Embed Size (px)

Citation preview

Evnine-Vaughan Associates, Inc.

A multi-timescale statistical feedback model of volatility:

Stylized facts and

implications for option pricing

Lisa BorlandOctober, 2005

Acknowledgements:

Jeremy Evnine Roberto Osorio

Jean-Philippe BouchaudBenoit Pochart

Layout• Stylized facts of markets

- Why we need a new model

• The non-Gaussian model -Properties -Applications: Options and Credit

• The multi-time scale model-Capturing the stylized facts

• Work in progress and conclusions

Properties of Financial Time-Series

• Power Law distributions, persistent over very many timescales: minutes to weeks

Cumulative distribution power law tail -3Gopikrishnan,Plerou,Nunes Amaral,Meyer,Stanley (1999)

Properties of Financial Time-Series

• Power Law distributions, persistent• Slow decay to Gaussian, as • Volatility clustering and correlation• Volatility relaxation (Omori law)• Close-to log-normal distribution of volatility• Returns normally diffusive over time-scales• Leverage effect (Skew: Negative returns higher volatility)• Time-Reversal asymmetry

25.0−τ

o Empirical--- Gaussian

q=1.43 Tsallis Distribution

Consequences

• Risk control: under-estimate rare events

• Derivative markets: (options, credit)wrong model of underlying leads to wrong pricing, wrong hedging

Challenge

• A model that can reproduce the stylized facts• A model that can reproduce option prices, credit etc.• A model that captures the correct dynamical features

Desirable• Intuition• Parsimony• Analytic tractability

• Stochastic volatility (Heston 1993)

• Levy noise• GARCH • Multifractal models (Bacry,Delour,Muzy, 2001)

Popular models

Problems• Typically converge too quickly to Gaussian• Less parsimonious• Do not reproduce time reversal assymmetry

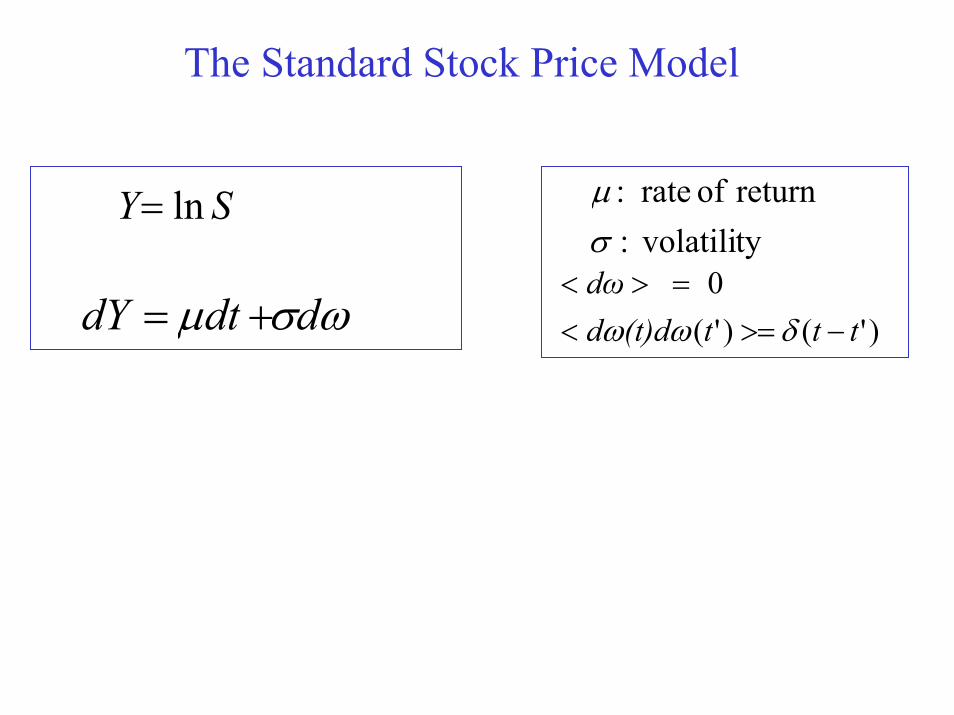

The Standard Stock Price Model

SY ln=

)'()'(0

ttt(t)dd dω

−>=<=><

δωω

ty volatili:returnofrate

σµ :

ωσµ ddtdY + =

The Standard Stock Price Model

)'()'(0

ttt(t) ω

−>=<=><

δωω

ty volatili:returnofrate

σµ :

Gaussian Distribution

Fokker-Planck Equation2

2

21

ωdPd

dtdP

=

)2

exp(21)(

2

ttP ω

πω −=

ωσµ ddtdY + =

SY ln=

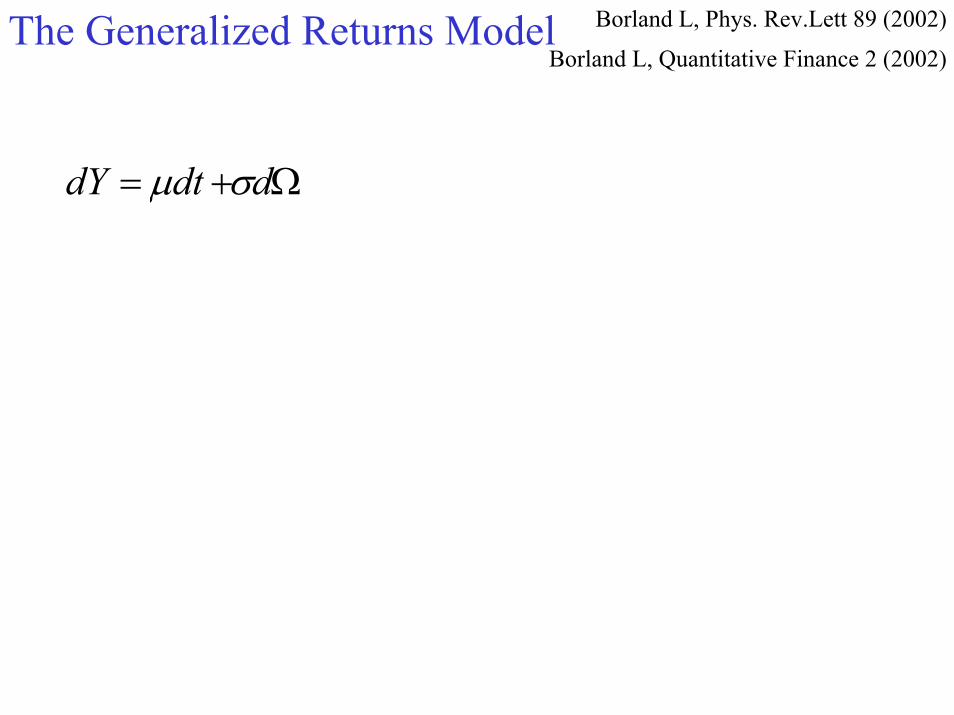

Ω+ = ddtdY σµ

The Generalized Returns Model Borland L, Phys. Rev.Lett 89 (2002)

