Embed Size (px)

DESCRIPTION

The New EU ETS and the Global Carbon Market Montréal 2010. Dr Nicola Notaro Deputy Head of the Water Unit DG Environment, European Commission. Context. Political framework. Overall EU objective: limit global warming to 2° C above pre-industrial level to avoid dangerous climate change - PowerPoint PPT Presentation

Citation preview

The New EU ETS and the

Global Carbon Market Montréal 2010

Dr Nicola Notaro

Deputy Head of the Water UnitDG Environment, European Commission

Context

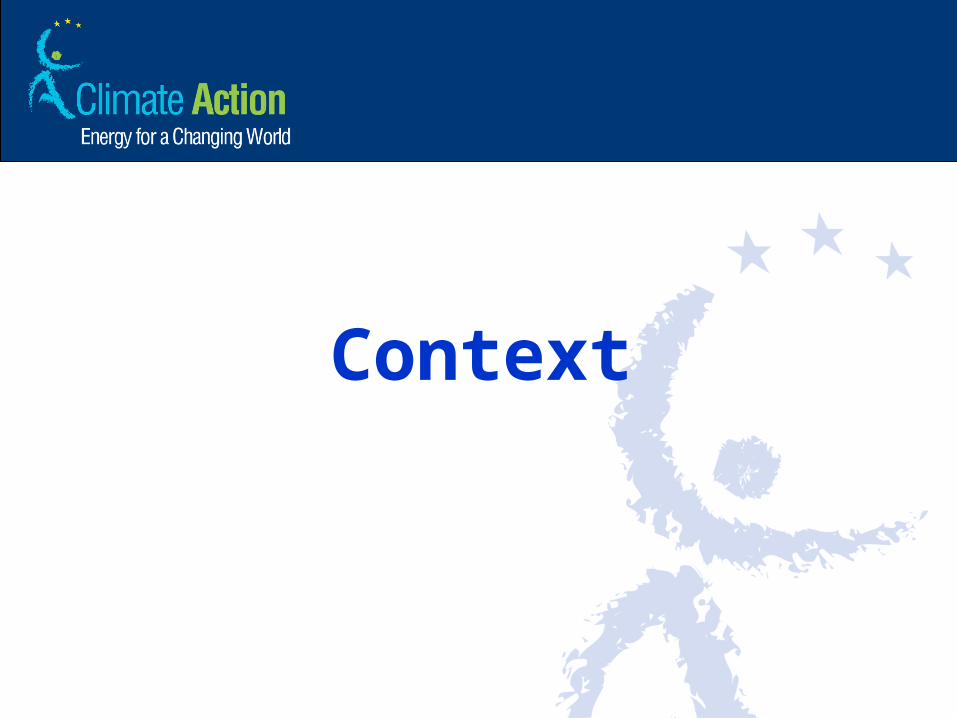

Political framework

Overall EU objective: limit global warming to 2° C above pre-industrial level to avoid dangerous climate change Stern report (2006): no action = costs of climate change to 5

– 20% of global GDP 4th IPCC report (2007): man-made climate change

“unequivocal”

European Council March 2007 20% reduction of GHG emissions by 2020, independently of

an international agreement 30% in case of satisfactory international agreement 20% share of renewable energy by 2020 20% increase of energy efficiency by 2020

The Climate and Energy Package

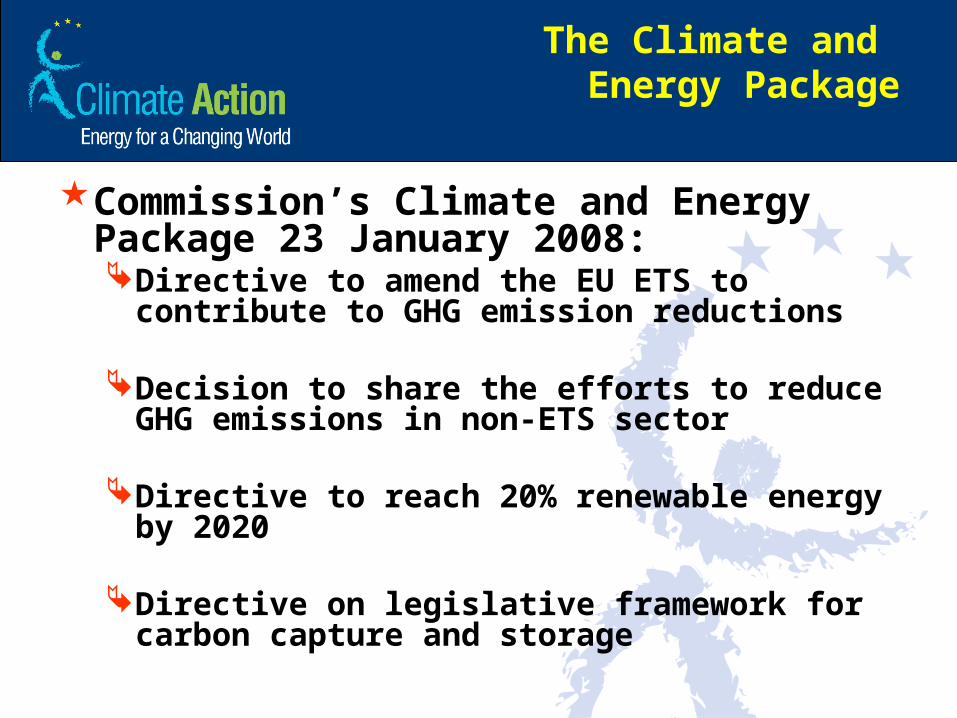

Commission’s Climate and Energy Package 23 January 2008:Directive to amend the EU ETS to contribute to

GHG emission reductions

Decision to share the efforts to reduce GHG emissions in non-ETS sector

Directive to reach 20% renewable energy by 2020

Directive on legislative framework for carbon capture and storage

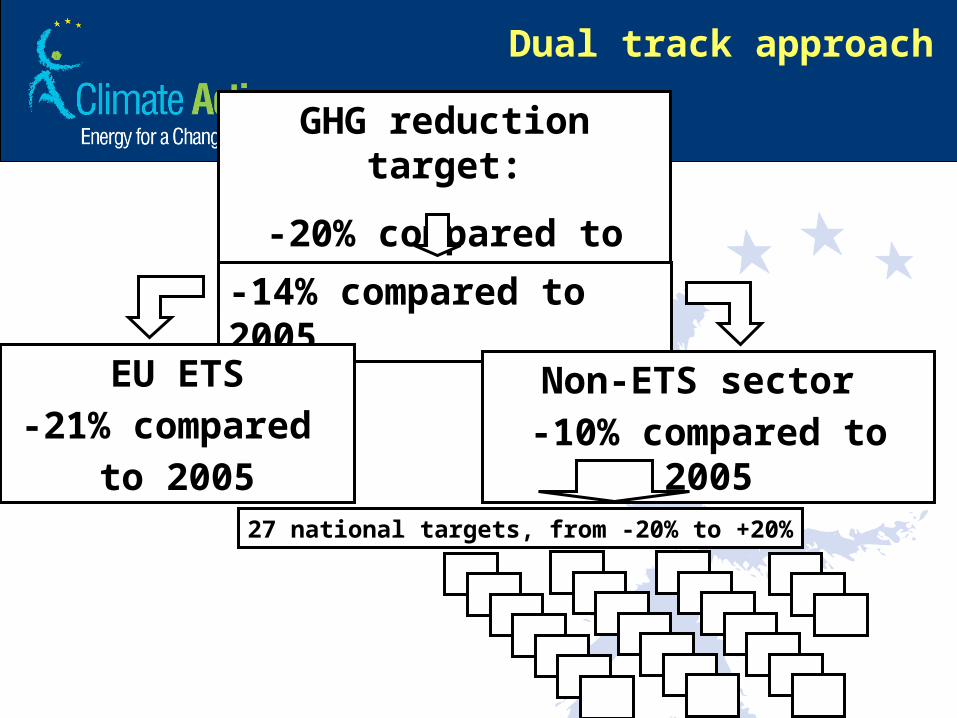

GHG reduction target:

