Embed Size (px)

Citation preview

The Enemy Within: Dealing with Employee Fraud in Your Pool….

Presentation to AGRiP Fall Educational Forum

October 2015

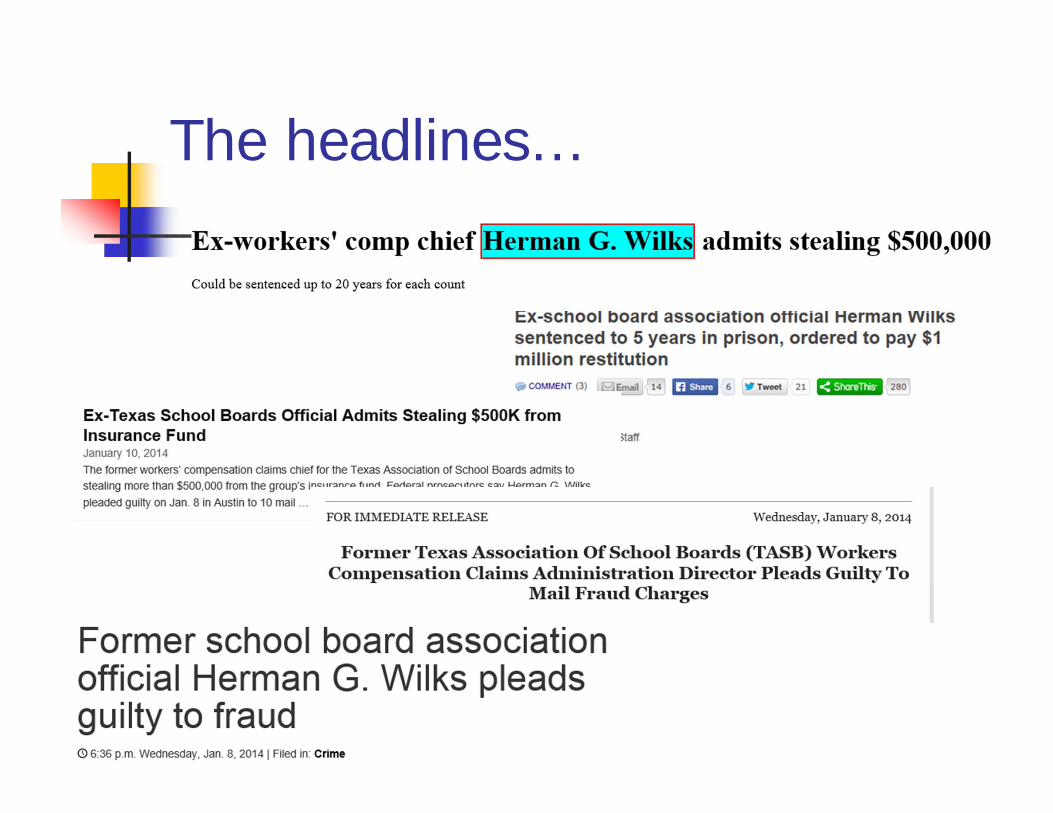

The headlines…

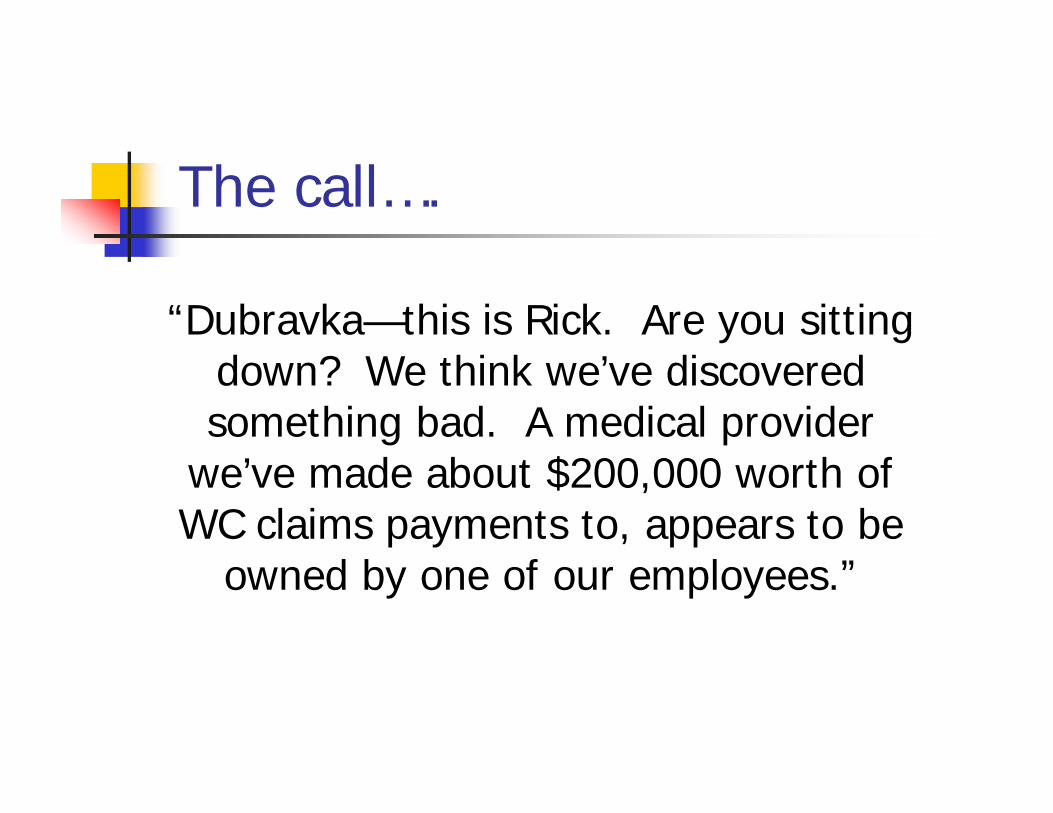

The call….

“Dubravka—this is Rick. Are you sitting down? We think we’ve discovered something bad. A medical provider

