Embed Size (px)

Citation preview

Advanced Taxation ROI May 2015 2nd Year Paper

Page 1 of 16 Adv. Taxation (ROI) S2015

Advanced Taxation Republic of Ireland

2nd Year Examination

May 2015 Exam Paper, Solutions & Examiner’s Comments

Advanced Taxation ROI May 2015 2nd Year Paper

Page 2 of 16 Adv. Taxation (ROI) S2015

NOTES TO USERS ABOUT THESE SOLUTIONS

The solutions in this document are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding possible answers to questions in our examinations. Although they are published by us, we do not necessarily endorse these solutions or agree with the views expressed by their authors. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the ideal or the one preferred by us. Alternative answers will be marked on their own merits. This publication is intended to serve as an educational aid. For this reason, the published solutions will often be significantly longer than would be expected of a candidate in an examination. This will be particularly the case where discursive answers are involved. This publication is copyright 2015 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2015.

Page 1 of 10 Adv. Taxation (ROI) S2015

Accounting Technicians Ireland

2nd

Year Examination: Summer 2015

Paper: ADVANCED TAXATION (Republic of Ireland)

Thursday 14 May 2015

2.30 p.m. to 5.30 p.m.

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

For candidates answering in accordance with the law and practice of the Republic of Ireland.

Candidates should answer the paper in accordance with the appropriate provisions up to and

including the Finance Act (No 2), 2013. The provisions of the Finance Act 2014 should be ignored.

Allowances and rates of taxation, to be used by candidates, are set out in a separate booklet

supplied with the examination paper.

Answer ALL THREE QUESTIONS in Section A, and ANY TWO of the FOUR questions in

Section B. If more than TWO questions are answered in Section B, then only the first two

questions, in the order filed, will be corrected.

Candidates should allocate their time carefully.

All workings should be shown.

All figures should be labelled as appropriate e.g. €s, units, etc.

Answers should be illustrated with examples, where appropriate.

Question 1 begins on Page 2 overleaf.

The following insert is included with this paper.

Tax Reference Material (ROI)

Page 2 of 10 Adv. Taxation (ROI) S2015

SECTION A

Answer QUESTION 1 and QUESTION 2 and QUESTION 3 (Compulsory) in this Section

QUESTION 1 (Compulsory)

Charlotte and Brian formally separated by a legal agreement dated 1 February 2014. Brian has custody

of the couple’s two children. They were jointly assessed for all years prior to separating. Charlotte was

the person assessed to tax prior to separation.

Charlotte is a self employed consultant. Her tax adjusted profits for the year to 31 December 2014

were €45,000.

On 1 January 2014 Charlotte’s office equipment had a tax written down value of €5,000. The office

equipment had cost €10,000 in 2010.

She had the following dealings in office equipment during the year:

1. She bought a new computer for €2,000.

2. She scrapped her old computer which cost her €3,000 when purchased in 2010.

As a result of the separation, Charlotte moved into the couple’s apartment. She rented out a room in

the apartment and received rent of €4,950 for 2014.

Charlotte also has the following income for 2014:

Dividend income from Irish company received net of dividend withholding tax €960

Deposit interest received net of DIRT €118

Charlotte pays Brian maintenance of €1,000 per month, of which €600 is specifically for the two

children.

Charlotte, who is aged 38 years, pays €800 per month into a Revenue approved pension scheme.

Brian works in a local supermarket on a part time basis and for 2014 he earned a salary of €1,000 per

month. No income tax was deducted from Brian’s salary in the 2014 tax year.

Requirement:

(a) Calculate Charlotte’s assessable Case II income, after capital allowances and relief for pension

contributions, for the 2014 year of assessment

6 marks

(b) Calculate Charlotte and Brian’s income tax for 2014, assuming they did not make an election

to continue to be jointly assessed after separating.

For the purposes of answering this question, you can ignore PRSI and USC

14 marks

Total 20 Marks

Page 3 of 10 Adv. Taxation (ROI) S2015

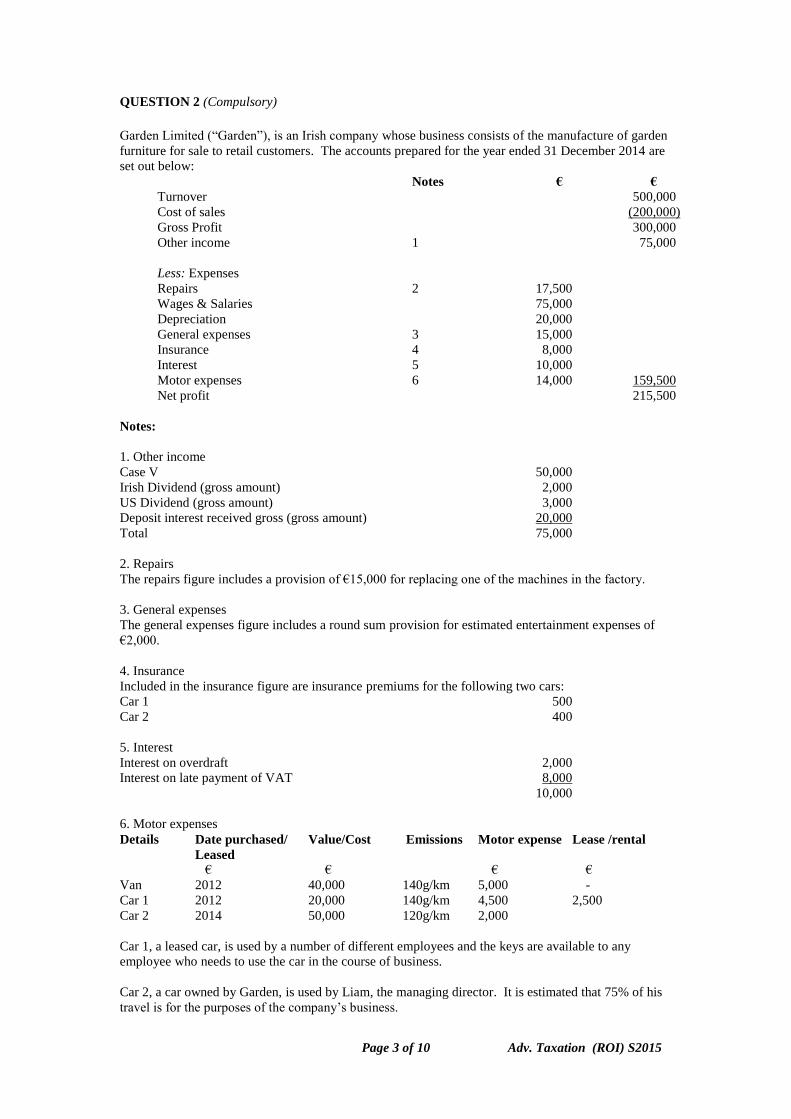

QUESTION 2 (Compulsory)

Garden Limited (“Garden”), is an Irish company whose business consists of the manufacture of garden

furniture for sale to retail customers. The accounts prepared for the year ended 31 December 2014 are

set out below:

Notes € €

Turnover 500,000

Cost of sales (200,000)

Gross Profit 300,000

Other income 1 75,000

Less: Expenses

Repairs 2 17,500

Wages & Salaries 75,000

Depreciation 20,000

General expenses 3 15,000

Insurance 4 8,000

Interest 5 10,000

Motor expenses 6 14,000 159,500

Net profit 215,500

Notes:

1. Other income

Case V 50,000

Irish Dividend (gross amount) 2,000

US Dividend (gross amount) 3,000

Deposit interest received gross (gross amount) 20,000

Total 75,000

2. Repairs

The repairs figure includes a provision of €15,000 for replacing one of the machines in the factory.

3. General expenses

The general expenses figure includes a round sum provision for estimated entertainment expenses of

€2,000.

4. Insurance

Included in the insurance figure are insurance premiums for the following two cars:

Car 1 500

Car 2 400

5. Interest

Interest on overdraft 2,000

Interest on late payment of VAT 8,000

10,000

6. Motor expenses

Details Date purchased/ Value/Cost Emissions Motor expense Lease /rental

Leased

€ € € €

Van 2012 40,000 140g/km 5,000 -

Car 1 2012 20,000 140g/km 4,500 2,500

Car 2 2014 50,000 120g/km 2,000

Car 1, a leased car, is used by a number of different employees and the keys are available to any

employee who needs to use the car in the course of business.

Car 2, a car owned by Garden, is used by Liam, the managing director. It is estimated that 75% of his

travel is for the purposes of the company’s business.

Page 4 of 10 Adv. Taxation (ROI) S2015

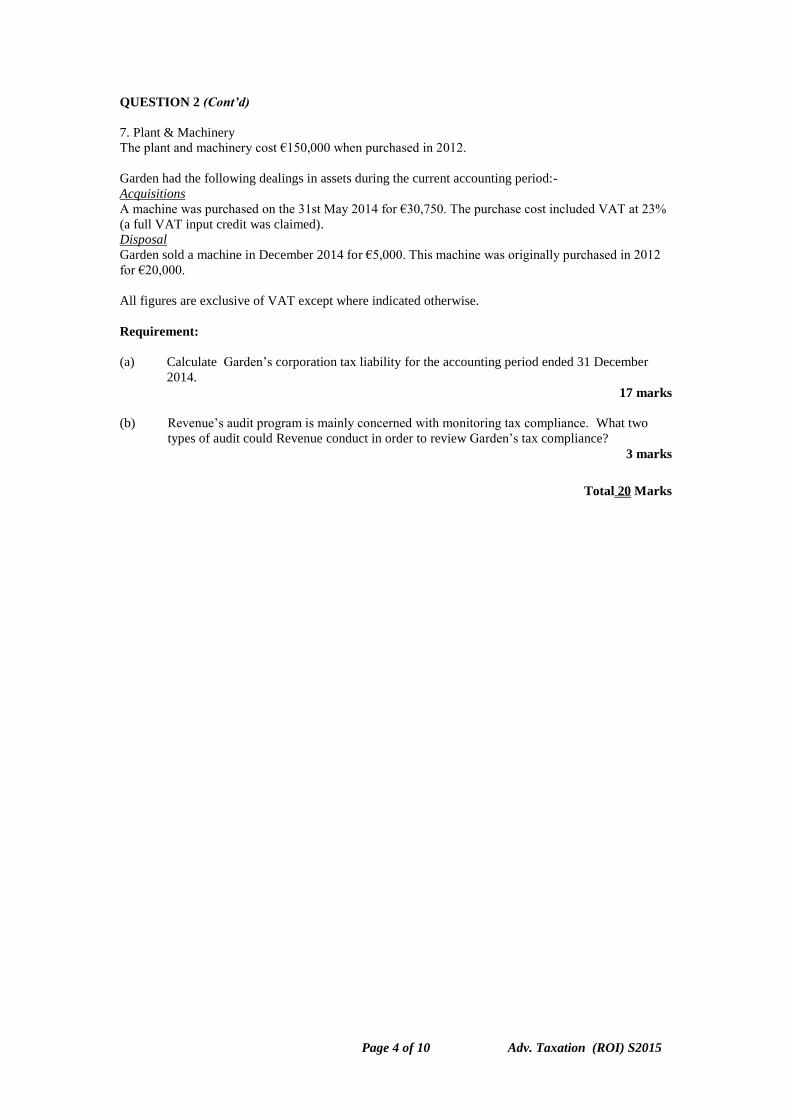

QUESTION 2 (Cont’d)

7. Plant & Machinery

The plant and machinery cost €150,000 when purchased in 2012.

Garden had the following dealings in assets during the current accounting period:-

Acquisitions

A machine was purchased on the 31st May 2014 for €30,750. The purchase cost included VAT at 23%

(a full VAT input credit was claimed).

Disposal

Garden sold a machine in December 2014 for €5,000. This machine was originally purchased in 2012

for €20,000.

All figures are exclusive of VAT except where indicated otherwise.

Requirement:

(a) Calculate Garden’s corporation tax liability for the accounting period ended 31 December

2014.

17 marks

(b) Revenue’s audit program is mainly concerned with monitoring tax compliance. What two

types of audit could Revenue conduct in order to review Garden’s tax compliance?

