Embed Size (px)

Citation preview

1

SUPPLEMENT NO. 5 DATED APRIL 3, 2018 TO THE OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN

DISCLOSURE BOOKLET DATED AUGUST 28, 2013

This Supplement No. 5 provides new and additional information beyond that contained in the August 28, 2013 Plan Disclosure Booklet and Participation Agreement (the “Disclosure Booklet”) of the Oklahoma College Savings Plan – Direct Plan (the “Plan”). It should be retained and read in conjunction with the Disclosure Booklet and prior supplements. I. TREATMENT OF ELEMENTARY AND SECONDARY EDUCATION TUITION COSTS Effective January 1, 2018, distributions for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school are Oklahoma and federal income tax free up to a maximum of $10,000 of distributions for such tuition expenses per taxable year per Beneficiary from all 529 Plans. II. ROLLOVERS Effective December 23, 2017, you may rollover amounts in an Account to a Section 529A Qualified ABLE Program (“ABLE”) for the same Beneficiary, or a Member of the Family thereof, federal income tax-free, subject to applicable ABLE contribution limits. Distributions from an Account in connection with any such rollover must occur before January 1, 2026.

III. OVERVIEW OF THE DIRECT PLAN On page 2 of the Disclosure Booklet, in the table entry for “Federal Tax Benefits,” the third bullet point is deleted and replaced in its entirety with the following: No federal gift tax on contributions of up to $75,000 (single filer) and $150,000 (married couple electing to split gifts) if prorated over 5 years. IV. ALLOCATION INSTRUCTIONS On page 4 of the Disclosure Booklet, the following paragraph is added as the second paragraph under the sub-heading “Choosing Investment Options”: Effective December 12, 2015, the Investment Option(s) you select and the percentage of your contribution you choose to be allocated to each Investment Option as indicated on your Application, if submitted after December 12, 2015, will be the allocation instructions for all future contributions made to your Account by any method (except payroll deduction) (“Allocation Instructions”). If you opened your Account prior to December 12, 2015 and you have not submitted Allocation Instructions for your Account for future contributions, you can submit Allocation Instructions at any time online, by telephone or by submitting the appropriate Plan form. You can change your Allocation Instructions at any time online, by telephone or by submitting the appropriate Plan form. On page 5 of the Disclosure Booklet, the paragraph under the sub-heading “Changing Investment Strategy for Future Contributions” is replaced with the following: You may change your Allocation Instructions for future contributions at any time online, by telephone or by submitting the appropriate Plan form. On page 5 of the Disclosure Booklet, the last sentence of the paragraph under the sub-heading “Checks,” is replaced with the following: If you opened your Account prior to December 12, 2015 and you have not submitted Allocation Instructions for your Account for future contributions, with each contribution by check, you will need to tell the Plan in which Investment Option(s) your contribution should be invested and how much of the contribution should be invested in each Investment Option. On page 6 of the Disclosure Booklet, the following sentence is added to the end of the paragraph under the sub-heading “One-time Electronic Funds Transfer”:

00208218

A40245 OK1803.XXP5

2

If you opened your Account prior to December 12, 2015 and you have not submitted Allocation Instructions for your Account for future contributions, with each contribution by a one-time electronic funds transfer, you will need to tell the Plan in which Investment Option(s) your contribution should be invested and how much of the contribution should be invested in each Investment Option.

V. DIRECT PLAN FEES Beginning on page 7 of the Disclosure Booklet, the section entitled “Direct Plan Fees” is deleted in its entirety and replaced with the following:

Direct Plan Fees The following table describes the Direct Plan’s current fees. The Board reserves the right to change the fees and/or to impose additional fees in the future. Fee Table

Investment Option Direct Plan

Manager Fee (1)(2)

Oklahoma Administrative

Fee

Estimated Expenses of an

Investment Option’s

Underlying Investments(3)

Total Annual Asset-Based

Fees(4)

Conservative Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.12% 0.42% Age Band 4–7 Years 0.30% None 0.12% 0.42% Age Band 8–11 Years 0.30% None 0.13% 0.43% Age Band 12–14 Years 0.30% None 0.11% 0.41% Age Band 15–17 Years 0.30% None 0.07% 0.37% Age Band 18 Years and over 0.30% None 0.05% 0.35%

Moderate Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.11% 0.41% Age Band 4–7 Years 0.30% None 0.12% 0.42% Age Band 8–11 Years 0.30% None 0.12% 0.42% Age Band 12–14 Years 0.30% None 0.13% 0.43% Age Band 15–17 Years 0.30% None 0.11% 0.41% Age Band 18 Years and over 0.30% None 0.08% 0.38%

Aggressive Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.10% 0.40% Age Band 4–7 Years 0.30% None 0.11% 0.41% Age Band 8–11 Years 0.30% None 0.12% 0.42% Age Band 12–14 Years 0.30% None 0.12% 0.42% Age Band 15–17 Years 0.30% None 0.13% 0.43% Age Band 18 Years and over 0.30% None 0.11% 0.41%

Diversified Equity Option 0.30% None 0.48% 0.78% Global Equity Index Option 0.30% None 0.10% 0.40% U.S. Equity Index Option 0.30% None 0.05% 0.35% Balanced Option 0.30% None 0.36% 0.66% Fixed Income Option 0.30% None 0.17% 0.47% Guaranteed Option(5) N/A N/A N/A N/A

3

(1) Although the Direct Plan Manager Fee is deducted from an Investment Option, not from your Account, each Account in the Investment Option indirectly bears its pro rata share of the Direct Plan Manager Fee as this fee reduces the Investment Option’s return.

(2) Each Investment Option (with the exception of the Guaranteed Option) pays the Direct Plan Manager a fee at an annual rate of 0.30% (30 basis points) of the average daily net assets held by that Investment Option. If the total market value of the assets in the Direct Plan becomes equal to or greater than $1 billion for a period of at least 90 consecutive days, the Direct Plan Manager fee will be reduced by 0.05% (5 basis points) to the annual rate of 0.25% (25 basis points).

(3) The percentages set forth in this column are based on the expense ratios of the mutual funds in which an Investment Option invests. The percentages are calculated using the expense ratio reported in each mutual fund’s most recent prospectus available prior to the printing of this Supplement and are weighted according to the Investment Option’s allocation among the mutual funds in which it invests. Although these expenses are not deducted from an Investment Option’s assets, each Investment Option (other than the Guaranteed Option, which does not invest in mutual funds) indirectly bears its pro rata share of the expenses of the mutual funds in which it invests, as these expenses reduce such mutual fund’s return.

(4) These figures represent the estimated weighted annual expense ratios of the mutual funds in which the Investment Options invest plus the fee paid to the Direct Plan Manager.

(5) The Guaranteed Option does not pay a Direct Plan Manager Fee. TIAA-CREF Life Insurance Company (“TIAA-CREF Life”), the issuer of the funding agreement in which this Investment Option invests and an affiliate of TFI, makes payments to the Direct Plan Manager. This payment, among many other factors, is considered by the issuer when determining the interest rate(s) credited under the funding agreement.

Investment Cost Example. The example in the following table is intended to help you compare the cost of investing in the different Investment Options over various periods of time. This example assumes that:

• You invest $10,000 in an Investment Option for the time periods shown below. • Your investment has a 5% compounded return each year. • You withdraw the assets from the Investment Option at the end of the specified periods for Qualified

Higher Education Expenses. • Total Annual Asset-Based Fees remain the same as those shown in the Fee Table above.

Although your actual costs may be higher or lower, based on the above assumptions, your costs would be:

INVESTMENT OPTION APPROXIMATE COST OF $10,000 INVESTMENT 1 Year 3 Years 5 Years 10 Years

Conservative Managed Allocation Option

Age Band 0–3 Years $43 $135 $236 $531 Age Band 4–7 Years $43 $135 $236 $531 Age Band 8–11 Years $44 $138 $241 $543 Age Band 12–14 Years $42 $132 $230 $518 Age Band 15–17 Years $38 $119 $208 $469 Age Band 18 Years and over $36 $113 $197 $444

Moderate Managed Allocation Option

Age Band 0–3 Years $42 $132 $230 $518 Age Band 4–7 Years $43 $135 $236 $531 Age Band 8–11 Years $43 $135 $236 $531 Age Band 12–14 Years $44 $138 $241 $543 Age Band 15–17 Years $42 $132 $230 $518 Age Band 18 Years and over $39 $122 $214 $481

4

INVESTMENT OPTION APPROXIMATE COST OF $10,000 INVESTMENT 1 Year 3 Years 5 Years 10 Years

Aggressive Managed Allocation Option

Age Band 0–3 Years $41 $129 $225 $506 Age Band 4–7 Years $42 $132 $230 $518 Age Band 8–11 Years $43 $135 $236 $531 Age Band 12–14 Years $43 $135 $236 $531 Age Band 15–17 Years $44 $138 $241 $543 Age Band 18 Years and over $42 $132 $230 $518

Diversified Equity Option $80 $250 $435 $969 Global Equity Index Option $41 $129 $225 $506 U.S. Equity Index Option $36 $113 $197 $444 Balanced Option $68 $212 $369 $825 Fixed Income Option $48 $151 $264 $592 Guaranteed Option N/A N/A N/A N/A

VI. INVESTMENT OPTIONS On pages 10-14 of the Disclosure Booklet, ticker symbols are added in parentheses next to or underneath the name of the following mutual funds: TIAA-CREF Equity Index Fund (TIEIX) TIAA-CREF International Equity Index Fund (TCIEX) TIAA-CREF Emerging Markets Equity Index Fund (TEQLX) TIAA-CREF Real Estate Securities Fund (TIREX) TIAA-CREF Bond Index Fund (TBIIX) TIAA-CREF Inflation-Linked Bond Fund (TIILX) TIAA-CREF High Yield Fund (TIHYX) TIAA-CREF Short Term Bond Index Fund (TNSHX) TIAA-CREF Growth & Income Fund (TIGRX) TIAA-CREF Large-Cap Growth Fund (TILGX) TIAA-CREF Large-Cap Value Fund (TRLIX) TIAA-CREF Mid-Cap Growth Fund (TRPWX) TIAA-CREF Mid-Cap Value Fund (TIMVX) TIAA-CREF Small-Cap Equity Fund (TISEX) TIAA-CREF Emerging Markets Equity Fund (TEMLX) VII. PAST PERFORMANCE Beginning on page 18 of the Disclosure Booklet, the performance tables under the heading “Past Performance” are deleted in their entirety and replaced with the following: Conservative Managed Allocation Option

Average Annual Total Returns for the Period Ended January 31, 2018

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 17.44% 8.46% 8.71% N/A 9.29% October 1, 2010

