Embed Size (px)

Citation preview

The impact of PPPs contracting on

Portugal’s fiscal position and

what can be done about it Presentation at the 4th Annual OECD Symposium on

PPP Working Party of Senior Budget Officials (SBO)

Professor Ricardo Ferreira Reis

Introduction

• Portugal´s current Public Finances situation.

• The Portuguese experience with PPPs.

• PPPs in the Memorandum of Understanding with

the EU/ECB/IMF (The Troika)

• The future of PPPs in Portugal: What solutions?

• The OPPP at the University: Our mission, organization and

work.

Public Finances

in Portugal

Public Finances in Portugal:

current situation

– Significant increase in public spending not followed by

economic growth

– Permanent deficits around 5% before 2008 financial

crisis

– After 2008, fast fiscal deterioration

– High levels of public debt with an increase in the interest

rates

– Unsustainable fiscal situation

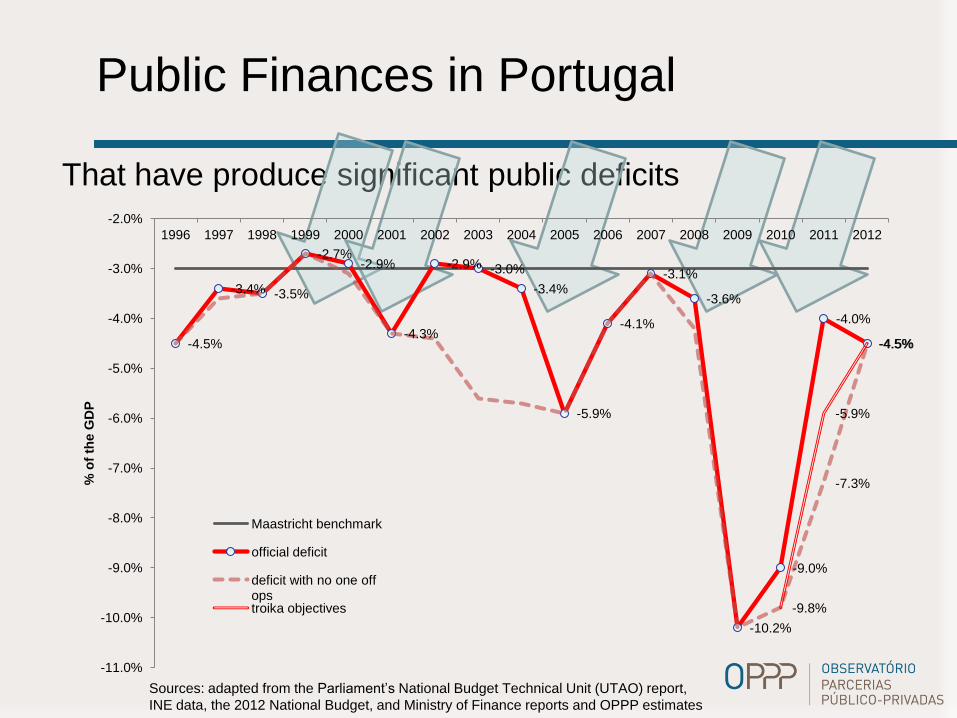

Public Finances in Portugal

That have produce significant public deficits

Sources: adapted from the Parliament’s National Budget Technical Unit (UTAO) report,

INE data, the 2012 National Budget, and Ministry of Finance reports and OPPP estimates