3 marks

Total 20 Marks

Page 5 of 10 Adv. Taxation (ROI) S2015

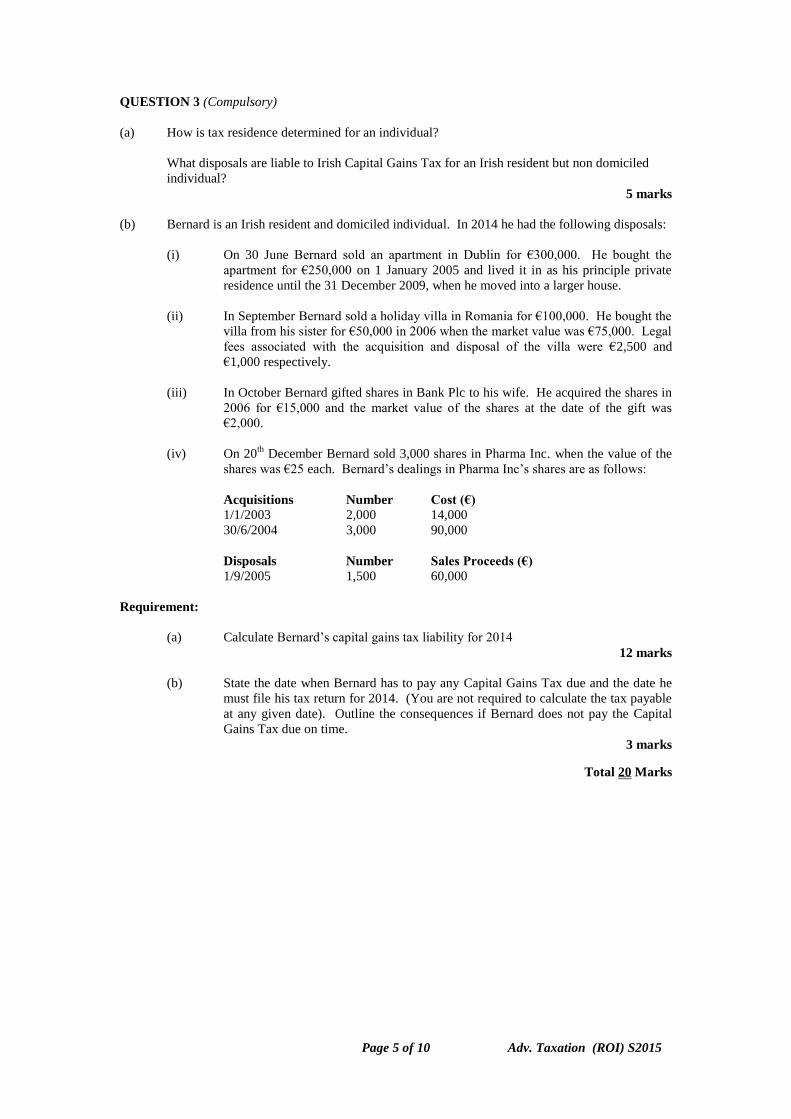

QUESTION 3 (Compulsory)

(a) How is tax residence determined for an individual?

What disposals are liable to Irish Capital Gains Tax for an Irish resident but non domiciled

individual?

5 marks

(b) Bernard is an Irish resident and domiciled individual. In 2014 he had the following disposals:

(i) On 30 June Bernard sold an apartment in Dublin for €300,000. He bought the

apartment for €250,000 on 1 January 2005 and lived it in as his principle private

residence until the 31 December 2009, when he moved into a larger house.

(ii) In September Bernard sold a holiday villa in Romania for €100,000. He bought the

villa from his sister for €50,000 in 2006 when the market value was €75,000. Legal

fees associated with the acquisition and disposal of the villa were €2,500 and

€1,000 respectively.

(iii) In October Bernard gifted shares in Bank Plc to his wife. He acquired the shares in

2006 for €15,000 and the market value of the shares at the date of the gift was

€2,000.

(iv) On 20th

December Bernard sold 3,000 shares in Pharma Inc. when the value of the

shares was €25 each. Bernard’s dealings in Pharma Inc’s shares are as follows:

Acquisitions Number Cost (€)

1/1/2003 2,000 14,000

30/6/2004 3,000 90,000

Disposals Number Sales Proceeds (€)

1/9/2005 1,500 60,000

Requirement:

(a) Calculate Bernard’s capital gains tax liability for 2014

12 marks

(b) State the date when Bernard has to pay any Capital Gains Tax due and the date he

must file his tax return for 2014. (You are not required to calculate the tax payable

at any given date). Outline the consequences if Bernard does not pay the Capital

Gains Tax due on time.

3 marks

Total 20 Marks

Page 6 of 10 Adv. Taxation (ROI) S2015

SECTION B

Answer ANY TWO of the FOUR questions in Section B

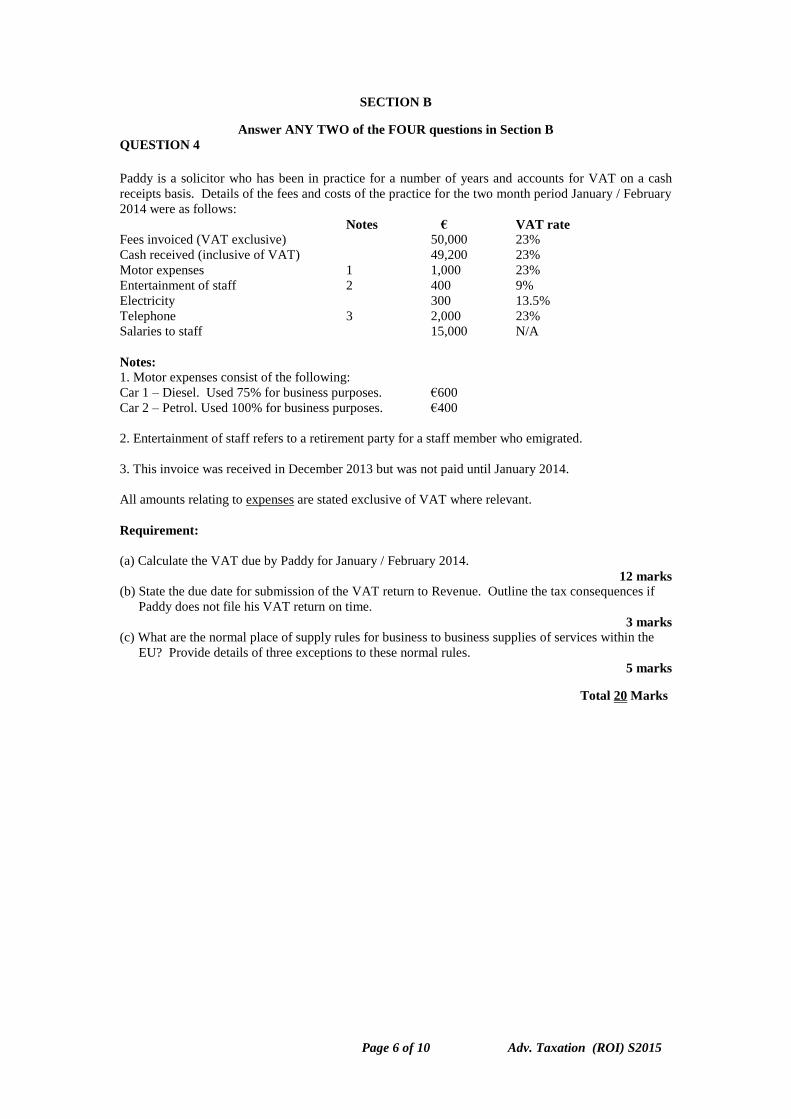

QUESTION 4

Paddy is a solicitor who has been in practice for a number of years and accounts for VAT on a cash

receipts basis. Details of the fees and costs of the practice for the two month period January / February

2014 were as follows:

Notes € VAT rate

Fees invoiced (VAT exclusive) 50,000 23%

Cash received (inclusive of VAT) 49,200 23%

Motor expenses 1 1,000 23%

Entertainment of staff 2 400 9%

Electricity 300 13.5%

Telephone 3 2,000 23%

Salaries to staff 15,000 N/A

Notes:

1. Motor expenses consist of the following:

Car 1 – Diesel. Used 75% for business purposes. €600

Car 2 – Petrol. Used 100% for business purposes. €400

2. Entertainment of staff refers to a retirement party for a staff member who emigrated.

3. This invoice was received in December 2013 but was not paid until January 2014.

All amounts relating to expenses are stated exclusive of VAT where relevant.

Requirement:

(a) Calculate the VAT due by Paddy for January / February 2014.

12 marks

(b) State the due date for submission of the VAT return to Revenue. Outline the tax consequences if

Paddy does not file his VAT return on time.

3 marks

(c) What are the normal place of supply rules for business to business supplies of services within the

EU? Provide details of three exceptions to these normal rules.

5 marks

Total 20 Marks

Page 7 of 10 Adv. Taxation (ROI) S2015

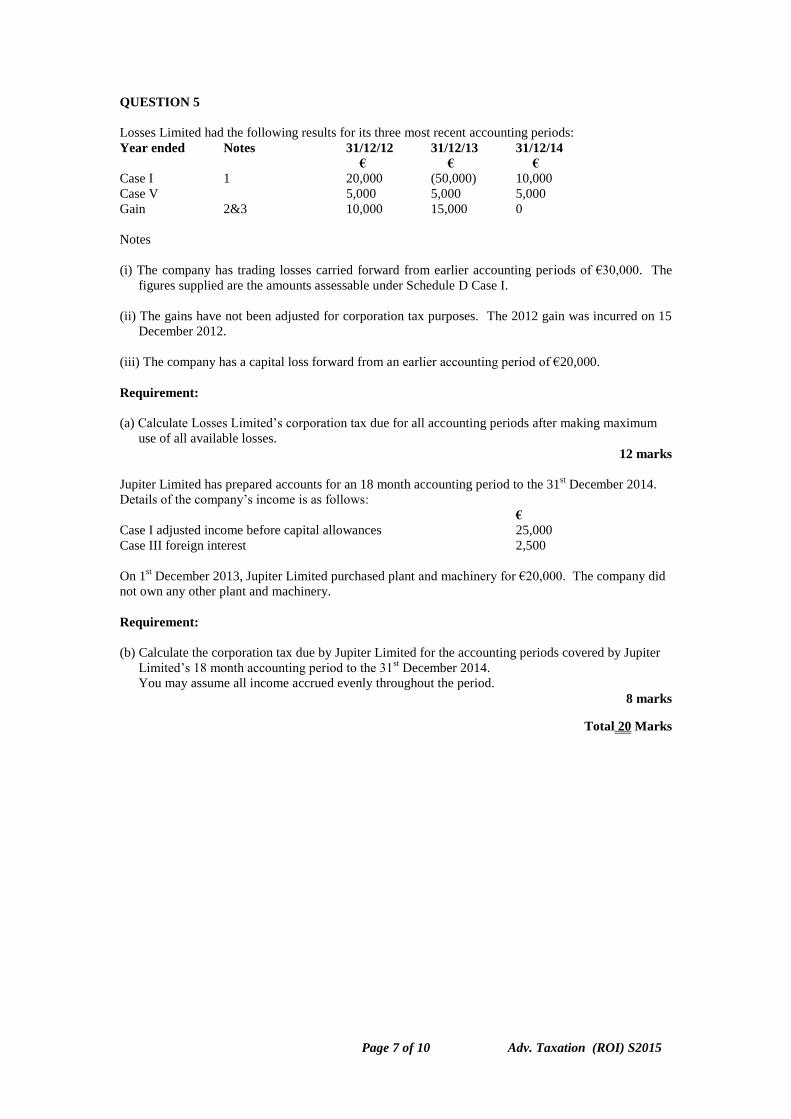

QUESTION 5

Losses Limited had the following results for its three most recent accounting periods:

Year ended Notes 31/12/12 31/12/13 31/12/14

€ € €

Case I 1 20,000 (50,000) 10,000

Case V 5,000 5,000 5,000

Gain 2&3 10,000 15,000 0

Notes

(i) The company has trading losses carried forward from earlier accounting periods of €30,000. The

figures supplied are the amounts assessable under Schedule D Case I.

(ii) The gains have not been adjusted for corporation tax purposes. The 2012 gain was incurred on 15

December 2012.

(iii) The company has a capital loss forward from an earlier accounting period of €20,000.

Requirement:

(a) Calculate Losses Limited’s corporation tax due for all accounting periods after making maximum

use of all available losses.

12 marks

Jupiter Limited has prepared accounts for an 18 month accounting period to the 31st December 2014.

Details of the company’s income is as follows:

€

Case I adjusted income before capital allowances 25,000

Case III foreign interest 2,500

On 1st December 2013, Jupiter Limited purchased plant and machinery for €20,000. The company did

not own any other plant and machinery.

