Embed Size (px)

Citation preview

THE EFFECT OF CORPORATE DIVERSIFICATION ON

THE FINANCIAL PERFORMANCE OF LISTED

MANUFACTURING FIRMS IN KENYA

EDWARD MWANGI

A RESEARCH PROJECT SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD

OF THE DEGREE OF MASTER OF BUSINESS

ADMINISTRATION, SCHOOL OF BUSINESS, UNIVERSITY OF

NAIROBI

NOVEMBER 2015

ii

DECLARATION

This research project is my original work and has not been presented to any other

institution. No section of this project may be reproduced or transmitted in any form

or by any means, without permission from the author or that of the University of

Nairobi.

Signature ………………………………………… Date………………………

Edward Mwangi

D61/64691/2013

This research project has been submitted for examination with my approval as the

University of Nairobi supervisor.

Signature ………………………………………… Date………………………

Dr. Cyrus Iraya

Lecturer,

Department of Finance and Accounting

Lecture, University of Nairobi

iii

ACKNOWLEDGEMENTS

I wish to thank a number of people and groups whom without them this project could

not have been successful. I sincerely want to thank my supervisor Dr. Cyrus Iraya for

his professional guidance and advice when I was writing my project.

The entire staff of the Nairobi Securities Exchange for the assistance that they

accorded to me during data collection period. Kindly, accept my appreciation.

The entire academic staff of the University of Nairobi, School of Business for their

support in one way or another during my study period.

Finally, to my parents, relatives and friends, I thank you all for your love, support and

encouragement when I was pursuing my studies.

iv

DEDICATION

This project is dedicated to my family for their love, support and understanding when

I was pursuing my project.

v

TABLE OF CONTENTS

DECLARATION.......................................................................................................... ii

ACKNOWLEDGEMENTS ...................................................................................... iii

DEDICATION............................................................................................................. iv

LIST OF TABLES ..................................................................................................... vii

ABBREVIATIONS AND ACRONYMS ................................................................ viii

ABSTRACT ................................................................................................................. ix

CHAPTER ONE: INTRODUCTION ........................................................................ 1

1.1 Background of the Study ......................................................................................... 1

1.1.1 Corporate Diversification .......................................................................... 2

1.1.2 Financial Performance .............................................................................. 3

1.1.3 The Effect of Corporate Diversification on Financial Performance ......... 4

1.1.4 Manufacturing Firms in Kenya ................................................................. 5

1.2 Research Problem .................................................................................................... 6

1.3 Research Objective .................................................................................................. 8

1.4 Value of the Study ................................................................................................... 8

CHAPTER TWO: LITERATURE REVIEW ......................................................... 10

2.1 Introduction ............................................................................................................ 10

2.2 Theoretical Framework .......................................................................................... 10

2.2.1 Capital Asset Pricing Model ................................................................... 10

2.2.2 Portfolio Diversification Model of Alliances ......................................... 11

2.2.3 Resource-Based Theory and Corporate Diversification ......................... 13

2.3 Determinants of Financial Performance ................................................................ 14

2.3.1 Size of the Firm ....................................................................................... 14

2.3.2 Management Efficiency .......................................................................... 15

2.3.3 Use of Leverage ...................................................................................... 16

2.3.4 Corporate Diversification ........................................................................ 17

2.3.5 Growth of the Firm ................................................................................. 18

2.3.6 Product Diversification ........................................................................... 18

2.4 Empirical Review................................................................................................... 19

2.5 Summary of the Literature Review ........................................................................ 23

vi

CHAPTER THREE: RESEARCH METHODOLOGY ........................................ 24

3.1 Introduction ............................................................................................................ 24

3.2 Research Design..................................................................................................... 24

3.3 Population .............................................................................................................. 24

3.4 Data Collection ...................................................................................................... 25

3.5 Data Analysis ......................................................................................................... 25

3.6 Analytical Model ................................................................................................... 25

3.6.1 Tests of Significance ............................................................................... 27

CHAPTER FOUR: DATA ANALYSIS, RESULTS AND DISCUSSION .......... 28

4.1 Introduction ............................................................................................................ 28

4.2 Response Rate ........................................................................................................ 28

4.3 Descriptive Statistics .............................................................................................. 28

4.4 Correlation Analysis .............................................................................................. 29

4.5 Regression Analysis and Hypothesis Testing ........................................................ 30

4.5.1 Analysis of Variance ............................................................................... 31

4.5.2 Model of Coefficients ............................................................................. 32

4.6 Discussion of Research Findings ........................................................................... 33

CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATIONS

...................................................................................................................................... 35

5.1 Introduction ............................................................................................................ 35

5.2 Summary of Findings ............................................................................................. 35

5.3 Conclusion ............................................................................................................. 36

5.4 Recommendations .................................................................................................. 37

5.5 Limitations of the Study......................................................................................... 38

5.6 Suggestions for Further Research .......................................................................... 39

REFERENCES ........................................................................................................... 41

APPENDICES ............................................................................................................ 47

APPENDIX I: Listed Manufacturing Firms: Industrial and Allied Sector ......... 47

APPENDIX II: Secondary Data ............................................................................... 48

APPENDIX III: Logarithm of Assets was obtained using Microsoft Excel

Formula for Natural Log........................................................................................... 51

APPENDIX IV: Listed Manufacturing Firms in Kenya ........................................ 52

vii

LIST OF TABLES

Table 4.1: Descriptive Statistics .................................................................................. 29

Table 4.2: Correlation between the Study Variables ................................................... 30

Table 4.3: Model Summary ......................................................................................... 31

Table 4.4: Analysis of Variance................................................................................... 31

Table 4.5: Model of Coefficients ................................................................................. 32

viii

ABBREVIATIONS AND ACRONYMS

CAPM Capital Asset Pricing Model

DTMFI’s Deposit Taking Microfinance Institutions in Kenya

NSE Nairobi Securities Exchange

REM Random Effect Model

ROA Return on Assets

RR Related Ration

RS Specialization Ratio

UK United Kingdom

WMP World Manufacturing Production

ix

ABSTRACT

Diversification is developing as one of the most important growth strategies adopted

by firms to boost performance. Some firms that have adopted diversification strategies

have succeeded while others have failed. The study sought to determine the effect of

corporate diversification on the financial performance of listed manufacturing firms in

Kenya. To achieve this objective the study used a descriptive survey. The population

of the study constituted all the 19 listed manufacturing firms at NSE. A census

approach was used and secondary data was used for five years (2010-2014). The data

was gathered from financial statements and records. Data analysis was done using a

regression model. The study found that corporate diversification was positively

related to financial performance of listed manufacturing firms in Kenya. Growth and

firm size were found to be negatively related to financial performance of listed

manufacturing firms. The correlation results were found to be weak but moderate

between corporate diversification and financial performance of listed manufacturing

firm. The study recommends that firms should offset the risk of doing business.

Through expanding, a firm is not dependent on a limited number of products,

locations, or markets in order to survive. A company may pursue this diversification

in reaction to a change in the market. The study was conducted within a limited time

and scope. The results and the conclusion drawn in this study cannot however; be

used to make generalization of all the manufacturing firms operating in Kenya.

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Corporate diversification has been significant issue in the modern business world.

This issue has an impact on firm’s financial performance. However, there is no

agreement about the negative, positive or neutral impact due to the turbulent nature of

the external environment. Mansi and Reeb (2002) indicate that firms in emerging

market may be justified to have a wider scope because market failures are more

prevalent in developing economies. Diversification provides benefits to managers that

are unavailable to investors since they stand to gain when the firm accrues better

returns from diversifying (Geringer, Tallman and Olsen, 2000).