-20% compared to 1990

-14% compared to 2005

EU ETS-21% compared

to 2005

Non-ETS sector -10% compared to 2005

27 national targets, from -20% to +20%

Dual track approach

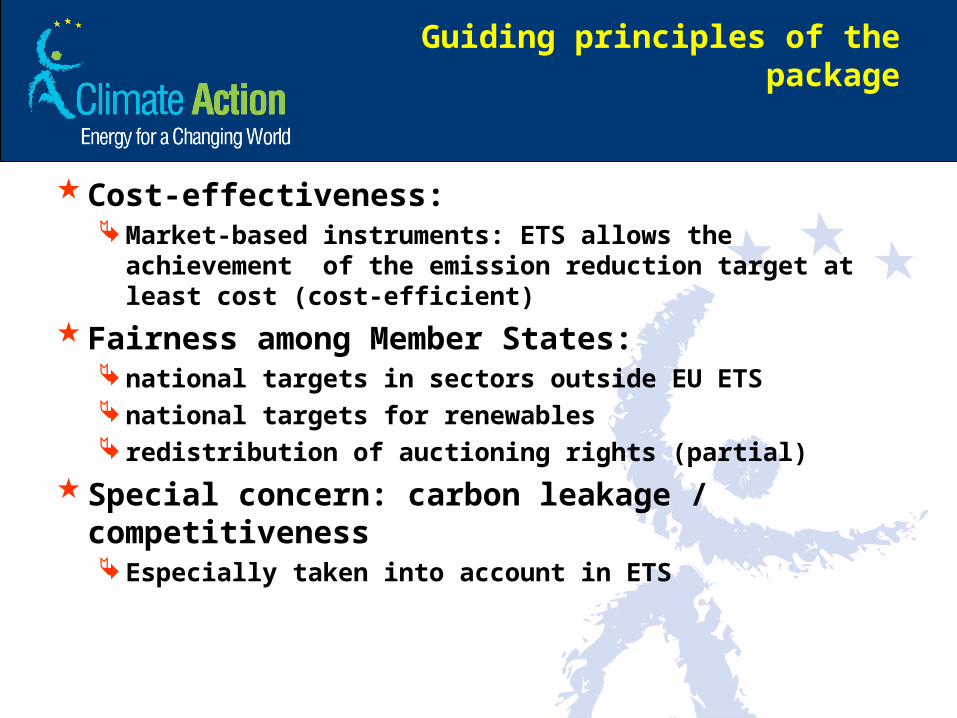

Guiding principles of the package

Cost-effectiveness: Market-based instruments: ETS allows the achievement of

the emission reduction target at least cost (cost-efficient)

Fairness among Member States: national targets in sectors outside EU ETS national targets for renewables redistribution of auctioning rights (partial)

Special concern: carbon leakage / competitiveness Especially taken into account in ETS

The EU ETS – Centrepiece of EU climate policy

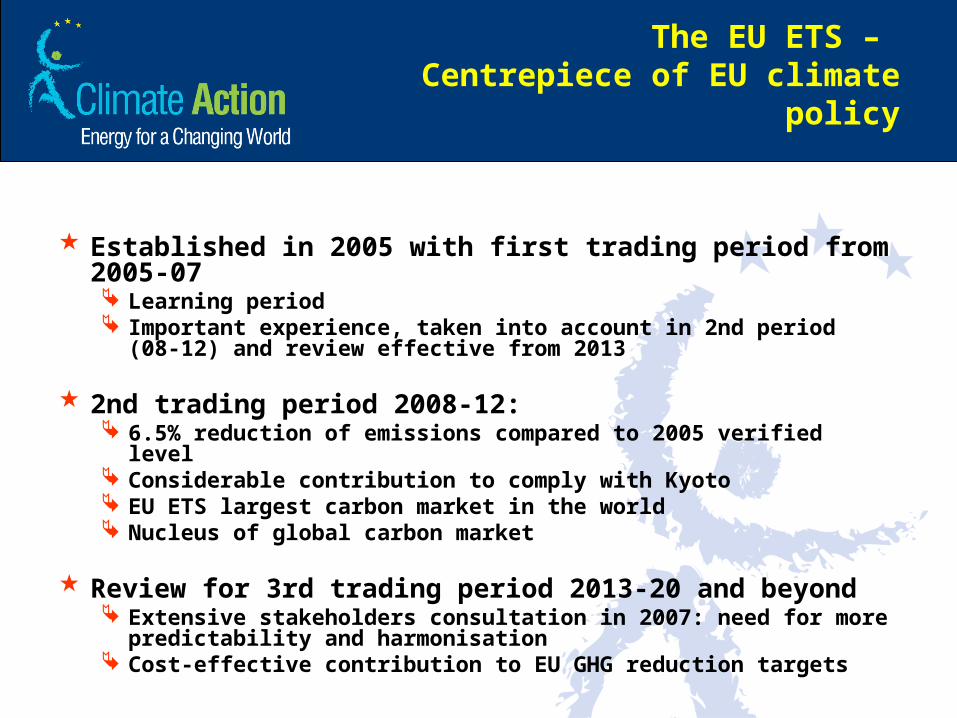

Established in 2005 with first trading period from 2005-07 Learning period Important experience, taken into account in 2nd period (08-12) and

review effective from 2013

2nd trading period 2008-12: 6.5% reduction of emissions compared to 2005 verified level Considerable contribution to comply with Kyoto EU ETS largest carbon market in the world Nucleus of global carbon market

Review for 3rd trading period 2013-20 and beyond Extensive stakeholders consultation in 2007: need for more

predictability and harmonisation Cost-effective contribution to EU GHG reduction targets

Main changes

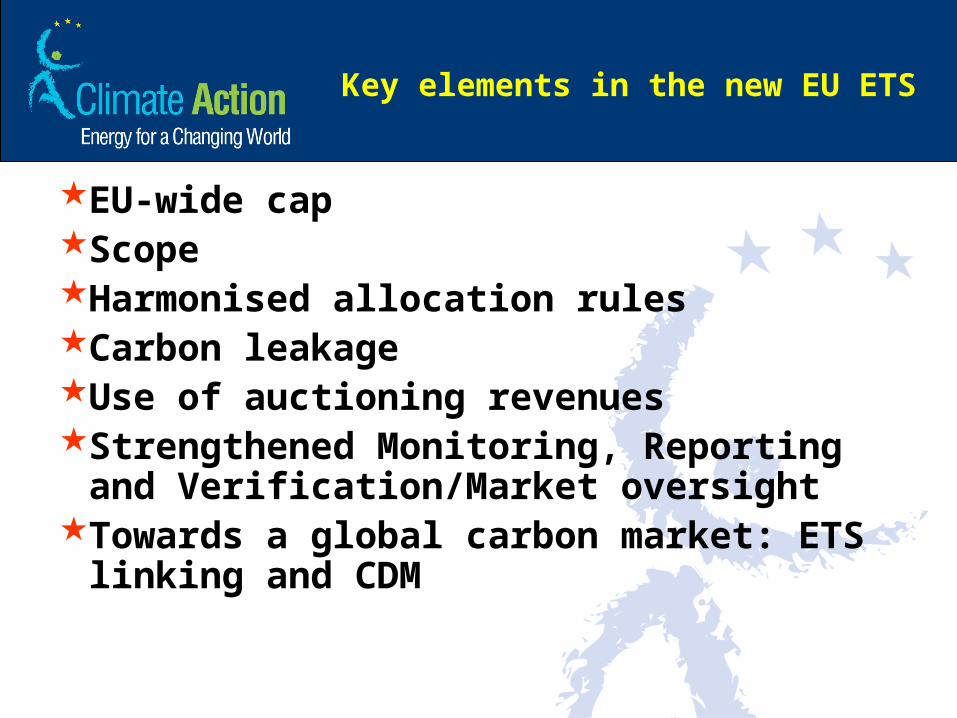

Key elements in the new EU ETS

EU-wide capScopeHarmonised allocation rulesCarbon leakageUse of auctioning revenuesStrengthened Monitoring, Reporting and

Verification/Market oversightTowards a global carbon market: ETS

linking and CDM

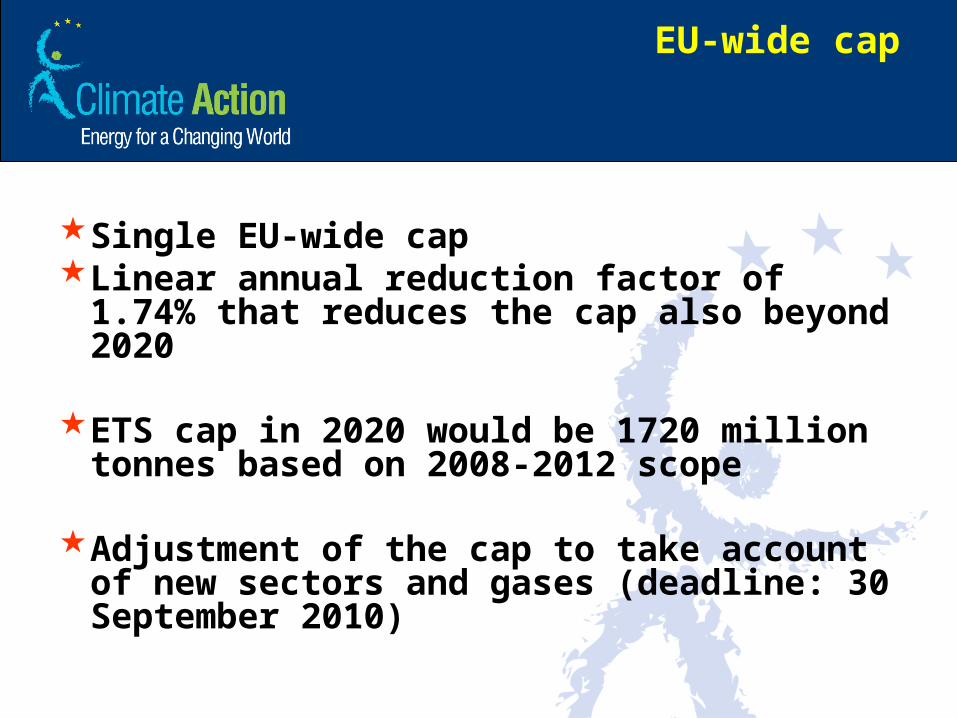

EU-wide cap

Single EU-wide capLinear annual reduction factor of 1.74% that

reduces the cap also beyond 2020

ETS cap in 2020 would be 1720 million tonnes based on 2008-2012 scope

Adjustment of the cap to take account of new sectors and gases (deadline: 30 September 2010)