Borland L, Quantitative Finance 2 (2002)

ωdPdq

21

)(−

Ω=Ω

Ω+ = ddtdY σµ

The Generalized Returns Model The Generalized Returns Model Borland L, Phys. Rev.Lett 89 (2002)

Borland L, Quantitative Finance 2 (2002)

The Generalized Returns Model The Generalized Returns Model Borland L, Phys. Rev.Lett 89 (2002)

Borland L, Quantitative Finance 2 (2002)

Tsallis Distribution

Nonlinear Fokker-Planck2

22

21

Ω=

−

dPd

dtdP q

qtqtZ

P −Ω−−= 11

2 ))()1(1()(

1 β

ωdPdq

21

)(−

Ω=Ω

Ω+ = ddtdY σµ

In other words:

State dependent deterministic model

ttttt dbqad ω21

2 ])1([ Ω−+=Ω

Work with

)(SΩ=Ω

as a computational tool allowing us to find the solution

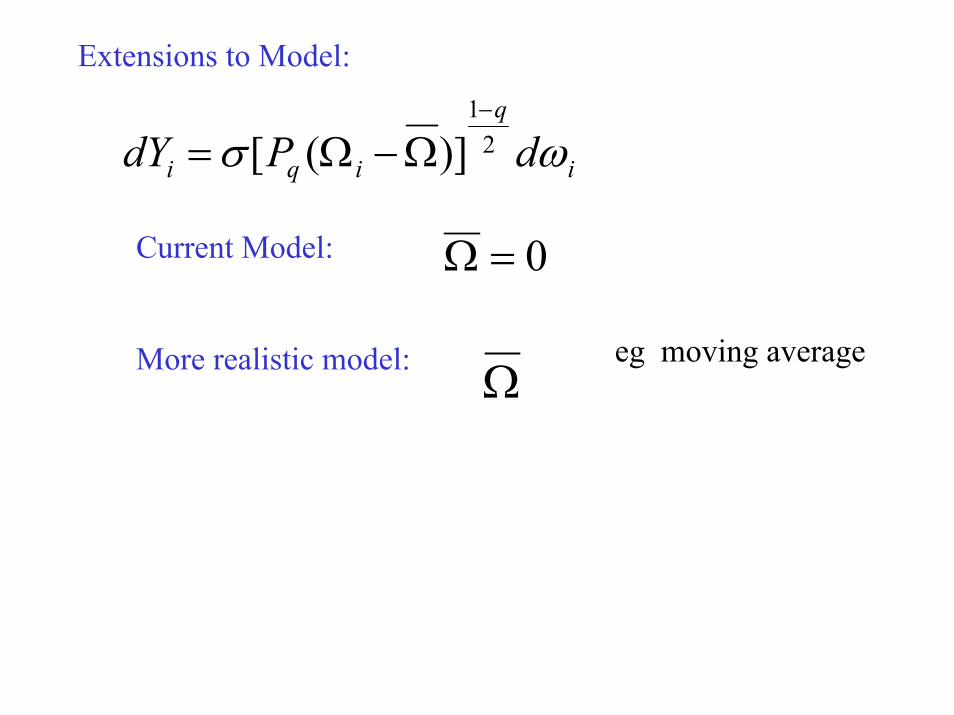

Extensions to Model:

i

q

iqi dPdY ωσ 21

)]([−

Ω−Ω=

0=ΩCurrent Model:

eg moving averageMore realistic model: Ω

Extensions to Model:

i

q

iqi dPdY ωσ 21

)]([−

Ω−Ω=

0=ΩCurrent Model:

eg moving averageMore realistic model: Ω

Or:

i

i

j

q

jiqi dPdY ωσ ∑−

=

−

ΩΩ=1

0

21

)]|([

(see later in this talk)

Not a perfect model of returns:

Well-defined starting price and time

Nevertheless:

Reproduces fat-tails and volatility clustering

Closed form option-pricing formulae

Success for options and credit (CDS) pricing

Example European CallQ

rT KTSec ]0,)(max[ −= −

Stock Price

⎭⎬⎫

⎩⎨⎧

Ω2

− + Ω= ∫ −2 T q

tT dtPrTSTS0

1)(exp)0()( σ

Example European CallQ

rT KTSec ]0,)(max[ −= −

Stock Price

⎭⎬⎫

⎩⎨⎧

Ω2

− + Ω= ∫ −2 T q

tT dtPrTSTS0

1)(exp)0()( σ

Integrate using generalized Feynman-Kac

2)(T

T Ω∝ γ

Example European CallQ

rT KTSec ]0,)(max[ −= −

Stock Price

⎭⎬⎫

⎩⎨⎧

Ω−−2

− + Ω=2

2)()1()(exp)0()(TT TgqTrTSTS γσ

21 dd T ≤Ω≤)( KTS >Payoff if

Example European CallQ

rT KTSec ]0,)(max[ −= −

∫ Τ− ΩΩ− =

2

1

)())((d

dTq

rT dPKTSec

σσ ,,)0( qrT

q KNeMS −−=

q = 1: P is Gaussian q >1 : P is fat tailed Tsallis dist.

