Embed Size (px)

Citation preview

1 Draft version 15 (01-08-13)

Tabcorp Holdings Limited ABN 66 063 780 709

Investor Day

17 October 2013

For

per

sona

l use

onl

y

2 Tabcorp Investor Day 17 October 2013

Exec GM Commercial Development Doug Freeman

MD Fixed Odds Craig Nugent

CFO Damien Johnston

Exec GM Corporate Legal & Regulatory Kerry Willcock

COO Media & International

Brendan Parnell

TABCORP CEO & MD David Attenborough

Tabcorp senior leadership team

Exec GM Human Resources Merryl Dooley

CIO Kim Wenn

Exec GM Distribution

Adam Rytenskild

Exec GM Marketing

David Ginnane

For

per

sona

l use

onl

y

3 Tabcorp Investor Day 17 October 2013

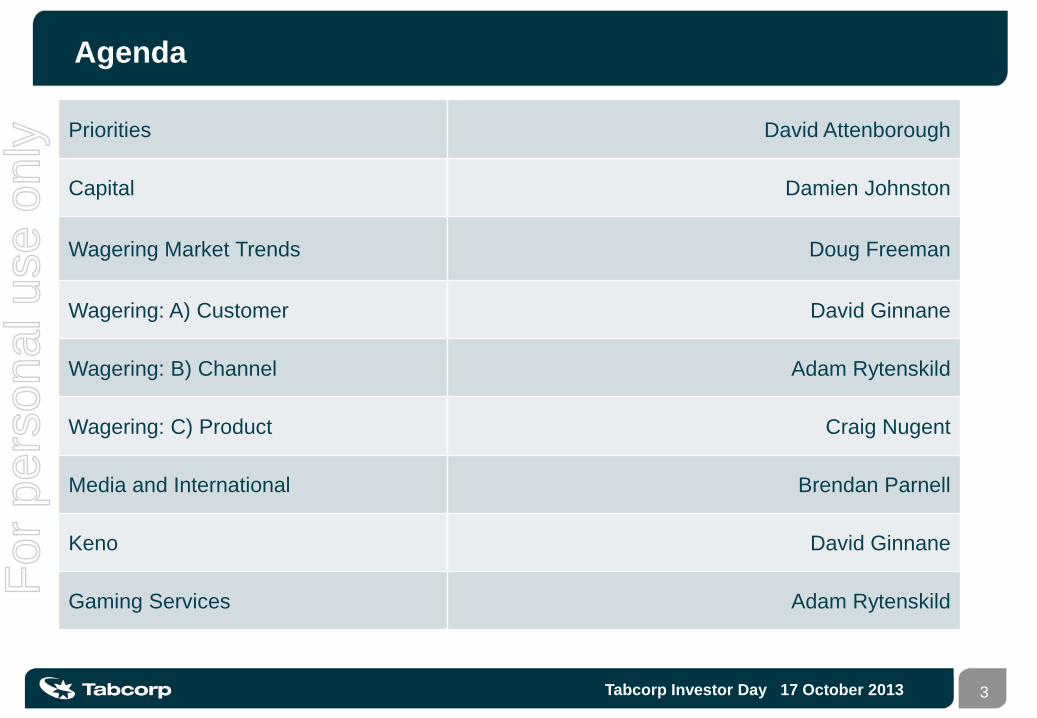

Agenda

Priorities David Attenborough

Capital Damien Johnston

Wagering Market Trends Doug Freeman

Wagering: A) Customer David Ginnane

Wagering: B) Channel Adam Rytenskild

Wagering: C) Product Craig Nugent

Media and International Brendan Parnell

Keno David Ginnane

Gaming Services Adam Rytenskild For

per

sona

l use

onl

y

4 Tabcorp Investor Day 17 October 2013

Quality integrated gambling entertainment businesses Long dated licences Strong trusted brands Unique multi-product / multi-channel distribution Geographic diversification

Strong cash generating businesses and defensive earnings profile

Product and technology innovation to lead both retail and digital channels

Driving growth from new investments

Business model underpinned by strong relationships with stakeholders

Tabcorp has an attractive investment case F

or p

erso

nal u

se o

nly

5 Tabcorp Investor Day 17 October 2013

Key priorities

Capital Optimise the use of and return on invested capital

Wagering Lead wagering transformation

Media & International Enhance integration with wagering

Keno Drive growth through product expansion

Gaming Services

Grow through venue, product and interstate expansion

Underpinned by the ability to attract, develop and retain talent For

per

sona

l use

onl

y

6 Tabcorp Investor Day 17 October 2013

Capital - Damien Johnston F

or p

erso

nal u

se o

nly

7 Tabcorp Investor Day 17 October 2013

Optimise the use of and return on invested capital

Returns

Increase return on invested capital

Productivity

Drive group-wide productivity improvement

Balance sheet

Maintain strong balance sheet

For

per

sona

l use

onl

y

8 Tabcorp Investor Day 17 October 2013

Tabcorp’s objective is ROIC of at least 14% by FY16

12%

14%+

FY13 FY16

Notes: 1. Return on Invested Capital (ROIC) is calculated as EBIT / Invested Capital (average of opening and closing Invested Capital for a year) 2. EBIT is Earnings Before Interest & Tax before significant items 3. Invested Capital comprises shareholders’ equity plus Net Debt. Invested Capital at 30 June 2013 was $2,529 million 4. Net Debt includes US$ debt at the A$ principal repayable under cross currency swaps 5. Assumes no material changes to current regulatory, taxation and racing industry arrangements

For

per

sona

l use

onl

y

9 Tabcorp Investor Day 17 October 2013

Productivity is a key focus: FY13 opex/revenue of 21% Target opex/revenue of 20-21%

Project “Future Fit” commenced in FY13 to identify opportunities to improve operating processes and practices. Initiatives identified include: Property optimisation Renegotiation of certain supplier contracts Continued focus on discretionary

expenses Enhancing our people capability in key

growth areas

Drive group-wide productivity improvement

Source: Income statement for the year ended 30 June 2013

36%

Advertising & promotions

9%

20% 10%

25%

Employment

Property

Other

Communications & technology

FY13 Operating Expenses $423m

For

per

sona

l use

onl

y

10 Tabcorp Investor Day 17 October 2013

400 400 400

150

284

250

84127

0

100

200

300

400

500

600

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22

$m

Bank facilities Medium Term notes (May 2014)Tabcorp Retail bonds (May 2014) Tabcorp Subordinated notesUS Private Placement

