Embed Size (px)

Citation preview

Taxation ROI 1st Year Examination

June 2021

Solutions, Examiners Comments & Marking Scheme

Taxation ROI October 2019 1st Year Paper

Page 2 of 21

NOTES TO USERS ABOUT THESE SOLUTIONS

The solutions in this document are published by Accounting Technicians Ireland. They are intended to

provide guidance to students and their teachers regarding possible answers to questions in our

examinations.

Although they are published by us, we do not necessarily endorse these solutions or agree with the views

expressed by their authors.

There are often many possible approaches to the solution of questions in professional examinations. It

should not be assumed that the approach adopted in these solutions is the ideal or the one preferred by us.

Alternative answers will be marked on their own merits.

This publication is intended to serve as an educational aid. For this reason, the published solutions will

often be significantly longer than would be expected of a candidate in an examination. This will be

particularly the case where discursive answers are involved.

This publication is copyright 2021 and may not be reproduced without permission of Accounting

Technicians Ireland.

© Accounting Technicians Ireland, 2021

Taxation ROI June 2021 1st Year Paper

Page 3 of 21 Taxation ROI June 2021

Accounting Technicians Ireland

1st Year: JUNE 2021

Paper: TAXATION (Republic of Ireland)

Tuesday 8 June 2021

Exam Duration: 4 Hours Exam

Upload: 30 Minutes

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

For candidates answering in accordance with the law and practice of the Republic of Ireland.

Candidates should answer the paper in accordance with the appropriate provisions up to and including the

Finance Act 2019. The provisions of the Finance Act 2020 should be ignored.

Allowances and rates of taxation, to be used by candidates, are set out in the Tax Reference material.

Answer Question 1 from SECTION A and ANY THREE of the four questions from Section B.

Candidates are not permitted to answer more than the required number of questions in Section B.

Candidates should allocate their time carefully.

All workings should be shown.

All figures should be labelled as appropriate e.g. €s, units etc.

Answers should be illustrated with examples, where appropriate.

UPLOAD INSTRUCTIONS

Each question must begin on a new document, excel or word.

Each question must be uploaded to Moodle individually.

Each file must include the candidate’s Registration Number, Subject Name, Question Number for example

RXXXXXX, TXR, Question 1.

Candidates must retain their original answers until after the release of exam results in July. ATI may request

to see the original files.

Taxation ROI June 2021 1st Year Paper

Page 4 of 21 Taxation ROI June 2021

SECTION A

Answer Question 1 (all parts) from Section A

QUESTION 1

All parts must be answered

Part A

Certain income is exempt from tax. Outline four types of income that are exempt.

(4 Marks)

Part B

Fred filed his 2019 tax return on 1 December 2020. His tax liability for 2019 was €20,000. Fred paid Preliminary

Tax of €15,000 for 2019 on 31 December 2019. Fred paid the balance of taxes owed for 2019 on 31 December

2020. Fred’s income tax liability for 2018 was €15,000. What will Fred’s final tax liability, including interest and

penalties, be for 2019 after he filed his tax return.

(4 Marks)

Part C

A married couple Jane and Sally, both aged 68 years had combined income of €40,000 in 2020. This was made

up as follows:

Jane earned €26,000 from her salary and was entitled to the employee tax credit.

Sally earned €14,000 net rental income from a rental property.

Calculate their income tax due for 2020.

(4 Marks)

Part D

Kevin is a non-proprietary director and is employed and earns a salary of €40,000 in 2020. In February 2020 the

company decided to pay a bonus of €10,000 in respect of 2019. The amount was paid through the February 2020

payroll and PAYE of €1,500 was deducted from it. Explain how Kevin will treat this in his tax return and whether

the bonus is in the 2019 or 2020 tax return.

(4 Marks)

Part E

VAT of €6,300 was paid on the acquisition of a motor vehicle on 1 November 2019. The motor vehicle qualified

for a VAT deduction and 20% of the VAT incurred on the purchase was reclaimed. The motor vehicle was sold

on 31 March 2020. Calculate the VAT clawback as a result of this disposal.

(4 Marks)

Part F

Adrienne rents out a room in her house. She charges €1,000 a month rent and an additional €200 a month for

laundry. This is Adrienne’s only source of income. She is single and aged 66. Outline Adrienne’s income tax

liability for 2020 (you can ignore PRSI and USC) and explain how you arrived at your answer.

(4 Marks)

Part G

Wiel receives the following Irish dividends from a private company in 2020:

€900 on 15 January 2020 – This was a final dividend for the year ended 31 October 2019.

