Embed Size (px)

Citation preview

The BC Economy to 2010 and Beyond

November 19, 2008West Vancouver Chamber of CommerceWest Vancouver, BC

Virginia GreenePRESIDENT and CHIEF EXECUTIVE OFFICER

Business Council of British Columbia

2

Business Council of British Columbia

• Cross-sectoral business association representing large and mid-sized firms drawn from 15+ industries with a presence in BC

• Membership of 230 organizations, mainly companies but also including several affiliated sector associations, which together = 25% of all paid jobs in BC

• Core mandate: 1) advocate for a growing and competitive economy; 2) encourage business investment and economic development

• Most work is done at the provincial level, with some attention to federal/local government issues

3

2008 – One for the Record Books!

• Global financial crisis and credit crunch

• US housing implosion

• Violent swings in oil prices – from US$70/bbl in January to $147 in July and $55 in mid November

• Start of a “world recession” likely in Q4

• Rapid fire restructuring of financial industries

• Shift from widespread fears of surging inflation in Q1 to initial worries about deflation by Q4

• Canada – commodity prices boost value of exports and now are a drag on exports

3

4

A newsflash…

5

World Real GDP Growth, PPP weighted

0

1

2

3

4

5

6

7

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06

Post 2002 Period Saw Robust Global Economic Expansion

Source: IMF, PPP=purchasing power parity.

per cent

6

Current World Situation

• Global economy is clearly losing steam

• US, Japan, Euro area and UK in recession » advanced economies as a group projected to shrink

0.3% next year (IMF)

• China, India, OPEC, and other emerging markets continue to grow but are slowing too

• Financial crisis clouds the outlook for 2009 (and 2010?)

• “Decoupling” a myth – global connections stronger than ever

6

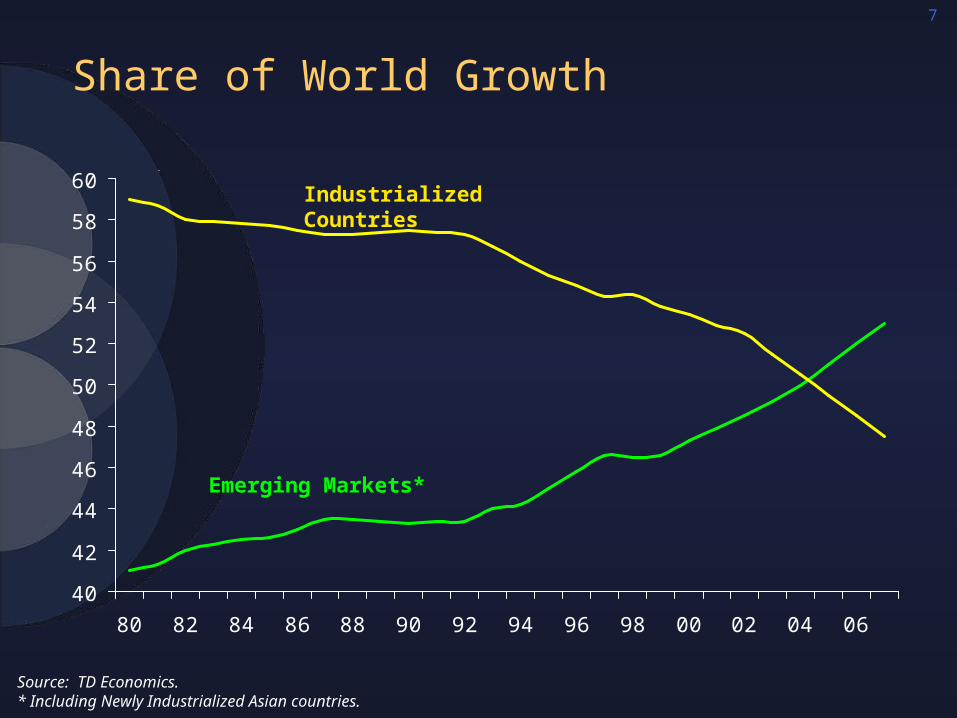

7

Share of World Growth

Source: TD Economics.* Including Newly Industrialized Asian countries.

