Embed Size (px)

Citation preview

1

The Alberta NHL Players Tax: A Precedent for Source-Based Taxation of Nonresident Athletes?

Alan Macnaughton and Kim Wood

November 2003 1. Introduction

For sports with regularly-scheduled games such as hockey, baseball and basketball, it is

common that an athlete lives in one country (the residence jurisdiction) and plays some games in

the other country (the source jurisdiction). The question this raises for taxation is how the

potential tax revenue is to be shared between the two jurisdictions.1 Although there are an

infinite number of possibilities, two are most commonly observed.2 The first approach would be

to give priority to the source jurisdiction, primarily on the policy basis that athletes “…benefit

from services and facilities funded with tax collections [in the source jurisdiction]—from the

stadium itself to the roads leading to the stadium to the costs of police protection and all the other

public services that are available.”3 Under this approach, the source jurisdiction taxes income

earned there by nonresidents, and the residence jurisdiction also taxes the income but gives a

foreign tax credit for the taxes paid to the source jurisdiction. Hence the source jurisdiction

receives most or all of the revenue from this income. The second approach would be to give

priority to the residence jurisdiction, so that only this jurisdiction taxes the income. The primary

1 Whereas for corporations these are the only two claimants for the tax base, for individuals the country of citizenship is a possible third claimant, particularly where this a developing country: J. Bhagwati and J. Wilson (eds.), Income Taxation and International Mobility (Lond: MIT Press, 1989), at xiii. 2 Other possibilities are: exclusive source taxation, in which the residence country does not tax the income at all; non-taxation of the income by both source and residence countries; and double taxation—taxation by both source and residence countries (Jinyan Li, International Taxation in the Age of Electronic Commerce: A Comparative Study (Toronto: Canadian Tax Foundation, 2003), at 48). 3 Richard G. Chandler, “Wisconsin’s Case for Taxing Athletes”, Milwaukee Journal Sentinel (July 10, 2002), 17A.

2

policy justification for this approach is that it is the residence jurisdiction that has the personal

allegiance of the athlete.4

The Canada-US treaty prohibits source-based taxation of an athlete’s income from league

games held in a country other than where the team is located, and hence the residence-based

approach applies to all such cross-border income. For example, if a Canadian resident playing

for the Toronto Maple Leafs has a game in the US, the Canadian federal government taxes this

income and the US federal government does not. Most Canadian provinces and US states and

cities voluntarily follow the treaty. 5 Thus, with the current residence-based approach, each

country collects roughly zero dollars from the income of this group of individuals; Canada

collects nothing from US-resident athletes on American teams performing in Canada, and the US

collects nothing from Canadian-resident athletes on Canadian teams performing in the US.

Despite the importance of the treaty, some existing taxes have a source-based flavor. US

states have had taxes on out-of-state athletes (“jock taxes”) since California pioneered this

concept in 1978.6 Such taxes are now almost universal in the US; of the 24 states that have

National Hockey League (NHL), National Basketball Association (NBA) or Major League

Baseball (MLB) teams, 20 (83%) have jock taxes, and the remaining 4 states either do not have a

personal income tax or tax only property income.7 These taxes are partly source-based and

partly residence-based; they are source-based taxes within the US since they tax out-of-state

4 Richard J. Vann, “International Aspects of Income Tax,” in V. Thuronyi (editor), Tax Law Design and Drafting, Volume 2 (New York: International Monetary Fund, 1998), at 749-750. 5 Exceptions are Alberta, California, New Jersey and the city of St. Louis. 6 Non-residents in various occupations had been theoretically taxable in many states for years, but California began enforcement with baseball players in 1978: Richard R. Difrischia, “State and Local Taxation of Nonresident Athletes” (2000), 18 Journal of State Taxation 120-130. 7 David K. Hoffman, State and Local Income Taxation of Nonresident Athletes Spreads to Other Professions (Washington, D.C.: Tax Foudation, 2003), at 2. The other 4 states are Florida, Texas, Tennessee and Washington. The National Football League (NFL) has no teams in states that do not also have NHL, NBA or MLB teams. The District of Columbia is prohibited by federal law from having a jock tax. Various US cities also have jock taxes, including Cleveland, Cincinnati, Columbus, Detroit, Indianapolis, Kansas City, Minneapolis, New York, Philadelphia, Pittsurgh and St. Louis.

3

athletes, but they are residence-based taxes when viewed internationally since they generally

exempt out-of-country athletes.

Alberta’s National Hockey League Players Tax, which was introduced in its 2002 budget,

differs from the US jock taxes in two main respects-- the revenue raised by the tax is to be given

to the Alberta teams rather than going into the general coffers, and the tax applies to all players

playing games in the province. However, it is shown below that 43% of the revenue from the

Alberta tax comes from players on American teams. Assuming that these players are resident in

the US, they would not otherwise be taxable here. Hence this portion of the tax can be

interpreted as a step towards source-based taxation of non-resident athletes.

Much previous literature has examined the US jock taxes, 8 and two recent Canadian

articles have examined the new Alberta tax. 9 However, tax policy research on source-based

taxation of nonresident athletes has been scant both in Canada and internationally.10 With

escalating player salaries raising the potential revenues of such a tax, the absence of a compelling

rationale for the existing residence-based approach, and the fact that a non-resident tax would

8 Hoffman, ibid.; Richard E. Green, “The Taxing Profession of Major League Baseball: A Comparative Analysis of Nonresident Taxation” (1998), 5 Sports Lawyers Journal 273-301; Jeffrey L. Krasney, “State Income Taxation of Nonresident Professional Athletes” (1995), 47 Tax Lawyer 395-424; Elizabeth C. Ekmekjian, “Perspective, The Jock Tax: State and Local Income Taxation of Professional Athletes” (1994), 4 Seton Hall Journal of Sports Law 229-252; Leslie A. Ringle, “Note: State and Local Taxation of Nonresident Professional Athletes” (1994), 2 Sports Lawyers Journal 169-184; Kevin Koresky, “Tax Considerations for US Athletes Performing in Multinational Team Sport Leagues or ‘You Mean I Don’t Get All of My Contract Money’ “ (2001), 8 Sports Lawyers Journal 101-123; Jeffrey Adams, “Why Come to Training Camp Out of Shape, When You Can Work Out in the Off-Season and Lower Your Taxes: The Taxation of Professional Athletes” (1999), 10 Indiana International and Comparative Law Review 79-113; James K. Smith, Ann T. King, and Kathryn B. Reeves, “State Income Taxation of Nonresident Professional Athletes” (1997), 16 Journal of State Taxation 1-8. 9 Donald J. S. Brean and Aldo Forgione, “Missing the Net: The Law and Economics of Alberta’s NHL Players Tax” (2003) , 41 Alberta Law Review 1-24; Mark Lavitt, “The Alberta NHL Players Tax: The Jock Tax Comes to Alberta –or Does It?”, mimeo., April 2003. Lavitt makes a number of comparisons of the Alberta tax to US jock taxes. Also see Aldo Forgione, “Alberta’s NHL Players Tax”, Canadian Tax Highlights (December 27, 2002). 10 The US jock tax studies have not examined this issue. The only Canadian study is Robert M. Wener (KPMG Ottawa), “Report on Major League Sports Visiting Players’ Tax”, mimeo., January 25, 2000, 7 pages. The general treaty article on athletes, but not the Canada-US league-based exemption, is discussed in Stephanie C. Evans, “US Taxation of International Athletes: A Reexamination of the Artiste and Athlete Article in Tax Treaties” (1995), 29 George Washington Journal of International Law and Economics 297-335.

4

essentially take the revenue from foreign treasuries rather than from the athletes, source-based

taxation deserves serious study.

The main purpose of this paper is to examine the design, revenue implications, and

advantages and disadvantages of Canadian taxation of nonresident athletes. Particular attention

is paid to a provincial tax since the treaty serves as a federal- level impediment, the provinces are

particularly in need of revenue in this era of rising health care costs, and the Alberta tax in its

present form expires at the end of 2005. Such a tax has been proposed for BC by the Vancouver

Canucks and for Ontario by the chair of the Ottawa-Carleton regional government.11 In response

to criticism of the heavy compliance burden of US jock taxes, care is taken to design a tax that is

simple to administer.

The specific tax we examine is a 15% flat-rate tax levied by the four provinces with

major- league professional sports teams—British Columbia, Alberta, Ontario and Quebec. In

contrast to opinion that non-resident taxes raise only “a bit of revenue”, 12 our findings are that

such a tax would raise just over $30 million in revenue annually for the provinces, and more in

future years if athletes’ salaries continue their past dramatic climb. Almost three-quarters of the

revenue would go to the Ontario government, mainly because the Canadian NBA and MLB

(excluding the Expos) teams are located there. Alberta would lose approximately 40% of the

revenues it raises from its existing tax because Canadian players would be exempted. For all

provinces, the increased revenue would be exactly matched by a decline in US federal income

tax revenue by the same amount. Athletes would not have an increased tax burden (and possibly

11 These proposals envisioned earmarking the revenue for assisting financially-troubled sports teams, but that is not a necessary part of such a tax. See: Terry Bell, “Canucks’ Bottom Line: They Don’t Want a Subsidy”, Vancouver Province, June 2, 2002; Iain MacIntyre and Jim Beatty, “Canucks Set to Win Some Scratch with Share of Sports Lottery Proceeds”, Vancouver Sun , September 30, 2003; Joe Halstead, “Toronto Staff Report: Provincial Visiting Player Tax” mimeo., April 27, 2000. 12 Brean and Forgione, supra note 9, at 23. Although this comment was made in the Alberta context, the revenue issue is the same in all provinces.

5

would not have any great increase in their compliance burden); thus, concerns about the

unfairness of taxing one particular profession seem to be misplaced.13 The Canadian federal

government would lose only an estimated $3 million in foreign tax credits, or 11% of the

revenue generated by the provinces.

A secondary purpose of the paper is to examine the issue of sports subsidies since a large

part of the public debate over the Alberta NHL Players Tax was not about the characteristics of

the tax itself but about the propriety of giving the funds produced by the tax to the two Alberta

teams.