€1,200 on 15 June 2020 – This was an interim dividend for the year ended 31 October 2020.

€900 on 15 August 2020 – This was a second interim dividend for the year ended 31 October 2020.

€1,050 on 15 January 2021 – This was a final dividend for the year ended 31 October 2020.

For the tax year 2020 outline which of the dividends Wiel will be taxed on and why.

(4 Marks)

Taxation ROI June 2021 1st Year Paper

Page 5 of 21 Taxation ROI June 2021

Part H

Outline the conditions that must be present in order for a deed of covenant to qualify for tax relief, when payable

to an adult. What is the maximum amount of tax relief available to the payee of a qualifying deed of covenant?

(4 Marks)

Part I

John, who is employed, earns €500 in June 2020 and €3,700 in July 2020. He is taxed on a month 1 basis. His

SRCOP is €2,941.67 per month and tax credits €275 per month. Calculate John’s income tax liability for July

2020 and explain what is meant by the “Month 1 basis”.

(4 marks)

Part J

Explain the difference between zero rated supplies and exempt supplies for VAT purposes and the VAT

implications for a business that supplies either of these types of goods. (4 marks)

Total 40 marks

Taxation ROI June 2021 1st Year Paper

Page 6 of 21 Taxation ROI June 2021

SECTION B

Answer THREE of the four questions in section B

QUESTION 2

Fiona Smith has been in business for several years and is a chiropractor. She has prepared accounts for the year

ended 31 December 2020 and these are reproduced below:

Accounts for the year ended 31 December 2020

Notes € €

Sales ................................................................................ 450,000

Cost of sales .................................................................... 383,500

Gross Profit ..................................................................... 66,500

Add

Dividends received ......................................................... 250

Rent received .................................................................. 550

Trade discount received .................................................. 150

950

67,450

Less

Employee costs ............................................................... (1) 29,300

Administrative costs ....................................................... (2) 1,300

Repairs ............................................................................ (3) 3,100

Motor expenses ............................................................... (4) 2,500

Advertising and promotion ............................................. (5) 600

Legal costs ...................................................................... (6) 300

Interest ............................................................................ (7) 800

Depreciation.................................................................... 5,500

Insurance ......................................................................... (8) 1,400

44,800

Net Profit 22,650

NOTES

€

(1) Employee costs

Drawings by Fiona Smith ................................................................................. 12,300

Staff wages ....................................................................................................... 5,600

PHI for Fiona .................................................................................................... 4,100

Christmas party for clients ................................................................................ 2,100

Pension payment for Fiona ............................................................................... 5,200

29,300

Fiona paid €5,000 for summer staff in 2020. These expenses have not been included in the accounts.

(2) Administrative costs €

Couriers ............................................................................................................ 700

Mobile phone bills ............................................................................................ 400

Magazines ......................................................................................................... 100

Stationery ......................................................................................................... 100

1,300

The mobile phone bill relates totally to personal use.

30% of the courier charge relates to Fiona paying couriers to deliver her Christmas presents to family as she

could not travel to see them due to COVID-19.

Taxation ROI June 2021 1st Year Paper

Page 7 of 21 Taxation ROI June 2021

QUESTION 2 (Cont’d)

(3) Repairs €

Painting existing business premises .................................................................. 800

Repair home shed ............................................................................................. 300

Repairs to office windows ................................................................................ 1,500

Front door replacement own house ................................................................... 500

3,100

(4) Motor expenses €

Parking fines ..................................................................................................... 500

Car expenses ..................................................................................................... 1,200

Car depreciation ................................................................................................ 800

2,500

Fiona uses the car 50% for business purposes and 50% for personal reasons.

(5) Advertising and promotion €

Trade show ....................................................................................................... 200

Google adwords ................................................................................................ 400

600

50% of the Google adwords were to advertise Fiona’s new book she wrote on flower arranging.

In addition, €600 was spent on a holiday to Spain where Fiona wore t-shirts advertising her business for

the whole holiday.

(6) Legal costs €

Appeal against employee dismissal .................................................................. 100

Solicitor’s fee for pursuing debtors ................................................................... 200

300

Other legal fees of €1,000 were incurred on business related matters. These have not yet been reflected in

the accounts.

