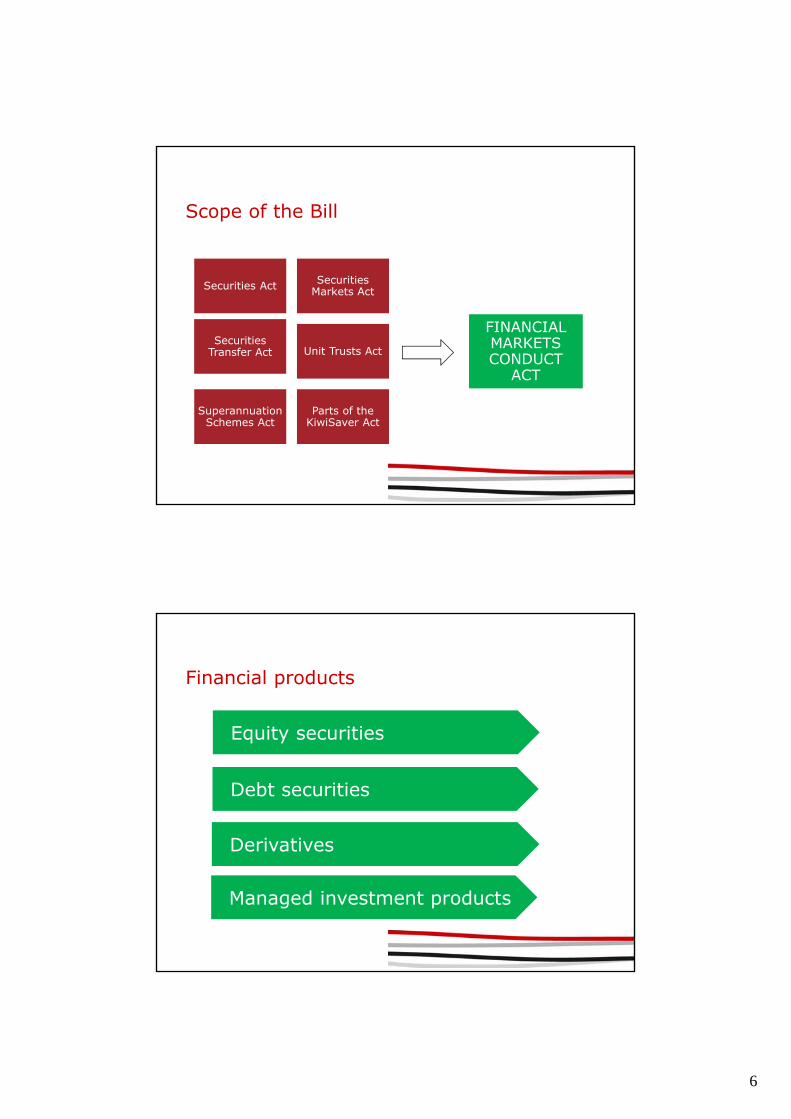

Scope of the Bill

Securities Act Securities Markets Act

Securities Transfer Act Unit Trusts Act

Superannuation Schemes Act

Parts of the KiwiSaver Act

FINANCIAL MARKETS CONDUCT

ACT

Financial products

Equity securities

Debt securities

Derivatives

Managed investment products

7

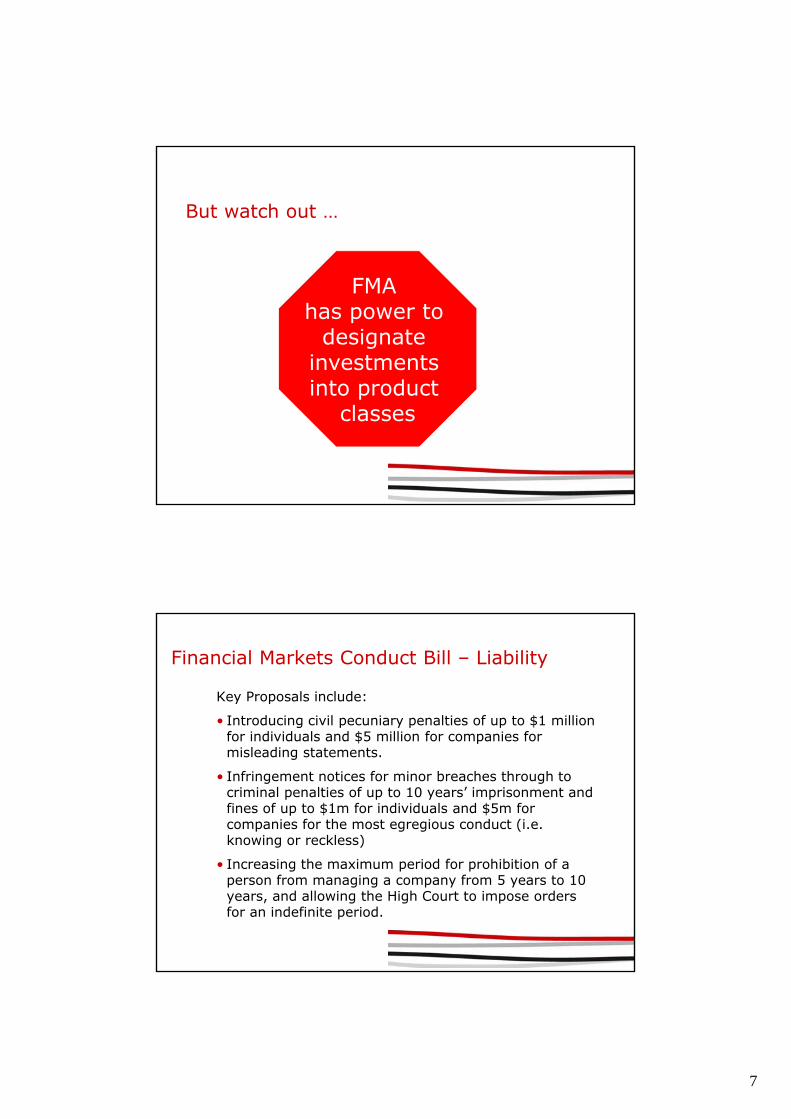

But watch out …

FMA has power to

designate investments into product

classes

Financial Markets Conduct Bill – Liability

Key Proposals include:

• Introducing civil pecuniary penalties of up to $1 million for individuals and $5 million for companies for misleading statements.

• Infringement notices for minor breaches through to criminal penalties of up to 10 years’ imprisonment and fines of up to $1m for individuals and $5m for companies for the most egregious conduct (i.e. knowing or reckless)

• Increasing the maximum period for prohibition of a person from managing a company from 5 years to 10 years, and allowing the High Court to impose orders for an indefinite period.

8

Financial Markets Conduct Bill – Disclosure

Key Proposals include:• Replacing the requirement for issuers to prepare a

prospectus and investment statement with a requirement to prepare a single product disclosure statement (PDS) tailored to retail investors.

• Creation of an online register for offers of financial products which, when read together with the PDS, must contain all material information in relation to an offer of financial products.

So basically disclosure is changing from

9

Financial Markets Conduct Bill – Licensing and MIS

Key proposals include (cont.):• Establishing licensing regimes for specific financial

sector participants: fund managers, independent trustees of workplace superannuation schemes, derivatives dealers, and peer-to-peer lenders.

• Introducing stricter requirements for retail managed investment schemes, including registration requirements, new duties on fund managers and supervisors and stronger governance requirements.