Diversification can also lead to the problem of moral hazard, the chance that people

will alter behavior after entering into a contract as in a conflict of interest by providing

insurance for managers who have invested in firm specific skills, and have an interest

in diversifying away a certain amount of firm specific risk and may look upon

diversification as a form of compensation. Rajan, Servaes and Zingales (2000)

elucidate that diversity assists a firm to build stability, when the firm concentrates too

heavily on a single industry or product, it may risk volatility in revenue and resources

as demand rises and falls. When the business stretches across many industries or

categories, it may have more predictability. Ishak and Napier (2004) explains that a

firm that wishes to succeed in diversification may have to spread out its business

investments and costs; this may prevent the firm from putting adequate finances in

products and cash cow-sectors this is because when the firm expands it needs experts

or partners with whom to achieve success in newer, unproven areas.

2

In reference to Lins and Servaes (2001), the significance of diversification of

unrelated businesses is to mitigate the risks involved in investing in one line of

business. Strategic diversification of unrelated businesses provides a strategic fit to

gain competitive advantage, and then use competitive advantage to achieve the

desired shareholder value. The reasons for diversifying into unrelated businesses,

hinge almost exclusively on opportunities for attractive financial gains (Ishak and

Napier, 2006).

1.1.1 Corporate Diversification

Mansi and Reeb (2002) define corporate diversification as the process of a company

expanding into different areas, such as industries and product lines. Companies

typically do this in order to build the business. Delios and Beamish (1999) puts forth

that diversification can involve expanding, revitalizing, or even saving a company.

Most investment professionals agree that, although it does not guarantee against loss,

diversification is the most important component of reaching long-range financial

goals while minimizing risk.

Rajan, Servaes and Zingales (2000) maintain that investors confront two main types

of risk when investing that is systematic and unsystematic risks. Systematic risk is

also called undiversifiable risk or market risk. Undiversifiable risk is associated with

every firm. The causes of this form of risk are for example: things like inflation rates,

exchange rates, political instability, war and interest rates. Geringer and Tallman

(2000) argue that the other form of risk is diversifiable risk, this risk is also known as

unsystematic risk and it is specific to a firm, the industry, market, economy or

country; it can be reduced through diversification. The most common sources of

3

unsystematic risk are business risk and financial risk. Thus, the aim is to invest in

various assets so that they will not all be affected the same way by market events.

Mansi and Reeb (2002) outlined that corporate diversification can be categorized into

four major categories of large companies. These four major categories are namely:

single business, dominant business, related business, and unrelated business. The

categorization can be based first on the specialization ratio (Rs), which expresses the

proportion of a firm’s revenues attributable to its largest single business in a given

year and second on the related ratio (Rr), which expresses the proportion of a firm’s

revenues attributable to its largest group of related business. Specialized business

diversification means that a company is basically committed to a single business

expressed as (Rs ≥ 0.95 and Rr ≥ 0.70).

According to Doaei and Anuar (2012) dominant business diversification refers to

companies that diversified to only a limited extent from the single business (0.70 ≤ Rs

<0.95 and Rr ≥0.70). Related diversification of nonvertically diversified firms

involves expansion into businesses related to the company’s core activities (Rs <0.70

and Rr ≥ 0.70). Unrelated diversification of nonvertically diversified firms includes

entry into businesses and markets unrelated to a company’s previous activity (Rs <

0.70 and Rr < 0.70).

1.1.2 Financial Performance

Penman (2007) defines financial performance as the level of performance of a

business over a specified period of time, expressed in terms of overall profits and

losses during that time. Evaluating the financial performance of a business allows

decision-makers to judge the results of business strategies and activities in objective

4

monetary terms. A subjective measure of how well a firm can use assets from its

primary mode of business and generate revenues.

According to Penman (2007) there are many different ways to measure financial

performance, but all measures should be taken in aggregation. Some of the indicators

of financial performance are return on equity, liquidity ratios, asset management

ratios, profitability ratios, leverage ratios and market value ratios.

Petersen and Kumar (2010) note that the other financial indicators of financial

performance include: sales growth, return on investment, return on sales and earnings

per share. The popular ratios that measure organizational performance can be

summarized as profitability and growth: return on asset, return on investment, return

on equity, return on sale, revenue growth, market shares, stock price, sales growth,

liquidity and operational efficiency (Petersen and Kumar, 2010).

1.1.3 The Effect of Corporate Diversification on Financial

Performance

According to Denis, Denis and Yost (2002), theoretical arguments indicate that

corporate diversification is associated with both costs and benefits to the firm which

leads to financial performance of the firm. Potential costs of diversification include

the use of larger discretionary resources to undertake value-decreasing investments,

cross-subsidies that allow poorly performing segments to drain resources from better-

performing segments, and misalignment of incentives between central and divisional

managers. This highly contributes to financial performance of firms since the

potential benefits of operating different lines of business leads to greater operating

efficiency, fewer incentives to forgo positive net present value projects, greater debt

capacity, and lower taxes (Jensen and Murphy, 1990).

5

In reference to Jensen and Murphy (1990) corporate diversification reduces the cost of

debt; similarly aggregating business segments that have imperfectly correlated cash

flow streams reduces the variability of earnings for the combined firm. Another set of

agency-based theoretical and empirical arguments takes the opposite view: that

corporate diversification increases the agency costs of debt. Diversified firms tend to

increase significantly in size, since the level of managerial compensation is positively

correlated with firm size which enhances firm performance. Berger and Ofek (1995)

argue that larger firms become more complex, thus making monitoring harder. In

addition; cross-subsidization between divisions’ increases the firm risk and the

probability of default.

Chakrabarti et al. (2007) examined the effect of corporate diversification on

performance for some firms acting in stable period and economy shock. They did

their research in six Asian countries between 1988 and 2003. They concluded that

diversification has a negative effect on performance in more developed institutional

environments; although, in least developed environments there is an improving

performance (Brammer and Pavelin, 2006).

1.1.4 Manufacturing Firms in Kenya

Manufacturing sector makes an important contribution to the Kenyan economy and

currently employs 254,000 people, which represents 13 per cent of total employment

with an additional 1.4 million people employed in the informal side of the industry.

To keep up the pace of the changing environmental needs most manufacturing firms

in Kenya have diversified their portfolios in both related and unrelated businesses to

mitigate their financial losses that may negatively impact on their financial

performance (World Manufacturing Production, 2014).

6

Manufacturing firms often diversify into related service activities due to expected

leverage effects of existing technological expertise, customer relationships and brand

identity. Most manufacturing firms in Kenya can easily achieve synergies by

diversifying into product related services. Estrada (2002) outlines that product and

service businesses represent strategic complements that can realize a super-additive

sales synergies and sub-additive cost synergies of a reciprocal nature. Manufacturing

firms invest in service diversification that contributes to overall performance, to the

extent that more traditional economies of scope can be achieved.

Due to uncertainties and risks in the external environment, most manufacturing firms

have invested a lot in diversification in order to increase their commanding market

share. By introducing new products, exploring new regions or targeting new groups of

customers, these firms have succeeded in expanding their customer base (Forbes,

2002).These have exposed the firms to more competition, potential changes in

customer preferences. Adoption of modern technologies for example information

communication technology has made the existing technology obsolete and thus the

firms have shifted to new technologies, this however has exposed the firms to too

much cost whereas there is no guarantee that every strategy is profitable (Brammer

and Pavelin, 2006).

1.2 Research Problem

Most firms globally are now engaging in risk management in order to mitigate

financial losses which may attract huge losses to the manufacturing firms.

Diversification has received a lot of attention as one of the key strategies in risk

reduction. Daud and Salamudin (2009) explained that most firms that have diversified

their portfolios of assets perform better than organizations that invest and only rely in

one line of business. Mansi and Reeb (2002) posit that in diversification, firms are

7

more likely to manage and mitigate their risks because if one investment does not

perform the other invests is more likely to perform since they may not be facing

similar risks; in this case the firm does not suffer total loss.