we’ve made about $200,000 worth of WC claims payments to, appears to be

owned by one of our employees.”

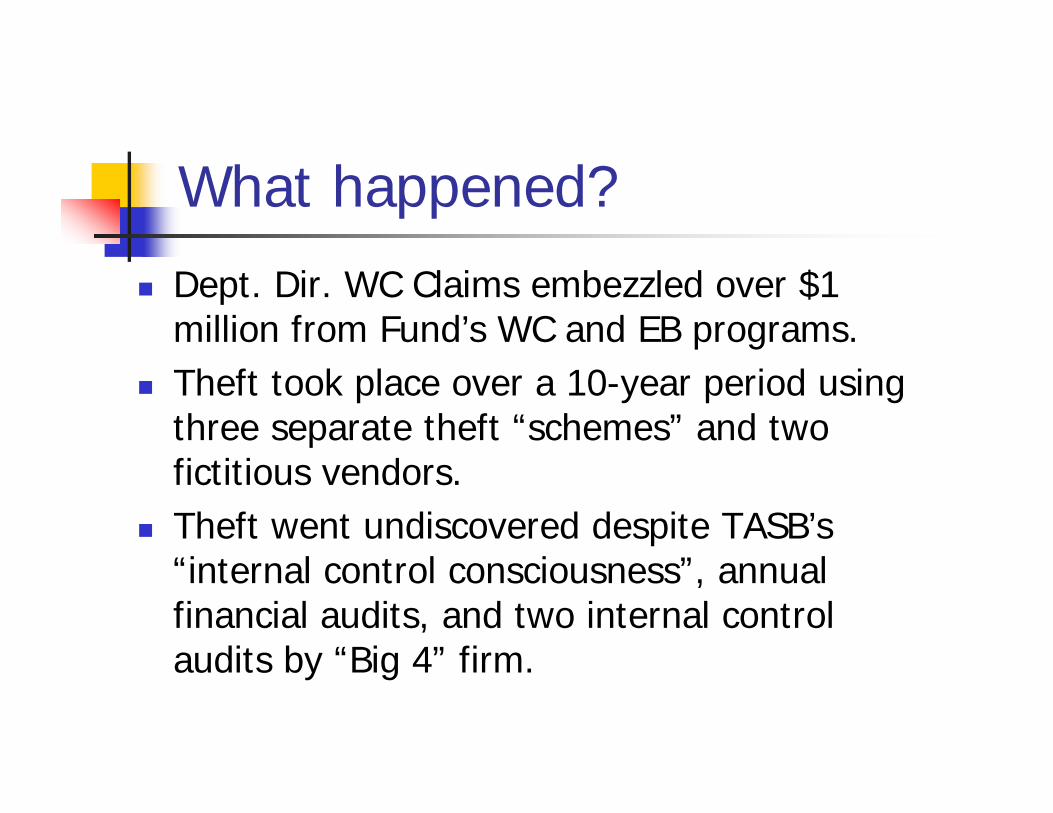

What happened? Dept. Dir. WC Claims embezzled over $1

million from Fund’s WC and EB programs. Theft took place over a 10-year period using

three separate theft “schemes” and two fictitious vendors.