(7) Interest €

Business bank overdraft .................................................................................... 250

Term loan for business ...................................................................................... 150

Late payment of PAYE/PRSI/USC .................................................................. 400

800

(8) Insurance €

Home insurance………………………………………………………………… 300

Business insurance ……………………………………………………………... 1,100

1,400

Required:

Compute Fiona Smith’s Schedule D, Case I tax adjusted profits for the year ended 31 December 2020 (includes

one mark for presentation).

(19 Marks)

Provide a brief explanation for your treatment of the €600 Fiona spent on the holiday to Spain.

(1 Mark)

Total 20 Marks

Taxation ROI June 2021 1st Year Paper

Page 8 of 21 Taxation ROI June 2021

QUESTION 3

Simon is aged 45 years old and was widowed in 2019. He has two children ages 8 and 10 years old. Simon

works for Flats are Clean Ltd and has a gross salary of €100,000 in 2020 with €15,000 PAYE deducted. Simon’s

employers pay €2,000 for him to be a gym member as they know fitness is important to him. They also pay

€600 for subsidised meals in the canteen for him. The meals are available to all employees of the company.

Simon has a house in Spain that he rented out in 2020. He received €6,000 gross rent and paid mortgage interest

of €2,000 and repairs of €500 for the year. He also bought a car in Spain in 2020 for €4,000 which he let the

tenants use for free.

Simon set up a covenant for his incapacitated mother in 2019. She is 70 years old and Simon pays her €5,000 a

year under the covenant.

Simon received €670 deposit interest (net) from Bank of Ireland in 2020 and €750 dividend (net) from CRH in

2020.

Simon was delighted in November 2020 when he won €50,000 on the lotto and immediately booked a family

holiday for 2022 to France.

Simon spent €200 going to the GP in 2020 and paid €500 to a specialist for the cost of a diagnostic

procedure on his eyes. Thankfully, he made a full recovery two months later.

Required:

Prepare an income tax computation for 2020 in respect of Simon and clearly outline if some items are not taxable

or allowed as expenses.

Total 20 Marks

N.B. For the purposes of answering this question ignore PRSI and the USC

Taxation ROI June 2021 1st Year Paper

Page 9 of 21 Taxation ROI June 2021

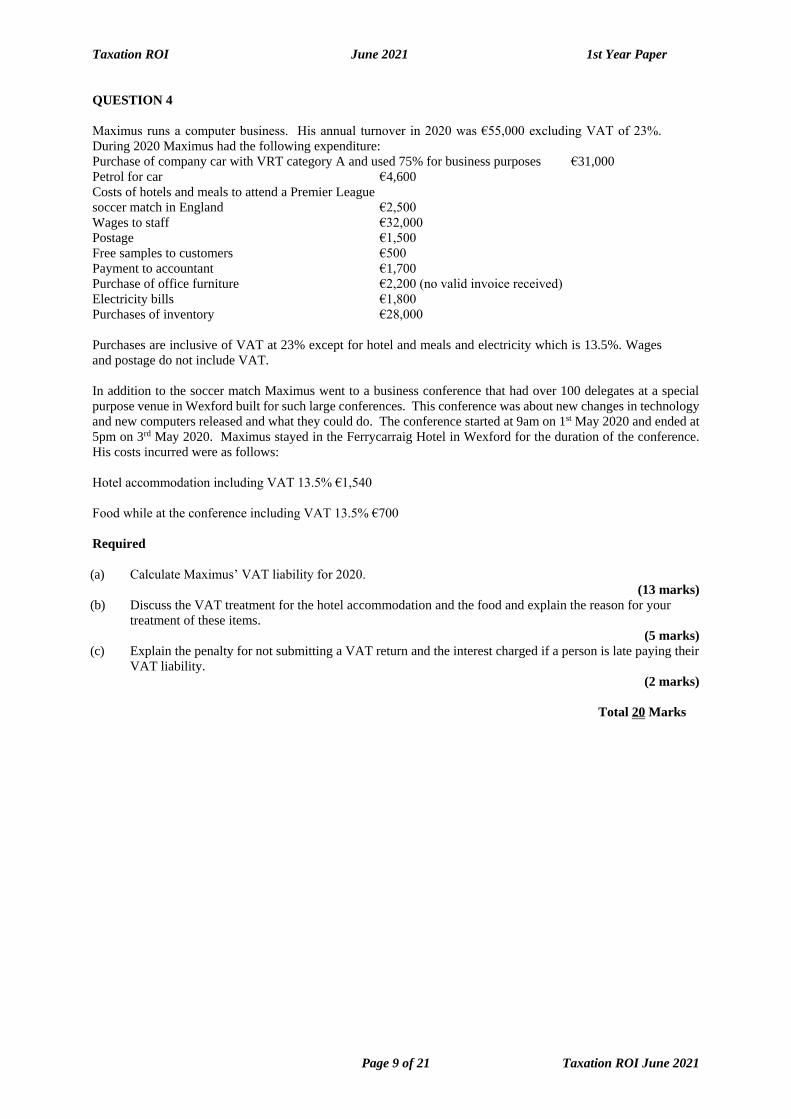

QUESTION 4

Maximus runs a computer business. His annual turnover in 2020 was €55,000 excluding VAT of 23%.

