Embed Size (px)

Citation preview

Nonlinear Dynamics, Psychology, and Life Sciences, Vol. 1, No. 4, 1997

Speculations on Nonlinear Speculative Bubbles

J. Barkley Rosser, Jr.1,2

This paper reviews a variety of issues related to speculative bubbles, especiallythose involving nonlinear dynamics. Models of irrational bubbles, rational bub-bles, and bubbles arising from heterogeneous agents with varying degrees ofknowledge or rationality are examined. The latter are shown to be prone tononlinear dynamics with catastrophic discontinuities, chaos, and other formsof complex phenomena. Empirical evidence regarding the existence of bubblesin various markets is reviewed, eventually examining strong evidence in closed-end country mutual funds markets.

KEY WORDS: speculation; bubbles; rationality; catastrophe; chaos.

INTRODUCTION

Speculative bubbles have long been studied yet remain among the mostmysterious and controversial of economic phenomena. They raise a conflictbetween the core economic concept of rationality and the irrational forcesof darkness apparently lurking in speculative bubbles. Charles MacKay(1852) characterized the latter view in his discussion of the Dutch "tulip-mania" of 1636-37 in his Memoirs of Extraordinary Delusions and the Mad-ness of Crowds. But for defenders of the faith, "the sun of rationality shineseven in the even in the apparent midnight of the most hysterical of panics"(Rosser, 1991, p. 57).

There is no resolution of this conflict. In this paper we shall examinea range of views, their underpinnings and their implications, especiallywhen they imply nonlinear complex dynamics. At one extreme is the view

1Department of Economics, James Madison University, Harrisonburg, Virginia.2Correspondence should be directed to J. Barkley Rosser, Jr., Department of Economics,James Madison University, Harrisonburg, VA 22807; E-mail: [email protected].

275

1090-0578/97/1000-0275$12.50/0 C 1997 Human Sciences Press, Inc.

that bubbles exist and fundamentally reflect irrational behavior, "the mad-ness of crowds." A more moderate version of this says that agents are ra-tional, but that some are merely less well-informed than others. Yet anothersays that bubbles.exist but that they are rational, self-fulfilling propheciesin which agents accurately forecast what will happen and in doing so actto make it happen. At the far extreme is the purest faith in market effi-ciency and rationality which denies the existence of bubbles and arguesthat all cases of apparent bubbles can be explained by alternative argu-ments.

This latter argument depends on the "misspecified fundamental" ar-gument (Flood & Garber, 1980), that any apparent econometric argumentfor a bubble involves some failure to understand what is really going on,in particular a misspecification of what was truly the fundamental involved.Those pushing this argument have argued that it is impossible to ever provethat bubbles exist. At the end of this paper we shall present argumentsthat strongly question this viewpoint. More broadly this paper will be sym-pathetic to models assuming heterogeneous agents who vary in their de-grees of knowledge or rationality. Such models are especially prone tocomplex nonlinear dynamics.

WHAT IS A SPECULATIVE BUBBLE?

A bubble exists for an asset if its price deviates for a significant periodof time from its fundamental value. Usually it is also presumed that thisis due to some kind of speculative behavior by agents wherein they arebuying or selling the asset according to expectations about future changesin its price. This definition is given in Eq. 1

where P is price, F is fundamental, B is bubble, and e is a stochastic errorterm that follows an identically and independently (IID) distributed proc-ess, each of these for time t. Clearly the action in this equation is in un-derstanding what each of these is and it is precisely at this point that thoseskeptical of the existence of bubbles leap in to argue that anything appear-ing to be a B is actually an F or an e .

The most difficult question is what constitutes the fundamental. A gen-eral definition would be that it represents a long-run general equilibriumprice. This becomes muddied if there are multiple equilibria, but we shalleschew this possibility for this paper.

276 Rosser

The easiest case involves assets which earn some kind of real return.For such assets the fundamental is considered to be the present value ofthe expected future stream of net real returns. This presumes knowingboth the future stream of net real returns and also the proper discountrate for carrying out the present value calculation. A central issue arisesas to whether or not such expectations must be rational3 and much of thecontroversy involves cases where such allegedly rationally expected net exante real returns differ substantially from actually observed ex post netreal returns. A general formula for a present value calculation is givenfor the discrete time case in Eq. 2, with PV being the present value, NR,being the net real returns in period t, and r, being the discount rate forperiod t:

VARIETIES OF IRRATIONAL BUBBLES

The original view of speculative bubbles among economists was thatthey are manifestations of irrational mob psychology. The experience notonly of the tulipmania, but of the large and spectacular Mississippi Bubblein France in 1719-20 and the South Sea Bubble in England in 1720 werevery much on the minds of many classical political economists such as JohnStuart Mill (1848).

Drawing on their work, Hyman Minsky (1972) and Charles Kindleber-ger (1989) lay out a stylized story of irrational speculative bubbles. Initiallythere is some displacement from the fundamental, usually upward. Thenspeculation develops as buyers make money with the price rising andeuphoria emerges. Usually some relaxation of credit makes the speculationeasier and as it proceeds, the smarter "insiders" bail out and less well-in-formed and less rational "outsiders" start buying. Often in more dramaticbubbles, fraud will develop as the bubble proceeds. As too many insidersget out the price reaches a peak and begins to drift downwards. This mayalso be triggered by some bad news regarding the fundamental. What fol-lows is the "period of distress" during which outsiders continue to hangon and expectations undergo a major change. Eventually something triggers

3 Agents have rational expectations if their subjective probability distributions of outcomes co-incide with the objective probability distributions of outcomes (Muth, 1961). This has cometo be a very widely used assumption in economic theory, partly due to its convenient impli-cation that on average agents expect what actually will occur, subject to random errors.

Speculation on Nonlinear Speculative Bubbles 277

the panic and crash. Everyone sells suddenly in a rush to get out, and theprice falls sharply.

Camerer (1989) details variations on this story in more recent litera-ture regarding the underlying motives of agents and the processes at work.One such model is the "greater fool" theory. Heterogeneous expectationslead an individual (or individuals) to believe the bubble will last longerthan does anybody else. They are the fool, the sucker, who gets stuck withthe "hot potato." Keynes (1936), Stiglitz (1982), and Roll (1986) advocatethis view. Smith, Suchanek, and Williams (1988) provide experimental evi-dence in support, although they suggest that people can learn not to befoolish with experience. However, a sucker is born every minute, and Tam-borski (1995) documents wild speculation in the newly opened Polish stockmarket, blaming it on the inexperience of those involved.

