Embed Size (px)

Citation preview

The Future of Stress Testing: An Integrated

Framework Aligned to Risk Appetite April, 2016

DRAFT

2

Table of Contents

1. Executive Summary

2. Evolution of Enterprise Stress Testing (ST)

3. An Integrated ST Framework Aligned to Enterprise Risk Appetite

5. Key Components of an Integrated Approach

9. Appendix

Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

7. Building Blocks of an Integrated ST Approach

4. Key Differences of Stressed Capital versus Economic Capital (EC)

6. Cross-functional Collaboration across C Suite

8. Conclusion

Executive Summary

3

While most financial institutions have invested heavily in enhancing risk models, processes, data, technology and human

capital associated with CCAR frameworks, integration of CCAR flows and results into enterprise risk appetite, capital and

performance management strategies is in nascent stages

Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

DRAFT

Many institutions are still in the early to mid stages of leveraging ST analysis and results for risk appetite alignment, capital

and performance management as evidenced by limited alignment of performance metrics, loosely integrated monitoring and

reporting frameworks

Shadow CCAR results/metrics are tracked but not integrated into risk appetite frameworks and capital management and

reporting

While there is an aspiration to link ST processes with internal business and performance management processes (pricing,

reserving, etc.) most institutions have made limited progress as the primary focus was on regulatory compliance. However, this

trend is likely to pick up significant momentum going forward as the industry focuses on efficiency gains and RoI considerations

Aligned decisions, common set of KPIs and integrated monitoring, analytics and reporting need to be the common

denominator for convergence of CEO/CFO/CRO Offices in shaping risk profile and financial performance of the institution as

expected by regulators

While linking EW risk appetite metrics to business strategies and risk limits can be as much art as science, we expect

banks to further ramp up use of ST results for managing risk appetite and capital/performance management going forward

Enhancement to

Models, Data,

Process and

Technology

Rush for

Compliance

Level of Enterprise

Integration

Compliance +

Risk Management

Integrated into

Business-As-Usual

Evolution of Stress Testing

“2009-2012”

Refinement of end-to-end

CCAR processes, models and

data flows

Limited use in risk

management activities such as

reserves, pricing but

disengaged from Economic

Capital and Risk Appetite

Elevated regulatory and

stakeholder expectation for

application in capital and

business planning

Supervisors shift focus to “Use

Test”, soundness of

processes, data,

documentation

Integrated risk and

capital

management

Reactive to comply with

CCAR requirements

Heavy investments in

infrastructure, data,

reporting and resources

Focused on capital

adequacy, with almost

no use for risk and

business decisions

Supervisors are focused

on meeting basic

requirements

1

2

3

Evolution of Enterprise Stress Testing – What lies ahead?

DRAFT

“2012-2015” “2016-2020”

ST scenarios and results are

integrated into key EW level

risk and performance

metrics

Integrated analytics and

reporting to embed ST

results into BAU applications

across all LoBs and

enterprise functions

Used as an anchor for

strategic planning and risk

appetite management

aligned with economic

capital processes

Supervisors take a more

holistic view of the CCAR

frameworks and leverage

integrated frameworks for

managing the risk and

trajectory of the system

Regulatory

Compliance driven

Low

Medium

High

“ Inception”

“ Current State”

“ Target State”

5

DRAFT

An Integrated Stress Testing framework should link the bank’s capital needs to its

strategic plan and risk appetite targets

Integration of LoB and EW scenario-driven

outcomes into risk strategies via measuring

impact on risk appetite metrics

Assess business-specific and firm-wide

resilience to regulatory and idiosyncratic stress

scenarios as well as extreme market and liquidity

events

Refinement/calibration of risk appetite targets

and tolerances based on key stress scenarios

Measure and monitor key risk indicators (e.g.,

limits, capital use) and performance through

integrated CCAR/Risk Appetite metrics,

analytics and monitoring capabilities

Fine-tune risk strategy, capital management and

performance decisions via dynamic impact

assessment of CCAR and Economic Capital

(EC) results

Optimization of risk-adjusted performance

within risk tolerances through

Forward-looking capital planning (regulatory

and economic capital)

Balance sheet optimization

Key Characteristics

Capital Management

Available

Capital

Regulatory

Capital

Economic

Capital Capital

Optimization

Enterprise Stress Scenarios

Performance Management

Strategy Investments Optimization Divesture/Exit

Regulatory Idiosyncratic Portfolio Market Liquidity

LOB Stress Test Scenarios

Regulatory Idiosyncratic Product Geography Operational

Bank Strategy Risk Strategy & Appetite

CCAR Framework

Board and Senior Management Oversight

Governance

Data & Technology

Integrated Stress Testing Framework

DRAFT

6

DRAFT

Despite earlier divergence, CCAR and Economic Capital can make a powerful

combination for integrated risk and capital management going forward

DRAFT

P

R

O

C

E

S

S

E

S

A

C

T

I

V

I

T

I

E

S

CCAR Reports filed

(Capital Plan,

FRY – 14 A/Q)

