Embed Size (px)

Citation preview

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Athens, 9th November 2017

The Future of Credit Risk and What it Means for Greece

2McKinsey & Company

What trends are shaping the future of credit risk?

What are the implications for banks and businesses?

What does it all mean for Greece?

3 questions to address today

3McKinsey & Company

3 macro trends transforming the financial sector and credit risk

▪ Fintechs maturing from product focus (e.g., payments) to

broader focus (e.g., API, Blockchain, non-bank lenders), from

B2C to B2B, from startups to larger platforms

▪ Cheap computational power, enhanced big data storage and

management, and advanced analytics toolkit

Increasing

competition

from fintechs

Expanding

breadth and

depth of

regulation

▪ Complex and ever expanding set of regulatory constraints

governs bank business models (e.g., liquidity, leverage)

▪ Unbundling of services, price transparency and “fairness”

▪ Stricter regulatory requirements for traditional financial

players

▪ Evolving customer behaviors and needs creating pressure for

banks to adapt in terms of services and speed

▪ Around-the-clock availability of customized services and

products

▪ Seamless access from different channels

▪ Almost real-time decisions

Dramatic shift in

customer

preferences

4McKinsey & Company

Startups

Increasing competition – Proliferation of players in the market NON EXHAUSTIVE

Non-traditional players Traditional players

Insurance

companies

Banks

Infra-

structure

suppliers

Other

industries

Telecom

e-commerce

and retail

Technology

5McKinsey & Company

Increasing competition – Fintechs have several markers of success, which

financial institutions can learn from

1 Co-operative competition

▪ Erosion of physical distribution makes cost a distinctive marker for

disruptive attackers, e.g., Fintech lenders have up to 400 bps cost

advantage over banks

Achieving step

reduction in the cost

to serve

▪ Fintech attackers find innovative ways to attract customers, e.g.

alternative payments POS attacker Poynt is increasing its scale via

partnerships and distribution agreements

Applying advantaged

modes of customer

acquisition

▪ Big Data and advanced analytics allow Fintechs to experiment with new

credit scoring approaches and to understand customer needs or “next

best actions”, e.g., by leveraging social media data

Using big data in

innovative ways

▪ Successful Fintech attackers cherry pick from banking products and

excel in focus segments, e.g., Wealthfront targets fee-averse Millennials

who favor automated service over human advisors

Focusing on

segment-specific

propositions

▪ Fintech attackers embrace “co-opetition”1 and find ways to engage with

existing ecosystem of banks, e.g., Lending Club’s credit supplier is Web

Bank, PayPal’s merchant acquirer is Wells Fargo

Leveraging existing

financial

infrastructure

▪ Regulation is a key swing factor in how FinTech disruption could play out

as once these attackers reach scale they will attract more regulatory

attention and the ones lacking the required capabilities could easily fail

Managing risk and

regulatory

stakeholders

6McKinsey & Company

Shift in customer preferences – Customer expectations far beyond

traditional product offering and level of service

Customers demand instant decisions, intuitive experiences on any device and customization

Banking as we know it today is

dead… Algorithms and automated

processes are the way to customer-

friendly banking.

Responding to customer needs,

Kabbage provides working capital in

under 10 minutes to small businesses

with no paperwork.

Kreditech Incumbent bank

▪ Applicant’s online accounts linked and

including unstructured data, such as:

– Online payment flows on PayPal

– Social media awareness (e.g., Twitter)