During 2020 Maximus had the following expenditure:

Purchase of company car with VRT category A and used 75% for business purposes €31,000

Petrol for car €4,600

Costs of hotels and meals to attend a Premier League

soccer match in England €2,500

Wages to staff €32,000

Postage €1,500

Free samples to customers €500

Payment to accountant €1,700

Purchase of office furniture €2,200 (no valid invoice received)

Electricity bills €1,800

Purchases of inventory €28,000

Purchases are inclusive of VAT at 23% except for hotel and meals and electricity which is 13.5%. Wages

and postage do not include VAT.

In addition to the soccer match Maximus went to a business conference that had over 100 delegates at a special

purpose venue in Wexford built for such large conferences. This conference was about new changes in technology

and new computers released and what they could do. The conference started at 9am on 1st May 2020 and ended at

5pm on 3rd May 2020. Maximus stayed in the Ferrycarraig Hotel in Wexford for the duration of the conference.

His costs incurred were as follows:

Hotel accommodation including VAT 13.5% €1,540

Food while at the conference including VAT 13.5% €700

Required

(a) Calculate Maximus’ VAT liability for 2020.

(13 marks)

(b) Discuss the VAT treatment for the hotel accommodation and the food and explain the reason for your

treatment of these items.

(5 marks)

(c) Explain the penalty for not submitting a VAT return and the interest charged if a person is late paying their

VAT liability.

(2 marks)