Requirement:

(b) Calculate the corporation tax due by Jupiter Limited for the accounting periods covered by Jupiter

Limited’s 18 month accounting period to the 31st December 2014.

You may assume all income accrued evenly throughout the period.

8 marks

Total 20 Marks

Page 8 of 10 Adv. Taxation (ROI) S2015

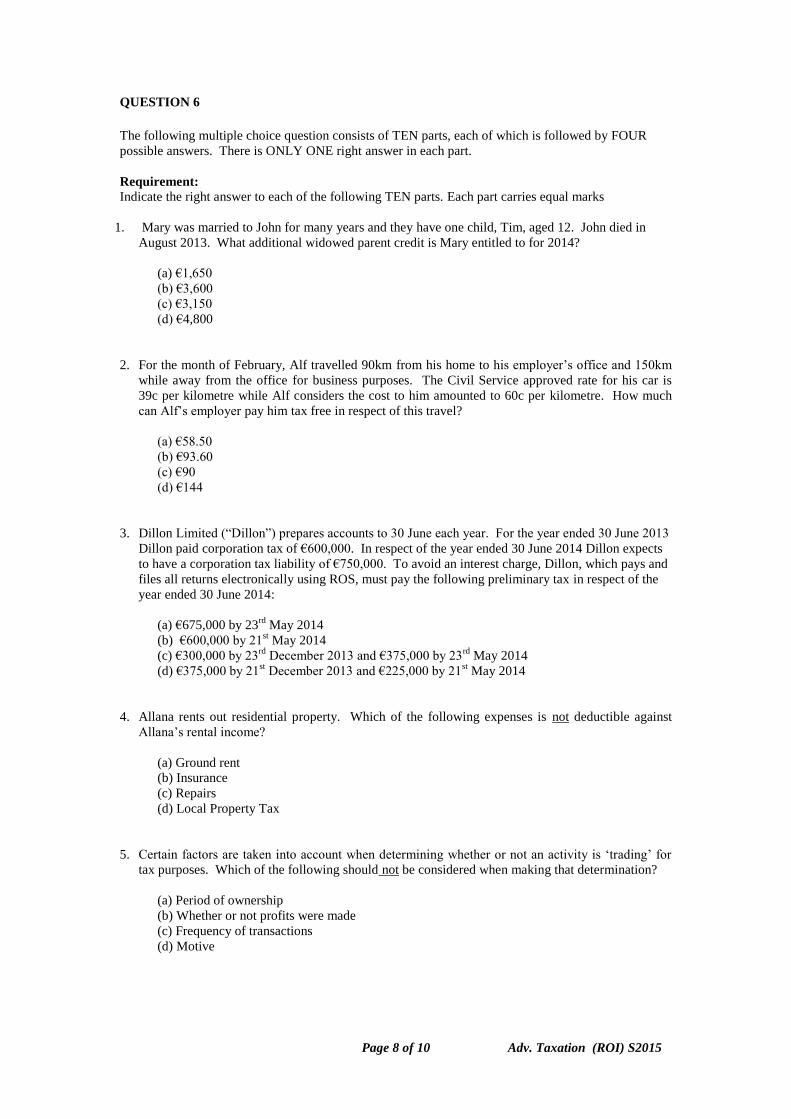

QUESTION 6

The following multiple choice question consists of TEN parts, each of which is followed by FOUR

possible answers. There is ONLY ONE right answer in each part.

Requirement:

Indicate the right answer to each of the following TEN parts. Each part carries equal marks

1. Mary was married to John for many years and they have one child, Tim, aged 12. John died in

August 2013. What additional widowed parent credit is Mary entitled to for 2014?

(a) €1,650

(b) €3,600

(c) €3,150

(d) €4,800

2. For the month of February, Alf travelled 90km from his home to his employer’s office and 150km

while away from the office for business purposes. The Civil Service approved rate for his car is

39c per kilometre while Alf considers the cost to him amounted to 60c per kilometre. How much

can Alf’s employer pay him tax free in respect of this travel?

(a) €58.50

(b) €93.60

(c) €90

(d) €144

3. Dillon Limited (“Dillon”) prepares accounts to 30 June each year. For the year ended 30 June 2013

Dillon paid corporation tax of €600,000. In respect of the year ended 30 June 2014 Dillon expects

to have a corporation tax liability of €750,000. To avoid an interest charge, Dillon, which pays and

files all returns electronically using ROS, must pay the following preliminary tax in respect of the

year ended 30 June 2014:

(a) €675,000 by 23rd

May 2014

(b) €600,000 by 21st May 2014

(c) €300,000 by 23rd

December 2013 and €375,000 by 23rd

May 2014

(d) €375,000 by 21st December 2013 and €225,000 by 21

st May 2014

4. Allana rents out residential property. Which of the following expenses is not deductible against

Allana’s rental income?

(a) Ground rent

(b) Insurance

(c) Repairs

(d) Local Property Tax

5. Certain factors are taken into account when determining whether or not an activity is ‘trading’ for

tax purposes. Which of the following should not be considered when making that determination?

(a) Period of ownership

(b) Whether or not profits were made

(c) Frequency of transactions

(d) Motive

Page 9 of 10 Adv. Taxation (ROI) S2015

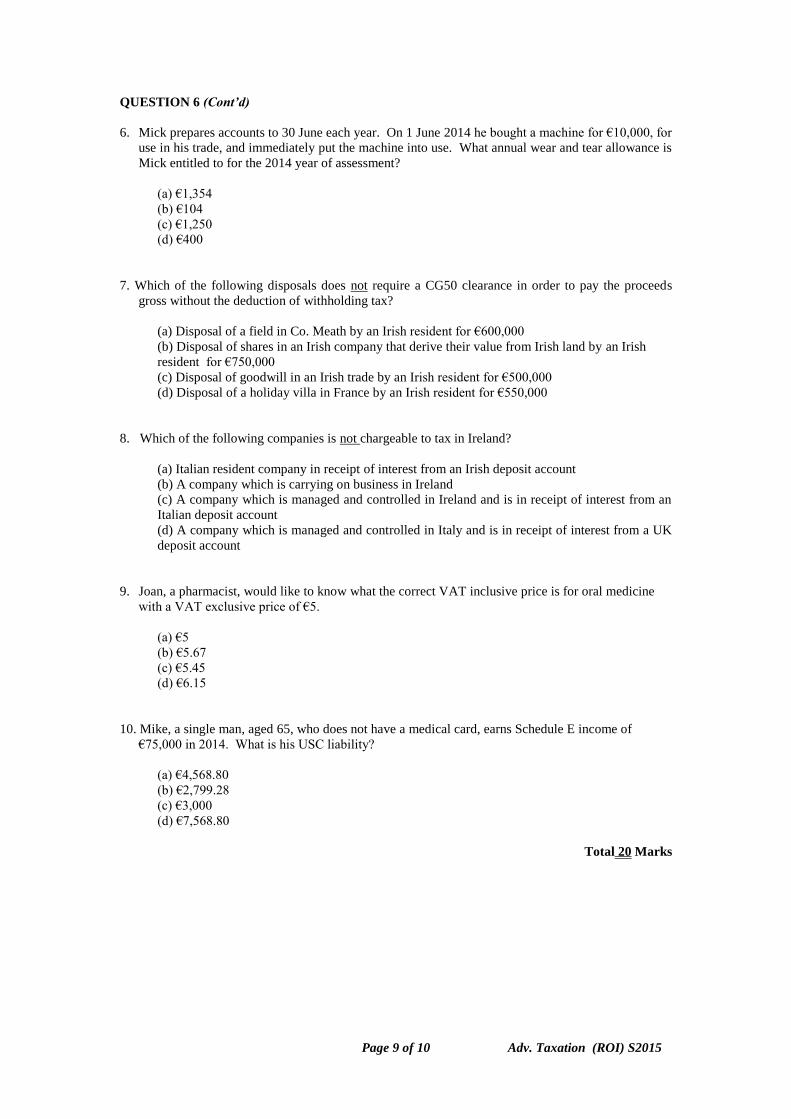

QUESTION 6 (Cont’d)

6. Mick prepares accounts to 30 June each year. On 1 June 2014 he bought a machine for €10,000, for

use in his trade, and immediately put the machine into use. What annual wear and tear allowance is

Mick entitled to for the 2014 year of assessment?

(a) €1,354

(b) €104

(c) €1,250

(d) €400

7. Which of the following disposals does not require a CG50 clearance in order to pay the proceeds

gross without the deduction of withholding tax?

(a) Disposal of a field in Co. Meath by an Irish resident for €600,000

(b) Disposal of shares in an Irish company that derive their value from Irish land by an Irish

resident for €750,000

(c) Disposal of goodwill in an Irish trade by an Irish resident for €500,000

(d) Disposal of a holiday villa in France by an Irish resident for €550,000

8. Which of the following companies is not chargeable to tax in Ireland?

(a) Italian resident company in receipt of interest from an Irish deposit account

(b) A company which is carrying on business in Ireland

(c) A company which is managed and controlled in Ireland and is in receipt of interest from an

Italian deposit account

(d) A company which is managed and controlled in Italy and is in receipt of interest from a UK

deposit account

9. Joan, a pharmacist, would like to know what the correct VAT inclusive price is for oral medicine

with a VAT exclusive price of €5.

(a) €5

(b) €5.67

(c) €5.45

(d) €6.15

10. Mike, a single man, aged 65, who does not have a medical card, earns Schedule E income of

€75,000 in 2014. What is his USC liability?

(a) €4,568.80

(b) €2,799.28

(c) €3,000

(d) €7,568.80

Total 20 Marks

Page 10 of 10 Adv. Taxation (ROI) S2015

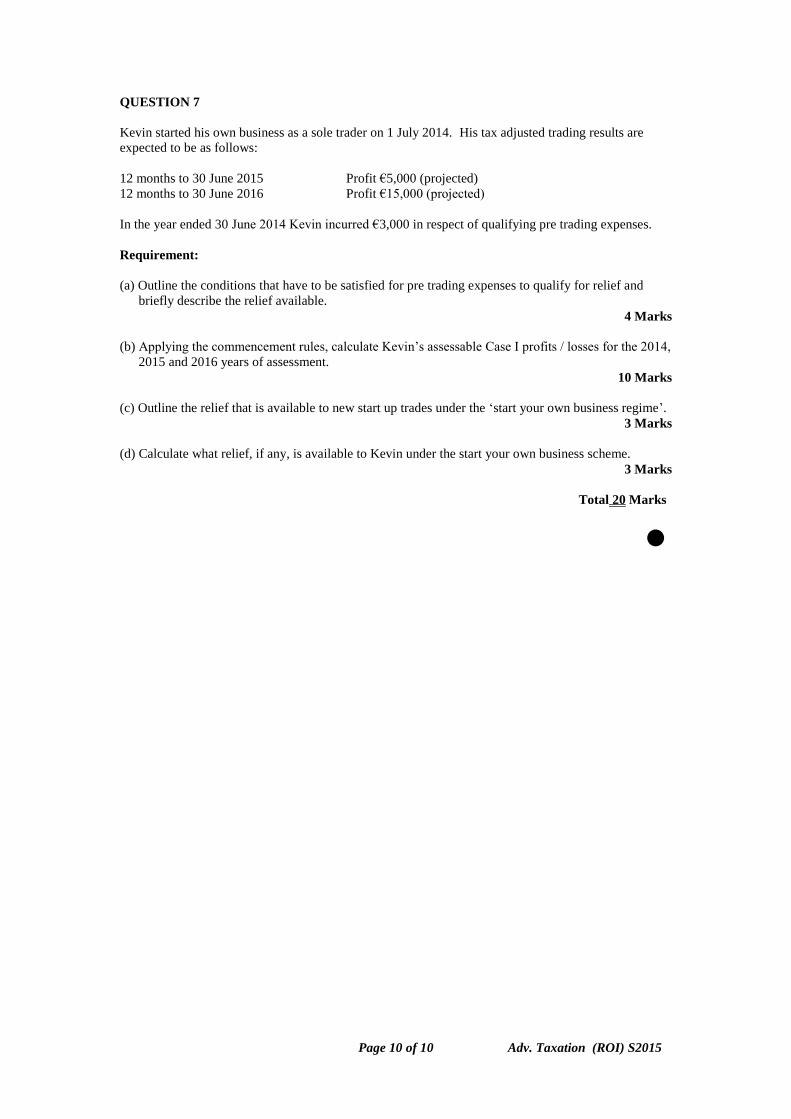

QUESTION 7

Kevin started his own business as a sole trader on 1 July 2014. His tax adjusted trading results are

expected to be as follows:

12 months to 30 June 2015 Profit €5,000 (projected)

12 months to 30 June 2016 Profit €15,000 (projected)

In the year ended 30 June 2014 Kevin incurred €3,000 in respect of qualifying pre trading expenses.

