Embed Size (px)

Citation preview

International Fiscal Association USA Branch

Young IFA Network

Summer Seminar | Wednesday, August 2, 2017

Tax Issues Faced by Financial Institutions

Emily Fett

Senior Manager

EY, LLP

Jonas Robison

Managing Associate

Orrick, Herrington & Sutcliffe

Daniel Simon

Partner

PwC, LLP

2International Fiscal Association │ YIN Summer Seminar | August 2, 2017

Overview

• Final Section 987 Regulations

– What Should Taxpayers Do Pre-Transition?

– What Should Taxpayers Do Post-Transition?

• Dodd Frank Margin Rules & Section 871(m) Developments

– Scope and Implementation

– Section 871(m) Developments

• Intermediate Holding Company Rules under Dodd Frank

– Overview of the Intermediate Holding Company Rules

– Changing Repo Markets and Shifting of Business

– Strategic Joint Ventures

3International Fiscal Association │ YIN Summer Seminar | August 2, 2017

SECTION 987 REGULATIONS

4International Fiscal Association │ YIN Summer Seminar | August 2, 2017

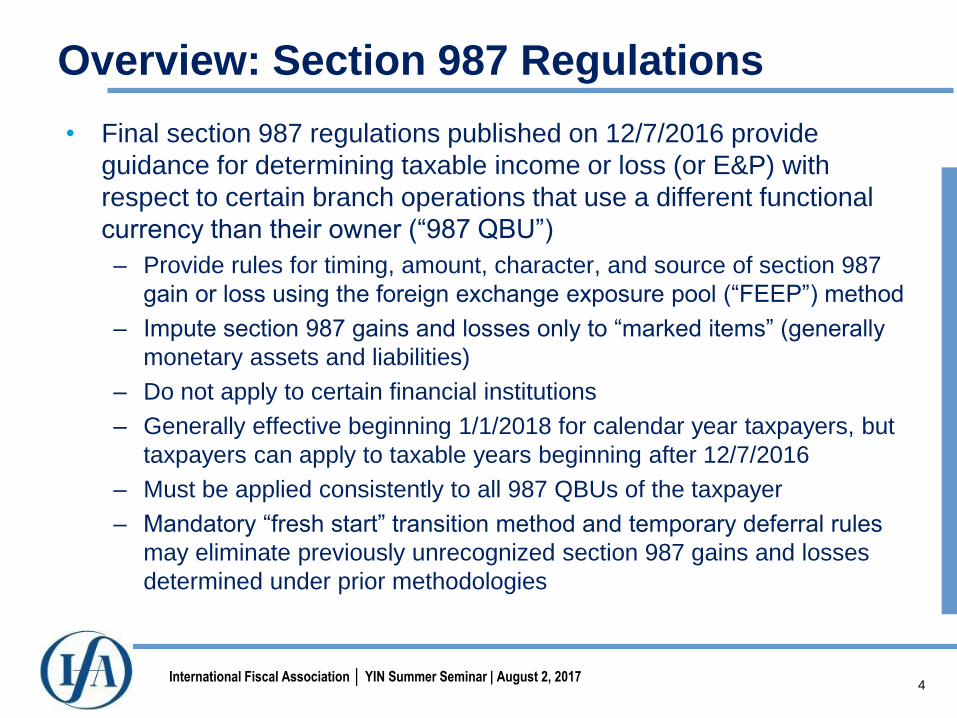

Overview: Section 987 Regulations

• Final section 987 regulations published on 12/7/2016 provide

guidance for determining taxable income or loss (or E&P) with

respect to certain branch operations that use a different functional

currency than their owner (“987 QBU”)

– Provide rules for timing, amount, character, and source of section 987

gain or loss using the foreign exchange exposure pool (“FEEP”) method

– Impute section 987 gains and losses only to “marked items” (generally

monetary assets and liabilities)

– Do not apply to certain financial institutions

– Generally effective beginning 1/1/2018 for calendar year taxpayers, but

taxpayers can apply to taxable years beginning after 12/7/2016

– Must be applied consistently to all 987 QBUs of the taxpayer

– Mandatory “fresh start” transition method and temporary deferral rules

may eliminate previously unrecognized section 987 gains and losses

determined under prior methodologies

5International Fiscal Association │ YIN Summer Seminar | August 2, 2017

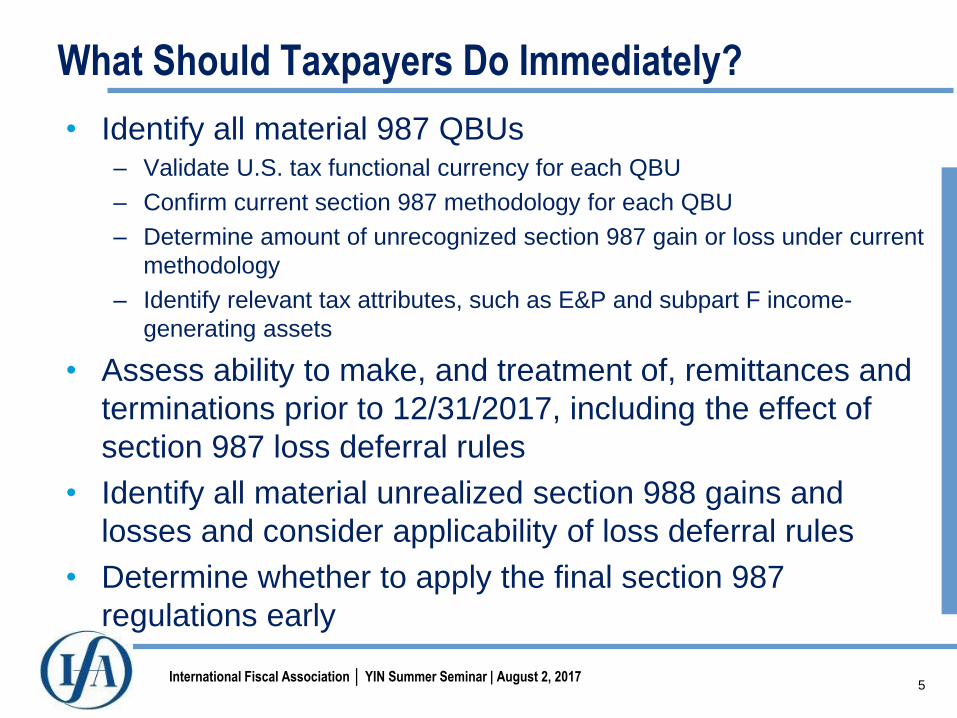

What Should Taxpayers Do Immediately?

• Identify all material 987 QBUs– Validate U.S. tax functional currency for each QBU

