Embed Size (px)

Citation preview

SWOT Analysis on the Capital Market Infrastructures

in the ASEAN+3 Member Countries and Its

Implications

February 2014

Korea Institute of Finance

CONTENTS

I. Background .................................................................................................................. 1

II. Scope of the Study ..................................................................................................... 2

III. Macroeconomic Environment and Financial Markets in ASEAN+3 .................. 4

1. Macroeconomic Environment ............................................................................................ 4

2. Financial Structure in ASEAN countries ........................................................................... 9

IV. SWOT analysis of ASEAN+3 Stock Markets ....................................................... 10

1. Stock markets and Economic Development ..................................................................... 10

2. Strengths in ASEAN+3 Stock Markets ............................................................................. 11

3. Weaknesses in ASEAN+3 Stock Markets ........................................................................ 17

4. Opportunities in ASEAN+3 Stock Markets ..................................................................... 19

5. Threats in ASEAN+3 Stock Markets ............................................................................... 19

V. Bond Markets of ASEAN+3 .................................................................................... 23

1. Bond Markets and Economic Development ..................................................................... 23

2. Strengths in ASEAN+3 Bond Markets............................................................................. 24

3. Weaknesses in ASEAN+3 Bond Markets ........................................................................ 25

4. Opportunities in ASEAN+3 Bond Markets ...................................................................... 27

5. Threats and Challenges in ASEAN+3 Bond Markets ...................................................... 29

VI. Implications and Concluding Remarks ................................................................. 31

LIST OF FIGURES

<Figure 1> Capital market infrastructure .......................................................................... 2

<Figure 2> Annual GDP growth, ASEAN+3 .................................................................... 4

<Figure 3> Ratio of Investments to GDP of ASEAN+3 ................................................... 6

<Figure 4> Current Account Balances of ASEAN+3, 2005~2012 ................................... 6

<Figure 5> Government Budget Surplus or Deficit for ASEAN+3, 2005~2012 .............. 7

<Figure 6> Ratio of FDI to GDP of ASEAN+3, 2005~2012 ............................................ 8

<Figure 7> FDI into ASEAN+3, 2005~2012 .................................................................... 8

<Figure 8> ASEAN Countries’ Financial Structures (Percent of GDP), 2009 ................. 9

<Figure 9> ASEAN +3 Debt to GDP ratio .................................................................... 20

<Figure 10> Corporate Bonds vs. Government Bonds ................................................. 25

<Figure 11> Foreign Investor’ Stock Investment and Bond Investment ........................ 26

LIST OF TABLES

<Table 1> GDP growth of ASEAN+3 and others ............................................................. 5

<Table 2> Gross National Savings in ASEAN Countries, 2010 ..................................... 10

<Table 3> GDP per Capital ASEAN Countries ............................................................... 10

<Table 4> ASEAN+3 Stock Exchanges .......................................................................... 12

<Table 5> Proposed Tick Size Reductions .................................................................... 13

<Table 6> Examples of implementation of KRX’s global strategy ................................ 16

<Table 7> ASEAN Vertical clearing and settlement structure for equity securities ....... 18

<Table 8> Comparison between the Current Law and Draft Law in relation to the limits

on foreign ownership ..................................................................................... 21

<Table 9> The ASEAN+3 scoring of economic freedom in 2010 .................................. 22

<Table 10> Recent Policy Changes on Bond Markets of ASEAN+3 ............................. 24

<Table 11> CRAs of ASEAN+3 ..................................................................................... 25

<Table 12> Bond CCP of ASEAN+3 Countries ............................................................. 26

1

I. Background

Despite uncertainty in the global economy and financial markets, so far the ASEAN+3 economies have been recovering from the global financial crisis without any major problem. Resilience of the regional economy has been underpinned by robust domestic demand, effective financial intermediation by healthy banking systems, and appropriate macroeconomic policies. However, remaining risks may still be prevalent. Policy uncertainty, private deleveraging, fiscal drag, and impaired credit intermediation continue to weigh on global growth prospects. Continuing global liquidity infusion could potentially induce excessive risk-taking and leverage, credit expansion, and asset bubble, meaning that the ASEAN+3 region shall remain vigilant of the unintended negative side effects stemming from an extended period of global monetary easing on the region as well as on the risk of global financial markets sentiment that could amplify volatility in capital flows and adversely affect regional financial stability. Therefore, it is more important than ever to develop and integrate capital markets together to promote market efficiency and market stability in the ASEAN+3 region.

To enhance the integration of the ASEAN+3 markets and strengthen the regional financial stability, the Chiang Mai Initiative (CMI) was established by the ASEAN+3 Finance Ministers Meeting (AFMM+3) in 2000 as a network of bilateral currency swap arrangements. The initiative purports to: (1) address short-term liquidity difficulties in the region and (2) supplement the existing international financial arrangements. In 2004, the AFMM+3 agreed to establish a more advanced framework for liquidity support that focused on the multilaterization of CMI (CMIM). Moreover, to support the implementation of the CMIM, an independent regional monitoring and surveillance unit, i.e., the ASEAN+3 Macroeconomic Research Office (AMRO), was established in Singapore in April 2011. Subsequently, to enhance the effectiveness of the ASEAN+3 financial cooperations, the economies concurred to transform the AMRO to be an international organization. This would enable AMRO to conduct objective surveillance as a credible, independent international organization, contributing further to the regional financial stability and strengthening the CMIM. Finally, in the 16th AFMM in New Delhi in May 2013, the ASEAN+3 members agreed to further strengthen the CMIM as part of the regional financial safety net and promote the issuance and facilitating demand of local currency denominated bonds (Asian Bond Market Initiative) .

We now have entered a stage where we should also consider the integration of the capital markets beyond the scope of bond markets while we strive further to build the infrastructure for our integrated bond market. The first steps toward the integration of our capital markets would be assessing our markets, agreeing on the direction of the integration, and finally planning to build the integrated infrastructure where necessary. The difference in the

2

development or size of the capital markets may hinder our efforts toward integration. However, if we build the infrastructure preemptively, it would not only accelerate the development of capital markets of emerging countries but also relieve the impediments caused by the discrepancy. Therefore, in this paper, we would like to assess the capital markets of the member countries and help to usher the member countries into enhancing the compatibility.

II. Scope of the Study

The scope and depth of coverage of infrastructure issues is surely vast. However, for the purpose of this report, we define market infrastructure as relating to all servicing layers along the trading value chain, including inter dealer brokers, exchanges, clearing houses, CSDs, CCP, custodians and so on .

<Figure 1> Capital market infrastructure

The trade facility (exchange) provides the trading platforms. However, not all securities are necessarily traded on a trading. Instead, some are traded in the over-the-counter (OTC). Post-trade infrastructure breaks down into two main types: the place in the process between a

3

trade being made on an exchange and an investor receiving their securities. Mainly, there is Central Counterparties (CCPs), which is a process by which financial transactions in equities are cleared by a single (i.e., "central") counterparty. Since CCP can guarantee the deal against default of trade by acting as the buyer to the seller and the seller to the buyer, it can reduce the systemic risk and strengthen the financial system. A Central Securities Depository (CSD) is a special financial organization holding securities and responsible for the transfer of the securities from the seller to the buyer. Therefore, CSD can provide proof of ownership with eliminating risk from the transaction, Recently, Trade Repositories (TRs) have emerged as an important new infrastructure. TRs centrally collect and maintain the records of derivative contracts. During the global financial crisis, market participants including regulators realized that it is hard to get data about OTC derivatives. So, it has been tried to strengthen the derivatives markets regulatory framework.

In this paper, we will conduct the SWOT analysis which is a useful technique for understanding Strengths and Weaknesses, and for identifying both the Opportunities open to capital market and the Threats it face. In each component, we try to sort out the common denominators by reviewing existing capital market products and evaluating the market infrastructure. We are sure that SWOT analysis can help us uncover opportunities that we are well placed to exploit. And by understanding the weaknesses of capital market infrastructure, we can manage and eliminate threats that would otherwise catch us unawares. Therefore, based on SWOT analysis, we discuss about a set of guidelines which are intended to provide a framework for developing capital market infrastructure not only in each country but also between countries for further capital market integration.