– UPS shipping volume

– Rating and volume on Amazon/eBay

▪ Fully online decision process within a few

minutes and Immediate disbursement

EXAMPLE

7McKinsey & Company

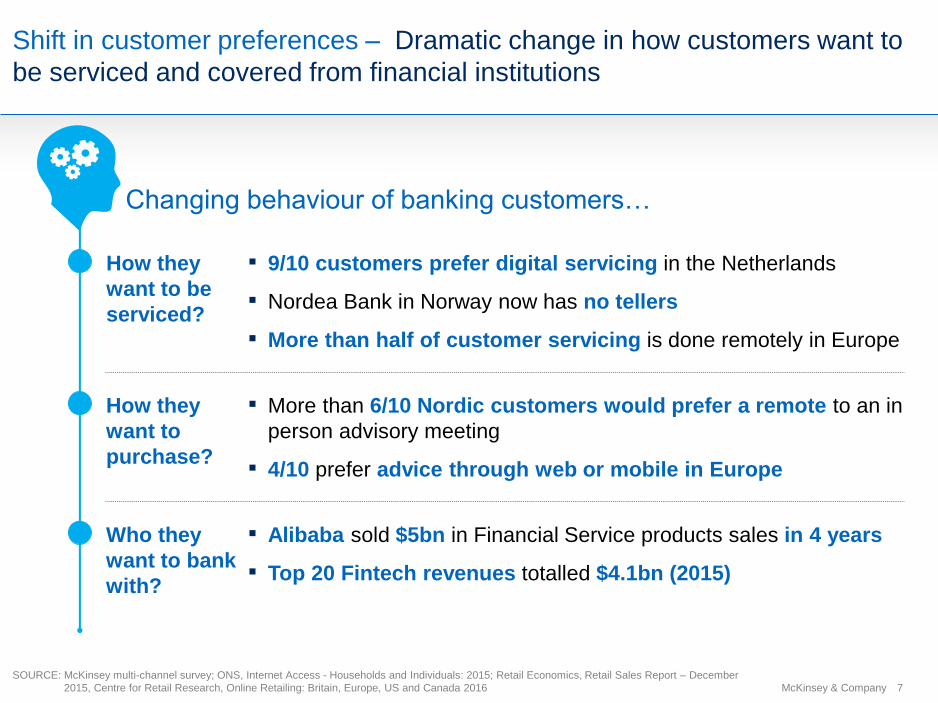

Shift in customer preferences – Dramatic change in how customers want to

be serviced and covered from financial institutions

SOURCE: McKinsey multi-channel survey; ONS, Internet Access - Households and Individuals: 2015; Retail Economics, Retail Sales Report – December

2015, Centre for Retail Research, Online Retailing: Britain, Europe, US and Canada 2016

Changing behaviour of banking customers…

How they

want to be

serviced?

▪ 9/10 customers prefer digital servicing in the Netherlands

▪ Nordea Bank in Norway now has no tellers

▪ More than half of customer servicing is done remotely in Europe

Who they

want to bank

with?

▪ Alibaba sold $5bn in Financial Service products sales in 4 years

▪ Top 20 Fintech revenues totalled $4.1bn (2015)

How they

want to

purchase?

▪ More than 6/10 Nordic customers would prefer a remote to an in

person advisory meeting

▪ 4/10 prefer advice through web or mobile in Europe

8McKinsey & Company

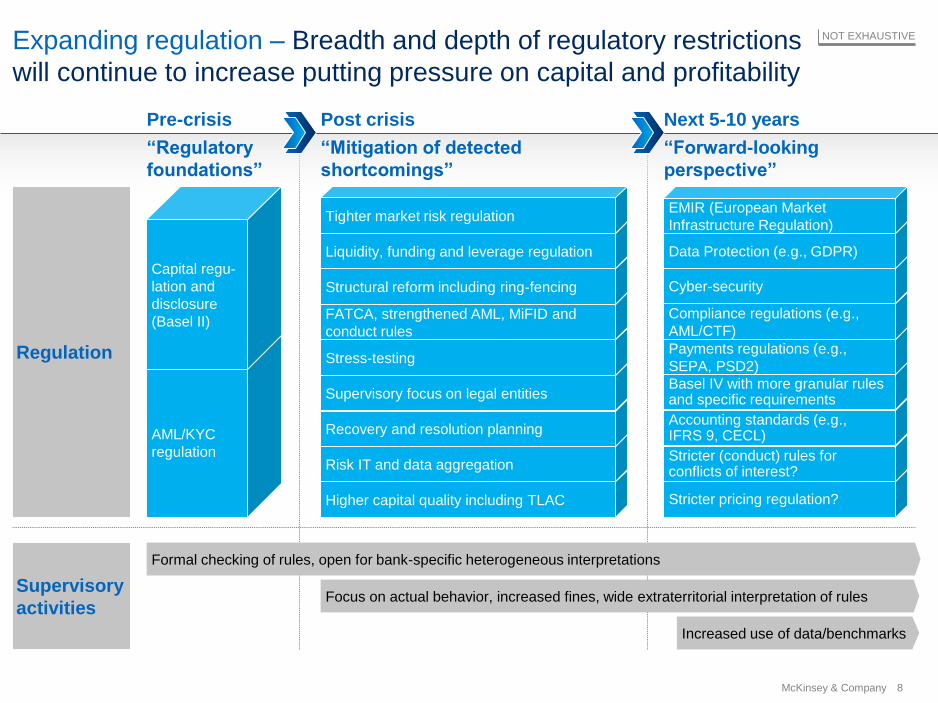

Expanding regulation – Breadth and depth of regulatory restrictions

will continue to increase putting pressure on capital and profitability

NOT EXHAUSTIVE

Regulation

Higher capital quality including TLAC

“Mitigation of detected

shortcomings”

“Regulatory

foundations”

“Forward-looking

perspective”

AML/KYC

regulation

Capital regu-

lation and

disclosure

(Basel II)

Risk IT and data aggregation

Recovery and resolution planning

Supervisory focus on legal entities

Stress-testing

FATCA, strengthened AML, MiFID and

conduct rules

Structural reform including ring-fencing

Liquidity, funding and leverage regulation

Tighter market risk regulation

Stricter pricing regulation?

