Embed Size (px)

Citation preview

1

The global Oil & Gas market trends Oil Supply scenarios, Demand-Supply balances, Stock changes and Price

Gas market in general with focus on the LNG market

Challenges and opportunities for Egypt

2

0

20

40

60

80

100

120

Inflated oil price (2015) (USD/bbl) Money of the day (USD / bbl) Linear (Inflated oil price (2015) (USD/bbl))

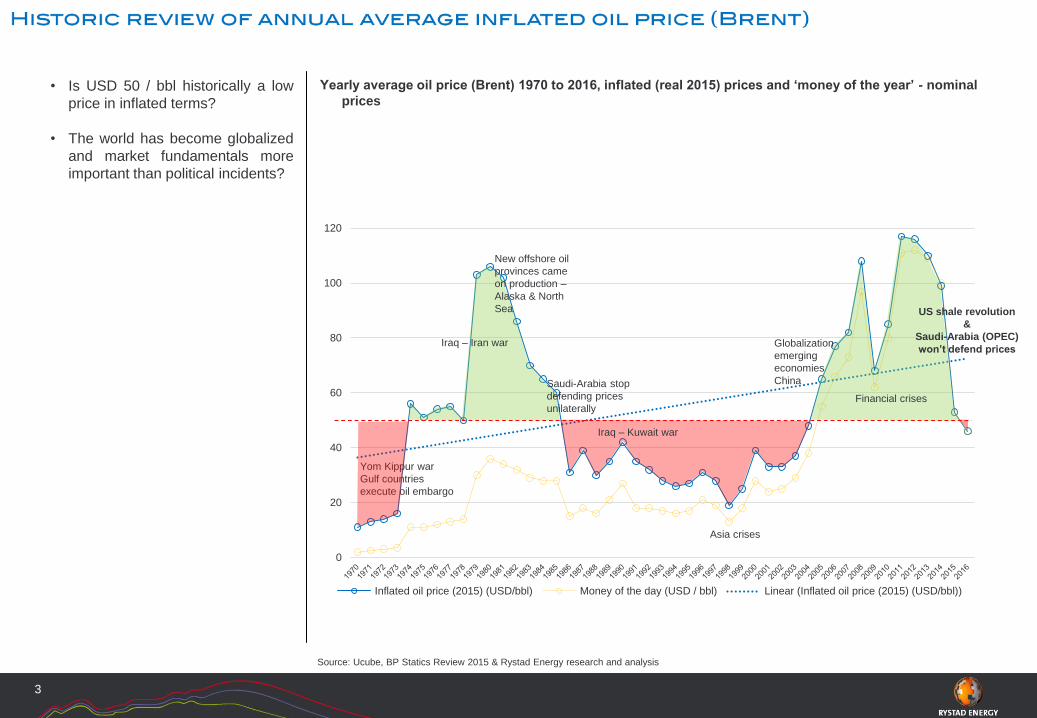

Source: Ucube, BP Statics Review 2015 & Rystad Energy research and analysis

Yearly average oil price (Brent) 1970 to 2016, inflated (real 2015) prices and ‘money of the year’ - nominal

prices

3

Yom Kippur war

Gulf countries

execute oil embargo

Iraq – Iran war

Iraq – Kuwait war

Asia crises

US shale revolution

&

Saudi-Arabia (OPEC)

won’t defend prices

New offshore oil

provinces came

on production –

Alaska & North

Sea

Saudi-Arabia stop

defending prices

unilaterallyFinancial crises

Globalization

emerging

economies

China

• Is USD 50 / bbl historically a low

price in inflated terms?

• The world has become globalized

and market fundamentals more

important than political incidents?

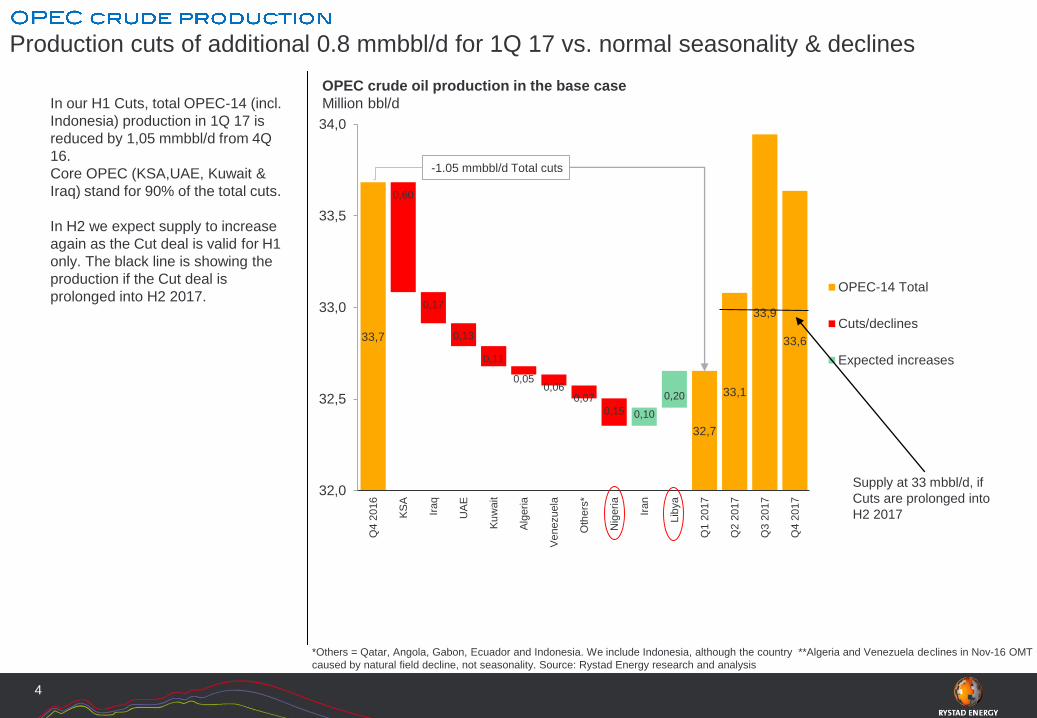

In our H1 Cuts, total OPEC-14 (incl.

Indonesia) production in 1Q 17 is

reduced by 1,05 mmbbl/d from 4Q

16.

Core OPEC (KSA,UAE, Kuwait &

Iraq) stand for 90% of the total cuts.

In H2 we expect supply to increase

again as the Cut deal is valid for H1

only. The black line is showing the

production if the Cut deal is

prolonged into H2 2017.

Production cuts of additional 0.8 mmbbl/d for 1Q 17 vs. normal seasonality & declines

*Others = Qatar, Angola, Gabon, Ecuador and Indonesia. We include Indonesia, although the country **Algeria and Venezuela declines in Nov-16 OMT

caused by natural field decline, not seasonality. Source: Rystad Energy research and analysis

4

OPEC crude oil production in the base case

Million bbl/d

33,7

32,7

33,1

33,9

33,6

0,60

0,17

0,13

0,11

0,050,06

0,07

0,15 0,10

0,20

32,0

32,5

33,0

33,5

34,0

Q4 2

016

KS

A

Iraq

UA

E

Ku

wait

Alg

eria

Ve

nezuela

Oth

ers

*

Nig

eria

Iran

Lib

ya

Q1 2

017

Q2 2

017

Q3 2

017

Q4 2

017

OPEC-14 Total

Cuts/declines

Expected increases

-1.05 mmbbl/d Total cuts

Supply at 33 mbbl/d, if

Cuts are prolonged into

H2 2017

H1 2017

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Jul-16

Au

g-1

6

Se

p-1

6

Oct-

16

No

v-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

Ma

r-1

7

Apr-

17

Ma

y-1

7

Ju

n-1

7

Ju

l-1

7

Au

g-1

7

Se

p-1

7

Oct-

17

No

v-1

7

De

c-1

7

Nigeria

Nigeria Ave 2016/2017levelLibya

Libya Ave 2016/2017levelLibya upside risk

ForecastHistorical

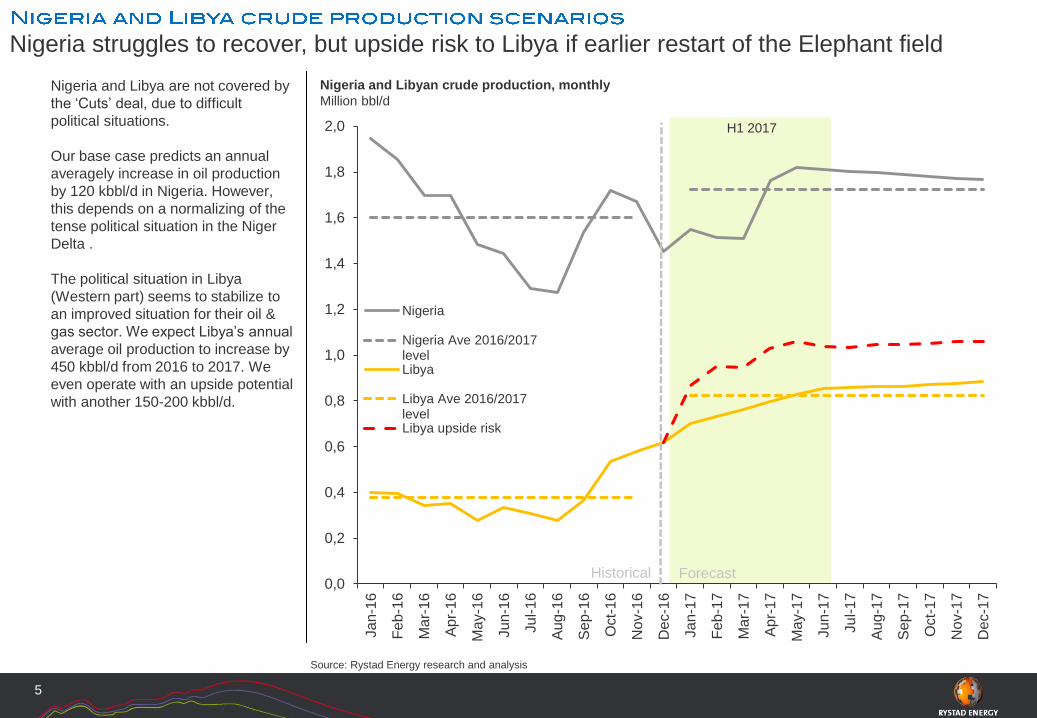

Nigeria and Libya are not covered by

the ‘Cuts’ deal, due to difficult

political situations.