Total 20 Marks

Taxation ROI June 2021 1st Year Paper

Page 10 of 21 Taxation ROI June 2021

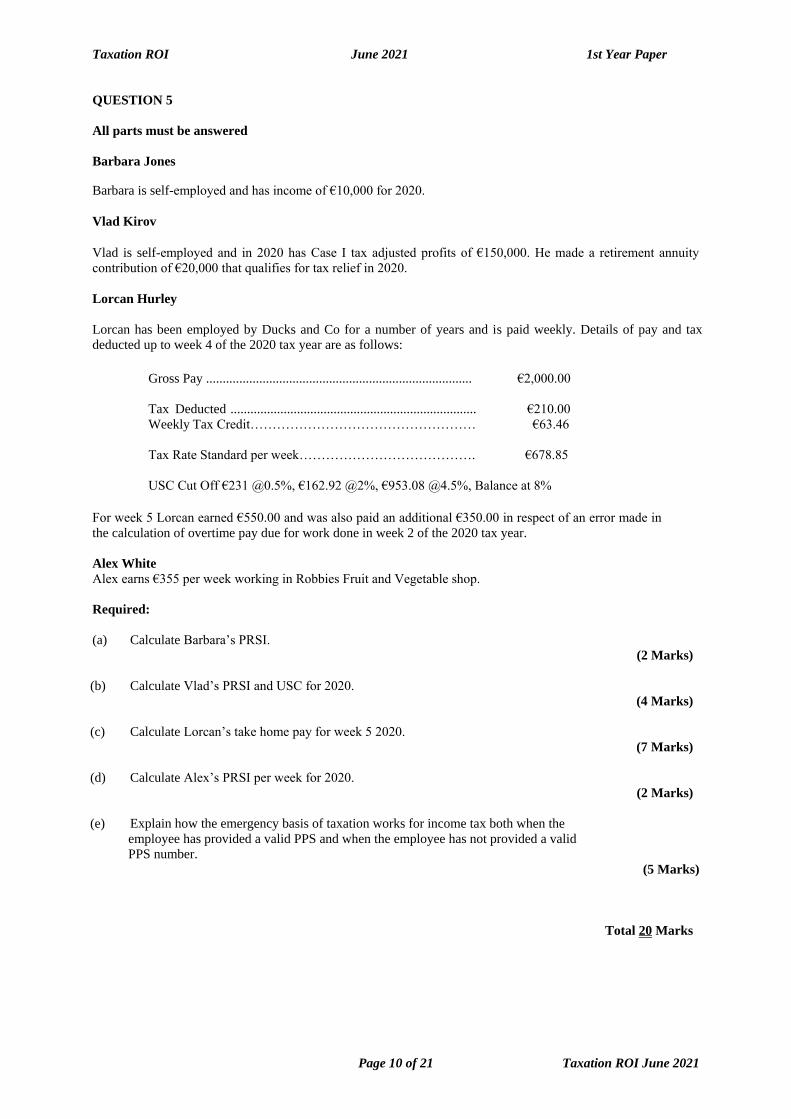

QUESTION 5

All parts must be answered

Barbara Jones

Barbara is self-employed and has income of €10,000 for 2020.

Vlad Kirov

Vlad is self-employed and in 2020 has Case I tax adjusted profits of €150,000. He made a retirement annuity

contribution of €20,000 that qualifies for tax relief in 2020.

Lorcan Hurley

Lorcan has been employed by Ducks and Co for a number of years and is paid weekly. Details of pay and tax

deducted up to week 4 of the 2020 tax year are as follows:

Gross Pay ................................................................................ €2,000.00

Tax Deducted .......................................................................... €210.00

Weekly Tax Credit…………………………………………… €63.46

Tax Rate Standard per week…………………………………. €678.85

USC Cut Off €231 @0.5%, €162.92 @2%, €953.08 @4.5%, Balance at 8%

For week 5 Lorcan earned €550.00 and was also paid an additional €350.00 in respect of an error made in

the calculation of overtime pay due for work done in week 2 of the 2020 tax year.

Alex White

Alex earns €355 per week working in Robbies Fruit and Vegetable shop.

Required:

(a) Calculate Barbara’s PRSI.

(2 Marks)

(b) Calculate Vlad’s PRSI and USC for 2020.

(4 Marks)

(c) Calculate Lorcan’s take home pay for week 5 2020.

(7 Marks)

(d) Calculate Alex’s PRSI per week for 2020.

(2 Marks)

(e) Explain how the emergency basis of taxation works for income tax both when the

employee has provided a valid PPS and when the employee has not provided a valid

PPS number.

(5 Marks)

Total 20 Marks

Taxation ROI June 2021 1st Year Paper

Page 11 of 21 Taxation ROI June 2021

1st Year Examination: June 2021

Taxation ROI

Suggested Solutions

and

Examiner’s Comments

Students please note: These are suggested solutions only; alternative answers may also be deemed to be correct

and will be marked on their own merits.

Statistical Analysis – By Question

Question No. 1 2 3 4 5

Average Mark 28.12 18.07 16.43 13.60 13.60

Nos. Attempting (%) 100% 94% 84% 43% 70%

Statistical Analysis - Overall

Pass Rate 92.55

Average Mark 73.83

Range of Marks Nos. of Students

0-49 49

50-64 89

65-79 195

80 and over 325

Total No. Sitting Exam 658

Total Absent 83

Total Approved Absent 7

Total No. Applied for Exam 748

General Comments:

This exam was an online exam that students were given four hours to complete and 30 minutes to upload

their solution. This exam was not invigilated. The exam had been written intended to be a closed book

invigilated online three-hour exam. These changes in circumstances very likely hugely increased the

overall marks and the rate of student performance.

Taxation ROI June 2021 1st Year Paper

Page 12 of 21 Taxation ROI June 2021

Examiner Comments on Question One

SOLUTION 1

a)

The following income is exempt from income tax:

- social welfare child benefit payments

- statutory redundancy payments

- lottery and betting winnings

- life assurance proceeds

- interest paid on An Post Saving Certificates and Instalment Saving Scheme

- qualifying artists income up to a limit

- Income from qualifying childcare services up to €15,000 per annum

- Certain rental income (rent a room) up to €14,000 per annum

- Individual over 65 years once they do not exceed income limits

b)

Kevin will be taxed in 2020 on the €40,000 salary

And the €10,000 received in 2020 (for the tax year 2019).

On his 2020 tax return it will include both the salary of €40,000 and the €10,000 bonus

As even though the bonus was for 2019, it was paid in 2020.

C)

Rent €1,000 x 12 = €12,000

Laundry rent €200 x 12 = €2,400

Total €14,400

Adrienne does not qualify for the rent a room exemption as the total rent is over €14,000.

Adrienne is not liable to income tax as she is over 65 years and her total income is less than €18,000.

(d)

€900 on 15 January 2020 – This was a final dividend for the year ended 31 October 2019.