-4.5%

-3.4% -3.5%

-2.7% -2.9%

-4.3%

-2.9% -3.0%

-3.4%

-5.9%

-4.1%

-3.1%

-3.6%

-10.2%

-9.0%

-4.0%

-4.5%

-7.3%

-9.8%

-5.9%

-4.5%

-11.0%

-10.0%

-9.0%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

% o

f th

e G

DP

Maastricht benchmark

official deficit

deficit with no one off ops troika objectives

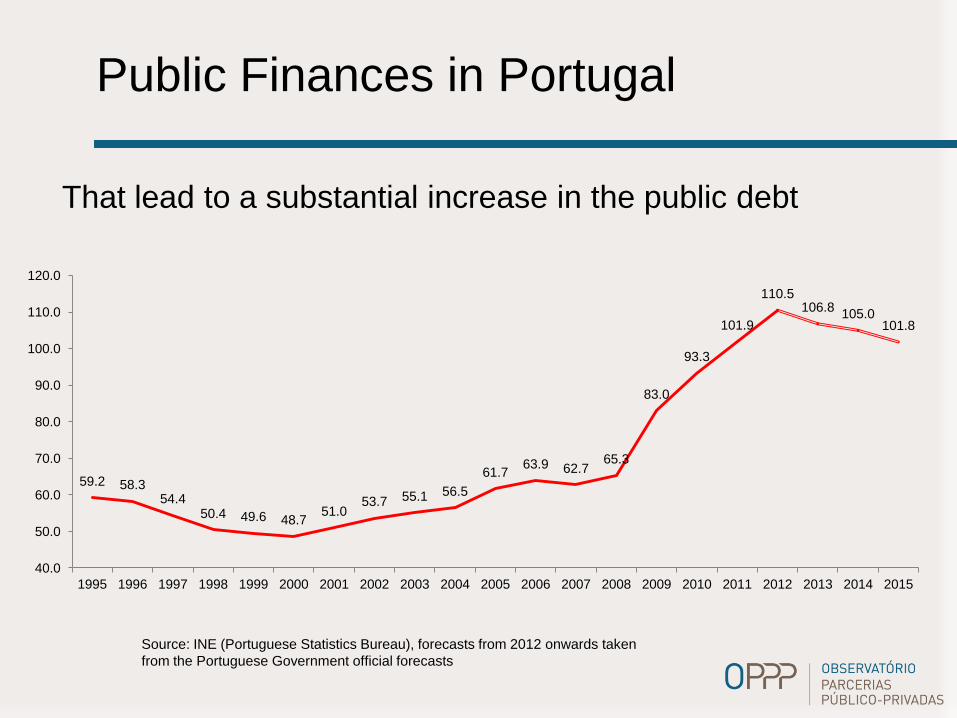

Public Finances in Portugal

59.2 58.3 54.4

50.4 49.6 48.7 51.0

53.7 55.1 56.5

61.7 63.9 62.7

65.3

83.0

93.3

101.9

110.5 106.8

105.0 101.8

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

That lead to a substantial increase in the public debt

Source: INE (Portuguese Statistics Bureau), forecasts from 2012 onwards taken

from the Portuguese Government official forecasts

Public Finances in Portugal

• Pro-cyclical deficits, with significant decrease in

revenues and increase in automatic stabilizers

• No particular concern with public debt, focus has

been mainly on deficit

• Election cycle does not help either, but has

consistently enhanced transparency

• Precarious fiscal consolidation recurrently

lead to off budget public spending solutions

The PPP Experience in

Portugal

The PPP Experience in Portugal

• Intensive use of PPP to close the “infrastructure gap”

• Portugal lead PPP projects when measure by the size

of the GDP

• “Off-budget temptation”, and not Value for Money, was

the main reason to choose PPP instead of traditional

procurement

• Affordability issued due to the high level of future

payments.

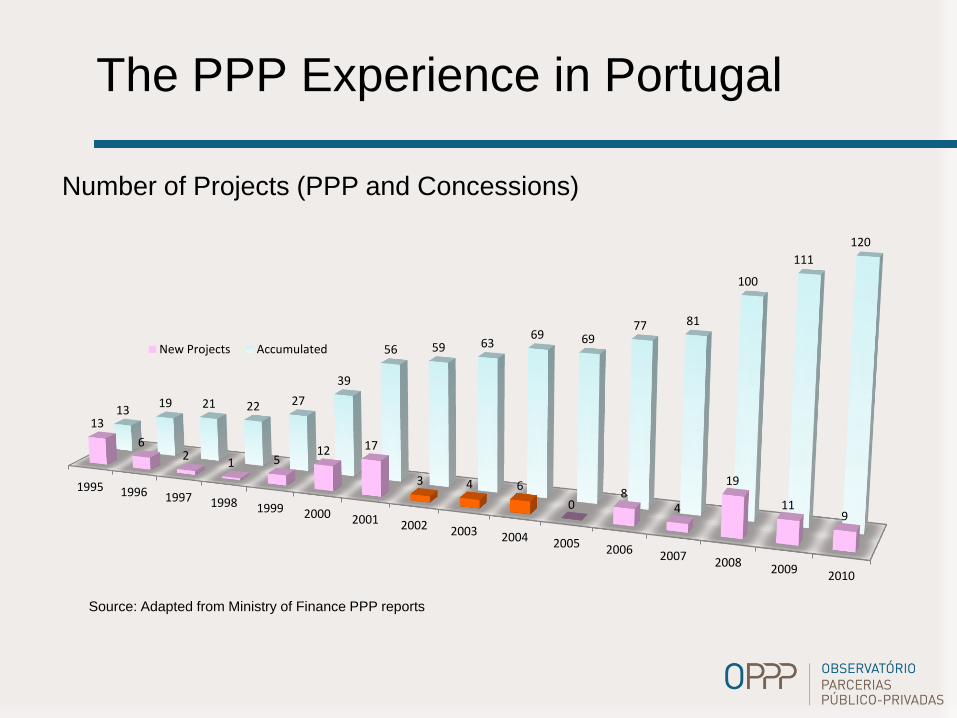

The PPP Experience in Portugal

Number of Projects (PPP and Concessions)