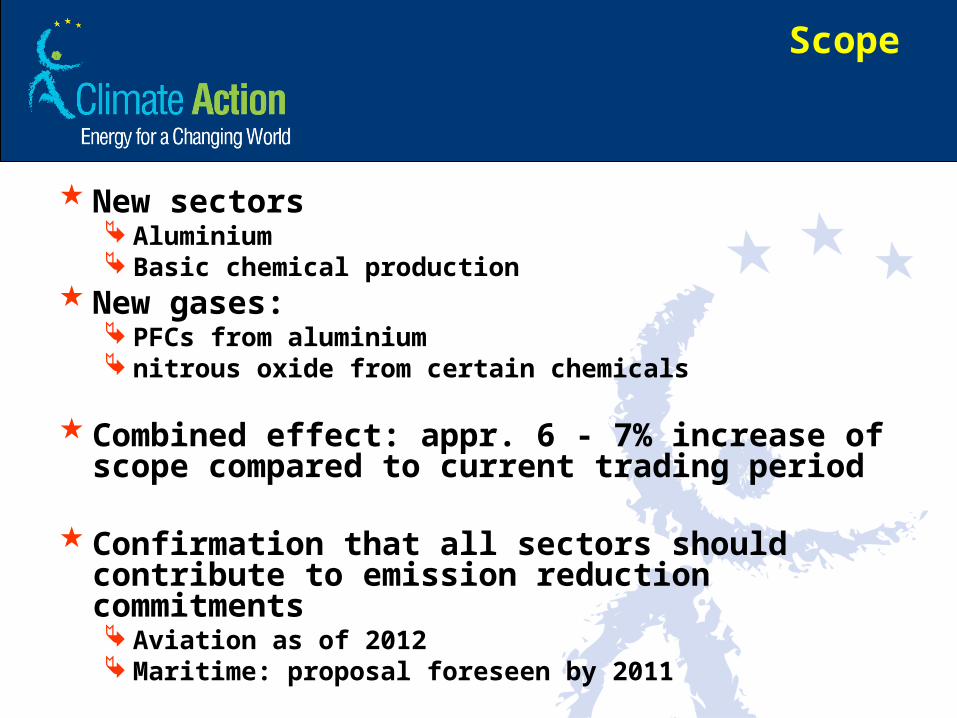

Scope

New sectors Aluminium Basic chemical production

New gases: PFCs from aluminium nitrous oxide from certain chemicals

Combined effect: appr. 6 - 7% increase of scope compared to current trading period

Confirmation that all sectors should contribute to emission reduction commitments Aviation as of 2012 Maritime: proposal foreseen by 2011

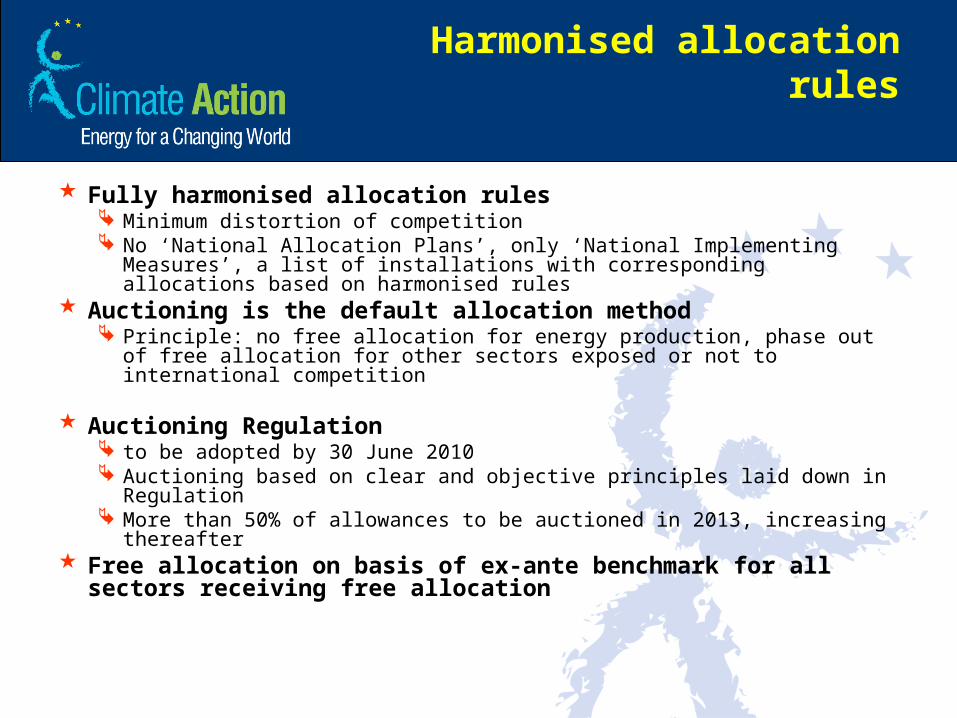

Harmonised allocation rules

Fully harmonised allocation rules Minimum distortion of competition No ‘National Allocation Plans’, only ‘National Implementing Measures’, a list

of installations with corresponding allocations based on harmonised rules Auctioning is the default allocation method

Principle: no free allocation for energy production, phase out of free allocation for other sectors exposed or not to international competition

Auctioning Regulation to be adopted by 30 June 2010 Auctioning based on clear and objective principles laid down in Regulation More than 50% of allowances to be auctioned in 2013, increasing thereafter

Free allocation on basis of ex-ante benchmark for all sectors receiving free allocation

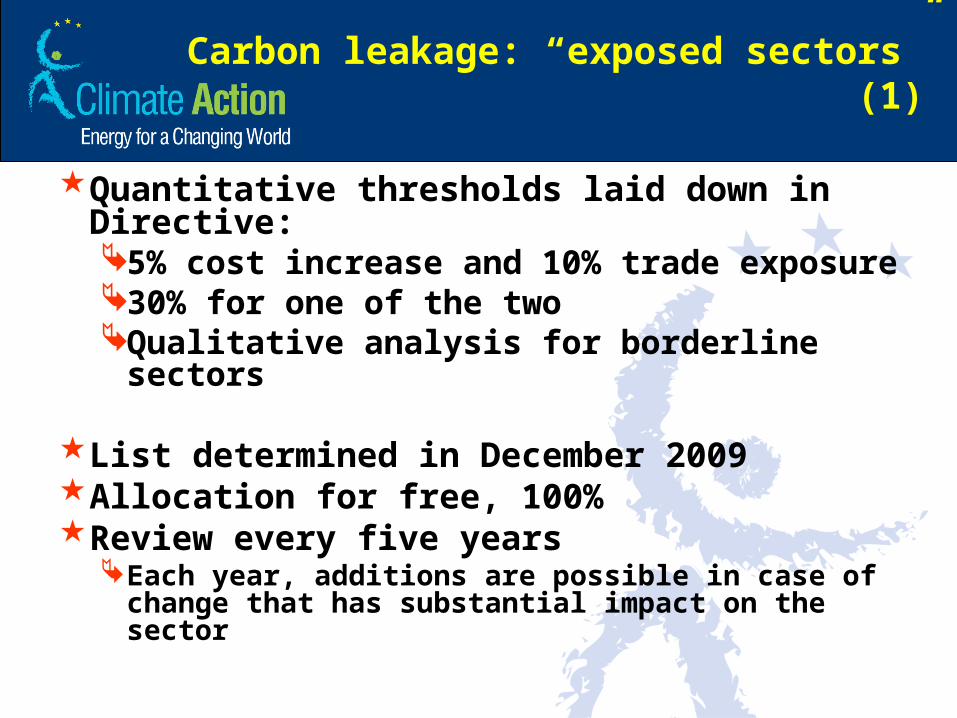

Carbon leakage: “exposed sectors” (1)

Quantitative thresholds laid down in Directive:5% cost increase and 10% trade exposure30% for one of the twoQualitative analysis for borderline sectors

List determined in December 2009Allocation for free, 100%Review every five years

Each year, additions are possible in case of change that has substantial impact on the sector

