Embed Size (px)

Citation preview

Please file this Supplement to the CollegeChoice Advisor 529 Savings Plan Disclosure Statement with your records.

CSINA_05411 1

SUPPLEMENT DATED APRIL 2018 TO THE COLLEGECHOICE ADVISOR 529 SAVINGS PLAN

DISCLOSURE STATEMENT DATED OCTOBER 2017

This Supplement describes important changes affecting the CollegeChoice Advisor 529 Savings Plan. Unless otherwise indicated, capitalized terms have the same meaning as those in the Disclosure Statement. On December 22, 2017, new federal tax reform legislation, Public Law 115-97 (H.R. 1) was signed into law. The law amended Section 529 of the Code to permit withdrawals from 529 Plan accounts up to $10,000 per year per student (in the aggregate across all Qualified Tuition Programs for that student) for tuition expenses in connection with enrollment and attendance at an elementary or secondary public, private or religious school (K-12 Tuition). The law also permits rollovers from a 529 Plan account to an ABLE Plan account (as authorized by Section 529A of the Code) up to the annual $15,000 contribution limit. As of the date of this supplement, although the Indiana Department of Revenue has not provided specific guidance to taxpayers, (1) Account Owners should be able to withdraw assets from their Account to pay K-12 Tuition and treat the withdrawals as Qualified Expenses for Indiana state tax law purposes; (2) contributions intended to be ultimately withdrawn for K-12 Tuition should be eligible for the 20% Indiana state income tax credit; and (3) action by the Indiana General Assembly may be required to extend favorable Indiana state tax treatment to rollovers to ABLE Plan accounts. However, during its 2018 regular session, the Indiana General Assembly considered legislation that would not extend these favorable Indiana state tax treatments, retroactive to the effective date of H.R. 1. The Indiana General Assembly will convene for a special session in May 2018, after which the treatment of withdrawals to pay K-12 Tuition or contributions intended to be withdrawn for K-12 Tuition should become clear. We are working on updating this Disclosure Booklet to reflect the new U.S. tax law and updates to Indiana state tax law that may follow the May 2018 special session. However, because of the uncertainty regarding Indiana state tax law treatment of the changes to Section 529 made by H.R.1, it is important for Indiana taxpayers to consult their tax advisors before (1) making a withdrawal for K-12 Tuition,(2) making a contribution which they intend to ultimately withdraw for K-12 Tuition, and/or (3) rolling over assets from their Account to an ABLE Plan account.

1

Please file this Supplement to the CollegeChoice Advisor 529 Savings Plan Disclosure Statement with your records.

SUPPLEMENT DATED OCTOBER 2017 TO THE

COLLEGECHOICE ADVISOR 529 SAVINGS

PLAN DISCLOSURE STATEMENT DATED

OCTOBER 2017

This Supplement describes important changes affecting the CollegeChoice Advisor 529 Savings Plan. Unless otherwise

indicated, capitalized terms have the same meaning as those in the Disclosure Statement.

NEW INDIVIDUAL PORTFOLIOS

Two new Individual Portfolios are being created. Two existing Portfolios will transfer assets into the two new Portfolios,

each of which will have a different Underlying Investment from the existing Portfolio. In the case of one of the existing

Portfolios, 100% of the assets will transfer to the corresponding new Portfolio. With respect to the other Portfolio, 20%

of the assets of the existing Portfolio will transfer into the new Portfolio and 80% will remain in the existing Portfolio. To

facilitate a smooth transition you will not be able to access your account, either online or by phone, while the plan

changes are being implemented, after 4:00 pm Eastern Time November 30 until 7:00 am Eastern Time December 4. For

specific details on what will happen and when, refer to the disclosures below. The Individual Portfolio changes are as

follows:

Existing Portfolio Existing Portfolio’s

Underlying

Investment

New Portfolio New Portfolio’s

Underlying

Investment

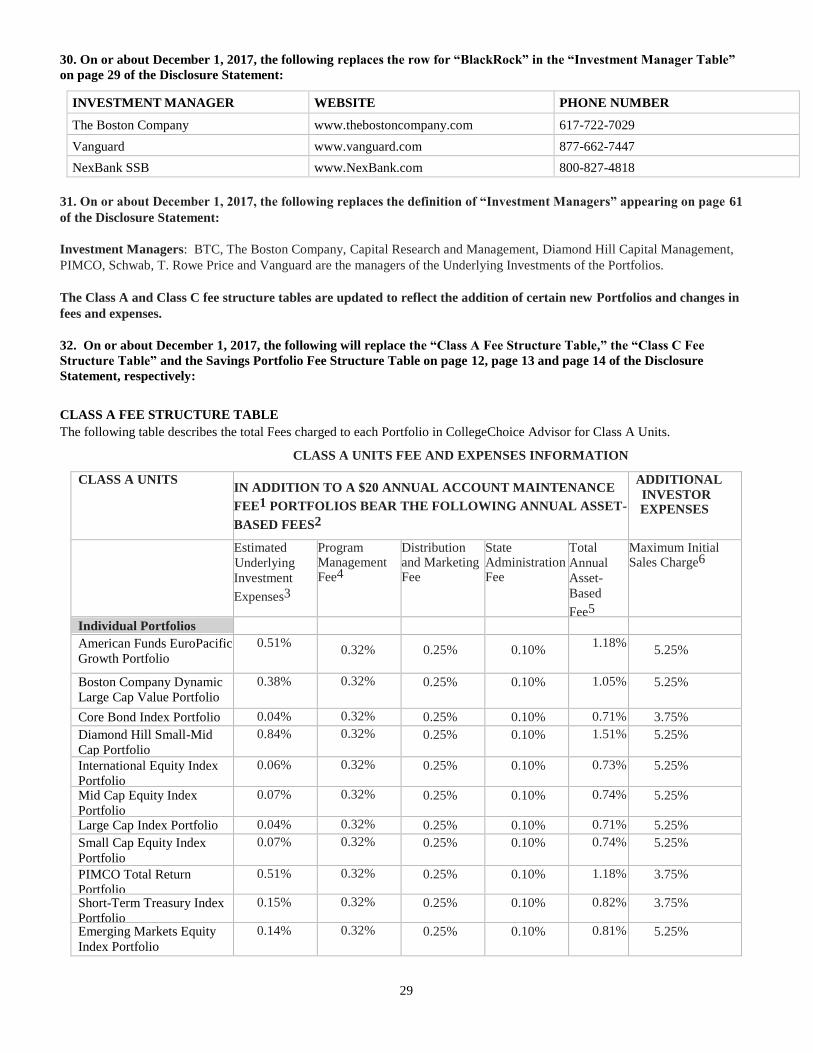

Percentage of Assets

of Existing Portfolio

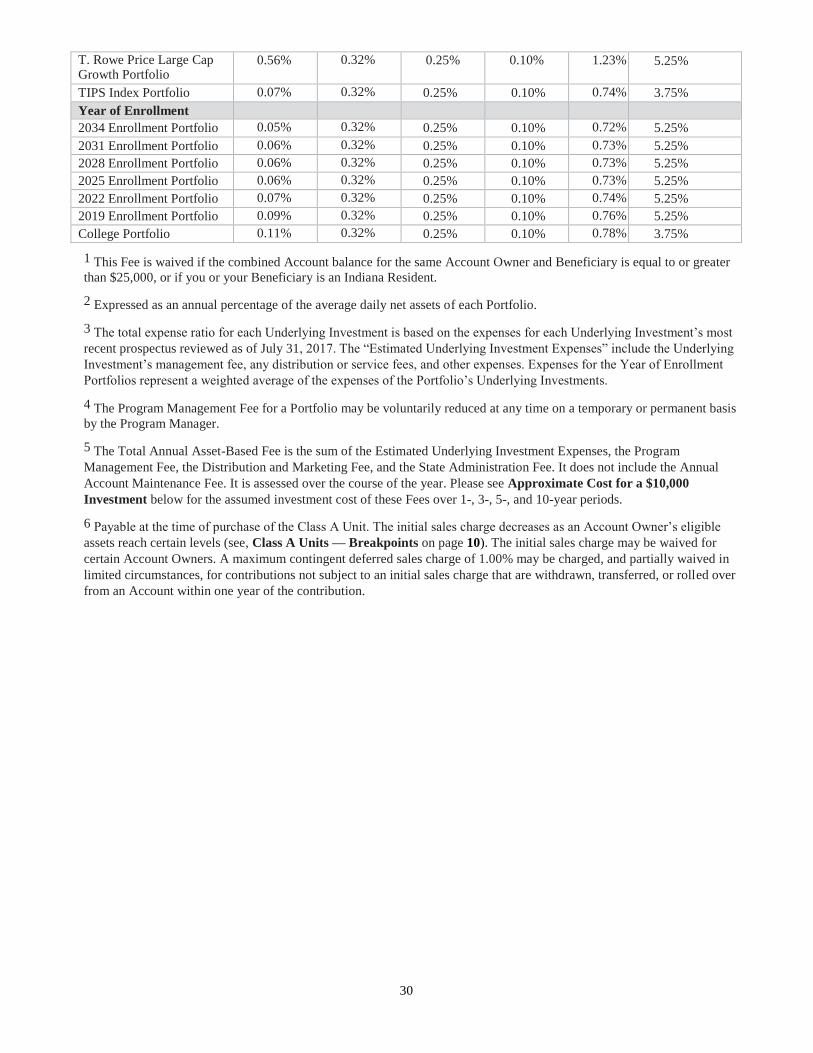

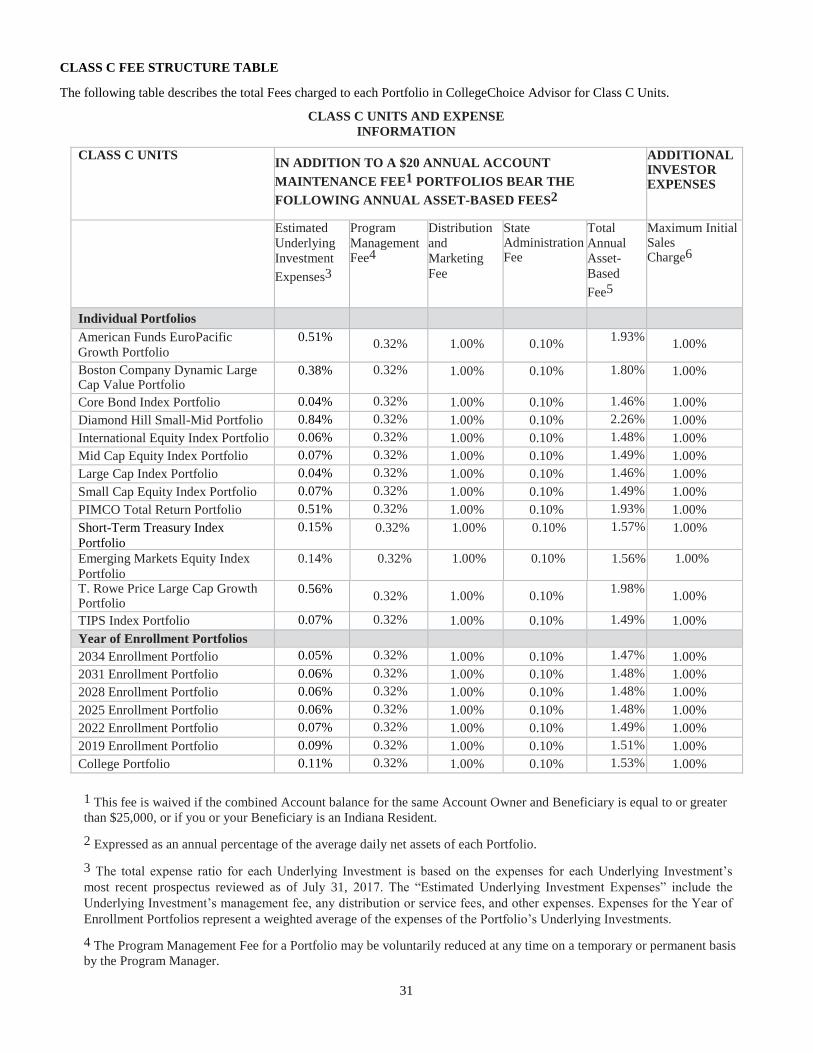

Transferring to New

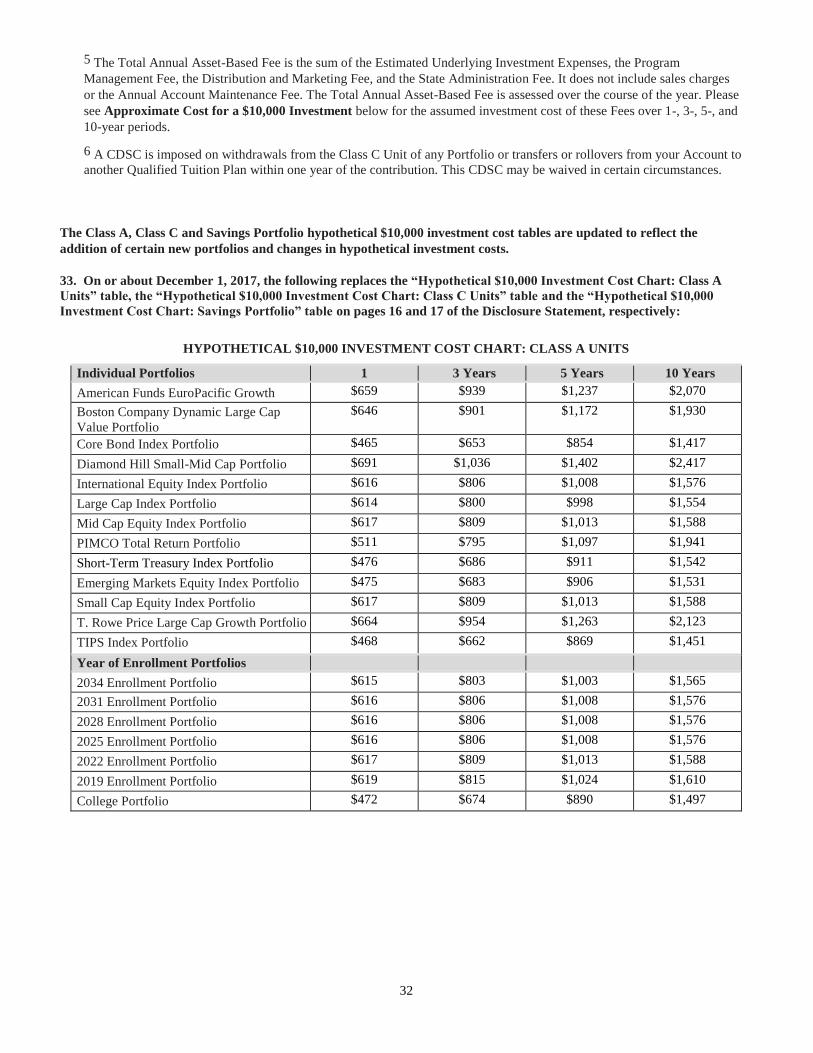

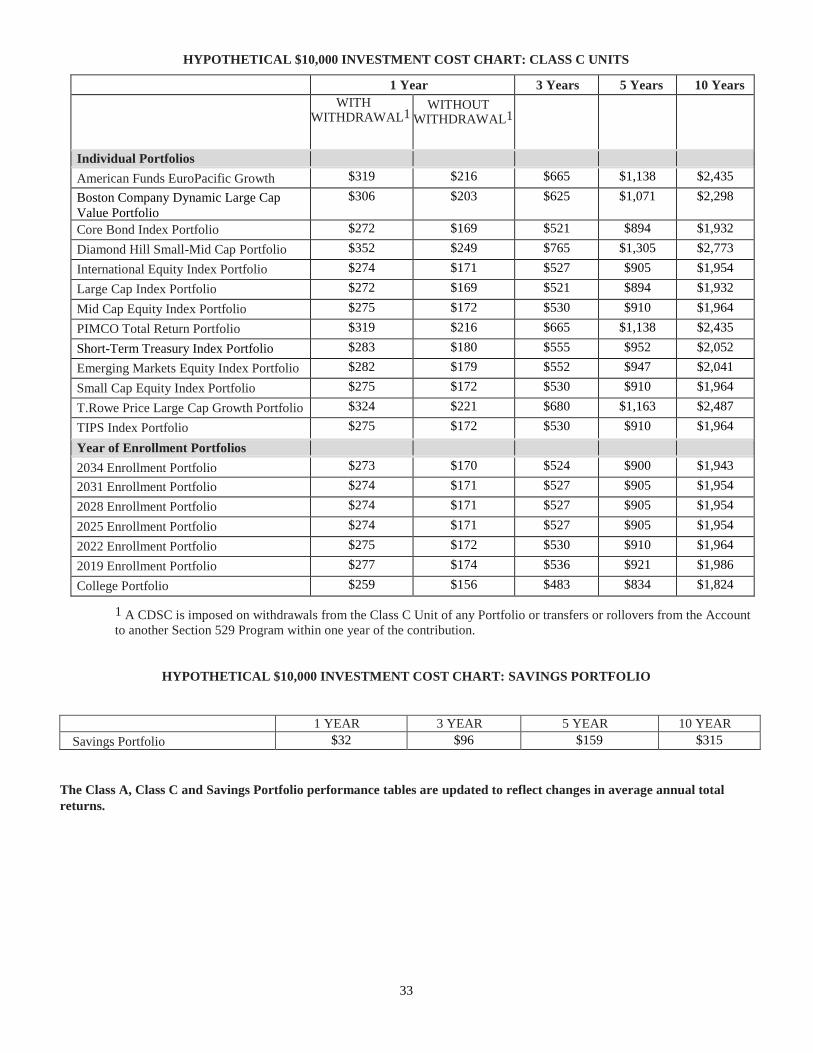

Portfolio

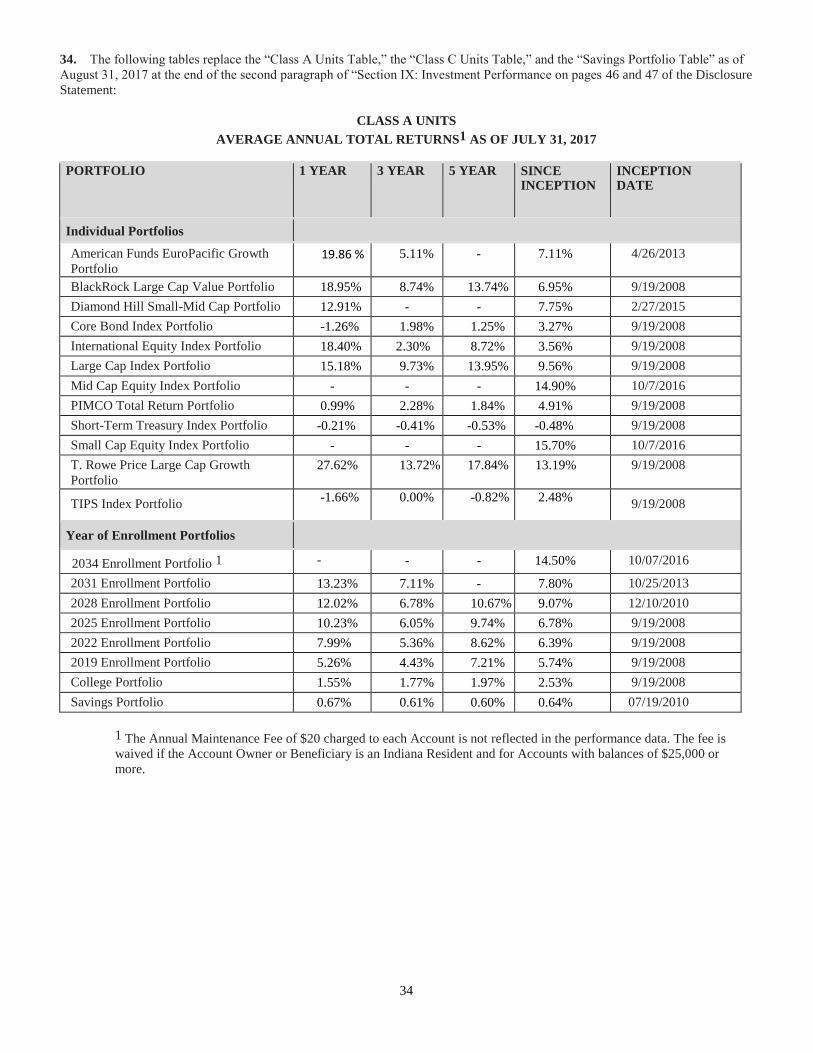

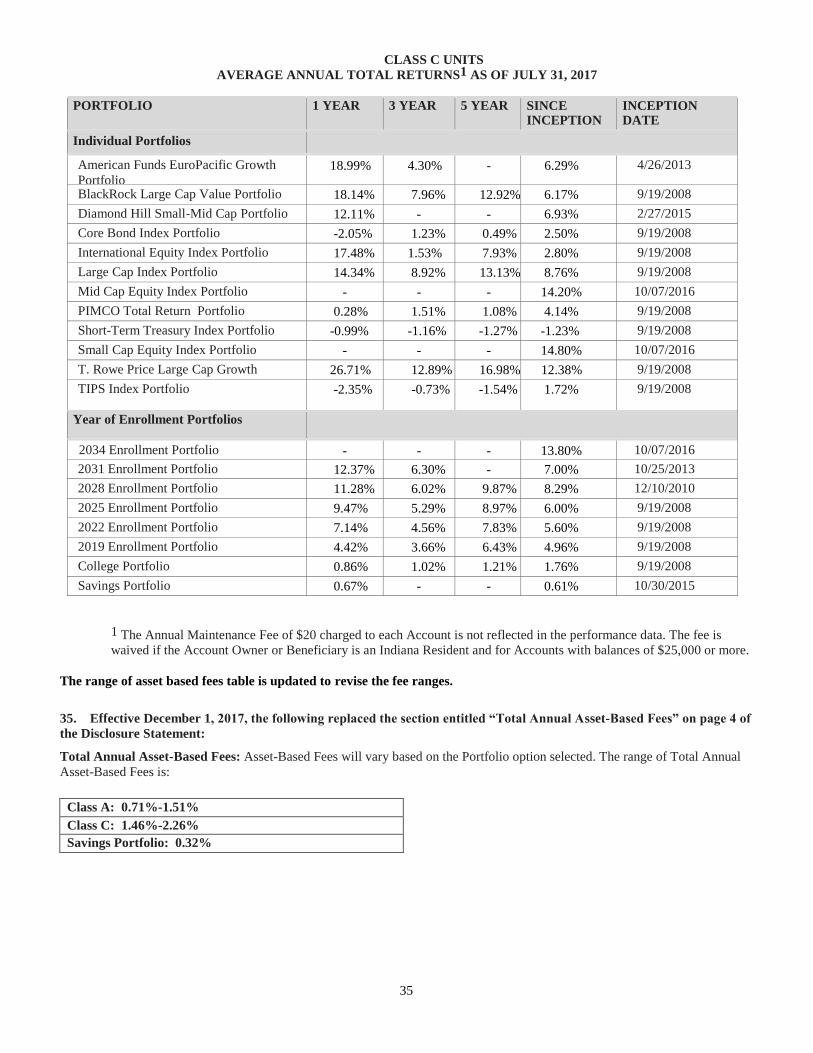

BlackRock Large

Cap Value Portfolio

BlackRock Large

Cap Value Fund

Boston Company

Dynamic Large Cap

Value Portfolio

The Boston Company

Dynamic Large Cap

Value Separate

Account

100%

International Equity

Index Portfolio

iShares Core MSCI

Total Institutional

Stock ETF

Emerging Markets

Equity Index

Portfolio

Vanguard FTSE

Emerging Markets

ETF

20%

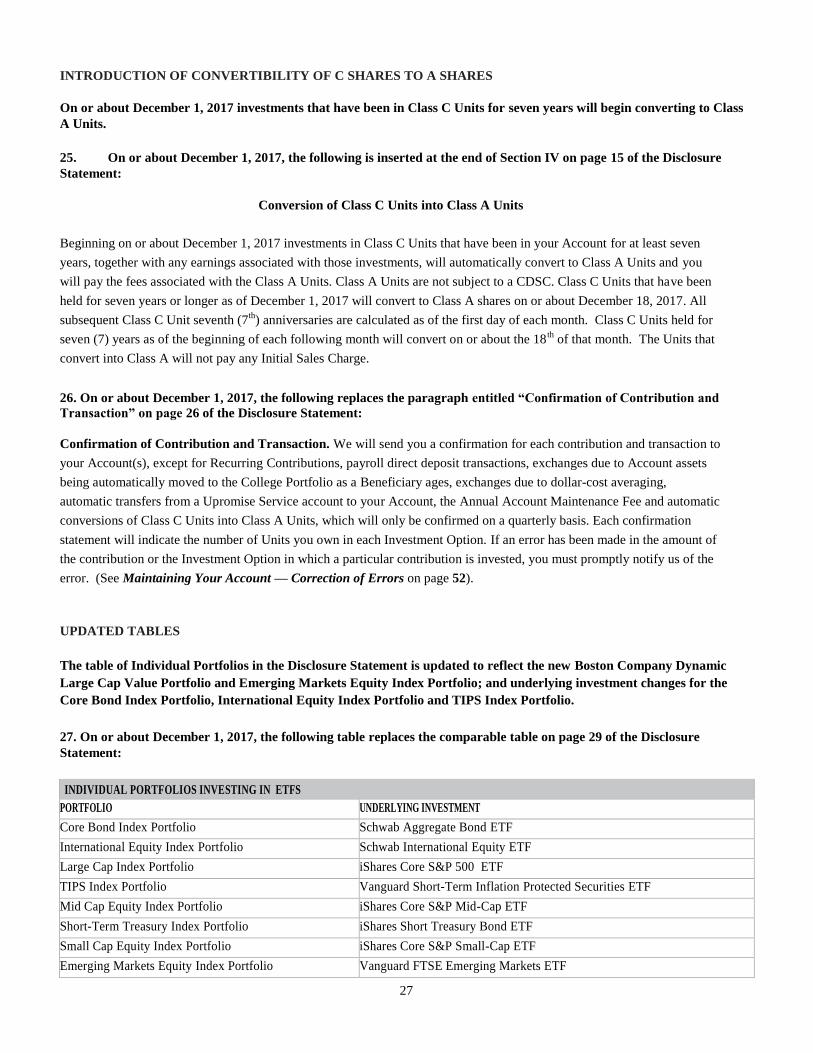

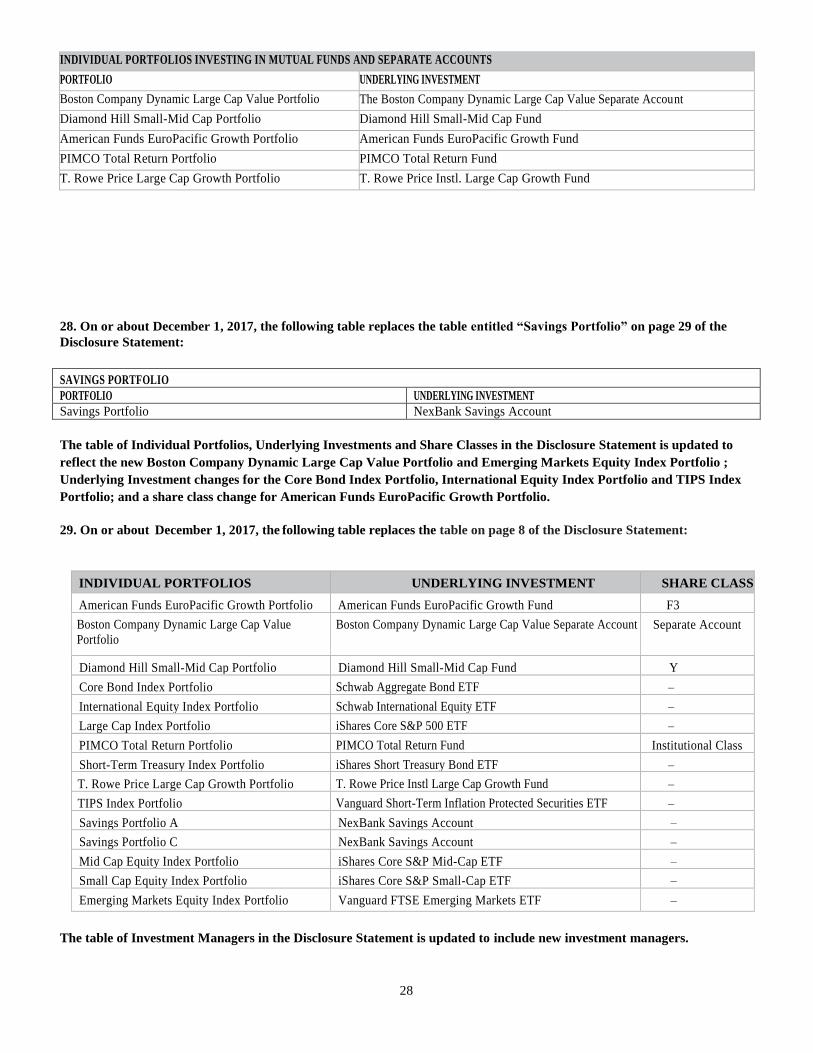

1. On or about December 1, 2017, we will begin to offer two new Individual Portfolios – Boston Company Dynamic

Large Cap Value Portfolio and Emerging Markets Equity Index Portfolio.

On or about December 1, 2017, we will begin to offer two new Individual Portfolios for Class A Units and Class C Units as

follows:

Portfolio Name Investment Manager

Boston Company Dynamic Large Cap Value Portfolio The Boston Company

Emerging Markets Equity Index Portfolio The Vanguard Group, Inc.

2. On or about December 1, 2017, the following replaces the section “BlackRock Large Cap Value Portfolio” under the

section entitled “Other Individual Portfolios” on page 37 of the Disclosure Statement:

Boston Company Dynamic Large Cap Value Portfolio

Investment Objective: The Portfolio seeks to outperform the Russell 1000 Value Index by 200 to 400 basis points over a full

market cycle (three to five years).

Investment Strategy: The Portfolio invests 100% of its funds into The Boston Company Dynamic Large Cap Value Separate

Account. It focuses on equity securities with attractive valuations relative to the market, sector and stock history. It seeks to

avoid the value trap and "being early" by combining traditional valuation measures with companies that exhibit business

improvement and strong fundamentals. It uses proprietary fundamental research resources that understand the past but are

focused on the future. It recognizes that one size does not fit all. It is flexible in performing analyses so as to solve for the right

2

company, sector and macro variables. It also employs risk controls at all levels of the portfolio construction process to minimize

unintended exposures and ensure performance is driven by stock selection while set up/down pricing targets ahead of establishing

new positions.

Principal Investment Risks. The Portfolio’s all-weather investment process is fundamental in nature and highly risk-controlled.

The greatest potential risk, given the Portfolio’s investment process, is the unsystematic risk associated with its fundamental

bottom-up stock selection.

3. On or about December 1, 2017, the following is inserted as a new subsection for the “Emerging Markets Equity Index

Portfolio” between the subsections for “International Equity Index Portfolio” and “Large Cap Equity Index Portfolio”

under the section entitled “Individual Portfolios” beginning on page 31 of the Disclosure Statement:

Emerging Markets Equity Index Portfolio

Investment Objective: The Portfolio seeks to track the performance of a benchmark index that measures the investment return

of stocks issued by companies located in emerging market countries.

Investment Strategy: The Portfolio invests 100% of its funds into the Vanguard FTSE Emerging Markets ETF. Through its

ownership in the fund, the Portfolio employs an indexing investment approach designed to track the performance of the FTSE

Emerging Markets All Cap China A Inclusion Index, a market-capitalization-weighted index that is made up of approximately

3,658 common stocks of large-, mid-, and small-cap companies located in emerging markets around the world. The fund invests

by sampling the index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the

index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as

certain financial measures, such as price/earnings ratio and dividend yield.

Principle Investment Risks: An investment in the Portfolio could lose money over short or even long periods. You should

expect the Portfolio’s share price and total return to fluctuate within a wide range. The Portfolio is subject to the following risks,

which could affect the Fund’s performance:

Stock market risk, which is the chance that stock prices overall will decline. Stock markets tend to move in cycles, with

periods of rising prices and periods of falling prices. The Portfolio’s investments in foreign stocks can be riskier than

U.S. stock investments. Foreign stocks tend to be more volatile and less liquid than U.S. stocks. The prices of foreign

stocks and the prices of U.S. stocks may move in opposite directions. In addition, the Portfolio’s target index may, at

times, become focused in stocks of a particular market sector, which would subject the Portfolio to proportionately

higher exposure to the risks of that sector.

Emerging markets risk, which is the chance that the stocks of companies located in emerging markets will be

substantially more volatile, and substantially less liquid, than the stocks of companies located in more developed foreign

markets because, among other factors, emerging markets can have greater custodial and operational risks; less developed