4

III. Macroeconomic Environment and Financial Markets in ASEAN+3

1. Macroeconomic Environment

In order to understand capital market well, we need to know member countries’ macroeconomic condition first. As seen in Figure X.X, majority of countries suffered from the recent global financial crisis including European sovereign-debt crisis during year 2008 and 2009. And they rebounded in 2011 and maintain the growth in 2012, too. Compare to each country, the growth rate of gross domestic product (GDP) varies. On average, Cambodia, China, Indonesia, Lao P.D.R, Myanmar, Singapore and Vietnam are fast growing, above average countries while Brunei Darussalam, Japan, Korea, Malaysia, Philippines and Thailand are relatively slow growing below average countries.

< Figure 2> Annual GDP growth, ASEAN+3

5

On the other hand, we can compare ASEAN+3 growth to other regions in Table x. According to the table, ASEAN+3 countries have luxurious economic growth compared to major industrialized economies which are United States and Euro Zone. ASEAN+3 have become the drivers of world economic growth since the global crisis. According to ADB (2012), strong domestic demands, especially domestic consumption, played the robust safety nets despite the weak external environment. The dynamics of ASEAN+3 growths are complex. But one reason is increasing economic integration.

<Table 1> GDP growth of ASEAN+3 and others (Units: Percent change)

Country 2005 2006 2007 2008 2009 2010 2011 2012 2013 Brunei 0.39 4.40 0.15 -1.94 -1.77 2.60 3.43 0.95 1.45 Cambodia 13.25 10.77 10.21 6.69 0.09 6.10 7.08 7.30 7.02

Indonesia 5.69 5.50 6.35 6.01 4.63 6.22 6.49 6.23 5.30

Lao P.D.R. 6.77 8.65 7.84 7.79 7.50 8.13 8.04 7.88 8.35

Malaysia 4.98 5.59 6.30 4.83 -1.51 7.43 5.13 5.64 4.70

Myanmar 13.57 13.08 11.99 3.60 5.14 5.35 5.91 6.36 6.82

Philippines 4.78 5.24 6.62 4.15 1.15 7.63 3.64 6.82 6.81

Singapore 7.37 8.62 9.02 1.75 -0.79 14.78 5.16 1.32 3.54

Thailand 4.64 5.09 5.04 2.48 -2.33 7.81 0.08 6.49 3.11

Vietnam 7.55 6.98 7.13 5.66 5.40 6.42 6.24 5.25 5.30

ASEAN 6.90 7.39 7.07 4.10 1.75 7.25 5.12 5.42 5.24

China 11.31 12.68 14.16 9.64 9.21 10.45 9.30 7.70 7.60

Japan 1.30 1.69 2.19 -1.04 -5.53 4.65 -0.59 1.96 1.95

Korea 3.96 5.18 5.11 2.30 0.32 6.32 3.68 2.04 2.84

+3 5.52 6.52 7.15 3.63 1.34 7.14 4.13 3.90 4.13

ASEAN+3 6.90 7.39 7.07 4.10 1.75 7.25 5.12 5.42 5.24

EU 3.39 4.42 4.60 0.84 -4.97 1.63 1.50 -0.69 -0.97

United States 3.35 2.67 1.79 -0.29 -2.80 2.51 1.85 2.78 1.56

Word 5.22 5.81 6.01 4.09 0.02 4.17 3.72 3.61 3.26

Source: IMF

On the contrary, investment component in the region staggered during the period. Investment refers to the goods purchased by individuals and firms to add to their stock of capital, which is a fundamental driver of the growth and vitality of financial markets. So the recent stagnation of the capital markets in the region can be explained by such macroeconomic circumstances.

6

<Figure 3> Ratio of Investments to GDP of ASEAN+3

Current account balances for ASEN+3 have been positive since mid-2000 as a whole. Since current account surpluses implies potential outbound investment demand from the countries, ASEAN+3 countries should keep improving performance of the foreign reserves from the surpluses. Asset management of the foreign reserves are usually channeled into U.S. treasury and other advanced countries’ government securities. To improve the performance and secure the regional financial development of the region, it is usually suggested that intra-regional financial investment is promoted.

<Figure 4> Current Account Balances of ASEAN+3, 2005~2012

7

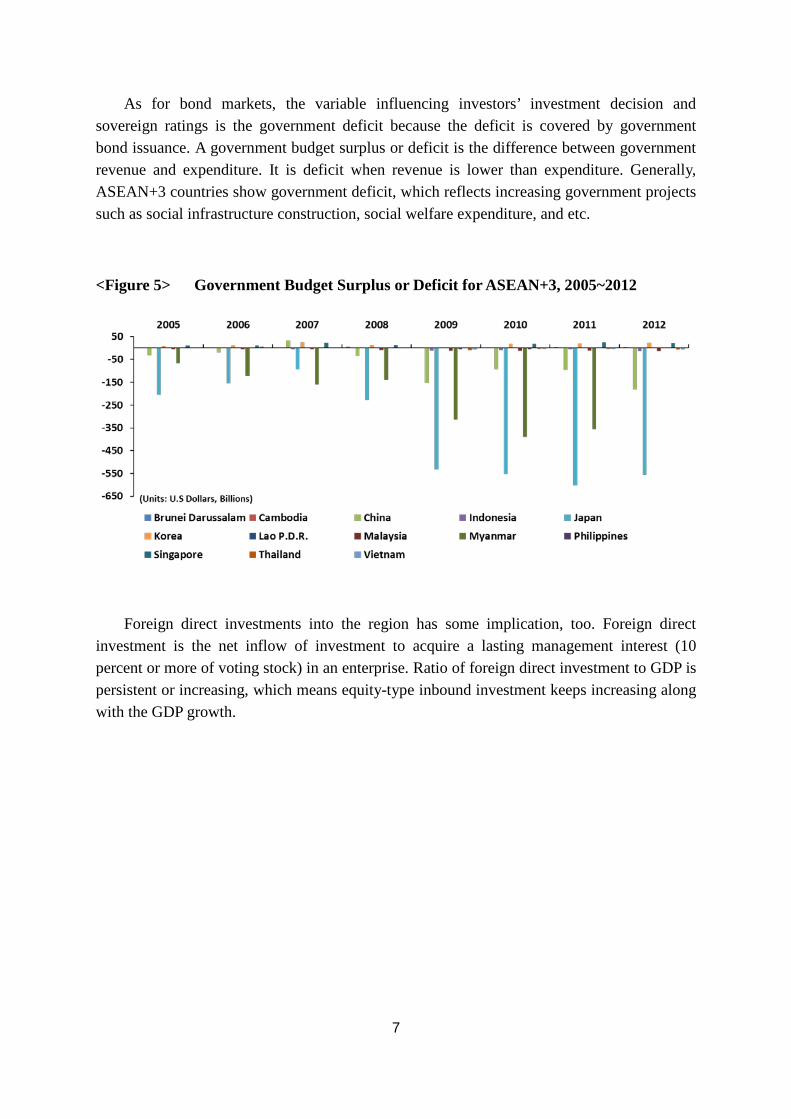

As for bond markets, the variable influencing investors’ investment decision and sovereign ratings is the government deficit because the deficit is covered by government bond issuance. A government budget surplus or deficit is the difference between government revenue and expenditure. It is deficit when revenue is lower than expenditure. Generally, ASEAN+3 countries show government deficit, which reflects increasing government projects such as social infrastructure construction, social welfare expenditure, and etc.

<Figure 5> Government Budget Surplus or Deficit for ASEAN+3, 2005~2012

Foreign direct investments into the region has some implication, too. Foreign direct investment is the net inflow of investment to acquire a lasting management interest (10 percent or more of voting stock) in an enterprise. Ratio of foreign direct investment to GDP is persistent or increasing, which means equity-type inbound investment keeps increasing along with the GDP growth.

8

<Figure 6> Ratio of FDI to GDP of ASEAN+3, 2005~2012

<Figure 7> FDI into ASEAN+3, 2005~2012

In order to integrate or promote cooperation among ASEAN+3 countries, the differences of exchange rate management systems must be taken into account. Indonesia, Malaysia, and Thailand have independent floating. Malaysia, Vietnam and Myanmar have a pegged system. Singapore, Cambodia and Lao PDR have managed floating systems.

