Embed Size (px)

Citation preview

TAX PROGRESSION UNDER COLLECTIVE WAGE BARGAINING AND INDIVIDUAL EFFORT

DETERMINATION

ERKKI KOSKELA RONNIE SCHÖB

CESIFO WORKING PAPER NO. 2024

CATEGORY 4: LABOUR MARKETS JUNE 2007

Presented at CESifo Area Conference on Employment and Social Protection, May 2007

An electronic version of the paper may be downloaded • from the SSRN website: www.SSRN.com • from the RePEc website: www.RePEc.org

• from the CESifo website: Twww.CESifo-group.deT

CESifo Working Paper No. 2024

TAX PROGRESSION UNDER COLLECTIVE WAGE BARGAINING AND INDIVIDUAL EFFORT

DETERMINATION

Abstract We study the impact of tax policy on wage negotiations, workers’ effort, employment, output and welfare when workers’ effort is only imperfectly observable. We show that the different wage-setting motives – rent sharing and effort incentives – reinforce the effects of partial tax policy measures but not necessarily those of more fundamental tax reforms. Although a higher degree of tax progression always leads to wage moderation, the well-established result from the wage bargaining literature that a revenue-neutral increase in the degree of tax progression is good for employment does not carry over to the case with wage negotiations and imperfectly observable effort. While it remains true that introducing tax progression increases employment and output, we cannot rule out negative effects from an increase in tax progression when tax progression is already very high. Welfare effects are ambiguous a priori but we derive sufficient conditions for welfare improving revenue-neutral increases in tax progression.

JEL Code: J41, J51, H22.

Keywords: wage bargaining, effort determination, tax progression.

Erkki Koskela Department of Economics

P.O. Box 17 Arkadiankatu 7

00014 University of Helsinki Finland

Ronnie Schöb School of Business & Economics

Free University Berlin Boltzmannstr. 20

14195 Berlin Germany

June 2007 This paper has been part of the CESifo project “How to construct Europe”. Koskela thanks Otto-von-Guericke-University Magdeburg for great hospitality as well as the Research Unit of Economic Structures and Growth at the University of Helsinki, the Yrjö Jahnsson Foundation and the Academy of Finland (grant No. 1117698) for financial support. Schöb thanks the WZB in Berlin for great hospitality. The authors are grateful for comments by Lazlo Goerke, Thomas Moutos and from seminar participants at the WZB, Göteborg University, Nordic Tax workshop in Bergen and CESifo area conference on Employment and Social Protection. The usual disclaimer applies.

1

1. Introduction

The result that tax progression leads to wage moderation and is good for employment has

been derived for different assumptions about the wage-setting motives such as rent sharing in

wage bargaining models (see, e.g., Holm and Koskela 1996, Koskela and Vilmunen 1996,

Koskela and Schöb 1999). The results for efficiency wage models, where firms unilaterally

decide upon both the wage rate and the employment level, are, however, still mixed. Wage

moderation has a positive effect on labour demand but a negative effect on individual labour

effort and thus workers’ productivity. Hoel (1990) was the first to analyze the overall effect of

tax progression in such a framework by showing that a higher marginal income tax rate,

which leaves the average tax level unchanged at the initial equilibrium wage rate, will

decrease the gross wage and unemployment (see also Goerke 1999) but Fuest and Huber

(1998) show that, for a rise in tax progression such that the tax burden per worker is the same

in the old and new equilibrium, the result might be reversed.1

It is important to emphasize that the effect of tax progression, however, has not yet been

analyzed in a uniform framework that combines these different wage-setting motives. So far,

only very few papers have combined wage bargaining and effort considerations at all. Early

contributions by Lindbeck and Snower (1991) and Sanfey (1993) do not provide a uniform

answer to the question as to how far different wage-setting motives analyzed in efficiency

wage and union bargaining models reinforce or weaken each other. Later, Bulkley and Myles

(1996) show that with imperfect monitoring of workers’ effort, monopoly trade unions will

set a higher wage than the pure efficiency wage set by the firms. This provides a higher bonus

for non-shirking and results in a higher level of effort than we would observe in a competitive

labor market. Garino and Martin (2000), on the other hand, show that efficiency wages offset

1 All these results do not carry over to models where workers differ in their productivity or when we allow for

market entry. A tax reform that raises marginal tax rates at all income levels and increases (decreases) average taxes at high (low) income levels may lead to higher gross wages and unemployment (see Andersen and Rasmussen 1999). With free entry and exit of firms, Rasmussen (2002) shows that in the long run, changes in profits may imply that higher wage tax progressivity will negatively affect employment if the marginal tax rate is too high.

2

the cost of higher wages and induce firms to make more concessions in wage negotiations.

Thus there is theoretical evidence that the different wage-setting motives reinforce each other.

Within such a framework, Altenburg and Straub (1998) analyze variations of the benefit-

replacement ratio. They find that, in contrast to the standard result in both efficiency wage and

union bargaining models, the effect of a higher reservation utility on wages, employment, and

effort is ambiguous when benefits are financed through lump-sum taxes. A higher

replacement ratio may then reduce the wage rate and raise employment. A higher reservation

utility of workers will induce firms to reduce their demand for effective labor. If, as a

consequence, the labor share decreases, firms experience a higher relative reduction in profits

from a wage increase. This explains why the wage may actually fall and – in the end –

employment will rise.

To our knowledge, only Garcia and Rios (2004) analyze the impact of taxes in this

framework. They adopt the Altenburg and Straub (2002) model to analyze revenue-neutral tax

reforms only numerically. Their numerical calculations suggest that a revenue-neutral

increase in the tax exemption that is financed by an increase in the wage tax increases

employment. This indicates that the result by Koskela and Schöb (1999), according to which a

revenue-neutral shift from payroll taxes to wage taxes raises employment when there is a

higher tax exemption for the latter, also applies when effort is unobservable. Furthermore,

they argue that it is better for employment in the case of constant fiscal revenues to

compensate higher tax exemption through increases in wage taxes rather than payroll taxes.

Since Garcia and Rios (2004) only provide numerical, rather than analytical, results, we first

present an analytical framework to elaborate the way in which tax policy affects wage

negotiations and employment when effort is only imperfectly observable and trade unions and

firms negotiate on wages and then study the impact of a revenue-neutral increase in tax

progression on wage formation, effort determination and employment.

Our comparative statics analysis indicates that the standard results from the trade union

literature must be modified in the case of imperfect monitoring of individual effort

determination. In these standard models, tax policy only affects wages by altering the size of

3

the labor surplus. When both wage-setting motives are present, however, tax policy also

affects the strength with which tax policy parameters affect the negotiated wage and

employment. When effort is not observable, tax policy affects the wage elasticity of effort,

which in turn affects the wage elasticity of labor demand. Since these elasticities alter the

scope with which workers can attract labor rents, this constitutes an additional channel by

which tax policy can influence the wage negotiation. As it turns out, this additional impact

reinforces the effects of partial tax policy measures that we observe in the standard

bargaining and efficiency models.