The outline of the paper is as follows. Section 2 provides more detail on the Alberta

NHL Players Tax and presents data on its application to various teams. Section 3 describes the

workings of the exemption from source taxation provided in the Canada-US treaty for league

athletes. Section 4, which is the core of the paper, presents the design of a simple provincial tax

on nonresident athletes, explains why it can be expected to raise significant revenue after

considering the loss of revenue through increased foreign tax credits, and presents revenue

estimates. The possibility that the tax could also apply to American athletes playing on Canadian

teams, which would raise another $27 million for the provinces at the expense of a similar

revenue loss to the federal government, is also discussed. Section 5 reviews the policy issues

concerning whether source-based or residence-based taxation of non-resident athletes is

preferable in policy terms. Section 6 considers the effects of removing the treaty provision

protecting non-resident athletes from source taxation and imposing a new flat-rate federal tax on

non-resident athletes. The issue of the disposition of the revenue is discussed in section 7—is

13 Brean and Forgione, supra note 9, at 9. However, the concern is justified to the extent the tax applies to Alberta residents.

6

there a case for sports subsidies and, if Ontario wishes to use the money from the tax to aid the

Ottawa Senators, what is the best subsidy form? Finally, a conclusion ends the paper.

2. The Alberta NHL Players Tax

Alberta introduced the NHL Players Tax in the 2002 Budget Speech. 14 Effective from

August 31, 2002 to December 31, 2005, the tax is levied under part 1.1 of the Alberta Personal

Income Tax Act and is calculated in accordance with Alberta Regulation 171/2002.15 The tax is

calculated as 12.5% of the NHL hockey income in Alberta of the NHL player for the year,

defined as the sum of the player’s taxable salary for all game days in the taxation year.16 Taxable

salary is determined by dividing the base salary17 of the player in effect on the game day18 by the

number of calendar days in the NHL regular season. 19 This special tax is in addition to normal

personal income tax rules, so non-residents pay only the 12.5% tax but Canadian residents pay

both the normal 10% Alberta personal income tax and the new 12.5% tax. The $6 million annual

revenue from the tax is to be given to the Alberta teams to help their financial situation and allow

them to stay in Alberta. 20

14 Alberta Budget Speech 2002, “The Right Decisions for Challenging Times”, March 19, 2002, online: http://www.finance.gov.ab.ca/publications/budget/. 15 NHL Tax Regulation – Alberta Regulation 171/2002, online: Canadian Legal Information Institute <http://www.canlii.org/ab/regu/ra/20030225/alta.reg.171-2002/whole.html> 16 As defined in subsection 2(2) of the Regulations, supra note 6. 17 Base salary is defined in subsection 2(1) of the NHL Tax Regulation to mean Paragraph 1 Salary as defined in the Collective Bargaining Agreement between the National Hockey League and the National Hockey League Players’ Association for the period September 16, 1993 to September 15, 2004. It is further explained in the related information circular that signing bonuses, deferred compensation or performance bonuses are not to be included. 18 Subsection 2(1) of the NHL Tax Regulation defines a game day as a day in the regular NHL season on which the player performs hockey duties or services in Alberta for an NHL team. Per subsection 48.1(2) of the Alberta Tax Act, (supra footnote 5) an NHL player performs hockey duties or services in Alberta as a player for an NHL team when the player either participates in an NHL hockey game in Alberta or is present in a facility in which an NHL game is being played for all or a part of the game. 19 For more detail, see Lavitt, supra note 9, and Brean and Forgione, supra note 9. 20 Alberta Budget 2002 backgrounder – NHL Players Tax, Alberta Treasury Department. This commitment appears to be informal and is not contained in the legislation.

7

Various sources indicate the losses suffered by the Edmonton Oilers and Calgary Flames

for the 2002/03 NHL season to be approximately $2 million and $8 million, respectively. 21

However, the two franchises are privately owned, so financial statements are not publicly

available to verify this information. One factor lending credibility to tales of the teams’ financial

woes is the departure of previous Canadian teams: two Canadian hockey teams (the Winnipeg

Jets and the Quebec Nordiques) folded in the mid-1990s; the Vancouver Grizzlies basketball

team moved away in 2001; and the Montreal Expos are in the process of moving. Also, the

Ottawa Senators filed for bankruptcy on January 9, 2003. Although a purchase offer of $71.8

million by Eugene Melnyk was finalized and accepted in August 2003, low revenues and a high

debt load continue to make the team’s future uncertain. 22

The new Alberta tax has attracted a great deal of public attention, partly because of

speculation that Ontario or other provinces would follow Alberta’s lead23 and partly because

there are many view of the merits of the tax itself. Team owners were grateful for the new

source of funds, and sports fans generally seemed to like the tax. Players and their collective

bargaining agent, the National Hockey League Players Association (NHLPA), vehemently

opposed the tax. Provincial officials defended the tax as helping Alberta’s NHL teams without

hurting taxpayers.

One difference between the Alberta tax and the US jock taxes is that the Alberta tax

applies only to NHL players while the US taxes apply to all athletes and even, at least in theory,

to all non-resident individuals performing services in the state. The big difference between the

Alberta tax and the US jock taxes, however, is that the jock taxes apply strictly to out-of-state

21 See Eric Francis, “Owners get a pat on the back”, online: Slam Sports <www.canoe.com/Slam030306/col_francis -sun.html>. 22 See “Melnyk finalizes purchase of Senators”, online: CBS Sportsline http://cbs.sportsline.com/nhl/story/6594071.

8

athletes while the Alberta tax also applies to Alberta athletes. Since the Players Tax is imposed

on the portion of the player’s salary that relates to game-days in Alberta, the tax amounts to an

additional levy equal to roughly 3% of the base salary of each Flames and Oilers player.24 In

effect, regular Alberta residents pay a 10% rate of Alberta tax, while Alberta players on NHL

teams pay 13%.25 Hence the tax may legitimately be criticized as “taxation by profession.”

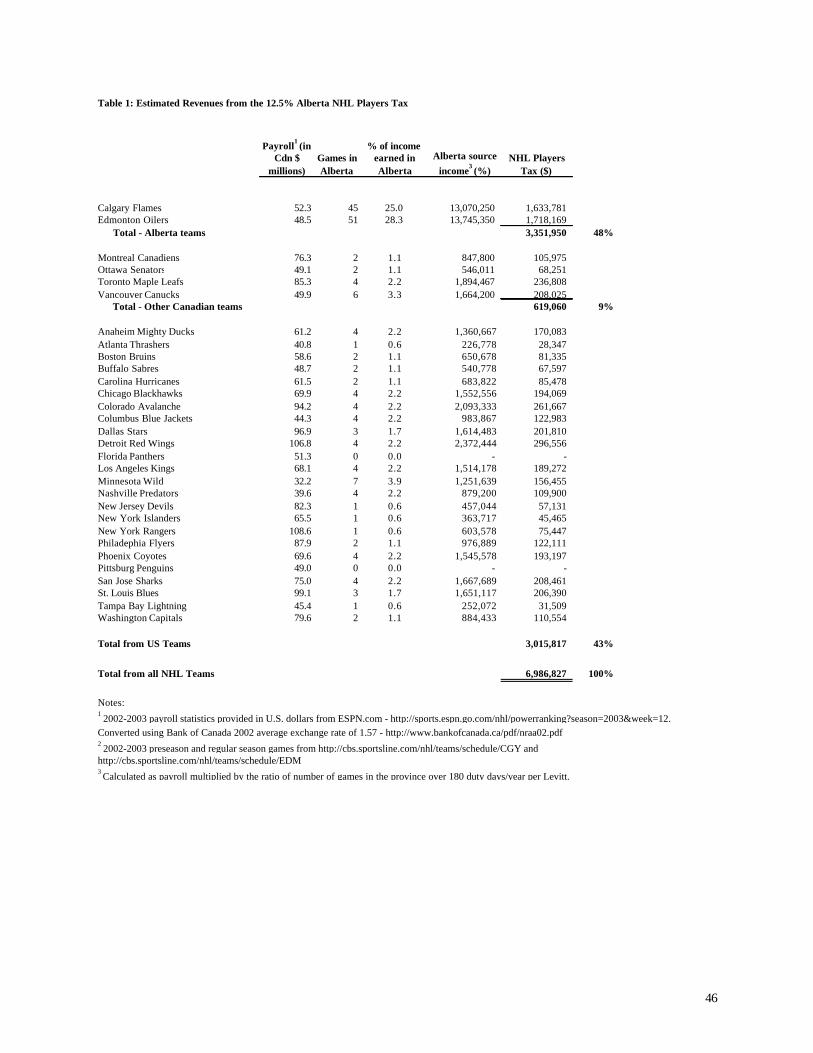

Data on the relative contributions to Alberta revenue of players from different teams are

given in Table 1. The figures are for the 2002-2003 NHL year and show total revenue of $6.9

million, which is reasonably close to the Alberta 2000 budget prediction of $6 million. As the

table shows, 43% of the revenue is from players on American teams, 48% is from players on

Alberta teams, and the remaining 9% is from players on other Canadian teams. Clearly, the

Alberta tax has set a precedent for provincial taxation of nonresident athletes.

3. The Treaty Exemption for League Athletes

Most treaties based on the OECD model contain a specific article providing that income

derived by non-resident athletes of one contracting state may be taxed in the state where the

income is derived, irrespective of whether they maintain a permanent establishment or fixed base

23 One Ontario supporter of a player’s tax is the Ottawa Senators Community Coalition, online: < http://www.oscc-ccso.net/media_en/feb25_2003.html 24 From Table 1, the Calgary Flames played 45 games in Alberta in 2002-2003, and 45/ 180 (game-days divided by the approximate length of the season) x 12.5% = 3.1%. A similar calculation for the Oilers yields 3.5%. 25 Some of the player reactions were: “I’m all right...But I’m about three per cent less happy than I normally would be...It’s very discriminatory” (Calgary Flame Denis Gauther) and “I guess our stance from a hockey player’s point of view is why does someone in the community who makes the same as me pay less taxes?....When you tell 20 or 25 guys in the whole province, you’re the only guys who are going to pay 42 or 41 per cent (tax rate) versus 38...I don’t know the legality of it.” (Calgary Flames co-captain Bob Bougher) in “Oilers Leery of Pro Tax” by Shane Holliday, The Edmonton Sun, March 19, 2002, p.7.