Requirement:

(a) Outline the conditions that have to be satisfied for pre trading expenses to qualify for relief and

briefly describe the relief available.

4 Marks

(b) Applying the commencement rules, calculate Kevin’s assessable Case I profits / losses for the 2014,

2015 and 2016 years of assessment.

10 Marks

(c) Outline the relief that is available to new start up trades under the ‘start your own business regime’.

3 Marks

(d) Calculate what relief, if any, is available to Kevin under the start your own business scheme.

3 Marks

Total 20 Marks

Advanced Taxation ROI May 2015 2nd Year Paper

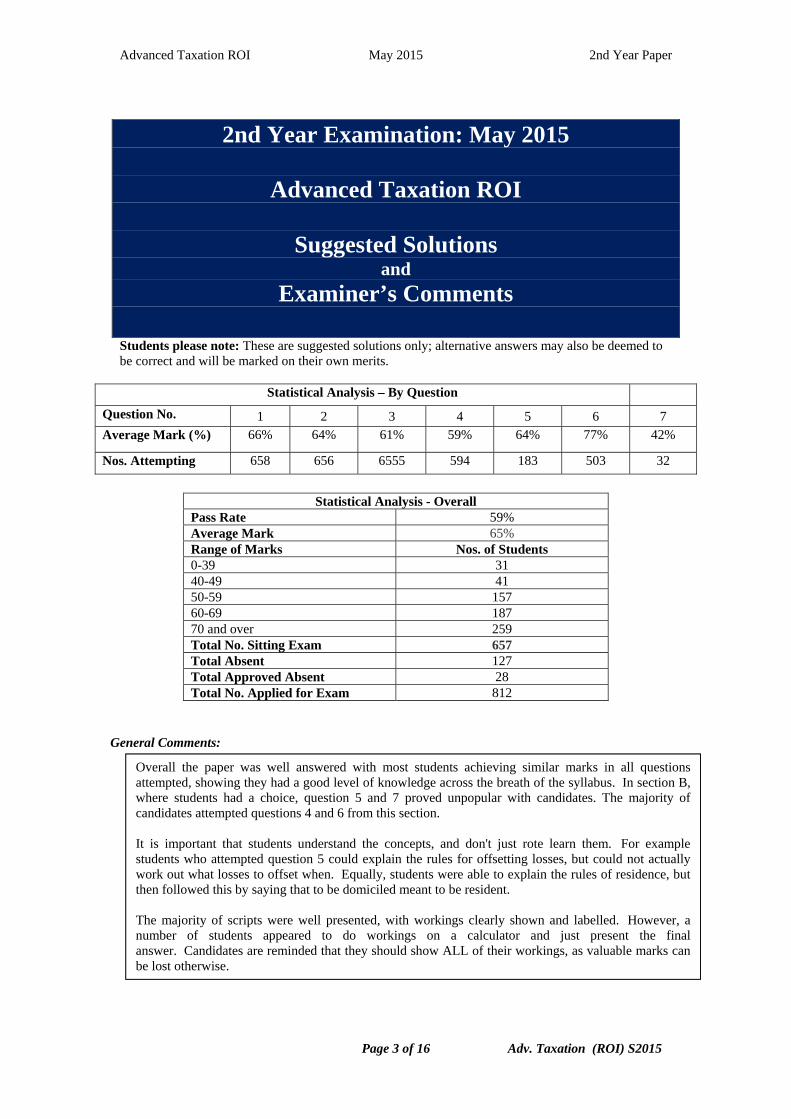

Page 3 of 16 Adv. Taxation (ROI) S2015

2nd Year Examination: May 2015

Advanced Taxation ROI

Suggested Solutions

and

Examiner’s Comments

Students please note: These are suggested solutions only; alternative answers may also be deemed to be correct and will be marked on their own merits.

Statistical Analysis – By Question

Question No. 1 2 3 4 5 6 7 Average Mark (%) 66% 64% 61% 59% 64% 77% 42%

Nos. Attempting 658 656 6555 594 183 503 32

Statistical Analysis - Overall

Pass Rate 59% Average Mark 65% Range of Marks Nos. of Students 0-39 31 40-49 41 50-59 157 60-69 187 70 and over 259 Total No. Sitting Exam 657 Total Absent 127 Total Approved Absent 28 Total No. Applied for Exam 812

General Comments:

Overall the paper was well answered with most students achieving similar marks in all questions attempted, showing they had a good level of knowledge across the breath of the syllabus. In section B, where students had a choice, question 5 and 7 proved unpopular with candidates. The majority of candidates attempted questions 4 and 6 from this section. It is important that students understand the concepts, and don't just rote learn them. For example students who attempted question 5 could explain the rules for offsetting losses, but could not actually work out what losses to offset when. Equally, students were able to explain the rules of residence, but then followed this by saying that to be domiciled meant to be resident. The majority of scripts were well presented, with workings clearly shown and labelled. However, a number of students appeared to do workings on a calculator and just present the final answer. Candidates are reminded that they should show ALL of their workings, as valuable marks can be lost otherwise.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 4 of 16 Adv. Taxation (ROI) S2015

SECTION A

Answer QUESTION 1 and QUESTION 2 and QUESTION 3 (Compulsory) in this Section

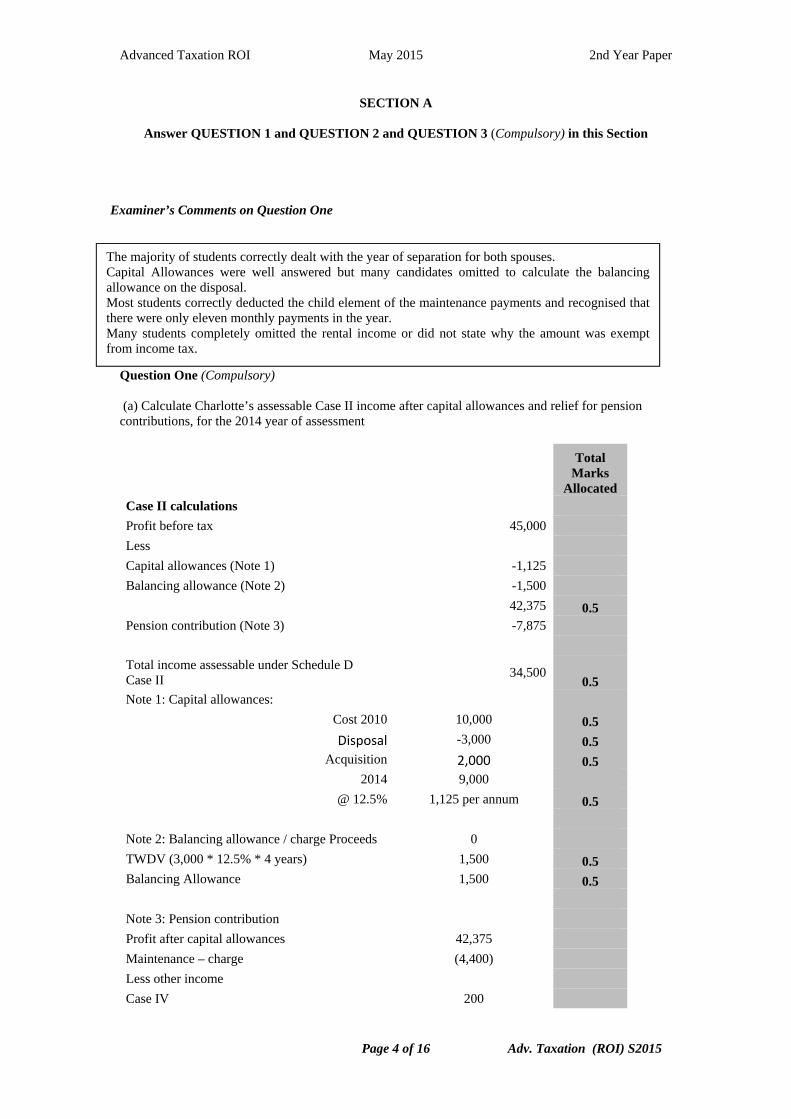

Examiner’s Comments on Question One

Question One (Compulsory) (a) Calculate Charlotte’s assessable Case II income after capital allowances and relief for pension contributions, for the 2014 year of assessment

Total Marks

Allocated Case II calculations Profit before tax 45,000 Less Capital allowances (Note 1) -1,125 Balancing allowance (Note 2) -1,500

42,375 0.5 Pension contribution (Note 3) -7,875 Total income assessable under Schedule D Case II

34,500 0.5

Note 1: Capital allowances:

Cost 2010 10,000 0.5

Disposal -3,000 0.5 Acquisition 2,000 0.5

2014 9,000

@ 12.5% 1,125 per annum 0.5

Note 2: Balancing allowance / charge Proceeds 0

TWDV (3,000 * 12.5% * 4 years) 1,500 0.5 Balancing Allowance 1,500 0.5

Note 3: Pension contribution

Profit after capital allowances 42,375

Maintenance – charge (4,400)

Less other income

Case IV 200

The majority of students correctly dealt with the year of separation for both spouses. Capital Allowances were well answered but many candidates omitted to calculate the balancing allowance on the disposal. Most students correctly deducted the child element of the maintenance payments and recognised that there were only eleven monthly payments in the year. Many students completely omitted the rental income or did not state why the amount was exempt from income tax.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 5 of 16 Adv. Taxation (ROI) S2015

Schedule F 1,200

Net Relevant Earnings 39,375 0.5 Max pension contribution @ 20% 7,875 0.5 Actual pension contributions (€800 * 12) 9,600 0.5 Maximum pension contributions 7,875 0.5

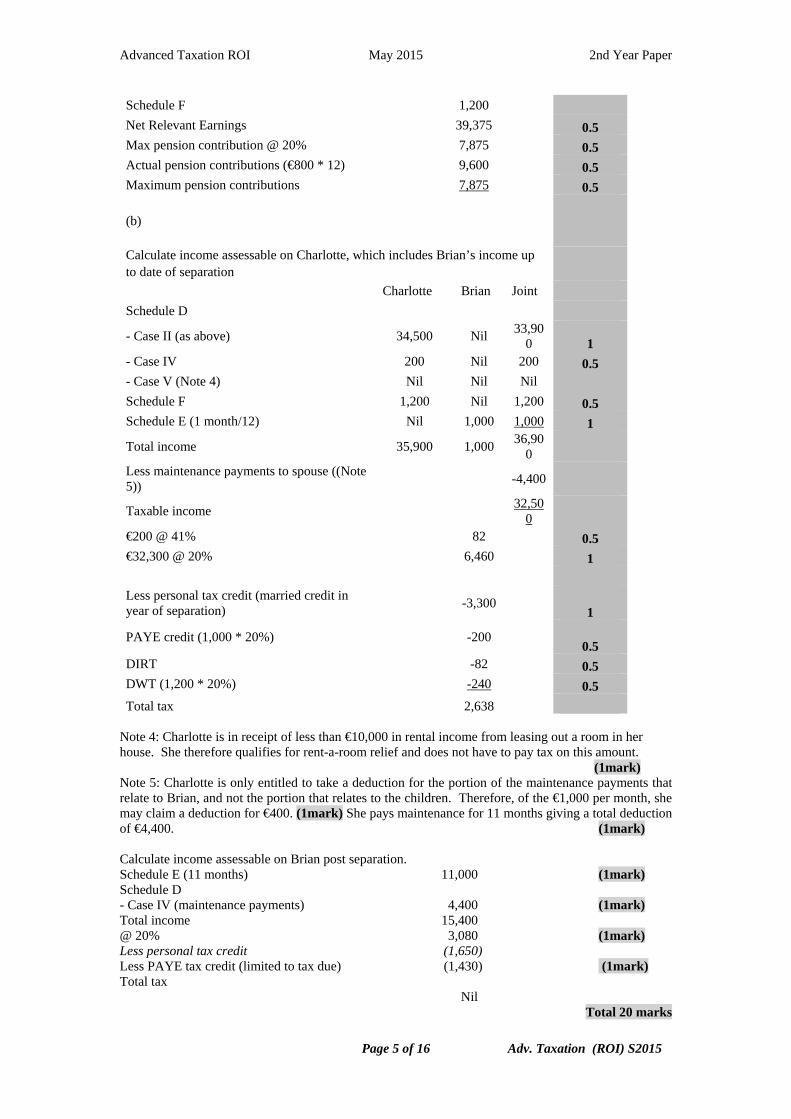

(b)

Calculate income assessable on Charlotte, which includes Brian’s income up to date of separation

Charlotte Brian Joint Schedule D

- Case II (as above) 34,500 Nil 33,90

0 1 - Case IV 200 Nil 200 0.5 - Case V (Note 4) Nil Nil Nil Schedule F 1,200 Nil 1,200 0.5 Schedule E (1 month/12) Nil 1,000 1,000 1

Total income 35,900 1,000 36,90

0 Less maintenance payments to spouse ((Note 5))

-4,400

Taxable income 32,50

0 €200 @ 41% 82 0.5 €32,300 @ 20% 6,460 1 Less personal tax credit (married credit in year of separation)

-3,300 1

PAYE credit (1,000 * 20%) -200 0.5

DIRT -82 0.5 DWT (1,200 * 20%) -240 0.5

Total tax 2,638 Note 4: Charlotte is in receipt of less than €10,000 in rental income from leasing out a room in her house. She therefore qualifies for rent-a-room relief and does not have to pay tax on this amount.