Shiller (1984) advocates the "fad" theory and especially emphasizesits epidemic and contagious nature. Although Shiller clearly favors irra-tionality as an explanation, Camerer (1989) emphasizes that fads are con-sistent with "near rational" mean reversion in which bubbles quietly die(Fama & French, 1988; Poterba & Summers, 1988). However, Lux (1995)shows that models with psychologically mimetic contagious fads can leadto oscillatory behavior as moods swing from optimistic to pessimistic withchanges in actual returns, as long as there are some fundamentalisttraders.

A famous model is of the "beauty contest" due to Keynes (1936) inwhich the winner is the judge who guesses best the guesses of the otherjudges, irrespective of the actual beauty of the contestants in the beautycontest. However, this could also reflect rational behavior in the case ofarbitrary expectations with asymmetric payoff structures where losers arepenalized more than winners win.

Yet another case is that of "overshooting bubbles" when prices andinformation are imperfectly linked due to "noise" (Black, 1986; DeBondt& Thaler, 1986; Grossman & Stiglitz, 1980). Markets simply overreact toactual changes in fundamentals. This is consistent with slow learning andgradual mean reversion to the fundamental. A variation on this is an "in-trinsic bubble" (Froot & Obstfeld, 1991; Sutherland, 1996) in which an ex-plosive bubble can arise even from a non-explosive oscillation of afundamental.

Finally we have the extreme case of noise known as "mirage trading"where traders mistake noise for information which then self-generates abubble (Grossman, 1976; Milgrom, 1981). Clearly many of these types ofirrational bubbles resemble each other and could be simultaneously oper-ating in particular situations. A general phenomenon that may be occurringin most of these cases is the fact that people can only focus on so much

278 Rosser

at a time which leads them to operate according to heuristic rules andoften to imitate those around them (Tversky & Kahneman, 1974). Manyare the paths of destruction in the world of irrational speculation.

WHEN ARE RATIONAL BUBBLES POSSIBLE?

Although implicit in Keynes (1936, Chap. 12), it was probably PaulSamuelson (1957) who first clearly suggested that a rational speculativebubble was a theoretical possibility. "The market literally lives on its owndreams, and each individual at every moment of time is perfectly rationalto be doing what he is doing" (Samuelson, 1957, p. 215). He notes that"all tulip manias have ended in finite time," but that there is no way tosay when they should end or even if they should.

Jean Tirole (1982) established that there can be no bubbles if thereare a finite number of risk-averse, infinitely lived agents, with common priorinformation and beliefs, trading a finite number of assets with real returnsin discrete time periods. The essence of this theorem is the "backward in-duction" principle, also known as the "hot potato" argument.

In the infinite time horizon a transversality condition holds that guar-antees wealth going to zero, ultimately arising from a limit on net indebt-edness. This means that any bubble that might exist must eventually end.But this means that no one will want to own a bubbly asset in the periodbefore it ends. And since everyone knows that no one wants it in that pe-riod, no one will want it in the period before that and so forth backwardsto time zero. There are no suckers to stick the hot potato with and so thebubble cannot even begin.

Relaxing the various conditions in the theorem can lead to cases whererational speculative bubbles of one sort or another can exist. Certainly ifagents are risk-loving bubbles can exist because they will not fear the like-lihood of a crash as they bid up prices in search of speculative returns. Aninfinity of finitely lived agents can allow for a bubble, most readily a hard-to-observe stationary one, as the hot potato can be handed on and on with-out anyone ever getting stuck with it. This case arises with overlappinggenerations (OLG) (Tirole, 1985) and indeed this framework was initiallydeveloped (Allais, 1947; Samuelson, 1958) to explain the existence of fiatmoney which has positive price but zero fundamental.

Failure to have common prior information or beliefs can open the doorto rational bubbles (Harrison & Kreps, 1978), or if there is asymmetricinformation between investors and portfolio managers (Allen & Gorton,1993), although Allen, Morris, and Postlewaite (1993) show that in the fi-nite time period case each agent must have private information, trades are

Speculation on Nonlinear Speculative Bubbles 279

not common knowledge, and each agent must be short sale constrained atsome point in the future.

An infinite dimensional commodity space also allows for bubbles toemerge in the infinite time horizon as "finitely additive charges" (Gilles,1989; Gilles & LeRoy, 1992; Magill & Quinzii, 1996) in non-summableprice systems, with the countably summable part being the fundamental, ifagents have sufficient patience. Another infinity that allows rational bubblesis if trading occurs continuously rather than discretely (Faust, 1989). Thenan infinity of trades can occur in finite time and Zeno's paradox effectivelyeliminates the "hot potato" problem.

AN OVERLAPPING GENERATIONS MODEL OF A PERMANENTBUBBLE

Tirole (1985) presents an overlapping generations model of a perma-nent bubble draws in a growth model with labor, capital, and a rent-earningasset. Agents live two periods, inelastically supplying a unit of labor in thefirst period, and possessing identical, well-behaved, and bounded fromabove and below utility functions of their two period consumption of asingle good. Population L grows at a rate n > 0. Wages at t will be wD thereal interest rate will be rD s(wt, rt+1) will be individual savings with aggre-gate savings being (1 + n) t. The good, Y, will be produced by a constantreturns to scale neoclassical production function using capital, K, and labor,L, with k = K/L.

280 Rosser

Capital is invested in the previous period. Competition gives

Savings can be invested in a rent-earning asset as well as in real capital.If rent in real goods per period is R, with rent possibly representing anunmeasurable utility stream, then the per capita value of the market fun-damental of the asset in t for a sequence of real interest rates will be

An equilibrium is "bubbly" if bt > 0 for some t, "permanently bubbly"if bt > 0 for all t, and "asymptotically bubbly" if bt does not converge tozero as t goes to infinity.

Tirole (1985) shows that if (3) holds for k0 > 0 then an asymptoticallybubbly equilibrium can exist and be efficient if the bubbleless and rentlessequilibrium value of r0 = r < n.4

The asset can earn zero rent, which would be the case for pure fiatmoney with a permanent positive value and no utility value for transactionspurposes. This solution implies a steady state value for the bubble, b, givenby

Thus, this is a model of non-explosive rational bubbles.