CCAR Model

Management

Risk Identification /

Scenario

Development

Projections /

Estimations (Model

Execution)

Capital Planning &

Adequacy

Regulatory

Reporting

Models

Implemented

and Validated

Stressed Risk

Factors

Capital

Decisions

Financial &

Capital Projections

over 9-Quarter

Horizon

Model Definition &

Implementation

Back Testing &

Validation

Model Approval and

Recertification

Model Inventory

Management

Scenario Definition

Scenario Library

Creation

FRB Scenarios

Projections (B/S,

PPNR)

Available Capital

Projection

Regulatory Capital

Projection

Assess Capital

Adequacy

Determine Capital

Actions

Develop Capital Plan

Report Submission

Report Certification

Risk Identification &

Material Risk Inventory

Projections (Losses)

Projections (RWA)

CCAR Lifecycle

CCAR Processes

CCAR framework requirements are focused around provision and consolidation

of end-to-end data, methodology and forecasting components from all

LOBs and relevant functional units across the enterprise

A minimum of 45 iterations of B/S, I/S and capital adequacy calculations (5

scenarios x 9 forecasted quarters) is needed

Risks identified and scenarios designed need to be pertinent to the size and

complexity of the institution with a typical inventory of 50-100 Risks

Requires comprehensive data management framework with accounting-

quality transaction data and understanding of data anomalies

CCAR Only Activities EC Overlapping Activities

Economic Capital Processes

Under the CCAR framework, Portfolio, LoB and Enterprise level

balances/CFs are forecasted based on the business/risk strategy of the

institution under stress conditions whereas EC excludes such forecasts

Economic capital takes place under a more Centralized operating model as

the methodology and forecasting requirements do not require the active

involvement of different constituents across the enterprise

In contrast, Economic capital results do not provide insights into the

consequences of specific stress scenarios/events

A hybrid of Point-in-time and Through-the-cycle risk parameters is used to

compute economic capital, which is calculated over one-year, invariably

causing dilution in results

Ke

y D

iffe

re

nc

es

7

DRAFT

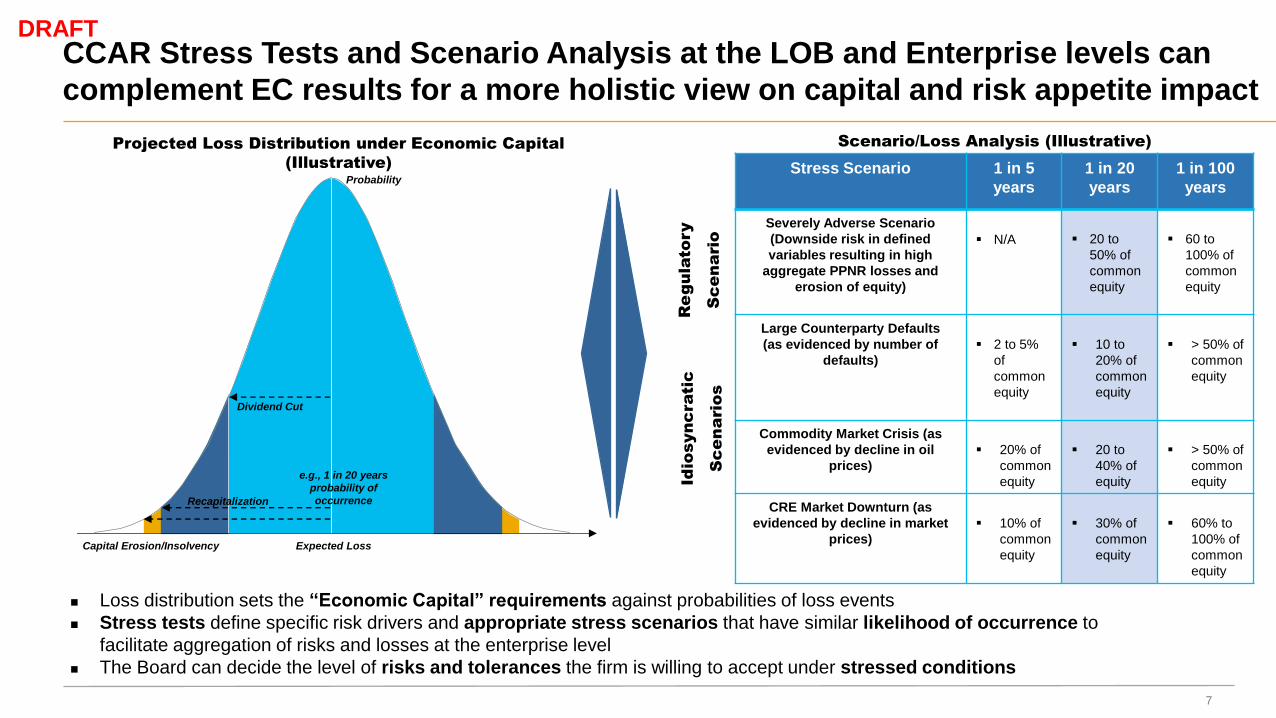

CCAR Stress Tests and Scenario Analysis at the LOB and Enterprise levels can

complement EC results for a more holistic view on capital and risk appetite impact