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

2010

13

6 2

1 5 12 17

3 4 6

0 8

4

19

11 9

13 19 21 22 27

39

56 59 63 69 69

77 81

100

111

120

New Projects Accumulated

Source: Adapted from Ministry of Finance PPP reports

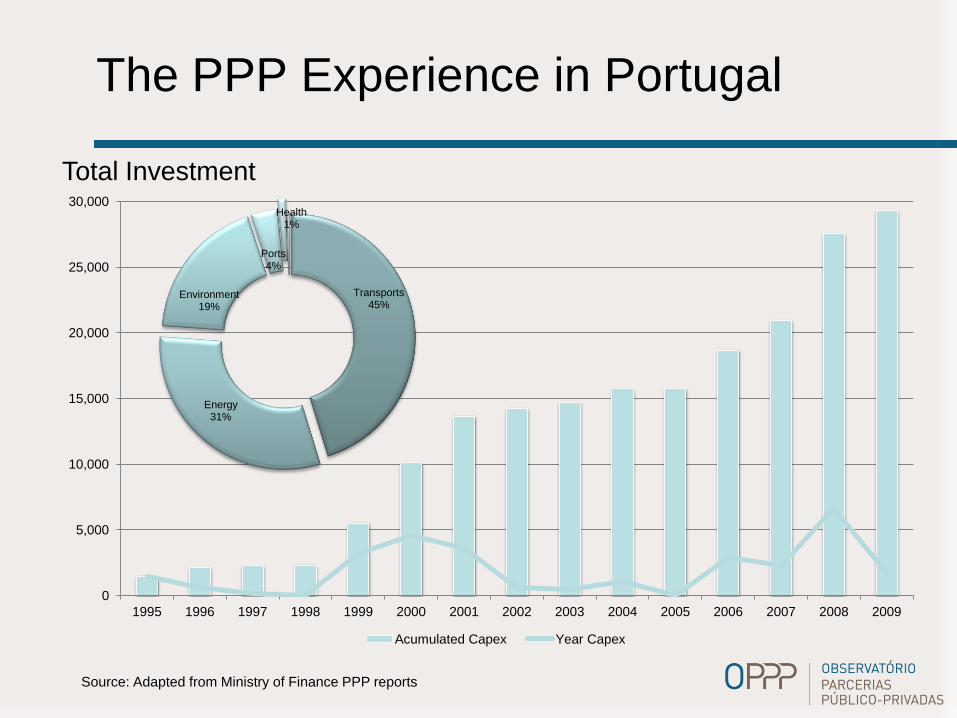

The PPP Experience in Portugal

0

5,000

10,000

15,000

20,000

25,000

30,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Acumulated Capex Year Capex

Total Investment

Source: Adapted from Ministry of Finance PPP reports

Transports 45%

Energy 31%

Environment 19%

Ports 4%

Health 1%

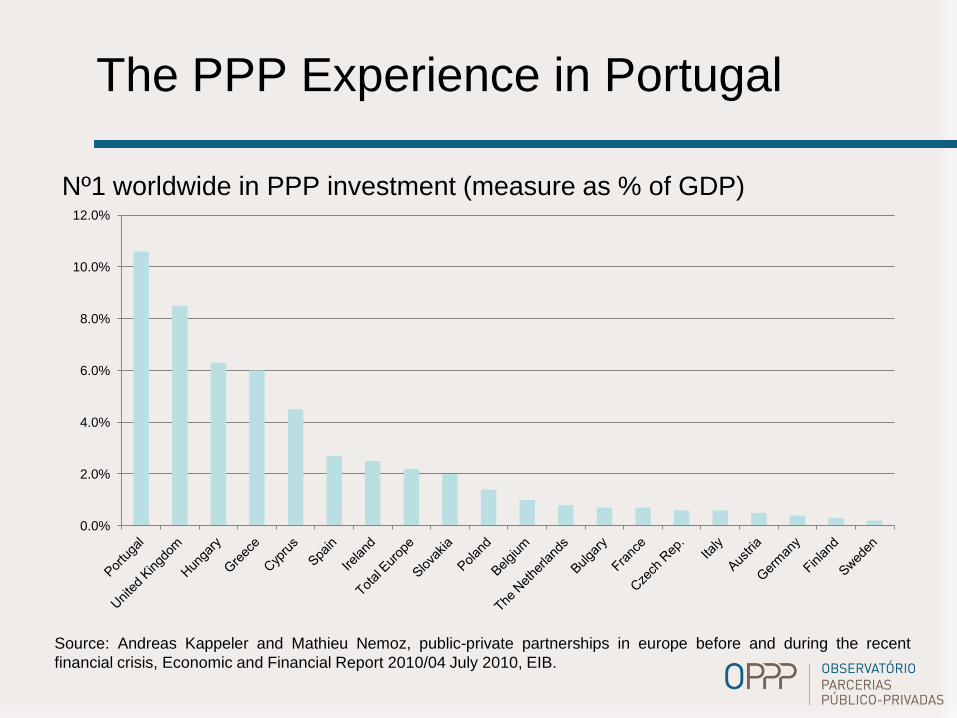

The PPP Experience in Portugal

Nº1 worldwide in PPP investment (measure as % of GDP)

Source: Andreas Kappeler and Mathieu Nemoz, public-private partnerships in europe before and during the recent

financial crisis, Economic and Financial Report 2010/04 July 2010, EIB.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