HETEROGENEOUS AGENTS AND SEMI-RATIONAL BUBBLES

Increasingly it is clear that the older story of heterogeneous agents isbetter at explaining what goes on in speculative markets than do those thatassume that everyone is equally rational or irrational, or equally well-informed or ill-informed. Different agents have different knowledge, dif-

4The condition that r0 = r < n can be relaxed and still have an efficient equilibrium with arational bubble if there is risk with high risk-aversion (Bertocchi, 1991), the speculative be-havior in effect replacing insurance markets, or in the case of a suitably specified endogenousgrowth model where bubbly "excessive optimism" based on naive expectations can lead to ahigher growth path than that arising from simple rational expectations (Nyssen, 1994).

A perfect foresight equilibrium will satisfy all of the above and also

Savings will be divided between capital investment and the rent-bear-ing asset, including its bubble component, thus

The asset price may contain a per capita bubble component, bD whichunder perfect foresight must bear the same yield as capital, thus

281Speculation on Nonlinear Speculative Bubbles

ferent attitudes, and play different roles in these markets, and their inter-actions can be the source of dynamics.5 Some old terminology dividesagents into "fundamentalists" who trade on fundamentals and "chartists"who chase trends (Goodman, 1968; Sethi, 1996; Zeeman, 19746). Lux(1995) has fundamentalists and "speculators." Day and Huang (1990) havefundamentalists, trend chasing "sheep," and market specialists. Gennotteand Leland (1990) have "uninformed investors" who only know prices,"price-informed investors" who have inside knowledge of asset fundamen-tals, and "supply-informed investors" who are market makers and knowabout future asset issues. De Long, Schleifer, Summers, and Waldmann(1990) have passive fundamentalists, "rational speculators" (insiders), andirrational noise traders (outsiders). All of these can be characterized asmodels of semi-rational bubbles or behavior, as they mix well-informed ra-tional agents with less well-informed possibly irrational agents, althoughRichard Thaler (1991) proposes the term "quasi-rational" for such models.

Rosser (1994) extends the De Long, Shleifer, Summers, and Waldmann(1990) model of "positive feedback investment" into the stochastic crashframework of Blanchard and Watson (1982). There are four periods of un-known length. In the first, price equals its fundamental. In the second, ra-tional speculators buy as do noise traders, while fundamentalists sell. Inthe third, rational speculators and fundamentalists sell, while noise traderskeep buying. This is the "period of distress" discussed by Kindleberger(1989). In the final period price has returned to its fundamental.

Excess demand in time t by fundamentalists is

Rosser282

where pt is the asset price in time t, pf is the unique fundamental price,and a is

where y is the risk-aversion coefficient and c2T is the variance of thefundamental. (1 - u) is the measure of the fundamentalists, with u thatof the rational speculators and one the measure of the noise traders.

5In a study of the pork market, Chavas (1995) estimates that only 23% of market participantsshow behavior consistent with rational expectations while the remaining 77% exhibit somebackward-looking element in their expectations.

6Ironically one of the major critiques of Zeeman's stock market model by Zahler and Sussman(1977) was its allowing for agents who did not have rational expectations, the chartists. Thiswas near the high water mark of when such a criticism would have been considered fatallydevastating, whereas today it merely seems silly.

The bubble begins at t = b with a demand shock from the rationalspeculators = e , p is the time rate of discount, and p is the probabilityof a crash in any time period. Excess demand by rational speculators inthe upward bubble portion is

A crash occurs when there is no equilibrium after which the noise traders'lag operator goes to zero and the price returns to the fundamental.

Price dynamics prior to the peak, while the rational speculators arestill buying will be

After the peak but prior to the crash, the price dynamics will be

given that the stability condition c>£bj=1 j = L j(B+d) holds.

If the reactive coefficient, d, is high such that at t -1 equals thebubble's peak,

After the peak, the rational speculators act like passive fundamentalists.B is a reactive coefficient for trend chasing, 8 is a reactive coefficient

to current market conditions, and X is a lag operator. Excess demand byirrational noise speculators is

Speculation on Nonlinear Speculative Bubbles 283

284 Rosser

Fig. 1. Semi-rational bubble with a sudden crash.

holds, then the noise traders will jump ship at the peak and there will bean immediate crash as in the tulipmania of the 1630s or the silver pricebubble of 1980. This is depicted in Fig. 1.

However, if the lag operator is very strong and the current reactivecoefficient is very weak such that if when

then,

then the price will decline from the peak with no visible crash as in Francein 1866 and in Britain in 1873 and 1907. This is depicted in Fig. 2.

In between these two extremes the system will exhibit what can beviewed as the most historically common model, with a bubble followed by

a period of distress followed by a crash, as in the Mississippi and SouthSea Bubbles in 1719-20, and the US stock market bubbles in 1929 and1987. This standard pattern is depicted in Fig. 3.

A CATASTROPHE THEORY VIEW

The first application of catastrophe theory to economics was the much-criticized model by Zeeman (1974) of stock price dynamics as a cusp

Fig. 3. Semi-rational bubble with period of distress before crash.

Speculation on Nonlinear Speculative Bubbles 285

Fig. 2. Semi-rational bubble with no crash.

Fig. 4. Bubble and crash as cusp catastrophe.

catastrophe.7 Letting J be the rate of change of prices, F be excess demandby fundamentalists, and C be excess demand by "chartists," can give anequilibrium manifold and associated dynamics as shown in Figure 4. Guas-tello (1995, pp. 292-297) has estimated a model of the 1987 stock marketcrash based on the Zeeman model.8

Casti and Swain (1975) present a butterfly catastrophe version of thisfor a model of urban property prices. The manifold for such a model isdiffeomorphic to

7Other applications of the cusp catastrophe to financial models include Ho and Saunders'(1980) model of bank failures and Gregory-Allen and Henderson's (1991) model of corporatefailures.

8Gennotte and Leland (1990) suggest a cusp catastrophe interpretation of their discontinuousdynamics results in their model of the 1987 crash. Their model has three categories of agentsand focuses on hedging strategies.

Rosser286

Fig. 5. Semi-rational bubble and crash as butterfly catastrophe.

We can identify this catastrophe with our model of semi-rational specu-lation by allowing x to equal the rate of change of prices, u1 to be a functionof £b j=1 Lj(B+d), the "butterfly" factor which creates the pocket when itis sufficiently strong and which reflects the trend chasing of the noise trad-ers, u2 to be a function of d, the "bias" factor tilting the cusp, u3 to be afunction of [(1 + p)/(1-p)]t-be, the "splitting" (or bifurcation) factor gen-erating the main cusp which reflects the impact of the rational speculators,and u4 be a function of a , the "normal" (or asymmetry) factor reflectingthe fundamentalist traders. This case with a butterfly pocket present is de-picted in Fig. 5.