(1mark) Note 5: Charlotte is only entitled to take a deduction for the portion of the maintenance payments that relate to Brian, and not the portion that relates to the children. Therefore, of the €1,000 per month, she may claim a deduction for €400. (1mark) She pays maintenance for 11 months giving a total deduction of €4,400. (1mark) Calculate income assessable on Brian post separation. Schedule E (11 months) 11,000 (1mark) Schedule D - Case IV (maintenance payments) 4,400 (1mark) Total income 15,400 @ 20% 3,080 (1mark) Less personal tax credit (1,650) Less PAYE tax credit (limited to tax due) (1,430) (1mark) Total tax Nil

Total 20 marks

Advanced Taxation ROI May 2015 2nd Year Paper

Page 6 of 16 Adv. Taxation (ROI) S2015

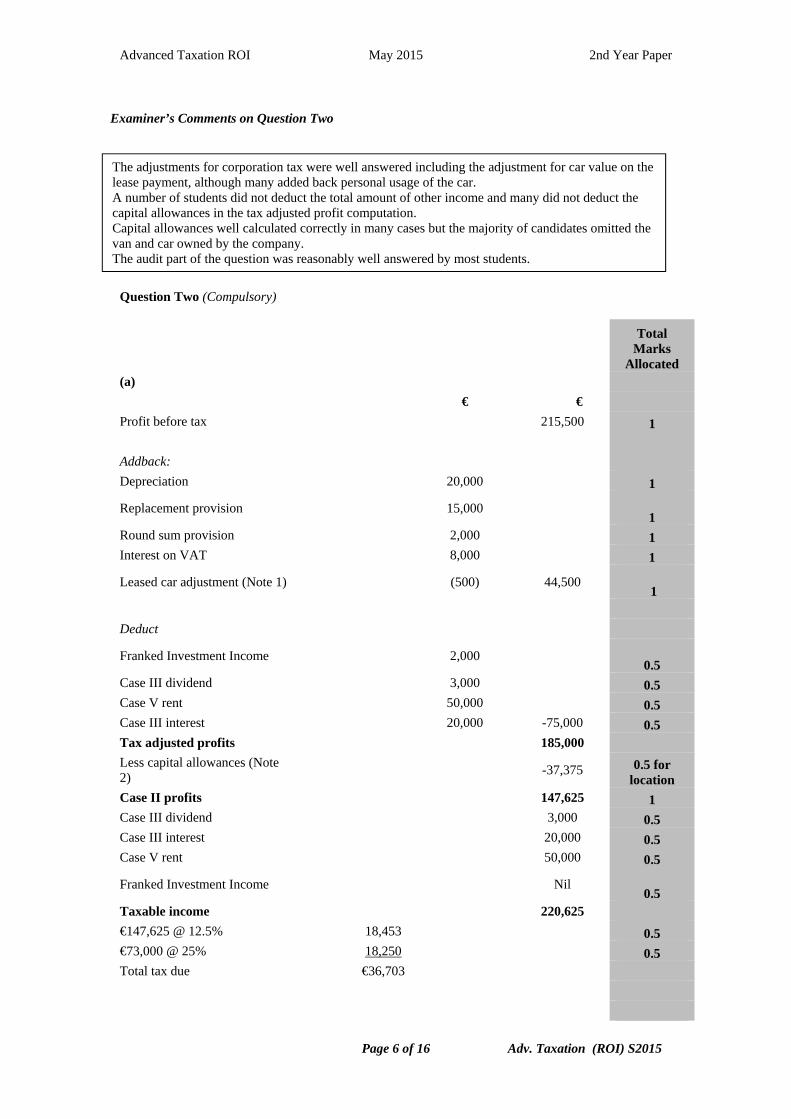

Examiner’s Comments on Question Two

Question Two (Compulsory)

Total Marks

Allocated (a)

€ € Profit before tax 215,500 1

Addback: Depreciation 20,000 1

Replacement provision

15,000 1

Round sum provision 2,000 1 Interest on VAT 8,000 1

Leased car adjustment (Note 1)

(500) 44,500 1

Deduct

Franked Investment Income

2,000 0.5

Case III dividend 3,000 0.5 Case V rent 50,000 0.5 Case III interest 20,000 -75,000 0.5 Tax adjusted profits 185,000 Less capital allowances (Note 2)

-37,375 0.5 for location

Case II profits 147,625 1 Case III dividend 3,000 0.5 Case III interest 20,000 0.5 Case V rent 50,000 0.5

Franked Investment Income

Nil 0.5

Taxable income 220,625 €147,625 @ 12.5% 18,453 0.5 €73,000 @ 25% 18,250 0.5 Total tax due €36,703

The adjustments for corporation tax were well answered including the adjustment for car value on the lease payment, although many added back personal usage of the car. A number of students did not deduct the total amount of other income and many did not deduct the capital allowances in the tax adjusted profit computation. Capital allowances well calculated correctly in many cases but the majority of candidates omitted the van and car owned by the company. The audit part of the question was reasonably well answered by most students.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 7 of 16 Adv. Taxation (ROI) S2015

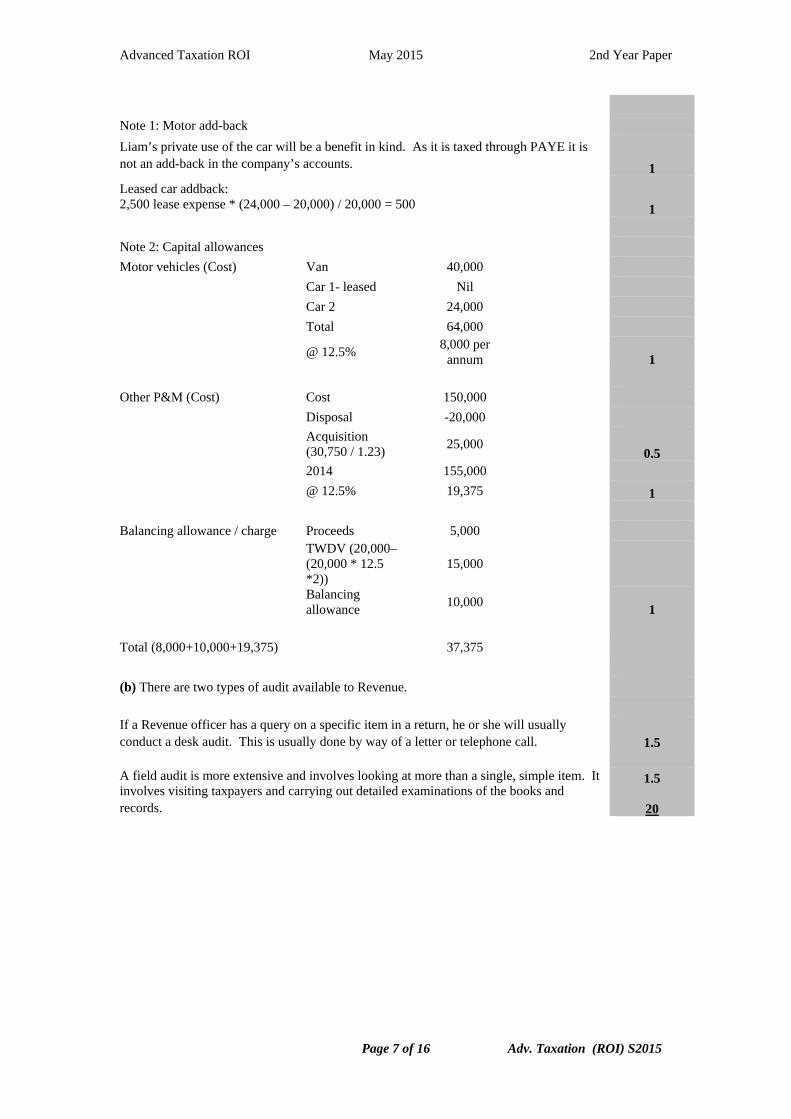

Note 1: Motor add-back

Liam’s private use of the car will be a benefit in kind. As it is taxed through PAYE it is not an add-back in the company’s accounts. 1

Leased car addback: 2,500 lease expense * (24,000 – 20,000) / 20,000 = 500 1

Note 2: Capital allowances Motor vehicles (Cost) Van 40,000

Car 1- leased Nil

Car 2 24,000

Total 64,000

@ 12.5% 8,000 per

annum 1 Other P&M (Cost) Cost 150,000

Disposal -20,000

Acquisition (30,750 / 1.23)

25,000 0.5

2014 155,000

@ 12.5% 19,375 1 Balancing allowance / charge Proceeds 5,000

TWDV (20,000– (20,000 * 12.5 *2))

15,000

Balancing allowance

10,000 1

Total (8,000+10,000+19,375) 37,375

(b) There are two types of audit available to Revenue.

If a Revenue officer has a query on a specific item in a return, he or she will usually conduct a desk audit. This is usually done by way of a letter or telephone call. 1.5 A field audit is more extensive and involves looking at more than a single, simple item. It involves visiting taxpayers and carrying out detailed examinations of the books and records.

1.5

20

Advanced Taxation ROI May 2015 2nd Year Paper

Page 8 of 16 Adv. Taxation (ROI) S2015

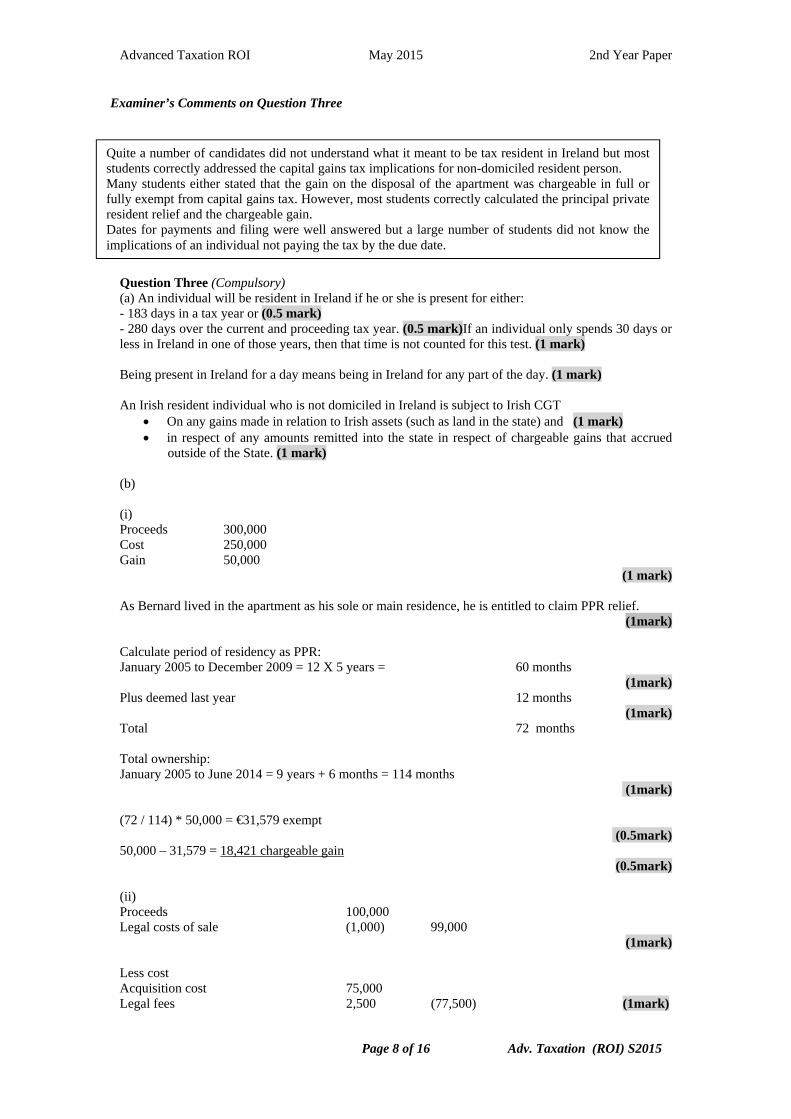

Examiner’s Comments on Question Three

Question Three (Compulsory) (a) An individual will be resident in Ireland if he or she is present for either: - 183 days in a tax year or (0.5 mark) - 280 days over the current and proceeding tax year. (0.5 mark)If an individual only spends 30 days or less in Ireland in one of those years, then that time is not counted for this test. (1 mark) Being present in Ireland for a day means being in Ireland for any part of the day. (1 mark) An Irish resident individual who is not domiciled in Ireland is subject to Irish CGT

On any gains made in relation to Irish assets (such as land in the state) and (1 mark) in respect of any amounts remitted into the state in respect of chargeable gains that accrued

outside of the State. (1 mark) (b) (i) Proceeds 300,000 Cost 250,000 Gain 50,000

(1 mark) As Bernard lived in the apartment as his sole or main residence, he is entitled to claim PPR relief.