Benchmark 16.77% 8.48% 8.82% N/A 9.21%

4–7 Years 14.71% 7.20% 7.52% N/A 7.90% October 1, 2010

Benchmark 14.40% 7.41% 7.70% N/A 8.22%

8–11 Years 12.38% 6.14% 6.39% N/A 6.71% October 11,

2010

5

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

Benchmark 12.07% 6.34% 6.59% N/A 7.04%

12–14 Years 8.92% 4.56% 4.71% N/A 5.01% October 11,

2010

Benchmark 8.44% 4.60% 4.78% N/A 5.21%

15–17 Years 5.22% 2.79% 2.78% N/A 3.08% October 4, 2010

Benchmark 4.76% 2.74% 2.83% N/A 3.23%

18 Years and over 1.42% 0.92% 0.80% N/A 0.97% October 11,

2010

Benchmark 1.22% 0.91% 0.93% N/A 1.16% Moderate Managed Allocation Option

Average Annual Total Returns for the Period Ended January 31, 2018

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 20.72% 9.95% 10.34% 7.06% 7.15% January 16,

2004

Benchmark 20.40% 10.09% 10.51% 7.34% 7.65%

4–7 Years 18.30% 8.83% 9.20% 6.53% 6.72% January 16,

2004

Benchmark 17.97% 9.02% 9.38% 6.96% 7.28%

8–11 Years 14.84% 7.30% 7.56% 5.88% 6.13% January 16,

2004

Benchmark 14.40% 7.41% 7.70% 6.34% 6.69%

12–14 Years 12.51% 6.20% 6.43% 5.43% 5.72% January 16,

2004

Benchmark 12.07% 6.34% 6.59% 5.89% 6.29%

15–17 Years 9.08% 4.58% 4.71% 4.21% 4.65% January 16,

2004

Benchmark 8.44% 4.60% 4.78% 4.69% 5.20%

18 Years and over 6.35% 3.31% 3.37% 3.09% 3.59% January 16,

2004

Benchmark 5.80% 3.26% 3.37% 3.29% 3.88% Aggressive Managed Allocation Option

Average Annual Total Returns for the Period Ended January 31, 2018

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 25.06% 11.92% 12.41% N/A 12.84% October 1, 2010

Benchmark 25.40% 12.24% 12.75% N/A 12.59%

4–7 Years 20.87% 10.00% 10.34% N/A 10.37% October 1, 2010

Benchmark 20.40% 10.09% 10.51% N/A 10.67%

8–11 Years 18.35% 8.90% 9.22% N/A 9.48% October 4, 2010

Benchmark 17.97% 9.02% 9.38% N/A 9.77%

12–14 Years 14.69% 7.22% 7.52% N/A 7.93% October 4, 2010

Benchmark 14.40% 7.41% 7.70% N/A 8.28%

15–17 Years 12.37% 6.15% 6.38% N/A 6.94% October 4, 2010

6

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

Benchmark 12.07% 6.34% 6.59% N/A 7.27%

18 Years and over 8.94% 4.58% 4.69% N/A 4.97% October 15,

2010

Benchmark 8.45% 4.61% 4.78% N/A 5.21% Risk-Based Investment Options

Average Annual Total Returns for the Period Ended January 31, 2018

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

Diversified Equity Option 28.49% 12.71% 12.83% 7.66% 7.76% July 19, 2006

Benchmark 25.36% 12.27% 12.78% 8.03% 7.99%

U.S. Equity Index Option 24.80% 13.73% 15.10% N/A 14.83% October 1, 2010

Benchmark 25.16% 14.11% 15.53% N/A 15.28% Global Equity Index

Option 24.96% 11.86% 12.38% 7.50% 5.90% April 27, 2001

Benchmark 25.40% 12.24% 12.75% 8.03% 6.68%

Balanced Option 18.24% 8.35% 8.57% 6.42% 6.70% July 19, 2006

Benchmark 15.67% 8.02% 8.42% 6.63% 6.88%

Fixed Income Option 1.74% 0.96% 1.41% 3.13% 3.70% July 28, 2006

Benchmark 2.20% 1.43% 1.91% 3.84% 4.50%

Guaranteed Option 1.57% 1.37% 1.29% 1.90% 2.64% May 1, 2001

VIII. FEDERAL GIFT, ESTATE AND GENERATION-SKIPPING TRANSFER TAX TREATMENT On pages 22-23 of the Disclosure Booklet, the disclosure under the sub-heading “Federal Gift, Estate and Generation-Skipping Transfer Tax Treatment” is amended by:

• replacing the individual annual exclusion amount of “$14,000” with “$15,000” in the second sentence of the second paragraph;

• replacing the combined annual exclusion of ”$28,000” with “$30,000” in the second sentence of the second paragraph;

• replacing the individual annual exclusion amount of “$14,000” with “$15,000” in the first sentence of the third paragraph;

• replacing the combined annual exclusion of ”$28,000” with “$30,000” in the first sentence of the third paragraph;

• replacing the ratable amount of ”$70,000” with “$75,000” in the first sentence of the third paragraph; • replacing the ratable amount of ”$140,000” with “$150,000” in the first sentence of the third paragraph; • replacing the individual lifetime exemption amount of “$5,250,000” with “$11,180,000” in the second

sentence of the fourth paragraph; • replacing the combined lifetime exemption amount of “$10,500,000” with “$22,360,000” in the third

sentence of the fourth paragraph; • replacing the estate tax exemption amount of “$5,250,000” with “$11,180,000” in the second to last

sentence of the fifth paragraph; and • replacing the generation-skipping transfer tax exemption amount of “$5,250,000” with “$11,180,000” in

the third to last sentence of the sixth paragraph.

1 TIAA PUBLIC

SUPPLEMENT NO. 4 DATED JUNE 14, 2017 TO THE

OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN DISCLOSURE BOOKLET DATED AUGUST 28, 2013

This Supplement No. 4 provides new and additional information beyond that contained in the August 28, 2013 Plan Disclosure Booklet and Participation Agreement, as supplemented (the “Disclosure Booklet”), of the Oklahoma College Savings Plan – Direct Plan (the “Direct Plan”). It should be retained and read in conjunction with the Disclosure Booklet and prior supplements. I. OVERVIEW OF THE DIRECT PLAN On page 2 of the Disclosure Booklet, the first bullet in description of “Investment Options” is deleted and replaced with the following:

• Three age-based options that invest in multiple funds and in a funding agreement. II. FREQUENTLY USED TERMS On page 3 of the Disclosure Booklet, the definition of “Qualified Higher Education Expenses” is deleted and replaced with the following: Generally, tuition, certain room and board expenses, fees, the cost of computers, hardware, certain software, and internet access and related services, and the cost of books, supplies and equipment required for the enrollment or attendance of a Beneficiary at an Eligible Educational Institution. III. CONTRIBUTIONS

On page 5 of the Disclosure Booklet, the sentence under the sub-heading “Impermissible Methods of Contribution” is revised to read: The Direct Plan cannot accept contributions made by cash, starter check, traveler’s check, credit card, convenience check, or money order.

IV. DIRECT PLAN FEES Beginning on page 7 of the Disclosure Booklet, the section entitled “Direct Plan Fees” is deleted in its entirety and replaced with the following:

Direct Plan Fees The following table describes the Direct Plan’s current fees. The Board reserves the right to change the fees and/or to impose additional fees in the future. Fee Table

Investment Option Direct Plan

Manager Fee (1)(2)

Oklahoma Administrative

Fee

Estimated Expenses of an

Investment Option’s

Underlying Investments(3)

Total Annual Asset-Based

Fees(4)

Conservative Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.12% 0.42% Age Band 4–7 Years 0.30% None 0.13% 0.43% Age Band 8–11 Years 0.30% None 0.13% 0.43% Age Band 12–14 Years 0.30% None 0.11% 0.41% Age Band 15–17 Years 0.30% None 0.07% 0.37% Age Band 18 Years and over 0.30% None 0.06% 0.36%

A40003

OK1706.XXP4

2 TIAA PUBLIC

Investment Option Direct Plan

Manager Fee (1)(2)

Oklahoma Administrative

Fee

Estimated Expenses of an

Investment Option’s

Underlying Investments(3)

Total Annual Asset-Based

Fees(4)

Moderate Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.11% 0.41% Age Band 4–7 Years 0.30% None 0.12% 0.42% Age Band 8–11 Years 0.30% None 0.13% 0.43% Age Band 12–14 Years 0.30% None 0.13% 0.43% Age Band 15–17 Years 0.30% None 0.11% 0.41% Age Band 18 Years and over 0.30% None 0.08% 0.38%

Aggressive Managed Allocation Option

Age Band 0–3 Years 0.30% None 0.10% 0.40% Age Band 4–7 Years 0.30% None 0.11% 0.41% Age Band 8–11 Years 0.30% None 0.12% 0.42% Age Band 12–14 Years 0.30% None 0.13% 0.43% Age Band 15–17 Years 0.30% None 0.13% 0.43% Age Band 18 Years and over 0.30% None 0.11% 0.41%

Diversified Equity Option 0.30% None 0.48% 0.78% Global Equity Index Option 0.30% None 0.10% 0.40% U.S. Equity Index Option 0.30% None 0.05% 0.35% Balanced Option 0.30% None 0.36% 0.66% Fixed Income Option 0.30% None 0.17% 0.47% Guaranteed Option(5) None None None None

(1) Although the Direct Plan Manager Fee is deducted from an Investment Option, not from your Account, each

Account in the Investment Option indirectly bears its pro rata share of the Direct Plan Manager Fee as this fee reduces the Investment Option’s return.

(2) Each Investment Option (with the exception of the Guaranteed Option) pays the Direct Plan Manager a fee at an annual rate of 0.30% (30 basis points) of the average daily net assets held by that Investment Option. If the total market value of the assets in the Direct Plan becomes equal to or greater than $1 billion for a period of at least 90 consecutive days, the Direct Plan Manager fee will be reduced by 0.05% (5 basis points) to the annual rate of 0.25% (25 basis points).

(3) The percentages set forth in this column are based on the expense ratios of the mutual funds in which an Investment Option invests. The percentages are calculated using the expense ratio reported in each mutual fund’s most recent prospectus available prior to the printing of this Supplement and are weighted according to the Investment Option’s allocation among the mutual funds in which it invests. Although these expenses are not deducted from an Investment Option’s assets, each Investment Option (other than the Guaranteed Option, which does not invest in mutual funds) indirectly bears its pro rata share of the expenses of the mutual funds in which it invests, as these expenses reduce such mutual fund’s return.

(4) These figures represent the estimated weighted annual expense ratios of the mutual funds in which the Investment Options invest plus the fee paid to the Direct Plan Manager.

(5) The Guaranteed Option does not pay a Direct Plan Manager Fee. TIAA-CREF Life Insurance Company (“TIAA-CREF Life”), the issuer of the funding agreement in which this Investment Option invests and an affiliate of TFI, makes payments to the Direct Plan Manager. This payment, among many other factors, is considered by the issuer when determining the interest rate(s) credited under the funding agreement.