Maintain strong balance sheet

Notes Tabcorp Subordinated Notes mature in March 2037, however illustrated above at the first call date in 2017

Well diversified debt structure Investment grade credit rating Refinancing underway with bank facility

extended. Focus on May 2014 bond maturities

For

per

sona

l use

onl

y

11 Tabcorp Investor Day 17 October 2013

Wagering market trends – Doug Freeman

For

per

sona

l use

onl

y

12 Tabcorp Investor Day 17 October 2013

The wagering market has shown consistent growth

Source: ARB Fact Books, internal Tabcorp data, includes some estimates

Australian Wagering Market

12

14

16

18

20

22

24

26

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Annu

al T

urno

ver (

$b)

FY01 - FY07 FY08 - FY13CAGR 7.9% 4.1%

For

per

sona

l use

onl

y

13 Tabcorp Investor Day 17 October 2013

Tabcorp market share has remained relatively stable since the recent increase in competition

Tabcorp’s share of wagering turnover

Source: ARB Fact Books, internal Tabcorp data, includes some estimates

Share of turnover

42.8% 42.5% 44.3% 43.7% 44.4% 43.6%

57.2% 57.5% 55.7% 56.3% 55.6% 56.4%

FY08 FY09 FY10 FY11 FY12 FY13

TAH share OtherFor

per

sona

l use

onl

y

14 Tabcorp Investor Day 17 October 2013

Tabcorp total wagering revenue CAGR of 4.7% since 20081

700

900

1,100

1,300

1,500

1,700

1,900

FY08 FY09 FY10 FY11 FY12 FY13

Growth on pcp % 7.6% 5.2% 0.5% 4.2% 5.9%

Fixed odds expansion, yield improvement, Trackside, and international have contributed to the 4.7% CAGR

Notes 1 Total revenue includes the Victorian JV partner interest, NSW represents 100% of revenue

For

per

sona

l use

onl

y

15 Tabcorp Investor Day 17 October 2013

Lead wagering transformation

Customer Drive deep customer relationships

Channel Digital leadership, underpinned by exclusive retail network

Product Expand product and optimise yield

For

per

sona

l use

onl

y

16 Tabcorp Investor Day 17 October 2013

Wagering customer - David Ginnane F

or p

erso

nal u

se o

nly

17 Tabcorp Investor Day 17 October 2013

Drive deep customer relationships

Customer Base Channels Brands

TAB1

Luxbet

Trackside1

Sky Racing2

Total Est. customer base

Total Customers

1,850,000

40,000

220,000

1,500,000

2,000,000+

Unparalleled breadth of customers, channels and brands in the domestic category underpins comprehensive customer insights and relationships

Notes 1 Internal Tabcorp data, includes some estimates 2 Represents active viewers

For

per

sona

l use

onl

y

18 Tabcorp Investor Day 17 October 2013

Customer acquisition and engagement continues to grow

TAB account customers

Unique active customers: customers who placed a bet during the financial year Acquired customers: new customers who signed up to a TAB account and placed a bet during the financial year

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

FY10 FY11 FY12 FY13

Active customers Acquired customers

6.4%

CAGR

FY10 – FY13

5.7%

For

per

sona

l use

onl

y

19 Tabcorp Investor Day 17 October 2013

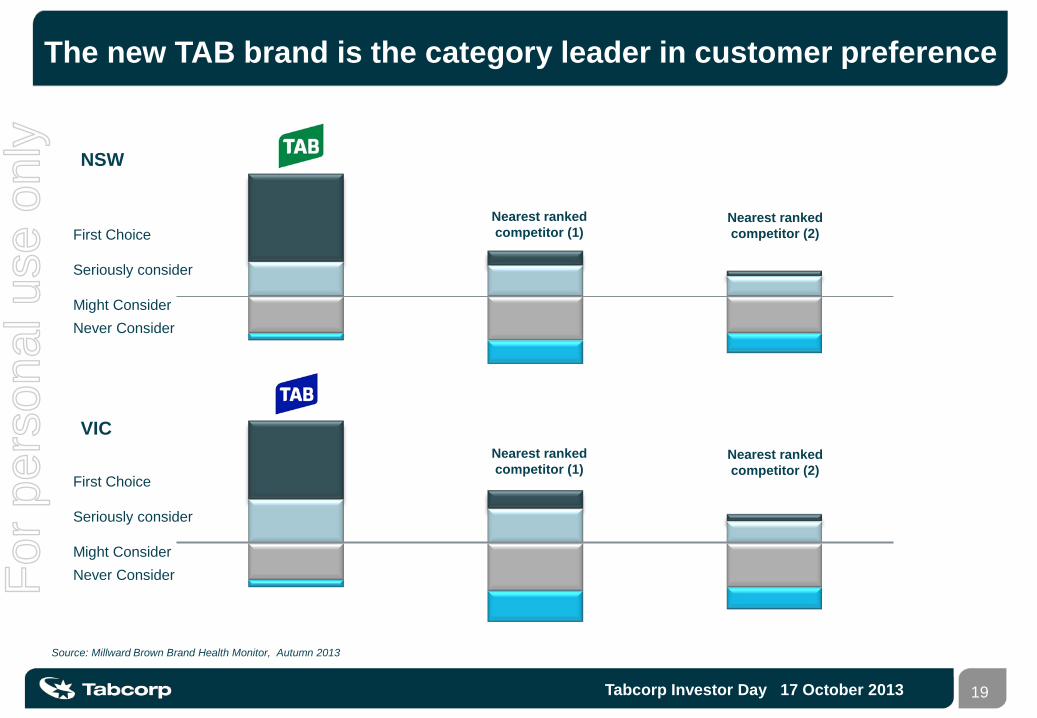

The new TAB brand is the category leader in customer preference

First Choice Seriously consider Might Consider Never Consider

First Choice Seriously consider Might Consider Never Consider

NSW

VIC

Nearest ranked competitor (1)