40

42

44

46

48

50

52

54

56

58

60

80 82 84 86 88 90 92 94 96 98 00 02 04 06

per cent of total

Emerging Markets*

Industrialized Countries

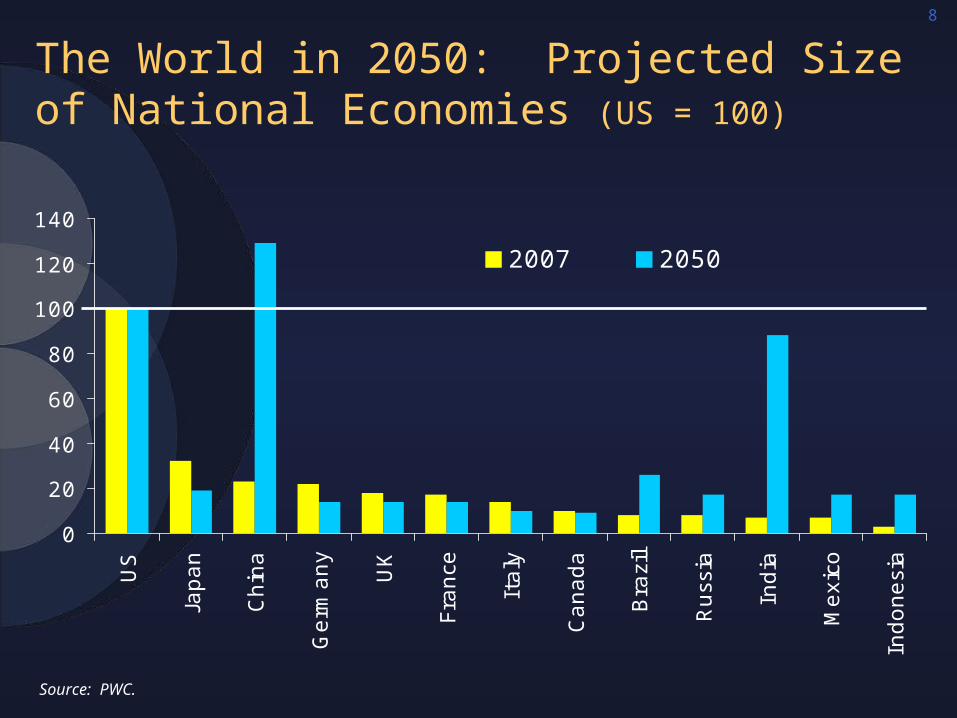

8

Source: PWC.

The World in 2050: Projected Size of National Economies (US = 100)

0

20

40

60

80

100

120

140

US

Japan

Chin

a

Germ

any

UK

France

Italy

Canada

Bra

zil

Russ

ia

India

Mexi

co

Indonesi

a

2007 2050

GDP at Market Exchange Rates in US Dollars

9

US Overview • US economy in recession

» contracted 0.3% in Q3» real personal consumption fell 3.1% » ISM Mfg. Index 38.9 in October» weak recovery in 2009 ?

• Employment falling » 9 consecutive months of job losses, employment down

year-over-year and unemployment up

• Consumer is the key to the outlook» fiscal stimulus package waning, housing bust continues to

unfold» energy and food prices hammered household budgets» financial crisis broadening

• US dollar devaluation is trimming trade deficit (boosted exports, lowering imports)