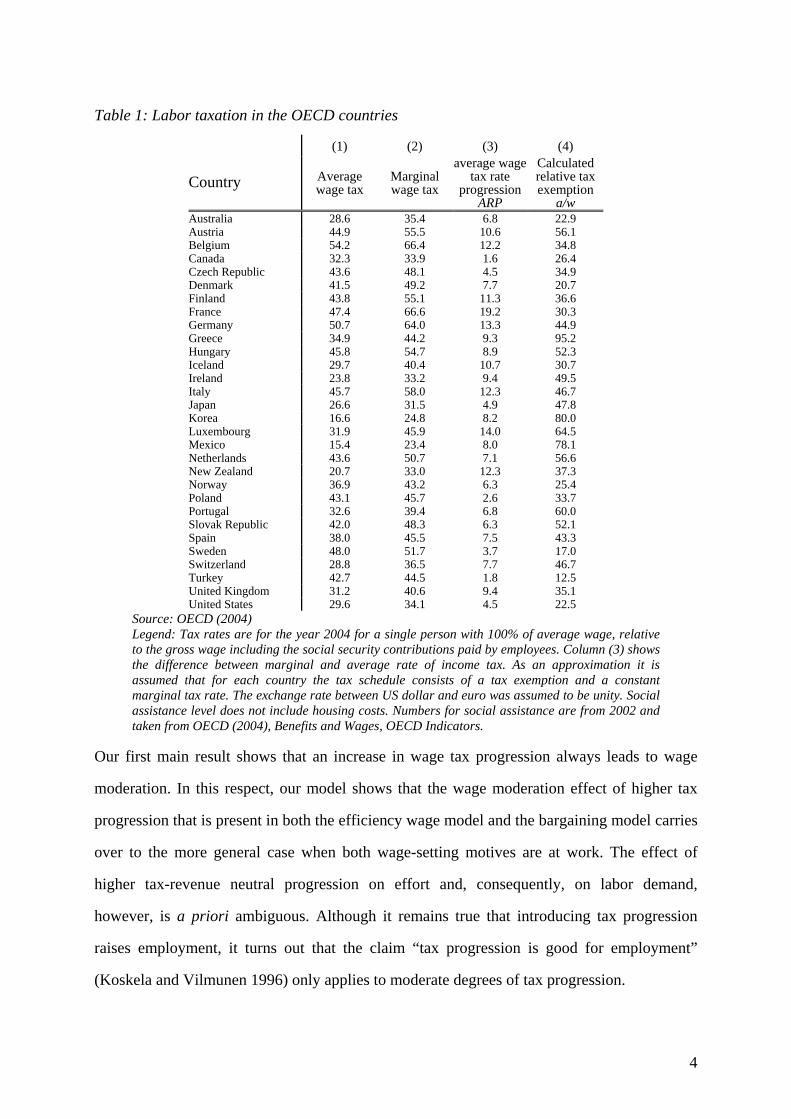

In the second main part of the paper, we then analyze revenue-neutral tax reforms that

change the degree of tax progression, and derive the qualitative effects such tax reforms have

on the negotiated wage, individual effort, and aggregate employment. Table 1 highlights the

importance of such an analysis. The labor tax systems in all the OECD countries are

progressive and show significant differences in the degree of tax progression. We measure tax

progression by the difference between marginal and average tax rates that are shown in the

first and second columns.2 This difference, reported in the third column, is known as the

average wage tax progression ARP (see Lambert 2001, chapters 7 and 8 and our section 5).

The higher this difference, the more progressive wage taxation is. The highest difference is

for France, with 19.2 percentage points, and the lowest one for Canada, with only 1.4

percentage points.

2 To make these figures comparable with our stylized model framework below, all tax rates are with reference

to the gross wage, including payroll taxes paid by the employer.

4

Table 1: Labor taxation in the OECD countries

(1) (2) (3) (4)

Country Average wage tax

Marginal wage tax

average wage tax rate

progressionARP

Calculated relative tax exemption

a/w Australia 28.6 35.4 6.8 22.9 Austria 44.9 55.5 10.6 56.1 Belgium 54.2 66.4 12.2 34.8 Canada 32.3 33.9 1.6 26.4 Czech Republic 43.6 48.1 4.5 34.9 Denmark 41.5 49.2 7.7 20.7 Finland 43.8 55.1 11.3 36.6 France 47.4 66.6 19.2 30.3 Germany 50.7 64.0 13.3 44.9 Greece 34.9 44.2 9.3 95.2 Hungary 45.8 54.7 8.9 52.3 Iceland 29.7 40.4 10.7 30.7 Ireland 23.8 33.2 9.4 49.5 Italy 45.7 58.0 12.3 46.7 Japan 26.6 31.5 4.9 47.8 Korea 16.6 24.8 8.2 80.0 Luxembourg 31.9 45.9 14.0 64.5 Mexico 15.4 23.4 8.0 78.1 Netherlands 43.6 50.7 7.1 56.6 New Zealand 20.7 33.0 12.3 37.3 Norway 36.9 43.2 6.3 25.4 Poland 43.1 45.7 2.6 33.7 Portugal 32.6 39.4 6.8 60.0 Slovak Republic 42.0 48.3 6.3 52.1 Spain 38.0 45.5 7.5 43.3 Sweden 48.0 51.7 3.7 17.0 Switzerland 28.8 36.5 7.7 46.7 Turkey 42.7 44.5 1.8 12.5 United Kingdom 31.2 40.6 9.4 35.1 United States 29.6 34.1 4.5 22.5

Source: OECD (2004) Legend: Tax rates are for the year 2004 for a single person with 100% of average wage, relative to the gross wage including the social security contributions paid by employees. Column (3) shows the difference between marginal and average rate of income tax. As an approximation it is assumed that for each country the tax schedule consists of a tax exemption and a constant marginal tax rate. The exchange rate between US dollar and euro was assumed to be unity. Social assistance level does not include housing costs. Numbers for social assistance are from 2002 and taken from OECD (2004), Benefits and Wages, OECD Indicators.

Our first main result shows that an increase in wage tax progression always leads to wage

moderation. In this respect, our model shows that the wage moderation effect of higher tax

progression that is present in both the efficiency wage model and the bargaining model carries

over to the more general case when both wage-setting motives are at work. The effect of

higher tax-revenue neutral progression on effort and, consequently, on labor demand,

however, is a priori ambiguous. Although it remains true that introducing tax progression

raises employment, it turns out that the claim “tax progression is good for employment”

(Koskela and Vilmunen 1996) only applies to moderate degrees of tax progression.

5

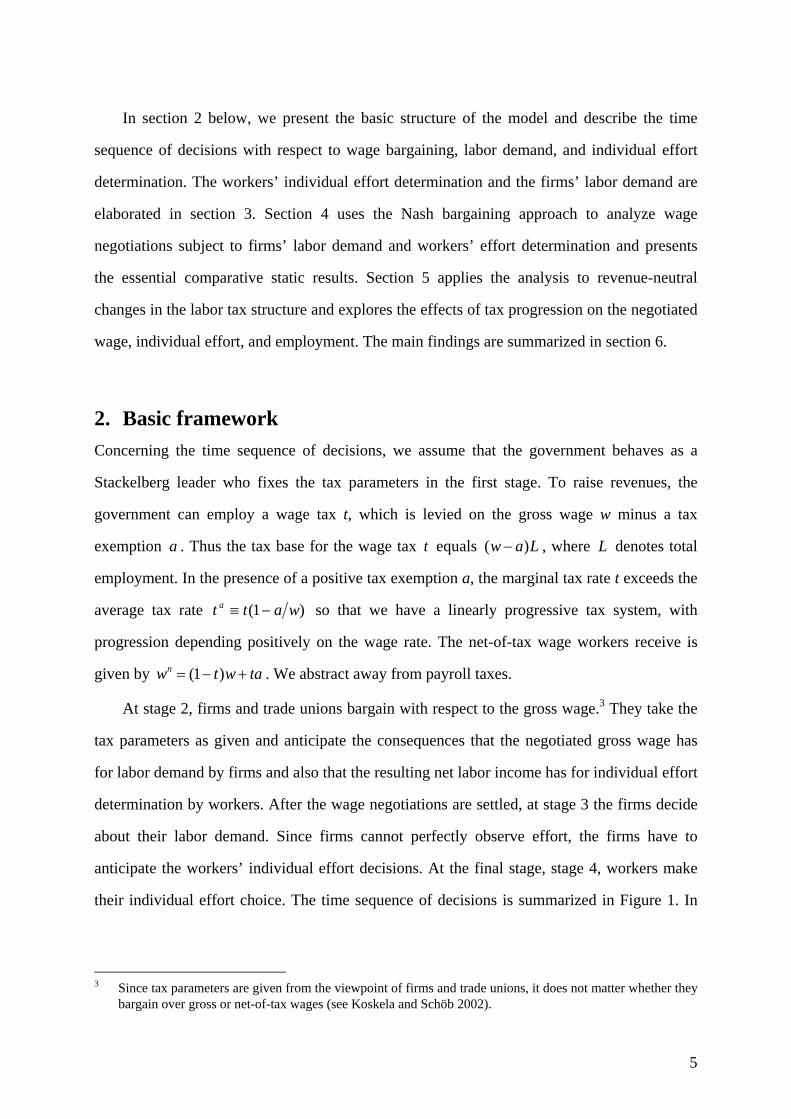

In section 2 below, we present the basic structure of the model and describe the time

sequence of decisions with respect to wage bargaining, labor demand, and individual effort

determination. The workers’ individual effort determination and the firms’ labor demand are

elaborated in section 3. Section 4 uses the Nash bargaining approach to analyze wage

negotiations subject to firms’ labor demand and workers’ effort determination and presents

the essential comparative static results. Section 5 applies the analysis to revenue-neutral

changes in the labor tax structure and explores the effects of tax progression on the negotiated

wage, individual effort, and employment. The main findings are summarized in section 6.