q=1.5

K=50, T=0.4, sigma=0.3, r=.06

q=1.5q=1

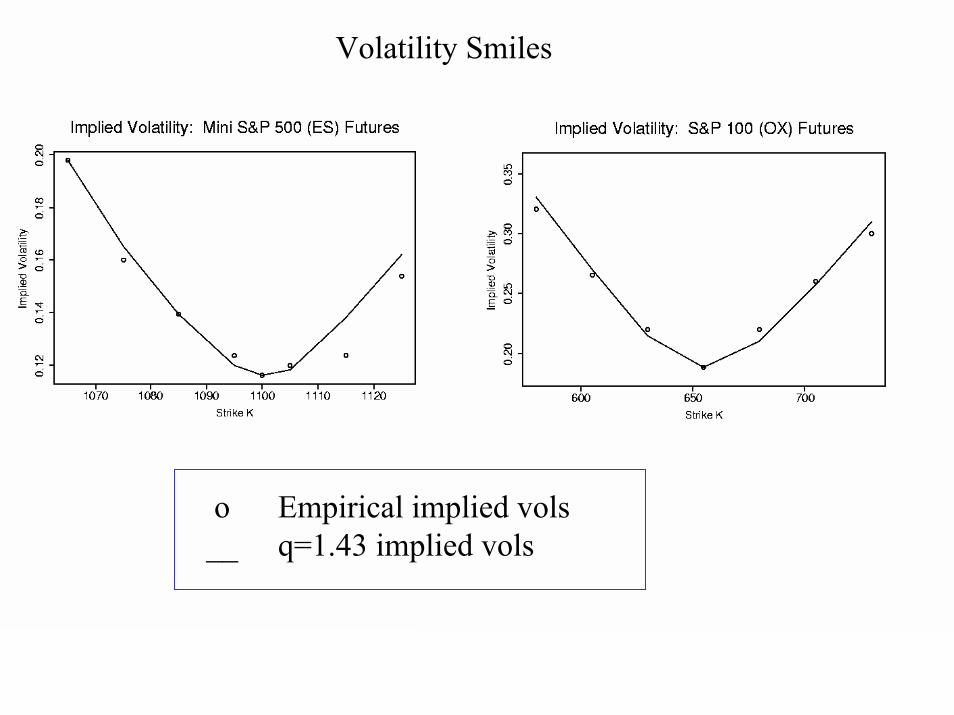

Volatility Smiles

o Empirical implied vols__ q=1.43 implied vols

72 76 80 84Strike

9

10

11

12

13

14

Vol

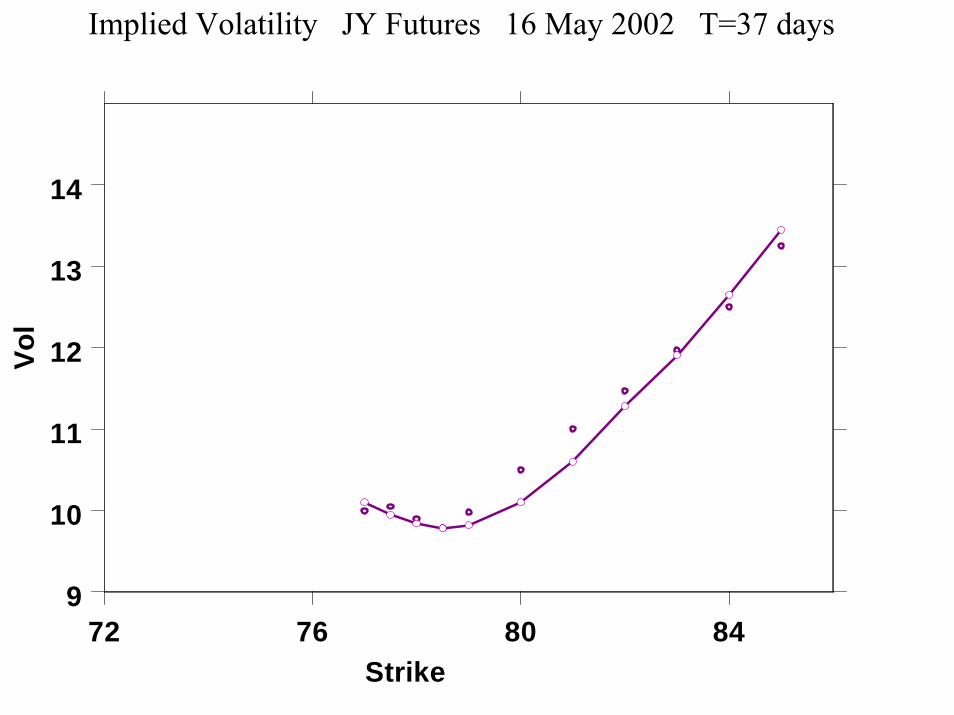

Implied Volatility JY Futures 16 May 2002 T=17 days

72 76 80 84Strike

9

10

11

12

13

14

Vol

Implied Volatility JY Futures 16 May 2002 T=37 days

72 76 80 84Strike

9

10

11

12

13

14

Vol

Implied Volatility JY Futures 16 May 2002 T=62 days

72 76 80 84Strike

9

10

11

12

13

14

Vol

Implied Volatility JY Futures 16 May 2002 T=82 days

72 76 80 84Strike

9

10

11

12

13

14

Vol

Implied Volatility JY Futures 16 May 2002 T=147 days

Example Currency Futures: (500 options)

1. 0.16

1.4 0.008

q Mean square relative pricing error

Benefits of a more parsimonious model:

1) Better pricing - arbitrage opportunities

2) Better hedging

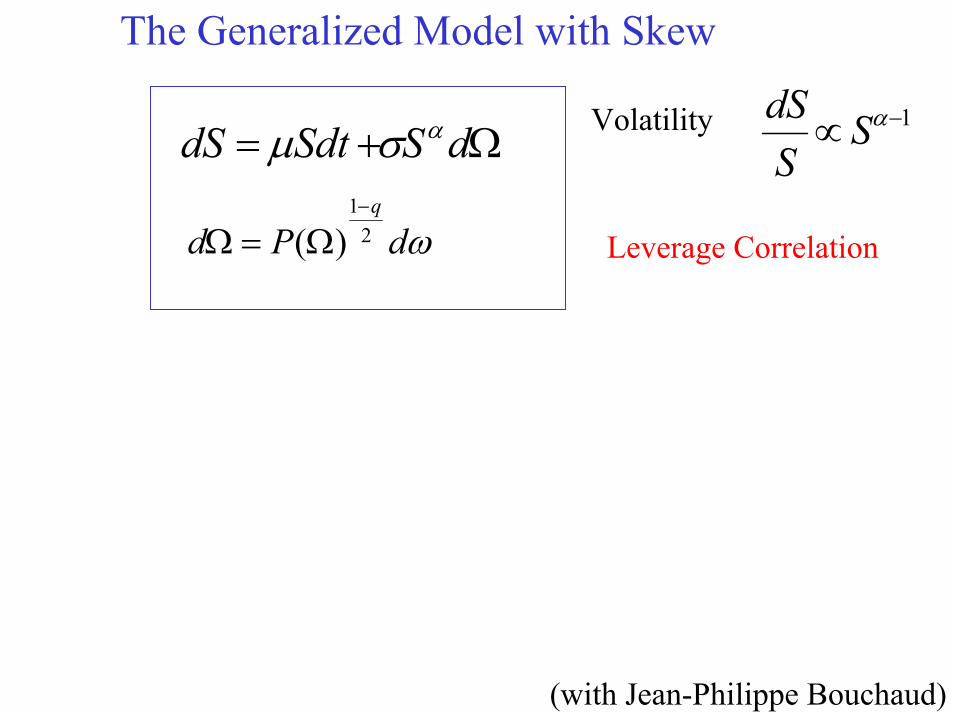

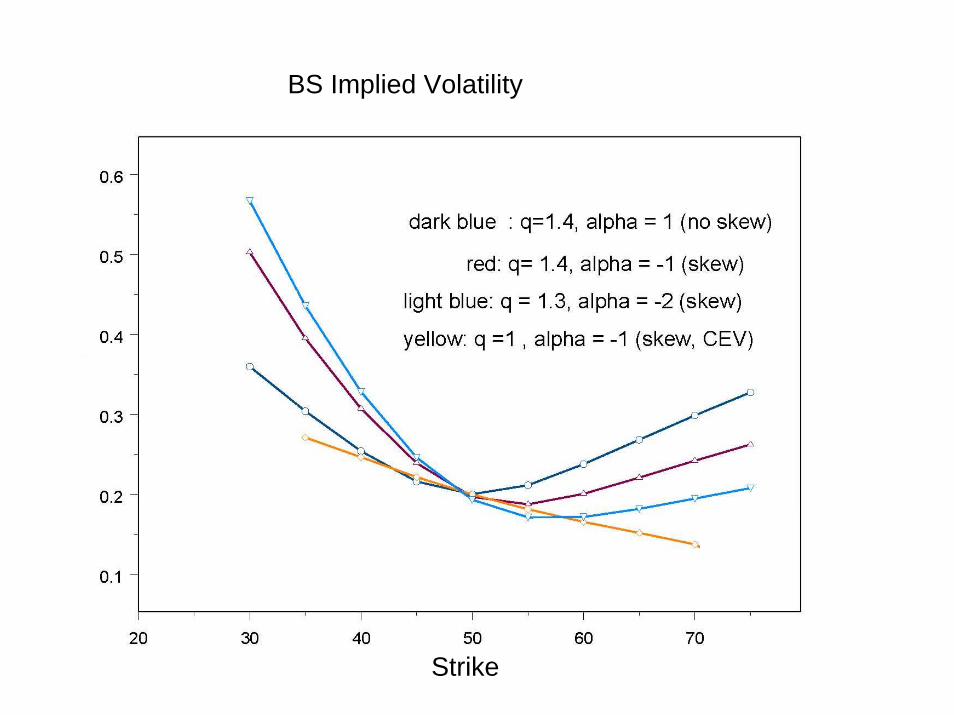

The Generalized Model with Skew

1−∝ αSSdS

Ω+ = dSSdtdS ασµ

ωdPdq

21

)(−

Ω=Ω

Volatility

Leverage Correlation

(with Jean-Philippe Bouchaud)

0 1 2 3 4

Time [Years]

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Ret

urn

[Hou

rly]

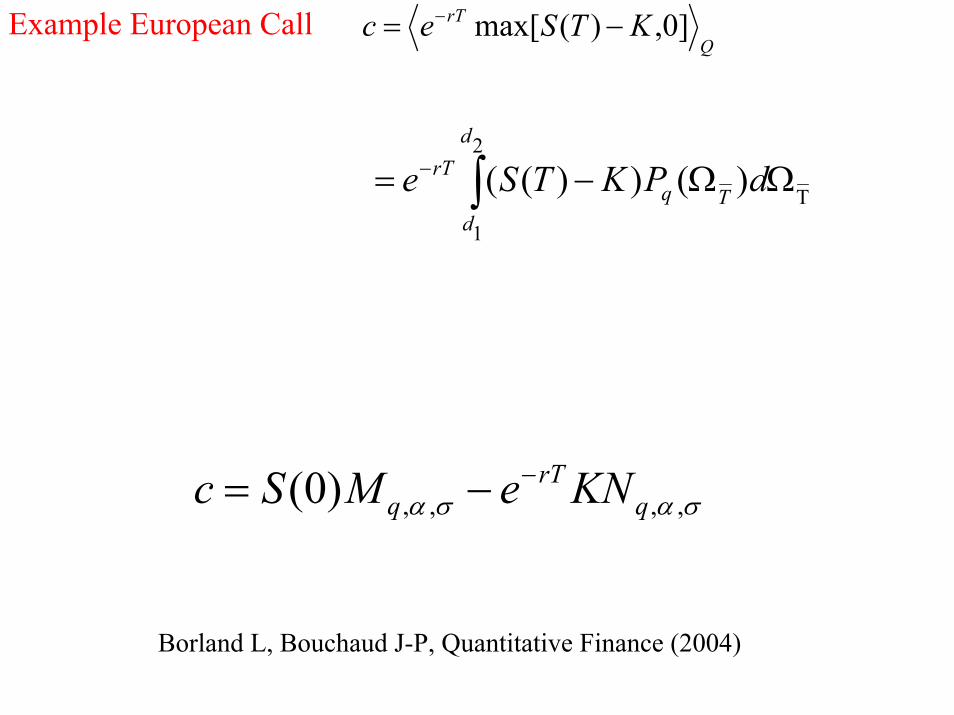

Example European CallQ

rT KTSec ]0,)(max[ −= −

∫ Τ− ΩΩ− =

2

1

)())((d

dTq

rT dPKTSe

σασα ,,,,)0( qrT

q KNeMSc −−=

Borland L, Bouchaud J-P, Quantitative Finance (2004)

5.0−=αq=1.5

Strike

BS Implied Volatility

Strike K Strike K

T=.03

T=0.1

T=0.2

T=0.3

T=0.55

SP500 OX q=1.5, alpha = -1.