Timetable

•Select Committee for public submissions – until 26 April 2012

•Draft regulations after enactment during 2012?

•New legislation effective (TBC)

•Transitional period • 2 years to transition existing schemes and funds

• New offers: have 12 months from commencement during which can elect either regime

• No allotments allowed under former enactments after 2 years

10

Financial Service Providers (Registration and Dispute Resolution) Act 2008

Financial Service Providers (Registration and Dispute Resolution) Act 2008:

FSP Act: Purpose

• Establish a compulsory register of financial service providers (FSPs)

• Prohibit certain persons from being owners, directors, and senior managers of FSPs

• Conform with New Zealand’s anti-money-laundering obligations

• Improve consumer access to redress and dispute resolution

11

FSP Act: Territorial scope

• Applies any person:

• Ordinarily resident or with a place of business in NZ; or

• Required to be licensed by FMA or RBNZ (eg insurers, banks and financial advisers)

• What is a “place of business”?

Financial Advisers Act 2008

12

Financial Advisers Act: Purpose

• Requires appropriate degree of care by advisers and brokers, and prohibits certain conduct

• Requires disclosure by advisers and brokers to retail clients

• Imposes competency requirements on certain advisers dealing with retail clients

• Ensures advisers accountable for services to retail clients and provides incentives to manage conflicts of interest

Financial Advisers Act: Territorial scope

• Applies, regardless of where the provider is resident, incorporated or carries on business, if the financial adviser service or broking service is received by a client in New Zealand

• In addition, general conduct obligations apply, if the provider is ordinarily resident, incorporated or has a place of business in New Zealand, to financial adviser services or broking services received outside New Zealand

