Embed Size (px)

Citation preview

Please file this Supplement to the CollegeChoice 529 Direct Savings Plan Disclosure Booklet with your records.

CSIND-05719

SUPPLEMENT DATED JUNE 2018 TO THE COLLEGECHOICE 529 DIRECT SAVINGS PLAN

DISCLOSURE BOOKLET DATED NOVEMBER 2014

This Supplement describes important changes affecting the CollegeChoice 529 Direct Savings Plan. Unless otherwise indicated,

capitalized terms have the same meaning as those in the Disclosure Booklet.

TAX REFORM UPDATE

In May 2018, Indiana Code Section 6-3-3-12 was amended (Amendment) to create a tax credit for those saving for tuition

expenses in connection with enrollment or attendance at an elementary or secondary public, private or religious school

located in Indiana (Indiana K-12 Tuition).

For the tax year beginning January 1, 2018, Indiana taxpayers (resident or non-resident) filing a single or joint return may

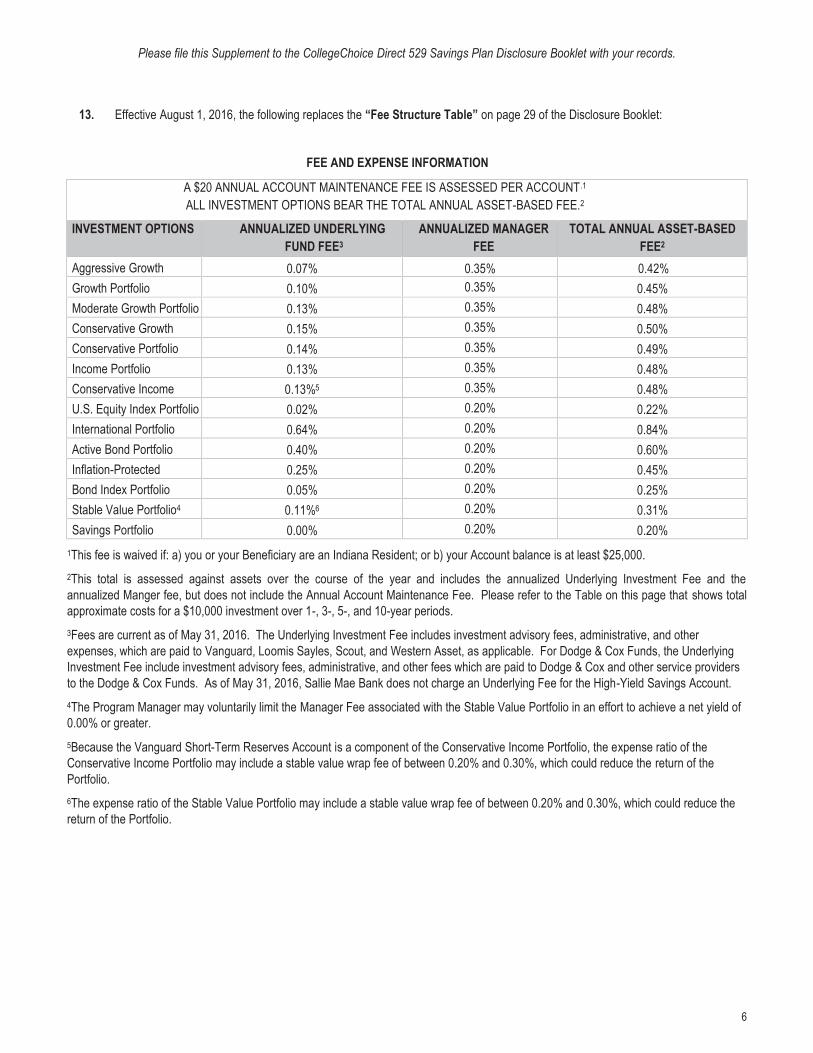

receive a ten percent (10%) Indiana state income tax credit against their Indiana adjusted gross income tax liability, up to a

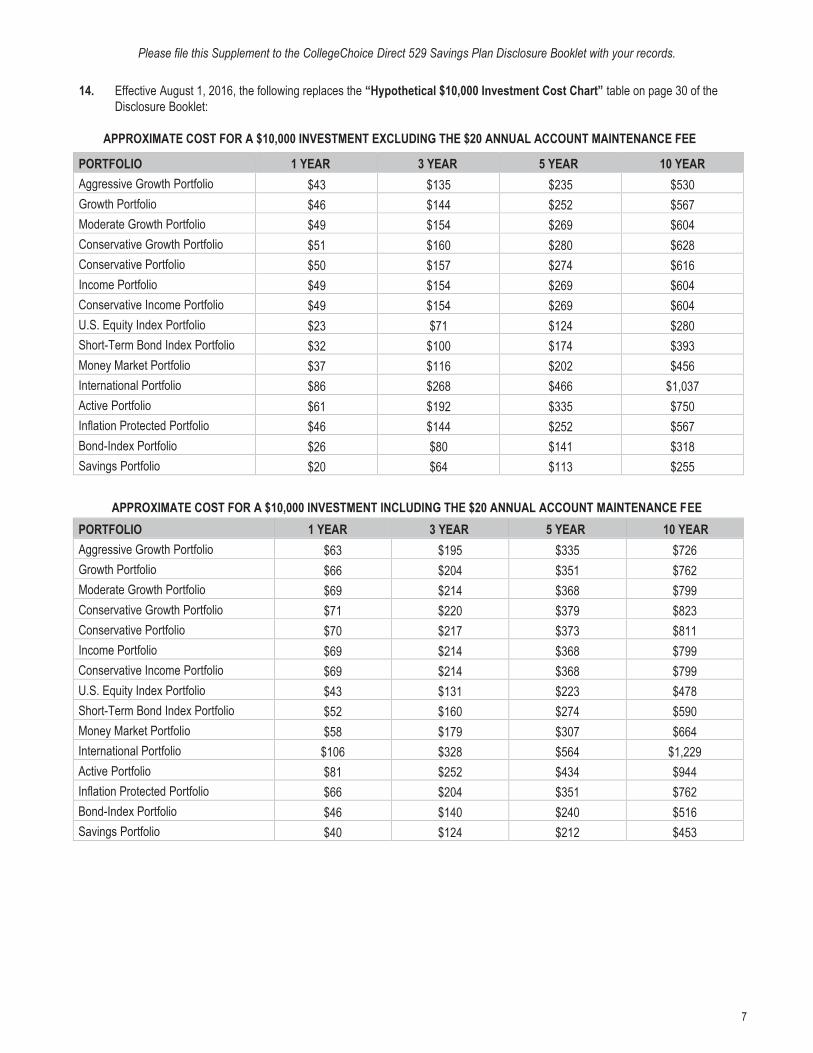

maximum of $500 for contributions to an Account that will be used to pay for Indiana K-12 Tuition. When combined with

the Indiana state income tax credit taken for Indiana Qualified Higher Education Expenses, the maximum annual income

tax credit cannot exceed $1000.

Effective January 1, 2019, the income tax credit for contributions made to an Account that will be used to pay Indiana K-12

Tuition increases to twenty percent (20%) up to a maximum, when combined with any Indiana state income tax credit

taken for Indiana Qualified Higher Education Expenses, of $1000.

Also effective January 1, 2019, at the time a contribution is made to an Account, the contributor must designate whether

the contribution is made for (i) Qualified Expenses that are not Indiana K-12 Tuition; or (ii) Indiana K-12 Tuition. Likewise,

at the time of a withdrawal from an Account, the Account Owner must designate whether the withdrawal will be used for

(i) Qualified Expenses that are not Indiana K-12 Tuition; or (ii) Indiana K-12 Tuition.

The Amendment also specifies that the Indiana income tax credit is not available for money credited to an Account that

will be transferred to an ABLE account (as defined in Section 529A of the Internal Revenue Code).

Accordingly, the following changes are made to the Disclosure Booklet:

1. The following replaces the question entitled “How does the Indiana state income tax credit work?” starting on page 6 of

the Disclosure Booklet:

How does the Indiana state income tax credit work?

If you are an Indiana taxpayer (resident or non-resident) filing a single or joint return, you may receive:

a 20% Indiana state income tax credit against your Indiana adjusted gross income tax liability, up to a maximum

of $1,000, for contributions to an Account that will be used to pay for Indiana Qualified Higher Education

Expenses;

For the tax year beginning January 1, 2018, a 10% Indiana state income tax credit against your Indiana adjusted

gross income tax liability, up to a maximum of $500, for contributions to an Account that will be used to pay for

Indiana K-12 Tuition. When combined with the Indiana state income tax credit taken for Indiana Qualified Higher

Education Expenses, the maximum annual state income tax credit cannot exceed $1000.; and

Effective January 1, 2019, a 20% Indiana state income tax credit against your Indiana adjusted gross income tax

liability, up to a maximum of $1000 when combined with any state income tax credit taken for Indiana Qualified

Higher Education Expenses, for contributions to an Account that will be used to pay for Indiana K-12 Tuition.

You do not need to be the Account Owner to take the Indiana state income tax credit. We will generally treat

contributions sent by U.S. mail as having been made in a given year if checks are postmarked on or before December 31

of the applicable year, and provided the checks are subsequently paid. For electronic contributions, we will generally treat

contributions received by us in a given year as having been made in that year if you initiate them on or before December

31 of that year and the funds are successfully deducted from your checking or savings account at another financial

CSIND-05719

institution. See How to Open and Fund Your Account - Contribution Date starting on page 13.

The Indiana state income tax credit is also available for contributions to both the CollegeChoice Advisor 529 Savings Plan

(CollegeChoice Advisor) and the CollegeChoice CD 529 Savings Plan (CollegeChoice CD) by individual Indiana taxpayers,

filing a single return or, to a married couple, filing a joint return. However, the maximum annual Indiana state income tax

credit that an Indiana taxpayer may receive cannot exceed the amounts described above. You (as the Account Owner)

may be subject to recapture of the tax credit in the event that you take certain Non-Qualified Distributions or a

distribution for K-12 Tuition for a school outside Indiana. For additional information, including how to calculate the

amount of the Indiana state income tax credit, please see State Tax Issues starting on page 55.

2. The following question is added to page 9 of the Disclosure Booklet.

Can I use my Account for K-12 Tuition?

Yes. On December 22, 2017, new federal tax reform legislation, Public Law 115-97 (H.R. 1) was signed into law. The law

amended Section 529 of the Code to permit withdrawals from 529 Plan accounts up to $10,000 per year per student (in

the aggregate across all Qualified Tuition Programs for that student) for tuition expenses in connection with enrollment

and attendance at an elementary or secondary public, private or religious school.

Under Indiana law, contributions that will be used to pay Indiana K-12 Tuition are eligible for the Indiana income tax

credit. Withdrawals taken to pay K-12 Tuition for a school outside Indiana will be subject to recapture of the Indiana state

income tax credit. For additional information, including how to calculate the amount of the Indiana state income tax

credit, please see State Tax Issues starting on page 55.

3. The following is added after the section titled “Minimum Contributions” on page 13.

Designation of Contributions. Effective no later than January 1, 2019, when making contributions to your Account, you

will be required to designate whether the contribution will be used for (i) Qualified Expenses that are not Indiana K-12

Tuition; or (ii) Indiana K-12 Tuition. If you contribute to your Account by AIP, all AIP contributions will be allocated to the

category of education savings you designate when you initiate the AIP unless you notify us that future contributions by

AIP will be designated for a different category of education savings.

4. The following replaces the section titled “Procedures for Distributions” on page 20.

Procedures for Distributions. Only the Account Owner may direct distributions from your Account. Qualified Distributions

made payable to the Account Owner, the Beneficiary or an Eligible Educational Institution may be requested online or by

phone by providing verifying Account information upon request. Otherwise you may call Client Service at 1-866-485-9415

to receive a Distribution Request Form or download the form on our website at www.collegechoicedirect.com. In order

for us to process a distribution request, you must complete and submit the distribution request form to us in good order

and provide such other information or documentation as we may, from time to time, require. Effective no later than

January 1, 2019, when taking a distribution from your Account, you will be required to designate whether the distribution

will be used for (i) Qualified Expenses that are not Indiana K-12 Tuition; or (ii) Indiana K-12 Tuition.

We will generally process a distribution from an Account within three (3) business days of accepting the request. During

periods of market volatility and at year-end, distribution requests may take up to five (5) business days to process. Please

allow ten (10) business days for the proceeds to reach you. We may also establish a minimum distribution amount and/or

charge a Fee for distributions made by federal wire.

5. The following replaces the first paragraph of the section titled “Other Distributions” on page 20.

Other Distributions. The distributions discussed below are not subject to the Distribution Tax. Except for a Rollover

Distribution, a Refunded Distribution and an ABLE Rollover Distribution, the earnings portion of each distribution

discussed will be subject to federal and to any applicable state income taxes. ABLE Rollover Distributions may be subject

to a recapture tax in Indiana (See Taxes – Federal Tax Issues - Transfers and Rollovers on page 54 and State Tax Issues on

CSIND-05719

page 55.) You should consult a tax advisor regarding the application of federal and state tax laws if you take any of these

distributions:

6. The following is added after the paragraph titled “Rollover Distributions” on page 21.

ABLE Rollover Distribution.

To qualify as an ABLE Rollover Distribution, you must reinvest the amount distributed from your Account into a Qualified

ABLE Program within 60 days of the distribution date. ABLE Rollover Distributions may be subject to certain state taxes

but are generally exempt from federal income taxes and the Distribution Tax. The Indiana Department of Revenue has

not provided information on whether an ABLE Rollover Distribution may also be subject to a recapture tax. Indiana state

taxation of ABLE Rollover Distributions is discussed in State Tax Issues starting on page 55.

7. The paragraph titled “Tax Considerations; Tax Credit Recapture” on page 35 is of the Disclosure Booklet is replaced in its

entirety as follows.

Tax Considerations; Tax Credit Recapture.

The federal and state tax consequences associated with participating in the Plan can be complex. In particular, you, as the

Account Owner (not the contributor), must repay all or part, depending on the circumstances, of the Indiana state income

tax credit claimed in prior taxable years by any contributors to your Account if you take a Recapture Distribution from your

Account. (See Taxes - State Tax Issues - Recapture of Income Tax Credit on page 56.) You should consult a tax advisor

regarding the application of tax laws to your particular circumstances.

8. The following is added to the end of the section titled “Risks” beginning on page 34.

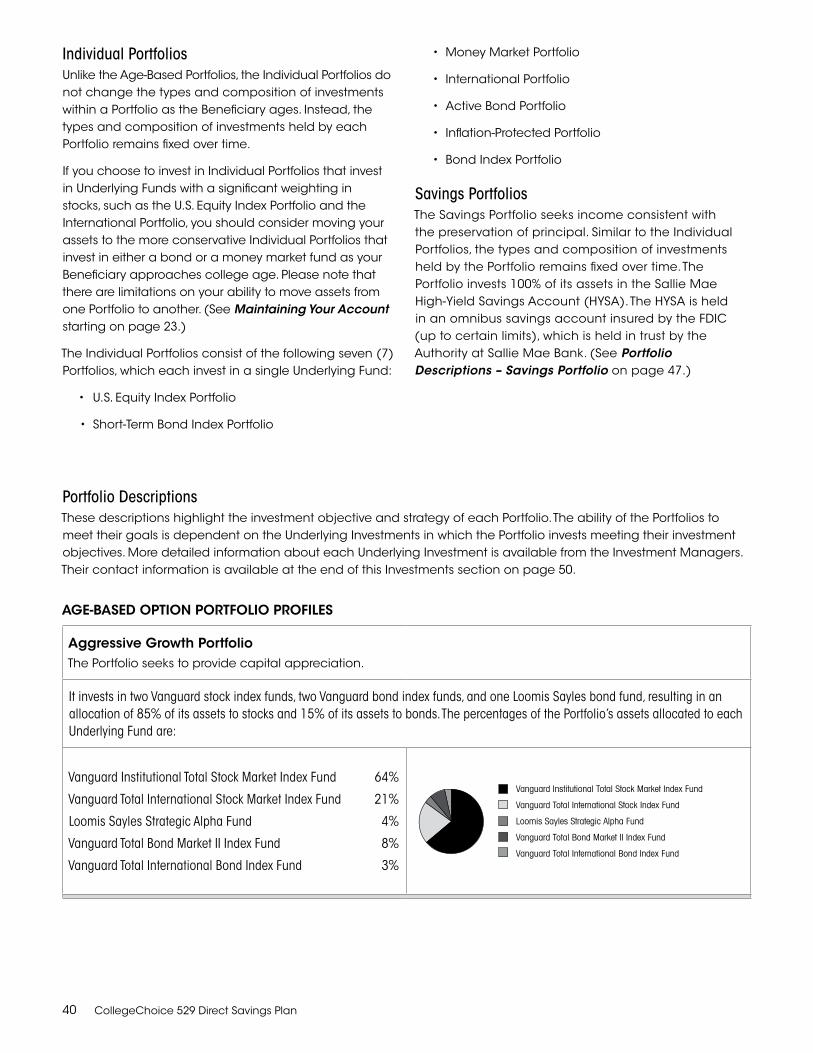

Investment Options Not Designed for Elementary and Secondary Tuition.