– Confirm current section 987 methodology for each QBU

– Determine amount of unrecognized section 987 gain or loss under current

methodology

– Identify relevant tax attributes, such as E&P and subpart F income-

generating assets

• Assess ability to make, and treatment of, remittances and

terminations prior to 12/31/2017, including the effect of

section 987 loss deferral rules

• Identify all material unrealized section 988 gains and

losses and consider applicability of loss deferral rules

• Determine whether to apply the final section 987

regulations early

6International Fiscal Association │ YIN Summer Seminar | August 2, 2017

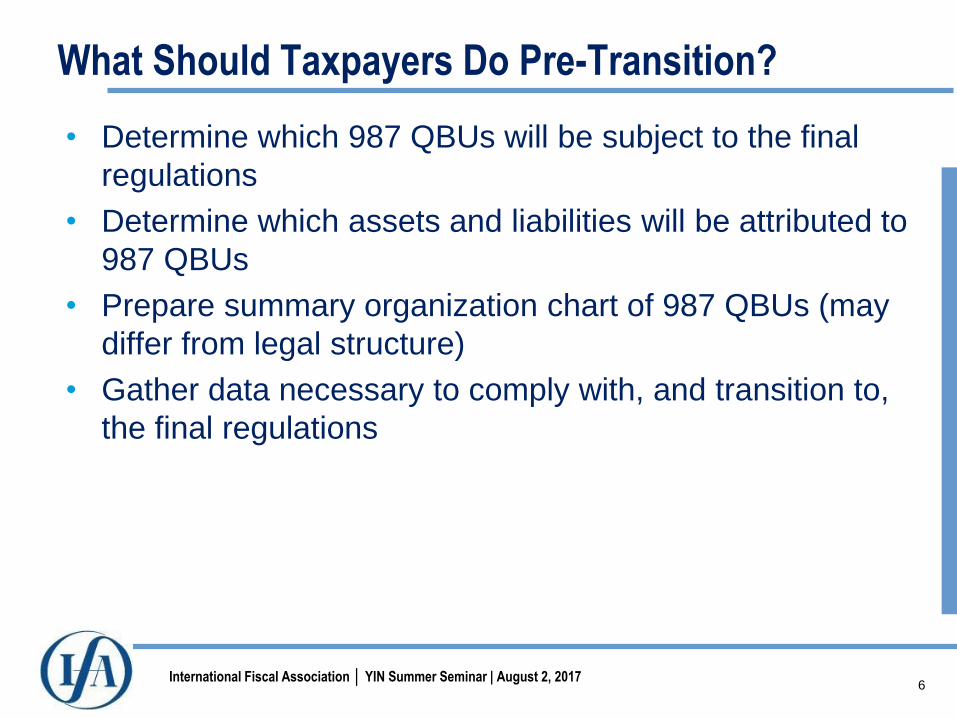

What Should Taxpayers Do Pre-Transition?

• Determine which 987 QBUs will be subject to the final

regulations

• Determine which assets and liabilities will be attributed to

987 QBUs

• Prepare summary organization chart of 987 QBUs (may

differ from legal structure)

• Gather data necessary to comply with, and transition to,

the final regulations

7International Fiscal Association │ YIN Summer Seminar | August 2, 2017

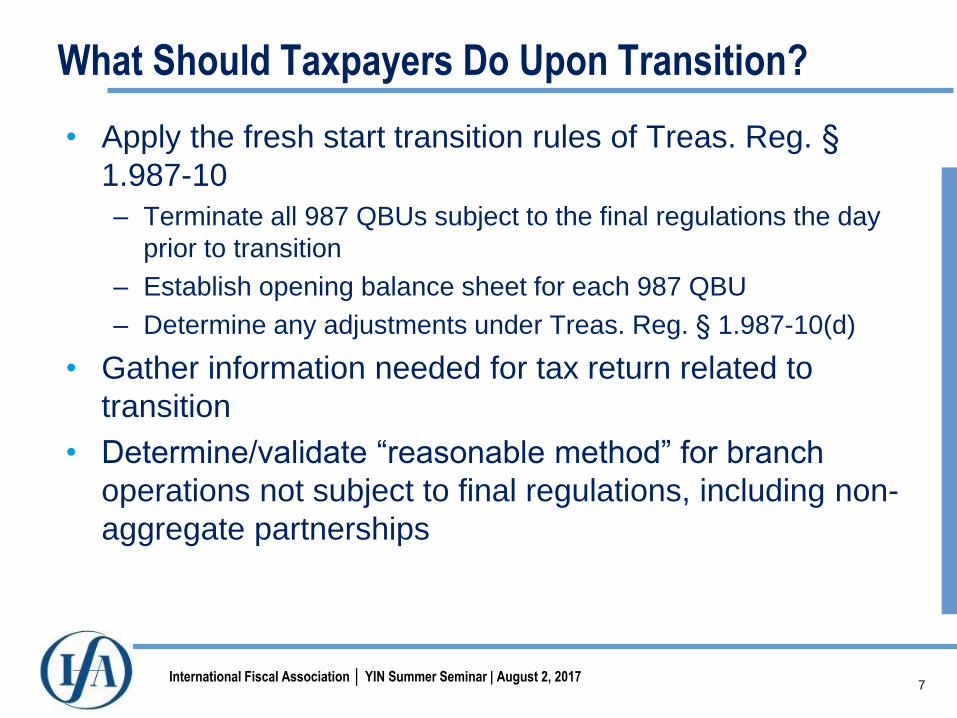

What Should Taxpayers Do Upon Transition?

• Apply the fresh start transition rules of Treas. Reg. §

1.987-10

– Terminate all 987 QBUs subject to the final regulations the day

prior to transition

– Establish opening balance sheet for each 987 QBU

– Determine any adjustments under Treas. Reg. § 1.987-10(d)

• Gather information needed for tax return related to

transition

• Determine/validate “reasonable method” for branch

operations not subject to final regulations, including non-

aggregate partnerships

8International Fiscal Association │ YIN Summer Seminar | August 2, 2017

MARGIN RULES UNDER DODD FRANK AND 871(M) IMPLEMENTATION

9International Fiscal Association │ YIN Summer Seminar | August 2, 2017

Dodd-Frank Margin Rules / 871(m)

This Discussion will Address Recent Developments in:

1) Implementation and cross-border application of uncleared swap margin rules

under Dodd-Frank.

2) Implementation of Section 871(m) regulations.

10International Fiscal Association │ YIN Summer Seminar | August 2, 2017

Uncleared Swap Margin Rules

Two Sets of Rules:

• Prudential Regulators

o The OCC, Federal Reserve, FDIC, FCA, and FHFA

o Rules applicable to banks

• CFTC

o Rules applicable to non-banks

The Two Rules are Closely Similar, with Certain Exceptions

11International Fiscal Association │ YIN Summer Seminar | August 2, 2017

Uncleared Swap Margin Rules

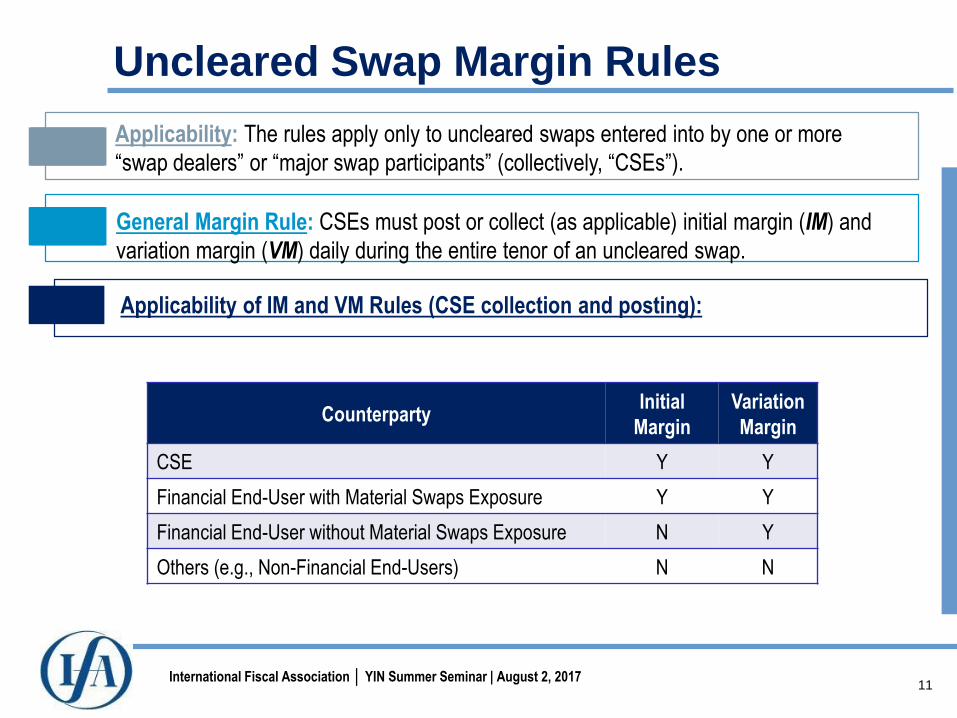

CounterpartyInitial

Margin

Variation

Margin

CSE Y Y

Financial End-User with Material Swaps Exposure Y Y

Financial End-User without Material Swaps Exposure N Y

Others (e.g., Non-Financial End-Users) N N

Applicability: The rules apply only to uncleared swaps entered into by one or more

“swap dealers” or “major swap participants” (collectively, “CSEs”).