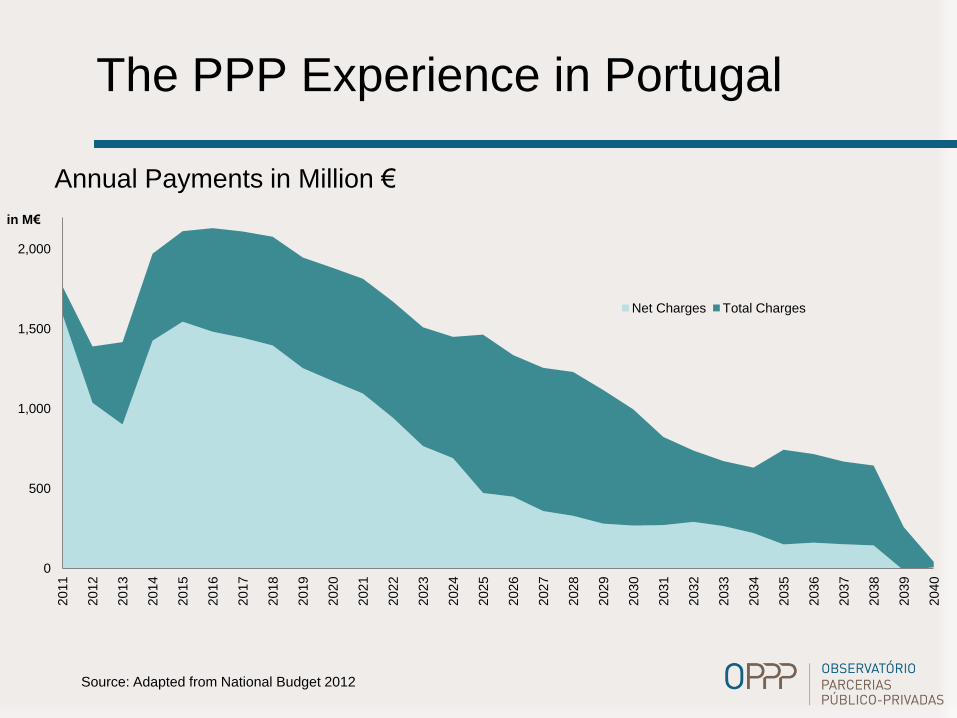

The PPP Experience in Portugal

Annual Payments in Million €

0

500

1,000

1,500

2,000

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

in M€

Net Charges Total Charges

Source: Adapted from National Budget 2012

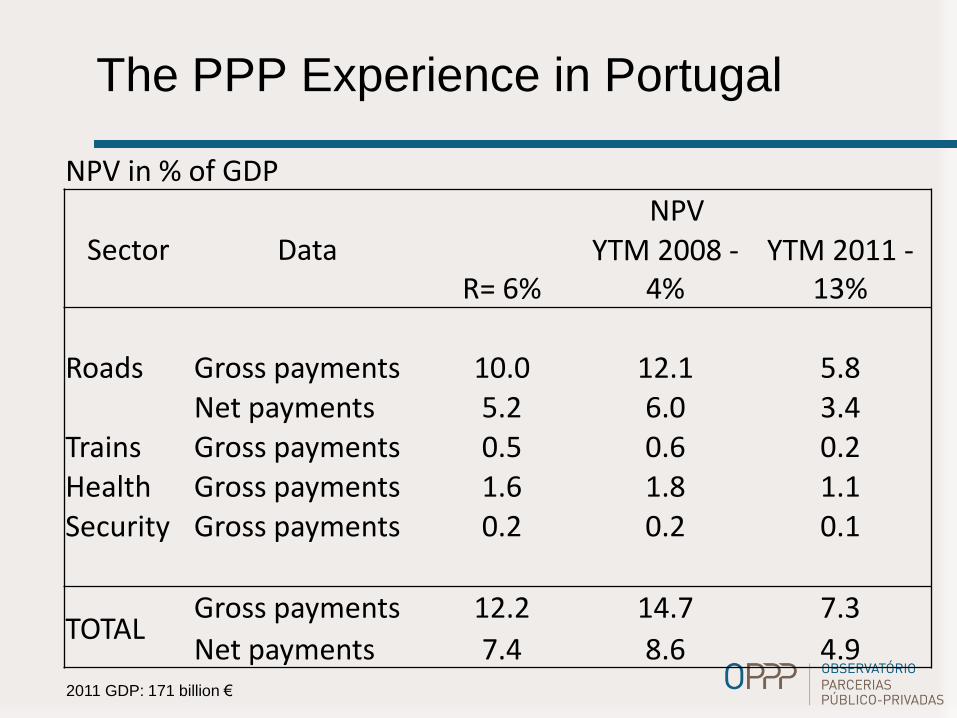

The PPP Experience in Portugal

2011 GDP: 171 billion €

NPV in % of GDP

Sector Data NPV

R= 6% YTM 2008 -

4% YTM 2011 -

13% Roads Gross payments 10.0 12.1 5.8 Net payments 5.2 6.0 3.4 Trains Gross payments 0.5 0.6 0.2 Health Gross payments 1.6 1.8 1.1 Security Gross payments 0.2 0.2 0.1

TOTAL Gross payments 12.2 14.7 7.3

Net payments 7.4 8.6 4.9

The PPP Experience in Portugal:

7 main reasons for concern

1. High levels of investment in a short period of time.

2. Deficit on structure and management skills.

3. Poor public management during the bidder process: PSC only after 2006

The PPP Experience in Portugal:

7 main reasons for concern

4. PPP focus only as off-budget operation.

5. Poor budget control of financial assumptions.

6. Incorrect risk valuation and allocation.

7. PPP renegotiations have systematically increased the payments for public

PPPs in the Memorandum of

Understanding with The Troika

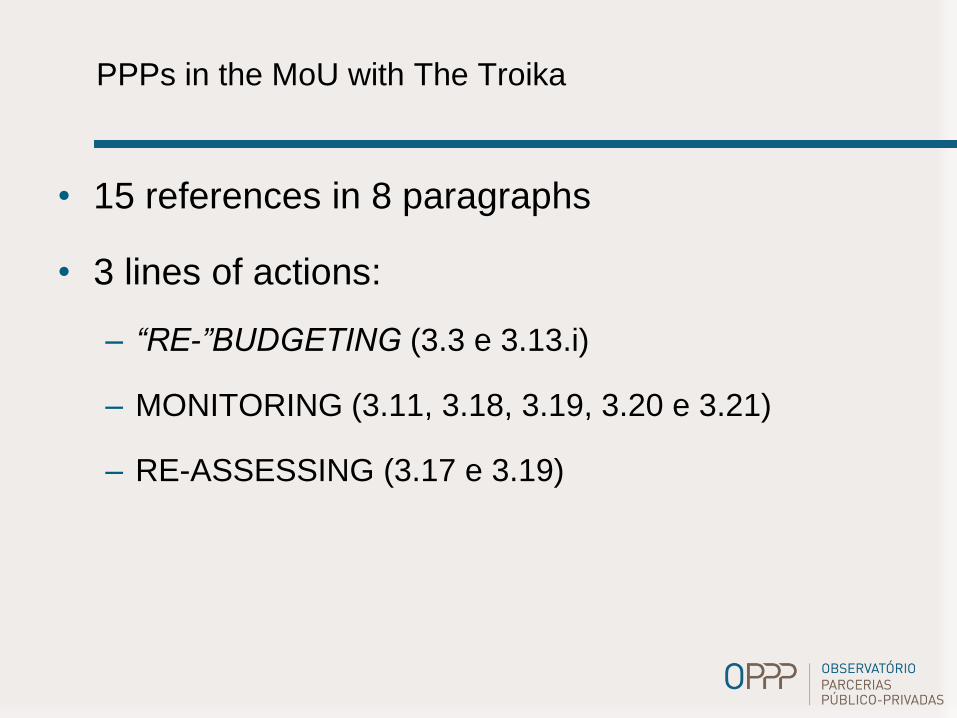

PPPs in the MoU with The Troika

• 15 references in 8 paragraphs

• 3 lines of actions:

– “RE-”BUDGETING (3.3 e 3.13.i)

– MONITORING (3.11, 3.18, 3.19, 3.20 e 3.21)

– RE-ASSESSING (3.17 e 3.19)

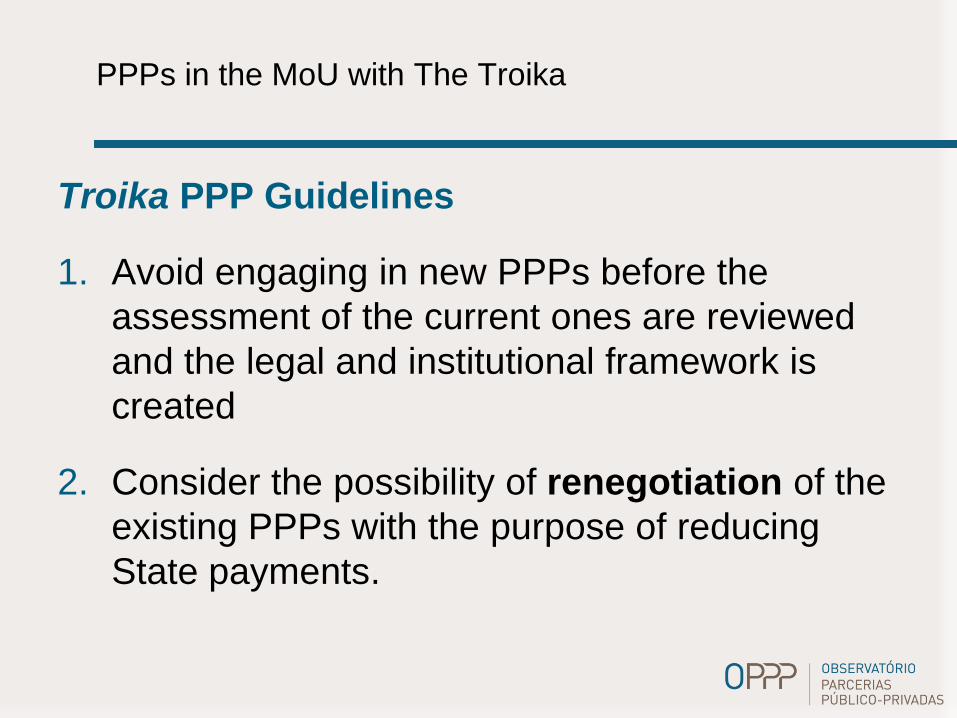

PPPs in the MoU with The Troika

Troika PPP Guidelines

1. Avoid engaging in new PPPs before the

assessment of the current ones are reviewed

and the legal and institutional framework is

created

2. Consider the possibility of renegotiation of the

existing PPPs with the purpose of reducing

State payments.

The future of PPP in

Portugal:

What solutions?