The Investment Options we offer through the Plan have been designed exclusively for you to save for Qualified Expenses.

They have not been designed to assist you in reaching your K-12 Tuition savings goals. Specifically, the Year of Enrollment

Portfolios are designed for Account Owners seeking to automatically invest in progressively more conservative Portfolios

as their Beneficiary approaches college age. The Year of Enrollment Portfolios’ time horizon and withdrawal periods may

not match those needed to meet your K-12 Tuition savings goals, which may be significantly shorter. In addition, if you

are saving for K-12 Tuition and wish to invest in the Individual Portfolios and the Savings Portfolio, please note that these

Portfolios are comprised of fixed investments. This means that your assets will remain invested in that Portfolio until you

direct us to move them to a different Portfolio. Please consult a qualified tax or investment advisor about your personal

circumstances.

9. The following paragraph is added in the section entitled “Investment Choices” at the bottom of page 38.

The Investment Options have been designed exclusively for you to save for Qualified Expenses. They have not been designed to assist you in saving for K-12 Tuition. Specifically, the Year of Enrollment Portfolios’ time horizon and withdrawal periods may not match those needed to meet your K-12 Tuition savings goals, which may be significantly shorter.

10. The following new paragraph is inserted after the Transfers and Rollovers paragraph on page 54 in the section entitled

“Federal Tax Issues”.

ABLE Rollover Distributions.

Where a distribution is placed in a Qualified ABLE Program account within 60 days of the distribution date, you may avoid

incurring federal income tax or a Distribution Tax if the transfer is for the same Beneficiary or for a Member of the Family

of the Beneficiary. Any distribution must be made before January 1, 2026 and cannot exceed the annual Qualified ABLE

Program $15,000 contribution limit.

Changes in your Beneficiary could potentially cause gift and/or generation-skipping transfer tax consequences to you and

CSIND-05719

your Beneficiary. Because gift and generation-skipping transfer tax issues are complex, you should consult with your tax

advisor.

11. The following replaces the section titled “Qualified Expense Distributions” on page 55 in the section entitled “Federal

Tax Issues”.

Qualified Expense Distributions. If you take a distribution from your Account to pay for Qualified Expenses, your

Beneficiary generally does not have to include as income any earnings distributed for the applicable taxable year if the

total distributions for that year are less than or equal to the total distributions for Qualified Expenses for that year minus

any tax-free Educational Assistance and expenses considered in determining any American Opportunity or Lifetime

Learning Credits claimed for that taxable year.

You, or your Beneficiary, as applicable, are responsible for determining the amount of the earnings portion of any

distribution from your Account that may be taxable and are responsible for reporting any earnings that must be included

in taxable income. You should consult with your tax advisor for further information.

12. The following replaces the section titled “Non-Qualified Distributions” on page 55 in the section entitled “Federal Tax

Issues”.

Non-Qualified Distributions. You, or the Beneficiary, as applicable, are subject to federal and state income tax and the

Distribution Tax on the earnings portion of any distribution that is not exempt from tax as described above. You will also

be subject to a recapture of the Indiana state income tax credit with respect to any Non-Qualified Distribution and certain

other withdrawals as discussed in State Tax Issues - Recapture of Income Tax Credit on page 56.

13. The paragraph titled “Income Tax Credit for Indiana Taxpayers” beginning on page 55 is of the Disclosure Booklet is

replaced in its entirety as follows:

Income Tax Credit for Indiana Taxpayers. If you are an individual Indiana taxpayer (resident or non-resident), filing a

single or joint return, you may receive an Indiana state income tax credit as discussed below. The contributor does not

need to be the Account Owner of an Account.

Income Tax Credit for Tax Years 2017 and earlier. For tax years prior to 2018, if you are an individual Indiana taxpayer

(resident or non-resident), filing a single or joint return, you may receive an Indiana state income tax credit against your

Indiana adjusted gross income tax liability for contributions to an Account that will be used to pay Indiana Qualified Higher

Education Expenses. The amount of the credit is the lesser of the following:

a. twenty percent (20%) of the amount of each contribution that will be used to pay Indiana Qualified Higher

Education Expenses during the taxable year;

b. one thousand dollars ($1,000); or

c. the amount of the taxpayer’s adjusted gross income tax liability for the taxable year reduced by the sum of all other

credits allowed.

Income Tax Credit for Tax Year 2018. For the tax year beginning January 1, 2018, if you are an Indiana taxpayer (resident

or non-resident), filing a single or joint return, you may receive an Indiana state income tax credit against your Indiana

adjusted gross income tax liability for contributions to an Account that will be used to pay Indiana Qualified Higher

Education Expenses and Indiana K-12 Tuition. The amount of the credit is the lesser of the following:

1. twenty percent (20%) of the amount of each contribution that will be used to pay Indiana Qualified Higher Education Expenses during the taxable year plus the lesser of ten percent (10%) of the amount of each contribution that will be used to pay Indiana K-12 Tuition during the taxable year or five hundred dollars ($500);

2. one thousand dollars ($1,000); or

3. the amount of the taxpayer’s adjusted gross income tax liability for the taxable year reduced by the sum of all

other credits allowed.

CSIND-05719

For example, if you are eligible to claim an Indiana state income tax credit for tax year 2018 for contributions to your

Account to pay Indiana Qualified Higher Education Expenses of seven hundred dollars ($700), you will be eligible for a

credit of no more than three hundred dollars ($300) for contributions made to pay Indiana K-12 Tuition, assuming no

other income tax credits are claimed.

Income Tax Credit Beginning Tax Year 2019. Effective January 1, 2019, the income tax credit for contributions made to an

Account that will be used to pay Indiana K-12 Tuition increases to twenty percent (20%). The amount of the credit is the

lesser of the following:

1. twenty percent (20%) of the amount of each contribution that will be used to pay Indiana Qualified Higher

Education Expenses during the taxable year plus twenty percent (20%) of the amount of each contribution that will be

used to pay Indiana K-12 Tuition during the taxable year;

2. one thousand dollars ($1,000); or

3. the amount of the taxpayer’s adjusted gross income tax liability for the taxable year reduced by the sum of all

other credits allowed.

Income Tax Credit Requirements. The Indiana state income tax credit is a nonrefundable credit. You may not carry

forward any unused Indiana state income tax credit. An Indiana taxpayer may not sell, assign, convey, or otherwise

transfer the tax credit. If you no longer have Indiana adjusted gross income, you will no longer be eligible to receive the

Indiana state income tax credit for subsequent contributions to an Account. Contributions must be postmarked or

initiated electronically by December 31 in order to qualify for the Indiana state income tax credit for a particular tax year.

For additional information, see the Indiana Department of Revenue Information Bulletin #98 available at

http://www.in.gov/dor/.

Effective January 1, 2010, rollover contributions from another Qualified Tuition Program into CollegeChoice 529 and

transfers from the Upromise Service into CollegeChoice 529 became ineligible for the Indiana state income tax credit

available to Indiana taxpayers (resident or non-resident, individual or married). In addition, the Indiana income tax credit

is not available for money credited to an Account that will be transferred to an ABLE account (as defined in Section 529A

of the Internal Revenue Code).

14. The paragraph titled “Recapture of Income Tax Credit” beginning on page 56 is of the Disclosure Booklet is replaced in

its entirety as follows:

Recapture of Income Tax Credit. You, as the Account Owner (not the contributor) must repay all or part of the state

income tax credit claimed by contributors in prior taxable years in a taxable year in which you take a Recapture

Distribution. A Recapture Distribution is a:

Non-Qualified Distribution (other than if the distribution is because of the death or Disability of the Beneficiary,

or if the Beneficiary received a scholarship that paid for all or part of the Qualified Expenses of the Beneficiary (to

the extent that the withdrawal or distribution does not exceed the amount of the scholarship), or a Refunded

Distribution);

distribution used to pay K-12 Tuition for a school outside of Indiana;

Rollover Distribution; or

termination of your Account within twelve months after your Account was opened.

Any repayment of the state income tax credit by you must be reported and paid on your Indiana income tax return for the

taxable year in which the Recapture Distribution was made. The Amount that you must repay is equal to the lesser of:

1. twenty percent (20%) of the total amount of Recapture Distributions made during the taxable year from your

Account; or

2. the excess of: (a) the cumulative amount of all Indiana state income tax credits that are claimed by any

contributor with respect to contributions made to your Account for all prior taxable years beginning on or after

January 1, 2007, over (b) the cumulative amount of your repayments for all prior taxable years beginning on or

after January 1, 2008.

CSIND-05719

Treatment of ABLE Rollover Distributions. The Indiana Department of Revenue has not issued guidance on whether an

ABLE Rollover Distribution would be considered a Qualified Distribution. However, Indiana law provides that money that

is credited to an Account that will be transferred to a Qualified ABLE Program account is not considered a contribution to

the Plan and is not eligible for the Indiana state income tax credit. Accordingly, an ABLE Rollover Distribution may be

subject to recapture of any previously taken Indiana state income tax credit. Accordingly, ABLE Rollover Distributions may

also be subject to an Indiana recapture tax if contributions made to your Account were deducted from the contributor’s

state income tax.

We are continuing to evaluate the new law and will provide additional supplements to this Program Description as details

about the Indiana state tax effects of the new federal tax law on ABLE Rollover Distributions become clear. Please consult

your tax advisor about your personal circumstances before initiating an ABLE Rollover Distribution.

15. The paragraph titled “Indiana Taxation of Non-Qualified and Other Distributions” on page 56 of the Disclosure Booklet

is replaced in its entirety as follows:

Indiana Taxation of Non-Qualified and Other Distributions. Because Indiana adjusted gross income is generally derived

from federal adjusted gross income, you or the Beneficiary, as applicable, will be subject to Indiana adjusted gross income

tax on the earnings portion of any Non-Qualified Distribution, or other distributions that are also included in your federal

adjusted gross income for a taxable year.

16. The following definitions are added to the Glossary beginning on page 66.

ABLE Rollover Distribution: A distribution to an account in a Qualified ABLE Program for the same Beneficiary or a Member of the Family of the Beneficiary. Any distribution must be made before January 1, 2026 and cannot exceed the annual $15,000 contribution limit prescribed by Section 529A(b)(2)(B)(i) of the Code.

Indiana K-12 Tuition: K-12 Tuition for a school located in Indiana.

Indiana Qualified Higher Education Expenses: Qualified Expenses, excluding K-12 Tuition.

K-12 Tuition: Qualified elementary and secondary tuition expenses as defined in the Code and as may be further limited by the Plan. These expenses are defined as expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school.

Qualified ABLE Program: A program designed to allow individuals with disabilities to save for qualified disability expenses. Qualified ABLE Programs are sponsored by states or state agencies and are authorized by Section 529A of the Code.

Recapture Distribution: A Non-Qualified Distribution (other than as a result of the death or Disability of the Beneficiary, the Beneficiary’s receipt of a scholarship that paid for all or part of the Qualified Expenses of the Beneficiary (to the extent that the withdrawal or distribution does not exceed the amount of the scholarship), a Refunded Distribution, or a distribution used to pay K-12 Tuition for a school outside of Indiana, a Rollover Distribution or any termination of your Account within 12 months after your Account was opened.

17. The following definition is replaced in its entirety in the Glossary beginning on page 68.

Qualified Expenses: Qualified higher education expenses as defined in the Code and as may be further limited by CollegeChoice

529. Generally, these include the following:

1. tuition, fees and the costs of textbooks, supplies, and equipment required for the enrollment or attendance of a

Beneficiary at an Eligible Educational Institution;

2. certain costs of the room and board of a Beneficiary for any academic period during which the student is enrolled

at least half-time at an Eligible Educational Institution;

CSIND-05719

3. expenses for special needs Beneficiaries that are necessary in connection with their enrollment or attendance at

an Eligible Educational Institution;

4. expenses for the purchase of computer or peripheral equipment (as defined in section 168(i)(2)(B) of the Code),

computer software (as defined in section 197(e)(3)(B) of the Code), or Internet access and related services, if the

equipment, software, or services are to be used primarily by the Beneficiary during any of the years the

Beneficiary is enrolled at an Eligible Educational Institution; and

5. K-12 Tuition.

FOREIGN CHECKS

Effective as of the date of this Supplement, we will no longer accept foreign checks denominated in U.S. dollars. Accordingly,

the following change is made to the Disclosure Booklet:

18. The following replaces the last paragraph on page 12 of the Disclosure Booklet:

We will not accept contributions made by cash, money order, travelers checks, foreign checks, checks dated more than 180 days

from the date of receipt, checks post-dated more than seven days in advance, checks with unclear instructions, starter or counter

checks, credit card or bank courtesy checks, third-party personal checks over $10,000, instant loan checks, or any other check we

deem unacceptable. We will also not accept stocks, securities, or other noncash assets as contributions to your Account. You can

allocate each contribution among any of the Investment Options; however, the minimum percentage per selected Investment

Option is 1% of the contribution amount. Your subsequent contributions can be made to different Investment Options than the

selection(s) you make on your Enrollment Form as long as investments in those different Investment Options are permissible.

Please file this Supplement to the CollegeChoice 529 Direct Savings Plan Disclosure Booklet with your records.

CSIND_05412 1

SUPPLEMENT DATED APRIL 2018 TO THE COLLEGECHOICE 529 DIRECT SAVINGS PLAN

DISCLOSURE BOOKLET DATED NOVEMBER 2014

This Supplement describes important changes affecting the CollegeChoice 529 Direct Savings Plan. Unless otherwise indicated, capitalized terms have the same meaning as those in the Disclosure Booklet. On December 22, 2017, new federal tax reform legislation, Public Law 115-97 (H.R. 1) was signed into law. The law amended Section 529 of the Code to permit withdrawals from 529 Plan accounts up to $10,000 per year per student (in the aggregate across all Qualified Tuition Programs for that student) for tuition expenses in connection with enrollment and attendance at an elementary or secondary public, private or religious school (K-12 Tuition). The law also permits rollovers from a 529 Plan account to an ABLE Plan account (as authorized by Section 529A of the Code) up to the annual $15,000 contribution limit. As of the date of this supplement, although the Indiana Department of Revenue has not provided specific guidance to taxpayers, (1) Account Owners should be able to withdraw assets from their Account to pay K-12 Tuition and treat the withdrawals as Qualified Expenses for Indiana state tax law purposes; (2) contributions intended to be ultimately withdrawn for K-12 Tuition should be eligible for the 20% Indiana state income tax credit; and (3) action by the Indiana General Assembly may be required to extend favorable Indiana state tax treatment to rollovers to ABLE Plan accounts. However, during its 2018 regular session, the Indiana General Assembly considered legislation that would not extend these favorable Indiana state tax treatments, retroactive to the effective date of H.R. 1. The Indiana General Assembly will convene for a special session in May 2018, after which the treatment of withdrawals to pay K-12 Tuition or contributions intended to be withdrawn for K-12 Tuition should become clear. We are working on updating this Disclosure Booklet to reflect the new U.S. tax law and updates to Indiana state tax law that may follow the May 2018 special session. However, because of the uncertainty regarding Indiana state tax law treatment of the changes to Section 529 made by H.R.1, it is important for Indiana taxpayers to consult their tax advisors before (1) making a withdrawal for K-12 Tuition,(2) making a contribution which they intend to ultimately withdraw for K-12 Tuition, and/or (3) rolling over assets from their Account to an ABLE Plan account.

