Embed Size (px)

Citation preview

SUSTAINABILITY ASSESSMENT OF TECHNOLOGIES

Applicability to Photovoltaics

Paolo Frankl

Brussels, EC/DG RTD, 24-25 April 2007

2

CONTENTS

Applicability of the methodology to existing Photovoltaic (PV) Systems

Assessment of long-term future PV systems Methodological issuesExperience from the IP project NEEDSSelected preliminary results

3

NEEDS - “New Energy Externalities Development for Sustainability”; (IP project, 2004-08)

SENSE - “Sustainability EvaluatioN of Solar Energy systems” (SENSE) EU Research project, (2003-06)

www. sense-eu.netECLIPSE - “Environmental and Ecological Life Cycle Inventories for present and future Power Systems in Europe”, Co-ordinator, EU research project, (2001-03)

www.eclipse-eu.orgPVACCEPT -“Improving PV Acceptability through Innovative Architectural Design” EU research project (2001-04)

www.pvaccept.de

CRYSTALCLEAR

REFERENCE PROJECTS

APPLICABILITY OF THE METHODOLOGY TO CURRENT /

EXISTING PV SYSTEMS

5

Life Cycle Approach

EPD-like approach for existing technologiesPCR TCR2-step approach: ISO14040 ref LCA + key performance indicators

Subsequent Simplified Assessment (STAR)

Actually only way to assess PV Fully feasibleSeveral large studies available as basis for TCRFeasible and desirable for STAR, benchmarking, ecodesign and assessment of future technologies

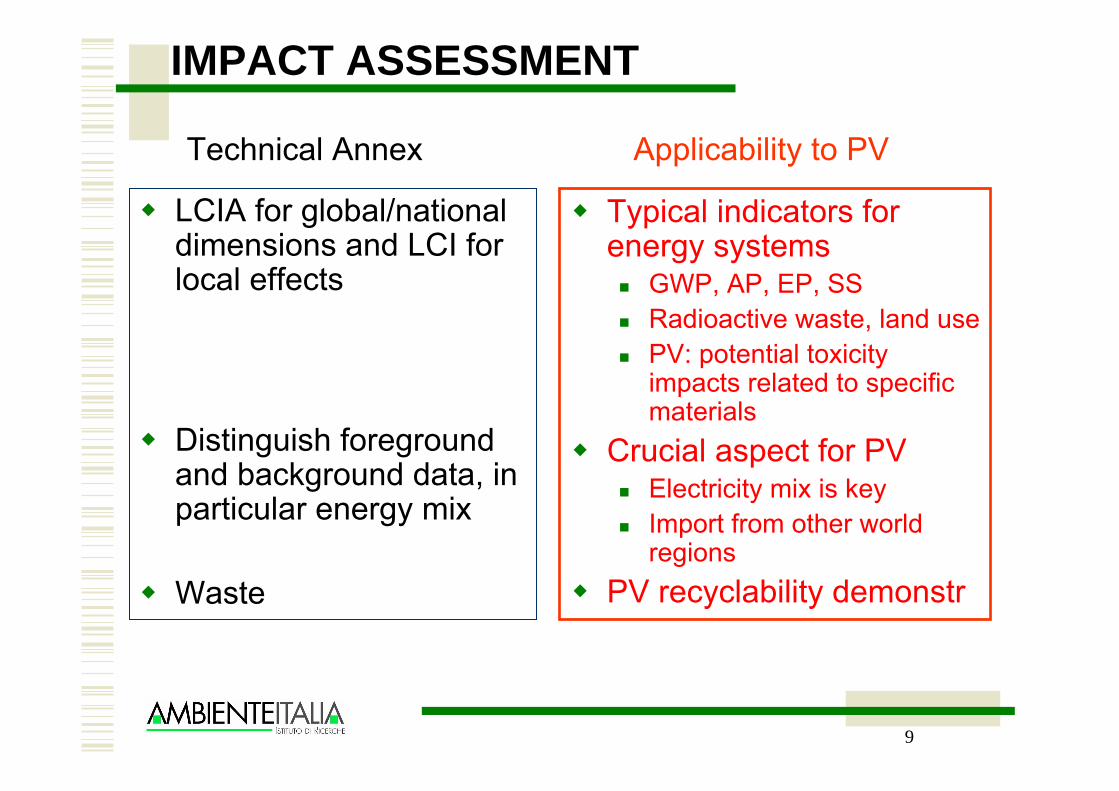

Technical Annex Applicability to PV

GENERAL FEASIBILITY ASPECTS

6

Not only marginal changes but consequences of implementation scenarios

Broaden concept of FU?

Address potential rebound effects?

Level-1: kWh Level-2:

Identify and assess possible future scenarios(see section 2)Qualitative “warning flags”or allocation (e.g. storage)Possible further distinction/refinement of FU:

Peak power vs. base loadDistributed generationBuilding integration and energy saving

Technical Annex Applicability to PV

FUNCTIONAL UNIT

7

Identification of thresholds

Cut-off criteria on mass and/or energy?

Existing PV technology family includes significantly different technologiesCut-off must relate to representativeness and uncertainty of dataMass can be problematic for thin films take into account potential toxicity impacts

Technical Annex Applicability to PV

CUT-OFF CRITERIA

8

Foreground data for technology specific processes

European Reference Life Cycle Data System (ELCD) for upstream and downstream

Alternative: hybrid LCA I/O for background data?

Feasible, but most impacts are indirect

Highly reliable background data are crucial for PV assessment

Electricity mixMain bulk materials

Technical Annex Applicability to PV

DATA

9

LCIA for global/national dimensions and LCI for local effects

Distinguish foreground and background data, in particular energy mix

Waste

Typical indicators for energy systems

GWP, AP, EP, SSRadioactive waste, land usePV: potential toxicity impacts related to specific materials

Crucial aspect for PVElectricity mix is keyImport from other world regions

PV recyclability demonstr

Technical Annex Applicability to PV

IMPACT ASSESSMENT

10

General information

Description of the proposed technology

LCI

LCIA

Totally feasible on full life cycle

End-of-life of PVDeutsche SolarEU-project SENSE

Technical Annex Applicability to PV

TCR

Economic dimension

12

LIFE CYCLE COSTING

Total Cost of Ownership fully feasible for PV systems

Production

Operation & Maintenance

Dismantling and End-of-life

Extension to external costs applicable, but limits to be highlighted

13

Emissions

Concentration & Deposition

Transport & chem. Conversion

Response of Receptors

e.g.EXPOSURE-RESPONSEFUNCTION Effect of ozone on crop yield

Nor

mal

ized

yie

ld

Concentration

Physical Impact

Change in UtilityChange in Utility

Welfare Losses

Costs

The ExternE Impact Pathway

RS1a

RS1b

€/t SO2, NOx, …

g/kWh SO2, NOx, …

EXTERNAL COSTS

Only average costs feasible

[Source: Krewitt 2007]

