Embed Size (px)

Citation preview

Module 4.2 Market Studies

Team Finland Mining Growth ProgramCHILE18 December 2015

Table of contents – Goals and content of the assignment– Introduction– Analysis & Recommendations– Market Landscape

– Market size and potential– Current key trends– Market opportunities

– Market Specific Issues– Regulatory Environment– Challenges– Key players in the value chain segments– Value Chain of the Chilean Mining Industry

– Expert Interviews– Comments from the Finnish companies about the Chilean market– Appendix

18.12.2015 Team Finland Mining Growth Program

2

Goals and content of the assignmentPurpose

The purpose of this assignment is to provide relevant market information for Finnish mining industry companies' decision-making on international growth

Goals

Improved understanding of market opportunities (market mapping), challenges, competitive situation, channels, operating models and other relevant facts of the Chilean market.

Content

Primary and secondary research

18.12.2015 Team Finland Mining Growth Program

3

Introduction– For the purpose of conducting our research, we have adopted a definition of

mining similar to that employed by the Chilean minerals industry. As such, the report will focus on the exploration, mining and processing of minerals, and not the oil/gas industries or fabricated metal production.

– Unless otherwise stated, all currencies are in American Dollars (USD) and prefixed with US$.

– Mining companies have been classified as major, mid-tier (intermediate) or junior, in line with the suggested definitions provided by SONAMI.

– Major mining projects at the committed stage of the development cycle have completed all commercial, engineering and environmental studies, received all required regulatory approvals and finalized the financing for the project. Such projects are considered to have received a positive FID from the owner, or owners, and are either under construction or preparing to commence construction. A project is classified as being at the Completed Stage when they have substantially finished their construction and commissioning activities to the point where initial commercial level production has commenced. Additional information is available in Appendix II.

18.12.2015 Team Finland Mining Growth Program

4

Analysis and recommendationsDrivers & trends

– Chile is a natural resource-based economy with long mining traditions and history. The country seeks to diversify its mining sector to also cover services, and is on the edge of the transition period. This offers business opportunities.

– Low commodity price for copper creates high concern among the players.

– Chile is not the cheapest natural resources producer, and local price level hasbeen raised as a challenge in almost all interviews.

– Key challenges for the future: productivity, energy, efficient use of water,innovation, training human capital, communities.

– Finland has exceptionally good mining country image in Chile.

– Chile has a good understanding of its challenges and is actively working on theissues.

18.12.2015 Team Finland Mining Growth Program

5

Analysis and recommendations Development areas & concerns

– Productivity needs to be improved. Failing to address this, coupled with increased mining costs, could jeopardise a successful future. Therefore innovation development is urgently needed to generate solutions.

– High technology will increase in the sector, which requires a skilled workforce. Chile currently faces a shortage of highly-educated engineers. Therefore training presents an opportunity for Finnish companies.

– High energy costs are currently one of the main barriers to expanding existing projects; as well as for new future projects. Renewable energy is considered as one solution for tackling the problem.

– Need for water: The mines are located in the Northern parts of Chile in an extremely dry region and the need for water is growing, estimated to be four times the current supply. The need for technology and services is real.

– Other development areas: New exploration methods, tailings and slag exploitation, recycling and drilling equipment.

18.12.2015 Team Finland Mining Growth Program

6

Analysis and recommendationsDevelopment areas & concerns (cont.)

– Future Projects: Current prices are requesting re-evaluations of several projects. This is creating a need for very fine engineering assessments. New and different solutions are searched.

– Finnish Technologies: Considered to be quite reliable. The existing situation to gain productivity represents a potential advantage for Finnish companies.

– Outlook: The main restriction is the budget cuts and reduction happening in the industry. This is expected to continue next year. From there on a slow recovery is considered. Challenges can be turned into opportunities when well managed.

– Junior mining sector: developing fast and purchasing procedures are lighter and easier compared to large mines. Financing is a challenge.

18.12.2015 Team Finland Mining Growth Program

7

Analysis and recommendationsCurrent suppliers and future needs

– Global (relatively high) competence for suppliers.– Finnish suppliers have a long history in Chile; Outokumpu had also its own

mine.– Finnish companies & education system are well known. This is an advantage for

new comers.– All respondents were interested in trying out new Finnish suppliers in case the

product and price are competitive.– Companies have different purchasing procedures; usually larger mines have

more complicated ones.– Main Finnish current suppliers: Outotec, Metso, Tamrock (Sandvik) and several

smaller ones. Strong local presence.– The green movement is strong among communities. The mining companies will

demand greener and improved services from its suppliers.– Need for suppliers in themes mentioned previously: innovation, training,

energy, water, recycling, pollution control, tailings, slag, etc.

18.12.2015 Team Finland Mining Growth Program

8

Analysis and recommendationsRecommendations for Finnish Companies

– Strong local presence, cooperation and active relationship management.

– SME suppliers should have cooperation with local companies.

– Identify opportunities in challenges.

– Deeper understanding of the Chilean mining industry.

– Train local staff: transfer your expertise as a long-term service.

– Organize seminars to connect with your potential clients.

– Participate local events, trade fairs and media.

– Give more attention to medium and small size mining companies.

– Create joint research with Chilean universities and mining institutions.

18.12.2015 Team Finland Mining Growth Program

9

10

Market Landscape

18.12.2015 Team Finland Mining Growth Program

Market Landscape– Chilean Mining Industry Snapshot– Mine Maps– Key Commodities– Key Mining Projects– Industry Events– Key Trends– Opportunities

18.12.2015 Team Finland Mining Growth Program

11

Market LandscapeChilean Mining Industry Snapshot

– According to government agency COCHILCO, the current mining investment portfolio stands at over US$77 billion for the period of 2015 to 2024. Mining companies have announced 53 mining projects that are in progress or undergoing review by the authorities.

– Products demanded in the mining area will reach US$2,4 billion approximately by the end of 2015, and services up to US$3,2 billion.

– China, Japan, Europe and South Korea are the principal markets for Chile’s copper exports.

– Mineral resources accounted for 59.7% of all goods and services and almost 70% of all goods exported in 2014-15.

18.12.2015 Team Finland Mining Growth Program

12

Market LandscapeChilean Mining Industry Snapshot

Chile is a strategic center for miningproduction globally, with– 33% of the world’s copper

production (1st ranking worldwide)– 53% of rhenium (1st ranking)– 15% of molybdenum (3rd ranking)– 7% of gold (13th ranking) and– 5% of silver (6th ranking)

18.12.2015 Team Finland Mining Growth Program

13

– Mining accounts for 9.6% of total GDP in Chile and was worth US$42 billion in 2014.

– Mining sector employed 240,000 in 2013-14, representing 9.7% of Chilean employment.

– 1100 mines currently in operation in Chile, as of February 2015.