Our base case predicts an annual

averagely increase in oil production

by 120 kbbl/d in Nigeria. However,

this depends on a normalizing of the

tense political situation in the Niger

Delta .

The political situation in Libya

(Western part) seems to stabilize to

an improved situation for their oil &

gas sector. We expect Libya’s annual

average oil production to increase by

450 kbbl/d from 2016 to 2017. We

even operate with an upside potential

with another 150-200 kbbl/d.

Nigeria struggles to recover, but upside risk to Libya if earlier restart of the Elephant field

Source: Rystad Energy research and analysis

Nigeria and Libyan crude production, monthly

Million bbl/d

5

18,22

17,89

17,81 17,8017,84

0,18

0,08

0,06

0,020,02

0,020,01

0,04

0,02 0,01 0,00

17,6

17,7

17,8

17,9

18,0

18,1

18,2

18,3

Tota

l N

on-O

PE

C *

Ru

ssia

Me

xic

o

Kazakhsta

n

Om

an

Aze

rbaija

n

Ma

laysia

Equa

toria

l G

uin

ea

South

Suda

n

Bru

nei

Suda

n

Bahra

in

1Q

2017

2Q

2017

3Q

2017

4Q

2017

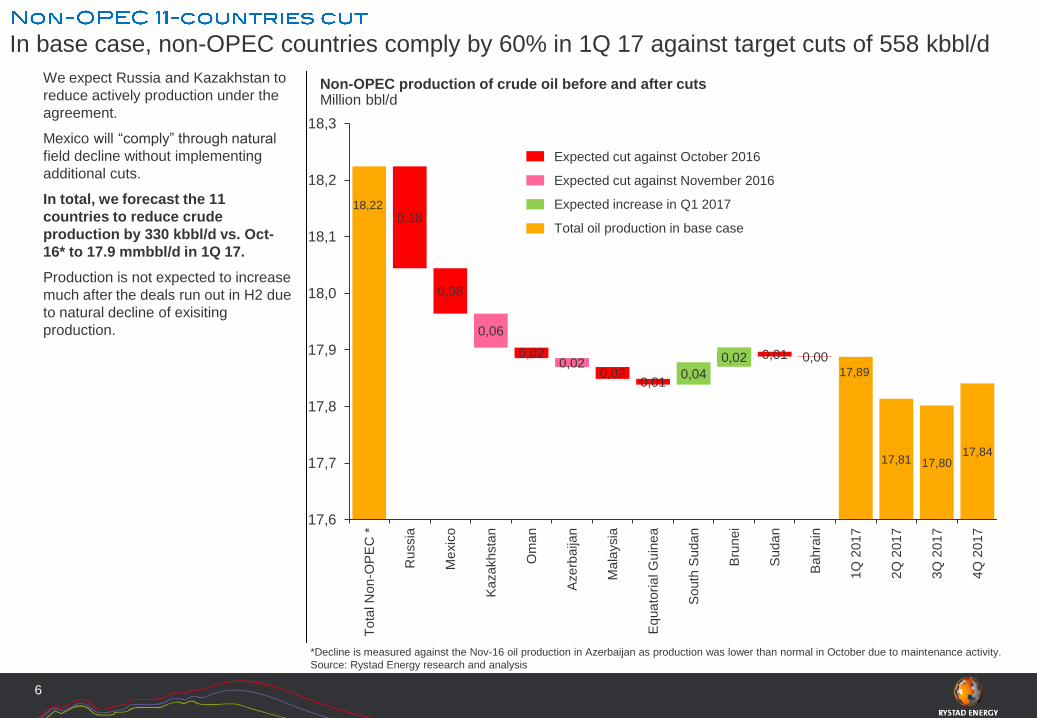

In base case, non-OPEC countries comply by 60% in 1Q 17 against target cuts of 558 kbbl/d

*Decline is measured against the Nov-16 oil production in Azerbaijan as production was lower than normal in October due to maintenance activity.

Source: Rystad Energy research and analysis

Non-OPEC production of crude oil before and after cutsMillion bbl/d

6

Expected cut against October 2016

Expected cut against November 2016

Expected increase in Q1 2017

Total oil production in base case

We expect Russia and Kazakhstan to

reduce actively production under the

agreement.

Mexico will “comply” through natural

field decline without implementing

additional cuts.

In total, we forecast the 11

countries to reduce crude

production by 330 kbbl/d vs. Oct-

16* to 17.9 mmbbl/d in 1Q 17.

Production is not expected to increase

much after the deals run out in H2 due

to natural decline of exisiting

production.

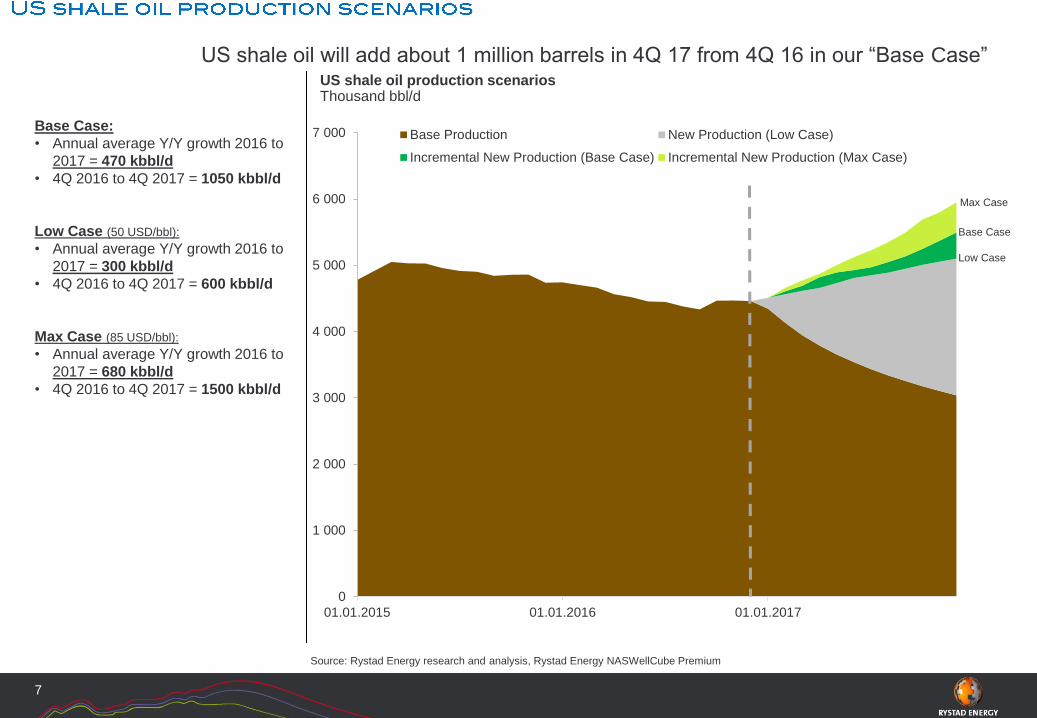

Base Case:

• Annual average Y/Y growth 2016 to

2017 = 470 kbbl/d

• 4Q 2016 to 4Q 2017 = 1050 kbbl/d

Low Case (50 USD/bbl):

• Annual average Y/Y growth 2016 to

2017 = 300 kbbl/d

• 4Q 2016 to 4Q 2017 = 600 kbbl/d

Max Case (85 USD/bbl):

• Annual average Y/Y growth 2016 to

2017 = 680 kbbl/d

• 4Q 2016 to 4Q 2017 = 1500 kbbl/d

US shale oil will add about 1 million barrels in 4Q 17 from 4Q 16 in our “Base Case”

Source: Rystad Energy research and analysis, Rystad Energy NASWellCube Premium

US shale oil production scenariosThousand bbl/d

7

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

01.01.2015 01.01.2016 01.01.2017

Base Production New Production (Low Case)

Incremental New Production (Base Case) Incremental New Production (Max Case)