Stress Scenario 1 in 5

years

1 in 20

years

1 in 100

years

Severely Adverse Scenario

(Downside risk in defined

variables resulting in high

aggregate PPNR losses and

erosion of equity)

N/A

20 to

50% of

common

equity

60 to

100% of

common

equity

Large Counterparty Defaults

(as evidenced by number of

defaults)

2 to 5%

of

common

equity

10 to

20% of

common

equity

> 50% of

common

equity

Commodity Market Crisis (as

evidenced by decline in oil

prices)

20% of

common

equity

20 to

40% of

equity

> 50% of

common

equity

CRE Market Downturn (as

evidenced by decline in market

prices)

10% of

common

equity

30% of

common

equity

60% to

100% of

common

equity

Re

gu

lato

ry

Sc

en

ario

Id

io

syn

cratic

Sc

en

ario

s

Scenario/Loss Analysis (Illustrative)

Expected Loss

Projected Loss Distribution under Economic Capital

(Illustrative)

Dividend Cut

Recapitalization

Capital Erosion/Insolvency

Loss distribution sets the “Economic Capital” requirements against probabilities of loss events

Stress tests define specific risk drivers and appropriate stress scenarios that have similar likelihood of occurrence to

facilitate aggregation of risks and losses at the enterprise level

The Board can decide the level of risks and tolerances the firm is willing to accept under stressed conditions