9

2. Financial Structure in ASEAN countries

According to ASEAN financial markets with the total asset composition in 2009, which are bond per GDP, stock market capitalization per GDP, and bank assets per GDP, the banking industry is the core of the financial system except Singapore.

<Figure 8> ASEAN Countries’ Financial Structures (Percent of GDP), 2009

To guess potential investors in the ASEAN Capital markets, gross national savings (GNS) and GDP per capital are examined. While Cambodia has a GNS below 20 percent, ASEAN countries have high to moderate potential to increase capital accumulation. GDP per capita among ASEAN countries are relatively low to the western advanced countries and there are wide gaps in there, too. Since GDP per capital has a high correlation with the development of the capital markets, so far capital markets in the region has a lot of room to improve.

10

<Table 2> Gross National Savings in ASEAN Countries, 2010

Countries 2010 Cambodia 13.431

China 52.229 Indonesia 33.041

Japan 23.536 Korea 32.423

Malaysia 34.231 Myanmar 23.143

Philippines 25.011 Singapore 48.185 Thailand 29.078 Vietnam 31.614

<Table 3> GDP per Capital ASEAN Countries

Countries 2010 Brunei Darussalam 31,981.87

Cambodia 752.677 China 4,422.66

Indonesia 2,985.77 Lao P.D.R. 1,071.77 Malaysia 8,658.67 Myanmar 811.084

Philippines 2,155.41 Thailand 4,740.33 Vietnam 1,297.85

IV. SWOT analysis of ASEAN+3 Stock Markets

1. Stock markets and Economic Development

Stock exchanges make it possible to trade ownership rights in firms. The creation of well functioning stock exchange can lower the costs of exchanging ownership rights in firms. Therefore, investors can easily invest to the firms which want to increase physical capital. With this physical capital, firms can expand products or services and start new business. If there is no stock market in the developed counties, a lot of companies would become cash constrained. So, economic efficiency could be increased when stock market is functioned well.

11

ASEAN+3 countries are fast developing or developed countries which would like to grow economy more. Therefore, stock market should be one of the most important institutions in their economic system in order for domestic firms to raise money from investors.

On the other hand, stock market infrastructure facilitates the clearing, settlement, and recording of stock and stock related transactions. Therefore, it can play a critical role in fostering stock market stability. If it is not properly managed, they can pose significant risks to the financial system and give negative effect on real economy.

In this section, we would like to examine and evaluate the current status of stock market in ASEAN+3 countries by SWOT analysis. Since the degree of development of Stock market in ASEAN+3 countries is very different, it is hard to compare the stock market infrastructure between ASEAN+3 and other region of the world. Therefore, as the strong and the weak components, we evaluate which part of infrastructure is developed well and which part is not developed. As the opportunity and the threat components, we look for which part can expect to positively affect the stock market and stock market infrastructure in the future or negatively affect them in the future.

2. Strengths in ASEAN+3 Stock Markets

Efficiency improvement of stock exchange

Most of ASEAN+3 countries have tried to improve efficiency of stock exchange. First, some stock exchanges have tried to improve efficiency by merging. For example, Tokyo Exchange(TSE) and Osaka exchange(OSE) in Japan merged to form Japan Exchange(JPX) group in 2013. By merger, JPX can improve their operational efficiency by restructuring duplicative IT or managerial systems. Furthermore, since TSE was not a listed company but OSE was a listed company, TSE had relatively bureaucratic culture while OSE was not bureaucratic but more active and market oriented. So, it is expected that culture of TSE will become more market oriented and increase efficiency in work. By the way, the exchanges’ operational stability will be also improved because JPX now operate well both cash equities trading and derivatives trading. Before merger, TSE was a comparative advantage in cash equities trading and OSE was a comparative advantage in derivatives trading.

In addition to Japan, it is known that, in Philippine, Philippine stock exchange(PSE) and the Philippine Dealing System start to discuss to merger and in Vietnam, Hanoi Stock exchange and Hochimin stock exchange(HOSE) discuss to merger.

12

<Table 4> ASEAN+3 Stock Exchanges

Stock Exchange Market

Capitalization (Million USD)

Number of listed company

Turnover ratio (%)

Indonesia IDX 396,772.1 459 23.3

Malaysia Bursa Malaysia 476,340.0 921 28.6

Singapore SGX 414,125.8 472 43.3

Thailand SET 382,999.1 502 70.4

Philippines PSE 264,142.9 268 16.2

Lao PDR LSX 1.0 3

Cambodia CSX 58.5 1

Vietnam HOSE HNX 32,933.1 311 13.2

Japan JPX

Nagoya Sapporo Fukuoka

3,680,982.1 3,470 99.8

China SSE SZSE 3,697,376.0 2,494 164.4

Korea KRX 1,180,473.4 1,767 139.2

Brunei Darussalam - - - -

Myanmar - - - - Note : based on end of 2012, but Cambodia is based on end 2013

On the other hand, Korea Stock Exchange(KRX) had a monopoly power and relatively bureaucratic culture. So, in order to increase competitiveness, Korean government allows creating alternative trading system. Alternative trading system is expected to lower trading cost and ensure best execution.

Electronic trading and Procession development

ASEAN developing countries, recently, launched more upgraded IT system which can speed up and stabilize the execution of trades. For example, in 2011, PSE launched PSETrade which can improve the ability to handle more transactions and give the Exchange the foundation for product portfolio expansion.

Indonesia upgraded their Stock Exchange trading system with completing in 2005-2009 Master Plan. In 2009, JATS-NextG was launched. Through this system, not only the ability to process securities improved, but also Indonesian stock exchange can have the ability to trade all financial products including stocks, derivatives and mutual funds in a single platform.

Bursa Malaysia Bhd is also launching BTS2 in this year. This new system is 1,000 times faster in order/trade execution, 10 times higher trade processing capacity. Therefore, some

13

functions such as dynamic limits and stop market and limit order will be possible in this system.

Tick size reduction

A couple of countries have tried to adjust a tick size to revitalize the stock market. Japan TSX reduced a tick size to fall in transaction costs and promote trading activities. In addition to Japan, the The Stock Exchange of Thailand(SET) also implemented tick size reduction on stock below THB 25. Recent empirical study showed that tick size reduction in SET led to a decline in spreads and quotes while having no significant impact on trading volume.

<Table 5> Proposed Tick Size Reductions*

current Stage I (3Q 08) Stage 2 (2H 09)

Price

Below

Tick

Size Min Max

Tick

Size Min Max

%chg

Tick

Size Min Max

%chg

(JPY) (JPY) (bps) (bps) (JPY) (bps) (bps) (JPY) (bps) (bps)

2,000 1 5.0 10,000.0 1 5.0 10,000.0 0% 1 5.0 10,000.0 0%

3,000 5 16.7 25.0 5 16.7 25.0 0% 1 3.3 5.0 -80%

5,000 10 20.0 33.3 10 20.0 33.3 0% 5 10.0 16.7 -50%

30,000 10 3.3 20.0 10 3.3 20.0 0% 10 3.3 20.0 0%

50,000 50 10.0 16.7 50 10.0 16.7 0% 50 10.0 16.7 0%

100,000 100 10.0 20.0 100 10.0 20.0 0% 100 10.0 20.0 0%

300,000 1,000 33.3 100.0 100 3.3 10.0 -90% 100 3.3 10.0 0%

500,000 1,000 20.0 33.3 1,000 20.0 33.3 0% 500 10.0 16.7 -50%

1,000,000 1,000 10.0 20.0 1,000 10.0 20.0 0% 1,000 10.0 20.0 0%

3,000,000 10,000 33.. 100.0 1,000 3.3 10.0 -90% 1,000 3.3 10.0 0%

5,000,000 10,000 20.0 33.3 10,000 20.0 33.3 0% 5,000 10.0 16.7 -50%

20,000,000 10,000 5.0 20.0 10,000 5.0 20.0 0% 10,000 5.0 20.0 0%

30,000,000 50,000 16.7 25.0 50,000 16.7 25.0 0% 50,000 16.7 25.0 0%

50,000,000 100,000 20.0 33.3 100,000 20.0 33.3 0% 100,000 20.0 33.3 0%

*As announced by Tokyo Stock Exchange (29 Jan 2008) Source: Deutsche bank

14

Trading system stability enhancement comparable to the global standards

In some countries, regulator have adopted global standard of regulation for HF, Algorithmic trading and so on. For example, the Hong Kong Securities and Futures Commission (SFC) launches new requirements to regulate Algorithmic traders, the service providers of internet trading and direct market access from 2014. New requirements are related to responsibility for orders sent to the market through an electronic trading system, management and supervision of the design, development, deployment and operation of the electronic trading system, adequacy of system, record keeping and so on. By amended Code of Conduct and Fund manager Code of conduct, the monitoring and supervision for their clients’ trading activities and the electronic platforms themselves has been strengthened.