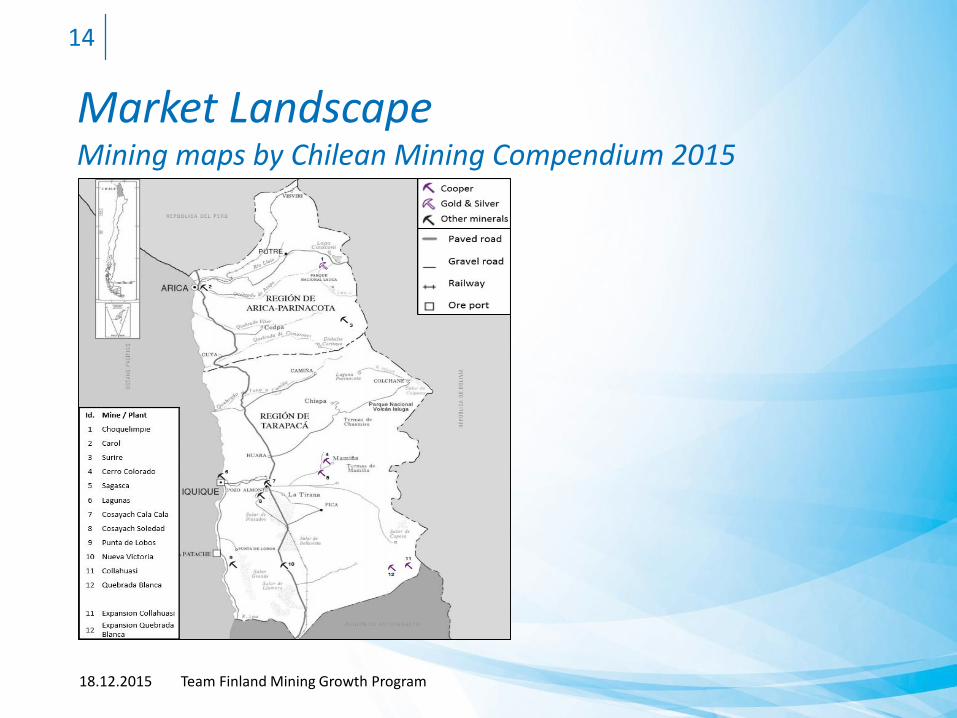

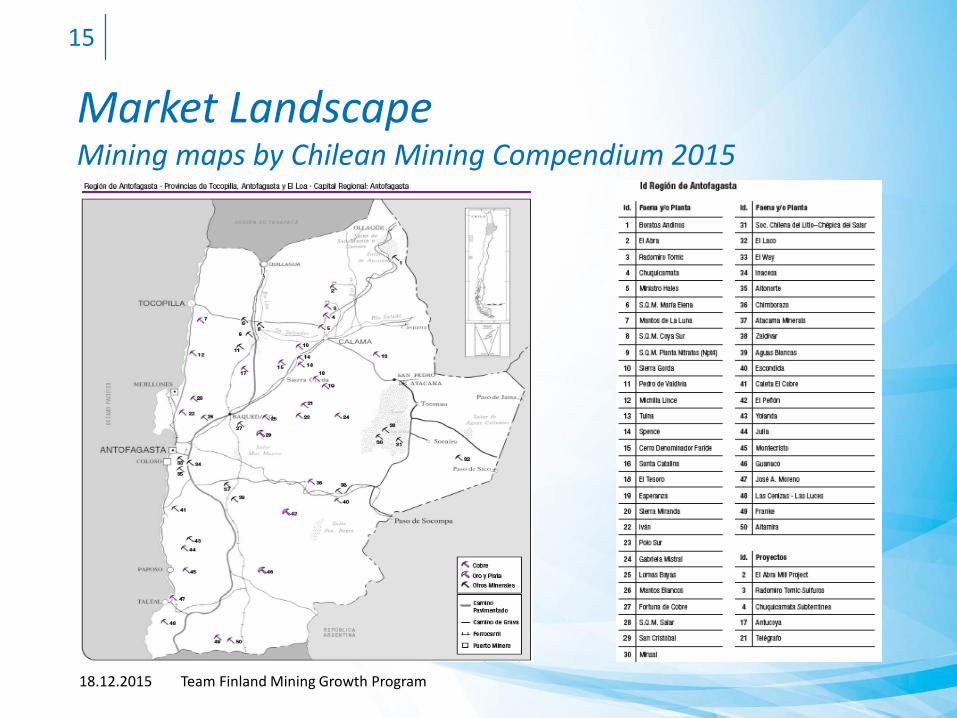

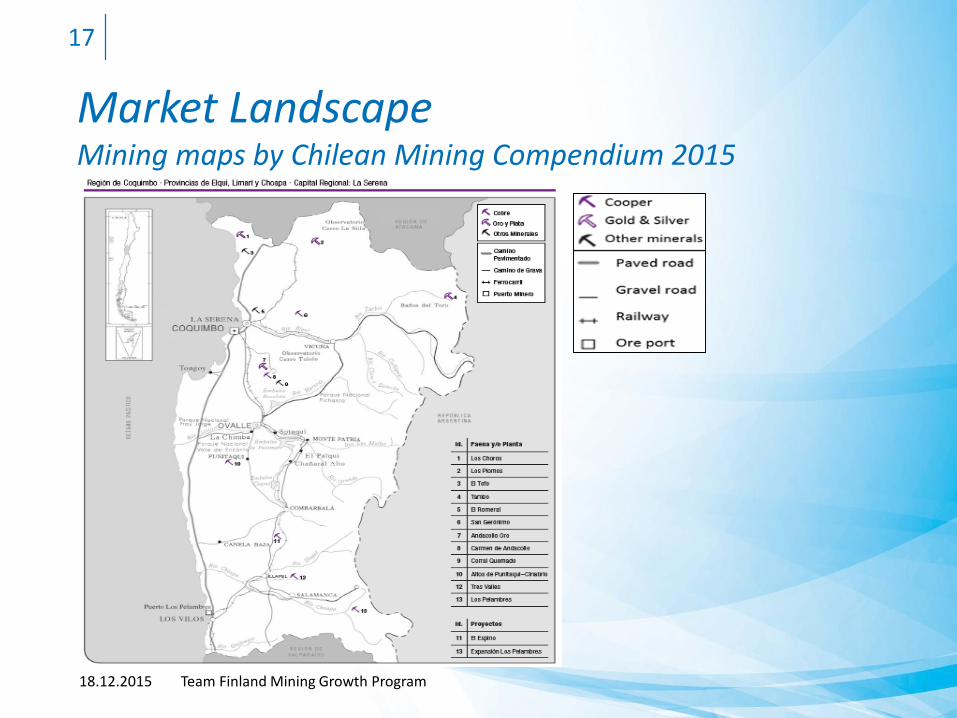

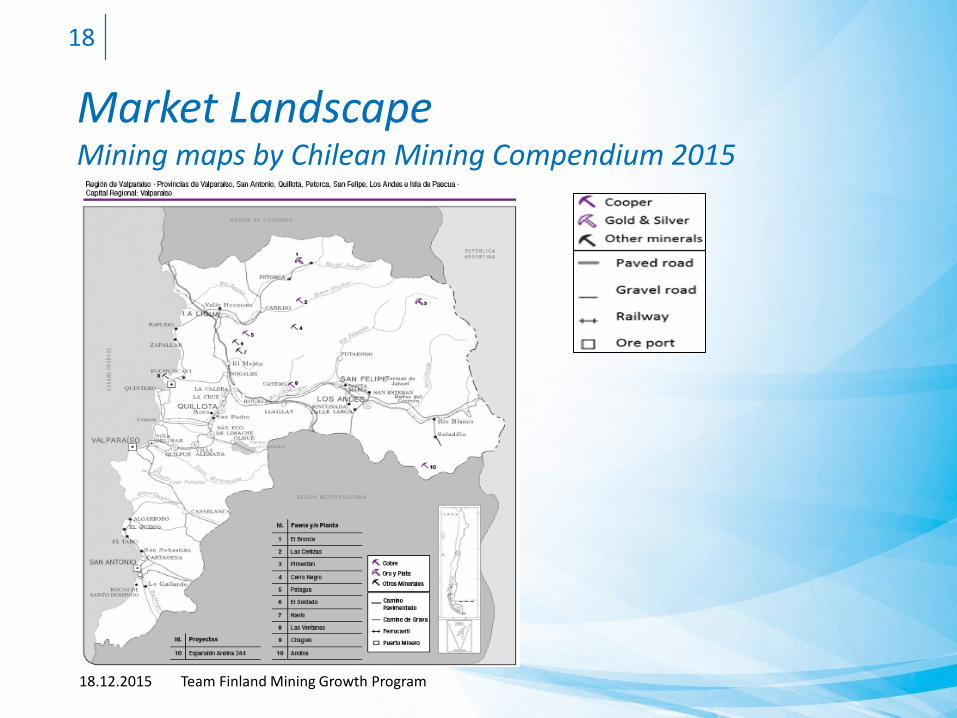

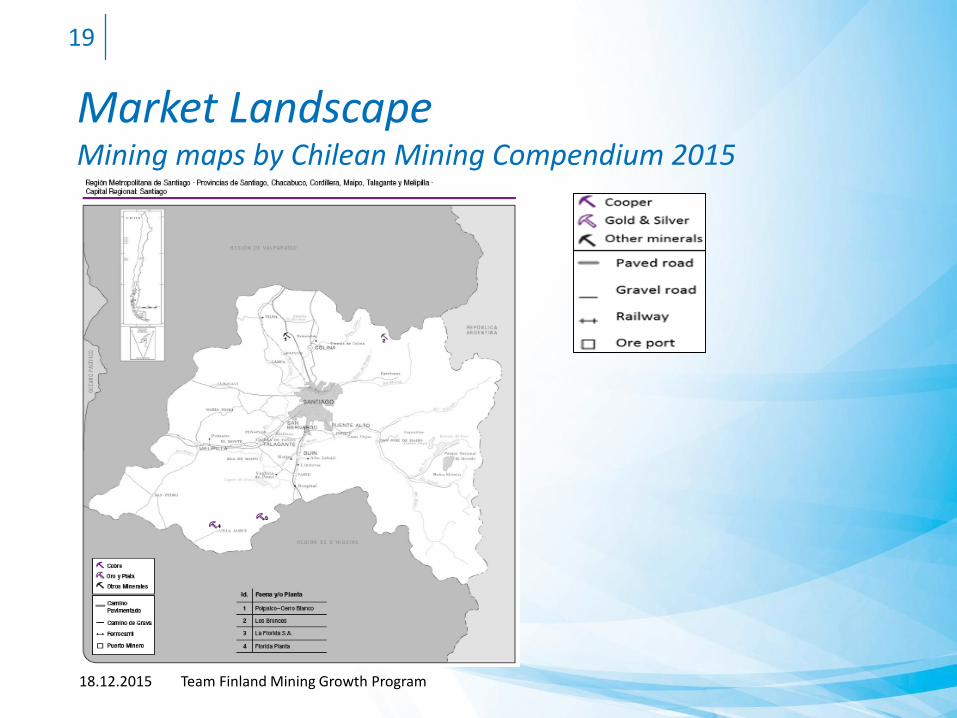

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

14

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

15

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

16

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

17

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

18

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

19

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

20

Market LandscapeMining maps by Chilean Mining Compendium 2015

18.12.2015 Team Finland Mining Growth Program

21

Market LandscapeChilean Mining Industry

Chile’s top mineral export commodities in 2014-2015

18.12.2015 Team Finland Mining Growth Program

22

ORE TYPERANKING IN WORLD

PRODUCTIONPARTICIPATION IN

WORLD PRODUCTIONPARTICIPATION INWORLD RESERVES

METALS

Copper 1o 31.1% 29.7%

Molybdenum 3o 16.0% 16.4%

Rhenium 1o 53.3% 53.0%

Silver 5o 5.8% 14.5%

Gold 18o 1.6% 7.0%

INDUSTRIAL MINERALS

Natural Nitrates 1o 100% 100.0%

Lithium 2o 35.8% 55.6%

Iodine 1o 66.4% 24.0%

Source: Editec Studies Area, based on the report “Mineral Commodity Summaries” 2015 (USGS), except the share of copper, molybdenum, silver and gold (Cochilco data).

