Embed Size (px)

Citation preview

The impact of the EU ETS on European energy and carbon markets

David Newbery

Danish Environmental Economic ConferenceSkodsborg Hotel 23 August 2010

http://www.eprg.group.cam.ac. uk

D Newbery Copenhagen 2010 2

Outline• Climate Change Challenge

– more carbon underground than we should release

– Kyoto then ETS sets targets

• The logic of EU targets

• GHG targets and the EU ETS

• EU 20-20-20 Directive and ETS

• R&D andEU SET Plan

D Newbery Copenhagen 2010 3

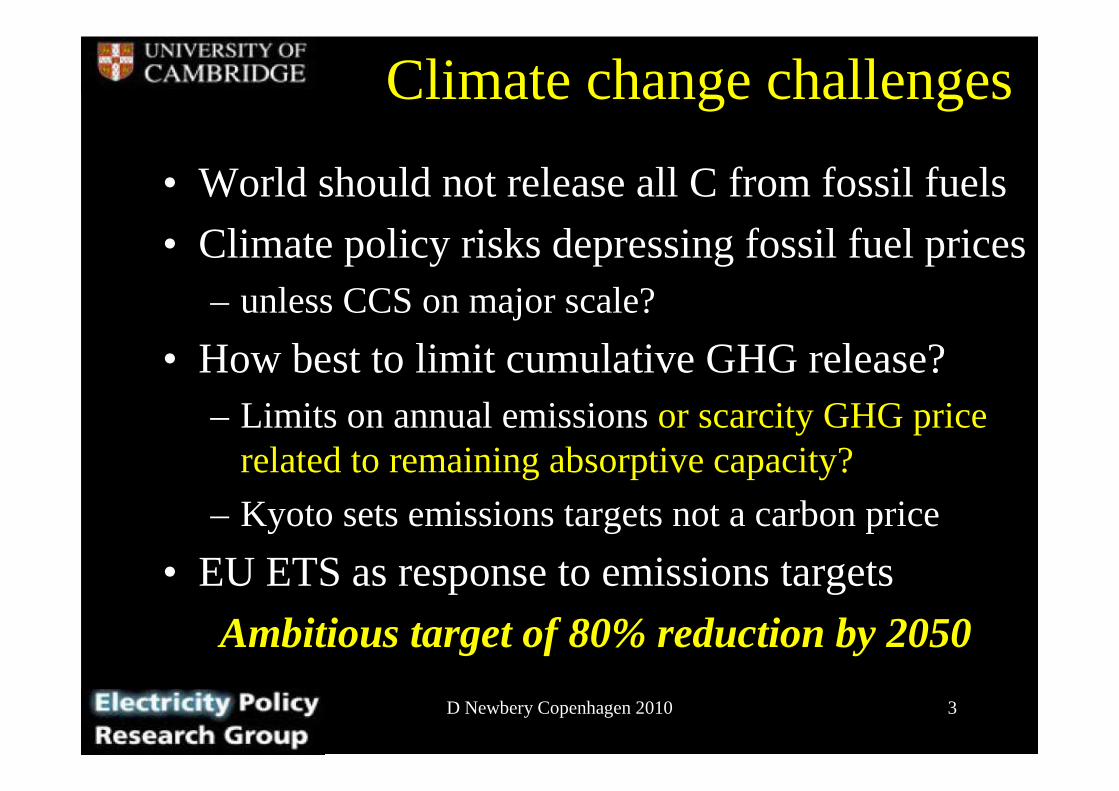

Climate change challenges

• World should not release all C from fossil fuels

• Climate policy risks depressing fossil fuel prices– unless CCS on major scale?

• How best to limit cumulative GHG release?– Limits on annual emissions or scarcity GHG price

related to remaining absorptive capacity?