Probability

e.g., 1 in 20 years

probability of

occurrence

DRAFT

0

2

4

6

8

10

12

14

16

Book ca

pita

l

Provision

s

Provision

s

Provision

s

Rev

alua

tions

Rev

alua

tions

Rea

l estate

risk

Risk in

Parti

cipa

tions

ALM ri

sk

Trading

risk

Cre

dit r

isk

Ope

ratio

nal r

isk

Busin

ess

risk EL

Exces

s ca

pita

l

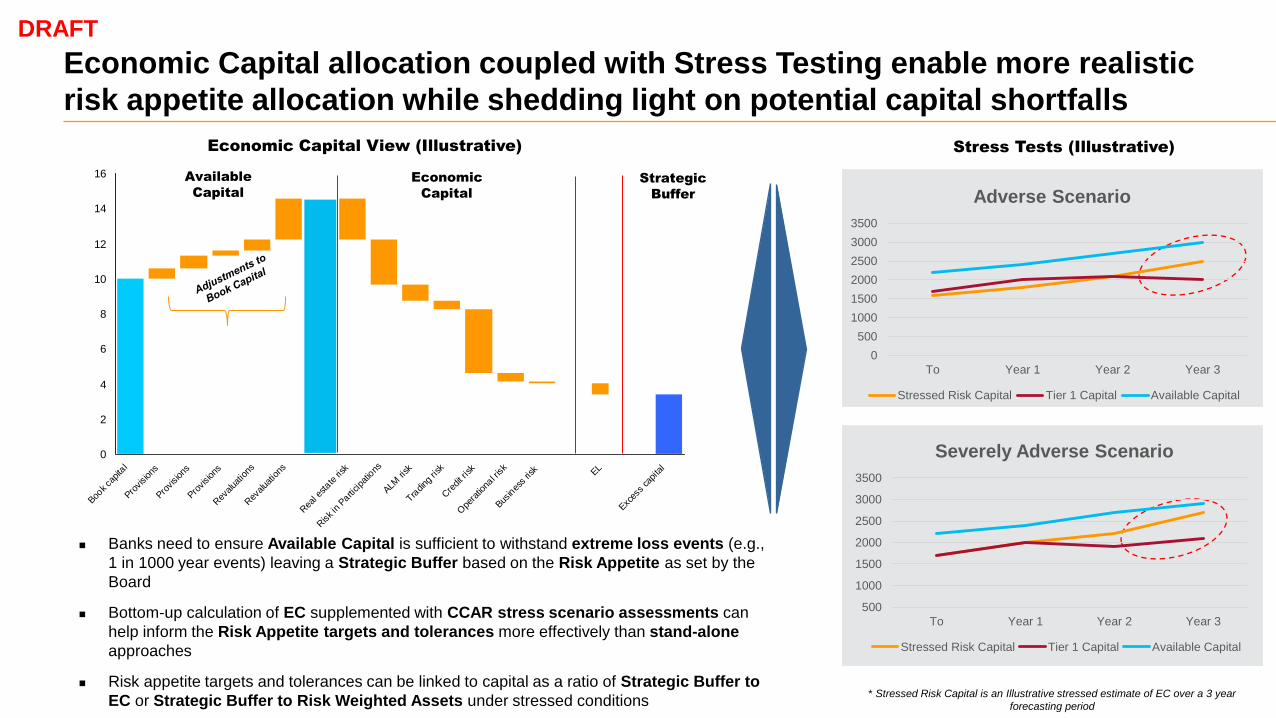

Banks need to ensure Available Capital is sufficient to withstand extreme loss events (e.g.,

1 in 1000 year events) leaving a Strategic Buffer based on the Risk Appetite as set by the

Board

Bottom-up calculation of EC supplemented with CCAR stress scenario assessments can

help inform the Risk Appetite targets and tolerances more effectively than stand-alone

approaches

Risk appetite targets and tolerances can be linked to capital as a ratio of Strategic Buffer to

EC or Strategic Buffer to Risk Weighted Assets under stressed conditions

Economic Capital allocation coupled with Stress Testing enable more realistic

risk appetite allocation while shedding light on potential capital shortfalls

Economic Capital View (Illustrative)

DRAFT

Stress Tests (Illustrative)

0

500

1000

1500

2000

2500

3000

3500

To Year 1 Year 2 Year 3

Adverse Scenario

Stressed Risk Capital Tier 1 Capital Available Capital

500

1000

1500

2000

2500

3000

3500

To Year 1 Year 2 Year 3

Severely Adverse Scenario

Stressed Risk Capital Tier 1 Capital Available Capital

Available

Capital

Economic

Capital

Strategic

Buffer

* Stressed Risk Capital is an Illustrative stressed estimate of EC over a 3 year

forecasting period

Leading institutions are increasingly focusing on integrated frameworks for

linking risk appetite allocation and capital management more dynamically…

Solvency risk appetite (defines capital requirements)

Regulatory capital

Economic capital

CCAR Stressed Capital

Available capital level and composition becomes the

defining factor (e.g., Tier 1 Capital/EC, Tier 1 Capital/RWA,

CET1 Capital/RWA, Leverage ratio under stress scenarios)

Concentration risk appetite

Exposures to sectors, counterparties, geographies

Profits in particular sectors, regions

Volatility risk appetite

Earnings

Economic profit/RAROC/RoE

Dividends

Provisions

Qualitative statements on non-financial risks will indicate

tolerance levels (e.g., policy breaches, # of risk incidents)

Risk Appetite defines at the top of the enterprise how much

risk an institution is willing to take while balancing the

interests of various stakeholders:

Creditors and regulators who are concerned with extreme

downside events

Shareholders who are concerned with events like

earnings/share price volatility

Reconciling between top-down risk appetite targets and bottom-

up limits have historically been a key challenge

However, more institutions are enhancing their data integration

and analytics capabilities to monitor and manage the impact of

granular limits (BU/portfolio level) on enterprise level risk

appetite

The integrated nature of CCAR/Stress testing processes

and data flows is likely to ease such reconciliation going

forward

DRAFT

Risk Appetite Considerations Typical Risk Appetite Measures/Capital Metrics

. 10 Confidential. Copyright © 2015 Accenture All rights reserved.

…Key components of an “Integrated Framework” include continuous

alignment and re-balancing of balance sheet, risk and capital decisions

Strategic Planning/Risk Appetite

Growth strategies and corporate risk

appetite that will impact the availability and

deployment of capital

Business plans linked to capital strategies

including capital allocation, risk adjusted

performance and incentives

Dynamic monitoring and re-calibration

of risk appetite targets and thresholds

Balance Sheet Management

Optimization of capital structure (equity and

debt instruments)

Determining “Strategic Buffer” capital levels

accounting for cyclicality

Liquidity stress testing and contingency

plans

Capital Management

Optimizing sources vs. uses of funds and

capital targets formulation

Refinement of capital distribution plans

(dividends, repurchases)

Capital contingency plans, KRIs and

triggers

Risk Management

Identification and assessment of all material

risks

Risk Management policies and procedures

linked to capital adequacy levels (e.g.,

limits)

Stress scenarios that will impact capital

access and funding requirements

DRAFT

11 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

This “Integrated Framework” will require extensive cross-functional collaboration

across the C-suite centered around common KPIs

Capital

Management

(CFO Office)

Strategy (CEO Office)

Risk

Management

(CRO Office)