legal, tax, regulatory, and accounting systems; and greater political, social, and economic instability than developed

markets.

Country/regional risk, which is the chance that world events—such as political upheaval, financial troubles, or natural

disasters—will adversely affect the value of securities issued by companies in foreign countries or regions. The Index’s,

and therefore the Portfolio’s, heavy exposure to China, Taiwan, India, Brazil, and South Africa subjects the Portfolio to

a higher degree of country risk than that of more geographically diversified international funds.

Currency risk, which is the chance that the value of a foreign investment, measured in U.S. dollars, will decrease

because of unfavorable changes in currency exchange rates. Currency risk is especially high in emerging markets.

China A-shares risk, which is the chance that the Portfolio may not be able to access a sufficient amount of China A-

shares to track its target index. China A-shares are only available to foreign investors through a quota license or the

China Stock Connect program.

Index sampling risk, which is the chance that the securities selected for the Portfolio, in the aggregate, will not provide

investment performance matching that of the Portfolio’s target index.

3

REMAPPING INTERNATIONAL EQUITY INDEX PORTFOLIO INTO INTERNATIONAL EQUITY INDEX

PORTFOLIO AND EMERGING MARKETS EQUITY INDEX PORTFOLIO

The International Equity Index Portfolio is changing in two ways. Twenty percent (20%) of its assets are transferring to

the newly created Emerging Markets Equity Index Portfolio. At the same time, the Underlying Investment of the

International Equity Index Portfolio is changing from iShares Core MSCI Total Institutional Stock ETF to Schwab

International Equity ETF.

4. On or about December 1, 2017, twenty percent (20%) of the assets in the International Equity Index Portfolio will

transfer into the Emerging Markets Equity Index Portfolio. On or about December 1, 2017, the International Equity Index Portfolio will invest substantially all of its assets in the Schwab

International Equity ETF (see No. 12. below) and we will begin to offer the Emerging Markets Equity Index Portfolio. In order

to more closely align Account Owner holdings in the newly redesigned Portfolios, twenty percent (20%) of all existing assets in

the International Equity Index Portfolio will automatically be transferred to the Emerging Markets Equity Index Portfolio on or

about Friday, December 1, 2017 (International Transition). Withdrawal or exchange requests received in good order after

4:00 p.m. Eastern Time on Thursday, November 30, 2017 and on Friday, December 1, 2017 will be processed on Monday,

December 4, 2017, using the net asset value of the International Equity Index Portfolio as of Monday, December 4, 2017. Any

contributions received in good order after 4:00 p.m. Eastern Time on Thursday, November 30, 2017 and on Friday, December

1, 2017 will be invested entirely in the International Equity Index Portfolio. The Emerging Markets Equity Index Portfolio will have an investment strategy and investment risks that are different than the

International Equity Index Portfolio.

You are allowed two investment exchanges per calendar year. Because this is a program initiated exchange, the International

Transition will not count as one of your investment exchanges. If you wish, however, to invest your existing balance

differently than as described above, you must contact us to request the change. This will count as one of your two annual

investment exchanges.

The International Transition will only affect assets in the International Equity Index Portfolio as of 4:00 p.m. Eastern Time on

Thursday, November 30, 2017. Allocations of future contributions to the International Equity Index Portfolio will be

contributed to the redesigned International Equity Index Portfolio (see No. 10 below). If you wish to change your allocations of

future contributions you may do so at any time by logging onto our website at www.collegechoiceadvisor529.com, by

submitting the Exchange/Future Contribution Allocation form by mail, or by calling 1-866-485-9413.

REMAPPING BLACKROCK LARGE CAP VALUE PORTFOLIO INTO BOSTON COMPANY DYNAMIC LARGE

CAP VALUE PORTFOLIO

5. On or about December 1, 2017, all of the assets in the BlackRock Large Cap Value Portfolio will transfer into the

Boston Company Dynamic Large Cap Value Portfolio. All existing assets in the BlackRock Large Cap Value Portfolio will automatically be transferred to the Boston Company

Dynamic Large Cap Value Portfolio on Friday, December 1, 2017 (Large Cap Value Transition). In order to facilitate the

Large Cap Value Transition, you will not be able to request a withdrawal or exchange from the BlackRock Large Cap Value

Portfolio after 4:00 p.m. Eastern Time on Thursday, November 30, 2017. Withdrawal or exchange requests received in good

order after 4:00 p.m. Eastern Time on Thursday, November 30, 2017 and on Friday, December 1, 2017 will be processed on

Monday, December 4, 2017, using the net asset value of the Boston Company Dynamic Large Cap Value Portfolio as of

Monday, December 4, 2017. Any contributions received in good order after 4:00 p.m. Eastern Time on Thursday, November

30, 2017 and on Friday, December 1, 2017 will be invested entirely in the Boston Company Dynamic Large Cap Value

Portfolio. The Boston Company Dynamic Large Cap Value Portfolio will have an investment strategy and investment risks that are

different than the BlackRock Large Cap Value Portfolio.