(1mark) Calculate period of residency as PPR: January 2005 to December 2009 = 12 X 5 years = 60 months

(1mark) Plus deemed last year 12 months

(1mark) Total 72 months Total ownership: January 2005 to June 2014 = 9 years + 6 months = 114 months

(1mark) (72 / 114) * 50,000 = €31,579 exempt

(0.5mark) 50,000 – 31,579 = 18,421 chargeable gain

(0.5mark) (ii) Proceeds 100,000 Legal costs of sale (1,000) 99,000

(1mark) Less cost Acquisition cost 75,000 Legal fees 2,500 (77,500) (1mark)

Quite a number of candidates did not understand what it meant to be tax resident in Ireland but most students correctly addressed the capital gains tax implications for non-domiciled resident person. Many students either stated that the gain on the disposal of the apartment was chargeable in full or fully exempt from capital gains tax. However, most students correctly calculated the principal private resident relief and the chargeable gain. Dates for payments and filing were well answered but a large number of students did not know the implications of an individual not paying the tax by the due date.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 9 of 16 Adv. Taxation (ROI) S2015

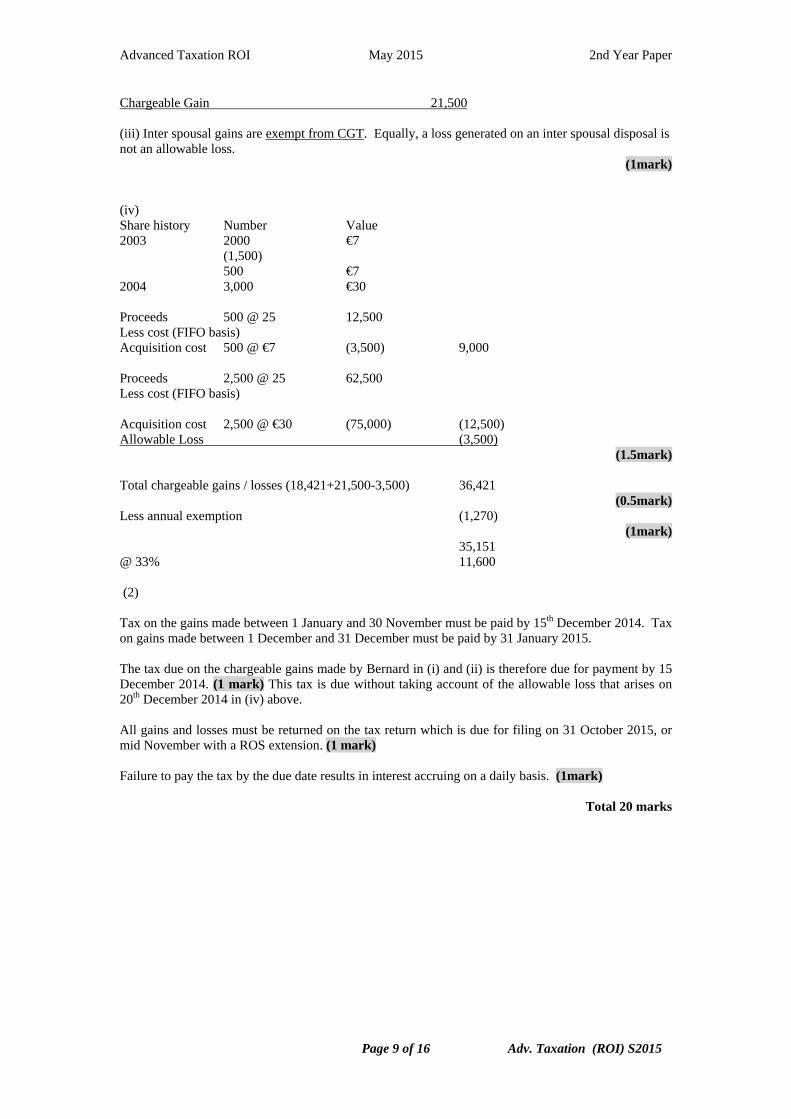

Chargeable Gain 21,500 (iii) Inter spousal gains are exempt from CGT. Equally, a loss generated on an inter spousal disposal is not an allowable loss.

(1mark) (iv) Share history Number Value 2003 2000 €7 (1,500) 500 €7 2004 3,000 €30 Proceeds 500 @ 25 12,500 Less cost (FIFO basis) Acquisition cost 500 @ €7 (3,500) 9,000 Proceeds 2,500 @ 25 62,500 Less cost (FIFO basis)

Acquisition cost 2,500 @ €30 (75,000) (12,500) Allowable Loss (3,500)

(1.5mark) Total chargeable gains / losses (18,421+21,500-3,500) 36,421

(0.5mark) Less annual exemption (1,270)

(1mark) 35,151 @ 33% 11,600 (2) Tax on the gains made between 1 January and 30 November must be paid by 15th December 2014. Tax on gains made between 1 December and 31 December must be paid by 31 January 2015. The tax due on the chargeable gains made by Bernard in (i) and (ii) is therefore due for payment by 15 December 2014. (1 mark) This tax is due without taking account of the allowable loss that arises on 20th December 2014 in (iv) above. All gains and losses must be returned on the tax return which is due for filing on 31 October 2015, or mid November with a ROS extension. (1 mark) Failure to pay the tax by the due date results in interest accruing on a daily basis. (1mark)

Total 20 marks

Advanced Taxation ROI May 2015 2nd Year Paper

Page 10 of 16 Adv. Taxation (ROI) S2015

SECTION B

Answer ANY TWO of the FOUR questions in Section B

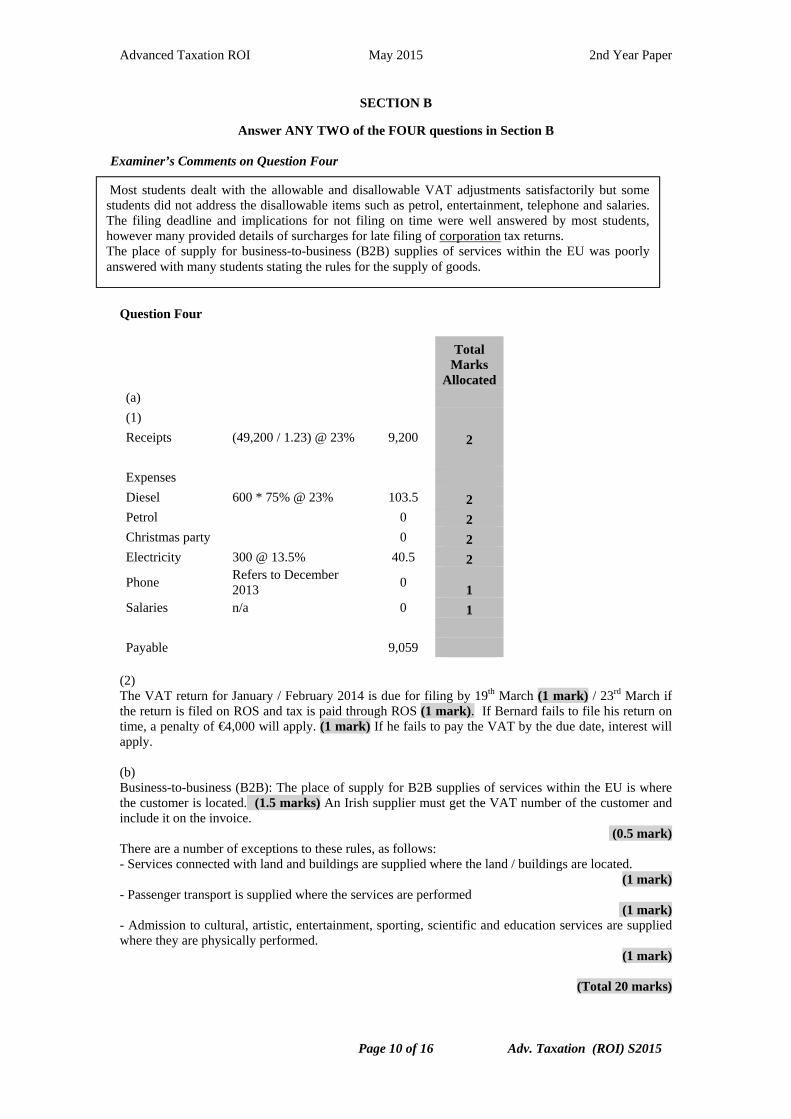

Examiner’s Comments on Question Four

Question Four

Total Marks

Allocated (a)

(1) Receipts (49,200 / 1.23) @ 23% 9,200 2 Expenses Diesel 600 * 75% @ 23% 103.5 2 Petrol 0 2 Christmas party 0 2 Electricity 300 @ 13.5% 40.5 2

Phone Refers to December 2013

0 1

Salaries n/a 0 1

Payable 9,059 (2) The VAT return for January / February 2014 is due for filing by 19th March (1 mark) / 23rd March if the return is filed on ROS and tax is paid through ROS (1 mark). If Bernard fails to file his return on time, a penalty of €4,000 will apply. (1 mark) If he fails to pay the VAT by the due date, interest will apply. (b) Business-to-business (B2B): The place of supply for B2B supplies of services within the EU is where the customer is located. (1.5 marks) An Irish supplier must get the VAT number of the customer and include it on the invoice.

(0.5 mark) There are a number of exceptions to these rules, as follows: - Services connected with land and buildings are supplied where the land / buildings are located.

(1 mark) - Passenger transport is supplied where the services are performed

(1 mark) - Admission to cultural, artistic, entertainment, sporting, scientific and education services are supplied where they are physically performed.