Aligned decision processes and shared KPIs

Integrated metrics, analytics and reporting

framework Risk appetite allocation granularity and dynamic

re-calibration capabilities

Organizational alignment

Strategic Planning

Market/Customer/Product/Channel Strategies

Risk Appetite & Risk Strategy

Investment Plan

Business Execution

DRAFT

Capital raising

Capital forecasts

Performance

measurement

Capital

optimization

“Capital Plan”

Holistic risk identification

Risk measurements

Model risk management

Key Enablers

Limit setting/monitoring

Economic Capital

Provisioning

CCAR & EC

reconciliation Contingency

planning

Capital adequacy

Convergence across the three Offices

spurred by an unprecented regulatory

and market urgency to align strategy,

capital and risk objectives

CRO Office has become the “Trusted

Business Partner” with a much higher

visibility in shaping the strategic

direction and risk appetite of the

institution

Historically, each C-level Office had a

different stance on optimal trade-

offs among strategy, capital and risk

Common set of KPIs that facilitate

unified objectives is key and should be

based on risk appetite measures

Portfolio analytics

Building Blocks of an Integrated Stress Testing Approach

12

Specific milestones and capabilities need to be established to successfully embed CCAR scenarios and results into the

risk appetite framework and capital management processes

Establish clear Board commitment and responsibility for reviewing and approving risk appetite metrics and tolerances stemming

from ST scenarios and results. Assign SME resources/know-how where required

Assess current Risk Appetite framework to ensure complete set of KPIs and tolerances for all material risk categories exist at the

EW and LoB level, refine as necessary

Ascertain that key data/MIS required for defined KPIs (risk appetite metrics) is automated and accessible as needed

Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

DRAFT

Foundation Setting &

Design

Develop an inventory of all key ST scenarios (regulatory and idiosyncratic) that will be linked to key risk appetite metrics and

tolerances

Develop measurement capabilities to quantify the impact of all ST stress scenarios/events on key risk appetite metrics

Scenario Integration

Review measured impact of ST scenarios/results and EC results on key risk appetite metrics and enterprise risk profile. Evaluate

whether it lies within tolerances

Identify and monitor any risk areas where potential deviation might occur from tolerances and desired risk profile. Recalibrate top-

down tolerance to align with bottom-up risk profile (if required)

Measurement &

Calibration

Develop integrated monitoring and reporting capabilities showing impact on risk limits, capital, liquidity and risk-adjusted

performance

Identify and track early warning indicators tied to specific remediation plans

Develop aggregate and LoB-specific dashboarding with specific drill-down capabilities

Review & Monitoring

Capital Management

Refine active balance sheet and capital management competencies from human capital to processes, methodologies and tools

Link data integration, analytics and portfolio management processes to the capital management function and operationalize dynamic

capital actions

Conclusion

13

While the financial services industry’s heavy focus on CCAR framework requirements in the post-crisis era seems to overshadow the

economic capital management practices and past achievements, institutions can benefit from the increased convergence in these two

areas

Scenario-driven forecasts of CCAR stressed capital can complement the scenario-agnostic EC estimates in shaping the true risk

appetite of the institution in the eyes of the regulators, creditors and shareholders

Reconciliation between EC allocations, CCAR results and Risk Appetite targets can be the catalyst in an integrated risk and capital

management framework going forward

From an organizational perspective, EC teams with Risk can serve as the final consolidation point in the CCAR lifecycle providing

review and oversight of CCAR results while highlighting and bridging the differences with EC allocation and results

CEO/CFO/CRO Offices should make a concentrated effort to institute integrated frameworks accounting for the strengths and limitations

of stand-alone capital planning approaches and leverage the cumulative benefit of the heavy CCAR investments made over the years

Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

DRAFT

Appendix

DRAFT

14 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

15

DRAFT

Despite earlier divergence, CCAR and Economic Capital can make a powerful

combination for integrated risk and capital management going forward

Economic Capital CCAR Stressed Capital Key Differences

Description Total capital required to safeguard the enterprise against

economic insolvency based on economic risks

undertaken over the specified time period

Total capital required to safeguard the enterprise against

regulatory insolvency under a set of stress scenarios over

the specified forecasting period

Economic capital is designed to reflect real economic risks facing the firm in terms of unexpected movements in the value of assets and liabilities and on the confidence level selected by management

CCAR stressed capital forecasts are based on defined stress conditions designed

to result in a more comprehensive assessment of capital under such conditions,

which trigger regulatory action when thresholds are breached

Under the CCAR framework, Portfolio, LoB and Enterprise level balances/CFs are

forecasted based on the risk strategy of the institution under stress conditions

whereas EC excludes such forecasts

Operating

Model

Oversight, modelling and management of economic

capital allocation is typically centralized at the

Enterprise level within Risk or EW level Risk Analytics

LOBs, Risk, Finance, Treasury serve as input providers

for parameterization and modelling purposes

Oversight and modelling of CCAR Stressed Capital

displays a more hybrid operating model with individual

LOBs developing models but aggregated results are

managed and communicated jointly by CFO and CRO

Offices

LOBs, Risk, Finance and Treasury have responsibilities

around modelling and forecasting of specific CCAR

components (e.g., balances, expenses, losses)