2. Basic framework Concerning the time sequence of decisions, we assume that the government behaves as a

Stackelberg leader who fixes the tax parameters in the first stage. To raise revenues, the

government can employ a wage tax t, which is levied on the gross wage w minus a tax

exemption a . Thus the tax base for the wage tax t equals Law )( − , where L denotes total

employment. In the presence of a positive tax exemption a, the marginal tax rate t exceeds the

average tax rate )1( watt a −≡ so that we have a linearly progressive tax system, with

progression depending positively on the wage rate. The net-of-tax wage workers receive is

given by tawtwn +−= )1( . We abstract away from payroll taxes.

At stage 2, firms and trade unions bargain with respect to the gross wage.3 They take the

tax parameters as given and anticipate the consequences that the negotiated gross wage has

for labor demand by firms and also that the resulting net labor income has for individual effort

determination by workers. After the wage negotiations are settled, at stage 3 the firms decide

about their labor demand. Since firms cannot perfectly observe effort, the firms have to

anticipate the workers’ individual effort decisions. At the final stage, stage 4, workers make

their individual effort choice. The time sequence of decisions is summarized in Figure 1. In

3 Since tax parameters are given from the viewpoint of firms and trade unions, it does not matter whether they

bargain over gross or net-of-tax wages (see Koskela and Schöb 2002).

6

the subsequent sections we derive the decisions taking place at different stages by using

backward induction.

Figure 1: Time sequence of decisions

1 s tag es t

Ta x policy( , )t a

W ag eba rga ining ( )w

La bo rde m an d ( )L

Effo rtde te rm in ation ( )e

2 s ta gen d 3 sta gerd 4 s taget h

3. Individual effort determination and labor demand We start by analyzing the 4th stage, where workers decide about their working effort, taking

the tax policy, the negotiated wage, and aggregate employment as given. Then we analyze

stage 3, where firms determine employment.

3.1. Individual effort determination

We focus on the choice that a single worker faces when employed by a representative firm in

a static framework. Since effort cannot be fully controlled by firms, they can set a standard

effort that we normalize to one. If workers meet this standard, their jobs are secure. If they

shirk by providing less effort, however, firms can fire them. The employment probability can

thus be described by a minimum function. For effort lower than the standard we assume, for

analytical convenience, an iso-elastic probability function of employment de where 0>d

denotes the (constant) employment probability elasticity of effort.4 The employment

probability rises with effort for 1<e and is 1 for higher effort level so that we have the

employment probability function ),1min( de≡ρ and the probability of being laid off is

),1min(1 de− . The parameter d is increasing in both monitoring intensity and monitoring

4 We exclude the case where d = 0 because in this case, the job would be secure even without providing effort

and total output would fall to zero. This would lead firms to set a wage rate equal to zero. Both employment supply and demand would then be indetermined. Futhermore, note that if the detection probability should be concave in effort, we would have to assume 1≤d .

7

efficiency. Low values of d makes it less risky for workers to shirk while +∞→d implies

perfect monitoring and the firing of all workers who do not meet the working effort standard.

Imperfect monitoring implies that when assuming a representative risk-neutral worker

and applying a specific utility function V that is additively separable and quasi-linear, we

obtain

(1) ( )beegweV dndw ),1min(1)]()[,1min( −+−= ,

where b denotes the workers’ outside option, which equals some exogenous unemployment

income, and )(eg denotes the disutility of effort e as a convex function, i.e.

0)('',0)(' >> egeg .5 Working time per worker is assumed to be fixed and normalized to

unity.

For the following, it is convenient to define the workers’ surplus as the difference

begws n −−≡ )( . This allows us to rewrite the utility function as bseV dw += , which splits

the utility into the expected surplus when working with effort e and the basic income b ,

which the household receives in any case. The optimal individual effort level can be derived

from the first-order condition 0)('1 =−= − egesdeV ddwe . The worker chooses an effort level at

which the expected utility loss of working harder, which occurs with probability de , equals

the expected utility gain from an increased probability of staying in employment and

receiving the surplus s. Using the parameterization 1,/)( >θθ= θeeg , the effort function

becomes:

(2) ( ) ( )θθθθ

−≡−⎟⎠⎞

⎜⎝⎛

θ+θ

=111

1

bwAbwd

de nn .

It is straightforward to show that individual effort is increasing in the net-of-tax wage rate,

and decreasing in the outside option. This implies that we have 0<te , because this lowers the

net-of-tax wage and thus reduces the penalty when caught shirking. Accordingly, we observe

5 In what follows, the derivatives of functions with one variable will be denoted by using primes, while partial

derivatives will be denoted by subscripts indicating what variable we are differentiating with respect to.

8

0>we and 0>ae . In fact, we have at et

awe )( −−= , a property we will employ later on. The

wage elasticity of effort is

(3) 0)(

)1(>

−θ−

=≡εbwtw

ewe

nw .

The respective partial derivatives with respect to the outside option b, the tax exemption a,

and the tax rate t are

(4) 0)()1(

2 <−θ−

−=εbw

ttwna ,

(5) 0)()(2

⎪⎭

⎪⎬

⎫

⎪⎩

⎪⎨

⎧

<=>

−θ−

=εbwabw

nt as 0⎪⎭

⎪⎬

⎫

⎪⎩

⎪⎨

⎧

<=>

− ab .

The partial derivatives (4) and (5) depend on the effects the respective parameters have on the

net-of-tax wage relative to the income surplus of working. With respect to an increase in the

tax rate, this effect is ambiguous since a rise in the wage tax lowers )1( tw − but at the same

time raises the effective tax credit ta . A higher tax rate always increases the difference

between the net-of-tax rate in absolute terms, but it may lower the relative difference, which is

decisive for the elasticity if the tax exemption a is very generous. If ab = , the wage elasticity

of effort is unaffected by t since in this case we have ))(1()( bwtbwn −−=− . A higher tax

exemption a implies that a wage rate increase has a lower relative impact on the net-of-tax

wage and thus implies a lower wage elasticity of effort. Only if ab > , a rise in the tax rate

increases the impact a rise in the wage rate has on effort: the higher t is, the stronger the

relative increase of bwn − due to a wage increase is and thus the stronger the relative effect

on individual effort.

The direct effect of a change in the tax exemption is unambiguous. An increase in the tax

exemption implies that a marginal wage increase now has a lower relative impact.

9

3.2. Labor demand

In the 3rd stage of the game, each firm takes the tax parameters and the negotiated wage as

given and decides about the labor demand L by taking into account how the representative

worker will adjust effort. To derive an explicit solution, we postulate a decreasing returns-to-

scale Cobb-Douglas production function in terms of labor and effort:

(6) δ−δ

−δδ

=1

)(1

)( eLeLf , 1>δ .

Profit is given by wLeLf −=π )( . Since firms anticipate the effort level, workers will provide

( 0=eV ), and the first order profit maximization condition is weeLfL −==π )('0 . Using this

specification, we obtain the following labor demand function:

(7) 1−δδ−= ewL .

The partial derivative of labor demand with respect to the tax parameters and the negotiated

wage rate are as follows: 0)1( 1 <−δ= −eeLL tt , 0)1( 1 >−δ= −eeLL aa ,

0))1(()1( 121)1( <δ+δ−ε−=−δ+δ−= −−δδ−−δ−δ− wLeewewL ww .Since the wage tax and the tax

exemption are levied on workers, they only affect labor demand via the workers’ individual

effort, which depends on the net-of-tax wage rate. The wage rate w affects labor demand in

two different ways. Note that the standard assumption that profit decreases with increases in

the wage rate implies that the wage elasticity of effort is smaller than one, i.e. 1<ε . For the

concave production function (6), the wage elasticity of labor demand depends on both the

technological parameter δ and the wage elasticity of individual effort ε as defined in (3):

(8) δ+δ−ε=δ≡− )1(*

LwLw .

The wage elasticity of labor demand is lower compared to the case where wages do not affect

effort. It now depends negatively on the wage elasticity of effort. For 10 <ε≤ we have

δ≤δ< *1 . Hence, in the presence of unobservable individual effort determination the wage

elasticity of labor demand depends on the tax structure and thus tax policy levied on workers.