14

Impacts covered in NEEDS

Climate change

Impacts to human health due to primary and secondary particles and ozone

Impacts to crops due to airborne pollutants: yield loss, additional lime requirement, reduction in fertiliser requirement

Impacts to building materials (material damage, restoration costs)

Loss of terrestrial biodiversity due to land use changes, biodiversity losses due to acidification and eutrophication

[Source: Philipp Preiss, 13.4.2007]

15

Representation of climate change impacts in a risk-matrix(Watkiss 2005) Uncertainty in Valuation

Market Non Market Socially Contingent

Projection Coastal protection

Loss of dryland

Energy (heating/cooling)

Heat stress

Loss of wetland

Regional costs

Investment

Bounded Risk

Agriculture

Water

Variability (drought, flood, storms)

Ecosystem change

Biodiversity

Loss of life

Secondary social effects

Comparative advantage and market structures

U

ncer

tain

ty in

Pre

dict

ing

Clim

ate

Cha

nge

System change and surprise

Above, plus

Significant loss of land and resources

Non-marginal effects

Higher order social effects

Regional collapse

Irreversible losses

Regional collapse

Climate Change

16

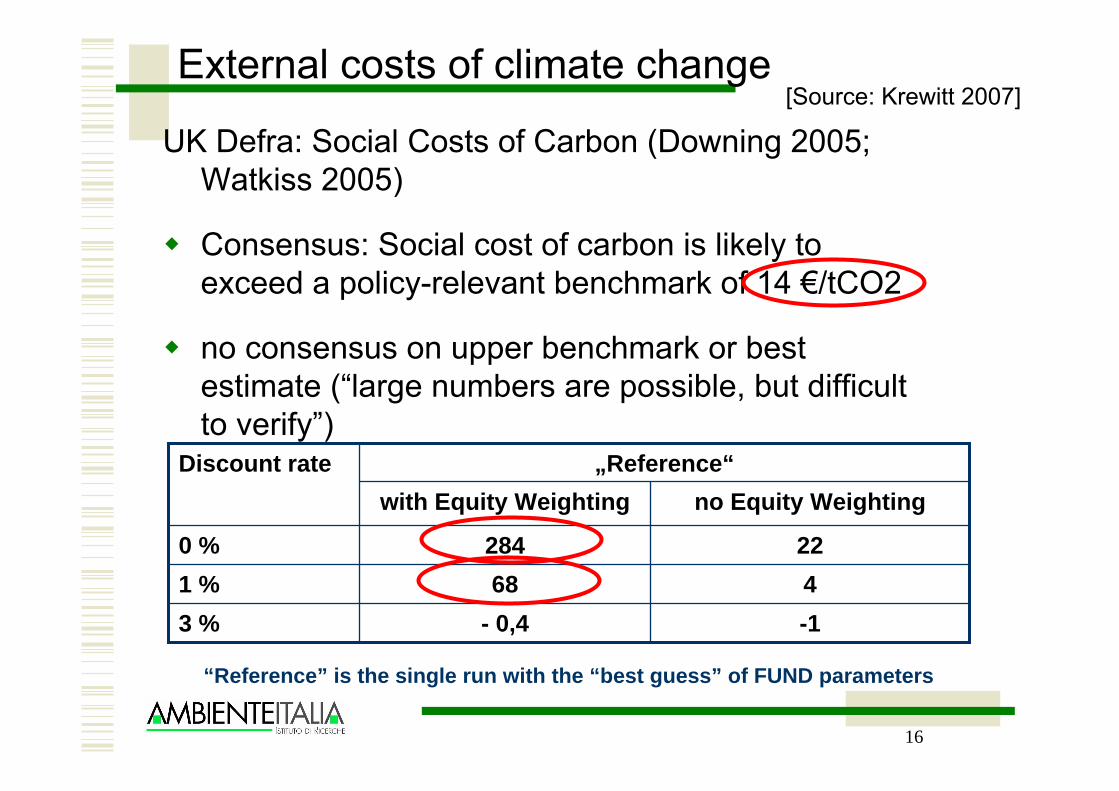

External costs of climate change

UK Defra: Social Costs of Carbon (Downing 2005; Watkiss 2005)

Consensus: Social cost of carbon is likely to exceed a policy-relevant benchmark of 14 €/tCO2

no consensus on upper benchmark or best estimate (“large numbers are possible, but difficult to verify”)

-1- 0,43 %4681 %222840 %

no Equity Weightingwith Equity Weighting„Reference“Discount rate

“Reference” is the single run with the “best guess” of FUND parameters

[Source: Krewitt 2007]