Market LandscapeMining Industry: Main Mines in Chile 1/2

18.12.2015 Team Finland Mining Growth Program

23

MINE PRODUCTION (t) MINERALAMALIA 11,000 COOPERATACAMA KOZAN 11,800 COOPERATACAMA MINERALS 1,200 IODINECANDELARIA 168,000 COOPERCARMEN DE ANDACOLLO 75,800 COOPERCAROLA 24,000 COOPERCEMIN 18,000 COOPERCERRO COLORADO 73,600 COOPERCERRO DOMINADOR 15,000 COOPERCERRO NEGRO 7,000 COOPERCODELCO ANDINA 236,700 COOPERCODELCO EL TENIENTE 450,400 COOPERCODELCO GABY 128,200 COOPERCODELCO SALVADOR 54,200 COOPERCODELCO CHUQUICAMATA 528,000 COOPERCODELCO R TOMIC 427,000 COOPERCODELCO M HALES 163,000 COOPERCOEMIN 15,000 COOPERCOSAYACH NEGREIROS 770,000 IODINECOSAYACH SOLEDAD 770,000 IODINEDAYTON 35000 (oz) GOLDDOÑA INES DE COLLAHUASI 440,500 COOPEREL ABRA 156,600 COOPEREL ALGARROBO CMP 12,000,000 COOPEREL PEÑON 317000 (oz) GOLDEL SOLDADO 51,500 COOPEREL TESORO 120,600 COOPER

Source: Direcmin

Market LandscapeMining Industry: Main Mines in Chile 2/2

18.12.2015 Team Finland Mining Growth Program

24

MINE PRODUCTION (t) MINERALEL TOQUI 41900 (oz) GOLDESCONDIDA 1,193,000 COOPERESPERANZA 177,100 COOPERFLORIDA 89000 (oz) GOLDGUANACO 3000 (oz) GOLDLAS CENIZAS 7,000 COOPERLOMAS BAYAS 74,200 COOPERLOS BRONCES 416,000 COOPERLOS PELAMBRES 419,200 COOPERMANTOS BLANCOS 54,600 COOPERMANTOS DE LA LUNA 23,000 COOPERMANTOS DE ORO 178000 (oz) GOLDMANTOVERDE 56,800 COOPERMICHILLA 37,700 COOPEROJOS DE SALADO 23,600 COOPERPIMENTON 70000 (oz) GOLDPUCOBRE 56,000 COOPERQUEBRADA BLANCA 100,000 COOPERQUIBORAX 36,000 COOPERRAYROCK 4,500 COOPERSAN GERONIMO 9,000 COOPERSANTA FE 1,800,000 IRONSOCIEDAD CHILENA DEL LITIO 41.2 MM Lbs. LITHIUMSPENCE 151,600 COOPERTRES VALLES 19,000 COOPERVALLE CENTRAL 71,000 COOPERZALDIVAR 126,500 COOPER

Source: Direcmin

Market LandscapeMining Industry: Main Mine Projects in Chile 1/2

18.12.2015 Team Finland Mining Growth Program

25

Project Company Mineral DateLos Pelambres Extension Antofagasta Min. Copper n/aAntucoya Antofagasta Min. Copper 2015Caspiche Minera Eton Gold 2017Cerro Blanco White Mountain Titanium 2016Cerro Casale Barrick Copper 2020Copaquire PBX Ventures Copper 2017Chuquicamata Underground Codelco Copper 2019Diego de Almagro Copec Copper n/aDistrito Centinela Antofagasta Min. Copper 2017El Abra Sulfolix Freeport McMoran Copper 2018El Espino Pucobre Copper 2017El Morro Goldcorp Gold/Copper n/aEscalones South American Gold/Copper n/aEscondida Phase V BHP Billiton Copper 2015Andina Extension 244 Codelco Copper 2021Collahuasi Extension Anglo American Copper 2019

Source: Mining Market in Chile 2015, VEDP

Market LandscapeMining Industry: Main Mine Projects in Chile 2/2

18.12.2015 Team Finland Mining Growth Program

26

Project Company Mineral DateJerónimo Yamana Gold 2016La Coipa Phase VII Kinross Gold 2016Lobo Marte SCM Santa Rosa Gold 2017Lomas Bayas III Glencore Copper 2017Los Sulfatos Anglo American Copper n/aEl Teniente New Level Codelco Copper 2017Pascua Barrick Gold n/aProductora Hot Chili Ltd. Copper 2018Quebrada Blanca Phase II Teck Copper 2019Radomiro Tomic Phase II Codelco Copper 2017Relincho Teck Copper 2019San Enrique Monolito Anglo American Copper 2019Santo Domingo Capstone Mining Copper 2017Tovaku Pucobre Copper 2018Volcán Hochschild Gold 2017

Source: Mining Market in Chile 2015, VEDP

Market LandscapeMining Industry: Some Selected Smelters & Treatment Plants in Chile

18.12.2015 Team Finland Mining Growth Program

27

SMELTER OR TREATMENT PLANT PRODUCTION (TONS) MINERAL

CODELCO - VENTANS SMELTER 401,000 COOPER

ALTONORTE SMELTER 11,600 COOPER

CHAGRES SMELTER 138,600 COOPER

ENAMI - TAL TAL PLANT 2,400 COOPER

ENAMI - SALADO PLANT 9,600 COOPER

ENAMI - MATTA PLANT 7,200 COOPER

ENAMI - VALLENAR PLANT 3,600 COOPER

ENAMI - DELTA PLANT 4,800 COOPER

ENAMI - HERNAN VIDELA PLANT 90,000 COOPER

Source: Direcmin

Market LandscapeKey Commodities – Copper Production by Mining Sites 1/2

18.12.2015 Team Finland Mining Growth Program

28

RANKING MINING SITES 2008 2009 2010 2011 2012 2013 2014DIFFERENCE 2014/2013

VAR.2014/2013

CODELCO-CHILE 1,547,705 1,781,604 1,760,214 1,769,169 1,757,553 1,791,525 1,840,692 49,167 2.74%

1o (1o) CODELCO ANGLO AMERICAN SUR (20%) - - - - 35,850 93,577 87,385 -6,192 -6.62%

2 o (2 o) CODELCO EL ABRA (49%) 81,255 79,606 71,131 60,923 75,178 76,257 81,545 5,288 6.93%

TOTAL CODELCO 1,466,450 1,701,998 1,689,083 1,735,246 1,646,525 1,621,691 1,671,762 50,071 3.09%

1 o (1 o) DIVISION EL TENIENTE 381,224 404,035 403,616 400,297 417,244 450,391 455,444 5,053 1.12%

2 o (3 o) DIVISION CHUQUICAMATA 469,865 520,808 528,377 443,381 355,091 339,012 340,363 1,351 0.40%

3 o (2 o) DIVISION RADOMINO TOMIC 285,393 353,940 375,344 470,096 27,791 379,589 327,278 -52,311 -13.78%

4 o (4 o) DIVISION ANDINA 219,554 209,727 188,494 234,348 249,861 236715 232,444 -4,271 -180.00%

5 o (7 o) DIVISION MINISTRO HALES - - - - - 33,572 141,206 107,634 320.61%

6 o (5 o) DIVISION GABRIELA MISTRAL 67,732 148,026 117,052 118,078 133,000 128,170 121,012 -7,158 -5.58%

7 o (6 o) DIVISION SALVADOR 42,682 65,462 76,200 69,046 62,728 54,242 54,015 -227 -0.42%

OTHER PRODUCERS 3,861,150 3,692,402 3,729,817 3,527,554 3,787,375 4,154,309 4,077,838 -76,471 -1.84%

1 o (1 o) ESCONDIDA 1,255,019 1,102,976 1,086,701 819,262 1,075,825 1,193,680 1,171,648 -22,032 -1.85%

2 o (3 o) COLLAHUASI 464,400 535,800 504,000 453,300 282,096 444,509 470,400 25,891 5.82%

3 o (2 o) ANGO AMERICAN SUR 283,500 279,400 257,700 264,100 416,600 467,400 436,911 -30,489 -6.52%

Continue >

Source: Chilean Mining Compendium, 2015

18.12.2015 Team Finland Mining Growth Program

29

Continuation >

RANKING MINING SITES 2008 2009 2010 2011 2012 2013 2014 DIFFERENCE 2014/2013

VAR.2014/2013

4o (4o) LOS PELAMBRES 351,200 311,600 384,600 411,800 403,700 405,300 391,300 -14,000 -3.45%5o (8o) SPENCE 164,800 162,300 178,100 18,100 166,700 151,215 176,064 24,849 16.43%

6o (5o)CENTINELA CONCENTRADOS

(EXESPERANZA)- - - 90,100 163,200 174,900 172,800 -2,100 -1.20%

7o (7o) EL ABRA 166,015 162,386 145,149 124,284 153,314 155,582 166,468 10,886 7.00%8o (6o) CANDELARIA 173,500 134,263 136,078 148,325 122,924 167,829 134,700 -33,129 -19.74%

9o (10o) ANGLO AMERICAN NORTE 148,900 151,700 139,700 130,800 116,500 111400 104,200 -7,200 -6.46%10o (9o) ZALDIVAR 133,500 13,700 144,400 132,300 131,100 126,500 100,600 -25,900 -20.47%

11o (11o)CENTINELA CATODOS

(EX - EL TESORO)90,800 90,200 95,300 97,064 105,008 105,600 93,800 -11,800 -11.17%

12o (14o) CERRO COLORADO 104,200 93,700 89,000 94,300 73,100 73,211 79,574 6,363 8.69%13o (12o) CARMEN DE ANDACOLLO 21,100 17,900 45,100 72,400 79,800 81,200 71,800 -9,400 -11.58%14o (13o) LOMAS BAYAS 59,200 73,100 71,800 73,600 73,299 74,200 66,600 -7,600 -10.24%15o (15o) QUEBRADA BLANCA 85,400 87,400 86,200 63,400 62,400 56,200 48,000 -8,200 -14.59%16o (16o) MICHILLA 47,700 40,600 41,200 41,600 37,700 38,300 47,000 8,700 22.72%17o (18o) CASERONES - - - - - 16,200 44,600 28,400 175.31%18o (17o) OJOS DE SALADO 28,576 33,566 29,937 26,308 24,040 23,587 22,226 -1,361 -5.77%19o (--) SIERRA GORDA - - - - - - 12,700 - -