Base Case

Low Case

Max Case

0,5

1,2

1,5

1,2

2,1

1,61,4

1,1 1,21,3 1,4

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Other Non-OECD

Other Middle East

Brazil

Russia

Saudi Arabia

India

China

OECD Europe

OECD Americas

OECD Asia and Oceania

Total World

Trend average 1,2 mbbld

ForecastHistorical

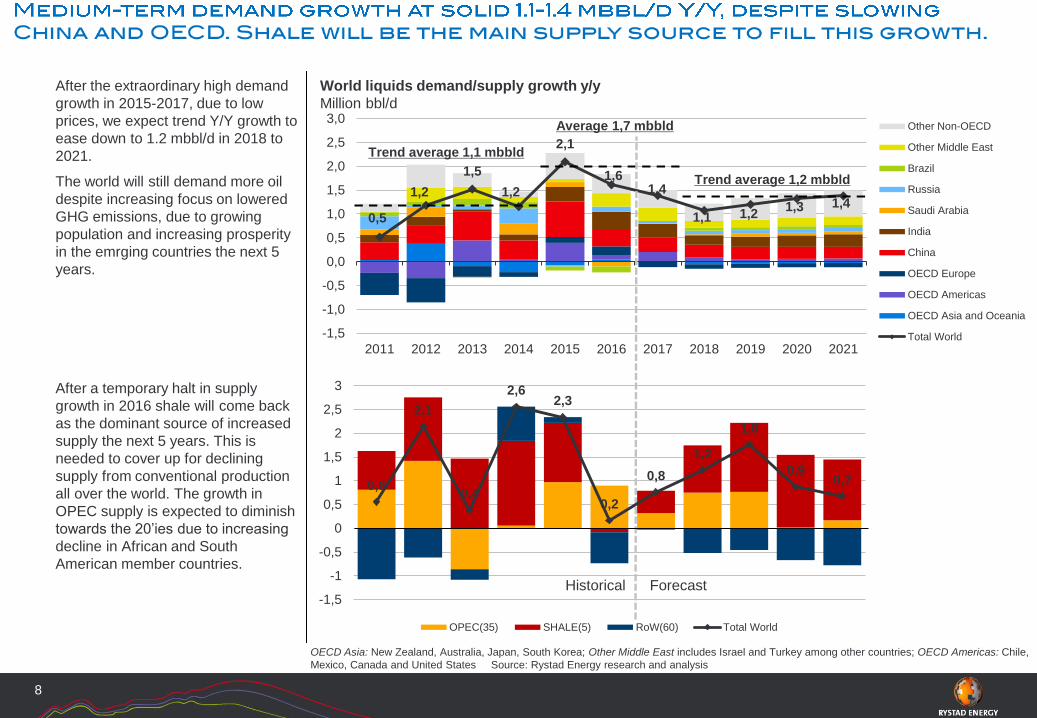

After the extraordinary high demand

growth in 2015-2017, due to low

prices, we expect trend Y/Y growth to

ease down to 1.2 mbbl/d in 2018 to

2021.

The world will still demand more oil

despite increasing focus on lowered

GHG emissions, due to growing

population and increasing prosperity

in the emrging countries the next 5

years.

OECD Asia: New Zealand, Australia, Japan, South Korea; Other Middle East includes Israel and Turkey among other countries; OECD Americas: Chile,

Mexico, Canada and United States Source: Rystad Energy research and analysis

World liquids demand/supply growth y/y

Million bbl/d

8

Trend average 1,1 mbbld

Average 1,7 mbbld

0,6

2,1

0,4

2,62,3

0,2

0,8

1,2

1,8

0,90,7

-1,5

-1

-0,5

0

0,5

1

1,5

2

2,5

3

OPEC(35) SHALE(5) RoW(60) Total World

After a temporary halt in supply

growth in 2016 shale will come back

as the dominant source of increased

supply the next 5 years. This is

needed to cover up for declining

supply from conventional production

all over the world. The growth in

OPEC supply is expected to diminish

towards the 20’ies due to increasing

decline in African and South

American member countries.

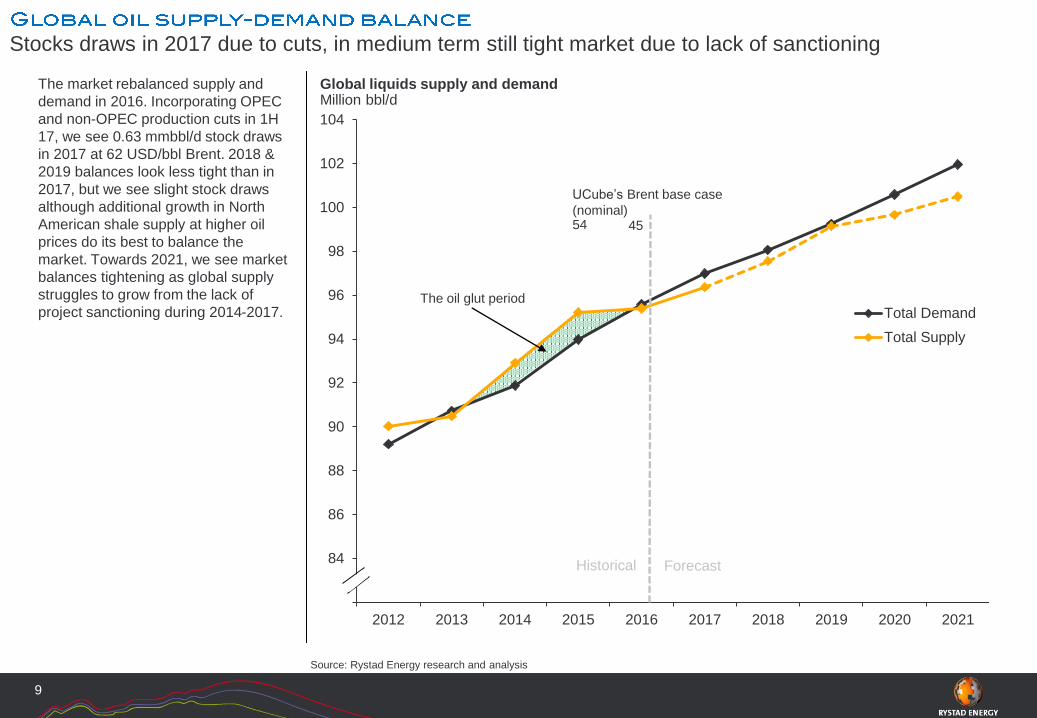

The market rebalanced supply and

demand in 2016. Incorporating OPEC

and non-OPEC production cuts in 1H

17, we see 0.63 mmbbl/d stock draws

in 2017 at 62 USD/bbl Brent. 2018 &

2019 balances look less tight than in

2017, but we see slight stock draws

although additional growth in North

American shale supply at higher oil

prices do its best to balance the

market. Towards 2021, we see market

balances tightening as global supply

struggles to grow from the lack of

project sanctioning during 2014-2017.

Stocks draws in 2017 due to cuts, in medium term still tight market due to lack of sanctioning

Source: Rystad Energy research and analysis

Global liquids supply and demandMillion bbl/d

9

82

84

86

88

90

92

94

96

98

100

102

104

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Demand

Total Supply

ForecastHistorical

4554

UCube’s Brent base case

(nominal)

The oil glut period

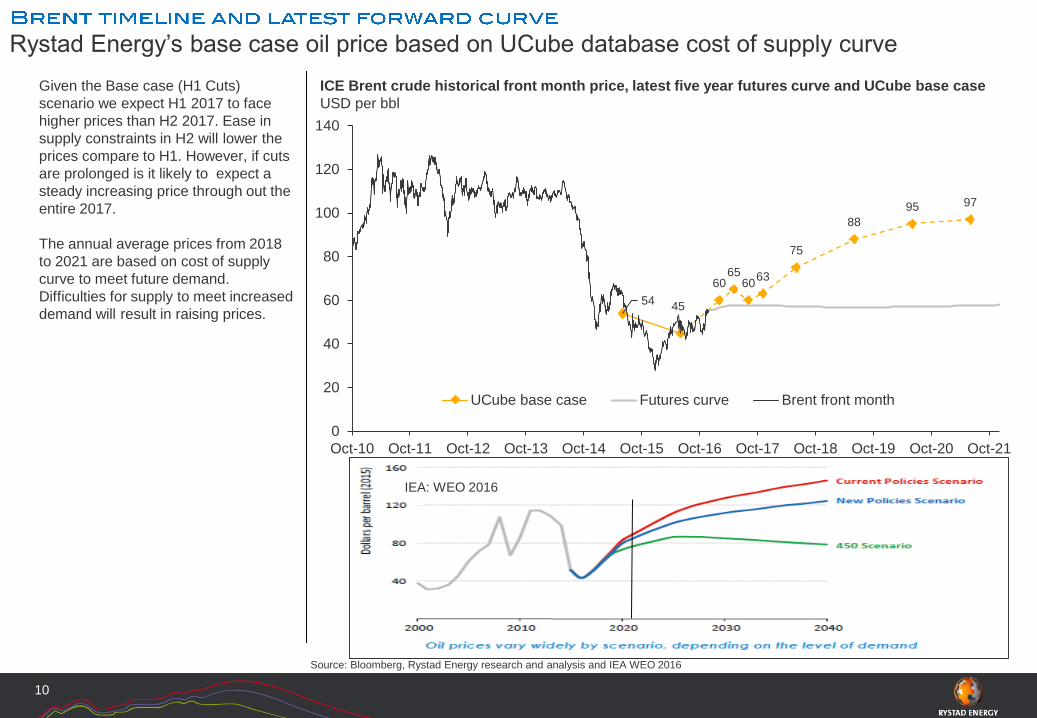

Given the Base case (H1 Cuts)

scenario we expect H1 2017 to face

higher prices than H2 2017. Ease in

supply constraints in H2 will lower the

prices compare to H1. However, if cuts

are prolonged is it likely to expect a

steady increasing price through out the

entire 2017.

The annual average prices from 2018

to 2021 are based on cost of supply

curve to meet future demand.

Difficulties for supply to meet increased

demand will result in raising prices.