In Kenya, world manufacturing production report (2014) provides that competition

in manufacturing industries creates pressures on the product margins, manufacturing

firms’ starts to differentiate by complementing and enriching their initial product

offerings with services. This attracts them to invest in unrelated lines of business in

order to mitigate risks. Lins and Servaes (2001) contends that diversification of

portfolio requires lots of plan and good effort in order to succeed in risk reduction,

most firms are diversifying their functions into services, and this has led to additional

growth in terms of revenue and profit.

Caper and Kotabe (2003), conducted a study on the effects of diversification on

financial performance on German firms in the service industry. The results of the

study showed that there was a positive relationship between diversification and

performance of German service firms. A study by Jung and Chan-Olmsted (2005) on

the relationship between related product and international diversification and financial

performance among media firms in United States concluded that, there was a positive

relationship between diversification and financial performance. Bammer et al. (2006)

investigated on the relationship between corporate social performance and

geographical diversification on a sample of UK firms. It was found that there was a

positive relationship between diversification and performance.

Maina (2013), did a study on the effect of product diversification on financial

performance of DTMFI’s. It was found that diversification of products and services

led to financial performance of deposit taking microfinance institutions. Maina (2013)

8

carried out a study on the relationship between product diversification and financial

performance of commercial banks in Kenya. It was concluded that product

diversification led to performance of commercial banks. Ongalo (2014) found that

there was an inverse relationship between diversification and corporate liquidity on

firms listed at Nairobi Securities Exchange.

This study therefore sought to determine the effect of corporate diversification on the

financial performance of listed manufacturing firms in Kenya by attempting to answer

the following question: what is the effect of corporate diversification on the financial

performance of listed manufacturing firms in Kenya?

1.3 Research Objective

To determine the effect of corporate diversification on the financial performance of

listed manufacturing firms in Kenya.

1.4 Value of the Study

The findings of the research study would be of significance to many people including

the following; manufacturing firms especially the listed ones. They will find the

findings of this study very informative in key investments decisions that lead to

diversification of service and unrelated businesses to mitigate their risk portfolio.

Financial consultants will find this research important, as it will provide information

on the significance of diversification to investors. Private practitioners such as

auditors and investment companies may use the study findings to advice firms on the

timings of diversification and how it may contribute to financial performance of the

firm.

9

The findings of this study may inform theory building. Academicians in the field of

finance and investments may find this piece of work a valuable addition to literature

especially in mitigating financial losses through corporate diversification. The study

findings and conclusions could also be used as reference point for further research.

10

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This section provides the theoretical framework of the study, the determinants of

financial performance, the empirical review and the summary of the literature review.

2.2 Theoretical Framework

This part covers theories that support the relationship between corporate

diversification and financial performance. The theories are namely capital asset

pricing model, portfolio diversification model of alliances and resource based theory

and corporate diversification.

2.2.1 Capital Asset Pricing Model

On the basis of mean variance rule, Sharpe (1964), Lintner (1965) developed the

capital asset pricing model (CAPM). Similarly, Treynor (1965), Sharpe (1966) and

Jensen (1968) developed the traditional performance measures based on mean

variance criterion. However, the traditional CAPM and these performance measures

are subjected to some limits, in particular those concerning the asymmetry of returns

and the risk perception of investors. Indeed, this model and these traditional

performance measures become inadequate when the returns are not normally

distributed (Harlow and Rao, 1989).

Moreover, the beta and the variance which are used as risk measures in this model do

not make distinction between the returns superior and those inferior to the mean.

According to Bawa and Lindenberg (1977), these risk measures consider them equally

undesirable, whereas the investors often associate the risk to the obtaining of returns

11

lower than the target return. In order to overcome these drawbacks, some studies

proposed the use of downside risk measures in the CAPM and in the traditional

performance measures to take into account the asymmetry of returns and the risk

perception of investors (Tobin, 1958).

The researches of Hogan and Warren (1974), contributed to the development of the

capital asset pricing models in the downside risk framework. Later Estrada (2002)

developed a new capital asset pricing model in the downside risk framework which

made it possible to overcome the drawbacks of the former models in this framework.

Indeed, Estrada (2002) detected that the cosemivariance determined by Hogan and

Warren (1974) has a limitation by proving that the co-semi variance between asset i

and the market portfolio M is different from that between the market portfolio M and

the asset i.

It was concluded that the downside beta of Estrada (2002) is more plausible than the

other downside betas, developed by Hogan and Warren (1974), Bawa and Lindenberg

(1977) and Harlow and Rao (1989), not only because it makes it possible to take into

account the asymmetry of returns not captured by traditional beta but also because it

makes it possible to overcome the problem of inequality of the co-semi variances

existing in the other downside betas.

2.2.2 Portfolio Diversification Model of Alliances

This theory was put forward by Holsti, Hopman and Sullivan (1973), the theory of

finance demonstrates that diversified investment portfolios produce superior

combinations of risk and return, and that investors may choose a portfolio reflecting

their preferred mix of risk and return. Morrow and James (1991), argue that these

12

techniques may be applied to military alliances. The rate of return and risk of an ally

follows a positive linear relationship, as predicted by capital asset pricing theory.

Morrow and James (1991) puts forth that random diversification of allies will, as with

investment portfolios, reduce the country-unique components of alliance risk toward

that which is inherent in the system as a whole. Some alliances will be more efficient

at producing greater return and lower risk. The most efficient alliances will be those

in which variations in ally effort move in opposite directions. Development of the

demand side of portfolio analysis may predict which alliances are optimal, and

therefore most likely to form. These principles are applied to the Triple Entente and

Triple Alliance between 1879 and 1914. It is suggested that the Entente had superior

efficiency characteristics and that ally choices were consistent with demand patterns.

Bennett and Scott (1997) explain that this theory provides that the basic purpose

behind forming alliances is capacity aggregation. When two or more states work

together, they become a more formidable potential fighting force. In most cases,

alliances do no perfectly coordinate military policy, but pre-war coordination and

planning allow states to fight together more effectively. While theorizing has focused

most often on the improved ability to deter attack with the promise of aid from allies

capability aggregation can be useful for advancing a variety of goals. Alfeld (1984)

and Lalman and Newman (1991) did a statistical analysis that show that most

alliances that states choose to form increase their security and should improve their

ability to deter attacks.

As in models of alliances, the assumption is that the primary benefit of alliances is

capability aggregation to form a strong force and win an attack. Specifying the goal of

an alliance activity is important in setting direction (Gibler, 1997). Gowa et al., (1993)

13

argue that the essence of this theory is the concepts of risk return. These are measured

and shown to follow a positive linear relationship for military allies as they do for

financial assets, a key prediction of the capital pricing model.

2.2.3 Resource-Based Theory and Corporate Diversification

The introduction of resource based theory in the 1980s and 1990s, along with closely

related ideas, such as distinctive competence (Hitt et al., 1997), dominant logic

(Prahalad & Bettis, 1986), and core competence (Prahalad & Hamel, 1990), offered a

unified theoretical framework for the broad corporate diversification research stream

that emphasizes the importance of firm resources.

According to Prahalad & Hamel (1990), from the perspective of resource based

theory, diversification research posits that related diversification can lead to superior

firm performance, compared to that of a focused strategy, because firms can

maximize their resources across several businesses to realize additional returns.

Operational economies of scope as afforded by related diversification facilitate a firm

to assemble a portfolio of businesses that are mutually reinforcing, as critical

resources can be shared among business units (Kor and Mahoney, 2004).

Hitt et al., (1997) argues that when viewing the benefits of diversification from this

perspective, firms with related diversification strategies can outperform those with

unrelated diversification strategies. To the extent that the key to superior performance

from a diversification strategy is contingent on the ability to share resources, a firm

that is diversified into unrelated businesses is unlikely to have resources that can be

useful for all its business units.