(1 mark)

(Total 20 marks)

Most students dealt with the allowable and disallowable VAT adjustments satisfactorily but some students did not address the disallowable items such as petrol, entertainment, telephone and salaries. The filing deadline and implications for not filing on time were well answered by most students, however many provided details of surcharges for late filing of corporation tax returns. The place of supply for business-to-business (B2B) supplies of services within the EU was poorly answered with many students stating the rules for the supply of goods.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 11 of 16 Adv. Taxation (ROI) S2015

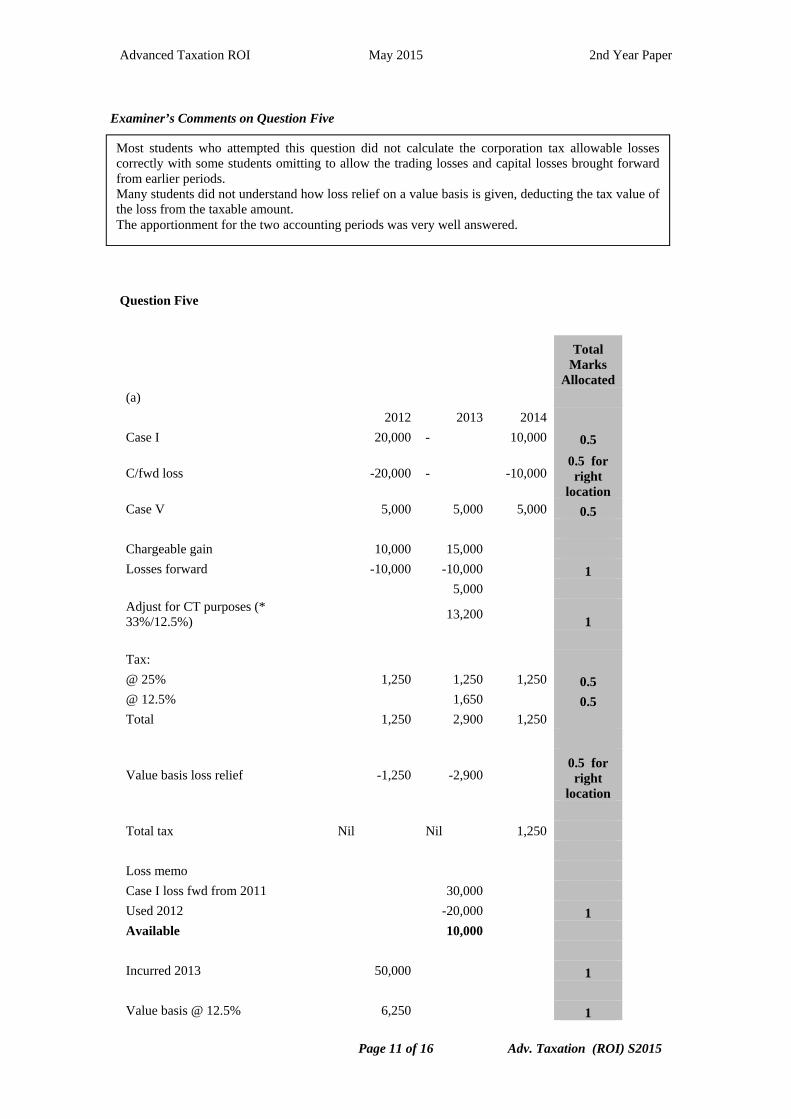

Examiner’s Comments on Question Five

Question Five

Total Marks

Allocated (a)

2012 2013 2014 Case I 20,000 - 10,000 0.5

C/fwd loss -20,000 - -10,000 0.5 for right

location Case V 5,000 5,000 5,000 0.5 Chargeable gain 10,000 15,000 Losses forward -10,000 -10,000 1

5,000 Adjust for CT purposes (* 33%/12.5%) 13,200 1 Tax: @ 25% 1,250 1,250 1,250 0.5 @ 12.5% 1,650 0.5 Total 1,250 2,900 1,250

Value basis loss relief -1,250 -2,900 0.5 for right

location Total tax Nil Nil 1,250 Loss memo Case I loss fwd from 2011 30,000 Used 2012 -20,000 1 Available 10,000 Incurred 2013 50,000 1 Value basis @ 12.5% 6,250 1

Most students who attempted this question did not calculate the corporation tax allowable losses correctly with some students omitting to allow the trading losses and capital losses brought forward from earlier periods. Many students did not understand how loss relief on a value basis is given, deducting the tax value of the loss from the taxable amount. The apportionment for the two accounting periods was very well answered.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 12 of 16 Adv. Taxation (ROI) S2015

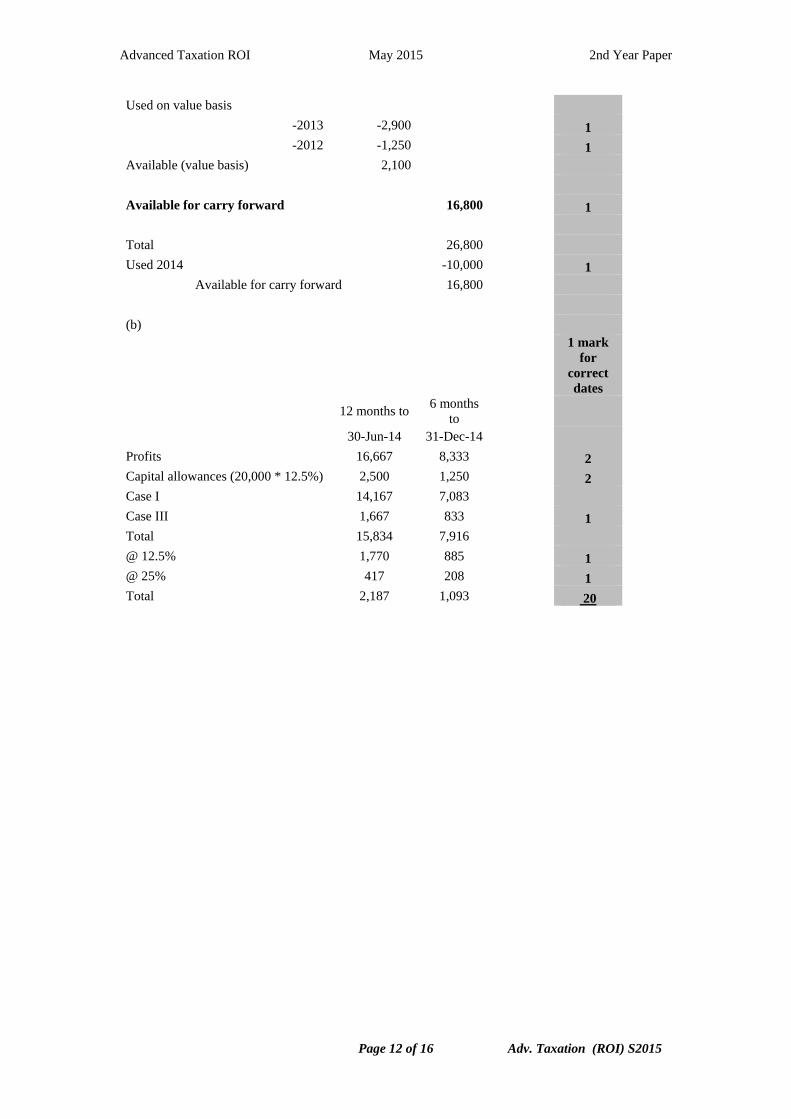

Used on value basis -2013 -2,900 1 -2012 -1,250 1

Available (value basis) 2,100 Available for carry forward 16,800 1 Total 26,800 Used 2014 -10,000 1

Available for carry forward 16,800 (b)

1 mark for

correct dates

12 months to 6 months

to

30-Jun-14 31-Dec-14 Profits 16,667 8,333 2 Capital allowances (20,000 * 12.5%) 2,500 1,250 2 Case I 14,167 7,083 Case III 1,667 833 1 Total 15,834 7,916 @ 12.5% 1,770 885 1 @ 25% 417 208 1 Total 2,187 1,093 20

Advanced Taxation ROI May 2015 2nd Year Paper

Page 13 of 16 Adv. Taxation (ROI) S2015

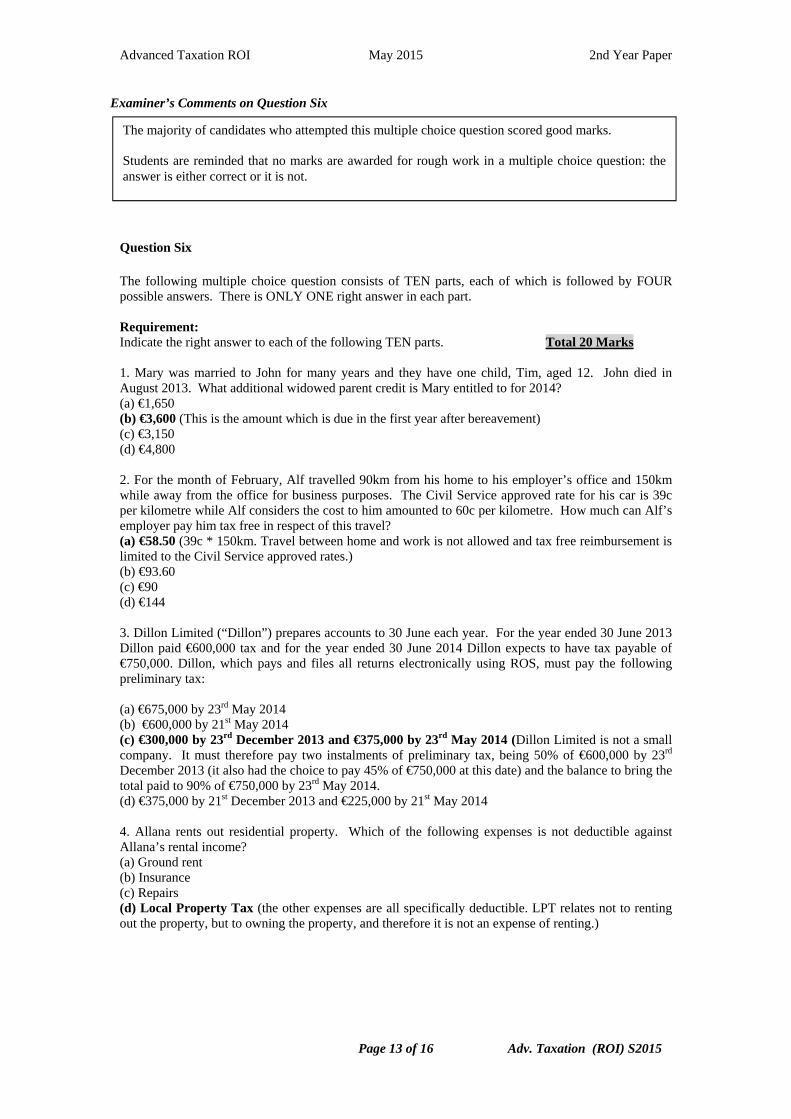

Examiner’s Comments on Question Six

Question Six The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part. Requirement: Indicate the right answer to each of the following TEN parts. Total 20 Marks 1. Mary was married to John for many years and they have one child, Tim, aged 12. John died in August 2013. What additional widowed parent credit is Mary entitled to for 2014? (a) €1,650 (b) €3,600 (This is the amount which is due in the first year after bereavement) (c) €3,150 (d) €4,800 2. For the month of February, Alf travelled 90km from his home to his employer’s office and 150km while away from the office for business purposes. The Civil Service approved rate for his car is 39c per kilometre while Alf considers the cost to him amounted to 60c per kilometre. How much can Alf’s employer pay him tax free in respect of this travel? (a) €58.50 (39c * 150km. Travel between home and work is not allowed and tax free reimbursement is limited to the Civil Service approved rates.) (b) €93.60 (c) €90 (d) €144 3. Dillon Limited (“Dillon”) prepares accounts to 30 June each year. For the year ended 30 June 2013 Dillon paid €600,000 tax and for the year ended 30 June 2014 Dillon expects to have tax payable of €750,000. Dillon, which pays and files all returns electronically using ROS, must pay the following preliminary tax: (a) €675,000 by 23rd May 2014 (b) €600,000 by 21st May 2014 (c) €300,000 by 23rd December 2013 and €375,000 by 23rd May 2014 (Dillon Limited is not a small company. It must therefore pay two instalments of preliminary tax, being 50% of €600,000 by 23rd December 2013 (it also had the choice to pay 45% of €750,000 at this date) and the balance to bring the total paid to 90% of €750,000 by 23rd May 2014. (d) €375,000 by 21st December 2013 and €225,000 by 21st May 2014 4. Allana rents out residential property. Which of the following expenses is not deductible against Allana’s rental income? (a) Ground rent (b) Insurance (c) Repairs (d) Local Property Tax (the other expenses are all specifically deductible. LPT relates not to renting out the property, but to owning the property, and therefore it is not an expense of renting.)