OTHERS 283,340 278,511 294,851 303,610 300,069 290,496 266,447 -24,049 -8.28%TOTAL CHILE 5,327,600 5,394,400 5,418,900 5,262,800 5,433,900 5,776,000 5,749,600 -26,400 -0.46%

Source: Chilean Mining Compendium, 2015

Market LandscapeKey Commodities – Copper Production by Mining Sites 1/2

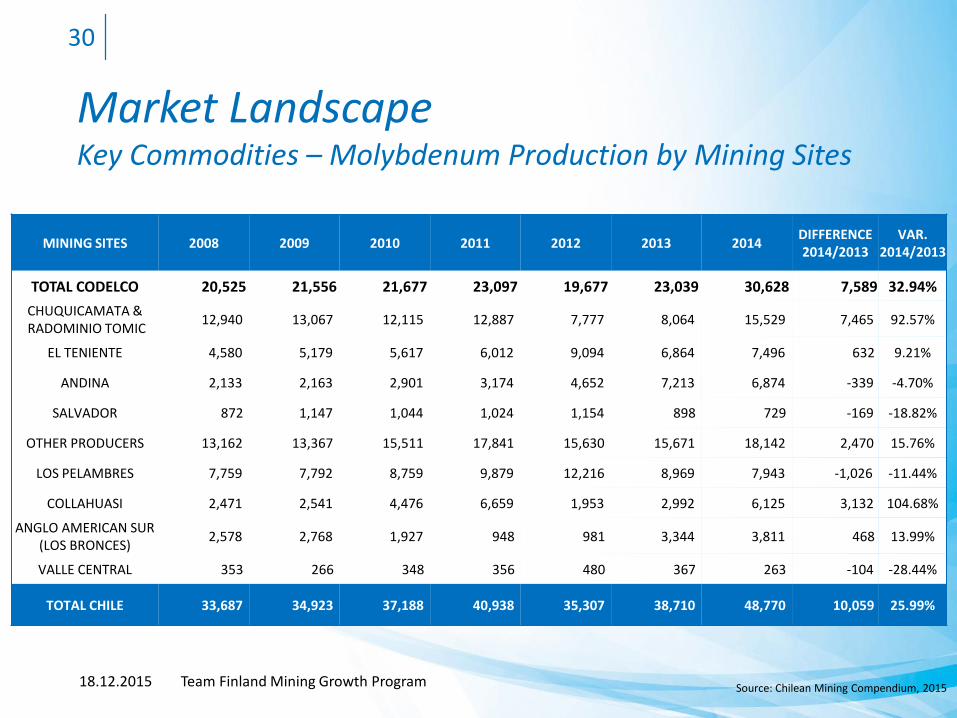

Market LandscapeKey Commodities – Molybdenum Production by Mining Sites

18.12.2015 Team Finland Mining Growth Program

30

MINING SITES 2008 2009 2010 2011 2012 2013 2014 DIFFERENCE 2014/2013

VAR. 2014/2013

TOTAL CODELCO 20,525 21,556 21,677 23,097 19,677 23,039 30,628 7,589 32.94%CHUQUICAMATA &RADOMINIO TOMIC 12,940 13,067 12,115 12,887 7,777 8,064 15,529 7,465 92.57%

EL TENIENTE 4,580 5,179 5,617 6,012 9,094 6,864 7,496 632 9.21%

ANDINA 2,133 2,163 2,901 3,174 4,652 7,213 6,874 -339 -4.70%

SALVADOR 872 1,147 1,044 1,024 1,154 898 729 -169 -18.82%

OTHER PRODUCERS 13,162 13,367 15,511 17,841 15,630 15,671 18,142 2,470 15.76%

LOS PELAMBRES 7,759 7,792 8,759 9,879 12,216 8,969 7,943 -1,026 -11.44%

COLLAHUASI 2,471 2,541 4,476 6,659 1,953 2,992 6,125 3,132 104.68%

ANGLO AMERICAN SUR (LOS BRONCES) 2,578 2,768 1,927 948 981 3,344 3,811 468 13.99%

VALLE CENTRAL 353 266 348 356 480 367 263 -104 -28.44%

TOTAL CHILE 33,687 34,923 37,188 40,938 35,307 38,710 48,770 10,059 25.99%

Source: Chilean Mining Compendium, 2015

Market LandscapeKey Commodities – Gold (Projects 1/2)

18.12.2015 Team Finland Mining Growth Program

31

PROJECT OWNERS OPERATORSTART-UP

YEARINVESTMENT

(MMUS$)

GOLD PRODUCTION(kg Au CONT.)

GOLD MINING (REPLACEMENT PRIMARY PRODUCTION)

JERONIMO 56.72% MINERA MERIDIAN43.28% CODELCO AGUA DE LA FALDA S.A 2016 423 4,665

EXPLOTACION DE MINERALESLA COIPA FASE 7 100% KINROSS GOLD CORP. COMPAÑÍA MINERA

MANTOS DE ORO 2017 200 6,220

GOLD MINING (ADDITIONAL PRIMARY PRODUCTION)

NUEVA ESPERANZA(EX ARQUEROS)

100% KINGSGATE INT. LAGUNA RESOURCES CHILE 2016 150 500

PASCUA-LAMA 100% BARRICK GOLD CORP. CIA. MINERA NEVADA 2016 4250 19,830

CASPICHE OXIDOS100% EXETER RESOURCE CORP.

ETON CHILE 2017 344 4,600

CERRO MARICUNGA100% ATACAMA PACIFIC GOLD CORP.

ATACAMA PACIFIC GOLD CHILE

2017 515 9,269

VOLCAN90.84% HOCHSCHILD MINING9.16% ANDINA MINERALS CHILE LTDA.

ANDINA MINERALS CHILE 2019 800 8,800

LOBO MARTE 100% KINROSS GOLD CORP. MINERA SANTA ROSA 2019 800 10,890

CERRO CASALE70% BARRICK GOLD CORP.30% KINROSS GOLD CORP.

MINERA CASALE 2020 6000 34,133

EL MORRO70% GOLDCORP INC.30% NEW GOLD

EL MORRO SCM 2021 3900 11,000

Source: Chilean Mining Compendium, 2015

Market LandscapeKey Commodities – Gold (Projects 2/2)

18.12.2015 Team Finland Mining Growth Program

32

PROJECT OWNERS OPERATORSTART-

UPYEAR

INVESTMENT

MMUS$

GOLD PRODUCTION(kg Au CONT.)

COOPER MINING (ADDITIONAL SECONDARY PRODUCTION)

SIERRA GORDA55% KGHM INTERNATIONAL LTDA.45% SMITOMO GROUP COMPANIES

SIERRA GORDA SCM 2014 4240 1928

PLANTA RECUPERADORADE METALES

66% LS-NIKKO34% CODELCO

PLANTA RECUPERADORA DE METALES SPA

2016 98 5000

SANTO DOMINGO70% CAPSTONE MINING CORP.30% COREA RESOURCES CORP.

MINERA SANTO DOMINGO 2017 1700 1493

EL ESPINO 100% PUROCOBRE EL ESPINO S.A 217 624 780

PRODUCTORA99.9% HOT CHILI0.1% KALGOORLIE AUTO SERVICEPTY LTDA.

SOCIEDAD MINERA EL AGUILALTDA.

2018 700 1307

DIEGO DE ALMAGRO 100% GRUPO COPECCOMPAÑÍA MINERA SIERRANORTE S.A

2018 597 713

INCA DE ORO60.45% PANAUST34% CODELCO5.55% OTHER INVESTORS

INCA DE ORO S.A. 2019 600 1244

ENCUENTRO DE SULFUROS(DISTRITO CENTINELA)

100% ANTOFAGASTA MINERALS S.A

MINERA ENCUETRO 2020 2700 4670

TOTAL CONTRIBUTION TO PRODUCTION PERIODS 2014-2020 116,157TOTAL INVESTMENT, PERIODS 2014-2015 (MMUS$ ) 28,016

Source: Chilean Mining Compendium, 2015

Market LandscapeKey Commodities – Silver production by Mining Sites

18.12.2015 Team Finland Mining Growth Program

33

RANKING MINING SITES 2009 2010 2011 2012 2013 2014DIFFERENCE2014/2013

VAR.2014/2013

1o (1 o) EL PEÑON 9,820,475 9,427,208 847,011 7,246,951 6,464,623 8,475,133 2,010,510 31.1%

2 o (11 o) CODELCO MINISTRO HALES - - - - 374,170 8,021,412 7,647,242 2043.8%

3 o (3) CODELCO CHUQUICAMATA - 7,316,733 6,774,479 3,437,780 3,208,321 6,010,288 2,801,968 87.3%

4 o (4 o) ESCONDIDA 4,808,696 4,998,261 4,954,783 3,340,870 2,960,000 4,271,000 1,311,000 44.3%

5 o (7 o) CODELCO EL TENIENTE - 2,526,050 2,629,125 2,661,147 2,957,063 3,109,682 152,619 5.2%

6 o (2 o) CERRO BAYO - - 1,318,665 2,959,289 3260057 3,450,979 190,922 5.9%

- (6o) LA COIPA 5,219,000 4,154,000 4,520,000 3,882,000 2,906,000 - -2,906,000 -100.0%

7 o (7 o) CODELCO ANDINA - 1,515,039 1,897,536 2,008,295 1,902,648 1,868,311 -34,337 -1.8%

8 o (9 o) CODELCO SALVADOR - 1,313,389 1,339,528 1,029,145 876,815 1,412,638 535,824 61.1%

9 o (8 o) MINERA FLORIDA 652,192 606,071 791,173 825,812 979,514 975,297 -4,217 -0.4%

- (10o) TALCUNA - 352,368 386,886 436,454 521,917 s/a - -

10 o (12 o) EL TOQUI 233,382 118,754 122,612 113,000 141,000 313,000 172,000 122.0%

