Embed Size (px)

Citation preview

The social housing regulator

Successful places with homes and jobs

A NATIONAL AGENCYWORKING LOCALLY

The regulator’s view of the sector

Matthew BailesDirector of Regulation, HCA

The social housing regulator

Overview The Regulator’s overall view of sector finances

Sector-wide risks

What we mean by diversification – what’s different?

When things go wrong

Changes to the Regulatory Framework and how we regulate

What do we want to see?

The social housing regulator

Sector finances are healthy…

Healthy balance sheet

Assets worth £118bn, largely valued at cost

Growing surpluses - £1.8bn in 2012

Access to funding at competitive rates, increasingly through the capital markets

Available security, albeit not evenly distributed

Position will be pretty stable in next global accounts

The social housing regulator

..but thanks in part to unusually benign conditions

Very low variable interest rates (1% on variable rate debt is worth c.£200m/annum)

Healthy profits from sales in a more buoyant market (profits from sales account for about 1/3 of the sector’s surplus)

RPI (rents) rising faster than wages

The social housing regulator

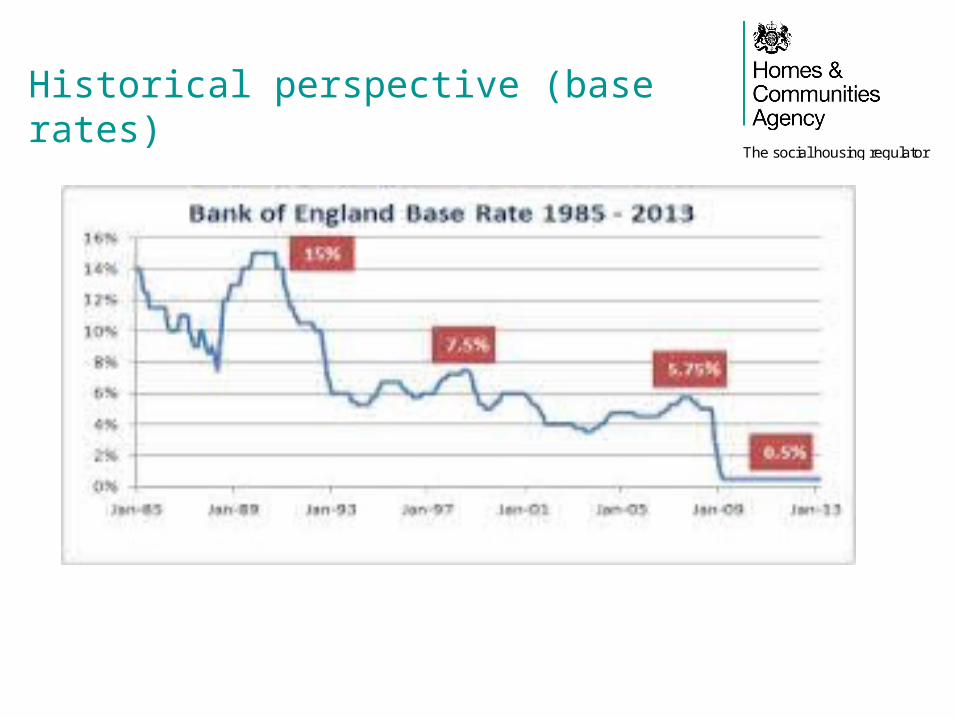

Historical perspective (base rates)

The social housing regulator

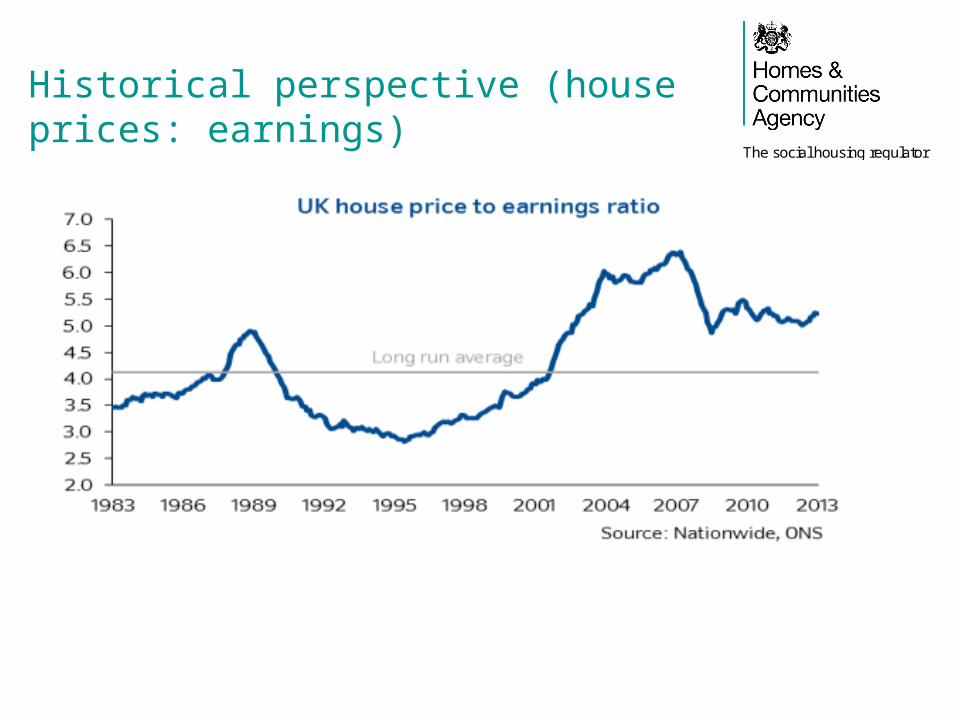

Historical perspective (house prices: earnings)