With a weak butterfly there will be no "pocket" and rational bubblebehavior will dominate with an immediate crash after the peak, correspond-ing to the simpler Zeeman scenario, from the top section of the manifoldto the bottom. With a strong butterfly a declining "period of distress" stage

Speculation on Nonlinear Speculative Bubbles 287

after the peak can exist, as the noise traders buoy up the bubble for awhile in the middle pocket. But if 8 is low enough and a is high enoughthe final crash can become insignificant, the trajectory dropping from thetop section to the even more expanded middle one without dropping tothe bottom one. Thus, our taxonomy of semi-rational bubbles can be quali-tatively depicted by the five-dimensional butterfly catastrophe model.

A CHAOS THEORY VIEW

Models of speculation with heterogeneous agents can also generatechaotic dynamics (Day & Huang, 1990; De Grauwe, Dewachter, & Em-brechts, 1993). Day and Huang (1990) present a canonical semi-rationalspeculation model with three categories of agents: rational fundamentalists,irrational trend-chasing "sheep" (noise traders), and market mediating spe-cialists who set prices.

There exists a constant fundamental, pf , an upper bound, pmax, and alower bound, pmin. Fundamentalists buy when pt is below pf and sell whenpt is above pf according to a weighting function, f(pt). Their excess demandis

The fundamentalists only trade within [pmin, pmax] because below pmin theyhave exhausted purchasing opportunities and above pmax they have ex-hausted selling opportunities.

Trend-chasing "sheep" (noise traders) create bubbles through theircontagious mimesis. Their excess demands are

Rosser288

with

in which case there will be two temporary equilibria, pl < pf and ph > pf

which will both be unstable if when pt is at either of them

In this case there will be both up and down bubbles as noisy sheep domi-nate the market. All dynamics will be bounded within [pmin, pmax], but ifthe equilibria are unstable the bubbles may continue without end, althoughthey may not be monotonic.

Furthermore they may be chaotic bubbles. The crucial condition is thatin addition to the temporary equilibria being unstable that positive (bull)bubble regimes can switch to being negative (bear) bubble regimes andvice versa (Day & Huang, 1990). This will hold if

Such a case is depicted in Fig. 6.Does this model or any variant of it have empirical relevance? Gu

(1993) finds empirical support for its general applicability to stock marketdata, but does not test for chaos.

which will be negative if pt > pf and the fundamentalists outweigh the sheepand zero or positive otherwise.

If noisy sheep outweigh rational fundamentalists, equilibrium at thefundamental is unstable. This occurs if

The market specialists influence dynamics through c in

which combine with the fundamentalist excess demand to give

Speculation on Nonlinear Speculative Bubbles 289

Fig. 6. Chaotically switching bull and bear bubbles.

The broader question of chaotic dynamics in stock markets in particularhas been very controversial. Numerous estimates have been made findingpositive Lyapunov exponents for some stock market return series or other(Eckmann, Kamphorst, Oliffson, & Scheinkman, 1988; Eldredge, Bernhardt,& Mulvey, 1993; Peters, 1991). But such estimates lack statistical reliabilitytests.9 Furthermore the inability of efforts to develop forecasting models us-ing chaotic models has been argued to mean that either there is no chaosor it is very high dimensional and thus indistinguishable from pure random-ness (Hsieh, 1991; Jaditz & Sayers, 1993; LeBaron, 1994).

9One way of attempting to test the robustness of Lyapunov exponent estimates is through"bootstrapping," (Theiler, Eubank, Longtin, Galdrikan, & Farmer, 1992) which generates anIID null through resampling of the data in a special way. Blank (1991) found positiveLyapunov exponents for a series on soybean futures which he supported through the use ofbootstrapping.

Rosser290

A COMPLEXITY THEORY VIEW

Further extrapolating the semi-rational approaches presented abovecan be done by allowing for agents to move from one type of behavior toanother as circumstances change and for the types of behavior themselvesto evolve over time. Complementary approaches to this have taken analyticand computational forms. A computational approach is due to a group atthe Santa Fe Institute (Palmer, Arthur, Holland, LeBaron, & Tayler, 1994;LeBaron, 1997), drawing on the classifier system of Holland (1992) andideas of inductive learning due to Arthur (1995).

Let there be N agents buying or selling shares of stock according toR rules, with aik representing an action (buy = 1, sell = -1) by the ithagent according to rule k. Each agent tracks each rule according to astrength, sik(t) representing the success of the rule at increasing wealth,given by

Speculation on Nonlinear Speculative Bubbles 291

where c is a rule strength accumulation parameter, p is share price, r isthe real interest rate, and d is share dividend. Rules depend on bits ofinformation and new rules can be generated according to a genetic algo-rithm, with new ones replacing old ones that are being the least used byagents. Thus the rules evolve as agents learn.

In very simple cases with few rules and agents, the system may con-verge on the fundamental equilibrium. However as the complexity of theenvironment increases, complex dynamics emerge with agents learningmore complex rules over time and increasingly diverging from each otherin their behavior. A very typical pattern for this Santa Fe model underthese circumstances is to stay close to fundamentals for extended periodsbut then to experience up or down deviations for periods that suddenlyend, namely bull and bear bubbles and crashes. Trading volume variesgreatly over time, but is not correlated with the bubble episodes. A self-organized wealth distribution emerges over time, even though individualagents move up and down within it.

Analytic analogues of this simulation approach have been developedby Brock (1997) and Brock and Hommes (1995, 1996). They study modelsin which agents choose among strategies in a risky environment with mem-ory of past success entering their selection and with an "intensity of choice"parameter that plays a crucial role in bifurcations of the system. If intensityof choice is low then there is little strategy switching, but there exist criticallevels of this intensity for which qualitative changes in behavior occur. This

draws on earlier discrete choice work of Brock (1993) that draws on modelsof interacting particle systems (IPS) (Kac, 1968).

In Brock and Hommes (1996) they examine the pattern of bifurcationsas the number of strategies goes to infinity, what they call the large typelimit method. They show that rational expectations strategies tend to domi-nate as memory increases, intensity of choice increases, and risk-aversionis lower. But if information is costly, non-rational expectations strategiescan survive.