€1,200 on 15 June 2020 – This was an interim dividend for the year ended 31 October 2020.

€900 on 15 August 2020 – This was a second interim dividend for the year ended 31 October 2020.

This question was designed to cross the entire syllabus and to test students knowledge. It had ten parts of

four arks each. Students performed very well here, in particular for the exemptions from income tax,

bonus payment, dividends, covenants, VAT. They performed slightly worse in the marginal relief and car

disposal parts. The least well answered part was the late filing of return.

Taxation ROI June 2021 1st Year Paper

Page 13 of 21 Taxation ROI June 2021

These are the actual dividends received by Wiel in 2020. The financial year from which they are paid from is

irrelevant.

(e)

Tax relief is available on covenants to an adult in the following circumstances:

- The covenant is in favour of a permanently incapacitated adult or

- The covenant is in favour of an adult aged over 65 years in which case the maximum amount on which tax

relief can be claimed is 5% of the covenanter’s income.

The covenant must be capable of lasting more than 6 years to qualify for tax relief.

(f)

Where a business supplies zero rated supplies it does not charge VAT. It may however be able to register for VAT

and claim back VAT on purchases.

Certain goods and services are exempt from VAT. Where a business supplies exempt services, it is not entitled to

register for VAT and cannot claim VAT on purchases

(g)

Fred filed his 2019 tax return on 1 December 2020. His tax liability for 2019 was €20,000. Fred

paid Preliminary Tax of €15,000 for 2019 on 31 December 2019. Fred’s paid the balance of taxes

owed for 2019 on 31 December 2020. Fred’s income tax liability for 2018 was €15,000. What will

Fred’s final tax liability, including interest and penalties, be for 2019 after he filed his tax return.

Preliminary tax for 2019 is the lower of 100% of 2018 (€15,000) or 90% of tax due 2019 (€18,000)

He paid €15,000 on 31 December 2019, €15,000 was due 31 October 2019.

Interest €15,000 x 0.0219% x 61 days = €200.39

Balance of €5,000 not paid until 31 December 2020 when he cleared his 2019 tax. Therefore as €5,000 extra was

due:

31 October 2020 to 31 December 2020

61 days x 0.0219% x €5,000 = €66.80

Income tax as calculated 20,000

Add: Surcharge late filing 5% 1,000

Add: Interest due

€200.39

€66.80

267.19

Total Liability 21,267.19

(h)

Jane and Sally

Taxation ROI June 2021 1st Year Paper

Page 14 of 21 Taxation ROI June 2021

Jane and Sally have a combined income of €40,000 in 2020. Based on the standard rate tax band of €44,300 and

tax credits of €5,440 they would have the following tax to pay:

Income €40,000

Taxed €40,000 @ 20% €8,000

Less non-refundable tax credits

Married €3,300

Employee tax credit €1,650

Aged tax credit €490

Total €5,440

Tax €2,560

Less: Marginal relief (€960)

Fina Tax Liability €1,600

Marginal relief applies.

Income €40,000

Specified limit €36,000

Excess €4,000

Taxed at 40% €1,600

Maximum Tax Liability €1,600

Taxed as normal €2,560

Marginal relief allowed (€2,560 - €1,600) €960

(i)

- Purchases 1 November 2019

- Sold 31 March 2020

Days

November 2019 30 days

December 2019 31 days

January 2020 31 days

February 2020 29 days

March 2020 31 days

Total number of days 152 days

VAT deducted x (4- N)/4

VAT deducted €6,300 x 20% = €1,260

N = (152/182) = 1 (rounded to nearest whole number

€1,260 x (4-1)/4 = €945 is clawed back and owed to Revenue Commissioners

in the next VAT return period.

Taxation ROI June 2021 1st Year Paper

Page 15 of 21 Taxation ROI June 2021

(j)

July 2020

Gross Income €3,700

Taxed as follows:

€2,941.67 x 20% = €588.33

€758.33 x 40% = €303.33

Total €891.66

Less: Tax Credits (€275.00)

Tax Due €616.66

As the employee is month 1 the €2,441.67 unused from June 2020 is not allowed be used in July 2020.