At the same time, it becomes challenging for the firm’s top management to manage an

increasingly diverse business portfolio. Taken together, diversification researchers

14

employing resource based theory perspective tend to suggest that levels of

diversification likely exhibit an inverted U-shaped relationship with firm performance

(Kock and Guillen, 2001). In essence, diversification research premised on resource

based theory holds that strategic interrelationships based on resource relatedness

shared by business units within the firm contribute to superior performance and thus

increase firm value to the point where resources become too complex to manage or

business units become unrelated.

One of the studies that support this theory is Kor and Mahoney (2004) who found that

related diversification improves firm performance only when it allows a business to

have preferential access to strategic assets, and any competitive advantage is

dependent on organizational structures that allow the firm’s divisions to share existing

strategic assets and to transfer the competence to build new ones efficiently.

2.3 Determinants of Financial Performance

The determinants for financial performance discussed in this study are: size of the

firm, management efficiency, use of leverage, corporate diversification and growth of

the firm.

2.3.1 Size of the Firm

Size of the firm is a key determinant of financial performance, this is because,

according to Kang and Aage (2001), size of the firm plays an important role in capital

structure, small firms are often managed by very few managers whose main objective

is to minimize the intrusion in their business and that is why internal funds will lie in

the first place of their preference of finance. If internal funds are not enough, small

firms will prefer debt to new equity mainly because debt means lower level of

intrusion and lower risk of losing control.

15

Keister (2001) emphasized that profit interacts with size; large firms are less

susceptible to bankruptcy because they tend to be more diversified than smaller

companies. Therefore, low levels of bankruptcy enable large firms to take on more

debts. The larger firms can reduce the level of information asymmetries in the market

and obtain financial resources more easy which in turns leads to financial

performance of a firm.

With reference to Kang and Aage (2001) in small firms, managers want to remain in

control of their companies because they obtain private benefit over the financial return

on their investment. They need to forgo some growth opportunities if the

opportunities are too extensive to be realized and rely more on debt. The growth of

small firms is more sensitive to internal finance than that of larger firms. Small firms

are more likely to face financial constraints; this prevents them to gain access to

finances from banks. These firms are prepared to pay higher interest rates for

additional loans and thus fail to consider issuing external equity in order to stay in

control (Lin, Ma and Xuan, 2011).

2.3.2 Management Efficiency

According to Khanna (2000) management efficiency is one of the key internal factors

that determine the financial performance of a firm. It is represented by different

financial ratios like total asset growth, loan growth rate and earnings growth rate.

Moreover, operational efficiency in managing the operating expenses is another

dimension for management quality.

Kumar (2001) contend that the performance of management is often expressed

qualitatively through subjective evaluation of management systems, organizational

discipline, control systems and quality of staff. Some financial ratios of the financial

16

statements act as a proxy for management efficiency. Management efficiency will be

measured using asset management ratios for example inventory turnover ratios which

is measured using net sales divided by inventory.

According to Kumar (2001) the capability of the management to deploy its resources

efficiently, income maximization, reducing operating costs can be measured by

financial ratios. One of these ratios used to measure management quality is operating

profit to income ratio. The higher the operating profits to total income the more the

efficient management is in terms of operational efficiency and income generation.

Keister (2001) explains that the other important ratio is expense to asset ratio. The

ratio of operating expenses to total asset is expected to be negatively associated with

profitability. Management quality in this regard, determines the level of operating

expenses and in turn affects profitability.

2.3.3 Use of Leverage

Khanna (2000) notes that leverage of the firm is a determinant of financial

performance of the firm. The firms leverage decisions centers on the allocation

between debt and equity on financing a firm. Leverage affects the level and variability

of the firm's after tax earnings and hence, the firm's overall risk and return. The study

of leverage is significant due to the following reasons: operating risk refers to the risk

of the firm not being able to cover its fixed operating costs. Since operating leverage

depends on fixed operating costs, larger fixed operating costs indicates higher degree

of operating leverage and thus, higher operating risk of the firm. High operating

leverage is good when sales are rising but risky when the sales are falling.

Kumar (2001) puts forward that total assets and sale turnover are commonly used as a

substitute for the size of the firm. Larger firms not only enjoy a higher turnover and

17

but also generate higher income. This is because they have better access to capital

markets and lower cost of borrowing. Large firms are more likely to manage their

working capitals more efficiently than small firms. Most large firms enjoy economies

of scale and thus they are able to minimize their costs and improve on the profitability

of the firm.

2.3.4 Corporate Diversification

Doaei, Anuar and Hamid (2012) argue that corporate diversification is a technique

that reduces risk by allocating investments among various financial instruments,

industries and other categories. It aims to maximize return by investing in different

areas that would each react differently to the same event. There are two primary types

of corporate diversification: related or unrelated. If the company consists of an

overarching structure that supports all of its different businesses, then it is engaging in

related diversification. When a company consists of a series of individual businesses

that do not share things such as customers and distribution channels then it has

unrelated diversification.

According to Daud, Salamudin and Ahmad (2009) the process of corporate

diversification often involves expanding the offerings of a business by entering a new

market. A company may do this because it is nearing market saturation with its

current product line. It may also diversify because public demand for its primary

product has declined.

Some companies will undergo product diversification solely to expand the business.

This process may also be called product diversification. Corporate diversification that

takes place in different locations is also referred to as geographic market

diversification. This is when the company is only expanding locations. It does not

18

involve the service or product the company offers. This kind of diversification is often

used for the growth of a thriving business, and particularly when the company reaches

local market saturation (Dennis et al., 2002).

2.3.5 Growth of the Firm

As the firms grow, their requirement of finance tends to increase. The capacity to

finance the increasing demand depends on internal finance. According to Robert and

Barro (2002) if a firm entirely relies on internal fund, then the growth may be

restricted. Managers may forgo some profitable projects. If a firm goes for external

finance, then chances of risk increases. Levine and Robert (2001) argue that firms

with growth potential will tend to have less capital structure.

Growth opportunities can produce moral hazard effects and push firms to take more

risk. In order to mitigate this problem, growth opportunities should be financed with

equity instead of debt. Levine and Robert (2001) indicated that a negative relationship

exists between debt and growth opportunities. Financing of firms using debt may

inhibit growth and expansion of business due to high interests involved in serving the

loan. The firm might end up using all its resources in financing the loan in the short-

term and thus negatively affect the long term objectives of the firm.

2.3.6 Product Diversification

Qian and Qian (2008) posit that a product diversification strategy is a form of

business development. Small businesses that implement the strategy can diversify

their product range by modifying existing products or adding new products to the

range. The strategy provides opportunities to grow the business by increasing sales to

existing customers or entering new markets.

19

Product diversification is the process of expanding business opportunities through

additional market potential of an existing product. Diversification may be achieved by

entering into additional markets and pricing strategies. Often the product may be

improved, altered or changed, or new marketing activities are developed. The

planning process includes market research, product adaptation analysis and legal

review (Delios and Beamish, 1999).

As observed by Siggelkow (2003) intra-industry product diversification may

positively affect firm performance with additional demands created by providing

assortments that maintain more options and reduce customers’ shopping costs. He

also found that the degree of product concentration positively relates to profitability.

It offers an option for customer to choose from among the products offered. This

minimizes the risks of stock out costs since customers have can have substitute

products. This contributes to improved sales and profitability of the firm.

2.4 Empirical Review

Ongalo (2014) tested the relationship between unrelated diversification and corporate

liquidity of 61 firms listed at NSE. He adopted a descriptive research design to show

the relationship between the variables using secondary data for five years. The data

was analyzed using a regression model and the results of the analysis showed that

there was an inverse relationship between diversification and corporate liquidity of

listed firms at NSE.