Please file this Supplement to the CollegeChoice 529 Direct Savings Plan Disclosure Booklet with your records.

CSIND-04662

SUPPLEMENT DATED JANUARY 2018 TO THE COLLEGECHOICE 529 DIRECT SAVINGS PLAN

DISCLOSURE BOOKLET DATED NOVEMBER 2014

This Supplement describes important changes affecting the CollegeChoice 529 Direct Savings Plan. Unless

otherwise indicated, capitalized terms have the same meaning as those in the Disclosure Booklet.

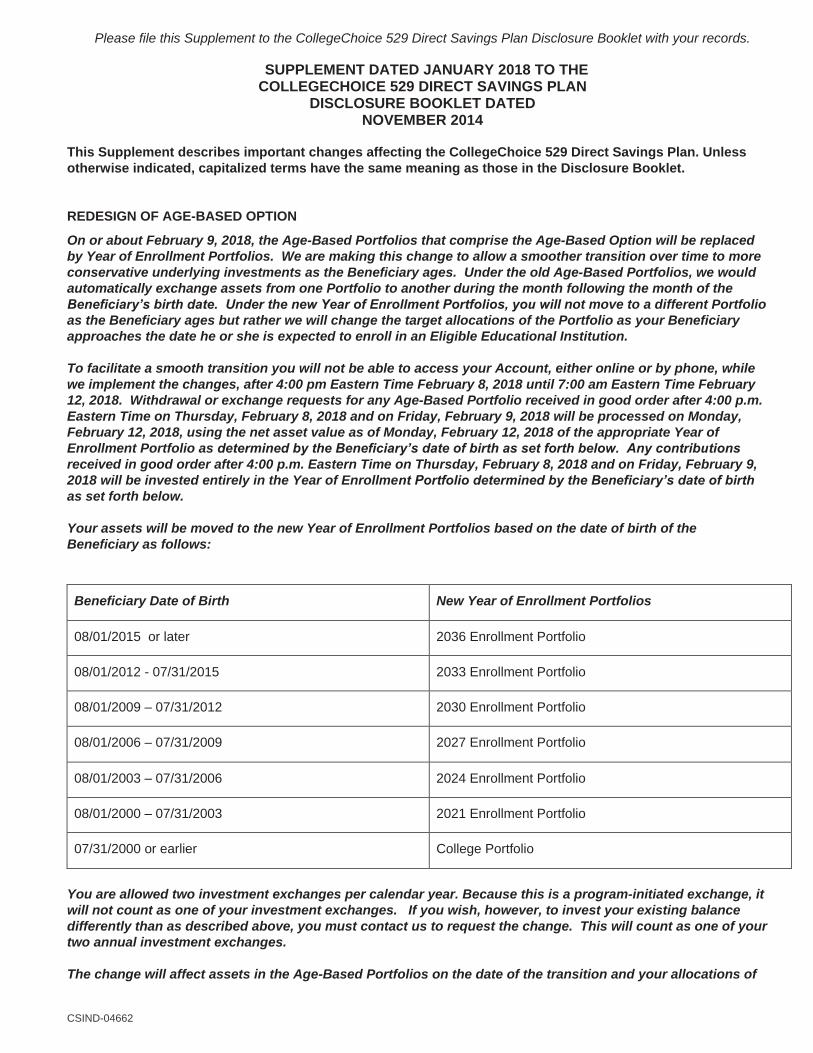

REDESIGN OF AGE-BASED OPTION

On or about February 9, 2018, the Age-Based Portfolios that comprise the Age-Based Option will be replaced

by Year of Enrollment Portfolios. We are making this change to allow a smoother transition over time to more

conservative underlying investments as the Beneficiary ages. Under the old Age-Based Portfolios, we would

automatically exchange assets from one Portfolio to another during the month following the month of the

Beneficiary’s birth date. Under the new Year of Enrollment Portfolios, you will not move to a different Portfolio

as the Beneficiary ages but rather we will change the target allocations of the Portfolio as your Beneficiary

approaches the date he or she is expected to enroll in an Eligible Educational Institution.

To facilitate a smooth transition you will not be able to access your Account, either online or by phone, while

we implement the changes, after 4:00 pm Eastern Time February 8, 2018 until 7:00 am Eastern Time February

12, 2018. Withdrawal or exchange requests for any Age-Based Portfolio received in good order after 4:00 p.m.

Eastern Time on Thursday, February 8, 2018 and on Friday, February 9, 2018 will be processed on Monday,

February 12, 2018, using the net asset value as of Monday, February 12, 2018 of the appropriate Year of

Enrollment Portfolio as determined by the Beneficiary’s date of birth as set forth below. Any contributions

received in good order after 4:00 p.m. Eastern Time on Thursday, February 8, 2018 and on Friday, February 9,

2018 will be invested entirely in the Year of Enrollment Portfolio determined by the Beneficiary’s date of birth

as set forth below.

Your assets will be moved to the new Year of Enrollment Portfolios based on the date of birth of the

Beneficiary as follows:

Beneficiary Date of Birth New Year of Enrollment Portfolios

08/01/2015 or later 2036 Enrollment Portfolio

08/01/2012 - 07/31/2015 2033 Enrollment Portfolio

08/01/2009 – 07/31/2012 2030 Enrollment Portfolio

08/01/2006 – 07/31/2009 2027 Enrollment Portfolio

08/01/2003 – 07/31/2006 2024 Enrollment Portfolio

08/01/2000 – 07/31/2003 2021 Enrollment Portfolio

07/31/2000 or earlier College Portfolio

You are allowed two investment exchanges per calendar year. Because this is a program-initiated exchange, it

will not count as one of your investment exchanges. If you wish, however, to invest your existing balance

differently than as described above, you must contact us to request the change. This will count as one of your

two annual investment exchanges.

The change will affect assets in the Age-Based Portfolios on the date of the transition and your allocations of

2

future contributions. If you wish to change your allocations of future contributions you may do so at any time

by logging onto our website at www. collegechoicedirect.com, by submitting the Exchange/Future

Contribution (Allocation) Form by mail, or by calling 1-866-485-9415.

1. Effective February 9, 2018, all references to the term “Age-Based Portfolios” are replaced with

references to the term “Year of Enrollment Portfolios.”

2. Effective February 9, 2018, the following replaces the section entitled “How does CollegeChoice 529

work?” on page 6 of the Disclosure Booklet:

How does CollegeChoice 529 work?

When you enroll in CollegeChoice 529, you choose to invest in at least one of three (3) different investment

approaches based on your preferences and the level of risk you are comfortable with.

One investment approach is the Year of Enrollment Option where your money is invested in a Portfolio that

automatically moves to progressively more conservative investments as your Beneficiary approaches college age.

There are seven (7) Portfolios available under the Year of Enrollment Option. These Portfolios invest in Underlying

Funds managed by Vanguard and Loomis Sayles.

The second investment approach is the Individual Portfolios Option, in which the types of investments (for example -

stocks, bonds or cash) the Portfolio invests in, remains fixed over time. Each Individual Portfolio invests in a single

Underlying Fund, three of which are managed by Vanguard (U.S. Equity Index Portfolio, the Bond Index Portfolio and

the Stable Value Portfolio). Other Individual Portfolios are managed by Dodge & Cox (International Portfolio), Carillon

Reams (Active Bond Portfolio), and Western Asset (Inflation Protected Portfolio).

The third investment approach is the Savings Portfolio Option. The Savings Portfolio invests in a Federal Deposit

Insurance Corporation (FDIC) insured omnibus savings account held in trust by the Authority at NexBank.

All of the contributions made to your Account grow tax-deferred and the distributions are free of federal and Indiana

state income taxes if used for Qualified Expenses.

3. Effective February 9, 2018, the following replaces the right column on page 38 of the Disclosure Booklet:

We offer:

• Seven (7) Year of Enrollment Portfolios, in which your money is invested in a Portfolio that automatically moves

to progressively more conservative investments as your Beneficiary approaches college age. Each Portfolio invests in

multiple Underlying Funds managed by Vanguard and Loomis Sayles;

• Seven (7) Individual Portfolios, in which the composition of investments within the Portfolio remains fixed over

time. Each portfolio invests in a single Underlying Fund, four (4) of which are managed by Vanguard and three (3) of

which are managed by Dodge & Cox, Carillon Reams, and Western Asset, respectively; and

• The Savings Portfolio, which invests in a FDIC-insured omnibus savings account held in trust by the Authority

at NexBank.

4. Effective February 9, 2018, the following replaces the section entitled “Confirmation of Contributions

and Transactions” on page 17 of the Disclosure Booklet:

Confirmation of Contributions and Transactions. We will send you a confirmation for each contribution and

transaction to your Account(s), except for AIPs, payroll deduction transactions, exchanges due to dollar-cost averaging,

automatic transfers from a Upromise Service account to your Account, and the Annual Account Maintenance Fee,

which will only be confirmed on a quarterly basis. Each confirmation statement will indicate the number of Units you

own in each Investment Option. If an error has been made in the amount of the contribution or the Investment Option in

which a particular contribution is invested, you have sixty (60) days from the date of the confirmation statement to notify

us of the error. (See Maintaining Your Account —Correction of Errors on page 25).

We use reasonable procedures to confirm that transaction requests are genuine. You may be responsible for losses

3

resulting from fraudulent or unauthorized instructions received by us, provided we reasonably believe the instructions

are genuine. To safeguard your Account, please keep your information confidential. Contact us immediately at 1-866-

485-9415 if you believe there is a discrepancy between a transaction you requested and the confirmation statement

you received, or if you believe someone has obtained unauthorized access to your Account. Contributions may be

refused if they appear to be an abuse of the Plan.

5. Effective February 9, 2018, the following replaces the first paragraph of the section entitled “Account

Statements” on page 24 of the Disclosure Booklet:

Account Statements. You will receive quarterly statements to reflect financial transactions only if you have made

financial transactions within the quarter. These transactions include: contributions made to your Account; exchanges

due to dollar-cost averaging; automatic transfers from a Upromise Service account to your Account; withdrawals made

from your Account; and transaction and maintenance fees incurred by your Account. The total value of your Account at

the end of the quarter will also be included in your quarterly statements. You will receive an annual Account Statement

even if you have made no financial transactions within the year.

6. Effective February 9, 2018, the following replaces the section entitled Options for Unused Contributions;

Changing a Beneficiary, Transferring Assets to Another of Your Accounts on page 24 of the Disclosure

Booklet:

Options for Unused Contributions; Changing a Beneficiary, Transferring Assets to Another of Your Accounts.

Your Beneficiary may choose not to attend an Eligible Educational Institution or may not use all the money in your

Account. In either case, you may name a new Beneficiary or take a distribution of your Account assets. Any Non-

Qualified Distribution from your Account will be subject to applicable income taxes and may be subject to the

Distribution Tax. (See How to Take a Distribution from your Account starting on page 19.)

You can change your Beneficiary at any time. To avoid negative tax consequences, the new Beneficiary must be a

Member of the Family of the original Beneficiary. Any change of the Beneficiary to a person who is not a Member of the

Family of the current Beneficiary is treated as a Non-Qualified Distribution subject to applicable federal and state

income taxes as well as the Distribution Tax. An Account Owner who is an UGMA/UTMA Custodian will not be able to

change the Beneficiary of the Account, except as may be permitted under the applicable UGMA/UTMA law. (See

Funding Methods — Moving Assets From An UGMA/UTMA Account on page 15.) To initiate a change of

Beneficiary, you must complete and submit a Beneficiary Change Form. The change will be made upon our receipt and

acceptance of the signed, properly completed form(s) in good order. We reserve the right to suspend the processing of

a Beneficiary transfer if we suspect that the transfer is intended to avoid the Plan’s exchange and reallocation limits

and/or the tax laws. Also, a Beneficiary change or transfer of assets may be denied or limited if it causes one or more

Accounts to exceed the Maximum Account Balance for a Beneficiary. There is no fee for changing a Beneficiary. You

may also initiate a change of Beneficiary online by logging into your Account at www.collegechoicedirect.com.

When you change a beneficiary, we will invest your assets in accordance with the Standing Investment Instruction for

the new Beneficiary’s Account. You can also transfer assets in your Account to a new Investment Option when you

change the Beneficiary for your Account.

7. Effective February 9, 2018, the following replaces the section entitled “Age-Based Portfolios” on Page 39

of the Disclosure Booklet:

Year of Enrollment Portfolios

The seven (7) Year of Enrollment Portfolios are a simplified approach to college investing. We have designed these

Portfolios to allow you to select a Portfolio based upon your risk tolerance and your Beneficiary’s anticipated year of

enrollment in an Eligible Educational Institution. For example, if you expect your Beneficiary to attend college beginning

in the year 2028, 2029 or 2030, you may choose to select the 2030 Enrollment Portfolio; or, you may choose one of the

other Year of Enrollment Portfolios.

The asset allocation of the money invested in these Investment Options is automatically adjusted semi-annually over

time to become more conservative as the Beneficiary’s year of enrollment in college draws nearer. The asset allocation

for the College Portfolio is not adjusted as the College Portfolio has already reached its most conservative phase.

About every three (3) years, a new Year of Enrollment Portfolio is created and assets of the oldest Year of Enrollment

4

Portfolio are folded into the College Portfolio.