Rystad Energy’s base case oil price based on UCube database cost of supply curve

Source: Bloomberg, Rystad Energy research and analysis and IEA WEO 2016

ICE Brent crude historical front month price, latest five year futures curve and UCube base case

USD per bbl

10

5445

6065

6063

75

88

95 97

0

20

40

60

80

100

120

140

Oct-10 Oct-11 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21

UCube base case Futures curve Brent front month

IEA: WEO 2016

11

The global Oil & Gas market trends Oil Supply scenarios, Demand-Supply balances, Stock changes and Price

Gas market in general with focus on the LNG market

Challenges and opportunities for Egypt

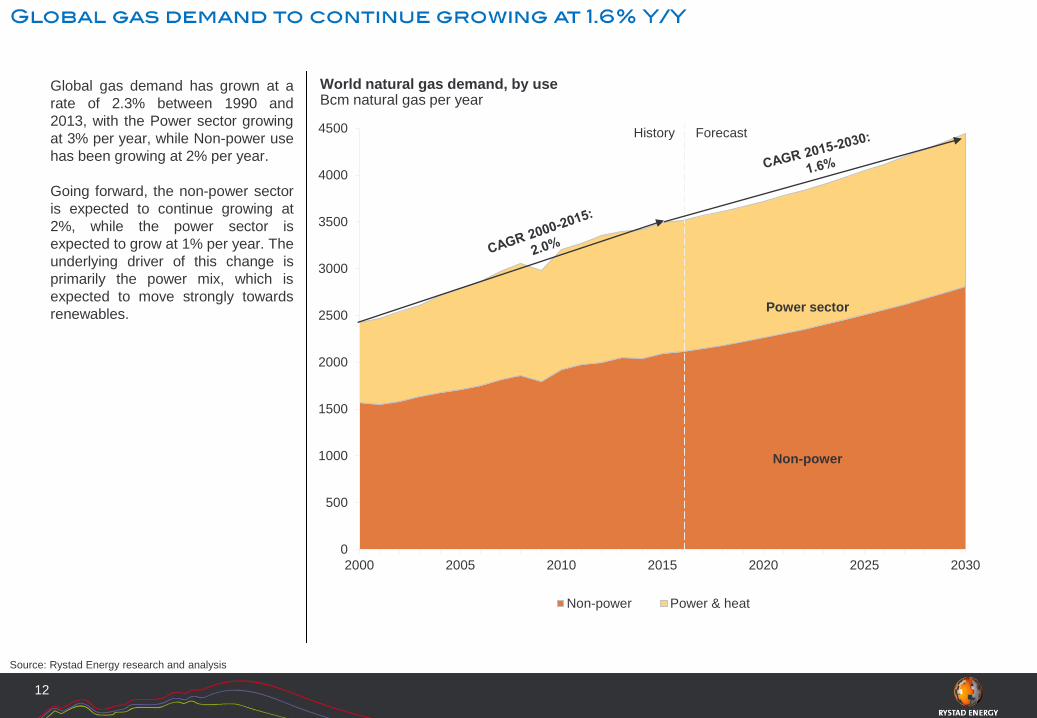

Global gas demand has grown at a

rate of 2.3% between 1990 and

2013, with the Power sector growing

at 3% per year, while Non-power use

has been growing at 2% per year.

Going forward, the non-power sector

is expected to continue growing at

2%, while the power sector is

expected to grow at 1% per year. The

underlying driver of this change is

primarily the power mix, which is

expected to move strongly towards

renewables.

Source: Rystad Energy research and analysis

World natural gas demand, by useBcm natural gas per year

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2000 2005 2010 2015 2020 2025 2030

Non-power Power & heat

Non-power

Power sector

ForecastHistory

12

-400

200

800

1400

Net Export Net import

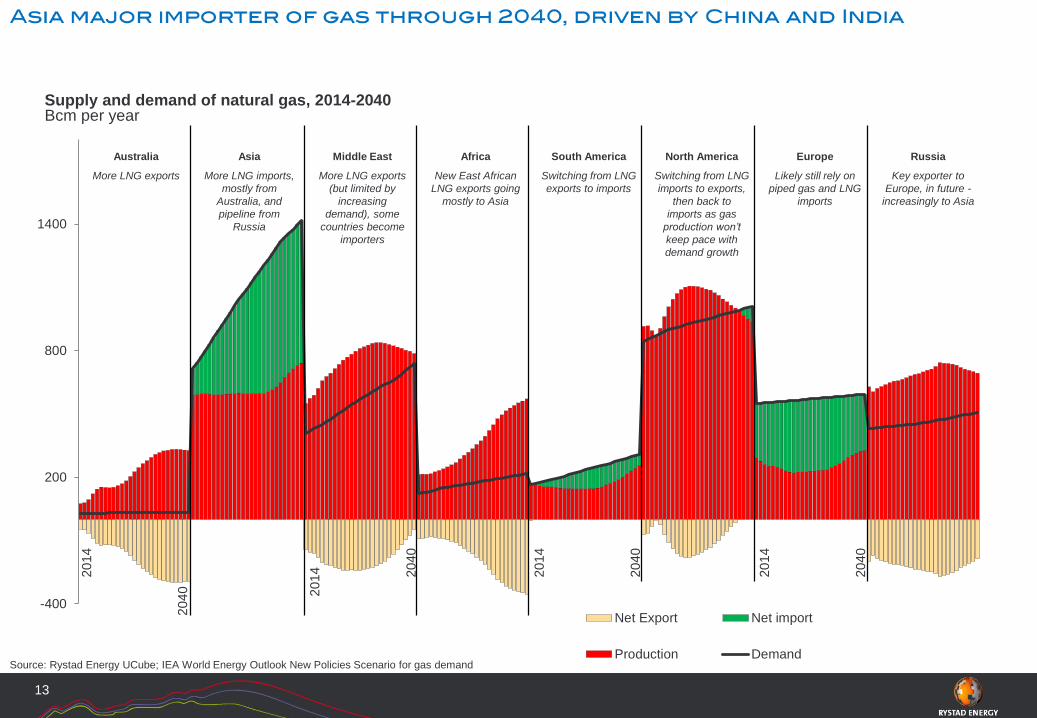

Production DemandSource: Rystad Energy UCube; IEA World Energy Outlook New Policies Scenario for gas demand

13

Supply and demand of natural gas, 2014-2040Bcm per year

Australia Asia Middle East Africa South America North America Europe Russia

More LNG exports More LNG imports,

mostly from

Australia, and

pipeline from

Russia

More LNG exports

(but limited by

increasing

demand), some

countries become

importers

New East African

LNG exports going

mostly to Asia

Switching from LNG

imports to exports,

then back to

imports as gas

production won’t

keep pace with

demand growth

Switching from LNG

exports to imports

Likely still rely on

piped gas and LNG

imports

Key exporter to

Europe, in future -

increasingly to Asia

2014

2040

2014

2040

2014 2040

2014

2040

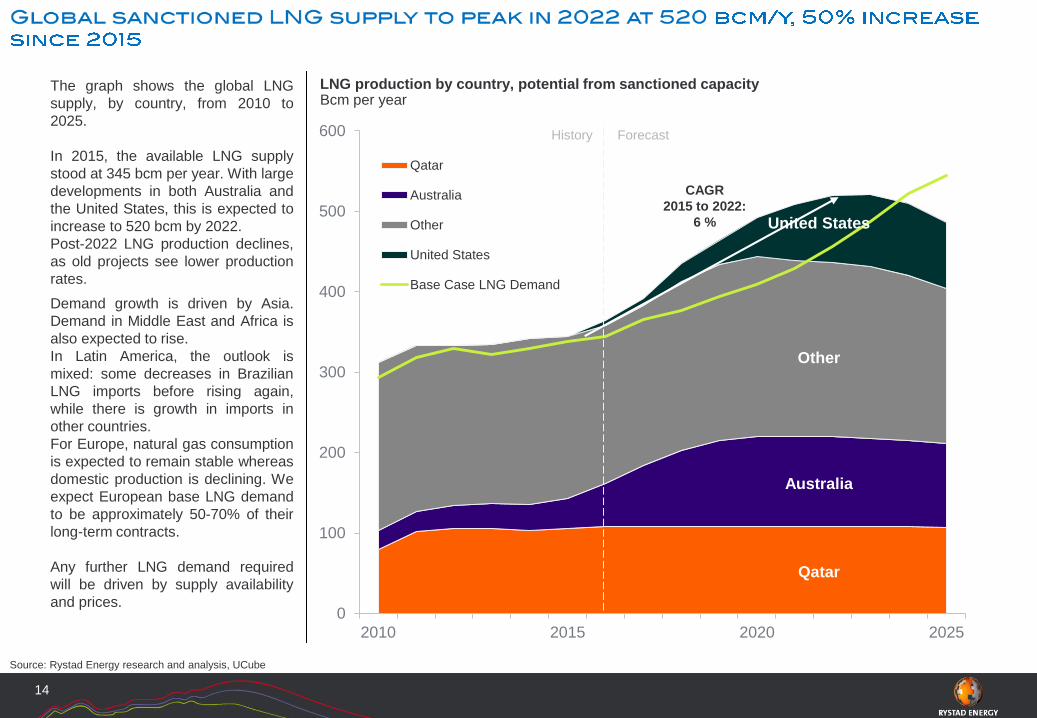

The graph shows the global LNG

supply, by country, from 2010 to

2025.

In 2015, the available LNG supply

stood at 345 bcm per year. With large

developments in both Australia and

the United States, this is expected to

increase to 520 bcm by 2022.

Post-2022 LNG production declines,

as old projects see lower production

rates.

Source: Rystad Energy research and analysis, UCube

LNG production by country, potential from sanctioned capacityBcm per year

14

0

100

200

300

400

500

600

2010 2015 2020 2025

Qatar

Australia

Other

United States

Base Case LNG Demand

United States

Other

Australia

Qatar

Demand growth is driven by Asia.

Demand in Middle East and Africa is

also expected to rise.

In Latin America, the outlook is

mixed: some decreases in Brazilian

LNG imports before rising again,

while there is growth in imports in

other countries.