10

If, for instance, a tax reform increases the wage elasticity of effort, labor demand would

become less elastic. A wage rise would then be less costly for a trade union since the firm

would then lay off fewer workers.

The firm’s indirect profit function, which we will use in the next section, can be obtained

by inserting labor demand (7) into the profit function wLeLf −=π )( :

(9) )1(

)(),(11

11*

−δ=−=π

−δδ−−δδ−δδ− ewewewfew .

Having analyzed workers’ and firms’ behavior with respect to effort and labor demand, we

can now turn to the collective wage bargaining of stage 2.

4. Collective wage bargaining

To derive the negotiated wage, we apply the Nash bargaining solution within a ‘right-to-

manage’ model according to which employment is unilaterally determined by the firms. The

wage bargaining takes place in anticipation of the optimal employment decision by the firms

and the optimal individual effort decision by workers (2).6

The trade union maximizes the sum of the workers utility wV , and the utility of the

unemployed. Since those caught shirking and fired are replaced by unemployed workers, the

expected utility of an unemployed worker is (for inner solutions with 1<ρ ):

(10) ))(()1()1(1 *egwLN

LebLN

LeV nddu −−

−+⎟⎠⎞

⎜⎝⎛

−−−= .

While we assume that a single worker who is caught shirking will become and remain

unemployed as well as receive b , from the viewpoint of the trade union, an unemployed

member will replace a laid-off worker with the lay-off probability, which is de−1 times the

6 Bulkley and Myles (1997) have analyzed the generalized Nash bargain between a trade union and a firm

over employment level and effort level and showed that higher union power will lead to a reduction in the agreed effort level. But they do not study the impact of labor taxes on employment and effort levels.

11

employment share. We can rewrite the linear utilitarian objective function of the trade union

as

(11) NbLesLNVLVU uw +=−+= ** )()(ˆ ,

where the first term captures the workers’ surplus from employment and the second term

captures the exogenously given minimum income for all N members. *L denotes optimal

employment and *e optimal effort in the s term. We denote the relative bargaining power of

the union by β , and that of the firm by )1( β− , and assume that the threat points of the trade

union and the firm are described by NbU =0 and 00 =π , respectively. Applying the Nash

bargaining solution, the negotiating parties decide on the wage w in order to solve

(12) {β−βπ=Ω

1*

)(

)( UwMaxw

, s.t. 0=π= LeV ,

where **0 )(ˆ LesUUU =−= is the bargaining surplus to the trade union by including the

disutility of effort and *π is the indirect profit, presented in equation (9). The Nash bargaining

solution satisfies the following first-order condition:

(13) 0)1( *

*

=ππ

β−+β=Ω www U

U .

As shown in appendix A, we can solve the first-order condition (13) to find the following

implicit Nash bargaining solution for the wage rate in the presence of individual effort

determination:

(14) ⎥⎦⎤

⎢⎣⎡

−−

≡⎥⎦⎤

⎢⎣⎡

−−

⎟⎟⎠

⎞⎜⎜⎝

⎛ε−−δε−−δ+β

=ttabM

ttabw

11)1)(1()1)(1( ,

where 1>M for 1<ε . The negotiated gross wage rate depends on the exogenous income b

when unemployed, the wage tax t and the tax exemption a . Furthermore, it also depends on

the mark-up M that, apart from exogenous parameters, also depends on the wage elasticity of

effort ε .

12

Before we analyze comparative statics of the general case (14), we will first briefly

discuss several special cases, which can be analyzed within the framework we have developed

here.

A. Observable effort

When effort is observable and verifiable, it can become part of the wage contract. If the

contract specifies some fixed effort level e , we obtain the standard right-to-manage model of

union bargaining, where the wage depends on the bargaining power of the trade union and the

(constant) wage elasticity of labor demand in the case of a Cobb-Douglas production function.

Since a constant individual effort e implies 0=ε and a zero probability of being caught

shirking, i.e. 1=ρ , we have

(15a) ⎥⎦⎤

⎢⎣⎡

−−+

≡⎥⎦⎤

⎢⎣⎡

−−+

⎟⎟⎠

⎞⎜⎜⎝

⎛−δ−δ+β

==ρ=ε

ttabegM

ttabegw

1)(

1)(

)1()1(

10 ,

which implies a surplus of =s ( )tabeg −+⎟⎟⎠

⎞⎜⎜⎝

⎛−δβ )(

)1(. From (15a), we can easily derive the

special cases of a monopoly union

⎥⎦⎤

⎢⎣⎡

−−+

⎟⎠⎞

⎜⎝⎛

−δδ

==β=ρ

=εt

tabegw1)(

110

and the competitive labor market outcome where unions have no bargaining power and the

gross wage only compensates for the disutility of working

⎥⎦⎤

⎢⎣⎡

−−+

==ρ

=β=εt

tabegw1)(

10 ,

in which case the firm exploits the complete workers’ surplus, i.e. 0=s .

Alternatively we can consider the case where worker can determine their effort

unilaterally but the firm can observe the effort level. It could then pay a wage per unit of

effective labor input eL. This requires a modification of (1) such that

)()1( egtaetwV w −+−= . Since the tax exemption does not affect the wage rate anymore, in

this case the optimal effort is [ ] 11

* )1( −θ−= twe and the effort elasticity 0)1/(1 >−θ=ε is

13

constant. The profit function becomes weLeLf −=π )( with the firm maximizing with

respect to eL . This gives the following wage elasticity of labor demand

ε+δ=δ≡− */ LwLw . The negotiated wage per worker then becomes7

(15b)

( )

[ ] ( )⎥⎥

⎦

⎤

⎢⎢

⎣

⎡

−−

⎟⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜⎜

⎝

⎛

−θ⎥⎦

⎤⎢⎣

⎡−θβ

−βε+−δ

θε+β+−δ=

⎥⎥

⎦

⎤

⎢⎢

⎣

⎡

−−+

⎟⎟⎠

⎞⎜⎜⎝

⎛βε+−δ

ε+β+−δ=

θ−θ

θ−θ

θ−θ

θ−θ

=ρ≠ε

)1(.

)1()1(

)1(

)1()1(

)1()(

)1()1()1(

1

1

1*

1

10

ttab

ttabegw

The results are similar to the results by Hansen (1999, his case 2) who develops a model

where workers can unilaterally determine their hours of work and where workers and firms

then negotiate upon the hourly wage. The structure of the solution (15b) is qualitatively

similar to that of (15a) in the sense that in both cases the mark-up is independent of tax

instruments.

B. Unobservable effort without bargaining

When 0=β , the firm unilaterally sets the wage. From the first-order condition 0* =πw , it

follows immediately that the firm acts according to the well-known Solow-condition (Solow

1979), i.e. we have 1=ε and thus

(16) ⎥⎦⎤

⎢⎣⎡

−−

≡⎥⎦⎤

⎢⎣⎡

−−

⎟⎠⎞

⎜⎝⎛

−θθ

==π t

tabMttabw

w 111 0.

The model therefore also captures the essence of the efficiency models with a (constant)

mark-up over the outside option.

C. Unobservable effort with bargaining: comparative statics

For the general case, we have 0)1( >ε− and the mark-up is larger than one when the trade

union has some bargaining power, i.e. 0>β . It increases with the relative bargaining power

7 A proof is available from the authors upon request.

14

of the trade union β , and depends negatively on the direct wage elasticity of labor demand δ .

The wage rate now depends, in addition to the relative bargaining power, the wage elasticity

of labor demand, the exogenous income, and the tax parameters, on the elasticity of effort

determination ε . Furthermore, unlike in the case of observable effort, the exogenous income

b when unemployed, the wage tax rate t , and the tax exemption a will also affect the wage

rate via the mark-up M .

The impact of a better monitoring of workers on the negotiated wage is zero as the wage

elasticity of effort is not affected by monitoring. We can thus focus on the comparative statics

of the tax parameters and the outside option in what follows.

The derivative of the mark-up with respect to ε is 0)1()1( 21 >ε−−δβ= −−εM . The mark-

up with respect to effort e is 0=eM . Since condition (14) is an implicit function of w , we

can derive the partial derivative with respect to, for example, a by taking the total derivative

( ) ( ) dattM

ttabM

ttabMdw aw ⎥

⎦

⎤⎢⎣

⎡⎟⎠⎞

⎜⎝⎛−−

+⎟⎠⎞

⎜⎝⎛

−−

ε=⎥⎦

⎤⎢⎣

⎡⎟⎠⎞

⎜⎝⎛

−−

ε− εε 1111 .