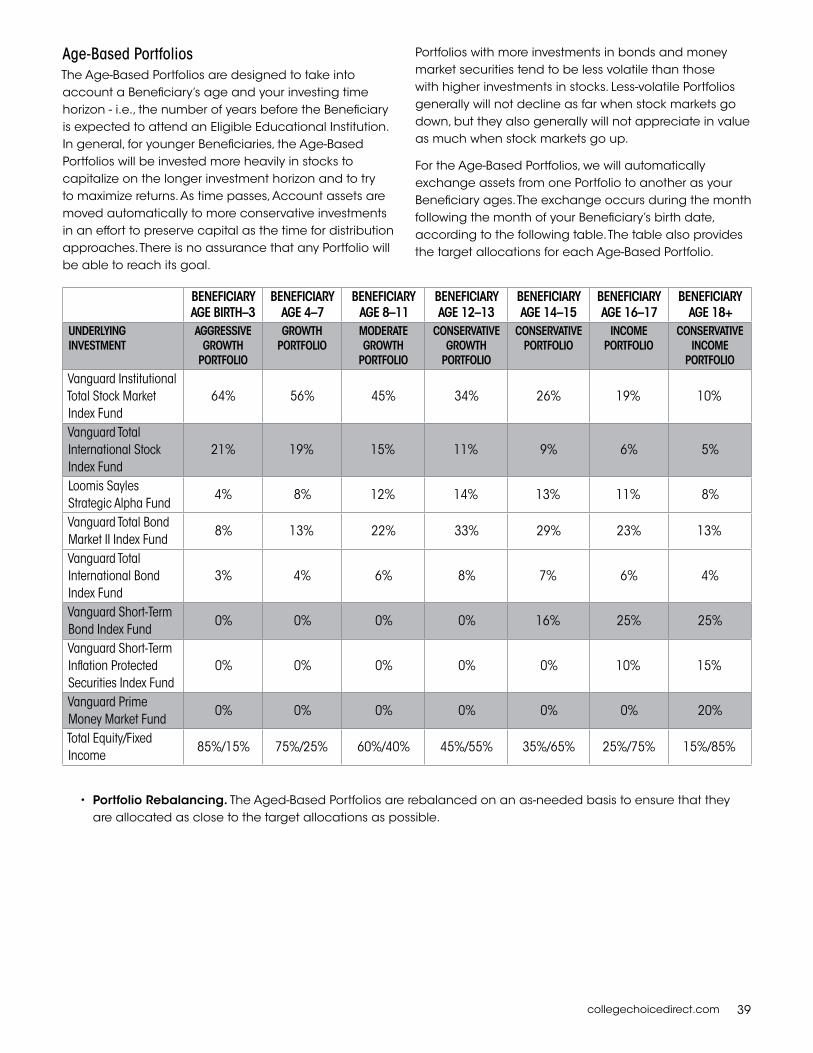

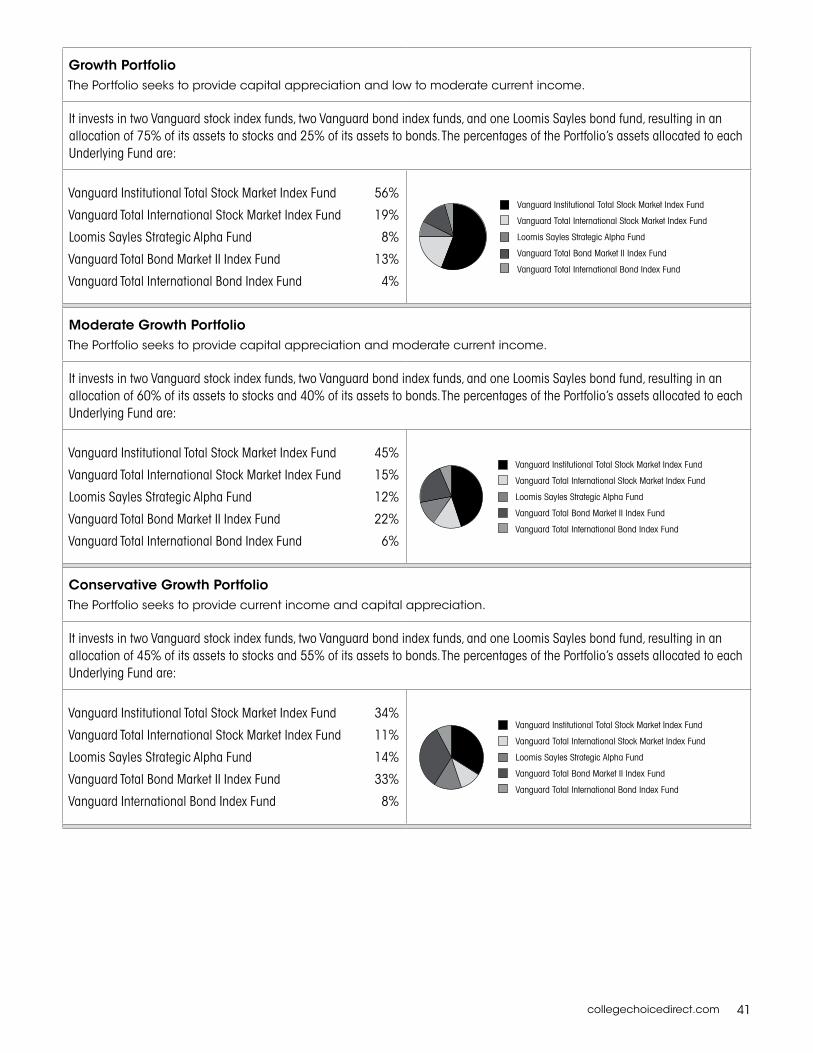

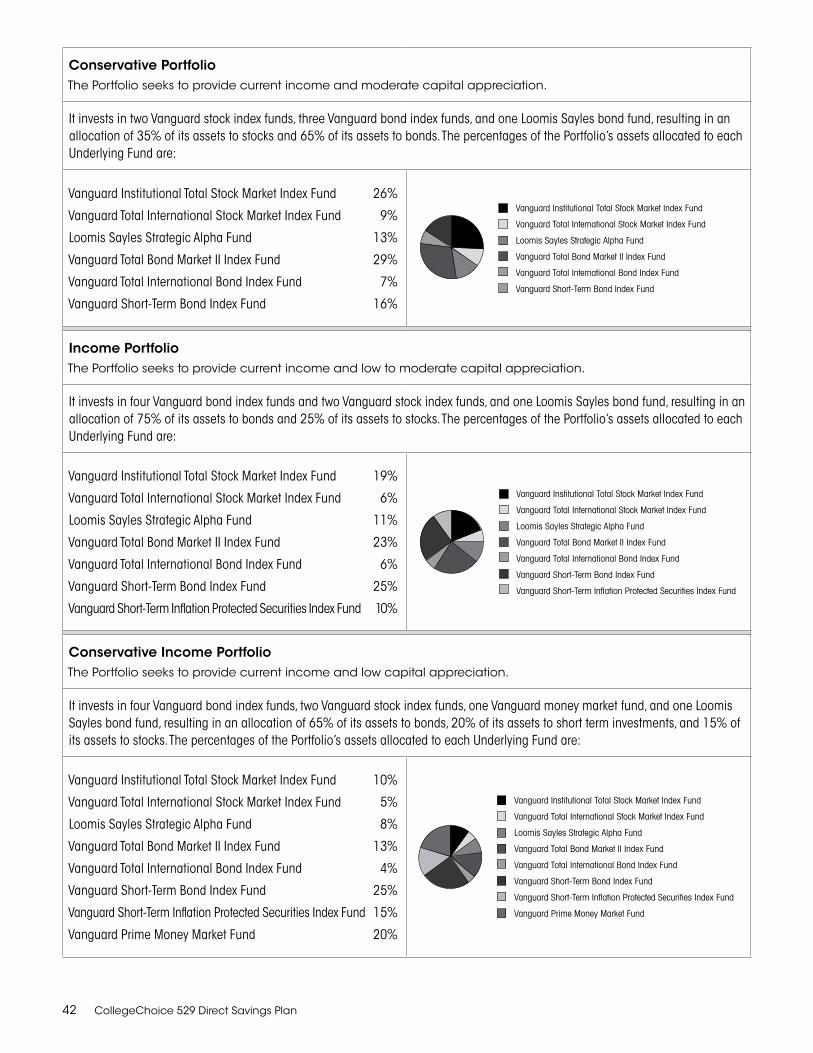

Portfolios with higher allocations to bonds and money market securities tend to be less volatile than those with higher stock allocations. Less-volatile Portfolios generally will not decline as far when stock markets go down, but they also generally will not appreciate in value as much when stock markets go up. There is no assurance that any Portfolio will be able to reach its goal.

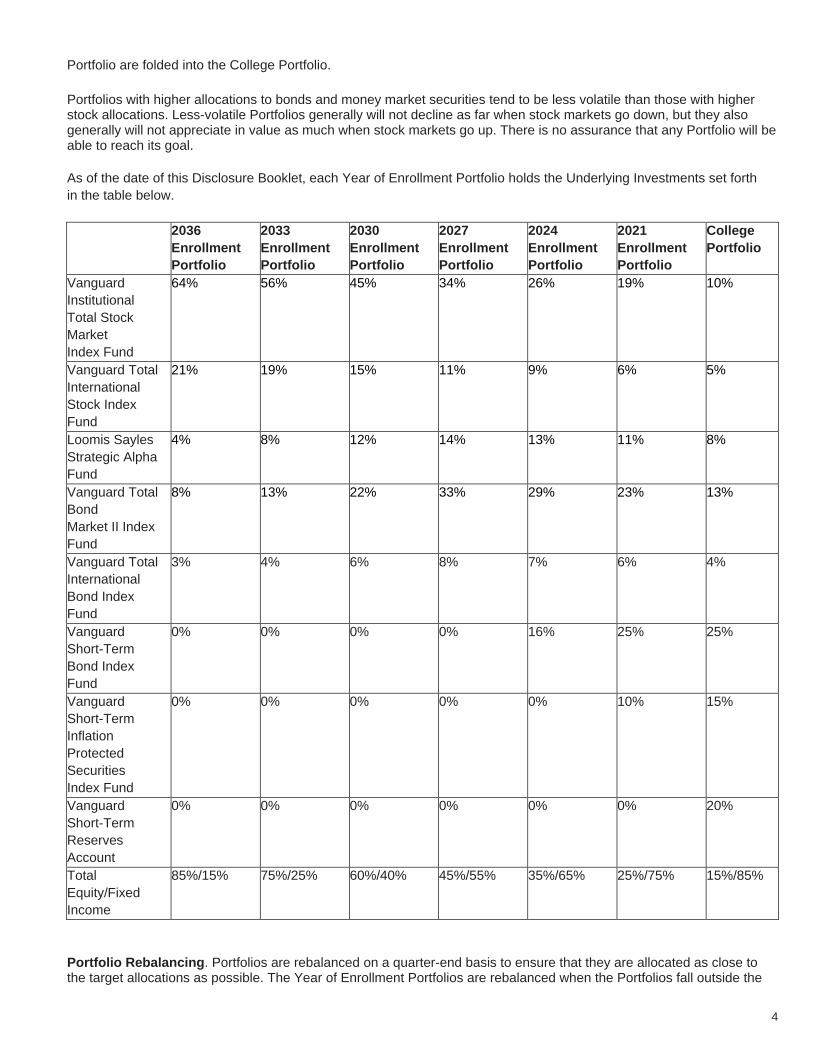

As of the date of this Disclosure Booklet, each Year of Enrollment Portfolio holds the Underlying Investments set forth

in the table below.

2036

Enrollment

Portfolio

2033

Enrollment

Portfolio

2030

Enrollment

Portfolio

2027

Enrollment

Portfolio

2024

Enrollment

Portfolio

2021

Enrollment

Portfolio

College

Portfolio

Vanguard

Institutional

Total Stock

Market

Index Fund

64% 56% 45% 34% 26% 19% 10%

Vanguard Total

International

Stock Index

Fund

21% 19% 15% 11% 9% 6% 5%

Loomis Sayles

Strategic Alpha

Fund

4% 8% 12% 14% 13% 11% 8%

Vanguard Total

Bond

Market II Index

Fund

8% 13% 22% 33% 29%

23% 13%

Vanguard Total

International

Bond Index

Fund

3% 4% 6% 8% 7% 6% 4%

Vanguard

Short-Term

Bond Index

Fund

0% 0% 0% 0% 16% 25% 25%

Vanguard

Short-Term

Inflation

Protected

Securities

Index Fund

0% 0% 0% 0% 0% 10% 15%

Vanguard

Short-Term

Reserves

Account

0% 0% 0% 0% 0% 0% 20%

Total

Equity/Fixed

Income

85%/15% 75%/25% 60%/40% 45%/55% 35%/65% 25%/75% 15%/85%

Portfolio Rebalancing. Portfolios are rebalanced on a quarter-end basis to ensure that they are allocated as close to the target allocations as possible. The Year of Enrollment Portfolios are rebalanced when the Portfolios fall outside the

5

strategic targets by more than one percentage point. Beginning in 2019, the asset allocations of the Year of Enrollment Portfolios will automatically transition semi-annually to more conservative allocations as the Beneficiary approaches college enrollment.

Model Risk. The allocation of each Year of Enrollment Portfolio is derived using quantitative models that have been

developed based on a number of factors. Neither the Year of Enrollment Portfolios nor the Plan can offer any assurance

that the recommended asset allocation will either maximize returns or minimize risk or be the appropriate allocation in all

circumstances for every investor with a particular time horizon or risk tolerance.

8. Effective February 9, 2018, all references to specific Age-Based Portfolios are replaced with references

to the corresponding new Year of Enrollment Portfolios as follows:

Aggressive Growth Portfolio becomes 2036 Enrollment Portfolio

Growth Portfolio becomes 2033 Enrollment Portfolio

Moderate Growth Portfolio becomes 2030 Enrollment Portfolio

Conservative Growth Portfolio becomes 2027 Enrollment Portfolio

Conservative Portfolio becomes 2024 Enrollment Portfolio

Income Portfolio becomes 2021 Enrollment Portfolio

Conservative Income Portfolio becomes College Portfolio

9. Effective February 9, 2018, the following replaces the section entitled “Age-Based Option Portfolio

Profiles” on page 40 of the Disclosure Booklet:

Year of Enrollment Option Portfolio Profiles

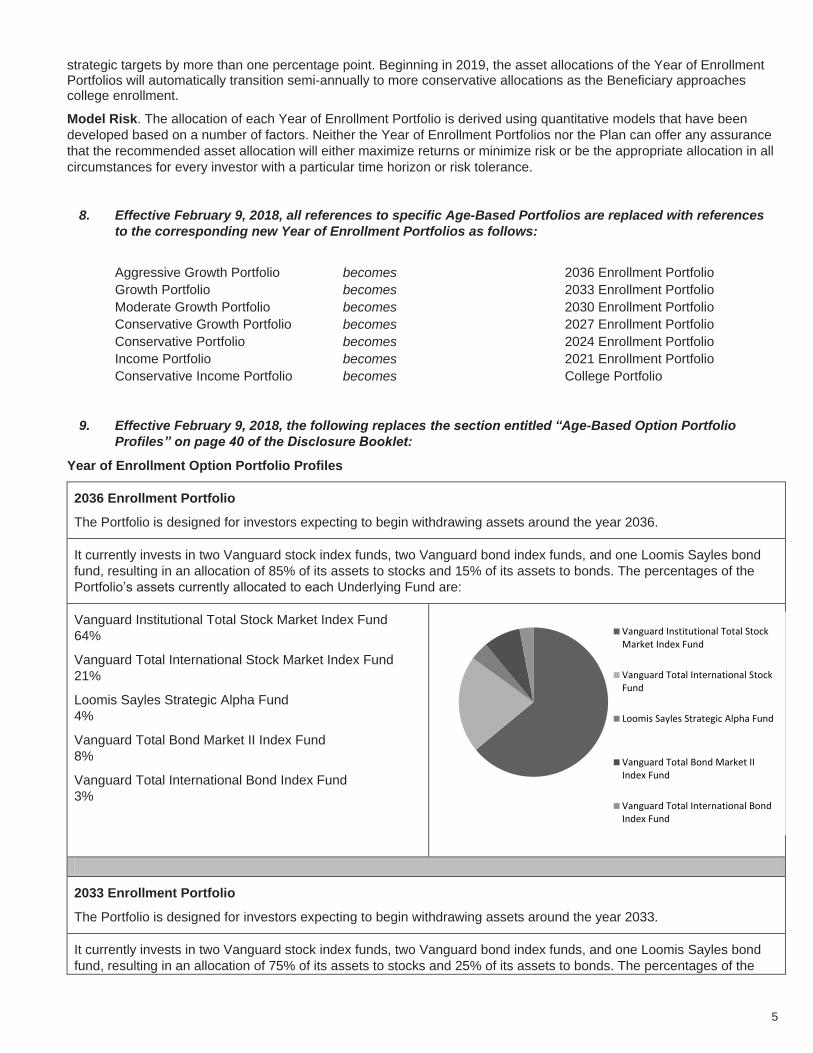

2036 Enrollment Portfolio

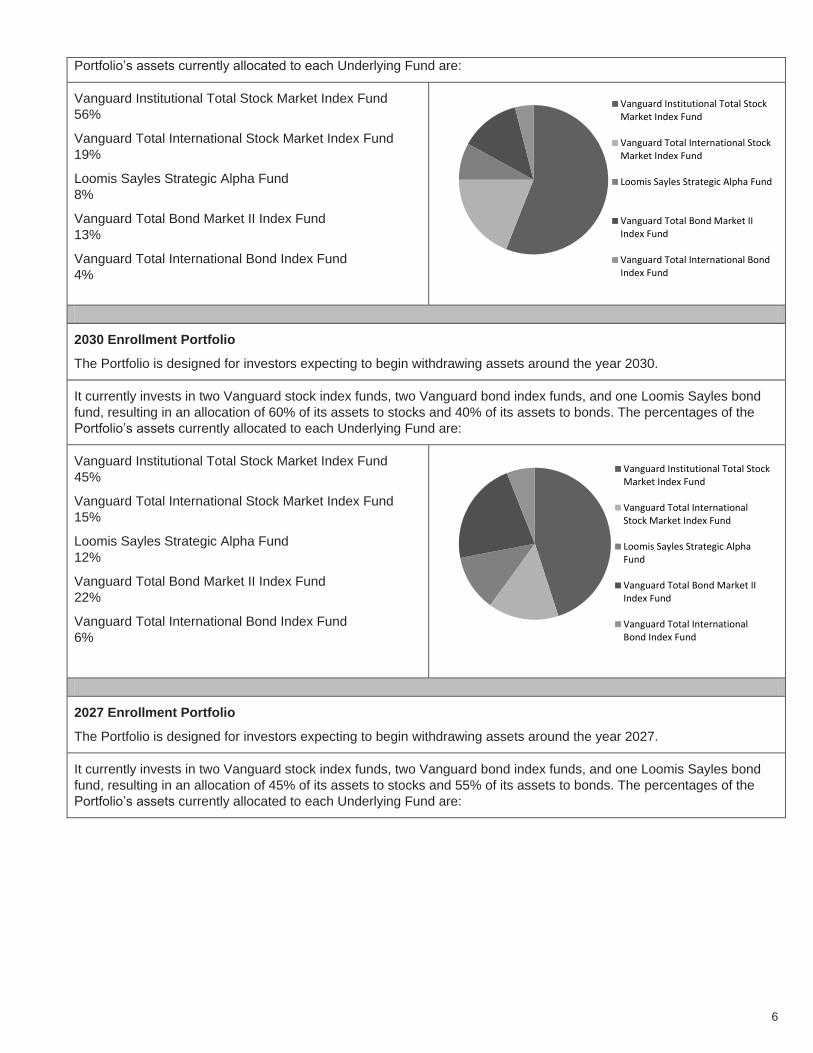

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2036.