Nearest ranked competitor (2)

Nearest ranked competitor (1)

Nearest ranked competitor (2)

Source: Millward Brown Brand Health Monitor, Autumn 2013

For

per

sona

l use

onl

y

20 Tabcorp Investor Day 17 October 2013

Analytics, CRM and loyalty

Highly targeted messaging and content: Right offer Right channel Right time

Analytics CRM Loyalty

Sophisticated analytics, CRM and loyalty capabilities support Tabcorp’s leadership position

Scale and analytics tools driving a big data advantage

Talent sourced from a range of highly developed CRM categories, including the UK wagering sector

Expansive customer and transactional information: Products Customers Transactions

Expands depth and breadth of customer data: Retail and account NSW and VIC Brings CRM to retail

For

per

sona

l use

onl

y

21 Tabcorp Investor Day 17 October 2013

85%

88%

86%

61%

82% 81% 85%

83%

79%

82%

79% 81%

85%

85%

85%

90%

59%

84%

79%

86% 84%

80%

80%

82% 83% 86%

Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Customer retention rates

Customer retention rates improve as CRM accelerates

CY12 retention rate CY13 retention rate

Uplift in underlying retention despite increasing competition

Retained customers worth ~3 times value of new or reactivated customers

Note: seasonality applies Post-SRC effect

Retention rate: % contactable customers who placed a bet in a given month, as well as the preceding month

For

per

sona

l use

onl

y

22 Tabcorp Investor Day 17 October 2013

Loyalty program 1:1 communication to retail cash customers

TAB Rewards member base (est FY14)

Customer retention rates underpinned by account customer CRM program

New loyalty program brings CRM to retail cash customers

Newly identified customers are folded into the CRM program

0

50

100

150

200

250

300

Account members Retail cash members

For

per

sona

l use

onl

y

23 Tabcorp Investor Day 17 October 2013

Our social and digital platforms provide extensive reach

Facebook: translates retail and on-course experiences into digital experiences

Twitter: rapid communication of product, price, event and service information

YouTube: new TAB branded YouTube page launch

Social platforms driving extremely high and growing volumes of viewing impressions, further strengthening our customer insights and relationships

For

per

sona

l use

onl

y

24 Tabcorp Investor Day 17 October 2013

Wagering channel - Adam Rytenskild F

or p

erso

nal u

se o

nly

25 Tabcorp Investor Day 17 October 2013

Digital leadership, underpinned by exclusive retail network

Wagering distribution channels work together for overall growth

Customers enjoy the multi-channel offering with 66% of account deposits in cash in retail

Rapidly increasing digital turnover driving overall growth

Further integration of retail and digital will make both stronger

FY10 FY13

Retail Digital Call centre Other

63%

17%

11% 9%

58%

24%

8% 10%

Wagering Turnover by Channel

CAGR 3.5%

For

per

sona

l use

onl

y

26 Tabcorp Investor Day 17 October 2013

Digital and retail strategies

1. Digital strategy for TAB and Luxbet

Increase capability and scale

Enhance mobile

Digital pathway 2. Retail and digital integration

Self-service

Digital information displays

Digital incentive program 3. Retail

Extract full value from exclusive retail channel F

or p

erso

nal u

se o

nly

27 Tabcorp Investor Day 17 October 2013

Increase digital capability and scale

In-housing and increasing digital capability to accelerate speed to market

Digital team to build to 40 people by January 2014, offset by saving of third party expenses

Digital leadership roles recruited in Commercial, Marketing and Technology. Previous expertise:

3 Mobile, Telstra/Big Pond Media

Google and BT

REA Group (realestate.com.au)

Increased agility driving improved speed to market

External hire, previous experience: • REA Group / realestate.com.au

For

per

sona

l use

onl

y

28 Tabcorp Investor Day 17 October 2013

FY10 FY11 FY12 FY13Mobile device Desktop

Enhance mobile

Mobile platform in place, continued enhancement to drive future performance

Mobile driving digital growth

At least 6 major releases for iPhone, iPad and Android each year to drive continuous improvement

Luxbet and Sky Mobile integrated to development

CAGR 16%

Tabcorp digital turnover

Today

49% 51%

For

per

sona

l use

onl

y

29 Tabcorp Investor Day 17 October 2013

Digital pathway

Provide the best experience on chosen device across all TAB channels & Luxbet

Continue to enhance current TAB.com.au and Luxbet.com Speed to load on TAB.com.au improved more than 50% in last 12 months New Luxbet site released in September 2013

HTML pathway

Lite.TAB.com.au (racing only) website optimised for tablet released October 2013 TAB.com.au Mobile site Self-service and then operator terminals in Retail

Developing a consistent experience across all devices

Lite.TAB.com.au

For

per

sona

l use

onl

y

30 Tabcorp Investor Day 17 October 2013

FY10 FY13FY10 FY13

Retail and digital integration

Self-service acts as the middle ground for retail and digital transactions

Self Service Terminal (SST) expansion has extended reach and improved customer experience

Digital platform in place - self-service to be integrated and then operator terminals

Digital form/information integration pathway to paperless

Digital incentive for top-tier venues (pilot complete)

c 4,700

c 2,600

40% 48%

+80%

+126%

No. of SST’s SST % of retail turnover SST turnover $b

22%

30%

40%

48%

FY10 FY11 FY12 FY13

1.4

3.3

For

per

sona

l use

onl

y

31 Tabcorp Investor Day 17 October 2013

Extract full value from exclusive retail channel

Retail foundation secured – network expansion

complete increasing footprint 13% FY10-FY13

Tiered venue model, supported by an efficient Kiosk

offer, has enabled extended reach

Sales team re-structured to drive top tier performance

Improve channel margin via appropriate venue

incentives, e.g. venues ‘legends league’

Targeted top-tier refresh continues (partly venue funded)

