Embed Size (px)

DESCRIPTION

The Construction Industry and Building Schools for the Future Tuesday 16 June 2009. The Construction Industry and BSF: The challenges and opportunities in working together 16 June 2009 Graham Watts Chief Executive Construction Industry Council. Education and Employment. - PowerPoint PPT Presentation

Citation preview

The Construction Industry and Building Schools for the Future

Tuesday 16 June 2009

The Construction Industry and BSF: The challenges and opportunities in

working together

16 June 2009

Graham Watts Chief Executive

Construction Industry Council

Education and Employment

• Unemployment rate 5.6% in Q2 2008 - up from 5.5% in Q2 2007. • 12.5% for those with no qualifications. • 2.5% for those with qualifications equivalent to level 4

or above.

International Labour Office unemployment rates by highest qualification held, England, Quarter 2 2008 (Source DFCS)

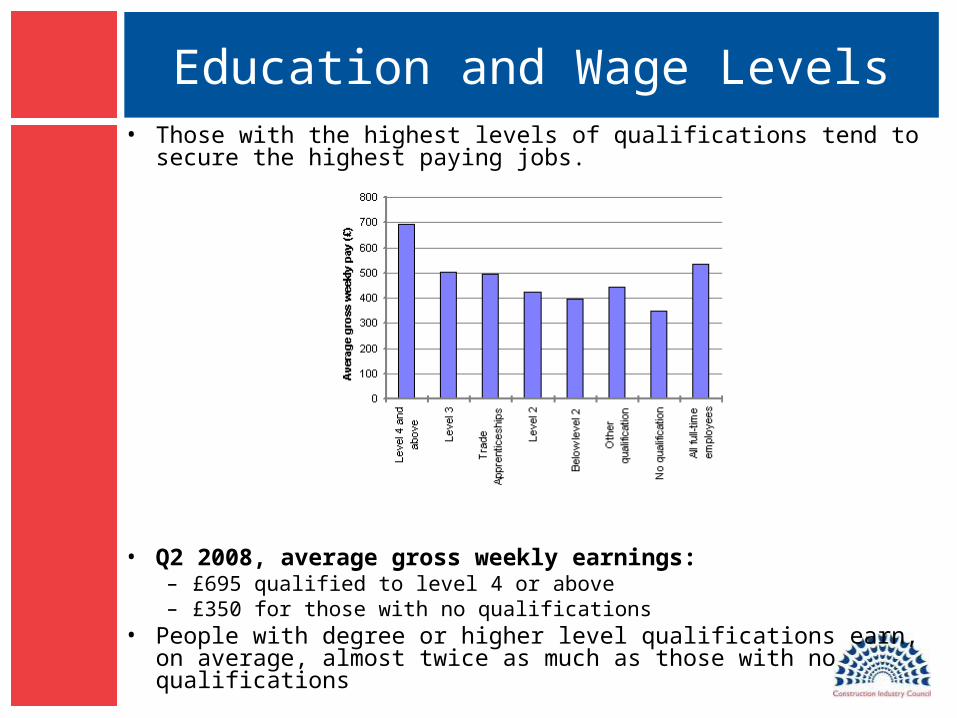

Education and Wage Levels• Those with the highest levels of qualifications tend to secure the

highest paying jobs.

• Q2 2008, average gross weekly earnings: – £695 qualified to level 4 or above – £350 for those with no qualifications

• People with degree or higher level qualifications earn, on average, almost twice as much as those with no qualifications

Pupils in mainstream schools

• 25% fall in the number of maintained nursery and primaryschool pupils: 1974 -1985

• 35% fall in the number of births: 1964 -1977• 26% fall in the number of secondary school pupils:

1979-1991

Education Spending• Birth rates and pupil numbers

are falling BUT most spending on education in 50 years– BSF covers 3,500

secondary schools in England

– Affects 3.3 million pupils in England

– Capital spend of £9.3 billion over the next three years

• Unprecedented opportunity to contribute to:– a lasting legacy, – investment in UK plc.