17

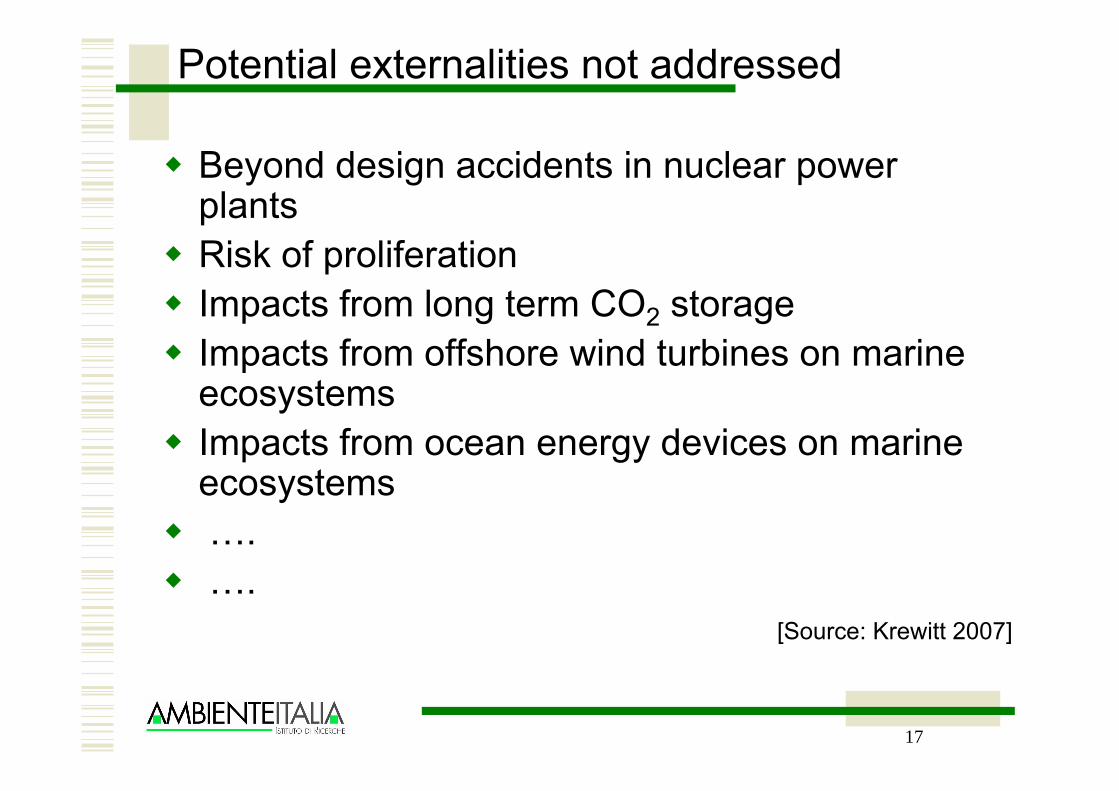

Potential externalities not addressed

Beyond design accidents in nuclear power plantsRisk of proliferationImpacts from long term CO2 storageImpacts from offshore wind turbines on marine ecosystemsImpacts from ocean energy devices on marine ecosystems….….

[Source: Krewitt 2007]

18

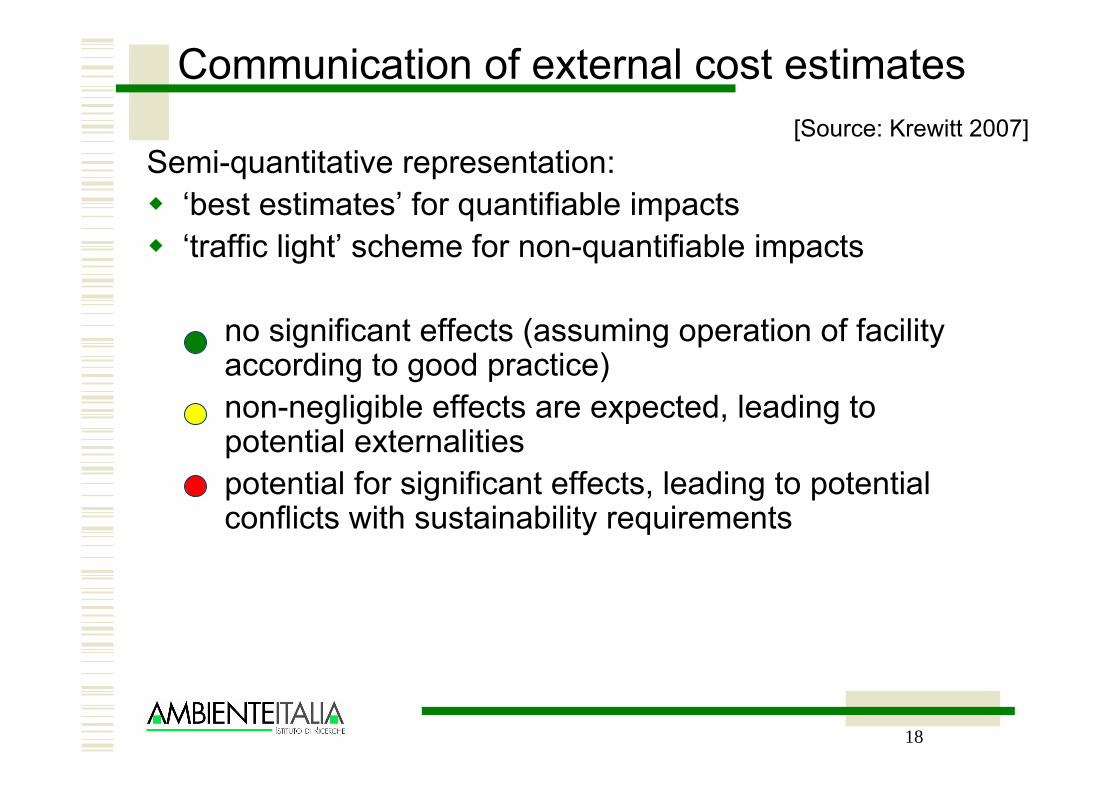

Communication of external cost estimates

Semi-quantitative representation:‘best estimates’ for quantifiable impacts‘traffic light’ scheme for non-quantifiable impacts

● no significant effects (assuming operation of facility according to good practice)

● non-negligible effects are expected, leading to potential externalities

● potential for significant effects, leading to potential conflicts with sustainability requirements

[Source: Krewitt 2007]

19

External costs of electricity supply

> 2,9

0,005

0,005

0,17

2,7

Erdgas GuD 57%

…

…

…

…

…

Kernenergie

> 6,4~ 0,09~ 0,58

Geo-pol. Effekte

Versorgungssicherheit

Proliferation

Große Risiken

0,0050,00040,004Ernteverluste

0,0080,0010,006Materialschäden

Ökosysteme

0,270,030,2Gesundheit

6,10,060,38Klimawandel

Braunkohle GuD 48%

Wind 2,5 MW

PV(2030)

> 2,9

0,005

0,005

0,17

2,7

Gas CC57%

…

…

…

…

…

Nuclear

> 6,4~ 0,09~ 0,58

Geo-political effects

Security of supply

Proliferation

Major accidents

0,0050,00040,004Crop losses

0,0080,0010,006Material damage

Ecosystem impacts

0,270,030,2Health effects

6,10,060,38Climate change

Lignite CC 48%

Wind 2,5 MW

PV(2030)

>> x

(based on DLR, ISI 2006; study commissioned by the German Ministry of the Environment)

[Source: Krewitt 2007]

Social aspects

21

SOCIAL ASPECTS

Occupation and creation of jobsDirectly in the PV sectorIndirect job creation (e.g. in building sector)

Very high social acceptance of PV“YPIMBY”Innovative design and high aesthetic value possibleEducation and trainingCommunication

NEEDS: MCDA with several social impact indicators

22

VISUAL IMPACTS OF INNOVATIVE PV Screenprinted CIS – La Spezia

Source: PVACCEPT (2005)

ASSESSMENT OF FUTURE PV SYSTEMS

Methodological issues&

Scenario approach

25

METHODOLOGICAL ISSUES

Technology-specificSeveral existing PV technologies have significant improvement potentialImpossible to model technology breakthroughs and unknown technologies

However, methodology should remain open to such options

System-relatedMutual influence between PV technology development path and diffusion scenario(s) and related background systems

26

METHODOLOGICAL ISSUES - SYSTEM

Technology development and performances depend on market diffusion scenarios and background system,e.g:

3rd generation PV devices only under favorable circumstancesVery large penetration of PV can only occur if effective and efficient grid-management and energy storage systems are available

Very large penetration of PV changes the background system

Positive and negative feedbacks possibleThe change of the system significantly changes LCA results

Dynamic or semi-dynamic approach needed

27

PROPOSED SCENARIO APPROACH

1. Technology development pathFactors affecting technological developmentIdentification of max. diffusion potential

2. Technology diffusion scenario analysisPessimistic scenarioOptimistic-realistic scenarioVery optimistic scenario

3. Parametric LCA per each scenarioWithout and with change of background system

28

TECHNOLOGY DEVELOPMENT PATH

PV hot spots Key parameters for LCA

Driving forcesRegulatory framework, distributed generation, technology spillovers, sustainable energy finance, etc.

