Embed Size (px)

Citation preview

Stern School of BusinessStern School of BusinessManagerial AccountingManagerial Accounting

Summer 2005 Summer 2005

Instructor: Instructor: Francois Brochet Francois Brochet

An Introduction to Managerial An Introduction to Managerial AccountingAccounting

How Managers Use Managerial Accounting How Managers Use Managerial Accounting InformationInformation

The Managerial Accounting The Managerial Accounting Function Function

Provides Information for Product Provides Information for Product and Service Costingand Service Costing

Provides Information for Planning Provides Information for Planning And Decision Making And Decision Making

Provides Information for Provides Information for Performance EvaluationPerformance Evaluation

Information to Determine the Information to Determine the Cost of Products and ServicesCost of Products and Services

Provides Information to determine the cost of Provides Information to determine the cost of manufactured products and servicesmanufactured products and services

Information for Decision MakingInformation for Decision Making

Calculate the financial consequences of Calculate the financial consequences of alternativesalternatives and and see how costs will differ among the alternatives.see how costs will differ among the alternatives.

Managerial accounting has little to do with recording Managerial accounting has little to do with recording past costs, and much to do with estimating past costs, and much to do with estimating future costsfuture costs..

Information for Planning and Information for Planning and Performance EvaluationPerformance Evaluation

Cost accountants help management develop Cost accountants help management develop effective planning tools and methods to effective planning tools and methods to

evaluate the performance of responsibility evaluate the performance of responsibility centers.centers.

Managerial AccountantsManagerial Accountants

Record, measure,determine andanalyze costs

Analyze operations and coststo find ways to improve operations and product

quality while reducing costs

Managerial Accounting and Managerial Accounting and GAAPGAAP

The primary purpose of The primary purpose of financial accountingfinancial accounting is to is to provide stakeholders provide stakeholders information regarding information regarding company and management company and management performance.performance.

The financial data prepared The financial data prepared for this purpose are governed for this purpose are governed by by GAAP.GAAP.

Generally AcceptedAccounting

Principles (GAAP) are the rules,

standards, andconventions that

guide thepreparation of

financial statementsfor stockholders.

Managerial Accounting and Managerial Accounting and GAAPGAAP

Cost data for managerial use Cost data for managerial use need not comply with GAAP.need not comply with GAAP.

Management is free to set its Management is free to set its own definitions for Managerial own definitions for Managerial Accounting Information.Accounting Information.

Decision makers often require Decision makers often require different information than that different information than that provided in financial statements provided in financial statements to shareholders.to shareholders.

Differences Between Financial Differences Between Financial and Managerial Accountingand Managerial Accounting

Creating Value in OrganizationsCreating Value in Organizations

Each step of the development, production, and Each step of the development, production, and distribution process should add value to the distribution process should add value to the

product or service offered.product or service offered.

Using Managerial Accounting Using Managerial Accounting Information to Increase ValueInformation to Increase Value

Nonvalue-added activities – activities that Nonvalue-added activities – activities that do not do not add add value to the product or service.value to the product or service.

Nonvalue-added

activitiesIdentify Eliminate

Cost-Benefit AnalysisCost-Benefit Analysis

The process of comparing benefits with costs The process of comparing benefits with costs associated with a proposed change within an associated with a proposed change within an

organization.organization.

CostsCosts

BenefitsBenefits

Strategic Cost AnalysisStrategic Cost Analysis

If a company can If a company can eliminate nonvalue-addedeliminate nonvalue-added activities, it can reduce costs without activities, it can reduce costs without reducing product value.reducing product value.

Reduced costs, with no loss in value, means Reduced costs, with no loss in value, means the company has a the company has a competitive advantagecompetitive advantage..

Global StrategiesGlobal Strategies

A strategic advantage exists when your A strategic advantage exists when your company has company has invested resourcesinvested resources that make it that make it difficult for competitors to match.difficult for competitors to match.

New entry into the market is difficult because New entry into the market is difficult because of the magnitude of investment required.of the magnitude of investment required.