Economic capital attribution takes place under a more Centralized operating model as

the methodology and forecasting requirements do not require the active involvement

of different constituents across the enterprise

In contrast, CCAR framework requirements are focused around provision and

consolidation of end-to-end data, methodology and forecasting components from all

LOBs and relevant functional units across the enterprise

While institutions target more centralization of CCAR frameworks, most institutions

are in the early to mid stages of that process

Risks and

Methodology

Economic capital results reveal the economic risks of the

institution

Typically encompasses credit, market and operational

risk categories with sub-risks included in respective

categories (e.g., CP risk in credit risk, ALM risk in market

risk)

Mostly top-down capital allocation based on BU/portfolio-

level estimates (e.g., PD, LGD and EAD and portfolio-

level default correlations in the case od credit risk; factor

sensitivities and correlations in the case of market risk; or

parameters of frequency/severity distributions and

dependency structure in the case of operational risk

More granular allocations require simulation-based

approaches with borrower, factor or loss type -level

correlations mainly applied to selective

portfolios/transactions (e.g., Large corporates in credit,

equities in market)

Calculated over a one-year time period

Capital impact of specific stress scenarios/events is modeled by stressing the balance sheet volumes and key risk parameters

Most CCAR banks developed/refined specific modeling

approaches to forecast CCAR capital or adapted existing

approaches (e.g., conditioned am IRB credit risk

parameter model on macroeconomic variables)

Forecasting of risk-weights under the Basel III Regulatory

Framework though there are differences in RWA

calculation methods across institutions

Portfolio/LOB balances, revenues, losses and RWAs are

modeled via numerous PPNR and risk models across the

forecasting horizon by LOBs and aggregated across the

enterprise

Capital adequacy based on regulatory minimum

thresholds for CET1, Tier 1 and Total Regulatory Capital

levels relative to RWAs

Calculated over a nine-quarter forecasting time period

Economic Capital: Economic capital results do not provide insights into the consequences of specific

stress scenarios/events “Tail” risks are still difficult to model due to limited data around extreme stress

events; however, additional data accumulated during the recent crisis can shed some

light in ongoing modelling efforts

Requires use of a capital multiplier based on selected confidence level for

calculation

Most institutions use a hybrid of Point-in-time and Through-the-cycle risk

parameters to compute economic capital, which is calculated over one-year,

invariably causing dilution in results

CCAR Stressed Capital:

CCAR methodologies require a longer horizon with nine-quarter forecasting of cash

flows and risk drivers

The CCAR capital framework is designed to estimate financial and capital impact

(revenues, losses, RWAs) of specific regulatory and idiosyncratic scenarios with

respect to each financial institution

Enterprise

Applications

Regulatory communication of risk profile Capital planning/management

Transaction structuring, pricing and limit setting

Portfolio optimization and risk-adjusted performance

decisions

Regulatory compliance

Scenario analysis

Reserving

Economic capital planning and use for risk management is more established across

the industry. Allocation granularity and risk and capital management applications

vary significantly across institutions

CCAR capital planning mainly focuses on meeting regulatory requirements with

limited use in other enterprise areas

Elevated expectations for CCAR integration into BAU decisions create new

opportunities for reconciliation with Economic Capital processes

Ove

rvie

w o

f C

CA

R S

tre

sse

d C

ap

ita

l

vs. E

co

no

mic

C

ap

ita

l

DRAFT

High-level Implementation Plan

16 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

DRAFT

Pilot Design Embed in EW Review & Refine

Define integrated framework,

key metrics and tolerances for

ST scenarios/events

Assess current EC and RAF

for any gaps in methodology,

process, data and reporting

and identify remediation plan

Establish roles and

responsibilities for review and

sign-off on key metrics and

tolerances, as well as

escalation procedures

Select a particular

portfolio/LoB for pilot

implementation prior to EW

roll out

Identify specific stress

scenarios and risk appetite

metrics within the context of

selected portfolio/LoB

Select and execute a series

of scenarios (historical,

regulatory, idiosyncratic) to

estimate portfolio impact and

impact on key BU metrics

(risk, capital, RAROC, etc.)