Furthermore, in case of Laos, even though its securities market established three years ago and the size of market is small, the legal framework has been structured to be complied with IOSCO principles and market infrastructure such as IT system of the exchange is using international standard.

Risk management enhancement

The stability of stock market infrastructure has been improved as the securities and risk management forced to strengthen especially after global financial crisis. In Hong Kong, regulator increased in clearing participants’ financial contributions, depending on their overall positions. Regulators actually revised certain price movement assumptions and counterparty default assumption in the stress testing as well as introduced a standard margin system and a Dynamic Guarantee Fund in the cash market at Hong Kong Securities Clearing Company Limited (HKSCC).

On the other hand, Singapore Exchange Limited (SGX) introduced margining of securities transactions cleared by members of the Central Depository Pte Limited(CDP), replacing the previous practice of maintaining a clearing fund to cover any losses. SGX also enhanced the clearing houses transparency. Specifically, SGX increased transparency on matters relating to its risk management processes and systems to enable participants to gain a greater understanding of their respective risk exposures to the clearing houses. For the market activities perspective, SGX tagged of securities orders which involve short selling in order to further enhance transparency of market activities. Daily reports on the total value and volume of short sales for each counter will be published.

In Indonesia, regulators has developed scheme to protect investors and customers. PT KSEI developed a system that monitored customer funds and securities in securities companies. In this system, customers would be able to monitor their assets of funds and securities in real time. In addition, an Investor Fund in Bapepam-LK was established for investor protection.

15

Cooperation among member countries’ infrastructure

ASEAN countries have been trying to integrate their stock market actively. In 2011, the ASEAN Central Bank Governors adopted the ASEAN Financial Integration Framework (AFIF) to provide a general approach to the liberalization and integration initiatives under the ASEAN Economic Community(AEC). Some of countries already accomplished a couple of step of integration. Bursa Malaysia, SGX and SET connected on the ASEAN Trading Link. Through this link, cross-border trades are transacted through local brokers via the main platforms developed by the exchanges. It is also known that PSE has a plan to join the link and the Ho Chi Minh City Stock Exchange (HOSE) discusses its potential for Vietnam.

On the other hand, In ASEAN+3, well developed Stock exchanges have supported other countries to open up their new stock exchange, upgrade IT system and so on. For example, KRX have worked six ASEAN countries stock exchanges together. Japan Exchange Group and Daiwa Securities Group are now assisting to start a stock exchange for Myanmar. Myanmar has a plan to set up a security exchange by 2015.

16

<Table 6> Examples of implementation of KRX’s global strategy

Country Partners Form of

collaboration Overview

Thailand Stock Exchange of Thailand(SET)

IT systems, etc.

Renewal of memorandum of understanding aiming to extend cooperation between both exchanges in exchanges in exchanging information, improving IT structure, and promoting collaborative investment and business opportunities (June 2012)

Malaysia Bursa Malaysia(BM) IT systems

Installation of bond trading system at both first and second stage (completed in March 2008 and January2009, respectively) Installation of market maker monitoring system (completed in April 2009) Development of Islam product trading (BCH) system (completed in August 2009)

Malaysia Bursa Malaysia(BM) IT systems

Development and rollout of derivative securities settlement system in conjunction with Burs a Malaysia and the CME Group (February 2012). System enables real*time risk management and real-time monitoring of market participants’ exposure.

Philippines Philippine Stock Exchange(PSE)

IT systems

Plan to roll out stock trading and market monitoring systems (as of 2011) KRX developed Total Market Surveillance (TMS) system introduced by Capital Markets Integrity Corporation (CMIC), a unit of the Philippines Stock Exchange, in May 2012.

Vietnam

HoChiMinh City Stock Exchange(HOSE) Hanoi Stock Exchange

IT systems

KRX selected by Vietnamese government as preferred bidder for project to build state-of-the-art trading system (October 2009). Scope of project includes development of 13 equity-related systems (for trading, market research, disclosure, data sharing, clearing, settlement, etc.) and their installation on the country’s two stock exchanges.

Cambodia Cambodian Minstry of Economy and Finance

Establishment and operation

of stock exchange

Establishment and operation of Cambodia Securities Exchange as a joint venture.

Laos Bank of the Lao PDR

Establishment and operation

of stock exchange

Establishment and operation of Lao Securities Exchange as a joint venture.

17

3. Weaknesses in ASEAN+3 Stock Markets

Structural Weakness

First, there are some countries which start stock market recently and the numbers of securities are still small. For example, Brunei Darussalam has only one market player or financial institution offering over-the-counter purchases and selling of company stocks/shares in the stock market. There are three listed companies in Lao Stock Exchanges and one listed company in Cambodia Stock exchange. This might be because most of enterprises are still in its first generation of conducting business and lack of experience in applying corporate governance principles.

Second, some stock exchanges need to develop more credible Business Continuity Plan (BCP) for market players. Whether threats can arise from internal or external factors, a credible BCP will enable the industry to manage risks related to abnormal business processes that are caused by disruptions to the internal infrastructure.

Third, since those market are in the early stage, not only capital market infrastructure but also capital market products are very limited.

Fourth, a couple of stock exchanges in ASEAN countries have not implemented upon demutualization. According to Islam and Islam(2011), a shift from not-for-profit mutual organization to for-profit organization with ownership separated from access to trading may allow the exchange to respond more effectively to competitive pressure and to act separately from the interests of individual members thereby creating a more streamlined and market-oriented exchange. They suggest the advantages of demutualization as follows. First, mutual exchanges often lack focused strategic goals and business purposes and tend not to have clear accountability. Moreover, it is hard to build a consensus among members. However, profit organizations for which creating shareholder value would not because they have to be concerned about exchange’s interests as a whole. They also criticize the governance structure of a mutual exchange because usually listed companies and investors, whose participation is crucial to a successful market, have no role unless appointed as “public” or “independent” members of the board of directors. However, a corporate governance structure of demutualised exchanges is far more effective in managing conflicts among market participants. In addition, demutualised exchanges can use their stock as currency in acquisitions and mergers and to facilitate strategic alliances. Stock option and purchase plans can also be significant compensation mechanisms for management and staff. Recently, demutualization in Hong Kong and Singapore facilitated the merger of stock and futures exchanges. So far, stock exchanges in Thailand, Vietnam and so on has not been demutualized yet. Demutualization cannot be the one of best solution for development of stock exchange. However, if self regulation and sound governance are well accomplished,

18

demutualization will be needed to increase efficiency of stock exchange.

Insufficient infrastructure of integration

The one of ultimate vision of the member countries is to integrate their stock market. As mentioned, ASEAN already started first step to integrate their market. However, compared with Europe which was already integrated, many infrastructures are still needed in ASEAN+3 countries. For example, in Europe, some Central Counterparties (CCP) has already started to interoperate and some Central Securities Depositories (CSD) operates cross-CSD links. However, ASEAN securities trading and post-trade infrastructure developments, so far, have limited in geographical boundaries. There are currently no infrastructure links existing between any of the ASEAN CSDs or CCPs.