It currently invests in two Vanguard stock index funds, two Vanguard bond index funds, and one Loomis Sayles bond

fund, resulting in an allocation of 85% of its assets to stocks and 15% of its assets to bonds. The percentages of the

Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total Stock Market Index Fund

64%

Vanguard Total International Stock Market Index Fund

21%

Loomis Sayles Strategic Alpha Fund

4%

Vanguard Total Bond Market II Index Fund

8%

Vanguard Total International Bond Index Fund

3%

2033 Enrollment Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2033.

It currently invests in two Vanguard stock index funds, two Vanguard bond index funds, and one Loomis Sayles bond

fund, resulting in an allocation of 75% of its assets to stocks and 25% of its assets to bonds. The percentages of the

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total International StockFund

Loomis Sayles Strategic Alpha Fund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total International BondIndex Fund

6

Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total Stock Market Index Fund

56%

Vanguard Total International Stock Market Index Fund

19%

Loomis Sayles Strategic Alpha Fund

8%

Vanguard Total Bond Market II Index Fund

13%

Vanguard Total International Bond Index Fund

4%

2030 Enrollment Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2030.

It currently invests in two Vanguard stock index funds, two Vanguard bond index funds, and one Loomis Sayles bond

fund, resulting in an allocation of 60% of its assets to stocks and 40% of its assets to bonds. The percentages of the

Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total Stock Market Index Fund

45%

Vanguard Total International Stock Market Index Fund

15%

Loomis Sayles Strategic Alpha Fund

12%

Vanguard Total Bond Market II Index Fund

22%

Vanguard Total International Bond Index Fund

6%

2027 Enrollment Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2027.

It currently invests in two Vanguard stock index funds, two Vanguard bond index funds, and one Loomis Sayles bond

fund, resulting in an allocation of 45% of its assets to stocks and 55% of its assets to bonds. The percentages of the

Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total International StockMarket Index Fund

Loomis Sayles Strategic Alpha Fund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total International BondIndex Fund

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total InternationalStock Market Index Fund

Loomis Sayles Strategic AlphaFund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total InternationalBond Index Fund

7

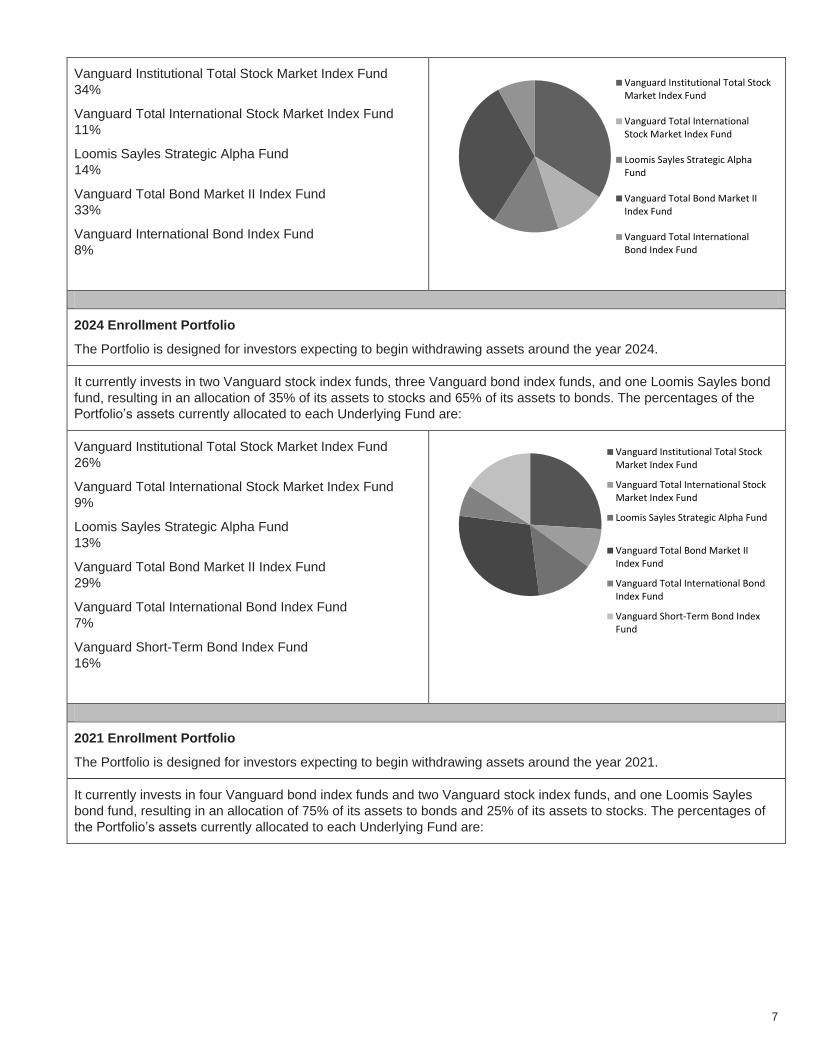

Vanguard Institutional Total Stock Market Index Fund

34%

Vanguard Total International Stock Market Index Fund

11%

Loomis Sayles Strategic Alpha Fund

14%

Vanguard Total Bond Market II Index Fund

33%

Vanguard International Bond Index Fund

8%

2024 Enrollment Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2024.

It currently invests in two Vanguard stock index funds, three Vanguard bond index funds, and one Loomis Sayles bond

fund, resulting in an allocation of 35% of its assets to stocks and 65% of its assets to bonds. The percentages of the

Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total Stock Market Index Fund

26%

Vanguard Total International Stock Market Index Fund

9%

Loomis Sayles Strategic Alpha Fund

13%

Vanguard Total Bond Market II Index Fund

29%

Vanguard Total International Bond Index Fund

7%

Vanguard Short-Term Bond Index Fund

16%

2021 Enrollment Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets around the year 2021.

It currently invests in four Vanguard bond index funds and two Vanguard stock index funds, and one Loomis Sayles

bond fund, resulting in an allocation of 75% of its assets to bonds and 25% of its assets to stocks. The percentages of

the Portfolio’s assets currently allocated to each Underlying Fund are:

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total InternationalStock Market Index Fund

Loomis Sayles Strategic AlphaFund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total InternationalBond Index Fund

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total International StockMarket Index Fund

Loomis Sayles Strategic Alpha Fund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total International BondIndex Fund

Vanguard Short-Term Bond IndexFund

8

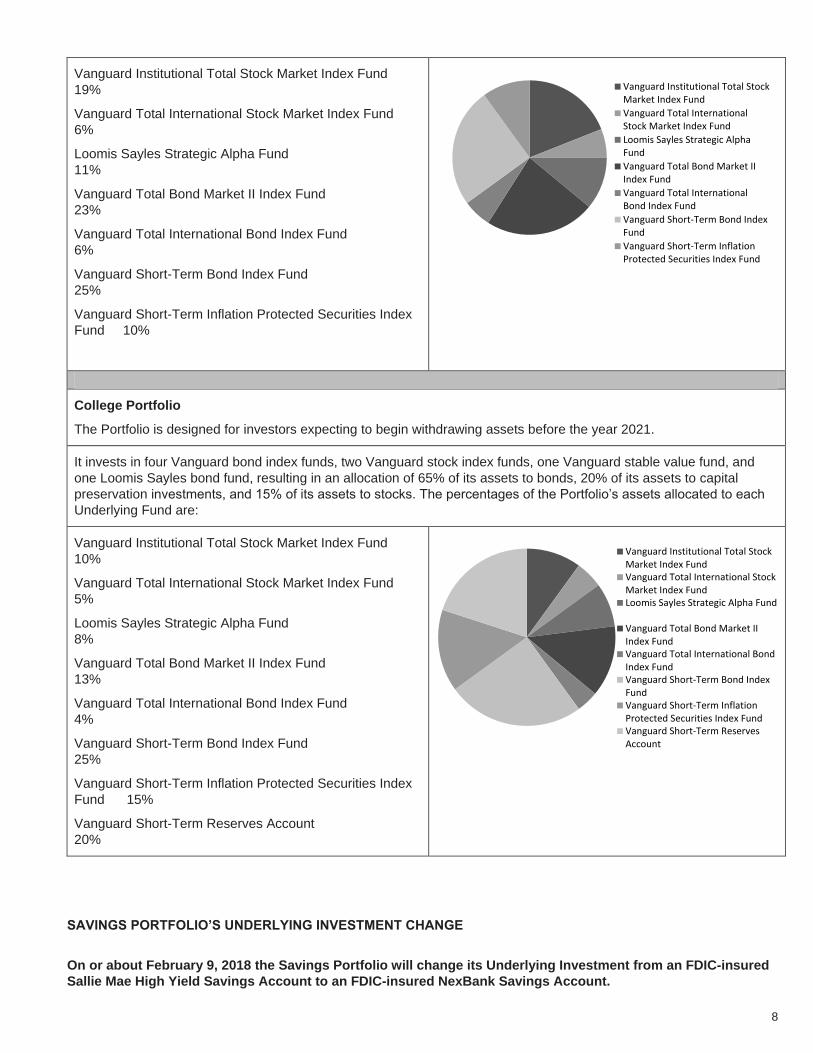

Vanguard Institutional Total Stock Market Index Fund

19%

Vanguard Total International Stock Market Index Fund

6%

Loomis Sayles Strategic Alpha Fund

11%

Vanguard Total Bond Market II Index Fund

23%

Vanguard Total International Bond Index Fund

6%

Vanguard Short-Term Bond Index Fund

25%

Vanguard Short-Term Inflation Protected Securities Index

Fund 10%

College Portfolio

The Portfolio is designed for investors expecting to begin withdrawing assets before the year 2021.

It invests in four Vanguard bond index funds, two Vanguard stock index funds, one Vanguard stable value fund, and

one Loomis Sayles bond fund, resulting in an allocation of 65% of its assets to bonds, 20% of its assets to capital

preservation investments, and 15% of its assets to stocks. The percentages of the Portfolio’s assets allocated to each

Underlying Fund are:

Vanguard Institutional Total Stock Market Index Fund

10%

Vanguard Total International Stock Market Index Fund

5%

Loomis Sayles Strategic Alpha Fund

8%

Vanguard Total Bond Market II Index Fund

13%

Vanguard Total International Bond Index Fund

4%

Vanguard Short-Term Bond Index Fund

25%

Vanguard Short-Term Inflation Protected Securities Index

Fund 15%

Vanguard Short-Term Reserves Account

20%

SAVINGS PORTFOLIO’S UNDERLYING INVESTMENT CHANGE

On or about February 9, 2018 the Savings Portfolio will change its Underlying Investment from an FDIC-insured

Sallie Mae High Yield Savings Account to an FDIC-insured NexBank Savings Account.

Vanguard Institutional Total StockMarket Index Fund

Vanguard Total InternationalStock Market Index Fund

Loomis Sayles Strategic AlphaFund

Vanguard Total Bond Market IIIndex Fund

Vanguard Total InternationalBond Index Fund

Vanguard Short-Term Bond IndexFund

Vanguard Short-Term InflationProtected Securities Index Fund

Vanguard Institutional Total StockMarket Index FundVanguard Total International StockMarket Index FundLoomis Sayles Strategic Alpha Fund

Vanguard Total Bond Market IIIndex FundVanguard Total International BondIndex FundVanguard Short-Term Bond IndexFundVanguard Short-Term InflationProtected Securities Index FundVanguard Short-Term ReservesAccount

9

10. Effective February 9, 2018, the following replaces the section entitled “Savings Portfolios” on page 40 of

the Disclosure Booklet:

Savings Portfolio

The Savings Portfolio seeks income consistent with the preservation of principal. Similar to the Individual Portfolios, the

types and composition of investments held by the Portfolio remains fixed over time. The Portfolio invests 100% of its

assets in the NexBank High-Yield Savings Account (HYSA). The HYSA is held in an omnibus savings account insured

by the FDIC (up to certain limits), which is held in trust by the Authority at NexBank. (See Portfolio Descriptions –

Savings Portfolio on page 47.)

11. Effective February 9, 2018, the following replaces the section entitled “Savings Portfolio” on page 47 of

the Disclosure Booklet:

PORTFOLIO AND INVESTMENT OBJECTIVE INVESTMENT STRATEGY

Savings Portfolio

The Portfolio seeks income consistent with the

preservation of principal.

The Portfolio invests 100% of its assets in the HYSA.

The HYSA is held in an omnibus savings account

insured by the FDIC (up to the limits set forth below),

which is held in trust by the Authority at NexBank.

Investments in the Savings Portfolio earn a varying rate

of interest. Interest on the HYSA will be compounded

daily based on the actual number of days in a year and

will be credited to the HYSA on a monthly basis. The

interest rate is expressed as an Annual Percentage

Yield (APY). The APY will be reviewed by NexBank on

a periodic basis and may be recalculated as needed at

any time. To see the current Savings Portfolio APY,

please visit www.collegechoicedirect.com or call 1-

866-485-9415.

FDIC insurance is provided for the Savings Portfolio

only. Contributions to and earnings on the investments

in the Savings Portfolio are insured by the FDIC on a

pass-through basis to each Account Owner up to the

maximum amount set by federal law – currently

$250,000. The amount of FDIC insurance provided to

an Account Owner is based on the total of:

1. the value of an Account Owner’s investment in the

Savings Portfolio; and

2. the value of all other accounts held by the Account

Owner at NexBank, as determined by NexBank and

FDIC regulations.

The Plan Officials are not responsible for determining

how an Account Owner’s investment in the Savings

Portfolio will be aggregated with other accounts held by

the Account Owner at NexBank for purposes of the

FDIC insurance.