In Brock and Hommes (1995) they study a particular case in whichthere are two strategies, a rational expectations "fundamentalist" one whichis costly, and a free "naive" trend-chasing one. The dynamics bear a certainsimilarity to what happens in the Santa Fe model. With certain zones ofparameter values, the system will oscillate toward and away from the fun-damental as agents switch back and forth between strategies. Near the fun-damental, it does not pay to obtain information to follow the rationalexpectations strategy and so trend-chasing and bubbles emerge. But as theprice moves away from the fundamental it starts to pay to switch to thefundamentalist strategy and the system tends to go back. Brock andHommes (1995) show that this can result in chaotic dynamics, fractal basinboundaries, and other complexity phenomena.

Brock (1997) characterizes this situation as the prediction paradox,with the "index paradox" being a special case. The index paradox is thatif everyone in the stock market invests in an index fund, then it will paysomeone to do securities analysis and invest in mispriced securities. How-ever, if everyone is doing costly securities analysis, then it will pay to avoidthese costs by investing in an index fund. Obviously the upshot of thisparadox is that complex or at least oscillatory dynamics can arise as agentsbounce back and forth between strategies.10

THE EMPIRICAL OBSERVABILITY OF BUBBLES

There has been an enormous literature on empirical studies of theexistence or nonexistence of speculative bubbles in many different kinds ofmarkets using a variety of econometric methods. We shall not attempt acomplete survey here (see Rosser, 1991). Rather, we shall simply note afew major surveys or studies regarding several categories of markets.

10This argument is a close relative of that of Grossman and Stiglitz (1980) that informationallyefficient markets are impossible because then there would be no incentive to trade, but with-out trades there would be no information.

292 Rosser

The most intensively studied of all markets for bubbles have been stockmarkets. Substantial reviews of these studies are in Shiller (1989) andLeRoy (1989). They present much evidence in favor of the existence ofbubbles in stock markets, although there has been great controversy overthese findings.

The evidence on bubbles in hyperinflationary situations is very mixed,with the German case in the 1920s a much studied example with resultsvarying depending on econometric techniques and assumptions about data(Casella, 1989).

That bubbles exist in foreign exchange markets has become so widelyaccepted as to have become almost a truism, although the greater difficultyof defining fundamentals in these markets has made for ongoing contro-versy. A review that supports the existence of such bubbles is Frankel andRose (1995).

Finally it has been argued that such bubbles have appeared in somereal estate markets. Case and Shiller (1989) present evidence for them insome US residential housing markets and Noguchi (1990) presents similarevidence for Japanese real estate markets in the 1980s.

Nevertheless, none of these studies can be viewed as decisive becauseall of them are subject to the misspecified fundamentals critique. The ob-served price movements may have reflected ex ante rationally expectedmovements of fundamentals which then did not transpire ex post.

CLOSED-END FUNDS AND THE END OF AMBIGUITY?

A theme running through this discussion has been that of the ultimateambiguity posed by the misspecified fundamentals problem, that any ap-parent bubble price dynamic may simply reflect a rationally expected butunobserved regime switch, as initially posed by Flood and Garber (1980).Hamilton (1986) shows that various kinds of bubbles can be perfectly mim-icked by particular specifications of expected but non-occurring changes infundamentals. However, extraneous influences upon expectations cannot beruled out a priori (Burmeister, Flood, & Garber, 1983).

One possible solution to the problem is to use survey evidence of whatagents claim to think, although this is often dismissed by believers in ra-tional expectations. Thus, Shiller and Pound (1987) find little concernamong market participants in the 1987 stock market crash regarding pos-sible changes in tax and takeover laws while Mitchell and Netter (1989)argue that such concerns fundamentally drove the crash. Although mostbelieve that the Mississippi and South Sea bubbles of 1719-20 are accuratelylabeled, Garber (1990) argues that both reflected genuine optimism regard-

Speculation on Nonlinear Speculative Bubbles 293

ing John Law's macroeconomic scheme. "Investors had to take positionson its potential success. It is curious that economists have accepted thefailure of the experiments as proof that the investors were foolishly andirrationally wrong" (Garber, ibid, p. 53). Thus, it would appear that thereis no resolution to this ambiguity; not only cannot bubbles be distinguishedfrom non-bubbles but rationality apparently cannot be distinguished fromirrationality.

But there may be a way around this problem. It involves closed-endfunds which consist of a basket of assets. In contrast to open-end funds,the value of the fund is not automatically adjusted to equal the net assetvalue (NAV) of its constituent components. The fund's price can divergefrom its NAV and they regularly do. The significance for us is that theNA V can be viewed as constituting the true fundamental of the closed-endfund, correcting for any transactions or tax costs. If the value of the fundis greater than its NAV it has a premium, if it is less it has a discount.

After running large premia in 1929,11 most closed-end funds in theUS have tended to run persistent discounts, a phenomenon called theclosed-end fund puzzle (Lee, Shleifer, & Thaler, 1990, 1991). Zweig (1973)uses the average size of this discount or premium as an index of "investorpsychology." Pontiff (1995) shows that investors can on average outper-form the market by purchasing and holding deeply discounted closed-endfunds; they are "ten dollar bills" lying around to be picked up. Possibleexplanations for this puzzle include management fees, limits to borrowingstocks to sell a fund short, management performance of a fund, possibleilliquidity of some of the assets, the impact of accumulated but unrealizedcapital gains or losses on taxes, and a grab bag of other agency and trans-actions costs (Kramer & Smith, 1995). But most studies suggest that theseare not able to explain the size or persistence of the discounts (Lee,Shleifer, & Thaler, 1990, 1991), or the apparent tendency for discountsand premia to be correlated across funds (Hardouvelis, La Porta, &Wizman, 1994).

A particularly dramatic episode in which it appears that there was aspeculative bubble that cannot be readily dismissed by reference to mis-specified fundamentals involves closed-end country funds (CECFs) in late1989 and early 1990. These are funds consisting of assets from particularcountries, and for some of these the problem of illiquidity of the underlyingassets due to national restrictions on capital movements is relevant. Butfor many it is not, especially the more developed economies with thick capi-tal markets such as Spain and Germany. Ahmed, Koppl, Rosser, and White

11De Long and Shleifer (1991) cite this as evidence that the 1929 US stock market was indeeda bubble, although it is only directly evidence of a bubble in the closed-end funds themselves.