By rearranging, we obtain

(17) {{

011

1<⎟

⎠⎞

⎜⎝⎛−−

Δ+⎟

⎠⎞

⎜⎝⎛

−−

⎟⎟⎠

⎞⎜⎜⎝

⎛ε

Δ=

−−

−+

ε

32143421ttM

ttabMw aa

with [ ] 0)1)((1 1 >−−ε−≡Δ −ε ttabM w . In the Nash bargaining solutions with observable effort

(15a) and (15b), the mark-up is independent of a . With unobservable effort, however,

workers will increase effort when the tax exemption rises. When workers have some

bargaining power, i.e. 0>β , this ceteris paribus lowers the mark-up because a lower wage

elasticity of effort implies a higher wage elasticity of labor demand (see equation (8)). A

higher wage then induces less effort, which makes the worker less productive. As a

consequence more layoffs result from a wage increase.

The effect of the wage tax rate can be expressed as

15

(18) {{

0)1(1

12 >⎟⎟⎠

⎞⎜⎜⎝

⎛−−

Δ+⎟

⎠⎞

⎜⎝⎛

−−

⎟⎟⎠

⎞⎜⎜⎝

⎛ε

Δ=

++

++

ε

4342143421tabM

ttabMw tt .

The total effect of a higher wage tax rate on the negotiated wage is a priori ambiguous. When

we assume ab ≥ , both the effect on the mark-up and the effect on the total outside option

with the given mark-up are unambiguously positive.

Hence, tax parameters in our model with both Nash wage bargaining and individual effort

determination affect both of these via a change in the difference between the net-of-tax wage

income and the outside option as well as via a change in the mark-up.

We summarize our new characterization of the negotiated wage under individual effort

determination in

Proposition 1: Unobservable individual effort determination strengthens the

partial effects tax policy measures have on the negotiated wage compared to the

case where effort is observable. Decreasing the tax exemption lowers the

negotiated wage, while an increase in the wage tax rate increases the negotiated

wage under a sufficient but not necessary condition ab ≥ .

We can easily verify that the effects indeed reinforce each other. If we take the partial

derivative of (15a), we obtain the comparative statics effect for the standard bargaining model

with

011

0 <⎟⎠⎞

⎜⎝⎛−−

==ρ=ε

ttMwa ,

( ) ⎟⎟⎠

⎞⎜⎜⎝

⎛−

−+=

=ρ=ε 21

01)(

tabegMwt .

For (15b), we similarily find

011

0 <⎟⎠⎞

⎜⎝⎛−−

==ρ≠ε

ttMwa ,

( ) ⎟⎟⎠

⎞⎜⎜⎝

⎛−−

==ρ≠ε 21

01 t

abMwt .

For ab ≥ , the effects tax parameter changes have on the negotiated wage when effort is

observable are always reinforced when effort is not observable. The partial derivative of

16

equation (16) with respect to a shows the same result for the efficiency wage model: the

different wage-setting motives thus reinforce the partial tax policy effects on gross wages. We

should note, however, that in the case where ab ≤ and 0)( >−+ abeg we would obtain

opposite partial effects for changes in the wage tax rate. An increase in the wage tax will then

increase the gross wage when effort is observable but will lower the gross wage when effort is

unobservable.8

As we pointed out when discussing (15b), the reinforcing effect is also present in a model

with endogenous effort determination.

5. The impact of a tax-revenue-neutral change in tax progression on wage formation, employment, effort, output, and welfare

We are now ready to analyze what are the impacts a revenue-neutral restructuring of the labor

tax, i.e. the degree of wage tax progression, on wage formation, individual effort

determination, and employment. The effect of wage tax progression, which keeps the tax

revenue [ ]LawtG )( −= constant, can be written in the following way:

[ ]dwLawttLtLdaLdtawdG w)()(0 −++−−== . Recalling the definition of the average tax

as ( )watt a −≡ 1 , this can be expressed as

(19) dwtttdt

tawda

a

dG

)()( *

0

δ−+

−=

=.

An appropriate and intuitive way to define tax progression is to look at the average tax rate

progression (ARP), which is given by the difference between the marginal tax rate t and the

average tax rate t a , attARP −= . The tax system is progressive if ARP is positive, and tax

progression is increased if the difference increases (at a given income level, see Lambert

8 We mentioned before that our model also allows us to capture the essence of a model where workers can

endogenously determine working hours when working hours are observable, see the discussion of equation (15b). Interpreting our model as a model of imperfectly observable effective working hours we can i) confirm the results derived by Hansen (1999) for perfectly observable working hours and ii) also find the reinforcing effect when effective working hours cannot be perfectly monitored.

17

2001, chapters 7 and 8). The term *δ− att indicates the marginal tax revenue per worker

when the gross wage increases. It can be decomposed in such a way that we have a tax

progression effect and a tax level effect: )1( *δ−+ atARP . The total effect is non-positive for

a linear tax system with 0=ARP since 0)1( * ≤δ− , but may eventually become positive if

the tax system is sufficiently progressive since the employment effect is weighted by the

average tax rate only. As we will see later on, the degree of tax progression is decisive for the

way in which a revenue-neutral change in tax progression affects both employment and

individual effort.

5.1 Revenue-neutral tax progression and the negotiated wage

The total effect of changes in the tax parameters t and a on the negotiated wage is

(20) dawdtwdw at += ,

with the partial derivatives derived in section 4. Substituting (19) into the RHS of (20) for da

gives

(21) dwtttwdtw

tawdtwdw

a

aat ⎥⎦

⎤⎢⎣

⎡ δ−+

−+=

*)( ,

and, thus, the total effect of a revenue-neutral increase in the wage tax rate is

(22) 1*0 )(1

)(

−= δ−−

−+

=tttw

wt

aww

dtdw

aa

at

dG

.

In what follows, we assume Laffer-efficiency in the sense that a higher wage tax increases tax

revenues while a higher tax exemption leads to lower tax revenues even when we take

account of the indirect effects via changes in w. With respect to the tax exemption, we then

have

01ˆ*

<⎟⎟⎠

⎞⎜⎜⎝

⎛ δ−−−=+−=

tttwtLwGtLG

a

aawa .

18

Substituting the partial derivatives aw from (17) and tw from (18) into the numerator of (22)

shows that the numerator is unambiguously positive (see appendix B). Hence, we have the

following:

Proposition 2 (wage moderation): A revenue-neutral increase in wage tax

progression will moderate the negotiated wage in the presence of individual effort

determination.

The interpretation is straightforward as it turns out that the numerator in equation (22) denotes

the compensated effect an increase in the tax rate has on the wage, keeping the value of the

Nash maximand constant (see appendix C). The revenue-neutral increase in the tax exemption

fully offsets the income effect of the higher wage tax so that only the substitution effect of this

progression-enhancing tax reform remains. This finding shows that the result from

conventional ‘right-to-manage’ models in the absence of effort considerations (see, e.g.,

Koskela and Vilmunen 1996) also applies when we allow for unobservable individual effort

determination.

5.2 Revenue-neutral tax progression and individual effort determination

The total effect of changes in the tax parameters t and a and the negotiated wage on effort

determination is dwedaedtede wat ++= . Substituting the RHS of the tax-revenue neutrality

(19) for da and using aw et

te )1( −= gives

(23)

( )

{( ) .)1(

1)(

0

*

0

*

00

43421

4342144 344 21

−

=+

−

==

=

δ−+−=

⎟⎠⎞

⎜⎝⎛ δ−++

−+=

dG

aa

dGa

awat

dG

dtdwttt

te

dtdwett

tee

tawe

dtde

The direct effects of tax progression parameters on effort will cancel out so that it is only the

induced wage-moderation that affects individual effort decisions. The term tea measures the

19

impact one additional euro has on individual effort. A wage reduction of one euro reduces the

net-of-tax wage by )1( t− so that effort falls by ttea )1( − . But wage-moderation also affects

the amount by which the tax exemption can be raised. It will be lower than the neutral effect

of raising a by taw )( − if 0* <δ− att . This always holds in a linear tax system because in

this case .0)1( * <δ−t But if the tax system becomes very progressive, so that given the

marginal tax rate t the average tax rate ( )watt a −≡ 1 becomes lower and thereby 01 * >δ− at

might be the case, individual effort eventually will fall. This case is also the more likely, the

smaller the wage elasticity of labor demand and the average tax burden are. If we assume a

labor share of 2/3, we have 3=δ , and an average tax below 1/3 would suffice to let effort fall

when tax progression rises. Formally, we have

(24) *

0

10 δ⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

>=<

⇔⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

<=>

=

a

dG

tdtde .

