-

7/31/2019 Session on Stylized Properties

1/45

1

Quantitative Applications inFinance

Distributional Properties of Returns Stylized Properties of

Financial Time Series

Readings: Chapter 1, Text

-

7/31/2019 Session on Stylized Properties

2/45

2

Dealing with Returns

Most financial studies involve returns, instead ofprices, of

assets.

Two main reasons: First, for average investors,

return of an asset is a complete and scale-freesummary of the

investment opportunity.

Second, return series are easier to handle thanprice series

because the former have more

attractive statistical properties.

-

7/31/2019 Session on Stylized Properties

3/45

3

Various definitions of an assetreturn

Pt= price of an asset at time index t

One-Period Simple Return:

(i) simplegross return, (1+Rt), (growth factor):

(ii) simplenet returnor simple return:

-

7/31/2019 Session on Stylized Properties

4/45

4

Multiperiod Simple Return

Holding the asset for kperiods between datestkand tgives a

k-period simplegrossreturn(1+Rt(k)):

k-period simplenetreturnis:

-

7/31/2019 Session on Stylized Properties

5/45

5

Average Return

Actual time interval is important in comparingreturns (e.g.,

monthly or annual) return).

If asset was held for k periods, then the average

(e.g. annualized) simple gross return is

Average (1+Rt(k))=

(geometric mean of the k one-period simplegross returns)

-

7/31/2019 Session on Stylized Properties

6/45

6

Average Net Return Rt(k)) =

Arithmetic Mean easier to compute than geometricmean and the

one-period returns tend to be small. Can use a first-order Taylor

expansion to approximatethe average net return Rt(k)) as:

-

7/31/2019 Session on Stylized Properties

7/45

7

Continuous Compounding

Rate of interest over a unit time (from t-1 to tperiod) = R

Pt-n = initial capital; Pt = net asset value after ntime

units

Discrete Compounding (m times in unit time):Pt =

Pt-n*(1+(R/m))

m*n

Continuous Compounding (over unit time):P

t= P

t-n*exp(n*r

c). Thus, continuously

compounded return rc is given by

==

)ln(1

)ln(nt

tc

nt

tc

P

P

nr

P

Pnr

-

7/31/2019 Session on Stylized Properties

8/45

8

Continuous Compounding

Continuous Compounding (over unit time): Pt =Pt-1*exp(rt). Thus,

continuously compoundedreturn (or log of simple gross return)

is

-

7/31/2019 Session on Stylized Properties

9/45

9

-

7/31/2019 Session on Stylized Properties

10/45

10

Multiperiod Continuously CompoundedReturn

Continuously compounded multiperiod returnis sum of continuously

compounded one-period

returns. Statistical properties of log returns are

moretractable.

-

7/31/2019 Session on Stylized Properties

11/45

11

Densities of Various Distributions

-

7/31/2019 Session on Stylized Properties

12/45

12

Standard Normal pdf

0.00

0.05

0.100.15

0.20

0.25

0.30

0.35

0.40

0.45

-4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0

x

p(x)

-

7/31/2019 Session on Stylized Properties

13/45

13

Log normal distribution

Log-return is

normal iff gross-return is lognormal

-

7/31/2019 Session on Stylized Properties

14/45

14

>win.graph(width=4.875,height=2.5,pointsize=8)>hist(logret,breaks=30,freq=FALSE,main='RIL

logret')

-

7/31/2019 Session on Stylized Properties

15/45

15

Shape of a Distribution

Measure of asymmetry = skewness,

Measure of Peaked-ness = kurtosis

-

7/31/2019 Session on Stylized Properties

16/45

16

Skewness

Mean = Median =ModeMean < Median < Mode Mode < Median

< Mean

Right-SkewedLeft-Skewed Symmetric

-

7/31/2019 Session on Stylized Properties

17/45

17

Distribution with a positive skewness has along right tail

-

7/31/2019 Session on Stylized Properties

18/45

18

Distribution with a negative skewness has along left tail

-

7/31/2019 Session on Stylized Properties

19/45

19

Positive kurtosis (or leptokurtosis, shown by solid

line)indicates that observations cluster more than those in

thenormal distribution and negative kurtosis (or platykurtosis,

shown by dotted line) indicates observations cluster less.

-

7/31/2019 Session on Stylized Properties

20/45

20

Higher kurtosis implies more of the variance is because of rare

extremedeviations, as opposed to frequent modestly-sized

deviations

UNIFORM dist

-

7/31/2019 Session on Stylized Properties

21/45

21

Skewness & Kurtosis of a r.v. X

S(x) = skewness

K(x) 3 is called the excess kurtosis [K(x) = 3

for a normal Distribution]. Positive excesskurtosis means

heavier tails.