- (-) LOS PELAMBRES - 1,470,800 1,774,300 1,832,591 s/a s/a - -

- (-)CENTINELA CONCENTRADOS

(EXESPERANZA)- - 724,300 1,323,200 s/a s/a - -

TOTAL CHILE 41,828,669 41,367,949 41,515,328 38,404,713 37,739,965 50,534,120 12,794,155 33.9%

Source: Chilean Mining Compendium, 2015

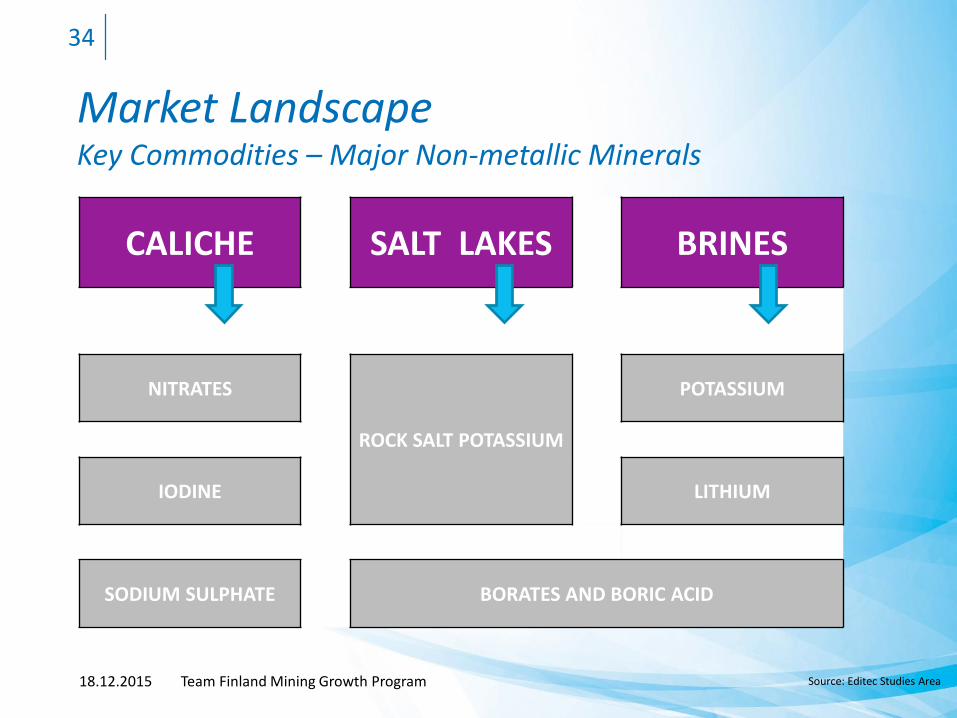

Market LandscapeKey Commodities – Major Non-metallic Minerals

18.12.2015 Team Finland Mining Growth Program

34

CALICHE SALT LAKES BRINES

NITRATES

ROCK SALT POTASSIUM

POTASSIUM

IODINE LITHIUM

SODIUM SULPHATE BORATES AND BORIC ACID

Source: Editec Studies Area

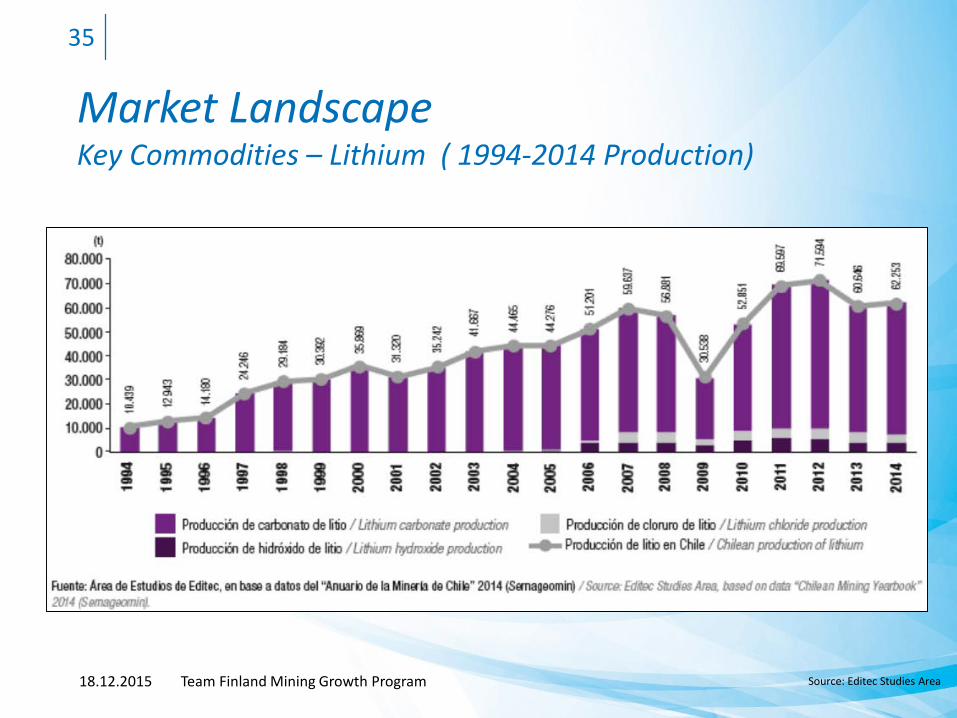

Market LandscapeKey Commodities – Lithium ( 1994-2014 Production)

18.12.2015 Team Finland Mining Growth Program

35

Source: Editec Studies Area

Market LandscapeUpcoming Key Industry Events in Chile

EVENT INSTITUTION FREQUENCY

IX Foro Internacional de Exploración, APRIL 2016 CESCO EVERY YEAR

15ava Conferencia Mundial del Cobre, APRIL 2016 CRU/CESCO EVERY YEAR

Seminario Proveedores Mineros, APRIL 2016 CESCO EVERY YEAR

Expomin, APRIL 2016 FISA EVERY 2 YEARS

Mine Excellence, APRIL 2016 GECAMIN EVERY YEAR

EXPONOR CHILE, Antofagasta, MAY 2017 AIA EVERY 2 YEARS

18.12.2015 Team Finland Mining Growth Program

36

Market Landscape Key Trends for Chile

– Chile currently ranks 40th (out of 145 countries) in the World Bank´s Knowledge Economy Index; the highest ranking of any Latin American country and 4th out of 34 upper-middle income countries.

– Chile depends on imported mining technology, equipment and services (METS) imports. It is an attractive destination to other leading METS exporters such as Canada and Australia.

– Chile seeks to decrease its dependence on METS exports. A joint initiative by the Chilean government, BHP Billiton and Codelco - the “World Class Providers Program” - aims to increase mining innovations and service exports. This development trend offers a great opportunity to further develop the mining service sector.

– Chile is very dependent on its copper exports and the global copper price. Developing a diverse mining sector, including services, would help to diversify the economy. This would contribute to strengthening Chile as more than a resource-based export economy.

18.12.2015 Team Finland Mining Growth Program

37

Source: The Future of Mining in Chile/CSIRO

Market Landscape Key Trends for Chile

– Chile has a strong commitment to global free trade. Developing a service-based export economy would align with this long-term vision.

– Recycling and other substitutes for copper have the potential to create new and increased competition for Chile´s mining industry.

– Lack of knowledge in recycling of copper: Chile has significant expertise in copper mining, one of the most recyclable materials, but has little expertise in recycling it.

18.12.2015 Team Finland Mining Growth Program

38

Source: The Future of Mining in Chile/CSIRO

Market LandscapeOpportunities – General Overview

Specific areas where the Chilean mining market needs support include:

– Environment-related products and services (tailing management, water treatment plants, software)

– Renewable energies

– Communities and research & development

– Underground mining and specialty block-caving

– Safety in mining

– Automation and robotics

– Land rehabilitation and mine closure

– Energy infrastructure

– Education and training for the industry

18.12.2015 Team Finland Mining Growth Program

39

Source: Mining Market in Chile 2015, VEDP

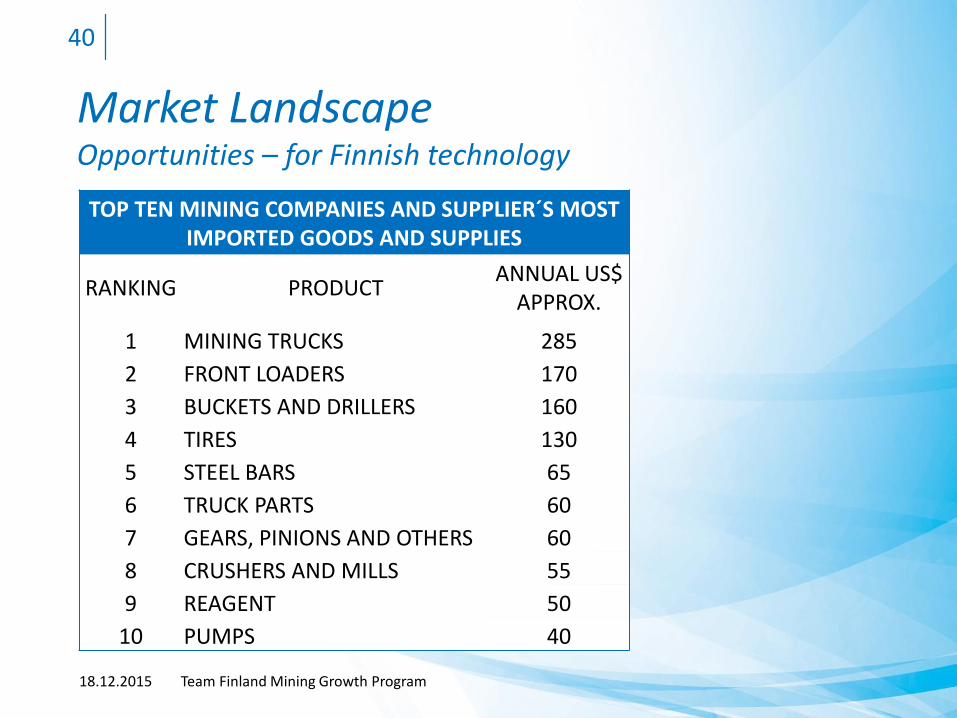

Market Landscape Opportunities – for Finnish technology

18.12.2015 Team Finland Mining Growth Program

40

TOP TEN MINING COMPANIES AND SUPPLIER´S MOSTIMPORTED GOODS AND SUPPLIES

RANKING PRODUCT ANNUAL US$ APPROX.