E-CommerceE-Commerce

During 2001, many dot.com businesses During 2001, many dot.com businesses failed that might have benefited from failed that might have benefited from

the application of managerial the application of managerial accounting tools:accounting tools:

– cost concepts (Chap. 2) cost concepts (Chap. 2) – cost measurement (Chap. 4)cost measurement (Chap. 4)– cost estimation (Chap. 5)cost estimation (Chap. 5)– cost-volume-profit (Chap. 6)cost-volume-profit (Chap. 6)– activity-based costing (Chap. 8)activity-based costing (Chap. 8)– budgeting (Chap. 9)budgeting (Chap. 9)– decision-making (Chap. 13)decision-making (Chap. 13)

Focusing on CustomersFocusing on Customers

Without customers, the organization Without customers, the organization loses its ability to exist.loses its ability to exist.

Customers provide the organization with Customers provide the organization with its focus.its focus.

Many companies identify customers’ Many companies identify customers’ needs before designing and producing needs before designing and producing products.products.

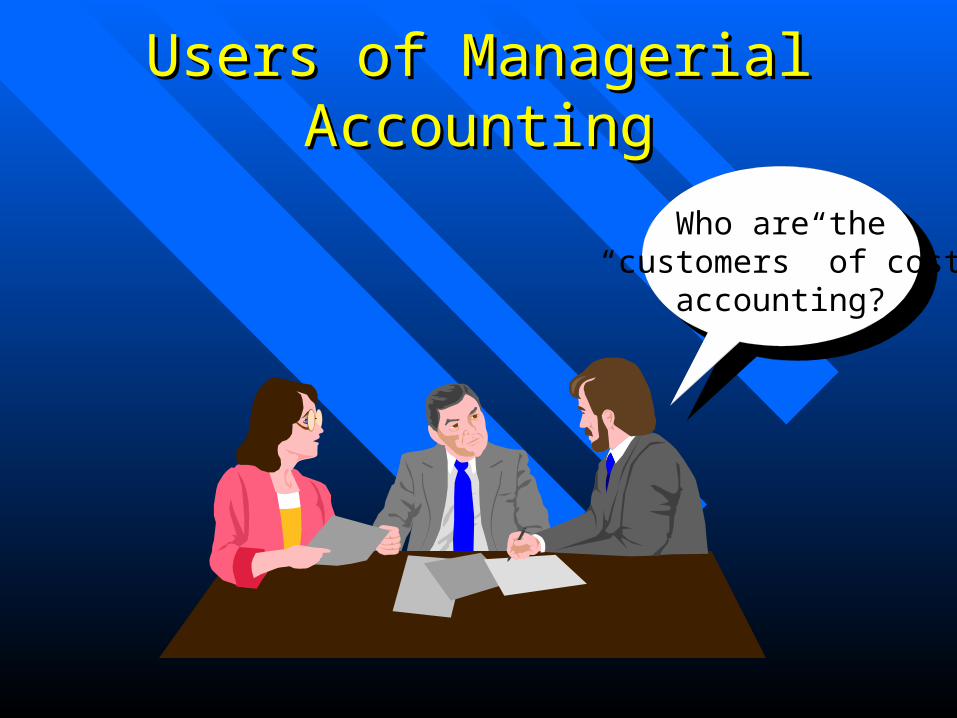

Users of Managerial AccountingUsers of Managerial Accounting

Who are the“customers” of cost

accounting?

Users of Managerial AccountingUsers of Managerial Accounting

Production needs costinformation to control

and improve operations.

Users of Managerial AccountingUsers of Managerial Accounting

Mid-level managersneed cost information that

serves as a warning signal whenoperations are different

from expectations.

Users of Managerial AccountingUsers of Managerial Accounting

I know that seniormanagers use somecost information to

assess overallperformance of the

company.

Managerial Accounting in High-Managerial Accounting in High-Tech Production SettingsTech Production Settings

Many companies have installed Many companies have installed computer-assisted methods ofcomputer-assisted methods of– Manufacturing products,Manufacturing products,– Merchandising products, orMerchandising products, or– Providing services.Providing services.

New technologies have had a New technologies have had a major impact on Managerial major impact on Managerial Accounting.Accounting.