Theft went undiscovered despite TASB’s “internal control consciousness”, annual financial audits, and two internal control audits by “Big 4” firm.

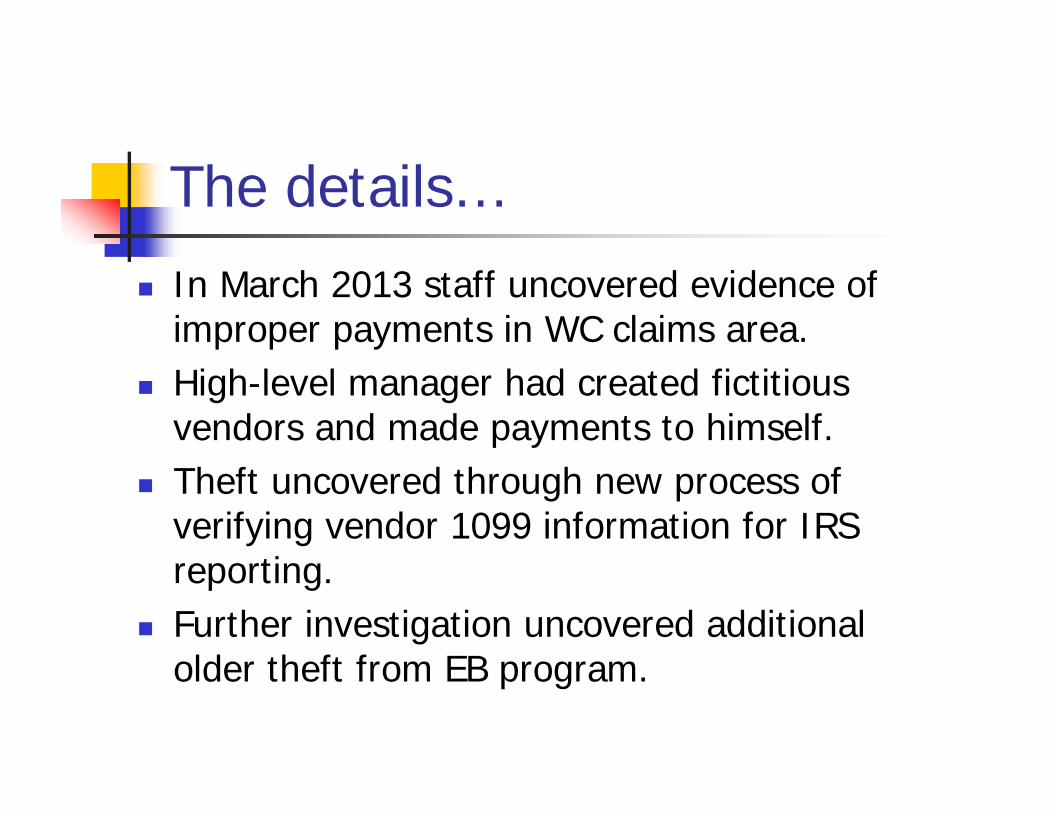

The details… In March 2013 staff uncovered evidence of

improper payments in WC claims area. High-level manager had created fictitious

vendors and made payments to himself. Theft uncovered through new process of

verifying vendor 1099 information for IRS reporting.

Further investigation uncovered additional older theft from EB program.