– Kyoto sets emissions targets not a carbon price

• EU ETS as response to emissions targets

Ambitious target of 80% reduction by 2050

MR Allen et al. Nature 458, 1163-1166(2009)doi:10.1038/nature08019

Peak CO2-warming vs cumulative emissions 1750–2500

Now

Proven L H

Unconventional oil +gas

Resource

If we want a 50% chance of lessthan 2oC rise we can only useanother 500 Gt C ever!

D Newbery Copenhagen 2010 5

The logic of EU targets

• easy to determine “fair” allocation– and can buy off opponents with free allocations

• does not impinge on sovereign tax powers– EU carbon tax failed

• easier to give impression of leadership/action– without spelling out costs

– ETS => electricity prices ⇑ unanticipated by voters

Targets should be translated into sensible policy

6

EUA price October 2004-April 2010

0

5

10

15

20

25

30

35

Oct-04 Apr-05 Sep-05 Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09 Mar-10

Eur

o/t

CO

2

Futures Dec 2007OTC IndexSecond period Dec 2008Second period next DecCER 09

start of ETS

Second period

CO2 prices are volatile and now too low

Actual emissions revealed

D Newbery Copenhagen 2010 7

Effect of quota driven ETS

• Scarcity of EUAs determines EUA price– rather than long-run view of required carbon price