The majority of candidates who attempted this multiple choice question scored good marks. Students are reminded that no marks are awarded for rough work in a multiple choice question: the answer is either correct or it is not.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 14 of 16 Adv. Taxation (ROI) S2015

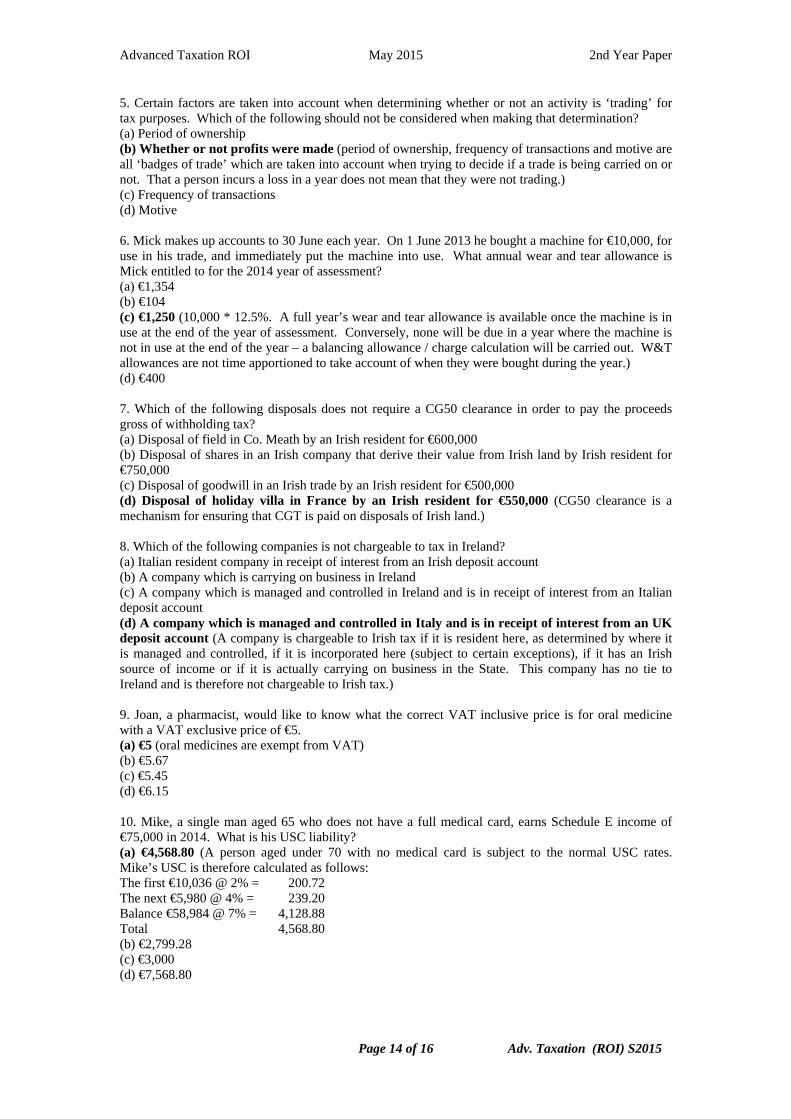

5. Certain factors are taken into account when determining whether or not an activity is ‘trading’ for tax purposes. Which of the following should not be considered when making that determination? (a) Period of ownership (b) Whether or not profits were made (period of ownership, frequency of transactions and motive are all ‘badges of trade’ which are taken into account when trying to decide if a trade is being carried on or not. That a person incurs a loss in a year does not mean that they were not trading.) (c) Frequency of transactions (d) Motive 6. Mick makes up accounts to 30 June each year. On 1 June 2013 he bought a machine for €10,000, for use in his trade, and immediately put the machine into use. What annual wear and tear allowance is Mick entitled to for the 2014 year of assessment? (a) €1,354 (b) €104 (c) €1,250 (10,000 * 12.5%. A full year’s wear and tear allowance is available once the machine is in use at the end of the year of assessment. Conversely, none will be due in a year where the machine is not in use at the end of the year – a balancing allowance / charge calculation will be carried out. W&T allowances are not time apportioned to take account of when they were bought during the year.) (d) €400 7. Which of the following disposals does not require a CG50 clearance in order to pay the proceeds gross of withholding tax? (a) Disposal of field in Co. Meath by an Irish resident for €600,000 (b) Disposal of shares in an Irish company that derive their value from Irish land by Irish resident for €750,000 (c) Disposal of goodwill in an Irish trade by an Irish resident for €500,000 (d) Disposal of holiday villa in France by an Irish resident for €550,000 (CG50 clearance is a mechanism for ensuring that CGT is paid on disposals of Irish land.) 8. Which of the following companies is not chargeable to tax in Ireland? (a) Italian resident company in receipt of interest from an Irish deposit account (b) A company which is carrying on business in Ireland (c) A company which is managed and controlled in Ireland and is in receipt of interest from an Italian deposit account (d) A company which is managed and controlled in Italy and is in receipt of interest from an UK deposit account (A company is chargeable to Irish tax if it is resident here, as determined by where it is managed and controlled, if it is incorporated here (subject to certain exceptions), if it has an Irish source of income or if it is actually carrying on business in the State. This company has no tie to Ireland and is therefore not chargeable to Irish tax.) 9. Joan, a pharmacist, would like to know what the correct VAT inclusive price is for oral medicine with a VAT exclusive price of €5. (a) €5 (oral medicines are exempt from VAT) (b) €5.67 (c) €5.45 (d) €6.15 10. Mike, a single man aged 65 who does not have a full medical card, earns Schedule E income of €75,000 in 2014. What is his USC liability? (a) €4,568.80 (A person aged under 70 with no medical card is subject to the normal USC rates. Mike’s USC is therefore calculated as follows: The first €10,036 @ 2% = 200.72 The next €5,980 @ 4% = 239.20 Balance €58,984 @ 7% = 4,128.88 Total 4,568.80 (b) €2,799.28 (c) €3,000 (d) €7,568.80

Advanced Taxation ROI May 2015 2nd Year Paper

Page 15 of 16 Adv. Taxation (ROI) S2015

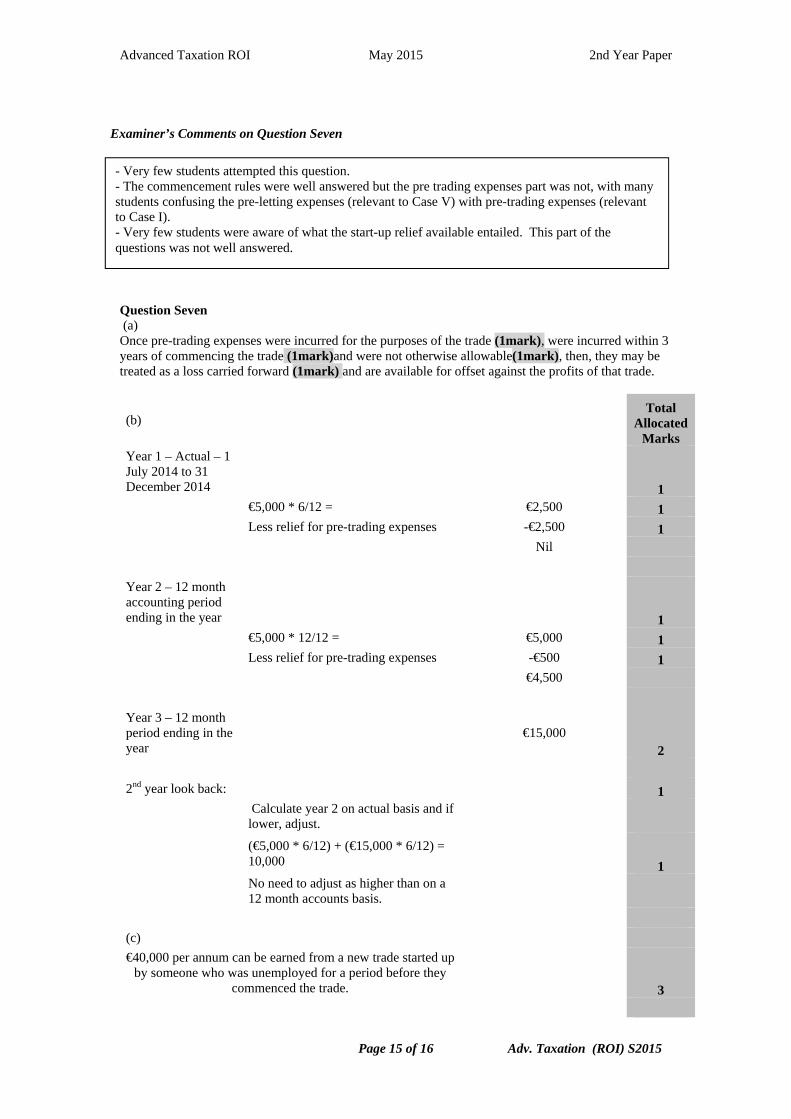

Examiner’s Comments on Question Seven

Question Seven (a) Once pre-trading expenses were incurred for the purposes of the trade (1mark), were incurred within 3 years of commencing the trade (1mark)and were not otherwise allowable(1mark), then, they may be treated as a loss carried forward (1mark) and are available for offset against the profits of that trade.

(b)

Total Allocated

Marks Year 1 – Actual – 1 July 2014 to 31 December 2014 1

€5,000 * 6/12 = €2,500 1

Less relief for pre-trading expenses -€2,500 1

Nil Year 2 – 12 month accounting period ending in the year 1

€5,000 * 12/12 = €5,000 1

Less relief for pre-trading expenses -€500 1

€4,500 Year 3 – 12 month period ending in the year

€15,000 2

2nd year look back: 1

Calculate year 2 on actual basis and if lower, adjust.

(€5,000 * 6/12) + (€15,000 * 6/12) = 10,000 1

No need to adjust as higher than on a 12 month accounts basis.

(c) €40,000 per annum can be earned from a new trade started up

by someone who was unemployed for a period before they commenced the trade. 3

- Very few students attempted this question. - The commencement rules were well answered but the pre trading expenses part was not, with many students confusing the pre-letting expenses (relevant to Case V) with pre-trading expenses (relevant to Case I). - Very few students were aware of what the start-up relief available entailed. This part of the questions was not well answered.

Advanced Taxation ROI May 2015 2nd Year Paper

Page 16 of 16 Adv. Taxation (ROI) S2015

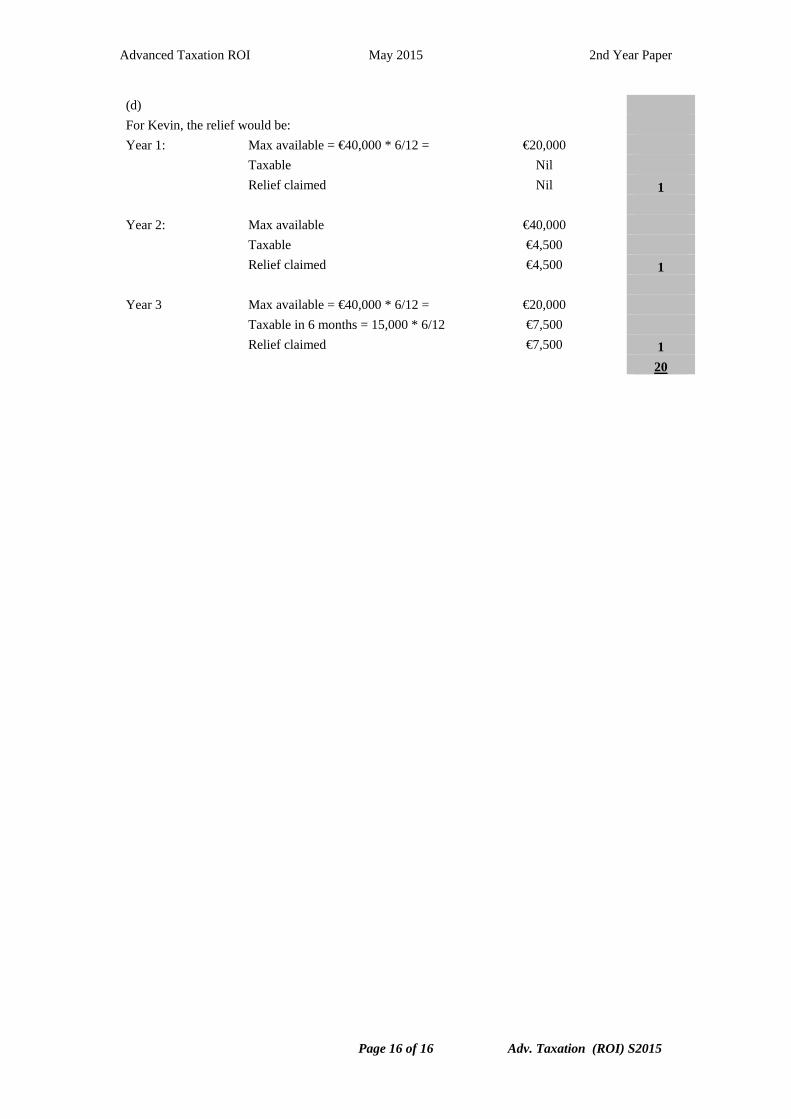

(d) For Kevin, the relief would be: Year 1: Max available = €40,000 * 6/12 = €20,000

Taxable Nil

Relief claimed Nil 1 Year 2: Max available €40,000

Taxable €4,500

Relief claimed €4,500 1 Year 3 Max available = €40,000 * 6/12 = €20,000

Taxable in 6 months = 15,000 * 6/12 €7,500

Relief claimed €7,500 1 20