Stricter (conduct) rules for conflicts of interest?

Accounting standards (e.g., IFRS 9, CECL)

Basel IV with more granular rules and specific requirements

Payments regulations (e.g.,

SEPA, PSD2)

Compliance regulations (e.g.,

AML/CTF)

Cyber-security

Data Protection (e.g., GDPR)

EMIR (European Market

Infrastructure Regulation)

Focus on actual behavior, increased fines, wide extraterritorial interpretation of rules

Formal checking of rules, open for bank-specific heterogeneous interpretations

Supervisory

activities

Increased use of data/benchmarks

Pre-crisis Post crisis Next 5-10 years

9McKinsey & Company

Looking ahead, several key factors can still swing the future market state;

besides regulation, digital will be the key enabler

Will banks embrace innovation and adapt their

business models fast?

Will regulation be extended to non-banks/fintechs?

Who will be trusted more by customers for cyber

security, banks or non-banks/fintechs?

How will non-banks/fintechs perform during the next

big recession?

10McKinsey & Company

What trends are shaping the future of credit risk?

What are the implications for banks and businesses?

What does it all mean for Greece?

3 questions to address today

11McKinsey & Company

Risk management has been transformed substantially over the last 15 years

▪ Business

model

adjustments

▪ ICAAP/risk

appetite

frameworks

▪ Extension to

liquidity and

other non-

financial risks

▪ Basel II

internal

models

▪ First economic

capital models

▪ Upgrade of

key credit risk

processes

▪ 3 lines

of defense,

conduct, risk

culture, and

stress-testing

▪ Risk in day-to-

day decision

making

▪ Risk-adjusted

metrics

▪ What are the

key trends?

▪ What are their

implications?

▪ How to

respond to

them?

▪ First

generation of

models

▪ Considerations

for market risk

2000 - 2007 2008 - 2011 2012 - today Future…Pre 2000

Upgrade key

risk methods

Rise to

strategic levels

Embed risk

management

across the bank

???

Achieve initial

capital

adequacy

12McKinsey & Company

Risk today – Selected observations throughout banks

▪ Highly skilled people spending significant time on manual work (e.g.,

gathering information, analyzing financial information)

▪ Significant working time spent on low value work (e.g., gathering

information, writing lengthy credit assessments)

Significant time

spent on low

value work

▪ “Silo” view by risk type leading to fragmentation of activities in

different parts of the Risk organisation (e.g., analytical intelligence, limit

setting, monitoring, approval support, business engagement, etc.)

Similar

capabilities in

different places

▪ Broad product offering to capture wide spectrum of customer needs

leading to relatively long processing time – low-complexity, non-

standardised risk management approaches

Large variety

of products

Slow

processing

▪ Manufacturing rather than industrial production including people-centric

decision-making and high share of paper-based information delivery

Manual

reporting

▪ Partly manual reporting and inconsistency of information between

reports due to different data sources

13McKinsey & Company

Risk tomorrow – Key thoughts about the future

▪ Networking with experts across the world (e.g., on cyber security)