294 Rosser

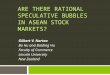

Fig. 7. Germany fund premium: October 6, 1989 to November 22, 1991.

(1996) examine the behavior of several CECFs in this period using switch-ing models and rescaled range analysis and find that premia emerged inmany of them that ran up dramatically in a significant manner.

These look like bubbles. On one day in September, 1989, the Spain fundrose over 40% while its NAV rose a mere 1%.12 The Germany Fund, espe-cially stimulated by the excitement over the fall of the Berlin Wall, rose toover twice its NAV by the bubble's peak in February, 1990. The behavior ofthe premium on the Germany Fund between October 6,1989 and November22, 1991 is depicted in Fig. 7, but it should be kept in mind that similarthings were happening to many other CECFs around the world. This was aglobal bubble and most of the funds crashed at about the same time as well.

The value of the premium or discount of a fund is

with PM being the premium (or discount if less than zero), P being thefund's price, and NAV being its net asset value, or presumed fundamental.

12This suggests a disjuncture and possible asymmetry between the perceptions of internationalinvestors who buy the CECFs and domestic investors who buy the underlying assets generally.Frankel and Shmukler (1996) use this to argue that the 1994 crash of the Mexican peso wastriggered by Mexican insiders fleeing the currency rather than outsiders, the evidence beingthe emergence of premia in the three Mexico funds just before the crash as NAVs droppedwhile fund values held up.

Speculation on Nonlinear Speculative Bubbles 295

The details of this episode draw together various threads of our dis-cussion of bubbles. It appears that the major participants were Japaneseinvestors, with over 80% of the Germany Fund being held by them at thepeak in February, 1990 (Ahmed, Koppl, Rosser, & White, 1996). The initialrunups in the late summer and fall of 1989 were largely triggered by massivepurchases by a "Big Player,"13 Nomura Securities. This was just prior tothe peak of the Japanese stock market bubble, and Nomura and other Japa-nese securities firms can be viewed as being the rational speculators orinsiders of the De Long-Shleifer-Summers-Waldmann (1990) model de-scribed above. After the Japanese stock market peaked and began to fallin December, 1989, the securities firms began to sell CECF shares to in-dividual Japanese investors, the irrational sheep or noise traders or outsid-ers of that model or the Day-Huang (1990) model, who bought during theperiod of distress. Nomura and the other big players got out in time andleft the individual Japanese investors fleeing the stock market crash in Ja-pan as the suckers holding the hot potato when the CECF bubble finallycrashed in February, 1990. If this was not a speculative bubble, then indeedthere is no such thing, rational or irrational.

CONCLUSIONS

This paper has reviewed theoretical and empirical issues surroundingspeculative bubbles, especially those involving nonlinear complex dynamics.A range of possible bubble models from those involving fully rational andwell-informed agents to those involving irrational or badly informed agentswere examined, with special emphasis on those with heterogeneous agentsvarying in their degrees of rationality or knowledge. Models of the latterwere presented which are capable of generating catastrophic discontinui-ties, chaotic dynamics, and broader categories of complex dynamics as well.

Finally the question of the existence of bubbles was directly con-fronted. Although many studies have argued for the existence of bubblesin numerous kinds of markets, most of these studies have been subject tothe misspecified fundamentals critique, that what was observed could havereflected a rational expectation by agents of changes in the fundamentalswhich then did not occur. However, we considered a study of the marketfor closed-end country funds where this problem apparently can be over-come and which found that a speculative bubble probably existed in late1989 and early 1990 in that market. Detailed examination of that episode

13See Gastineau and Jarrow (1991) and Koppl and Yeager (1996) for the theory of the BigPlayer in speculation.

296 Rosser

suggests that the assumption that agents are heterogeneous in their degreesof rationality and knowledge is probably correct.

ACKNOWLEDGEMENTS

This paper is based on a plenary lecture delivered on June 25, 1996at the annual conference of the Society for Chaos Theory in Psychology& Life Sciences at Berkeley, and the author wishes to thank the participantsfor their useful remarks. The author also wishes to acknowledge comments,receipt of materials, or other useful inputs from Ehsan Ahmed, Peter M.Allen, Anthony Bopp, William A. Brock, Jean-Paul Chavas, Carl Chiarella,David Colander, Richard H. Day, Steven M. Durlauf, S. Kirk Elwood, TWindsor Fields, Peter M. Garber, Stephen J. Guastello, Roger Guesnerie,James D. Hamilton, Cars M. Hommes, Ted Jaditz, Steve Keen, RogerKoppl, Francis Kramarz, Blake LeBaron, Charles M.C. Lee, Thomas Lux,Elliott Middleton, Alexandra M. Post, Rajiv Sethi, Richard G. Sheehan,Max Stevenson, Mark van Boening, Mark V White, William C. Wood, andtwo anonymous referees. None of the above are responsible for any errorsor questionable interpretations contained within this paper.

REFERENCES

Ahmed, E., Koppl, R., Rosser, Jr., J.B. & White, M.V (1996). Complex bubble persistencein closed-end country funds. Journal of Economic Behavior and Organization, forthcoming.

Allais, M. (1947). Economie et interet. Paris: Imprimerie National.Allen, F. & Gorton, G. (1993). Churning bubbles. Review of Economic Studies, 60, 813-836.Allen, E, Morris, S. & Postlewaite, A. (1993). Finite bubbles, with short sale constraints and

asymmetric information. Journal of Economic Theory, 61, 206-229.Arthur, W. B. (1995). Complexity in economic and financial markets. Complexity, 1, 20-25.Bertocchi, G. (1991). Bubbles and inefficiencies. Economics Letters, 35, 117-122.Black, F.(1986). Noise. Journal of Finance, 41, 529-543.Blanchard, O.J. & Watson, M.W. (1982). Bubbles, rational expectations, and financial markets.

In P Wachtel (Ed.), Crises in the economic and financial structure (pp. 295-315). Lexington:Lexington Books.

Blank, S.C. (1991). "Chaos" in the financial markets? A nonlinear dynamical analysis. Journalof Futures Markets, 11, 711-728.

Brock, W.A. (1993). Pathways to randomness in the economy: Emergent nonlinearity andchaos in economics and finance. Estudios Economicos, 8, 3-55.

Brock, W.A. (1997). Asset price behavior in complex environments. In W.B. Arthur, S. Durlauf,and D. Lane (Eds.), The economy as a complex evolving system, II. Redwood City:Addison-Wesley, in press.