A sufficient, but not a necessary, condition for individual effort to fall is 1<δt since we have

δ<δ* and tta < . These findings can be summarized in

Proposition 3 (individual effort determination): A revenue-neutral increase in

wage tax progression will decrease (increase) individual effort if (i) the wage

elasticity of labor demand and/or (ii) the marginal tax rate are sufficiently low

(high). A sufficient condition is 1<δt ( 1>δt ).

5.3 Revenue-neutral tax progression and employment

Finally, we consider the employment effect. The total effect of changes in the tax parameters t

and a and the negotiated wage on employment is dwLdaLdtLdL wat ++= . Substituting the

RHS of the tax-revenue neutrality for da and using ** )(at e

tawe −

= , wLLw

*** δ

−= and

*

** )1(

eeL a

a−δ

= gives

20

(25)

( )

( )0

****

**

0

***

0

***

*

0

)1(

1))(()1(

=

==

=

⎥⎦

⎤⎢⎣

⎡−−

−=

⎟⎠⎞

⎜⎝⎛ −++

−+

−=

dGa

a

dGa

awat

dG

dtdw

wLett

teL

dtdwLtt

tLe

tawe

eL

dtdL

δδδ

δδ

44 344 21

The first two terms cancel out since they cover the change in t and a that ceteris paribus

would leave the average tax burden, and thus the net-of-tax wage, constant. Hence, we are left

with two effects. As we have seen in section 5.2, the tax reform affects individual effort

depending on the wage elasticity of labor demand and the size of tax parameters. If – as is

likely - effort decreases, labor productivity falls and ceteris paribus employment. On the other

hand, the wage-moderating effect increases labor demand for any given effort level. The total

effect thus becomes ambiguous. From proposition 3 we can immediately infer

Proposition 4 (rising employment): A sufficient, but not necessary, condition

that a revenue-neutral increase in wage tax progression will increase employment

is tt a ≥δ* .

From proposition 4 follows immediately that starting from a linear tax system with tt a = ,

employment will definitely rise. This leads to

Corollary 1 (rising employment): Introducing tax progression is good for

employment when wages are negotiated and effort is determined individually.

Although we have seen that different wage-setting motives reinforce tax policy effects on

gross wages, this is not no longer true with respect to employment. With observable and

verifiable effort, employment is always increasing when tax progression rises. When effort is

unobservable and not verifiable, we find a countervailing effect via the adverse effect a rise in

tax progression has on individual effort.

21

5.4 Revenue-neutral tax progression and output

Effort and employment may go in opposite directions so that the output effect is a priori

ambiguous. Substituting equation (7) in equation (6) shows that output is proportional to wL .

The total effect of a revenue-neutral tax reform is then given by

[ ]LdwwdLeLdf +−δδ= −1)1()( . Substituting in equation (25) thus yields for a revenue-

neutral rise in tax progression

(26) 0

***

*

0

1)()1(1

)(==

⎥⎦

⎤⎢⎣

⎡−+−

−−

=dG

aa

dG dtdwtt

teewL

dteLdf δδδ

δδ .

If tt a ≥δ* , i.e. 1)1( 1* ≥−δ −aw , output is increasing. This can be summarized in

Proposition 5 (rising output): A sufficient, but not necessary, condition that a

revenue-neutral increase in wage tax progression will increase employment is

tt a ≥δ* .

Proposition 5 implies that starting from a linear tax system with tt a = , output will also rise

when tax progression is introduced so that we have

Corollary 2 (rising output): Introducing tax progression raises output when

wages are negotiated and effort is determined individually.

5.5 Revenue-neutral tax progression and welfare

Finally we want to briefly discuss the welfare implications. An appropriate measure of

welfare in our framework is the sum of profits and workers’ surplus, i.e.

(27) [ ]

[ ] [ ] bNLegbwLbNLegbeLf

GLNbLegtatwwLeLfW

++−−δδ

=++−=

+−+−+−+−=

)(1

)()(

)()()1()(

where wLeweLeLf 1111)1(

1 )1()1()()1()( −−δδ−−δ−δ

− −δδ=−δδ=−δδ= . In general the welfare

effects are affected in different directions by the parameters that specify the production

22

technology and the disutilty from effort so that general unambiguous statements cannot be

derived. However, the properties of the model allow us to derive at least some sufficient

conditions for welfare to improve.

First, note that the worker’s surplus s is increasing in effort. This follows from the

worker’s optimal effort choice, i.e. 0)('1 =−= − egesdeV ddwe , from which follows that

)(1 egds −θ= . Hence, when worker chooses a higher level of individual effort they are always

better off. Second, when employment rises those additional workers that find employment are

better since 0)( >−− begwn . Thus no worker will lose when employment is rising. Finally,

profit is increasing in output as profit is given by )()1( 11 eLfwL −− δ=−δ Hence, a sufficient

condition for a positive welfare effect is that the reform does not lead to a fall in effort,

employment and output. A necessary condition for the first requirement to hold is 1* ≥δat . A

sufficient condition for the latter two requirements is tt a ≥δ* . Thus 1* ≥δat suffices to fullfill

all three requirements. This leads to our last proposition.

Proposition 6 (rising welfare): Welfare is always increasing when a revenue-

neutral increase in wage tax progression will increase effort.

Workers only increase effort when they are better off. Since for a revenue-neutral increase in

tax progression, higher effort is always associated with higher employment and output, more

workers benefit from the higher surplus per worker and profit increases as well.

6. Conclusions

We have provided an extended framework to study the implications of the imperfectly

observable individual effort of workers on the negotiated wage and the impact of a revenue-

neutral change in the wage tax progression on wage negotiations, individual effort,

employment, output and welfare. The first, and most important, result is that a higher degree

of tax progression in this framework always leads to wage moderation. Our model confirms

this result for the case of observable effort and wage bargaining as well as for the case where

23

firms set efficiency wages unilaterally: the different wage-setting motives reinforce partial tax

policy effects present in each model. However, when effort is not observable and verifiable,

the clear-cut effect well-known from the wage bargaining literature that tax progression is

good for employment does not carry over to the case of imperfectly observable effort. In the

general case, it remains true that introducing tax progression is good for employment, but if

the adverse effect on effort becomes sufficiently large due to too high a degree of tax

progression, we cannot rule out the case where employment falls as a consequence of a

progressivity-enhancing tax reform. Since higher effort level are only observed when workers

are better off by providing more effort, increasing effort indicates that welfare is

unambiguously improving. Since in this case both profits and workers’ surplus increase,

increasing effort as a consequence of a revenue-neutral increase in tac progression is even a

sufficient condition for a strict Pareto improvement.

References

Altenburg, L. and M. Straub (1998): Efficiency wages, trade unions, and employment, Oxford Economic Papers, 50, 726-746.

Andersen, T. M., Rasmussen, B. S. (1999): Effort, taxation and unemployment, Economics Letters 62, 97-103.

Bulkley, G. and G. Myles (1997): Bargaining over effort, European Journal of Political Economy, 13, 375-384.

Bulkley, G. and G. Myles (1996): Trade unions, efficiency wages and shirking, Oxford Economic Papers, 48, 75-88.

Diamond, P. and M. Yaari (1972): Implications of the theory of rationing for consumer choice under uncertainty, American Economic Review, 62, 333-343.

Fuest, C. and B. Huber (1998): Efficiency wages, employment, and the marginal income-tax rate: A note, Journal of Economics 68, 79-84.

Garcia, J. R. and J. C. Rios (2004): Effects of tax reforms in a shirking model with union bargaining, WP-AD2004-42.

Garino, G. and C. Martin (2000): Efficiency wages and union-firm bargaining, Economics Letters, 69, 181-185.

Goerke, L. (1999): Efficiency wages and taxes, Australian Economic Papers 38, 131-142. Hoel, M. (1990): Efficiency wages and income taxation, Journal of Economics 51, 89-99. Hansen, C. T. (1999): Lower tax progression, longer hours and higher wages, Scandinavian

Journal of Economics, 101, 49-65. Holm, P. and E. Koskela (1996): Tax progression, structure of labour taxation and

employment, FinanzArchiv, 53, 28-46. Koskela, E. and J. Vilmunen (1996): Tax progression is good for employment in popular

models of trade union behaviour, Labour Economics, 3, 65-80.