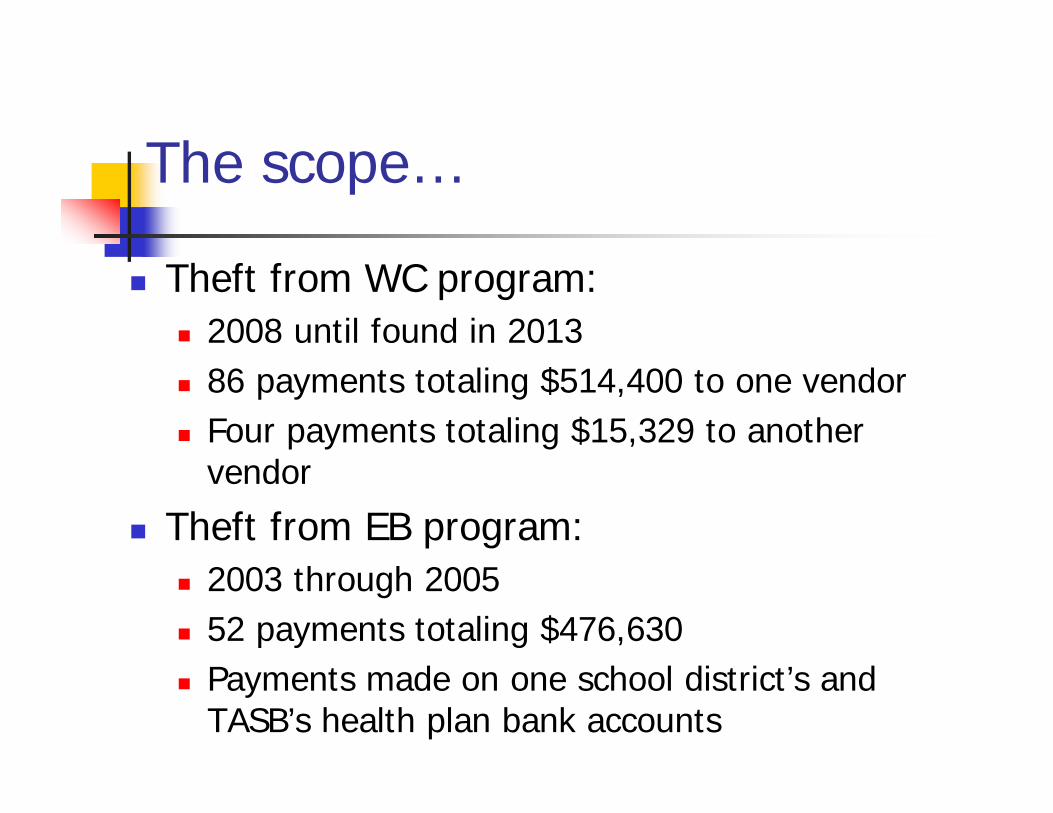

The scope…

Theft from WC program: 2008 until found in 2013 86 payments totaling $514,400 to one vendor Four payments totaling $15,329 to another

vendor Theft from EB program:

2003 through 2005 52 payments totaling $476,630 Payments made on one school district’s and