3 TIAA PUBLIC

Investment Cost Example. The example in the following table is intended to help you compare the cost of investing in the different Investment Options over various periods of time. This example assumes that:

• You invest $10,000 in an Investment Option for the time periods shown below. • Your investment has a 5% compounded return each year. • You withdraw the assets from the Investment Option at the end of the specified periods for Qualified Higher

Education Expenses. • Total Annual Asset-Based Fees remain the same as those shown in the Fee Table above.

Although your actual costs may be higher or lower, based on the above assumptions, your costs would be:

INVESTMENT OPTION APPROXIMATE COST OF $10,000 INVESTMENT 1 Year 3 Years 5 Years 10 Years

Conservative Managed Allocation Option

Age Band 0–3 Years $43 $135 $236 $531 Age Band 4–7 Years $44 $138 $241 $543 Age Band 8–11 Years $44 $138 $241 $543 Age Band 12–14 Years $42 $132 $230 $518 Age Band 15–17 Years $38 $119 $208 $469 Age Band 18 Years and over $37 $116 $202 $456

Moderate Managed Allocation Option

Age Band 0–3 Years $42 $132 $230 $518 Age Band 4–7 Years $43 $135 $236 $531 Age Band 8–11 Years $44 $138 $241 $543 Age Band 12–14 Years $44 $138 $241 $543 Age Band 15–17 Years $42 $132 $230 $518 Age Band 18 Years and over $39 $122 $214 $481

Aggressive Managed Allocation Option

Age Band 0–3 Years $41 $129 $225 $506 Age Band 4–7 Years $42 $132 $230 $518 Age Band 8–11 Years $43 $135 $236 $531 Age Band 12–14 Years $44 $138 $241 $543 Age Band 15–17 Years $44 $138 $241 $543 Age Band 18 Years and over $42 $132 $230 $518

Diversified Equity Option $80 $250 $435 $969 Global Equity Index Option $41 $129 $225 $506 U.S. Equity Index Option $36 $113 $197 $444 Balanced Option $68 $212 $369 $825 Fixed Income Option $48 $151 $264 $592 Guaranteed Option None None None None

V. INVESTMENT OPTIONS

On page 9 of the Disclosure Booklet, the first sentence under the sub-heading “Investments of the Investment Options” is deleted and replaced with the following: Each Investment Option will be invested in one or more mutual funds and/or in a funding agreement. On page 9 of the Disclosure Booklet, the following sentence is added to the end of the first paragraph

under the sub-heading “Investment Strategy” for the age-based Investment Options: Most age bands also invest a portion of their assets in a funding agreement. The percentage of the age band invested in a funding agreement grows as the Beneficiary ages.

4 TIAA PUBLIC

On page 9 of the Disclosure Booklet, the third paragraph under the sub-heading “Investment Strategy” for the age-based Investment Options is deleted and replaced with the following: Each age band invests in multiple mutual funds to varying degrees, and certain age bands also invest in a funding agreement to varying degrees. The percentages of each age band’s assets allocated to the mutual funds or to the funding agreement are set forth in the tables on the following pages On page 10 of the Disclosure Booklet, the seventh paragraph, including the corresponding bullets, under the sub-heading “Investment Strategy” for the age-based Investment Options is deleted and replaced with the following: In addition to the investments described above, to varying degrees, certain age bands invest a percentage of their assets in a funding agreement issued by TIAA-CREF that is substantially similar to the funding agreement in which the Guaranteed Option invests 100% of its assets. (See “Guaranteed Option” for a description of the funding agreement in which the Guaranteed Option invests.) As a Beneficiary ages, investments in mutual funds will decrease and investments in the funding agreement will increase. On page 10 of the Disclosure Booklet, the sub-section “Investment Risks” for the age-based Investment Options is deleted and replaced with the following: Investment Risks. Because the age-based Investment Options invest in mutual funds that, taken together, invest in a diversified portfolio of securities, the age-based Investment Options are subject to the following risks to varying degrees: Active Management Risk, Call Risk, Credit Risk, Derivatives Risk, Downgrade Risk, Emerging Markets Risk, Extension Risk, Fixed Income Foreign Investment Risk, Floating and Variable Rate Securities Risk, Foreign Investment Risk, Illiquid Investments Risk, Income Volatility Risk, Index Risk, Interest Rate Risk, Issuer Risk, Large-Cap Risk, Market Risk, Market Volatility, Liquidity and Valuation Risk, Mid-

Cap Risk, Non-Investment-Grade Securities Risk, Prepayment Risk, Real Estate Investing Risk, Senior Loan Risk, Small-Cap Risk, Special Risks for Inflation-Indexed Bonds, and U.S. Government Securities Risk. With respect to the funding agreement in which the age-based Investment Options invest, there is a risk that TIAA-CREF Life could fail to perform its obligations under the funding agreement for financial or other reasons. The age bands for younger Beneficiaries are subject to Emerging Markets Risk, Foreign Investment Risk, Large-Cap Risk, Market Risk, Mid-Cap Risk, Real Estate Investing Risk, and Small-Cap Risk to a greater extent than the age bands for older Beneficiaries. Likewise, the age bands for older Beneficiaries are subject to Call Risk, Credit Risk, Derivatives Risk, Downgrade Risk, Extension Risk, Fixed Income Foreign Investment Risk, Floating and Variable Rate Securities Risk, Illiquid Investments Risk, Income Volatility Risk, Interest Rate Risk, Market Volatility, Liquidity and Valuation Risk, Non-Investment-Grade Securities Risk, Prepayment Risk, Senior Loan Risk, Special Risks for Inflation-Indexed Bonds, and U.S. Government Securities Risk to a greater extent than the age bands for younger Beneficiaries. The age bands for older Beneficiaries are subject to the risk associated with investments in the funding agreement to a greater extent than are the age bands for older Beneficiaries. On page 10 of the Disclosure Booklet, the information under “Conservative Managed Allocation Option” is deleted in its entirety and replaced with the following: Each age band in the Conservative Managed Allocation Option will invest a larger percentage of its assets in mutual funds that invest primarily in debt securities and in a funding agreement than will the corresponding age band within the Moderate or Aggressive Managed Allocation Option. Likewise, each age band in the Conservative Managed Allocation Option will invest a smaller percentage of its assets in mutual funds that invest primarily in equity securities than will the corresponding age band within the Moderate or Aggressive Managed Allocation Options.