• Fuel cost + EUA of marginal plant sets electricity price

• When coal and gas competitive in electricity market

– EUA price set by coal-gas relative price

=> coal and gas-fired plant costs move together

Lax quantity target keeps coal competitive

Discourages greater CO2 reduction

D Newbery Copenhagen 2010 8NETA\Pxdata\fuel_choice

Fuel choices in UK electricity generation, 2000-10

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

0 2 4 6 8 10 12 14 16 18 20 22

Coal price Euros/MWht

Gas

pric

e E

uros

/MW

ht

Fuel post ETS

fuel pre-ETS

fuel +EUA cost Phase I

fuel + EUA Phase II

Gas cheaper than coal

Coal cheaper than gas

Coal 38%, gas 50%

Coal 34%, gas 55%

EUAs can make coal and gas competitive in GB

D Newbery Copenhagen 2010 9

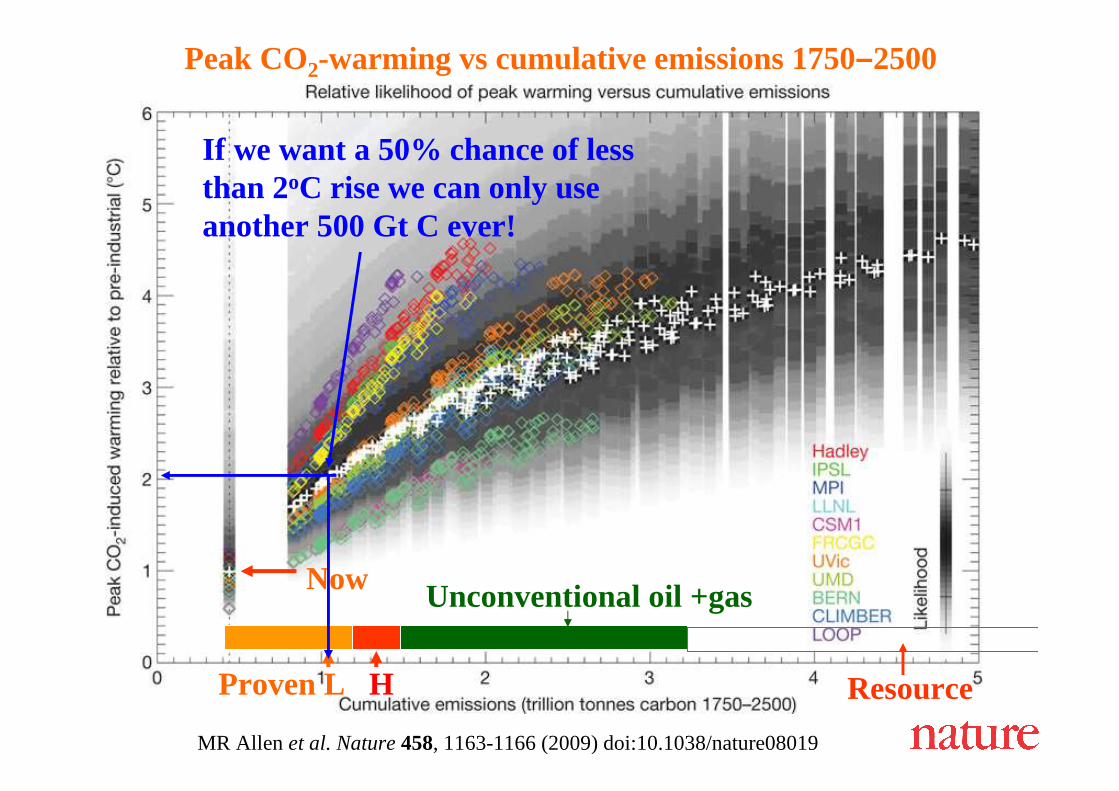

UK price movements: 2007 to 2009 in €

0

20

40

60

80

100

120

1-Ja

n-07

1-Apr-

07

1-Ju

l-07

1-Oct

-07

1-Ja

n-08

1-Apr

-08

1-Ju

l-08

1-O

ct-0

8

1-Jan

-09

€/M

Wh

e

Electricity forward 2010 (€/MWh)

Gas cost forward (2010) + EUA

Coal cost forward (2010) + EUA

EUA price in €/tCO2

Correlation of coal+EUA on gas+EUA high at 96%Source: Bloomberg data

D Newbery Copenhagen 2010 10

Collapse in EUA price impacts electricity pricesForward base year contracts - France and Germany Aug 2005-May 2006