General Margin Rule: CSEs must post or collect (as applicable) initial margin (IM) and

variation margin (VM) daily during the entire tenor of an uncleared swap.

Applicability of IM and VM Rules (CSE collection and posting):

12International Fiscal Association │ YIN Summer Seminar | August 2, 2017

Uncleared Swap Margin Rules

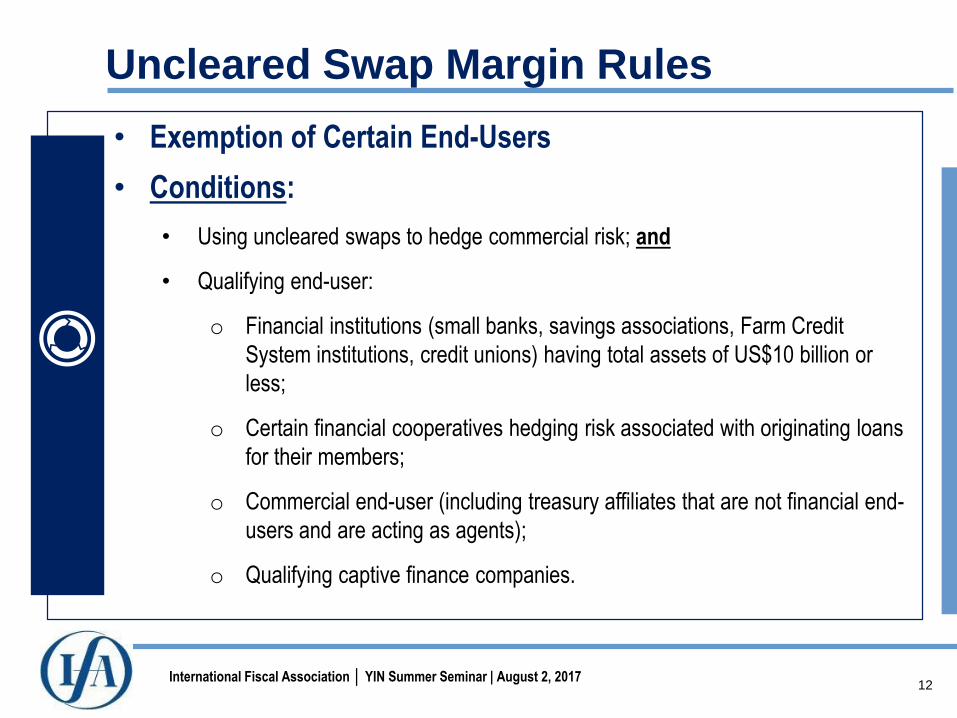

• Exemption of Certain End-Users

• Conditions:

• Using uncleared swaps to hedge commercial risk; and

• Qualifying end-user:

o Financial institutions (small banks, savings associations, Farm Credit

System institutions, credit unions) having total assets of US$10 billion or

less;

o Certain financial cooperatives hedging risk associated with originating loans

for their members;

o Commercial end-user (including treasury affiliates that are not financial end-

users and are acting as agents);

o Qualifying captive finance companies.

13International Fiscal Association │ YIN Summer Seminar | August 2, 2017

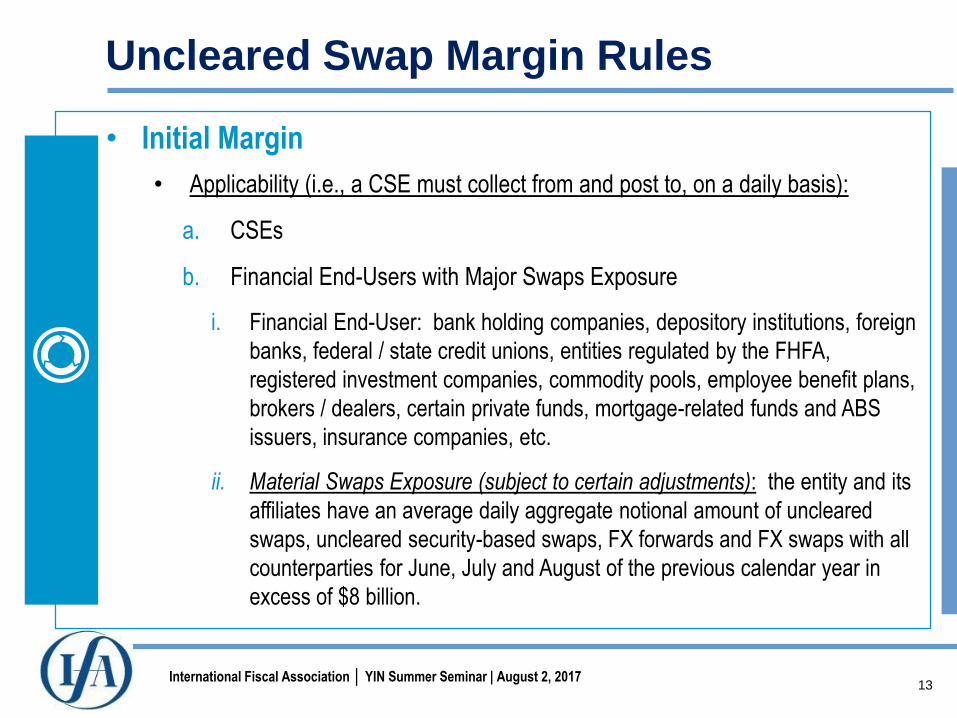

Uncleared Swap Margin Rules

• Initial Margin

• Applicability (i.e., a CSE must collect from and post to, on a daily basis):

a. CSEs

b. Financial End-Users with Major Swaps Exposure

i. Financial End-User: bank holding companies, depository institutions, foreign

banks, federal / state credit unions, entities regulated by the FHFA,

registered investment companies, commodity pools, employee benefit plans,

brokers / dealers, certain private funds, mortgage-related funds and ABS

issuers, insurance companies, etc.

ii. Material Swaps Exposure (subject to certain adjustments): the entity and its

affiliates have an average daily aggregate notional amount of uncleared

swaps, uncleared security-based swaps, FX forwards and FX swaps with all

counterparties for June, July and August of the previous calendar year in

excess of $8 billion.

14International Fiscal Association │ YIN Summer Seminar | August 2, 2017

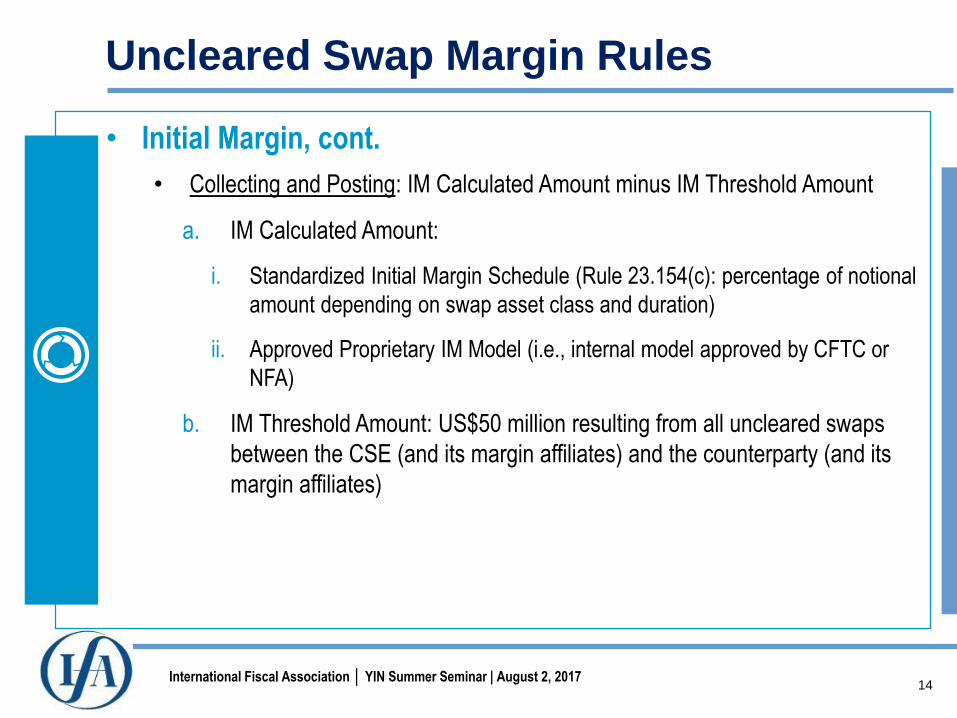

Uncleared Swap Margin Rules

• Initial Margin, cont.