10

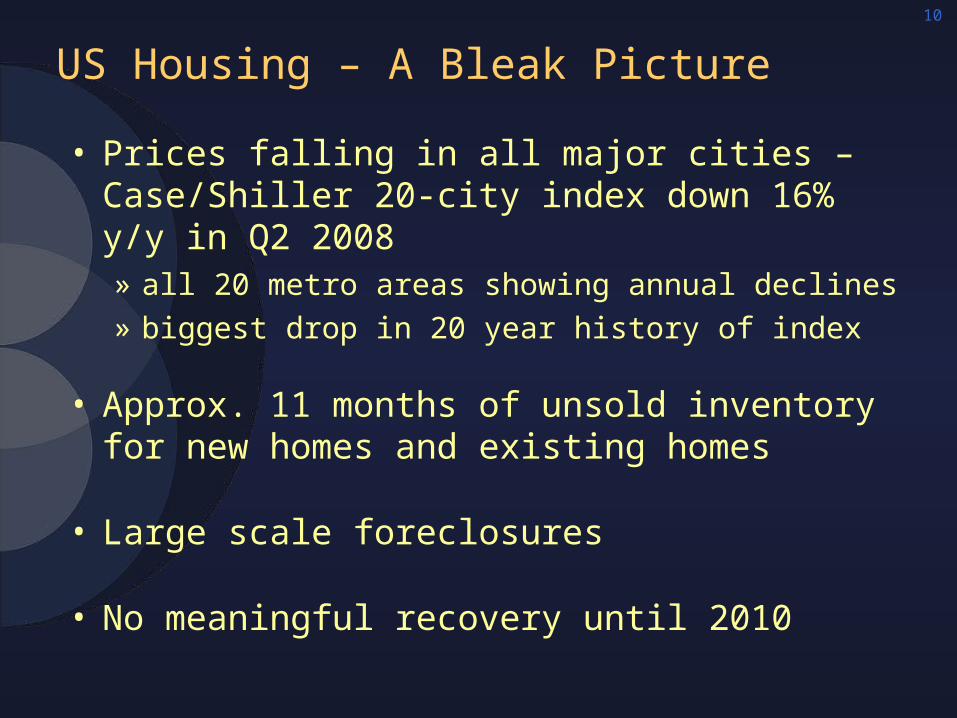

US Housing – A Bleak Picture

• Prices falling in all major cities – Case/Shiller 20-city index down 16% y/y in Q2 2008» all 20 metro areas showing annual declines» biggest drop in 20 year history of index

• Approx. 11 months of unsold inventory for new homes and existing homes

• Large scale foreclosures

• No meaningful recovery until 2010

11

US Housing Startsmonthly, S.A. annual rates

800

1000

1200

1400

1600

1800

2000

2200

2400

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

New Home Construction Tumbles

Source: US Census Bureau.

thousands

Latest September 2008

12

Global Credit Market Turmoil

• Began in Q2 2007 and is still ongoing

• Underlying causes include:

» rapid growth of securitization of debt (“originate and distribute model” at banks and investment firms)

» poor risk management

» financial innovation and complexity of products

» malfeasance by credit rating agencies

» skewed incentives for financial actors

• But perhaps the most important factor was the benign economic environment – the ‘perfect calm’: several years of strong global growth, low interest rates, subdued inflation

13

Financial Crisis – Some Consequences

• Liquidity impairment amidst mounting risk aversion, plus ongoing de-leveraging, leading to…» weaker global economy in 2009-2010» rapid-fire restructuring of financial industries

• Massive government intervention, followed by tightened regulation

• Some of the costs of the financial and the preceding sub-prime mortgage crises:» IMF: financial institutions’ losses = $1.5 trillion» US household net worth down perhaps $3 trillion (housing

plus equities)» Government bailouts/backstops in US, Japan, EU, UK –

unknown cost

• Undermines consumer confidence

14

Homeowners Net Equity as % of Household Real Estate

Source: Global Insight.

45

50

55

60

65

70

75

80

62 71 80 89 98 07

United States

Canada

%

1515

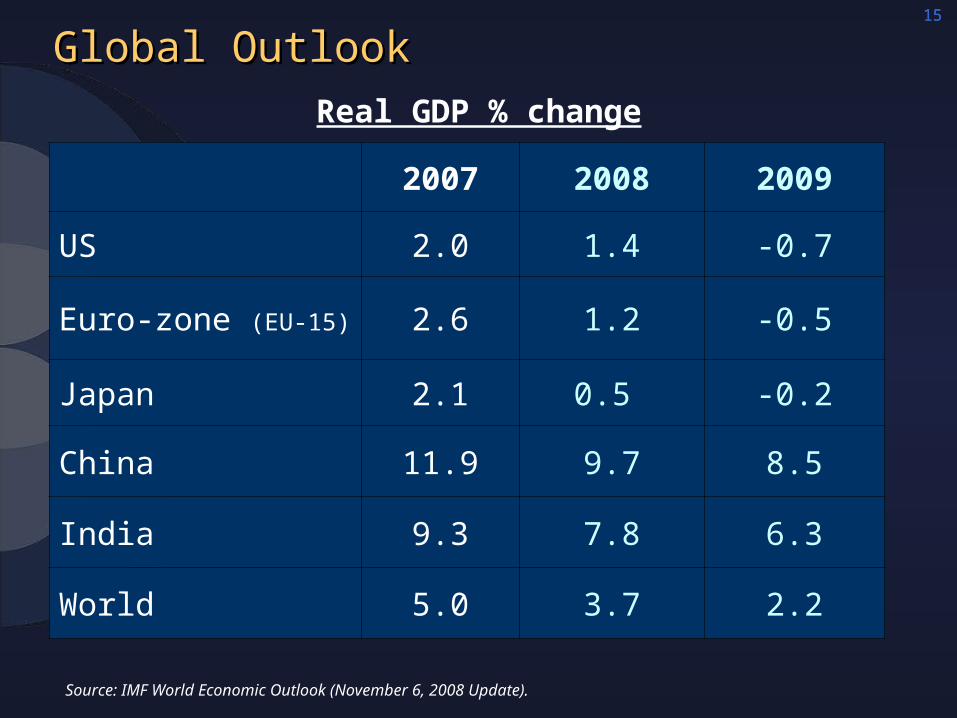

Global Outlook Global Outlook

Source: IMF World Economic Outlook (November 6, 2008 Update).