0

10

20

30

40

50

60

70

29-Aug-05

13-Sep-05

28-Sep-05

13-Oct-05

28-Oct-05

12-Nov-05

27-Nov-05

12-Dec-05

27-Dec-05

11-Jan-06

26-Jan-06

10-Feb-06

25-Feb-06

12-Mar-06

27-Mar-06

11-Apr-06

26-Apr-06

11-May-

06

Eur

os/M

Wh

FR base 2007

DE base 2007

EUA coalcost

EUA gas cost

Source: EEX

D Newbery Copenhagen 2010 11

But not price less EUA cost => EUA directly feeds through to electricity price

Forward 2007 annual prices - France and Germany 2006

0

10

20

30

40

50

60

70

80

90

1-Ja

n-06

16-Ja

n-06

31-Ja

n-06

15-F

eb-06

2-Mar

-06

17-M

ar-06

1-Apr-0

6

16-A

pr-06

1-May

-06

16-M

ay-06

Eur

os/M

Wh

FR peak less gasEUA

DE peak less gasEUA

FR base less gasEUA

DE base less gasEUA

DE base less coalEUA

coal EUA cost

EUA cost inCCGT

Source: EEX

D Newbery Copenhagen 2010 12

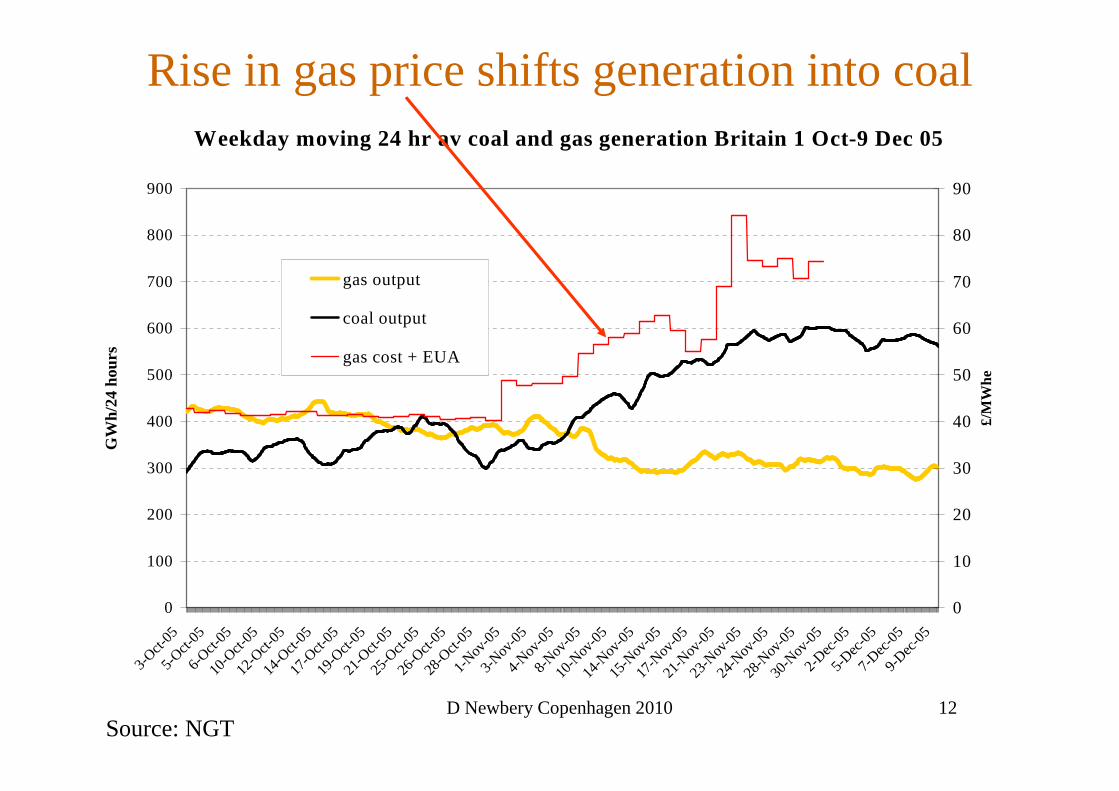

Rise in gas price shifts generation into coalWeekday moving 24 hr av coal and gas generation Britain 1 Oct-9 Dec 05

0

100

200

300

400

500

600

700

800

900

3-Oct-

055-

Oct-05

6-Oct-

0510

-Oct-

0512

-Oct-

0514

-Oct-

0517

-Oct-

0519

-Oct-

0521

-Oct-

0525

-Oct-

0526

-Oct-

0528

-Oct-

051-

Nov-0

53-

Nov-0

54-

Nov-0

58-

Nov-0

510

-Nov

-05

14-N

ov-0

515

-Nov

-05

17-N

ov-0

521

-Nov

-05

23-N

ov-0

524

-Nov

-05

28-N

ov-0

530

-Nov

-05

2-Dec

-05

5-Dec

-05

7-Dec

-05

9-Dec

-05

GW

h/24

hou

rs

0

10

20

30

40

50

60

70

80

90

£/M

Whe

gas output

coal output

gas cost + EUA

Source: NGT

D Newbery Copenhagen 2010 13

Impact on gas market

• Suppose gas price increases– initially: demand falls (fuel switch gas => coal)

=> demand for EUAs rises => EUA price ⇑

=> partially offsets advantage of coal

=> offsets some demand reduction for gas

=> reduces elasticity of demand for gas, ε– Lerner Index (p-c)/p = 1/ε=> increases market power of gas suppliers

• Gazprom, and suppliers with protected markets

Bad idea

D Newbery Copenhagen 2010 14

Demand for gas

Demand for gas in ESI

Priceof Gasg

Price rise

Initial demand fall (gas-coal)

EUA price rise induces someswitch back to gas

Demand for gas if EUA price constant

Demand for gas if EUA price varies

D Newbery Copenhagen 2010 15

Policy implications

• Imposing extra constraint on market reduces demand elasticities, amplifies market power

• If the price of EUAs is independent of gas demand then there is no multiplier effect=> banking over longer periods helps