<Table 7> ASEAN Vertical clearing and settlement structure for equity securities

Indonesia Malaysia Philippines Singapore Thailand Vietnam

(HNX)

Vietnam

(HOSE)

Trading Indonesia Stock Exchange (IDX)

Bursa Malaysia (BM)

Philippine Stock Exchange (PSE)

Singapore Exchange (SGX) Stock

Exchange of Thailand (SET)

Hanoi Stock Exchange (HNX)

Ho Chi Minh Stock Exchange (HOSE)

Matching Kustodian Sentral Efek Indonesia (KSEI) Bursa

Malaysia Securities Clearing (BMSC)

Philippine Depository& Trust Corporation (PDTC)

Central Depository (CDP)

Vietnam Securities Depository (VSD)

Vietnam Securities Depository (VSD)

Clearing Kliring Penjaminan Efek Indonesia (KPEI)

Securities Clearing Corporation of the Philippines (SCCP)

Thailand Clearing House(TCH)

Securities

Settlement

Kustodian Sentral Efek Indonesia (KSEI)

Bursa Malaysia Depository (BMD)

Philippine Depository& Trust Corporation (PDTC)

Source: Deutsche Bank(2013)

19

Lack of human capital

Most governments in ASEAN countries are eager to develop the stock market more rapidly. So, they increase their investment to expand market infrastructure and try to establish better regulatory framework. However, one of obstacles is that the human capital for stock market is insufficient. In our survey, Thailand evaluates that lack of local expertise in the capital markets industry forces a lot of activities being outsource. Brunei Darussalam also evaluate that there are lack of suitable directors and managements as well as, lack of human resources in term of management technique, marketing and international law. On the other hand, Korea want to develop their capital market as international financial center but human capital of Korea who can play an important role in the international financial market is really limited. Since human capital cannot accumulate in a short time, there is a risk that new infrastructure or regulatory framework may not establish or work efficiently.

4. Opportunities in ASEAN+3 Stock Markets

Competitive macroeconomic environment

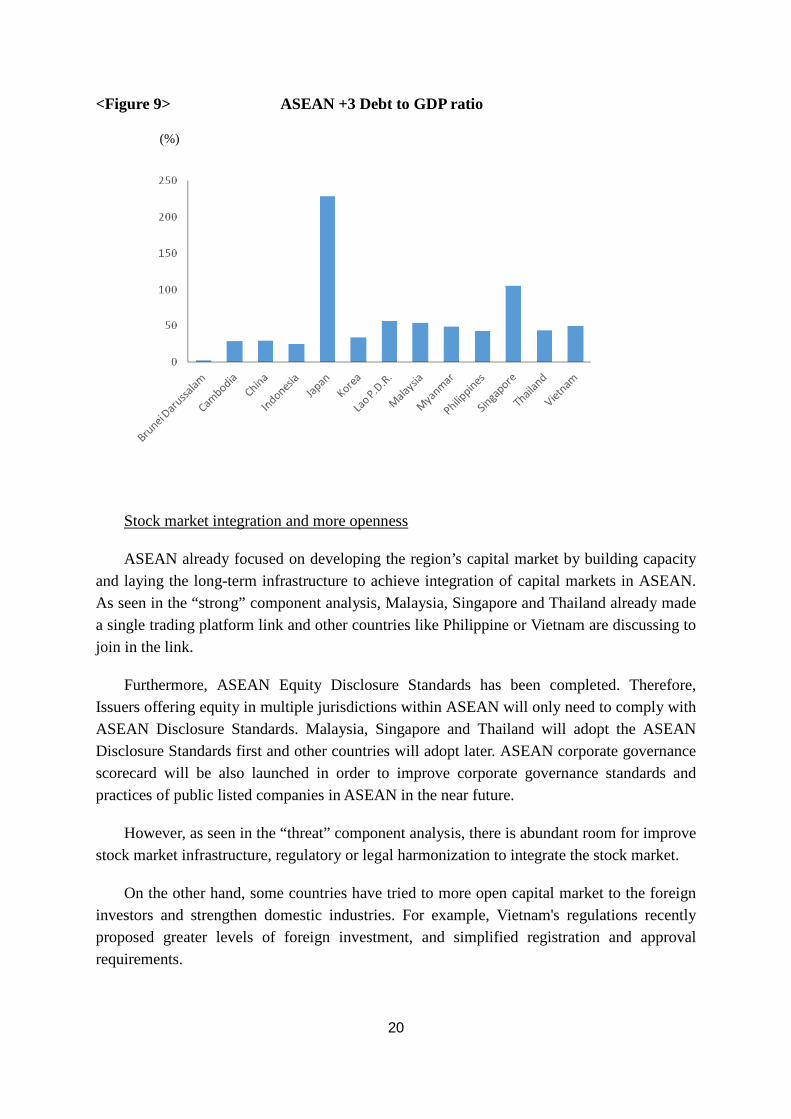

Macroeconomic potential and stability is important for companies and investors in the stock market. As seen in the macroeconomic analysis, ASEAN+3 countries’ macroeconomic potential is favorable. ASEAN countries have recorded above 5% growth on average recent 3 years and expect to continue the solid growth trends. Furthermore, Debt to GDP ratio in most of ASEAN+3 countries are not high. Therefore, governments will be able to play a role in supporting the market-based economy by fiscal policy.

20

<Figure 9> ASEAN +3 Debt to GDP ratio

(%)

Stock market integration and more openness

ASEAN already focused on developing the region’s capital market by building capacity and laying the long-term infrastructure to achieve integration of capital markets in ASEAN. As seen in the “strong” component analysis, Malaysia, Singapore and Thailand already made a single trading platform link and other countries like Philippine or Vietnam are discussing to join in the link.

Furthermore, ASEAN Equity Disclosure Standards has been completed. Therefore, Issuers offering equity in multiple jurisdictions within ASEAN will only need to comply with ASEAN Disclosure Standards. Malaysia, Singapore and Thailand will adopt the ASEAN Disclosure Standards first and other countries will adopt later. ASEAN corporate governance scorecard will be also launched in order to improve corporate governance standards and practices of public listed companies in ASEAN in the near future.

However, as seen in the “threat” component analysis, there is abundant room for improve stock market infrastructure, regulatory or legal harmonization to integrate the stock market.

On the other hand, some countries have tried to more open capital market to the foreign investors and strengthen domestic industries. For example, Vietnam's regulations recently proposed greater levels of foreign investment, and simplified registration and approval requirements.

21

<Table 8> Comparison between the Current Law and Draft Law in relation to the limits

on foreign ownership

Current Law Draft Law

Any foreign investor and its affiliates, not being a

foreign credit institution or foreign strategic investor-

5per cent

Any foreign credit institution and its affiliates-10

per cent

Any strategic investor and its affiliates-10percent(or

20per cent with Prime Ministerial approval)

Total level of shareholding of all foreign investors

and their affiliates-30 per cent

Any foreign individual-5 per cent

Any foreign organisation-15 per cent

Any foreign strategic investor-20 per cent

Total level of shareholding of all foreign investors

and their affiliates-30per cent (can be increased by the

Prime Minister in special cases of restructuring of

weak credit institutions.)

Potential IPO companies or investors

It is hard to evaluate potential IPO companies or investors but most of ASEAN developing countries would have many potential IPO companies or investors. According to SEADI(2013), based on group discussion and in-depth-interview, one of main strengths of Indonesia is many potential investors and companies to be listed in the capital market. Despite having the largest population among ASEAN countries, Indonesia has few investors in the capital market in comparison—only about 200,000 investors. But with sustained economic growth, the size of the middle class is expected to grow, and growth in the Indonesian middle class will eventually increase the number of investors. Despite the large number of eligible companies, only 440 firms had gone public in Indonesia by 2011. Interviewers expect that the number of companies that can go public is significantly higher. It is expected that most of high macro growth ASEAN countries would be in the similar situation.

5. Threats in ASEAN+3 Stock Markets

A Fragile Dependence on Foreign Capital

Asian countries tend to export safe capital while import risk capital. And imported risk capital would outflow in a short time if there is internal or external crisis. Asian countries already learned lessons from Asian financial crisis and global financial crisis. Several new financial policies have been implemented. However, most of ASEAN counties are still

22

vulnerable to volatile capital flows. In order to avoid this vulnerability, Capital markets should be more deepening and broadening. Corporate governance and transparency should be more improved and regulatory and supervisory frameworks should be more strengthened. However, most of market are still small and has narrow investor base with lacking institutional investors.

Low economic freedom

Economic freedom would be important to attract the cross border investment. However, according to Kiseleva(2012), there is huge gap of economic freedom between ASEAN + 3 countries. Especially, the widest gap among the ASEAN+3 countries is on the investment freedom. Singapore and Hong Kong was ranked first and second while most of countries are out of 50th. He said that all of the ASEAN + 3 countries needs to enhance the conditions for cross border investments. If not, the existing gap in the investment attractiveness may grow rapidly with increasing ineqqality and disproportions in the ASEAN.