Arasa (2014) studied the effect of the diversification strategy on the performance of

Kenya Commercial Bank group. Both primary and secondary data were collected by

the researcher. Primary data was successfully collected from five senior managers of

the bank, whereas secondary data was collected from the audited financial reports of

20

Kenya Commercial Bank group limited. The study took the form of a case study of

KCB group. Trend and content analysis were used to establish the effect of

diversification on performance. The findings revealed that Kenya Commercial Bank

group has adopted three main diversification strategies. It was concluded that as the

income from diversification increases, the total profits of the banks also registered

significant increment.

Maina (2013) determined the relationship between diversification of products and

services and financial performance of Deposit Taking Microfinance institutions. The

population of the study involved all the nine deposit taking microfinance institutions

in Kenya. The study used descriptive research design; secondary data for five years

was used since the nature of the study was quantitative in nature. The data was

analyzed using a multiple regression model and the results of the analysis concluded

that there was a positive relationship between diversification of products and services

and financial performance of deposit taking microfinance institutions.

Maina (2013) established the level of income source diversification of the 43 licensed

commercial banks in Kenya”. The study used a descriptive research design to test the

association between the variables. Secondary data for five years was used and the data

was analyzed using a multiple regression model. The findings revealed that product

diversification among Kenyan commercial banks exhibited a positive relationship

with performance.

Karanja (2013) did a study on the diversification strategy and the performance of

Kenolkobil limited in Kenya. The study was done using a case study design and the

object of the case study was KenolKobil Ltd. Data was collected from both primary

and secondary sources. The primary source was an interview with senior management

21

and secondary source was obtained from published information on Kenol Kobil. The

data was analyzed using content analysis and discussed to determine the

diversification strategy adopted by Kenol Kobil and its performance. The findings

were summarized and presented in this research project. It has been established that

the firm adopted related, unrelated and multinational diversification strategies. The

study also established that this diversification has increased the sales, net profits and

shareholder equity of Kenol Kobil.

Chen and Yu (2011) examined the relationship between corporate diversification and

financial performance 98 firms listed on the Taiwan Stock Exchange. An exploratory

study was used to establish the relationship between the variables. Secondary data

was used from 2001 to 2005. A multiple regression model was adopted for data

analysis and the results of the analysis showed a positive relationship between

corporate diversification and financial performance of the listed firms. It was further

concluded that firms that engaged in unrelated diversification outperformed those that

engaged in related diversification.

Daud, Salamudin and Ahmad (2009) examined diversification and performance of 70

Malaysian firms using secondary data from years 1999 to 2003. The study adopted a

descriptive design to show the association between the variables. The study used a

regression model for data analysis: the independent variable was number of

diversified segments, the dependent variables were ROA and market measure and the

control variables were risk, size, inflation and leverage. The results showed that there

was a positive relationship between corporate diversification and financial

performance of firms.

22

Bammer et al. (2006) investigated between corporate social performance and

geographical diversification on a sample of large UK firms. The sample size consisted

of 50 UK firms from commercial and services sector. An explorative survey was used

to test the relationship between the variables, the results of the study found a positive

correlation between diversification and performance in UK firms.

A study by Jung and Chan-Olmsted (2005) found out a positive relation between

related product and international diversification and financial performance among 100

media firms in United States. The study used a longitudinal study. Secondary data for

10 years was used and a multiple regression model was used for analysis. It was

concluded that the more related product and international diversification, the more the

financial performance.

Caper and Kotabe (2003) conducted a study on the effects of diversification on

financial performance on German firms in the service industry. A descriptive research

design was used and the used random effect model (REM) for generalized least

squares (GLS) estimation model. Secondary data was used from 2001 to 2005 and

analysis was done using a multiple regression model. The results of the study

concluded that there was a positive relationship between a curvilinear relationship

between multinationality and performance in German service firms.

23

2.5 Summary of the Literature Review

From the literature review, the empirical studies and theories show a positive

relationship between diversification and financial performance of firms locally and

internationally. This has been supported by a number of studies: (Chen and Yu, 2011)

and (Daud, Salamudin and Ahmad, 2009). Local studies by Maina (2012) and Maina

(2013) also established that diversification of products and services led to financial

performance in the finance sector in Kenya.

With reference to the above theories: (portfolio diversification model of alliances,

capital asset pricing model and resource-based theory and corporate diversification),

firms diversify their businesses to mitigate the level of risks and boost performance.

This is consistent with both global and local empirical studies: Daud et al., (2009),

Bammer et al., (2006), Arasa (2014) and Maina (2013). This is also coherent with the

hypothesis of this study which predicts a positive relationship between corporate

diversification and financial performance of listed manufacturing firms in Kenya.

From the above review, these studies have not investigated the relationship between

corporate diversification and financial performance of manufacturing firms in Kenya.

Therefore this study seeks to fill this gap by seeking an answer to the following

research question: what is the effect of corporate diversification on financial

performance of listed manufacturing firms in Kenya?

24

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter discusses the methodology that was used for this study. It gives a plan on

how data was collected, the tools and instruments that was used as well as how data

was analyzed.

3.2 Research Design

This study used a descriptive survey. This is because descriptive studies are

conducted to demonstrate associations or relationships between two variables.

According to Mitchell and Jolley (2013) descriptive research is used to obtain

information concerning the current status of the phenomena to describe what exists

with respect to variables or conditions in a situation. The methods involved ranged

from the survey which describes the status quo, the correlation study which

investigates the relationship between variables, to developmental studies which seek

to determine changes over time.

3.3 Population

The population of the study consisted of all the 19 listed manufacturing firms in

Kenya. Kothari (2004) defines a population as a well-defined collection of individuals

or objects known to have similar characteristics. All individuals or objects within a

certain population usually have a common, binding characteristic or trait. With

reference to the Kenya Association of Manufacturers (KAM, 2014) there are 19

manufacturing firms licensed to work and operates in Kenya. A census approach was

used.

25

3.4 Data Collection

The study used secondary data since the nature is quantitative. Data collection is

gathering empirical evidence in order to gain new insights about a situation and

answer questions that prompt undertaking of the research (Kothari, 2004). The

secondary data was collected from consolidated financial statements. Nairobi

Securities Exchange hand books of years 2013-2014 and 2014-2015 were used.

Secondary data for five years (2010-2014) was gathered from financial statements and

records for analysis. The study utilized 75 data points (observations) that were

obtained by multiplying the period of five years with 15 listed manufacturing firms in

Kenya. This period was sufficient for determining the extent to which corporate

diversification affects financial performance of listed manufacturing firms in Kenya.

3.5 Data Analysis

According to Mugenda and Mugenda (2005) data collected should be cleaned, sorted,

coded and analyzed in order to obtain a meaningful report. The data collected was

cleaned, sorted and coded and organized before capturing it in Statistical Packages for

Social Sciences (SPSS) for analysis. The main variables in the study were financial

performance which was the dependent variable; it was measured using net income

divided by total assets. Corporate diversification was measured using diversification

index. This was achieved through adopting Herfindahi Hirschmann Index (HHI)

advanced by (Maina, 2013) as indicated below.

3.6 Analytical Model

To achieve the objective of this study, the researcher used a multiple regression model

to determine the effect of corporate diversification on financial performance of listed

manufacturing firms in Kenya.