The social housing regulator

Put another way…

The sector is in good shape

But we can’t bank on current good weather forever

The social housing regulator

Sector risks

Second sector risk profile published September 2013

Welfare reform

– Under-occupation

– Benefit cap

– Direct payment

– Net effect of welfare changes – how will tenants behave?

– What’s round the corner?

Historic debt and gearing covenants, in a world in which lenders are losing money on pre-credit crunch deals

Sales and development risks

IFRS, pensions and, for some, loss of rent convergence

The social housing regulator

Diversification

Exists already, but now driven by end of “vanilla” option

Diversification of activities and funding

Risk profile of activities varies considerably, e.g:– High turnover, low margin, limited liabilities

– long-term liabilities that rely on non-social housing revenues

– Exposure on sales receipts

Our interest lies in the potential recourse to social housing assets

The social housing regulator

When things go wrong

Weak internal controls – including on basics

Lack of understanding of risk in aggregate

Treasury management, including putting in place security

Understanding of charity law, including pricing of risk

Non-recourse activity that isn’t really non-recourse

Poor judgement / inadequate advice

Complacency and the case for Board renewal

The social housing regulator

Likely Regulatory Framework changes

Stress-testing of businesses – e.g. higher interest rate / sales risk scenario

Forensic grip of assets and liabilities, including recourse to social housing assets

Appropriate pricing of risk, in line with charitable vires/investment powers where appropriate

Skills and capability that measure up to market exposures

Specific provisions for new for-profit providers

The social housing regulator

What do we want to see? Underlying premise – Boards as custodians of assets for long-

term provision of community benefits, accountable for meeting our standards

Prudent risk taking to meet your objectives, including on new supply

Strategic choices grounded in commercial and financial realities

Iron grip on risks, and strategy for dealing with a more difficult market

Value for money to enable you to continue to meet your objectives. Absolutely not an add on / nice to have

Don’t lose sight of the basics – e.g. gas servicing

The social housing regulator

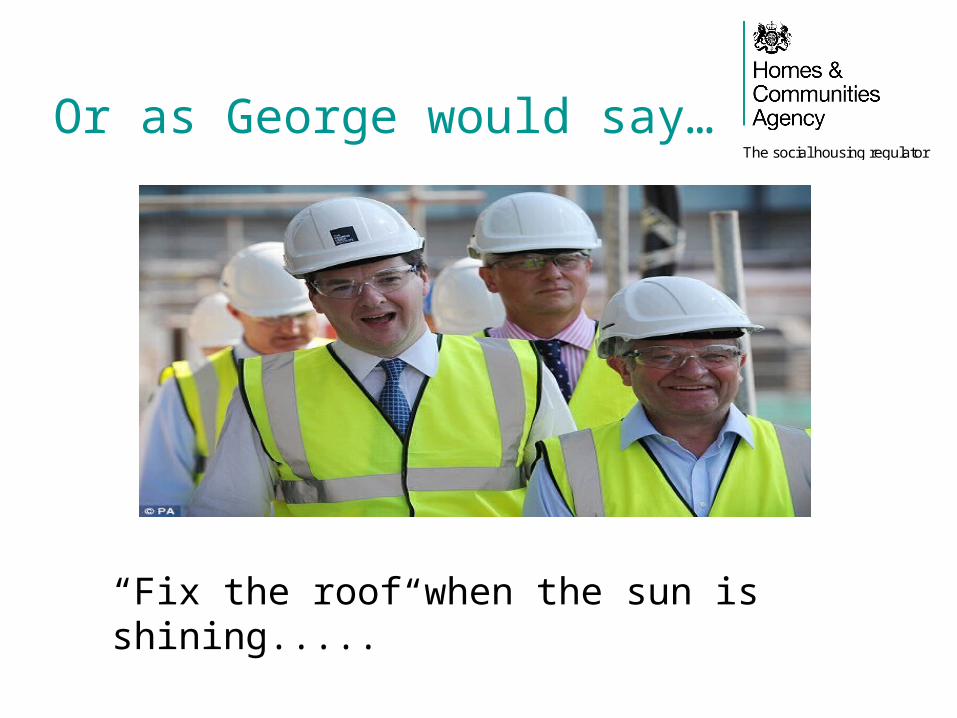

Or as George would say…

“Fix the roof when the sun is shining.....”