<Table 9> The ASEAN+3 scoring of economic freedom in 2010

LABOR

FREEDOM MONETARY FREEDOM

INVESTMENT FREEDOM

world rank

regional rank

Brunei Darussalam NA NA NA NA NA

Cambodia 43.6 70.5 60 107 18

China 53.2 70.6 20 140 31

Hong Kong SAR, China 87.4 83.1 90 1 1

Indonesia 50.8 70.8 35 114 21

Japan 82.4 88.8 60 19 5

Korea, Rep 47.1 77.4 70 31 8

Lao PDR 58.9 73.5 20(*) 138 30

Malaysia 71.4 76.7 30 59 9

Myanmar NA NA NA NA NA

Philippines 51.9 72.7 40 109 20

Singapore 98.9 80.9 75 2 2

Thailand 73.6 40 70(*) 66 10

Vietnam 68.4 58.1 20 144 33

23

Politically, unclear issues for integration

Not only stock market infrastructure, there are many unclear issues to integrate the stock market in ASEAN countries. They will be the presence of capital controls, exchange restrictions, differences in tax regimes, uneven development, portfolio restrictions on institutional investors, differences in product range, large differences in regulatory regimes, and differences in corporate governance standards. For example, corporate disclosure regulations differ between countries. While listed companies in the Philippines, Singapore, Thailand, and Malaysia have to effectively disclose holdings of 5% and more, there is no such requirement in Indonesia. However, although investors in Indonesian stocks have strong pre-emption rights, investors in Malaysia, the Philippines, Singapore, or Thailand have not. Iif they cannot control properly, it will negatively affect on the whole market.

V. Bond Markets of ASEAN+3

1. Bond Markets and Economic Development

Since bond markets are a part of financial system, we can justify reasons of bond market development in the context of efficient financial markets’ benefits. Efficient financial markets promote efficient fund flow from saving to investment, which contributes to economic growth and living standard improvement. To elaborate, bond markets are merited in risk-sharing and risk-shedding in economies. And bond markets are more appropriate for financing large investment projects than bank financing because such projects tend to be risky and take time before they yield returns. Bond markets can spread these risks over a large number of bond holders because bonds can be traded allowing investors to transfer the risks to others even before the projects are completed. As ASEAN+3 countries develop, many large projects, such as social infrastructure construction, need funding. This is a reason that ASEAN+3 countries want better bond markets.

And on the supply side of funds, bonds are better accessible to foreign investors than simple bank deposits or bilateral lending contracts. Considering deficient saving in countries, funds inflow from the foreign investors are important source of ASEAN+3’s development projects; bond markets are convenient vehicles to the foreign investors. In addition, ASEAN+3 countries need alternative channel in case that the banks encountered difficulty. Currently, the countries are too bank-centric. For example, short-term borrowing from foreign investors suffers from a double mismatch, which is maturity and currency mismatch. To this problem, ideally, longer-term domestic currency denominated bond issues can lessen the both

24

mismatches. And there is an advantage that firms could reduce their dependence on foreign capital markets abroad.

2. Strengths in ASEAN+3 Bond Markets

Strong Policy Initiatives

ASEAN+3 countries put considerable efforts into developing their domestic bond markets. For example, the Philippines launched an inter-dealer platform to encourage exchange trading of fixed income securities. Malaysia established Foreign Exchange Administration rules of no withholding tax, no capital gains tax, and no restrictions on investing in Malaysian ringgit bonds. Notably, Malaysia’s market has been boosted by efforts to promote Islamic bonds. Singapore overcame its intrinsic narrow issuer base by encouraging overseas firms to issue in the local currency market.

In the region, when bond markets exist, Central Clearing Counterparties (CCPs) exist in the form of markets operated by the regular exchanges, which are tightly monitored or affected by government policies or regulation authorities. However, in the region, majority of bond trading takes place OTC and settles on a bilateral basis without the intervention of a CCP. This is a weakness in the region.

<Table 10> Recent Policy Changes on Bond Markets of ASEAN+3

Disclosure Rules Comparable to the Global Standards

ASEAN countries fare well on disclosure requirements with international best practices. But in the context of enforcement of regulations, there is room to improve. [Examples will be added here]

Advancing Roles of Information Providers

The countries in the region are strengthening the oversight of important information providers, such as credit rating agencies (CRAs) and external auditors. This is where the region as a whole go along well compared to international best practices. [Integrated CRAs will be added here]

25

<Table 11> CRAs of ASEAN+3

3. Weaknesses in ASEAN+3 Bond Markets

Structural Weakness

First, ASEAN countries’ bond markets are small-sized. ASEAN+3 excluding +3 countries, bond markets have not grown relative to GDP, roughly 50 percent of regional GDP stagnating in the emerging markets bond universe.

Second, corporate bond markets are even weaker and the small bonds markets are highly concentrated on the government bonds. Big portion of local currency bonds (around 35% of GDP) are issued by government not private corporates. For the past decade, budget deficits remained low and there is no need for extra expansion. Corporate firms seem to have no strong reason to expand their issuance, either.

<Figure 10> Corporate Bonds vs. Government Bonds

Third, investor base for the regional bond markets expanded but still risk-averse. Actually ASEAN+3 domestic investor base expanded considerably. In Indonesia, the Philippines, and Thailand, the assets of pension funds are hovering around 10 percent of GDP. While Malaysia and Singapore have are relatively high amount of pension funds by emerging market standards, they have not shown any trend growth. But we can find fast increasing trends of domestic mutual funds. Mutual funds, insurance companies and banks are relatively conservative investors and are buy-and-hold strategists rather than active managers.

Forth, macroeconomic investment is staggering and corporates prefer to using the equity markets. During the early 1990s, investment in macroeconomics reached 40% percent of GDP in many ASEAN+3 countries. It keeps falling during the recent decade. In the Philippines and Malaysia the trends were even worse, reaching around 15~20 % of GDP during the mid-2000s. Low investment incentives due to lower returns, greater uncertainty, and failure of finding new business opportunities discouraged corporate bond issuance. At the same time investors became more cautious in extending funds to businesses, as perception of business deterioration. That is, causation went both ways resulting in the vicious cycles.

And another reason is that firms found alternative ways to fund their investment projects, which are internal cash reserves and equity financing. In the post-Asian crisis, survived firms

26

made better profits, and were able to fund their projects from their own internal cash. At the same time, industrial structures changed because of the Asian crisis. Manufacturing industry survived rather than construction whose projects are better fit for the bond funding. At the same time, firms’ financing preferences changed. Teranishi, Fukuda, and Liu (2007) found that companies from Thailand, Malaysia and Indonesia rely for their long-term funding much more heavily on equity finance and much less on banks and potentially bond issuance as well. ASEAN+3 countries show that equities account for nearly two-thirds of corporate domestic financing with bank borrowing and bonds splitting the remainder.

Foreign Investors Prefer Equities and Government Bonds to Corporate Bonds

<Figure 11> Foreign Investors’ Stock Investment and Bond Investment

Majority of Bonds are Traded OTC rather than via CCP

Even though Central Clearing Counterparties (CCPs) exist in the form of markets operated by the regular exchanges, majority of bond trading takes place OTC and settles on a bilateral basis without the intervention of a CCP. This is a weakness in the region.

<Table 12> Bond CCP of ASEAN+3 Countries

Room to Improve on Information Providers

Singapore have yet to implement registration obligation for CRAs, as required by the International Organization of Securities Commissions (IOSCO). External auditors of issuers should be subject to oversight by a publicly reputable independent entity such as the securities regulator. It is good that many of the countries are strengthening such systems of independent oversight as the IOSCO principles now require. In Thailand, the SEC is in the process of establishing an effective supervisory model of independent oversight. In Malaysia, a law approved in 2009 created the Auditor Oversight Board, which began operations in April 2010. Such boards have proven to be useful in assisting securities regulators to oversee external auditors.

27

Underdeveloped Derivatives Markets

Despite relatively well-developed securities infrastructure, the countries show considerable variation in derivatives and repo markets related with bonds or interest rate products. In Singapore, interest rate swaps, interest rate futures and bond futures markets provide vehicles for bond investors to hedge their interest rate risks. In many other countries, suitable derivatives are absent and so investors engage in more costly cash transactions to replicate hedge positions or leave their position risks not managed properly.