26

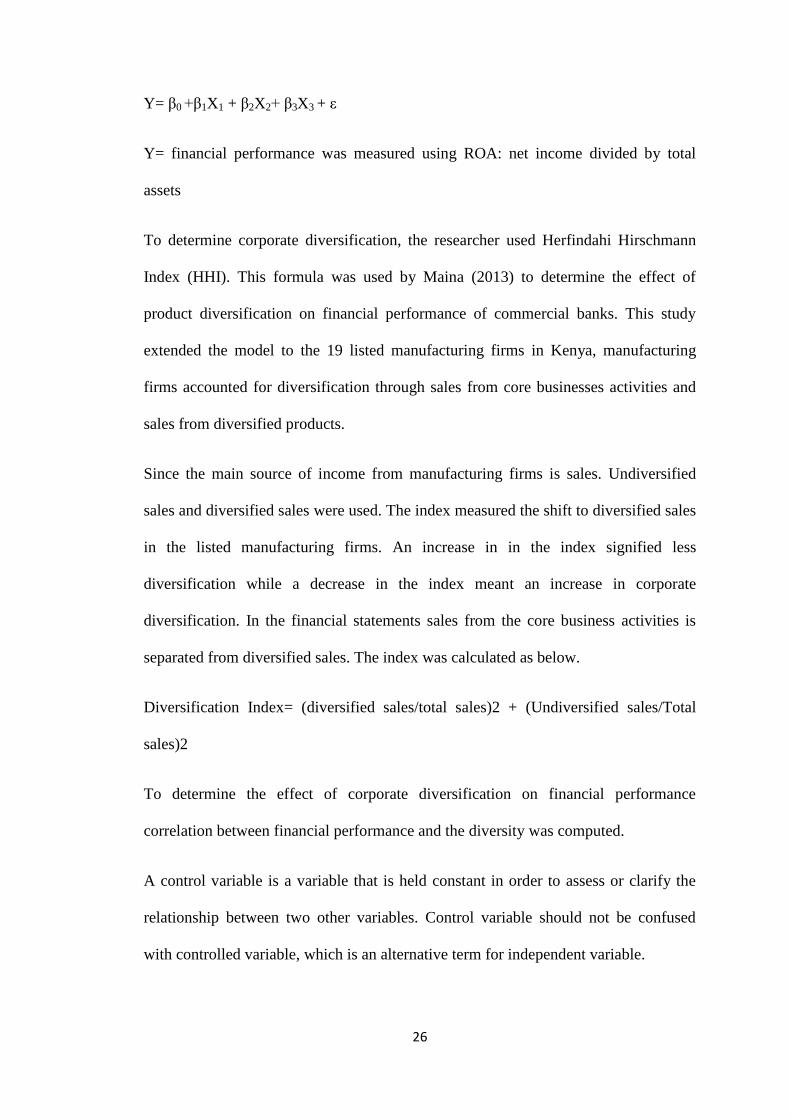

Y= β0 +β1X1 + β2X2+ β3X3 + ε

Y= financial performance was measured using ROA: net income divided by total

assets

To determine corporate diversification, the researcher used Herfindahi Hirschmann

Index (HHI). This formula was used by Maina (2013) to determine the effect of

product diversification on financial performance of commercial banks. This study

extended the model to the 19 listed manufacturing firms in Kenya, manufacturing

firms accounted for diversification through sales from core businesses activities and

sales from diversified products.

Since the main source of income from manufacturing firms is sales. Undiversified

sales and diversified sales were used. The index measured the shift to diversified sales

in the listed manufacturing firms. An increase in in the index signified less

diversification while a decrease in the index meant an increase in corporate

diversification. In the financial statements sales from the core business activities is

separated from diversified sales. The index was calculated as below.

Diversification Index= (diversified sales/total sales)2 + (Undiversified sales/Total

sales)2

To determine the effect of corporate diversification on financial performance

correlation between financial performance and the diversity was computed.

A control variable is a variable that is held constant in order to assess or clarify the

relationship between two other variables. Control variable should not be confused

with controlled variable, which is an alternative term for independent variable.

27

X2 = Size of the firm was measured using natural logarithm of total assets (fixed

assets plus current assets).

X3= Growth of the firm was measured using net assets. This was computed using total

assets minus total liabilities.

b= Slope of the regression, it was used to measure the unit change in Y linked with a

unit change in X

ε =is the error term within a confidence interval of 5%

3.6.1 Tests of Significance

From the empirical evidence and the theories, it is evident that there existed a positive

relationship between corporate diversification and financial performance. Therefore,

the alternative hypothesis was assumed that there existed a relationship between

corporate diversification and financial performance of listed manufacturing firms in

Kenya. The study considered a one-tail test, if the p-value was less than 5% then the

alternative hypothesis was true since this meant that there was a positive relationship

between the variables and the opposite was true. The tests were performed at 95%

degree of confidence.

28

CHAPTER FOUR

DATA ANALYSIS, RESULTS AND DISCUSSION

4.1 Introduction

This chapter consists of data analysis and findings as provided in the research

objective and research methodology. The results are presented in tables. The study

used secondary data that was obtained from financial statements of listed

manufacturing firms in Nairobi Securities Exchange. The study sought to collect data

from 19 listed manufacturing firms at the Nairobi Securities Exchange.

The researcher managed to collect secondary data from all the 19 listed manufacturing

firms in a period of five years between 2010 – 2014 (See Appendix, II and III). With

the help of: Herfindahi Hirschmann Index (HHI) product diversification was based on

split up sales of listed manufacturing companies under the following categories single

business (SB), dominant business (DB), related business (RB) and unrelated business

(UB).

4.2 Response Rate

The researcher managed to collect secondary data from 15 listed manufacturing

companies. This represents an estimated 80% response rate which was considered

sufficient for making generalization on all the listed manufacturing firms in Kenya.

4.3 Descriptive Statistics

Descriptive statistics was used to show the summary of the analyzed data on the

relationship between corporate diversification and financial performance of listed

manufacturing firms in Kenya. The results are presented in table 4.1 below:

29

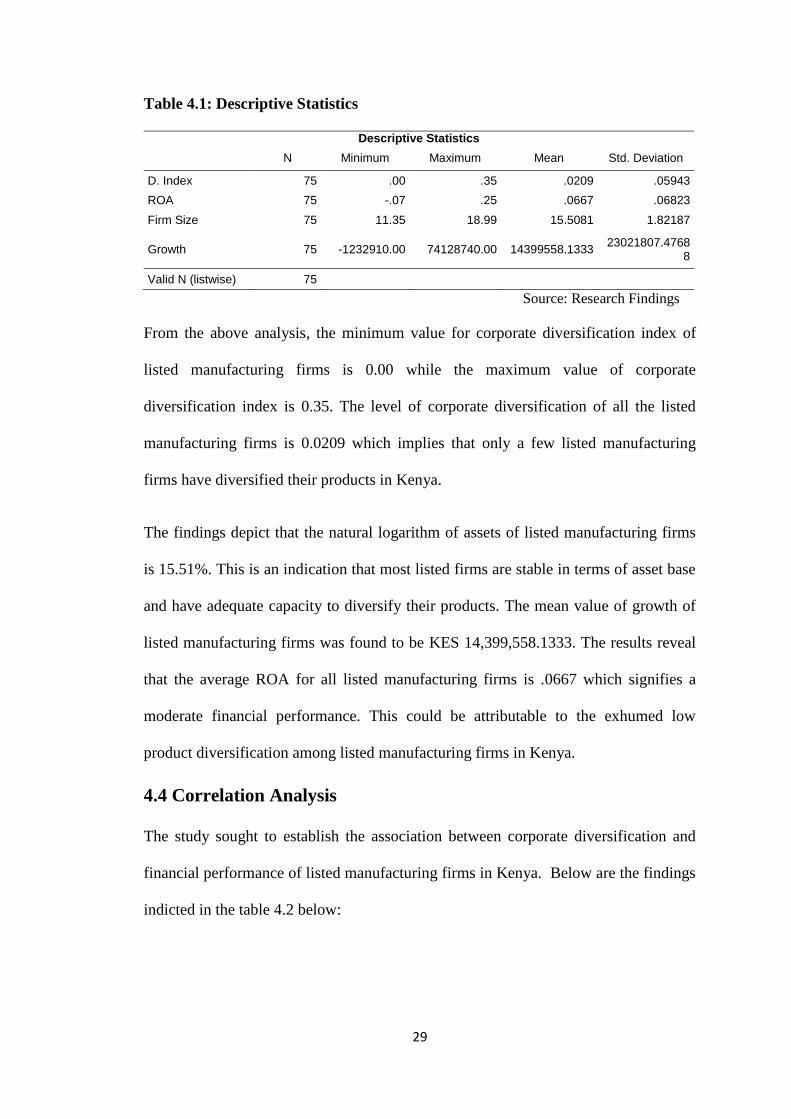

Table 4.1: Descriptive Statistics

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

D. Index 75 .00 .35 .0209 .05943

ROA 75 -.07 .25 .0667 .06823

Firm Size 75 11.35 18.99 15.5081 1.82187

Growth 75 -1232910.00 74128740.00 14399558.1333 23021807.4768

8

Valid N (listwise) 75

Source: Research Findings

From the above analysis, the minimum value for corporate diversification index of

listed manufacturing firms is 0.00 while the maximum value of corporate

diversification index is 0.35. The level of corporate diversification of all the listed

manufacturing firms is 0.0209 which implies that only a few listed manufacturing

firms have diversified their products in Kenya.