13

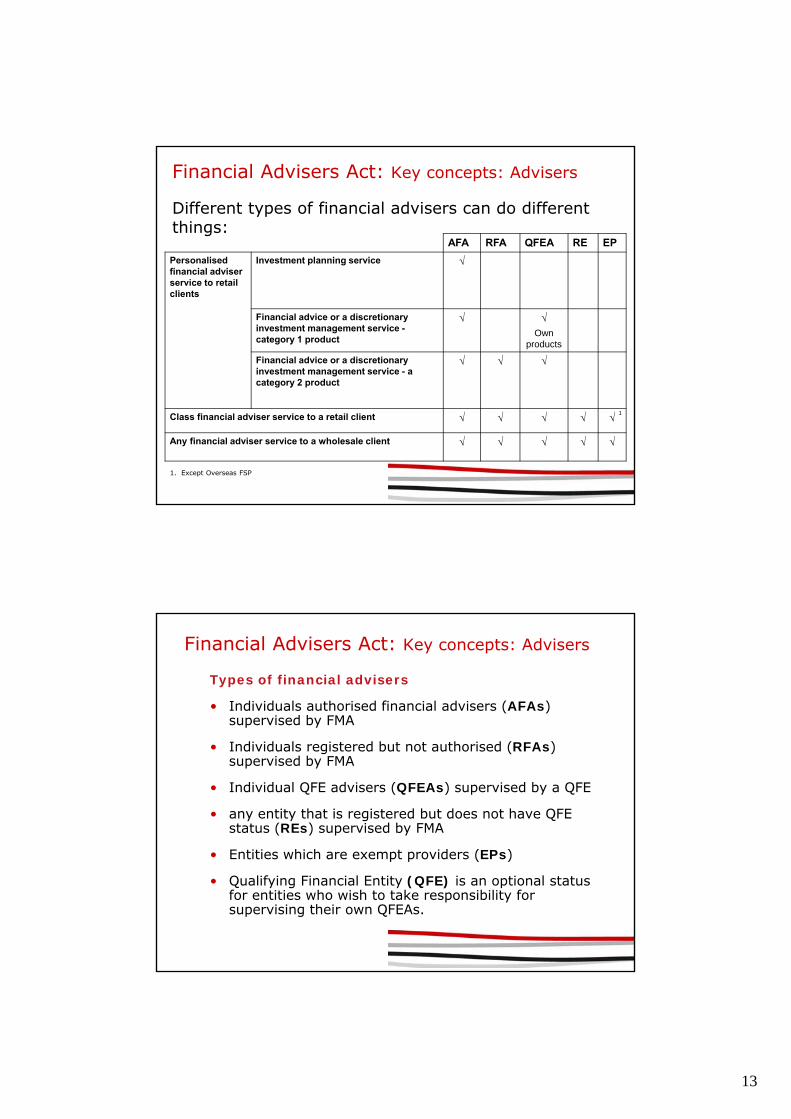

Financial Advisers Act: Key concepts: Advisers

Different types of financial advisers can do different things:

AFA RFA QFEA RE EP

Personalised financial adviser service to retail clients

Investment planning service √

Financial advice or a discretionary investment management service -category 1 product

√ √Own

products

Financial advice or a discretionary investment management service - a category 2 product

√ √ √

Class financial adviser service to a retail client √ √ √ √ √

Any financial adviser service to a wholesale client √ √ √ √ √

1

1. Except Overseas FSP

Types of financial advisers

• Individuals authorised financial advisers (AFAs) supervised by FMA

• Individuals registered but not authorised (RFAs) supervised by FMA

• Individual QFE advisers (QFEAs) supervised by a QFE

• any entity that is registered but does not have QFE status (REs) supervised by FMA

• Entities which are exempt providers (EPs)

• Qualifying Financial Entity (QFE) is an optional status for entities who wish to take responsibility for supervising their own QFEAs.

Financial Advisers Act: Key concepts: Advisers

14

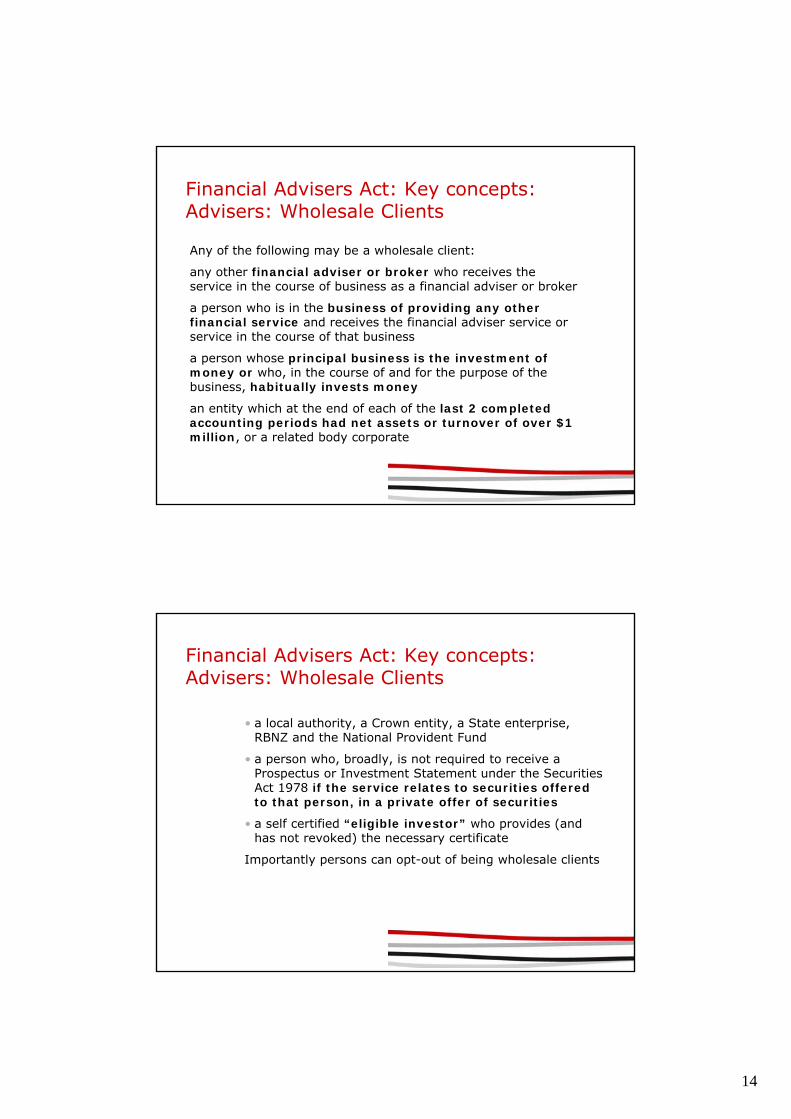

Financial Advisers Act: Key concepts: Advisers: Wholesale Clients

Any of the following may be a wholesale client:

any other financial adviser or broker who receives the service in the course of business as a financial adviser or broker

a person who is in the business of providing any other financial service and receives the financial adviser service or service in the course of that business

a person whose principal business is the investment of money or who, in the course of and for the purpose of the business, habitually invests money

an entity which at the end of each of the last 2 completed accounting periods had net assets or turnover of over $1 million, or a related body corporate