Even with considerable growth over the recent past, local derivatives markets are generally underdeveloped in the countries, with exception of Singapore, and Plus-Three countries. The development of derivatives and bond markets affect each other positively by virtuous cycle. So derivatives market initiatives should be considered simultaneously with the bond market policy initiatives. Since derivatives markets are also tightly related with the efficient cash management market, short-term cash markets are to be in the processes, too.

4. Opportunities in ASEAN+3 Bond Markets

Expansion of Foreign Investment and Domestic Investment

Foreign investors are eager to expand their investments in ASEAN+3 local fixed incomes. Foreign participation can improve the cultures of regional bond markets as well as contributing to ample liquidity and efficient price discovery. Foreign investors frequently exert pressure for more transparency which reduces price volatility because it improves the quality and increases the frequency of information. Such changes reduce the risk that there will be sudden disclosures of accumulated negative news. So it attenuates the price impact because it broadens what would otherwise have been a thinner market.

Attracting foreign issuance supply into the region is another possible opportunity. For example, middle-Asian supply and demand for the bonds can be imagined to be incubated into ASEAN+13 countries. Malaysia’s experience plus Singapore policy version can be put together for this. In addition, Singapore experiences tells important things. Currently member countries’ firms are reluctant to issue corporate bonds for many reasons, which is a part of the vicious cycle on bond markets. Inbound issuance can break the cycle. Once the vicious cycle is cut, people can expect good scenario, virtuous circle.

Investor base is likely to expand in both domestic and foreign investors. Responding to these, pro-active policies are needed to smooth the development path and minimize the market risks such as market volatility. Rapid growth of contractual savings schemes, such as pension funds will encourage demand for long-term domestic currency bonds. In turn, firms

28

respond by issuing more bonds.

The Recent Global Crisis is Not that Bad

The recent global financial crisis was a good opportunity showing potential possibility of corporate bonds in ASEAN+3 countries. The countries’ corporates typically do not rely much on bond issuance for funding. But right after the most severe financial circumstances, the corporates used bond issuance and the investors responded to the demands. The bond markets adjusted faster than bank credits.

Consolidation and Standardization of Depository and Settlement Systems

Some consolidation and standardization of depository and settlement systems at the local level would increase market efficiency. A central securities depository (CSD) promotes efficiency by reducing the number securities accounts and connections required by an investor or trader and economizes on the cash settlement leg. Thailand has a book entry system for both government and corporate bonds that is centralized ina single CSD. And Malaysia has CSD which captures unlisted bonds issued by both the government and corporates. Thus, some of the countries could explore further consolidation of book-entry systems. In addition, the Philippines could consider strengthening key legal concepts in clearing and settlement such as finality, novation, and netting by embedding these in the legal framework rather than only in regulations.

Some standardization of market infrastructure across ASEAN+3 would help promote intra-regional intermediation. Currently each country has its own market infrastructure and no effective linkages have been established with infrastructures of other countries. For example, none of the CSDs has linkages to the others. Furthermore, only in the cases of Malaysia and Singapore does the local CSD have links with international CSDs. Linkages of market infrastructures will decrease transaction costs and encourage mutual investment in the region. For the linkage, Asian International CSD (ICSD) versus simple connection of independent CSDs can be considered.

Asian International CCP is an alternative way to realize CCP in the region. While the benefits of a CCP in terms of management of counterparty risk are very clear, the costs of implementing it are significant. CCPs have sizable fixed costs that are characterized by economies of scale that is a minimum settlement volume is needed to make them economically feasible. In each domestic market which does not have CCP in the ASEAN+3, such cost factors might outweigh the benefits. Thus when considering a regional International CSD, it is useful to consider the implementation of a regional International CCP at the same time.

29

Unified Information from Information Providers

Promoting the comparability of ratings across countries will strengthen the investors’ credibility encouraging the regional cross-border investment. While there are local rating agencies in each jurisdiction, they all use different rating scales and methodologies, which hinders the comparability of ratings across countries. And domestic rating agencies have yet to build a track record to retain international reputation. The authorities of countries could encourage the adoption of a common regional methodology and rating scale, which would provide one more building block to regional integration by making investments across the regional markets easier to compare by investors. In this context, it is a good idea to analyze benefits of establishing a regional credit rating agency.

5. Threats and Challenges in ASEAN+3 Bond Markets

Speculative Grade Bonds and Commercial Papers

Current bond markets tend to alienate SMEs, which many need a diversity of funding sources, relatively to the famous large companies. The SMEs are future growth engine to economies, and the synergies and benefits from their development are shared among participants in the economy. So, governments are to step in to help SMEs considering the future positive externalities. Enhancing and promoting the speculative corporate bond markets are needed.

Commercial papers (CP) in the region is widely used just like the corporate bonds. But the regulations are not comparable with those of corporate bonds. This can cause regulation arbitrage damaging market transparency and credibility.

Bond markets in the Crisis and Foreign Investment

Bond markets should work when they are needed most, that is, in the crisis. Around the periods of the recent global crisis, bond markets played as spare tires in the economies and were faster than banking intermediaries. In the last quarter of 2008 and the first quarter of 2009, when the crisis was at its peak, markets effectively shut down. While bond finance came back more quickly than bank finance, making bond markets function faster in the crisis is a challenge to the member countries.

The issue is also related with the foreign investors in the region. The bond markets in the region relay on foreign investment with respect to markets’ liquidity and price discovery. This makes the regional bond markets very sensitive to the inflow and outflow of foreign

30

investment. As for the foreign fund flows, pro-active policy measures are needed especially to the monetary policies. ASEN+3 countries are familiar with the problems associated with the equity investment and bank lending from the foreign investors. But issues related with the bond markets are rather new to us. Inflows are mainly channeled into government bonds, which build up benchmark yield curves and their affects general shape of the yield curves. One of the issues is the flattening yield curves, which hinder long term capital markets. The second is the increased interest rate volatility. In order to tame it, well-functioning corresponding markets are needed such as interest rates derivatives markets. But it is not the case. So we suspect some distortions and inefficiencies in the interest rate markets.

Foreign Investment into Corporate Bonds

Issuing bonds denominated in domestic currency and convincing foreign investors to invest them are the most challenge to the ASEAN+3 countries. This phenomenon is occurring already in the government bond markets or their equivalents. However, we wish the tendency to be extended into the regional corporate bond markets. Prices of government bonds or risk free bonds benchmark the yield curves of the countries. And the corporate bonds are priced on the basis of the yield curves. If foreign investment is active only in the benchmark bonds and not in the corporate bonds, we suspect some distortions exist in the bond markets.

Regional Liquidity Providers

We need local or domestic institutional investors specialized in providing liquidity for bond markets and making price discovery efficient. Currently even Plus Three countries as well as ASEAN countries deeply rely on foreign participants for these. To enhance liquidity and price discovery in bond markets, we need diversity of preferences and views in the market. But most of the domestic institutional investors follow buy-and-hold strategies. This is a reason that the regional bond markets cannot neglect foreign investors and also a reason that regional special institutional investors who are very strong in liquidity providing, such as hedge funds.

Handling with Off-shore Activities.

The rise of foreign interest in ASEAN+3 bonds has another import threat, which is growing off-shore activities. Because there are impediments or costs to entering the onshore markets, foreign investors are increasingly obtaining exposure to emerging markets by offshore special vehicles such as non-deliverable forwards (NDFs) and credit-linked notes. Off-shore transactions fragment the regional markets and reduce liquidity on-shore, thereby

31

impairing price discovery. Over time, it may be beneficial to try to bring such markets onshore. One way to this is by reducing or eliminating withholding taxes.

Other challenges

Cross-border investors in the region would face an additional settlement risk even when the linkages among the infrastructures are established. In a cross-border transaction, settlement involves a foreign exchange settlement risk in addition to the settlement risk of the bond trade itself. Furthermore, timing difference between the securities and cash movements are also involved in the risk.