The anticipated role of PV in a future energy supply system

What can be reached? Development targets for PV up to 2050

Main competitors of PV systems and benchmark technologies

Technology development pathway of PVWhich technology developments are necessary? How likely are these technology developments

Specification of future PV systems in 2050

29

Empirical forecast – S curveBased on:

Available industry and sector roadmapsMarket growth estimatesBenchmark with competing electricity generation technologies

Markal – 3E modeling (2007-08)Direct costs with learning curvesExternal costs

Multi-criteria decision analysis (2007-08)Taking also social criteria into account

SCENARIO FORECASTS - NEEDS

Technologydiffusionscenario

Backgroundsystem

scenario

30

TECHNOLOGY DIFF SCENARIOS - PV‘Pessimistic’

Current incentives for PV will not be supported long enough for the technology to ever become competitive with bulk electricityGrowth severely stunted by 2025

‘Optimistic-realistic’Three different PV co-existing ‘families’ (crystalline Si, thin film, novel devices) Growth according to industry (EPIA) predictions, after 2025 reduced growth rates (GP/EREC scenario)

‘Very optimistic’Market still growing until 2050 (yearly growth rate down to 4%) By mid 2030’s large scale energy storage infrastructure availableVery rapid expansion of PV based on novel technologies after 2025 (technological breakthrough)

50% of total PV market in 2050

31

TECHNOLOGY DIFFUSION SCENARIOS

Key parameter: percentage market growth

“Very Optimistic / Technological Breakthrough” scenario

Year

Yearly installed

capacity

(GWp)

Avg. % annual

market growth rate

Cumulative

installed capacity

(GWp)

Total annual

electricity

production (TWh)

2006 1.9 34% 6.4 6

2010 5.6 21% 22.5 23

2020 44.5 23% 230 290

2025 89 15% 575 720

2030 180 15% 1,270 1,600

2040 388 8% 4,080 5,800

2050 575 4% 8,930 12,700

“Optimistic / Realistic” scenario

Year

Yearly installed

capacity

(GWp)

Avg. % annual

market growth rate

Cumulative

installed capacity

(GWp)

Total annual

electricity

production (TWh)

2006 1.9 34% 6.4 6

2010 5.6 21% 22.5 23

2020 34 19% 206 260

2025 55 11% 434 550

2030 71 5% 755 950

2040 82 1.5% 1,520 2,170

2050 86 0.5% 2,360 3,400

“Pessimistic” scenario

Year

Yearly installed

capacity

(GWp)

Avg. % annual

market growth rate

Cumulative

installed capacity

(GWp)

Total annual

electricity

production (TWh)

2006 1.9 34% 6.4 6

2010 5.6 21% 22.5 23

2020 11 7% 105 130

2025 13 3% 166 210

2030 15 3% 236 300

2040 15 0% 384 550

2050 15 0% 532 760

32

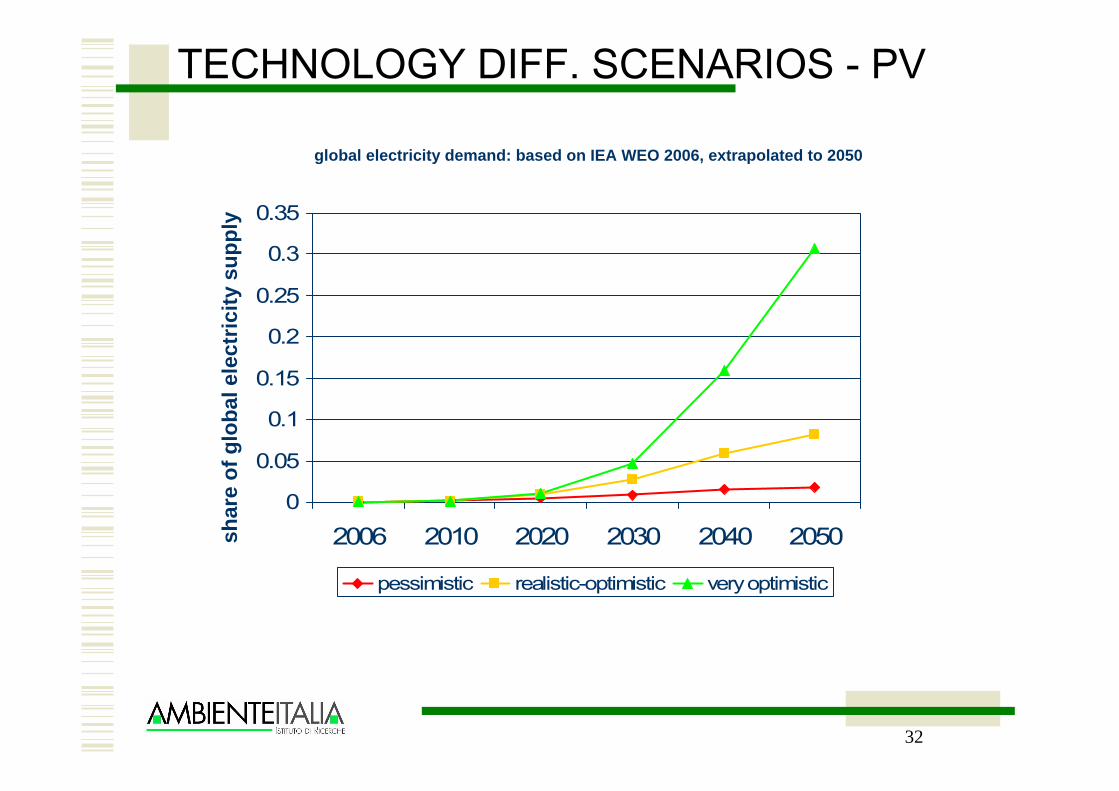

TECHNOLOGY DIFF. SCENARIOS - PV

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2006 2010 2020 2030 2040 2050

pessimistic realistic-optimistic very optimistic

shar

eof

glo

bal e

lect

ricity

sup

ply

global electricity demand: based on IEA WEO 2006, extrapolated to 2050

33

TECHNOLOGY SHIFT

c-Si technologiessc-Simc-Si waferc-Si ribbon

Thin films: Amorphous silicon (a-Si)Copper Indium Gallium Diselenide (CIGS)Cadmium Telluride (CdTe)

New concept devices: Ultra-low cost (Dye-sensitized cells, Organic cells)Ultra-high efficiency (3rd generation, Quantum wellNanostructures, Concentrators)

34

Cumulative installed capacity worldwide per technology

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Present(2006)

2010 2020 2030 2040 2050

Year

GW

Novel DevicesThin Filmsc-Si

GW

p

VERY OPTIMISTIC/BREAKTHROUGH SCEN.