Aggregate portfolio/impact to

top-down enterprise risk

appetite metrics and identify

range in tolerances

Analyze results and identify

areas of improvement with key

stakeholders

Refine and prepare for EW

level launch

Assess firm-wide

organization, processes,

measurement, monitoring

and reporting capabilities

Refine governance model

and escalation criteria

based on key ST scenarios

Embed risk appetite and

tolerances tied to key ST

scenarios in EW level risk

appetite statements and

policies

Cascade EW level risk

appetite metrics into

LoB/portfolio limits and

controls

Upgrade reporting capabilities

with integrated ST/RA metrics

with traffic light risk triggers

and action tracking

Institute BAU process and

operationalize

Dynamic review of existing risk

profile versus target profile

Periodic Board and SM review

and sign-off of key ST events

on enterprise risk profile

Recalibrate if required

Credential: Integrated Planning & CCAR for Large US Bank

DRAFT

17 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

The Credit Card Services business unit reached out to Accenture to assess their

planning capability against best practices and industry peers. Card leadership

hypothesized that the current 7+ week forecasting cycle was excessive, and

requested assistance to identify areas for improvement. Bank recently had also

received MRAs related to CCAR submission to address excessive management

judgment in forecast models, weakness in data integration and a lack of governance

and controls in future submissions. Bank was looking for assistance to create a

single solution for both financial planning and CCAR regulatory reporting.

Accenture worked with Bank to conduct an assessment of the planning process and

methodology used at Credit Card Services. Through this engagement, the team

designed an integrated planning and forecasting framework, a data architecture

design and developed a roadmap to improve the planning capability through a

series of initiatives.

• Evaluated current planning capability against peers and leading practices

• Recommended a target state vision that addresses the current challenges in the

planning process by creating an integrated performance management framework

and capability rigorously focused on the drivers of shareholder value and

regulatory compliance

• Designed operating model that integrates CCAR into standard business and

financial planning cycle

• Reduced 7+ week forecasting process to <1 week through elimination of sequential steps, and enhanced automation of baseline and scenarios

• Addressed all current MRAs in latest CCAR submission

• Standardized and integrated a repeatable forecasting process that includes audit check-points and strong governance

• Enhanced statistical models to rely on Fed supplied macro-factors rather than excessive management judgment

• Increased transparency of forecast with ability to drill back to drivers and perform root cause analysis

Business Challenge Approach

High Performance Delivered

The large US Bank is a financial holding company, and provides various financial services worldwide. Its Retail Financial Services segment offers consumer and business, and

mortgage banking products and services that include checking and savings accounts, mortgages, home equity and business loans, and investments. The company’s Card

Services and Auto segment provides payment processing and merchant acquiring services.

Client Profile

Credential: CCAR Modeling Framework, Model Dev. and Implementation for

Regional Bank

DRAFT

18 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

Accenture provided services across the following areas:

Operating Model

• Reviewed existing retail CCAR loss forecasting models for multiple lines of business and conducted ‘As-is’ assessment of current process for compliance the US

regulations

Enterprise Risk and Stress Testing Framework

• Reviewed the existing vendor model documents and model validation MRA’s for as-is state assessment

• Developed a robust CCAR loss forecasting framework and worked with vendors to ensure the best in class model development practices are integrated

• Performed stress tests on Fed recommended scenarios for vendor supported applications

• Developed and Implemented model delivery lifecycle for retail CCAR loss forecasting models across multiple vendor applications

• For bank’s Auto lending portfolio, developed forecasting models for outstanding Balance and Deposit Service Charge. Also, supported model documentation for revenue

forecasting model for Cards portfolio

Risk Analytics and Execution Platform

• Review and automate the data processes to make the execution platform efficient and consistent

• Perform UAT for Moody’s Credit Cycle, Strategic analytics and Look ahead applications to ensure the accuracy of execution platform

Developed and implemented CCAR Loss Forecasting models utilizing vendor solutions – Moody’s Credit Cycle, Strategic Analytics and LPS • Led efforts to understand and document vendor models and Banks’ CCAR/stress testing methodologies

• Managed the Bank’s CCAR modeling program by leveraging a off-shore visa enabled delivery team

• Trained and provided oversight to internal modeling team

• Highlighted by SVP of Model Validation as reason bank will meet CCAR deadlines this year.

Business Challenge and Approach

High Performance Delivered

The bank was advised by the Fed to demonstrate understanding of vendor loss forecasting models for multiple retail portfolios, as part of its Fed CCAR submissions. The effort

required significant subject matter expertise to ensure completion of multiple vendor model development, validation and stress testing efforts based on industry best practices

and approaches.

Client Profile

Credential: CCAR Model Doc. and Reporting Framework for Global Bank

DRAFT

19 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

Accenture provided services across the following areas:

Operating Model

• Accenture team of 9 resources (6 US / 3 India) delivered on the documentation of bank’s CCAR models and successfully delivered on the comprehensive package of

resubmission narratives for six of bank’s lines of businesses under tight timescales.