For

per

sona

l use

onl

y

32 Tabcorp Investor Day 17 October 2013

Fixed odds wagering product - Craig Nugent F

or p

erso

nal u

se o

nly

33 Tabcorp Investor Day 17 October 2013

FY13 Fixed Odds Revenue Tabcorp NT Corporate Bookmakers

TAB Fixed Odds Luxbet 9 Wagering Operators $404m $39m *$500m

* TAH estimate, excludes Luxbet

Tabcorp is Australia’s largest bookmaker and is maintaining market leadership via its two brands TAB and Luxbet

Our dual brand strategy allows us to offer customers all wagering products, across all distribution channels

Tabcorp continues to be the fixed odds market leader F

or p

erso

nal u

se o

nly

34 Tabcorp Investor Day 17 October 2013

674

1,254

1,660

FY11 FY12 FY13

16

29

46

FY11 FY12 FY13

11.9% 12.4%

14.2%

FY11 FY12 FY13

80

156

236

FY11 FY12 FY13

Ticket and turnover growth shows the popularity of fixed odds racing

Fixed odds racing accounted for 25% of the ‘win and place’ racing revenue in FY13

Revenue growth is exceeding turnover growth

Tickets (millions) Turnover $m

Revenue $m Yield %

Fixed odds racing - growing tickets, turnover and yields F

or p

erso

nal u

se o

nly

35 Tabcorp Investor Day 17 October 2013

1,259 1,326

1,245

FY11 FY12 FY13

11.7% 12.4%

13.5%

FY11 FY12 FY13

147 165 168

FY11 FY12 FY13

28 30 31

FY11 FY12 FY13

Turnover performance impacted by shift in customer mix

Growth in yields driven by enhanced risk management

Tickets (millions) Turnover $m

Revenue $m Yield %

Fixed odds sport market remains competitive F

or p

erso

nal u

se o

nly

36 Tabcorp Investor Day 17 October 2013

Enhanced risk management structure driving more quality product at better yields

Fixed odds risk management employees have increased by over 50% since FY11

Algorithm based customer scoring system provides real time risk assessment

‘Intercept’ and ‘partialling’ selected bets across all channels

64 Employees

Racing Team Sport Team

Harn

ess,

Gre

yhou

nds &

In

tern

atio

nal

NSW

Vict

oria

Que

ensla

nd

Live

Dom

estic

Foo

tbal

l an

d O

ther

Socc

er

Tenn

is

US

Spor

ts

Analysts – Algorithm based scoring system

Risk Management Structure

TAB has increased people and technology capability F

or p

erso

nal u

se o

nly

37 Tabcorp Investor Day 17 October 2013

Expansion of fixed odds products - a key driver of revenue growth

FY14 fixed odds product expansion:

Expanded books in greyhounds and harness to maintain market leadership

Automated Market Management (AMM) – Sports books scaled to match global offering

18

28

36

-

5

10

15

20

25

30

35

40

FY11 FY12 FY13

thou

sand

s

No. of Racing Books

193

267 288

-

50

100

150

200

250

300

350

FY11 FY12 FY13

thou

sand

s

No. of Sport Books

Fixed odds products expansion F

or p

erso

nal u

se o

nly

38 Tabcorp Investor Day 17 October 2013

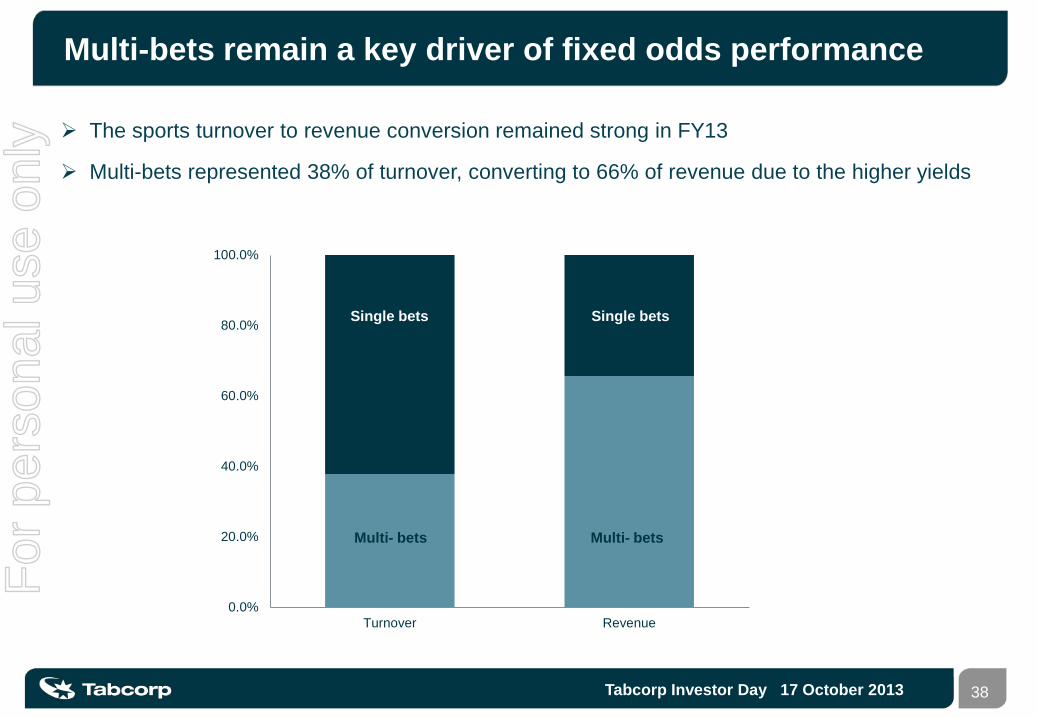

The sports turnover to revenue conversion remained strong in FY13

Multi-bets represented 38% of turnover, converting to 66% of revenue due to the higher yields

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Turnover Revenue

Single bets Single bets

Multi- bets Multi- bets

Multi-bets remain a key driver of fixed odds performance F

or p

erso

nal u

se o

nly

39 Tabcorp Investor Day 17 October 2013

American sports growth is outperforming domestic sports

A diversified sports offering leaves Tabcorp less susceptible to a series of abnormal results in any one sport