24

Koskela, E. and R. Schöb (1999): Does the composition of wage and payroll taxes matter under Nash bargaining?, Economics Letters,64, 343-349.

Koskela, E. and R. Schöb (2002): Optimal factor income taxation in the presence of unemployment, Journal of Public Economic Theory 4.2002, 387-404.

Lambert, P. J. (2001): The distribution and redistribution of income, 3rd edition, Manchester University Press.

Lindbeck, A. and D. J. Snower (1991): Interactions between the efficiency wage and insider-outsider theories, Economics Letters, 37, 193-196.

Rasmussen, B. S. (2002): Efficiency wages and the long-run incidence of progressive taxation, Journal of Economics 76, 155-175.

Sanfey, P. J. (1993): On the interaction between efficiency wages and union-firm bargaining models, Economics Letters, 41, 319-324.

Shapiro, C. and J. E. Stiglitz (1984): Equilibrium unemployment as a worker discipline device, American Economic Review, 74, 433-444.

Solow, R. M. (1979): Another possible source of wage stickiness, Journal of Macroeconomics, 1, 79-82.

Sorensen, P. B. (1999): Optimal tax progressivity in imperfect labour markets, Labour Economics, 6, 435-452.

Appendix A: the negotiated wage

This appendix develops the expressions for the terms ** ππw and UUw in the first-order

condition (13) that determines the Nash bargaining solution. We start by looking at the profit

response of the firm to a change in the wage rate. The indirect profit function was presented in

equation (9). By applying the envelope theorem, according to which the effect which takes

place through the labor demand vanishes at the optimum, we find that

(A1) [ ]

[ ] ,01)(1)(

))(1())(1()1(

1

11111

121*

<ε−−=⎥⎦⎤

⎢⎣⎡ −=

−δ−−δ−δ

=π

−δδ−−−δδ−

−δδ−−δδ−

wew

ewewew

eweew

w

ww

from which it follows that

(A2) 0)1)(1(*

*

<ε−−δ

−=ππ

ww

as .1<ε With respect to the trade union’s utility, we find that

(A3) [ ]))((')1( ***

begwwegtwwLU n

ww −−δ−−−= ,

25

where *

** )1(

LwLw−=ε+ε−δ=δ . Thus, it follows that

(A4) ⎥⎥⎦

⎤

⎢⎢⎣

⎡

−−

−−δ−−−=

begwbegwwegtw

wUU

n

nww

)())((')1(1

*

**

.

Substituting (A4) and (A2) into (14) yields

(A5) [ ][ ] )1)(1)(1(

)())((')1(

*

**

ε−−δβ−=−−

−−δ−−−β

begwbegwwegtw

n

nw .

This can be rewritten as:

(A6)

[ ]

[ ][ ]

[ ][ ][ ]**

*

*

*

*

**

)1)(1)(1()(

)1)(1)(1)(1()1(')1(*)1)(1)(1())((

)1)(1)(1(')1()1)(1)(1)()((

)1)(1)(1())((')1(

βδ+ε−−δβ−−+−=

ε−−δβ−−−−δ−−−β

⇔βδ+ε−−δβ−+−=

ε−−δβ−−δ−−−β

⇔ε−−δβ−+−=

ε−−δβ−−−−δ−−−β

tabeg

twtwwegtwbeg

wwwegtwbeg

wbegwwegtw

w

nnw

nnw

.

Using the definition of the total wage elasticity of labor demand *δ , we obtain by making use

of equations (2) and (3)

(A7) [ ][ ])1)(1()()1(

')1)(1()1( * ε−−δ+β−+=⎥⎥⎦

⎤

⎢⎢⎣

⎡

−β+ε−−δ− tabeg

twwegtw w

so that

(A8) [ ][ ])1)(1()()(

)1)(1()1( * ε−−δ+β−+=⎥⎦

⎤⎢⎣

⎡+θ

β+ε−−δ− tabegd

dtw

Using the explict functional form for effort yields for the disutility of effort

[ ]btatwddeg −+−θ+= − )1()()( 1* . Substituting in (A8) yields

(A9) [ ]

( ) [ ])1)(1(1

)1)(1()(

)1)(1()1(

ε−−δ+β⎥⎦

⎤⎢⎣

⎡−⎟

⎠⎞

⎜⎝⎛

θ+−=

⎥⎦

⎤⎢⎣

⎡ε−−δ+β

θ+−

+θβ+ε−−δ−

tabd

d

dd

ddtw

26

Rearranging yields

(A10) [ ][ ])1)(1()1)(1()1( ε−−δ+β−θ+

θ=⎥⎦

⎤⎢⎣⎡

θ+θ

ε−−δ− tabdd

tw

which gives equation (14).

Appendix B: the sign of the numerator of (22)

Substituting the partial derivatives (19) and (20) into the numerator of (22) yields

(B1) .0

)1()(

)1(

1)1()()(

2

2

<−−

Δ−

−ε

Δ−=

⎥⎦

⎤⎢⎣

⎡⎟⎠⎞

⎜⎝⎛

−−

−−−

Δ+⎟

⎠⎞

⎜⎝⎛ ε

−+ε

Δ=

−+

ε

ε

tbwM

tM

taw

tabM

tawMw

taww

n

atat

Appendix C: the Slutzky-decomposition for the total effect of the wage tax on the negotiated wage

Differentiating the indirect Nash maximand 01** Ω=π=Ω β−βU , where *sLU = and **** )1()( LswLef +−=π , with respect to t and a gives

(C1) (i) 0)(*1*11*1* <−πβ−=πβ=Ω β−−ββ−−β awLUUU tt ,

(ii) 0*1*11*1* >πβ=πβ=Ω β−−ββ−−β tLUUU aa .

The wage tax has a negative effect and tax exemption has a positive effect on the Nash

maximand. Using the comparative statics, the indirect Nash maximand can be inverted in

terms of a for the function ),( 0Ω= tha . Substituting this for a in 01** VU =π=Ω β−β gives

the compensated indirect Nash maximand 00* )),(,( Ω=ΩΩ tht .9 Differentiating this

compensated indirect Nash maximand with respect to t gives 0** =Ω+Ω att h so that

tawh att /)(/ ** −=ΩΩ−= . This describes the relationship of tax parameters to keep the Nash

maximand constant.

9 See Diamond and Yaari (1972).

27

According to the duality theorem, the Nash maximand wage function w and the

compensated wage function cw at the same Nash maximand level are equal, so that we have

),()),(,( 00 Ω=Ω twthtw c . Differentiating this with respect to the wage tax gives ctatt wwhw =+ so that we obtain the Slutsky equation

(C2) actt w

tawww )( −

−= ,

where the total effect of the wage tax rate has been decomposed into the negative substitution

effect ( 0<ctw , see Appendix C) and the positive income effect ⎟

⎠⎞

⎜⎝⎛ −− aw

taw )( . QED.

CESifo Working Paper Series (for full list see Twww.cesifo-group.de)T

___________________________________________________________________________ 1956 Panu Poutvaara and Lars-H. R. Siemers, Smoking and Social Interaction, March 2007 1957 Stephan Danninger and Fred Joutz, What Explains Germany’s Rebounding Export

Market Share?, March 2007 1958 Stefan Krasa and Mattias Polborn, Majority-efficiency and Competition-efficiency in a

Binary Policy Model, March 2007 1959 Thiess Buettner and Georg Wamser, Intercompany Loans and Profit Shifting –

Evidence from Company-Level Data, March 2007 1960 Per Pettersson-Lidbom and Mikael Priks, Behavior under Social Pressure: Empty Italian

Stadiums and Referee Bias, April 2007 1961 Balázs Égert and Carol S. Leonard, Dutch Disease Scare in Kazakhstan: Is it real?,

April 2007 1962 Paul De Grauwe and Pablo Rovira Kaltwasser, Modeling Optimism and Pessimism in

the Foreign Exchange Market, April 2007 1963 Volker Grossmann and Thomas M. Steger, Anti-Competitive Conduct, In-House R&D,

and Growth, April 2007 1964 Steven Brakman and Charles van Marrewijk, It’s a Big World After All, April 2007 1965 Mauro Ghinamo, Paolo M. Panteghini and Federico Revelli, FDI Determination and