1 MINING TRUCKS 2852 FRONT LOADERS 1703 BUCKETS AND DRILLERS 1604 TIRES 1305 STEEL BARS 656 TRUCK PARTS 607 GEARS, PINIONS AND OTHERS 608 CRUSHERS AND MILLS 559 REAGENT 50

10 PUMPS 40

Market Landscape Opportunities – for Finnish technology

Other important goods and supplies in the mining industry are:– Diesel engines– Sulphur acid– Filters– Valves and appliances– Spare parts and parts of fans and air compressors– Diesel motor parts and replacements– Electric engines– Drilling machines– Converters, transformers and parts– Nuts, bolts, pins, and plugs– The main country of origin is the US, representing 55% of all imports of mining

goods and supplies.

18.12.2015 Team Finland Mining Growth Program

41

Source: Mining Market in Chile 2015, VEDP

Market Landscape Opportunities for Finnish technology

ENGINEERING– Over 20 engineering companies operate in Chile, representing annual sales of

more than US$ 45 million, and 75% have foreign capital.– Mining accounts for 57% of the demand.– There is a portfolio of projects worth US$ 105 billion.– The increase in operating costs calls for innovative solutions.– Mine closure law.

Value of the Opportunity:– Demand of engineering is estimated to reach over US$ 36 billion in 2014-2020.– A similar value is estimated for sectors other than mining.– Construction work and equipment related to engineering companies may

represent a further US$ 29 billion.– Engineering for closure plans may reach US$ 20 million.

18.12.2015 Team Finland Mining Growth Program

42

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

UNDERGROUND EQUIPMENT– Much of the technology used is not developed locally.– This equipment is used in a few larger mines but not in many small and mid-

sized mines. The most used items are low-profile front loaders and Jumbo drills.– Over the past five years, around 250 LHD loaders have been imported.

Value of the Opportunity:– It is estimated that over 850 LHD loaders will be acquired between 2014-2020.– Provision of LHD equipment can be expanded to include supply of Jumbo drills

and tippers.– The total value reaches over US$ 535 million.

18.12.2015 Team Finland Mining Growth Program

43

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

CONVEYOR BELTS – At present, an estimated 88% of conveyor belts supplied to the Chilean

mining industry are imported and even local products correspond to international brands produced directly in Chile.

– The total market has an annual value of approximately US$ 90 million.– There is an opportunity for manufacturing and marketing related to

services.

Value of the Opportunity:– Installed capacity of conveyor belts in Chile will reach over 501,000 meters

by 2020.– Purchases in 2014-2020 will reach US$ 686 million.

18.12.2015 Team Finland Mining Growth Program

44

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

MILL BALLS– The market has an estimated annual value of US$ 800 million.– Over 95% of the market is supplied by multinational companies with plants in

Chile.– This is an expanding market undergoing structural changes: mergers and

acquisitions. – Products need to cost less, last longer and be more sustainable.

Value of the Opportunity:– Accumulated demand for mill balls in Chile will reach over 3,2 million tones in

2014-2020.– Purchases in 2014-2020 could reach US$ 6,7 billion.

18.12.2015 Team Finland Mining Growth Program

45

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

EXPLOSIVES

– Demand for explosives and specifically, ammonium nitrate in Chile reaches almost 650,000 tones per year, equivalent to some US$ 360 million.

– Growing output combined with lower ore grades implies estimated annual growth of over 5% in 2014-2020.

Value of the Opportunity:

– Purchases of explosives in 2014- 2020 will reach US$ 3 billion.

– Services related to rock fragmentation are estimated to be worth 10% of the value of explosives.

18.12.2015 Team Finland Mining Growth Program

46

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

REAGENTS – FLOTATION

– Growing output of concentrate combined with lower ore grades and the increasing use of thickened tailings implies estimated annual growth of over 10% in 2014-2020.

Value of the Opportunity:

– Purchases of flocculants alone are estimated to reach US$ 1,5 billion in 2014-2020.

18.12.2015 Team Finland Mining Growth Program

47

Source: Foreign Investment Committee

Market LandscapeOpportunities for Finnish technology

TRAINING

– At present, large-scale mining companies devote approximately US$ 35 million to training.

– It is estimated that over 52,000 operators will need to be trained for the mining industry by 2020.

– Market without leadership.

Value of the Opportunity:

– Training in the sector will be worth over US$ 200 million in 2014-2020.

18.12.2015 Team Finland Mining Growth Program

48

Source: Foreign Investment Committee

49

Market Specific Issues

18.12.2015 Team Finland Mining Growth Program

Market Specific IssuesRegulatory Environment & Regulations

– REGULATORY EFFICIENCY The regulatory regime sustains business formation and operation. Starting a business takes seven procedures and six days on average and costs less than one per cent of the level of average annual income. Labor regulations are rigid, with broad wage settlements and high unionization. Government price supports for agriculture are less than five per cent of total farm receipts, one of the lowest rates among OECD countries.

– OPEN MARKETS Chile has a 4.0 per cent average tariff rate. Most imports enter duty-free, and tariffs have been reduced through the Pacific Alliance. Chile is very open to foreign investment. A well-capitalized and dynamic banking sector provides a wide range of services, and the financial system remains one of the region’s most advanced. Credit is issued on market terms, and domestic and foreign financial firms receive equal treatment.

– RULE OF LAW Chile is among South America’s least corrupted countries. Courts are generally free from political interference. Although President Bachelet campaigned in 2013 on a promise to reform the constitution, adopted in 1980 during the return to democratic self-government, Chile most likely will retain its independent and competent judiciary. Property rights and contracts are strongly respected, and expropriation is rare.

18.12.2015 Team Finland Mining Growth Program

50

Market Specific Issues Challenges facing the mining industry

1. Geological Conditions– Mines are getting old -> Lower ore grades, deeper mines, longer hauling distances2. Human Capital– In the year 2020 large-scale copper mining will demand 64% more workers– Critical factors: costs, recruitment, training and maintenance3. Communities:– Environmental awareness– “Chileans are satisfied with their lives, but critical towards society” – UNDP4. Water management - Use of sea water– New projects demand more water in arid areas.– Critical factors: costs, diversification of sources (seawater), reuse.5. Energy Management - Energy consumption– By the year 2020, the copper mining industry will need additional electric power of 3,000

MW in order to produce 39.4 TWh, 80% more than in 2010.– Critical factors: Costs, matrix diversification, development of NCRE (Non Conventional

Renewable Energy) and energy efficiency

Sources: Ministry of Mining & expert interviews18.12.2015 Team Finland Mining Growth Program

51

Market Specific IssuesOther challenges, competitive situation, operative models

– Expertise in closing down mines: New requirements were introduced in 2011 for closing down mines. In 2014 more than 100 mines submitted their closure plans which add up to US$12 billion.

– Smelters must be upgraded: New emission standards were introduced in 2013. In order to meet the regulations, the smelters require major investments in their acid plants and infrastructure. There are seven smelters with production of 1.6 M tons of anode.

– Need for skilled work force: More than 27,000 jobs are estimated to be generated by the mining industry in the near future (2016-2023).

– Competition: All the main suppliers have a strong presence through local subsidiaries. Some countries (Germany, South Korea, Japan) support their companies through different marketing and higher-level actions. Chinese companies are entering the market yet without strong success.

– Operative models are quite variable: Large companies usually have a direct presence, while medium and smaller companies prefer to associate with local organizations.

18.12.2015 Team Finland Mining Growth Program

52

Market Specific IssuesKey Players – Mining Companies in Chile 1/2

– Amerigo Resources Ltd.

– Anglo American Plc.

– Antofagasta Minerals Plc.

– Apogee Silver ltd.

– Atacama Minerals Corp.

– Atacama Pacific Gold Corp.

– Barrick Gold Corp.

– BHP Billiton

– CAP S.A.

– Capstone Mining Corp.

– Compañía Minera Candelaria

– CODELCO

– Endeavour Silver Corp.

– Freeport-McMoran Copper

– Glencore Xstrata

– Goldcorp Inc.

18.12.2015 Team Finland Mining Growth Program

53

Source: KPMG Global Mining Institute

Market Specific IssuesKey Players – Mining Companies in Chile 2/2

– Kinross Gold Corp.

– Lachlan Star Ltd.

– Minera Antucoya

– Minera Centinela

– Minera Michilla S.A.

– Molibdeno y Metales S.A.

– New Gold Inc.

– Polar Star Mining Corp.

– Rio Tinto

– Sierra Gorda SCM.

– SQM Industrial S.A.

– Soc. Punta del Cobre S.A.

– Teck Resources Ltd.

– Yamana Gold Inc.

18.12.2015 Team Finland Mining Growth Program

54

Source: KPMG Global Mining Institute

Market Specific IssuesKey Players – Medium-Small Size Mining Snapshot in Chile

– Medium–Small Size Mining in Chile represents mine operations producing 1,200 to 49.000 t/year fine copper.

– Sector total yearly production: approx. 350.000t/ fine Cu.

– Most of the production sold to ENAMI (Chilean National Mining Corporation, which promotes small and medium size private sector mining).

– Several projects available for development or expansion (US$ 3 million investment in total).

18.12.2015 Team Finland Mining Growth Program

55

– Medium-Small size mining sector represents some 100.000 employees.

– Currently they have special needs for the following issues:

– Water, energy, productivity, innovation, modern equipment and well trained people.