9

in that state.26 The effect of this article is to protect Canada’s right to tax Canadian-source

income of foreign athletes

In the Canada-U.S. Tax Convention, this exemption is found in Article 16 – Artistes and

Athletes.27 Similar to the OECD model, it permits source taxation of income from personal

activities earned by entertainers, musicians and athletes.28 However, the Canada-U.S. treaty is

unusual in that it contains a paragraph specifically negating the effect of the other paragraphs of

article 16 for athletes in respect of his activities an employee of a team which participates in a

league with regularly scheduled games in both Canada and the US. The technical explanation to

this paragraph indicates these multi-jurisdictional league athletes will be subject to the rules of

Article 15 – Dependent Personal Services. Paragraph 1 of this article indicates that the income is

taxable in the state where the employment is exercised, giving Canada the right to tax the income

from games played in Canada. However, paragraph 2 of this article prohibits such taxation where

the amount is below $10,000 in a calendar year or the recipient is present in Canada for less than

183 days and the remuneration is borne by a U.S. resident. It is highly likely that most athletes

on US teams could, if they wished, meet the second condition, since they could be in Canada

only for scheduled games (under 183 days per year) and their salary is paid by an American

sports franchise or club.29 Thus, the treaty overrides domestic law and Canada does not have the

26 Chagnon, Francois. “Cross-Border Taxation of Artists, Entertainers, and Athletes”, 1997 Conference Report, Canadian Tax Foundation, p. 24:2. 27 Convention Between Canada and the United States of America With Respect to Taxes on Income and on Capital, as amended by the protocols signed on June 14, 1983, March 28, 1984, March 17, 1995 and July 29, 1997, (herein referred to as “Canada-U.S. treaty”), paragraphs 1 and 2 28 The Canada-U.S. treaty article 16 also contains a de minimus rule in paragraph 1which exempts any income amounts not exceeding $15,000 from source taxation. 29 For a discussion of how U.S. resident athletes can minimize their U.S. tax liability by structuring their off-season schedule around this 183-day rule, see Adams, supra note 8 and Robert E. Beam, Stanley N. Laiken and Daren A. Raoux, “The Taxation of Non-Resident US Athletes Employed by Canadian-Based Professional Sports Teams: Attracting Athletes to Canada” (1999), 47 Canadian Tax Journal 305-340.

10

right to tax such U.S. athletes on their employment income earned while playing in Canada.30

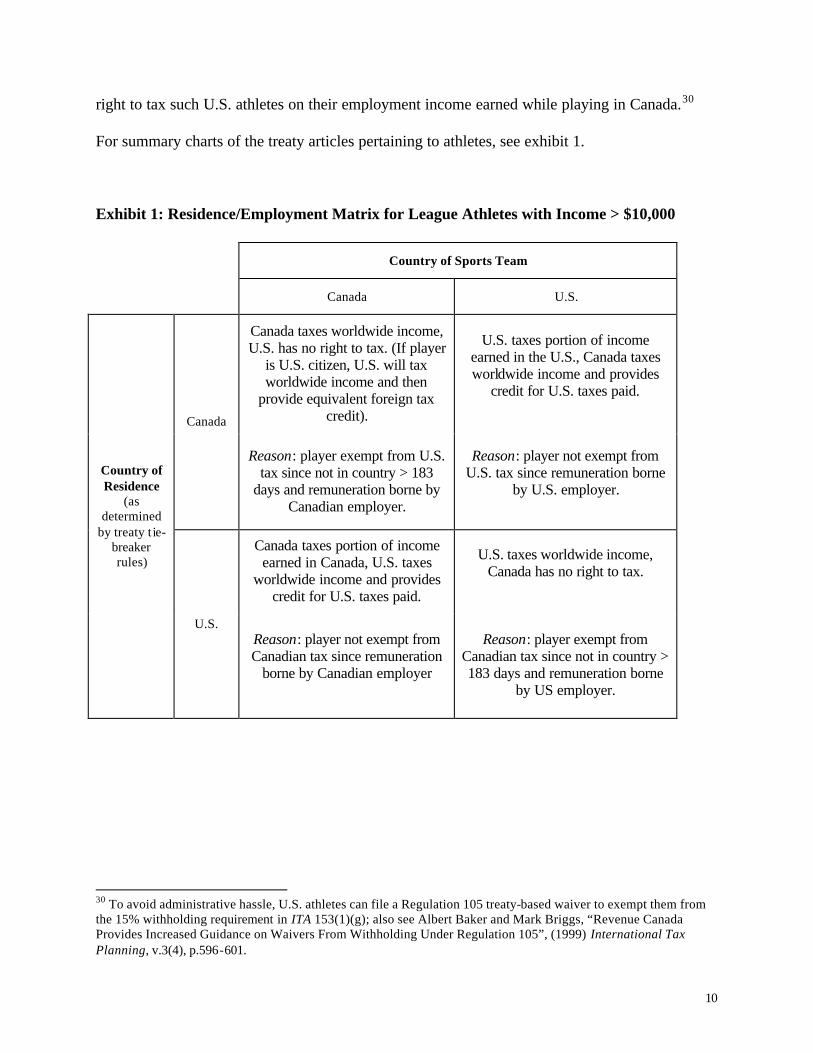

For summary charts of the treaty articles pertaining to athletes, see exhibit 1.

Exhibit 1: Residence/Employment Matrix for League Athletes with Income > $10,000

Country of Sports Team

Canada U.S.

Canada taxes worldwide income, U.S. has no right to tax. (If player

is U.S. citizen, U.S. will tax worldwide income and then

provide equivalent foreign tax credit).

U.S. taxes portion of income earned in the U.S., Canada taxes worldwide income and provides

credit for U.S. taxes paid.

Canada

Reason: player exempt from U.S. tax since not in country > 183

days and remuneration borne by Canadian employer.

Reason: player not exempt from U.S. tax since remuneration borne

by U.S. employer.

Canada taxes portion of income earned in Canada, U.S. taxes

worldwide income and provides credit for U.S. taxes paid.

U.S. taxes worldwide income, Canada has no right to tax.

Country of Residence

(as determined

by treaty t ie-breaker rules)

U.S. Reason: player not exempt from Canadian tax since remuneration

borne by Canadian employer

Reason: player exempt from Canadian tax since not in country > 183 days and remuneration borne

by US employer.

30 To avoid administrative hassle, U.S. athletes can file a Regulation 105 treaty-based waiver to exempt them from the 15% withholding requirement in ITA 153(1)(g); also see Albert Baker and Mark Briggs, “Revenue Canada Provides Increased Guidance on Waivers From Withholding Under Regulation 105”, (1999) International Tax Planning, v.3(4), p.596-601.

11

4. A Proposed Provincial Tax on Non-Resident Athletes

(1) Scope

Let us consider a provincial tax that is restricted to non-resident athletes. The first

question to address is which non-residents should be taxed. Current federal and provincial

personal income tax laws tax the income of athletes resident in countries other than the US,31

US-resident athletes who play for Canadian teams, and non-resident athletes who do not play in

leagues with regularly-scheduled games (e.g., golfers). Thus, the principal gap in these laws is

athletes playing on American teams who are residents of the US.

If the source basis is viewed from the perspective of the province, the new tax could also

apply to athletes who live in other provinces within Canada. However, for at least 40 years

Canada has taxed all employment income in the province of residence on December 31

regardless of the province in which it was earned.32 This is a condition of the tax collection

agreements, both under the previous tax-on-tax version and the new tax-on-income approach,

since this rule is part of the definition of taxable income.33 Hence, if a province is to adhere to

the principles underlying the tax collection agreements, it cannot tax Canadian athletes who are

resident in other provinces. It would seem wise to continue this tradition, particularly in view of

the many problems that have been caused by state taxation of nonresident citizens in the US.34

31 Most of Canada’s other tax treaties follow the OECD model with slight modifications, the end result being that Canada has the right to tax non-resident athletes from non-U.S. countries on their source income. See Daniel Sandler, The Taxation of International Entertainers and Athletes: All the World’s a Stage (Netherlands: Kluwer, 1995), at 57-58, Table A. Also see Daniel Sandler, “Canada” in The International Guide to the Taxation of Sportsmen and Sportswomen (International Bureau for Fiscal Documentation, 2002). 32 Ernest H. Smith, Federal-Provincial Tax Sharing and Centralized Tax Collection in Canada (Toronto: Canadian Tax Foundation, 1998), at 124 and 152. 33 See Department of Finance, Federal Administration of Provincial Taxes: New Directions (Ottawa: Department of Finance, 2000). 34 See David Schmudde, “Constitutional Limitations on State Taxation of Nonresident Citizens” (1999), Law Review of Michigan State University – Detroit College of Law 95-169. Table 1 shows that Alberta raises 9% of its revenue from Canadians living outside Alberta, so in that respect it taxes out-of-province athletes in the same way that the US jock taxes apply to out-of-state athletes. The fact that Alberta contemplates providing tax credits if other

12

Taxing athletes on American teams who are not residents of Canada also appears to be a

violation of the tax collection agreements since it redefines income for tax purposes for these

athletes. However, the Alberta NHL Players Tax also redefines income for athletes and the

federal government has not complained, at least not publicly. Perhaps the Canada Customs and

Revenue Agency (CCRA) would even collect the tax for a fee, although Alberta has chosen to

collect the tax itself. In any event, it appears that the tax collection agreements, as they are

currently administered, would not prevent imposing the proposed provincial tax on non-resident

athletes.

In summary, the proposed tax is to apply to the Canadian-source income of all athletes

who are residents of the US and who play for American teams that participate in leagues with

regularly-scheduled games. The tax is source-based only on an international basis, and in this

respect it differs from the American jock taxes.

The most important leagues that the new tax would apply to are the NHL, NBA and

MLB. There are at least four other professional leagues which have teams in Canada: the

National Lacrosse League has teams in Toronto, Calgary and Vancouver, the American Hockey

League has teams in Manitoba, St. John’s, Toronto and Hamilton; the North American Football

League has a team on Hamilton; and the International League (baseball) has a team in Ottawa.