-

7/31/2019 Session on Stylized Properties

22/45

22

Estimates of skewness and kurtosis

Let {x1, . . . , xT} be a random sample of Xwith Tobs. Define

sample mean, standard deviation,skewness and kurtosis by

-

7/31/2019 Session on Stylized Properties

23/45

23

Test of skewness

Under the normality assumption, sampleskewnessand (sample

kurtosis 3) aredistributed asymptotically as normal with zero

mean and variances 6/Tand 24/T . Given an asset return series

{r1, . . . , rT}, to test

skewness of the returns, we consider the nullhypothesis H0:

S(r)=0

-

7/31/2019 Session on Stylized Properties

24/45

24

Test of Kurtosis

Under the normality assumption, (samplekurtosis 3) is

distributed asymptotically asnormal with zero mean and variances

24/T .

Given an asset return series {r1, . . . , rT}, to testexcess

kurtosis of the returns, we consider thenull hypothesis H0:

K(r)-3=0

-

7/31/2019 Session on Stylized Properties

25/45

25

Jarque Bera Test of Normality

Jarque and Bera (1987) combine two prior testsand use the test

statistic

JBis asymptotically distributed as a chi-squared

random variable with 2 degrees of freedom, to testfor normality

of rt .

-

7/31/2019 Session on Stylized Properties

26/45

26

Modified Jarque-Bera (JB) test statistic is anothermeasure of

departure from normality, based on thesample kurtosis and skewness.

The test statistic is

defined as (taking into account k number of

estimatedcoefficients used to create series for which normality

isbeing tested)

where S= skewness, K= kurtosis, T = number ofobservations.

The JB statistic has an asymptotic 2

2-distribution

+

=

4

)3(

6

)(

22 KS

kTJBModified

-

7/31/2019 Session on Stylized Properties

27/45

27

> x jarque.bera.test(x)

Jarque Bera Testdata: xX-squared = 0.2494, df = 2, p-value =

0.8828

> x jarque.bera.test(x)

Jarque Bera Testdata: xX-squared = 7.4205, df = 2, p-value =

0.02447

-

7/31/2019 Session on Stylized Properties

28/45

28

Shapiro-Wilks test

Shapiro-Wilks test tests the null hypothesis that

a sample x1, ..., xncame from a normallydistributed

population.

Test statistic W is square of correlation coeff fordata

(x(1),z(1)), (x(2),z(2)), , (x(n),z(n)) where

x(i) = i-th ordered value from the sample andz(i) = i-th ordered

value from the sample taken from

N(0,1) [ e.g., z(i) = -1( (i0.5)/n ) ]

If W-value is close to 1 then data support the null

hypothesis of normality. Why ?

How close is close ?

-

7/31/2019 Session on Stylized Properties

29/45

29

If W-value is close to 1 then data support thenull hypothesis of

normality. Why ?

If X~N(, 2) and Z~N(0,1) then X(i) + Z(i)

Hence X(i) and Z(i) are supposed to be highlycorrelated if the

null hypothesis is true.

-

7/31/2019 Session on Stylized Properties

30/45

30

References

1. Shapiro, S. S. and Wilk, M. B. (1965). "Ananalysis of

variance test for normality (completesamples)", Biometrika, 52, 3

and 4, pages 591-611.

2. Bera, Anil K., Carlos M. Jarque (1980)."Efficient tests for

normality, homoscedasticityand serial independence of

regressionresiduals". Economics Letters6 (3): 255259.

3. Bera, Anil K., Carlos M. Jarque (1981)."Efficient tests for

normality, homoscedasticityand serial independence of

regressionresiduals: Monte Carlo evidence". EconomicsLetters7 (4):

313318

http://en.wikipedia.org/w/index.php?title=Carlos_Jarque&action=edithttp://en.wikipedia.org/w/index.php?title=Carlos_Jarque&action=edithttp://en.wikipedia.org/w/index.php?title=Carlos_Jarque&action=edithttp://en.wikipedia.org/w/index.php?title=Carlos_Jarque&action=edit

-

7/31/2019 Session on Stylized Properties

31/45

31

Skewness test for IBM Return

t=(-0.0775/0.023966) = -3.2337

http://faculty.chicagobooth.edu/ruey.tsay/teaching/fts2/ (Tsay

Book data)

-

7/31/2019 Session on Stylized Properties

32/45

32

RIL log(price) 23 Aug 2004 -17Aug 2009

-

7/31/2019 Session on Stylized Properties

33/45

33

RIL logret 23 Aug 2004 -17Aug 2009

-

7/31/2019 Session on Stylized Properties

34/45

34

RIL log return data

> jarque.bera.test(logret)

Jarque Bera Test

data: logret

X-squared = 11897.81, df = 2, p-value < 2.2e-16

> # Another normality test method>

shapiro.test(na.omit(logret)) # Reported on Cryer-Chan p.283

Shapiro-Wilk normality test

data: na.omit(logret)W = 0.8969, p-value < 2.2e-16

-

7/31/2019 Session on Stylized Properties

35/45

35

Normal Q-Q Plot

A Q-Q plot ("Q" stands for quantile) is a graphical

method for comparing two distributions by plotting

theirquantiles against each other. If the two distributionsbeing

compared are similar, the points in the Q-Q plotwill approximately

lie on the line y= x.