Taxation ROI June 2021 1st Year Paper

Page 16 of 21 Taxation ROI June 2021

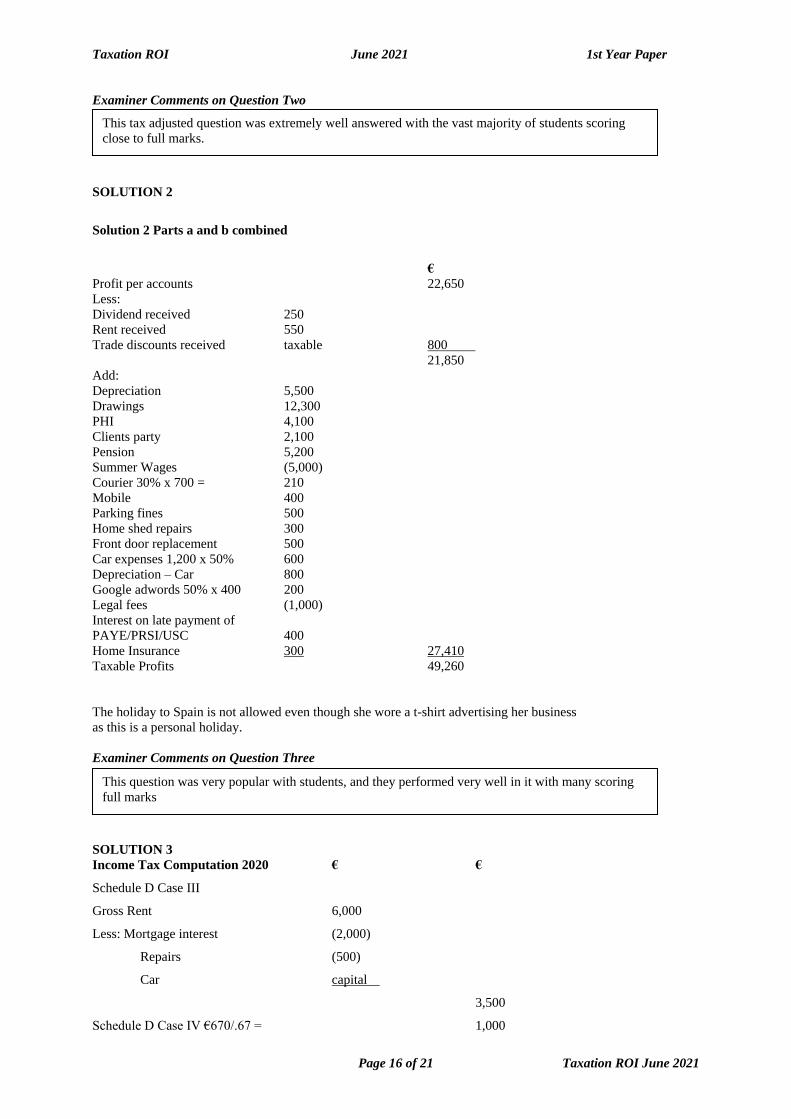

Examiner Comments on Question Two

SOLUTION 2

Solution 2 Parts a and b combined

€

Profit per accounts 22,650

Less:

Dividend received 250

Rent received 550

Trade discounts received taxable 800

21,850

Add:

Depreciation 5,500

Drawings 12,300

PHI 4,100

Clients party 2,100

Pension 5,200

Summer Wages (5,000)

Courier 30% x 700 = 210

Mobile 400

Parking fines 500

Home shed repairs 300

Front door replacement 500

Car expenses 1,200 x 50% 600

Depreciation – Car 800

Google adwords 50% x 400 200

Legal fees (1,000)

Interest on late payment of

PAYE/PRSI/USC 400

Home Insurance 300 27,410

Taxable Profits 49,260

The holiday to Spain is not allowed even though she wore a t-shirt advertising her business

as this is a personal holiday.

Examiner Comments on Question Three

SOLUTION 3

Income Tax Computation 2020 € €

Schedule D Case III

Gross Rent 6,000

Less: Mortgage interest (2,000)

Repairs (500)

Car capital

3,500

Schedule D Case IV €670/.67 = 1,000

This tax adjusted question was extremely well answered with the vast majority of students scoring

close to full marks.