However, it is perhaps best to exclude these other leagues as relatively little revenue is involved

relative to the compliance burden. 35 Exempting these leagues while catching the main ones

could be done in the law by setting a threshold requirement for being subject to the tax in terms

provinces taxed Alberta athletes is consistent with this view: see paragraph 48.5( c) of the Alberta NHL Players Tax and Lavitt, supra note 8,at 33, footnote 72. 35 A non-athlete example of a situation to avoid is of a musical group with total annual income of $22,000 that was subject to tax in 22 states. The accountant chose to file only some of the required returns in order to reduce the burden of fees charged (M. Bryan and R. Hawkins, “The Biggest NFL Losers—Some Nonresident Athlete State Income Tax Calculations” (2003), State Tax Notes (September 15, 2003), 761-764, at 763).

13

of a minimum dollar value rather than a minimum number of days of physical presence.36

Players in the Canadian Football League and the National Football League would not be subject

to the tax as these teams currently have no cross-border games.

Four provinces have NHL teams—Alberta, British Columbia, Ontario and Quebec—

while the NBA and MLB (excluding the Expos) are restricted to Ontario. Thus, this proposal is

an expansion of taxing power for British Columbia, Ontario and Quebec, since these provinces

presently levy no taxes on such non-resident athletes on non-Canadian teams. On the other hand,

this proposal restricts the application of the Alberta NHL Players Tax, which currently applies to

all NHL players playing in Alberta. As noted above, since the Alberta tax is scheduled to exp ire

at the end of 2005, this might be an appropriate time to review its design.37

One potential concern about the proposed tax is that the Alberta government has stated

that the reason it taxed all athletes under the NHL Players Tax instead of just non-residents is

that the latter type of tax would not withstand a North American Free Trade Agreement 38

(NAFTA) challenge.39 However, it has been noted that income tax measures are generally

outside the scope of NAFTA. 40 Thus, the imposition of a tax on non-resident athletes would not

be a NAFTA violation. Also, US states have been taxing Canadian athletes on their source

taxation for numerous years without any discussion of a NAFTA problem.

NAFTA could potentially apply if a provincial government were to provide the tax

revenues to a particular hockey team, such as if Ontario gave money to the Senators to help them

36 Brian Arnold, “Threshold Requirements for Taxing Business Profits Under Tax Treaties”, in Canadian Tax Foundation, forthcoming, at 2:31. 37 Lavitt, supra note 8, at 39, suggests that the Alberta tax is a stopgap measure to help the Alberta teams survive until the NHL and the NHL Players’ Association work out a new collective bargaining agreement in 2004. 38 North American Free Trade Agreement Between the Government of Canada, the Government of Mexico and the Government of the United States, December 17,1992 39 Why doesn’t this new tax violate NAFTA? All players are being treated in the same fashion, which complies with NAFTA”, Alberta Budget 2002 backgrounder – NHL Players Tax, Alberta Treasury Department. 40 Brean and Forgione, supra note 9.

14

to remain in Ottawa. This could be a violation of NAFTA’s national treatment principles, as all

investors are to be treated equally regardless of any preference for locality. 41 However, many US

cities and states have used massive amounts of tax revenues to support professional sports teams

and facilities without prompting a NAFTA challenge. Furthermore, it has been argued that

Canada should be taking action under the realm of NAFTA to prevent any further US state or

local subsidies, or to potentially pursue a claim for financial compensation equal to the dollar

value of the inability of Canadian sports teams to receive equal government treatment compared

to their American counterparts.42

Overall, it appears that NAFTA would not be a barrier to the imposition of a provincial

tax on non-resident athletes.

(2) Rate Structure

A major criticism of the US jock taxes is that they impose high compliance costs, mainly

because each player must submit a return and pay tax to each state imposing a jock tax. One way

to solve this problem, as recommended by the Federation of Tax Administrators, is to put the

responsibility on the team rather than the individual player.43 One composite return is filed by

each team for all of its team members, and the team is also be responsible for withholding tax

from team member compensation and submitting it to the tax authority. Although this method

41 Article 1102, supra note 40 42 B. Appleton & M. Neceski, “Submission: NAFTA and Sports” (May 12, 1998). Online: Appleton & Associates International Lawyers <http://www.appletonlaw.com/6bsports.htm>. The NAFTA challenge submission was presented to the government of Canada over 4 years ago; thus, it appears Canada has decided that pursuing such a challenge is too uncertain or not worthwhile. For an evaluation of the Appleton & Neceski submission, see Heather Manweiller and Bryan Schwartz, “Trade and Sports: Time Out: Canadian Professional Sports Team Franchise – is the Game Really Over?” Asper Review of International Business and Trade Law (2001), v.1, p.199 43 James Wetzler (chair), State Income Taxation of Nonresident Professional Team Athletes: A Uniform Approach (Task Force on Nonresident Income Tax Issues, Federation of Tax Administrators, 1994).

15

has not so far been used in the US, it is used by the Alberta NHL players tax. 44 Technically the

levy is on the player, but the team is required to act as a withholding agent. This is a departure

from current law in that the non-Canadian teams have no permanent establishment in Canada;

however, the treaty has no application at the provincial level and, since employees of the teams

visit Canada for games, it should not be difficult to enforce the tax obligations.

The composite-return method is much simpler to apply using a flat-rate tax rather than a

progressive rate structure with personal reliefs and tax credits. A flat-rate tax can be calculated

simply from knowledge of the team’s payroll, while the more complex progressive structure

requires a separate calculation for each player.45

A flat-rate tax may also be justified on equity grounds. For example, the average NHL

player makes $1.6 million Canadian and a common percentage of that income allocated to a

province could be 2%, so in-province income would be $32,000. Taxing based on an income of

$32,000 and not considering the player’s out-of-province income might seem to be

underestimating the player’s ability to pay and not giving the source country a proper share of

the player’s world tax liability.

California has dealt with this issue by calculating tax on a worldwide basis and then

multiplying by the ratio of California income to worldwide income to determine tax owing. 46

Applying that approach would essentially mean that all league athletes would have most of their

income taxed at the top marginal provincial rate, since the current minimum salaries in US

44 Lavitt, supra note 9, at 25 and 27 and NHL Tax Regulation – Alberta Regulation 171/2002, Section 50 varied (4), (5). 45 Difrischia, supra note 6, at 129, notes that many athletes would be willing to pay more tax in order to have a simple system, as present jock tax rules involve considerable aggravation and costs. 46 Ekmekjian, supra note 8, at 246, footnote 103. This method is also applied by Switzerland to part-year residents. Ssee Kees van Raad, “Non-Discriminatory Income Taxation of Non-Resident Taxpayers by Member States of the European Union: A Proposal” (2001), 26 Brooklyn Journal of International Law 1482-1492, at 1488.

16

dollars are $150,000 for the NHL, $367,000 for the NBA, and $200,000 for MLB. 47 However,

applying a flat-rate tax at approximately the top marginal rate achieves the same equity objective

but is simpler, requires less intrusion on the player’s privacy, and does not pose the same

enforcement problems in terms of determining income outside of the country. 48

As for the personal reliefs, most authors believe it is more appropriate that the residence

country should be the one which takes into account the taxpayer’s personal attributes, such as

those relating to medical costs, subsidies for home ownership, basic exemption, etc. since it is

the country that has the personal allegiance of the taxpayer.49

The choice of a rate is more difficult. It would be desirable to pick a rate that is

reasonable across the country since various provinces may wish to launch such a tax and, ideally,

it would be administered by the CCRA on a national basis to reduce compliance and

administrative costs. The 2003 top rates for the provinces that have professional sports teams are

as follows: 14.7% for BC, 24% for Quebec, 17.41% for Ontario, and 10% for Alberta. In

addition, the section 120 rate for non-residents taxable in Canada is 13.92% (48% of the top

federal rate of 29%). Based on this comparison, 15% might be a suitable rate. This rate also has

the advantage of producing horizontal equity with non-resident actors and entertainers, who

presently face a 15%withholding rate on fees paid for services rendered in Canada. 50

Given that the proposed tax is similar to the Alberta NHL Players Tax in that the

collection and returns are the responsibility of the teams rather than individual players, the

47 Sources: http://sportsillustrated.cnn.com/hockey/nhl/2001free_agency/ for the NHL, http://www.nba.com/news/cap_030715.html for the NBA, and http://sportsillustrated.cnn.com/baseball/mlb/news/2000/04/05/mlb_salaries_ap/ for MLB. 48 This approach is currently used in Canada at the federal level for inter vivos trusts. Alternatively, the tax could be imposed at the flat rate with an election for the player to calculate tax using the California method: see van Raad, supra note 46, at 1492. 49 Vann, supra note 4, at 749-750. 50 ITA 153(1)(g), Regulation 105. However, this rate is further reduced to 10% on the first $5,000 of income under the Canada-U.S. Tax Convention, Article 17, Paragraph 1

17

administration costs may be similar to the Alberta estimate of a quite reasonable $150,000

annually—2.5% of the projected revenues.51

(3) Tax Base

The next issue is the determination of the Canadian-source income. There are two

quantities to be determined—the athlete’s employment income and the proportion of that income

that is earned in the province. There are three possible models: the US jock taxes, the Alberta

NHL players tax, and the Income Tax Act’s calculations for non-resident athletes who are not

eligible for the treaty exemption (principally non-resident players on Canadian teams).

The Alberta52 tax calculates employment income as the player’s base salary only. 53 In

contrast, the US jock taxes may include signing bonuses, performance bonuses and deferred

compensation54 and the Income Tax Act’s concept of employment income is similarly broad.

The Income Tax Act also taxes total signing bonuses at a 15% rate, thus avoiding disputes about

the allocation to the various jurisdictions. It would seem reasonable to follow the Income Tax

Act approach in order to provide uniformity of treatment on a federal-provincial basis and to

reduce the scope for tax planning which moves income from base salary to non-taxed forms of

remuneration. 55

Similar issues arise with respect to the formula for determining the proportion of total

employment income that is taxable in the province. Once again, the Alberta tax opts for extreme

simplicity, using the ratio of game days in Alberta to the total number of days in the NHL regular

51 Alberta Budget 2002 Backgrounder – NHL Players Tax. 52 Lavitt, supra note 9, at 25 to 27, makes the case that the Alberta method is superior. 53 NHL Tax Regulation – Alberta Regulation 171/2002, paragraph 2(1)(a). 54 Endorsements and other money paid to athletes other than from a team is probably self-employment income and hence is not taxable in the source country because there is no permanent establishment. See Jackson E. Donley, “State Taxation of Endorsement and Royalty Income of Nonresident Professional Athletes” (1998), 16 Journal of State Taxation 1-14.