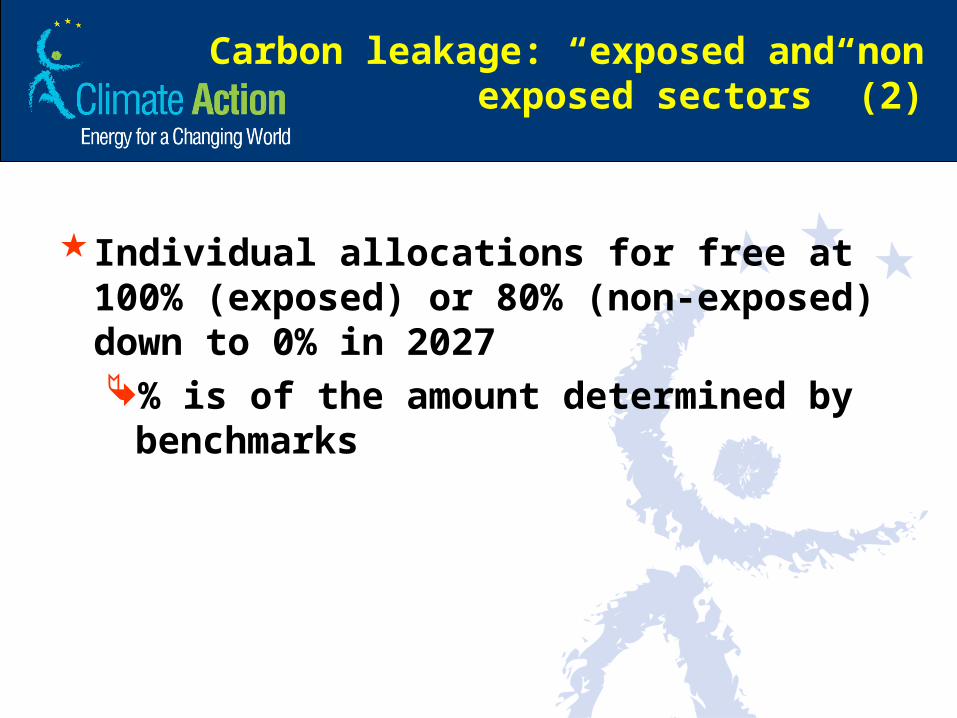

Carbon leakage: “exposed and non exposed sectors” (2)

Individual allocations for free at 100% (exposed) or 80% (non-exposed) down to 0% in 2027% is of the amount determined by

benchmarks

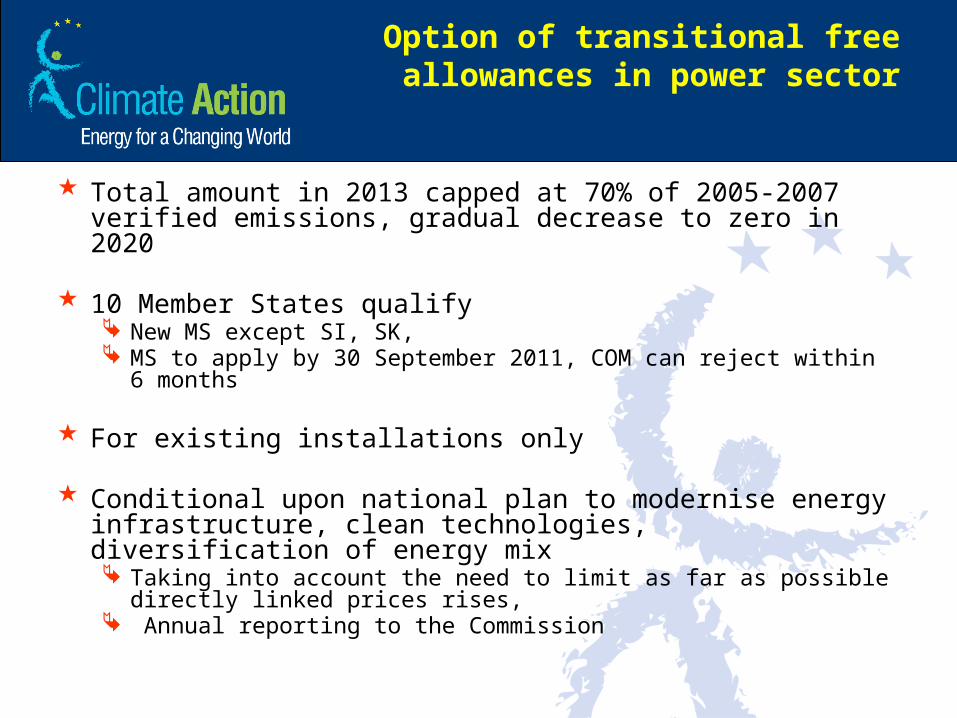

Option of transitional free allowances in power sector

Total amount in 2013 capped at 70% of 2005-2007 verified emissions, gradual decrease to zero in 2020

10 Member States qualify New MS except SI, SK, MS to apply by 30 September 2011, COM can reject within 6 months

For existing installations only

Conditional upon national plan to modernise energy infrastructure, clean technologies, diversification of energy mix Taking into account the need to limit as far as possible directly linked

prices rises, Annual reporting to the Commission

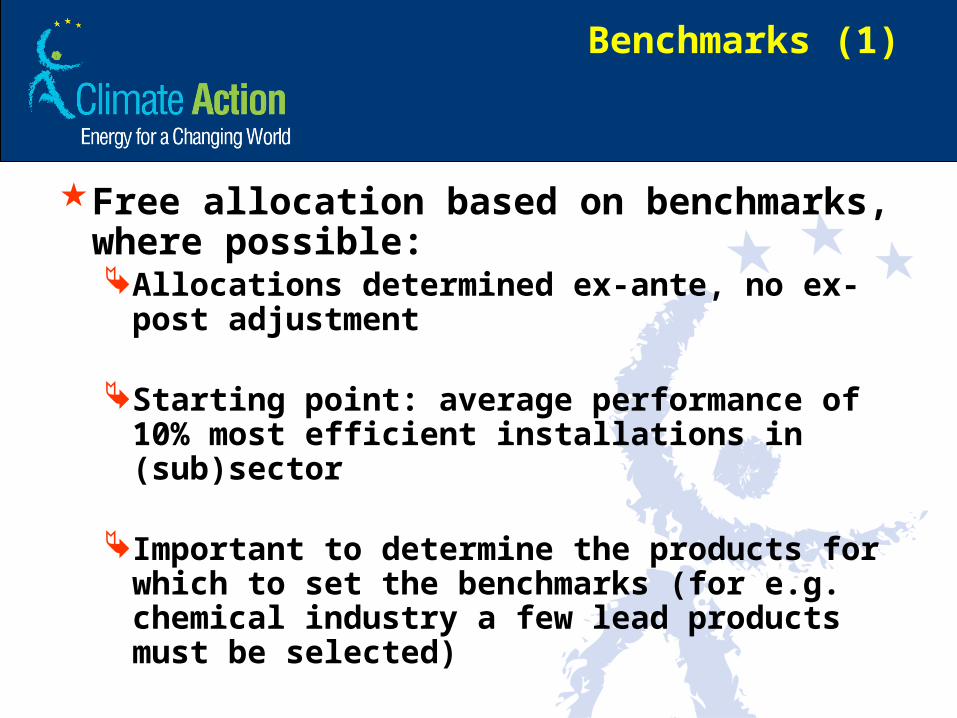

Benchmarks (1)

Free allocation based on benchmarks, where possible:Allocations determined ex-ante, no ex-post

adjustment

Starting point: average performance of 10% most efficient installations in (sub)sector

Important to determine the products for which to set the benchmarks (for e.g. chemical industry a few lead products must be selected)

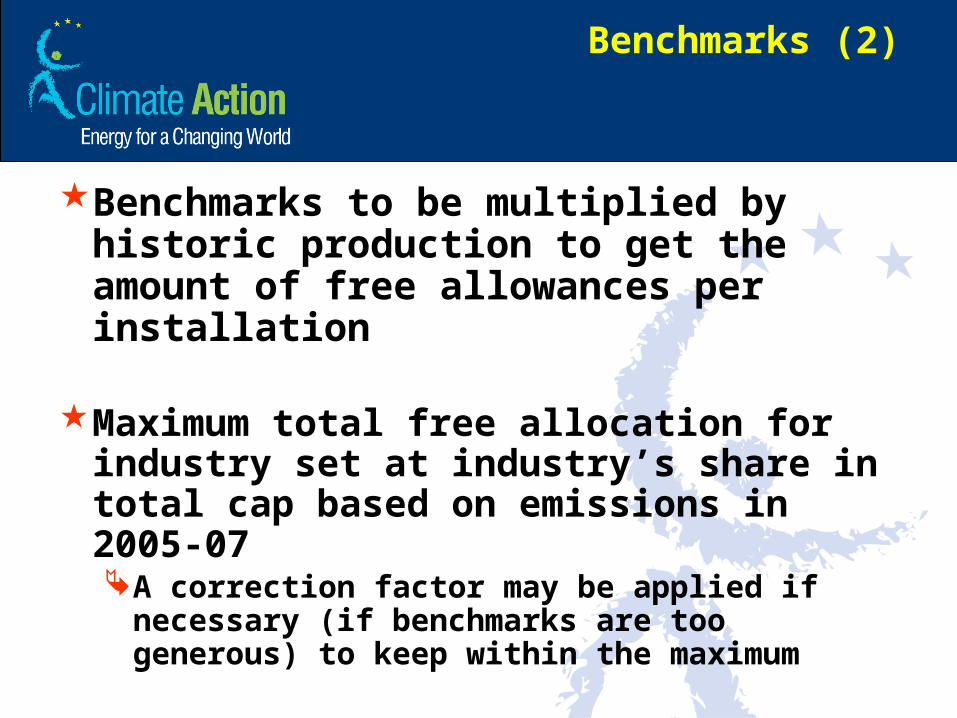

Benchmarks (2)