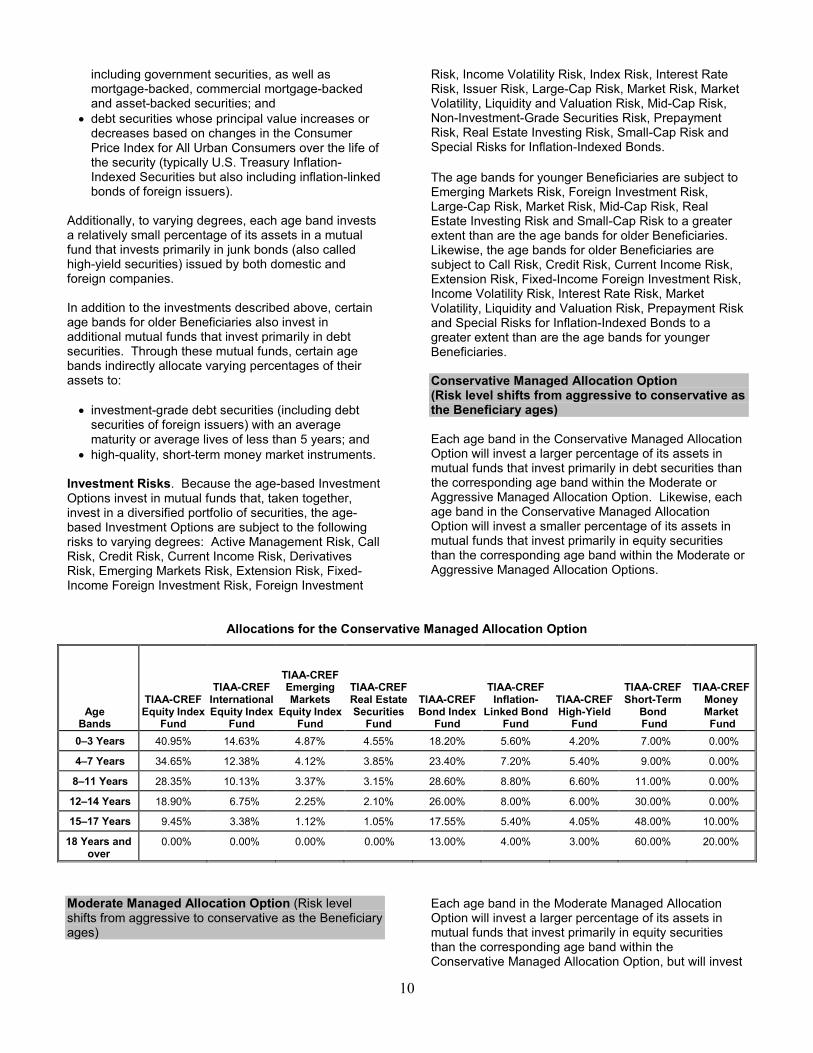

Allocations for the Conservative Managed Allocation Option

Age Bands

TIAA-CREF Equity Index Fund

TIAA- CREF

International Equity Index

Fund

TIAA-CREF

Emerging Markets Equity Index Fund

TIAA-CREF Real

Estate Securities

Fund

TIAA-CREF Bond Index Fund

TIAA-CREF

Inflation-Linked Bond Fund

TIAA- CREF

High-Yield Fund

TIAA- CREF

Short-Term Bond

Index Fund

TIAA-CREF Life Funding

Agreement

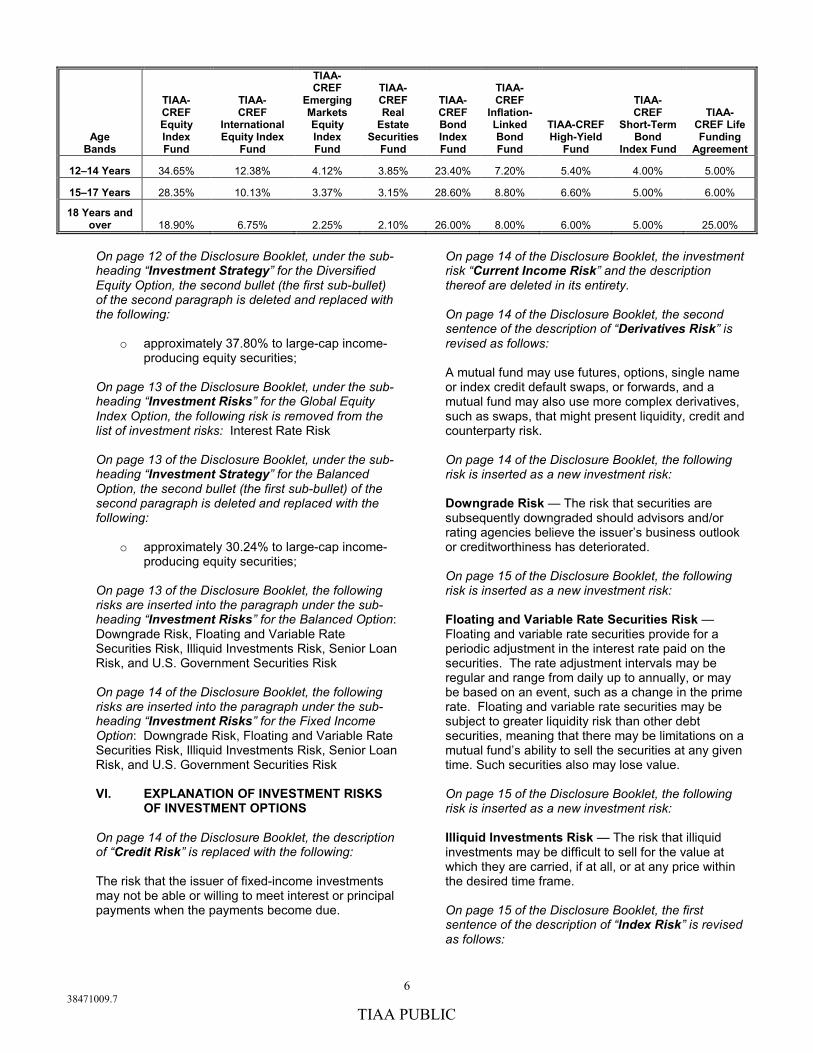

0–3 Years 40.95% 14.63% 4.87% 4.55% 18.20% 5.60% 4.20% 3.00% 4.00%

4–7 Years 34.65% 12.38% 4.12% 3.85% 23.40% 7.20% 5.40% 4.00% 5.00%

8–11 Years 28.35% 10.13% 3.37% 3.15% 28.60% 8.80% 6.60% 5.00% 6.00%

12–14 Years 18.90% 6.75% 2.25% 2.10% 26.00% 8.00% 6.00% 6.00% 24.00%

15–17 Years 9.45% 3.38% 1.12% 1.05% 17.55% 5.40% 4.05% 8.00% 50.00%

5 TIAA PUBLIC

Age Bands

TIAA-CREF Equity Index Fund

TIAA- CREF

International Equity Index

Fund

TIAA-CREF

Emerging Markets Equity Index Fund

TIAA-CREF Real

Estate Securities

Fund

TIAA-CREF Bond Index Fund

TIAA-CREF

Inflation-Linked Bond Fund

TIAA- CREF

High-Yield Fund

TIAA- CREF

Short-Term Bond

Index Fund

TIAA-CREF Life Funding

Agreement 18 Years and

over 0.00% 0.00% 0.00% 0.00% 13.00% 4.00% 3.00% 15.00% 65.00% Beginning on page 10 of the Disclosure Booklet, the information under “Moderate Managed Allocation Option” is deleted in its entirety and replaced with the following: Each age band in the Moderate Managed Allocation Option will invest a larger percentage of its assets in mutual funds that invest primarily in equity securities than the corresponding age band within the Conservative Managed Allocation Option, but will invest a smaller percentage of its assets in such mutual funds

than will the corresponding age band within the Aggressive Managed Allocation Option. Likewise, each age band in the Moderate Managed Allocation Option will invest a larger percentage of its assets in mutual funds that invest primarily in debt securities and in a funding agreement than the corresponding age band within the Aggressive Managed Allocation Option, but will invest a smaller percentage of its assets in such mutual funds and in the funding agreement than will the corresponding age band within the Conservative Managed Allocation Option.

Allocations for the Moderate Managed Allocation Option

Age Bands

TIAA-CREF Equity Index Fund

TIAA- CREF

International Equity Index

Fund

TIAA-CREF

Emerging Markets Equity Index Fund

TIAA-CREF Real

Estate Securities

Fund

TIAA-CREF Bond Index Fund

TIAA-CREF

Inflation-Linked Bond Fund

TIAA- CREF

High-Yield Fund

TIAA- CREF

Short-Term Bond

Index Fund

TIAA-CREF Life Funding

Agreement

0–3 Years 50.40% 18.00% 6.00% 5.60% 10.40% 3.20% 2.40% 2.00% 2.00%

4–7 Years 44.10% 15.75% 5.25% 4.90% 15.60% 4.80% 3.60% 3.00% 3.00%

8–11 Years 34.65% 12.38% 4.12% 3.85% 23.40% 7.20% 5.40% 4.00% 5.00%

12–14 Years 28.35% 10.13% 3.37% 3.15% 28.60% 8.80% 6.60% 5.00% 6.00%

15–17 Years 18.90% 6.75% 2.25% 2.10% 26.00% 8.00% 6.00% 6.00% 24.00%

18 Years and over 12.60% 4.50% 1.50% 1.40% 14.56% 4.48% 3.36% 12.60% 45.00%

On page 11 of the Disclosure Booklet, the information under “Aggressive Managed Allocation Option” is deleted in its entirety and replaced with the following: Each age band in the Aggressive Managed Allocation Option will invest a larger percentage of its assets in mutual funds that invest primarily in equity securities than the corresponding age band within the

Conservative or Moderate Managed Allocation Options. Likewise, each age band in the Aggressive Managed Allocation Option will invest a smaller percentage of its assets in mutual funds that invest primarily in debt securities and in a funding agreement than will the corresponding age band within the Conservative or Moderate Managed Allocation Options.

Allocations for the Aggressive Managed Allocation Option

Age Bands

TIAA- CREF Equity Index Fund

TIAA- CREF

International Equity Index

Fund

TIAA- CREF

Emerging Markets Equity Index Fund

TIAA-CREF Real

Estate Securities

Fund

TIAA-CREF Bond Index Fund

TIAA-CREF

Inflation-Linked Bond Fund

TIAA-CREF High-Yield

Fund

TIAA- CREF

Short-Term Bond

Index Fund

TIAA- CREF Life Funding

Agreement

0–3 Years 63.00% 22.50% 7.50% 7.00% 0.00% 0.00% 0.00% 0.00% 0.00%

4–7 Years 50.40% 18.00% 6.00% 5.60% 10.40% 3.20% 2.40% 2.00% 2.00%

8–11 Years 44.10% 15.75% 5.25% 4.90% 15.60% 4.80% 3.60% 3.00% 3.00%

6 38471009.7

TIAA PUBLIC

Age Bands

TIAA- CREF Equity Index Fund

TIAA- CREF

International Equity Index

Fund

TIAA- CREF

Emerging Markets Equity Index Fund

TIAA-CREF Real

Estate Securities

Fund

TIAA-CREF Bond Index Fund

TIAA-CREF

Inflation-Linked Bond Fund

TIAA-CREF High-Yield

Fund

TIAA- CREF

Short-Term Bond

Index Fund

TIAA- CREF Life Funding

Agreement

12–14 Years 34.65% 12.38% 4.12% 3.85% 23.40% 7.20% 5.40% 4.00% 5.00%

15–17 Years 28.35% 10.13% 3.37% 3.15% 28.60% 8.80% 6.60% 5.00% 6.00%

18 Years and over 18.90% 6.75% 2.25% 2.10% 26.00% 8.00% 6.00% 5.00% 25.00%

On page 12 of the Disclosure Booklet, under the sub-heading “Investment Strategy” for the Diversified Equity Option, the second bullet (the first sub-bullet) of the second paragraph is deleted and replaced with the following:

o approximately 37.80% to large-cap income-producing equity securities;

On page 13 of the Disclosure Booklet, under the sub-heading “Investment Risks” for the Global Equity Index Option, the following risk is removed from the list of investment risks: Interest Rate Risk On page 13 of the Disclosure Booklet, under the sub-heading “Investment Strategy” for the Balanced Option, the second bullet (the first sub-bullet) of the second paragraph is deleted and replaced with the following:

o approximately 30.24% to large-cap income-producing equity securities;

On page 13 of the Disclosure Booklet, the following risks are inserted into the paragraph under the sub-heading “Investment Risks” for the Balanced Option: Downgrade Risk, Floating and Variable Rate Securities Risk, Illiquid Investments Risk, Senior Loan Risk, and U.S. Government Securities Risk On page 14 of the Disclosure Booklet, the following risks are inserted into the paragraph under the sub-heading “Investment Risks” for the Fixed Income Option: Downgrade Risk, Floating and Variable Rate Securities Risk, Illiquid Investments Risk, Senior Loan Risk, and U.S. Government Securities Risk VI. EXPLANATION OF INVESTMENT RISKS

OF INVESTMENT OPTIONS On page 14 of the Disclosure Booklet, the description of “Credit Risk” is replaced with the following: The risk that the issuer of fixed-income investments may not be able or willing to meet interest or principal payments when the payments become due.

On page 14 of the Disclosure Booklet, the investment risk “Current Income Risk” and the description thereof are deleted in its entirety. On page 14 of the Disclosure Booklet, the second sentence of the description of “Derivatives Risk” is revised as follows: A mutual fund may use futures, options, single name or index credit default swaps, or forwards, and a mutual fund may also use more complex derivatives, such as swaps, that might present liquidity, credit and counterparty risk. On page 14 of the Disclosure Booklet, the following risk is inserted as a new investment risk: Downgrade Risk — The risk that securities are subsequently downgraded should advisors and/or rating agencies believe the issuer’s business outlook or creditworthiness has deteriorated. On page 15 of the Disclosure Booklet, the following risk is inserted as a new investment risk: Floating and Variable Rate Securities Risk — Floating and variable rate securities provide for a periodic adjustment in the interest rate paid on the securities. The rate adjustment intervals may be regular and range from daily up to annually, or may be based on an event, such as a change in the prime rate. Floating and variable rate securities may be subject to greater liquidity risk than other debt securities, meaning that there may be limitations on a mutual fund’s ability to sell the securities at any given time. Such securities also may lose value. On page 15 of the Disclosure Booklet, the following risk is inserted as a new investment risk: Illiquid Investments Risk — The risk that illiquid investments may be difficult to sell for the value at which they are carried, if at all, or at any price within the desired time frame. On page 15 of the Disclosure Booklet, the first sentence of the description of “Index Risk” is revised as follows:

TIAA PUBLIC

The risk that an index fund’s performance may not correspond to its benchmark index for any period of time and may underperform such index or the overall financial market. On page 15 of the Disclosure Booklet, the second sentence of the description of “Interest Rate Risk” is deleted and replaced with the following sentences: This risk is heightened to the extent the fund invests in longer duration fixed-income investments and during periods when prevailing interest rates are low or negative. Currently, interest rates in the United States and in certain foreign markets are at or near historic lows, which may increase a mutual fund’s exposure to risks associated with rising interest rates. In general, changing interest rates could have unpredictable effects on the markets and may expose fixed-income and related markets to heightened volatility. On page 16 of the Disclosure Booklet, the following risk is inserted as a new investment risk: Senior Loan Risk — Many senior loans present credit risk comparable to high-yield securities. The liquidation of the collateral backing a senior loan may not satisfy the borrower’s obligation to a mutual fund in the event of non-payment of scheduled interest or principal. Senior loans also expose a mutual fund to call risk and illiquid investments risk. The secondary market for senior loans can be limited. Trades can be infrequent and the values for senior loans may experience volatility. In some cases, negotiations for the sale or settlement of senior loans may require weeks to complete, which may impair a mutual fund’s ability to raise cash to satisfy redemptions, pay dividends, pay expenses or to take advantage of

other investment opportunities in a timely manner. If an issuer of a senior loan prepays or redeems the loan prior to maturity, a mutual fund will have to reinvest the proceeds in other senior loans or instruments that may pay lower interest rates. On page 16 of the Disclosure Booklet, the following risk is inserted as a new investment risk: U.S. Government Securities Risk — Securities issued by the U.S. Government or one of its agencies or instrumentalities may receive varying levels of support from the U.S. Government, which could affect a mutual fund’s ability to recover should they default. To the extent a mutual fund invests significantly in securities issued or guaranteed by the U.S. Government or its agencies or instrumentalities, any market movements, regulatory changes or changes in political or economic conditions that affect the securities of the U.S. Government or its agencies or instrumentalities in which the mutual fund invests may have a significant impact on the mutual fund’s performance. On page 16 of the Disclosure Booklet, the heading and first sentence of the sub-section “Information about the Funding Agreement and the Mutual Funds in Which the Investment Options Invest” are deleted and replaced with the following: Information about the Funding Agreements and the Mutual Funds in which the Investment Options Invest. Information about the funding agreement in which the Guaranteed Option invests is contained in this Disclosure Booklet. The funding agreement in which the age-based Investment Options invest is substantially similar to the funding agreement in which the Guaranteed Option invests.

VII. PAST PERFORMANCE Beginning on page 18 of the Disclosure Booklet, the performance tables under the heading “Past Performance” are deleted in their entirety and replaced with the following:

Conservative Managed Allocation Option Average Annual Total Returns for the Period Ended April 30, 2017

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 11.47% 5.49% 8.18% N/A 8.41% October 1, 2010

Benchmark 11.22% 5.77% 7.93% N/A 8.38%

4–7 Years 9.67% 4.88% 6.67% N/A 7.17% October 1, 2010

Benchmark 9.79% 5.27% 7.01% N/A 7.56%

8–11 Years 8.22% 4.36% 5.74% N/A 6.10% October 11, 2010

Benchmark 8.38% 4.77% 6.08% N/A 6.52%

12–14 Years 6.25% 3.42% 4.28% N/A 4.60% October 11, 2010

TIAA PUBLIC

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

Benchmark 5.99% 3.71% 4.49% N/A 4.89%

15–17 Years 3.79% 2.25% 2.60% N/A 2.89% October 4, 2010

Benchmark 3.41% 2.38% 2.69% N/A 3.09%

18 Years and over 1.24% 1.02% 0.83% N/A 0.97% October 11, 2010

Benchmark 0.99% 1.15% 0.97% N/A 1.19% Moderate Managed Allocation Option

Average Annual Total Returns for the Period Ended April 30, 2017

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 13.37% 6.19% 9.03% 5.03% 6.42% January 16, 2004

Benchmark 13.39% 6.50% 9.30% 5.31% 6.96%

4–7 Years 11.87% 5.68% 8.10% 4.79% 6.10% January 16, 2004

Benchmark 11.94% 6.02% 8.38% 5.28% 6.70%

8–11 Years 9.87% 4.93% 6.74% 4.64% 5.66% January 16, 2004

Benchmark 9.79% 5.27% 7.01% 5.19% 6.28%

12–14 Years 8.41% 4.42% 5.81% 4.53% 5.36% January 16, 2004

Benchmark 8.38% 4.77% 6.08% 5.09% 5.99%

15–17 Years 6.08% 3.40% 4.25% 3.75% 4.42% January 16, 2004

Benchmark 5.99% 3.71% 4.49% 4.34% 5.04%

18 Years and over 4.32% 2.51% 3.10% 2.87% 3.45% January 16, 2004

Benchmark 4.08% 2.63% 3.15% 3.15% 3.79% Aggressive Managed Allocation Option

Average Annual Total Returns for the Period Ended April 30, 2017

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

0–3 Years 16.01% 7.12% 11.57% N/A 11.47% October 1, 2010

Benchmark 16.33% 7.44% 11.11% N/A 11.17%

4–7 Years 13.41% 6.18% 8.95% N/A 9.21% October 1, 2010

Benchmark 13.39% 6.50% 9.30% N/A 9.59%

8–11 Years 11.85% 5.68% 8.06% N/A 8.50% October 4, 2010

Benchmark 11.94% 6.02% 8.38% N/A 8.87%

12–14 Years 9.87% 4.95% 6.71% N/A 7.21% October 4, 2010

Benchmark 9.79% 5.27% 7.01% N/A 7.62%

15–17 Years 8.45% 4.40% 5.77% N/A 6.38% October 4, 2010

Benchmark 8.38% 4.77% 6.08% N/A 6.78%

18 Years and over 6.18% 3.43% 4.27% N/A 4.58% October 15, 2010

Benchmark 5.99% 3.71% 4.49% N/A 4.89%

TIAA PUBLIC

Risk-Based Investment Options Average Annual Total Returns for the Period Ended April 30, 2017

Age Bands 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date

Diversified Equity Option 16.90% 7.16% 10.86% 4.81% 6.46% July 19, 2006

Benchmark 16.27% 7.51% 11.13% 5.30% 6.84%

U.S. Equity Index Option 18.21% 9.70% 13.12% N/A 13.63% October 1, 2010

Benchmark 18.58% 10.10% 13.57% N/A 14.07%

Global Equity Index Option 16.00% 7.12% 10.73% 4.79% 5.06% April 27, 2001

Benchmark 16.33% 7.44% 11.11% 5.29% 5.86%

Balanced Option 11.19% 5.39% 7.35% 4.93% 5.97% July 19, 2006

Benchmark 10.60% 5.71% 7.62% 5.30% 6.31%

Fixed Income Option 1.68% 2.16% 1.83% 3.78% 3.91% July 28, 2006

Benchmark 2.01% 2.65% 2.35% 4.56% 4.74%

Guaranteed Option 1.46% 1.23% 1.27% 2.05% 2.68% May 1, 2001

VIII. WITHDRAWALS On page 20 of the Disclosure Booklet, under the sub-heading “Qualified Withdrawals,” the first sentence of the second paragraph is revised as follows: Qualified Higher Education Expenses are defined generally to include tuition, certain room and board expenses, fees, the cost of computers, hardware, certain software, and internet access and related services, and the cost of books, supplies and equipment required for the enrollment or attendance of a Beneficiary at an Eligible Educational Institution. On page 20 of the Disclosure Booklet, under the sub-heading “Qualified Withdrawals,” the following sentences are added to the end of the second paragraph: To be treated as Qualified Higher Education Expenses, computers, hardware, software, and internet access and related services must be used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Qualified Higher Education Expenses do not include expenses for computer software designed for sports, games, or hobbies unless the software is predominantly educational in nature. IX. FEDERAL TAX INFORMATION

On page 22 of the Disclosure Booklet, under the sub-heading “Withdrawals,” the last sentence is revised as follows: The proportion of contributions and earnings for each withdrawal is determined by the Direct Plan based on

the relative portions of earnings and contributions as of the withdrawal date for the Account from which the withdrawal was made. On page 22 of the Disclosure Booklet, the paragraph under the sub-heading “Refunds of Payments of Qualified Higher Education Expenses” is deleted and replaced with the following: If an Eligible Educational Institution refunds any portion of an amount previously withdrawn from an Account and treated as a Qualified Withdrawal, unless you contribute such amount to a qualified tuition program for the same Beneficiary not later than 60 days after the date of the refund, you may be required to treat the amount of the refund as a Nonqualified Withdrawal or Taxable Withdrawal (depending on the reason for the refund) for purposes of federal income tax. Different treatment may apply if the refund is used to pay other Qualified Higher Education Expenses of the Beneficiary. On pages 22-23 of the Disclosure Booklet, the disclosure under the sub-heading “Federal Gift, Estate and Generation-Skipping Transfer Tax Treatment” is amended by: • replacing the individual lifetime exemption

amount of “$5,250,000” with “$5,490,000” in the second sentence of the fourth paragraph;

• replacing the combined lifetime exemption amount of “$10,500,000” with “$10,980,000” in the third sentence of the fourth paragraph;

• replacing the estate tax exemption amount of “$5,250,000” with “$5,490,000” in the second to last sentence of the fifth paragraph; and

The Board of Trustees of The Oklahoma College Savings Plan, Administrator and Trustee TIAA-CREF Tuition Financing, Inc., Direct Plan Manager

TIAA-CREF Individual & Institutional Services, LLC, Distributor/Underwriter

TIAA PUBLIC

• replacing the generation-skipping transfer tax exemption amount of “$5,250,000” with

“$5,490,000” in the third to last sentence of the sixth paragraph.