18

season. In contrast, the CCRA determines the income of non-resident athletes taxable in Canada

by the ratio of duty days in Canada to total duty days in the year, where duty days include not

only games but practices, pre-season training camps, etc.56 The CCRA approach is better for

three reasons. First, the CCRA method was established earlier and, with this issue as well as the

others discussed above, conformity with the CCRA approach is desirable because it reduces

compliance costs and eliminates the possibility of double taxation, which could occur within

Canada if different provinces levied such a tax and adopted different income-allocation

approaches.57 Second, although the Alberta approach is easier to enforce, the Federation of Tax

Administrators in the US recommended the duty-days approach since it was viewed as more

equitable in that it took into account all of the athlete’s contractual obligations to the team.58

Finally, the Alberta approach generates too low an allocation of income in that the numerator is

game-days in the jurisdiction but the denominator is not just total game-days but also non-game

days in the regular season. 59

(4) Athletes’ Tax Burdens and the Retaliation Issue

One issue that might be a concern is that the imposition of the new provincial tax might

cause US states to retaliate by taxing Canadian-resident athletes. At present, only 2 of the 20

states with jock taxes—California and New Jersey—tax Canadian-resident athletes. This is

inconsistent with the intent of the Canada-US treaty, but the treaty only applies at the federal-

55 See Beam et al, supra note 29. 56 Ibid., at 309-310. 57 This can occur either because of the use of different allocation fractions or because of different definitions of duty days. See Ekmekjian, supra note 8, at 242. 58 Wetzler, supra note 43. 59 The Alberta approach seems designed to reduce the tax liability of Alberta players. As Table 1 above shows, the Alberta approach implies that only 25% of Flames players’ income and 28% of Oilers players’ income is earned in the province. This result is absurd since half of all games are home games, played in Alberta, and most of the team

19

government level. If the other 18 moved in the same direction, would that hurt Canadian athletes

or Canadian provincial and federal tax revenues? And is it likely that they would do so? These

questions require some background.

For athletes resident in Canada, personal income taxes paid to foreign governments,

including US states, are eligible for a foreign non-business tax credit against Canadian federal

income tax. Credit for foreign taxes is only given at the provincial level on a residual basis, i.e.,

to the extent that full credit has not been given at the federal level. Given that no US federal

taxes are imposed (because of the treaty) and US state tax rates are far below the tax rates at the

Canadian federal level, the US state tax should be fully creditable at the Canadian federal level

and provincial tax credit is unlikely to be used. Thus, the imposition of American jock taxes on

Canadian athletes would not reduce provincial revenue or increase the athletes’ tax burden.

The extra jock taxes would add to the compliance burden of Canadian athletes, however.

A Canadian NHL player might have to file 15 state tax returns if all states with jock taxes and

NHL teams imposed these taxes on Canadian players. It has been estimated that in 1994 these

returns cost between $250 and $750 US to prepare. If accountants’ charges have increased in

line with Canadian inflation of 21% from then until now, the extra 13 returns would cost

between $5,000 and $15,000 in cur rent Canadian dollars annually. 60

For those concerned about federal revenues and taxpayer compliance burdens, one might

ask whether it is likely that the application of new provincial tax applies to athletes would cause

more states to tax Canadian athletes. This is an open question. 61 On the one hand, retaliation

would seem unlikely in that the proposed provincial tax would not reduce a state’s revenue

practice time also occurs in the province. Lavitt, supra note 9, also discusses this issue but does not address the revenue effect. 60 See the Bank of Canada’s inflation calculator at http://www.bankofcanada.ca/en/inflation_calc.htm.

20

(unlike taxes imposed by other US states). For athletes resident in the US, personal income taxes

paid to a Canadian province are eligible for a foreign tax credit on the athlete’s US federal return.

No state credit is given. Perhaps for this reason, the Alberta NHL Players’ Tax seems not to have

inspired any such reaction.

On the other hand, it is certainly fair that if Canada adopts source-based taxation of non-

resident athletes then the US could adopt similar measures. In addition, the state might not like

the fact that its athletes are taxed by a foreign country, even if that did not actually increase the

athletes’ tax burden. Also, it might be viewed as anomalous that states do not presently tax out-

of-country athletes even though they tax out-of-state athletes. The fact that two states already

have this policy makes it not so strange. On balance, it seems likely that all of the states levying

a jock tax would eventually retaliate and tax Canadian athletes. This is the assumption in the

revenue estimates below.

(5) Would Canada as a Whole Gain Revenue?

Given the conclusion above that athletes’ tax burdens would not be increased by the

proposed tax, it is apparent that source-based taxation versus residence-based taxation is a zero-

sum game among 4 levels of government: Canadian provincial and federal governments and US

state and federal governments. This raises the question of whether implementing the proposed

tax, and moving to source-based taxation, is a zero-sum game within Canada. More specifically,

would the loss of revenue to the Canadian federal government from granting foreign tax credits

to Canadian players in respect of taxes paid to the US on games there offset the gain to the

provincial governments from taxing Americans on games here? One might at first think so,

61 It is reported that seven unnamed states have reciprocal exemptions which would cease if the visiting player tax were enacted in Ontario: Wener, supra note 10, at 4.

21

since schedules in the NHL, NBA and MLB ensure that the numbers of cross-border games

played in Canada and the US are exactly equal (since any team plays the same number of home

games as away games). Hence one US commentator claims that US jock taxes raise “a pitifully

small amount of revenue once all the credits are taken.”62

There would be circumstances in which this could happen. To illustrate, consider the

situation where Ontario and Michigan each have one team with a payroll of $60 million

Canadian, and each team spends 10% of its duty days visiting the other country. All the Ontario

players live in Ontario, and all the Michigan players live in Michigan.

Suppose initially Michigan has a 15% tax on nonresident athletes that it does not apply to

Canadian athletes, and Ontario legislates its own 15% tax. If Michigan begins to apply its tax to

Canadians, both Ontario and Michigan would have revenue of 15% x 10%% x $60 million, or

$900,000. The Canadian federal government would grant a foreign tax credit of $900,000 to the

Ontario athletes for taxes paid to the Michigan government, and the US federal government

would similarly grant a foreign tax credit of $900,000 to the Michigan athletes for taxes paid to

Ontario.63 Thus, in this hypothetical situation, the proposed tax would accomplish only a

redistribution of revenue from the two federal governments to the provincial and state

governments. Canada as a whole would have zero additional net revenue relative to residence-

based taxation. 64

One obvious reason why this scenario does not hold in real life, and Canada as a whole

would gain from taxing nonresident athletes, is that the 15% proposed provincial tax rate is

higher than US state tax rates. Michigan’s top rate of jock tax (which is the same as its top

62 David Hoffman, “ ‘Jock Tax’ Singles Out Athletes”, Tax Notes (August 4, 2003), at 730. 63 The credit given is equal to the lesser of the foreign taxes paid and the domestic taxes that would have been paid on the foreign-source income.

22

marginal rate for all residents) is 4.1%, and the top marginal tax rate applying in the 20 jock-tax

states is 9.3% in California. In contrast, every province in Canada has a top marginal tax rate of

10% or more and we propose a flat rate of 15% for the proposed tax. Also, as discussed above,

all states but California give non-residents the benefit of the graduated rate structure.

A second reason why Canada would gain is that the payrolls of Canadian teams are

smaller than those of American teams. Although this is not true in basketball ($86 million

American average versus $90 million for the Raptors), it is true of hockey ($68 million American

average vs. $60 million Canadian average) and baseball ($128 million American average versus

$96 million for the Blue Jays).65

The third reason Canada as a whole gains is that more players in cross-border games have

American residence than Canadian residence. Although athletes almost always have the same

country of residence as where their team is located, the one exception is that baseball and

basketball players playing for Canadian teams are believed by the player advisors to which we

have spoken to have US residence, probably because of the lower taxes there and the athletes’

US upbringing.66 This does not affect their status under the proposed tax—all players on

Canadian teams would be exempted—but it means that no foreign tax credits would have to be

granted by Canada for MLB and NBA players. The explanation is as follows. The nonresident

64 The US as a whole would also have zero net revenue because the $900,000 in Ontario tax would reduce US federal revenues by an equal amount through the foreign tax credit system, just offsetting the $900,000 in Michigan revenue. 65 See Tables 2, 3 and 4 below. This is somewhat similar to the idea that developing countries benefit from source taxation because they are capital-importing countries (Li, supra note 2, at 56); Canada is a net importer of athlete labour, so source taxation of that income benefits Canada. 66 Wener, supra note 10, at 4, states that players employed by US teams almost invariably are US residents. For baseball, this is confirmed by the report that only 7 of the 764 MLB players in 1997 list Canada as the country of residence (Green, supra note 8, at 273, note 151). For the Toronto Blue Jays, the official information is that of their 56 players, 50 live in the US, 3 live in the Dominican Republic, 2 live in Venezuala, 1 lives in the Netherlands Antilles, and none live in Canada (Dan Diamond, 2003 Toronto Blue Jays Official Guide (Toronto: Polar Bear Press, 2003) pp. 24-160). .

23

Blue Jays and Raptors players are taxable in Canada on their Canadian-source income,67 so they

should be exempt from the proposed tax (as should be any players on Canadian teams who are

resident in Canada, since they are also already taxable here). However, nonresident Blue Jays

and Raptors players would not be eligible for foreign tax credits on their Canadian returns for US

jock taxes paid.

These three factors means that applying the proposed tax to the visiting athletes playing a

Canadian sports team creates a net profit for Canada as a whole, even assuming that all states

retaliate and tax Canadians on that team under their jock taxes. The overall benefit then

increases with the number of sports teams. 68 Thus, Ontario, with its 4 professional sports teams,

generates the biggest net advantage to Canada under the proposed tax.