There is no other insurance and there are no other

guarantees for the Savings Portfolio. Therefore, like all

of the Portfolios, neither your contributions to the

Savings Portfolio nor any investment return earned on

your contributions are guaranteed by the Plan Officials.

In addition, the Savings Portfolio does not provide a

10

guarantee of any level of performance or return.

12. Effective February 9, 2018, the following replaces the definition of “HYSA” on page 67 of the Disclosure

Booklet:

HYSA: NexBank’s High-Yield Savings Account.

13. Effective February 9, 2018, the definition of “Sallie Mae Bank” on page 68 of the Disclosure Booklet is

deleted in its entirety

14. Effective February 9, 2018, the following definition is added after the definition of “Member of the

Family” and before the definition of “Non-Qualified Distributions” on page 67 of the Disclosure Booklet:

NexBank: NexBank SSB, a state-chartered Texas bank.

15. Effective February 9, 2018, the following replaces the definition of “Savings Portfolio Manager” on page

68 of the Disclosure Booklet:

Savings Portfolio Manager: NexBank.

16. Effective February 9, 2018, the following replaces the row entitled “Savings Portfolio” on page 76 of the

Disclosure Booklet:

Savings Portfolio To the extent that FDIC insurance applies, the Portfolio is primarily subject to income risk. This risk is discussed under NexBank Investment Risks on page 86.

17. Effective February 9, 2018, the following replaces the section entitled “Sallie Mae Bank Investment

Risks” on page 86 of the Disclosure Booklet:

NexBank Investment Risks

Income Risk. This is the risk that the return of the underlying FDIC-insured HYSA will vary from week to week because of changing interest rates and that the return of the HYSA will decline because of falling interest rates.

18. Effective February 9, 2018, the following replaces the first paragraph at the bottom of the back cover of

the Disclosure Statement:

CollegeChoice 529 Direct Savings Plan (CollegeChoice 529) is administered by the Indiana Education Savings Authority (Authority). Ascensus Broker Dealer Services, Inc., the Program Manager, and its affiliates, have overall responsibility for the day-to-day operations, including investment advisory, recordkeeping and administrative services, and marketing. CollegeChoice 529’s Portfolios invest in: (i) mutual funds; (ii) a stable value account held in trust by the Authority at Vanguard; and/or (iii) an FDIC-insured omnibus savings account held in trust by the Authority at NexBank. Except for the Savings Portfolio, investments in CollegeChoice 529 are not insured by the FDIC. Units of the Portfolios are municipal securities and the value of units will vary with market conditions.

UPDATED TABLES

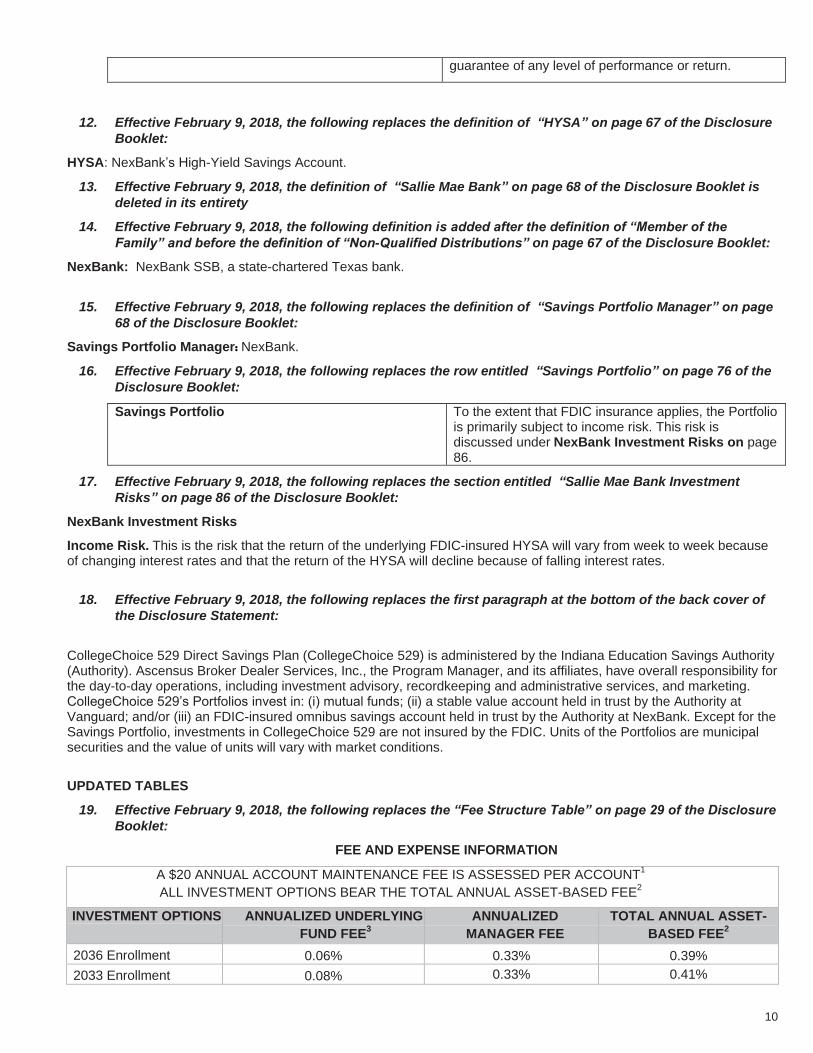

19. Effective February 9, 2018, the following replaces the “Fee Structure Table” on page 29 of the Disclosure

Booklet:

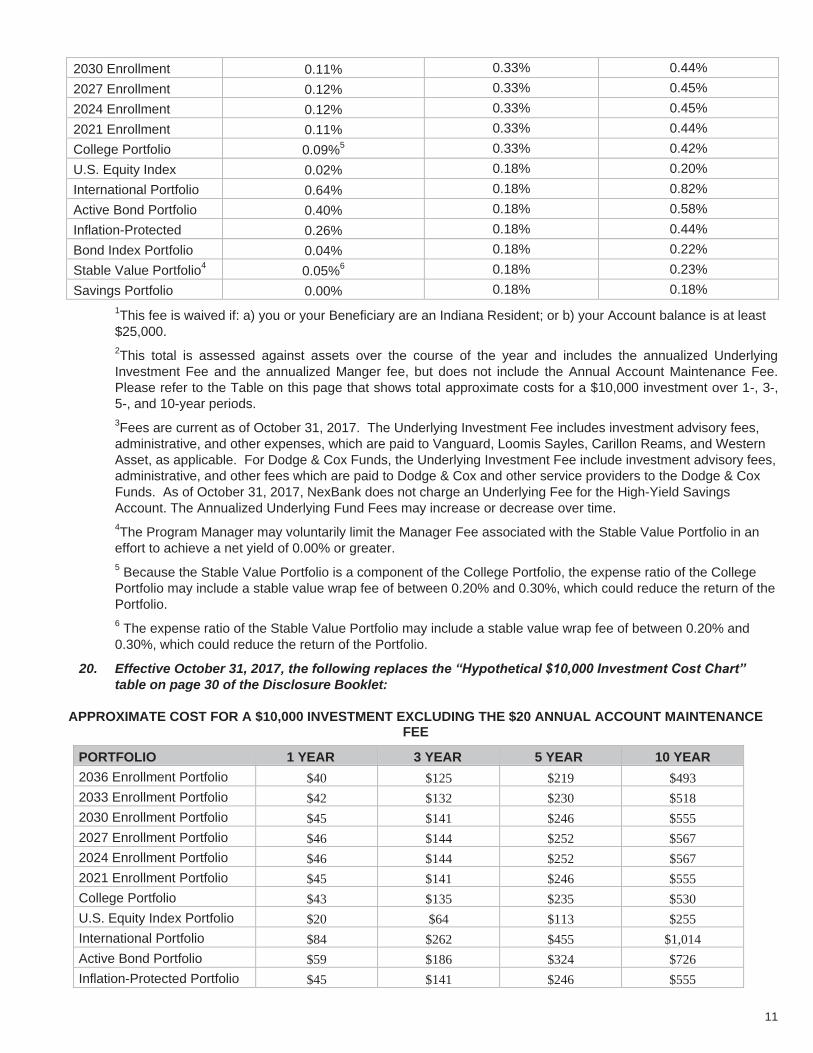

FEE AND EXPENSE INFORMATION

A $20 ANNUAL ACCOUNT MAINTENANCE FEE IS ASSESSED PER ACCOUNT1

ALL INVESTMENT OPTIONS BEAR THE TOTAL ANNUAL ASSET-BASED FEE2

INVESTMENT OPTIONS ANNUALIZED UNDERLYING

FUND FEE3

ANNUALIZED

MANAGER FEE

TOTAL ANNUAL ASSET-

BASED FEE2

2036 Enrollment Portfolio

0.06% 0.33% 0.39%

2033 Enrollment Portfolio

0.08% 0.33% 0.41%

11

2030 Enrollment Portfolio

0.11% 0.33% 0.44%

2027 Enrollment Portfolio

0.12% 0.33% 0.45%

2024 Enrollment Portfolio

0.12% 0.33% 0.45%

2021 Enrollment Portfolio

0.11% 0.33% 0.44%

College Portfolio 0.09%5 0.33% 0.42%

U.S. Equity Index Portfolio

0.02% 0.18% 0.20%

International Portfolio 0.64% 0.18% 0.82%

Active Bond Portfolio 0.40% 0.18% 0.58%

Inflation-Protected Portfolio

0.26% 0.18% 0.44%

Bond Index Portfolio 0.04% 0.18% 0.22%

Stable Value Portfolio4 0.05%

6 0.18% 0.23%

Savings Portfolio 0.00% 0.18% 0.18%

1This fee is waived if: a) you or your Beneficiary are an Indiana Resident; or b) your Account balance is at least

$25,000.

2This total is assessed against assets over the course of the year and includes the annualized Underlying

Investment Fee and the annualized Manger fee, but does not include the Annual Account Maintenance Fee.

Please refer to the Table on this page that shows total approximate costs for a $10,000 investment over 1-, 3-,

5-, and 10-year periods.

3Fees are current as of October 31, 2017. The Underlying Investment Fee includes investment advisory fees,

administrative, and other expenses, which are paid to Vanguard, Loomis Sayles, Carillon Reams, and Western

Asset, as applicable. For Dodge & Cox Funds, the Underlying Investment Fee include investment advisory fees,

administrative, and other fees which are paid to Dodge & Cox and other service providers to the Dodge & Cox

Funds. As of October 31, 2017, NexBank does not charge an Underlying Fee for the High-Yield Savings

Account. The Annualized Underlying Fund Fees may increase or decrease over time.

4The Program Manager may voluntarily limit the Manager Fee associated with the Stable Value Portfolio in an

effort to achieve a net yield of 0.00% or greater.

5 Because the Stable Value Portfolio is a component of the College Portfolio, the expense ratio of the College

Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the

Portfolio.

6 The expense ratio of the Stable Value Portfolio may include a stable value wrap fee of between 0.20% and

0.30%, which could reduce the return of the Portfolio.

20. Effective October 31, 2017, the following replaces the “Hypothetical $10,000 Investment Cost Chart”

table on page 30 of the Disclosure Booklet:

APPROXIMATE COST FOR A $10,000 INVESTMENT EXCLUDING THE $20 ANNUAL ACCOUNT MAINTENANCE FEE

PORTFOLIO 1 YEAR 3 YEAR 5 YEAR 10 YEAR

2036 Enrollment Portfolio $40 $125 $219 $493

2033 Enrollment Portfolio $42 $132 $230 $518

2030 Enrollment Portfolio $45 $141 $246 $555

2027 Enrollment Portfolio $46 $144 $252 $567

2024 Enrollment Portfolio $46 $144 $252 $567

2021 Enrollment Portfolio $45 $141 $246 $555

College Portfolio $43 $135 $235 $530

U.S. Equity Index Portfolio $20 $64 $113 $255

International Portfolio $84 $262 $455 $1,014

Active Bond Portfolio $59 $186 $324 $726

Inflation-Protected Portfolio $45 $141 $246 $555

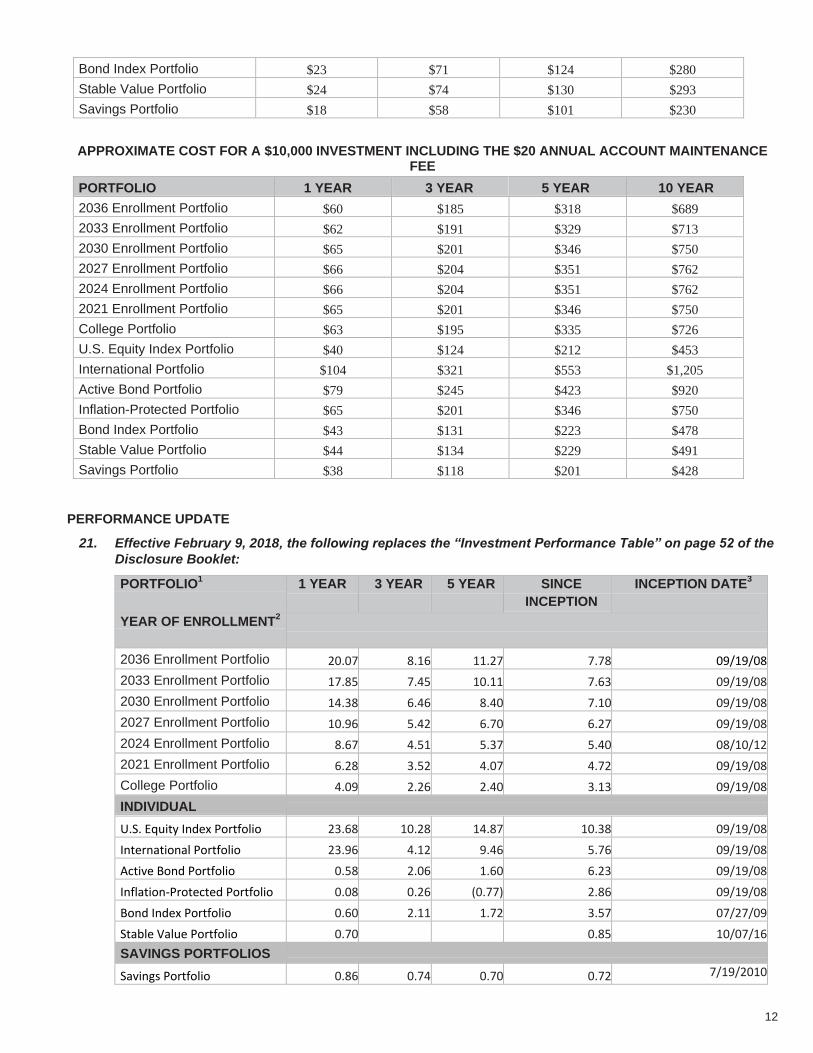

12

Bond Index Portfolio $23 $71 $124 $280

Stable Value Portfolio $24 $74 $130 $293

Savings Portfolio $18 $58 $101 $230

APPROXIMATE COST FOR A $10,000 INVESTMENT INCLUDING THE $20 ANNUAL ACCOUNT MAINTENANCE FEE

PORTFOLIO 1 YEAR 3 YEAR 5 YEAR 10 YEAR

2036 Enrollment Portfolio $60 $185 $318 $689

2033 Enrollment Portfolio $62 $191 $329 $713

2030 Enrollment Portfolio $65 $201 $346 $750

2027 Enrollment Portfolio $66 $204 $351 $762

2024 Enrollment Portfolio $66 $204 $351 $762

2021 Enrollment Portfolio $65 $201 $346 $750

College Portfolio $63 $195 $335 $726

U.S. Equity Index Portfolio $40 $124 $212 $453

International Portfolio $104 $321 $553 $1,205

Active Bond Portfolio $79 $245 $423 $920

Inflation-Protected Portfolio $65 $201 $346 $750

Bond Index Portfolio $43 $131 $223 $478

Stable Value Portfolio $44 $134 $229 $491

Savings Portfolio $38 $118 $201 $428

PERFORMANCE UPDATE

21. Effective February 9, 2018, the following replaces the “Investment Performance Table” on page 52 of the

Disclosure Booklet:

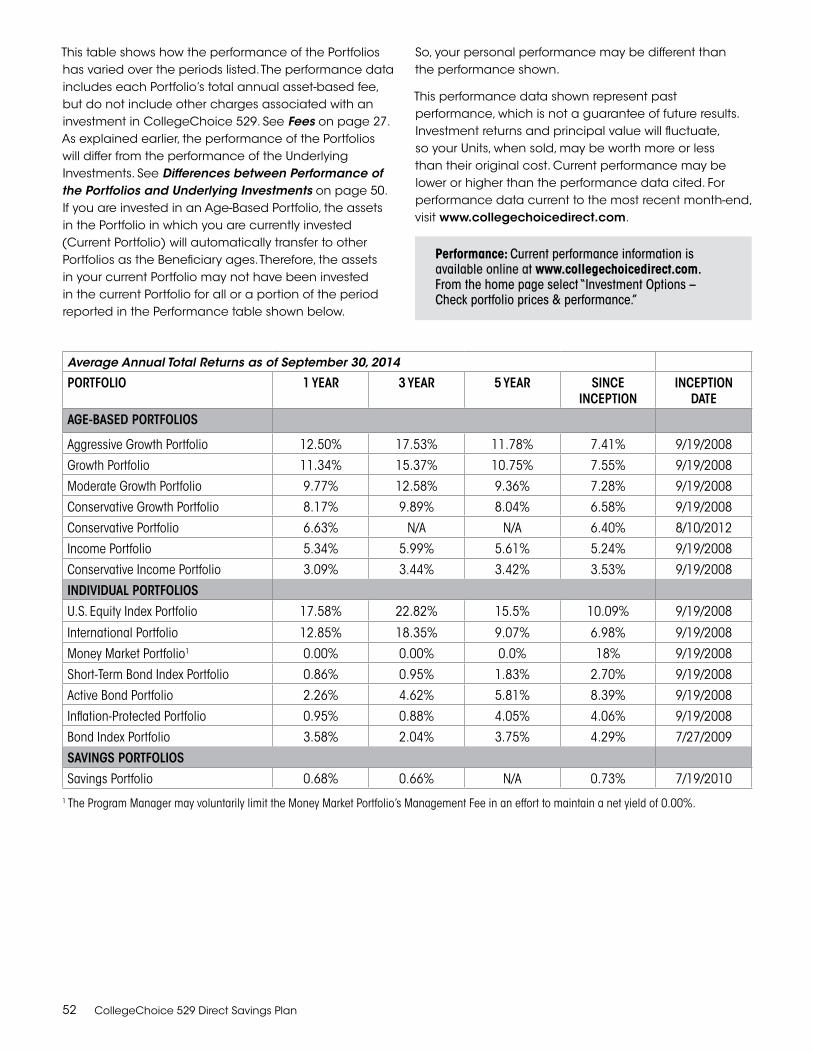

PORTFOLIO1 1 YEAR 3 YEAR 5 YEAR SINCE

INCEPTION

INCEPTION DATE3

YEAR OF ENROLLMENT2

2036 Enrollment Portfolio 20.07 8.16 11.27 7.78 09/19/08

2033 Enrollment Portfolio 17.85 7.45 10.11 7.63 09/19/08

2030 Enrollment Portfolio 14.38 6.46 8.40 7.10 09/19/08

2027 Enrollment Portfolio 10.96 5.42 6.70 6.27 09/19/08

2024 Enrollment Portfolio 8.67 4.51 5.37 5.40 08/10/12

2021 Enrollment Portfolio 6.28 3.52 4.07 4.72 09/19/08

College Portfolio 4.09 2.26 2.40 3.13 09/19/08

INDIVIDUAL PORTFOLIOS

U.S. Equity Index Portfolio 23.68 10.28 14.87 10.38 09/19/08

International Portfolio 23.96 4.12 9.46 5.76 09/19/08

Active Bond Portfolio 0.58 2.06 1.60 6.23 09/19/08

Inflation-Protected Portfolio 0.08 0.26 (0.77) 2.86 09/19/08

Bond Index Portfolio 0.60 2.11 1.72 3.57 07/27/09

Stable Value Portfolio 0.70 0.85 10/07/16

SAVINGS PORTFOLIOS

Savings Portfolio 0.86 0.74 0.70 0.72 7/19/2010

13

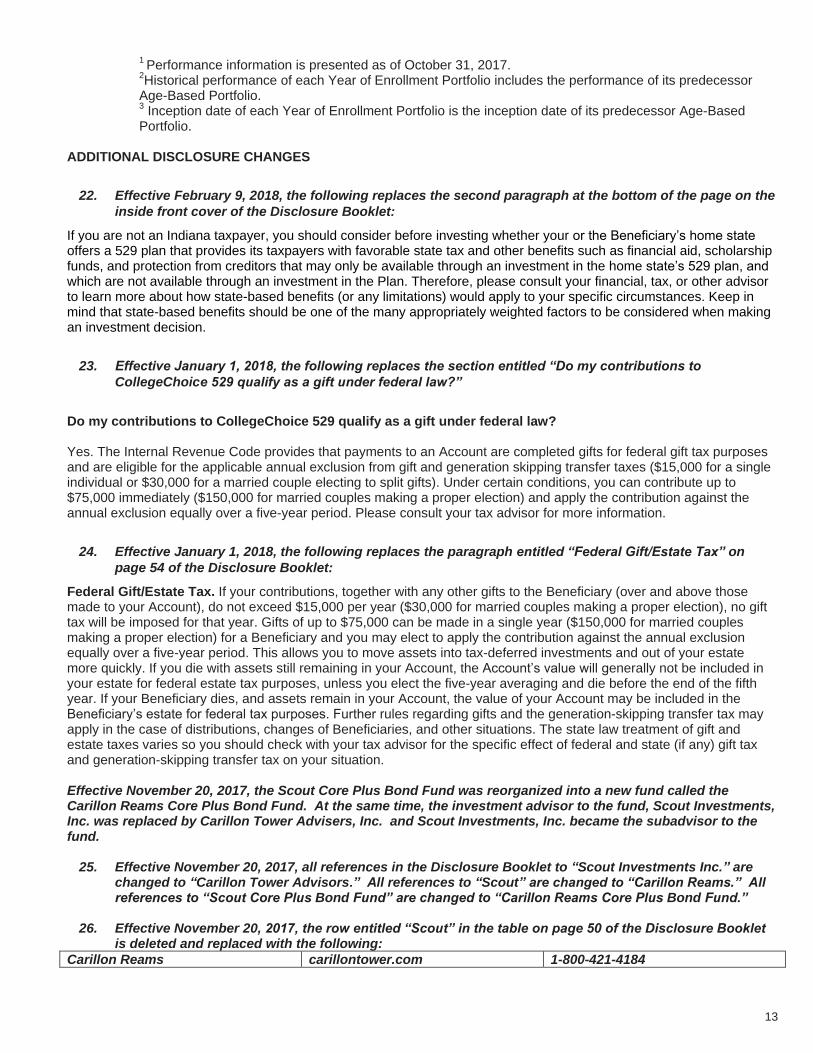

1 Performance information is presented as of October 31, 2017.

2Historical performance of each Year of Enrollment Portfolio includes the performance of its predecessor

Age-Based Portfolio. 3 Inception date of each Year of Enrollment Portfolio is the inception date of its predecessor Age-Based

Portfolio. ADDITIONAL DISCLOSURE CHANGES

22. Effective February 9, 2018, the following replaces the second paragraph at the bottom of the page on the

inside front cover of the Disclosure Booklet:

If you are not an Indiana taxpayer, you should consider before investing whether your or the Beneficiary’s home state offers a 529 plan that provides its taxpayers with favorable state tax and other benefits such as financial aid, scholarship funds, and protection from creditors that may only be available through an investment in the home state’s 529 plan, and which are not available through an investment in the Plan. Therefore, please consult your financial, tax, or other advisor to learn more about how state-based benefits (or any limitations) would apply to your specific circumstances. Keep in mind that state-based benefits should be one of the many appropriately weighted factors to be considered when making an investment decision.

23. Effective January 1, 2018, the following replaces the section entitled “Do my contributions to

CollegeChoice 529 qualify as a gift under federal law?”

Do my contributions to CollegeChoice 529 qualify as a gift under federal law? Yes. The Internal Revenue Code provides that payments to an Account are completed gifts for federal gift tax purposes and are eligible for the applicable annual exclusion from gift and generation skipping transfer taxes ($15,000 for a single individual or $30,000 for a married couple electing to split gifts). Under certain conditions, you can contribute up to $75,000 immediately ($150,000 for married couples making a proper election) and apply the contribution against the annual exclusion equally over a five-year period. Please consult your tax advisor for more information.

24. Effective January 1, 2018, the following replaces the paragraph entitled “Federal Gift/Estate Tax” on

page 54 of the Disclosure Booklet:

Federal Gift/Estate Tax. If your contributions, together with any other gifts to the Beneficiary (over and above those made to your Account), do not exceed $15,000 per year ($30,000 for married couples making a proper election), no gift tax will be imposed for that year. Gifts of up to $75,000 can be made in a single year ($150,000 for married couples making a proper election) for a Beneficiary and you may elect to apply the contribution against the annual exclusion equally over a five-year period. This allows you to move assets into tax-deferred investments and out of your estate more quickly. If you die with assets still remaining in your Account, the Account’s value will generally not be included in your estate for federal estate tax purposes, unless you elect the five-year averaging and die before the end of the fifth year. If your Beneficiary dies, and assets remain in your Account, the value of your Account may be included in the Beneficiary’s estate for federal tax purposes. Further rules regarding gifts and the generation-skipping transfer tax may apply in the case of distributions, changes of Beneficiaries, and other situations. The state law treatment of gift and estate taxes varies so you should check with your tax advisor for the specific effect of federal and state (if any) gift tax and generation-skipping transfer tax on your situation. Effective November 20, 2017, the Scout Core Plus Bond Fund was reorganized into a new fund called the Carillon Reams Core Plus Bond Fund. At the same time, the investment advisor to the fund, Scout Investments, Inc. was replaced by Carillon Tower Advisers, Inc. and Scout Investments, Inc. became the subadvisor to the fund.

25. Effective November 20, 2017, all references in the Disclosure Booklet to “Scout Investments Inc.” are changed to “Carillon Tower Advisors.” All references to “Scout” are changed to “Carillon Reams.” All references to “Scout Core Plus Bond Fund” are changed to “Carillon Reams Core Plus Bond Fund.”

26. Effective November 20, 2017, the row entitled “Scout” in the table on page 50 of the Disclosure Booklet

is deleted and replaced with the following:

Carillon Reams carillontower.com 1-800-421-4184

Please file this Supplement to the CollegeChoice 529 Direct Savings Plan Disclosure Booklet with your records.

CSIND-02976

SUPPLEMENT DATED MARCH 2017 TO THE COLLEGECHOICE 529 DIRECT SAVINGS PLAN

DISCLOSURE BOOKLET DATED NOVEMBER 2014

This Supplement describes important changes affecting the CollegeChoice 529 Direct Savings Plan. Unless otherwise indicated, capitalized terms have the same meaning as those in the Disclosure Booklet.

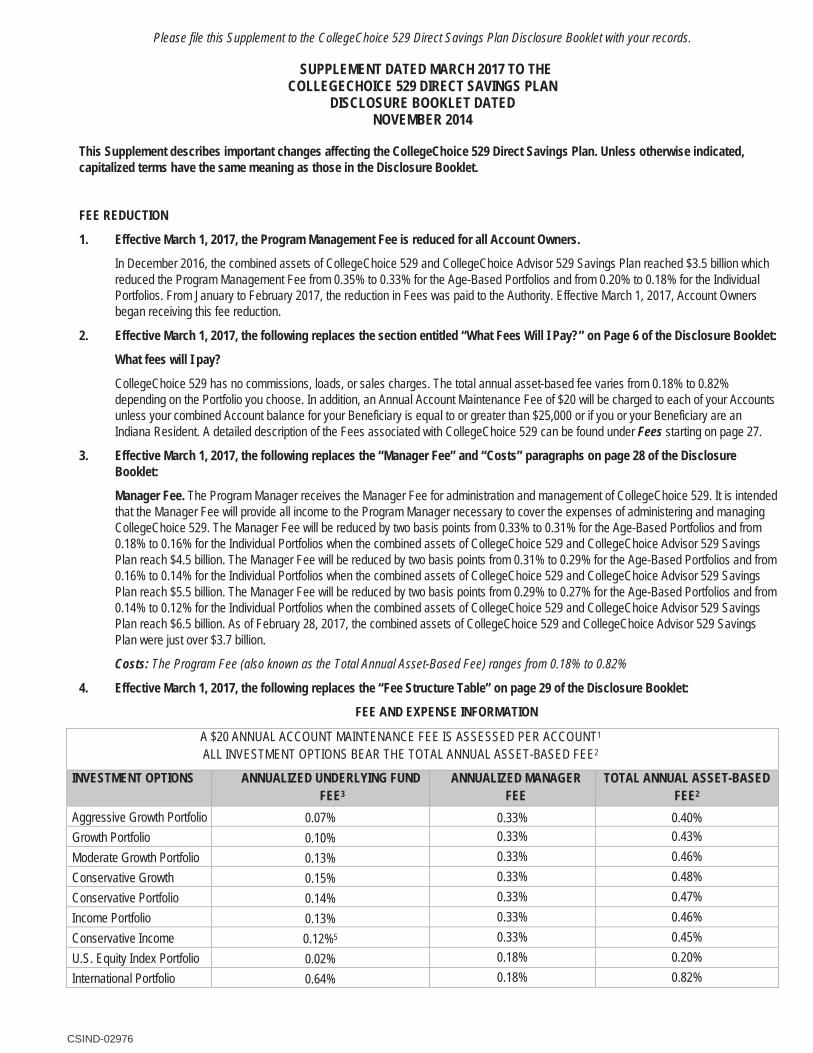

FEE REDUCTION

1. Effective March 1, 2017, the Program Management Fee is reduced for all Account Owners.

In December 2016, the combined assets of CollegeChoice 529 and CollegeChoice Advisor 529 Savings Plan reached $3.5 billion whichreduced the Program Management Fee from 0.35% to 0.33% for the Age-Based Portfolios and from 0.20% to 0.18% for the IndividualPortfolios. From January to February 2017, the reduction in Fees was paid to the Authority. Effective March 1, 2017, Account Ownersbegan receiving this fee reduction.

2. Effective March 1, 2017, the following replaces the section entitled “What Fees Will I Pay?” on Page 6 of the Disclosure Booklet:

What fees will I pay?

CollegeChoice 529 has no commissions, loads, or sales charges. The total annual asset-based fee varies from 0.18% to 0.82%depending on the Portfolio you choose. In addition, an Annual Account Maintenance Fee of $20 will be charged to each of your Accountsunless your combined Account balance for your Beneficiary is equal to or greater than $25,000 or if you or your Beneficiary are anIndiana Resident. A detailed description of the Fees associated with CollegeChoice 529 can be found under Fees starting on page 27.