2007 2008 2009

US 2.0 1.4 -0.7

Euro-zone (EU-15) 2.6 1.2 -0.5

Japan 2.1 0.5 -0.2

China 11.9 9.7 8.5

India 9.3 7.8 6.3

World 5.0 3.7 2.2

Real GDP % change

16

Canadian Backdrop

• Economic growth is slowing and will continue to moderate in the coming quarters» recession likely» job market still relatively strong

• Manufacturing as a whole in recession for more than a year

• Dwindling trade surplus a major drag on growth

• Western provinces (BC, Alta, Sask) still doing better than the rest

• Interest rates – Bank of Canada coordinated cut Oct. 8 then trimmed another 25 bps

17

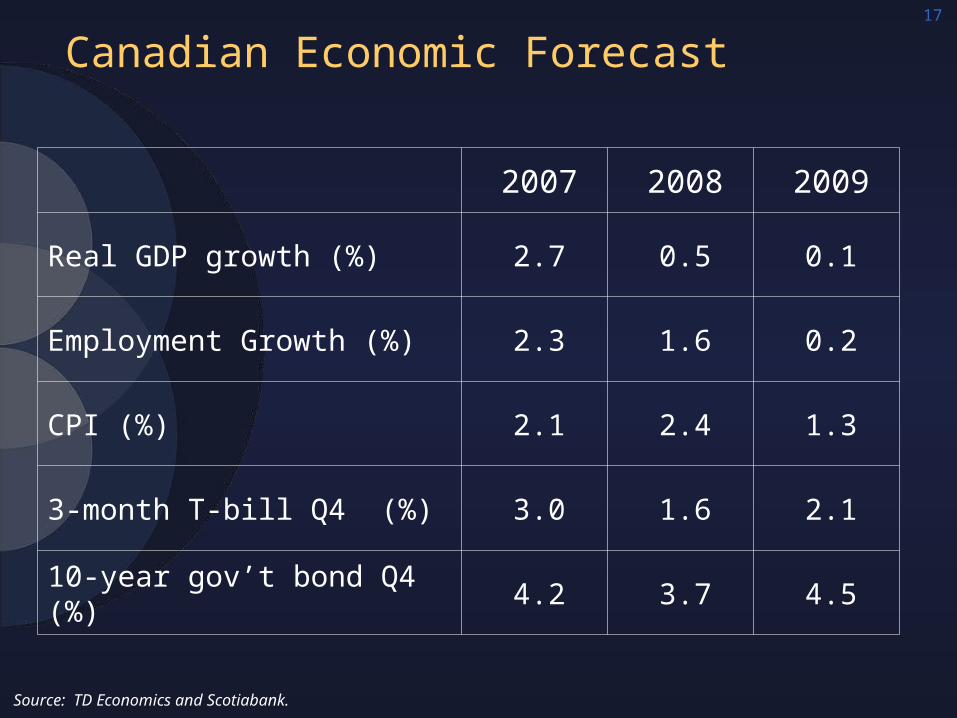

Canadian Economic Forecast

2007 2008 2009

Real GDP growth (%) 2.7 0.5 0.1

Employment Growth (%) 2.3 1.6 0.2

CPI (%) 2.1 2.4 1.3

3-month T-bill Q4 (%) 3.0 1.6 2.1

10-year gov’t bond Q4 (%) 4.2 3.7 4.5

Source: TD Economics and Scotiabank.

18

Real GDP Growth, Western Canada (aggregate)

0

1

2

3

4

5

6

7

98 99 00 01 02 03 04 05 06 07

per cent

Western Canada

Rest of Canada

Stronger Economies in the WestStronger Economies in the West

Source: Statistics Canada.