Pre-competitivephase

Peak power1% of supply

Base-load“critical mass”10% of supply

Mass-diffusion3rd generation devStorageFull exploitation of PV benefits “YPIMBY”

Sustained incentives

needed

Cumulative installed capacity

0

5

10

15

20

25

Present (2006) 2010Year

GW

p

Other Thin Films

a-Si Thin Films

c-Si

GW

p

35

P V T e c h n o lo g y M a r k e t S h a r e

0 %1 0 %2 0 %3 0 %4 0 %5 0 %6 0 %7 0 %8 0 %9 0 %

1 0 0 %

2 0 0 3 2 0 1 0 2 0 2 0 2 0 3 0 2 0 4 0 2 0 5 0

Y e a r

Mar

ket S

hare

N o ve l D e vi c e sO t h e r T h in F i lm s T h in F i lm s S i l i c o n T h i n F i lm s C r y s t a l l i n e S i

2025

2050

TECHNOLOGY SHIFT vs. SCENARIO

P V T e c h n o lo g y M a r k e t S h a r e

0 %1 0 %2 0 %3 0 %4 0 %5 0 %6 0 %7 0 %8 0 %9 0 %

1 0 0 %

2 0 0 3 2 0 1 0 2 0 2 0 2 0 3 0 2 0 4 0 2 0 5 0

Y e a r

Mar

ket S

hare

N o ve l D e vi c e sO t h e r T h in F i lm s T h in F i lm s S i l i c o n T h i n F i lm s C r y s t a l l i n e S i

Optimistic-realistic

2050

2025

Pessimistic

36

Technology specification vs. scenarios

Cum. Capacity GWp

sc-Si mc-Si ribbon a-Si CIS CdTe sc-Si mc-Si ribbon (thick)

ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell sc-Si mc-Si ribbon

(thick)ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell

c-Si layer thickness um 250 250 300 100 100 150 100 100 100 100 50Module efficiency 14% 13% 11% 10% 10% 9% 22% 20% 20% 12% 15% 20% 18% 10% 35% 35% 28% 25% 25% 16% 20% 25% 22% 17% 50% 50%Module techn. life years 10 30 30 15 45 45Installed capacity GWp Share of market %Cost €/Wp

Cum. Capacity GWp

sc-Si mc-Si ribbon a-Si CIS CdTe sc-Si mc-Si ribbon (thick)

ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell sc-Si mc-Si ribbon

(thick)ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell

c-Si layer thickness um 250 250 300 100 100 150 100 100 100 100 50Module efficiency 14% 13% 11% 10% 10% 9% 22% 20% 20% 12% 15% 20% 18% 10% 35% 35% 25% 22% 22% 14% 18% 25% 22% 15% 40% 40%Module techn. life years 10 30 30 10 35 35Installed capacity GWp Share of market %Cost €/Wp

Cum. Capacity GWp

sc-Si mc-Si ribbon a-Si CIS CdTe sc-Si mc-Si ribbon (thick)

ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell sc-Si mc-Si ribbon

(thick)ribbon (thin) a-Si CIS CdTe DSC Conc Q-cell

c-Si layer thickness um 250 250 300 150 150 200 150 100 100 150 100Module efficiency 14% 13% 11% 10% 10% 9% 17% 14% 14% 12% 10% 14% 12% 22% 18% 18% 12% 15% 18% 16% 10% 35% 35%Module techn. life years 10 30 30Installed capacity GWp Share of market %Cost €/Wp

Technology

Technology

Technology

V.Optimistic

Opt. / Realistic

Pessimistic

5.3 1.5

25

25

35

35

30

25

0

N/A

1.0

5.3 1.0 0.4

5.3 1.1 0.6

N/A

30

25

25

25

30

30

25

N/A

35

29045% 5%

720

N/A N/A

novel devices430

N/A

N/A N/A N/A N/A

22050%

0.3 19045%

N/A N/A N/A

45001300 310040

2050

50%

N/AN/A

N/A

15% 35%

2050

35%205%

24045%

05%0%

27050%

14085%

3015%

2.790%

2.790%

3

2.790%

0.310%

Present 2025 2050

crystalline-Si thin films novel devicesthin films crystalline-Si thin films3

novel devicescrystalline-Si

Present 2025 2050

0.310% 50%

260

N/A

thin films

2025Present

570 8 900

2 400crystalline-Si thin films crystalline-Si thin films

novel devices3 170 530

crystalline-Si thin films crystalline-Si thin films novel devices crystalline-Si

crystalline-Si thin films novel devices

10%84030%

84035%

40 35

Preliminary LCI results

38

METHOD

1. Identify technology hot-spots and key parameters influencing LCA results

2. Parametric LCA model3. Technological improvement –

experience and industry roadmaps4. Technology diffusion scenario

Exogenous variable, possibly based on economic learning curves

5. Technological improvement matrix for each technology and scenario

39

METHOD – cont.

6. Screening analysis and preliminary LCI results

7. Uncertainty calculation8. Choice of average or selected

representative results9. Final results vs. time with adapted

background systemPossibly semi-dynamic modelling

10. Final results vs. capacity – “Environmental learning curve”

Specific environmental impact vs. cumulative installed capacity

40

Key parameters for PV systems

Module efficiency Module lifetimeMaterial resource consumption

kg/Wp of semiconductor feedstock

Energy resource consumptionkWhel/Wp of semiconductor feedstock kg/Wp of fuels

Non recyclable wasteKg/Wp of waste (dangerous and not, radioactive)

BOS performance ratio in function ofApplicationLocation

41

source: Goetzberger (2002)

EX: PV EFFICIENCY INCREASEExperience and forecast

42

ASSUMPTION: TECHNOLOGY DIFFUSION SCENARIO

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2006 2010 2020 2030 2040 2050

pessimistic realistic-optimistic very optimistic

shar

eof

glo

bal e

lect

ricity

sup

ply

global electricity demand: based on IEA WEO 2006, extrapolated to 2050

43

TECH MATRIX: Ribbon c-Si (v.optim)

Sent to external experts for review and approvalEPIA, companies, experts

KEY PARAMETERS Unit

Module efficiencyModule technical life yThicknessMaterials (technology specific) Material content Consumption Material content Consumption Material content Consumption

poly Si g/m2770 917 350 390 230 240

graphite g/m214 11 (-20%) 10 (-30%)

argon g/m24380 3500 (-20%) 3100 (-30%)