Brock, W.A. & Hommes, C.H. (1995). Rational routes to randomness. Social Systems ResearchInstitute Paper No. 9506, University of Wisconsin-Madison.

Brock, W.A. & Hommes, C.H. (1996). Adaptive beliefs and the emergence of complex dynamicsin asset pricing models. Mimeo, University of Wisconsin-Madison, University of Amster-dam.

Speculation on Nonlinear Speculative Bubbles 297

Burmeister, E., Flood, R.P & Garber, P.M. (1983). On the equivalence of solutions in rationalexpectations models. Journal of Economic Dynamics and Control, 5, 311-321.

Camerer, C. (1989). Bubbles and fads in asset prices: A review of theory and evidence. Journalof Economic Surveys, 3, 3-41.

Case, K.E. & Shiller, R.J. (1989). The efficiency of the market for single family homes. Ameri-can Economic Review, 79, 135-137.

Casella, A. (1989). Testing for rational bubbles with exogenous or endogenous fundamentals:The German hyperinflation once more. Journal of Monetary Economics, 24, 109-122.

Casti, J.L. & Swain, H. (1975). Catastrophe theory and urban processes. RM-75-14, InternationalInstitute for Applied Systems Analysis, Laxenburg, Austria.

Chavas, J.-E (1995). On the economic rationality of market participants: The case of expectationsin the U.S. pork market. Mimeo, Department of Agricultural Economics, University ofWisconsin-Madison.

Day, R.H. & Huang, W (1990). Bulls, bears, and market sheep. Journal of Economic Behaviorand Organization, 14, 299-329.

De Grauwe, E, Dewachter H. & Embrechts, M. (1993). Exchange rate theory: Chaotic modelsof foreign exchange rates. Oxford: Blackwell.

De Bondt, W.F.M. & Thaler, R.H. (1986). Does the stock market overreact? Journal ofFinance, 40, 793-807.

De Long, J.B. & Shleifer, A. (1991). The stock market bubble of 1929: Evidence from closed-end mutual funds. Journal of Economic History, 51, 675-700.

De Long, J.B., Shleifer, A., Summers, L.H. & Waldmann, R.J. (1990). Positive feedback in-vestment strategies and destabilizing rational speculation. Journal of Finance, 45, 379-395.

Eckmann, J.E, Kamphorst, S.O., Ruelle, D. & Scheinkman, J.A. (1988). Lyapunov exponentsfor stock returns. In EW. Anderson, K.J. Arrow, and D. Pines (Eds.), The economy as acomplex evolving system (pp. 301-304). Redwood City: Addison-Wesley.

Eldredge, R.M., Bernhardt, C. & Mulvey, I. (1993). Evidence of chaos in the S&P cash index.Advances in Futures and Options Research, 6, 179-192.

Fama, E.E & French, K.R. (1988). Permanent and temporary components of stock prices.Journal of Political Economy, 96, 246-273.

Faust, J.W. (1989). Supernovas in monetary theory: Does the ultimate sunspot rule out money?American Economic Review, 79, 872-881.

Flood, R.E & Garber, EM. (1980). Market fundamentals versus price-level bubbles: The firsttests. Journal of Political Economy, 88, 745-770.

Frankel, J.A. & Rose, A.K. (1995). A survey of empirical research on nominal exchange rates.In G. Grossman and K. Rogoff (Eds.), The handbook of international economics. Amster-dam: North-Holland, in press.

Frankel, J.A. & Shmukler, S.L. (1996). Country fund discounts, asymmetric information andthe Mexican crisis of 1994: Did local residents turn pessimistic before international investors?Center for International and Development Economics Research Working Paper No. C96-067, University of California at Berkeley.

Froot, K.A. & Obstfeld, M. (1991). Intrinsic bubbles: The case of stock prices. American Eco-nomic Review, 81, 1189-1214.

Garber, EM. (1990). Famous first bubbles. Journal of Economic Perspectives, 4, 35-54.Gastineau, G.L. & Jarrow, R.M. (1991). Large-trader impact and market regulation. Financial

Analysts Journal, 47, 40-51.Gennotte, G. & Leland, H. (1990). Market liquidity, hedging, and crashes. American Economic

Review, 80, 999-1021.Gilles, C. (1989). Charges as equilibrium prices and asset bubbles. Journal of Mathematical

Economics, 18, 155-167.Gilles, C. & LeRoy, S.F. (1992). Bubbles and charges. International Economic Review, 33, 323-

339.Goodman, G. ["Adam Smith"] (1968). The money game. New York: McGraw-Hill.Gregory-Allen, R.B. & Henderson, Jr., G.V (1991). A brief review of catastrophe theory and

a test in a corporate failure context. The Financial Review, 26, 127-155.

298 Rosser

Grossman, S.J. (1976). On the efficiency of competitive stock markets. Journal of Finance, 31,573-585.

Grossman, S.J. & Stiglitz, J.E. (1980). On the impossibility of informationally efficient markets.American Economic Review, 70, 393-408.

Gu, M. (1993). An empirical examination of the deterministic component in stock price vola-tility. Journal of Economic Behavior and Organization, 22, 239-252.

Guastello, S.J. (1995). Chaos, catastrophe, and human affairs: Applications of nonlinear dynam-ics to work, organizations, and social evolution. Mahwah: Lawrence Erlbaum Associates.

Hamilton, J.D. (1986). On testing for self-fulfilling speculative price bubbles. International Eco-nomic Review, 27, 545-552.

Hardouvelis, G.A., La Porta, R. & Wizman, T.A. (1994), What moves the discount on countryfunds? National Bureau of Economic Research Working Paper No. 4261.

Harrison, J.M. & Kreps, D.M. (1978). Speculative behavior in a stock market with heteroge-neous expectations. Quarterly Journal of Economics, 92, 323-336.

Ho, T & Saunders, A. (1980). A catastrophe model of bank failure. Journal of Finance, 35,1189-1207.

Holland, J.H. (1992). Adaptation in natural and artificial systems. Cambridge: MIT Press.Hsieh, D.A. (1991). Chaos and nonlinear dynamics: Applications to financial markets. Journal

of Finance, 46, 1839-1877.Jaditz, T & Sayers, C.L. (1993). Is chaos generic in economic data? International Journal of

Bifurcations and Chaos, 3, 745-755.Kac, M. (1968). Mathematical mechanisms of phase transitions. In M. Chretien, E. Gross,

and S. Deser (Eds.), Statistical physics: Transitions and superfluidity, Vol. 1 (pp. 241-305).Brandeis University Summer Institute in Theoretical Physics, 1966.