19

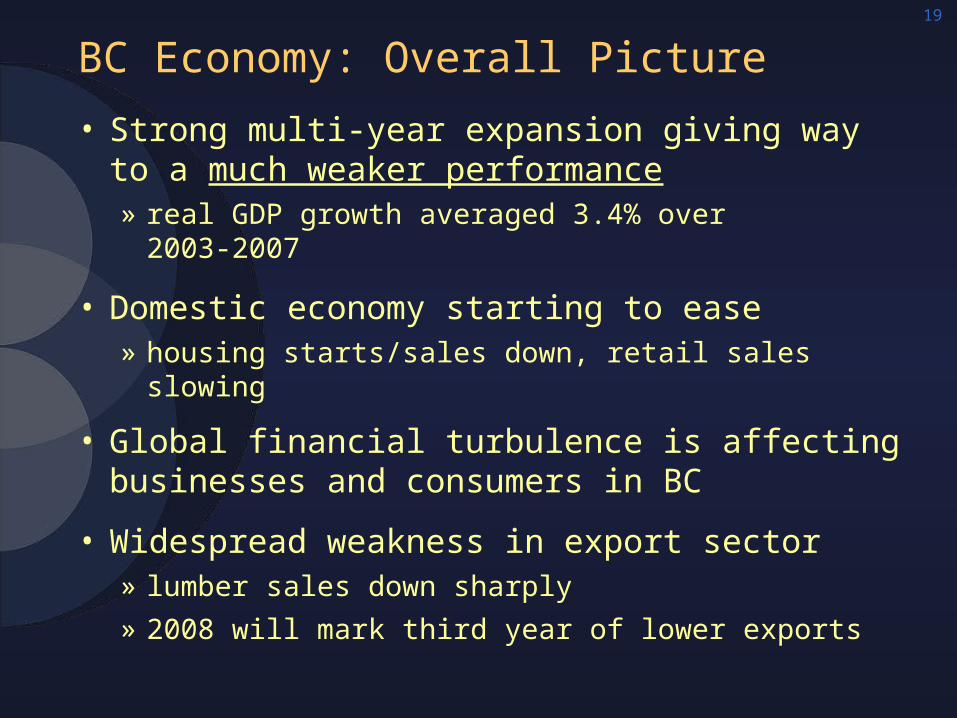

BC Economy: Overall Picture

• Strong multi-year expansion giving way to a much weaker performance » real GDP growth averaged 3.4% over

2003-2007

• Domestic economy starting to ease » housing starts/sales down, retail sales slowing