– Financing is a key element for this sector.

– The size of the medium mining is quite similar to the Finnish mining industry.

Market Specific IssuesValue Chain

There are five core stages in the Chilean mining value chain

18.12.2015 Team Finland Mining Growth Program

56

Stage/Process OpportunitiesGeoscience Research and Development (R&D)

Exploration Exploration, joint ventures, R&D, Mining Equipment, technology and Services (METS)

Developing Projects Partnership agreements, R&D, METS

Mining Mergers, product purchase and sale, R&D productivity, METS

Processing (ore purchase and product upgrade for premium sales)

R&D productivity and sales ability, METS

57

Section 3Expert Interviews and

comments from Finnish companies

18.12.2015 Team Finland Mining Growth Program

Expert Interviews

18.12.2015 Team Finland Mining Growth Program

58

No. NAME OF THE COMPANY/ORGANIZATION

SIZE (S/L/M) NAME TITLE EMAIL PHONE ADDRESS

1 Universidad Católica Valparaíso Marco Alfaro

Director Ingenieríade Minas

[email protected] 56 32 227 3737 General Cruz 34, Valparaiso

2 Codelco L Alvaro Puig Gerente Técnico [email protected] 56 2 2690 3000 Huerfanos 1270, piso 8,

Santiago

3 ENAMI L Ivan Fortín Gerente Comercial [email protected] 562 2 435 5000 Mac Iver 459 , Santiago

4 Centro de EstudiosMinerales Consulting Edmundo

TulcanazaDirector Ejecutivo [email protected] 56 9 6303 2659 General Cruz 151 ,

Valparaiso

5 Next Minerals S Nicolás Fuster Gerente [email protected] 56 2 224 53160 Av. Presidente Riesco 5335 of 602, Santiago

6 Santiago Metals S Waldo Cuadra Presidente [email protected] 562 2653 7280 Lo Fontecilla 201 , of.

534, Santiago

7 Ingetesa Consulting Helios Corvalán

Gerente General [email protected] 56 02 2638 3745 Mosqueto 491, of.212,

Santiago

Company info - State owned Major Copper company , largest copper producer.- Seven mines Divisions ( Chuquicamata, El Abra, Radomiro Tomic, Ministro Hales,

Gabriela Mistral, El Salvador , Andina , El Teniente mines) plus de Ventanas Smelter ( since 2005).

- Main products : Copper & Molybdenum.- Adjusted EBITDA achieved US$ 5.4 bn ( 2014).- Sales 2014 : US$ 13,827 million.

Trends / Drivers - Biggest ongoing projects : Chuquicamata Underground (US$ 4.2 bn) , RT sulfides phase II( US$ 5.4 bn), Andina Reallocation, El Teniente new mine level (US$ 3.4 bn), Salvador Inca pit and Andina Expansion.

- Main trends and drivers are Efficient mining production and Production increases.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

59

Codelco

Concerns / Development areas

- Main concerns: Mining costs and innovation of exploration, development and production activities. Lack of innovated products and services to improve productivity and reduce production costs.

- Products or services of greatest interest are Mining equipment and new exploration tools.

- Main development areas are new projects & mining productivity.

Suppliers - Familiar with Finnish suppliers (e.g. Outotec )- Products or services selection : Reviewing the Suppliers and Services market.

Selecting those with a better professional history. - Main strengths that are searched: Quality and Service level.- Currently looking for new suppliers in Underground mining, Smelters and

Exploration projects.- Preference for local based companies.- Essential Requirements /prerequisites for (new) suppliers are: Professional quality

and good services record.

Recommendations - Local presence, broad knowledge of Chile´s mining situation. - Areas to expand: innovation on mining productivity, smelters, people training,

exploration tools.- Direct contacts with clients. Publications in magazines.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

60

Codelco

Company info - State owned agency. Service Provider: Minerals Purchase and Treatment to produce refined copper and by products in their plants and smelter. ENAMI’s assets include one smelter, five processing plants, purchasing agencies, and a network of technical support and technology transference facilities, focused on some 2.000 small size private sector producers of copper and precious metals.

Trends / Drivers - To promote small and medium size private sector mining by providing incentives aimed at correcting market failures, and supplying technical, financial, metallurgical production and trading services. ENAMI´s incentives and services enable small and medium size mining firms to access international metal markets, and thus to benefit from the better position of ENAMI to attain competitive “economies of scale” and “economies of scope”. Renewal of the Paipote Smelter. Normal maintenance of their five processing plants. Completion of the Delta project (flotation plant expansion).

Concerns - Economic downturn and metal prices- Lack of credits for medium/small size producers.- Additional innovation for medium size mines and plants.- Tailings and dumps materials handling.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

61

Enami

Development areas - Renewal of the Paipote Smelter. - Normal maintenance of their five processing plants. - Completion of the Delta project (flotation plant expansion). - Development of small and medium size private mining operations in Chile.

Suppliers - Enami´s purchase procedures: Each unit (plants and smelters) indicate their own needs Then a public bidding process must be established.

- Main strengths of Enami's suppliers are Quality and costs. - Enami is looking for new suppliers for renewal of the smelter and tailings re-

processing:- Preference for companies that are well established in Chile OR with official

representation.- Prerequisites for (new) suppliers are: Quality and competitive prices. Hopefully with

some credit facilities.

Recommendations - Market areas to expand: Smelters, tailings treatment, innovation and robotics.- For foreign companies wishing to enter the market: “Launch your products/services

in the country by sending a delegation and organizing a seminar to present products & services.”

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

62

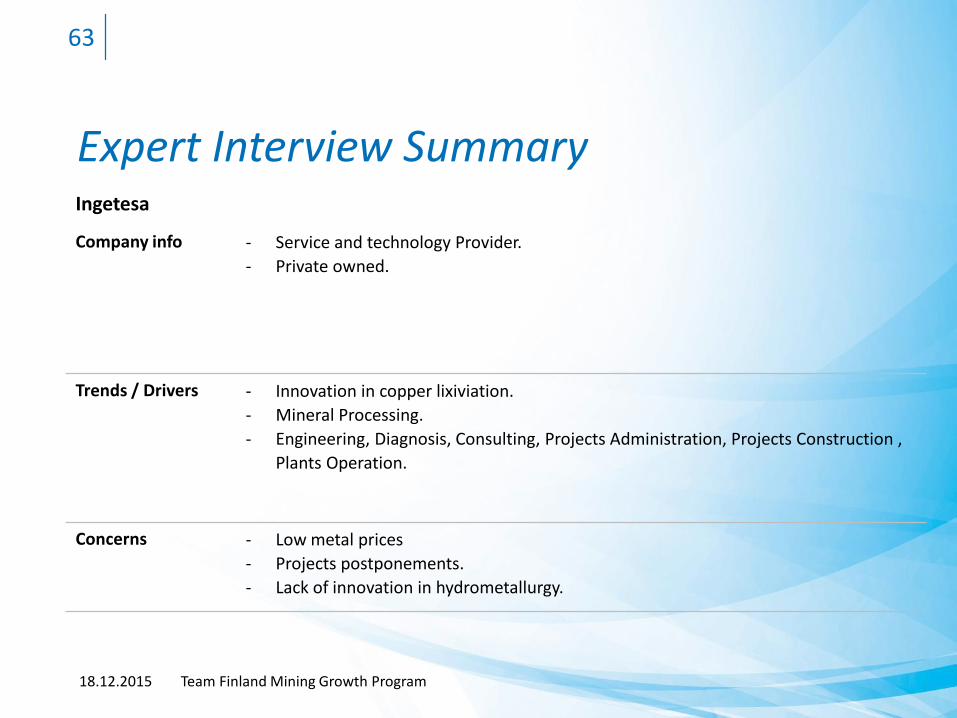

Enami

Company info - Service and technology Provider.- Private owned.

Trends / Drivers - Innovation in copper lixiviation.- Mineral Processing.- Engineering, Diagnosis, Consulting, Projects Administration, Projects Construction ,

Plants Operation.

Concerns - Low metal prices- Projects postponements.- Lack of innovation in hydrometallurgy.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

63

Ingetesa

Development areas - Biggest ongoing projects at the moment: SX Unit to produce Copper Sulfates.- Planned and/or in study phase investment projects in next five years: Several

Metallurgical project, mainly copper lixiviation.

Suppliers - Products or services occur following the project needs as well as client preferences. - Main strengths of potential suppliers are quality, prices and local service availability.- Looking for new suppliers related to our current or future projects.- Preferences for local based companies to secure guarantee and services.- Key requirements /prerequisites for (new) suppliers are reputation and professional

experience. - Ready to consider new suppliers from Finland if they could provide the needed

quality with competitive prices.

Recommendations - Increase the understanding of future needs in the Chilean mining industry.- Consider: mineral processing; tailings treatment. New environmental services.- New environmental services.- Augment presence in important mining exhibitions.- Organization of specific products/services presentations or mining seminars.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

64

Ingetesa

Company info - Junior Exploration and Mining Company.- Private.- Investment in exploration and development for medium size mining projects ( Cu,

Au, Fe).

Trends / Drivers - Continue exploration efforts plus development of one medium size Cu, Au, Fe project.

- Medium size metals mining.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

65

NEXT Minerals

Concerns / Development areas

- Lack of credits to fund medium size project development. - Currently there is restriction in investment sources. Medium size mining includes

much more projects availability.- Equipment and Processing Plants adjusted to scale of medium to small size mining. It

also apply to drilling.- Exploration/acquisition program in Central and Northern Chile. - Evaluation of old mining districts.- Continue exploration efforts plus development of one medium size Cu, Au, Fe

project.

Suppliers - Purchase the products or services adjusted to the project size needs. - Suppliers to stand out from the competition are those with accessible prices

providing needed quality.- Next Minerals prefers local, based product/services to secure guarantee and long

term service and maintenance.- Basic requirements for new suppliers are good knowledge of the medium size

mining industry in Chile. Coupled with good prices and related credit lines, when possible.