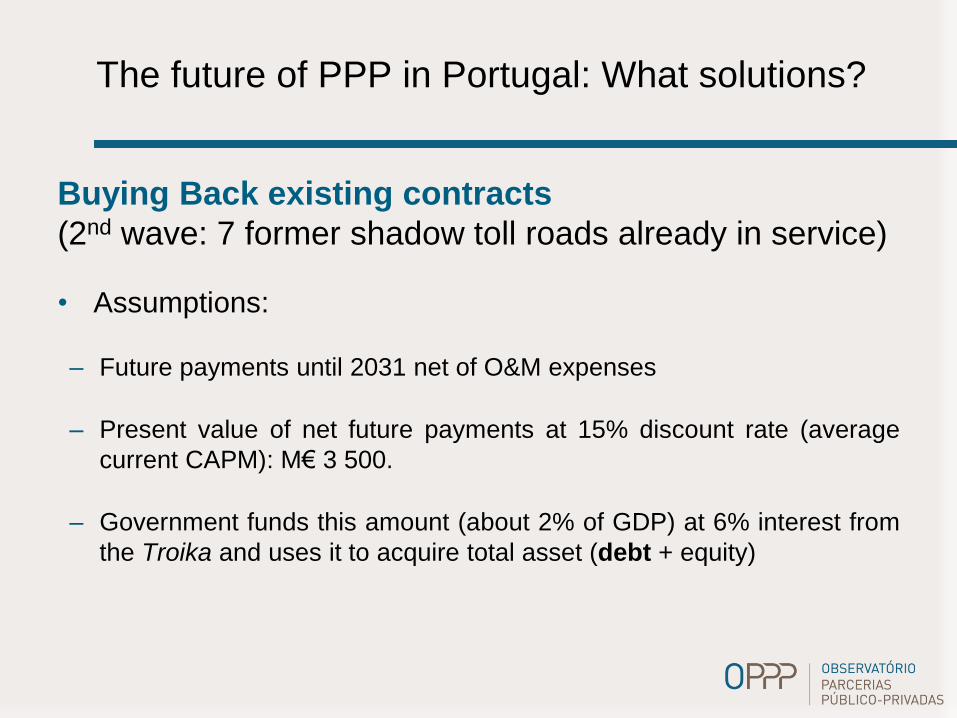

The future of PPP in Portugal: What solutions?

Buying Back existing contracts

(2nd wave: 7 former shadow toll roads already in service)

• Assumptions:

– Future payments until 2031 net of O&M expenses

– Present value of net future payments at 15% discount rate (average

current CAPM): M€ 3 500.

– Government funds this amount (about 2% of GDP) at 6% interest from

the Troika and uses it to acquire total asset (debt + equity)

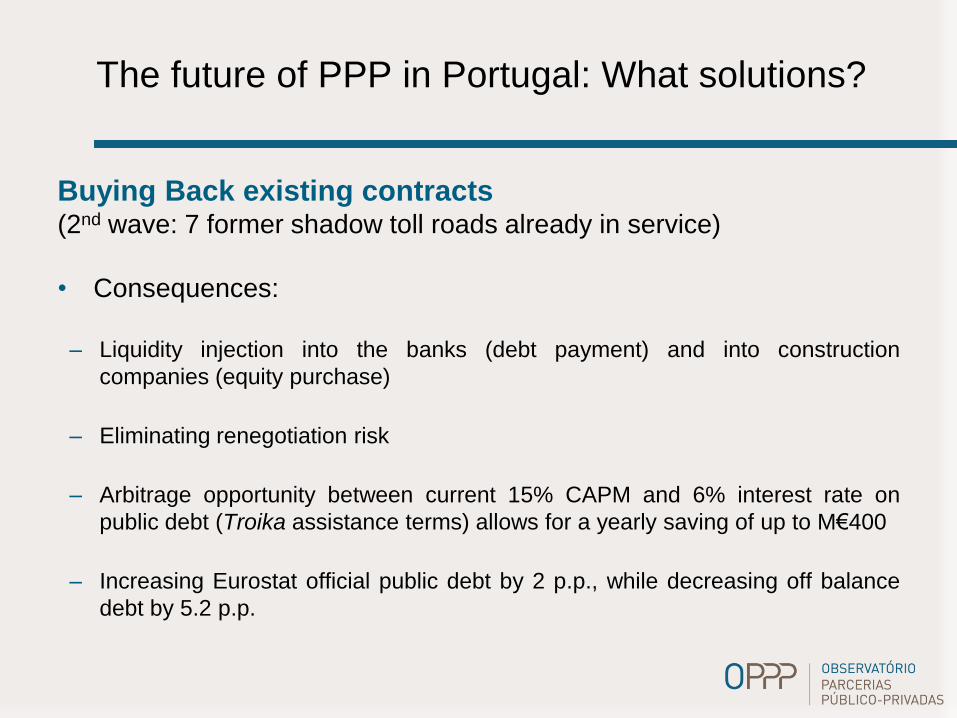

The future of PPP in Portugal: What solutions?

Buying Back existing contracts (2nd wave: 7 former shadow toll roads already in service)

• Consequences:

– Liquidity injection into the banks (debt payment) and into construction

companies (equity purchase)

– Eliminating renegotiation risk

– Arbitrage opportunity between current 15% CAPM and 6% interest rate on

public debt (Troika assistance terms) allows for a yearly saving of up to M€400

– Increasing Eurostat official public debt by 2 p.p., while decreasing off balance

debt by 5.2 p.p.