Product fees to sports controlling bodies are payable on domestic sports

A key focus in FY14 will be the Soccer World Cup in partnership with Football Federation Australia and broadcaster SBS

TAB Sports Product Sales Share

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

AFL Rugby League Soccer Tennis US Sports Cross SportMulti

Other

FY12 FY13

International sports product continues to grow in popularity F

or p

erso

nal u

se o

nly

40 Tabcorp Investor Day 17 October 2013

71

115

50

<= $20 > $20 to <=$200 > $200

23.1%

16.2%

7.7%

<= $20 > $20 to <=$200 > $200

53

72

43

<= $20 > $20 to <=$200 > $200

27.3%

16.5%

6.9%

<= $20 > $20 to <=$200 > $200

Customer demand for fixed odds racing increasing

Higher levels of pari-mutuel substitution in < $20 range, with favourable impact on yields

< $20 bets made up 41% of pari-mutuel ‘win and place’ turnover in FY13

In sport, the yield for bets up to $20 is the highest at 27.3%, largely driven by multi bets

Fixed Odds Racing Revenue $m Yield

Fixed Odds Sport Revenue $m Yield

Yield optimisation will continue to be a focus F

or p

erso

nal u

se o

nly

41 Tabcorp Investor Day 17 October 2013

12

21

28

39

FY10 FY11 FY12 FY13

The Luxbet offering differs to TAB and growth is continuing

476

559 572 643

FY10 FY11 FY12 FY13

68% of Luxbet Sales are derived from Credit and Tote derivative products which are not able to be offered by TAB Wagering

42% Revenue growth in FY13 was best in Corporate Bookmaker category

Turnover $m Revenue $m

EBITDA $m Yield %

-6.3

0.0 0.2

1.5

FY10 FY11 FY12 FY13

2.5%

3.8%

4.9%

6.1%

FY10 FY11 FY12 FY13

For

per

sona

l use

onl

y

42 Tabcorp Investor Day 17 October 2013

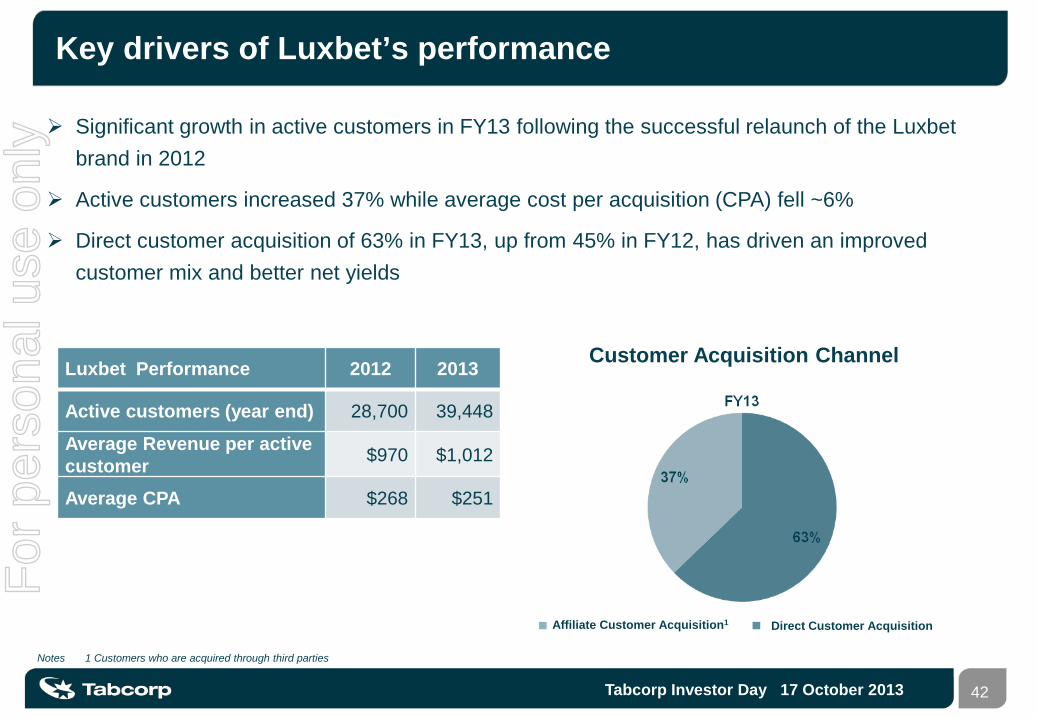

Significant growth in active customers in FY13 following the successful relaunch of the Luxbet brand in 2012

Active customers increased 37% while average cost per acquisition (CPA) fell ~6%

Direct customer acquisition of 63% in FY13, up from 45% in FY12, has driven an improved customer mix and better net yields