(6) Provincial Revenue Estimates

This section of the paper estimates the revenue that would be raised if all provinces with

a MLB, NBA or NHL sports team (Alberta, British Columbia, Ontario and Quebec) levy a 15%

tax on US-resident athletes who play for American teams in these leagues. The base of the tax

would be employment income earned in the province, measured by multiplying employment

income received from the team by the ratio of duty days in the province to total duty days in the

year.

As noted above, we assume that all players on American teams are US residents and

hence subject to the tax. Given this assumption and a flat-rate tax with no deductions or credits,

the tax can be computed at the team level, even though it would be levied on individual athletes.

67 For such athletes, Article XVI of the treaty is silent. Also, they are not exempted from tax under Article XV as their remuneration is borne by an employer who is resident in Canada. 68 Smith, supra note 8, at 3. Smith also points out the tax rate issue discussed above.

24

The calculations below are based on the reported payrolls of each team in the three

leagues.69 Payroll definitions are not given in these sources, so to the extent that these figures

reflect only the base salaries, the revenue figures will be understated. For duty days, we follow

Hoffman and assume that duty days are 1.3 times game-days for baseball and 1.2 times game-

days for basketball and hockey, with 210 total duty days in the season for hockey and baseball

and 105 for basketball.70 The numbers of game-days are from the posted schedules of the teams.

We use the figures reported after the season is over since factors such as rain-outs and which

teams make the playoffs affect the figures. Our figures are intended to be the same as those of

the CCRA but their actual number are unknown.

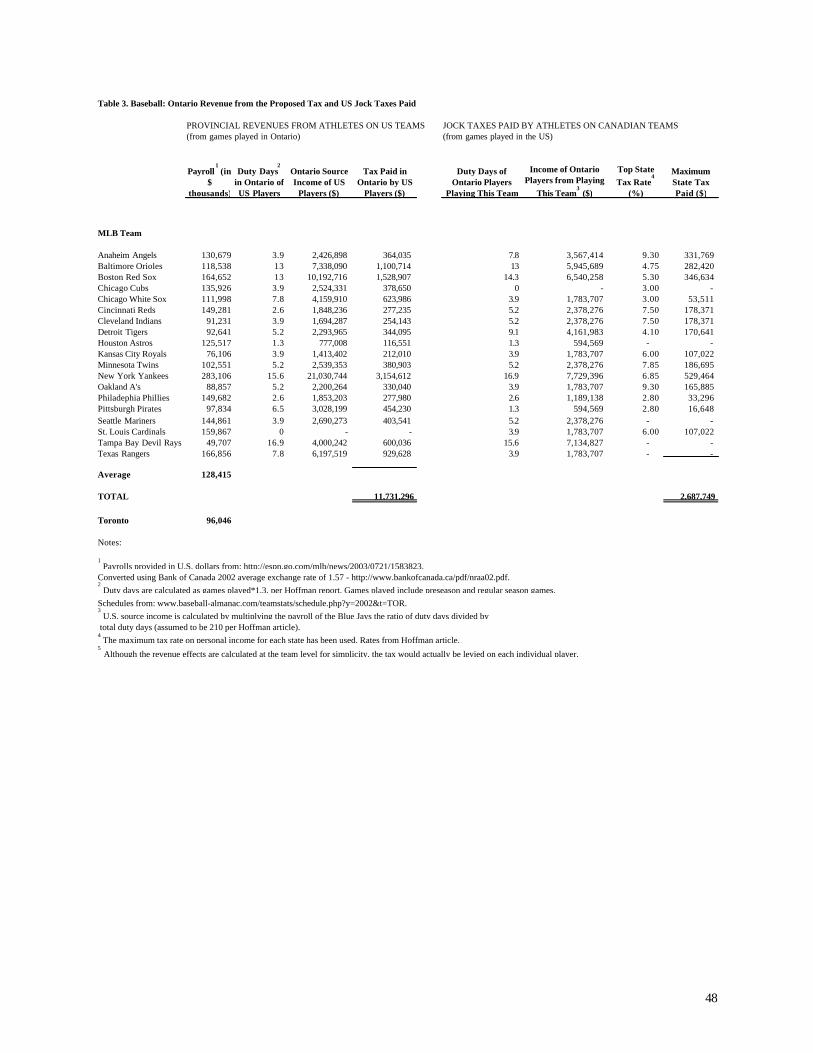

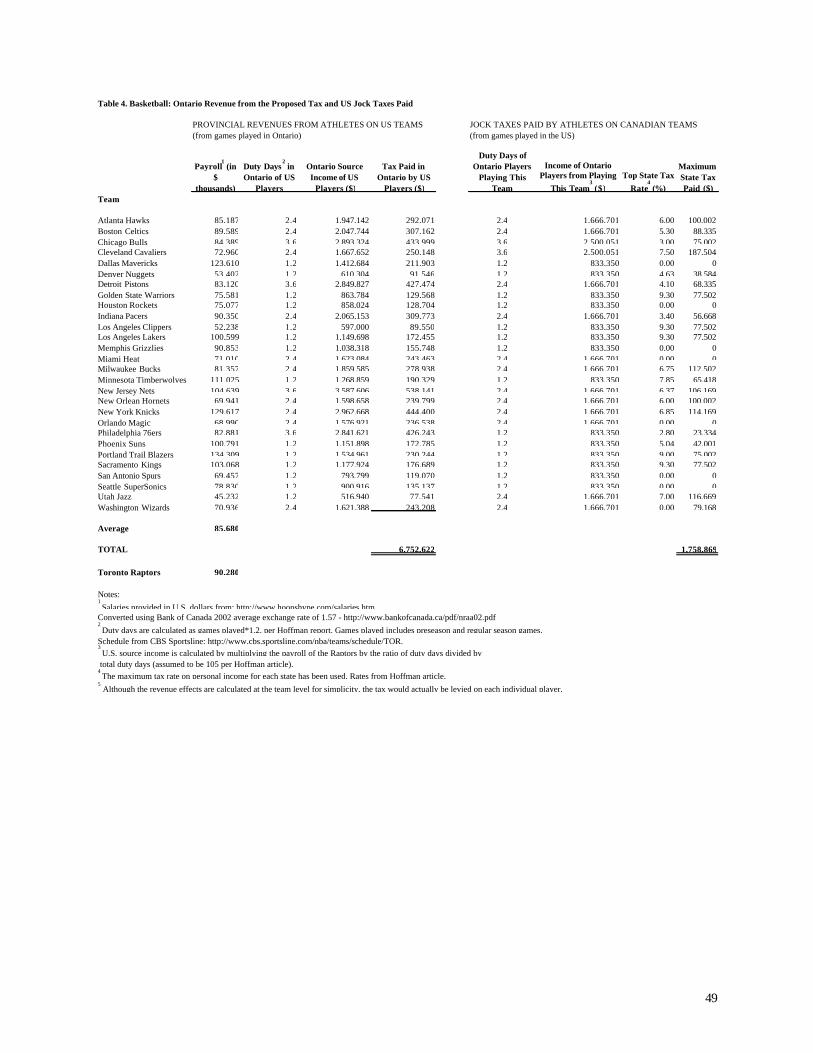

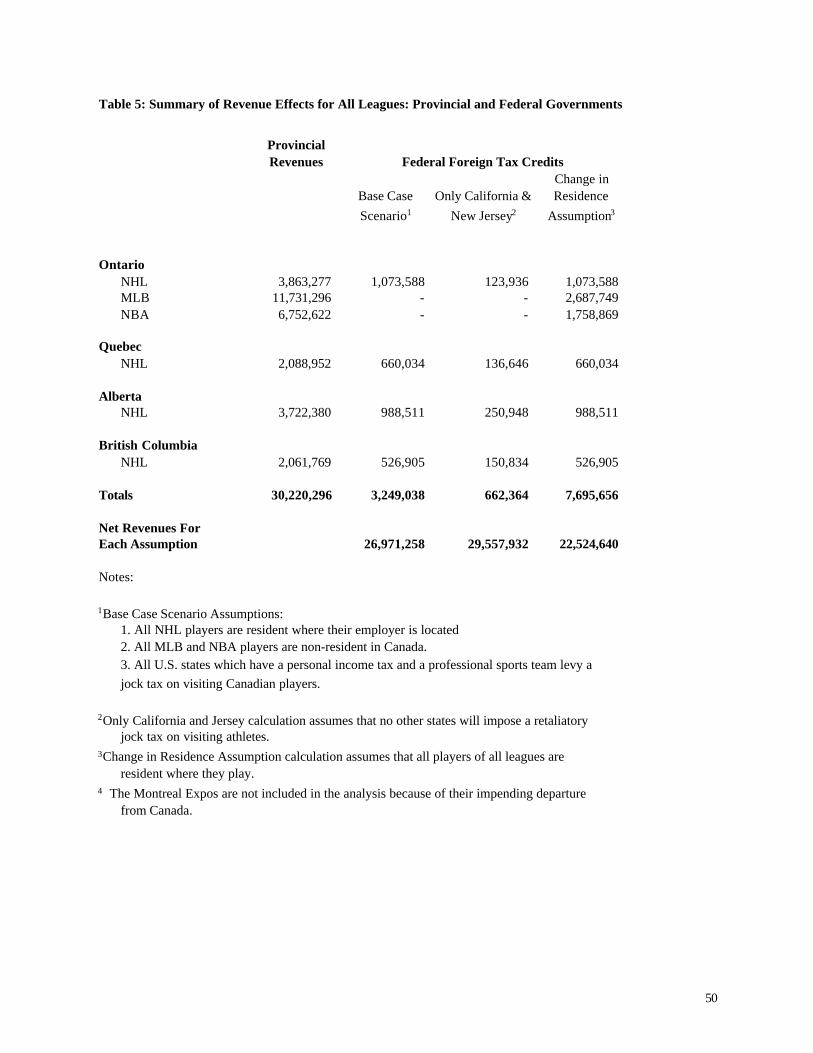

The left-hand panels of Tables 2, 3 and 4 estimate the revenue that might be derived by

Ontario from the NHL, MLB and NBA respectively. The total revenue figures at the bottom of

the left panel of each of these tables appears in the first column of a summary table, which is

Table 5. This table also shows revenue figures for Quebec, Alberta and British Columbia, which

have NHL teams but no MLB or NBA teams.71 Detailed calculations for these provinces are

omitted but on publication of this article they will be posted on the first author’s website.