The Board of Trustees of The Oklahoma College Savings Plan, Administrator and Trustee TIAA-CREF Tuition Financing, Inc., Direct Plan Manager

TIAA-CREF Individual & Institutional Services, LLC, Distributor/Underwriter

The Board of Trustees of The Oklahoma College Savings Plan, Administrator and Trustee TIAA-CREF Tuition Financing, Inc., Direct Plan Manager

TIAA-CREF Individual & Institutional Services, LLC, Distributor/Underwriter 30466435.1

SUPPLEMENT NO. 3 DATED DECEMBER 31, 2015, TO THE

OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN DISCLOSURE BOOKLET DATED AUGUST 28, 2013

This Supplement No. 3 provides new and additional information beyond that contained in the August 28, 2013 Plan Disclosure Booklet and Participation Agreement, as supplemented (the “Disclosure Booklet”) of the Oklahoma College Savings Plan – Direct Plan (the “Direct Plan”). It should be retained and read in conjunction with the Disclosure Booklet and prior supplements. I. THE DIRECT PLAN MANAGER On page 21 of the Disclosure Booklet, the first paragraph of the section entitled “The Direct Plan Manager” is deleted in its entirety and replaced with the following: The Board selected TFI as the Direct Plan Manager. TFI is a wholly owned, direct subsidiary of Teachers Insurance and Annuity Association of America (“TIAA”). TIAA, together with its companion organization, the College Retirement Equities Fund (“CREF”), forms one of America’s leading financial services organizations and one of the world’s largest pension systems, based on assets under management. Effective December 31, 2015, TIAA-CREF Individual & Institutional Services, LLC (“Services”), a wholly owned, direct subsidiary of TIAA, serves as the primary distributor and underwriter for the Direct Plan and provides certain underwriting and distribution services in furtherance of TFI’s marketing plan for the Direct Plan. Services is registered as a broker-dealer under the Securities Exchange Act of 1934 and is a member of the Financial Industry Regulatory Authority. II. OTHER INFORMATION

On page 21 of the Disclosure Booklet, the section entitled “Confirmations, Account Statements and Tax Reports” is renamed “Other Information”. The following paragraph is added at the end of the section:

Continuing Disclosure. To comply with Rule 15c2-12(b)(5) of the Securities and Exchange Commission promulgated under the Securities Exchange Act of 1934, as amended (“Rule 15c2-12”), the Direct Plan Manager has executed a Continuing Disclosure Certificate (the “Continuing Disclosure Certificate”) for the benefit of the Account Owners. Under the Continuing Disclosure Certificate, the Direct Plan Manager will provide certain financial information and operating data (the “Annual Information”) relating to the Direct Plan and notices of the occurrence of certain enumerated events set forth in the Continuing Disclosure Certificate, if material. The Annual Information will be filed on behalf of the Direct Plan with the Electronic Municipal Market Access system (the “EMMA System”) maintained by the Municipal Securities Rulemaking Board (the “MSRB”). Notices of certain enumerated events will also be filed on behalf of the Direct Plan with the MSRB.

00158979

A15251OK1512.XXP3

A14792

SUPPLEMENT NO. 2 DATED APRIL 1, 2015, TO THE OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN

DISCLOSURE BOOKLET DATED AUGUST 28, 2013

This Supplement No. 2 provides new and additional information beyond that contained in the August 28, 2013 Direct – Plan Disclosure Booklet and Participation Agreement (the “Disclosure Booklet”) of the Oklahoma College Savings Plan – Direct Plan (the “Direct Plan”). It should be retained and read in conjunction with the Disclosure Booklet. SPECIAL NOTICE — TWO TRANSFERS AMONG INVESTMENT OPTIONS PERMITTED Effective January 1, 2015, the Internal Revenue Service allows the Direct Plan to permit Account Owners to transfer funds among Investment Options twice per calendar year, rather than once per calendar year as set forth in the Disclosure Booklet. OK1504.XXP2 00138213

1

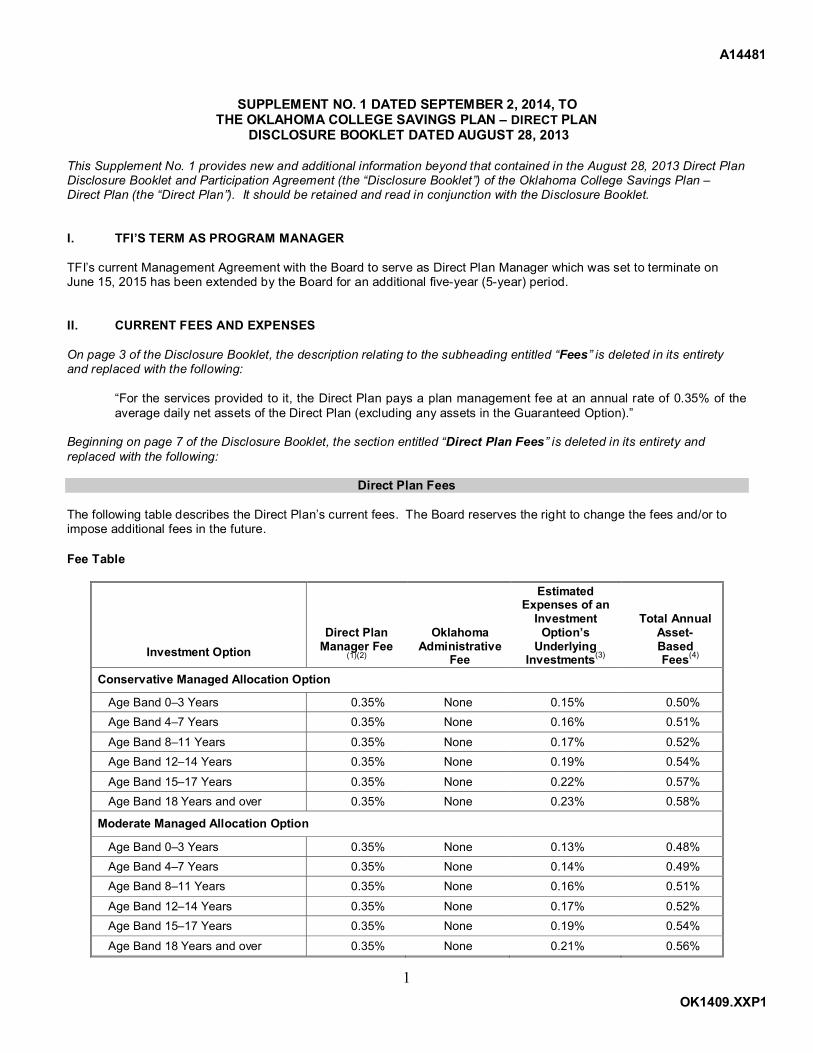

SUPPLEMENT NO. 1 DATED SEPTEMBER 2, 2014, TO THE OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN

DISCLOSURE BOOKLET DATED AUGUST 28, 2013 This Supplement No. 1 provides new and additional information beyond that contained in the August 28, 2013 Direct Plan Disclosure Booklet and Participation Agreement (the “Disclosure Booklet”) of the Oklahoma College Savings Plan – Direct Plan (the “Direct Plan”). It should be retained and read in conjunction with the Disclosure Booklet. I. TFI’S TERM AS PROGRAM MANAGER TFI’s current Management Agreement with the Board to serve as Direct Plan Manager which was set to terminate on June 15, 2015 has been extended by the Board for an additional five-year (5-year) period. II. CURRENT FEES AND EXPENSES On page 3 of the Disclosure Booklet, the description relating to the subheading entitled “Fees” is deleted in its entirety and replaced with the following:

“For the services provided to it, the Direct Plan pays a plan management fee at an annual rate of 0.35% of the average daily net assets of the Direct Plan (excluding any assets in the Guaranteed Option).”

Beginning on page 7 of the Disclosure Booklet, the section entitled “Direct Plan Fees” is deleted in its entirety and replaced with the following:

Direct Plan Fees The following table describes the Direct Plan’s current fees. The Board reserves the right to change the fees and/or to impose additional fees in the future. Fee Table

Investment Option Direct Plan

Manager Fee (1)(2)

Oklahoma Administrative

Fee

Estimated Expenses of an

Investment Option’s

Underlying Investments(3)

Total Annual Asset- Based

Fees(4)

Conservative Managed Allocation Option

Age Band 0–3 Years 0.35% None 0.15% 0.50% Age Band 4–7 Years 0.35% None 0.16% 0.51%

Age Band 8–11 Years 0.35% None 0.17% 0.52% Age Band 12–14 Years 0.35% None 0.19% 0.54%

Age Band 15–17 Years 0.35% None 0.22% 0.57% Age Band 18 Years and over 0.35% None 0.23% 0.58%

Moderate Managed Allocation Option

Age Band 0–3 Years 0.35% None 0.13% 0.48% Age Band 4–7 Years 0.35% None 0.14% 0.49% Age Band 8–11 Years 0.35% None 0.16% 0.51%

Age Band 12–14 Years 0.35% None 0.17% 0.52% Age Band 15–17 Years 0.35% None 0.19% 0.54%

Age Band 18 Years and over 0.35% None 0.21% 0.56%

A14481

OK1409.XXP1

2

Investment Option Direct Plan

Manager Fee (1)(2)

Oklahoma Administrative

Fee

Estimated Expenses of an

Investment Option’s

Underlying Investments(3)

Total Annual Asset- Based

Fees(4)

Aggressive Managed Allocation Option

Age Band 0–3 Years 0.35% None 0.12% 0.47%

Age Band 4–7 Years 0.35% None 0.13% 0.48% Age Band 8–11 Years 0.35% None 0.14% 0.49% Age Band 12–14 Years 0.35% None 0.16% 0.51%

Age Band 15–17 Years 0.35% None 0.17% 0.52% Age Band 18 Years and over 0.35% None 0.19% 0.54%

Diversified Equity Option 0.35% None 0.51% 0.86% Global Equity Index Option 0.35% None 0.12% 0.47% U.S. Equity Index Option 0.35% None 0.07% 0.42% Balanced Option 0.35% None 0.38% 0.73% Fixed Income Option 0.35% None 0.18% 0.53% Guaranteed Option(5) None None None None

(1) Although the Direct Plan Manager Fee is deducted from an Investment Option, not from your Account,

each Account in the Investment Option indirectly bears its pro rata share of the Direct Plan Manager Fee as this fee reduces the Investment Option’s return.

(2) Each Investment Option (with the exception of the Guaranteed Option) pays the Direct Plan Manager a fee at an annual rate of 0.35% (35 basis points) of the average daily net assets held by that Investment Option. If the total market value of the assets in the Direct Plan becomes equal to or greater than $750 million for a period of at least 90 consecutive days, the Direct Plan Manager fee will be reduced by 0.05% (5 basis points) to the annual rate of 0.30% (30 basis points). If the total market value of the assets in the Direct Plan becomes equal to or greater than $1 billion for a period of at least 90 consecutive days, the Direct Plan Manager fee will be reduced by 0.05% (5 basis points) to the annual rate of 0.25% (25 basis points).

(3) The percentages set forth in this column are based on the expense ratios of the mutual funds in which an Investment Option invests. The percentages are calculated using the expense ratio reported in each mutual fund’s most recent prospectus available prior to the date of this Disclosure Booklet and are weighted according to the Investment Option’s allocation among the mutual funds in which it invests. Although these expenses are not deducted from an Investment Option’s assets, each Investment Option (other than the Guaranteed Option, which does not invest in mutual funds) indirectly bears its pro rata share of the expenses of the mutual funds in which it invests, as these expenses reduce such mutual fund’s return.

(4) These figures represent the estimated weighted annual expense ratios of the mutual funds in which the Investment Options invest plus the fee paid to the Direct Plan Manager.

(5) The Guaranteed Option does not pay a Direct Plan Manager Fee. TIAA-CREF Life Insurance Company (“TIAA-CREF Life”), the issuer of the funding agreement in which this Investment Option invests and an affiliate of TFI, makes payments to the Direct Plan Manager. This payment, among many other factors, is considered by the issuer when determining the interest rate(s) credited under the funding agreement.