Encapsulation materialsglass g/m2

8080 6000 6000

EVA (Ethyl Vinyl Acetate) g/m21000 1000 1000

Tedlar g/m2256 256 256

Production material yield

Electricity consumption (direct) kWh/m2

Data from literatureAdapted from literatureEstimate/assumptionCalculated

20% (EPIA 2006)

45.7

35 (PVTRAC)

84%

330 150

36.6 (-20%)

90%

Present (Crystalclear 2005) Future 2025

96%

32 (-30%)

100

Future 2050

25%50

11%25

44

TECH MATRIX: DSC (v.optimistic)

KEY PARAMETERS Unit

Module efficiencyModule technical life yMaterials (technology specific) Material content Consumption Material content Consumption Material content Consumption

tin g/m21.9 (*) (*)

metalization paste g/m27.2 (*) (*)

TiO2 g/m216 (*) (*)

Terpineol in TiO2 screen print paste g/m250 (*) (*)

ethylcellulose in TiO2 synthesis g/m23.5 (*) (*)

Ruthenium g/m20.1 (*) (*)

acetonitrile g/m220 (*) (*)

Platiunum g/m20.05 (*) (*)

Polyethilene g/m220 (*) (*)

Poliester resin g/m220 (*) (*)

Iodine (electrolyte) g/m20.45 (*) (*)

Encapsulation materialsSolar glass g/m2

15000 12000 -

Poly-Ethylene Terephtalate (PET) g/m2- - 175

Electricity consumption (direct) kWh/m2

Data from literatureAdapted from literatureEstimate/assumption

(*) = due to the large uncertainty associated to this new technology, it is impossible to make reliable predictions onthe quality and quantity of the technology-specific material inputs

13

Present(Veltkamp & de Wild-Schoelten 2006)

Future 2025

5-6% (NEDO 2004)5

10% (NEDO 2004)10

10.4 9.1

Future 2050

17%15

45

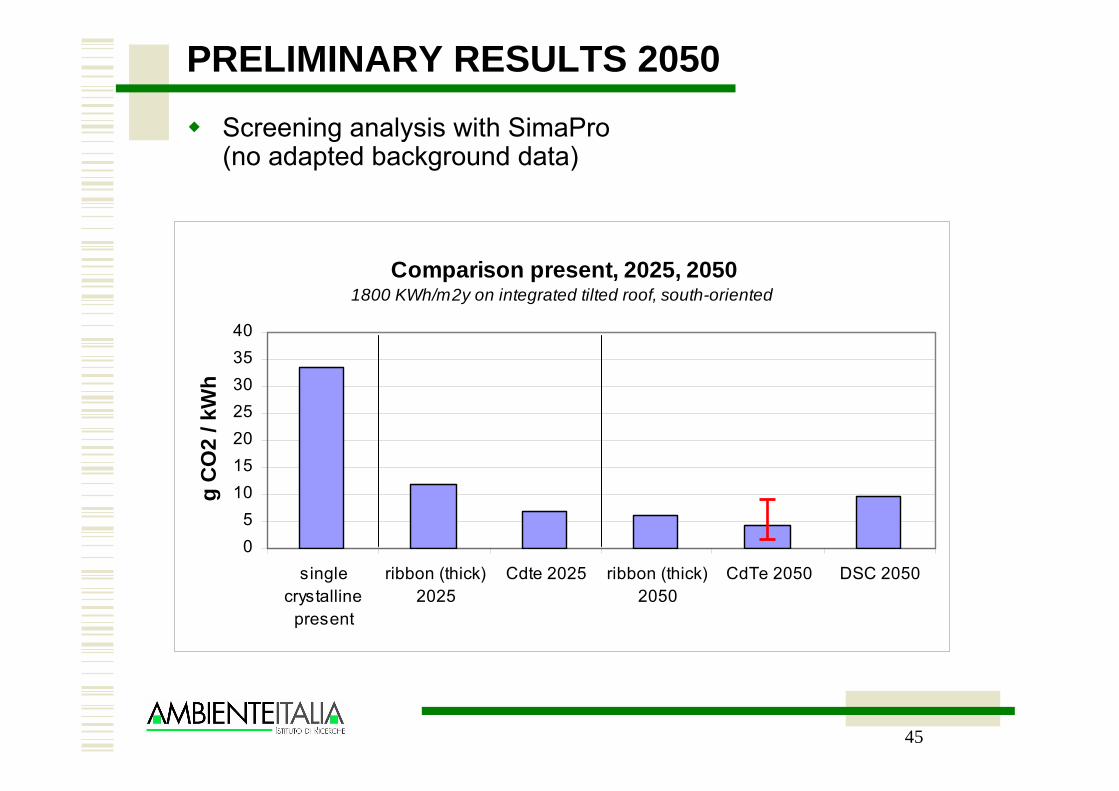

Comparison present, 2025, 20501800 KWh/m2y on integrated tilted roof, south-oriented

05

10152025303540

singlecrystalline

present

ribbon (thick)2025

Cdte 2025 ribbon (thick)2050

CdTe 2050 DSC 2050

g C

O2

/ kW

h

PRELIMINARY RESULTS 2050

Screening analysis with SimaPro(no adapted background data)

46

GWP PAST PRESENT AND FUTURE PV SYSTEMS

0,00

50,00

100,00

150,00

200,00

250,00

PAST - mc-si, retrofit roof PRESENT - mc-si, retrofitroof

FUTURE - CIGS,integrated roof

g CO

2/kW

h el

End of lifeBOS mecBOS elFrameModule

INNOVATION AND LEARNING EFFECTSPreliminary results

IP-Project NEEDS - New Energy Externalities Developments for Sustainability (2004-08)

[mid-90’ dataSource: Eclipse 2003]

[2004 CRYSTALCLEAR data + estimateSource: NEEDS 2006]

GWP of future CIGS systems

0

2

4

6

8

10

12

Future CIGS - 25%, integrated roof, 35y, 1800 kWh/m2gC

O2e

q/kW

h

gCO2/kWh

47

NEXT STEPS

Adapted background system per each scenario

Electricity mix, main materials, transports, wastePossibly dynamic or semi-dynamic consistent background system analysis

NEEDS: Energy system Markal modelling taking into account learning curves (direct and external costs) of all renewable energy technologies, advanced fossil and nuclearInertia of energy system taken into account