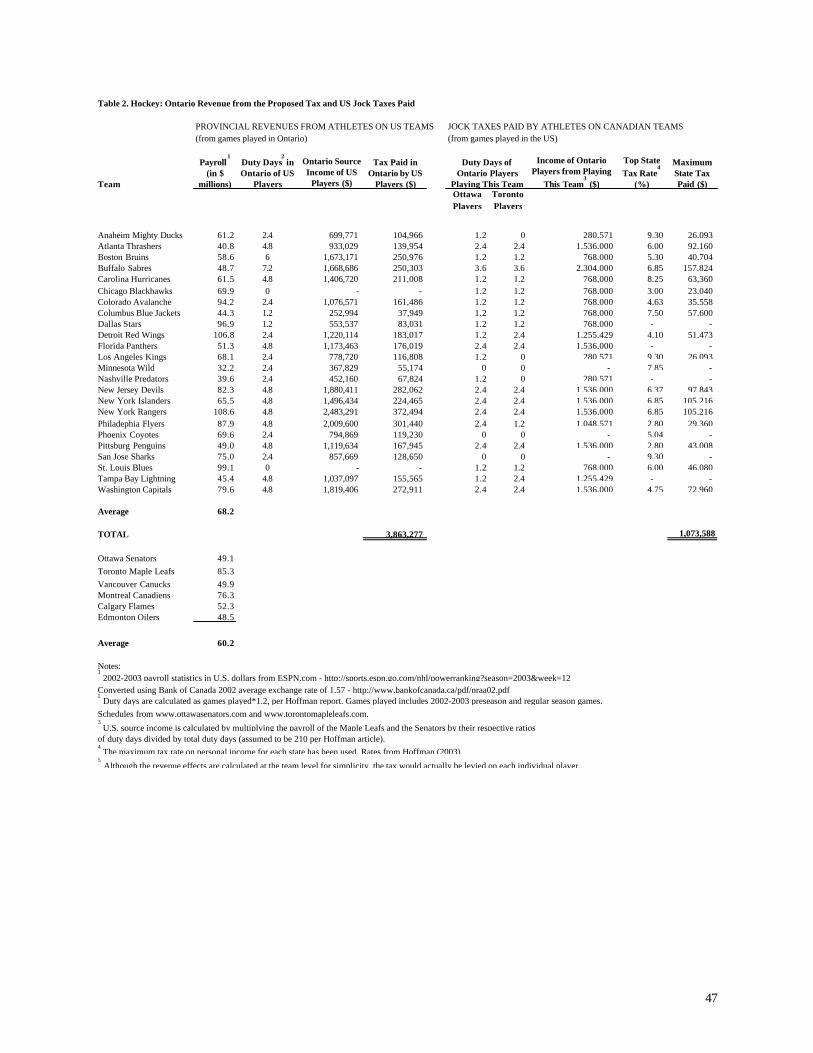

For an example of the Ontario revenue calculations, consider the first row in Table 2,

which is for the Anaheim Mighty Ducks hockey team. Their 2002-2003 payroll is $61.2 million

Canadian. They played 2 games in Ontario that season, which gives them 1.2 x 2 = 2.4 duty-

days in Ontario out of the total of 210.72 Thus, Ontario-source income is the $61.2 million

multiplied by 2.4 and divided by 210, or $699,771. Tax revenue is 15% of that, or $104,966.

69 Hockey: 2002-2003 payroll statistics from ESPN.com - http://sports.espn.go.com/nhl/powerranking?season=2003&week=12. MLB: 2002 payrolls from http://espn.go.com/mlb/news/2003/0721/1583823. NBA: 2002-2003 salaries from: http://www.hoopshype.com/salaries.htm 70 Hoffman, supra note 7, at 6. These figures actually vary by team; Green, supra note 8, at 295 and 298, calculates the duty days of two players on different baseball teams for the 1998 season at 227. 71 The Montreal Expos are not included in the tables due to their impending departure from Canada.

25

Making a similar calculation for all US-based NHL teams playing in Canada in that season

produces estimated total tax revenue to Ontario of roughly $3.8 million. The calculations for the

Toronto Blue Jays baseball team in Table 3 and the Toronto Raptors basketball team in Table 4

are similar; the only difference in calculation are in the assumptions of duty-days per game-day

and in total duty days for the season, as described above. Although tax is based on the calendar

year and these figures are for sports season that can straddle two calendar years, this should not

make a difference other than for the first calendar year the tax applies.

The overall results, as shown in the left-hand column of Table 5, are that $30 million in

revenue would be raised by the proposed tax in 4 Canadian provinces. The great majority (74%)

is from Ontario, while other provinces are as follows: $2 million (7% of the total) each for

Quebec and BC; and $4 million (12% of the total) for Alberta.

Revenues from the existing Alberta NHL Players Tax are not included in the above

figures. Alberta would lose 47% of the revenue by moving to a non-resident tax, even though the

rate would rise from 12.5% to 15%. The reason for the decline is that Canadian players, which

are assumed to be coincident with players for Canadian teams, are no longer being taxed.

Revenue from non-residents actually goes up by 23%, largely because of the rate increase,

although a small amount is due to the change in the allocation formula to duty days from

Alberta’s game-day-to-season- length ratio.

The distribution by sport is that baseball and hockey each amount to 39% of the revenue

while basketball amounts to 22%. However, these fractions come from the visiting athletes

playing just one baseball team and one basketball team, as opposed to 5 hockey teams. Baseball

and basketball are bigger on a per-team basis because the average American baseball and

basketball team has a higher payroll ($128 million and $86 million vs. $68 million) and the

72 Duty-days are not actually fractional amounts such as 1.2, so this figure should be interpreted as an average only.

26

proportions of games in Canada that involve an American team are higher (100% for the Raptors

and 98% for the Blue Jays vs. 67% for the Leafs). This is why Ontario’s revenues are so high—

it has the only Canadian baseball (excluding the Expos) and basketball teams.

(7) Estimates of Federal Revenue Loss

The right-hand panels of Tables 2, 3 and 4 give figures for the amounts of jock taxes that

would be paid by players of Canadian sports teams in respect of games in the US if the players

were subject to these taxes.73 The conditions under which this could occur are discussed below.

For an example of the jock-tax calculations, consider the second row of the right-hand

panel of Table 2, which concerns the calculation for players on Ontario NHL teams (the Toronto

Maple Leafs and Ottawa Senators) in respect of their games in the US with the Atlanta

Thrashers. The Leafs had 2.4 duty days (2 games) in Atlanta out of their total of 210 duty days,

so Leafs players Georgia-source income is the Leafs payroll of $85.3 million times 2.4 and

divided by 210, or $974,857. Similarly, the Ottawa Senators, with a payroll of $49.1 million,

also had 2.4 duty days in Georgia, so their players’ estimated jock tax liability is that payroll

amount times 2.4 divided by 210, or $561,143. Hence the Georgia-source income of all Ontario

players was $1,536,000. Applying the top Georgia marginal tax rate of 6% produces a Georgia

jock tax liability of $92,160, which is shown on the second row, far right column of the table.

The jock tax amounts shown are probably too high. 74 This upward bias arises from

several sources, of which the most important is probably the assumption that the top rate of tax

applies on the athlete’s whole income, although most states apply a graduated rate structure.

Another source of bias is our implicit assumption of effective enforcement of the tax law. Some

73 Jock taxes imposed by US cities are omitted as they are relatively small. 74 One reason they could be slightly too low is that jock taxes levied by US cities are not included.

27

authors contend that athletes may choose not to file in some states, notably Massachusetts and

Maryland, which take a non-aggressive approach in collecting state income taxes.75 Still another

source is that some states tax an athlete only income over a certain threshold,76 or only if the

athlete is present in the state for more a certain number of days.77 Fixing these biases and

producing an accurate calculation of jock taxes would be possible, since salaries for individual

athletes are publicly available, but it would require detailed knowledge of state tax rules and the

degree of compliance with these laws by Canadian athletes.78

The implications of these jock-tax amounts for Canadian federal revenues vary with

assumptions made about residency and the response of US states to the introduction of the

proposed tax. As our base case, we assume that all players on Canadian NHL teams are

residents of Canada, all players on the Toronto NBA and MLB teams are US residents, and all

US states levying jock taxes will apply these taxes to Canadian-resident athletes after the

proposed tax is enacted. For hockey, the implication is that the jock taxes paid by hockey

players on Canadian teams would be as shown in the right-hand panel of Table 2—hockey

players would now be subject to these taxes—and these would also be the amounts of foreign tax

credits granted at the Canadian federal level. As discussed above, the jock tax rates are

sufficiently low relative to Canadian federal rates that the foreign tax credits should equal the

taxes paid and no provincial foreign tax credit would occur. For baseball and basketball players,

the jock taxes would be paid, but as American residents they would not be claiming these taxes

75 Green, supra note 8, at 273, note 190. 76 See the survey of state tax authorities reported in Richard Hawkins, Terri Slay and Sally Wallace, “Play Here, Pay Here: An Analysis of the State Income Tax on Athletes”, Tax Notes (December 30, 2002), 1735, Table 1. 77 For example, Massachusetts only taxes athletes who are present in the state for more than 10 days in the year. Thus, Blue Jays players would be taxable but Raptors players and hockey players would not be. Smith, supra note 8, at 7. 78 A thorough account of sources for state tax research is given in Charles W. Swenson, Sanjay Gupta, John E. Karayan and Joseph Neff, State and Local Taxation: Principles and Planning , Second Edition (Boca Raton, Florida: J. Ross Publishing, 2004)., at 255-260.

28

as foreign tax credits on their Canadian returns as the taxes do not relate to their Canadian-source

income. Hence the total revenue loss for the federal government from foreign tax credits would

be as shown in the second column of Table 5.

The key result is that the revenue loss to the federal government is $3.3 million, which is

11% of the provincial revenue. Clearly, this is not even close to offsetting the provincial

revenue. The three reasons for this are noted in the previous section: the 15% proposed

provincial tax rate is higher than US state tax rates; the payrolls of Canadian teams are smaller

than those of American teams; and more players in cross-border games have American residence

than Canadian residence.