Just-in-Time MethodJust-in-Time Method

In production or purchasing, each unit is purchased or In production or purchasing, each unit is purchased or produced produced just in timejust in time for its use.for its use.

Lean ProductionLean Production

Companies eliminate inventories between Companies eliminate inventories between production departments . . .production departments . . .– Making the quality and efficiency of production the Making the quality and efficiency of production the

highest priority,highest priority,– Providing the flexibility to change quickly from Providing the flexibility to change quickly from

one product to another, andone product to another, and– Emphasizing training and worker skills.Emphasizing training and worker skills.

Total Quality ManagementTotal Quality Management

The organization is managed to The organization is managed to excel excel on all on all dimensions and quality is ultimately defined dimensions and quality is ultimately defined

by the by the customer.customer.

Benchmarking and Benchmarking and Continuous ImprovementContinuous Improvement

Benchmarking – The Benchmarking – The continuous continuous processprocess of of measuring measuring one’s own one’s own products, services and activities products, services and activities against the against the best levels of best levels of performance.performance.

ContinuousContinuous – Managers and – Managers and employees are not satisfied with employees are not satisfied with a particular performance but a particular performance but seek seek ongoing improvement.ongoing improvement.

Theory of ConstraintsTheory of Constraints

Every organization usually has at least one Every organization usually has at least one bottleneckbottleneck that limits production. that limits production.

Management focuses on maximizing profits Management focuses on maximizing profits by by identifying constraintsidentifying constraints and increasing and increasing capacity.capacity.

4. Coordinate processes

4. Coordinate processes

1. Measure process capacity

1. Measure process capacity

2. Identify process

constraints

2. Identify process

constraints

3. Use bottlenecks effectively.

3. Use bottlenecks effectively.

Only actions that strengthen the weakest link in the “chain” improve the process.

Theory of ConstraintsTheory of Constraints

Activity-Based CostingActivity-Based Costingand Managementand Management

A product costing method that is useful in A product costing method that is useful in industries where industries where overhead is high overhead is high relative to relative to

other costs.other costs.

Activity-based costing assigns costs to Activity-based costing assigns costs to products based on products based on several different several different

activities activities whereas traditional costing whereas traditional costing methods only assign costs to products on methods only assign costs to products on

one one oror twotwo different activitiesdifferent activities.. ABC

Activity-Based CostingActivity-Based Costingand Managementand Management

A product costing method that is useful in A product costing method that is useful in industries where industries where overhead is high overhead is high relative to other relative to other

costs.costs.

ABC Traditionalmethod

Products Products

ActivitiesActivities““cost drivers”cost drivers”

Importance of EthicsImportance of Ethicsin Accountingin Accounting

Ethical accounting practices build trust and Ethical accounting practices build trust and promote loyal, productive relationships with promote loyal, productive relationships with users of accounting information.users of accounting information.

Many companies and professional Many companies and professional organizations, such as the Instituteorganizations, such as the Instituteof Management Accountants (IMA),of Management Accountants (IMA),have written codes of ethics whichhave written codes of ethics which

serve as guides for employees.serve as guides for employees. – Code of Conduct for Management AccountantsCode of Conduct for Management Accountants

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Four broad areas of Four broad areas of responsibility:responsibility:

Maintain a high level of Maintain a high level of professional competenceprofessional competence

treat sensitive matters with treat sensitive matters with confidentialityconfidentiality

Maintain personal integrityMaintain personal integrity Be objective in all disclosuresBe objective in all disclosures

CompetenceCompetence

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Follow applicable laws, regulations and

standards.

Follow applicable laws, regulations and

standards.

Maintain professional competence.

Maintain professional competence.

Prepare complete and clear reports after appropriate

analysis.

Prepare complete and clear reports after appropriate

analysis.

ConfidentialityConfidentiality

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Do not disclose confidential information unless legally

obligated to do so.

Do not disclose confidential information unless legally

obligated to do so.

Ensure that subordinates do not disclose confidential

information.

Ensure that subordinates do not disclose confidential

information.

Do not use confidential

information for personal

advantage.

Do not use confidential

information for personal

advantage.