Investment Cost Example. The example in the following table is intended to help you compare the cost of investing in the different Investment Options over various periods of time. This example assumes that:

● You invest $10,000 in an Investment Option for the time periods shown below. ● Your investment has a 5% compounded return each year. ● You withdraw the assets from the Investment Option at the end of the specified periods for Qualified Higher

Education Expenses. ● Total Annual Asset-Based Fees remain the same as those shown in the Fee Table above.

3

Although your actual costs may be higher or lower, based on the above assumptions, your costs would be:

INVESTMENT OPTIONS APPROXIMATE COST OF $10,000 INVESTMENT 1 Year 3 Years 5 Years 10 Years Conservative Managed Allocation Option

Age Band 0–3 Years $51 $161 $280 $629 Age Band 4–7 Years $52 $164 $286 $642 Age Band 8–11 Years $53 $167 $291 $654 Age Band 12–14 Years $55 $174 $302 $678 Age Band 15–17 Years $58 $183 $319 $715 Age Band 18 Years and over $59 $186 $325 $727

Moderate Managed Allocation Option

Age Band 0–3 Years $49 $154 $269 $605 Age Band 4–7 Years $50 $158 $275 $617 Age Band 8–11 Years $52 $164 $286 $642 Age Band 12–14 Years $53 $167 $291 $654 Age Band 15–17 Years $55 $174 $302 $678 Age Band 18 Years and over $57 $180 $314 $703

Aggressive Managed Allocation Option Age Band 0–3 Years $48 $151 $264 $592 Age Band 4–7 Years $49 $154 $269 $605 Age Band 8–11 Years $50 $158 $275 $617 Age Band 12–14 Years $52 $164 $286 $642 Age Band 15–17 Years $53 $167 $291 $654 Age Band 18 Years and over $55 $174 $302 $678

Diversified Equity Option $88 $275 $479 $1,064 Global Equity Index Option $48 $151 $264 $592 U.S. Equity Index Option $43 $135 $236 $531 Balanced Option $75 $234 $407 $909 Fixed Income Option $54 $170 $297 $666 Guaranteed Option $0 $0 $0 $0

III. PAST PERFORMANCE The following tables show the returns of each Investment Option over the time period(s) indicated. (For purposes of this discussion, each Age Band in the Conservative Managed Allocation Option, Moderate Managed Allocation Option and Aggressive Managed Allocation Option is considered a separate Investment Option.)

The tables below compare the average annual total return of an Investment Option (after deducting fees and expenses) to the returns of a benchmark. The benchmark included in the tables combine the benchmark(s) for the underlying investment(s) in which an Investment Option invests weighted according to the allocations to those underlying investments and adjusted to reflect any changes in the allocations and/or benchmark(s) during the relevant time period. Benchmarks are not available for investment, are not managed, and do not reflect the fees or expenses of investing.

Past performance is not a guarantee of future results. Performance may be substantially affected over time by changes in the allocations and/or changes in the investments in which each Investment Option invests. Investment returns and the principal value will fluctuate, so that your Account, when redeemed, may be worth more or less than the amounts contributed to your Account.

4

For monthly performance information, visit the Direct Plan’s website or call the Direct Plan. Conservative Managed Allocation Option

Average Annual Total Returns For the Period Ended July 31, 2014

Age Bands 1 Year 3 Year 5 Year

10 Year Since

Inception Inception Date 0–3 Years 10.99% 10.27% N/A N/A 10.67% October 1, 2010

Blended Index 11.59% 9.76% N/A N/A 10.49%

4–7 Years 9.88% 8.38% N/A N/A 8.97% October 1, 2010

Blended Index 10.36% 8.71% N/A N/A 9.41%

8–11 Years 8.66% 7.27% N/A N/A 7.50% October 11, 2010

Blended Index 9.13% 7.65% N/A N/A 8.32%

12–14 Years 6.60% 5.36% N/A N/A 5.55% October 11, 2010

Blended Index 6.77% 5.62% N/A N/A 6.14%

15–17 Years 4.03% 3.12% N/A N/A 3.39% October 4, 2010

Blended Index 4.02% 3.30% N/A N/A 3.63%

18 Years and over 1.47% 0.89% N/A N/A 0.91% October 11, 2010

Blended Index 1.52% 1.13% N/A N/A 1.30%

Moderate Managed Allocation Option

Average Annual Total Returns For the Period Ended July 31, 2014

Age Bands 1 Year 3 Year 5 Year

10 Year Since

Inception Inception Date 0–3 Years 12.77% 11.15% 12.88% 7.10% 6.54% January 16, 2004

Blended Index 13.44% 11.32% 13.32% 7.74% 7.21%

4–7 Years 11.62% 9.95% 11.80% 6.78% 6.26% January 16, 2004

Blended Index 12.20% 10.29% 12.29% 7.50% 7.01%

8–11 Years 9.85% 8.34% 10.11% 6.34% 5.89% January 16, 2004

Blended Index 10.36% 8.71% 10.72% 7.08% 6.66%

12–14 Years 8.61% 7.28% 9.12% 6.04% 5.65% January 16, 2004

Blended Index 9.13% 7.65% 9.65% 6.77% 6.42%

15–17 Years 6.56% 5.33% 6.73% 5.00% 4.72% January 16, 2004

Blended Index 6.77% 5.62% 7.28% 5.72% 5.47%

18 Years and over 4.69% 3.80% 4.61% 3.92% 3.72% January 16, 2004

Blended Index 4.60% 3.84% 4.87% 4.31% 4.13%

5

Aggressive Managed Allocation Option Average Annual Total Returns For the Period Ended July 31, 2014

Age Bands 1 Year 3 Year 5 Year

10 Year Since

Inception Inception Date 0–3 Years 15.16% 14.39% N/A N/A 14.88% October 1, 2010

Blended Index 15.92% 13.38% N/A N/A 14.22%

4–7 Years 12.74% 10.90% N/A N/A 11.58% October 1, 2010

Blended Index 13.44% 11.32% N/A N/A 12.10%

8–11 Years 11.65% 9.90% N/A N/A 10.72% October 4, 2010

Blended Index 12.20% 10.29% N/A N/A 11.03%

12–14 Years 9.87% 8.34% N/A N/A 9.01% October 4, 2010

Blended Index 10.36% 8.71% N/A N/A 9.41%

15–17 Years 8.77% 7.26% N/A N/A 7.95% October 4, 2010

Blended Index 9.13% 7.65% N/A N/A 8.32%

18 Years and over 6.53% 5.34% N/A N/A 5.47% October 15, 2010

Blended Index 6.77% 5.62% N/A N/A 6.14%

Risk-Based Investment Options

Average Annual Total Returns for the Period Ended July 31, 2014

Investment Option 1 Year 3 Year 5 Year 10 Year Since

Inception Inception Date Diversified Equity Option 14.29% 12.59% 15.07% N/A 6.22% July 19, 2006

Blended Index 15.86% 13.37% 15.31% N/A 6.76%

U.S. Equity Index Option 15.90% 16.07% N/A N/A 16.57% October 1, 2010

Blended Index 16.37% 16.58% N/A N/A 17.11%

Global Equity Index Option 15.12% 12.93% 14.73% 7.37% 4.68% April 27, 2001

Blended Index 15.92% 13.37% 15.34% 8.17% 5.64%

Balanced Option 10.21% 8.95% 11.13% N/A 6.18% July 19, 2006

Blended Index 11.28% 9.34% 11.29% N/A 6.65%

Fixed Income Option 3.77% 2.81% 4.58% N/A 4.58% July 28, 2006

Blended Index 4.32% 3.38% 5.13% N/A 5.55%

Guaranteed Option 1.16% 1.53% 1.95% 2.61% 2.98% May 1, 2001

IV. TAX INFORMATION — FEDERAL GIFT, ESTATE AND GENERATION-SKIPPING TRANSFER TAX

TREATMENT Beginning on page 22 of the Disclosure Booklet, under the heading “Federal Tax Information,” the “Federal Gift, Estate and Generation-Skipping Transfer Tax Treatment” section is amended by:

● replacing the individual lifetime exemption amount of “$5,250,000” with “5,340,000” in the second sentence of the fourth paragraph of that section;

● replacing the combined lifetime exemption amount of “10,500,000” with “$10,680,000” in the third

sentence of the fourth paragraph of that section; and

● replacing the estate tax exemption amount of “$5,250,000” with “$5,340,000” in the second to last sentence of the fifth paragraph of that section.

THE OKLAHOMA COLLEGE SAVINGS PLAN – DIRECT PLAN

DISCLOSURE BOOKLET AND

PARTICIPATION AGREEMENT

AUGUST 28, 2013

TRUSTEE: THE BOARD OF TRUSTEES OF THE OKLAHOMA COLLEGE SAVINGS PLAN

A14098

OK1308.XXP

i

Please keep this Disclosure Booklet and the Participation Agreement with your other records about the Oklahoma College Savings Plan – Direct Plan (the “Direct Plan”). You should read and understand this Disclosure Booklet before you make contributions to the Direct Plan. You should rely only on the information contained in this Disclosure Booklet and the attached Participation Agreement. No person is authorized to provide information that is different from the information contained in this Disclosure Booklet and the attached Participation Agreement. The information in this Disclosure Booklet is subject to change without notice.

This Disclosure Booklet does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of a security in the Direct Plan by any person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. If you or your intended beneficiary reside in a state other than Oklahoma, or have taxable income in a state other than Oklahoma, it is important for you to note that if that state has established a qualified tuition program under Section 529 of the Internal Revenue Code (a “529 Plan”), such state may offer favorable state tax or other benefits that are available only if you invest in that state’s 529 Plan. Those benefits, if any, should be one of the many appropriately weighted factors you consider before making a decision to invest in the Direct Plan. You should consult with a qualified advisor or review the offering document for that state’s 529 Plan to find out more about any such benefits (including any applicable limitations) and to learn how they may apply to your specific circumstances.

An Account in the Direct Plan should be used only to save for qualified higher education expenses of a designated beneficiary. Accounts in the Direct Plan are not intended for use, and should not be used, by any taxpayer for the purpose of evading federal or state taxes or tax penalties. The tax information contained in this Disclosure Booklet was written to support the promotion and marketing of the Direct Plan and was neither written nor intended to be used, and cannot be used, by any taxpayer for the purpose of avoiding federal or state taxes or tax penalties. Taxpayers should consult with a qualified advisor to seek tax advice based on their own particular circumstances. None of the State of Oklahoma, the Board of Trustees of the Oklahoma College Savings Plan, the Program (including the Direct Plan), the Federal Deposit Insurance Corporation, nor any other government agency or entity, nor any of the service providers to the Direct Plan insures any Account or guarantees any rate of return or any interest on any contribution to the Direct Plan.