Financial Advisers Act: Key concepts: Advisers: Wholesale Clients

• a local authority, a Crown entity, a State enterprise, RBNZ and the National Provident Fund

• a person who, broadly, is not required to receive a Prospectus or Investment Statement under the Securities Act 1978 if the service relates to securities offered to that person, in a private offer of securities

• a self certified “eligible investor” who provides (and has not revoked) the necessary certificate

Importantly persons can opt-out of being wholesale clients

15

Australian Financial Advisers and the New Zealand Market

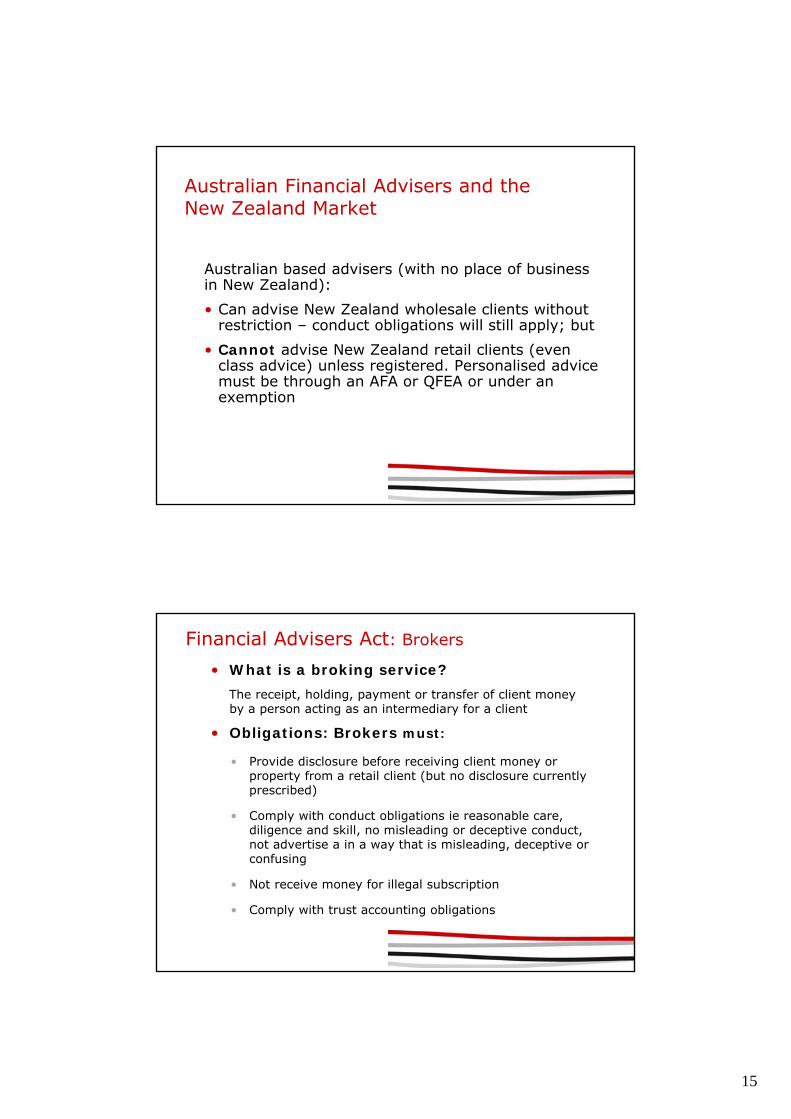

Australian based advisers (with no place of business in New Zealand):• Can advise New Zealand wholesale clients without

restriction – conduct obligations will still apply; but• Cannot advise New Zealand retail clients (even

class advice) unless registered. Personalised advice must be through an AFA or QFEA or under an exemption

Financial Advisers Act: Brokers

• What is a broking service?The receipt, holding, payment or transfer of client money by a person acting as an intermediary for a client

• Obligations: Brokers must:

• Provide disclosure before receiving client money or property from a retail client (but no disclosure currently prescribed)

• Comply with conduct obligations ie reasonable care, diligence and skill, no misleading or deceptive conduct, not advertise a in a way that is misleading, deceptive or confusing

• Not receive money for illegal subscription

• Comply with trust accounting obligations

16

Trans-Tasman Mutual Recognition of Securities Offerings

Trans-Tasman Mutual Recognition of Securities Offerings

● What is it?• Issuer can offer securities or interests in collective

or managed investment schemes in both countries using one disclosure document

• Comply with minimal entry and ongoing requirements agreed to between the two countries and prescribed in each country's law

● Who runs it?• Australia – the Australian Securities and

Investments Commission (ASIC)• NZ - the Registrar of Companies and the

Securities Commission – now the Financial Markets Authority (FMA)