This question was very popular with students, and they performed very well in it with many scoring

full marks

Taxation ROI June 2021 1st Year Paper

Page 17 of 21 Taxation ROI June 2021

Schedule E

Salary 100,000

Gym 2,000

Meals allowed

Total 102,000

Less: Covenant (5,000)

97,000

Lottery win Nil

Schedule F €750/.75 = 1,000

Gross Income 102,500

Taxed as follows:

€39,300 x 20% 7,860

€1,000 x 33% 330

€62,200 x 40% 24,880

33,070

Less: Non-refundable Tax Credits

Single person 1,650

Single person child carer credit 1,650

Employee 1,650

Widowed person 3,600

DIRT 330

Medical €700 x 20% 140

(9,020)

24,050

Less: Refundable Tax Credits

PAYE 15,000

DWT 250

(15,250)

8,800

Add: Tax on covenant €5,000 x 20% 1,000

Tax Due 9,800

Taxation ROI June 2021 1st Year Paper

Page 18 of 21 Taxation ROI June 2021

Examiner Comments on Question Four

SOLUTION 4

a)

€

VAT on sales/Output VAT

€55,000 x 23% = 12,650

VAT on purchases/Input VAT

Car €31,000/1.23 x .23 x 20% = 1,159

Petrol Not allowed

Hotels and meals Not allowed

Wages No VAT

Postage No VAT

Free samples Not supplies for VAT

Accountant €1,700/1.23 x .23 = 318

Office Furniture Not allowed (no invoice)

Electricity €1,800/1.135 x .135 = 214

Inventory €28,000/1.23 x .23 = 5,236

Conference food Not allowed

Hotel Conference Accommodation

€1,540 / 1.135 x .135= 183 7,110

VAT due to Revenue 5,540

b)

The hotel accommodation qualifies as “qualifying accommodation” to attend a

“qualifying conference”. The accommodation commences the night before

the Conference and ends on the day the Conference finishes. The

Conference is a “qualifying Conference” as it is in the course of furtherance of

business that is organised for more than 50 delegates at a venue designed to hold

such an event.

VAT paid on food is not allowed as an input credit even when the expense is

incurred for business reasons.

The hotels and meals in relation to the soccer match are disallowed due to personal nature.

c)

The penalty for not submitting a VAT return is €4,000.

VAT was not as popular as the income tax or tax adjusted profits question. The marks for this

question were weaker but overall students still performed very strongly. Not all students recognized

the qualifying conference and some students included VAT on wages and this is an area that students

would be expected to know.

Taxation ROI June 2021 1st Year Paper

Page 19 of 21 Taxation ROI June 2021

If a VAT payment is not submitted by the due date, interest is charged at 0.0274%

per day.

Examiner Comments on Question Five

SOLUTION 5

a)

Barbara’s PRSI

€10,000 x 4% = €400

Minimum in year €500

b)

Tax adjusted profits €150,000

Retirement annuity contribution (€20,000)

Case I income €130,000

PRSI €150,000 x 4% = €6,000

USC

€12,012 x 0.5% = €60.06

€8,472 x 2% = €169.44

€49,560 x 4.5% = €2,230.20

€29,956 x 8% = €2,396.48

€50,000 x 11% €5,500.00

€150,000 €10,356.18

This question was probably the least popular. There were mixed results in the answers with some

students scoring high marks and others unsure how to do the calculations.

Taxation ROI June 2021 1st Year Paper

Page 20 of 21 Taxation ROI June 2021

c)

Lorcan Hurley

PRSI Class A1

Employee Week 5 Take Home Pay Week 5

Pay 900.00

900.00 4% 36.00 Tax 52.70

PRSI 36.00

USC 27.19

-115.89

Take home 784.11

USC

162.92@2%

900

1.16

3.26

22.77

27.19

Tax

5 weeks

€2,000 + €900 = €2,900

Tax

(€678.85 x 5 = €3,394.25) so €2,900 x

20% = €580

Total tax = €580.00

Less: Tax credits €63.46 x 5 (€317.30)

Balance €262.70

Less: Paid

(€210.00)

Tax due before credits €52.70

d)

PRSI €355 x 4% = €14.20

Less: PRSI credit as income between €352.01 and €424 per week

€12 less (€355 - €352.01 x 1/6) (€11.50)

PRSI Liability €2.70

e)

The emergency basis will apply if

- The employee cannot or has not provided a PPS number or

- An RPN cannot be provided by the Revenue Commissioners

Normal emergency rules apply where a valid PPS number has been

provided but no RPN is available:

Weekly Pay 1 -4 SRCOP €679 Tax Credit €0

Week 5 onwards SRCOP €0 Tax Credit €0

Taxation ROI June 2021 1st Year Paper

Page 21 of 21 Taxation ROI June 2021

Monthly Pay Month 1 SRCOP €2,942 Tax Credit €0

Month 2 onwards SRCOP €0 Tax Credit €0

Where the employee does not provide a PPS number there is no SRCOP or tax credits applied

at all and all income is taxed at 40% from the date of commencement of the employment.