Because of the uncertainty surrounding key assumptions, we present alternative estimates

of foreign tax credit amounts. The optimistic alternative is that no states retaliate and the only

taxation of Canadian residents by US states is by the two states that do it now, which are

California and New Jersey. In this scenario foreign tax credits are about $700,000, or 2% of new

provincial revenues. The pessimistic alternative is that all states retaliate as before, but Jays and

Raptors players are actually Canadian residents rather than American residents. The effect of

this change in assumption is that they would be entitled to foreign tax credits on their US taxes

paid. This raises foreign tax credits to about $8 million, or 26% of provincial revenue. The

conclusion is that even in the pessimistic scenario, foreign tax credits are much less than

provincial revenue. This conclusion is reinforced by the fact there is a degree of upward bias

built into our foreign tax credit calculations.

29

(8) Players on Canadian Teams Who Are American Residents

The proposed tax described above does not apply to players on Canadian teams who are

resident of the US because these athletes are already taxable in Canada. Their income is

considered income not earned in a province, so there is no provincial tax. Instead, section 120

imposes a surcharge of 48% of the regular tax. This approach might seem reasonable for some

types of property income or capital gains earned in Canada which it is difficult to allocate to a

province, but for the income of athletes earned from games played in particular cities, it is rather

obvious what province their income should be allocated to. Therefore, there is a case for the

federal government dropping its surcharge for these athletes and instead allowing the provinces

to include them in the proposed tax.

Under our base case assumptions on residency, the Jays and Raptors players are the only

players who affected by the tax on income not earned in a province. Thus, the amount of

provincial revenue that would be generated by allowing the provinces the tax room to tax this

income would be 15% of the total payrolls of the Jays ($96 million) and Raptors ($91 million),

or $27 million. All of this tax would go to Ontario. This is almost equal to the revenue raised

from taxing players on American teams calculated above.

The true figure could be even higher as the $27 million does not include the effect of

taxing American players in the Canadian Football League. However, the 15% flat rate might

perhaps be too high in this case as athletes in this league would have a lot of income which is

presently being taxed at less than the top marginal federal rate.

30

5. The Choice Between Source-Based and Residence-Based Taxation

A voluminous literature has developed on the relative merits of source-based taxation and

residence-based taxation. The context has most often been international taxation rather than state

and provincial taxation, but the issues are not very different. 79 The more important distinction is

that the literature is more about corporate income taxation and capital flows than personal

income taxation and labor flows, and this difference does matter. This section of the paper

briefly reviews the arguments as they relate to athlete taxation by provinces in Canada.

We begin by noting that some arguments are inapplicable in the context of a provincial

tax on non-resident athletes. It is often argued that source-based taxation of athletes would not

raise a significant amount of revenue, but the tables above prove this argument would not apply

to Canada. It is quite possible that taxation of non-residents in other professions might not be as

productive, however. Also, as noted above, the proposed provincial tax on non-resident athletes

would not raise the tax burden on athletes because it should be fully creditable at the US federal

level;80 it simply changes the allocation of tax revenue among different governments, and the

fact that an athlete is paying tax to more jurisdictions should not matter (apart from the

compliance cost issue discussed below). This has several implications. First, it does not make

sense in the Canadian context to use non-neutrality as an argument either for81 or against82

source taxation. In particular, the introduction of the proposed tax would not influence an athlete

79 A recent reference is Stephen E. Shay, J. Clifton Fleming Jr. and Robert J. Perroni, “ ‘What’s Source Got to Do With It?’: Source Rules and International Taxation” (2002), 56 Tax Law Review 81-155. 80 This is quite different from jock taxes, which raise the athlete’s total tax liability if the tax rate in the source jurisdiction is higher than in the residence jurisdiction. See Green, supra note 8, Table 3, at 297 for some examples. 81 J. Andrew Hoerner, “A Nation of Migrants: When a Taxpayer has Income from Several States”, State Tax Notes (April 13, 1992), citing Wetzler, argues that source taxation is necessary to prevent athletes from avoiding the tax by moving to a low-tax state.

31

in any of the following dimensions: in which country or province/state to live; which team to

work for; and (assuming the athlete had any influence on this) where the team’s games are to be

played.83 Second, the discriminatory treatment of athletes (and artists and entertainers, who are

already taxed at 15% under current law) versus other employees providing personal services,

such as airline pilots, lawyers, surgeons and executives, is not a real economic burden. However,

it is certainly discrimination in appearance and it would be difficult to communicate the true

situation to the public.84 Presumably, it is only matters of administrative convenience that

prevent extending the nonresident tax to these groups. Finally, the idea that a jurisdiction that

switches to source-based taxation would then become a less attractive place to locate a sports

team is not convincing. 85 While all of these may be valid criticisms of the US jock taxes, they

are inapplicable in the context of the tax proposed in this paper.

The primary argument given in the literature for source taxation is that source taxation is

fair because the jurisdiction in which the income is earned has normally provided significant

services to the person who earned in the income.86 In the case of athletes, this could involve

airports, roads, stadiums, policing, fire departments, etc. This is the well-known concept of

taxation according to the benefit principle, and has been characterized in the international context

as a “national rental charge” for the use of the country’s resources, interpreted in the broadest

sense.87 More recently it has been argued that source taxation should be regarded as charge for

82 Green, supra note 8, notes that jock-tax create an incentive for athletes to move to a low-tax state. 83 Smaller non-neutralities might exist, such as the possibility that the duty-day calculation might cause an athlete to want to leave the province right after a game to avoid creating another duty day (Lavitt, supra note 8, at 26). 84 For sample complaints of this type, see: Hoffman, at 10; Gordon Henderson, “All Aboard the Tax Express”, Tax Notes (January 25, 1993), 507. 85 Ekmekjian, supra note 8, at 278, describing the view of a past governor of Georgia. MLB has indicated that a baseball team would not be located in Washington, D.C. if there is a jock tax there. 86 See Chandler, supra note 3, and also James W. Wetzler, “Gordon Henderson’s Tax Express: A Reply”, Tax Notes (February 8, 1993), 803. 87 Peggy Musgrave, as quoted in Michael J. Graetz, Foundations of International Income Taxation (New York: Foundation Press (an affiliate of Carswell), 2003).

32

market access and the income earned in the jurisdiction can be regarded as a reasonable and

practical measure of the value of that access.88

One factor that supports source-based taxation of employment income is that it is

relatively easy to establish a connection to a country (nexus) for labor income than for capital

income, in that for labor income one can establish nexus just by the person being physically

present in the country to do the work. 89 Thus, in the case of an athlete, being present in the

country to participate in the sporting event establishes nexus. Also, the amount of the income

attributable to each source country is relatively easy to measure, at least by the admittedly

arbitrary method of a pro rata allocation by time spent in each source country.

One problem with the argument that source-based taxation is necessary to fund public

services in the source jurisdiction is that it ignores the fact that having one’s residence in a

jurisdiction also creates the need for public services. Thus, perhaps part of the revenue should be

going to the residence jurisdiction. 90

Also, source-based taxation presents some problems in defining the source of an athlete’s

income. One author argues that athletes earn their money at home rather than on the road, citing

the fact that teams earn revenues from broadcasting rights, ticket sales and merchandise

contracts, but the reply is that although the team may earn its income at home, the athlete earns

his income wherever he plays.91 More significantly, it has been argued that the game is only the

place of performance of the final skill, even though there may have been years of preparation in

88 Shay et al., supra note 79at 92. 89 Brian J. Arnold & Michael J. McIntyre , International Tax Primer: Second Edition (The Hague: Kluwer, 2002),, at 22. 90 See Henderson, supra note 86, at 1121. 91 See Hoffman, supra note 7, at 10-11 and the reply by Harley Duncan, “Jock Tax Analysis Was Way Off Base”, Tax Notes (December 16, 2002), 1489.

33

the residence country, so it should not be the case that 100% of the tax goes to the source

country. 92

Source-based taxation has been said to be “taxation without representation”, and hence it

is argued that a government could be too keen to establish a “tax on foreigners”. Although this

point may raise valid questions about voting laws, it is not an argument against taxing non-

residents.93

Source-based taxation has been criticized on the basis that one jurisdiction moving in that

direction could inspire the other jurisdiction to retaliate and do the same, either because of the

loss in revenue or the perception that “they are taxing our athletes, so we should respond”. As

discussed above, this prediction has certainly been true in the past. However, it is not so much

an argument against source-based taxation as a warning that jurisdictions contemplating a move

in this direction should expect that neighboring jurisdictions could respond in kind. Provided

this is taken into account and proves to be a small effect, as is shown in Table 5 above, it is not a

problem. California, New Jersey and St. Louis already tax Canadian athletes, so it is

unreasonable to suggest that the Alberta tax or the proposed tax constitute any kind of

unprecedented move that could cause “irritation” to the US.94

Another argument sometimes raised against source taxation is that residence countries

may find it easier to obtain information to ensure proper payment of tax. A study by the Auditor

General found that fewer than 2% of non-resident individuals who received payment for services

in Canada filed a tax return. 95 This is not likely to be a problem with league athletes, whose

92 Shay et al, supra note 79, at 138; also Gordon Henderson, “Henderson’s Tax Express: A Response to Commissioner Wetzler”, Tax Notes (February 22, 1993), 1121. 93 Li, supra note 2, at 56. 94 Brean and Forgione, supra note 9, at 23. 95 Auditor General of Canada, Report 2001 (Ottawa: Auditor General, 2002), at 18 (in chapter: “International Tax Administration: Non-Residents Subject to Canadian Income Tax”). On compliance problems, see also Organisation

34

schedules and salaries are publicly available, although there may be a problem with some of the

incentive and signing-bonus components of income.

The major argument against source-based taxation in Canada is the increase in

compliance costs for taxpayers and administrative costs for government. Although no formal

studies have been undertaken, these costs are likely to be higher since residence-based taxation

involves only one country’s tax system while source-based taxation involves both countries’ tax

systems, possibly with multiple tax returns in each country. For example, if the proposed tax

was implemented and in response states in the US moved to tax Canadian athletes, a Canadian

NHL player might have to file as many as 18 state tax returns.

It remains to be seen how much of the problem of compliance costs can be solved with

better tax design. US state jock taxes are almost a model of what not to do in terms of lack of