4

You are allowed two investment exchanges per calendar year. Because this is a program-initiated exchange, the Large Cap

Value Transition will not count as one of your investment exchanges. If you wish, however, to invest your existing balance

differently than as described above, you must contact us to request the change. This will count as one of your two annual

investment exchanges.

The Large Cap Value Transition will only affect assets in the BlackRock Large Cap Value Portfolio on the date of the Large

Cap Value Transition. If you wish to change your allocations of future contributions you may do so at any time by logging onto

our website at www.collegechoiceadvisor529.com, by submitting the Exchange/Future Contribution Allocation form by mail,

or by calling 1-866-485-9413.

REDESIGN OF YEAR OF ENROLLMENT PORTFOLIOS

On or about December 1, 2017 the Year of Enrollment Portfolios will change investment allocations and underlying

funds.

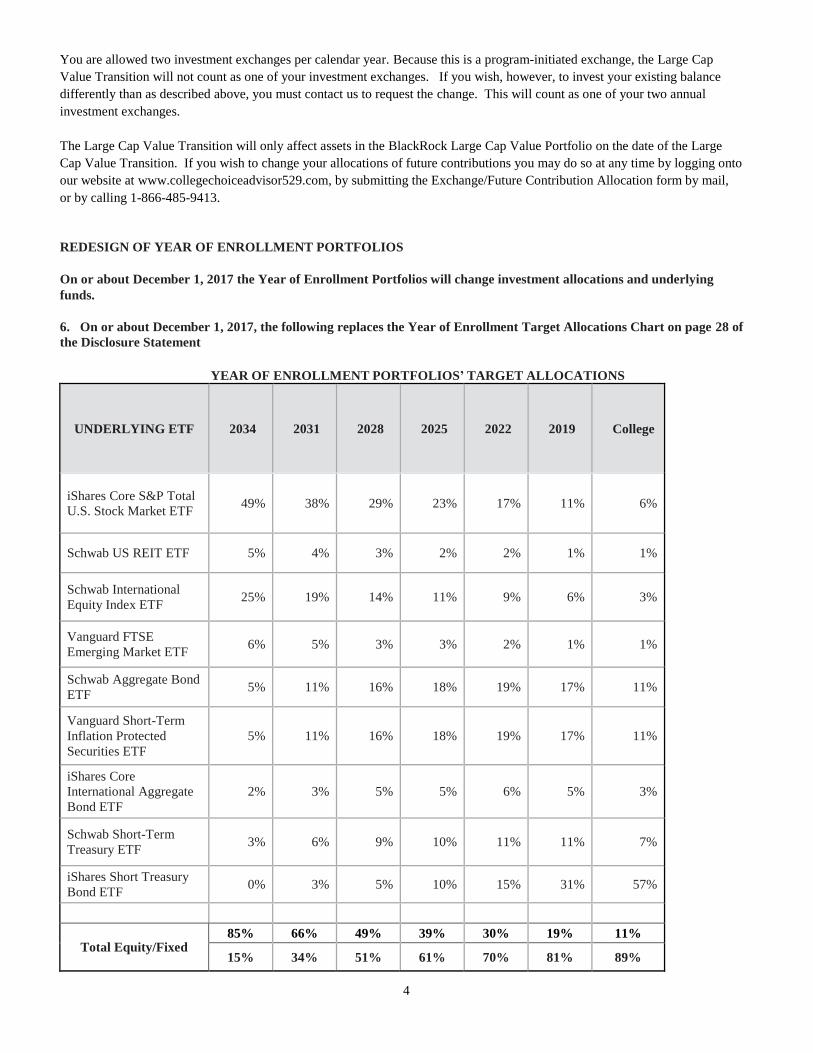

6. On or about December 1, 2017, the following replaces the Year of Enrollment Target Allocations Chart on page 28 of

the Disclosure Statement

YEAR OF ENROLLMENT PORTFOLIOS’ TARGET ALLOCATIONS

UNDERLYING ETF 2034 2031 2028 2025 2022 2019 College

iShares Core S&P Total

U.S. Stock Market ETF 49% 38% 29% 23% 17% 11% 6%

Schwab US REIT ETF 5% 4% 3% 2% 2% 1% 1%

Schwab International

Equity Index ETF 25% 19% 14% 11% 9% 6% 3%

Vanguard FTSE

Emerging Market ETF 6% 5% 3% 3% 2% 1% 1%

Schwab Aggregate Bond

ETF 5% 11% 16% 18% 19% 17% 11%

Vanguard Short-Term

Inflation Protected

Securities ETF

5% 11% 16% 18% 19% 17% 11%

iShares Core

International Aggregate

Bond ETF

2% 3% 5% 5% 6% 5% 3%

Schwab Short-Term

Treasury ETF 3% 6% 9% 10% 11% 11% 7%

iShares Short Treasury

Bond ETF 0% 3% 5% 10% 15% 31% 57%

Total Equity/Fixed 85% 66% 49% 39% 30% 19% 11%

15% 34% 51% 61% 70% 81% 89%

5

The Program Manager monitors and rebalances the underlying asset allocations of the Year of Enrollment Portfolios on a

quarterly basis. The Year of Enrollment Portfolios are rebalanced when the Portfolios fall outside the strategic targets by more

than 1%. The asset allocations of the Year of Enrollment Portfolios automatically transition semi-annually to more conservative

allocations as the Beneficiary approaches college enrollment.

7. On or about December 1, 2017, the following replaces the section entitled “Year of Enrollment Portfolios” on

pages 30 and 31 of the Disclosure Statement:

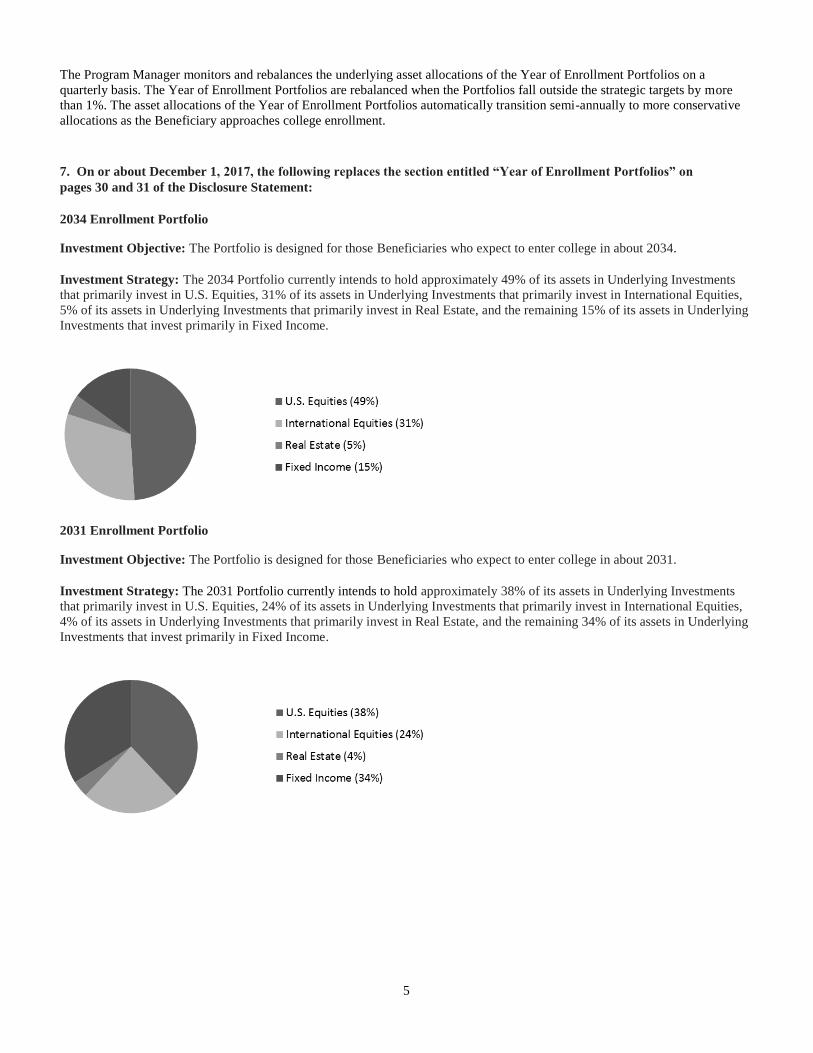

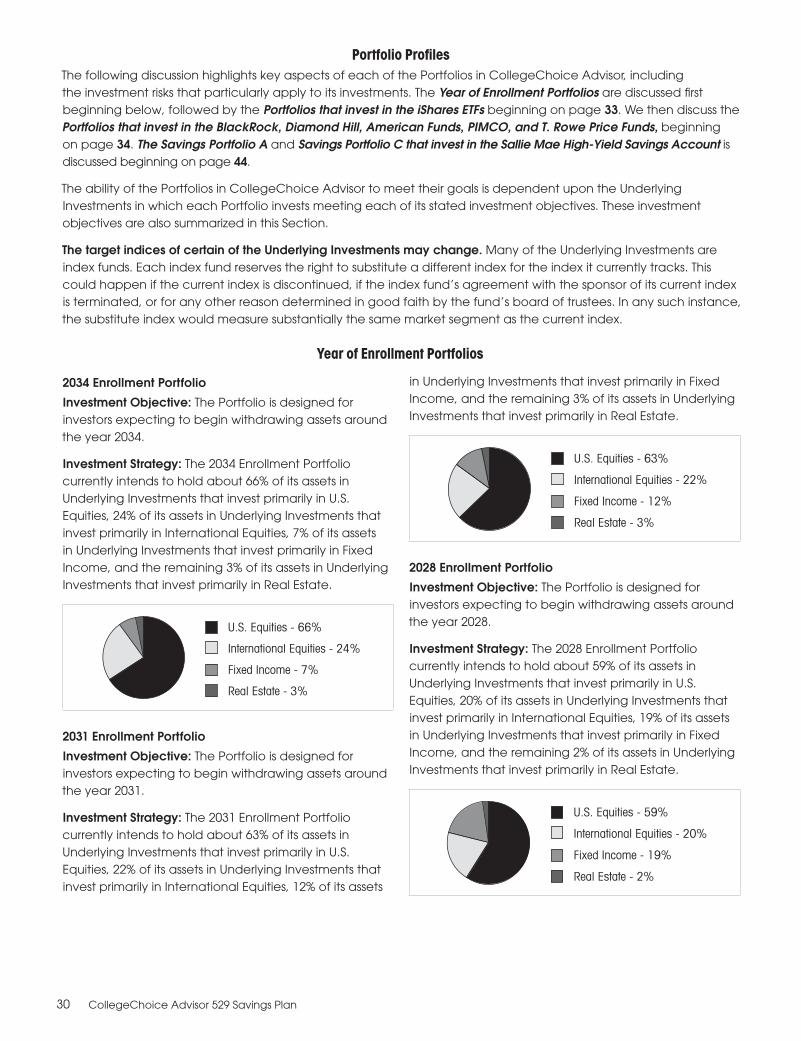

2034 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2034.

Investment Strategy: The 2034 Portfolio currently intends to hold approximately 49% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 31% of its assets in Underlying Investments that primarily invest in International Equities,

5% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 15% of its assets in Underlying

Investments that invest primarily in Fixed Income.

2031 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2031.

Investment Strategy: The 2031 Portfolio currently intends to hold approximately 38% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 24% of its assets in Underlying Investments that primarily invest in International Equities,

4% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 34% of its assets in Underlying

Investments that invest primarily in Fixed Income.