The findings depict that the natural logarithm of assets of listed manufacturing firms

is 15.51%. This is an indication that most listed firms are stable in terms of asset base

and have adequate capacity to diversify their products. The mean value of growth of

listed manufacturing firms was found to be KES 14,399,558.1333. The results reveal

that the average ROA for all listed manufacturing firms is .0667 which signifies a

moderate financial performance. This could be attributable to the exhumed low

product diversification among listed manufacturing firms in Kenya.

4.4 Correlation Analysis

The study sought to establish the association between corporate diversification and

financial performance of listed manufacturing firms in Kenya. Below are the findings

indicted in the table 4.2 below:

30

Table 4.2: Correlation between the Study Variables

ROA Diversification

index

Firm Size Growth

ROA 1

Diversification

index

.366 1

Firm Size -.354 -.109 1

Growth -.239 -.048 .917 1

Source: Research Findings

The strength of the association between the variables was propounded by Pearson

correlation scale where the values between 0.0 to 0.3 indicate that there is no

correlation regardless of the sign, between 0.31 to 0.5 shows a weak correlation,

between 0.51 to 0.7 a moderate correlation and between 0.71 to 1.0 indicates that

there is a strong correlation between the variables. This type of inference has also

been applied by other previous works such as Jayakumar (2002).

From the above findings, the study found a weak positive correlation between

corporate diversification and financial performance of listed manufacturing firm as

follows R=0.366. Similarly, there was a weak positive relationship between firm size

and financial performance of listed manufacturing firms. The correlation was found to

be R=-.354. Further there was no correlation between growth of the firm and financial

performance of manufacturing firms. The result was as follows R=-.239.

4.5 Regression Analysis and Hypothesis Testing

Regression analysis was used to determine the extent to which the independent

variables contributed to the dependent variable. A linear regression model was used

and the results are presented in the table 4.3 below.

31

Table 4.3: Model Summary

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the Estimate

1 .513a .264 .233 .05978

a. Predictors: (Constant), Firm Size, D. Index, Growth

source: research findings

From the above findings, R represents multiple correlation which shows that there is a

moderate correlation between the variables as follows R=.513. The coefficient of

determination which is represented by R 2 is 26.4%. This shows that the extent to

which the variance in the dependent variable which is financial performance can be

explained by the independent variables. This means that the model is partially a

reliable predictor.

4.5.1 Analysis of Variance

To test the goodness of fit for the analysis, a regression model was used for this

purpose and the results are provided in the table 4.4 below.

Table 4.4: Analysis of Variance

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression .091 3 .030 8.473 .000b

Residual .254 71 .004

Total .345 74

a. Dependent Variable: ROA

b. Predictors: (Constant), Firm Size, D. Index, Growth source: research findings

From the above findings, the p-value of 0.000 is a clear indication that the regression

model is statistically significant in predicting the relationship between corporate

diversification and financial performance of manufacturing firms.

32

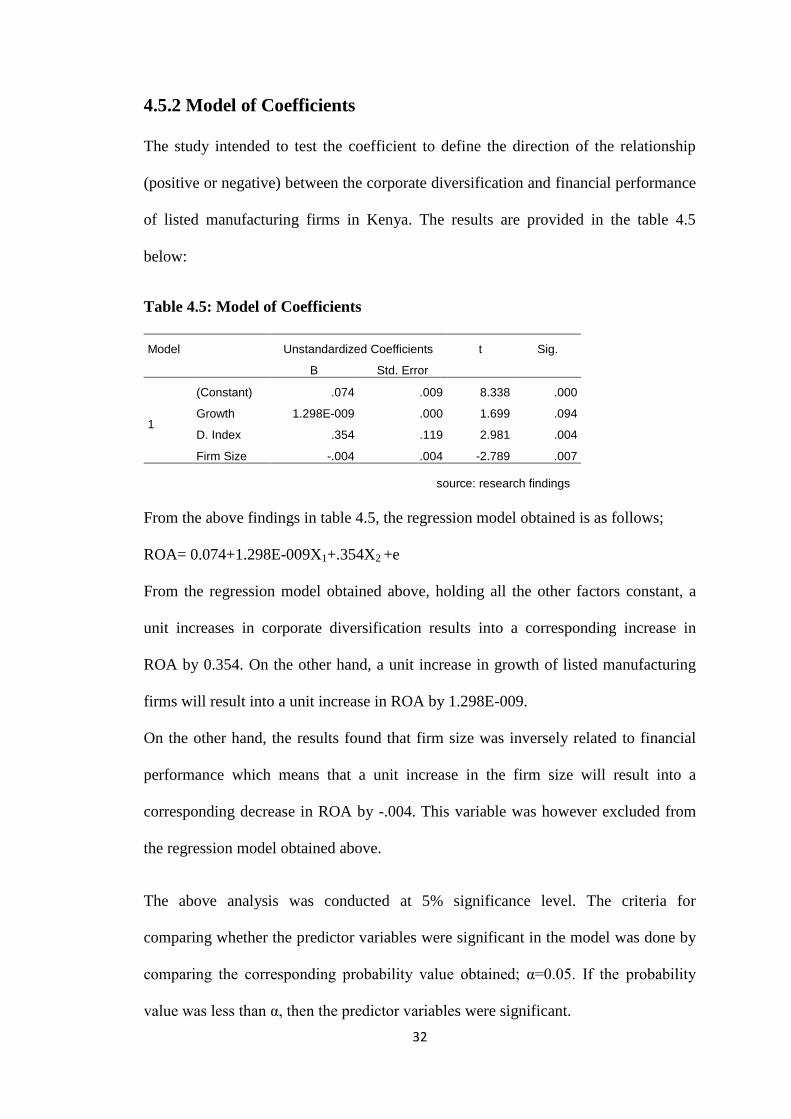

4.5.2 Model of Coefficients

The study intended to test the coefficient to define the direction of the relationship

(positive or negative) between the corporate diversification and financial performance

of listed manufacturing firms in Kenya. The results are provided in the table 4.5

below:

Table 4.5: Model of Coefficients

Model Unstandardized Coefficients t Sig.

B Std. Error

1

(Constant) .074 .009 8.338 .000

Growth 1.298E-009 .000 1.699 .094

D. Index .354 .119 2.981 .004

Firm Size -.004 .004 -2.789 .007

source: research findings

From the above findings in table 4.5, the regression model obtained is as follows;

ROA= 0.074+1.298E-009X1+.354X2 +e

From the regression model obtained above, holding all the other factors constant, a

unit increases in corporate diversification results into a corresponding increase in

ROA by 0.354. On the other hand, a unit increase in growth of listed manufacturing

firms will result into a unit increase in ROA by 1.298E-009.

On the other hand, the results found that firm size was inversely related to financial

performance which means that a unit increase in the firm size will result into a

corresponding decrease in ROA by -.004. This variable was however excluded from

the regression model obtained above.