3. Effective March 1, 2017, the following replaces the “Manager Fee” and “Costs” paragraphs on page 28 of the DisclosureBooklet:

Manager Fee. The Program Manager receives the Manager Fee for administration and management of CollegeChoice 529. It is intendedthat the Manager Fee will provide all income to the Program Manager necessary to cover the expenses of administering and managingCollegeChoice 529. The Manager Fee will be reduced by two basis points from 0.33% to 0.31% for the Age-Based Portfolios and from0.18% to 0.16% for the Individual Portfolios when the combined assets of CollegeChoice 529 and CollegeChoice Advisor 529 SavingsPlan reach $4.5 billion. The Manager Fee will be reduced by two basis points from 0.31% to 0.29% for the Age-Based Portfolios and from0.16% to 0.14% for the Individual Portfolios when the combined assets of CollegeChoice 529 and CollegeChoice Advisor 529 SavingsPlan reach $5.5 billion. The Manager Fee will be reduced by two basis points from 0.29% to 0.27% for the Age-Based Portfolios and from0.14% to 0.12% for the Individual Portfolios when the combined assets of CollegeChoice 529 and CollegeChoice Advisor 529 SavingsPlan reach $6.5 billion. As of February 28, 2017, the combined assets of CollegeChoice 529 and CollegeChoice Advisor 529 SavingsPlan were just over $3.7 billion.

Costs: The Program Fee (also known as the Total Annual Asset-Based Fee) ranges from 0.18% to 0.82%

4. Effective March 1, 2017, the following replaces the “Fee Structure Table” on page 29 of the Disclosure Booklet:

FEE AND EXPENSE INFORMATION

A $20 ANNUAL ACCOUNT MAINTENANCE FEE IS ASSESSED PER ACCOUNT1 ALL INVESTMENT OPTIONS BEAR THE TOTAL ANNUAL ASSET-BASED FEE2

INVESTMENT OPTIONS ANNUALIZED UNDERLYING FUND FEE3

ANNUALIZED MANAGER FEE

TOTAL ANNUAL ASSET-BASED FEE2

Aggressive Growth Portfolio 0.07% 0.33% 0.40% Growth Portfolio 0.10% 0.33% 0.43% Moderate Growth Portfolio 0.13% 0.33% 0.46% Conservative Growth

0.15% 0.33% 0.48%

Conservative Portfolio 0.14% 0.33% 0.47% Income Portfolio 0.13% 0.33% 0.46% Conservative Income

0.12%5 0.33% 0.45%

U.S. Equity Index Portfolio 0.02% 0.18% 0.20% International Portfolio 0.64% 0.18% 0.82%

2 CSIND-02976

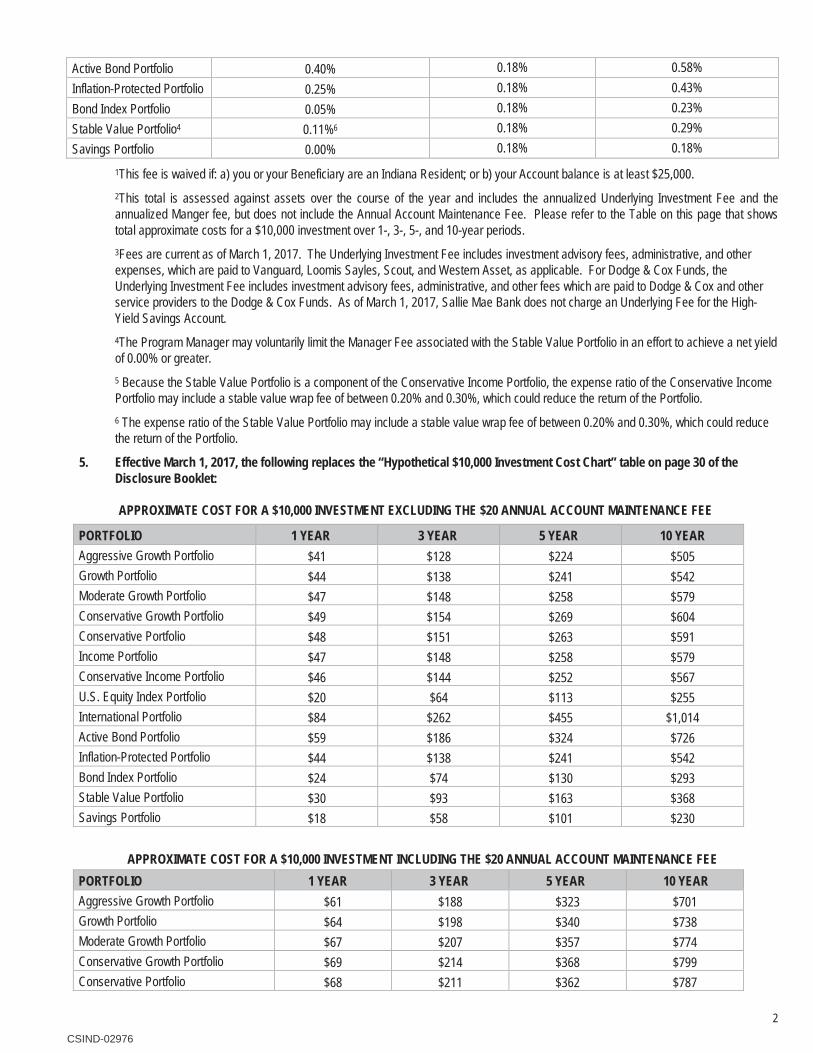

Active Bond Portfolio 0.40% 0.18% 0.58% Inflation-Protected Portfolio 0.25% 0.18% 0.43% Bond Index Portfolio 0.05% 0.18% 0.23% Stable Value Portfolio4 0.11%6 0.18% 0.29% Savings Portfolio 0.00% 0.18% 0.18%

1This fee is waived if: a) you or your Beneficiary are an Indiana Resident; or b) your Account balance is at least $25,000. 2This total is assessed against assets over the course of the year and includes the annualized Underlying Investment Fee and the annualized Manger fee, but does not include the Annual Account Maintenance Fee. Please refer to the Table on this page that shows total approximate costs for a $10,000 investment over 1-, 3-, 5-, and 10-year periods. 3Fees are current as of March 1, 2017. The Underlying Investment Fee includes investment advisory fees, administrative, and other expenses, which are paid to Vanguard, Loomis Sayles, Scout, and Western Asset, as applicable. For Dodge & Cox Funds, the Underlying Investment Fee includes investment advisory fees, administrative, and other fees which are paid to Dodge & Cox and other service providers to the Dodge & Cox Funds. As of March 1, 2017, Sallie Mae Bank does not charge an Underlying Fee for the High-Yield Savings Account. 4The Program Manager may voluntarily limit the Manager Fee associated with the Stable Value Portfolio in an effort to achieve a net yield of 0.00% or greater. 5 Because the Stable Value Portfolio is a component of the Conservative Income Portfolio, the expense ratio of the Conservative Income Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the Portfolio. 6 The expense ratio of the Stable Value Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the Portfolio.

5. Effective March 1, 2017, the following replaces the “Hypothetical $10,000 Investment Cost Chart” table on page 30 of the Disclosure Booklet:

APPROXIMATE COST FOR A $10,000 INVESTMENT EXCLUDING THE $20 ANNUAL ACCOUNT MAINTENANCE FEE PORTFOLIO 1 YEAR 3 YEAR 5 YEAR 10 YEAR Aggressive Growth Portfolio $41 $128 $224 $505 Growth Portfolio $44 $138 $241 $542 Moderate Growth Portfolio $47 $148 $258 $579 Conservative Growth Portfolio $49 $154 $269 $604 Conservative Portfolio $48 $151 $263 $591 Income Portfolio $47 $148 $258 $579 Conservative Income Portfolio $46 $144 $252 $567 U.S. Equity Index Portfolio $20 $64 $113 $255 International Portfolio $84 $262 $455 $1,014 Active Bond Portfolio $59 $186 $324 $726 Inflation-Protected Portfolio $44 $138 $241 $542 Bond Index Portfolio $24 $74 $130 $293 Stable Value Portfolio $30 $93 $163 $368 Savings Portfolio $18 $58 $101 $230

APPROXIMATE COST FOR A $10,000 INVESTMENT INCLUDING THE $20 ANNUAL ACCOUNT MAINTENANCE FEE

PORTFOLIO 1 YEAR 3 YEAR 5 YEAR 10 YEAR Aggressive Growth Portfolio $61 $188 $323 $701 Growth Portfolio $64 $198 $340 $738 Moderate Growth Portfolio $67 $207 $357 $774 Conservative Growth Portfolio $69 $214 $368 $799 Conservative Portfolio $68 $211 $362 $787

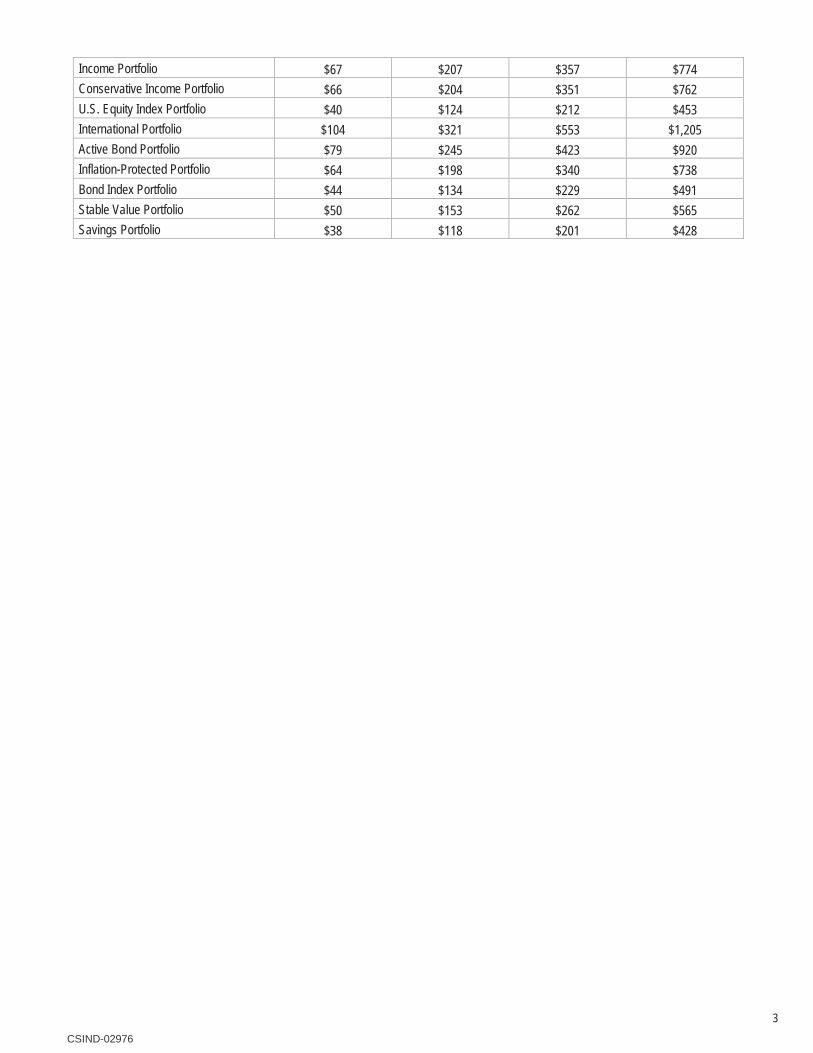

3 CSIND-02976

Income Portfolio $67 $207 $357 $774 Conservative Income Portfolio $66 $204 $351 $762 U.S. Equity Index Portfolio $40 $124 $212 $453 International Portfolio $104 $321 $553 $1,205 Active Bond Portfolio $79 $245 $423 $920 Inflation-Protected Portfolio $64 $198 $340 $738 Bond Index Portfolio $44 $134 $229 $491 Stable Value Portfolio $50 $153 $262 $565 Savings Portfolio $38 $118 $201 $428

Please file this Supplement to the CollegeChoice 529 Direct Savings Plan Disclosure Booklet with your records.

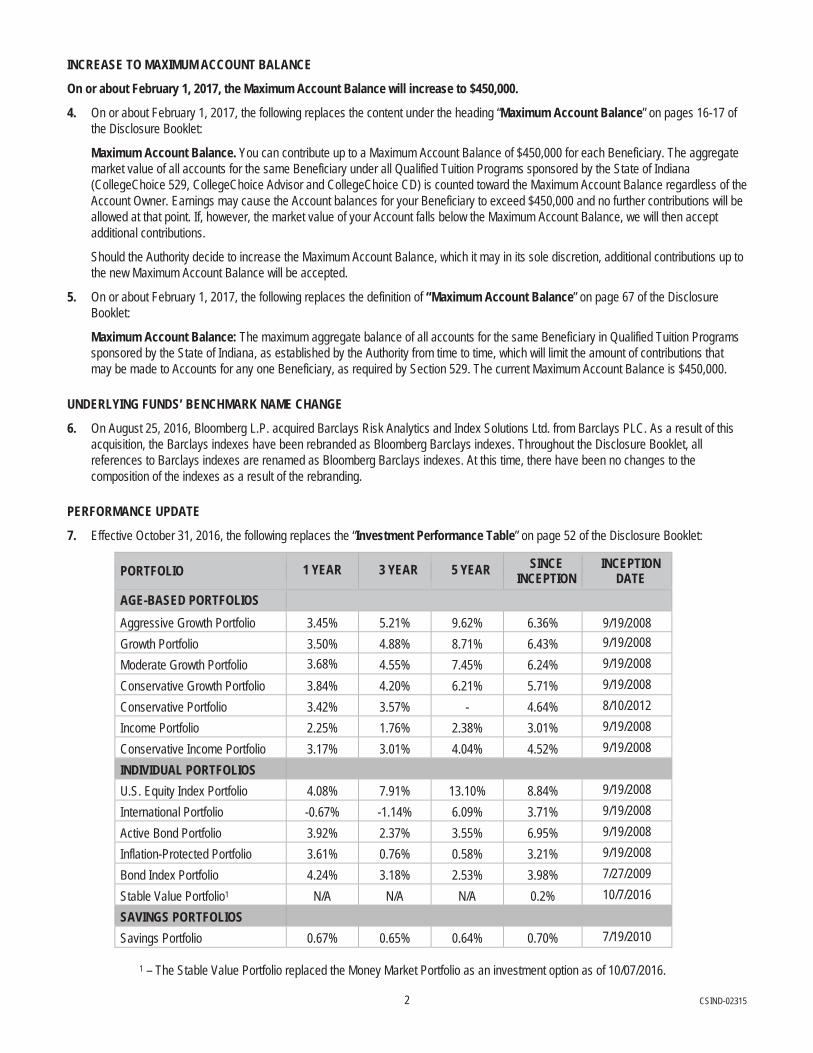

1 CSIND-02315

SUPPLEMENT DATED JANUARY 2017 TO THE COLLEGECHOICE 529 DIRECT SAVINGS PLAN

DISCLOSURE BOOKLET DATED NOVEMBER 2014

This Supplement describes important changes affecting the CollegeChoice 529 Direct Savings Plan. Unless otherwise indicated, capitalized terms have the same meaning as those in the Disclosure Booklet.

PLAN MAILING ADDRESS CHANGE

On or about April 1, 2017, the mailing address of the Plan will change.

1. On or about April 1, 2017, the following replaces the content under the heading “How do I contact the Plan?” on page 9 of theDisclosure Booklet:

Phone: 1-866-485-9415

Monday through Friday, 8 a.m. to 8 p.m. Eastern time

Online: www.collegechoicedirect.com

Regular Mail:College Choice 529 Direct Savings PlanP.O. Box 219418Kansas City, MO 64121

Overnight Delivery:CollegeChoice 529 Direct Savings Plan920 Main Street, Suite 900Kansas City, MO 64105

2. On or about April 1, 2017, the following replaces the content under the heading “Program Manager Address” on page 64 of theDisclosure Booklet:

Program Manager Address. 920 Main Street, Suite 900, Kansas City, MO 64105. All general correspondence, however, should beaddressed to CollegeChoice 529 Direct Savings Plan, P.O. Box 219418, Kansas City, MO 64121.

3. On or about April 1, 2017, the following replaces the content under the heading “Contact Information” on page 88 of the DisclosureBooklet:

Phone: 1-866-485-9415