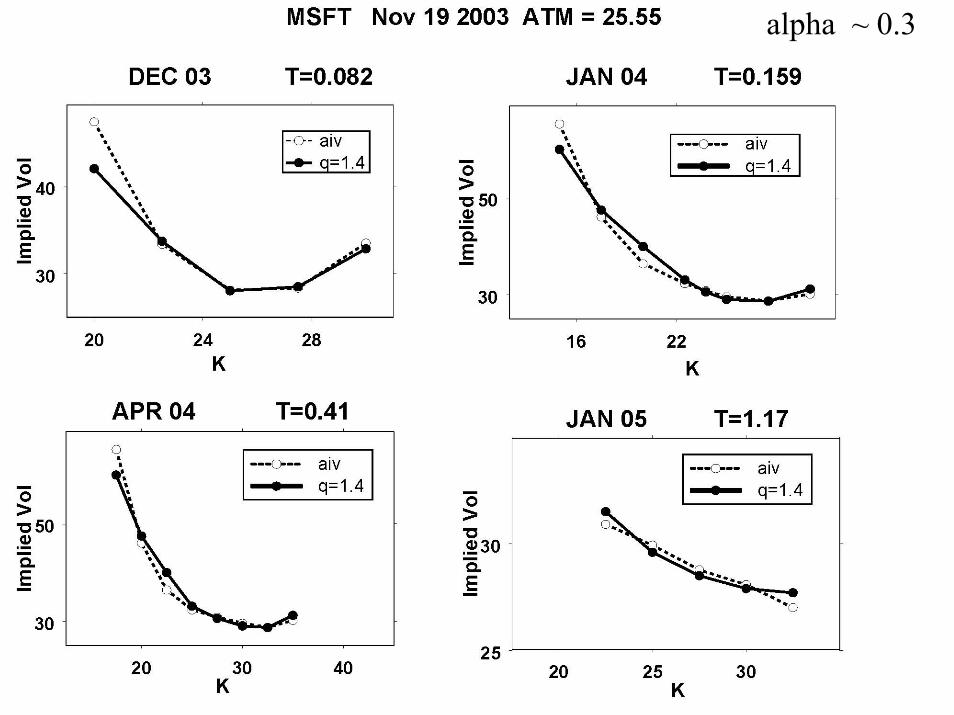

alpha ~ 0.3

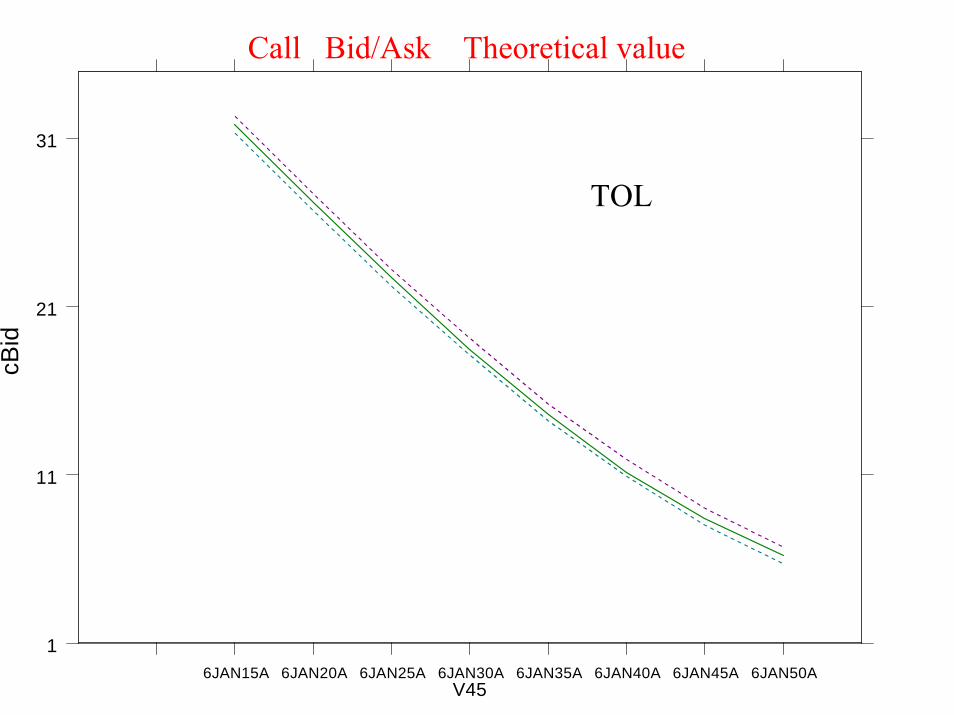

4OCT30A 4OCT35A 4OCT40A 4OCT45A 4OCT50ASeries

0

5

10

15

cBid

Call Bid/Ask Theoretical value

TOL

4NOV35A 4NOV40A 4NOV45A 4NOV50AV12

0

2

4

6

8

10

12cB

id

Call Bid/Ask Theoretical value

TOL

0

5

10

15

20

cBid

4DEC25A 4DEC30A 4DEC35A 4DEC40A 4DEC45A 4DEC50A 4DEC50A 4DEC50AV56

Call Bid/Ask Theoretical value

TOL

5JAN10A 5JAN15A 5JAN20A 5JAN25A 5JAN30A 5JAN35A 5JAN40A 5JAN45A 5JAN50AV23

0

10

20

30

cBid

Call Bid/Ask Theoretical value

TOL

5MAR30A 5MAR35A 5MAR40A 5MAR45A 5MAR50AV34

0

5

10

15

cBid

Call Bid/Ask Theoretical value

TOL

6JAN15A 6JAN20A 6JAN25A 6JAN30A 6JAN35A 6JAN40A 6JAN45A 6JAN50AV45

1

11

21

31

cBid

Call Bid/Ask Theoretical value

TOL

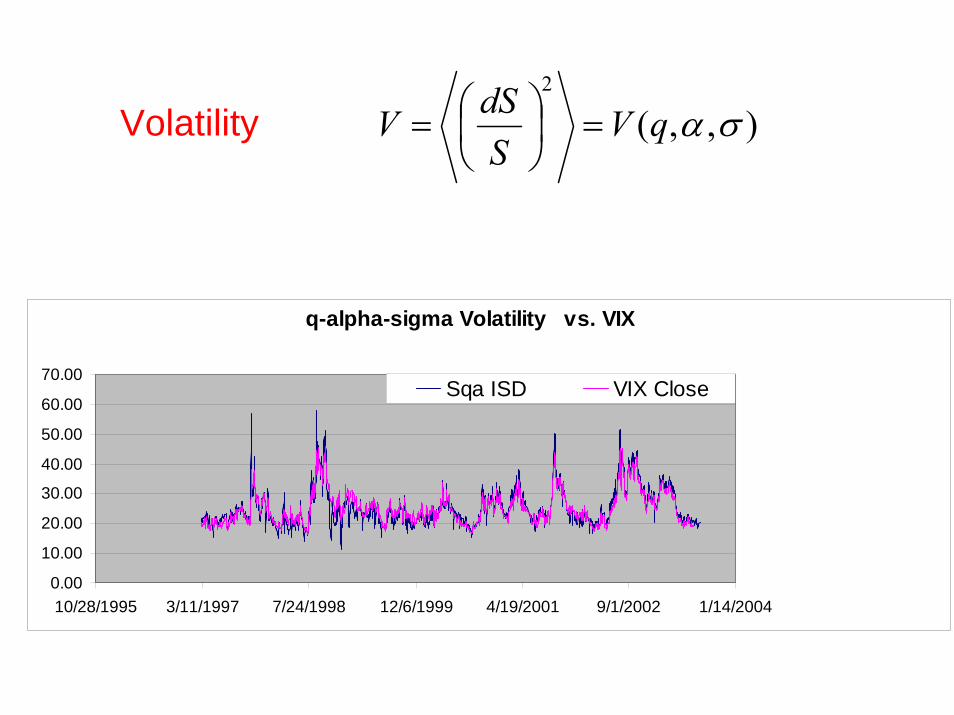

),,(2

σαqVS

dSV =⎟⎠⎞

⎜⎝⎛=Volatility

),,(2

σαqVS

dSV =⎟⎠⎞

⎜⎝⎛=Volatility

q-alpha-sigma Volatility vs. VIX

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

10/28/1995 3/11/1997 7/24/1998 12/6/1999 4/19/2001 9/1/2002 1/14/2004

Sqa ISD VIX Close

Options look good ….

What about pricing credit?