• Collecting and Posting: IM Calculated Amount minus IM Threshold Amount

a. IM Calculated Amount:

i. Standardized Initial Margin Schedule (Rule 23.154(c): percentage of notional

amount depending on swap asset class and duration)

ii. Approved Proprietary IM Model (i.e., internal model approved by CFTC or

NFA)

b. IM Threshold Amount: US$50 million resulting from all uncleared swaps

between the CSE (and its margin affiliates) and the counterparty (and its

margin affiliates)

15International Fiscal Association │ YIN Summer Seminar | August 2, 2017

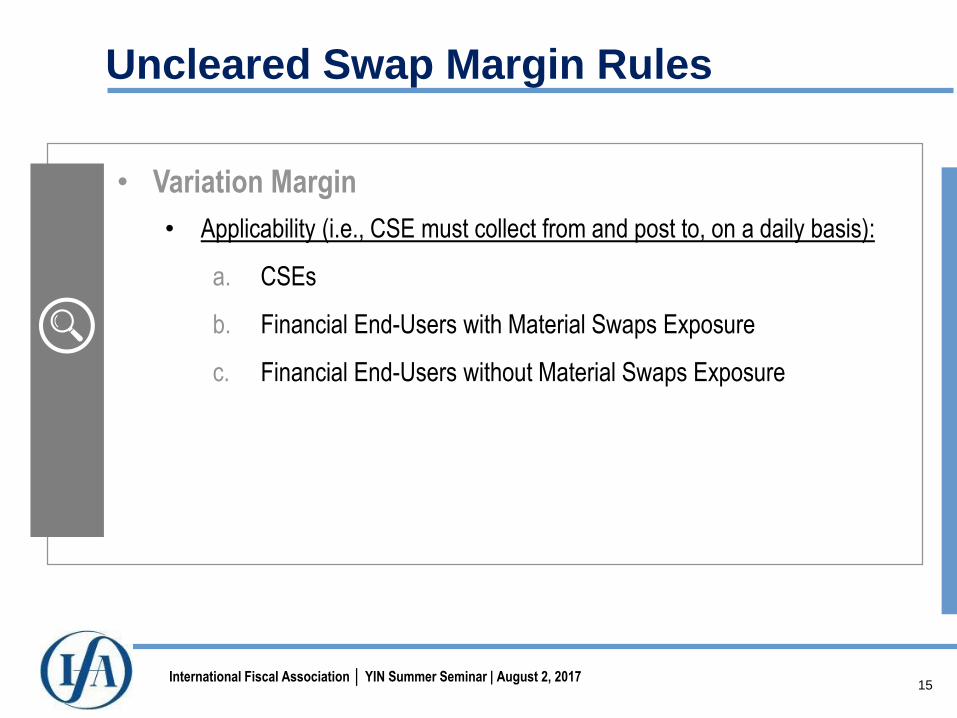

Uncleared Swap Margin Rules

• Variation Margin

• Applicability (i.e., CSE must collect from and post to, on a daily basis):

a. CSEs

b. Financial End-Users with Material Swaps Exposure

c. Financial End-Users without Material Swaps Exposure

16International Fiscal Association │ YIN Summer Seminar | August 2, 2017

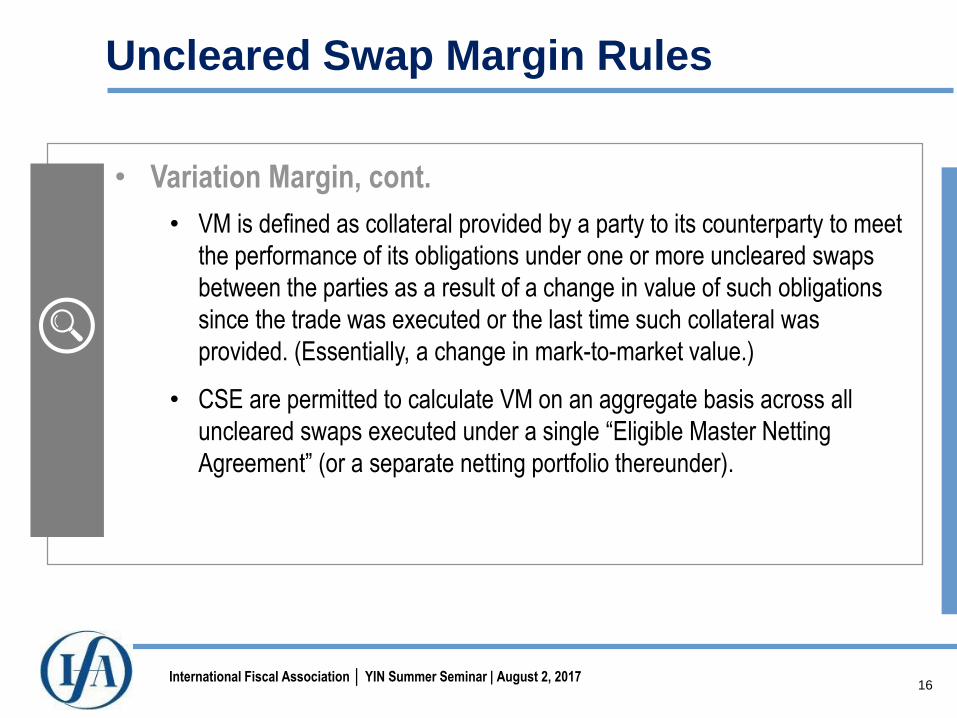

Uncleared Swap Margin Rules

• Variation Margin, cont.

• VM is defined as collateral provided by a party to its counterparty to meet

the performance of its obligations under one or more uncleared swaps

between the parties as a result of a change in value of such obligations

since the trade was executed or the last time such collateral was

provided. (Essentially, a change in mark-to-market value.)

• CSE are permitted to calculate VM on an aggregate basis across all

uncleared swaps executed under a single “Eligible Master Netting

Agreement” (or a separate netting portfolio thereunder).