6

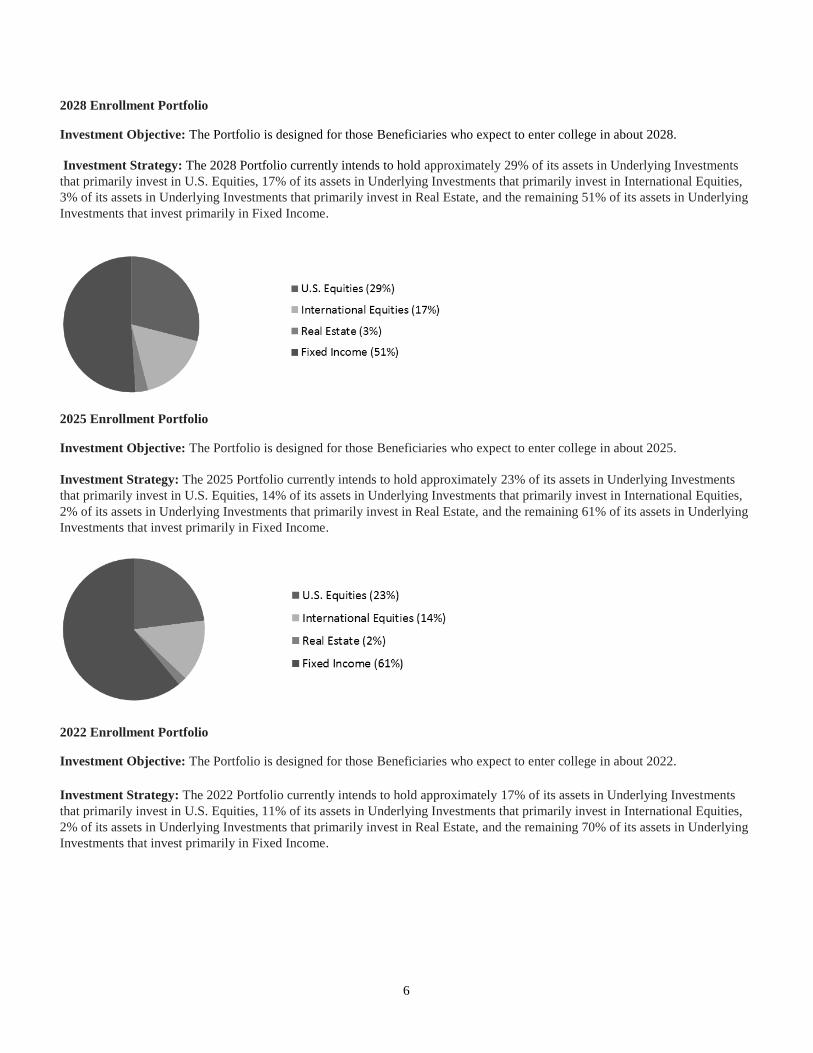

2028 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2028.

Investment Strategy: The 2028 Portfolio currently intends to hold approximately 29% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 17% of its assets in Underlying Investments that primarily invest in International Equities,

3% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 51% of its assets in Underlying

Investments that invest primarily in Fixed Income.

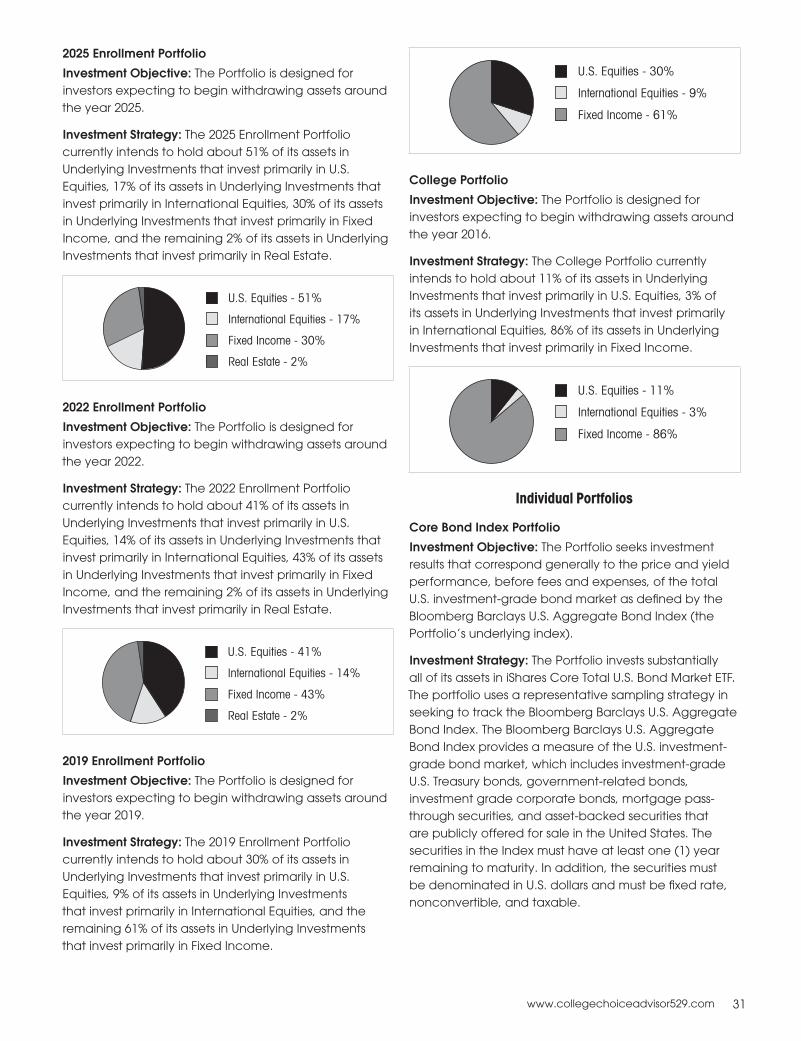

2025 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2025.

Investment Strategy: The 2025 Portfolio currently intends to hold approximately 23% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 14% of its assets in Underlying Investments that primarily invest in International Equities,

2% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 61% of its assets in Underlying

Investments that invest primarily in Fixed Income.

2022 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2022.

Investment Strategy: The 2022 Portfolio currently intends to hold approximately 17% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 11% of its assets in Underlying Investments that primarily invest in International Equities,

2% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 70% of its assets in Underlying

Investments that invest primarily in Fixed Income.

7

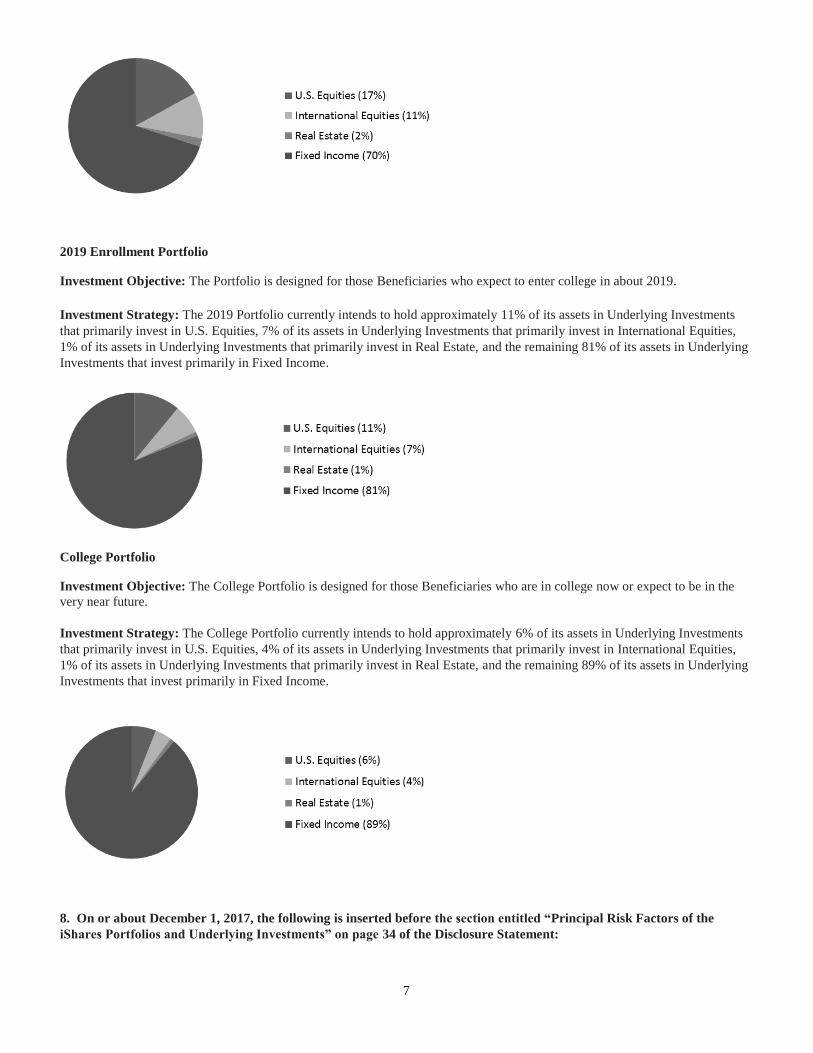

2019 Enrollment Portfolio Investment Objective: The Portfolio is designed for those Beneficiaries who expect to enter college in about 2019.

Investment Strategy: The 2019 Portfolio currently intends to hold approximately 11% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 7% of its assets in Underlying Investments that primarily invest in International Equities,

1% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 81% of its assets in Underlying

Investments that invest primarily in Fixed Income.

College Portfolio Investment Objective: The College Portfolio is designed for those Beneficiaries who are in college now or expect to be in the

very near future.

Investment Strategy: The College Portfolio currently intends to hold approximately 6% of its assets in Underlying Investments

that primarily invest in U.S. Equities, 4% of its assets in Underlying Investments that primarily invest in International Equities,

1% of its assets in Underlying Investments that primarily invest in Real Estate, and the remaining 89% of its assets in Underlying

Investments that invest primarily in Fixed Income.

8. On or about December 1, 2017, the following is inserted before the section entitled “Principal Risk Factors of the

iShares Portfolios and Underlying Investments” on page 34 of the Disclosure Statement:

8

Principal Risk Factors of the Year of Enrollment Portfolios

Principal Risks:

As with any investment, you could lose all or part of your investment in the Portfolio, and the Portfolio’s performance could trail

that of other investments. The Portfolio is subject to certain risks, including the principal risks noted below, any of which may

adversely affect the Portfolio’s NAV, trading price, yield, total return and ability to meet its investment objective.

Agency Debt Risk, Asset Class Risk, Assets Under Management (AUM) Risk, Authorized Participant Concentration Risk, Call

Risk, Cash Transaction Risk, China A-shares Risk, Concentration Risk, Country/Regional Risk, Credit Risk, Currency Hedging

Risk, Currency Risk, Cyber Security Risk, , Derivatives Risk, Emerging Markets Risk, Equity Risk, ETF Trading Risk, Extension

Risk, Financials Sector Risk, Geographic Risk, Foreign Investment Risk, High Portfolio Turnover Risk, Income Risk, Income

Fluctuations Risk, Index-Related Risk, Index Sampling Risk, Industrials Sector Risk, Information Technology Sector Risk,

Interest Rate Risk, Investment Style Risk, Issuer Risk, Large-Capitalization Companies Risk, Liquidity Risk, Management Risk,

Market Capitalization Risk, Market Risk, Market Trading Risk, Mid-Cap Company Risk, Mortgage-Backed and Mortgage Pass-

Through Securities Risk, Non-U.S. Issuer Risk, Operational Risk, Partners Risk, Passive Investment Risk, Prepayment and

Extension Risk, Portfolio Turnover Risk, Real Estate Investment Risk, REITs Risk, Risk of Investing in Developed Countries,

Risk of Investing in the United States, Sampling Index Tracking Risk, Securities Lending Risk, Security Risk, Small Cap

Company Risk, Sovereign and Quasi-Sovereign Obligations Risk, Stock Market Risk, Structural Risk, Tax Risk, and Tracking

Error Risk.

For more information on each of the risks listed above see “Principal Risk Factors of the Underlying Investments” below.

Principal Risk Factors of the Underlying Investments

The information provided below is only a summary of the main risks of the Underlying Investments composed of iShares ETFs,

Schwab and Vanguard products. Each Underlying Investment’s current prospectus and statement of additional information

contains additional information not summarized herein and identifies additional principal risks to which the respective

Underlying Investment may be subject. Please work with your Financial Advisor to understand the specific risks associated with

each Year of Enrollment Portfolio.

Principal Risk Factors of the Vanguard ETFs

Stock market risk

Stock market risk is the chance that stock prices overall will decline. Stock markets tend to move in cycles, with periods of rising

prices and periods of falling prices. The fund’s investments in foreign stocks can be riskier than U.S. stock investments. Foreign

stocks tend to be more volatile and less liquid than U.S. stocks. The prices of foreign stocks and the prices of U.S. stocks may

move in opposite directions. In addition, the fund’s target index may, at times, become focused in stocks of a particular market

sector, which would subject the fund to proportionately higher exposure to the risks of that sector.