• Other reasons for fixing C-price, not quantity:

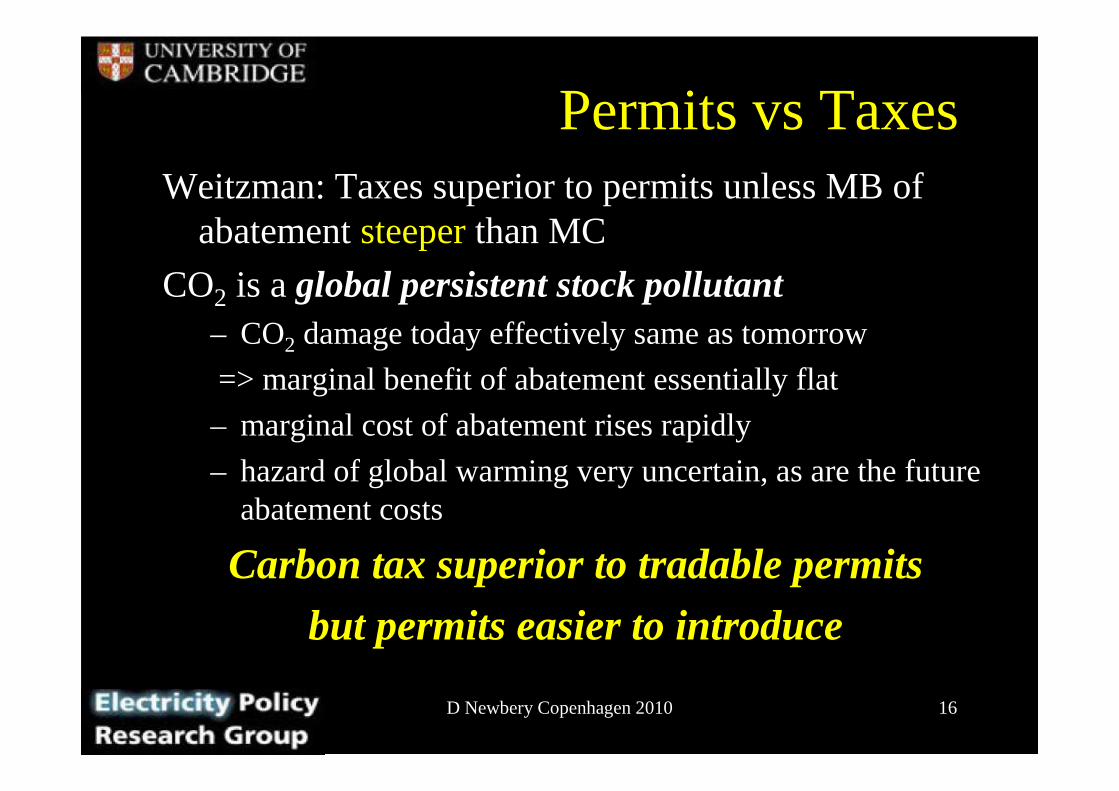

Prices vs Quantities (Weitzman, 1974)

D Newbery Copenhagen 2010 16

Permits vs TaxesWeitzman: Taxes superior to permits unless MB of

abatement steeperthan MC

CO2 is a global persistent stock pollutant– CO2 damage today effectively same as tomorrow

=> marginal benefit of abatement essentially flat

– marginal cost of abatement rises rapidly

– hazard of global warming very uncertain, as are the future abatement costs

Carbon tax superior to tradable permits

but permits easier to introduce

D Newbery Copenhagen 2010 17Newbery IIB 1 17

Start of ETS

Costs of errors setting prices or quantities

Reductions in emissions

Correct MC

MC

Best estimate of Marginal cost of abatement

MB, Marginal benefit from abatement

£/tC

efficiency lossfrom charge

efficiency lossfrom quota

t

Q* Q

t*

D Newbery Copenhagen 2010 18

Reforming ETS

• Reform EU ETS to provide rising price floor– sufficient for nuclear or on-shore wind or CCS

• Commitment to raise CO2 price at 3% p.a. over life of plant may suffice– €25/EUA 2010 => €34 in 2020, €61 in 2040 ...