TABLE OF CONTENTS

ii

Introduction to the Direct Plan....................................................................................................................... 1

Overview of the Direct Plan .......................................................................................................................... 2

Frequently Used Terms ................................................................................................................................ 3 Opening an Account ..................................................................................................................................... 4

Making Changes to Your Account ................................................................................................................ 5

Contributions ................................................................................................................................................. 5

Unit Value...................................................................................................................................................... 6

Direct Plan Fees ........................................................................................................................................... 7

Investment Options ....................................................................................................................................... 9 Risks of Investing in the Direct Plan ........................................................................................................... 16

Past Performance ....................................................................................................................................... 17

Withdrawals................................................................................................................................................. 19

Administration of the Direct Plan................................................................................................................. 21

The Direct Plan Manager ............................................................................................................................ 21

Confirmations, Account Statements and Tax Reports ................................................................................ 21 Federal Tax Information .............................................................................................................................. 21

Oklahoma Tax Information .......................................................................................................................... 23

Other Information About Your Account ....................................................................................................... 24

Participation Agreement .............................................................................................................................. I-1

Privacy Policy ............................................................................................................................................. II-1

1

Introduction to the Direct Plan

The Oklahoma College Savings Plan (the “Program”), created by the State of Oklahoma (“Oklahoma”), provides a tax-advantaged way to encourage individuals to save for postsecondary education. The Direct Plan was implemented by and is administered as part of the Program by the Board of Trustees of the Program (the “Board”). The Program is intended to meet the requirements of a qualified tuition program under Internal Revenue Code (“IRC”) Section 529 (“Section 529”). The Program consists of two college savings plan components – the Direct Plan, which is offered directly to Account Owners, and an advisor plan (the “Advisor Plan”), which can be purchased only through certain brokers or financial advisors. The Direct Plan and the Advisor Plan consist of different investment options and are subject to different fees and expenses. For more information about the Advisor Plan, please contact your broker or financial advisor. The Program is authorized by Sections 3970.1 through 3970.12 of Title 70 of the Oklahoma Statutes, entitled the Oklahoma College Savings Plan Act, as amended (the “Statute”).

To contact the Direct Plan: Visit the Direct Plan’s website at www.ok4saving.org; Call the Direct Plan toll-free at 1-877-ok4-saving (1-877-654-7284); or Write to the Direct Plan at P.O. Box 8193, Boston, MA 02266-8193.

2

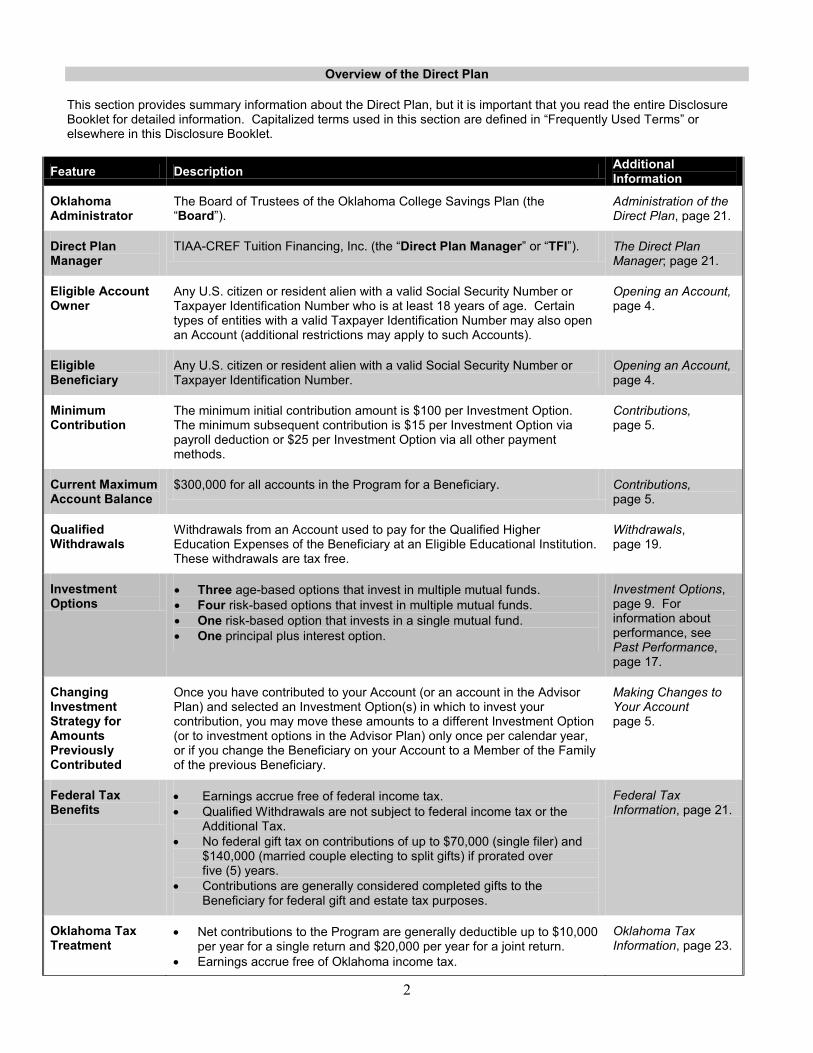

Overview of the Direct Plan

This section provides summary information about the Direct Plan, but it is important that you read the entire Disclosure Booklet for detailed information. Capitalized terms used in this section are defined in “Frequently Used Terms” or elsewhere in this Disclosure Booklet.

Feature Description Additional Information

Oklahoma Administrator

The Board of Trustees of the Oklahoma College Savings Plan (the “Board”).

Administration of the Direct Plan, page 21.

Direct Plan Manager

TIAA-CREF Tuition Financing, Inc. (the “Direct Plan Manager” or “TFI”). The Direct Plan Manager; page 21.

Eligible Account Owner

Any U.S. citizen or resident alien with a valid Social Security Number or Taxpayer Identification Number who is at least 18 years of age. Certain types of entities with a valid Taxpayer Identification Number may also open an Account (additional restrictions may apply to such Accounts).

Opening an Account, page 4.

Eligible Beneficiary

Any U.S. citizen or resident alien with a valid Social Security Number or Taxpayer Identification Number.

Opening an Account, page 4.

Minimum Contribution

The minimum initial contribution amount is $100 per Investment Option. The minimum subsequent contribution is $15 per Investment Option via payroll deduction or $25 per Investment Option via all other payment methods.

Contributions, page 5.

Current Maximum Account Balance

$300,000 for all accounts in the Program for a Beneficiary. Contributions, page 5.

Qualified Withdrawals

Withdrawals from an Account used to pay for the Qualified Higher Education Expenses of the Beneficiary at an Eligible Educational Institution. These withdrawals are tax free.

Withdrawals, page 19.

Investment Options

• Three age-based options that invest in multiple mutual funds. • Four risk-based options that invest in multiple mutual funds. • One risk-based option that invests in a single mutual fund. • One principal plus interest option.

Investment Options, page 9. For information about performance, see Past Performance, page 17.

Changing Investment Strategy for Amounts Previously Contributed

Once you have contributed to your Account (or an account in the Advisor Plan) and selected an Investment Option(s) in which to invest your contribution, you may move these amounts to a different Investment Option (or to investment options in the Advisor Plan) only once per calendar year, or if you change the Beneficiary on your Account to a Member of the Family of the previous Beneficiary.

Making Changes to Your Account page 5.

Federal Tax Benefits

• Earnings accrue free of federal income tax. • Qualified Withdrawals are not subject to federal income tax or the

Additional Tax. • No federal gift tax on contributions of up to $70,000 (single filer) and

$140,000 (married couple electing to split gifts) if prorated over five (5) years.

• Contributions are generally considered completed gifts to the Beneficiary for federal gift and estate tax purposes.

Federal Tax Information, page 21.

Oklahoma Tax Treatment

• Net contributions to the Program are generally deductible up to $10,000 per year for a single return and $20,000 per year for a joint return.

• Earnings accrue free of Oklahoma income tax.

Oklahoma Tax Information, page 23.

3

Feature Description Additional Information

• Qualified Withdrawals are not subject to Oklahoma income tax. • Withdrawals other than Qualified Withdrawals may cause deductions

for contributions to be limited or recaptured. • Oklahoma tax benefits related to the Direct Plan are only available

to Oklahoma taxpayers.

Fees For the services provided to it, the Direct Plan pays a plan management fee at an annual rate of 0.40% of the average daily net assets of the Direct Plan (excluding any assets in the Guaranteed Option).

Direct Plan Fees, page 7.

Risks of Investing in the Plan

• Assets in an Account are not guaranteed or insured. • The value of your Account may decrease. You could lose money,

including amounts you contributed. • Federal or Oklahoma tax law changes could negatively affect the

Direct Plan. • Fees could increase. • The Board may terminate, add or merge Investment Options, change

the investments in which an Investment Option invests, or change allocations to those investments.

• Contributions to an Account may adversely affect the Beneficiary’s eligibility for financial aid or other benefits.

Risks of Investing in the Direct Plan, page 16.

Frequently Used Terms

For your convenience, certain frequently used terms are defined below.

Account An account in the Direct Plan.

Account Owner/You

The individual or entity that opens an Account in the Direct Plan.

Additional Tax A 10% additional federal tax imposed on the earnings portion of a Nonqualified Withdrawal.

Beneficiary The beneficiary for an Account as designated by you, the Account Owner.

Eligible Educational Institutions

Any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education. This includes virtually all accredited public, nonprofit, and proprietary (privately owned profit-making) postsecondary institutions. The educational institution should be able to tell you if it is an eligible educational institution. Certain educational institutions located outside the United States also participate in the U.S. Department of Education’s Federal Student Aid (FSA) programs.

Investment Options

The Direct Plan investment options in which you may invest your contributions.

Member of the Family

A person related to the Beneficiary as follows: (1) a child or a descendant of a child; (2) a brother, sister, stepbrother or stepsister; (3) the father or mother, or an ancestor of either; (4) a stepfather or stepmother; (5) a son or daughter of a brother or sister; (6) a brother or sister of the father or mother; (7) a son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law or sister-in-law; (8) the spouse of any of the foregoing individuals or the spouse of the Beneficiary; or (9) a first cousin of the Beneficiary. For this purpose, a child includes a legally adopted child and a stepson or stepdaughter, and a brother or sister includes a half-brother or half-sister.

Nonqualified Withdrawal

Any withdrawal from an Account that does not meet the requirements of being: (1) a Qualified Withdrawal; (2) a Taxable Withdrawal; or (3) an outgoing rollover to another state’s 529 Plan or to an Account within the Direct Plan or an account in the Advisor Plan for a different Beneficiary that is a Member of the Family of the previous Beneficiary.

Qualified Higher Education Expenses