TASB’s health plan bank accounts

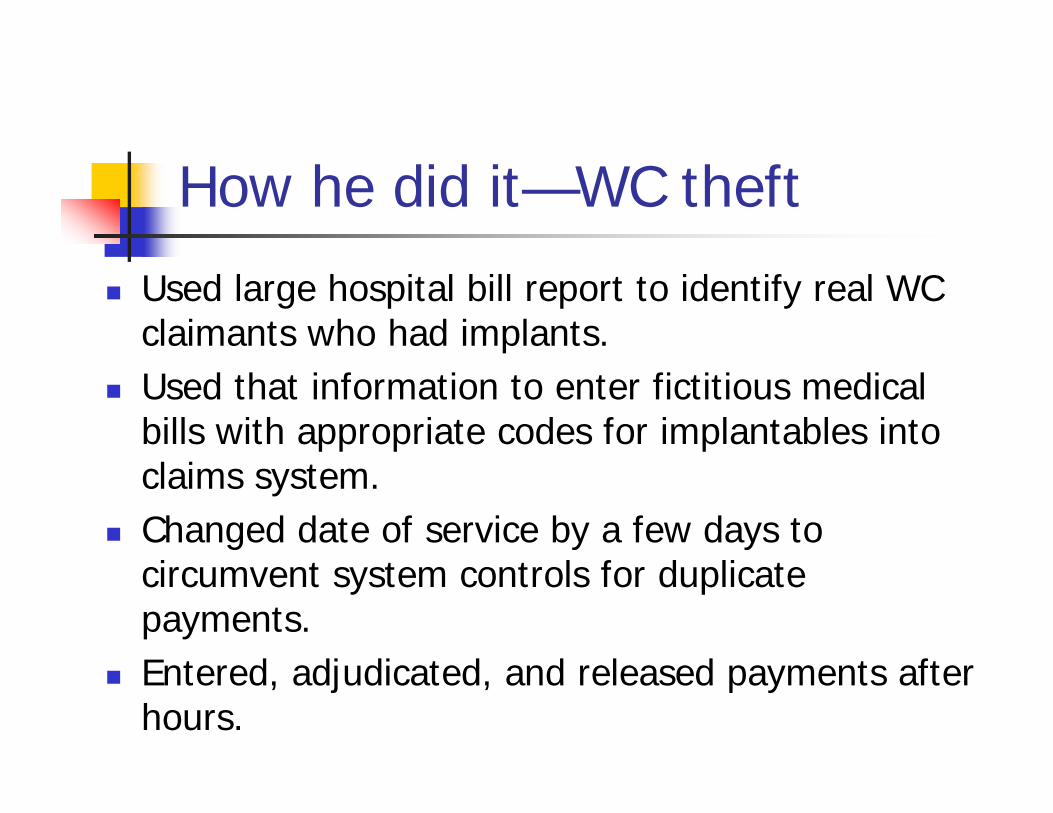

How he did it—WC theft Used large hospital bill report to identify real WC

claimants who had implants. Used that information to enter fictitious medical

bills with appropriate codes for implantables into claims system.

Changed date of service by a few days to circumvent system controls for duplicate payments.

Entered, adjudicated, and released payments after hours.

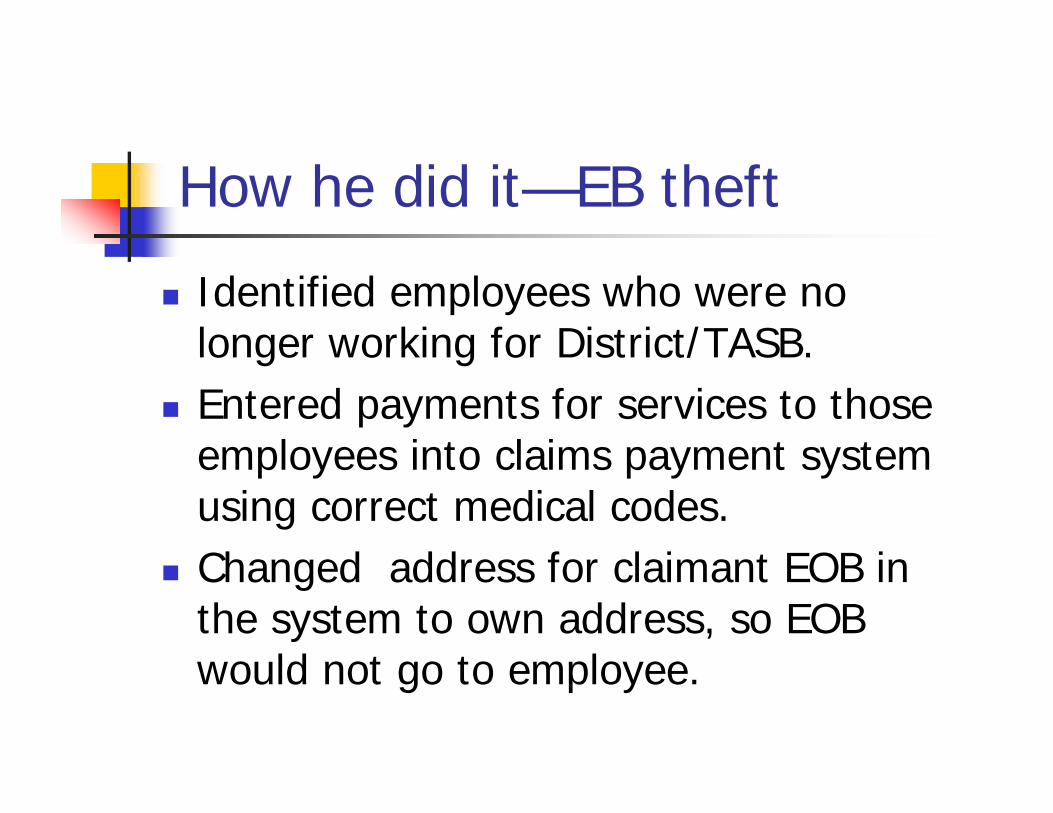

How he did it—EB theft Identified employees who were no

longer working for District/TASB. Entered payments for services to those

employees into claims payment system using correct medical codes.

Changed address for claimant EOB in the system to own address, so EOB would not go to employee.