17

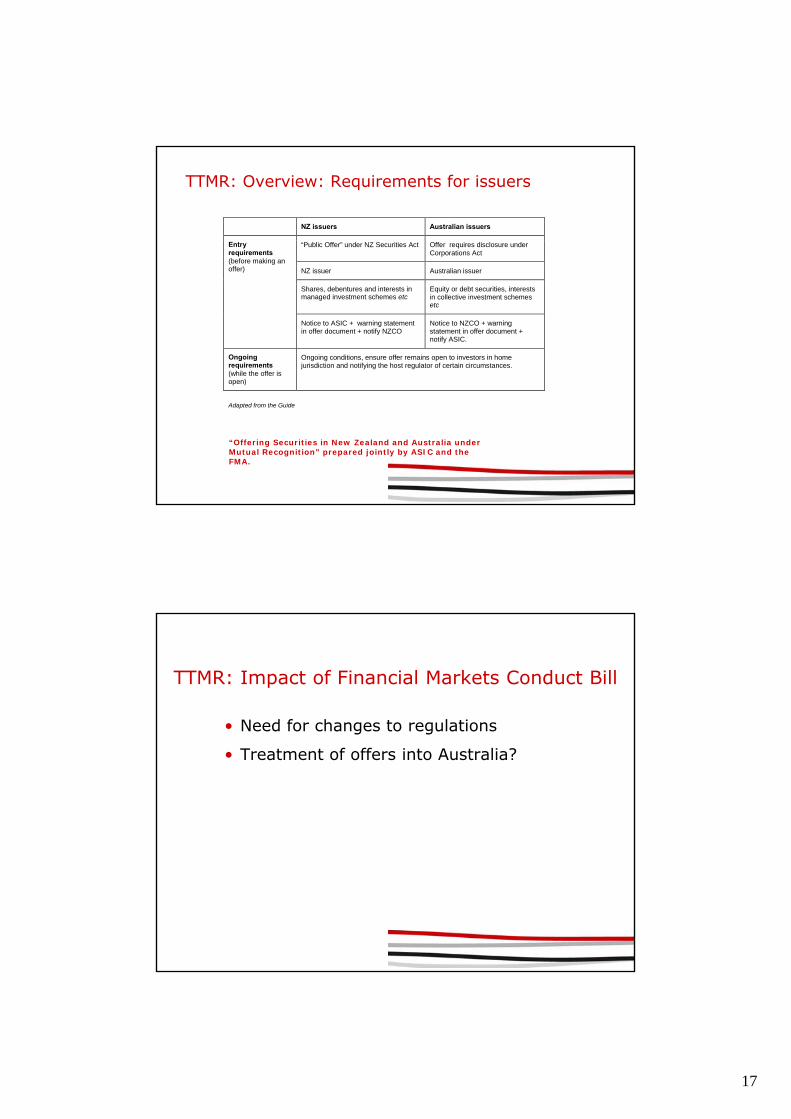

TTMR: Overview: Requirements for issuers

NZ issuers Australian issuers

“Public Offer” under NZ Securities Act Offer requires disclosure under Corporations Act

NZ issuer Australian issuer

Shares, debentures and interests in managed investment schemes etc

Equity or debt securities, interests in collective investment schemes etc

Entry requirements (before making an offer)

Notice to ASIC + warning statement in offer document + notify NZCO

Notice to NZCO + warning statement in offer document + notify ASIC.

Ongoing requirements (while the offer is open)

Ongoing conditions, ensure offer remains open to investors in home jurisdiction and notifying the host regulator of certain circumstances.

Adapted from the Guide

“Offering Securities in New Zealand and Australia under Mutual Recognition” prepared jointly by ASIC and the FMA.

TTMR: Impact of Financial Markets Conduct Bill

• Need for changes to regulations

• Treatment of offers into Australia?