BAU-REFPessimistic

450 ppmVery optimistic550 ppmOptimistic-realistic

Markal scenarioTechnology scen

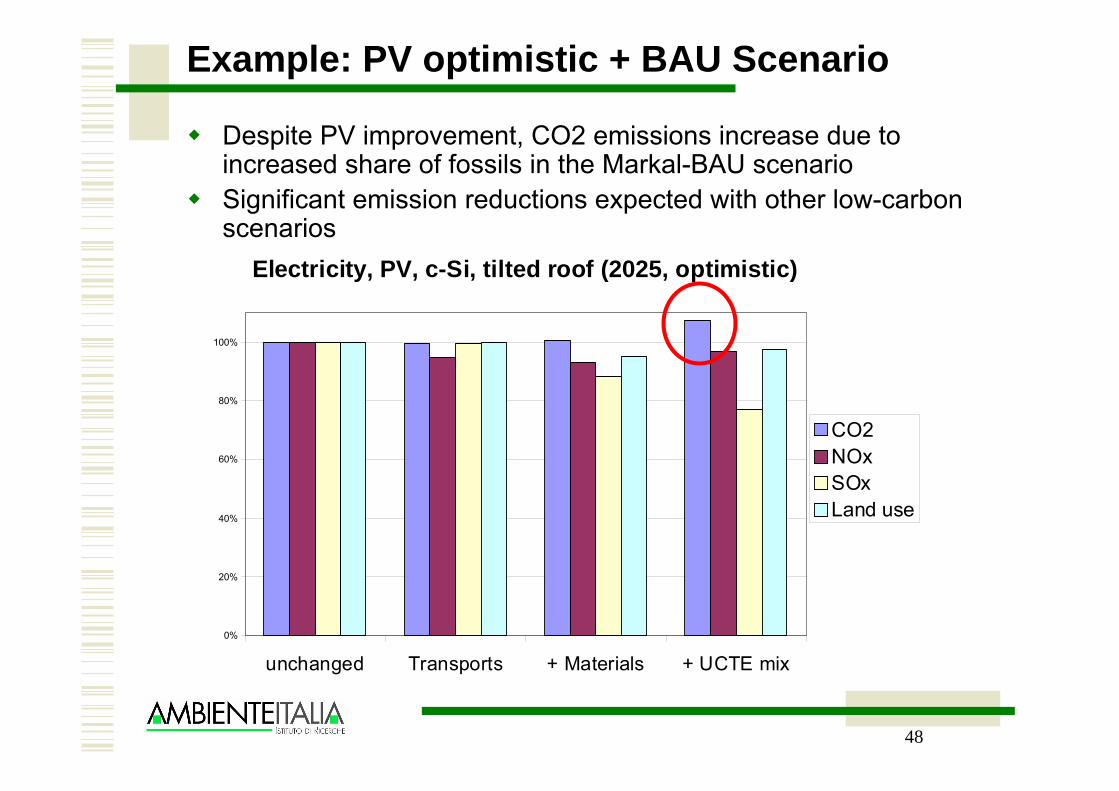

48

Example: PV optimistic + BAU Scenario

Despite PV improvement, CO2 emissions increase due to increased share of fossils in the Markal-BAU scenarioSignificant emission reductions expected with other low-carbon scenarios

Electricity, PV, c-Si, tilted roof (2025, optimistic)

0%

20%

40%

60%

80%

100%

unchanged Transports + Materials + UCTE mix

CO2NOxSOxLand use

49

RECOMMENDATIONS

Show results bothWithout changing background system, in order to highlight technology-specific improvementsWith adapted background system, in order to identify possible positive and negative feedbacks