And, the “shadow banking” issues are potential to the region as the financial markets keep growing. So far, substantial maturity transformation and liquidity transformation via shadow banking instruments are observed in this region. In the recent global crisis, we could find that shadow banking sector, which is almost another name of sophisticated capital markets, was a threat to the whole economy if the appropriate safety nets are not imposed on the sector. This suggests that investors should only rely on the liquidity of money or capital market instruments to the extent that liquidity providers are in a position to meet any calls on liquidity in bad circumstances as well as in a good mood. This in turn requires appropriate regulation and supervision. For instance a pension fund required by its regulator to hold a certain proportion of cash assets should not treat a money market investment as equivalent to a bank deposit. Also, this characteristic is often not recognized to the retail investors (individuals). This makes the retail investors vulnerable to sudden disasters as Dong-Yang scandals in Korea. So the shadow banking regulations should tightly reflect financial consumer protection mechanisms in there.

VI. Implications and Concluding Remarks

ASEAN+3 countries have been working to develop capital markets in the region. ABMI, ASEAN exchange, and policy or regulation changes in each domestic market are examples. Thanks to the efforts, the capital markets have grown very rapidly; both stock and bond markets are around three times compared to the early 2000. Especially, in 2009 and 2010, after the 2008 global financial crisis, the outstanding of emerging East Asian local currency bonds grew 16.2% and 13.6% respectively, reaching $5.2 trillion in 2010. These shows that the capital markets can now function as another financial intermediary channels in the ASEAN+3 regions as well as the banking system. Now, the share of emerging East Asian stocks and bonds in the world’s total has reached around 20% and 8% in 2010 respectively.

32

ASEAN+3 capital market products have become an important asset class and cannot be overlooked by global investors, too.

This project is implemented to evaluate current status of fast growing capital markets in ASEAN+3 and to find clues for the development directions and future visions. The future directions should include cooperative development or integrated growth in the region. For the methodology for evaluating the current status, the SWOT analysis was employed.

The study focused on the capital infrastructures rather than such fundamental demand and supply of the capital markets as domestic large institutional investors, foreign investment, and etc. Improving capital market infrastructures offer a better playground for the market participants through more efficient capital markets. With this, development of capital market infrastructure leads to capital markets’ supply and demand additionally. For example, HTS (Home Trading Systems) made a diversity of individual investors participate in the capital market trading and CCP of the bond markets induced many kinds of investors into the markets through enhanced transparency and reduced counterparty risks. On the other way around, developed demand and supply in the capital markets request the advancement of capital market infrastructures. For example, as the investor’s trading technology evolves, demand for handling faster trading orders and finding better price discoveries across markets increased. Therefore, investors request to improve speed of trading infrastructures and establish information repositories or CCPs in the region to reduce the counterparties’ risks.

The capital market infrastructures are considered as policy variables because their development can be promoted by government or policy authorities’ efforts. Especially, in the ASEAN+3 regions, each country’s government implemented strong initiatives for the capital market infrastructure development. Therefore, with allowing different development stages of capital markets and economic growth of member countries, the efforts as a whole evaluated to be successful. Putting aside the countries without capital markets’ demand and supply, all the countries are equipped with electronic trading systems comparable with the Western advanced countries. The centralized securities depositories (CSDs) are established and trading information is gathered in information repositories or CSDs. As for bond markets, bonds are traded on the CCPs in some countries just as stock trading and if the trades are OTC, the clearing and settlement are implemented in CSDs. When considering that the OTC trades are more prevalent than exchange trades even in the Western advanced countries, less utilization of CCPs in bond markets is not a serious weakness in the region.

When excluding the issues of capital markets’ linkages among the member countries, it is hard to find any detrimental weaknesses in the each member country. Delay of demutualization or privatization of a couple of stock exchanges, small numbers of listed products and narrow range of listed sectors, weak enforcement of regulations to the bond market information providers and etc. are all weaknesses in the region. However, these are not at the devastating level to the capital markets but rather at the tolerable level in the development stage of each country. To the contrary, the linkages among the capital markets in

33

the region seem to have a lot of room to improve. Capital markets in the region are far less integrated compared to the trade linkages and supply chain network created in the region. This shows a serious imbalance between real sectors and financial sectors, which may leads to concentration of financial risks and inefficient risk management in the region. This imbalance is a systemic risk factor in the region.

The future opportunities of regional capital markets are found in the context of regional cooperation and integration of capital markets, as well as foreign investors from outside of the region. Of course, matured capital markets’ demand and supply stemming from the fundamental growth of each country will play a set of opportunities at the domestic level. However, the current circumstances that the many large projects and technology modernization of the region rely heavily on the foreign financial and technology investments imply that inter-regional cooperation and foreign relationship outside of the region will be vivid opportunities to the regional economies.

Likewise, challenges and threats of the regional capital markets are more related with the intra-regional cooperation or integration and foreign sectors outside of the region. These related factors are rather exogenous factors, which cannot be perfectly controlled by an individual country’s efforts. The exogeniety plays a double-edged sword in a view point of an individual country as it provides with chance for development but may increase market risk which individual government cannot control. For example, while enhancing cross-border trading in the region promotes efficiency of financial intermediation matching better saving and investment opportunities, the trading channel can also work as a contaminating or propagating route from an exogenous shock.

The following implications are inferred from the SWOT analysis. First, in the context of each country’s domestic perspective, the countries have to develop their own capital markets in concert with their own development stages. For example, if the credibility to the domestic currencies and banking systems are not high enough, it is utmost important to establish traditional and basic financial intermediation before the capital market development. For this, instituting sound electronic payment system, deposit insurance scheme and stabilizing domestic currency value are to be done far before the stock and bond markets. However, even in these cases, preparing primitive capital markets is required, too. It is not for attaining economic prosperity via capital market development, but because capital markets have to be working right at the times the markets are needed in the future. Therefore, to these countries, we suggest that the simple capital markets be set up and more importantly, the long-term road map of financial market development be prepared.

Second, in order to achieve the regional cooperation or integration of the capital markets, transferring technologies necessary to run capital market infrastructures (e.g. IT equipment, programming know-how) and sharing the development experiences are even more important than unifying the modules associated with the capital markets and standardizing the domestic rules. While synchronizing the institutional aspects is efficient for the integration of countries

34

that have similar developing level, it does not have much utility to the countries that have different development level. Instead the countries with advanced technologies of capital markets have to support the less advanced countries with practical technologies, which will lead to the environment where syncing the institutional characteristics is easier and more efficient. It is because, in the long run, the member countries will share the benefits from the regional cooperation and integration. Of course, pecuniary incentives have to be discussed because the technologies are not belong to the public entities not private sectors and those are not free.

Third, the cooperation efforts from financial demanders’ perspective, i.e. listing firms, bond issuers, are to be encouraged furthermore. ABMI, regional CSD establishment, regional credit rating agencies, and unifying the information rules are mostly targeted to improving investors’ playground, rather than financial demanders’. When cooperative or integrating efforts from investors or financial suppliers’ perspectives progress well enough, such efforts from the business firms’ perspectives are required. For example, in a situation that investors reside in Korea and investment opportunities exist in Vietnam, current efforts or initiatives are focusing on facilitating Korean investors in assessing Vietnamese projects and making investment into Vietnam through standardizing credit information, securing securities deposits, and etc. In the other way around, if Vietnamese firms list their equities in Korean exchanges and register their bond issuance in Korea, it is the linkage from the financial demanders’ perspective. Other than investors’ circumstances of securities investment, firms’ efforts and their environments to utilize the regional cross-border financing have to be promoted at the same time. When the both sides (i.e. demanders and suppliers’ sides) are pushed together, the cooperative or integrating efforts will generate the outcomes we expect. For this, it is suggested that regional cross-border listing of stocks and cross-border securities issuance and registrations be studied.

Forth, it is desirable to set up an initiative or committee, similar to ABMI, targeting to enhance derivatives market cooperation or integration. As seen in ABMI and ASEAN exchange, many cooperative efforts have been implemented for the stock and bond markets. However, except for inter-country currency swap agreements (CMI), there have been few efforts to encourage derivatives market cooperation or integration in the region. The derivatives markets constitute the virtuous cycle of capital market development together with stock and bond markets. The well-functioning derivatives markets make risk management of capital markets and price discovery more efficient. On the other hand, developed stock and bond markets promote derivatives markets. It may be possible that derivatives markets are under-evaluated when the capital markets are tardy in development. However, considering the long-run of the financial markets, well-functioning derivatives markets are to be primed for the case that the derivatives are needed.