Corporate Tax Competition in a Volatile World, April 2007 1966 Inés Macho-Stadler and David Pérez-Castrillo, Optimal Monitoring to Implement Clean

Technologies when Pollution is Random, April 2007 1967 Thomas Eichner and Ruediger Pethig, Efficient CO2 Emissions Control with National

Emissions Taxes and International Emissions Trading, April 2007 1968 Michela Redoano, Does Centralization Affect the Number and Size of Lobbies?, April

2007 1969 Christian Gollier, Intergenerational Risk-Sharing and Risk-Taking of a Pension Fund,

April 2007 1970 Swapan K. Bhattacharya and Biswa N. Bhattacharyay, Gains and Losses of India-China

Trade Cooperation – a Gravity Model Impact Analysis, April 2007 1971 Gerhard Illing, Financial Stability and Monetary Policy – A Framework, April 2007

1972 Rainald Borck and Matthias Wrede, Commuting Subsidies with two Transport Modes,

April 2007 1973 Frederick van der Ploeg, Prudent Budgetary Policy: Political Economy of Precautionary

Taxation, April 2007 1974 Ben J. Heijdra and Ward E. Romp, Retirement, Pensions, and Ageing, April 2007 1975 Scott Alan Carson, Health during Industrialization: Evidence from the 19th Century

Pennsylvania State Prison System, April 2007 1976 Andreas Haufler and Ian Wooton, Competition for Firms in an Oligopolistic Industry:

Do Firms or Countries Have to Pay?, April 2007 1977 Eckhard Janeba, Exports, Unemployment and the Welfare State, April 2007 1978 Gernot Doppelhofer and Melvyn Weeks, Jointness of Growth Determinants, April 2007 1979 Edith Sand and Assaf Razin, The Role of Immigration in Sustaining the Social Security

System: A Political Economy Approach, April 2007 1980 Marco Pagano and Giovanni Immordino, Optimal Regulation of Auditing, May 2007 1981 Ludger Woessmann, Fundamental Determinants of School Efficiency and Equity:

German States as a Microcosm for OECD Countries, May 2007 1982 Bas Jacobs, Real Options and Human Capital Investment, May 2007 1983 Steinar Holden and Fredrik Wulfsberg, Are Real Wages Rigid Downwards?, May 2007 1984 Cheng Hsiao, M. Hashem Pesaran and Andreas Pick, Diagnostic Tests of Cross Section

Independence for Nonlinear Panel Data Models, May 2007 1985 Luis Otávio Façanha and Marcelo Resende, Hierarchical Structure in Brazilian

Industrial Firms: An Econometric Study, May 2007 1986 Ondřej Schneider, The EU Budget Dispute – A Blessing in Disguise?, May2007 1987 Sascha O. Becker and Ludger Woessmann, Was Weber Wrong? A Human Capital

Theory of Protestant Economic History, May 2007 1988 Erkki Koskela and Rune Stenbacka, Equilibrium Unemployment with Outsourcing and

Wage Solidarity under Labour Market Imperfections, May 2007 1989 Guglielmo Maria Caporale, Juncal Cunado and Luis A. Gil-Alana, Deterministic versus

Stochastic Seasonal Fractional Integration and Structural Breaks, May 2007 1990 Cláudia Costa Storti and Paul De Grauwe, Globalization and the Price Decline of Illicit

Drugs, May 2007

1991 Thomas Eichner and Ruediger Pethig, Pricing the Ecosystem and Taxing Ecosystem

Services: A General Equilibrium Approach, May 2007 1992 Wladimir Raymond, Pierre Mohnen, Franz Palm and Sybrand Schim van der Loeff, The

Behavior of the Maximum Likelihood Estimator of Dynamic Panel Data Sample Selection Models, May 2007

1993 Fahad Khalil, Jacques Lawarrée and Sungho Yun, Bribery vs. Extortion: Allowing the

Lesser of two Evils, May 2007 1994 Thorvaldur Gylfason, The International Economics of Natural Resources and Growth,

May 2007 1995 Catherine Roux and Thomas von Ungern-Sternberg, Leniency Programs in a

Multimarket Setting: Amnesty Plus and Penalty Plus, May 2007 1996 J. Atsu Amegashie, Bazoumana Ouattara and Eric Strobl, Moral Hazard and the

Composition of Transfers: Theory with an Application to Foreign Aid, May 2007 1997 Wolfgang Buchholz and Wolfgang Peters, Equal Sacrifice and Fair Burden Sharing in a

Public Goods Economy, May 2007 1998 Robert S. Chirinko and Debdulal Mallick, The Fisher/Cobb-Douglas Paradox, Factor

Shares, and Cointegration, May 2007 1999 Petra M. Geraats, Political Pressures and Monetary Mystique, May 2007 2000 Hartmut Egger and Udo Kreickemeier, Firm Heterogeneity and the Labour Market

Effects of Trade Liberalisation, May 2007 2001 Andreas Freytag and Friedrich Schneider, Monetary Commitment, Institutional

Constraints and Inflation: Empirical Evidence for OECD Countries since the 1970s, May 2007

2002 Niclas Berggren, Henrik Jordahl and Panu Poutvaara, The Looks of a Winner: Beauty,

Gender, and Electoral Success, May 2007 2003 Tomer Blumkin, Yoram Margalioth and Efraim Sadka, Incorporating Affirmative

Action into the Welfare State, May 2007 2004 Harrie A. A. Verbon, Migrating Football Players, Transfer Fees and Migration Controls,

May 2007 2005 Helmuth Cremer, Jean-Marie Lozachmeur and Pierre Pestieau, Income Taxation of

Couples and the Tax Unit Choice, May 2007 2006 Michele Moretto and Paolo M. Panteghini, Preemption, Start-Up Decisions and the

Firms’ Capital Structure, May 2007

2007 Andreas Schäfer and Thomas M. Steger, Macroeconomic Consequences of Distributional Conflicts, May 2007

2008 Mikael Priks, Judiciaries in Corrupt Societies, June 2007 2009 Steinar Holden and Fredrik Wulfsberg, Downward Nominal Wage Rigidity in the

OECD, June 2007 2010 Emmanuel Dhyne, Catherine Fuss, Hashem Pesaran and Patrick Sevestre, Lumpy Price

Adjustments: A Microeconometric Analysis, June 2007 2011 Paul Belleflamme and Eric Toulemonde, Negative Intra-Group Externalities in Two-

Sided Markets, June 2007 2012 Carlos Alós-Ferrer, Georg Kirchsteiger and Markus Walzl, On the Evolution of Market

Institutions: The Platform Design Paradox, June 2007 2013 Axel Dreher and Martin Gassebner, Greasing the Wheels of Entrepreneurship? The

Impact of Regulations and Corruption on Firm Entry, June 2007 2014 Dominique Demougin and Claude Fluet, Rules of Proof, Courts, and Incentives, June

2007 2015 Stefan Lachenmaier and Horst Rottmann, Effects of Innovation on Employment: A

Dynamic Panel Analysis, June 2007 2016 Torsten Persson and Guido Tabellini, The Growth Effect of Democracy: Is it

Heterogenous and how can it be Estimated?, June 2007 2017 Lorenz Blume, Jens Müller, Stefan Voigt and Carsten Wolf, The Economic Effects of

Constitutions: Replicating – and Extending – Persson and Tabellini, June 2007 2018 Hartmut Egger and Gabriel Felbermayr, Endogenous Skill Formation and the Source

Country Effects of International Labor Market Integration, June 2007 2019 Bruno Frey, Overprotected Politicians, June 2007 2020 Jan Thomas Martini, Rainer Niemann and Dirk Simons, Transfer Pricing or Formula

Apportionment? Tax-Induced Distortions of Multinationals’ Investment and Production Decisions, June 2007

2021 Andreas Bühn, Alexander Karmann and Friedrich Schneider, Size and Development of

the Shadow Economy and of Do-it-yourself Activities in Germany, June 2007 2022 Michael Rauscher and Edward B. Barbier, Biodiversity and Geography, June 2007 2023 Gunther Schnabl, Exchange Rate Volatility and Growth in Emerging Europe and East

Asia, June 2007 2024 Erkki Koskela and Ronnie Schöb, Tax Progression under Collective Wage Bargaining

and Individual Effort Determination, June 2007