Benchmarks to be multiplied by historic production to get the amount of free allowances per installation

Maximum total free allocation for industry set at industry’s share in total cap based on emissions in 2005-07A correction factor may be applied if necessary (if

benchmarks are too generous) to keep within the maximum

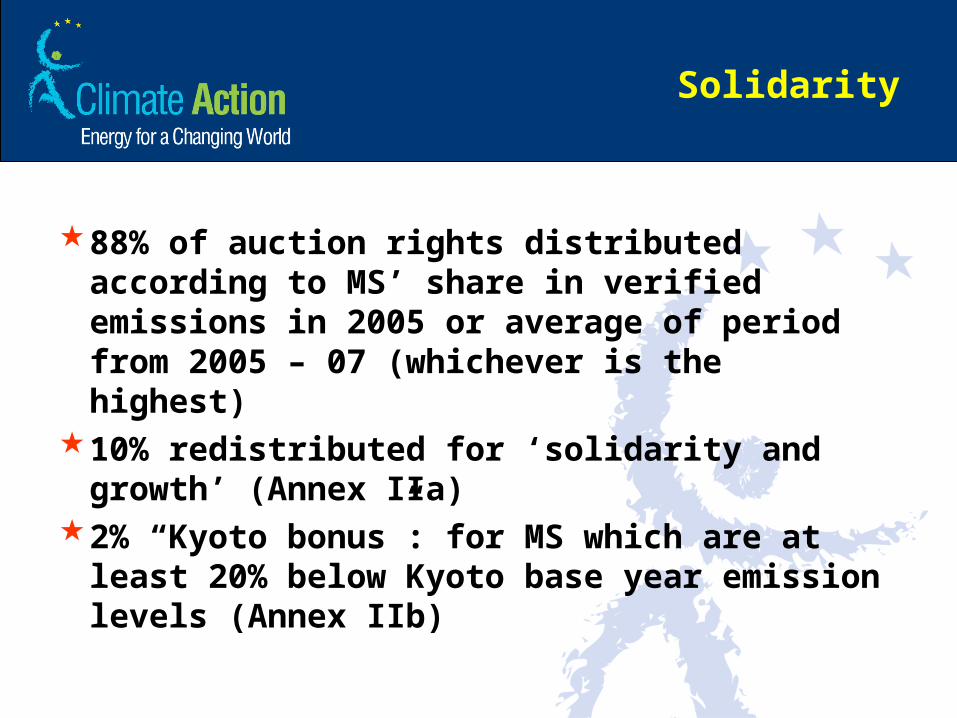

Solidarity

88% of auction rights distributed according to MS’ share in verified emissions in 2005 or average of period from 2005 – 07 (whichever is the highest)

10% redistributed for ‘solidarity and growth’ (Annex IIa)

2% “Kyoto bonus”: for MS which are at least 20% below Kyoto base year emission levels (Annex IIb)

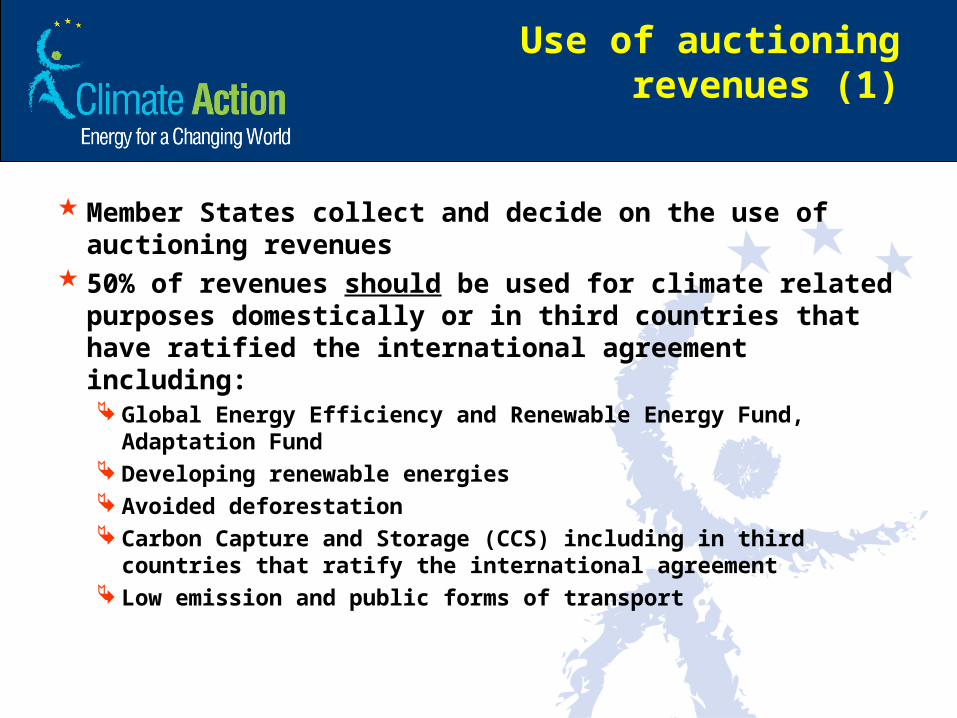

Use of auctioning revenues (1)

Member States collect and decide on the use of auctioning revenues

50% of revenues should be used for climate related purposes domestically or in third countries that have ratified the international agreement including: Global Energy Efficiency and Renewable Energy Fund,

Adaptation Fund Developing renewable energies Avoided deforestation Carbon Capture and Storage (CCS) including in third countries

that ratify the international agreement Low emission and public forms of transport

Use of auctioning revenues (2)

Fiscal or financial support policies can be accounted for

MS to inform COM on use of revenues by means of the reports under the Kyoto implementation decision 280/2004/EC

Incentivising CCS and RES projects

300 million allowances available for CCS and innovative renewable energy technology demonstration projectsUntil 31 December 2015 To be given via Member StatesProjects selected on the basis of objective and

transparent criteriaGeographically balanced supportSupport for a single project no more than 15% of

total number of allowancesRules to be determined by comitology

Market oversight provisions (1)

Commission to monitor carbon marketRegular annual reporting to Council and

Parliament If evidence of malfunctioning, special

report along with proposals to improve market functioning

Member States to report on auctions; to be published on Commission website

Market oversight provisions (2)

Insider dealing and market manipulation: By end of 2010, examination whether market is sufficiently

protected from insider dealing and market manipulation If appropriate, proposals to eliminate insider dealing and

market manipulation Excessive price fluctuations:

Definition: average price of allowances in a six months period more than three times of the two preceding years;

Climate Change Committee to meet and consider possible measures (alternatively):

• Bring forward auctions; • Authorise auctioning of up to 25% of remaining NER

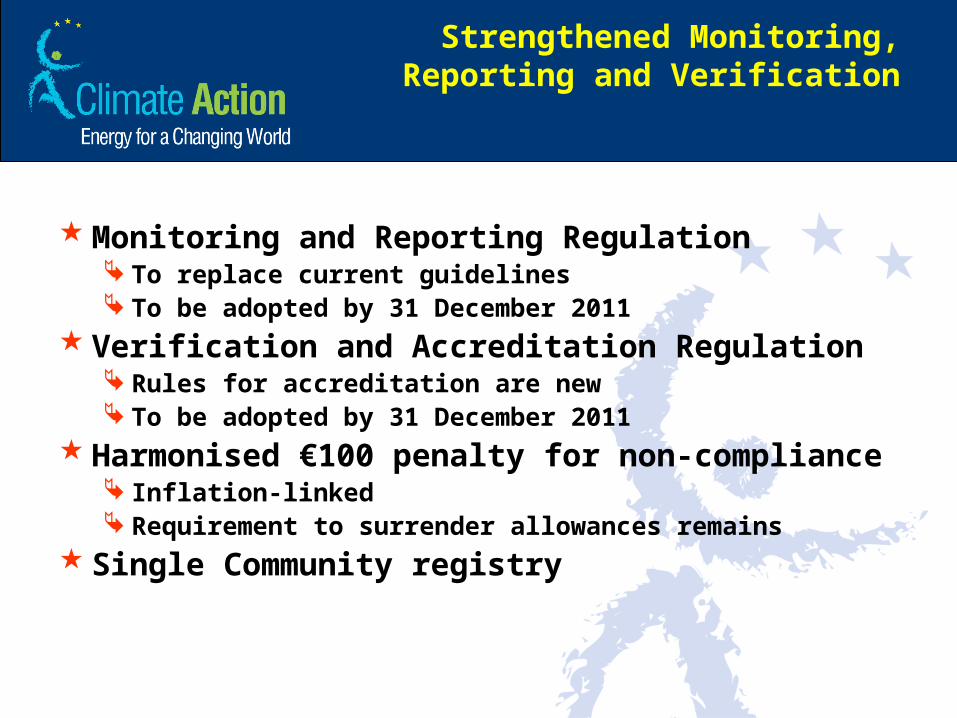

Strengthened Monitoring, Reporting and Verification

Monitoring and Reporting Regulation To replace current guidelines To be adopted by 31 December 2011

Verification and Accreditation Regulation Rules for accreditation are new To be adopted by 31 December 2011