18

AML/CFT Act Combating Money Launderers and Terrorists

AML/CFT: Key messages

• Act now in force – clock is ticking on implementation – 30 June 2013 go live

• Exemption Applications now

• Regime similar, but not identical to Australian regime

• Many NZ market participants behind the game

19

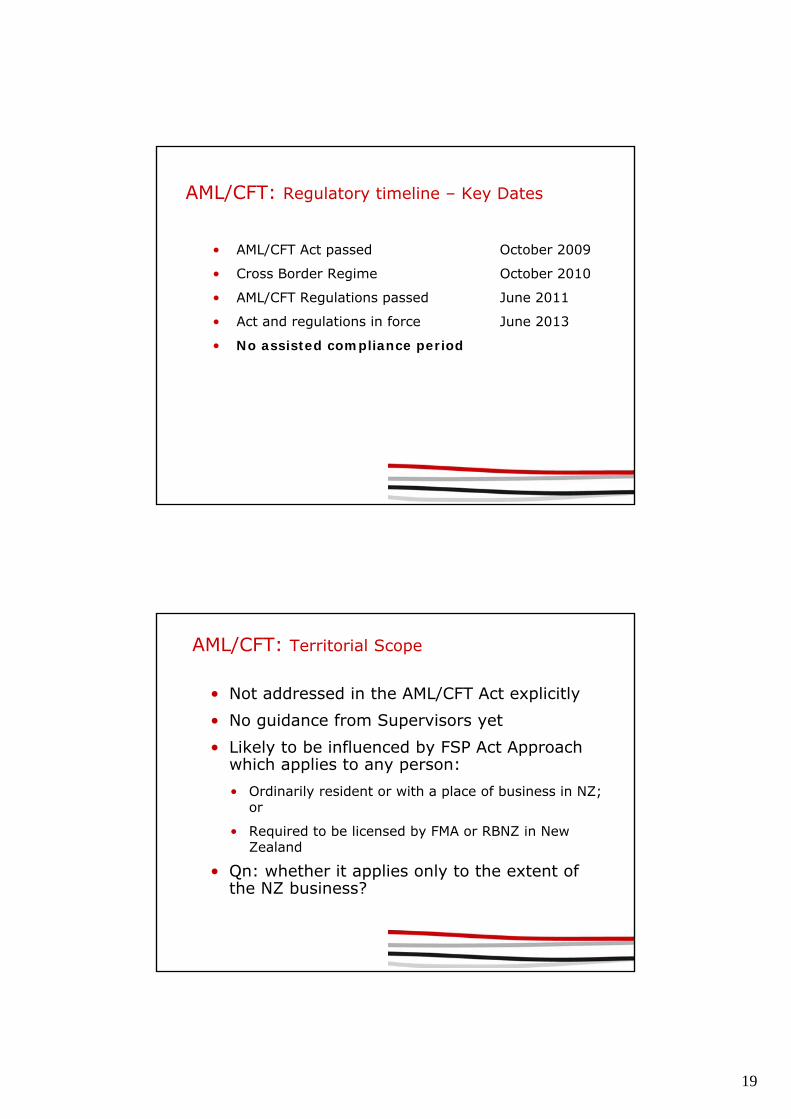

AML/CFT: Regulatory timeline – Key Dates

• AML/CFT Act passed October 2009

• Cross Border Regime October 2010

• AML/CFT Regulations passed June 2011

• Act and regulations in force June 2013

• No assisted compliance period

AML/CFT: Territorial Scope

• Not addressed in the AML/CFT Act explicitly• No guidance from Supervisors yet• Likely to be influenced by FSP Act Approach

which applies to any person:• Ordinarily resident or with a place of business in NZ;

or

• Required to be licensed by FMA or RBNZ in New Zealand

• Qn: whether it applies only to the extent of the NZ business?

20

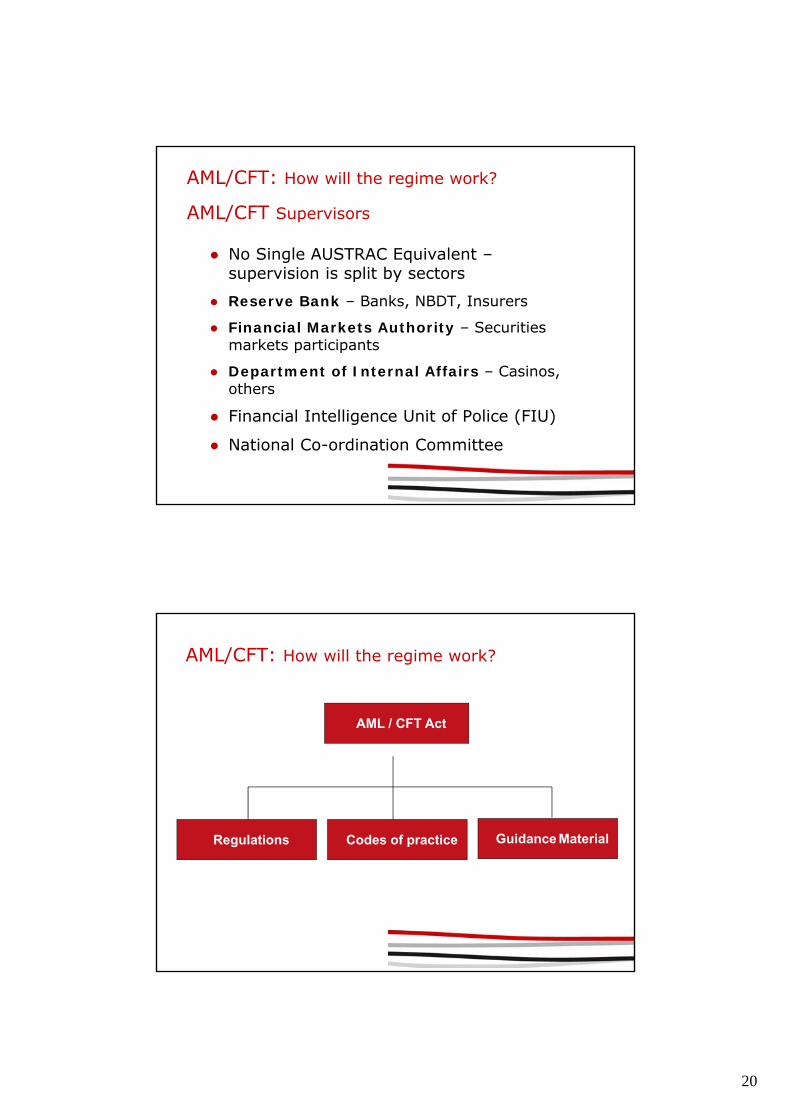

AML/CFT: How will the regime work?

AML/CFT Supervisors

● No Single AUSTRAC Equivalent –supervision is split by sectors

● Reserve Bank – Banks, NBDT, Insurers

● Financial Markets Authority – Securities markets participants

● Department of Internal Affairs – Casinos, others

● Financial Intelligence Unit of Police (FIU)

● National Co-ordination Committee

AML/CFT: How will the regime work?

AML / CFT Act

Regulations Codes of practice Guidance Material

21

AML/CFT: How will the regime work?