Luxbet Performance 2012 2013

Active customers (year end) 28,700 39,448

Average Revenue per active customer $970 $1,012

Average CPA $268 $251

Affiliate Customer Acquisition1 Direct Customer Acquisition

Key drivers of Luxbet’s performance

Customer Acquisition Channel

Notes 1 Customers who are acquired through third parties

For

per

sona

l use

onl

y

43 Tabcorp Investor Day 17 October 2013

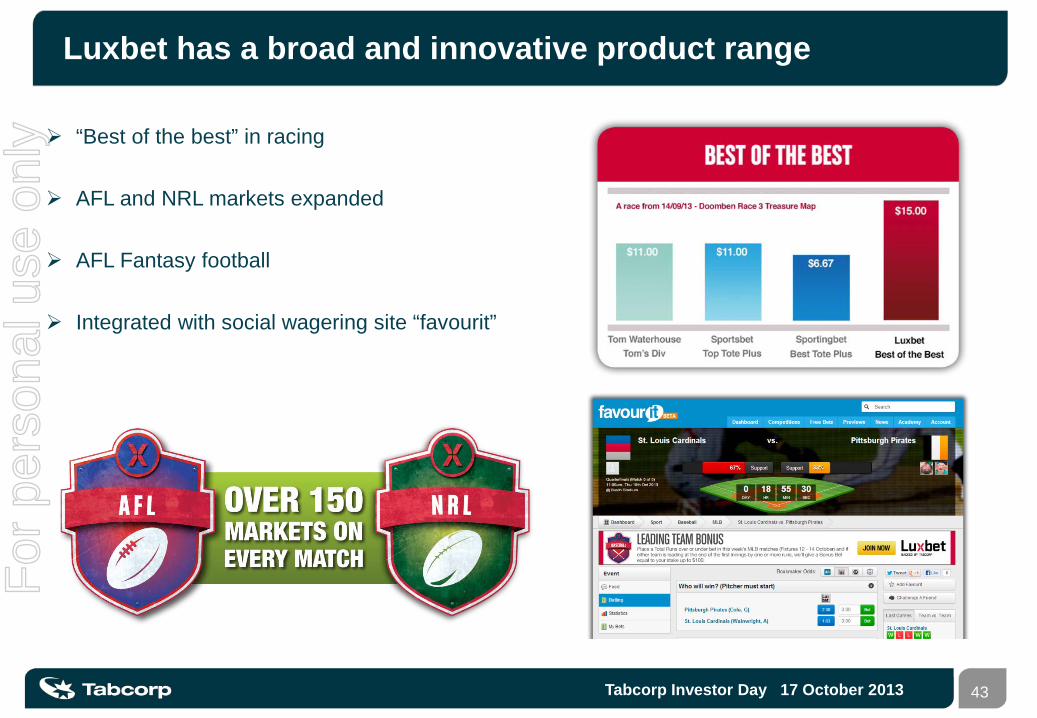

“Best of the best” in racing

AFL and NRL markets expanded

AFL Fantasy football

Integrated with social wagering site “favourit”

Luxbet has a broad and innovative product range F

or p

erso

nal u

se o

nly

44 Tabcorp Investor Day 17 October 2013

Media and International - Brendan Parnell F

or p

erso

nal u

se o

nly

45 Tabcorp Investor Day 17 October 2013

Enhance integration with wagering

Product Secure rights and broaden product base

Customer experience Expand digital media and optimise content

International Expand international co-mingling and export of racing

For

per

sona

l use

onl

y

46 Tabcorp Investor Day 17 October 2013

Sky Racing – world leader in race broadcasting

Business overview

Sky Racing: a multi-platform, multi-media network Sky Racing channels Sky Sports Radio Sky Racing digital (web, apps, media services)

Extensive network coverage 5,400 retail outlets – hotels, clubs and TABs Pay TV across 2.4 million homes

International growth Export to 51 countries Importing international race content from 10 countries Co-mingling

TV Channels

Retail Digital

Homes

Radio

Sky and Wagering – a symbiotic relationship

Betting stimulated by synchronised racing vision and commentary

Promoting betting through data, vision and audio display

International and local relationships – foster wagering and sustain racing

For

per

sona

l use

onl

y

47 Tabcorp Investor Day 17 October 2013

Aim to secure and extend rights Renew TVN media rights Extend media rights portfolio

Broaden base of product Expanded wagering day Sports betting content integration

Media Rights Overview

Type Race Meets

Rights Held New Media

Thoroughbred

QLD/NT 517

WA 259

SA 177

ACT 26

TAS 70

Internat’l 1,854

Greyhound & Harness

AUS & Internat’l 5761

NSW and VIC t’breds 11301

X2

Note: 1. TVN content is 16.6% of Australian race meetings FY13 (excludes International races) 2. Telstra currently holds TVN’s New Media rights.

Secure rights and broaden product base F

or p

erso

nal u

se o

nly

48 Tabcorp Investor Day 17 October 2013

Expand digital media Seeking TVN digital content Unique digital services - Watch & Bet Customisable products i.e. Dual screen player

Optimise content to support wagering

Race scheduling enhancement Wagering display enhancements Fixed odds integration

Weekly Digital Stats1 #’s1 Growth on pcp Internet Page Views 851k +33%

Internet Visits 153k +74%

Digital Visitors – All2 413k +4%

Note: 1. Weekly figures for w/c 29 September 2013; 2. App, web and Sky Form consumers

TAB-SKY Watch & Bet

Dual Screen Media Centre

Expand digital media and optimise content F

or p

erso

nal u

se o

nly

49 Tabcorp Investor Day 17 October 2013

Co-mingling includes Direct or Indirect as well as Hosting and Guesting. Benefits include: Increased pool liquidity Enhanced viability of product

Tabcorp International provides a 1 stop shop Integrated form, data & vision (multi-language, multi-media) Co-mingling

Co-mingling expansion plans PGI – the global tote gateway Expanded Hosting and Guesting Connecting Asia

Continued focus on strategic partnerships (HK, NZ, Sth Africa, Singapore)

Expand international co-mingling and export of racing

Chinese digital form guide

For

per

sona

l use

onl

y

50 Tabcorp Investor Day 17 October 2013

Keno - David Ginnane F

or p

erso

nal u

se o

nly

51 Tabcorp Investor Day 17 October 2013

Drive Keno growth through product expansion

Customer Increase participation by lotteries and EGM players

Product Extend and develop product range

Channel Drive optimal retail experience

For

per

sona

l use

onl

y

52 Tabcorp Investor Day 17 October 2013

Increase participation by lotteries and EGM players

Tabcorp’s Keno customers are awarded more than $68m per month in prizes Games are offered on average every 3 minutes Prizes range from $1 to multi million dollar jackpots

Source: Tabcorp estimates based on Annual Reports, internal data

6.9%

CAGR

FY07 – FY13

4.3%

4.8%

Total 5.1%

711 724

845 860 942 1,008

1,064

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Turn

over

($m

)

Lotteries TAH Keno Non TAH Keno

Australian Lotteries FY13 Turnover ~$6.9 billion

For

per

sona

l use

onl

y

53 Tabcorp Investor Day 17 October 2013

There are opportunities to shift share of the ‘gambling wallet’ with a compelling Keno product and prize offers

Source: Millward Brown Health Monitor Spring 2012

Keno customer cross-product utilisation (%)