Always present contribution analysisElectricity mix

Start with UCTE mix, Allow regional mixes (import) and/or national mixes

Main materialsTransportsWaste

50

Example contribution analysis

CdTe 2050 + BAU background system1 MJ

electricity,photovoltaic, tilted

roof, CdTe,100%

4.22E-6 p1 kWp tilted roof

installation, CdTe,on roof 2050

91.4%

1.92E-5 m2photovoltaic

opaque module,frameless, Cdte

38.3%

0.000179 kgSolar glass,low -iron, at

regional8.79%

0.00261 MJElectricity, mediumvoltage, productionUCTE, at grid/UCTE26.9%

1.92E-5 m2tilted roof

contruction,integrated

25.6%

4.22E-6 pinverter, 1,5 kW, at

plant

20.4%

4.22E-6 pelectric installation,

photovoltaicsystem in

7.09%

4.22E-6 pdisposal, tiltedroof, integrated

8.61%

2.96E-5 kgDisposal, plastics,

mixture, 15.3%w ater, to municipal5.5%

51

SUMMARY – ENVIR. LEARNING CURVE

Techn Hot-spotsAnd

Key parameters

LCI

XpEnd of life - Sha re s

RER: LANDFILLHOUSING OFFICE

R ER: LANDFILLMONITOR CRT

RER: LANDFILLMONITOR TFT

RER: LANDFILL PCWITHOUT HOUSINGOFFICE

INCINERATIONMONITOR TFT

INCINERATIONMONITOR CRT

INCINERATIONHOUSING

INCINER ATION PCWITHOUT MONITOR

pR ECYCLING PCWITHOUT HOUSING

pRECYCLING HOUSING

pRECYCLING MONITORCRT

pRECYCLING MONITORTFT

CO2 CH4

CFCs

UV - radiation

AbsorptionReflection

Infraredradiation

Trace gases i n the a tmosphe re

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

SO2

NOX

H2SO44

HNO3

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

LCIAGeneric Modules

Product system modelling Environmental evaluation

2

LCA

pLCI

XpEnd of life - Sha re s

RER: LANDFILLHOUSING OFFICE

R ER: LANDFILLMONITOR CRT

RER: LANDFILLMONITOR TFT

RER: LANDFILL PCWITHOUT HOUSINGOFFICE

INCINERATIONMONITOR TFT

INCINERATIONMONITOR CRT

INCINERATIONHOUSING

INCINER ATION PCWITHOUT MONITOR

pR ECYCLING PCWITHOUT HOUSING

pRECYCLING HOUSING

pRECYCLING MONITORCRT

pRECYCLING MONITORTFT

XpEnd of life - Sha re s

RER: LANDFILLHOUSING OFFICE

R ER: LANDFILLMONITOR CRT

RER: LANDFILLMONITOR TFT

RER: LANDFILL PCWITHOUT HOUSINGOFFICE

INCINERATIONMONITOR TFT

INCINERATIONMONITOR CRT

INCINERATIONHOUSING

INCINER ATION PCWITHOUT MONITOR

pR ECYCLING PCWITHOUT HOUSING

pRECYCLING HOUSING

pRECYCLING MONITORCRT

pRECYCLING MONITORTFT

XpEnd of life - Sha re s

RER: LANDFILLHOUSING OFFICE

R ER: LANDFILLMONITOR CRT

RER: LANDFILLMONITOR TFT

RER: LANDFILL PCWITHOUT HOUSINGOFFICE

INCINERATIONMONITOR TFT

INCINERATIONMONITOR CRT

INCINERATIONHOUSING

INCINER ATION PCWITHOUT MONITOR

pR ECYCLING PCWITHOUT HOUSING

pRECYCLING HOUSING

pRECYCLING MONITORCRT

pRECYCLING MONITORTFT

CO2 CH4

CFCs

UV - radiation

AbsorptionReflection

Infraredradiation

Trace gases i n the a tmosphe re

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

SO2

NOX

H2SO44

HNO3

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

CO2 CH4

CFCs

UV - radiation

AbsorptionReflection

Infraredradiation

Trace gases i n the a tmosphe re

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

Waste water

Air pollution

Fertilisation

PO4-3

NO3-

NH4+

NOXN2O

NH3

SO2

NOX

H2SO44

HNO3

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

CFCsNitrogen oxide

Stratosphere15 - 50 km Absorption Absorption

UV - radiation

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

HydrocarbonsNitrogen oxides

Dry and warmclimate

Hydrocarbons

Nitrogen oxides

Ozone

LCIAGeneric Modules

Product system modelling Environmental evaluation

2

LCA

p

TECHNOLOGY mc-Si: multi-crystalline Literature dataEstimated dataCalculated data

KEY PARAMETERS Unit 2005 2010 2020 2030 2040 2050

Module efficiency % 13,2% 16,0% 18,0% 21,0% 23,0% 25,0%Module technical life years 25,00 30,00 35,00 40,00 45,00 50,00

Material consumption

Silicon External Feedstock

(mass/kWp)kg/kWp 12,82 7,82 3,91 3,15 2,90 2,76

Wafer thickness µm 300,00 180,00 100,00 100,00 100,00 100,00Kerf loss µm 200,00 160,00 150,00 150,00 150,00 150,00

Environmental impact g CO2 eq/ kWhel 31,00 23,25 - - - 11,00

MJ/kWp 26.515 19.886 - - - 13.800

Cost/Prices (module) €/Wp 3,00 2,00 1,00 0,70 0,60 0,50

0

50

100

150

200

250

300

1,E-02

1,E-01

1,E+0

01,E

+01

1,E+0

21,E

+03

1,E+0

51,E

+06

1,E+0

81,E

+09

Cumulative Installed Capacity

Spec

ific

Envi

ronm

enta

l Im

pact

Technology 2 maxTechnology 2 minTechnology 1 maxTechnology 1 min

Tech. 1 - ConventionalTech. 1 - Conventional

Tech. 2 - NewTech. 2 - New

52

“ENVIRONMENTAL LEARNING CURVE”

Independent from actual diffusion speedAlways report uncertainty

0

50

100

150

200

250

300

1,E-02

1,E-01

1,E+0

01,E

+01

1,E+0

21,E

+03

1,E+0

51,E

+06

1,E+0

81,E

+09

Cumulative Installed Capacity

Spec

ific

Envi

ronm

enta

l Im

pact

Technology 2 maxTechnology 2 minTechnology 1 maxTechnology 1 min

Tech. 1 - Conventional

Tech. 2 - New

Long-term policy decisions have to be made on expected future impacts, despite uncertainty

Preliminary economic results

54

PV Learning CurvesPV system Geographical

area

Time period PR Source

PV modules

(crystalline silicon)

Japan

1979-1988 79% (Tsuchiya, 1992)

PV modules USA 1976-1988 78% (Cody and Tiedje, 1997)

PV modules USA 1976- 1992 82% (Williams and Terzian, 1993)

PV modules Japan 1981-1995 80% (Watanabe, 1999?)

PV modules

1981-2000 77% (Parente et al., 2002) (data

source unknown)

PV modules

1968-1998 80% (Harmon, C. 2000) (several

different data source)

PV modules

(crystalline silicon)

1976-1996 84%,

53%,79%

(OECD/IEA 2000: based on the

EU atlas project and Nitsch

1998)

PV modules Germany app. 90% (Schaeffer et al., 2004)

PV modules

the Netherlands app. 90% (Schaeffer et al., 2004)

PV modules Globally* 1976-2001 75-80% (Schaeffer et al., 2004)

PV BOS Germany 1992-2001 78% (Schaeffer et al., 2004)

PV BOS The Netherlands 1992-2001 81% (Schaeffer et al., 2004)

74% Maycock, 2002, in Nemet

PV modules 1976-2001

1987-2001

80%

77%

Strategies Unlimited, in

Schaeffer et al., 2004

Average learning rate (LR=1-PR):20%

55

PV Learning Curve and cost reduction

Source: (PHOTEX 2004, as retrieved in PV-TRAC 2005)

Source: EPIA 2004

Average learning rate (LR=1-PR):20%

56

PV direct cost reduction vs. scenario

PV system cost reduction

0

1

2

3

4

5

6

7

2000 2010 2020 2030 2040 2050 2060

Year

€/W

p

Pessimistic Optimistic / Realistic V. Optimistic / Techn. Breakthrough

2010: 3 - 3.5 €/Wp (PV-TRAC)

2020: 2 €/Wp (PV-TRAC)

2030: 1 €/Wp (PV-TRAC)

2040: < 1 €/Wp (PV-TRAC)

2004: 5 €/W p (PV-TRAC)

LR 20% throughout the whole periodMost optimistic scenario has techn. breakthrough in 2030Other two scenarios: diffusion is limited but LR is the sameSensitivity analysis: LR =10% after 2030 carried out

57

Some German studies (2001): up to 1,7 c€/kWh

ExternE for Germany (EC brochure 2003) : 0,6 c€/kWh

Alsema & Fhtenakis (2005):Externe-Pol damage factorsmc-Si: 0,17 c€/kWhCdTe: 0,13 c€/kWh

NEEDS (on-going): revision and refinement of specific emission damage factors and costs

First estimate future PV systems: 0,02-0,08 c€/kWh

EXTERNAL COSTS OF PV

58

Very large uncertainty dominated by different estimates of impacts of climate change

Several important environmental issues not quantifiable with current state-of-the art of external costs

At least qualitative “warning flags” needed

Important valuable additional information, but limits must be clearly expressed

EXTERNAL COSTS OF PV

PRELIMINARY CONCLUSIONS

60

PRELIMINARY CONCLUSIONS

SAT and proposed approach certainly feasible to assess PV systems

Not looking just at marginal impactsAssessment of absolute large-scale impacts through semi-dynamic scenario analysis

Trade-off between precision of assessment and long-term uncertainty

Goal and objectives of SAT to be clearly definedLong-term implications crucial for policy-making, despite intrinsic uncertainties

Existing PV technologies have major improvement potential

Distinction between level-1 and level-2 might be further discussed