For Europe, natural gas consumption

is expected to remain stable whereas

domestic production is declining. We

expect European base LNG demand

to be approximately 50-70% of their

long-term contracts.

Any further LNG demand required

will be driven by supply availability

and prices.

ForecastHistory

CAGR

2015 to 2022:

6 %

4,6

5,4

5,96,3 6,4 6,4 6,5

6,9

7,3

0

1

2

3

4

5

6

7

8

9

10

11

12

13

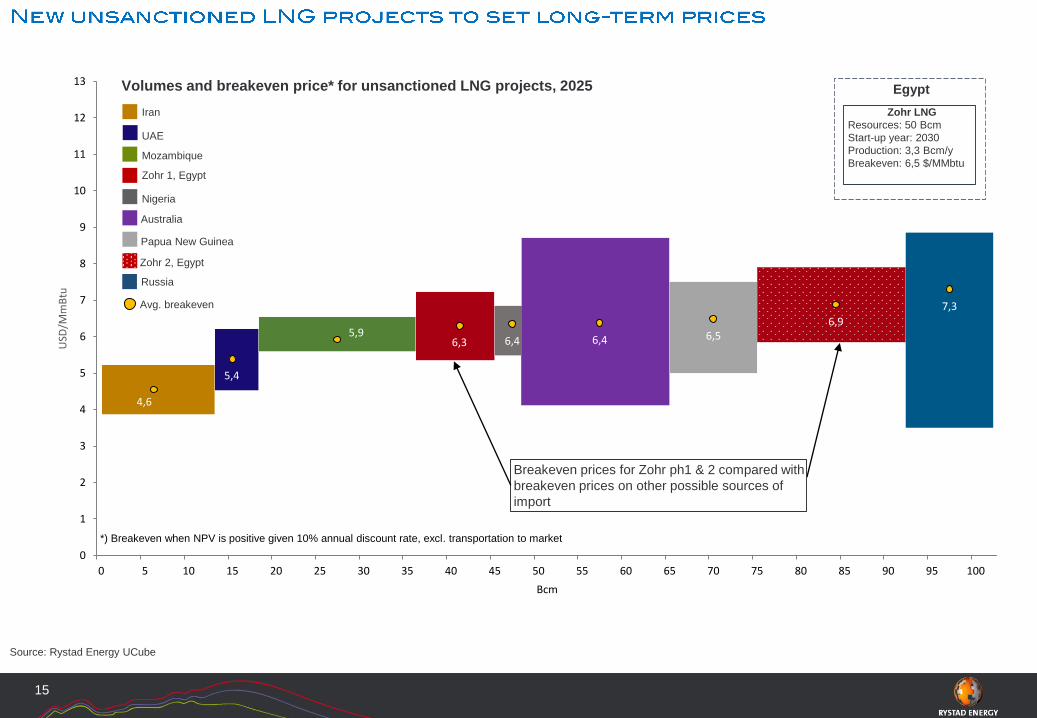

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

USD

/Mm

Btu

Bcm

*) Breakeven when NPV is positive given 10% annual discount rate, excl. transportation to market

Egypt

Zohr LNG

Resources: 50 Bcm

Start-up year: 2030

Production: 3,3 Bcm/y

Breakeven: 6,5 $/MMbtu

Source: Rystad Energy UCube

15

Volumes and breakeven price* for unsanctioned LNG projects, 2025

Iran

UAE

Mozambique

Zohr 1, Egypt

Nigeria

Australia

Avg. breakeven

Papua New Guinea

Zohr 2, Egypt

Russia

Breakeven prices for Zohr ph1 & 2 compared with

breakeven prices on other possible sources of

import

6,4

9,3

10,5

4,7

5,9

8,1

0

20

40

60

80

100

0

2

4

6

8

10

12

14

16

18

2010

201

1

2012

2013

2014

2015

2016

2017

201

8

2019

2020

2021

2022

2023

2024

202

5

USD

/bb

l

USD

/MM

Btu

Henry Hub NBPEast Asian spot LNG JCC-indexedBrent crude history Brent crude - Rystad Energy's base caseBrent crude forward

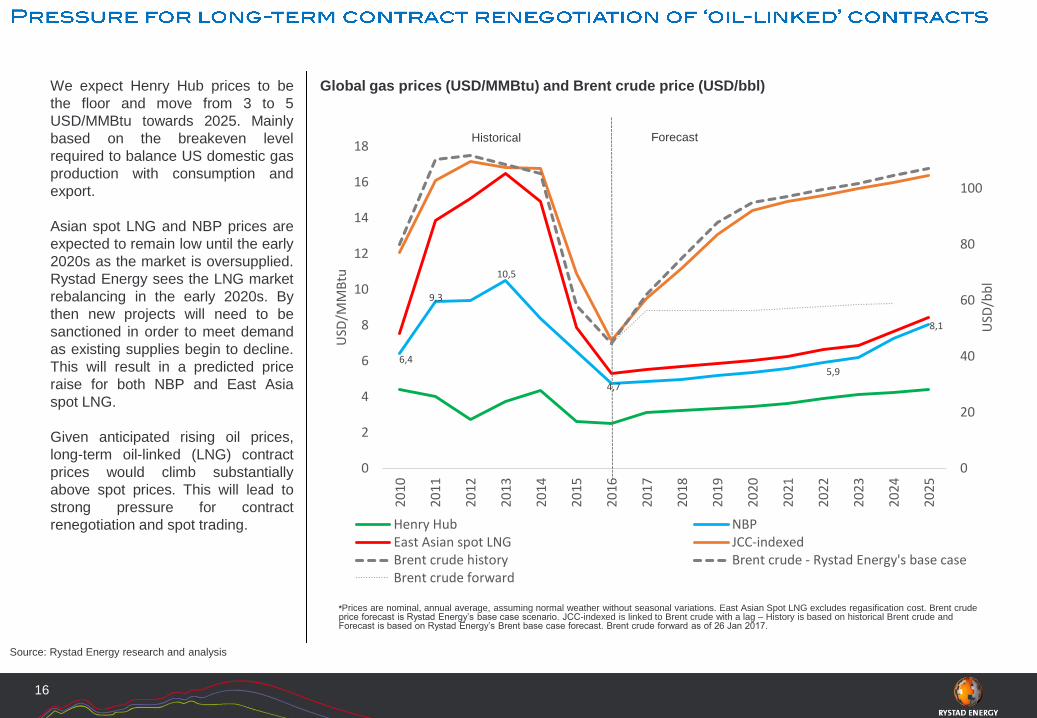

We expect Henry Hub prices to be

the floor and move from 3 to 5

USD/MMBtu towards 2025. Mainly

based on the breakeven level

required to balance US domestic gas

production with consumption and

export.

Asian spot LNG and NBP prices are

expected to remain low until the early

2020s as the market is oversupplied.

Rystad Energy sees the LNG market

rebalancing in the early 2020s. By

then new projects will need to be

sanctioned in order to meet demand

as existing supplies begin to decline.

This will result in a predicted price

raise for both NBP and East Asia

spot LNG.

Given anticipated rising oil prices,

long-term oil-linked (LNG) contract

prices would climb substantially

above spot prices. This will lead to

strong pressure for contract

renegotiation and spot trading.

Source: Rystad Energy research and analysis

Global gas prices (USD/MMBtu) and Brent crude price (USD/bbl)

16

ForecastHistorical

*Prices are nominal, annual average, assuming normal weather without seasonal variations. East Asian Spot LNG excludes regasification cost. Brent crude price forecast is Rystad Energy’s base case scenario. JCC-indexed is linked to Brent crude with a lag – History is based on historical Brent crude and Forecast is based on Rystad Energy’s Brent base case forecast. Brent crude forward as of 26 Jan 2017.

17

The global Oil & Gas market trends Oil Supply scenarios, Demand-Supply balances, Stock changes and Price