Keynes, J.M. 1936. General theory of employment, interest and money. London: Harcourt Brace.Kindleberger, C.P. 1989. Manias, panics, and crashes, 2nd edition. New York: Basic Books.Koppl, R. & Yeager, L.B. (1996). Big players and the Russian ruble: Lessons from the nine-

teenth century. Explorations in Economic History, 33, 367-383.Kramer, C. & Smith, R.T (1995). Recent turmoil in emerging markets and the behavior of coun-

try-fund discounts: Removing the puzzle of the pricing of closed-end mutual funds. Interna-tional Monetary Fund Working Paper 95/68.

LeBaron, B. (1994). Chaos and nonlinear forecastibility in economics and finance. Philosophi-cal Transactions of the Royal Society of London A, 348, 397-404.

LeBaron, B. (1997). Experiments in evolutionary finance. In W.B. Arthur, S. Durlauf, and D.Lane (Eds.), The economy as a complex evolving system, II. Redwood City: Addison-Wesley, in press.

Lee, C.M.C., Shleifer, A. & Thaler, R.H. (1990). Closed-end mutual funds. Journal of Eco-nomic Perspectives, 4, 153-164.

Lee, C.M.C., Shleifer, A. & Thaler, R.H. (1991). Investor sentiment and the closed-end fundpuzzle. Journal of Finance, 46, 75-110.

LeRoy, S.E (1989). Efficient capital markets and martingales. Journal of Economic Literature,27, 1583-1622.

Lux, T (1995). Herd behaviour, bubbles and crashes. Economic Journal, 105, 881-896.MacKay, C. (1852). Memoirs of extraordinary delusions and the madness of crowds. London:

Office of the National Illustrated Library.Magill, M.J.P. & Quinzii, M. (1996). Incomplete markets over an infinite horizon: Longlived

securities and speculative bubbles. Journal of Mathematical Economics, 26, 133-170.Milgrom, P. (1981). Rational expectations, information acquisition, and competitive bidding.

Econometrica, 49, 921-944.Mill, J.S. (1848). Principles of political economy. London: Parker.Minsky, H.R (1972). Financial instability revisited: The economics of disaster. Reappraisal of

the Federal Reserve Discount Mechanism, 3, 97-136.Mitchell, M.L. & Netter, J.M. (1989). Triggering the 1987 stock market crash: Antitakeover

provisions in the proposed house ways and means bill? Journal of Financial Economics,24, 37-68.

Speculation on Nonlinear Speculative Bubbles 299

Muth, J.T (1961). Rational expectations and the theory of price movements. Econometrica,19, 315-335.

Noguchi, Y. (1990). Land problem in Japan. Hitotsubashi Journal of Economics, 31, 73-86.Nyssen, J. (1994). Social efficiency of bubbles in the Grossman and Helpman endogenous

growth model. Economics Letters, 45, 197-202.Palmer, R.G., Arthur, WB., Holland, J.H., LeBaron, B. & Tayler, P (1994), Artificial economic

life: A simple model of a stockmarket. Physica D, 75, 264-274.Peters, E.E. (1991). A chaotic attractor for the S&P 500. Financial Analysts Journal, 47, 55-62.Pontiff, J. (1995). Closed-end fund premia and returns: Implications for financial market equi-

librium. Journal of Financial Economics, 37, 341-370.Poterba, J.M. & Summers, L.H. (1988). Mean reversion in stock returns: Evidence and im-

plications. Journal of Financial Economics, 22, 27-59.Rosser, Jr., J.B. (1991). From catastrophe to chaos: A general theory of economic discontinuities.

Boston: Kluwer Academic Publishers.Rosser, Jr., J.B. (1994). Higher dimensional crashes of semi-rational bubbles. Mimeo, James

Madison University.Samuelson, P.A. (1957). Intertemporal price equilibrium: A prologue to the theory of specu-

lation. Weltwirtschaftliches Archiv, 79, 181-219.Samuelson, EA. (1958). An exact consumption-loan model of interest with or without the

social contrivance of money. Journal of Political Economy, 66, 467-482.Sethi, R. (1996). Endogenous regime switching in speculative markets. Structural Change and

Economic Dynamics, 7, 99-118.Shiller, R.J. (1984). Stock rices and social dynamics. Brookings Papers on Economic Activity,

2, 457-498.Shiller, R.J. (1989). Market volatility. Cambridge: MIT Press.Shiller, R.J. & Pound, J. (1987). Investor behavior in the October 1987 stock market crash.

National Bureau of Economic Research Working Paper No. 2446.Smith, VL., Suchanek, G.L. & Williams, A.W. (1988). Bubbles, crashes, and endogenous

expectations. Econometrica, 56, 1119-1151.Stiglitz, J.E. (1982). Information and capital markets. In W. Sharpe and C. Cootner (Eds.),

Financial economics: Essays in honor of Paul Cootner. Englewood Cliffs: Prentice Hall.Sutherland, A. (1996). Intrinsic bubbles and mean-reverting fundamentals. Journal of Monetary

Economics, 37, 163-173.Tamborski, M. (1995). Efficiency of new financial markets: The case of Warsaw stock exchange.

Institut de Recherche Economique et Sociale Discussion Paper no. 9504, Universit6Catholique de Louvain.

Thaler, R.H. (1991). Quasi rational economics. New York: Russell Sage Foundation.Theiler, J., Eubank, S., Longtin, A., Galdrikian, B. & Farmer, J. (1992). "testing for nonlinearity

in time series: The method of surrogate data. Physica D, 58, 77-94.Tirole, J. (1982). On the possibility of speculation under rational expectations. Econometrica,

50, 1163-1181.Tirole, J. (1985). Asset bubbles and overlapping generations. Econometrica, 53, 1499-1528.Tversky, A. & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Sci-

ence, 185, 1124-1131.Zahler, R. & Sussman, H. (1977). Claims and accomplishments of applied catastrophe theory.

Nature, 269, 759-763.Zeeman, E. C. (1974). On the unstable behavior of the stock exchanges. Journal of Mathe-

matical Economics, 1, 39-44.Zweig, M.E. (1973). An investor expectations stock price predictive model using closed-end

fund premiums. Journal of Finance, 28, 67-87.

300 Rosser