17International Fiscal Association │ YIN Summer Seminar | August 2, 2017

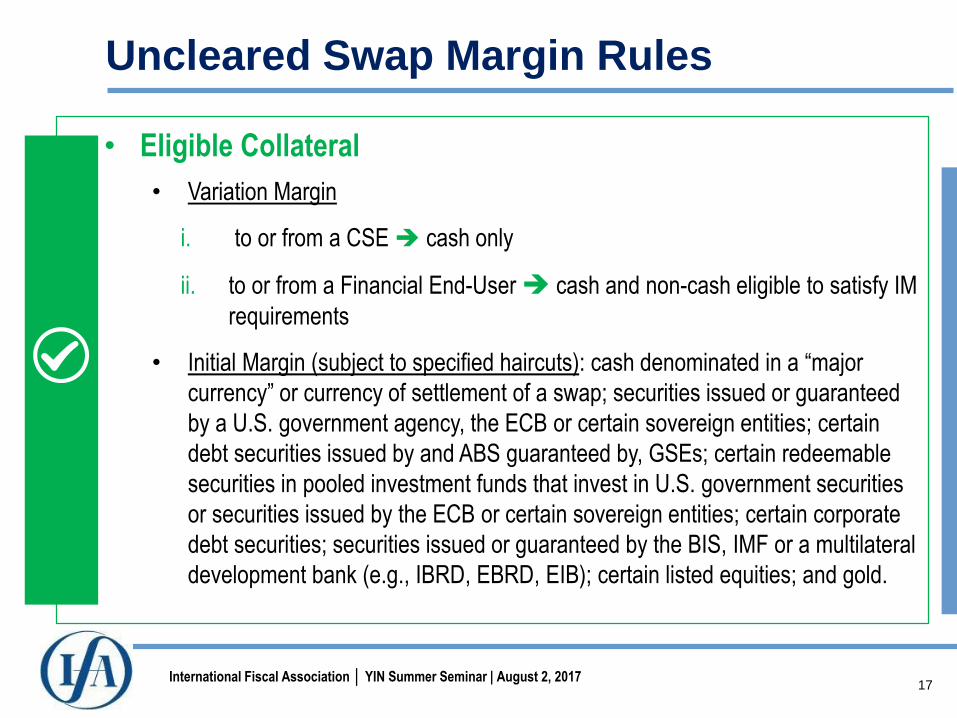

Uncleared Swap Margin Rules

• Eligible Collateral

• Variation Margin

i. to or from a CSE cash only

ii. to or from a Financial End-User cash and non-cash eligible to satisfy IM

requirements

• Initial Margin (subject to specified haircuts): cash denominated in a “major

currency” or currency of settlement of a swap; securities issued or guaranteed

by a U.S. government agency, the ECB or certain sovereign entities; certain

debt securities issued by and ABS guaranteed by, GSEs; certain redeemable

securities in pooled investment funds that invest in U.S. government securities

or securities issued by the ECB or certain sovereign entities; certain corporate

debt securities; securities issued or guaranteed by the BIS, IMF or a multilateral

development bank (e.g., IBRD, EBRD, EIB); certain listed equities; and gold.

18International Fiscal Association │ YIN Summer Seminar | August 2, 2017

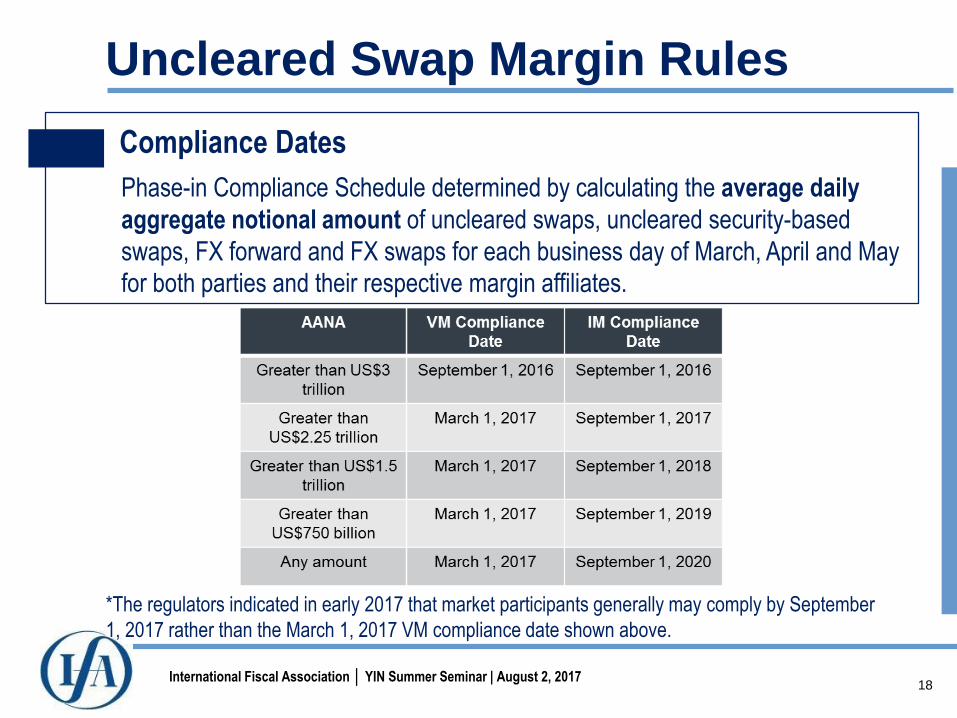

Uncleared Swap Margin Rules

Compliance Dates

Phase-in Compliance Schedule determined by calculating the average daily

aggregate notional amount of uncleared swaps, uncleared security-based

swaps, FX forward and FX swaps for each business day of March, April and May

for both parties and their respective margin affiliates.

*The regulators indicated in early 2017 that market participants generally may comply by September

1, 2017 rather than the March 1, 2017 VM compliance date shown above.

19International Fiscal Association │ YIN Summer Seminar | August 2, 2017

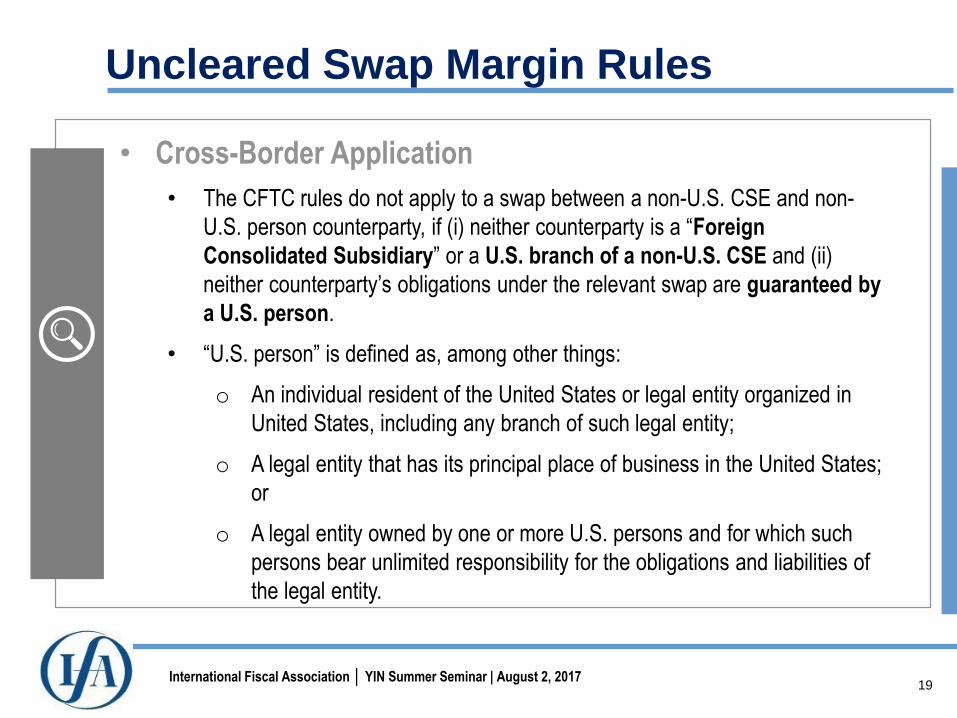

Uncleared Swap Margin Rules

• Cross-Border Application

• The CFTC rules do not apply to a swap between a non-U.S. CSE and non-

U.S. person counterparty, if (i) neither counterparty is a “Foreign

Consolidated Subsidiary” or a U.S. branch of a non-U.S. CSE and (ii)

neither counterparty’s obligations under the relevant swap are guaranteed by

a U.S. person.

• “U.S. person” is defined as, among other things:

o An individual resident of the United States or legal entity organized in

United States, including any branch of such legal entity;

o A legal entity that has its principal place of business in the United States;

or

o A legal entity owned by one or more U.S. persons and for which such

persons bear unlimited responsibility for the obligations and liabilities of

the legal entity.