• Global financial turbulence is affecting businesses and consumers in BC

• Widespread weakness in export sector» lumber sales down sharply

» 2008 will mark third year of lower exports

20

Unemployment Rate

3

4

5

6

7

8

05 06 07 08

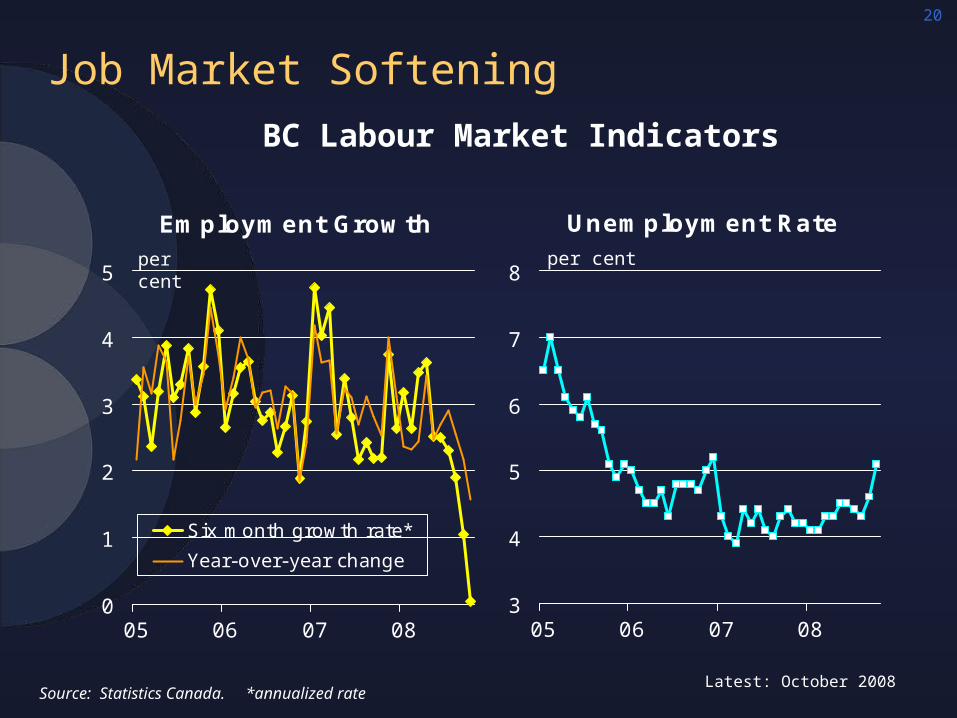

Job Market Softening

Employment Growth

0

1

2

3

4

5

05 06 07 08

Six month growth rate*

Year-over-year change

BC Labour Market Indicators

per cent per cent

Source: Statistics Canada. *annualized rateLatest: October 2008

21

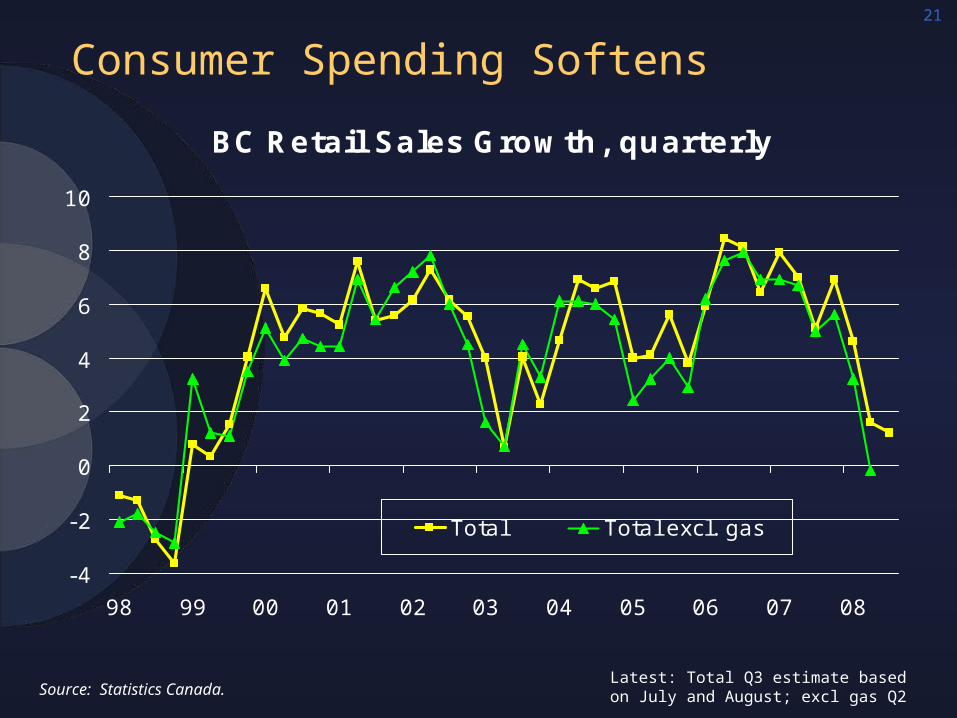

Consumer Spending Softens

BC Retail Sales Growth, quarterly

-4

-2

0

2

4

6

8

10

98 99 00 01 02 03 04 05 06 07 08

Total Total excl. gas

y/y per cent change

Latest: Total Q3 estimate based on July and August; excl gas Q2Source: Statistics Canada.

22

Softer Housing Market Dampening Retail Activity

Source: Statistics Canada.

BC Retail Sales Growth by Sector

-5

0

5

10

15

Homecentres

Furn. &home

furnishings

Appliances& electron.

Buildingmaterials& garden

stores

Autos (new &used)

Clothingstores

Total Gasstations

Avg. 2004-07

J an-J une 2008

y/y per cent change

23

Annual Change in Price of Homes Sold*

-10

-5

0

5

10

15

20

25

30

02 03 04 05 06 07 08

Housing Market Slowing

Sales & New Listings, monthly SA

1500

2500

3500

4500

5500

02 03 04 05 06 07 08

Sales Listings

Greater Vancouver Housing Indicators

units per cent

Source: CREA; * average price of all homes sold through MLS®.Latest: September 2008

24

Investment Turns Lower

BC Non-Residential I nvestment, quarterly

400

600

800

1000

1200

1400

1600

98 99 00 01 02 03 04 05 06 07 08

Current $

2002 $

millions $

Latest: Q2 2008Source: Statistics Canada.

25

BC Economic Forecast(annual % change unless noted; as of Oct 1/08)

Source: Statistics Canada and Business Council of British Columbia.

actual actual forecast

2006 2007 2008 2009 2010

Real GDP 3.3 3.1 1.6 1.0 2.8

Employment 3.1 3.2 2.3 1.2 1.9

Retail sales 6.5 7.0 3.5 3.0 7.5

Foreign exports -2.0 -5.6 -2.0 -5.0 3.0

Housing starts(units)

36,500 39,200 33,000 26,000 28,000

26

Some Progress in Closing BC’s “Prosperity Gap” with Canada

Source: Statistics Canada, Provincial Economic Accounts.