Gas market in general with focus on the LNG market

Challenges and opportunities for Egypt

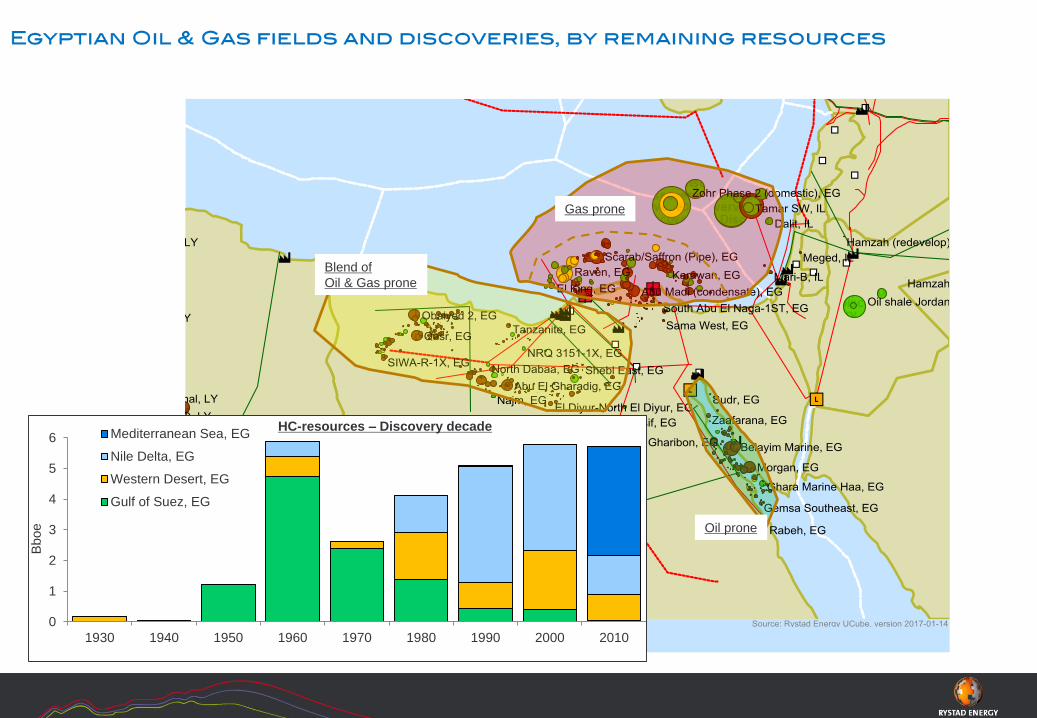

Oil prone

Gas prone

Blend of

Oil & Gas prone

0

1

2

3

4

5

6

1930 1940 1950 1960 1970 1980 1990 2000 2010

Mediterranean Sea, EG

Nile Delta, EG

Western Desert, EG

Gulf of Suez, EG

Bboe

HC-resources – Discovery decade

- 60 - 40 - 20 0 20 40 60 80

Produced

Liquids

Gas

Source: Rystad Energy research and analysis and UCube

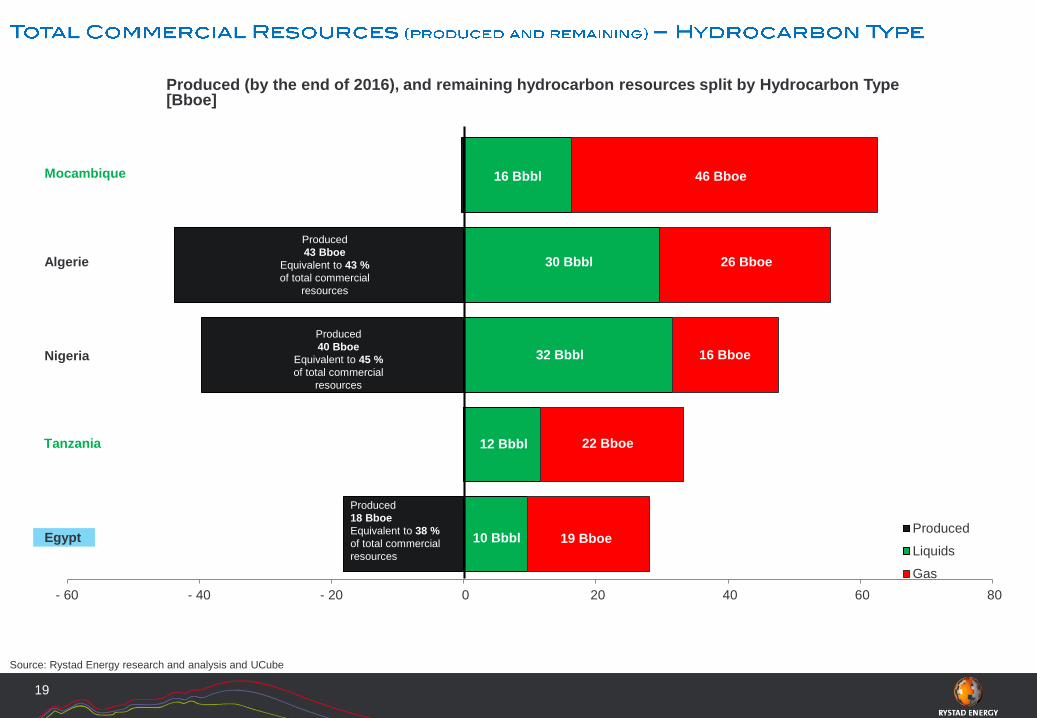

19

Produced (by the end of 2016), and remaining hydrocarbon resources split by Hydrocarbon Type[Bboe]

30 Bbbl 26 Bboe

12 Bbbl 22 Bboe

Produced

40 Bboe

Equivalent to 45 %

of total commercial

resources

Produced

18 Bboe

Equivalent to 38 %

of total commercial

resources

Produced

43 Bboe

Equivalent to 43 %

of total commercial

resources

16 Bbbl 46 BboeMocambique

Algerie

Nigeria

Egypt

Tanzania

10 Bbbl 19 Bboe

32 Bbbl 16 Bboe

Source: Rystad Energy research and analysis and UCube

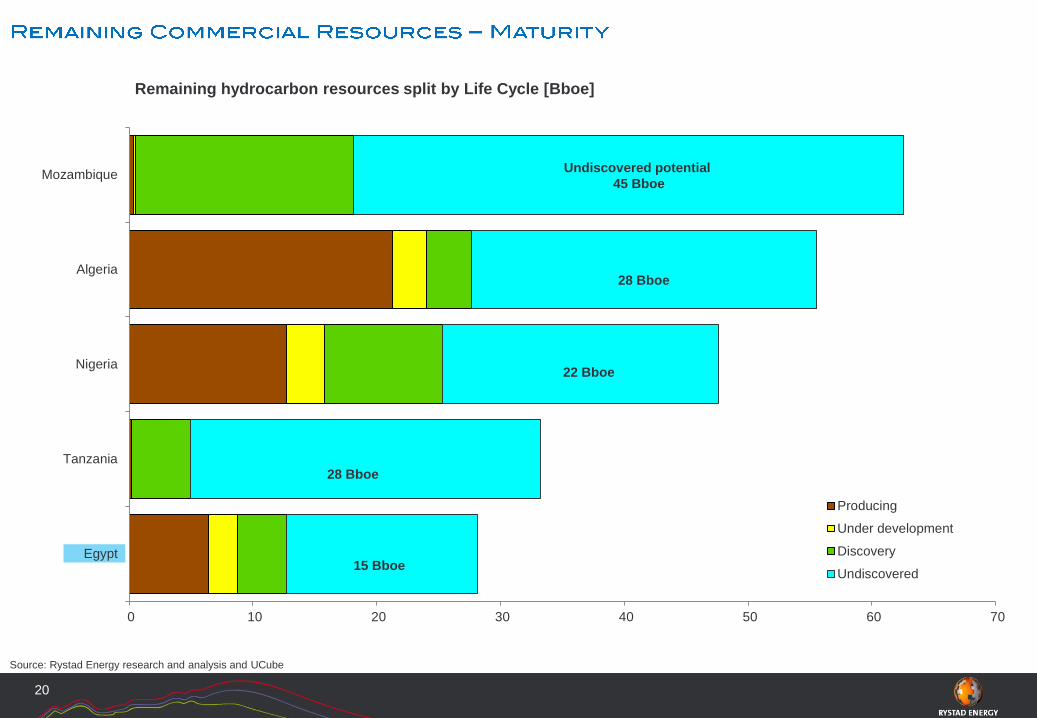

20

Remaining hydrocarbon resources split by Life Cycle [Bboe]

0 10 20 30 40 50 60 70

Mozambique

Algeria

Nigeria

Tanzania

Egypt

Producing

Under development

Discovery

Undiscovered

28 Bboe

15 Bboe

Undiscovered potential

45 Bboe

28 Bboe

22 Bboe

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000 Gas

Liquids

Source: Ucube & Rystad Energy research and analysis.

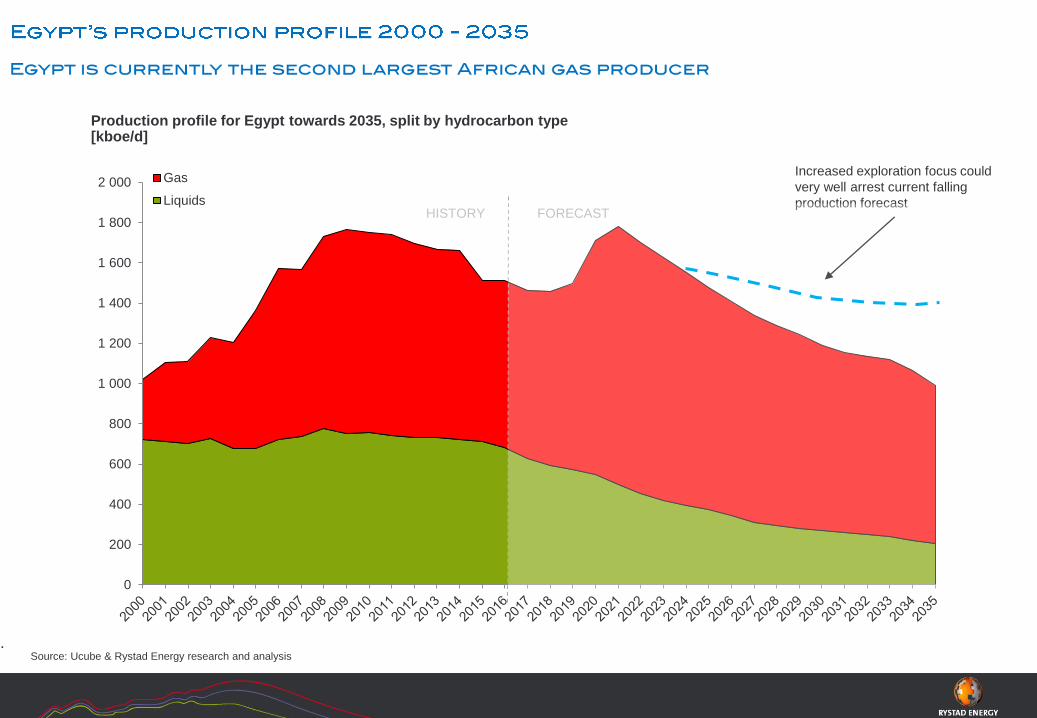

Production profile for Egypt towards 2035, split by hydrocarbon type[kboe/d]