▪ Identifying emerging trends and understanding of underlying risks and

how to measure them

Constant and

far-out

identification of

emerging risks

Risk appetite

and limit nerve

centre

▪ Constantly looking at control and dashboard info, monitoring changes

to performance

▪ Refining/maintaining risk appetite for different businesses/asset classes

▪ Developing comprehensive risk taxonomy and risk policy framework

Analytical

intelligence

and advanced

data

capabilities

▪ Building/refreshing models based on advanced analytical methods

▪ Conducting granular portfolio diagnostics and adjusting risk

allocation keys

▪ Enabling zero-time and rule-based decisions that are compliant with

regulation and ensuring constant automated controls

Industrialisation

including 3rd

party

integration

▪ Forming SLAs with internal, external data and ops providers and

ensuring delivery of automated controls and generation of reports

▪ Implementing a strong risk culture with Business working within

transparent and mandatory boundaries

14McKinsey & Company

A digital credit transformation is underpinning the future of risk – allowing

faster and better decisions, as well as more efficient operations

Automation/Digitization

▪ Natural language

recognition to automate

customer interactions (e.g.,

chat-bots) and risk reporting

▪ Cognitive computing

algorithms autonomously

reviewing regulatory

documentation and

monitoring compliance

▪ Straight-through-

processing of front office and

back-office operations

▪ Self-serve branches with

automated customer

onboarding and credit

adjudication

Advanced analytics

▪ Machine learning algorithms

enhancing or replacing

traditional approaches

▪ Deep learning models

identifying extremely complex

patterns and supporting online

learning

▪ Natural language processing

and generation algorithms

enabling machine-to-human

conversation

▪ Advanced econometric

methods accounting for time-

varying economic environment

Emerging sources of data

▪ Integrated data silos linking

data across banking products

▪ Digital communications

including social media

▪ Machine-to-machine data

performing passive data

collection

▪ Clickstream data describing

customer journeys

▪ Geospatial data and satellite

imagery identifying high risk

locations

▪ Customer interactions

recorded on video or voice

recordings

15McKinsey & Company

Broader digital transformation programs require significant

investment budgets…

3.3

EUR bn

2.1

EUR bn

4.3

EUR bn

over 7 years

1.2

EUR bn

over 4 years

1.9

EUR bn

over 3 years1.0

EUR bn

over 5 years

1.0

EUR bn

until 2020

SOURCE: Company websites, press search, McKinsey

Group-wide

investments in

digital

Integration of

branches into

multi-channel

offering and

E2E process

digitizationOptimization and

simplification of

corporate

banking (e.g.,

E2E process

optimization)

Development

of new core

banking

system

Further

enhancement

of multi-channel

offering (e.g.,

big data,

mobile)

Integration

of branches

into multi-

channel

offering as

well as IT

and process

optimization

Bank

digitalization

(products

capabilities

process) and

enhancement

of customer

experience

▪ Digital initiatives are bringing significant impact in retail (~70%) and corporate banking (~30%)

▪ Initiatives cover broad range from operations efficiency at the back-office to improved customer

experience at the front-end

EXAMPLES

16McKinsey & Company

…as well as a very different way of working, connecting a broad range of

functions and capabilities

A digital

transformation

requires…

…strong people

commitment

20 to 30 people for each

process digitization (from

IT, Risk, Credit, Business,

Compliance, etc.)

…new roles and

capabilities

New roles such as

Business Owner, Delivery

Manager, Scrum Master

…training and

skill building

Intense comms

and training to

roll-out change

…new delivery

models

Agile and rapid

prototyping are at the

core of digital

transformation

…full-time

investment

team detached

from other activities

and co-located in

digital labs

…full IT support

IT developers and testers

located with the rest of

team; within 16-week

timeline, user-ready

processes generated

17McKinsey & Company

What trends are shaping the future of credit risk?

What are the implications for banks and businesses?

What does it all mean for Greece?

3 questions to address today

18McKinsey & Company

Corporate digital maturity is lagging behind in Greece vs EU

Only 1.3%

ICT specialists over

total workforce (vs.

3.7% EU average)

Only 6.1%

of SMEs are online

(vs. 16.0% EU

average)

Only 1.2%

of the turnover of

SMEs come from e-

commerce (vs. 9.4%

EU average)

Connectivity

Digital public

services

Integration of

digital

Use of

internet

Human

capital

EU average

Average of countries

falling behind

Greece

SOURCE: European Commission Digital Scoreboard 2016

19McKinsey & Company

While credit risk practices have also been lagging in Greece vs. abroad until

today…

▪ Priority of banks on NPEs/capital;

Advanced Analytics use cases in the

area of retail and small business

collections, and economic value and for

mid and large corporates

▪ Launch of digitization efforts with a

focus on retail and distribution

channels; credit risk digitization not yet

“on-the-radar”

▪ Emerging fintech activity mostly

focused on payments; some

collaboration initiatives driven by banks

▪ Access to new healthy lending

remains very limited (even healthy

customers in promising sectors penalized

due to magnitude of historic losses)

▪ Credit processes remain

cumbersome, with significant amount of

paperwork and manual steps

What we have seen to-date What it means for customers

20McKinsey & Company

… we expect to see increasing use of advanced analytics and digitization in

the years to come

▪ Gradual increase in level of

digitization of banks to build

competitive advantage, capturing also

key credit processes typically starting

from retail/small business and expanding

to corporate

▪ Potential (cautious) emergence of

competition from fintech for credit to

healthy individuals and businesses

▪ Potential alliances between banks and

fintech to enhance capabilities and

speed up automation/digitalization

process

▪ Improved access to credit for

businesses in sectors where Greece

can win (e.g., tourism, energy, food

processing, medical tourism and long

term care, waste management, logistics)

▪ Faster, more customer-friendly

processes for credit

What we could see in the future What it means for customers

21McKinsey & Company

We may be starting with a lag, but disruptive technologies will transform

credit risk in Greece too

“I do believe in the horse.

The automobile is a

transitory phenomenon.”

– Wilhelm II (last German emperor)

22McKinsey & Company