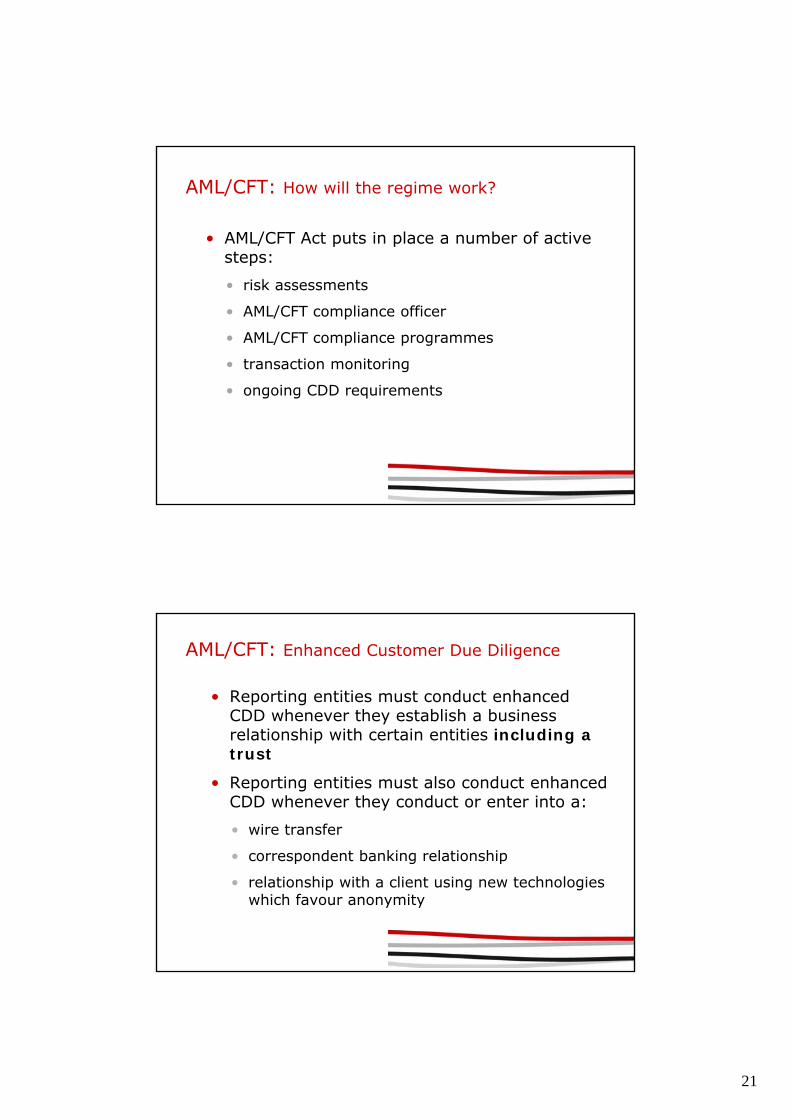

• AML/CFT Act puts in place a number of active steps:

• risk assessments

• AML/CFT compliance officer

• AML/CFT compliance programmes

• transaction monitoring

• ongoing CDD requirements

AML/CFT: Enhanced Customer Due Diligence

• Reporting entities must conduct enhanced CDD whenever they establish a business relationship with certain entities including a trust

• Reporting entities must also conduct enhanced CDD whenever they conduct or enter into a:

• wire transfer

• correspondent banking relationship

• relationship with a client using new technologies which favour anonymity

22

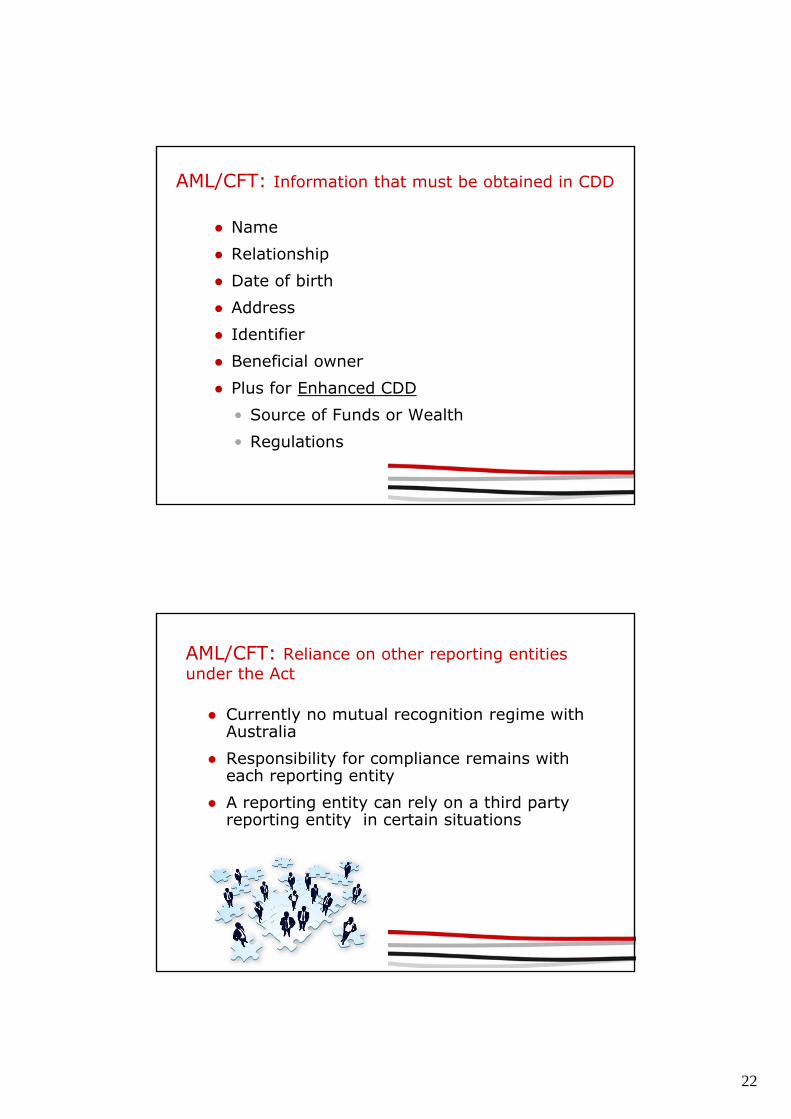

AML/CFT: Information that must be obtained in CDD

● Name● Relationship● Date of birth● Address● Identifier● Beneficial owner● Plus for Enhanced CDD

• Source of Funds or Wealth• Regulations

AML/CFT: Reliance on other reporting entities under the Act

● Currently no mutual recognition regime with Australia

● Responsibility for compliance remains with each reporting entity

● A reporting entity can rely on a third party reporting entity in certain situations

23

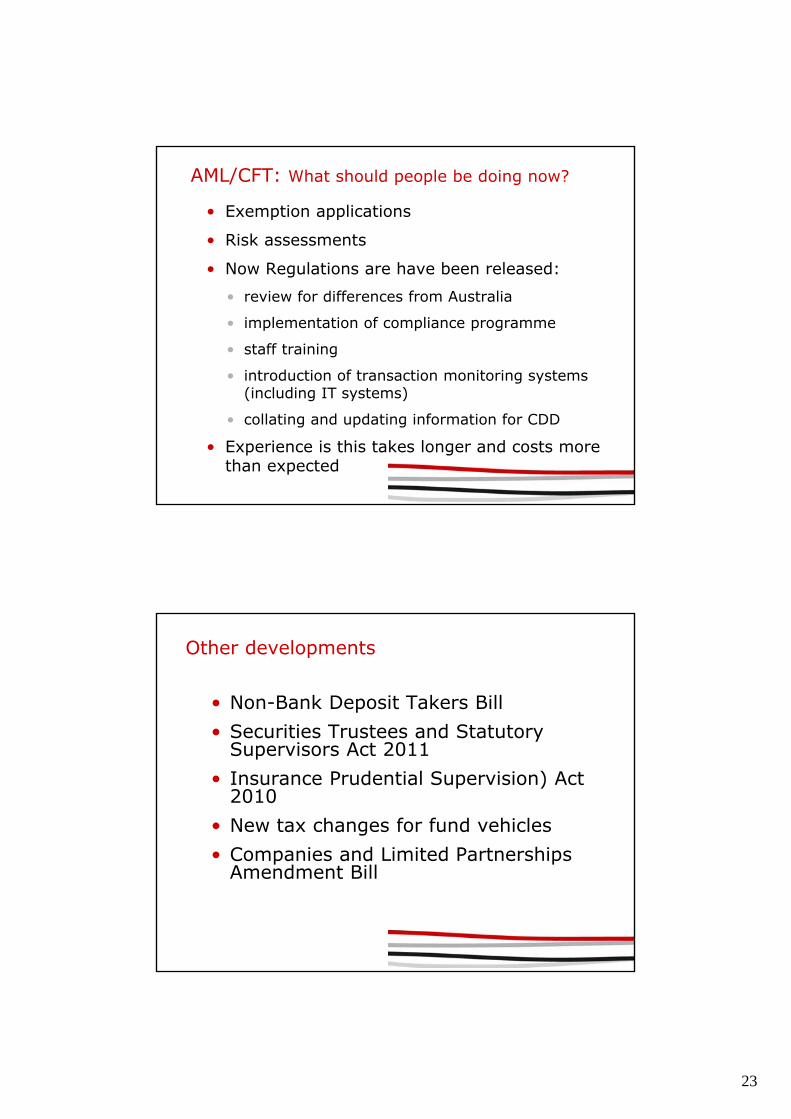

AML/CFT: What should people be doing now?

• Exemption applications

• Risk assessments

• Now Regulations are have been released:

• review for differences from Australia

• implementation of compliance programme

• staff training

• introduction of transaction monitoring systems (including IT systems)

• collating and updating information for CDD

• Experience is this takes longer and costs more than expected

Other developments

• Non-Bank Deposit Takers Bill• Securities Trustees and Statutory

Supervisors Act 2011• Insurance Prudential Supervision) Act

2010 • New tax changes for fund vehicles• Companies and Limited Partnerships

Amendment Bill

24

Disclaimer

The information contained in this update is intended as aguide only. Professional advice should be sought beforeapplying any of the information to particular circumstances.While every reasonable care has been taken in the preparationof this update, Minter Ellison Rudd Watts does not acceptliability for any errors it may contain.

Lloyd Kavanagh Partner T +64 9 353 9976 M +64 21 786 172 Jeremy Muir Partner T +64 9 353 9819 M +64 21 625 319Kara Daly Special Counsel T +64 4 498 5008 M +64 27 450 0693 Darryl Hong Senior Associate T +64 9 353 9916 M +64 21 265 9136 Karen Mace Senior Associate T +64 4 498 5106 M +64 21 221 7513

Team contacts

EMAIL [email protected]

25