Emerging markets risk

Emerging markets risk is the chance that the stocks of companies located in emerging markets will be substantially more volatile,

and substantially less liquid, than the stocks of companies located in more developed foreign markets because, among other

factors, emerging markets can have greater custodial and operational risks; less developed legal, tax, regulatory, and accounting

systems; and greater political, social, and economic instability than developed markets.

Country or regional risk

Country risk is the chance that world events—such as political upheaval, financial troubles, or natural disasters—will adversely

affect the value of securities issued by companies in foreign countries or regions. The Index’s, and therefore the fund’s, heavy

exposure to China, Taiwan, India, Brazil, and South Africa subjects the fund to a higher degree of country risk than that of more

geographically diversified international funds.

Currency risk

9

Currency Risk is the chance that the value of a foreign investment, measured in U.S. dollars, will decrease because of unfavorable

changes in currency exchange rates. Currency risk is especially high in emerging markets.

China A-shares risk

China A-shares risk is the chance that the Fund may not be able to access a sufficient amount of China A-shares to track its target

index. China A-shares are only available to foreign investors through a quota license or the China Stock Connect program.

Index sampling risk

Index sampling risk is the chance that the securities selected for an Underlying Investment, in the aggregate, will not provide

investment performance matching that of the Underlying Investment’s target index. Because ETF shares are traded on an

exchange, they are subject to additional risks: The Fund’s ETF shares are listed for trading on NYSE Arca and are bought and

sold on the secondary market at market prices. Although it is expected that the market price of an ETF Share typically will

approximate its NAV, there may be times when the market price and the NAV differ significantly. Thus, you may pay more or

less than NAV when you buy ETF shares on the secondary market, and you may receive more or less than NAV when you sell

those shares. Although the fund’s ETF shares are listed for trading on NYSE Arca, it is possible that an active trading market

may not be maintained. Trading of the fund’s ETF shares may be halted by the activation of individual or market-wide trading

halts (which halt trading for a specific period of time when the price of a particular security or overall market prices decline by a

specified percentage). Trading of the fund’s ETF shares may also be halted if (1) the shares are delisted from NYSE Arca without

first being listed on another exchange or (2) NYSE Arca officials determine that such action is appropriate in the interest of a fair

and orderly market or for the protection of investors.

Principal Risk Factors of the iShares ETFs

Agency Debt Risk

Underlying Investments may invest in unsecured bonds or debentures issued by government agencies, including the Federal

National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). Bonds or

debentures issued by government agencies, government-sponsored entities, or government corporations, including, among others,

Fannie Mae and Freddie Mac, are generally backed only by the general creditworthiness and reputation of the government

agency, government-sponsored entity, or government corporation issuing the bond or debenture and are not guaranteed by the

U.S. Department of the Treasury (U.S. Treasury) or backed by the full faith and credit of the U.S. government. As a result, there

is uncertainty as to the current status of many obligations of Fannie Mae, Freddie Mac and other agencies that are placed under

conservatorship of the federal government. Government National Mortgage Association securities are generally backed by the

full faith and credit of the U.S. Government.

Asset Class Risk

Securities and other assets in the Portfolio’s underlying index or in an Underlying Investment may underperform in comparison to

the general financial markets, a particular financial market or other asset classes.

Assets Under Management Risk

From time to time, an Authorized Participant (as defined below), a third- party investor, an Underlying Investment’s adviser or an

affiliate of an Underlying Investment’s adviser, or a fund may invest in an Underlying Investment and hold its investment for a

specific period of time in order to facilitate commencement of the Underlying Investment’s operations or for the Underlying

Investment to achieve size or scale. There can be no assurance that any such entity would not redeem its investment or that the

size of the fund would be maintained at such levels, which could negatively impact the Underlying Investment.

Authorized Participant Concentration Risk

Only an Authorized Participant may engage in creation or redemption transactions directly with an ETF. An Underlying

Investment has a limited number of institutions that may act as Authorized Participants on an agency basis (i.e., on behalf of other

market participants). To the extent that Authorized Participants exit the business or are unable to proceed with creation and/or

redemption orders with respect to an Underlying Investment and no other Authorized Participant is able to step forward to create

10

or redeem Creation Units (as defined in the Purchase and Sale of Fund Shares section of the Underlying Investment’s

Prospectus), an Underlying Investment’s shares may be more likely to trade at a premium or discount to NAV and possibly face

trading halts and/or delisting. An “Authorized Participant” is an entity chosen by an ETF sponsor to undertake the responsibility

of obtaining the underlying assets needed to create an ETF. Authorized Participants are typically large institutional organizations,

such as market makers or specialists.

Bond Investment Risk

The risks of fixed-income investing include short-term and prolonged price declines because of a rise in interest rates, issuer

quality considerations, and other economic considerations.

Call Risk

During periods of falling interest rates, an issuer of a callable bond held by an Underlying Investment may “call” or repay the

security before its stated maturity, and the Underlying Investment may have to reinvest the proceeds in securities with lower

yields, which would result in a decline in the Underlying Investment’s income, or in securities with greater risks or with other less

favorable features.

Cash Transactions Risk

Each Underlying Investment expects to effect all of its creations and redemptions for cash, rather than in-kind securities. As a

result, an Underlying Investment may have to sell portfolio securities at inopportune times in order to obtain the cash needed to

meet redemption orders. This may cause an Underlying Investment to sell a security and recognize a capital gain or loss that

might not have been incurred if it had made a redemption-in-kind. The use of cash creations and redemptions may also cause an

Underlying Investment’s shares to trade in the market at greater bid-ask spreads or greater premiums or discounts to the

Underlying Investment’s NAV.

Concentration Risk

An Underlying Investment may be susceptible to an increased risk of loss, including losses due to adverse events that affect the

Underlying Investment’s investments more than the market as a whole, to the extent that the Underlying Investment’s

investments are concentrated in the securities of a particular issuer or issuers, country, group of countries, region, market,

industry, group of industries, sector or asset class.

Credit Risk

Debt issuers and other counterparties may be unable or unwilling to make timely interest and/or principal payments when due or

otherwise honor their obligations. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness

may also adversely affect the value of an Underlying Investment’s investment in that issuer. The degree of credit risk depends on

the issuer’s financial condition and on the terms of the securities.

Currency Hedging Risk

When a derivative is used as a hedge against a position that an Underlying Investment holds, any loss generated by the derivative

generally should be substantially offset by gains on the hedged investment, and vice versa. While hedging can reduce or eliminate

losses, it can also reduce or eliminate gains. Hedges are sometimes subject to imperfect matching between the derivative and its

reference asset, and there can be no assurance that an Underlying Investment’s hedging transactions will be effective.

Currency Risk

Because an Underlying Investment’s NAV is determined in U.S. dollars, an Underlying Investment’s NAV could decline if one

or more of the currencies of the non-U.S. markets in which an Underlying Investment invests depreciates against the U.S. dollar

and the depreciation of one currency is not offset by appreciation in another currency and/or an Underlying Investment’s attempt

to hedge currency exposure to the depreciating currency or currencies is unsuccessful. Generally, an increase in the value of the

U.S. dollar against the component currencies will reduce the value of a security denominated in the component currencies, as

applicable. In addition, fluctuations in the exchange rates between currencies could affect the economy or particular business

11

operations of companies in a geographic region, including securities in which an Underlying Investment invests, causing an

adverse impact on an Underlying Investment’s investments in the affected region and the United States. As a result, investors

have the potential for losses regardless of the length of time they intend to hold fund shares. Currency exchange rates can be very

volatile and can change quickly and unpredictably. As a result, an Underlying Investment’s NAV may change quickly and

without warning.

Cyber Security Risk

Failures or breaches of the electronic systems of an Underlying Investment, an Underlying Investment’s adviser, distributor, and

other service providers, market makers, Authorized Participants or the issuers of securities in which an Underlying Investment

invests have the ability to cause disruptions and negatively impact an Underlying Investment’s business operations, potentially

resulting in financial losses to an Underlying Investment and its shareholders. While each Underlying Investment has established

business continuity plans and risk management systems seeking to address system breaches or failures, there are inherent

limitations in such plans and systems. Furthermore, an Underlying Investment cannot control the cyber security plans and

systems of an Underlying Investment’s service providers, the Index Provider, market makers, Authorized Participants or issuers

of securities in which an Underlying Investment invests.

Derivatives Risk

An Underlying Investment may use currency forwards and Non-Deliverable Forwards to hedge the currency exposure resulting

from investments in the foreign currency denominated securities held by an Underlying Investment. An Underlying Investment’s

use of these instruments, like investments in other derivatives, may reduce an Underlying Investment’s returns, increase volatility

and/or result in losses due to credit risk or ineffective hedging strategies. Volatility is defined as the characteristic of a security, a

currency, an index or a market, to fluctuate significantly in price within a defined time period. Currency forwards, like other

derivatives, are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its

contractual obligation. A risk of an Underlying Investment’s use of derivatives is that the fluctuations in their values may not

correlate perfectly with the value of the currency or currencies being hedged as compared to that of the U.S. dollar. The possible

lack of a liquid secondary market for derivatives and the resulting inability of an Underlying Investment to sell or otherwise close

a derivatives position could expose an Underlying Investment to losses and could make derivatives more difficult for an

Underlying Investment to value accurately. An Underlying Investment could also suffer losses related to its derivatives positions

as a result of unanticipated market movements, which losses are potentially unlimited. Blackrock’s use of derivatives is not

intended to predict the direction of securities prices, currency exchange rates, interest rates and other economic factors, which

could cause an Underlying Investment’s derivatives positions to lose value. Derivatives may give rise to a form of leverage and

may expose an Underlying Investment to greater risk and increase its costs. The U.S. and certain other countries have adopted or

are in the process of adopting regulatory reforms affecting the derivatives markets. These regulations may make derivatives more

costly, may limit the availability of derivatives, and may otherwise adversely affect the value and performance of derivatives.

Emerging Markets Risk

Some foreign markets are considered to be emerging markets. Investment in these emerging markets is subject to a greater risk of

loss than investments in more developed markets. This is due to, among other things, greater market volatility, lower trading

volume, inflation, political and economic instability, greater risk of market shutdown, and more governmental limitations on

foreign investment than those typically found in a developed market.

Equity Securities Risk

Investments in equity securities are subject to changes in value that may be attributable to market perception of a particular issuer

or to general stock market fluctuations that affect all issuers. Investments in equity securities may be more volatile than

investments in other asset classes.

Extension Risk

During periods of rising interest rates, certain debt obligations may be paid off substantially more slowly than originally

anticipated and the value of those securities may fall sharply, resulting in a decline in an Underlying Investment’s income and

potentially in the value of an Underlying Investment’s investments.

12

Financials Sector Risk

Performance of companies in the financials sector may be adversely impacted by many factors, including, among others,

government regulations, economic conditions, credit rating downgrades, changes in interest rates, and decreased liquidity in

credit markets. The impact of more stringent capital requirements, recent or future regulation of any individual financial company

or of the financials sector as a whole cannot be predicted. In recent years, cyber attacks and technology malfunctions and failures

have become increasingly frequent in this sector and have caused significant losses to companies in this sector, which may

negatively impact an Underlying Investment.

Geographic Risk

A natural or other disaster could occur in a geographic region in which an Underlying Investment invests, which could affect the

economy or particular business operations of companies in the specific geographic region, causing an adverse impact on an

Underlying Investment’s investments in the affected region.

High Portfolio Turnover Risk

An Underlying Investment may engage in active and frequent trading of its portfolio securities. High portfolio turnover

(considered by each Underlying Investment to mean higher than 100% annually) may result in increased transaction costs to an

Underlying Investment, including brokerage commissions, dealer markups and other transaction costs on the sale of the securities

and on reinvestment in other securities.

Income Risk

An Underlying Investment’s income may decline when yields fall. This decline can occur because an Underlying Investment may

subsequently invest in lower-yielding bonds when bonds in its portfolio mature, near maturity or are called, bonds in the

Underlying Index are substituted, or an Underlying Investment otherwise needs to purchase additional bonds.

Index-Related Risk

There is no guarantee that an Underlying Investment will achieve a high degree of correlation to the Underlying Index and

therefore achieve its investment objective. Market disruptions and regulatory restrictions could have an adverse effect on an

Underlying Investment’s ability to adjust its exposure to the required levels in order to track the Underlying Index. Errors in

index data, index computations and/or the construction of the Underlying Index in accordance with its methodology may occur

from time to time and may not be identified and corrected by the Index Provider for a period of time or at all, which may have an

adverse impact on an Underlying Investment and its shareholders.