Enterprise Risk and Stress Testing Framework

• Delivered documentation for more than 100 CCAR models that drive loss forecasting, PPNR revenue forecasting, acquisitions, and balances. Also, supported model

validation and governance effort

• Delivered comprehensive package of CCAR Narratives (covering PPNR, Loss, Balance Sheet, RWA) for Cards, Consumer Deposit, Business Banking, Cards, Mortgages,

Students Loan & Auto

• The team is currently delivering quality documentation for – (a) Cards division on loan loss reserving (b) Business Banking division on more than 50 CCAR models (c) AML

policies and technical specifications (d) Narratives for 2014 End Year CCAR submissions

Regulatory Reporting

• Developed an End-to-end industrialized reporting process, including CCAR reporting templates and mock-ups, to streamline the communication of loan loss reserves

results to various stakeholders (e.g., regulators, external auditors and senior management)

• Developed agility and precision to support the bank in meeting tough regulatory deadline for CCAR re-submission. The Card CFO called the Accenture team as the key

success driver for 2013.

• Accenture’s documentation was declared as the “Gold Standard” benchmark for all business units to emulate

• For outstanding contributions, personalized “Appreciation Letters” were awarded by bank’s Chairman and CEO

Business Challenge and Approach

High Performance Delivered

Bank’s cards division received a series of findings on its CCAR submission that required enhancements prior to its FY 13 submittal. The redeveloped CCAR models (Pre

Provision Net Revenue (PPNR), Loss, Acquisition, OS migration, CCAR Integration) needed to be documented and CCAR packages to be delivered to Fed under tight

timescale

Client Profile

Credential: Stress Testing and Risk Reporting Analytics Outsourcing for a

Global Investment Bank

DRAFT

20 Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information

The client wanted to maintain and enhance the Credit Risk System functionality and flexibility, speeding up time to implement changing regulatory requirements specified

under Basel II and III accord.

Accenture provided Business Intelligence solutions using SAS, Oracle, Unix and Java to support the client’s Credit Risk reporting system. In doing so, Accenture were able

to

• Develop system changes based on Basel II and III regulatory requirements. (Change-The-Bank)

• Enable Financial Stress Testing by developing and maintaining a robust platform and performing the daily Operations. (STE)

• Perform Release-based Assembly Testing. (CI/INT Testing)

• Perform deployment, assist in release management and provide 3rd level production support . (Run-The-Bank)

Business Challenge and Approach

High Performance Delivered

A leading global investment bank operating in over 70 countries with presence in major emerging markets, including the Asia-Pacific, Central and Eastern Europe and Latin

America

Client Profile

Implemented Credit Risk System enhancements with high service quality • Developed a Stress Testing platform that evolved to be a corner stone of the client’s financial adverse scenario simulations. This has enabled bank to do 400+

adverse scenario simulations per year.

• Testing Team pioneered usage of the ALM Tool for Test Management and Defect tracking. Testing effectiveness at 100% ensuring zero defect leakage to UAT.

• Our Dev and 3rd Level Support to the client’s Basel III initiatives enables the bank to go live with Basel III as the leading system on schedule.

• 100% Manila ownership of Deployment in all INT, UAT and PROD environments ensuring timely credit risk reporting based on accurate release-based changes.

Credential: European FBO –

Dodd-Frank Section 165 Business and Technology Architecture Definition

DRAFT

21

Enhanced Prudential Standards (EPS), highlighted by Dodd–Frank Section 165

demands Foreign Banking Organizations to establish an Intermediate Holding

Company (IHC) by July 1, 2016. The regulations place varying demands for change

in banking processes, including improved capital planning, liquidity monitoring, and

risk management

• Being an IHC also demands alignment of process technology and data across

legal entities within the United States

• Our client was accountable for safe delivery of the technology and data

architecture for the IHC

• Limited availability of business SMEs given competing demands for input to the

CCAR process

• Continued business model and regulator commitment coordination with parent

resulted in contradictory imperatives

• Introduce subject matter experts to drive requirements gathering, with business

stakeholders at discovery workshops

• Develop end-to-end architecture for the bank’s response to the IHC

requirements, including:

o Functional architecture

o Application architecture

o Data architecture

o Data sourcing strategy (including interface, application, and infrastructure

inventories)

• Identify key transition states for the end-to-end architectures

• Define an implementation plan for day 1 IHC and through 2017, including

required investment and resource needs

• Mobilization of the governance to oversee implementation of the delivery plan

• Certainty around the technology and data architecture required for delivery of the IHC

• Integration with bank-wide planning for the IHC, including an understanding of key inter-dependencies

• Business awareness of the operational reality of being an IHC and the preparation required

• Ability to communicate the journey to becoming an IHC for key internal and external stakeholders

Business Challenge Approach

High Performance Delivered

Leading European financial services institution

Client Profile

Copyright © 2015 Accenture. All right reserved. Accenture Confidential Information