84%

60%

65%

14%

Play Lotto

Bought scratch cards

Play poker machines

Play Trackside

Increase participation by lotteries and EGM players F

or p

erso

nal u

se o

nly

54 Tabcorp Investor Day 17 October 2013

Product innovation is core to refreshing the Keno proposition to existing and new customers

Keno Racing Jackpot Pooling Keno Roulette

• NSW only • Traditional roulette bet types • Targets younger hotel patron

• Intention to pool jackpots • Accelerates win frequencies • Regulatory approvals being

sought

• Pilot underway in QLD • Animated racing offer • Fixed odds pay table

Extend and develop product range F

or p

erso

nal u

se o

nly

55 Tabcorp Investor Day 17 October 2013

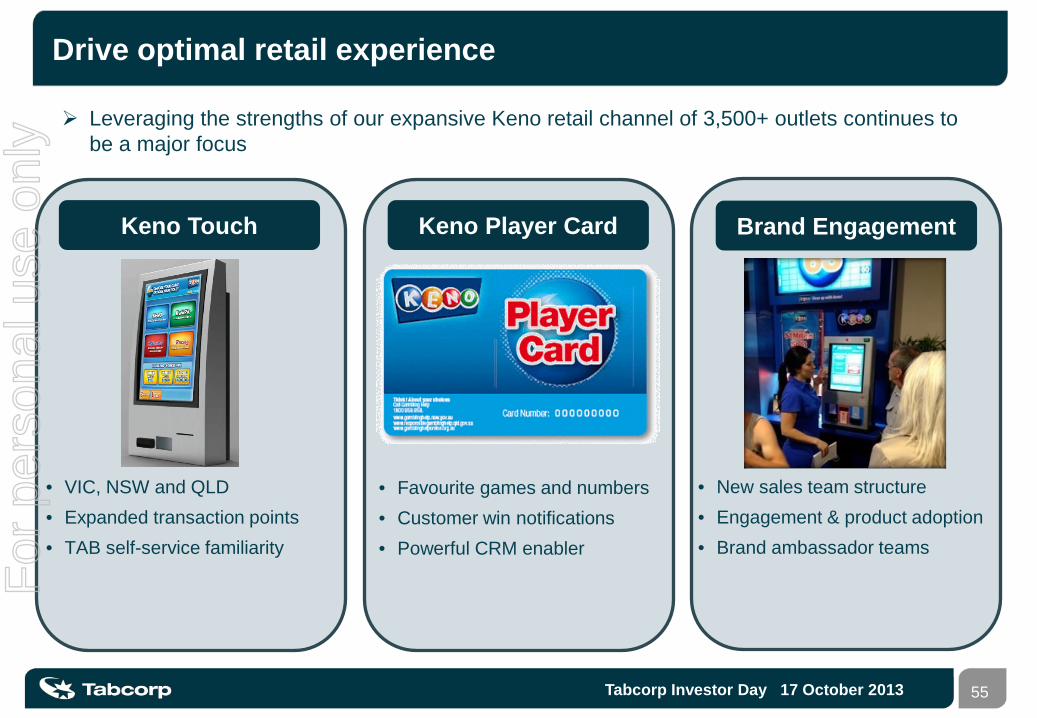

Leveraging the strengths of our expansive Keno retail channel of 3,500+ outlets continues to be a major focus

Keno Touch Keno Player Card Brand Engagement

• New sales team structure • Engagement & product adoption • Brand ambassador teams

• Favourite games and numbers • Customer win notifications • Powerful CRM enabler

• VIC, NSW and QLD • Expanded transaction points • TAB self-service familiarity

Drive optimal retail experience F

or p

erso

nal u

se o

nly

56 Tabcorp Investor Day 17 October 2013

Gaming Services - Adam Rytenskild F

or p

erso

nal u

se o

nly

57 Tabcorp Investor Day 17 October 2013

Grow through venue, product and interstate expansion

Customer Expand value added services

Expand in Victoria Drive performance to generate new venue sign-ups

Expand interstate Expand TGS into other jurisdictions, an initial focus on NSW

For

per

sona

l use

onl

y

58 Tabcorp Investor Day 17 October 2013

Solid foundation laid in first year

TGS Model: Built on core gaming expertise Long term contracts; 75% 10 years, 25% minimum 6 years Transportable to other jurisdictions, especially where other Tabcorp businesses exist

Product: over 3,000 new EGMs and Game upgrades deployed since April13

Loyalty: The Diamond Rewards program is unique, with 130,000 active members

Service offer: 30 TGS venues refurbished, supported by TGS

For

per

sona

l use

onl

y

59 Tabcorp Investor Day 17 October 2013

EGM procurement - large scale purchase and exclusivity of key machines EGM advice and business intelligence – floor analysis, product mix and predictive analytics Loyalty - Customer behaviour analytics - tailor product and service to local customer Venue design and project management Responsible Gambling - Dow Jones Sustainability global index leader

Value added services

Source: Tabcorp estimates

Provider EGMs Supply EGMs

Business Intelligence

Break Fix Loyalty BDMs Venue Design

RSG

TGS 8,440 Competitor 1 1,817 Competitor 2 1,793 Competitor 3 1,388 Competitor 4 1,024 Competitor 5 749 Competitor 6 298

For

per

sona

l use

onl

y

60 Tabcorp Investor Day 17 October 2013

In-EGM loyalty will further differentiate TGS

TGS expected to gain first-mover advantage in the Victorian market for in-EGM loyalty, with exclusive distribution of the IGT Advantage system

First with Voluntary Pre-Commitment capability in Victoria

The system provides differentiation for TGS via: Loyalty points for customers redeemable in-venue Advertising and messaging on EGMs Ability to promote offers to customers Provides platform for Voluntary Player Pre Commitment

Expand value added services F

or p

erso

nal u

se o

nly

61 Tabcorp Investor Day 17 October 2013

TGS growth levers include machine top ups, key account expansion and new account acquisition

Performance drivers in place and building Focus on value for Key Account partners to drive performance Product mix and speed to market Expert new machine/game advice and seamless deployment Diamond Rewards and in-EGM launch Loyalty Zone Customer service program Venue design expertise with a whole-of-venue focus