TASB’s immediate actions…

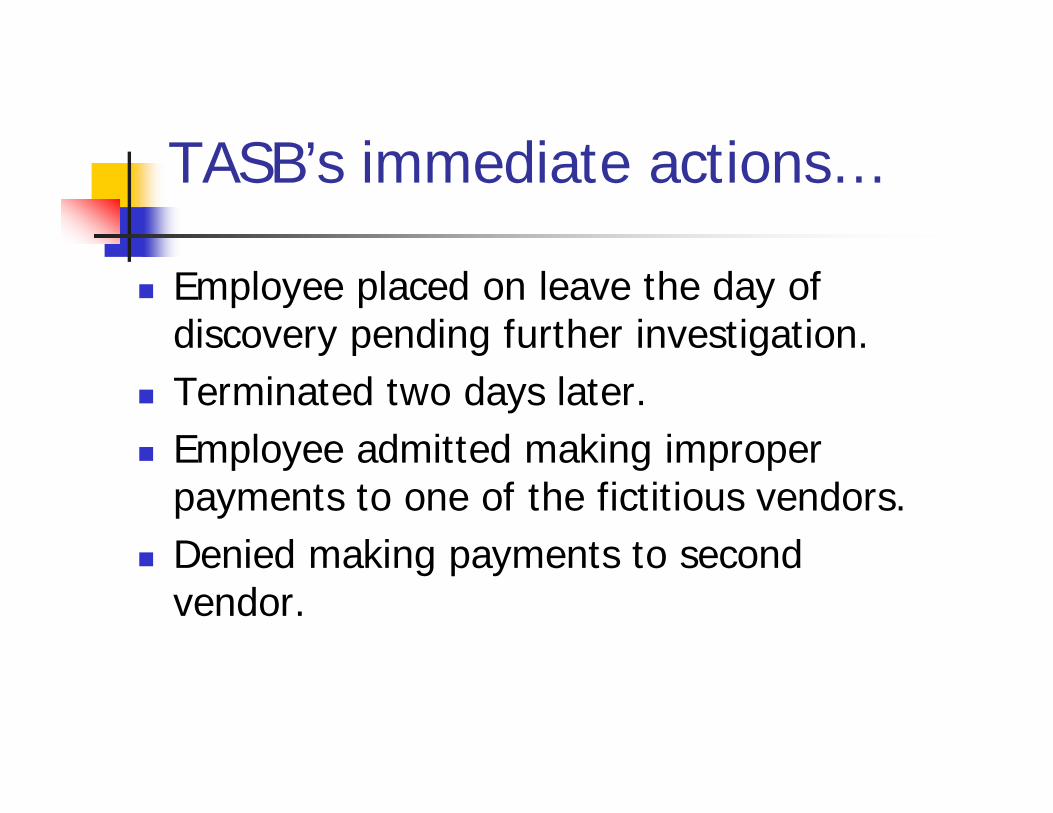

Employee placed on leave the day of discovery pending further investigation.

Terminated two days later. Employee admitted making improper

payments to one of the fictitious vendors. Denied making payments to second

vendor.