20International Fiscal Association │ YIN Summer Seminar | August 2, 2017

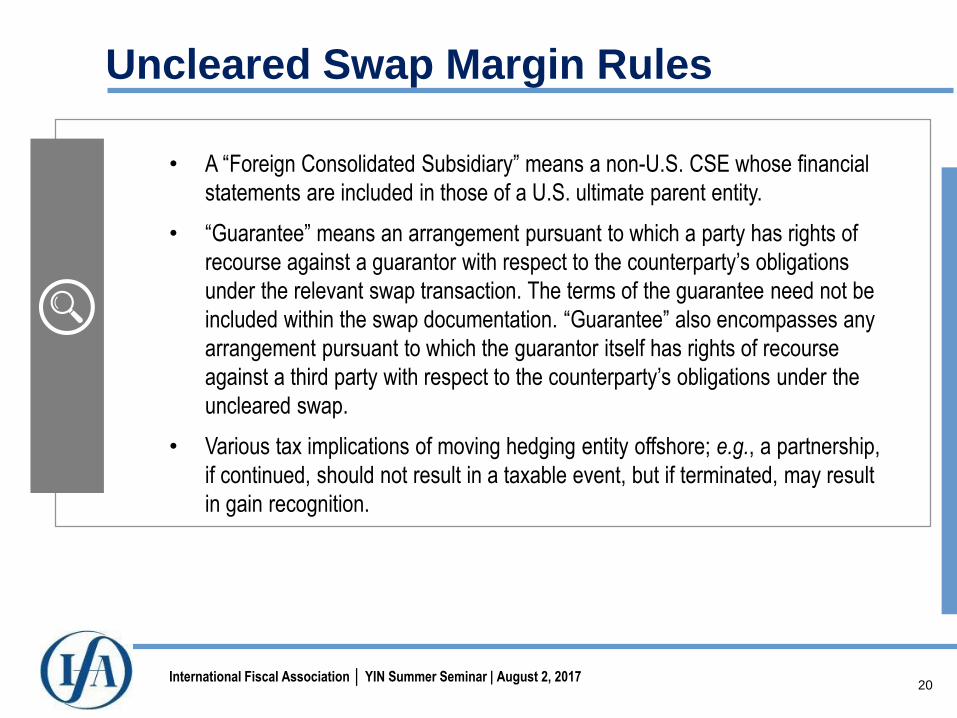

Uncleared Swap Margin Rules

• A “Foreign Consolidated Subsidiary” means a non-U.S. CSE whose financial

statements are included in those of a U.S. ultimate parent entity.

• “Guarantee” means an arrangement pursuant to which a party has rights of

recourse against a guarantor with respect to the counterparty’s obligations

under the relevant swap transaction. The terms of the guarantee need not be

included within the swap documentation. “Guarantee” also encompasses any

arrangement pursuant to which the guarantor itself has rights of recourse

against a third party with respect to the counterparty’s obligations under the

uncleared swap.

• Various tax implications of moving hedging entity offshore; e.g., a partnership,

if continued, should not result in a taxable event, but if terminated, may result

in gain recognition.

21International Fiscal Association │ YIN Summer Seminar | August 2, 2017

871(m) developments

• Background

• Certain payments on equity derivatives with respect to securities that

produce U.S.-source dividend income will be treated as U.S. source

dividends.

• Applies to “dividend equivalent payments” made on “simple contracts” with

a delta equal to or greater than 0.8 or to “complex contracts” that fail a

“substantial equivalence test.”

22International Fiscal Association │ YIN Summer Seminar | August 2, 2017

871(m) developments

• Definitions

• A “simple contract” has (i) a single, fixed number of shares of the

underlying security and (ii) a single exercise or maturity date.

• A “complex contract” is any contract that is not a simple contract.

• Delta Test

• Delta is “the ratio of the change in the fair market value of the derivative to

a small change in the fair market value of the number of underlying

reference shares.”

• Test works well, for example, for vanilla calls and puts. E.g., for a long call,

delta increases from 0 to 1.

• Delta roughly corresponds to probability of the derivative expiring in-the-

money.

23International Fiscal Association │ YIN Summer Seminar | August 2, 2017

• Problems with the Delta Test for Complex Instruments

• Complex structures have features that make it impossible to determine “the

number of underlying reference shares”:

o E.g., a structured note with 100% downside and 200% upside on the

underlying – should the denominator be 1 or 2?

o Barrier options or structured notes knock-in / knock-out features.

• In such cases, the “substantial equivalence test” should be used.

• The substantial equivalence test is much more complicated than delta, but

works for any instrument.

• If an instrument is “substantially equivalent” to a long position in the underlying

equity, it is subject to 871(m).

871(m) developments

24International Fiscal Association │ YIN Summer Seminar | August 2, 2017

• Compliance Dates

• Pursuant to Notice 2016-76, 871(m) implementation with respect to non-delta

one transactions is postponed until January 1, 2018.

• 871(m) is currently effective with respect delta one transaction issued on or

after January 1, 2017.

• Recent Developments

• Issuers are currently providing disclosure that a transaction is not delta one.

• Application of the delta one standard for complex contracts is unclear.

• Most issuers use the substantial equivalence test for complex contracts.

• Will the Trump administration modify the final regulations because of their

complexity?

871(m) developments

25International Fiscal Association │ YIN Summer Seminar | August 2, 2017

INTERMEDIATE HOLDING COMPANY RULES UNDER DODD FRANK

26International Fiscal Association │ YIN Summer Seminar | August 2, 2017

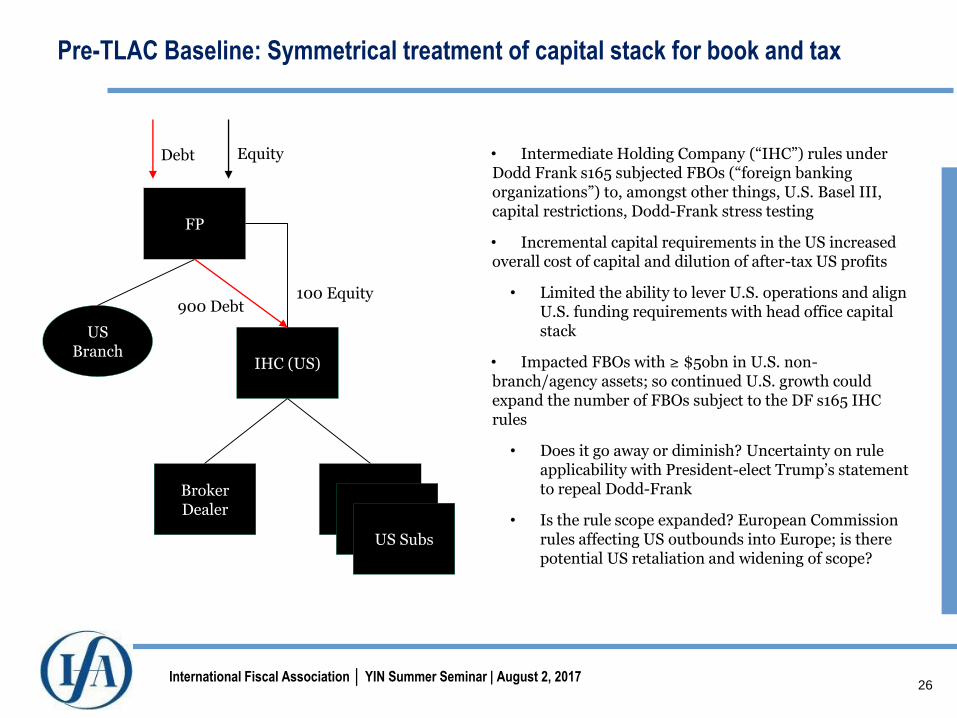

Pre-TLAC Baseline: Symmetrical treatment of capital stack for book and tax

• Intermediate Holding Company (“IHC”) rules under Dodd Frank s165 subjected FBOs (“foreign banking organizations”) to, amongst other things, U.S. Basel III, capital restrictions, Dodd-Frank stress testing

• Incremental capital requirements in the US increased overall cost of capital and dilution of after-tax US profits

• Limited the ability to lever U.S. operations and align U.S. funding requirements with head office capital stack

• Impacted FBOs with ≥ $5obn in U.S. non-branch/agency assets; so continued U.S. growth could expand the number of FBOs subject to the DF s165 IHC rules

• Does it go away or diminish? Uncertainty on rule applicability with President-elect Trump’s statement to repeal Dodd-Frank

• Is the rule scope expanded? European Commission rules affecting US outbounds into Europe; is there potential US retaliation and widening of scope?