TGS targeted Victorian expansion

In-EGM Loyalty expansion a key initiative to capture increased market share Build scale and team capability to deliver growth post foundation year

Drive performance to generate new sign-ups F

or p

erso

nal u

se o

nly

62 Tabcorp Investor Day 17 October 2013

93,933 EGMs

42,730 EGMs

26,202 EGMs

12,744 EGM’s

0 EGM’s

NSW Key Milestones Status

Dealer’s Licence

Gaming Services Agreement

Industry Engagement

Venue Readiness

Formal approval pending

1,186 EGM’s

2,379 EGMs

EGMs do not include casinos

An initial focus on NSW

Well understood market due to existing wagering and keno business

Mid-sized Clubs a sizeable immediate market

2-3 TGS venues initially to demonstrate performance

Expand TGS into other jurisdictions F

or p

erso

nal u

se o

nly

63 Tabcorp Investor Day 17 October 2013

Long term licences

Unique multi product / multi channel customer proposition

Experienced management team

Focus on increasing returns

Conclusion F

or p

erso

nal u

se o

nly

64 Tabcorp Investor Day 17 October 2013

Appendix: Business overview

Above statistics are as at 30 June 2013, rounded % EBITDA based on FY13 results

Product Brands Licence expiry % EBITDA Retail distribution

Wagering NSW 2097Victoria 2024

NSW 2,130 outletsVictoria 750 outlets

260 with oncourse wagering facilities

NSW 2097Victoria 2024 57% NSW 2,100 outlets

Victoria 750 outlets

NT 2015

KenoNSW 2022

Queensland 2047Victoria 2022

16%Queensland 1,170 outlets

NSW 1,800 outletsVictoria 680 outlets

TGS n/a 13% 8,440 EGMs contracted166 outlets

Media n/a 14%5,400 retail outlets

Broadcasting from 200 Australian racetracksF

or p

erso

nal u

se o

nly

65 Tabcorp Investor Day 17 October 2013

Disclaimer This Presentation contains summary information about Tabcorp Holdings Limited (Tabcorp) and its subsidiaries (Tabcorp Group). It should be read in conjunction with the Tabcorp Group’s other periodic and continuous disclosure announcements lodged with the Australian Securities Exchange (ASX), which are available at www.asx.com.au. The information contained in this Presentation is of a general nature and has been prepared by Tabcorp in good faith and with due care but no representation or warranty, express or implied, is provided as to the correctness, quality, accuracy, timeliness, adequacy, reliability or completeness of any statements, estimates or opinions or other information contained in this Presentation. To the maximum extent permitted by law, each member of the Tabcorp Group and their respective directors, officers, partners, employees, advisers and agents and any other person involved in the preparation of this Presentation (each a Disclaiming Party) disclaim all liability and responsibility (including, without limitation, any liability arising from the fault or negligence on the part of any Disclaiming Party) for any direct, indirect or consequential loss or damages which may be suffered by a recipient through the use of or reliance on anything contained in or omitted from this Presentation. This Presentation is for information purposes only and is not a prospectus, product disclosure statement or other disclosure or offering document under Australian or any other law. This Presentation does not constitute an offer, invitation or recommendation to subscribe for or purchase any security and neither this Presentation nor anything contained in it shall form the basis of any contract or commitment. This Presentation is not a recommendation to acquire Tabcorp securities. The information provided in this Presentation is not financial product advice and has been prepared without taking into account any recipient's investment objectives, financial circumstances or particular needs, and should not be considered to be comprehensive or to comprise all the information a recipient may require in order to make an investment decision regarding Tabcorp securities. All dollar values are in Australian dollars (A$) unless otherwise stated. No Disclaiming Party warrants or guarantees the future performance of Tabcorp or any return on any investment made in Tabcorp. This Presentation may contain certain 'forward-looking statements'. The words 'anticipate', 'aim', 'believe', 'expect', 'project', 'forecast', 'estimate', 'will', 'likely', 'intend', 'should', 'could', 'may', 'target', 'plan' and other similar expressions (including indications of 'objectives') are intended to identify forward-looking statements. Indications of, and guidance on, financial position and performance are also forward-looking statements. These statements may involve significant elements of subjective judgement and analysis. No Disclaiming Party makes any representation or warranty, express or implied, as to the fairness, accuracy, completeness, correctness, likelihood of achievement or reasonableness of any forecasts, forward-looking statements or projections contained in this Presentation. Such forecasts, forward-looking statements or projections are not guarantees of future performance. Any such forecasts, forward-looking statements or projections contained in this Presentation have been based on Tabcorp's intent, belief or current expectations with respect to its business and operations, market conditions, results of operations and financial condition, risk management practices and other future events as at the date of this Presentation and are subject to significant uncertainties, risks and contingencies, many of which are beyond the control of the Tabcorp Group, that could cause actual results to differ materially from the intentions, beliefs and expectations expressed or implied. You are cautioned not to place undue reliance on forecasts, forward-looking statements or projections. Except as required by law or regulation (including the ASX Listing Rules), Tabcorp undertakes no obligation to publicly update these forward-looking statements. In particular, forward-looking statements are underpinned by certain market, operational, financial, regulatory and other assumptions. An investment in Tabcorp is also subject to investment risks including possible loss of income and principal invested. Certain key risks that may affect the Tabcorp Group, its financial and operating performance and the accuracy of any forward-looking statements included in this Presentation include (without limitation): (i) changes in the regulatory environment (including taxes and levies), (ii) changes to race field fees, (iii) the suspension, cancellation or termination of the Tabcorp Group's wagering, gaming and other licences, (iv) relevant racing industries failing to provide programs of events, (v) the minimum financial performance arrangements applying in favour of the Victorian racing industry under the Victorian joint venture, and (vi) Tabcorp being able to renegotiate its key broadcast arrangements on satisfactory terms. For further information, see section 5.3 (Risk factors associated with the Tabcorp Group) of the prospectus, dated 22 February 2012, relating to the issue of Tabcorp Subordinated Notes. Past performance information given in this Presentation is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance.

For

per

sona

l use

onl

y

66 Tabcorp Investor Day 17 October 2013

For

per

sona

l use

onl

y