Borland L, Evnine J, Pochart B, cond-mat/0505359 (2005)

Chirayathumadom R, et al, Investment Practice Report Project, Stanford University (2004)

Merton Model (1974)

• Equity is a call option on underlying assets of firm

Assets = Debt + Equity

:DAT < Bond holders receive TA

Stock holders receive 0

:DAT > Stock holders receive DAT −

Bond holders receive D

• Key assumptions

- Underlying assets follow stochastic log normal process

- Debt in terms of single zero coupon bond

- Black-scholes valuation for European call option

• Asset Process:

dA = µA dt + σAdz

• Key assumptions

- Underlying assets follow stochastic log normal process

- Debt in terms of single zero coupon bond

- Black-scholes valuation for European call option

• Asset Process:

dA = µA dt + σAdz

• Generalized Process:

dA= µA dt + σA Ωdα

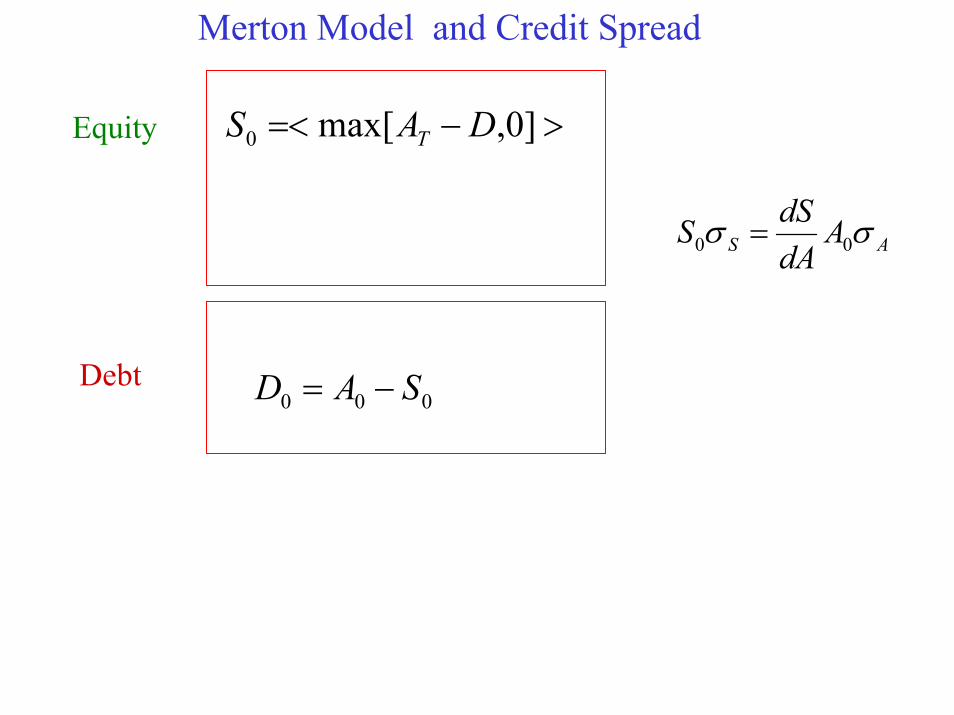

Merton Model and Credit Spread

>−=< ]0,max[ 0 DAS TEquity

000 SAD −=

AS AdAdSS σσ 00 =

Debt

Merton Model and Credit Spread

>−=< ]0,max[ 0 DAS TEquity

000 SAD −=

AS AdAdSS σσ 00 =

Debt0DDe yT =−

⎟⎠⎞

⎜⎝⎛−=− −rTDe

DT

ry 0log1Credit Spread y=risky yield

Merton Model and Credit Spread

>−=< ]0,max[ 0 DAS TEquity

000 SAD −=

AS AdAdSS σσ 00 =αα ,,00 q

rTq DNeMAS −−=

Debt0DDe yT =−

⎟⎠⎞

⎜⎝⎛−=− −rTDe

DT

ry 0log1Credit Spread y=risky yield

AnalysisSectors 1 through 7 are Aerospace, Communication, Construction, Energy, High tech equipment, Financial services and Retail

Q

00.20.40.60.8

11.21.41.6

aero

spac

e, a

uto

man

ufac

turin

g,ai

rline

s

Com

mun

icat

ion,

IT

elec

trica

l,co

nstru

ctio

nm

achi

nery

ener

gy

Equ

ipm

ents

(med

ical

and

elec

troni

c)

Fina

ncia

l ser

vice

s

reta

il, p

erso

nal

prod

ucts

, foo

dpr

oces

sing

Q values across Industry sectors

1

1.1

1.2

1.3

1.4

1.5

1.6

1

Companies

Q

q across industries q

0.4 0.6 0.8 1.0 1.2 1.4 1.6

d

0.12

0.17

0.22

0.27

0.32

0.37q=1, alpha=0q=1.2, alpha=1q=1.4, alpha=1q=1.4, alpha=0.5q=1.4, alpha=0

Standard model

“Reality”

Credit Implied volatility

D/A(0)

Results

- q mainly in range 1.2 – 1.5 and α = 0.3

- Extremely good model prediction

Summary

Non-Gaussian model well describes many features of:

Stock MarketsOption MarketsDebt and Credit Markets

Now :

Extending model of underlying

A multi-time scale non-Gaussian model of stock returns[Borland L., cond-mat/0412526 2004]

i

i

j

qjiqij dyyPw

Wdy ωσ ∑

−

−∞=

−=1

1)]|([

))()1(1(1 21jiij

ij

qq yyq

ZP −−−=− β

Motivation: Traders act on all different time horizons

A multi-time scale non-Gaussian model of stock returns[Borland L., cond-mat/0412526 2004]

i

i

j

qjiqij dyyPw

Wdy ωσ ∑

−

−∞=

−=1

1)]|([

))()1(1(1 21jiij

ij

qq yyq

ZP −−−=− β

Motivation: Traders act on all different time horizons

0jijw δ=Single-time model:

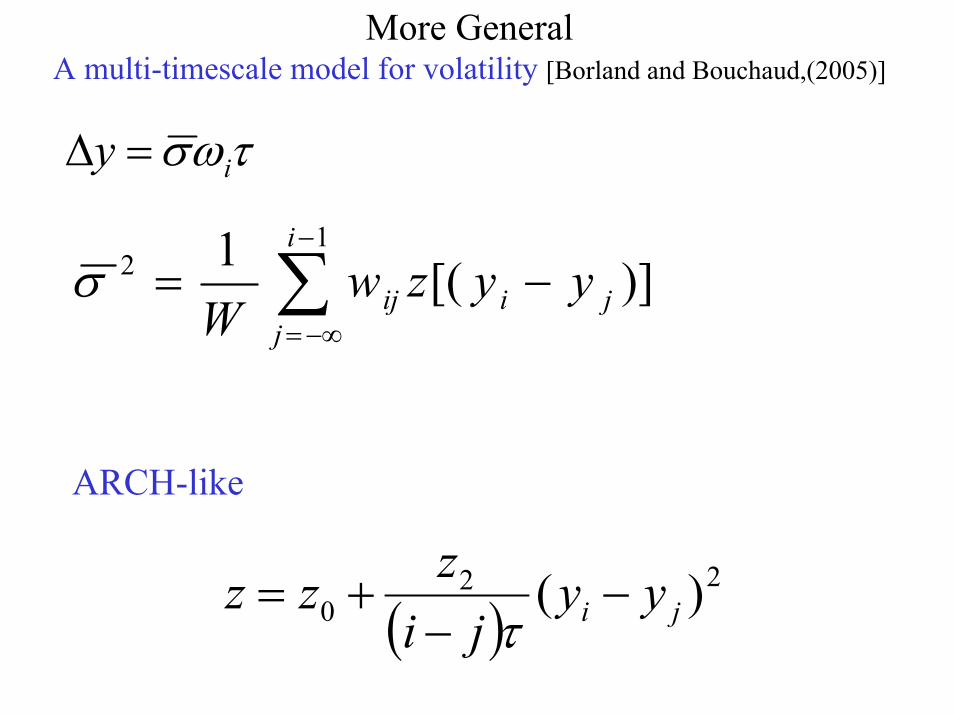

More GeneralA multi-timescale model for volatility [Borland and Bouchaud,(2005)]

τωσ iy =∆

)][(1 12

ji

i

jij yyzw

W−= ∑

−

−∞=

σ

ARCH-like

( )22

0 )( ji yyji

zzz −−

+=τ

A multi-timescale model for volatility [Borland and Bouchaud,(2005)]

τωσ iy =∆

)][(1 12

ji

i

jij yyzw

W−= ∑

−

−∞=

σ

ARCH-like

( )221

0 )()()( jiji yy

jizyy

jizzz −

−+−

−+=

ττ

A multi-timescale model for volatility [Borland and Bouchaud,(2005)]