Harmonised €100 penalty for non-compliance Inflation-linked Requirement to surrender allowances remains

Single Community registry

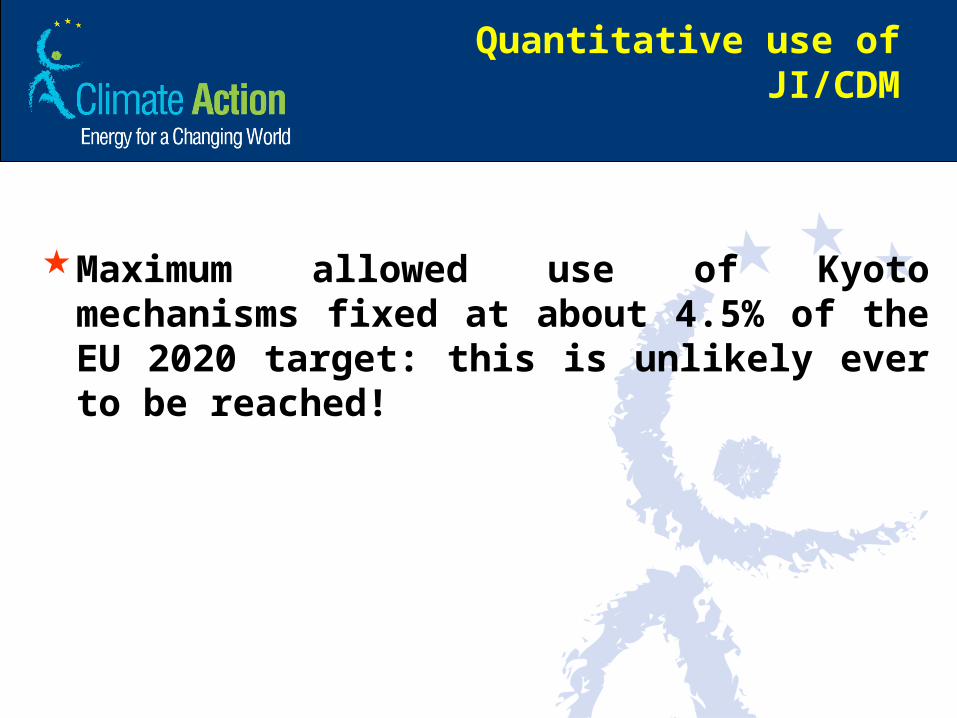

Quantitative use of JI/CDM

Maximum allowed use of Kyoto mechanisms fixed at about 4.5% of the EU 2020 target: this is unlikely ever to be reached!

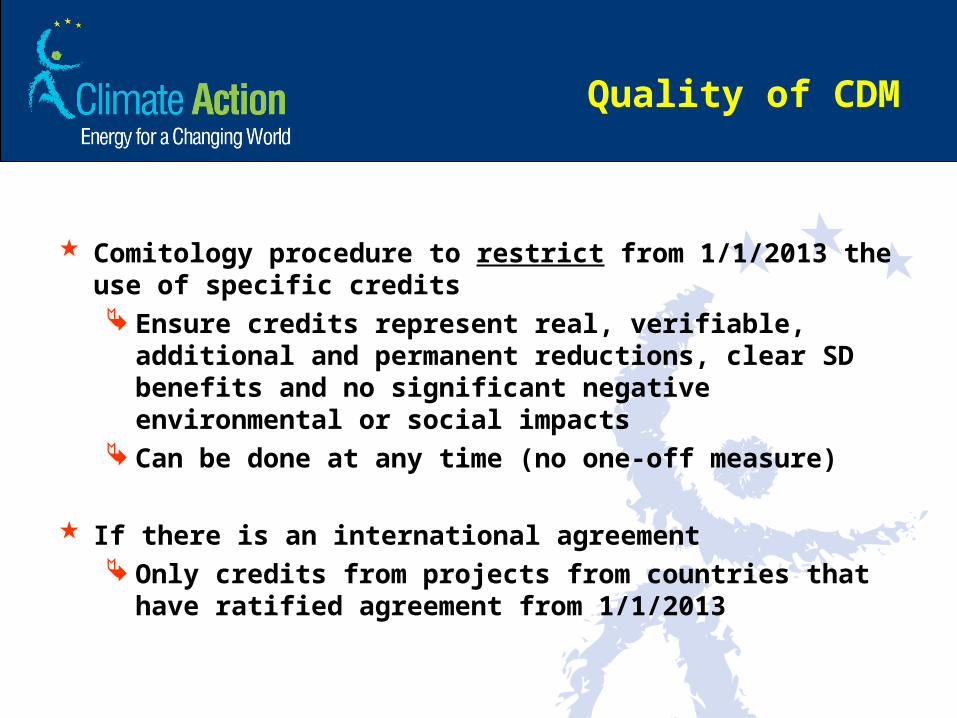

Quality of CDM

Comitology procedure to restrict from 1/1/2013 the use of specific credits Ensure credits represent real, verifiable, additional and

permanent reductions, clear SD benefits and no significant negative environmental or social impacts

Can be done at any time (no one-off measure)

If there is an international agreement Only credits from projects from countries that have ratified

agreement from 1/1/2013

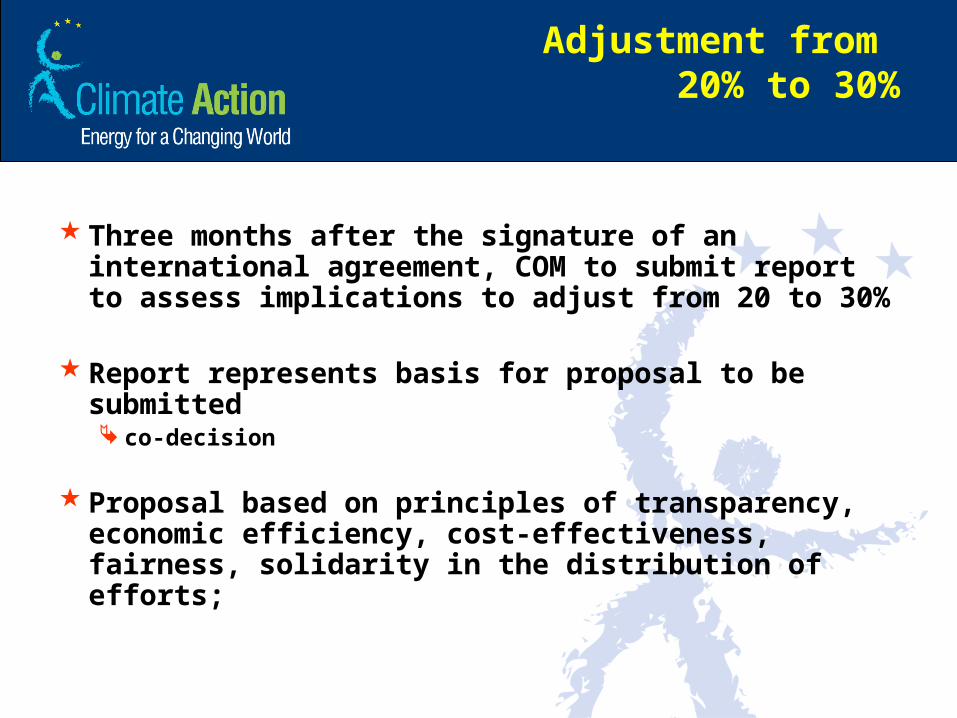

Adjustment from 20% to 30%

Three months after the signature of an international agreement, COM to submit report to assess implications to adjust from 20 to 30%

Report represents basis for proposal to be submitted co-decision

Proposal based on principles of transparency, economic efficiency, cost-effectiveness, fairness, solidarity in the distribution of efforts;

28

The international carbon market and linking emissions trading

systems

29

Where we are

The EU ETS has been the core of the ‘global carbon market’• An absolute emissions cap covering 30

countries for around 11,500 installations and emissions from aircraft

• EU ETS and EU Member States have provided the main demand for Clean Development Mechanism (CDM) credits

• The EU: around 10% of global GHG emissions

30

Where we need to go

Limit global temperature increase to 2°C All countries, including emerging economies, need to

take more action to reduce emissionsPledges under Copenhagen AccordEmission trading systems are a cost-effective way to

do soCap and trade in place or in discussion: US (Federal,

RGGI and WCI), Australia (2013?), Japan, Switzerland, New Zealand and others. ETS developments in Mexico, South Korea, China and India…