• Making it credible: write CfD on this path– offer CfD at €45/EUA for 20y from commissioning?

makes extra carbon savings additional

D Newbery Copenhagen 2010 19

Carbon tax alternative

• Each Member State imposes a Carbon tax – tax bads not goods as part of fiscal adjustment

– rebated by EUA price for covered sector

– can start low: €20/t CO2 and escalate at 5% p.a. above RPI = €34/t by 2020

• Tax or full EUA auctioning to finance SET-Plan and RES, avoid taxing electricity

D Newbery Copenhagen 2010 20

Supporting RD&D

• 80% GHG reduction => decarbonising electricity

• Zero-C electricity requires renewables– and CCS + nuclear

• RES is not yet commercial (except in niches)– requires support now to drive down future costs

• R&D + deployment drives innovation and learning

• But RD&D is a public good benefiting the whole world

So how to gain collective support for RD&D?

D Newbery Copenhagen 2010 21

ETS and Renewables

• Aim: deliver low-C solutions for world

• Need to explore a portfolio of possible solutions– Then select those which show most promise

• Danger with RES target – choose cheapest– Fortunately MS have differing resources to explore

– And differing aspirations to industrial leadership

20-20-20 Directive: least bad feasible solution?

D Newbery Copenhagen 2010 22

Experience curves justify deployment support

Source: IEA

D Newbery Copenhagen 2010 23

2050 projected CO2 price

0

10

20

30

40

50

60

70

with 12.5% renewables with 20% renewables 2009 projections

Eur

os/to

nne

CO

2

Source: Committee on Climate Change, 2008 and 2009

2008 projections 2009 projections

after Renewables Directive andrecessionRenewables

depressesC-price

D Newbery Copenhagen 2010 24

Failures of ETS

• Current ETS sets quota for total EU emissions

• Renewables Directive increases RES=> increased RES does not reduce CO2

=> but does reduce price of EUAs

=> prejudices other low-C generation like nuclear

• Risks undermining support for RES

Solved by fixing EUA price instead of quota

D Newbery Copenhagen 2010 25

Reforming 2020 Directive• Not to reduce CO2 - ETS ensures no impact

– ETS intended to price CO2– but fails to give credible signals

• not to support low-C generation, only RES

=> support to RD&D to drive down costs of RES

• How? Support investment or generation?

• Learning comes from:– design (cost, reliability, controllability, etc)

– production, installation, siting/planning, grid integration

but not from operation (provided reliable)

D Newbery Copenhagen 2010 26

Implications for RES support• No RES should bid below SRMC

– Given that it can rapidly reduce output=> support should be for availability, not output

• RES should not have automatic priority– merit order should be based on avoided costs

=> if RES is more costly than alternatives (including balancing, redispatch), back it off=> foregone RES generation should count to RES

target (as it has no CO2 credit)– unless ETS reformed to support CO2 price

D Newbery Copenhagen 2010 27

Conclusions• ETSto price CO2

– but volatile, price too low, impacts gas market power• RES Directiveto support deployment and learning

=> Well defined MS funding in place through obligations• But RES Directive undermines ETS

– risks bringing ETS into disrepute=> Reform ETS – provide floor price

– de-links gas and coal markets– reduces risk of low-C generation investment– makes Renewables contribute to reduced emissions