Trends affecting school use and design

Economic Trends:• From a production based economy to a service (and knowledge)

based economy.

Social Trends:• Children in western societies are increasingly denied access to

outdoors.• Reduction in contact with adults and other children. • Loss of informal experience and learning.• Schools become increasingly important for social interaction.

Technological Trends:• The traditional design of schools is being transformed into

specialised teaching spaces.

Positive impact of good school building

Educational challenges

• Meeting targets in relation to:– Literacy,

– Numeracy,

– ICT;

• Encouraging under-performing groups, particularly young boys;• Encouraging those over 16 to remain at school; • Combating low attainment levels in relation to GCSEs;• Coping with pupil diversity and catering for specialisms.

Positive impact of good school building

Design challenges

• Scale and proportion of the building• Functional and efficient layout• Build quality and durability• Accessibility• Energy use• Acoustics• Flexibility and adaptability• Sustainability

Evaluating Design Quality• Evaluating design quality is vital and this

is the reason why CIC has developed the Design Quality Indicator.

• Developed in 1999 at the time of Sir John Egan’s review.

• DQI measures the quality and effectiveness of the built product.

• It is used on many types of projects across the UK and in the USA

• DQI is being used on every BSF project

Interior street and library, Frederick Bremer School, Waltham Forest, BSF

Project

Evaluating Design Quality• Measurement is one of the key

reasons DQI was developed.

• Actively engages people in the design, construction and refurbishment of buildings.

• DQI can be used at all stages of a building’s development and plays a fundamental role in contributing to the improved quality of school buildings.

• Accessibility is one of the key features of DQI and helps demystify the design process.

Playgrounds, Frederick Bremer School, Waltham Forest, BSF Project

Evaluating Design Quality• DQI has been a great success in

the school programme, giving voice to over 1000 pupils.

• There has been a 3% increase in opinions of users about design quality of proposed schools from 2007-2008.

• In 2009 to date we have seen a further increase of 3%. (Source DQI data)

Anti-bullying toilets, Frederick Bremer School, Waltham Forest, BSF Project

Delivery

• CIC welcomes and supports the aims of BSF.However delivery is a key concern for the construction industry.

• BSF has been persistently over-optimistic in relation to delivery of the programme.

• A key issue is the complexity of the delivery chain.

BSF: Roles of the main parties

Department for Children,

Schools and Families

Develops policy and provides funding

Partnership for Schools

(PfS)

Manages programme, supports Local Authorities

and approves funding

Partnerships UK (PUK)

Helps fund and manage PfS

Local Authority

Leads local delivery and provides additional funding

Local Educations Partnership (LEP)

Joint venture to scope projects and manage

PFI project companies over 10 years

Schools

Buildings and Services

Capital funding

PFI Credits and grant

Private Sector Partner

A consortium of supply chain and finance

companies

BSFI

Joint Venture between the Department and

PUK

Delivery• Local Education Partnerships (LEPS)

– Value for money has yet to be proven.

– LEPS offers the potential to achieve procurement and partnering efficiencies if their lifetime value outweighs high upfront costs.

• If the challenge of renewing all secondary schools by 2023 is to be met there needs to be:

– A doubling of the number of schools in procurement and construction.

– 8-9 local authorities to start BSF each year.

– The construction of 250 schools a year from 2011 onwards

The Future

• The BSF programme is exciting for all concerned.

• BSF has faced some difficulties but is beginning to deliver.

• Positive signs that more lenders are providing finance for BSF schemes.

• Still questions over PFI arrangements to be resolved.

Work Streams:• Strengthening the relationship between BSF &

the industry

• The Procurement Process: can the length & complexity be improved?

• Getting into LEPS: accessibility for SMEs

![Sustainable Schools for Tuesday 18th nov.ppt [Read-Only]](https://img.pdfslide.us/doc/110x75/61fb5ccc2e268c58cd5d470b/sustainable-schools-for-tuesday-18th-novppt-read-only.jpg)