TASB’s immediate actions…

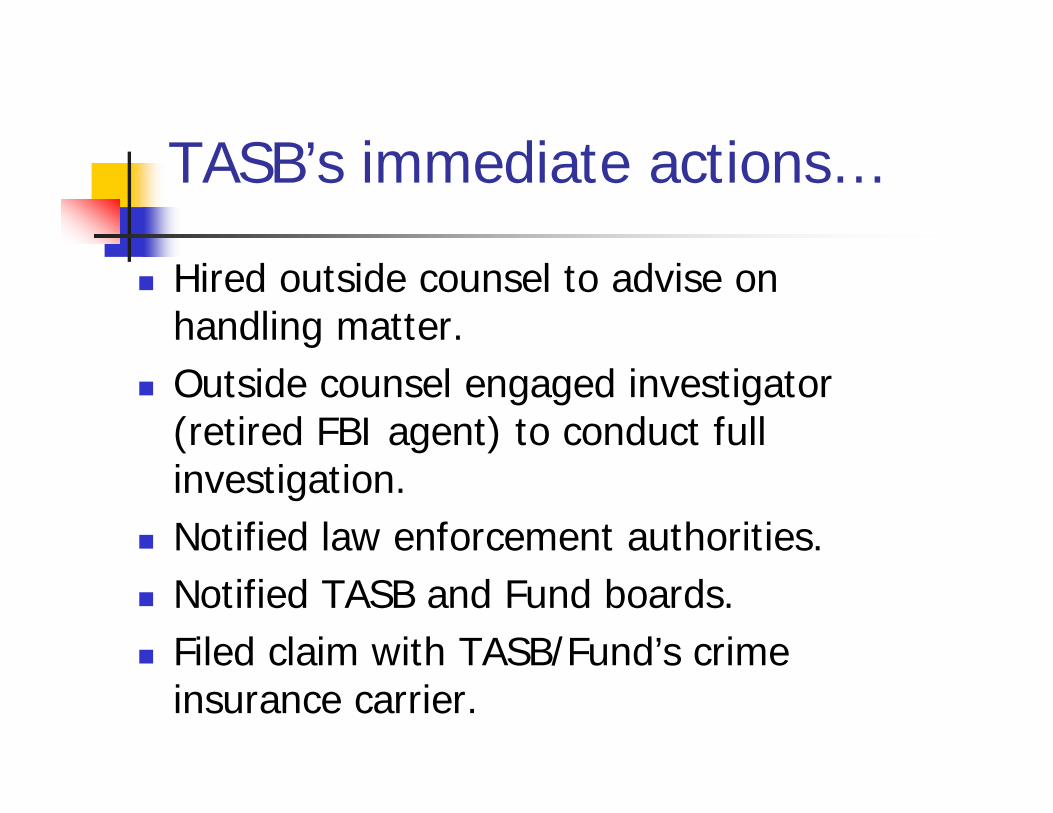

Hired outside counsel to advise on handling matter.

Outside counsel engaged investigator (retired FBI agent) to conduct full investigation.

Notified law enforcement authorities. Notified TASB and Fund boards. Filed claim with TASB/Fund’s crime

insurance carrier.

After the initial shock…

Outside investigation concluded. No evidence of involvement by other TASB

employees. Information turned over to FBI. TASB staff met with affected district to

advise of issue. Comprehensive review of how theft

occurred.

How on earth could this have happened?

Thief was a long-term employee involved in the design and implementation of the claims system.

Able to circumvent a four-step claims adjudication process due to his position and intimate knowledge of the system.

Employees who suspected something was amiss regarding provider went to him for help. He “handled it.”

How on earth could this have happened?

Unclear if he had inappropriate system access because: System access wasn’t changed after he changed jobs. Had broader access as back-up for releasing claims if

needed. Discovered way to access payments that no one knew

about. No routine reviews of payments initiated and

released by same individual.

Corrective steps taken… Comprehensive review of internal controls

and processes. External experts engaged to evaluate system

set-up and security on all RMS payment systems.

Changes implemented in: Vendor set-up and maintenance process IT system security and set-up Segregation of duties

Corrective steps (cont.)

Outside audit firm engaged to conduct risk assessment for all TASB operations.

Internal audit functions expanded: Annual ongoing internal audit reviews by outside

firm for TASB operations. Fund engaged same outside firm to provide

outsourced internal audit services. Ongoing work to increase everyone’s

awareness of need for strong internal controls.

Corrective steps (cont.)

Developed expanded integrity reporting processes.

Increased focus and training on fraud awareness and TASB’s ethics values.

Reviewed and strengthened policies in other areas susceptible to fraud (vendor relationships, expense reporting, etc.)

The rest of the story… In January 2014, employee pled guilty to 10 counts of

mail fraud. Sentenced in March to 63 months in federal prison plus

full restitution. US Attorney’s office issued press release resulting in

widespread media coverage. TASB posted notice about matter on website. No

reaction from members. Crime policy partially reimbursed for stolen funds. Fund reimbursed District for stolen funds.

Lessons learned… Fraud really can (and does) happen. Deal with that

reality. Collateral damage is as bad as financial damage:

Loss of trust Sense of betrayal Extra work to review processes

Internal controls are EVERYONE’s responsibility, not just Finance Dept.

Maintaining energy and enthusiasm for internal controls can be a challenge over the long haul.

Easy things you can do… Vendor management process

What controls/segregation of duties are in place for vendor set up/changes?

How do you verify validity of vendors? How often do you clean up vendor database?

System set-up and security Decide whose job it is to review and verify system

security. Conduct system access reviews on a regular basis. Implement process for managing access/changes.

Easy things you can do… EMPHASIZE culture of ethics and

integrity Starts at the top Don’t assume people know organizational

values Be prepared

Response plan Crisis communication plan Recovery plan

Finally…

What doesn’t kill you makes you stronger. Today we are better and stronger (and a little wiser, too!)