• Failing which encourage MS to impose C tax– With rebates for EUA’s surrendered

The impact of the EU ETS on European energy and carbon markets

David Newbery

Danish Environmental Economic ConferenceSkodsborg Hotel 23 August 2010

http://www.eprg.group.cam.ac. uk

Spare slides on SET-Plan

D Newbery Copenhagen 2010 30

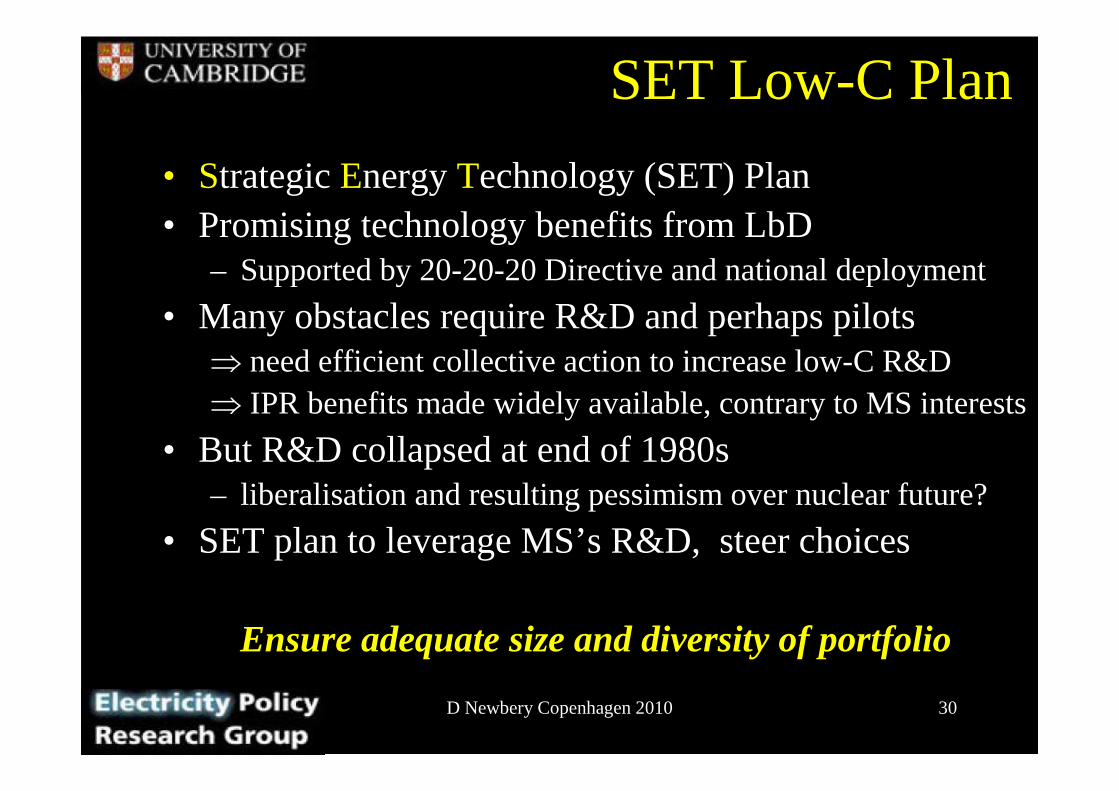

SET Low-C Plan

• Strategic Energy Technology (SET) Plan• Promising technology benefits from LbD

– Supported by 20-20-20 Directive and national deployment

• Many obstacles require R&D and perhaps pilots⇒ need efficient collective action to increase low-C R&D⇒ IPR benefits made widely available, contrary to MS interests

• But R&D collapsed at end of 1980s– liberalisation and resulting pessimism over nuclear future?