Increased exploration focus could

very well arrest current falling

production forecastHISTORY FORECAST

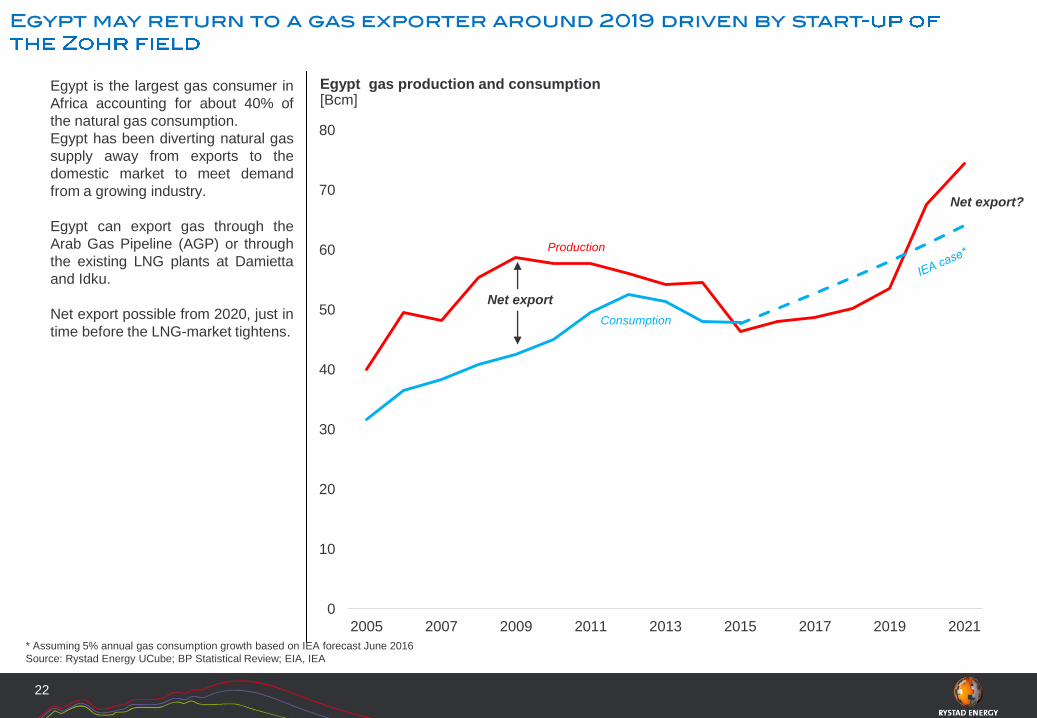

Egypt is the largest gas consumer in

Africa accounting for about 40% of

the natural gas consumption.

Egypt has been diverting natural gas

supply away from exports to the

domestic market to meet demand

from a growing industry.

Egypt can export gas through the

Arab Gas Pipeline (AGP) or through

the existing LNG plants at Damietta

and Idku.

Net export possible from 2020, just in

time before the LNG-market tightens.

Egypt gas production and consumption[Bcm]

22

0

10

20

30

40

50

60

70

80

2005 2007 2009 2011 2013 2015 2017 2019 2021

Production

Consumption

Net export

Net export?

* Assuming 5% annual gas consumption growth based on IEA forecast June 2016

Source: Rystad Energy UCube; BP Statistical Review; EIA, IEA

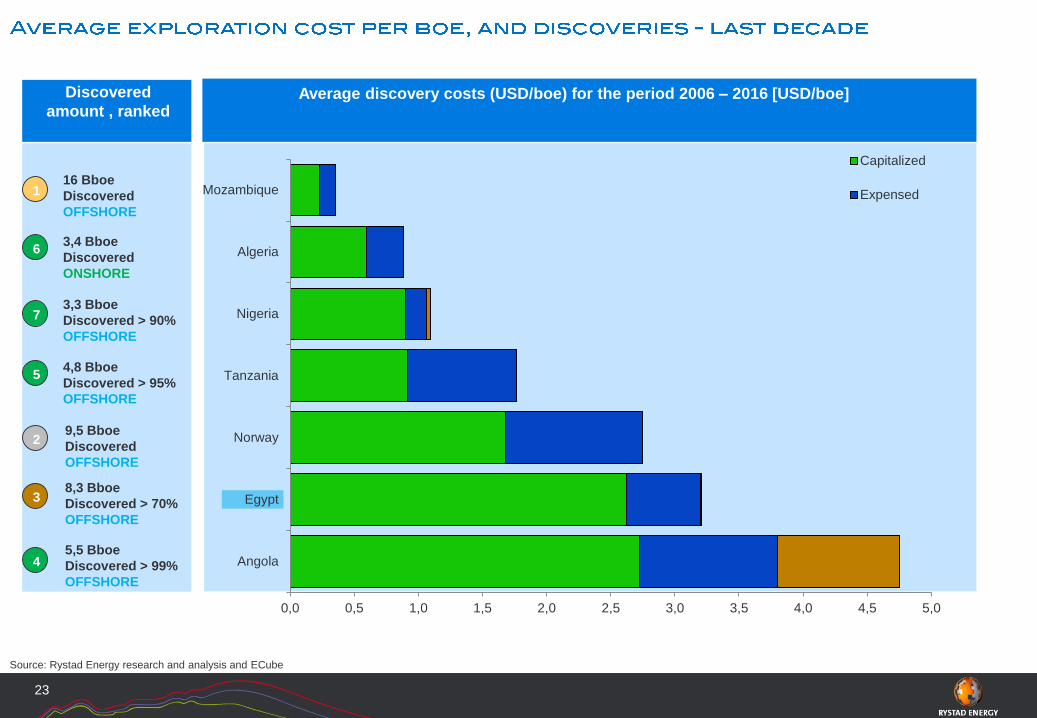

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0

Mozambique

Algeria

Nigeria

Tanzania

Norway

Egypt

Angola

Capitalized

Expensed

Source: Rystad Energy research and analysis and ECube

23

Average discovery costs (USD/boe) for the period 2006 – 2016 [USD/boe]

3,3 Bboe

Discovered > 90%

OFFSHORE

4,8 Bboe

Discovered > 95%

OFFSHORE

3,4 Bboe

Discovered

ONSHORE

8,3 Bboe

Discovered > 70%

OFFSHORE

16 Bboe

Discovered

OFFSHORE

9,5 Bboe

Discovered

OFFSHORE

5,5 Bboe

Discovered > 99%

OFFSHORE

1

6

7

5

2

3

4

Discovered

amount , ranked

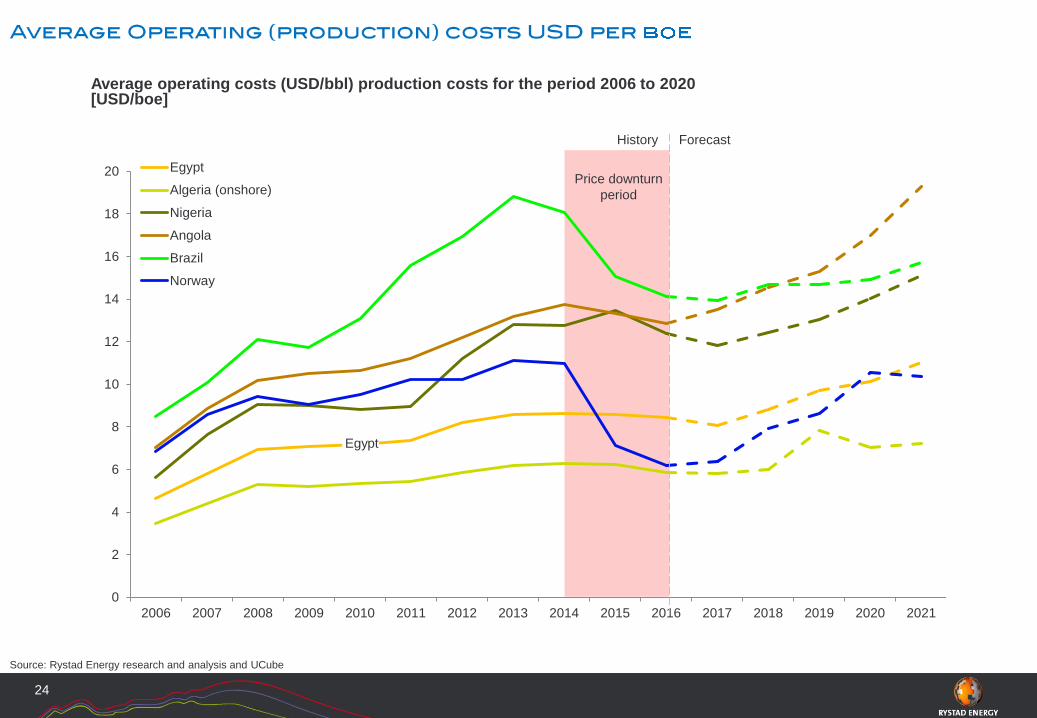

ForecastHistory

0

2

4

6

8

10

12

14

16

18

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Egypt

Algeria (onshore)

Nigeria

Angola

Brazil

Norway

Source: Rystad Energy research and analysis and UCube

24

Average operating costs (USD/bbl) production costs for the period 2006 to 2020[USD/boe]