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Avoid conflicts of interest and advise others of potential conflicts.

Avoid conflicts of interest and advise others of potential conflicts.

Recognize and communicate personal and

professional limitations.

Recognize and communicate personal and

professional limitations.

Do not subvert organization’s

legitimate objectives.

Do not subvert organization’s

legitimate objectives.

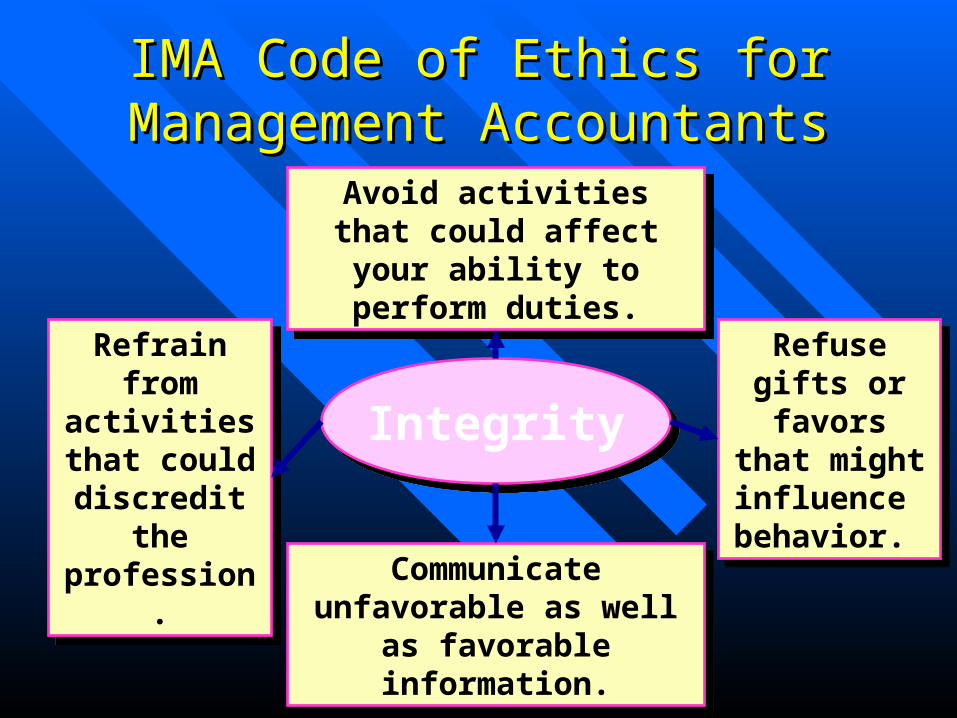

IntegrityIntegrity

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

IntegrityIntegrity

Avoid activities that could affect your ability to

perform duties.

Avoid activities that could affect your ability to

perform duties.

Communicate unfavorable as well as favorable information.

Communicate unfavorable as well as favorable information.

Refrain from activities that could

discredit the profession.

Refrain from activities that could

discredit the profession.

Refuse gifts or favors

that might influence behavior.

Refuse gifts or favors

that might influence behavior.

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Communicate information fairly and objectively.

Communicate information fairly and objectively.

Disclose all information that might be useful to

management.

Disclose all information that might be useful to

management.

ObjectivityObjectivity

Resolution of Ethical ConflictResolution of Ethical Conflict

Follow established policies.Follow established policies.

For unresolved ethical conflicts: For unresolved ethical conflicts:

– Discuss the conflict with immediate superior.Discuss the conflict with immediate superior.

– If immediate superior is the CEO, consider the If immediate superior is the CEO, consider the board of directors or the audit committee. board of directors or the audit committee.

– Except where legally prescribed, maintain Except where legally prescribed, maintain confidentiality.confidentiality.

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants

Resolution of Ethical ConflictResolution of Ethical Conflict

Clarify issues in a confidential discussion Clarify issues in a confidential discussion withwithan objective advisor.an objective advisor.

Consult an attorney as to legal obligations.Consult an attorney as to legal obligations.

The last resort is to resign.The last resort is to resign.

IMA Code of Ethics for IMA Code of Ethics for Management AccountantsManagement Accountants