kurtosis decay

)][(1 12

ji

i

jij yyzw

W−= ∑

−

−∞=

σ

τωσ iy =∆ aij jiw −−= )(

tailsskew

elementary timescale

( )221

0 )()()( jiji yy

jizyy

jizzz −

−+−

−+=

ττ

ARCH-like

1

0

z

z

g

τ

α

2zParameters: controls the tails

controls the memory

the elementary time scale

base volatility

skew

Calibration Universal

1

0

2

min7300/1

15.1

85.0

z

z

z

==

=

=

τ

α

controls the tails

controls the memory

the elementary time scale

base volatility

skew

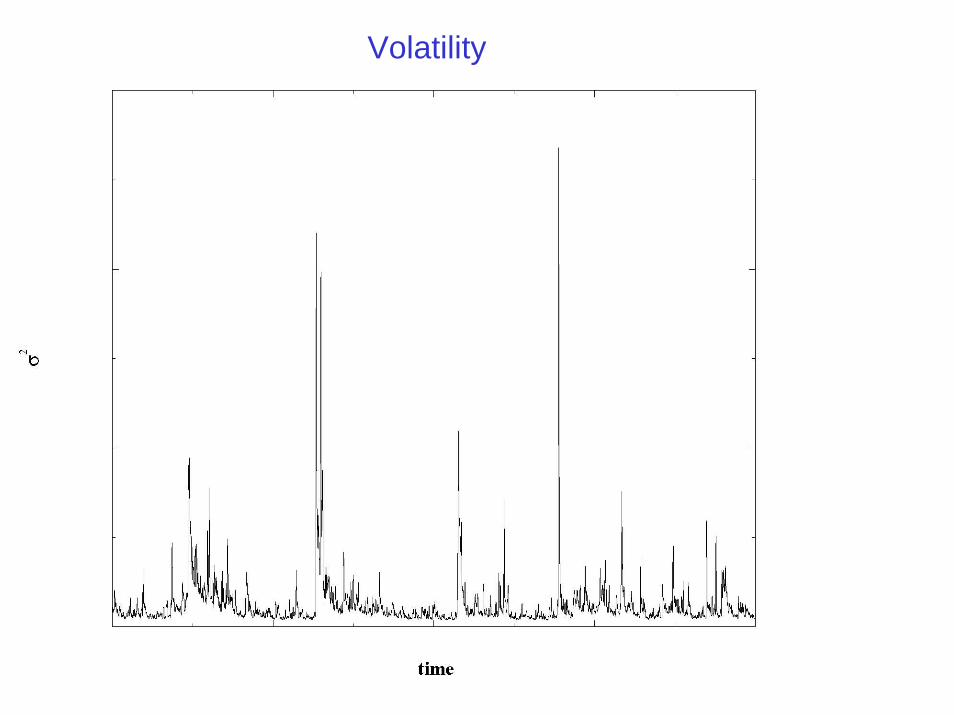

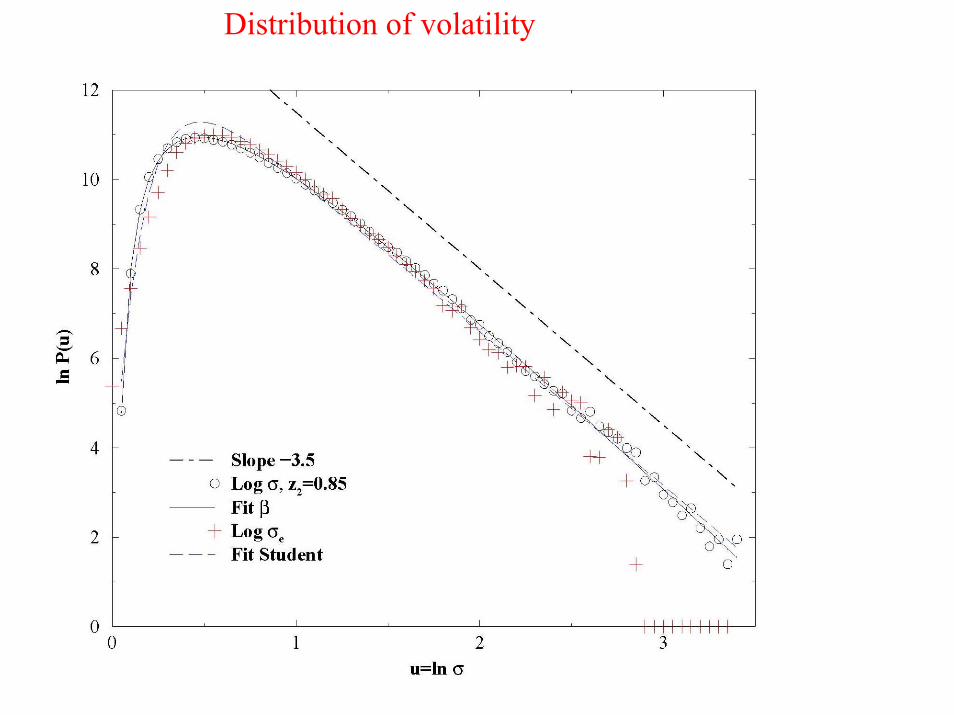

Volatility

Distribution of volatility

Volatility-Volatility correlation variogram

α−2l

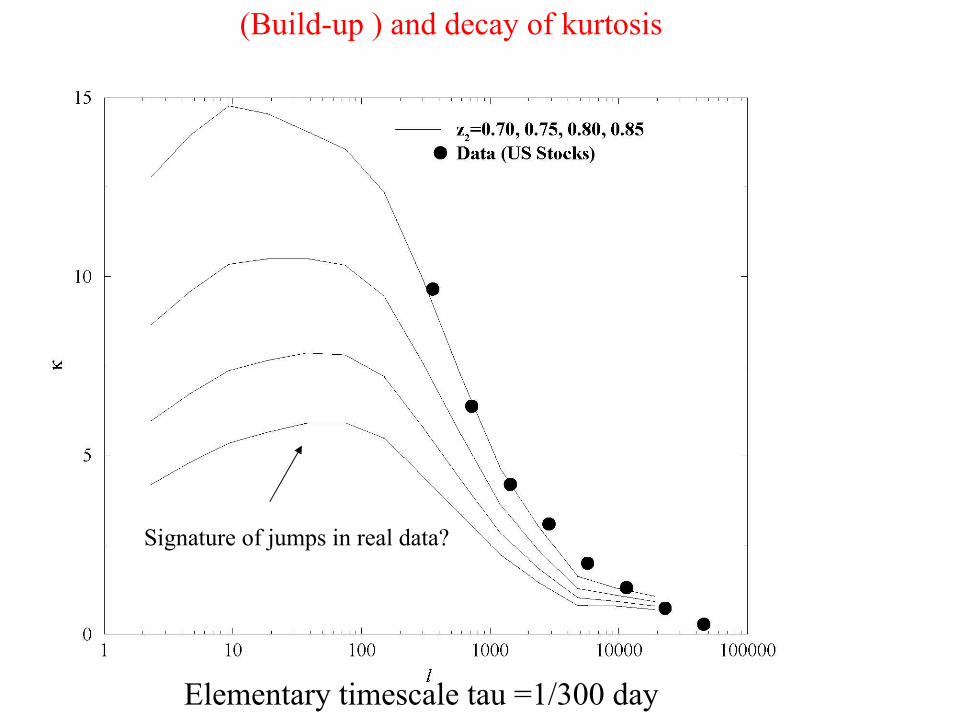

(Build-up ) and decay of kurtosis

Elementary timescale tau =1/300 day

Signature of jumps in real data?

Multifractal scaling

nlAxxlM nn

ilinζ=−= + ||)(

Evolution of 2σ conditioned on an initial volatility se22σVolatility relaxation

Matches results for SP500 [Sornette, Malevergne, Muzy, 2003)]

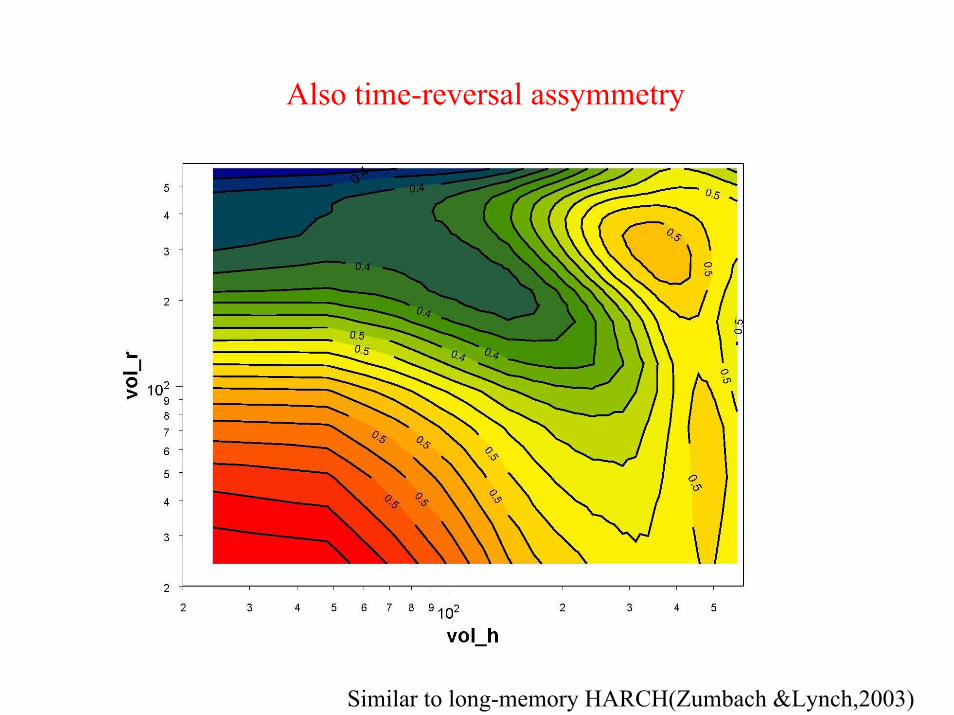

Also time-reversal assymmetry

Similar to long-memory HARCH(Zumbach &Lynch,2003)

∑∞

=+

−−=

11

2)(l

liii l

yyX α

Regression gives 9.02 ≈z

Analytic results Borland,Bouchaud 2005

• Volatility-volatility correlations: decay as

• Model well-defined with power-law tails for

• Volatility normally diffusive

α−2l

Numerical results• Tsallis distribution excellent description on all time-scales • Distribution of volatility• Multifractal scaling• Volatility relaxation• Time-reversal assymmetry• Tested premise of model on real data

tz

zy ∆−

=∆2

02

1)(

1,12 >< αz

Summary

Implications of model to market

• Soft-calibration (due to long relaxation)

• Model operating close to an instability

• Past price changes do influence future investor behavior

• Jumps (news) in addition to feedback effects

Implications for option pricing

• Price depends on past path history :Low vol period different price than high vol period

• Returns: Tsallis-Student distributions on all time-scalesq 1 in a predictable way

• Approximation: Use single-time model with q(T).

ασq

Conclusions

- Simple multi-time scale model

-Captures many statistical properties of real returns

-Closed form solution for single time case: options,credit

-Current and future work: General analytic solution

References:

Borland L, Phys. Rev.Lett 89 (2002)

Borland L, Quantitative Finance 2 (2002)

Borland L, Bouchaud J-P, Quantitative Finance(2004)

Chirayathumadom R, et al, Investment Practice Report Project, Stanford University (2004)

Borland L, cond-mat/04122526 (2004)

Borland L, Evnine J, Pochart B, cond-mat/0505359 (2005)

Borland L, Bouchaud J-P, Muzy J-F, Zumbach G, Wilmott Magazine, (March 2005)

Borland L, Bouchaud J-P,arXiv:physics/0507073 (2005)