The above analysis was conducted at 5% significance level. The criteria for

comparing whether the predictor variables were significant in the model was done by

comparing the corresponding probability value obtained; α=0.05. If the probability

value was less than α, then the predictor variables were significant.

33

From the model of coefficients, corporate diversification and firm size were found to

be statistically significant in the model. This is because their probability values were

lower than 5%. The results were as follows p=0.004 and P=0.007 respectively. These

findings are consistent with the hypothesis of the study which predicts a positive

relationship between corporate diversification and financial performance of listed

manufacturing firms in Kenya.

Further, it was observed that growth of listed manufacturing firms was statistically

insignificant this is because its probability value was more than 5%, p=0.094. These

findings contradict with the hypothesis of this study which predicted a statistically

significant relationship between corporate diversification and financial performance

of listed manufacturing firms in Kenya.

4.6 Discussion of Research Findings

From the above findings, descriptive results reveal that a few listed manufacturing

firms have diversified their products in the Kenyan market. This was proved by the

mean value of corporate diversification index which was 0.0209.

The correlation results found that there a moderate correlation between corporate

diversification and financial performance of listed manufacturing firms. These

findings are consistent to the findings by Daud, Salamudin and Ahmad (2009) who

found that there was a positive and moderate relationship between corporate

diversification and financial performance of Malaysian firms.

The regression results in table 4.5 above have concluded that there exists a positive

relationship between corporate diversification and financial performance of listed

manufacturing firms in Kenya. These findings are consistent with the findings by

34

Maina (2013), who examined the relationship between diversification of products and

services and financial performance of Deposit Taking Microfinance institutions. The

results concluded that there was a positive relationship between diversification of

products and services and financial performance of deposit taking microfinance

institutions. These findings are also supported by Maina (2013) who did a study on

the relationship between product diversification and financial performance of

commercial banks in Kenya; he found that there was positive relationship between

product diversification and financial performance of commercial banks in Kenya.

35

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 Introduction

This chapter gives the results and discussions drawn from the analysis presented in

chapter four. The chapter is structured into summary of findings, conclusions,

limitations, recommendations and areas for further research.

5.2 Summary of Findings

The analysis has been done in line with the objective of the study which was to

establish the relationship between corporate diversification and financial performance

of listed manufacturing firms in Kenya. From the descriptive results, it was found that

a few listed manufacturing firms had diversified their products. The mean value of

listed manufacturing firms that had diversified their products was 0.0209. This mean

value shows that the level of corporate diversification is moderate. The findings

revealed that the average size of listed manufacturing firms was 15.51%. This was an

indication that most listed manufacturing firms are stable in terms of asset base and

had adequate capacity to diversify their products and mitigate risks. The financial

performance of listed manufacturing firms was found to 6.7% which is a moderate

performance.

The results found that that there was a weak positive correlation between corporate

diversification and financial performance of listed manufacturing firm as follows

R=0.366. These findings are consistent with a study by Bammer et al. (2006) who

found a positive correlation between diversification and performance in UK firms.

36

Firm size and financial performance was found to have a weak positive relationship

which was represented by R= -.354. There was no relationship between growth of the

firm and financial performance of manufacturing firms. The result was as follows R=-

.239. These findings conform to a study Karanja (2013) on the diversification strategy

and the performance of Kenolkobil limited in Kenya. Although he found a positive

relationship between diversification strategy and the performance of Kenolkobil

limited in Kenya, there was no statistical relationship between growth and financial

performance.

From the model of coefficients, corporate diversification was found to be statistically

significant in the model. This is because its p-value was lower than 5%. The results

were as follows p=0.004. These finding are consistent with the hypothesis of the study

which predicts a positive relationship between corporate diversification and financial

performance of listed manufacturing firms in Kenya. These findings are consistent

with Chen and Yu (2011) who found a positive relationship between corporate

diversification and financial performance of the listed firms. Further, it was observed

that firm size and growth of listed manufacturing firms were statistically insignificant.

The results obtained were as follows p=0.007 and p=0.094. These findings contradict

with the hypothesis of this study which predicted a statistically significant relationship

between corporate diversification and financial performance of listed manufacturing

firms in Kenya.

5.3 Conclusion

The results of the descriptive statistics shows that listed firms have the potential and

the capacity to diversify their products although the uptake for product

diversifications among the listed manufacturing firms is still low.

37

The correlation findings concluded that corporate diversification is weak but

positively related to financial performance of listed manufacturing firms in Kenya.

The study therefore puts more emphasis on corporate diversification to boost financial

performance of listed manufacturing firms.

The regression results conclude also concludes that that there is a statistically

significant relationship between corporate diversification and financial performance

of listed manufacturing firms in Kenya. This was proved by the probability value of

corporate diversification which was found to be less than 5%. Even though firm size

and growth variables showed an insignificant relationship with financial performance,

corporate diversification and financial performance were considered because they are

the two main variables of this study.

5.4 Recommendations

From the above findings in table 4.5, the regression results have found that firm size

and growth of the firm were statistically insignificant. This could have been as a result

of low product diversification among listed manufacturing firms. The study therefore

recommends that policy makers like capital markets authority to promote policies that

encourage listed firms to practice product diversification to mitigate their financial

losses and boost their profitability.

From the above findings in table 4.2, the results concluded that there was a positive

moderate correlation between corporate diversification and financial performance.

The study recommends that listed manufacturing firms should increase their level of

corporate diversification to build stability other than concentrating on a single

industry or product. This will enhance their predictability about the future and thus

boost their financial strengths through making profitable investments decisions.

38

The study recommends the need for corporate diversification by most firms to offset

the risk of doing business. Through expanding, a firm is not dependent on a limited

number of products, locations, or markets in order to survive. A company may pursue

corporate diversification in reaction to a change in the market to create a buffer for

uncontrollable risks.

The study recommends that when choosing diversification strategies; firms should

look at their current customer base to determine if they can sell them different items

or if you can add new customers by selling them a similar product at a different price

or under a different name. Review your current suppliers, sales reps and distribution

partners to determine if you can use them to sell different products, reducing your

start-up costs.

5.5 Limitations of the Study

One of the limitations that the researcher faced during data collection was accessing

the secondary data from Nairobi Securities Exchange. Obtaining the values of

corporate diversification index was not easy; some listed manufacturing firms

practiced product diversification while others did not. The researcher had to look for

someone who works with NSE to assist in data collection.

The study was conducted within a limited time and scope. This forced the researcher

to study 19 listed manufacturing firms in Kenya in order to have adequate time to

produce quality research work that is more accurate. The results and the conclusion

drawn in this study cannot however; be used to make generalization of all the

manufacturing firms operating in Kenya.

The other limitation faced by the researcher was lack of adequate time to do the

project. The researcher had to work through the night to beat the deadline for defense

39

and project submission date for review by external examiners. This however was not

easy balancing school, family and employment. I had to go out of my way to create

extra time to learn and perfect my skills on APA style of writing and researching

using electronic journals.

The study utilized secondary sources of data for a period of five years (2010-2014).

This data is historical in nature and might not necessary reflect the actual needs of the

researcher this might have affected the validity and reliability of data and thus impact

negatively on the findings obtained.

The study was limited to four variables only. These variables are corporate

diversification, financial performance, firm size and growth. There are other macro-

economic variables that could affect the relationship between corporate diversification

and financial performance of listed manufacturing firms in Kenya. It is advisable for

future researchers to consider incorporating other variables and determine whether the

results are consistent.

5.6 Suggestions for Further Research

A study should be carried out on the effect of corporate diversification on the

financial performance in other lines other than product diversification. Examples

would be investments in terms of percentage of shareholding or even assets. This

would provide a wide range of parameters to investigate and establish relationships.

Areas of commonalities or unique factors can then be identified.