FP

US Branch

IHC (US)

100 Equity900 Debt

Broker Dealer

US Subs

Debt Equity

27International Fiscal Association │ YIN Summer Seminar | August 2, 2017

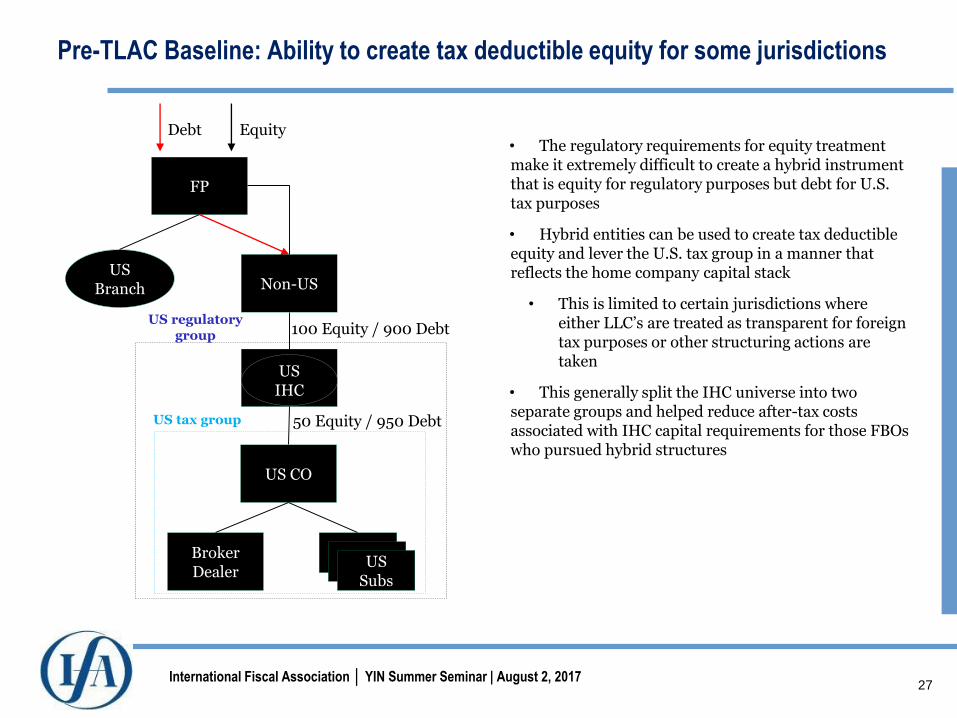

Pre-TLAC Baseline: Ability to create tax deductible equity for some jurisdictions

Debt Equity• The regulatory requirements for equity treatment make it extremely difficult to create a hybrid instrument that is equity for regulatory purposes but debt for U.S. tax purposes

• Hybrid entities can be used to create tax deductible equity and lever the U.S. tax group in a manner that reflects the home company capital stack

• This is limited to certain jurisdictions where either LLC’s are treated as transparent for foreign tax purposes or other structuring actions are taken

• This generally split the IHC universe into two separate groups and helped reduce after-tax costs associated with IHC capital requirements for those FBOs who pursued hybrid structures

FP

US Branch Non-US

US IHC

US CO

Broker Dealer

US Subs

US regulatory group

US tax group

100 Equity / 900 Debt

50 Equity / 950 Debt

28International Fiscal Association │ YIN Summer Seminar | August 2, 2017

…and then there was TLAC: Asymmetrical treatment of capital stack for book and tax going

against the FBO

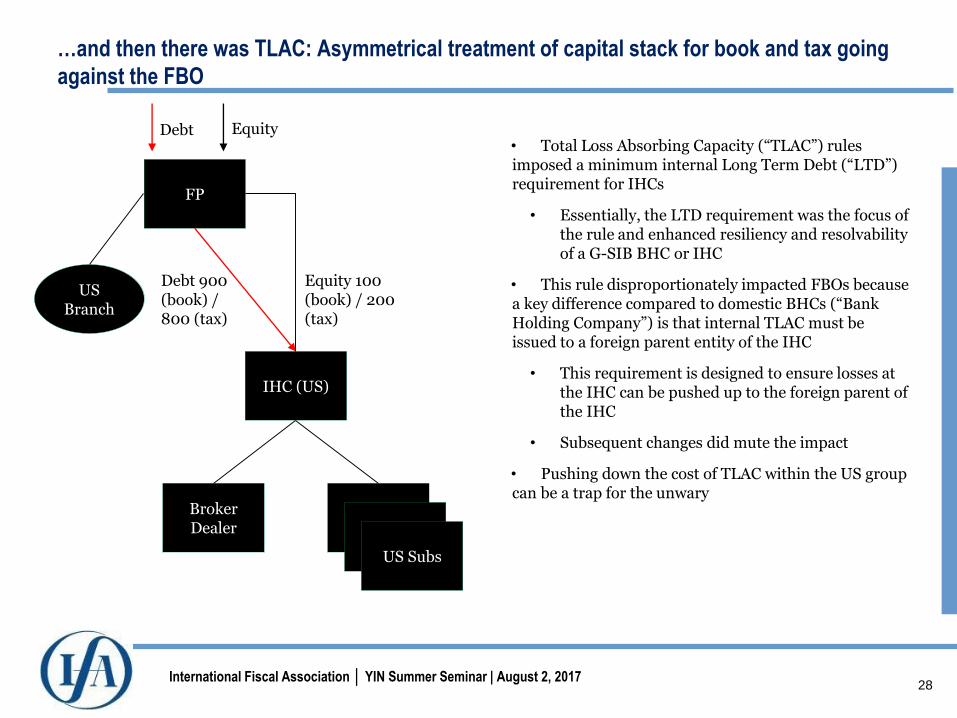

• Total Loss Absorbing Capacity (“TLAC”) rules imposed a minimum internal Long Term Debt (“LTD”) requirement for IHCs

• Essentially, the LTD requirement was the focus of the rule and enhanced resiliency and resolvability of a G-SIB BHC or IHC

• This rule disproportionately impacted FBOs because a key difference compared to domestic BHCs (“Bank Holding Company”) is that internal TLAC must be issued to a foreign parent entity of the IHC

• This requirement is designed to ensure losses at the IHC can be pushed up to the foreign parent of the IHC

• Subsequent changes did mute the impact

• Pushing down the cost of TLAC within the US group can be a trap for the unwary

FP

US Branch

IHC (US)

Equity 100 (book) / 200 (tax)

Debt 900 (book) / 800 (tax)