31

An important source of climate finance

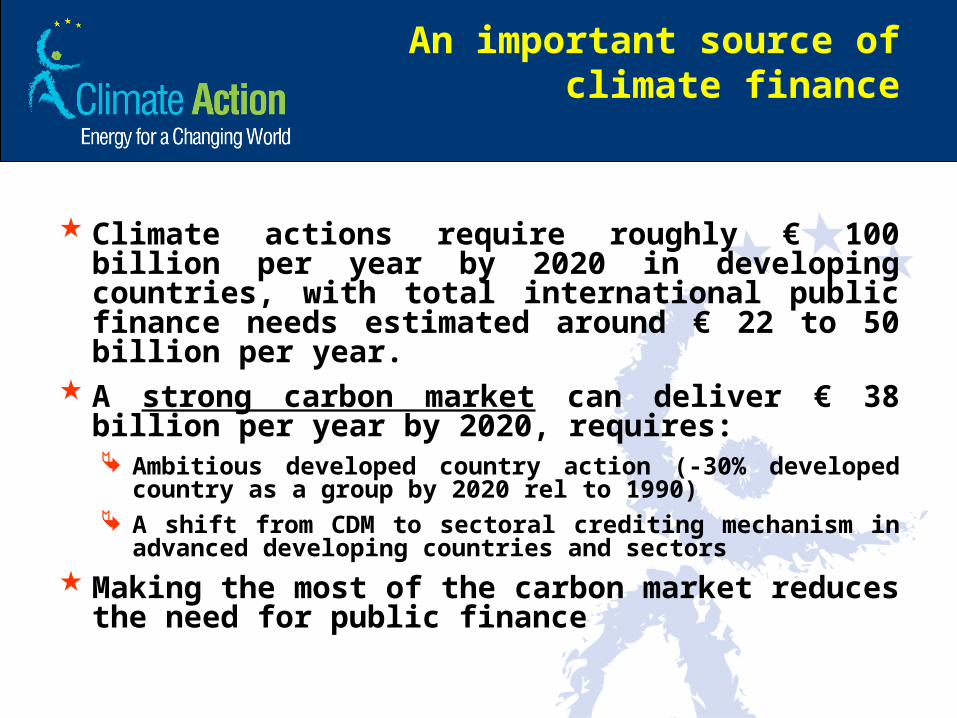

Climate actions require roughly € 100 billion per year by 2020 in developing countries, with total international public finance needs estimated around € 22 to 50 billion per year.

A strong carbon market can deliver € 38 billion per year by 2020, requires: Ambitious developed country action (-30% developed country

as a group by 2020 rel to 1990) A shift from CDM to sectoral crediting mechanism in advanced

developing countries and sectors

Making the most of the carbon market reduces the need for public finance

32

A robust international carbon market

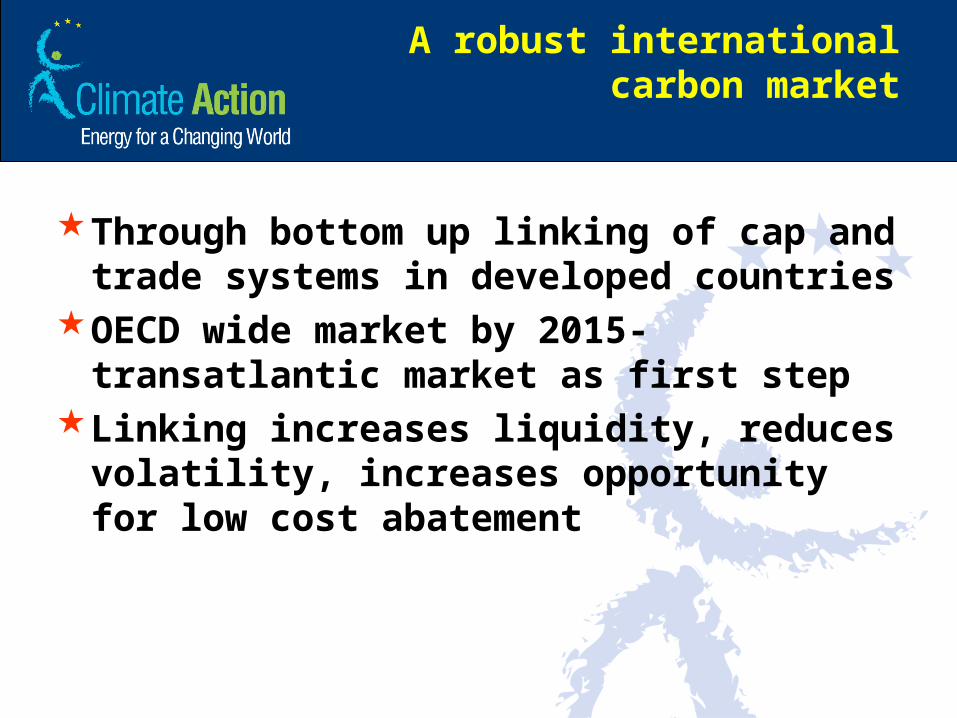

Through bottom up linking of cap and trade systems in developed countries

OECD wide market by 2015- transatlantic market as first step

Linking increases liquidity, reduces volatility, increases opportunity for low cost abatement

33

A robust international carbon market

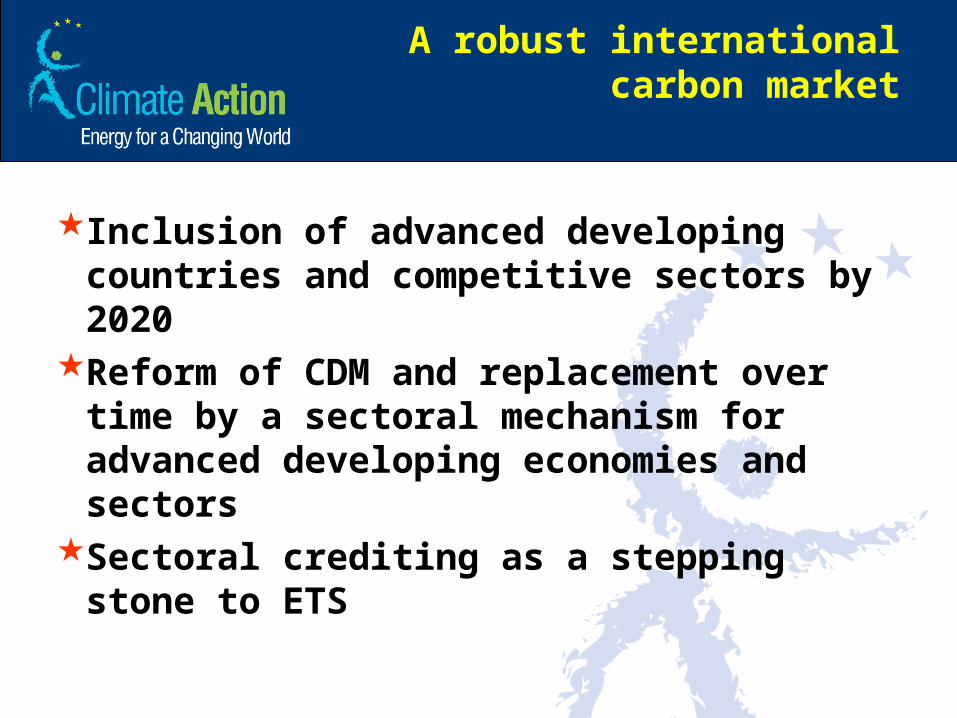

Inclusion of advanced developing countries and competitive sectors by 2020

Reform of CDM and replacement over time by a sectoral mechanism for advanced developing economies and sectors

Sectoral crediting as a stepping stone to ETS

34

International Carbon Action Partnership ICAP

Public authorities committed to cap and trade Technical exchange on best practice to improve design and promote

compatible systems

Members: EU: European Commission, Denmark , France , Germany, Greece ,

Ireland, Italy , Netherlands , Portugal , Spain , United Kingdom North America:

Regional Greenhouse Gas Initiative Members (RGGI): Maine, Maryland, Massachusetts, New Jersey, New York

Western Climate Initiative Members (WCI): Arizona, British Columbia, California, Manitoba, New Mexico, Ontario, Oregon, Québec, Washington

Others: Australia, New Zealand, Norway, Tokyo Metropolitan Government

Plus Observers: Japan and Ukraine www.icapcarbonaction.com

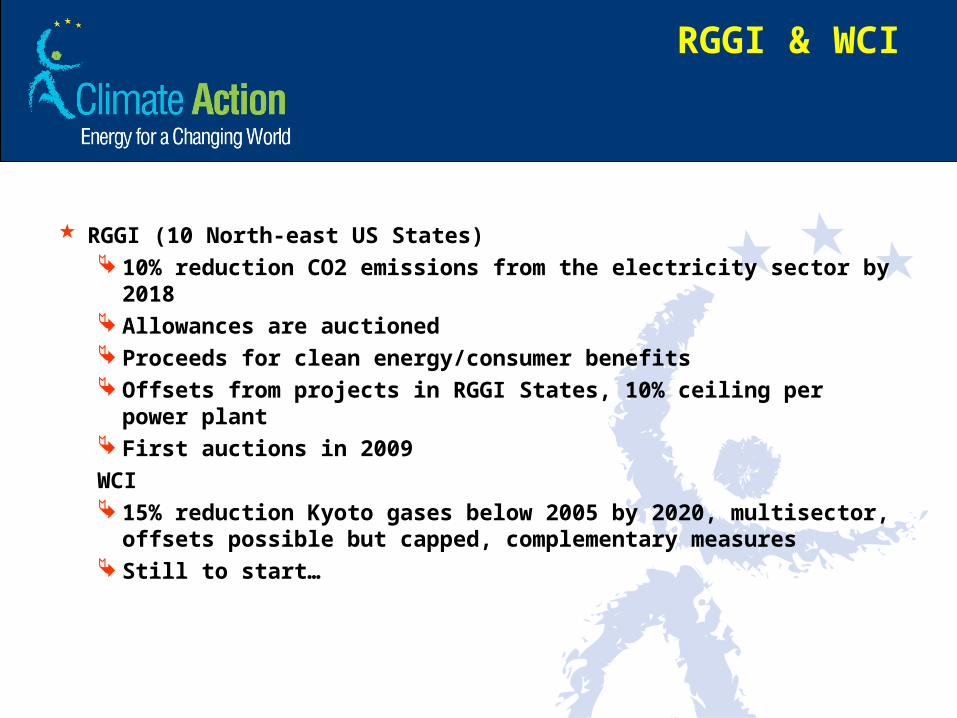

RGGI & WCI

RGGI (10 North-east US States) 10% reduction CO2 emissions from the electricity sector by 2018 Allowances are auctioned Proceeds for clean energy/consumer benefits Offsets from projects in RGGI States, 10% ceiling per power plant First auctions in 2009