Industrials Sector Risk

The industrials sector may be adversely affected by changes in the supply of and demand for products and services, product

obsolescence, claims for environmental damage or product liability and general economic conditions, among other factors.

Interest Rate Risk

An increase in interest rates may cause the value of securities held by an Underlying Investment to decline, may lead to

heightened volatility in the fixed-income markets and may adversely affect the liquidity of certain fixed-income investments. The

current historically low interest rate environment increases the risks associated with rising interest rates.

Information Technology Sector Risk

Information technology companies face intense competition and potentially rapid product obsolescence. They are also heavily

dependent on intellectual property rights and may be adversely affected by the loss or impairment of those rights.

Issuer Risk

13

The performance of an Underlying Investment depends on the performance of individual securities to which an Underlying

Investment has exposure. Changes in the financial condition or credit rating of an issuer of those securities may cause the value of

the securities to decline.

Large-Capitalization Companies Risk

Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions.

Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller

capitalization companies. During different market cycles, the performance of large capitalization companies has trailed the

overall performance of the broader securities markets.

Liquidity Risk

Liquidity risk exists when particular investments are difficult to purchase or sell. This can reduce an Underlying Investment’s

returns because an Underlying Investment may be unable to transact at advantageous times or prices.

Market Risk

An Underlying Investment could lose money over short periods due to short-term market movements and over longer periods

during more prolonged market downturns.

Management Risk

As an Underlying Investment may not fully replicate the Underlying Index, it is subject to the risk that the investment manager’s

investment strategy may not produce the intended results.

Market Trading Risk

An Underlying Investment faces numerous market trading risks, including the potential lack of an active market for fund shares,

losses from trading in secondary markets, periods of high volatility and disruptions in the creation/redemption process. ANY OF

THESE FACTORS, AMONG OTHERS, MAY LEAD TO AN UNDERLYING INVESTMENT’S SHARES TRADING AT A

PREMIUM OR DISCOUNT TO NAV.

Non-Diversification Risk

An Underlying Investment may invest a large percentage of its assets in securities issued by or representing a small number of

issuers. As a result, an Underlying Investment’s performance may depend on the performance of a small number of issuers.

Non-U.S. Issuers Risk

Securities issued by non-U.S. issuers carry different risks from securities issued by U.S. issuers. These risks include differences in

accounting, auditing and financial reporting standards, the possibility of expropriation or confiscatory taxation, adverse changes

in investment or exchange control regulations, political instability, regulatory and economic differences, and potential restrictions

on the flow of international capital. An Underlying Investment may be specifically exposed to European Economic Risk

Operational Risk

An Underlying Investment may be exposed to operational risks arising from a number of factors, including, but not limited to,

human error, processing and communication errors, errors of an Underlying Investment’s service providers, counterparties or

other third-parties, failed or inadequate processes and technology or systems failures. An Underlying Investment and the

investment manager seek to reduce these operational risks through controls and procedures. However, these measures do not

address every possible risk and may be inadequate to address these risks.

Passive Investment Risk

An Underlying Investment may not be actively managed, and the investment manager generally does not attempt to take

defensive positions under any market conditions, including declining markets.

14

Real Estate Investment Risk

Investment in equity securities in the real estate sector is subject to many of the same risks associated with the direct ownership of

real estate, such as adverse changes in national, state, or local real estate conditions (resulting from, for example, oversupply of or

reduced demand for space and changes in market rental rates); obsolescence of properties; changes in the availability, cost, and

terms of mortgage funds; and the impact of tax, environmental, and other laws.

Reliance on Trading Partners Risk

An Underlying Investment may invest in countries or regions whose economies are heavily dependent upon trading with key

partners. Any reduction in this trading may have an adverse impact on an Underlying Investment’s investments. Through its

portfolio companies’ trading partners, An Underlying Investment may be specifically exposed to Asian Economic Risk, European

Economic Risk and North American Economic Risk.

Risk of Investing in Developed Countries

An Underlying Investment’s investment in developed country issuers may subject an Underlying Investment to regulatory,

political, currency, security, economic and other risks associated with developed countries. Developed countries tend to represent

a significant portion of the global economy and have generally experienced slower economic growth than some less developed

countries. In addition, developed countries may be adversely impacted by changes to the economic conditions of certain key

trading partners, regulatory burdens, debt burdens and the price or availability of certain commodities.

Risk of Investing in the United States

An Underlying Investment may have significant exposure to U.S. issuers. Certain changes in the U.S. economy, such as when the

U.S. economy weakens or when its financial markets decline, may have an adverse effect on the securities to which an

Underlying Investment has exposure.

Securities Lending Risk

An Underlying Investment may engage in securities lending. Securities lending involves the risk that an Underlying Investment

may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. An

Underlying Investment could also lose money in the event of a decline in the value of collateral provided for loaned securities or

a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for

an Underlying Investment.

Sovereign and Quasi-Sovereign Obligations Risk

An Underlying Investment may invest in securities issued by or guaranteed by non-U.S. sovereign governments and by entities

affiliated with or backed by non U.S. sovereign governments, which may be unable or unwilling to repay principal or interest

when due. In times of economic uncertainty, the prices of these securities may be more volatile than those of corporate debt

obligations or of other government debt obligations.

Structural Risk

The countries in which an Underlying Investment invests may be subject to considerable degrees of economic, political and social

instability.

Tax Risk

An Underlying Investment may invest in derivatives. The federal income tax treatment of a derivative may not be as favorable as

a direct investment in an underlying asset. Derivatives may produce taxable income and taxable realized gain. Derivatives may

adversely affect the timing, character and amount of income an Underlying Investment realizes from its investments. As a result,

15

a larger portion of an Underlying Investment’s distributions may be treated as ordinary income rather than as capital gains. In

addition, certain derivatives are subject to mark-to-market or straddle provisions of the Internal Revenue Code of 1986, as

amended (the “Internal Revenue Code”). If such provisions are applicable, there could be an increase (or decrease) in the amount

of taxable dividends paid by an Underlying Investment. Income from swaps is generally taxable. In addition, the tax treatment of

certain derivatives, such as swaps, is unsettled and may be subject to future legislation, regulation or administrative

pronouncements issued by the U.S. Internal Revenue Service (“IRS”). As part of an Underlying Investment’s currency hedging

strategy, an Underlying Investment may match foreign currency forward contracts with the non-U.S. dollar denominated

securities whose currency risk is intended to be hedged wholly or partially by such contracts. If an Underlying Investment were to

perform such matching for income tax purposes, this matching would potentially result in an Underlying Investment’s deferral for

U.S. federal income tax purposes of the realized gains or losses attributable to foreign currency forward contracts until such gains

or losses offset the currency related losses on the matched non-U.S. dollar denominated securities. If the IRS were to disagree

with such deferral treatment or the matching methodology used, an Underlying Investment’s income could become undistributed

and incur tax liabilities. An Underlying Investment may reevaluate, adjust, begin, or discontinue the matching of such contracts in

the future.

Tracking Error Risk

Tracking error is the divergence of an Underlying Investment’s performance from that of the applicable underlying index.

Tracking error may occur because of differences between the securities and other instruments held in an Underlying Investment’s

portfolio and those included in the applicable underlying index, pricing differences, differences in transaction costs, an

Underlying Investment’s holding of uninvested cash, differences in timing of the accrual of or the valuation of dividends or

interest, tax gains or losses, changes to the applicable underlying index or the costs to an Underlying Investment of complying

with various new or existing regulatory requirements. This risk may be heightened during times of increased market volatility or

other unusual market conditions. Tracking error also may result because an Underlying Investment incurs fees and expenses,

while the applicable underlying index does not.

Treasury Obligations Risk

Treasury obligations may differ from other S-11 securities in their interest rates, maturities, times of issuance and other

characteristics and may provide relatively lower returns than those of other securities. Similar to other issuers, changes to the

financial condition or credit rating of a government may cause the value of an Underlying Investment’s treasury obligations to

decline.

Valuation Risk

The price an Underlying Investment could receive upon sale of a security or unwind of a financial instrument or other asset may

differ from an Underlying Investment’s valuation of the security, instrument or other asset and from the value used by the

Underlying Index, particularly for securities or other instruments that trade in low volume or volatile markets or that are valued

using a fair value methodology. In addition, the value of the securities or other instruments in an Underlying Investment’s

portfolio may change on days or during time periods when shareholders will not be able to purchase or sell an Underlying

Investment’s shares.

Principal Risk Factors of the Schwab ETFs

Concentration Risk

To the extent that an Underlying Investment’s or the index’s portfolio is concentrated in the securities of issuers in a particular

market, industry, group of industries, sector or asset class (including the real estate industry, as described above), an Underlying

Investment may be adversely affected by the performance of those securities, may be subject to increased price volatility and may

be more vulnerable to adverse economic, market, political or regulatory occurrences affecting that market, industry, group of

industries, sector or asset class.

Derivatives Risk

16

An Underlying Investment’s use of derivative instruments involves risks different from, or possibly greater than, the risks

associated with investing directly in securities and other traditional investments. An Underlying Investment’s use of derivatives

could reduce an Underlying Investment’s performance, increase an Underlying Investment’s volatility and could cause an

Underlying Investment to lose more than the initial amount invested. In addition, investments in derivatives may involve

leverage, which means a small percentage of assets invested in derivatives can have a disproportionately large impact on an

Underlying Investment.

Equity Risk

The prices of equity securities rise and fall daily. These price movements may result from factors affecting individual companies,

industries or the securities market as a whole. In addition, equity markets tend to move in cycles which may cause stock prices to

fall over short or extended periods of time.

Investment Style Risk

An Underlying Investment may not be actively managed. Therefore, an Underlying Investment follows the securities included in

the index during upturns as well as downturns. Because of its indexing strategy, an Underlying Investment does not take steps to

reduce market exposure or to lessen the effects of a declining market. In addition, because of an Underlying Investment’s

expenses, an Underlying Investment’s performance may be below that of the index.

Large-Cap Company Risk

Large-cap companies are generally more mature and the securities issued by these companies may not be able to reach the same

levels of growth as the securities issued by small- or mid-cap companies.

Liquidity Risk

An Underlying Investment may be unable to sell certain securities, such as illiquid securities, readily at a favorable time or price,

or an Underlying Investment may have to sell them at a loss.

Market Risk

Financial markets rise and fall in response to a variety of factors, sometimes rapidly and unpredictably. As with any investment

whose performance is tied to these markets, the value of an investment in an Underlying Investment will fluctuate, which means

that an investor could lose money over short or long periods.

Market Capitalization Risk

Securities issued by companies of different market capitalizations tend to go in and out of favor based on market and economic

conditions. During a period when securities of a particular market capitalization fall behind other types of investments, an

Underlying Investment’s performance could be impacted.

Market Trading Risk

Although fund shares are listed on national securities exchanges, there can be no assurance that an active trading market for fund

shares will develop or be maintained. If an active market is not maintained, investors may find it difficult to buy or sell fund

shares. Shares of an Underlying Investment may trade at prices other than NAV. Underlying Investment shares may be bought

and sold in the secondary market at market prices. Although it is expected that the market price of the shares of an Underlying

Investment will approximate an Underlying Investment’s net asset value (NAV), there may be times when the market price and

the NAV vary significantly. An investor may pay more than NAV when buying shares of an Underlying Investment in the

secondary market, and an investor may receive less than NAV when selling those shares in the secondary market. The market

price of fund shares may deviate, sometimes significantly, from NAV during periods of market volatility.

Mid-Cap Company Risk

17

Mid-cap companies may be more vulnerable to adverse business or economic events than larger, more established companies and

the value of securities issued by these companies may move sharply.

Real Estate Investment Risk

Due to the composition of the index, an Underlying Investment concentrates its investments in real estate companies and

companies related to the real estate industry. As such, an Underlying Investment is subject to risks associated with the direct

ownership of real estate securities and an investment in an Underlying Investment will be closely linked to the performance of the

real estate markets. These risks include, among others: declines in the value of real estate; risks related to general and local

economic conditions; possible lack of availability of mortgage funds or other limits to accessing the credit or capital markets;

defaults by borrowers or tenants, particularly during an economic downturn; and changes in interest rates.

REITs Risk

In addition to the risks associated with investing in securities of real estate companies and real estate related companies, REITs

are subject to certain additional risks. Equity REITs may be affected by changes in the value of the underlying properties owned

by the trusts. Further, REITs are dependent upon specialized management skills and cash flows, and may have their investments

in relatively few properties, or in a small geographic area or a single property type. Failure of a company to qualify as a REIT

under federal tax law may have adverse consequences to an Underlying Investment. In addition, REITs have their own expenses,

and an Underlying Investment will bear a proportionate share of those expenses.