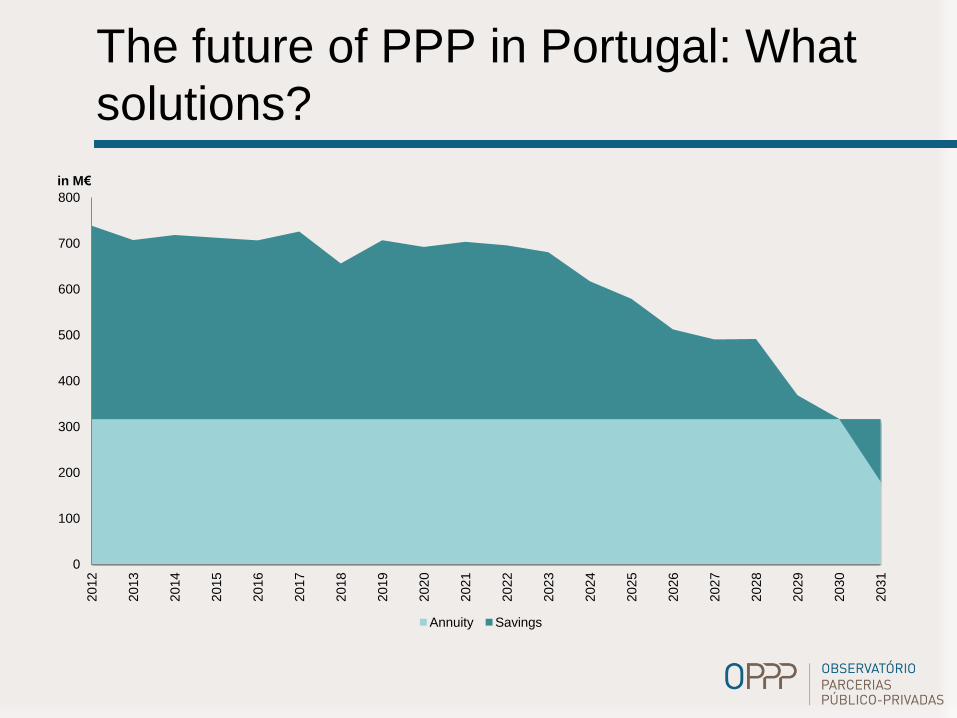

The future of PPP in Portugal: What

solutions?

0

100

200

300

400

500

600

700

800

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

in M€

Annuity Savings

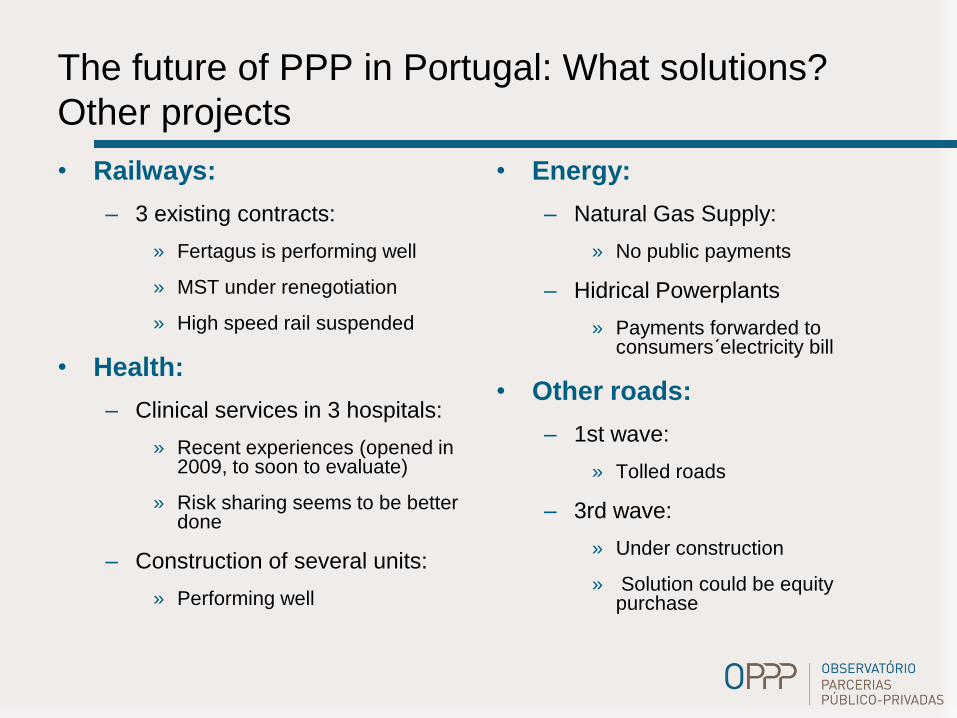

The future of PPP in Portugal: What solutions?