> win.graph(width=4.875,height=3,pointsize=8)>

qqnorm(logret,

ylab='logret data for RIL')> qqline(logret)

-

7/31/2019 Session on Stylized Properties

36/45

36

Stylized Properties of Financial

Time Series(Tsay, p.19, Sec 3.1 (p.98)

-

7/31/2019 Session on Stylized Properties

37/45

37

What is a Stylized Fact?

Empirical studies on financial time series showsseemingly random

variations of asset prices do

share some quite nontrivial statistical properties,across a wide

range of instruments, markets andtime periods.

Such properties are called stylized empiricalfacts.

-

7/31/2019 Session on Stylized Properties

38/45

38

Some Stylized Statistical Propertiesof Asset Returns

Mean of daily return series usually close to zero

Skewness of daily return is not a serious problem

Heavy tails (e.g., daily returns tend to have highexcess

kurtosis)

Absence of autocorrelations in many assetreturns

Gain/loss asymmetry (one observes large draw-downs in stock

prices but not equally largeupward movements)

-

7/31/2019 Session on Stylized Properties

39/45

39

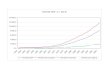

RELIND log return (in %) over 20 Aug 2004 to 17 Aug

2009

-30.0

-25.0

-20.0

-15.0-10.0

-5.0

0.0

5.0

10.015.0

20.0

8/23/2004

2/23/2005

8/23/2005

2/23/2006

8/23/2006

2/23/2007

8/23/2007

2/23/2008

8/23/2008

2/23/2009

-

7/31/2019 Session on Stylized Properties

40/45

40

Summary

> summary(logret)Min. 1st Qu. Median Mean 3rd Qu. Max.

-29.0900 -1.1730 0.1943 0.1155 1.4750 19.1400>

mean(logret)

[1] 0.1154729> var(logret)[1] 7.529715> sd(logret)[1]

2.744033> skewness(logret)[1] -1.122057> kurtosis(logret)[1]

15.00814

-

7/31/2019 Session on Stylized Properties

41/45

41

Histogram

0

50

100

150

200

250

300

350

400

450

-29.5

-24.7

-19.9

-15.0

-10.2

-5.4

-0.6 4.

39.

113

.918

.7

Bin

Frequency

Mean 0.11547

Standard Error 0.07793

Median 0.19432Standard Devia 2.74403

Kurtosis 15.0736

Skewness -1.1234

Range 48.2329

Minimum -29.094Maximum 19.1391

Sum 143.186

Count 1240

-

7/31/2019 Session on Stylized Properties

42/45

42

>win.graph(width=4.875,height=2.5,pointsize=8)>hist(logret,breaks=30,freq=FALSE,main='RIL

logret')

-

7/31/2019 Session on Stylized Properties

43/45

43

> stem(logret)The decimal point is at the |

-28 | 1-26 |

-24 |-22 |-20 |-18 | 0-16 |-14 |-12 | 74-10 |-8 | 6400-6 |

99877762088888644330-4 | 854433211100098876544433222211110-2 |

99999998887776666655554444444322222221100000099998888888877777776666+55-0

|

99999999998888888888888877777777777777666666666655555555555555555544+2930

|

00000000000000011111111111111111111111111122222222222222222222222233+3602

|

00000000000000111111111111111112222222333333333334444444444555555555+85

4 | 0001111111222333445567777778889990000122456796 |

012234589033578 | 0161

10 | 112 | 914 |16 |18 | 1

S

-

7/31/2019 Session on Stylized Properties

44/45

44

Stylized Properties of VolatilitySec 3.1 (p.98)

Volatility means (conditional) variance of log-return of an

underlying asset

First, there exist volatility clusters (i.e., volatility

may be high for certain time periods and low forother

periods).

Second, volatility evolves over time in acontinuous manner

(i.e., volatility jumps are rare).

-

7/31/2019 Session on Stylized Properties

45/45

45

Stylized Properties on Volatility (contd)

Third, volatility does not diverge (i.e., volatilityvaries

within some fixed range). Statisticallyspeaking, volatility is

often stationary.

Fourth, volatility seems to react differently to abig price

increase or a big price drop, referred toas the leverageeffect.

EGARCH model was developed to capture the

asymmetry in volatility induced by big positive and

negative asset returns.