Egypt

Price downturn

period

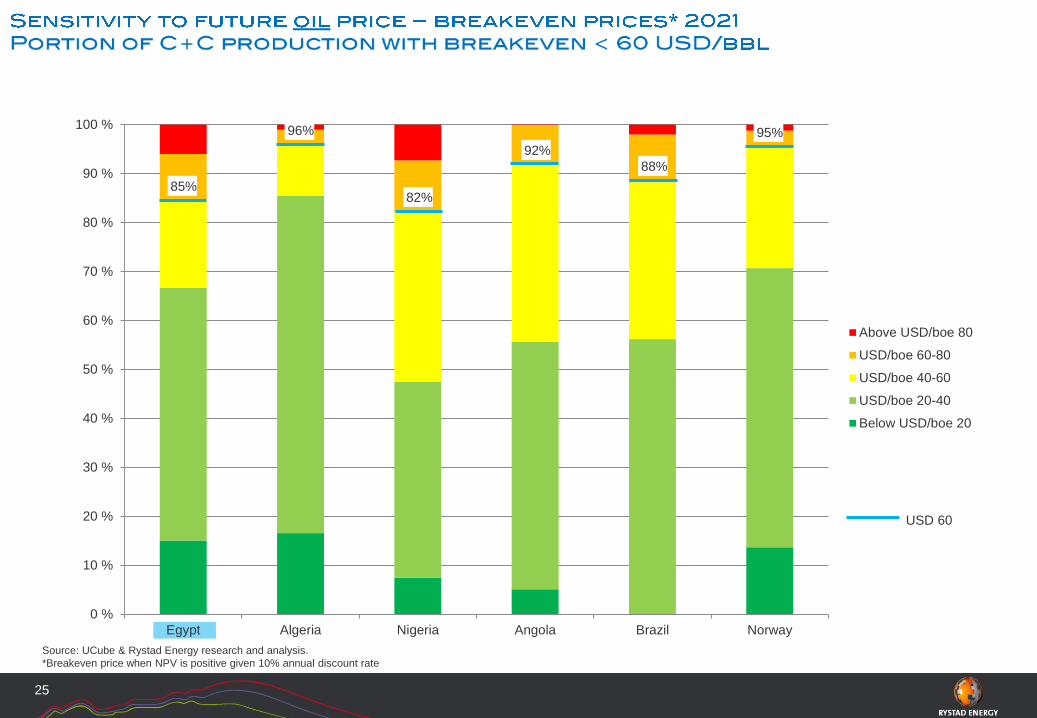

25

USD 60

Source: UCube & Rystad Energy research and analysis.

*Breakeven price when NPV is positive given 10% annual discount rate

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

Egypt Algeria Nigeria Angola Brazil Norway

Above USD/boe 80

USD/boe 60-80

USD/boe 40-60

USD/boe 20-40

Below USD/boe 20

92%

95%

85%

96%

82%

88%

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

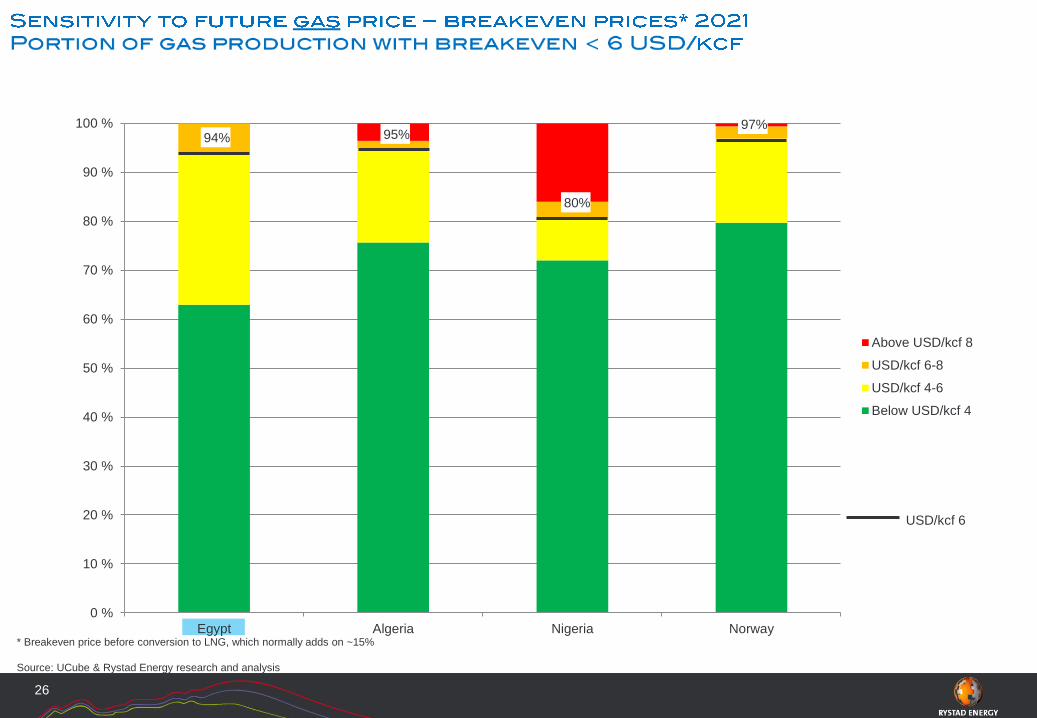

Egypt Algeria Nigeria Norway

Above USD/kcf 8

USD/kcf 6-8

USD/kcf 4-6

Below USD/kcf 4

80%

26

USD/kcf 6

* Breakeven price before conversion to LNG, which normally adds on ~15%

Source: UCube & Rystad Energy research and analysis

94% 95%97%

0 50 100 150 200 250 300 350 400 450 500

Algeria

Nigeria

Angola

Egypt

Mozambique

Tanzania

Free Cash Flow

Government Profit Oil

Royalty effects

Income Tax

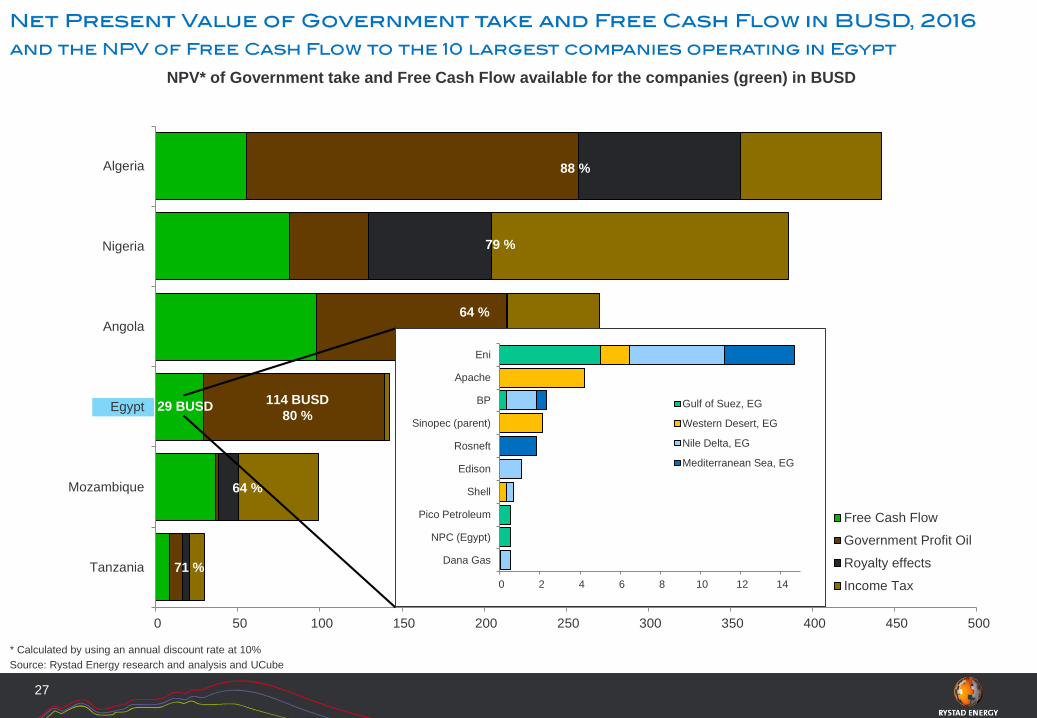

Source: Rystad Energy research and analysis and UCube

27

NPV* of Government take and Free Cash Flow available for the companies (green) in BUSD

114 BUSD

80 %

88 %

71 %

6 BUSD

36 %

2 BUSD

15 %

79 %

64 %

64 %

29 BUSD

* Calculated by using an annual discount rate at 10%

0 2 4 6 8 10 12 14

Eni

Apache

BP

Sinopec (parent)

Rosneft

Edison

Shell

Pico Petroleum

NPC (Egypt)

Dana Gas

Gulf of Suez, EG

Western Desert, EG

Nile Delta, EG

Mediterranean Sea, EG

28

Keep a long term E&P mindset, which encompasses a balance between exploration, development and

production. Egypt has produced about 40% of its potential only.

Encourage exploration by opening new acreage, offer regular licensing rounds and maybe also consider tax

revisions in order to arrest falling production from the mid 20’ies.

Scrutinize cost improvements through out the entire development chain (exploration to production), even

though break even prices for most projects seem quite robust to low prices.

Don’t flare unsellable gas – re-inject it to maintain reservoir pressure, which increases recovery and lowers

emissions.

Continue the process on removing consumer subsidies.

Tax level maybe in the high end, even though the national participation is low. This may prevent industrial

investments and E&P development .

![M12 Power - Farnell · Number of positions 4 (3 + PE) 4 5 (4 + PE) 5 (4 + PE) AWG [mm2] 0,5 – 1,5 0,5 – 1,5 0,75 – 2,5 0,75 – 2,5 AWG 20 – 16 AWG 20 – 16 AWG 18 – 14](https://img.pdfslide.us/doc/110x75/5f0685397e708231d4186643/m12-power-number-of-positions-4-3-pe-4-5-4-pe-5-4-pe-awg-mm2-05.jpg)