Broker Dealer

US Subs

Debt Equity

29International Fiscal Association │ YIN Summer Seminar | August 2, 2017

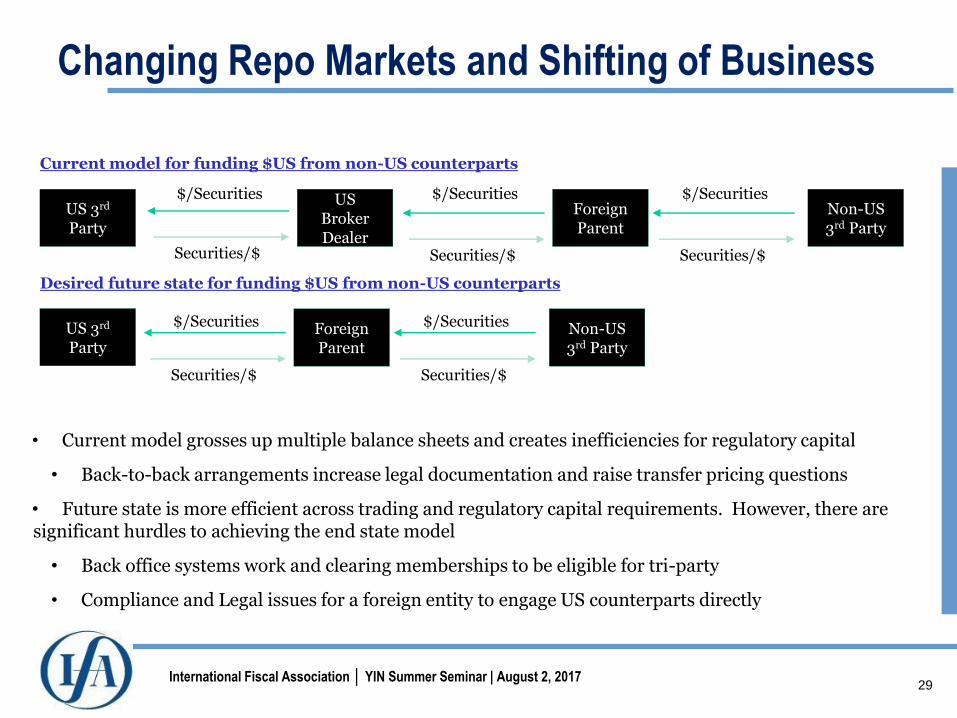

Changing Repo Markets and Shifting of Business

USBroker Dealer

Foreign Parent

Non-US 3rd Party

$/Securities

Securities/$

$/Securities

Securities/$

$/Securities

Securities/$

US 3rd

Party

Current model for funding $US from non-US counterparts

Foreign Parent

Non-US 3rd Party

$/Securities

Securities/$

$/Securities

Securities/$

US 3rd

Party

Desired future state for funding $US from non-US counterparts

• Current model grosses up multiple balance sheets and creates inefficiencies for regulatory capital

• Back-to-back arrangements increase legal documentation and raise transfer pricing questions

• Future state is more efficient across trading and regulatory capital requirements. However, there are significant hurdles to achieving the end state model

• Back office systems work and clearing memberships to be eligible for tri-party

• Compliance and Legal issues for a foreign entity to engage US counterparts directly

30International Fiscal Association │ YIN Summer Seminar | August 2, 2017

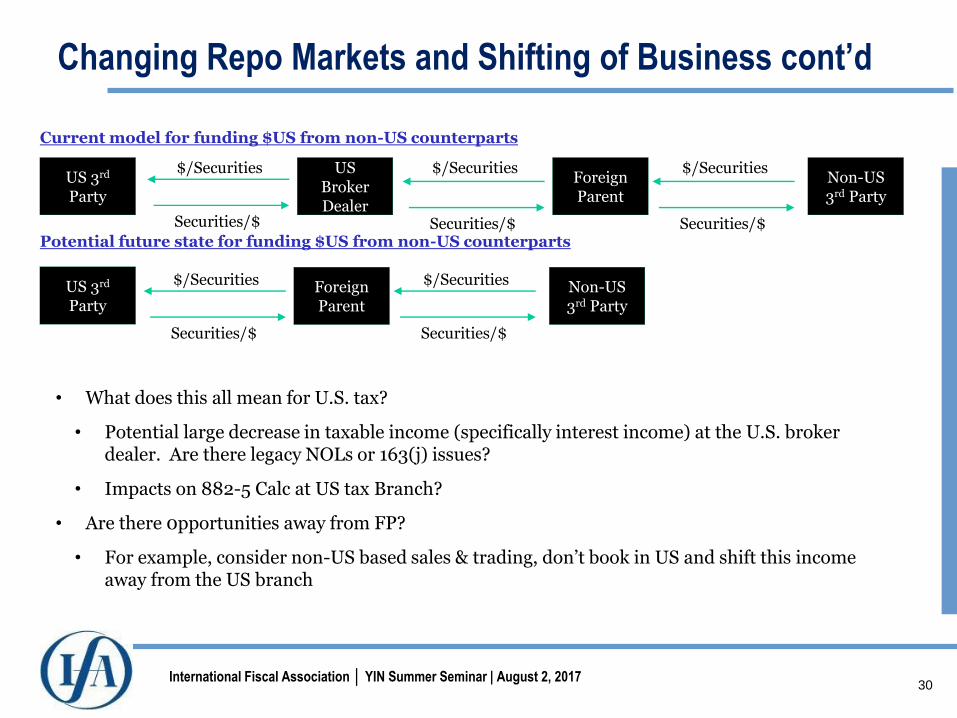

Changing Repo Markets and Shifting of Business cont’d

USBroker Dealer

Foreign Parent

Non-US 3rd Party

$/Securities

Securities/$

$/Securities

Securities/$

$/Securities

Securities/$

US 3rd

Party

Current model for funding $US from non-US counterparts

Foreign Parent

Non-US 3rd Party

$/Securities

Securities/$

$/Securities

Securities/$

US 3rd

Party

Potential future state for funding $US from non-US counterparts

• What does this all mean for U.S. tax?

• Potential large decrease in taxable income (specifically interest income) at the U.S. broker dealer. Are there legacy NOLs or 163(j) issues?

• Impacts on 882-5 Calc at US tax Branch?

• Are there 0pportunities away from FP?

• For example, consider non-US based sales & trading, don’t book in US and shift this income away from the US branch

31International Fiscal Association │ YIN Summer Seminar | August 2, 2017

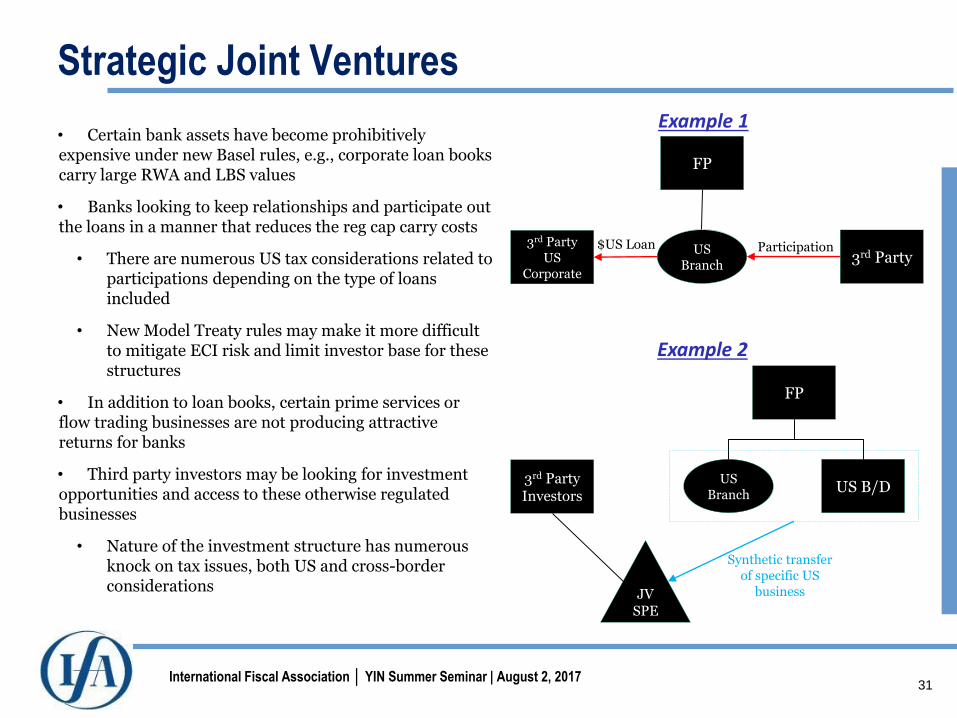

Strategic Joint Ventures

• Certain bank assets have become prohibitively expensive under new Basel rules, e.g., corporate loan books carry large RWA and LBS values

• Banks looking to keep relationships and participate out the loans in a manner that reduces the reg cap carry costs

• There are numerous US tax considerations related to participations depending on the type of loans included

• New Model Treaty rules may make it more difficult to mitigate ECI risk and limit investor base for these structures

• In addition to loan books, certain prime services or flow trading businesses are not producing attractive returns for banks

• Third party investors may be looking for investment opportunities and access to these otherwise regulated businesses

• Nature of the investment structure has numerous knock on tax issues, both US and cross-border considerations

$US Loan3rd Party US

Corporate3rd Party

FP

US Branch

Participation

3rd Party Investors

US B/D

FP

US Branch

JV SPE

Synthetic transfer of specific US

business

Example 2

Example 1