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2001 2007 2001 2007

Canada BC

Real GDP per Capita Real Disposable Income per Capita

$4,040 gap

$2,656 gap

$552 gap

$237 gap

$ 2002

27

Premier’s 10 Point Plan

• Provides some support to consumer confidence» cumulative stimulus of $485 million over the next three years,

plus accelerated infrastructure spending

• A number of items relevant to BC business» school property tax rebate for light and heavy industry ($115 m

over three years), building upon reductions in Budget 2008» tax relief for small business – tax rate cut to 2.5%, from 3.5%

starting December 1st ($146 million over three years)» double commission paid to business for PST & hotel room tax

• Individuals will see a cut in income tax - $144 million in total, retroactive benefit on 2008 tax return

• Pension “opportunity” – private sector pension plan available to employers, employees and self-employed (no details)

• Speed up infrastructure spending

28

Key BC Key BC Medium-TermMedium-Term Economic Economic Challenges Challenges

• Labour scarcity, skill shortages

• Weak export base, growing trade deficit

• Managing fallout from the pine beetle disaster

• Economic diversification (especially as forest sector declines)

• Improving BC’s poor productivity record

• Strengthening performance on innovation and research

29

Lacklustre Productivity Growth

Source: Centre for the Study of Living Standards.

Productivity Growth by Province 1987-2006

0 10 20 30 40 50

British Columbia

New Brunswick

Manitoba

Nova Scotia

Prince Edward I sland

Quebec

Ontario

Alberta

Saskatchewan

Nfld & Labrador

per cent

30

Trade More Important to BC’s Economy

BC Exports and Imports as a Share of GDP

20

40

60

80

100

1983 1988 1993 1998 2006

Exports Imports Exports + Imports

Source: Statistics Canada.

per cent

Up 26 percentage

points since 1983

31

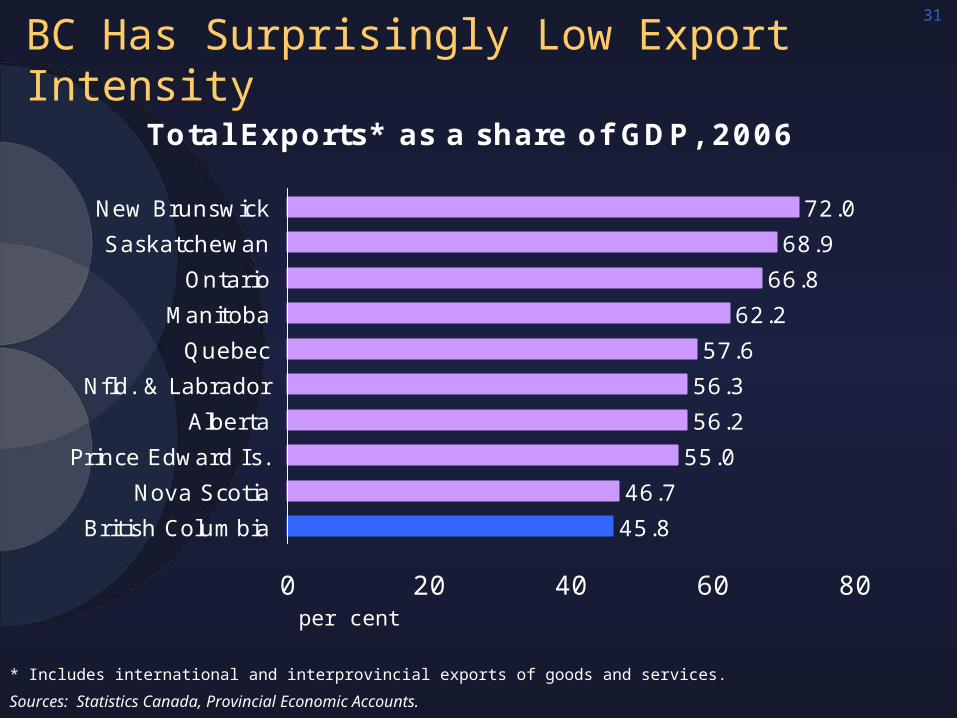

BC Has Surprisingly Low Export Intensity

Sources: Statistics Canada, Provincial Economic Accounts.

* Includes international and interprovincial exports of goods and services.

Total Exports* as a share of GDP, 2006

45.8

46.7

55.0

56.2

56.3

57.6

62.2

66.8

72.0

68.9

0 20 40 60 80

British Columbia

Nova Scotia

Prince Edward I s.