• SET plan to leverage MS’s R&D, steer choices

Ensure adequate size and diversity of portfolio

D Newbery Copenhagen 2010 31

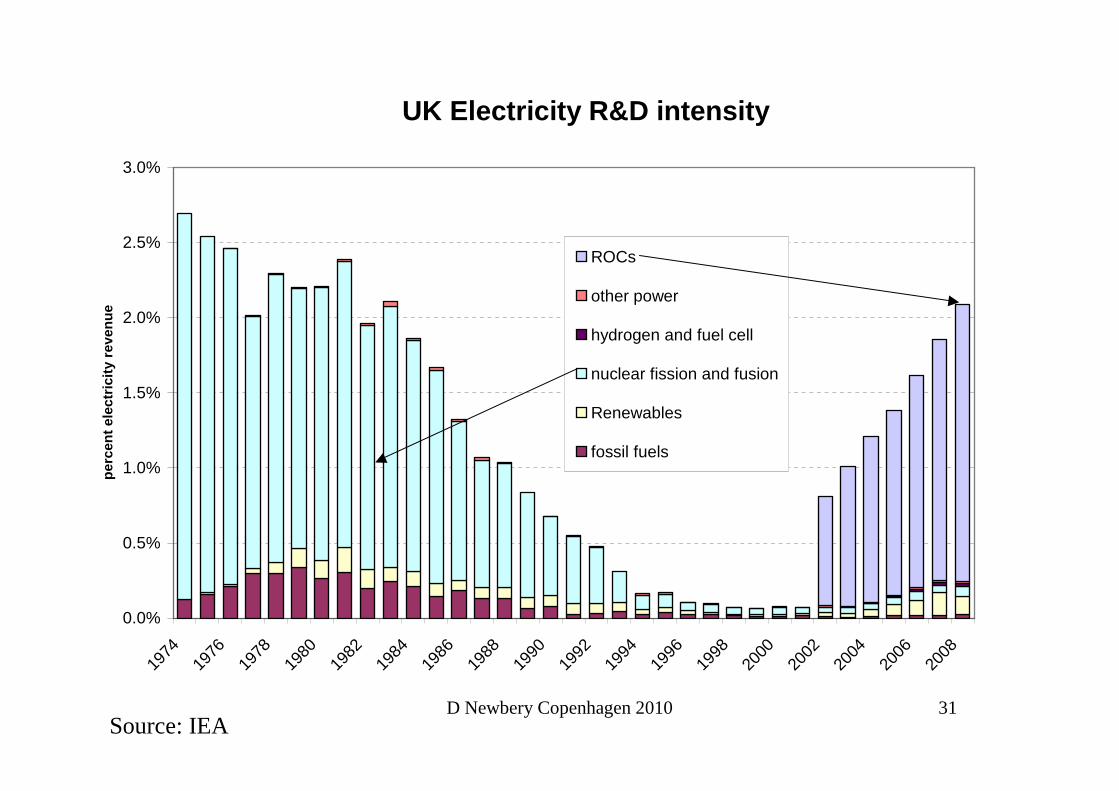

UK Electricity R&D intensity

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

perc

ent e

lect

ricity

rev

enue

ROCs

other power

hydrogen and fuel cell

nuclear fission and fusion

Renewables

fossil fuels

Source: IEA

D Newbery Copenhagen 2010 32

UK Renewables R&D intensity (3-yr moving average)

0.00%

0.05%

0.10%

0.15%

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

perc

ent e

lect

ricity

rev

enue

geo-thermal

bio-energy

ocean

wind

solar

Source: IEA

D Newbery Copenhagen 2010 33

SET support schemes

• 2007 SET R&D non-nuclear ∼ €2.4bn (Nuclear €0.94)– 70:30 private:public; 80:20 MS:EC

• SET plan to 2020 total €70 bn or double current rate– Grid: €2bn; fuel cells + H2: €5bn; Wind: €6bn;

– nuclear fission €7bn; bio-energy € 9bn;

– smart cities €11 bn; CCS €13 bn; Solar: €16bn;

• Joint programming to amplify MS R&D– CCS as an example

ETS auction revenues as funding source?

D Newbery Copenhagen 2010 34

Three pillars of EU low-C policy

• ETSto price CO2

– for mature low-C investments - reform needed

• 20-20-20 Directive: demand pull for renewables– justified by learning spillovers and burden sharing

– induces near-commercial low-C deployment

• EU SET-Plan to treble R&D spend– to support less mature low-C options

Ensure they work together not in conflict