Recommendations - To study current status and needs in the medium size mining level. Provide the needed information to potential customers (e.g. recommendation to organize an info seminar).

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

66

NEXT Minerals

Company info - Junior Exploration and Mining Company .- Private funds. - Copper project development plus grass root exploration on tenements with high

chance of success .- Northern Chile ( III Region near Inca de Oro).

Trends / Drivers - Copper project ( Planta Chatal) near Inca de Oro to produce 8,000 t/y cathodes (EXSW).

- Complete the new plant and initiate production. - Produce copper cathodes and exploration for new deposits.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

67

Santiago Metals

Concerns / Development areas

- Copper prices and to develop our project in time at a normal cost. - Copper oxides production. - To have enough water sources to develop a 8,000 t fine copper/year project.

Suppliers - Suppliers of interest: those who provide the needed product at a good price with a proved service.

- Preference for local based producers/services (hopefully from III Region).

Recommendations - Recommendations regarding market areas to expand: Trucks, Water management. EXSW plants parts and reagents.

- To present the Finnish products directly after visiting our projects and sites.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

68

Santiago Metals

Company info - Services (Consultant Company) - Private- Engineering, Projects Evaluation

Trends / Drivers - Mining Industry Services- Cost reductions and Project Certifications

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

69

Centro de Estudios Minerales

Concerns / Development areas

- Decrease in mining project investment.- Lack on services related to Project certification.- Use of inadequate software for mining projects evaluation and development.- Innovation in mining processes.- Robotics in mining operations.

Suppliers - Purchase of products /services according the project needs, considering quality and prices and client requests.

- Main strengths of suppliers are quality, prestige and prices.- Currently looking for new products such as computer hardware and software.- Preferences for local based suppliers to obtain enough guaranty, training and

services.

Recommendations - Mining Innovation, Sustainable Development & Technical Training.- Launch your Finnish products/services in Chile by organizing a related Seminar to the

mining community.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

70

Centro de Estudios Minerales

Company info - Mining Engineering Career - Private - Teaching and Research

Trends / Drivers - Professional Education.- Keep progressing professional teaching. - Mining industry investigation.- Several new educational centers are appearing due the previous expansion in the

mining industry.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

71

Universidad Católica de Valparaíso

Concerns / Development areas

- To provide an updated view to solve current mining industry problems: productivity, environmental contamination, new equipment.

- Development of Technical Institutes.- Training of specialized workers. Mining machines operators. - Lack of good productivity levels. - Higher operational costs.

Suppliers - Purchase of products /services according the project needs - Suppliers strengths must be their academic or scientific value.- Prerequisites for (new) suppliers are scientific strength, prestige and value.- Ready to consider new suppliers from Finland if they are in line with our teaching/

research lines.

Recommendations - Association with local providers. Academic alliances with Chilean universities- Finnish products/services to be promoted by means of a Seminar directed to the

different participants in the mining industry: companies, universities and government entities.

Expert Interview Summary

18.12.2015 Team Finland Mining Growth Program

72

Universidad Católica de Valparaíso

Comments from the Finnish companiesabout the Chilean marketSaija Luukkanen, Ex-Pöyry

– Stable business environment; Chileans really appreciate Finnish know-how; existing networks available also for new Finnish companies.

– Large players have already a stable market position and the competition is hard. It’s maybe easier to enter as a new comer to Peru.

– English language skills limited.

Janne Pöllänen, Sleipner Finland Oy

– Huge market potential and Chileans appreciate Finnish products as well as Finnish business culture. Finnish large suppliers have a long history in the region.

– It’s almost a must to know some Spanish, good to have some knowledge about the local mining business and existing networks with local companies. If you handle all by yourself, it’s going to be very expensive.

18.12.2015 Team Finland Mining Growth Program

73

Comments from the Finnish companiesabout the Chilean marketErika Hietamäki, Kopar Oy

– Most European style of doing business in Latin America and pretty stable country politically and financially.

– Good connections are a must. This has been emphasized in our business especially during the last years. A good product is not alone enough.

– Codelco changes its higher management often, which reflects the projects; existing can be cancelled and new investments are difficult to get accepted.

18.12.2015 Team Finland Mining Growth Program

74

Examples of Finnish Mining industry Companies Operating in Chile

18.12.2015 Team Finland Mining Growth Program

75

Altogether there are estimated 120 Finnish companies operating in Chile (Source: Finpro)

76

Section 3Appendix

18.12.2015 Team Finland Mining Growth Program

Appendix 1Chile - General Overview

– Chile is a global center for mining production with 33% of global copper reserves.

– The mining industry is clearly the most important driver of the Chilean economy, contributing to 9,6% of the GDP.

– Chile is one of the most attractive business destinations in South America, with well-functioning market economy, with healthy fiscal balances, sophisticated financial markets and a robust institutional environment.

– Since the 1990s, Chile has been one of Latin America’s fastest growing economies with an average growth rate of 3-5%.

– After a decade-long commodities boom came to an end last year, Chile will grow this year estimated 2,7% (2015), but is projected to pick up gradually over the next two years according to FMI.

18.12.2015 Team Finland Mining Growth Program

77

Appendix 1Chile - General Overview

– Economic growth in Latin America is weak reflecting global low commodity prices, the weight of the economies in the region will fall from 7% in 2014 to 5% in 2020.

– Chile has a free trade agreement with the European Union. It has one of the highest numbers of bilateral or regional trade agreements globally.

– In 2013 Finland and Chile signed a Memorandum of Understanding (MOU) on Mining. The agreement promotes research into sustainable mining products and services.

– 63 % of the technology for mining is imported to Chile. Chile has emphasized Finland as an example of succeeding in the mining industry by innovating technology although Finland has relatively limited mining industry.

– EUI ranking: Chile ranked 14th among the 82 countries covered business environment ranking for 2007–2011, highest in the Latin America region.

18.12.2015 Team Finland Mining Growth Program

78

Appendix 1Chile - General Overview

18.12.2015 Team Finland Mining Growth Program

79

Source: Central Bank of Chile

ECONOMIC OVERVIEW

External Debt US$ 119 bn

Unemployment Rate 6,40%

Population Below Poverty Line 14,40%

Export Partners China, Europe, Japan, USA

ExportCommodities

Copper & other minerals, forestry products, wine, fish.

Import Partners China, USA, Korea, USA, Argentina

Import Commodities

Oil, machinery, clothes, cars

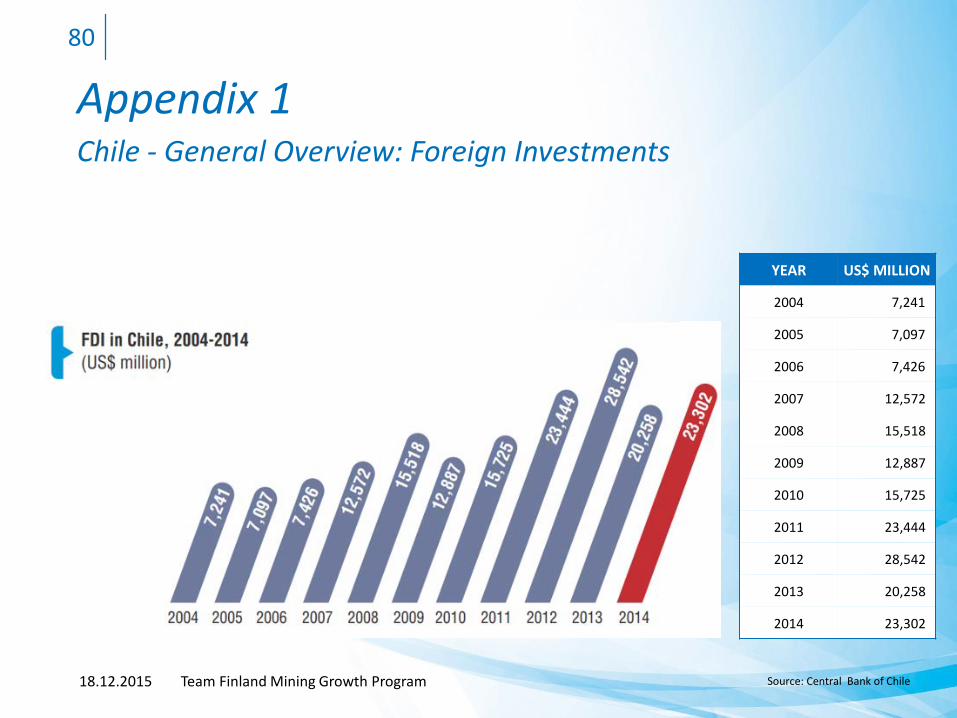

Appendix 1Chile - General Overview: Foreign Investments

18.12.2015 Team Finland Mining Growth Program

80

YEAR US$ MILLION

2004 7,241

2005 7,097

2006 7,426

2007 12,572

2008 15,518

2009 12,887

2010 15,725

2011 23,444

2012 28,542

2013 20,258

2014 23,302

Source: Central Bank of Chile

Appendix 1Chile - General Overview

The main success factors in Chilean mining development are:– Geological potential– Social and political stability– Strong and stable economy– Infrastructure and qualified personnel– Legal certainty and institutions

18.12.2015 Team Finland Mining Growth Program

81

Source: Mining Ministry

82

Thank you!

18.12.2015 Team Finland Mining Growth Program

![Octave-GTK 24/02/05 © Octave-GTK Team 24/02/05 Octave-GTK Team Octave-GTK, a language bindings project Hemant Muthu Rams Manik {gnufied, gnumuthu, chaosglare,manickam}@users.sourceforge.net]](https://img.pdfslide.us/doc/110x75/56649e7d5503460f94b806d1/octave-gtk-240205-octave-gtk-team-240205-octave-gtk-team-octave-gtk.jpg)