Alberta

Nfld. & Labrador

Quebec

Manitoba

Ontario

Saskatchewan

New Brunswick

per cent

32

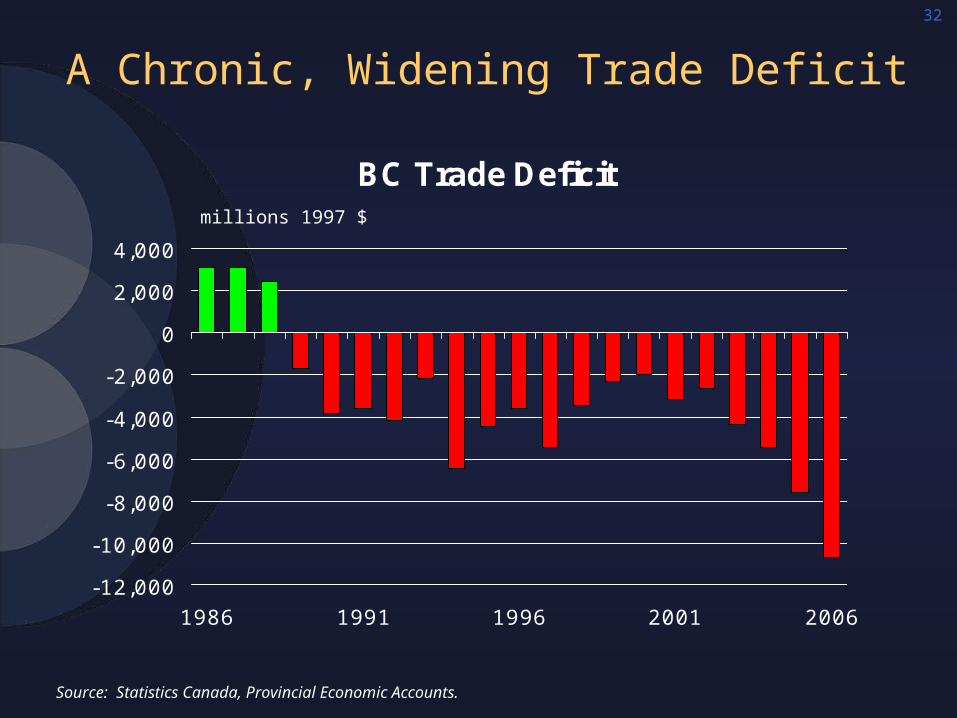

A Chronic, Widening Trade Deficit

Source: Statistics Canada, Provincial Economic Accounts.

BC Trade Deficit

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

1986 1991 1996 2001 2006

millions 1997 $

33

Goods (75% of total BC exports) Resource industries Resource processing Secondary manufacturing High tech manufacturing

Services (25% of total BC exports) Business/commercial/financial services Tourism Communications Culture/entertainment services (film/t.v./new media) Other high tech services Professional services (engineering, law, accounting, architecture)

Transportation (mostly linked to trade in goods)

Maritime-related services Royalties/license fees Education

The Structure of BC’s Export Base

3434

Need for Diversification

• Forestry = 40-45% of BC’s international merchandise exports and a similar share of manufacturing output

• Forestry destined to shrink, due topine beetle and ongoing decline in the size and economic contribution of pulp/paper industry

• Mining and energy are much better positioned to grow.

• Tourism struggling, based on the past few years’ performance.

• Bottom line: BC needs new engines of wealth creation, capable of exporting or otherwise generating inflows of income to the province

35

Opportunity BC 2020 Project Overview Opportunity BC 2020 Project Overview

• Focus on BC’s economic prospects to 2020

• Initial think piece, followed by 25 individual topic papers

• Drafts of the papers will be developed in 2008/09 and reviewed by relevant business stakeholders before finalized in spring 2009

• Public communication strategy and rollout of selected topic papers (partnership with Canwest Global)

• Major June 2009 conference on BC’s economic future

• Synthesis report

• All topic papers and final report available at no charge via website

36

Opportunity BC 2020 Project – Opportunity BC 2020 Project – Core Questions Core Questions

1. What are the key trends that will define the economic and demographic environment for BC to 2020?

2. How can BC, as a small, open economy, continue to prosper in a more competitive and increasingly knowledge-based world?

3. What steps can be taken to improve upon current policies, institutions, attitudes, and practices to strengthen the foundations for prosperity in the province?

37

Conclusions

• Global recession, unprecedented credit market crisis (not yet resolved) adds significant downside risk

• Canadian economy stalling

• Much slower growth ahead for BC economy, weakening evident then global financial turmoil» no significant growth engines

» export sector remains soft, prompting more regional variation

» BC may continue to out-perform Canada, but gap will narrow

• Labour market conditions will ease, but over the medium term the job market will continue to reflect the shift toward an environment of relative labour scarcity

• BC also confronted by a number of medium-term challenges (the export base, weak productivity, pine beetle, aging population, carbon constraints)

38

For a copy of this presentation, For a copy of this presentation, please contactplease contact

Barbara McNicholls Barbara McNicholls atat

[email protected]@bcbc.comoror

604-684-3384604-684-3384