Other projects

• Railways:

– 3 existing contracts:

» Fertagus is performing well

» MST under renegotiation

» High speed rail suspended

• Health:

– Clinical services in 3 hospitals:

» Recent experiences (opened in 2009, to soon to evaluate)

» Risk sharing seems to be better done

– Construction of several units:

» Performing well

• Energy:

– Natural Gas Supply:

» No public payments

– Hidrical Powerplants

» Payments forwarded to consumers´electricity bill

• Other roads:

– 1st wave:

» Tolled roads

– 3rd wave:

» Under construction

» Solution could be equity purchase

The OPPP: Our mission,

organization and work.

TR

IPLE

CR

OW

N

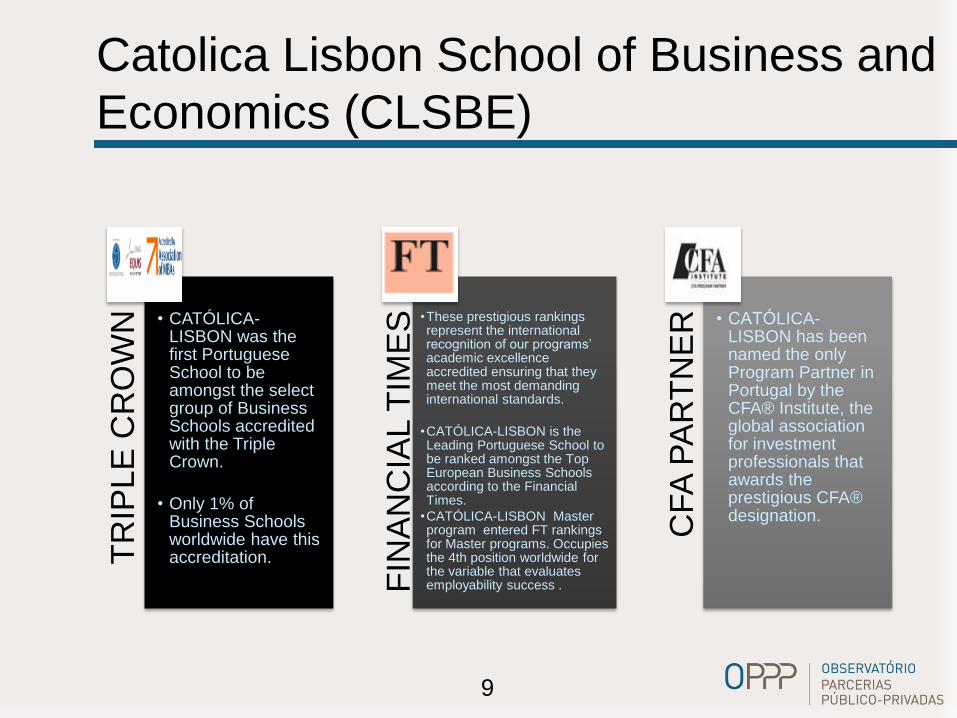

• CATÓLICA-LISBON was the first Portuguese School to be amongst the select group of Business Schools accredited with the Triple Crown.

• Only 1% of Business Schools worldwide have this accreditation.

FIN

AN

CIA

L T

IME

S

•These prestigious rankings represent the international recognition of our programs’ academic excellence accredited ensuring that they meet the most demanding international standards.

•CATÓLICA-LISBON is the Leading Portuguese School to be ranked amongst the Top European Business Schools according to the Financial Times.

•CATÓLICA-LISBON Master program entered FT rankings for Master programs. Occupies the 4th position worldwide for the variable that evaluates employability success .

CF

A P

AR

TN

ER

• CATOLICA-LISBON has been named the only Program Partner in Portugal by the CFA® Institute, the global association for investment professionals that awards the prestigious CFA® designation.

Catolica Lisbon School of Business and

Economics (CLSBE)

9

Center for Applied Studies (CEA)

• Applied research and consulting unit of CLSBE.

• Mission: to provide a continuous link between

the academic world and companies, offering

consulting services in the areas of economics

and management to private, public and social

institutions.

• These services are mainly driven by the

aplication, to real world situations, of several

research topics conducted by CLSBE faculty.

10

The OPPP

• Created in 2009, the Public-Private Partnerships

Observatory (OPPP) is an independent, not for

profit, research driven organization, based in

CLSBE

• The Observatory develops a systematic approach

to PPPs in Portugal, providing rigorous analytical

information to its members, and keeping them

also informed about relevant market

developments.

11

The OPPP

• Currently (October 2011) the OPPP has 30

paying members, among public entities and

regulators, private contractors and

concessionaries, banking and finance institutions,

consulting companies and law firms.

• The independence of the OPPP is promoted by

the balance in the composition of its membership

base: every category of players in the PPPs’

contract is always well represented.

12

The OPPP

• This balanced diversity of members also adds to

the expertise, knowledge base, and networking of

the OPPP, turning it into the perfect forum for

open, frank and insightful discussion on PPPs in

the country.

• Each member pays a yearly fee and gets first

hand access to all the research produced

internally and participates in the discussions and

events organized by the OPPP. The fees are

used exclusively to cover the research activities of

the Observatory. 13

Research Projects at OPPP

• PPP risk assessment methodology

(2008-2009)

• Portuguese PPP risk assessment and

Regressions analysis (since 2009)

• Public Sector Comparator (2010)

• Renegotiation and Refinancing (2011-2012)

• Corporate Governance (2012-2013)

14