Securities Lending Risk

Securities lending involves the risk of loss of rights in, or delay in recovery of, the loaned securities if the borrower fails to return

the security loaned or becomes insolvent.

Small-Cap Company Risk

Securities issued by small-cap companies may be riskier than those issued by larger companies, and their prices may move

sharply, especially during market upturns and downturns.

Tracking Error Risk

As an index fund, an Underlying Investment seeks to track the performance of its index, although it may not be successful in

doing so. The divergence between the performance of an Underlying Investment and the index, positive or negative, is called

“tracking error.” Tracking error can be caused by many factors and it may be significant.

OTHER UNDERLYING FUND CHANGES

On or about December 1, 2017, the Underlying Funds in each of the Core Bond Index Portfolio, the International Equity

Index Portfolio and the TIPS Index Portfolio will change as follows:

Portfolio Portfolio’s Existing Underlying

Investment

Portfolio’s New Underlying Investment

Core Bond Index

Portfolio

iShares Core Total U.S. Bond Market

ETF

Schwab Aggregate Bond ETF

International Equity

Index Portfolio

iShares Core MSCI Total Institutional

Stock ETF

Schwab International Equity ETF

TIPS Index Portfolio iShares TIPS Bond ETF Vanguard Short-Term Inflation Protected

Securities ETF

18

9. On or about December 1, 2017, the following replaces the section entitled “Core Bond Index Portfolio” on page

31 of the Disclosure Statement:

Investment Objective:

The Portfolio’s goal is to track as closely as possible, before fees and expenses, the total return of the Bloomberg Barclays U.S.

Aggregate Bond Index.

Investment Strategy:

The Portfolio invests substantially all of its assets in Schwab Aggregate Bond ETF. To pursue its goal, the fund generally invests

in securities that are included in the Bloomberg Barclays U.S. Aggregate Bond Index. The index is a broad-based benchmark

measuring the performance of the U.S. investment grade, taxable bond market, including U.S. Treasuries, government-related and

corporate bonds, mortgage pass-through securities, commercial mortgage-backed securities, and asset-backed securities that are

publicly available for sale in the United States. To be eligible for inclusion in the index, securities must be fixed rate, non-

convertible, U.S. dollar denominated with at least $250 million or more of outstanding face value and have one or more years

remaining to maturity. The index excludes certain types of securities, including tax-exempt state and local government series

bonds, structured notes embedded with swaps or other special features, private placements, floating rate securities, inflation-

linked bonds and Eurobonds. The index is market capitalization weighted and the securities in the index are updated on the last

business day of each month.

As of March 31, 2017, there were approximately 9,304 securities in the index. It is the fund’s policy that under normal

circumstances it will invest at least 90% of its net assets (net assets plus borrowings for investment purposes) in securities

included in the index, including To Be Announced (TBA) transactions, as defined below. The fund will notify its shareholders at

least 60 days before changing this policy.

Under normal circumstances, the fund may invest up to 10% of its net assets in securities not included in its index. The principal

types of these investments include those that the Investment Manager believes will help the fund track the index, such as

investments in (a) securities that are not represented in the index but the Investment Manager anticipates will be added to the

index; (b) high-quality liquid short-term investments, such as securities issued by the U.S. government, its agencies or

instrumentalities, including obligations that are not guaranteed by the U.S. Treasury, and obligations that are issued by private

issuers that are guaranteed as to principal or interest by the U.S. government, its agencies or instrumentalities; (c) other

investment companies; and (d) derivatives, principally futures contracts. The fund may use futures contracts and other derivatives

primarily to help manage interest rate exposure. The fund may also invest in cash, cash equivalents and money market funds, and

lend its securities to minimize the difference in performance that naturally exists between an index fund and its corresponding

index.

Because it is not possible or practical to purchase all of the securities in the index, the fund’s Investment Manager will seek to

track the total return of the index by using statistical sampling techniques. These techniques involve investing in a limited number

of index securities that, when taken together, are expected to perform similarly to the index as a whole. These techniques are

based on a variety of factors, including interest rate and yield curve risk, maturity exposures, industry, sector and issuer weights,

credit quality, and other risk factors and characteristics.

The fund generally expects that its weighted average duration will closely correspond to the weighted average duration of the

index, which as of March 31, 2017, was 5.82 years. As of March 31, 2017, approximately 28.34% of the bonds represented in the

index were U.S. fixed-rate agency mortgage pass-through securities. U.S. fixed rate agency mortgage pass-through securities are

securities issued by entities such as Fannie Mae and Freddie Mac that are backed by pools of mortgages. Most transactions in

fixed-rate mortgage pass-through securities occur through standardized contracts for future delivery in which the exact mortgage

pools to be delivered are not specified until a few days prior to settlement, and are often referred to as “to-be-announced

transactions” or “TBA transactions.” In a TBA transaction, the buyer and seller agree upon general trade parameters such as

agency, settlement date, par amount and price. The actual pools delivered generally are determined two days prior to settlement

date; however, it is not anticipated that the fund will receive the pools, but will instead participate in rolling TBA transactions.

The fund anticipates that it may enter into such contracts on a regular basis. This may result in a significantly higher portfolio

turnover for the fund than a typical index fund.

The fund, pending settlement of such contracts, will invest its assets in high-quality liquid short-term instruments, including

Treasury securities and shares of money market mutual funds. The fund will assume its pro rata share of the fees and expenses of

any money market fund that it may invest in, in addition to the fund’s own fees and expenses. The fund will concentrate its

19

investments (i.e., hold 25% or more of its total assets) in a particular industry, group of industries or sector to approximately the

same extent that its index is so concentrated. For purposes of this limitation, securities of the U.S. government (including its

agencies and instrumentalities), and repurchase agreements collateralized by U.S. government securities are not considered to be

issued by members of any industry.

The Investment Manager seeks to achieve, over time, a correlation between the fund’s performance and that of its index, before

fees and expenses, of 95% or better. However, there can be no guarantee that the fund will achieve a high degree of correlation

with the index. A number of factors may affect the fund’s ability to achieve a high correlation with its index, including the degree

to which the fund uses a sampling technique. The correlation between the performance of the fund and its index may also diverge

due to transaction costs, asset valuations, timing variances, and differences between the fund’s portfolio and the index resulting

from legal restrictions (such as diversification requirements) that apply to the fund but not to the index.

10. On or about December 1, 2017, the following replaces the section entitled “International Equity Index Portfolio”

on page 32 of the Disclosure Statement:

Investment Objective:

The Portfolio’s goal is to track as closely as possible, before fees and expenses, the total return of the FTSE Developed ex US

Index.

Fund Strategy:

The Portfolio invests substantially all of its assets in Schwab International Equity ETF. To pursue its goal, the fund generally

invests in stocks that are included in the FTSE Developed ex US Index. The index is comprised of large and mid-capitalization

companies in developed countries outside the United States, as defined by the index provider. The index defines the large and

mid-capitalization universe as approximately the top 90% of the eligible universe. As of August 31, 2016, the index was

composed of 1,479 stocks in 24 developed market countries.

It is the fund’s policy that under normal circumstances it will invest at least 90% of its net assets in these stocks, including

depositary receipts representing securities of the index; depository receipts may be in the form of American Depositary receipts

(ADRs), Global Depositary receipts (GDRs) and European Depositary receipts (EDRs). The fund will notify its shareholders at

least 60 days before changing this policy. The fund may sell securities that are represented in the index in anticipation of their

removal from the index, or buy securities that are not yet represented in the index in anticipation of their addition to the index.

Under normal circumstances, the fund may invest up to 10% of its net assets in securities not included in the index. The principal

types of these investments include those that the Investment Manager believes will help the fund track the index, such as

investments in (a) securities that are not represented in the index but the Investment Manager anticipates will be added to the

index or as necessary to reflect various corporate actions (such as mergers and spin-offs), (b) other investment companies, and (c)

derivatives, principally futures contracts. The fund may use futures contracts and other derivatives primarily to seek returns on the

fund’s otherwise uninvested cash assets to help it better track the index. The fund may also invest in cash and cash equivalents,

and may lend its securities to minimize the difference in performance that naturally exists between an index fund and its

corresponding index. The fund does not hedge its exposure to foreign currencies.

Because it may not be possible or practicable to purchase all of the stocks in the index, the Investment Manager seeks to track the

total return of the index by using statistical sampling techniques. These techniques involve investing in a limited number of index

securities which, when taken together, are expected to perform similarly to the index as a whole. These techniques are based on a

variety of factors, including performance attributes, tax considerations, country weightings, capitalization, industry factors, risk

factors and other characteristics.

The fund will concentrate its investments (i.e., hold 25% or more of its total assets) in a particular industry, group of industries or

sector to approximately the same extent that the index is so concentrated. For purposes of this limitation, securities of the U.S.

government (including its agencies and instrumentalities), and repurchase agreements collateralized by U.S. government

securities are not considered to be issued by members of any industry. The Investment Manager seeks to achieve, over time, a

correlation between the fund’s performance and that of the index, before fees and expenses, of 95% or better. However, there can

be no guarantee that the fund will achieve a high degree of correlation with the index. A number of factors may affect the fund’s

ability to achieve a high correlation with the index, including the degree to which the fund utilizes a sampling technique. The

correlation between the performance of the fund and the index may also diverge due to transaction costs, asset valuations,

20

corporate actions (such as mergers and spin-offs), timing variances, and differences between the fund’s portfolio and the index

resulting from legal restrictions (such as diversification requirements) that apply to the fund but not to the index.

11. On or about December 1, 2017, the following replaces the section entitled “TIPS Index Portfolio” on page 32 of

the Disclosure Statement:

Investment Objective:

The Portfolio seeks to track the performance of a benchmark index that measures the investment return of inflation-protected

public obligations of the U.S. Treasury with remaining maturities of less than 5 years.

Investment Strategy:

The Portfolio invests substantially all of its assets in Vanguard Short-Term Inflation Protected Securities ETF. The fund employs

an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Treasury Inflation-Protected

Securities (TIPS) 0-5 Year Index. The Index is a market-capitalization-weighted index that includes all inflation-protected public

obligations issued by the U.S. Treasury with remaining maturities of less than 5 years. The fund attempts to replicate the target

index by investing all, or substantially all, of its assets in the securities that make up the Index, holding each security in

approximately the same proportion as its weighting in the Index. The fund maintains a dollar-weighted average maturity

consistent with that of the target index, which generally does not exceed 3 years.

12. On or about December 1, 2017, the following is inserted in front of the section entitled “Other Individual

Portfolios” on page 36 of the Disclosure Statement:

Principal Risk Factors of the Vanguard Portfolios

As with any investment, your investment in the Vanguard Portfolios could lose money or the Portfolios’ performance could

trail that of other investments. Each Portfolio has a different level of risk. The information provided below is only a summary

of the main risks of the Underlying Investments composed of Vanguard ETFs. Each Underlying Investment’s current

prospectus and statement of additional information contains additional information not summarized herein and identifies

additional principal risks to which the respective Underlying Investment may be subject. You should check with your

Financial Advisor to understand the specific risks associated with each Vanguard Portfolio.

For a discussion of China A-shares risk, Country/regional risk, Currency risk, Emerging markets risk, Index sampling

risk, and Stock market risk, please see Principal Risk Factors of the Vanguard ETFs above.

ETF Trading, The fund’s ETF shares are listed for trading on Nasdaq and are bought and sold on the secondary market at market

prices. Although it is expected that the market price of an ETF Share typically will approximate its net asset value (NAV), there

may be times when the market price and the NAV differ significantly. Thus, you may pay more or less than NAV when you buy

ETF shares on the secondary market, and you may receive more or less than NAV when you sell those shares.

Although the fund’s ETF shares are listed for trading on Nasdaq, it is possible that an active trading market may not be

maintained.

Trading of the fund’s ETF shares may be halted by the activation of individual or marketwide trading halts (which halt trading for

a specific period of time when the price of a particular security or overall market prices decline by a specified percentage).

Trading of the fund’s ETF shares may also be halted if (1) the shares are delisted from Nasdaq without first being listed on

another exchange or (2) Nasdaq officials determine that such action is appropriate in the interest of a fair and orderly market or

for the protection of investors.

Income fluctuations. The fund’s quarterly income distributions are likely to fluctuate considerably more than the income

distributions of a typical bond fund. In fact, under certain conditions, the fund may not have any income to distribute. Income

fluctuations associated with changes in interest rates are expected to be low; however, income fluctuations associated with