WCI 15% reduction Kyoto gases below 2005 by 2020, multisector,

offsets possible but capped, complementary measures Still to start…

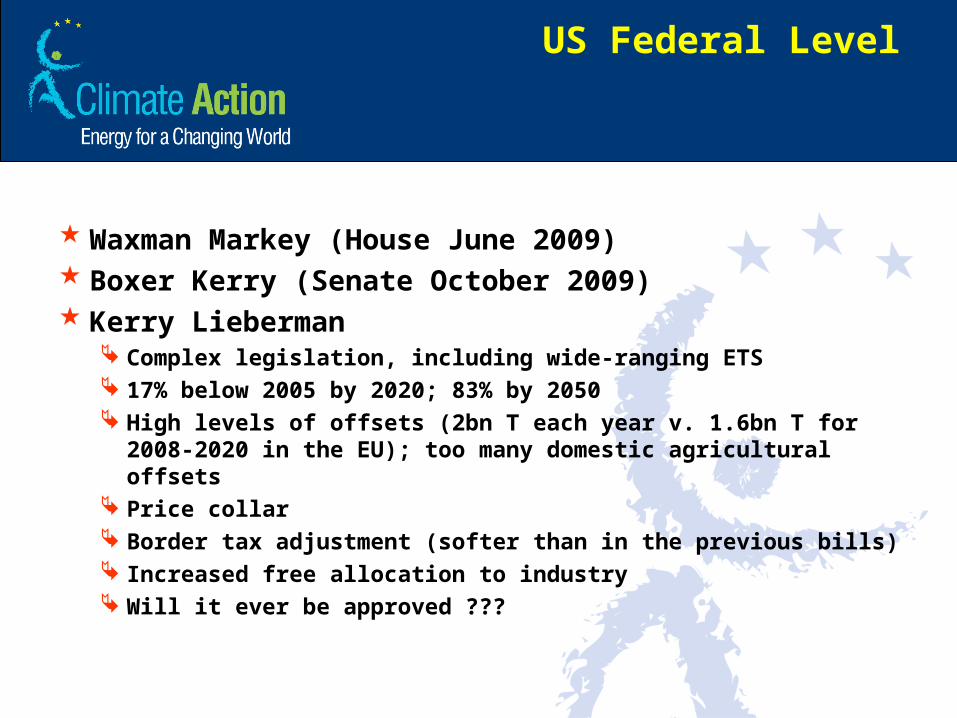

US Federal Level

Waxman Markey (House June 2009) Boxer Kerry (Senate October 2009) Kerry Lieberman

Complex legislation, including wide-ranging ETS 17% below 2005 by 2020; 83% by 2050 High levels of offsets (2bn T each year v. 1.6bn T for 2008-2020

in the EU); too many domestic agricultural offsets Price collar Border tax adjustment (softer than in the previous bills) Increased free allocation to industry Will it ever be approved ???

37

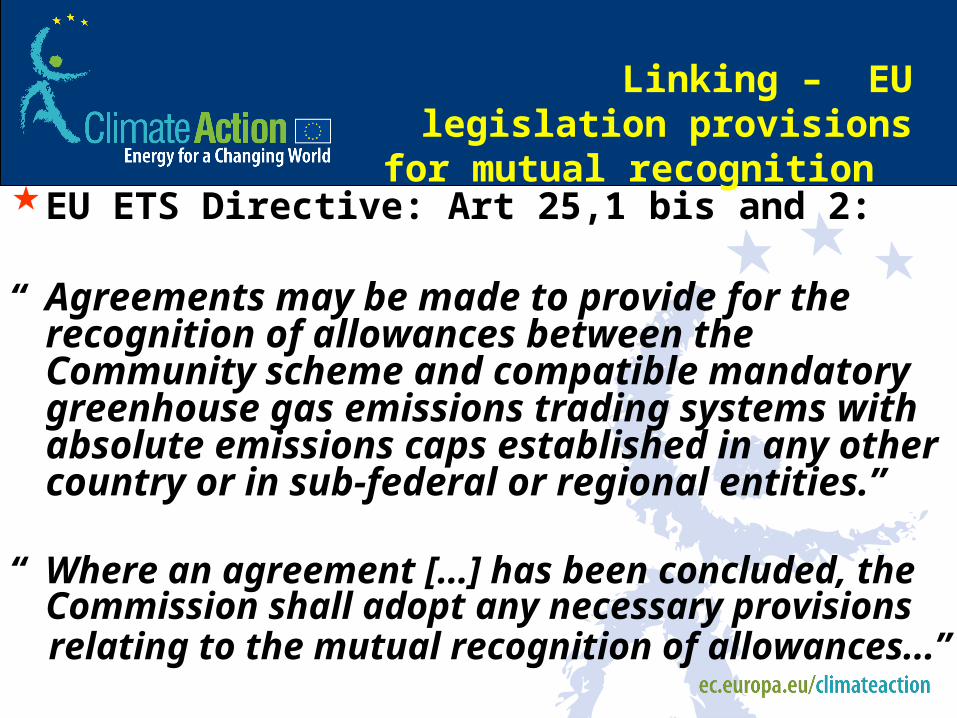

Linking – EU legislation provisions for mutual

recognition EU ETS Directive: Art 25,1 bis and 2:

“ Agreements may be made to provide for the recognition of allowances between the Community scheme and compatible mandatory greenhouse gas emissions trading systems with absolute emissions caps established in any other country or in sub-federal or regional entities.”

“ Where an agreement […] has been concluded, the Commission shall adopt any necessary provisions

relating to the mutual recognition of allowances...”

38

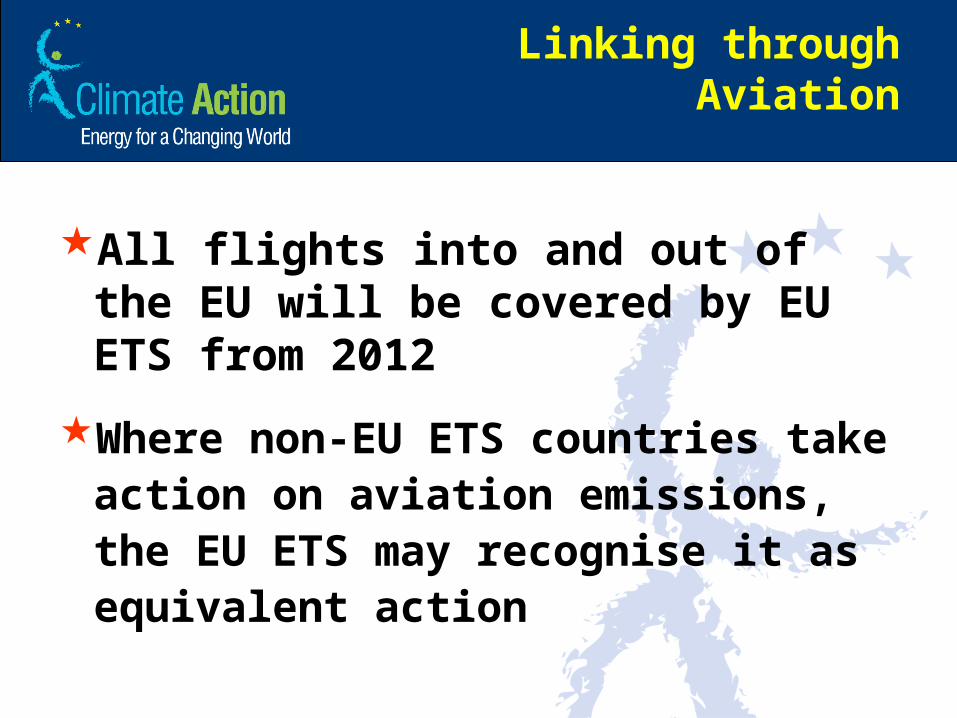

Linking through Aviation

All flights into and out of the EU will be covered by EU ETS from 2012

Where non-EU ETS countries take action on aviation emissions, the EU ETS may recognise it as equivalent action

39

Importance of coordination of recognition policies

In practice two systems accepting the same international credits for compliance will be linked through these international credits

Need for cooperation in the development phase

40

Info on the Climate Action and Renewable Energy Package at http://ec.europa.eu/environment/climat/climate_action.htm